Crypto World

Goldman Sachs Dumps XRP and SOL: Altcoins Market Could Crash

Goldman Sachs has reduced exposure to XRP and Solana, according to recent portfolio disclosures. The timing raises an obvious question: is this institutional profit-taking, or something more structural?

Both assets have catalysts on the horizon, but the exit signal from one of Wall Street’s most-watched desks is hard to ignore.

The bank’s exit reflects an institutional shift away from higher-beta altcoins and toward large-cap anchors like BTC and ETH. While XRP’s regulatory overhang has been resolved, SOL’s sharp one-week drawdown of nearly 11% has reignited questions about its dependence on speculative memecoin cycles, even with the Foundation President’s statement on memecoins.

— Solana Community (@SolCommunityy) May 18, 2026

INSIGHT: Solana Foundation President Lily Liu says, “Memecoins don’t define Solana.” https://t.co/OYMj63YQs4 pic.twitter.com/kSY8jhX9Sc

INSIGHT: Solana Foundation President Lily Liu says, “Memecoins don’t define Solana.” https://t.co/OYMj63YQs4 pic.twitter.com/kSY8jhX9Sc

Neither asset delivered a clear breakout in recent sessions despite windows of opportunity. The data points to a market in transition, with altcoin liquidity thinning and institutional appetite shifting to infrastructure plays closer to Bitcoin’s base layer.

Discover: The best pre-launch token sales

Can XRP and SOL Survive Goldman Sachs Exit?

XRP is holding a narrow range between $1.38 and $1.42, with bulls defending the $1.35 support floor established during recent consolidation. Resistance sits at $1.50, a zone where XRP has stalled repeatedly across the past several weeks.

XRP’s moves remain tightly correlated with altcoin flows rather than any idiosyncratic driver, meaning upside depends heavily on macro risk sentiment flipping positive.

SOL’s picture is sharper and more painful. Down almost 12% on the week, the current $85 level is its last support. A hold there opens a potential rebound toward $95. However, a clean break below $80 would expose prior consolidation zones with limited technical support.

Solana’s roadmap developments, including Alpenglow and MEV design changes, remain longer-term positives, but they do not resolve near-term selling pressure.

Discover: The best crypto to diversify your portfolio with

Bitcoin Hyper Targets Early Mover Upside as XRP and SOL Test Key Levels

When established altcoins face institutional exits and technical stress simultaneously, capital doesn’t disappear; it rotates. SOL’s 12% weekly drawdown and XRP’s range-bound stagnation are exactly the conditions that push active traders to look earlier in the cycle.

Bitcoin’s own price action has been consolidating, but the infrastructure being built on top of it is accelerating.

Bitcoin Hyper is positioning itself at that intersection. The project is the first-ever Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration. It smart contract that executes at Solana-level speeds, secured by Bitcoin’s network.

The pitch is direct: break Bitcoin’s core constraints like slow transactions, high fees, and no programmability, without sacrificing its trust model. The presale has raised more than $32.7 million to date, with $HYPER currently priced at $0.01368. Staking is live alongside the presale buy option at the current rate of 35% APY.

Bitcoin Hyper presale details are available here.

The post Goldman Sachs Dumps XRP and SOL: Altcoins Market Could Crash appeared first on Cryptonews.

Robinhood Chain has recorded $500 million in daily Uniswap trading volume within just eight days of launch, lifting total value locked above $106 million and pushing the Arbitrum-powered network into the top ranks of decentralized finance activity.

Summary

- Robinhood Chain reached $500 million in daily Uniswap trading volume within eight days of launch.

- Ethena’s $50 million deposit helped push the network’s TVL above $106 million.

- Pump.fun integration, tokenized stocks, and gas fee waivers have accelerated early ecosystem growth.

DeFiLlama data shows the network’s total value locked climbed to more than $106 million after surging 159% in 24 hours, while cumulative addresses approached 200,000. The same data places Robinhood Chain behind only Ethereum mainnet in 24-hour Uniswap trading volume, an unusually rapid rise for a newly launched Layer 2 network.

Uniswap activity on the chain reached $500 million on July 8 after cumulative trading volume had already crossed $250 million during its first week.

Institutional liquidity has fueled the TVL jump

Most of the recent capital increase has come from institutional DeFi flows rather than retail participation.

According to DeFiLlama, nearly $90 million of Robinhood Chain’s locked value is held on the Morpho lending protocol, which powers the roughly 7% annual percentage yield available through Robinhood Earn on USDG deposits.

The largest catalyst came from Ethena, which deposited $50 million into a Steakhouse Financial-managed USDG vault on Morpho in a single transaction. That transfer accounted for much of the network’s sharp one-day TVL increase and highlighted how concentrated institutional liquidity can rapidly reshape early DeFi metrics.

Robinhood Chain also launched with full support for Uniswap’s v2, v3, v4 and UniswapX infrastructure from day one. Trading activity has centered on Wrapped Ether (WETH), memecoins and tokenized equity assets including NVDA, AAPL and GOOG, giving the network exposure to both crypto-native and tokenized real-world asset markets.

Ecosystem expansion has drawn fresh market attention

Robinhood chief executive Vlad Tenev has continued to position the network around tokenized real-world assets while acknowledging growing meme coin demand. In a July 8 post on X, Tenev wrote that as Robinhood develops Robinhood Chain into “the best chain for RWA,” it is “a great chain for memes, too.”

Support from Pump.fun arrived the same day, allowing users to trade Robinhood Chain tokens directly using SOL without bridging assets. The integration quickly boosted activity around the memecoin CASHCAT, adding another source of transaction volume shortly after the chain’s launch.

A separate filing with the U.S. Securities and Exchange Commission disclosed that Tenev sold 375,000 Class B HOOD shares under a prearranged Rule 10b5-1 trading plan.

According to the filing, the shares were sold between $112.22 and $118.13, generating roughly $43.6 million after HOOD stock had already gained more than 40% over the previous month, supported in part by enthusiasm surrounding Robinhood Chain.

Activity on the network has also lifted related crypto assets. UNI, Uniswap’s governance token, rose as much as 14% alongside the surge in trading volume. Robinhood Chain processes blocks every 100 milliseconds compared with Ethereum’s roughly 12-second block time, while Chainlink supplies oracle infrastructure for tokenized equities. Robinhood is also waiving gas fees for the network’s first 90 days, reducing transaction costs during its early growth phase.

Institutional interest in tokenized finance had already been building before the launch. Earlier this week, ARK Invest increased exposure to crypto-related stocks, adding to expectations that companies connected to tokenized assets could continue attracting investor attention.

At the same time, regulatory risks remain. SEC guidance published in January 2026 identified tokenized debt securities as an area for increased scrutiny, while Robinhood Chain’s current TVL remains heavily concentrated in Morpho, meaning large liquidity withdrawals could materially affect the network’s headline metrics.

Decentralized finance tokens have outperformed Bitcoin over the past month, a divergence Bitwise says may reflect a “quiet re-rating” of the sector rather than a short-lived bounce. In its latest crypto market review, the firm pointed to a steep change in relative performance during June: Bitcoin fell about 22%, while Bitwise’s index of tokens tracking major DeFi protocols declined roughly 4% over the same period.

Bitwise described the relative stability as unusual because DeFi tokens are typically among the first assets traders trim when risk appetite drops. The report argues that the sector’s volatility profile may be shifting as more traditional institutions use DeFi infrastructure—support that, in Bitwise’s view, has helped stabilize the broader ecosystem.

Key takeaways

- Bitwise’s DeFi token index fell about 4% in June versus Bitcoin’s ~22% drop, suggesting DeFi held up unusually well.

- Bitwise links the resilience to improving token economics and a narrowing gap between DeFi usage and token value.

- Institutional participation is cited as a stabilizing force as firms build on major DeFi names such as Morpho and Jupiter, with Aave highlighted for generating roughly $900 million in the past year.

