Crypto World

How Prediction Markets Resolve: UMA Oracle Explained

Billions of dollars in prediction market positions settle every month based on a machine for deciding truth that most traders have never examined. This guide explains how UMA’s optimistic oracle turns real-world events into on-chain payouts, why the system usually works, the cases where it has failed spectacularly, and the rival settlement designs trying to replace it.

Prediction markets had their breakout year in 2026. Combined volume across the major venues hit $44.8 billion in June alone, driven by a World Cup that turned Polymarket into a multi-billion-dollar sportsbook. The trading side of these platforms is easy to understand: shares in Yes or No, priced between zero and one dollar, paying out one dollar if you are right. The hard part is invisible until it breaks. Someone, or something, has to decide what actually happened.

That decision layer is called resolution, and it is the load-bearing wall of the entire sector. A prediction market is only as good as its ability to decide truth, and a blockchain cannot observe the real world. It cannot see who won an election, whether a company sold an asset, or whether a bill passed. The bridge between reality and the smart contract is an oracle, and for the largest on-chain prediction market, that oracle is UMA. Understanding how it works, and how it fails, is the single most useful piece of due diligence a prediction market trader can do.

The oracle problem, event edition

Crypto solved one version of the oracle problem years ago. Price feeds from networks like Chainlink and Pyth deliver asset prices on-chain by aggregating data from many independent publishers. That works because prices are public, continuous, machine-readable, and available from dozens of redundant sources.

Event markets break every one of those assumptions. The questions are one-off rather than continuous. The answers often live in press releases, court rulings, regulatory filings, or a referee’s whistle. And the phrasing matters enormously: a market asking whether a politician says a specific word five times needs a resolution process that can read, interpret, and withstand challenge. No price feed can answer questions like that. What the sector needed was an oracle for arbitrary facts, with a built-in way to contest wrong answers.

Enter UMA and optimistic verification

UMA, short for Universal Market Access, is an oracle protocol built by Risk Labs. Its core product, the Optimistic Oracle, resolves outcomes for Polymarket’s main venue, which cleared around $14 billion in monthly volume during the World Cup peak. The word optimistic describes the design philosophy: submitted answers are assumed true unless someone challenges them, with economic incentives doing the policing instead of a central referee.

The flow for a typical Polymarket market runs through a version of the oracle called OOv2, and it has four stages:

- Request. When a market’s end conditions are met, the market contract asks the oracle for the outcome, referencing the exact resolution criteria written when the market was created.

- Proposal. A proposer submits the answer, Yes or No, and posts a bond of $750 in USDC. If the proposal is wrong, the bond is forfeited. If it stands, the proposer earns a reward.

- Challenge window. The proposal sits open for two hours. Anyone who believes it is wrong can dispute it by posting a matching bond.

- Escalation. If a dispute lands, the question goes to UMA’s Data Verification Mechanism, the DVM, where UMA token holders research the question and vote on the correct answer. Voters who side with the final outcome earn rewards; voters who miss or vote against it lose a slice of their stake. The DVM’s ruling is final, the losing bond pays the winner, and the market settles.

To make that concrete, follow one uncontested market through its whole life. A market opens asking whether a central bank cuts rates at its June meeting, with resolution criteria naming the official statement as the source. Traders price Yes at 70 cents through the month. The decision lands at 2 p.m., the statement confirms a cut, and within minutes an approved proposer submits Yes with the $750 bond. For two hours, anyone on earth with a matching bond could object; nobody does, because the statement is public and unambiguous. The window closes, the oracle reports Yes to the market contract, and every Yes share becomes redeemable for one dollar in USDC. Total elapsed time from event to payout: under three hours, no human authority involved, no appeal needed. That is the experience for the overwhelming majority of markets, and it is why the system scaled.

The bond arithmetic deserves a sentence of its own, because it is the whole security model in miniature. Seven hundred fifty dollars sounds trivial next to markets carrying tens of millions in open interest, and read one way, it is: a wrong proposal on a whale-scale market risks $750 to potentially swing a payout worth thousands of times that. The design’s answer is that the bond does not defend the market alone, the challenge window does. A false proposal only profits if nobody in the world notices for two hours, on a venue where every large market has thousands of position holders watching resolution like hawks and a matching bond waiting for whoever catches the error. The bond prices the cost of forcing a dispute, not the value of the market, and the escalation layer is supposed to carry the real weight. That framing also locates the true weak point precisely: the system is only as strong as the layer disputes escalate to.

