Crypto World

Hong Kong awards first stablecoin licenses to HSBC, Standard Chartered-led group

Hong Kong granted its first two stablecoin issuer licenses to HSBC and Anchorpoint Financial, a Standard Chartered-led consortium that includes Animoca Brands on Friday.

The approvals by the Hong Kong Monetary Authority (HKMA), the territory’s central bank, mark the first batch under the Stablecoins Ordinance, which took effect in August 2025.

“We look forward to the issuers launching business according to their plans, exploring growth opportunities while properly managing risks,” HKMA chief executive Eddie Yue said in an announcement on Friday.

“We hope their promotion of regulated stablecoins will address pain points in financial and economic activities, create values for both individuals and businesses, and support the healthy development of digital assets in Hong Kong.”

The HKMA assessed 36 applications and had signaled that the initial round would be limited. Financial Secretary Paul Chan said in his February budget address that only “a small number” would be approved, with the regulator prioritizing risk management, reserve quality, and anti-money-laundering controls.

The decision to license the city’s note-issuing banks first appears to be deliberate. HSBC and Standard Chartered are two of only three commercial banks authorized to print Hong Kong dollar banknotes, a system that dates to 1846, when private banks began issuing currency backed by silver deposits in the absence of a colonial central bank.

Today, each note-issuing bank deposits U.S. dollars with the government’s Exchange Fund at the fixed rate of HK$7.80 per dollar and receives Certificates of Indebtedness in return, against which it prints banknotes.

Yue drew the parallel in a December 2023 blog post.

Pre-1935 banknotes issued by commercial banks in exchange for deposited silver were a form of “private money,” Yue wrote, and stablecoins function as their blockchain-based equivalent — tokens with stable value that can serve as a medium of exchange on-chain.

A strict identity regime

The licenses come with one of the world’s strictest KYC frameworks for digital money.

Under the HKMA’s AML guidelines, licensed stablecoins can only be transferred to wallets whose owners have been identity-verified. The travel rule applies to transfers above HK$8,000 (~$1,000).

In practice, this means HKD stablecoins will likely embed compliance checks into their smart contracts, restricting transfers to wallets listed in an on-chain white list. That makes them structurally different from freely transferable tokens like USDT or USDC.

A HKD CBDC takes a back seat

The bank-led stablecoin model also reflects the HKMA’s decision to deprioritize its central bank digital currency for retail use, as an 11-group pilot program completed in October found the retail case was weak.

CBDCs have historically been a big theme at Hong Kong Fintech Week. Last year, there was barely a mention. Instead, stablecoins were the hot topic.

Standard Chartered CEO Bill Winters said at the time Hong Kong’s push into stablecoins and tokenized deposits could “lay the foundation for a new era of digital trade settlement,” positioning them as a new medium for cross-border commerce.

Whether the market agrees remains to be seen.

Stablecoins are a roughly $310 billion asset class, and USD-denominated tokens dominate nearly all of it.

Data from CoinGecko shows that the largest stablecoins by market cap are dollar-pegged, with no euro-or yen-pegged tokens breaking into the top ranks.

Hong Kong is betting that regulated, bank-issued HKD stablecoins can carve out a role in regional trade settlement, issued by the same institutions, under the same constraints, on new rails.

The question is whether a non-dollar stablecoin, however tightly regulated, can build the network effects needed to compete.

Digital assets have moved well beyond the hype cycle. What began as an experiment in decentralized value transfer has evolved into a serious conversation about how capital markets, custody, settlement and asset ownership could be re-imagined for the digital age. Tokenization, programmable money and distributed ledgers may deliver faster settlement, greater transparency and new efficiencies across the financial system.

The opportunity is both real and transformative, but accelerated adoption of digital assets is not guaranteed.

The ecosystem’s success will not be determined by any single technology, protocol, innovator or platform. Instead, it will hinge on whether the industry embraces a principle that traditional markets have relied on and come to expect for more than a century: choice.

If investors, issuers and intermediaries are forced into narrow paths and left without options, the promise of digital assets risks being constrained by the very silos they were meant to dismantle. For Web3 to flourish, market participants must be able to choose how, where and when they engage.

Choice in blockchain networks: avoiding silos

One of the most pressing challenges facing digital assets adoption today is fragmentation. New blockchains and networks continue to emerge, each optimized for different use cases, governance models or performance requirements. While innovation is healthy, disconnected ecosystems can quickly become a barrier to scale.

Without interoperability, assets risk being locked into isolated environments, limiting liquidity, mobility and investor access. The result is a digital version of the same inefficiencies that have historically plagued financial markets, with the added benefits of being faster and more complex.

Interoperability has the potential to change that result. A “network of networks” approach enables assets to move securely across platforms, enabling market participant firms and investors to take full advantage of tokenization’s potential while preserving market integrity and scale. It simplifies use cases, unlocks new business models and supports regulatory consistency, without forcing the industry to converge on a single chain.

Indeed, some investors may prefer open, public blockchains, while others may gravitate toward private blockchains. It’s not a matter of ‘or’ – both can and should be available.