- Despite token strength, total DeFi value locked has fallen—CryptoRank reported a decline to just over $70 billion from around $115 billion in January.

- Bitwise expects stablecoin-focused announcements to intensify before the GENIUS Act takes effect in January 2027, and it flags the CLARITY Act as a near-term volatility catalyst.

Why Bitwise thinks DeFi is being re-priced

Bitwise’s core observation is that DeFi’s traditional pattern—bigger swings than Bitcoin during downturns—has not played out in the most recent month. The firm said the relative performance difference is both “unusual” and largely absent from mainstream discussion, implying that market positioning may be lagging what token-level pricing is already signaling.

The report also frames this as more than a simple momentum story. Bitwise argues that DeFi token economics have been improving and that the historical disconnect between how much the platforms are used and how valuable their tokens become is narrowing. In that framing, outperformance is less about speculation and more about demand for DeFi services translating into token relevance.

Bitwise further points to real-world institutional usage as a stabilizer. It specifically names Morpho and Jupiter as examples of areas where institutions have started building, and it cites Aave’s activity—stating that Aave generated approximately $900 million in the past year—as evidence that core DeFi markets remain economically active even when the broader crypto market cools.

What’s inside Bitwise’s DeFi index

Bitwise’s DeFi index fund is market-cap weighted, and its current composition sheds light on why the basket has been resilient. The index allocates about 61% of weight to Hyperliquid’s native token (HYPE), which is tied to the perpetuals exchange ecosystem. Bitwise noted that HYPE has gained more than 160% so far this year.

The index also includes other prominent DeFi exposure, including Uniswap (UNI), Ondo (ONDO), and Aave (AAVE), among others. Despite being major constituents, these names have generally declined over the year-to-date period, with Bitwise stating that several of them are down double digits. That matters for investors because it suggests the overall index performance is being supported by a concentrated outlier (HYPE) while other widely followed protocols face their own drawdowns.

Value locked is down—resilience may not mean growth

Token performance does not automatically translate into increased capital deployment. While Bitwise’s index held up better than Bitcoin in June, CryptoRank reported that total value locked (TVL) in DeFi declined sharply throughout 2026.

According to CryptoRank data cited on June 24, DeFi TVL dropped nearly 40% so far this year, falling to just over $70 billion from roughly $115 billion in January. The data provider attributed much of the decline to a major correction in early October that followed a prior peak in the broader crypto market—when Bitcoin reached a high of more than $126,000.

CryptoRank also suggested the current drawdown is smaller than what occurred during the 2022 bear market, implying relative durability. Taken together, the token-vs-TVL split points to an important nuance for readers: DeFi can experience weaker liquidity and still see token pricing stabilize or improve—especially if parts of the ecosystem (like derivatives venues or specific liquidity markets) remain relatively favored by traders and institutions.

Policy catalysts: stablecoins and the CLARITY Act

Bitwise’s report extends beyond performance comparisons by highlighting regulatory and legislative developments it expects to influence market conditions. One major focus is stablecoins ahead of the GENIUS Act, a stablecoin-regulating bill that was made law in the US last year and is set to take effect in January 2027.

Bitwise said it expects “a steady run of large firms” to announce stablecoin projects ahead of GENIUS implementation. The firm also noted that stablecoin supply has remained supported through the recent downturn. In Bitwise’s view, continued supply growth should benefit major settlement rails such as Ethereum and Solana during the current quarter as regulators finalize rulemaking around the GENIUS Act.

On market structure, Bitwise said the next three months could be “make-or-break” for the CLARITY Act, currently under review and negotiation in the Senate. Bitwise said it believes the bill has an unlikely chance of passing before the November elections.

The report outlines a two-path scenario. If CLARITY passes, Bitwise argues it could signal the bottom of the current bear market. If it fails, Bitwise expects volatility at first, followed by a period of “clearing of uncertainty” as the industry continues building under a regulatory environment it characterizes as more pro-SEC and CFTC focused.

For investors, the practical takeaway is that the market may be balancing near-term uncertainty on structure policy with longer-term momentum from stablecoin-related deployment. With DeFi tokens holding up comparatively well against Bitcoin even as TVL falls, traders may increasingly look at whether liquidity breadth returns—or whether token strength continues to concentrate in specific segments.