The percentages favor the happy path. Roughly 99% of assertions since 2021 have gone undisputed, meaning most markets settle in the two-to-four-hour window after an event without any human argument. The system processes upward of 7,000 proposals per month, and Risk Labs has automated much of the pipeline: language models draft proposals for around half a cent per request, and bots like OOTruthBot summarize evidence threads and flag suspicious submissions, cutting routine resolution from hours to seconds.

Inside the DVM: what a token vote actually looks like

Since the DVM is the backstop everything escalates to, its mechanics deserve a closer look than most traders ever give them.

When a dispute triggers a vote, the question enters a voting round for UMA token holders who have staked into the voting system. Voting runs in two phases. In the commit phase, each voter submits an encrypted vote, hidden from everyone including other voters, which prevents late voters from simply copying the visible majority. In the reveal phase, voters decrypt and publish what they committed. Votes are weighted by staked tokens, and the outcome that carries the stake-weighted majority becomes the oracle’s answer.

The incentive design is the load-bearing part. Voters who land with the final outcome earn rewards from protocol emissions. Voters who miss a round or land against the outcome lose a slice of their stake. The design intends to pay for diligence, and it mostly does, but it carries a known theoretical flaw inherited from every majority-rewarded oracle: the profitable strategy is voting with the expected majority, not with the truth, and in ordinary cases those two targets coincide. The failure cases are the ones where they separate, and where a large holder can make the majority whatever they need it to be.

There is also a timing cost. An undisputed market settles within hours; a disputed one waits for the full commit and reveal cycle, stretching resolution to days while positions stay frozen and traders argue in evidence threads. For anyone holding size, a dispute is not just a risk to the payout but a lockup on capital.

In November 2025 the system got its most significant overhaul, the Managed Optimistic Oracle V2. MOOv2 restricted the right to propose resolutions to 37 pre-approved addresses, a mix of Risk Labs staff and Polymarket users with high historical accuracy, while keeping disputes open to anyone. The change targeted premature and spam proposals, which had been a chronic source of delays and gamesmanship. Proposing became curated; challenging stayed permissionless.

Where the machine breaks

The design has one structural soft spot, and 2026 has stress-tested it in public: the final arbiter is a token vote, and tokens can be bought, concentrated, and conflicted. The numbers behind that concern are not speculative. A Wall Street Journal investigation published in May found that in most disputed Polymarket markets, more than half of the UMA votes came from the ten largest wallets. At least 60% of active UMA voters could be linked to live Polymarket accounts, and roughly one in five disputes had at least one voter with a financial stake in the market they were ruling on. The dispute pipeline itself is swelling: Polymarket logged more than 1,150 disputed markets in the first five months of 2026, already past its full-year 2025 total.

Two cases show what that looks like in practice.

The first was a 2025 market on a United States minerals agreement, where a single large UMA holder cast five million tokens across three accounts, about 25% of the vote in that dispute round, pushing a contested market to resolve early against the plain reading of events. Traders on the wrong side of that ruling lost roughly $7 million. The vote was legal under the system’s rules. That was precisely the criticism.

The second came in June 2026 and drew more than $60 million in volume: a market asking whether Strategy would sell any Bitcoin by May 31. A regulatory filing published on June 1 disclosed that the company had sold 32 BTC between May 26 and May 31 at an average price of $77,135, its first disposal since 2022, inside the market’s cutoff. Two proposed resolutions were challenged, the question escalated to a token vote, and the market ultimately resolved No. Shares tracking the documented answer traded at 12 cents while the dispute ran. Critics across the industry framed the episode as a structural verdict: when ambiguous rules meet concentrated voting power, the payout can diverge from the facts, and the holders of the settlement token can be the same people holding positions in the market being settled.

None of this means most markets resolve wrongly. The overwhelming majority settle cleanly and fast. It means the tail risk is governance-shaped: the worst outcomes cluster in high-volume, ambiguously worded markets where a motivated whale has both the tokens and the position.

Why Polymarket keeps the system anyway

Given the 2026 dispute record, the obvious question is why the largest on-chain venue has not replaced its oracle. The answer is a stack of practical reasons that critics tend to skip.

The happy path really is that good. Ninety-nine percent of markets settling within hours, at a cost of fractions of a cent per automated proposal, across every category from elections to award shows, is a service level no alternative currently matches for open-ended questions. Deterministic settlement cannot touch subjective markets at all, and regulated clearing brings jurisdiction constraints that would gut the international product.

The system also iterates. MOOv2 was a direct response to the proposal-spam era and measurably cut premature resolutions. The language model pipeline and evidence bots were responses to speed and quality complaints. Bond sizes, challenge windows, and proposer sets are all tunable parameters, and Risk Labs has shown willingness to tune them under pressure. Whether tuning can fix a voting-power concentration problem is the open question, since the DVM backstop itself is the part no parameter change reaches.