Achieving this vision will require collaboration. Market infrastructure providers, technology firms and regulators must work together to establish frameworks that prioritize compatibility and interoperability over control. In a recent white paper authored by The Depository Trust & Clearing Corporation (DTCC) in collaboration with Clearstream, Euroclear and BCG, we explored how shared standards and coordinated governance could help advance interoperability while maintaining trust and resilience. The message was and remains clear: interoperability is foundational to scale and the future growth of digital markets.

Choice in what assets to tokenize (and when!)

Tokenization is often discussed as an inevitability, but inevitability should not be confused with immediacy. Not every asset will tokenize, and those that do will not do so at the same pace.

For example, while The Depository Trust Corporation (DTC), as a securities depository, facilitates the post‑trade settlement of securities representing over $100 trillion in value, we are not advocating for broad, indiscriminate, or immediate tokenization. Particularly in the early stages of this ecosystem, disciplined sequencing, intentionality, and caution are essential.

Certain asset classes, especially those with clear operational inefficiencies, high reconciliation costs or settlement frictions, are natural early candidates for tokenization. Others may follow as technology matures, regulatory clarity increases, and market demand evolves. Giving issuers and investors the ability to decide what makes sense for their needs, and on their timeline, reduces risk and builds confidence.

Choice, in this context, is about sequencing and needs. It allows the market to learn, adapt and scale responsibly rather than forcing adoption before the infrastructure is ready.

Choice in how investors want to hold real-world assets

Digital transformation does not mean abandoning established investing principles and processes.

For many institutional investors, tokenized assets will coexist with traditional holdings for many years to come. Some will prefer onchain representations for their operational efficiency or programmability. Others will continue to rely on established custody models, particularly as compliance and risk frameworks evolve.

A successful digital asset ecosystem can support both. Investors should be able to hold assets in tokenized form alongside traditional securities – and even switch back and forth between them – without sacrificing legal certainty, operational continuity or even the feeling of being in control. Flexibility ensures participation is driven by value, not obligation, and that trust is earned, not assumed.

Choice in wallets: empowering the client

Perhaps the most tangible expression of choice is the wallet.

As digital assets enter mainstream financial markets, participants will bring different preferences, risk tolerances and operational requirements. Some will prioritize self-custody. Others will rely on institutional-grade solutions. Many will want the freedom to change over time.

Wallet selection should belong to clients (market participant firms). No prescribed wallet. No mandated standard. This model empowers market participants to choose based on their own security needs, regulatory considerations, geographic requirements or internal controls.

This flexibility is essential for adoption at scale. Markets will thrive when financial institutions have the opportunity to engage on their own terms and can make decisions based on their clients’ and investors’ strategies, needs and preferences.

The path forward

The success of the digital assets ecosystem will not be built on constraints and limitations. Instead, it will be built on options: choice in blockchain, in assets, in custody and in wallets. These are practical requirements for facilitating growth.

If the industry gets this right, digital assets can deliver on their promise: more inclusive, efficient and resilient markets. If it gets it wrong, it risks recreating the limitations of the past on faster rails.

Choice is the key to making digital assets work for everyone.

The White House warned staff against improperly using confidential information to place bets in futures markets after suspicious oil trades ahead of President Donald Trump’s March 23 Iran announcement drew scrutiny, according to Reuters.

Reuters reported on Thursday that the White House sent the internal email on March 24, a day after Trump ordered a five-day delay in attacks on Iran’s energy infrastructure.

The warning followed a roughly $500 million bet on Brent and West Texas Intermediate crude futures placed in a one-minute burst shortly before Trump’s March 23 announcement, according to Reuters calculations based on exchange data. Oil prices fell about 15% after the policy shift.

The episode has intensified scrutiny of whether officials or politically connected traders could profit from nonpublic information tied to military or policy decisions. It has also added momentum to a broader push in Washington to tighten rules around prediction-market trading.

The STOCK Act amendment in the Commodity Exchange Act (CEA) prohibits federal officials, congress members, executive staff and judicial officers from using non-public information derived from their positions to trade commodity, futures or options markets. The amendment was signed into law on April 4, 2012.

Cointelegraph has approached the White House for a copy of the internal email.

Related: US Senate bill targets prediction markets on war and assassinations

Lawmakers respond to prediction market insider trading concerns

Lawmakers have also stepped up scrutiny of prediction markets, where well-timed bets tied to military and political events have raised similar concerns about the misuse of privileged information. Polymarket traders netted around $1 million by accurately betting when the US would strike Iran.

In response to the concerns, Congressman Adrian Smith and Congresswoman Nikki Budzinski introduced the Preventing Real-time Exploitation and Deceptive Insider Congressional Trading Act (PREDICT Act) on March 25, a bipartisan bill seeking to ban members of Congress and federal officials from prediction market trading.