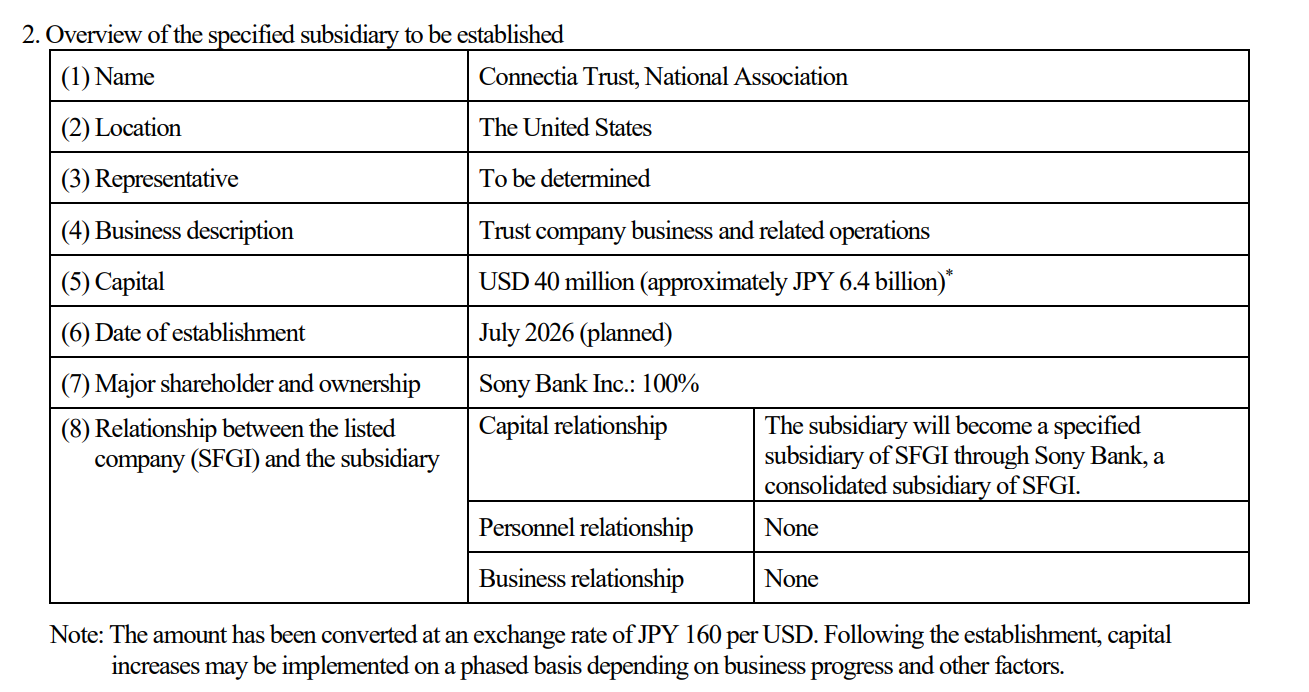

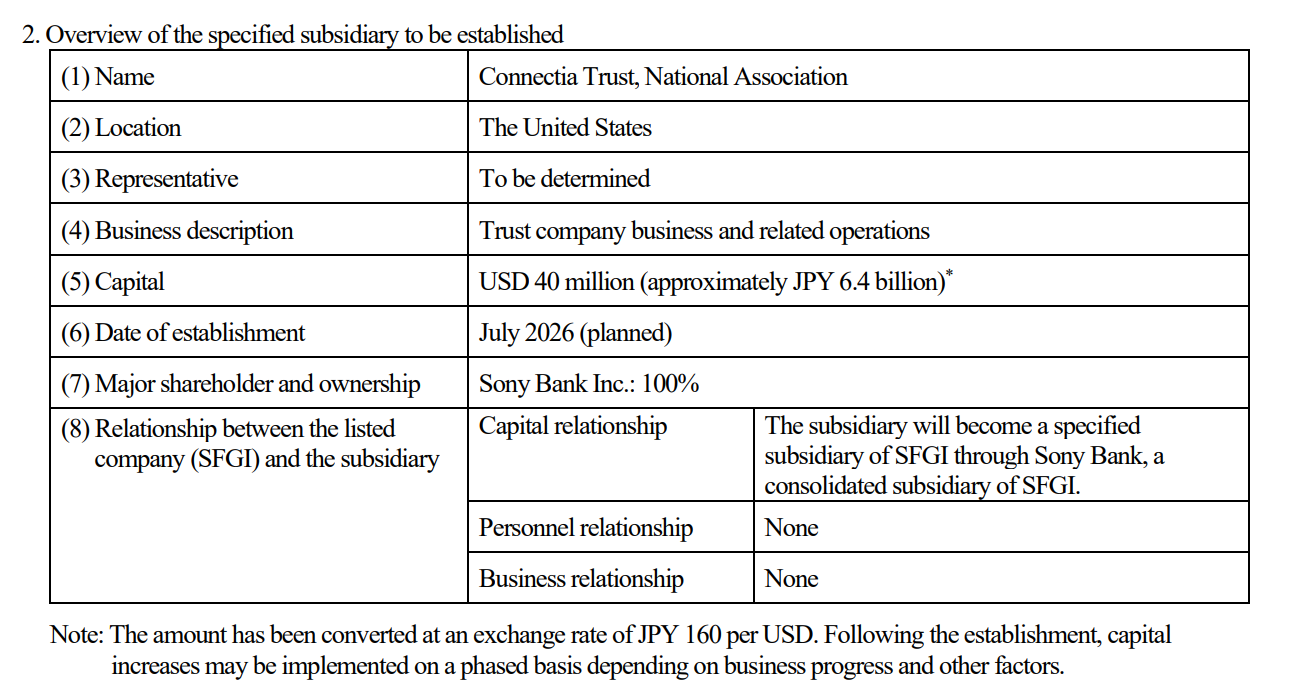

Sony Bank, a subsidiary of Sony Financial Group, said it’s received preliminary approval to establish a new US national trust bank subsidiary that will issue US dollar-denominated stablecoins.

The new unit, Connectia Trust, National Association, gained preliminary approval from the Office of the Comptroller of the Currency (OCC) on July 2.

It will be fully owned by Sony Bank and will support the issuance and management of US dollar-denominated stablecoins, according to a Monday announcement by Sony Financial Group.

The approval signals Sony’s entry into regulated US stablecoin issuance, part of a long-term digital asset business foundation, which it is backing with $40 million in starting capital.

Sony Bank said that no business activities or stablecoin issuance will be conducted until all approvals and authorizations are received, including the final approval from the OCC. The conglomerate plans to launch the stablecoin subsidiary this month.

Cointelegraph has approached Sony Bank for more details about the business and whether it would include the launch of a proprietary stablecoin, but did not receive a reply by time of publication.

Earlier in March, Sony Bank signed a memorandum of understanding with stablecoin issuer JPYC Inc. to study whether the Japanese yen-pegged stablecoin can be connected more directly to the bank’s deposit rails.

Overview of the specified Sony Bank subsidiary to be established in the US. Source: Sony Bank

Banks seek stablecoin integrations despite regulatory headwinds

More of the world’s biggest banks are seeking to integrate stablecoin infrastructure into traditional systems, despite regulatory headwinds in the US.

Last Thursday, British multinational bank Standard Chartered and USDC issuer Circle said they developed a system that lets institutions mint and redeem the USDC stablecoin through a bank-led onboarding process. Clients will be able to mint and redeem the US dollar-backed stablecoin directly through StanChart’s platform instead of opening separate accounts with Circle.

Related: SWIFT launches blockchain ledger with 17-bank tokenized deposit pilot

Meanwhile, Congressional progress on the first regulatory framework for digital assets in the US, the CLARITY Act, remains stalled, prompting Galaxy Digital to cut its odds of the bill becoming law in 2026 to 50%.

While the legislation is set for a House of Representatives hearing on July 17, Galaxy’s head of research, Alex Thorn, warned that the bill may not have enough floor time before the Senate is scheduled to leave for its traditional four-week recess on Aug. 8

The bill cleared the Senate Banking Committee in May, but faced pushback from most Democrats and the banking industry over concerns it would allow crypto firms to offer yields on stablecoins without facing the same requirements as traditional financial institutions.

At the beginning of June, more than 200 crypto companies and related organizations urged the Senate to pass the CLARITY Act, in a letter shared by crypto lobby group Stand With Crypto.

In May, JPMorgan CEO Jamie Dimon told Fox Business that banks will continue to “fight” against the current version of the CLARITY Act and said that crypto companies wanting to offer yield-bearing products “should apply for banking charters.”

Magazine: Wall Street’s tokenization boom has a liquidity problem: Axis CEO

PI is down 12% this week and is quickly approaching $0.10. Will buyers return there?

PI Network (PI) Price Predictions: Analysis

Key support levels: $0.10, $0.085

Key resistance levels: $0.13, $0.16

PI Arrives at $0.10

As expected, the price of PI has reached the 10-cent support, a key psychological level. So far, sellers appear to have total control, considering that the price has crashed 12% since last week.

If buyers plan to return, then this is a key moment for them to take back control. Ideally, they defend the $0.10 level and send PI into a bounce. The current resistance is found at $0.13, and only if this level breaks can we hope for a sustained rally.

Decisive Moment Ahead

With the $0.10 key support under pressure, PI is found at a crossroads. Bounce here, and buyers have a chance to recover some of the most recent losses. Fail to defend this level, and PI may crash even more and into single digits.

A look at the momentum indicators does not give much confidence that buyers stand a chance. The daily RSI is below 30, and the MACD has been making lower lows since a bearish cross in late June.

Sell Volume Explodes

Since mid-June, the sell volume has been making higher highs. That’s a clear bearish signal, and there is little hope this can reverse any time soon. Best to wait for a reaction at the 10 cents support, if it comes.

If the current momentum doesn’t change, expect sellers to continue to have the upper hand as they push PI to new record lows, with $0.085 as the next key target.

The post Why Is the Pi Network (PI) Price Down This Week? appeared first on CryptoPotato.

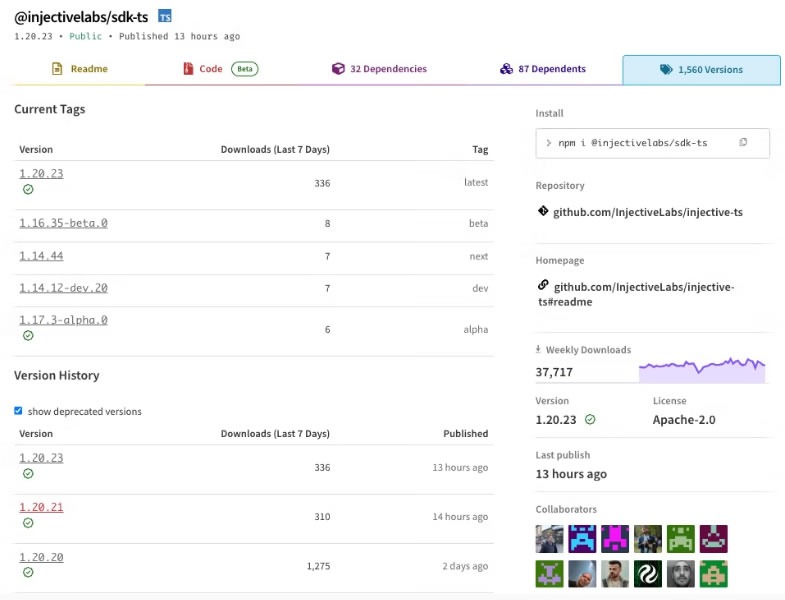

Hackers compromised a widely used Injective software package in a supply chain attack with malware designed to steal crypto wallet private keys, adding to a growing attack vector involving attackers using legitimate platforms to deliver malicious payloads.