And there is a structural argument: for a venue whose regulatory story leans on decentralization, outsourcing truth to an external token-holder process is a feature. Polymarket does not decide outcomes, and that sentence has legal value. The company’s answer to the United States market was not to change the oracle but to split the product, running the domestic venue through a CFTC-regulated framework while the international book kept UMA. The two-track structure is itself a verdict on where each settlement model belongs.

The rival designs

The dispute wave has made resolution architecture a competitive battleground, and three alternative models are now live at scale.

Deterministic validator settlement. Hyperliquid’s HIP-4 outcome markets, live since May 2026, remove the token vote entirely. Settlement runs through the chain’s validator set executing automated resolution against pre-specified objective data sources: no dispute window, no escalation, no path for a market participant to vote on a market. The constraint is scope, since deterministic settlement only fits questions with clean data sources, which is why the first HIP-4 contracts are Bitcoin price thresholds. Our companion guide to HIP-3 and HIP-4 covers the full design, and the market has been pricing Hyperliquid’s prediction market ambitions since the February announcement.

Regulated clearing. Kalshi reaches finality through the opposite architecture: a centralized exchange clearinghouse, registered with the CFTC as a derivatives clearing organization since August 2024, resolving markets under rules filed with a federal regulator and publishing results on-chain through Pyth and RedStone. Disputes go through exchange procedures, not token votes. The model trades decentralization for accountability, and its structured markets rarely face the ambiguity problems that plague open-ended questions. Polymarket’s separate United States venue, itself a CFTC-registered designated contract market that did $3.04 billion in June, follows the same regulated path, while the international venue still settles through UMA.

Purpose-built feeds. For objective, high-frequency questions, oracles built for prices work fine, and Polymarket already uses Chainlink to settle its fast crypto price markets, where no public discourse about the answer is needed. FIFA’s own licensed prediction market partner for the World Cup runs on Chainlink infrastructure, part of the tournament’s broader crypto buildout. Further out, web proof systems could let a resolution cite a cryptographically verified source document instead of a screenshot, a use case covered in our zkTLS explainer.

History adds a warning label to all of it, because decentralized resolution has been tried before and the graveyard is instructive. Augur, the sector’s first major attempt, launched in 2018 with REP token staking where reporters earned by landing with the consensus outcome, and the platform learned quickly that rewarding agreement with the majority is not the same as rewarding truth, especially once invalid and ambiguously worded markets entered the mix. Omen outsourced disputes to Kleros, a decentralized juror court whose participants were likewise paid for voting with the crowd, and inherited the same incentive plus slow rulings and heavy gas costs. Both platforms also discovered that resolution is a liquidity problem in disguise: traders avoid venues where the payout rules feel lottery-shaped, so unreliable settlement starves the order books that make prediction markets useful at all. Every resolution design since is a wager about which failure mode is most tolerable: token capture, institutional discretion, or narrow scope.

What traders should actually check

Resolution risk is checkable before entry, and the checklist is short.

Read the resolution criteria as literally as a hostile lawyer would, because the oracle will. The Strategy market turned on exact wording and an exact cutoff. If the criteria name a specific source, that source is the truth regardless of what every news outlet reports. Check the venue’s settlement path: UMA-resolved international Polymarket, a CFTC clearinghouse, a validator-settled chain, and a Chainlink price feed are four different risk profiles wearing the same Yes and No interface. Prefer markets with objective, single-source answers when size matters, since ambiguity is the raw material of every resolution scandal. And in a disputed market, watch the UMA vote rather than the news cycle, because the vote is what pays.

Two habits separate professionals from tourists here. The first is position sizing by resolution clarity: the same trader who is comfortable with six figures on a rate decision, where the source is official and the answer binary, keeps ambiguous cultural or political wording to entertainment-sized stakes. The second is tracking the dispute docket itself. Markets with pending UMA votes, and the wallets voting in them, are public on-chain information, and the recurring names in contested rulings are known to anyone who looks. In a system where the referee list is visible, not reading it is a choice.

One more number worth holding in mind: UMA’s entire token traded around a $63 million market capitalization earlier this year, while the markets it settles cleared billions per month. The economic security of a token-voted oracle is bounded by the cost of acquiring the tokens, and that ratio is the quiet argument behind every alternative design now gaining ground.