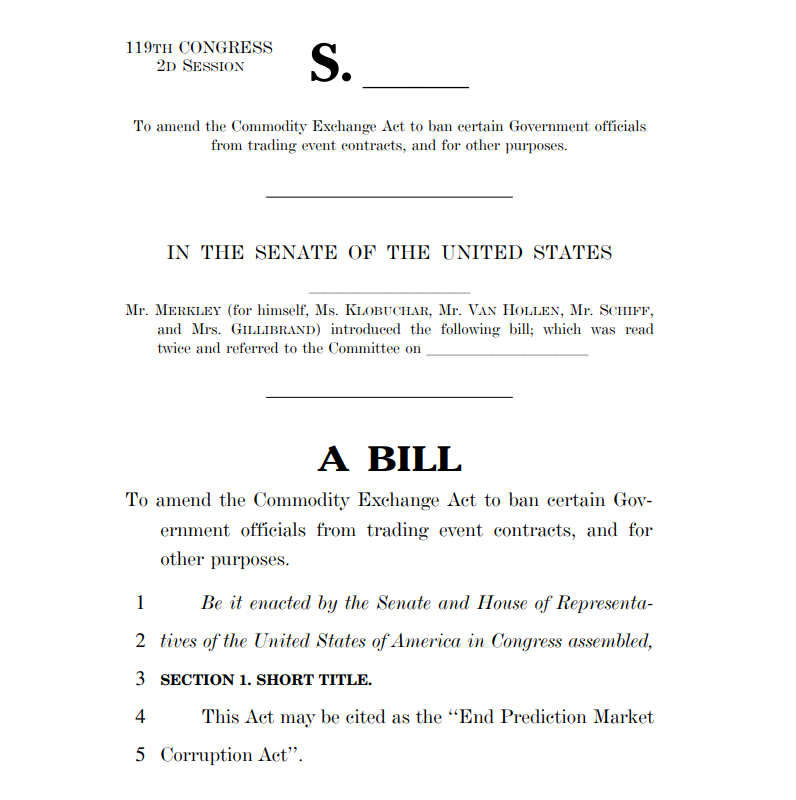

On March 26, US lawmakers Todd Young, Elissa Slotkin, John Curtis and Adam Schiff unveiled the bipartisan Public Integrity in Financial Prediction Markets Act of 2026, a bill aimed at curbing prediction market insider trading by government officials.

The same day, Senator Jeff Merkley introduced the End Prediction Market Corruption Act, seeking to ban event contract trading by government officials with “material non-public information,” including the president, vice president and members of Congress.

Magazine: Crypto traders ‘fool themselves’ with price predictions — Peter Brandt

Bitcoin traded near the $73,000 zone after the March CPI print came in cooler than some forecasts, easing some inflation fears and setting the stage for a cautious push higher. The Bureau of Labor Statistics showed the consumer price index rose modestly, with energy costs driving the month’s big moves.

Gasoline, in particular, surged by a hefty margin, helping push gasoline prices higher within the energy component. The CPI release also highlighted that energy costs remained elevated, even as the overall inflation picture topped by the energy spike did not portend an immediate shift in policy expectations. Traders recalibrated their bets as futures markets signaled that a near-term rate cut by the Federal Reserve remained unlikely for now.

The day’s momentum reflected a broader market narrative: traders parsed the data for hints on the Federal Reserve’s trajectory while monitoring Bitcoin’s own resistance and support levels in a chart that has shown both resilience and volatility in recent weeks.

Key takeaways

- Bitcoin hovered around $73,000 as the March CPI print came in below market expectations, suggesting a softer near-term inflation path than anticipated.

- The CPI energy component rose notably, with the gasoline index up 21.2% month over month, contributing to a 10.9% year-over-year rise in energy costs for March.

- Despite the energy spike, the overall CPI surprised to the downside relative to expectations, reinforcing a caution stance on aggressive monetary tightening or imminent rate cuts.

- Traders highlighted technical setups near critical zones, with liquidity pockets identified below $71,000 and resistance in the $73,000–$74,000 area, shaping short-term risk and reward for BTC.

- Analysts continued to weigh the broader macro context, including Fed expectations and potential chart-driven catalysts, amid a mixed inflation backdrop.

CPI dynamics and Bitcoin’s path to local highs

Markets absorbed a CPI reading that showed a tepid move versus forecasts. The data pointed to a pause in hotter inflation pressures, even as energy costs remained a focal point for investors. The gas price spike, in particular, was a reminder that energy components can dominate monthly price shifts and influence policy discourse. The official release underscored that “The index for energy rose 10.9 percent in March, led by a 21.2-percent increase in the index for gasoline,” a figure that fed into traders’ cautious posture about near-term inflation trajectories.

In the context of Bitcoin, the price action around $73,000 signals a test of nearby supply zones rather than a breakout run. Market commentary from traders noted a narrowing wedge pattern forming in the BTC/USD space, a setup that could precipitate a decisive move if support or resistance gives way. The sense of pending direction was reinforced by observations of order-book liquidity, with attention focused on levels just below $74,000 and pockets around $71,000 on the downside.

Analysts have previously linked RSI-like signals to potential trend reversals in Bitcoin, citing a pattern that some observers say echoes the late-2022 bear-market bottom. While such indicators are not guarantees, they contribute to the ongoing discourse around whether BTC can extend a move toward fresh local highs or face renewed resistance in the near term.

Near-term technical context and the broader market backdrop

From a technical standpoint, traders have kept a close eye on how BTC responds to key price levels in the coming sessions. A recent analysis from a market analyst known as JDK Analysis described BTC/USD as operating within a narrowing wedge, suggesting that the next substantial move could hinge on a breakout above a prior high or a rejection that tests support. In practical terms, that means watching how BTC behaves near the $73,000–$74,000 zone and whether selling interest tightens below $71,000.

