Crypto World

GENIUS Act deadline puts stablecoin issuers on notice

The GENIUS Act is moving into a key rulemaking stage as digital dollar users and stablecoin issuers face a June 9, 2026 deadline for comments on FinCEN and OFAC proposals.

Summary

- FinCEN and OFAC comments close June 9 for GENIUS Act stablecoin compliance rules.

- The proposed rule treats permitted stablecoin issuers as financial institutions under Bank Secrecy Act rules.

- Crypto.news reported banks want comment periods paused until primary stablecoin rules become clearer.

The post shared by Digital Perspectives cited June 9 for FinCEN-OFAC comments and July 18, 2026 for full rules. The dates place stablecoin compliance back at the center of U.S. crypto regulation.

FinCEN and OFAC set June 9 comment deadline

FinCEN and OFAC are seeking public comments on proposed rules for permitted payment stablecoin issuers. The proposal would apply anti-money laundering and sanctions compliance duties to firms that issue payment stablecoins.

The Federal Register notice says comments must be received by June 9, 2026. The proposal follows the GENIUS Act’s direction to treat permitted stablecoin issuers as financial institutions under the Bank Secrecy Act.

The rules would require issuers to maintain compliance programs suited to their size and business model. They would also bring stablecoin firms closer to the same oversight used for other financial companies.

The proposal covers customer checks, sanctions controls, suspicious activity monitoring, and other systems aimed at reducing illicit finance risks.

July 18 marks another GENIUS Act milestone

The second date cited in the post is July 18, 2026. That date marks one year after the GENIUS Act became law on July 18, 2025.

Legal trackers list July 18, 2026 as a key deadline for several implementing rules under the stablecoin law. These include rules tied to foreign issuer registration requests and related appeals.

This gives regulators a narrow window to turn the law into working standards. It also gives issuers a clearer timeline for planning compliance, licensing, reserves, and reporting.

For stablecoin users, the rulemaking could shape how digital dollars move across exchanges, wallets, apps, and payment networks.

Banks push back on stablecoin rulemaking

Crypto.news reported that major U.S. banking groups asked regulators to pause several GENIUS Act comment periods. They want the Office of the Comptroller of the Currency to finish its primary stablecoin framework first.

The banks argued that firms need a clearer base rule before responding to related comment periods. Their request shows that traditional finance still wants more detail before the rules harden.

Crypto.news also reported that stablecoin firm Agora filed for a national trust bank charter with the OCC on April 24. The move could place Agora under federal oversight before the new rules fully settle.

That shows two different responses to the same rulemaking race. Banks want more time, while some stablecoin firms are trying to secure federal status early.

Stablecoin issuers face a tighter compliance path

The GENIUS Act gives the U.S. its first federal framework for payment stablecoins. It focuses on reserve backing, issuer oversight, consumer safeguards, and compliance with financial crime rules.

For issuers, the next stage is practical. They must show how they will screen users, manage sanctions risks, monitor transactions, and respond to lawful orders.

The June 9 deadline matters because it is one of the last chances for firms, banks, and users to shape the FinCEN-OFAC rule before regulators finalize it.

The July 18 milestone then brings the wider stablecoin framework closer to full use. Stablecoin issuers now face a clear message from regulators: digital dollar products will need bank-style compliance controls.

The pound strengthened following the outcome of the US Federal Reserve meeting, where the central bank, as expected, kept interest rates unchanged. However, the Fed did not provide the market with clear signals of an imminent shift towards rate cuts, maintaining a cautious approach to future monetary policy. Despite the Fed’s cautious tone, the dollar failed to gain fresh momentum, allowing the British currency to partially recover its recent losses.

Market attention is now almost entirely focused on the Bank of England meeting, as its decision is expected to be the main driver for sterling through the end of the week. Investors also do not expect a change in interest rates, but the key factors will be the Monetary Policy Committee’s vote split, the accompanying statement and comments from Bank of England Governor Andrew Bailey. Any signals regarding the timing of potential monetary policy easing could trigger notable volatility in the pound.

For the euro, today will also bring a number of important macroeconomic releases. Markets will focus on preliminary inflation and GDP data from Germany, as well as GDP and inflation figures from Spain. These reports will help investors assess the resilience of the eurozone economy and adjust expectations regarding the European Central Bank’s future actions. Stronger data could support the euro, while weaker figures may reinforce expectations of further ECB policy easing.