Truth as infrastructure

Prediction markets are routinely praised as truth machines, better than polls and faster than newsrooms. The praise is half-earned. Prices aggregate beliefs brilliantly, but the settlement layer decides which beliefs get paid, and that layer is built from bonds, challenge windows, token votes, clearinghouse rules, and validator scripts, each with a distinct way of being wrong. The sector’s next phase will be decided as much by resolution engineering as by volume, because traders forgive losing on the outcome and do not forgive losing on the ruling. The machinery for deciding truth is now a product category of its own. It deserves to be read as carefully as the odds.

Frequently asked questions

How does Polymarket decide who won a market?

Polymarket’s international venue outsources resolution to UMA’s Optimistic Oracle. After an event, an approved proposer submits the outcome with a $750 USDC bond, and a two-hour challenge window opens. If nobody disputes, the market settles on that answer, usually within two to four hours. If a dispute lands, UMA token holders vote through the Data Verification Mechanism, and their ruling is final.

What is UMA’s optimistic oracle?

It is an oracle protocol by Risk Labs for bringing arbitrary real-world facts on-chain. It is called optimistic because proposed answers are assumed true unless challenged during a dispute window, with bonds and rewards making honesty profitable and false proposals costly. Around 99% of assertions since 2021 have gone undisputed, and contested cases escalate to a token-holder vote.

What happens when a Polymarket resolution is disputed?

The disputer posts a bond matching the proposer’s, and the question escalates to UMA’s Data Verification Mechanism. UMA token holders research the question and vote, with rewards for voting with the final outcome and penalties for missing or voting against it. The losing side’s bond pays the winning side. Disputes stretch resolution from hours to days, and the DVM ruling cannot be appealed.

Why is UMA’s system controversial in 2026?

Concentration and conflicts. A Wall Street Journal investigation found most disputed markets saw over half their votes come from the ten largest wallets, and about one in five disputes included a voter holding a position in the market being judged. More than 1,150 markets were disputed in the first five months of 2026, and a $60 million market on a Strategy Bitcoin sale resolved against a documented regulatory filing.

What was the Strategy Bitcoin market dispute?

A Polymarket contract asked whether Strategy would sell any Bitcoin by May 31, 2026. A June 1 regulatory filing showed the company sold 32 BTC between May 26 and May 31, inside the window. The resolution was challenged twice, went to a UMA token vote, and the market resolved No anyway. The episode became the leading exhibit in the argument against token-voted settlement.

What is MOOv2?

The Managed Optimistic Oracle V2, deployed in November 2025, restricted resolution proposals to 37 pre-approved addresses with strong accuracy records while keeping disputes open to everyone. Paired with language model automation that drafts proposals for fractions of a cent and bots that summarize evidence, it cut spam proposals and sped up routine settlement without changing the token-vote backstop.

How do Kalshi and Hyperliquid settle markets differently?

Kalshi resolves through its CFTC-registered clearinghouse under federally filed rules, then publishes results on-chain via Pyth and RedStone, with disputes handled by exchange procedure. Hyperliquid’s HIP-4 uses deterministic settlement by the validator set against pre-specified data sources, with no dispute window at all. Neither involves a token vote, and both are positioned as answers to UMA’s governance risk.

Can a prediction market resolve incorrectly and stay that way?

Yes. DVM rulings are final, and Polymarket has honored controversial outcomes rather than overriding the oracle. The practical defenses are all pre-trade: read the resolution criteria literally, check which settlement system the venue uses, prefer objectively verifiable questions for larger positions, and treat ambiguous wording as a risk factor priced into the odds.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 3, 2026.

U.S. President Donald Trump has pushed back against criticism over his 2025 financial disclosures, telling CNBC that there was “nothing illegal” and “nothing wrong” with profiting from crypto-related investments while in office. In the interview, Trump also suggested that other parties were responsible for certain investment activity, adding that he did not “even know who they are,” an answer that did not directly address conflict-of-interest concerns.

The comments came after the U.S. Office of Government Ethics released Trump’s 2025 financial disclosure report, which shows he received more than $2 billion from business and investment holdings during the year, with roughly $1.4 billion tied to crypto ventures. Advocacy groups have argued that such earnings create incentives to shape policy in ways that benefit related projects.

Key takeaways

- Trump told CNBC he saw “nothing illegal” in profiting from crypto investments while president, even as critics highlighted potential conflicts.

- The 2025 disclosure report from the U.S. Office of Government Ethics ties about $1.4 billion of Trump’s income to crypto-related activity.

- Disclosure breakdown cited in the report includes $636 million from a memecoin, $588 million from World Liberty, and $197 million connected to equity in a stablecoin venture.

- Public Citizen says crypto-linked contributors have put $189 million into the 2026 U.S. election cycle as of June.