Security firm Socket discovered on Thursday that a popular npm (node package manager) package with around 50,000 weekly downloads used for building on the Injective blockchain was maliciously modified to steal wallet private keys and seed phrases.

The large number of downloads makes the incident “significant for developers and applications that handle Injective wallet workflows,” Socket researchers said. The malicious code has since been removed.

The software supply chain attack is a relatively new attack vector in which hackers don’t target a blockchain’s cryptography or smart contracts directly, but instead compromise trusted developer tools used to build wallets, exchanges and apps.

Injective is an interoperable layer 1 designed for DeFi applications. Its usage has dwindled over the past two years, with total value locked shrinking by 88% to current levels of $8.2 million from its $71 million peak in mid-2024, according to DefiLlama.

Secretly copying private keys and phrases

Version 1.20.21 of the @injectivelabs/sdk-ts npm package was modified through a compromised developer GitHub account, with suspicious commits beginning June 8. It was also pinned across 17 other packages in the Injective Labs npm scope, “exposing users who may not have installed the SDK [software development kit] directly,” Socket said.

“The malicious release hooks wallet key-derivation functions, records private keys and mnemonics, and exfiltrates them through fake telemetry,” Socket explained.

The malicious code hooked into normal functions used to generate wallet keys, and whenever a developer’s app used these functions, it secretly copied the seed phrase or private key. The compromised data was then encoded and sent to a web address that looked like a legitimate Injective network server.

“Any keys or mnemonics passed through affected packages should be treated as compromised,” Socket added.

Related: ‘TrapDoor’ malware targets crypto dev tools in supply chain attack

Socket reported that the developer whose account was infiltrated quickly detected the compromise, but the malware had been downloaded more than 300 times, and “the campaign itself isn’t yet fully contained.”

Injective CEO Eric Chen said, “it’s already fixed, and the affected versions on npm are already deprecated.” No funds on the network are at risk, he added, and Socket did not specify whether any funds were stolen in the incident.

The compromised npm package was downloaded 310 times. Source: Socket

Wallet compromises most costly this year

The Security Alliance (SEAL) said in its second-quarter threat report that attackers are increasingly using legitimate platforms like GitHub, npm and Google to deliver payloads.

“In some cases, compromised systems are being used to push malicious code directly into a company’s own GitHub repositories, turning a single compromise into a distribution channel for the next one.”

SEAL added that the malware itself has also gotten more comprehensive, “with cross-platform payloads, including a rise in macOS-specific campaigns, that combine infostealers, RATs (remote access trojans) and backdoor capabilities in a single package.”

A similar supply chain attack hit Axios npm releases in March, while a malware campaign called TrapDoor was discovered in May targeting crypto, DeFi, AI and security developers.

GitHub itself was exploited on May 20 when it reported unauthorized access to its internal repositories following the compromise of an employee’s device.

Wallet compromises were the most costly attack vector in the first half of 2026, with $444 million stolen across 33 incidents, CertiK reported Monday.

Features: Bitcoin’s quantum dilemma: Bigger blocks or STARK proofs?

WD-40 Company shares traded as much as 14.5% higher in Thursday overnight trading via Blue Ocean ATS. The household lubricant maker beat Wall Street’s revenue and profit estimates by wide margins.

WD-40 also raised its full year guidance. The company pointed to stronger than expected demand for its core spray lubricant business.

Revenue and Profit Both Clear Estimates

WD-40 reported $195.1 million in sales, a 24.3% jump from a year ago. That easily beat the $173 million Wall Street expected. Profit per share also beat expectations. WD-40 earned $2.24 for every share, well above the $1.57 analysts had penciled in.

Two other numbers show how efficiently WD-40 turned sales into profit. Operating margin, the share of revenue left after covering core costs, rose to 20.7% from 17.4% a year ago. That means the company kept more of every dollar it made.

Free cash flow margin, the actual cash left over after running the business, dipped to 15% from 21.6%. Even with that dip, it still beat WD-40’s average over the past two years.

Zooming out, WD-40 has grown sales by 8.6% a year on average over the past three years. Analysts now expect growth to slow to just 3% over the next 12 months, a sign that this quarter’s strength may be hard to repeat.

While Chips Dominate, WD-40 Delivers

Wall Street’s biggest gains this year have mostly gone to one theme: AI chips and the infrastructure behind them. Nvidia, Micron, and their peers have swung by double digits on a single earnings report, driven by massive bets on data centers and computing power. WD-40 makes none of that, but still found a way to beat expectations and reward shareholders.

The company raised its full-year revenue guidance to $682.5 million at the midpoint, a 6.2% increase from its prior $642.5 million target. Full-year profit guidance also climbed, with earnings per share now expected to reach $6.20 at the midpoint, above what analysts had projected.

Shares closed at $272.00 after the report, pushing WD-40’s market capitalization to $3.02 billion. That’s a fraction of a single AI chipmaker’s daily swing in market value, but it’s a reminder that steady, unglamorous businesses can still deliver when they execute well.

The post WD-40 Greases Wall Street’s Expectations With Blowout Q2 Beat appeared first on BeInCrypto.

Spot Bitcoin and crypto ETFs have become the largest force in the market, absorbing and releasing billions of dollars of coins through a mechanism most of their own investors have never seen. This guide opens the machine: authorized participants, the creation and redemption loop, in-kind versus cash models, why a dollar of flow becomes a dollar of real buying or selling, how the arbitrage keeps ETF prices honest, and how to read the daily flow numbers everyone quotes.

Summary

- Spot crypto ETFs create and redeem shares through authorized participants, making ETF inflows and outflows translate into real buying and selling of cryptocurrencies.

- The creation and redemption process keeps ETF prices closely aligned with the value of the underlying coins through continuous arbitrage.

- Daily ETF flow data reflects actual spot market demand rather than investor sentiment alone, making it one of the market’s most closely watched indicators.

The most important trading desk in crypto does not trade on a crypto exchange. It sits inside a handful of Wall Street firms called authorized participants, and its job is to keep the price of spot crypto exchange-traded funds glued to the price of the coins they hold, by creating and destroying ETF shares in industrial quantities. When headlines report that Bitcoin funds bled $4.51 billion in a month, or took in $221.7 million in a day, they are reporting this machine’s output, and the machine’s mechanics, not sentiment, are why those flows translate directly into buying and selling of actual coins.

The spot ETF era has made these funds the marginal force in crypto’s market structure: they hold coins worth more than most national reserves, their daily flows are the most watched data series in the asset class, and their behavior in stress, as the recent record outflow month showed, can dominate price for quarters at a time. Yet the mechanism underneath, creation units, authorized participants, in-kind transfers, net asset value arbitrage, remains folk knowledge at best among the traders who quote its outputs daily.

This guide is the missing manual. It covers what a spot crypto ETF actually is and how it differs from the futures products and trusts that preceded it, the creation and redemption loop that is the entire engine, the in-kind versus cash distinction and why it matters for taxes and mechanics, the arbitrage that keeps the share price tracking the coins, why flows equal real spot demand and supply, what the daily flow numbers do and do not mean, and the honest list of what can go wrong.

What a spot ETF is, and what it replaced

A spot crypto ETF is a fund that holds the actual asset, real Bitcoin or Ether in institutional custody, and issues shares that trade on a stock exchange, each share representing a claim on a sliver of the coin pile. The design goal is simple to state and hard to engineer: make the share price track the coin price, continuously, within basis points, so that buying the ETF is economically equivalent to buying the coin, inside a brokerage account, with no wallets, keys, or crypto exchanges involved.