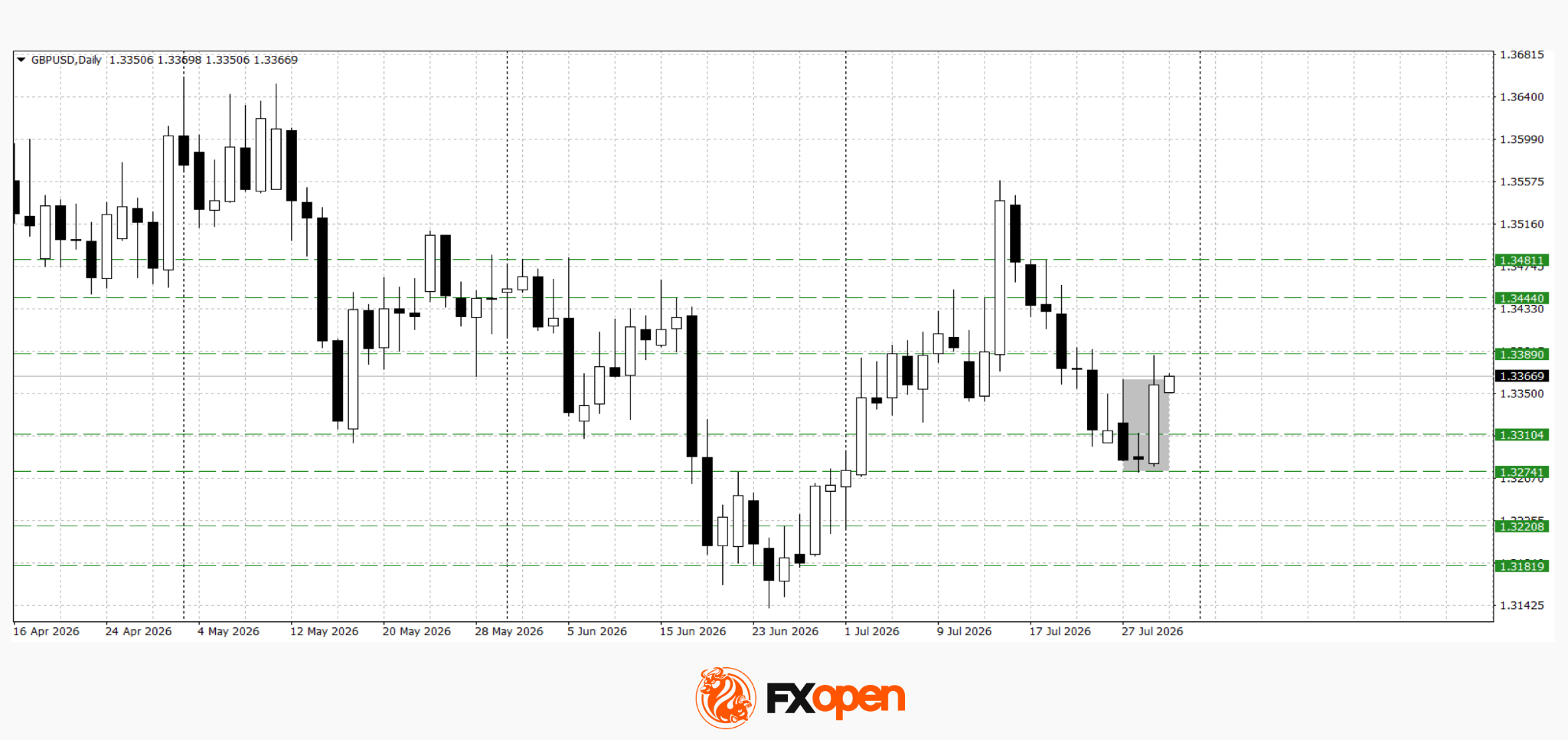

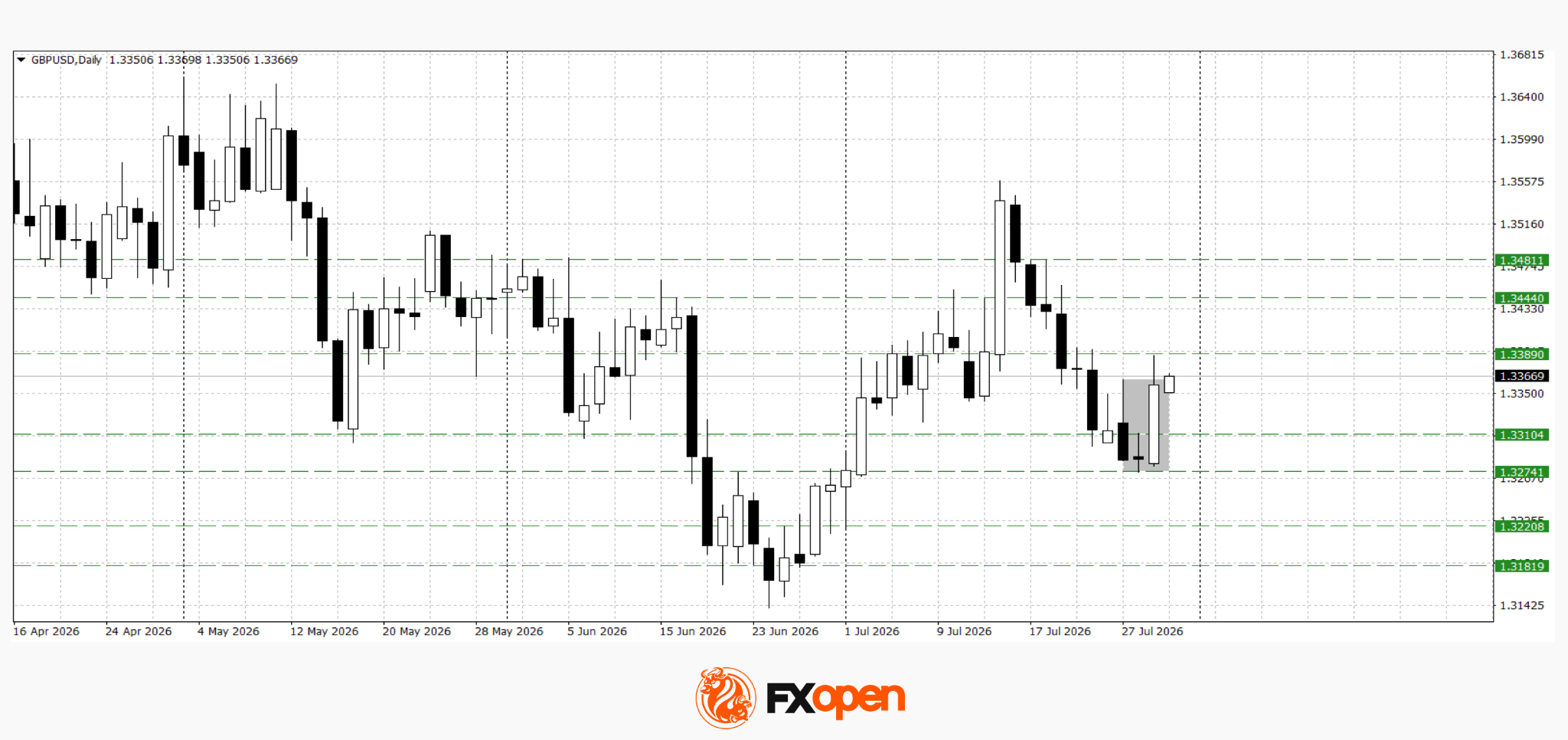

GBP/USD

Following yesterday’s Fed meeting, GBP/USD moved towards the 1.3400 area. A rebound from the 1.3270 support level and a sharp daily rally allowed buyers to form a bullish engulfing pattern. Technical analysis of GBP/USD points to the possibility of further gains towards 1.3440–1.3480 if the 1.3270–1.3300 range becomes established as support. A decisive move below yesterday’s low could trigger a renewed decline towards 1.3180–1.3220.

Key events for GBP/USD:

- Today at 14:00 (GMT+3): Bank of England interest rate decision;

- Today at 14:30 (GMT+3): speech by Bank of England Governor Andrew Bailey;

- Today at 15:30 (GMT+3): US initial jobless claims.

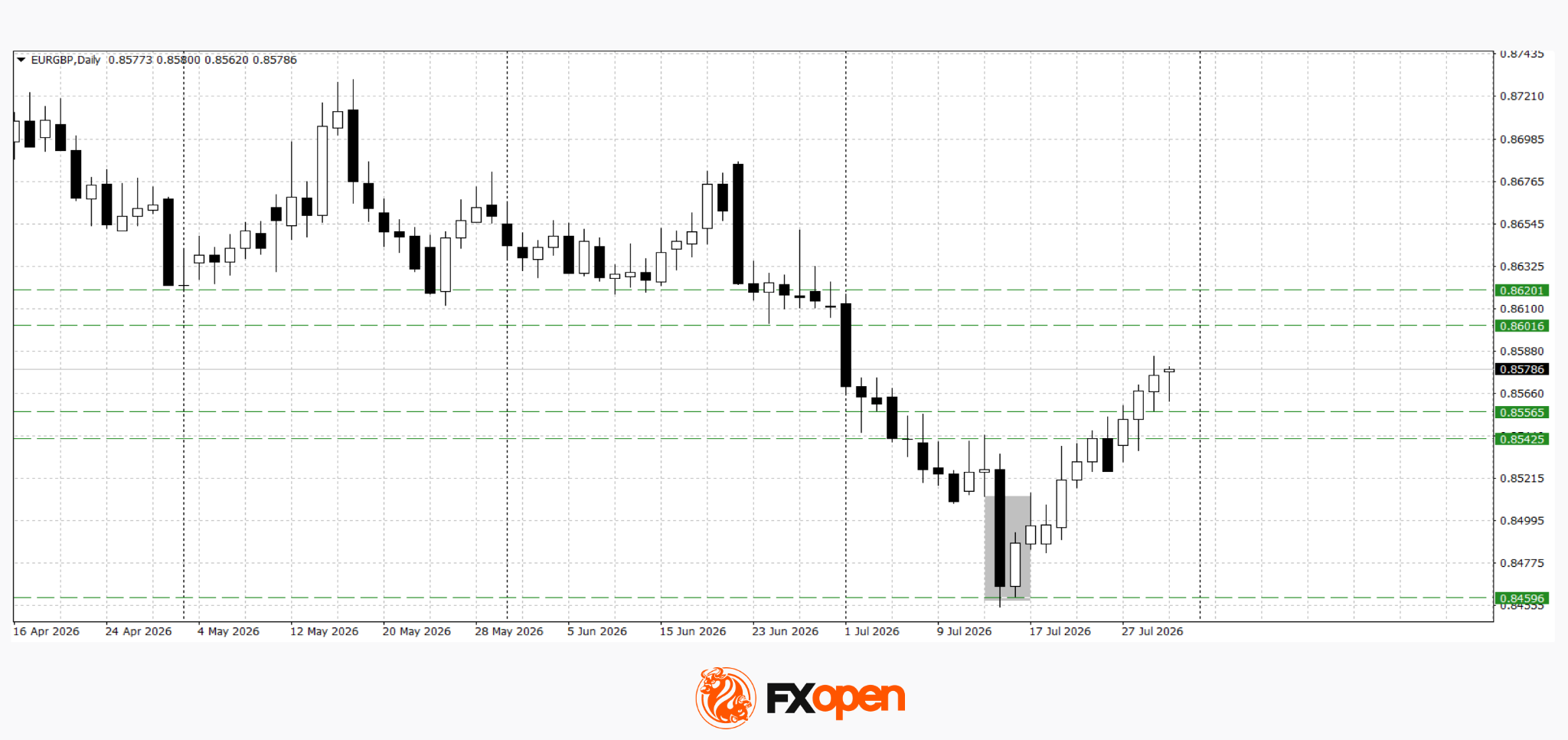

EUR/GBP

EUR/GBP is showing signs of recovery after forming a bullish harami pattern on the daily timeframe. If market participants are disappointed by today’s Bank of England decision, the pair could extend its advance towards 0.8600–0.8620. The bullish scenario would be invalidated after a decisive break below the 0.8540–0.8560 support area.