What Trump said after the disclosure release

During a Thursday appearance on CNBC with Joe Kernen, Trump responded to questions surrounding the 2025 financial disclosures. He maintained that profiting from crypto investments as president was not improper, framing the controversy as baseless.

When pressed on the issue of who managed or executed the investments, Trump did not provide a straightforward explanation of how he handled potential conflicts. Instead, he argued that others were responsible for the investments and said he did not know the people involved, leaving open key questions that critics say are central to public trust.

Trump’s remarks followed the release of his 2025 disclosure report by the U.S. Office of Government Ethics, an agency responsible for collecting and publishing high-level financial information from top federal officials.

How the 2025 figures connect to crypto projects

According to coverage of the filing, Trump reported more than $2 billion in income from his businesses and investments in 2025, with about $1.4 billion connected to crypto-related activities. Among the crypto-linked components cited were his memecoin, the family platform World Liberty Financial, and an equity stake associated with a stablecoin venture.

Specifically, the crypto-related totals described include approximately $636 million generated by his memecoin, about $588 million from World Liberty sales, and roughly $197 million from equity in a stablecoin venture. Together, these figures form the bulk of the reported $1.4 billion crypto-related income highlighted by critics.

Advocacy organizations have characterized these investments as a form of “grift,” arguing that political influence—whether direct or indirect—could advantage projects tied to Trump and his family. One such critique referenced in the reporting linked the donations and leverage question to proposed legislative efforts, including the Digital Asset Market Clarity (CLARITY) Act.

Earlier reporting on the disclosure emphasized the scale of the crypto-linked earnings and the overlap with areas where U.S. policy could affect digital asset markets.

From skepticism to industry alignment

Trump’s evolving posture toward crypto has been a defining theme of the past several years. In the wake of his first term, he had referred to Bitcoin as a “scam.” However, in the period leading up to the 2024 election, he increasingly associated himself with high-profile crypto figures and industry executives.

As described in the reporting, the shift included engagement with Gemini co-founders Cameron and Tyler Winklevoss, alongside relationships with executives from mining companies and crypto exchanges. During that same broader period, Trump launched a memecoin known as Official Trump (TRUMP), while his family’s involvement with World Liberty and American Bitcoin placed additional attention on crypto-native business activity.

The contrast between earlier skepticism and later engagement is central to why the disclosure controversy has attracted significant attention: critics argue the president’s financial exposure to crypto projects makes it harder to separate policy decisions from personal or business incentives.

Election spending: crypto money looks set to stay active in 2026

The controversy over Trump’s disclosures arrives amid evidence that crypto-related money is becoming a fixture of U.S. electoral spending. After digital asset firms and figures reportedly spent $170 million to support “pro-crypto” candidates to Congress in 2024, political action committees and aligned organizations appear to be applying a similar approach for 2026.

According to Public Citizen, companies and individuals tied to the crypto industry contributed $189 million to this year’s election cycle as of June. Public Citizen also reported that the $189 million figure makes up most of $294 million spent so far by crypto, AI, Big Tech, and online betting companies to support or oppose politicians.

With Trump’s term ending in January 2029, the current political landscape matters for more than symbolic scrutiny: all 435 seats in the U.S. House of Representatives and 35 seats in the Senate are up for election in 2026. For digital asset firms, stablecoins, exchanges, miners, and token issuers, legislative outcomes in the next cycle could shape compliance rules, market structure, and the pace of regulatory clarity.

Related coverage pointed to how these spending patterns reflect a sustained effort to influence policy direction during election years.

Pressure and counterpressure from within Trump’s orbit

Criticism is not limited to advocacy groups outside Trump’s circle. In comments relayed from a Friday interview with CNN’s Anderson Cooper, Mary Trump—his niece—accused him of pushing boundaries and argued that people could evade consequences due to the president’s use of the presidential pardon power.

While her remarks were not directly focused on the legal interpretation of financial disclosure rules, they underscore the broader narrative opponents are advancing: that public officials with substantial financial exposure to crypto-related enterprises face intensified scrutiny over potential conflicts of interest and the consequences for those who invest based on political proximity.

What to watch next

As scrutiny continues, the next signals to monitor are how regulators and watchdogs interpret the disclosure details in the context of federal ethics rules, and whether the 2026 election cycle brings additional policy movement on digital assets—especially in areas that intersect with stablecoins, token issuance, and broader market structure.