On the liquidity front, observers have pointed to local order-book dynamics as a guiding factor for the short-term path. One trader highlighted that liquidity around critical levels—roughly below $71,000 and above $73,000–$74,000—would likely influence the pattern of any impending breakout or pullback. Such micro-structure considerations matter in a market where macro headlines intermittently drive risk appetite and liquidity conditions.

Intraday commentary also echoed the role of macro policy expectations in shaping BTC moves. Market participants have largely priced in a cautious stance from the Federal Reserve, with rate-cut prospects pushed further into the future by recent data. The CME FedWatch Tool and related market-implied probabilities have reinforced the view that policy normalization remains gradual, supporting a context in which Bitcoin could act as a risk-on or risk-off asset depending on the liquidity environment and broader risk sentiment.

Earlier coverage from Cointelegraph noted that a copycat RSI signal had appeared to mirror the conditions seen at the end of the 2022 bear market, a reminder that momentum indicators can align with longer-term price cycles in unexpectedly telling ways. This backdrop continues to color how traders interpret periodic pullbacks and rallies in BTC as they weigh the odds of a renewed leg higher versus a renewed test of the lower boundary.

This article follows the inflation release in a week that has underscored the complexity of the macro picture: energy costs are pushing CPI moves, policy expectations remain cautious, and bitcoin’s price action continues to respond to a combination of macro data and micro-structure signals. As investors weigh the next steps, attention remains on how BTC negotiates the $74,000 resistance and whether the $71,000 level will provide a firmer foothold for a sustained recovery or a further dip.

This article is intended for informational purposes and reflects data from official sources and market commentary available at the time of publication. Readers should perform their own due diligence before making any investment decisions.

What remains uncertain is how sustained energy-driven volatility will influence both inflation trajectories and the timeline for policy normalization, as well as how Bitcoin’s price will respond to any changes in risk appetite as new data comes in.

Key Highlights

- Erayak Power (RAYA) shares climbed 71% Friday following a strategic transformation announcement targeting the U.S. market.

- The manufacturer is transitioning from China-centric operations to a U.S.-oriented research and development model via Nexora, its North American arm.

- A new lineup of Tri-Fuel Inverter Generators (9kW–13kW) capable of operating on gasoline, propane, and natural gas was introduced.

- The strategic transformation followed comprehensive market research spanning 5,000 miles across five American states and a product presentation at the 2026 National Hardware Show in Las Vegas.

- The company established fresh distribution agreements with North American retail chains and wholesale partners during the trade event.

Erayak Power (RAYA) experienced a 71% surge Friday following its announcement of a fundamental business restructuring focused on the American market through Nexora, its subsidiary, while introducing innovative Tri-Fuel power generators and securing retail distribution agreements at the 2026 National Hardware Show.

Erayak Power Solution Group Inc., RAYA

The significant stock movement followed Erayak’s disclosure of comprehensive operational changes. The enterprise, which historically accessed North American customers mainly through third-party export arrangements, is establishing a direct American footprint.

The transformation revolves around Nexora, Erayak’s North American division. According to the revised business structure, Nexora will manage research and development, customer relations, and market strategy for the United States, while production operations continue through the Ruike Electronics manufacturing plant.

Prior to implementing the new strategy, Erayak executives undertook an extensive 5,000-mile investigation across California, Arizona, Texas, Florida, and New York. This comprehensive tour focused on identifying specific regional power requirements throughout diverse American markets.

The organization presented its latest innovations at the 2026 National Hardware Show in Las Vegas. This platform simultaneously facilitated the establishment of strategic partnerships with premium retailers and industrial distribution networks throughout North America.

Innovative Product Portfolio

Erayak’s 2026 flagship offerings feature Tri-Fuel Inverter Generators spanning 9kW to 13kW capacity. These generators operate on multiple fuel sources—gasoline, propane, or natural gas—and incorporate Auto Transfer Switch capabilities.

These power units integrate with commercial-grade UPS Solar Inverters. According to Erayak, the integrated systems deliver consistent emergency power solutions, including support for AI-edge computing infrastructure and connected home technologies.

The organization identified Texas and Florida as priority markets, referencing persistent electrical grid stability challenges in these regions. The generators incorporate reduced total harmonic distortion technology, which Erayak indicates makes them appropriate for powering delicate electronic equipment.

Erayak characterizes its market penetration strategy as a “Twin-Track” framework. This approach merges Nexora’s direct consumer sales channel with a broadened wholesale distribution infrastructure.

Business Transformation

CEO Lingyi Kong positioned the initiative as an evolution beyond traditional manufacturing. “By establishing Nexora as our North American face, we are moving beyond manufacturing to become a vertically integrated power solutions provider,” Kong said.

Before this strategic announcement, Erayak’s North American operations functioned predominantly through indirect export mechanisms. The current organizational structure represents a significant departure from previous approaches.

The company indicated the Nexora framework aims to enhance operational clarity and deliver greater shareholder value.

RAYA commenced Friday trading with substantial volume following the strategic disclosure. The stock registered a 71% gain by market close, with peak intraday appreciation reaching 87%.

The 2026 National Hardware Show presentation combined with the Nexora strategy announcement emerged as the principal drivers behind Friday’s significant price movement.