Key events for EUR/GBP:

- Today at 08:30 (GMT+3): France GDP;

- Today at 11:00 (GMT+3): Germany GDP;

- Today at 15:00 (GMT+3): Germany Consumer Price Index (CPI).

Overall, the near-term direction of sterling will depend primarily on the Bank of England’s decision, the Monetary Policy Committee’s vote split and Andrew Bailey’s comments on the future outlook for interest rates. For the euro, inflation and GDP releases from the eurozone’s largest economies will remain important, as they could influence expectations for the European Central Bank’s next policy steps. With the market impact of the Fed meeting now fading, European economic data and signals from the Bank of England could become the main drivers of GBP/USD and EUR/GBP through the end of the week.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

China Business Journal says fraudsters impersonated the publication, demanding Bitcoin to suppress purported investigative reports about targeted companies.

Firefighters in France and Spain are battling ferocious wildfires in an effort to control the blazes before the next heat wave arrives later this week.

French President Emmanuel Macron on Monday described the “completely unprecedented” crisis as the “toughest since the Second World War.” He urged firefighters to “stay strong” as they prepared to face the wildfire in the Gironde region, near Bordeaux.

An estimated 220,000 people have been evacuated in the Gironde region, since the most pervasive fire broke out last week. The Landes region further south has seen at least 30,000 people evacuated.

The fire in Landes is now under control, Macron said, but he warned it “remains virulent” and urged extreme caution over the coming days.

“Our country is going through an unprecedented fire season: 116,085 hectares have already burned and 13,566 fire starts have been recorded since January,” France’s Prime Minister Sébastien Lecornu said on Monday. (116,000 hectares is roughly 287,000 acres.)

In Spain, officials fighting the blazes near Madrid say they are the worst the region has ever experienced. Firefighters are also battling a wildfire in Castellón, a province near Valencia.

More than 100,000 people have been ordered to evacuate their homes or take shelter as emergency services attempt to get the flames under control in the face of changing winds.

Spanish Prime Minister Pedro Sánchez told reporters Tuesday that the authorities “can begin to see the light at the end of the tunnel” in the fight against the wildfires, but he expressed concern about the approaching heat wave.

The authorities “will continue to mobilize all resources until the last flame is extinguished,” he vowed.

Sánchez has referred to the wildfire crisis as “the most painful expression” of the climate emergency.

As the European countries reckon with the remaining blazes and brace for the potential impact of the incoming heat wave, here are photos showing the devastation caused by the wildfires so far.

Crypto exchange Luno is reportedly cutting around 20% of its workforce as it restructures operations and shifts more focus toward institutional clients, financial infrastructure, and business-to-business services. The move follows earlier headcount reductions and comes as many crypto firms continue to prioritize cost control and automation amid uneven market conditions.

In a report published by Bloomberg on Tuesday, Luno CEO James Lanigan said the company has invested in automation and other operational improvements, changing the resources required to run the business. He also indicated that further cost trimming will be paired with ongoing investments in compliance, core infrastructure, and retail products. According to the filing discussed in earlier coverage, Luno is owned by Digital Currency Group and operates in Africa and the Asia-Pacific region, serving roughly 16 million users.

Key takeaways

- Luno is reportedly reducing headcount by about 20%, citing automation and operational changes that alter staffing needs.

- The exchange says it will also pursue cost reductions while continuing investment in compliance, core infrastructure, and retail offerings.

- This is not Luno’s first major restructuring; the company previously cut 35% of staff in January 2023.

- July 2026 saw a cluster of disclosed layoffs and restructurings across crypto, with industry tracker CryptoJobsList recording hundreds of roles affected.

- Several firms point to AI and efficiency upgrades as a common factor behind staffing changes, though the scale and drivers vary by company.

Luno’s restructuring and why staffing is changing

Luno’s reported layoffs are framed as an outcome of “run-rate” changes rather than a simple demand shock. Bloomberg reports that CEO James Lanigan attributed the restructuring to investments in automation and broader operational improvements, which in turn reduced the staffing required for core functions. The company also plans to trim costs in line with market conditions, while directing resources toward areas it views as strategic—compliance, core infrastructure, and retail products.

For users and customers, this type of restructuring can translate into slower expansion in some areas, but it can also mean that teams previously handling manual processes are redeployed toward system reliability, risk controls, and institutional service delivery. Luno has previously expanded beyond retail trading into infrastructure and institutional offerings, including providing crypto infrastructure for banks and fintech firms—an angle that typically requires different operational capabilities than consumer exchange experiences.

Importantly, Luno has already gone through a larger round of reductions before. In January 2023, Cointelegraph reported that DCG-affiliated companies laid off more than 500 employees, with Luno cutting 35% of its staff—affecting nearly 330 employees—during a period of turbulence across parts of the technology and crypto sectors.