Everything distinctive about the structure exists to serve that tracking, and the point is sharpest against what came before. Futures-based ETFs held derivative contracts rather than coins and bled value to the cost of rolling those contracts month after month. Closed-end trusts held real coins but issued a fixed number of shares with no redemption mechanism, so their prices drifted to enormous premiums and discounts against their holdings, famously reaching double-digit discounts, because nothing forced the share price and the coin value together. The spot ETF’s innovation is precisely the forcing mechanism: an open-ended share supply that expands and contracts through arbitrage, executed by authorized participants. That mechanism is also, not incidentally, what separates an ETF from the treasury companies whose share prices float freely above and below their coin holdings: a treasury stock has no redemption loop, so its premium is a sentiment gauge; an ETF has one, so its premium is an arbitrage error measured in hundredths of a percent.

The engine: creation and redemption

The heart of every ETF is a wholesale market invisible to retail holders. ETF shares are not created when an investor clicks buy; they are created in bulk blocks called creation units, typically tens of thousands of shares at a time, by authorized participants, large trading firms and banks that hold agreements with the fund’s issuer.

The creation loop runs like this. When investor demand pushes the ETF’s market price even slightly above the value of the coins backing each share, its net asset value, an authorized participant sees free money: it buys the equivalent amount of actual coin on crypto markets, delivers it to the fund (or delivers cash the fund uses to buy the coin, a distinction the next section unpacks), receives newly minted ETF shares at NAV in exchange, and sells those shares into the stock market at the premium price. The AP pockets the spread; the share supply expands; the premium collapses back toward zero. Redemption is the mirror: when the ETF trades below NAV, an AP buys cheap shares on the stock market, returns them to the fund, receives coin (or cash from coin sales) worth full NAV, and sells the coin, pocketing the discount and shrinking the share supply until the price snaps back.

Read the loop again and notice what it implies, because it is the single most important fact in this guide: every net creation is real coin purchased on the market, and every net redemption is real coin sold. The flows are not sentiment surveys or paper reallocations; they are the visible exhaust of actual spot transactions, executed by the APs against crypto exchanges and OTC desks. A $500 million inflow day means roughly $500 million of coins were bought and moved into custody; a $4.51 billion outflow month means that much was sold out of it. This is why ETF flow data moves markets and why it deserves the obsessive attention it gets: it is the rare series that measures demand in the units that matter, coins actually changing hands, disclosed daily, to the dollar.

In-kind versus cash: the plumbing distinction

Creations and redemptions come in two flavors, and the difference, invisible to holders, shapes everything behind the scenes. In an in-kind model, the AP delivers and receives the actual asset: coins go in for shares, shares come back for coins, and the fund itself never trades. In a cash model, the AP delivers and receives dollars, and the fund’s own trading desk executes the coin purchases and sales. US spot crypto ETFs launched under a cash-creation regime, a regulatory choice that kept broker-dealers at arm’s length from handling coins, and the industry has since moved toward permitting in-kind, the structure ETFs use for every other asset class.

The distinction matters three ways. Mechanically, in-kind is cleaner: the fund holds coins and swaps them for shares, full stop, while cash models interpose a trading step where execution costs and timing slippage live. Tax-wise, in-kind is the quiet superpower of the ETF wrapper, letting funds shed appreciated assets through redemptions without realizing taxable gains, an efficiency cash models partially forfeit. And market-structure-wise, the cash model makes the fund itself a large, scheduled trader in the underlying market, whose execution patterns around creations and redemptions are studied, and sometimes anticipated, by everyone else. Either way, the coins end up in institutional custody, segregated wallets at qualified custodians, whose addresses on-chain observers track as a real-time audit of the funds’ holdings, one of the few places where traditional finance’s opacity meets crypto’s radical transparency and transparency wins.

The decade-long fight to exist

The mechanics above were nearly a decade in the courts and dockets before they were allowed to run, and the history explains several of the structure’s present quirks. The first spot Bitcoin ETF application was filed in 2013; the following ten years produced an unbroken record of rejections, with regulators citing manipulation risk in underlying crypto markets and the absence of surveillance agreements. The industry routed around the wall with inferior vehicles, the futures ETFs with their roll costs, the closed-end trusts with their wild premiums and discounts, and each inferior vehicle’s flaws became, ironically, evidence in the eventual case: the trust’s persistent discount showed concretely that investors were being harmed by the absence of a redemption mechanism, and a federal court’s 2023 ruling that rejecting spot products while approving futures ones was arbitrary broke the dam. The January 2024 approvals arrived as a batch, launching a dozen funds into simultaneous competition, which is why the market’s structure is a fee war among near-identical products rather than one dominant fund, and why issuer competition drove management fees to levels that undercut most of the world’s equity index funds within weeks of launch.

The cash-only creation requirement was the approvals’ regulatory fingerprint, imposed so that broker-dealers never touched coins directly, and its gradual relaxation toward in-kind is the quiet second act of the products’ regulatory story, unlocking the tax efficiency and mechanical cleanliness the wrapper was always meant to have. Ether funds followed Bitcoin’s, staking-enabled versions followed those, and the approval architecture built for two assets is now the template every other crypto asset’s ETF hopes, conditional on the classification framework Congress is deciding, to pass through. Ten years of rejection, in hindsight, built the most consequential piece of the structure: by the time the machine was switched on, the custody, benchmark, and surveillance infrastructure had been argued into institutional grade, which is a large part of why it has run through record inflows, record outflows, and a full market cycle without a single structural incident.

What holding the ETF actually costs

The wrapper’s convenience has a price list worth itemizing, because it is subtracted silently. The management fee, deducted daily from the fund’s assets, compounds into the tracking: a fund charging a quarter of a percent will lag its coin by exactly that much per year, before anything else. The NAV-timing gap adds a subtler cost for traders: the official NAV is struck once daily against an index snapshot, so orders executed at market prices far from the snapshot inherit tracking noise, trivial for holders, real for anyone trading the products tactically. Spreads and premiums cost basis points on entry and exit, tightest in the giant funds and wider in the small ones, and the arbitrage that minimizes them is weakest at the open and around crypto’s violent hours. And the structural exclusions, no staking yield in most products, no on-chain utility, no self-custody, are opportunity costs rather than fees, the value surrendered for the brokerage account’s convenience. Summed, the wrapper costs a diversified long-term holder a fraction of a percent annually against holding coins directly, which is, by the standards of what the access is worth to the capital that uses it, among the better bargains in finance, and knowing the itemization is what separates choosing the bargain from defaulting into it.

Why the tracking holds, and when it slips

The arbitrage loop keeps spot ETF prices within a whisker of NAV in normal conditions, but the whisker is worth understanding, because its width is a live diagnostic of market health.

The ETF trades during stock-market hours; the coins trade around the clock. Overnight and on weekends, the share price is frozen while the asset moves, so every open begins with a gap the APs arbitrage away in minutes, and the fund’s official NAV, struck once daily against a benchmark index of crypto exchange prices, is itself a snapshot of a moving target. Small premiums and discounts, hundredths to tenths of a percent, are therefore constant and meaningless. What matters is persistence: a discount that survives arbitrage signals that APs cannot or will not close it, because coin markets are too volatile to hedge, because borrowing shares is hard, or because redemption plumbing is stressed, and persistent dislocations in ETF land have historically been the smoke that precedes fire in the underlying market. The same logic runs through every wrapped-asset structure in finance, tokenized stocks keep their pegs by the identical mint-and-redeem loop, and the universal rule holds here: the wrapper is only as good as the arbitrage that binds it, and the arbitrage is only as good as the least reliable step in its loop.

One more participant deserves a paragraph: the basis trader. Because ETF shares can be held long against short futures positions, a meaningful fraction of ETF holdings at any time belongs not to investors who want crypto exposure but to arbitrageurs harvesting the spread between spot and futures prices. When that spread compresses, these holders redeem, mechanically, with no view on the asset, which means headline outflows always mix conviction selling with carry-trade unwinding in proportions no outside observer can fully separate. It is the single most important caveat when reading the flow numbers, and it cuts both ways: some of the most alarming outflow streaks in the products’ history were substantially plumbing, and some of the most celebrated inflow runs were substantially leverage.