MoonPay, WalletConnect, and Ingenico announced a partnership to enable stablecoin payments at physical retail locations globally using MoonPay Virtual Accounts for fiat settlement.

MoonPay announced a partnership with WalletConnect and Ingenico to bring stablecoin payments to physical retail locations at global scale. The integration leverages MoonPay Virtual Accounts to enable fast fiat settlement for in-store transactions powered by stablecoins.

WalletConnect provides wallet connectivity infrastructure, while Ingenico brings point-of-sale terminal capabilities and retail distribution. The partnership targets enabling merchants worldwide to accept stablecoin payments directly at checkout with immediate conversion to fiat currency.

Sources: MoonPay

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

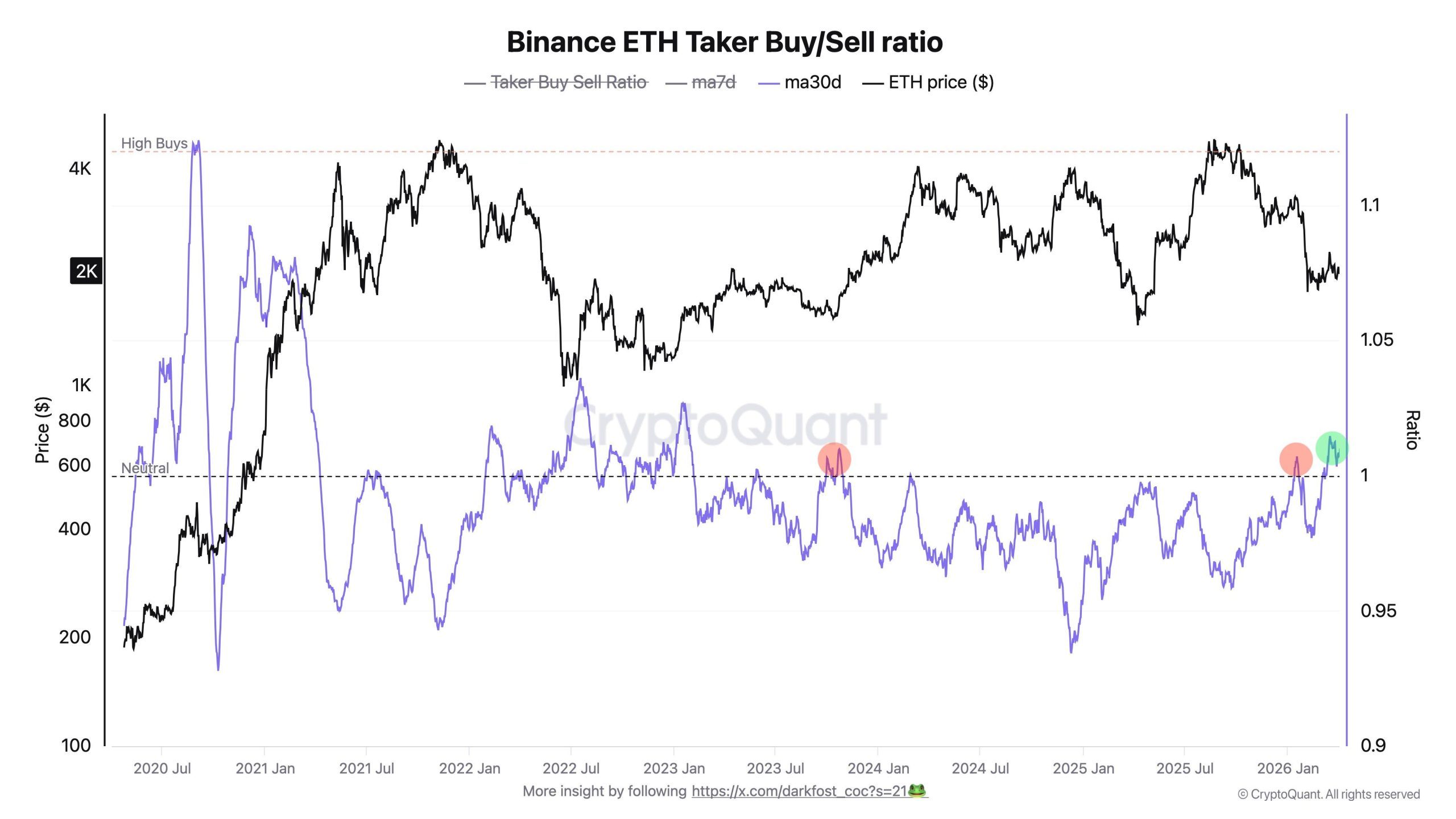

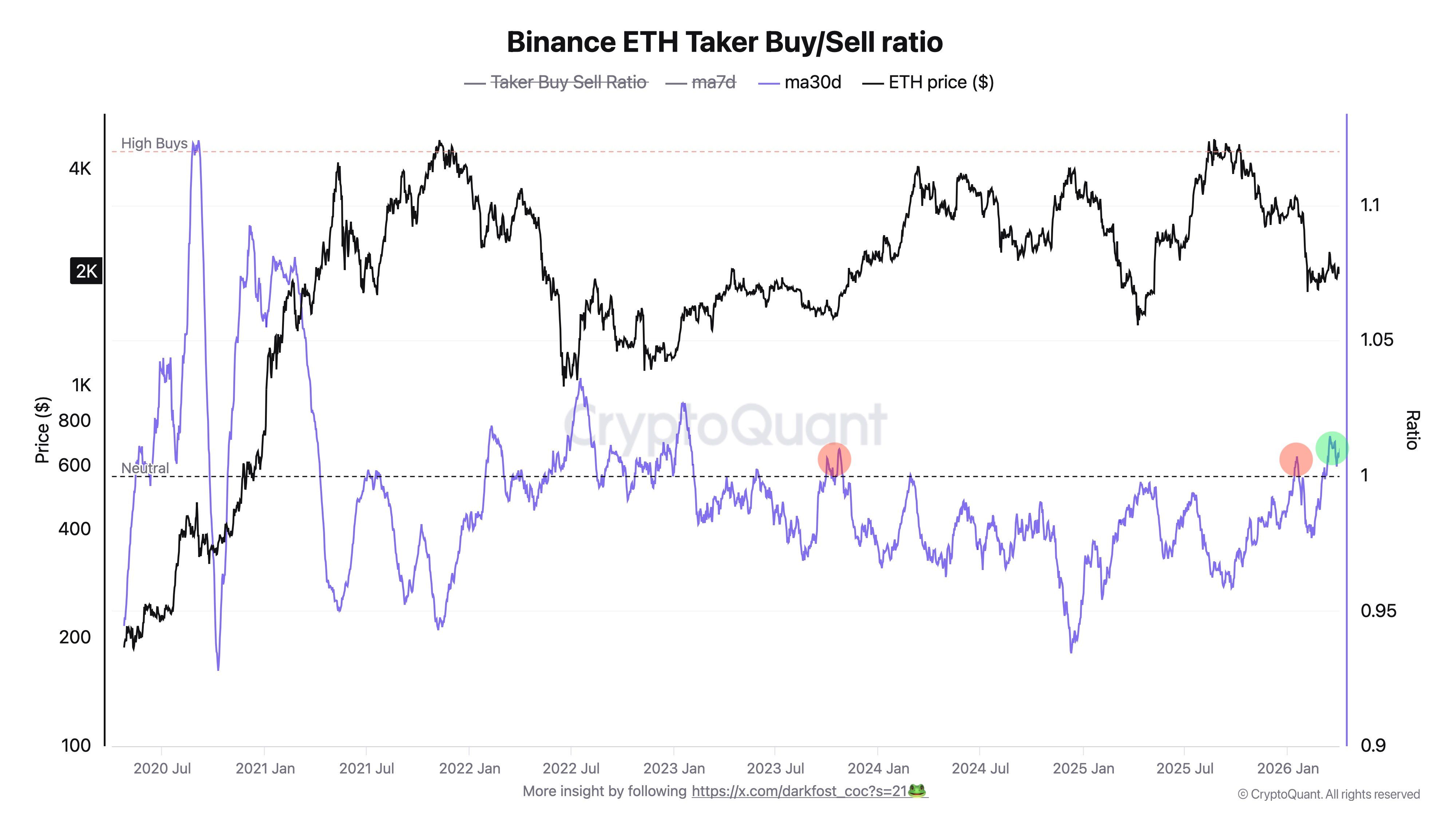

Ethereum’s (ETH) Taker Buy-Sell Ratio on Binance is flashing a signal not seen in nearly three years. The monthly average has climbed to around 1.016 and has held above 1 for several consecutive days.

The shift suggests that market-buy orders are outpacing sells on Binance’s ETH perpetual contracts, a signal CryptoQuant analyst Darkfost flagged as “early stages of a more constructive trend.”

Why Derivatives Data Matters More For ETH

For context, the Taker Buy Sell Ratio tracks the balance between market buy and sell volumes on perpetual contracts. A reading above 1 means aggressive buyers are outpacing sellers.