Automation, AI, and cost controls spreading across the sector

Luno’s stated rationale echoes a pattern other crypto companies have cited in recent months: automation, AI, and efficiency improvements are often presented as reasons to reduce staffing. While the details differ by firm—ranging from internal process upgrades to product and platform changes—the theme is consistent: companies are trying to maintain or improve service levels while reducing operating costs.

One reason this matters for the industry is that layoffs can reshape what businesses prioritize. Where consumer-focused teams previously led growth efforts, many companies now appear to be redirecting investment toward infrastructure, compliance, and enterprise-grade services—areas where budgets can be more predictable and where automation may reduce operational friction.

What July’s layoff data suggests (and what it can’t tell)

Beyond Luno, the broader wave of job cuts continues to show up in public trackers. CryptoJobsList, which monitors crypto and crypto-adjacent workforce reductions, recorded layoffs or restructurings at 12 crypto and crypto-adjacent companies in July. Disclosed figures totaled 894 jobs affected, according to the tracker’s reporting.

CryptoJobsList’s data is meant to be an indicator of sector activity rather than a complete measure of all crypto-related cuts. The tracker notes that its figures include adjacent financial technology firms, and they are also skewed by unusually large reductions such as Block’s reported 4,000-person layoff in February.

Still, the concentration of announcements in a short period gives investors and builders a practical signal: staffing is being reassessed across multiple segments of the crypto ecosystem, and companies appear to be acting faster than in downturn cycles when cost reductions sometimes lag demand shifts.

Other notable restructurings in July

Earlier in July, Cointelegraph reported that crypto wallet company Exodus announced plans to cut 25% of its staff while reorganizing around a full-stack card-issuance and stablecoin-payments platform. Exodus said the changes could produce between $10 million and $13 million in annual operating savings, positioning the restructuring as an effort to concentrate resources on a specific product direction.

Separately, blockchain infrastructure developer Gnosis took a different approach to workforce reductions. In July, the company invited organizations hiring across roles including engineering, product, design, marketing, developer relations, and customer relations to contact it for introductions to former employees affected by a recent restructuring. In a statement dated July 17, Gnosis said it reduced its workforce following a review of its consumer-facing Gnosis App.

These examples show how restructuring rationales can vary: some companies cite platform efficiency and automation, while others tie changes to product review cycles or a strategic pivot. For employees, the practical impact differs as well—some reorganizations focus on relocating talent, while others involve more direct role elimination.

What to watch next

With Luno’s reported cut and a continuing pattern of restructurings recorded across the sector, the next question for readers is whether these moves translate into measurable improvements—such as higher reliability, faster enterprise onboarding, or more consistent compliance execution—or whether they mainly reduce capacity at the cost of long-term growth. Investors and builders should keep an eye on how companies balance automation-driven efficiency with the operational load required by regulators, institutional clients, and evolving product demands.

Cash Cat (CASHCAT) rose about 16% in 24 hours and reclaimed its spot as the top token by market capitalization on Robinhood Chain, after the company’s second-quarter earnings call.

The move pushed the token back past Pons (PONS), which had taken the spot while CASHCAT drifted lower through July. Its trading volume still dwarfs every other asset on the network.

What Happened on the Robinhood Earnings Call

Robinhood reported record second-quarter revenue of $1.3 billion on July 29, up 32% from a year earlier. Earnings per share reached $0.62. Moreover, cryptocurrency transaction revenue reached $100 million.

Tenev spent part of the call demonstrating the Robinhood apps and the stock tokens on his phone. Traders spotted CASHCAT sitting in his recent search list. The token climbed shortly afterward. He also addressed the Robinhood chain during the call.

“I mean, I think that we built Robinhood chain to be purpose-built for real-world assets. I should clarify, I like memes as well,” Tenev said during the call.

Follow us on X to get the latest news as it happens

CASHCAT Retakes the Lead After a 47% Slide

CASHCAT borrows its name from the working title Robinhood used before its rebrand. Its initial rally arrived after the chain went live on July 1. The token pushed past a $200 million market cap before stalling.

The token fell roughly 47.2% over the past two weeks. PONS overtook it as the chain’s largest token by market cap. That position has now reversed. At press time, CASHCAT traded near $0.0469, up about 16% on the day.

CASHCAT also remains the most traded asset on the network. It has logged 1.57 million trades from 51,638 unique traders since launch. Cumulative volume stands at $890.5 million, according to Dune data.

Its $28.2 million in 24-hour volume is more than four times that of second-placed PONS, which traded $6.3 million.

CASHCAT sits about 79% below its record high of $0.228, set on July 11. The near-term test is whether demand holds once the earnings attention fades.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Cash Cat Reclaims Robinhood Chain Crown After Q2 Earnings Call appeared first on BeInCrypto.

Crypto prices went almost nowhere over the past day. The leverage underneath them was destroyed anyway.

About $286 million in positions were liquidated across 87,294 traders in 24 hours, according to CoinGlass, while bitcoin closed flat at roughly $63,900 and ether slipped to $1,900. Longs accounted for $186 million of the damage and shorts $100 million, the signature of a market that moved hard in both directions and settled back where it started.

Bitcoin’s split shows it plainly. Roughly $57 million of bitcoin positions were cleared, and the balance was almost even, about $28 million in longs against $29 million in shorts. The price swung between $63,247 and $64,660 during the window, a range of barely 2%, which was enough to clear traders positioned either way.

Ether recorded the largest total at about $58 million, tilted toward longs, as prices ranged between $1,920 and $1,850.

The single biggest liquidation was a $2.9 million bitcoin position on Binance.