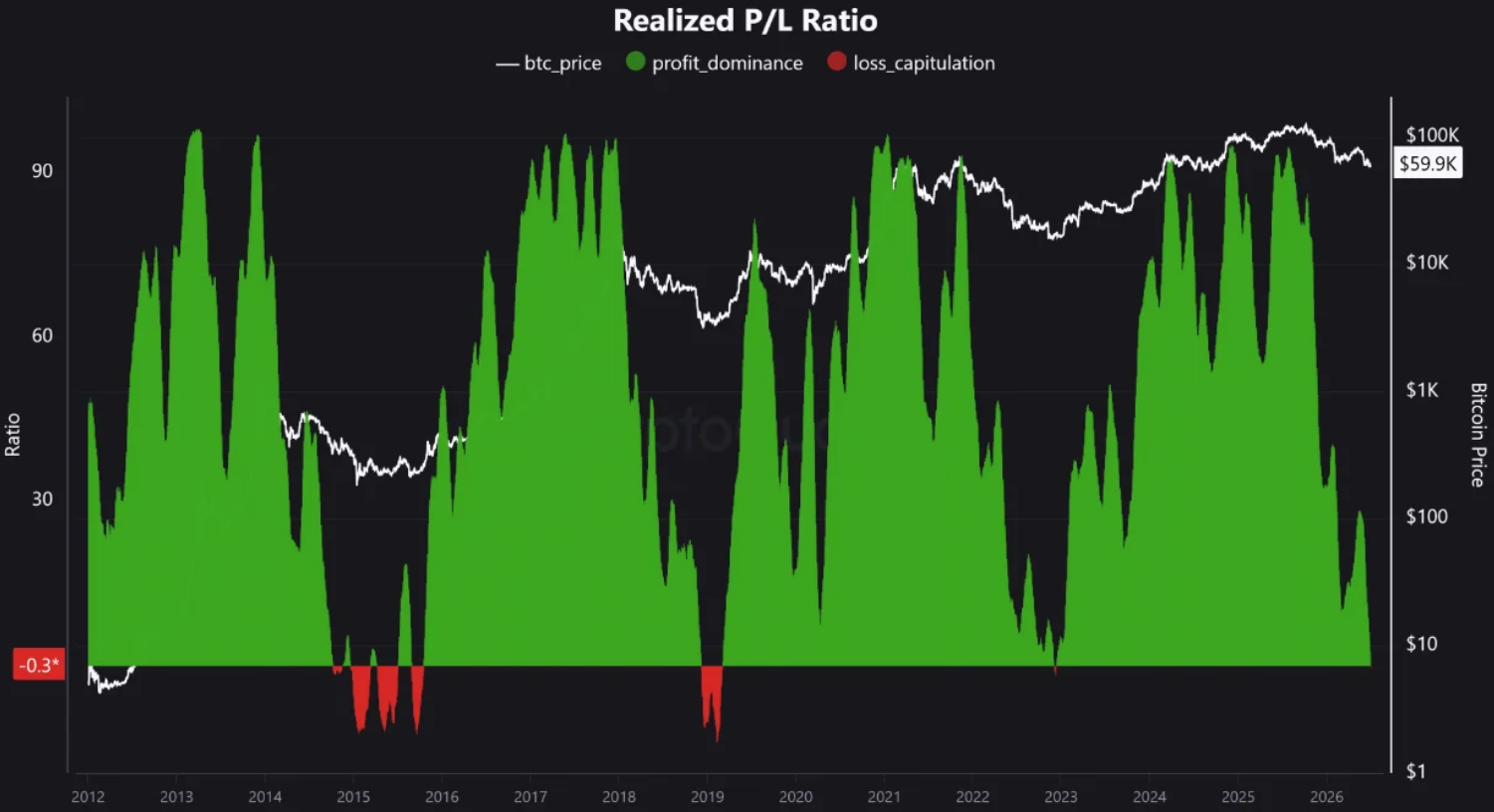

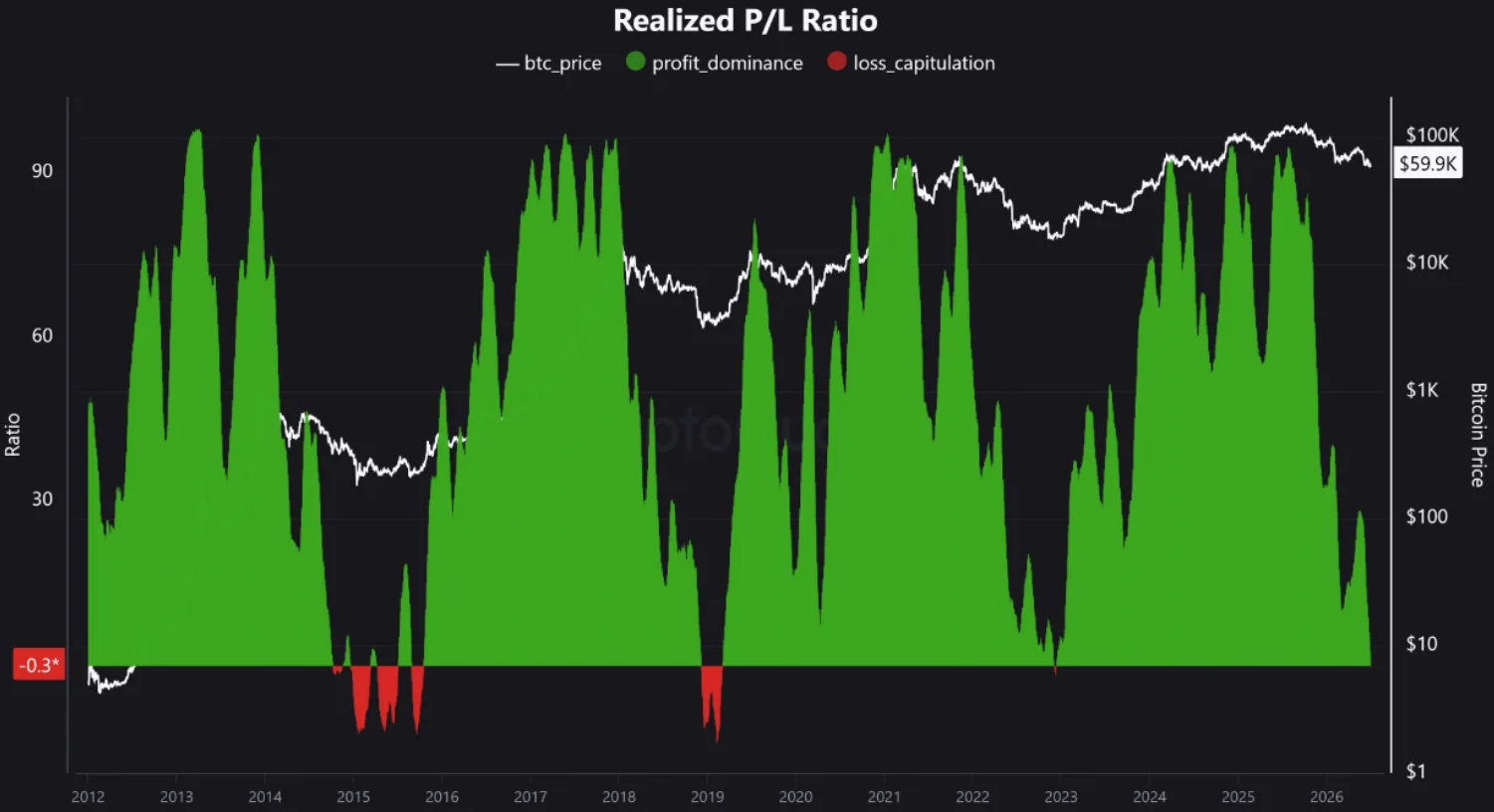

Bitcoin is flashing a highly unusual on-chain signal: its realized profit-and-loss ratio has fallen to a 43-month low of -0.35, an indicator CryptoQuant says reflects “extreme” loss conditions across the market. Historically, CryptoQuant adds, that type of reading has tended to appear close to major price bottoms.

The metric has not been this low since shortly after the FTX collapse, when Bitcoin traded below $16,000 in late 2022. With BTC still recovering from a steep drawdown that began after a peak near $126,080 in October, the new data is adding fuel to a broader debate among analysts over whether the market is past its worst stress—or merely approaching it.

Key takeaways

- CryptoQuant reports Bitcoin’s realized P&L ratio hit -0.35, the lowest reading in 43 months, last seen around late 2022.

- CryptoQuant says past occurrences of readings below -0.35 in 2015 and 2019 preceded subsequent rallies.

- CryptoQuant’s on-chain stress signal is arriving as “Fear and Greed” sentiment has moved off near-record lows and Bitcoin has bounced more than 7% from a June 25 trough near $58,190.

- Some analysts link the current drawdown to Strategy’s Stretch (STRC) preferred-stock offering and related concerns about dividend coverage.

- Other commentators argue investors should not wait for a “bottom” to be obvious because historical discount zones have been associated with strong 6- and 12-month forward returns.