A worked example ties the machinery together. Suppose strong demand lifts a Bitcoin ETF’s market price 0.2% above its NAV during a rally. An authorized participant simultaneously buys, say, $50 million of Bitcoin across exchanges and OTC desks and shorts the equivalent in ETF shares at the rich price, locking the 0.2% spread, about $100,000, minus costs. It delivers the coins (or cash) to the fund, receives creation units at NAV, and uses the new shares to close its short. Net result: the AP earned a riskless spread, the fund grew by $50 million of coins in custody, the day’s flow report shows a $50 million inflow, and the ETF’s premium collapsed back to a basis point or two. Reverse every step for a redemption into a discount. Multiply by every AP, every fund, and every trading day, and the aggregate is the flow series the market watches: not a survey, but the arithmetic residue of thousands of such loops, each one a real spot transaction with a paper trail. When the loops run large in one direction for weeks, as they did through June’s record redemptions, the ETF complex is not reflecting the market’s direction; at the margin, it is the market’s direction.

One design detail rounds out the picture: creation units keep the wholesale and retail layers honest simultaneously. Retail investors trade shares among themselves on the exchange all day without touching the fund at all, and only the net imbalance, the demand the secondary market cannot internally match, flows through the APs into creations or redemptions. The fund’s coin pile therefore moves only when the market’s aggregate position actually changes, which is why the flow series is such a clean demand signal: it nets out all the churn and reports only the residual conviction.

Reading the flows like a professional

The daily numbers reward a few disciplined habits. Read trends, not days: single sessions are noise, dominated by one fund’s creation calendar or one AP’s book, while multi-week runs, like the ten-day outflow streak that marked June’s low, are regime information. Distinguish flows from assets: net asset values fall when prices fall even while money flows in, and rise in rallies even during redemptions, so AUM headlines are mostly price echoes; the flow line is the demand signal. Watch the spread of participation: inflows concentrated in one fund are a product story, inflows across all issuers are an allocation story, and the custody balances that flows build are a structural supply force in their own right. Note the interaction with market hours: flows print against a US trading day, so they lag and compress around-the-clock crypto moves, and Monday’s number carries the weekend. And always carry the basis-trade caveat: the flow series measures shares created and destroyed perfectly, and measures investor belief only through that imperfect proxy.

Held together, the mechanics justify a conclusion stronger than the usual disclaimers: the spot ETF is the most consequential piece of market structure crypto has ever imported, precisely because its plumbing converts distant, regulated, advised capital into spot demand and supply with industrial efficiency and daily disclosure. It made the asset class legible to the largest pools of money on earth, and it made those pools’ behavior legible to everyone else, a two-way window that did not exist before 2024. The machine is neutral; June proved it pumps out as efficiently as it pumps in. Understanding the loop, APs, units, NAV, in-kind, basis, is what separates reading the window from being read through it.

One forward note completes the manual: the machine described here is still being extended. In-kind creation is arriving, staking-enabled funds have begun passing yield through the wrapper, options markets on the ETFs have layered a derivatives complex on top of the flow machine, and the same creation-redemption architecture is being fitted to additional assets as the regulatory perimeter settles. Each extension changes the reading of the flow data slightly, staking funds attract different holders than pure price trackers, options hedging generates mechanical creations and redemptions of its own, and the professional habit is to re-learn the machine’s output as its parts change. What does not change is the core: an arbitrage loop, run by profit-seeking intermediaries, converting the world’s brokerage demand into spot transactions, in public, every day. Crypto spent a decade fighting for that machine, and understanding it is the closest thing the asset class offers to reading its own pulse.

The reader’s bookmark list, finally, is short: each issuer’s daily holdings and flow disclosures, the aggregated flow dashboards the market quotes, the funds’ premium-discount trackers, and the custodian wallet monitors that let anyone verify the coins on-chain. Fifteen minutes a week across those four sources reproduces everything in this guide with live numbers, and turns the most quoted data series in crypto from a headline you consume into a machine you can actually read.

A last piece of perspective for scale: the creation-redemption machine described here is not a crypto invention but a thirty-year-old piece of market technology, refined across equity and bond ETFs holding trillions, and its arrival in crypto was less an experiment than a transplant of proven plumbing into a new asset. That pedigree is why it worked immediately at record scale, and it is also the quiet reassurance inside the daily drama of the flow numbers: whatever the coins do, the machine that wraps them has been stress-tested by every market crisis since the 1990s, and it has never been the thing that broke.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Structural details are current as of July 9, 2026, and may change. Always do your own research.

Frequently asked questions

How does a spot crypto ETF work in simple terms?

The fund holds real coins in institutional custody and issues shares that trade on a stock exchange, with each share representing a fraction of the coin pile. Large trading firms called authorized participants create new shares by delivering coins or cash to the fund, and destroy shares by redeeming them for coins or cash, an arbitrage loop that keeps the share price tracking the coin price within tiny margins.

What is an authorized participant?

An authorized participant, or AP, is a large financial firm with an agreement to create and redeem ETF shares in bulk blocks called creation units. APs arbitrage gaps between the ETF’s market price and the value of its holdings: buying coins and minting shares when the ETF trades rich, redeeming shares for coins when it trades cheap. Their profit motive is the mechanism that keeps the ETF honest.

Why do ETF flows move the crypto market?

Because flows are real spot transactions. A net inflow means authorized participants bought actual coins to create new shares; a net outflow means coins were sold to fund redemptions. Unlike sentiment indicators, the flow data measures coins genuinely changing hands, which is why sustained flow trends have become one of the most powerful forces in crypto price formation.

What is the difference between in-kind and cash creation?

In-kind creation swaps coins directly for shares, with the fund never trading; cash creation has the AP deliver dollars, which the fund’s own desk uses to buy coins. In-kind is mechanically cleaner and more tax-efficient, and it is the standard across ETFs generally; US spot crypto funds launched cash-only for regulatory reasons, with the industry since moving toward in-kind.

Can a spot ETF trade at a premium or discount?

Briefly and slightly, yes, especially at market opens after the coins moved overnight, but arbitrage closes gaps within minutes in normal conditions. Persistent premiums or discounts are rare and diagnostic: they signal that the creation-redemption loop is stressed, which historically has been a warning sign worth taking seriously. This tight tracking is the key difference from closed-end trusts and treasury stocks, which can drift far from their holdings’ value.

Do ETF outflows always mean investors are bearish?

No. A significant share of ETF positions belongs to basis traders holding shares against short futures to harvest the spread, and when that spread compresses, they redeem mechanically with no market view. Headline outflows therefore mix genuine de-risking with carry-trade plumbing, which is why flow trends matter more than single prints and why context from funding and futures data helps.

Where are the ETF’s coins actually kept?

With qualified institutional custodians, in segregated cold-storage wallets whose addresses on-chain analysts track publicly. The holdings are disclosed daily by the funds and independently observable on the blockchain, making spot crypto ETFs among the most transparent pooled investment vehicles in existence.

Is buying the ETF the same as buying the coin?

Economically it is very close: the tracking is tight and the convenience is real. The differences are structural: ETF investors hold shares, not coins, cannot self-custody or use the assets on-chain, trade only during market hours, pay an annual management fee, and rely on the fund’s custody arrangements. For brokerage-account exposure those trade-offs are usually acceptable; for crypto-native uses they are disqualifying.

Decentralized finance (DeFi) tokens have held up unusually well against Bitcoin over the past month, suggesting the market may be “quietly re-rating” the sector, says crypto index fund maker Bitwise.

Bitcoin (BTC) fell about 22% in June, while Bitwise’s index tracking tokens from major DeFi protocols fell only 4% over the same period, Bitwise said in a report Thursday.

“DeFi usually swings much harder than Bitcoin, so holding up this well is unusual, and almost no one is talking about it,” it said.