The Federal Reserve’s rate decision on Wednesday sits inside that window, and the bulk of the damage came in the 12 hours around it, with $188 million liquidated and longs bearing $130 million.

Binance is set to broaden its regulated commodity offering by launching USDT-settled options on gold and silver through its Abu Dhabi exchange venue. The new contracts are designed to give traders exposure to bullion price movements without requiring delivery of physical metals, fitting a growing pattern of crypto-native derivatives tied to traditional assets.

The options will be listed via Nest Exchange Limited, Binance’s Abu Dhabi Global Market (ADGM) regulated Recognized Investment Exchange. For users, the structure is also tailored to who can trade: retail participants will be limited to buying options, while eligible institutional users and liquidity providers can write (sell) contracts.

Key takeaways

- Binance plans to list USDT-settled gold and silver options on its Abu Dhabi-regulated Nest Exchange Limited.

- Retail users can buy options only, while certain institutions and liquidity providers may also write options.

- The product is built on Binance’s existing gold and silver perpetual futures that began in January.

- The launch adds to a wider commodity-linked ecosystem that includes tokenized bullion products such as Tether’s XAUt and Paxos’s XAUT-like offerings.

USDT-settled options, delivered without physical metals

According to Binance, the new gold and silver options will be settled in USDT, allowing traders to manage exposure in a stablecoin-denominated format rather than by taking delivery of physical bullion. Options also introduce a different risk profile compared with futures or spot exposure because the buyer’s loss is generally limited to the premium paid.

Binance said its decision to restrict retail users to buying options is meant to cap downside risk to the premium, while allowing eligible institutional participants and liquidity providers to write options so they can collect premiums. That split is important for how these markets may develop: option writing tends to require more sophisticated risk management and typically increases liquidity, but it also changes who bears the tail risk in stressed scenarios.

Link to Binance’s broader move into regulated commodities

This options launch follows Binance’s introduction of gold and silver perpetual futures in January. While perpetuals allow traders to take leveraged directional bets on the metal prices, options provide additional flexibility—such as constructing strategies that can hedge other positions or express expectations about volatility and price ranges.

By adding options under an ADGM-regulated framework, Binance is effectively extending the same “traditional asset” theme into a more complex derivatives layer. For investors, traders, and firms evaluating how crypto venues integrate with conventional markets, product expansion like this can matter as it broadens the toolkit available inside regulated jurisdictions.

Tokenized bullion sits alongside derivatives

Binance’s new options add to an expanding set of commodity-linked crypto products, but they coexist with a different approach: tokenization of physical bullion rather than derivatives trading. In particular, companies including Tether and Paxos have focused on representing stored metal in token form.

Tether’s XAUt represents one troy ounce of gold stored in Swiss vaults. The token recently received Shariah certification from Amanah Advisors, a step aimed at improving accessibility for Islamic financial institutions. Earlier in the same broader push, ADGM also recognized XAUt as an accepted spot commodity, which supports the idea that regulated firms can build services around the tokenized asset.

While options and tokenized bullion are distinct products—options are primarily for price exposure and hedging, tokenized bullion is intended for holding metal representation—both trends point to a common direction: crypto market infrastructure is increasingly being used to connect with traditional commodity exposure.

What the growth in tokenized commodities suggests

RWA.xyz estimates that the tokenized commodities sector has grown to roughly $4.56 billion in distributed value. According to the same estimate, Tether Gold and Paxos Gold account for more than 90% of that market, indicating that liquidity and adoption in this niche are currently concentrated in a small set of issuers.

For market watchers, that concentration is a double-edged sign. It shows demand for regulated, tokenized access to bullion—yet it also suggests that the overall pace of expansion could depend heavily on a limited number of products and partners. Binance’s derivatives expansion, meanwhile, may attract another category of participants: those who prefer trading wrappers (like options) rather than holding tokenized commodities directly.

Why the retail/institutional split matters

Binance’s choice to allow retail users to buy options only, while enabling eligible institutions and liquidity providers to write contracts, is more than a compliance decision—it will shape how these markets function on day one and beyond. Buyers typically act as hedgers or speculators with capped loss, while writers can provide liquidity and earn premiums, but they also need adequate capital and controls to manage exposure.

As these contracts launch, traders will likely watch for practical indicators such as bid-ask spreads, the depth of liquidity across strike prices, and how consistently institutions are willing to write—especially during periods when volatility in gold and silver tends to rise.

Looking ahead, the key question will be how quickly Binance’s Abu Dhabi-listed options gain traction and whether the structured access for retail versus institutions becomes a model other regulated venues follow. Traders and investors should also keep an eye on how tokenized bullion adoption evolves, since it may influence where derivatives demand concentrates—either in hedging token holdings or in independent strategies tied purely to metal price movements.