What stands out now is the monthly average holding above 1 for multiple consecutive days.

“This reflects a progressive return of buyer dominance on perpetual markets, suggesting the early stages of a more constructive trend,” the analyst said. “This therefore marks a constructive development for Ethereum, not seen since 2023.”

Follow us on X to get the latest news as it happens

The signal carries added weight because futures activity on Binance now dwarfs spot trading. The exchange’s spot-to-futures volume ratio recently fell to 0.13, meaning roughly $7 in futures changes hands for every $1 in actual ETH buying.

That imbalance makes derivatives positioning the primary driver of short-term price action. Moreover, Binance accounts for approximately 37% of global ETH open interest. According to the analyst, this dominance makes it a key venue for assessing derivatives positioning.

Notably, the ratio’s move above 1 has been incremental rather than sudden. The analyst considers this pattern healthier than a sharp spike, which tends to create overleveraged positioning and trigger cascading liquidations.

The development comes despite ongoing macroeconomic and geopolitical uncertainty, suggesting early-stage structural improvement in ETH sentiment. However, the derivatives-heavy market structure still poses risks. A futures-led rally without matching spot demand could amplify volatility if positions unwind quickly.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Ethereum Flashes Bullish Signal Not Seen Since 2022 on Binance Futures appeared first on BeInCrypto.