DeFi tokens have a reputation for being highly volatile during crypto market swings, as they’re the first to be sold by risk-averse traders. However, Bitwise said this is changing as traditional institutions have begun to use the protocols, which have stabilized the wider DeFi ecosystem.

“We think DeFi is quietly re-rating,” Bitwise said. “Token economics are improving, the gap between usage and token value is closing, and real institutions are building on names like Morpho and Jupiter, with Aave alone generating ~$900 million in the past year.”

“We expect DeFi’s outperformance to keep playing out in Q3, the kind of shift the market tends to notice late,” it added.

Source: Bitwise

Bitwise’s DeFi index fund weighs assets by market capitalization, and its current holdings are weighted 61% toward Hyperliquid (HYPE), the native token used by the crypto perpetuals exchange of the same name that has gained more than 160% so far this year.

The index also holds Uniswap (UNI), Ondo (ONDO) and Aave (AAVE), among others, all of which have fallen by double-digit percentages year to date.

DeFi value locked drops over 2026

While HYPE has propped up the value of DeFi tokens, total value locked in DeFi has fallen nearly 40% so far this year through June, declining to just over $70 billion from roughly $115 billion in January, CryptoRank reported June 24.

The crypto data aggregator attributed the market decline to the major correction in early October, which came after the crypto market peak, when Bitcoin hit a high of more than $126,000.

However, the company said the current drawdown remains smaller than during the 2022 bear market, suggesting a more resilient DeFi market.

Bitwise says expect stablecoins, volatility if CLARITY fails

In its report, Bitwise also noted key upcoming events it expects will affect the crypto market.

It said it expects “a steady run of large firms to announce stablecoin projects” ahead of the GENIUS Act, a stablecoin-regulating bill the US made law last year that takes effect in January 2027.

Related: EU lawmakers urge assessing DeFi, staking, NFT regulation

Stablecoin supply has held amid the crypto market downturn, it added, and their growth will positively affect blockchains such as Ethereum and Solana this quarter as regulators finalize their rules for the GENIUS Act.

Bitwise said it also expects the next three months will be “make-or-break for the CLARITY Act,” the crypto market structure bill currently under review and negotiation in the Senate that Bitwise said has an unlikely chance of passing before the November elections.

“If it passes, we believe it likely marks this bear market’s bottom,” Bitwise said. “If it fails, expect volatility initially, then a clearing of uncertainty as the industry keeps building under a pro-crypto SEC and CFTC.”

Features: DeFi hacks shake institutional confidence as risks outpace yields

Shiba Inu saw its largest burn in the last six months, which is typically interpreted as a bullish signal.

However, SHIB’s price remains heavily suppressed in the bear market, and multiple factors point to further downside in the short term.

The Burn and More

On July 8, the SHIB team and community scorched almost 110 million coins. However, the USD equivalent of the coins sent to a dead wallet is negligible, and with roughly 585 trillion coins still in circulation, much bigger burns will be required to trigger a major upswing.

The burning mechanism was introduced in 2022, and its ultimate goal is to make the token scarcer and potentially more valuable (should demand remain stable or head north). It is also important to note that Vitaliк Buterin contributed a significant portion of the approximately 410.8 trillion tokens that have already been burned.

As of this writing, SHIB trades at around $0.00000429, an 8% decline for the past month and a whopping 95% collapse since the all-time high witnessed in 2021. Its market capitalization has dropped to around $2.5 billion, making the meme coin (once among the 20 biggest cryptocurrencies) the 37th-largest digital asset.

Back in the day, Shiba Inu was the subject of numerous optimistic price predictions, but lately the interest in it has faded, and the forecasts are rather grim. Not long ago, the popular trader James Wynn labeled the meme coin “old, dead, and boring,” predicting a potential revival in 5-10 years, when “a bit of nostalgia” could bring it back.

The Bearish Signals

SHIB’s downfall coincides with its falling daily trading volume. X account BSCN revealed that the figure has seen a steady decrease over the last 12 months, plummeting from $637 million in July 2025 to around $50-$100 million nowadays.

The stalled activity on Shibarium is another worrying sign. The layer-2 scaling solution, launched in the summer of 2023 to boost speed, enhance scalability, and lower fees, initially processed millions of transactions. However, following an exploit that disrupted operations last year, daily activity has fallen dramatically to mere thousands.

Weak interest in the broader meme coin sector is another factor that could limit SHIB’s ability to stage a decisive comeback. Dogecoin (DOGE) and many of its rivals were among the best-performing tokens during the last bull cycle, but they are now a pale shadow of their former glory. The market capitalization of the meme coin sector, which once crossed $120 billion, now stands at less than $23 billion.

The post Shiba Inu Burn Rate Goes Parabolic, Yet SHIB Keeps Bleeding: Details appeared first on CryptoPotato.

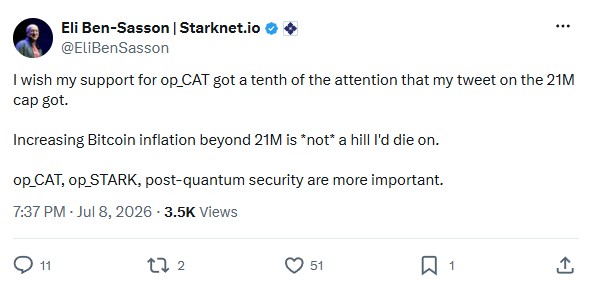

ZK STARKs are the best way to deal with the issues created with making Bitcoin quantum-safe — and to reach mass adoption at the same time — says StarkWare co-founder Eli Ben-Sasson.

What’s more, he claims Blockstream founder Adam Back agrees.

Ben-Sasson has been in the news this week for his controversial suggestion on X to increase Bitcoin inflation to 4% annually. Grok’s analysis of the replies found “zero clear support for the proposal.”

But as the co-inventor of STARKs — quantum-secure, hash-based zero-knowledge proofs — he’s on much firmer ground, with some leading Bitcoin researchers supporting the concept.

Ben-Sasson’s own project Starknet last week announced its own three phase project to become quantum secure.

The problem of large PQ signatures on Bitcoin

Adding zero-knowledge proofs to Bitcoin does not make the blockchain quantum secure by itself. ZK proofs are a way to deal with the problems caused by adding much larger post-quantum (PQ) signature schemes to Bitcoin.

The current crop of PQ signatures approved by the National Institute of Standards and Technology (NIST) is 10 to 100 times larger than Bitcoin’s existing ECDSA and Schnorr signature schemes.

Some argue this could slow the blockchain to fewer than 1 transaction per second. But all of the large transaction signatures for a block could be compressed into a tiny ZK STARK proof. Because the proof would be much smaller than even including the existing signatures, the blockchain may end up running faster.

“If they don’t allow for ZK STARK aggregation, then definitely it will be a very unfortunate move because it won’t really solve the problem … where the problem is ‘can everyone actually use Bitcoin?’” Ben-Sasson said.

“So for that you need massive scale. And for that, you need things like signature aggregation and just increasing the block size isn’t enough.”

Related: StarkWare CEO suggests 4% annual Bitcoin inflation to replace 21M cap

The quantum alternative: Increase Bitcoin’s block size

Marin Ivezic, author of PostQuantum.com and founder of Applied Quantum, told Cointelegraph that Bitcoin’s SegWit scheme reduced the impact of large signatures by up to 75%. But his modeling of NIST’s ML-DSA-44 scheme, which has 2,420 bytes per signature, “puts block capacity at roughly 500 to 700 transactions, down from 2,500 to 3,000 today. That is where the block-size debate comes in.”

Increasing Bitcoin’s block size is a genuine alternative, but the community split over a proposal to double the block size back in 2017. Many of the arguments against remain relevant, as it’s a blunt fix that requires every node to carry, store and verify much more data. That’s more expensive and requires more equipment, which critics argue pushes the network toward centralization.