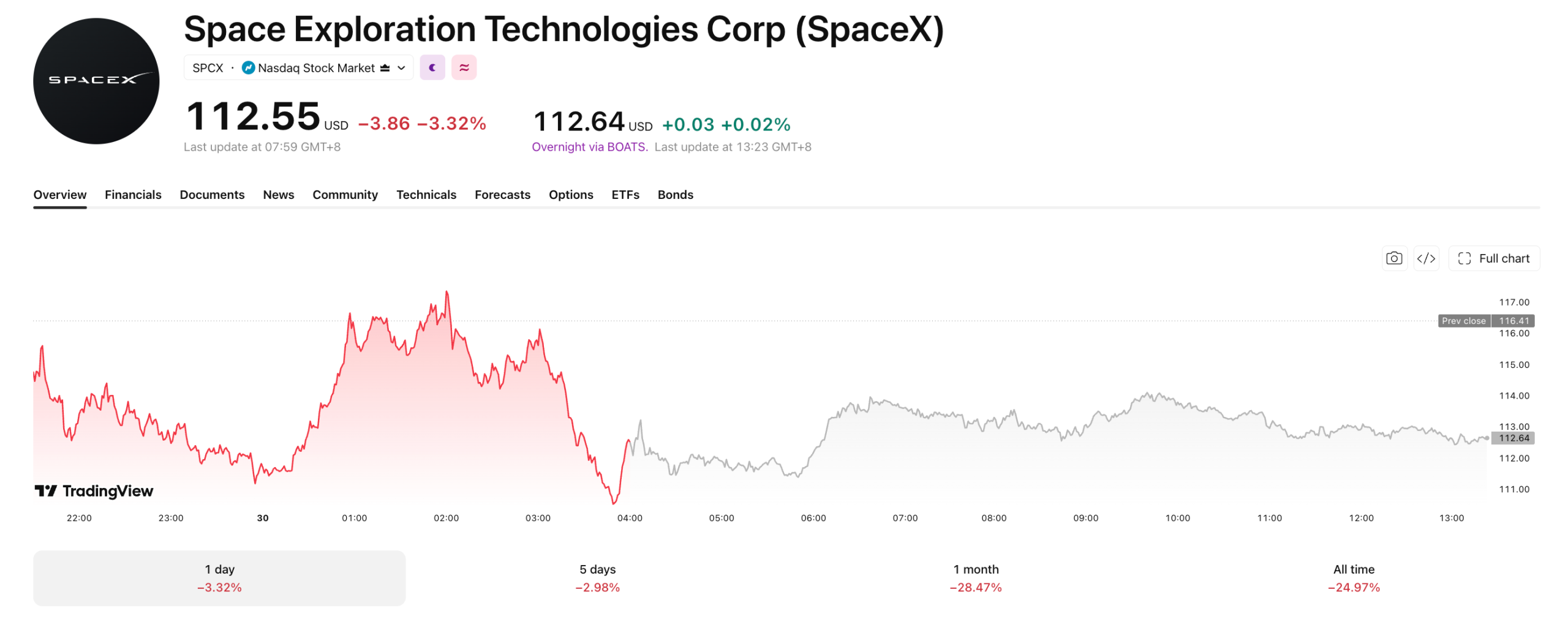

SpaceX shares fell 3.32% on Wednesday, July 29, closing at $112.55. The drop came even as the company landed a fresh $1.6 billion order from the US Space Force covering 18 Falcon 9 launches through 2027.

The slide is part of a broader unraveling since SpaceX’s Nasdaq debut. The stock priced its IPO at $135, then surged to an all-time high of $225.64 in mid-June before reversing hard.

A Contract That Couldn’t Halt the Slide

Wednesday’s drop extends a rough stretch for SpaceX stock. Shares hit a record low of $107.01 on Tuesday and still trade below the company’s $135 IPO price. The stock has fallen roughly 29% over the past month. Investors are now bracing for a share unlock around August 6 that could add fresh supply to the market.

Rivals face setbacks of their own. ULA is still working through a months-long technical review of a booster separation issue on its Vulcan rocket. Blue Origin is still investigating a launchpad explosion that grounded its New Glenn rocket in May.

Those problems leave SpaceX with an even wider lead in Pentagon launch work. Some lawmakers still question the military’s reliance on a single contractor.

Inside Space Force’s Latest Order

Space Force split the missions across two task orders under its National Security Space Launch Phase 3 Lane 1 program. SpaceX competes there with United Launch Alliance, Blue Origin, and other US launch firms for military work. The rockets will carry satellites that detect and track airborne threats. That work falls under the Pentagon’s Space Based Sensing and Targeting effort.

The order builds on May’s Space Force win, when SpaceX picked up $6.5 billion for military satellite work. Reuters reports the company has now landed at least $7 billion in Pentagon deals this year. Much of that spending ties back to the Trump administration’s roughly $185 billion Golden Dome missile defense program.

The new contract adds fresh revenue. It may not steady the stock, though, ahead of the August share unlock and SpaceX’s August 4 earnings report. Investor sentiment, not Pentagon spending, may decide that outcome.

The post SpaceX Stock Extends Slide Despite $1.6B Space Force Deal appeared first on BeInCrypto.

Telegram has faced legal action in Australia after the country’s online safety regulator accused the messaging platform of failing to remove terrorist and extremist content despite repeated notices.

Summary

- Australia’s online safety regulator has taken Telegram to court over alleged failures to remove terrorist and extremist content.

- The regulator says videos linked to the Christchurch and Buffalo attacks remained available after Telegram was notified.

- Telegram has denied the allegations, said it will fight the case in court, and cited thousands of extremist communities blocked this year.

- The Australian case comes a day after Russia placed Telegram founder Pavel Durov on an international wanted list over separate terrorism related allegations.

According to Australia’s eSafety Commissioner, the regulator has commenced Federal Court proceedings against Telegram, alleging the platform left videos linked to terrorist executions and mass shootings accessible even after it had been formally notified that the material breached Australia’s online safety rules.