Bitcoin (BTC) tagged $73,000 following Friday’s Wall Street open as crucial US inflation numbers came in below expectations.

Key points:

-

Bitcoin edges higher as US CPI data remains slightly below market expectations.

-

Gasoline prices see a historic surge within the CPI release.

-

Bitcoin traders plan out key resistance levels overhead.

BTC price seeks new local highs after CPI

Data from TradingView showed BTC price eyeing new multi-week highs as markets digested the March print of the Consumer Price Index (CPI).

This was the week’s key macro data release, and the first CPI report to reflect the impact of the US and Israel war in Iran.

Gasoline prices jumped over 21% month-on-month, the Bureau of Labor Statistics (BLS) confirmed, but overall CPI finished 0.1% lower than markets’ expectations.

“Over the last 12 months, the all items index increased 3.3 percent before seasonal adjustment,” an official news release read.

“The index for energy rose 10.9 percent in March, led by a 21.2-percent increase in the index for gasoline which accounted for nearly three quarters of the monthly all items increase.”

Reacting, trading resource The Kobeissi Letter noted that the gas-price CPI jump was the largest monthly gain since 1967. The energy increase, it added in a further post on X, was the largest since 2005.

With the resulting mixed picture of inflationary forces, US stocks were mostly flat at the open, while BTC price action also avoided major moves up or down.

Markets, however, had no hope for the Federal Reserve cutting interest rates — a conclusion already in place on the back of Thursday’s Personal Consumption Expenditures (PCE) index release, per data from CME Group’s FedWatch Tool.

Bitcoin traders draw the next resistance zones

Among Bitcoin market participants, there was modest reason for optimism over the short-term price outlook.

Related: Bitcoin analysis sees $55K BTC price ‘iron bottom’ by December 2026

In their latest X analysis, trader JDK Analysis flagged BTC/USD acting within a narrowing wedge — a topic of debate since February.

“If price makes another attempt at the current key high, the reaction there will be critical!” they wrote in accompanying commentary.

Trader Daan Crypto Trades meanwhile eyed exchange order-book liquidity below $74,000.

$BTC Liquidity levels to watch in close proximity are that ~$71K region below, and $73K-$74K above (local high). pic.twitter.com/BlKsaZXdpb

— Daan Crypto Trades (@DaanCrypto) April 10, 2026

Earlier, Cointelegraph reported on a copycat signal from Bitcoin’s relative strength index (RSI) that began to echo the end of the 2022 bear market.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

Binance offered its staff in the United Arab Emirates the option to temporarily relocate to Hong Kong, Tokyo, Kuala Lumpur and Bangkok amid regional tensions, the company told CoinDesk Friday.

“Given the recent regional tensions, we offered employees the option to temporarily relocate as a precautionary, employee-first measure to provide flexibility and support during a period of uncertainty,” a Binance spokesperson said. “As a remote-first organization, we are well set up to support this kind of flexibility without disruption to our operations.”

The spokesperson also said its operations in the UAE remain unchanged and that many employees have chosen to stay.

“Our operations in the UAE continue as normal — a large number of our team has chosen to remain in the UAE. We remain deeply committed to the UAE as a key hub for Binance and to the broader region,” the spokesperson said. “As a global company, we continue to operate seamlessly and serve our users without interruption.”

The offer of relocation comes after a ceasefire agreement, following roughly six weeks of escalating regional conflict that has disrupted business activity in the UAE. The country has intercepted hundreds of missiles and drones since hostilities began in late February, according to the UAE Ministry of Defense, with additional interceptions reported on April 8.

The Middle East conflict has already disrupted major crypto, business and sports events across the UAE. TOKEN2049 Dubai has been postponed to 2027, while TON Gateway was canceled due to security and travel concerns. Other large events, including Middle East Energy Dubai and the Dubai International Boat Show, have also been delayed, and the Bahrain and Saudi Arabian Formula 1 races, key for crypto sponsorship exposure, are set to be canceled.

In December, Abu Dhabi Global Market (ADGM) said Binance’s global platform would operate under its regulatory framework, marking a significant step in formalizing the exchange’s structure.

Binance, which reportedly has 1,000 staff members or 20% of its total global workforce in the UAE, has also indicated that its worldwide operations are supported from Abu Dhabi, though it has not clearly defined a single global headquarters.

Securitize announced integration with TRON Network to bring tokenized assets to one of the world’s largest blockchains, expanding its multichain presence.

Securitize integrated with TRON Network on April 10, enabling tokenized assets issued by Securitize to be deployed on TRON, one of the world’s largest blockchains. The partnership expands Securitize’s multichain footprint and brings institutional-grade assets to a high-performance network designed for efficient, programmable financial systems.

The integration aligns with growing demand for tokenization infrastructure that bridges traditional finance and blockchain networks. TRON operates as a high-throughput blockchain platform, and this partnership enables Securitize’s tokenized assets—which typically include securities and institutional products—to access TRON’s user base and ecosystem.

Sources: Securitize

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

Bittensor token price has collapsed by 17% in less than 6 hours after one of the network’s most prominent subnet developers publicly torched its relationship with the ecosystem, and the price prediction is getting bearish. The governance bombshell driving this selloff raises a harder question than most traders are asking right now.