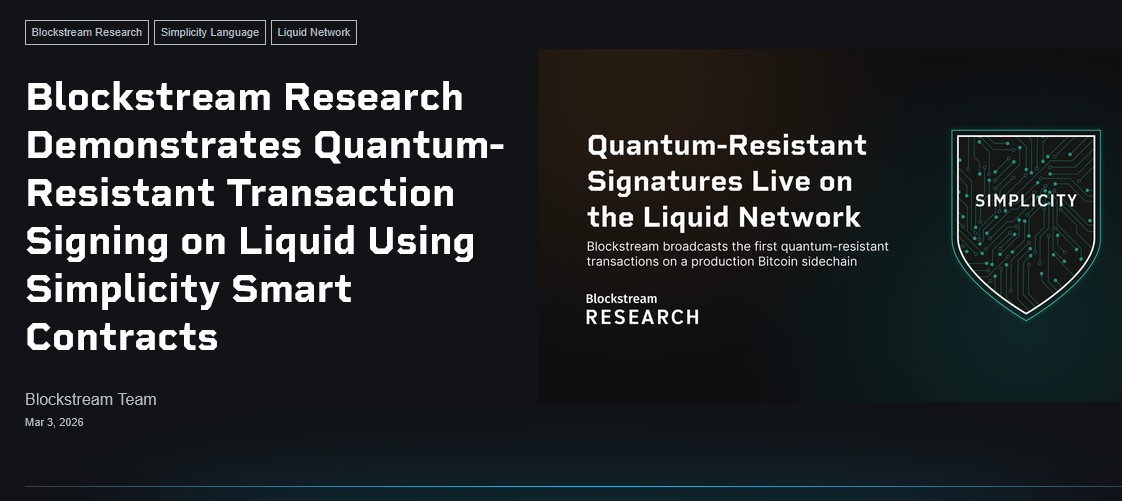

Blockstream Research has been experimenting in recent months with compressing the size of hash-based post-quantum signature schemes for use with Bitcoin. It has come up with the promising SHRINCS and SHRIMPS schemes, which have everyday signatures around five times larger than Bitcoin’s current ones, but up to 40 times larger if you lose your wallet and need to resurrect it.

While SHRINCS has been used to sign real transactions on the Liquid sidechain, its development is at an early stage and there are drawbacks in terms of complexity and usability. The much larger signatures would also slow the blockchain down, unless the block size was increased.

“Raising capacity natively is the simple engineering answer and the hardest governance answer,” said Marin Ivezic, author of PostQuantum.com and founder of Applied Quantum, about a block size increase. “We just don’t have time for those debates.”

ZK proof aggregation has advantages

ncrease, but it would arguably be much better at preserving decentralization while also making Bitcoin more efficient.

At their simplest, ZK proofs are a way to mathematically prove that something exists without needing to include all the details. For example, a ZK proof could demonstrate that you know the combination to a safe, without telling the other person what the combination is.

Generating a ZK proof for a single block technically only needs to be done once (although it’s safer to generate additional backups for redundancy), and the equipment required to do so looks like it would be much less expensive than a commercial mining setup.

Lean Ethereum’s specs are for proving equipment that costs under $100,000 (and can be run from an ordinary home). Verifying a ZK proof, meanwhile, can be done on almost any equipment, including a Raspberry Pi.

Ben-Sasson said that early Bitcoin devs like Greg Maxwell and Mike Hearn were “very bullish about ZK STARKs, which are post-quantum secure and have no trusted setup,” and that he believes Bitcoin Core developer Luke Dashjr and Blockstream founder Adam Back are coming around to the idea.

“I heard this myself from them. They are bullish on things related to and using ZK STARKs. I think each of them has spoken well, definitely privately but also publicly, in favor. Adam Back and Luke Dashjr don’t exactly see everything eye to eye, but on this I think they actually agree that it’s a great technology that, under the right terms, could find its way to Bitcoin.”

Cointelegraph contacted Back for comment, but did not receive a response.

Ethereum researcher Justin Drake has spoken publicly about his desire for Bitcoin to adopt Lean Ethereum’s ZK proof aggregation technology so that it becomes standard across the industry. This may be unfeasible for political reasons.

Ethereum aims to be post quantum by 2029. Source: Ethereum Foundation

Bitcoin specific ZK proposals

Given Bitcoin’s conservative culture, the most politically pragmatic way to add ZK to Bitcoin would likely be to re-enable OP_CAT, which is nine lines of code written by Satoshi.

“[He] even introduced and then he removed it,” said Ben-Sasson said. “And if you add that, you can get things like STARK proofs and then aggregation and post-quantum security.”

“I think it’s the best and safest solution that will really, really just jump-start again this journey that Satoshi really started and wanted.”

But despite a flurry of interest in OP_CAT about 12 to 24 months ago, it seems to have lost momentum more recently (although Bitcoin governance moves in mysterious ways).

There are also more speculative proposals, including OP_STARK_VERIFY, that would add opcodes specifically designed to more efficiently verify STARKs on Bitcoin. And BIP-360 co-author Ethan Heilman proposed aggregating Bitcoin’s signatures and public keys into a single STARK proof under the name BitZip.

Heilman told Cointelegraph earlier this year there are two main ways to achieve the desired result:

“Either add a bunch of general purpose opcodes to Bitcoin and then build something like a ZKRollup in Bitcoin or support STARKs at the consensus layer of Bitcoin. Alternatively, other less powerful aggregation schemes, such as CISA [Cross Input Signature Aggregation] might help here as well.”

What are the chances though?

Ivezic says Bitcoin governance, rather than technological capability, is the sticking point.

“Eli’s cryptography is rock solid: pure hash assumptions, no trusted setup, thousands of signatures compressed into one small proof. The problem is everything around the cryptography,” he says.

“Bitcoin Script cannot verify a STARK today, and a production verifier is a massive consensus surface compared with a narrow hash-signature opcode. Given that a tiny opcode like OP_CAT has spent years in debate, a base-layer STARK verifier is realistically a 2030s conversation.”

Meanwhile, Ethereum is targeting 2029 for its transition to post-quantum, and Solana has also been experimenting with adding post-quantum signatures. StarkNet’s three-phase transition will benefit from account abstraction, which enables the underlying cryptography to be upgraded without making every user manually transfer to new accounts.

As a result, Ben-Sasson said that Solana and Ethereum’s post-quantum roadmap will be “extremely hard.”

“On Starknet, we have this big advantage that we have already native account abstraction and smart wallets, which means that nothing is enshrined so its very easy to upgrade the wallets and the infrastructure to be post quantum.“

Features: The biggest blockchain upgrades still to come in 2026

General Hospital: Carly & Valentin’s Explosive Romance – What Happens Next?

Meghan Markle Financial Demand To King Charles Sparks Royal Crisis

NVDW ETF: Hedge Your Nvidia Position With This Cash Generator (BATS:NVDW)

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: High Hopes

-

NewsBeat5 days ago

NewsBeat5 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Crypto World6 days ago

Crypto World6 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Fashion3 days ago

Fashion3 days agoOpen Thread: What Great Books Have You Read Recently?

-

Politics7 days ago

Politics7 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Fashion17 hours ago

Fashion17 hours agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

News Videos3 days ago

News Videos3 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Tech3 days ago

Tech3 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Crypto World6 days ago

Crypto World6 days agoESMA Expands Crypto Register by 37 Firms Following MiCA Transition Period

-

Business3 days ago

Business3 days agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports2 days ago

Sports2 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Crypto World3 days ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

Crypto World5 days ago

Crypto World5 days agoSouth Africa proposes crypto tax guidance under existing rules

-

News Videos3 days ago

News Videos3 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech5 days ago

Tech5 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business7 days ago

Business7 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Sports2 days ago

We have punished the disrespect

-

News Videos4 days ago

News Videos4 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

-

Crypto World7 days ago

Crypto World7 days agoAlibaba bans Claude Code over alleged backdoor security concerns

-

Tech5 days ago

Tech5 days agoNeuralink Threads Its Way Straight Through the Brain’s Armor

You must be logged in to post a comment Login