The case centers on content associated with some of the most well-known extremist attacks in recent years, including the 2019 Christchurch mosque shootings in New Zealand and the 2022 Buffalo supermarket shooting in the United States. Australia’s regulator alleges the material remained available to users for an extended period after enforcement notices had been issued.

“We allege that this content remained accessible on the service long after Telegram had been put on notice,” eSafety Commissioner Julie Inman Grant said in a statement announcing the legal action.

If the court finds Telegram breached Australia’s industry codes and standards, the company could face civil penalties of up to A$54.6 million, or about $38 million.

Australia says Telegram failed to remove extremist material

Filed by the Office of the eSafety Commissioner, the lawsuit accuses Telegram of failing to comply with obligations requiring online platforms to remove or restrict access to terrorist and violent extremist content.

According to the regulator, the disputed material includes videos connected to some of the most notorious acts of extremist violence in recent history. Authorities contend that the platform did not act quickly enough after being alerted to the content.

Julie Inman Grant said the case concerns material linked to the Christchurch and Buffalo attacks, arguing that the platform continued to make the content available despite receiving notice from Australian authorities.

The lawsuit represents another attempt by Australian regulators to enforce the country’s online safety framework, which places legal obligations on digital platforms to address harmful content within prescribed timeframes.

Telegram rejects allegations and plans court challenge

Telegram has denied the allegations and said it will defend its moderation practices in court.

“We reject these allegations and will contest them in court,” a Telegram spokesperson said in response to requests for comment.

The spokesperson added that the company’s efforts to combat terrorism are well established, saying Telegram blocked thousands of extremist communities during 2026 alone as part of its enforcement program.

While rejecting Australia’s claims, Telegram maintained that it continues to remove extremist content and take action against communities that violate its policies.

Pavel Durov faces mounting legal pressure in multiple countries

The Australian proceedings arrive as Telegram founder Pavel Durov continues to face legal scrutiny in more than one jurisdiction.

Only a day earlier, Russia’s Federal Security Service charged Durov with facilitating terrorist activity and placed him on an international wanted list, according to Russian news agency Interfax. Russian authorities allege Telegram allowed channels, bots and group chats linked to Ukrainian intelligence services, terrorist organizations and extremist groups to remain active despite claims they were used to coordinate attacks, recruit members and conduct cyber fraud.

Durov has rejected those accusations. Responding to the Russian investigation in February through a post on X, he described the case as politically motivated and accused Moscow of attempting to pressure Telegram into weakening user privacy and limiting freedom of speech.

Outside Russia, Durov also remains under criminal investigation in France over allegations that Telegram failed to adequately prevent criminal activity on the platform.

French authorities arrested Durov near Paris in August 2024 while investigating claims involving organized crime, drug trafficking, cybercrime and child sexual abuse material. Although French officials later eased his travel restrictions, the criminal case remains open.

Responding to the French investigation over the past year, Durov argued that holding the head of a communications platform personally liable for content created by users would establish an unsound legal precedent. He also said Telegram responds to valid legal requests through established procedures and applies moderation standards comparable to other major technology companies.

Telegram’s role keeps attracting government scrutiny

Founded by Russian-born Pavel Durov, Telegram relocated its operations to Dubai in 2017 after he left Russia in 2014.

The platform has become one of the primary communication channels used during Russia’s war in Ukraine, serving government officials, military observers and civilians on both the Russian and Ukrainian sides of the conflict.

At the same time, governments in several countries have intensified scrutiny of Telegram’s approach to content moderation, privacy and cooperation with law enforcement.

Following Durov’s detention in France in 2024, Telegram introduced updates to its terms of service and privacy policy that clarified how it responds to legally valid requests from authorities. Even after those changes, Durov has repeatedly said the company intends to protect user privacy while cooperating with lawful investigations carried out through appropriate legal channels.

Australia’s lawsuit now adds another regulatory challenge for Telegram, with the Federal Court set to determine whether the platform breached the country’s online safety standards by failing to remove terrorist and extremist material within the required time.

US spot Bitcoin ETFs recorded $32.1 million in inflows on Wednesday despite Bitcoin dipping below $64,000, ending a four-session outflow streak.

GBP/USD and EUR/GBP Await Key Bank of England Decision

5 picks our gambling expert loves this week

Samsung’s Mobile Division Posts First-Ever Loss Due To Soaring Memory Prices

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Brooks Brothers

-

Sports3 days ago

Sports3 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business12 hours ago

Business12 hours agoWhy Trees Belong on the Risk Register

-

Tech3 days ago

Tech3 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Politics3 days ago

Politics3 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World5 days ago

Crypto World5 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics2 days ago

Politics2 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Entertainment6 days ago

Entertainment6 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

News Videos3 days ago

News Videos3 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Fashion6 days ago

Fashion6 days ago16 Dresses for the High Summer Event

-

Sports6 days ago

Sports6 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

News Videos7 days ago

News Videos7 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Business1 day ago

Business1 day agoMajor shareholder moves on Canyon

-

Crypto World4 days ago

Crypto World4 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Politics4 days ago

Politics4 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Crypto World7 days ago

Crypto World7 days agoUniswap (UNI) pushes deeper into tokenized RWAs with permissioned trading pools

-

Entertainment2 days ago

Entertainment2 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Tech5 days ago

Tech5 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

Entertainment4 days ago

Entertainment4 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

News Videos2 days ago

News Videos2 days agoClaude: Build Financial Dashboards in Minutes (2026)

You must be logged in to post a comment Login