On Thursday, Covenant AI, the team behind the Covenant-72B model, widely credited as the largest decentralized LLM pre-training run in history, announced its exit from Bittensor.

— BSCN (@BSCNews) April 10, 2026

LATEST: BITTENSOR DROPS 16% AS COVENANT AI EXITS THE NETWORK OVER CENTRALIZATION CONCERNS

LATEST: BITTENSOR DROPS 16% AS COVENANT AI EXITS THE NETWORK OVER CENTRALIZATION CONCERNS

Covenant AI (@covenant_ai) has exited Bittensor citing concerns over centralized control.

The team said governance is not truly decentralized in practice. It alleged key decisions remain… pic.twitter.com/QlA4AoMWbG

Founder Sam Dare stated that “the promise that drew builders, miners, validators, and investors into this ecosystem is a lie,” accusing co-founder Jacob Steeves of asserting centralized control over Covenant’s subnet after it grew too prominent to ignore.

Steeves has not publicly responded. The statement hit markets like a circuit breaker. TAO had surged 140% over six weeks, with 105% of those gains coming since March 8 alone, largely on the back of Covenant-72B’s success narrative and Grayscale’s filing for a TAO Trust. That entire credibility stack just developed a serious crack.

Discover: The best crypto to diversify your portfolio with

Bittensor Price Prediction: Can TAO Recover?

At current levels near $280, TAO sits in genuinely dangerous technical territory. $300 was the immediate support level, and the price is already trading below it, which means the level has effectively been lost.

On-chain data confirms the severity of the move, with TAO’s 24-hour decline registering among the steepest in the large-cap AI token sector. The April 9 rejection at $360 resistance preceded a bearish MACD crossover, with sellers already positioning before the news dropped.

Social dominance for TAO reached a one-year high in early April, yet retail sentiment shows only 1.5 positive comments per negative comment, suggesting conviction in the prior rally was thinner than price action implied.

TAO needs to reclaim $300 within 48 hours on a credible response from Steeves or Bittensor’s governance structure for it to stage a recovery toward $320–$330. But continued silence from leadership and further subnet departures can accelerate selling pressure toward $250 or lower.

The parallel to other ecosystem selloffs triggered by major internal exits suggests recoveries can take weeks, not days. Watch the $300 level; this is the line.

Discover: The best pre-launch token sales

Bitcoin Hyper Draws Early Movers as TAO Tries to Recover

Governance risk just repriced TAO’s entire decentralization premium, and that’s the precise vulnerability traders with longer memory have warned about. When a network’s core value proposition gets called a lie by its most successful builder, rotating capital doesn’t wait for confirmation. It moves.

One destination attracting that rotated attention is Bitcoin Hyper ($HYPER), a Bitcoin Layer 2 project positioning itself as the first-ever BTC chain with Solana Virtual Machine (SVM) integration.

The pitch is structural: Bitcoin’s security and liquidity combined with sub-Solana-speed smart contract execution, breaking through BTC’s native limitations of slow transactions, high fees, and zero programmability. No governance triumvirate. No subnet politics.

The presale has raised $32 million at a current price of $0.0136, with staking available for early participants. The project’s Decentralized Canonical Bridge handles BTC transfers natively.

Research Bitcoin Hyper before the next price step triggers.

The post Bittensor Price Prediction: Covenant AI Exits TAO, Forcing 16% Drop appeared first on Cryptonews.

Melania Trump’s speech has the media ignoring one big thing

UFC 327 weigh-ins: Prochazka, Ulberg on target with pounds to spare

AI Is Coming for Car Salesmen

![[KLPGA 2026] iM Financial Group Open 2026 / Round 2 (ENG Commentary)](https://wordupnews.com/wp-content/uploads/2026/04/1775832050_maxresdefault-80x80.jpg)

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business5 days ago

Business5 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports6 days ago

Sports6 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business6 days ago

Business6 days agoExpert Picks for Every Need

-

Tech3 days ago

Tech3 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business5 days ago

Business5 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion4 days ago

Fashion4 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Fashion3 days ago

Fashion3 days agoLet’s Discuss: DEI in 2026

-

Crypto World2 days ago

Crypto World2 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Business6 days ago

Business6 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Crypto World1 day ago

Crypto World1 day agoCanary Capital Files SEC Registration for PEPE ETF

-

Politics6 days ago

Politics6 days agoThe UK should not pay a penny in slavery reparations

-

Tech4 days ago

Tech4 days agoSamsung just gave up on its own Messages app

-

Tech4 days ago

Tech4 days agoHaier is betting big that your next TV purchase will be one of these

-

Tech7 days ago

Tech7 days agoFlat tire? Dead battery? Speedy’s serves stranded Seattle riders as a quicker e-bike picker-upper

-

Fashion7 days ago

Fashion7 days agoWeekly News Update, 4.3.26 – Corporette.com

-

Sports7 days ago

A Kevin O’Connell Theory Can Now Be Retired

-

NewsBeat7 days ago

NewsBeat7 days agoKemi Badenoch talks ‘spring cleaning’ Reform defections

-

Tech4 days ago

Tech4 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

-

Business3 hours ago

Business3 hours agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

You must be logged in to post a comment Login