Realized P&L reaches a historically rare loss zone

According to CryptoQuant, the Bitcoin realized profit-and-loss (P&L) ratio has dropped to -0.35. The realized P&L ratio measures the net percentage of Bitcoin currently in profit or loss relative to total supply, using on-chain cost basis information. In practical terms, a more negative reading indicates that a larger share of holders are underwater on their realized entry prices.

CryptoQuant emphasized that the -0.35 threshold has shown a strong historical relationship with major bottoming behavior. In its analysis published Thursday, the firm said that realized P&L has “marked BTC bottoms with extreme precision,” citing earlier periods where the ratio slipped below -0.35 before later rebounds.

The indicator’s last comparable level came around December 2022, shortly after the FTX collapse exposed fragile market liquidity. Back then, Bitcoin fell to levels under $16,000—an episode that many market participants still reference as a stress test for crypto’s risk assets.

What the signal may mean for sentiment and timing

CryptoQuant’s indicator arrives during a sharp correction cycle that began from a high set in October near $126,080, after which Bitcoin experienced a roughly 50% drawdown. While past realized P&L readings can be informative, timing remains the key question for investors: a bottom signal can appear before prices fully recover, and it does not rule out additional volatility.

Still, broader sentiment gauges show signs of stabilization. The “Fear and Greed” index has risen cautiously over the past 10 days, according to the index page on Alternative.me. During the same window, Bitcoin has climbed more than 7% after falling to a near two-year low of about $58,190 on June 25, as reflected in prior reporting by Cointelegraph.

In other words, the on-chain data and the sentiment recovery are moving in the same direction, even if they don’t provide a precise “day of the bottom” forecast.

Strategy’s STRC episode and the leverage unwind narrative

A significant part of the discussion around the latest selloff centers on corporate Bitcoin exposure. Cointelegraph previously reported that analysts attributed much of the recent weakness to Strategy—the largest corporate Bitcoin holder—after its top perpetual preferred stock offering, Stretch (STRC), deviated from its $100 par value. The move reportedly pushed STRC below $75, raising concerns that Strategy’s dividend model may have been strained.

On Thursday, Cointelegraph noted that Bitwise chief investment officer Matt Hougan said the STRC incident likely helped “squeeze out excess leverage” and could be pushing the market closer to a bottom as participants work through the fallout.

For traders and long-term holders alike, this matters because leveraged positioning can magnify moves on the way down. If leverage is truly being unwound—whether through forced deleveraging, hedging adjustments, or repricing of capital-market products—then the market may become less mechanically vulnerable to sudden liquidations. What remains unclear is how much of that unwind is complete and whether new risk reappears as prices rise.

Why some analysts say buying before the “bottom” may be rational

Not all commentary is framed around waiting for confirmation. Swan Bitcoin analyst Adam Livingston pointed to how close Bitcoin is currently trading relative to its realized price—the network’s aggregate cost basis, which often acts as a reference point in on-chain analysis.

According to Livingston, Bitcoin is trading about 16% above the realized price. He argued that this historically aligns with strong forward returns, citing research showing 41% gains over six months and 81% gains over 12 months following similar discount conditions.

Livingston acknowledged that buying at this stage “feels awful,” but he argued the psychological discomfort is part of why the opportunity can appear. In his view, waiting for a “bottom” is flawed because bottoms rarely announce themselves in a way that’s reliable enough to time entries perfectly.

While that argument is not a guarantee, it reframes the debate: rather than trying to predict the exact turn, investors may focus on whether market-wide indicators—on-chain loss concentration, realized valuation levels, and sentiment—suggest that downside pressure is fading.

What to watch next

For the near term, traders and investors will likely keep comparing this realized P&L trough with subsequent price action: if Bitcoin continues to stabilize while sentiment improves and leverage unwinds, the market may be shifting from capitulation toward consolidation. The key uncertainty is whether the current signals mark a decisive bottoming phase—or simply another stage in a volatile transition.

Bitcoin’s realized profit and loss ratio has fallen to a 43-month low of -0.35, a figure that signals extreme market-wide loss conditions but has historically coincided with market bottoms, blockchain analytics platform CryptoQuant said.

The Bitcoin realized P&L ratio — which measures the net percentage of Bitcoin (BTC) in profit or loss relative to total supply — hasn’t fallen this low since December 2022, shortly after FTX shockingly collapsed and sent Bitcoin below $16,000.

“Historically the indicator has marked BTC bottoms with extreme precision,” CryptoQuant said on Thursday. In 2015 and 2019 the Bitcoin realized P&L ratio also fell below -0.35 before price rallies followed.

Change in Bitcoin’s P/L ratio since 2012. The data was taken when Bitcoin was trading at $59,000. Source: CryptoQuant

The data could lift market sentiment, which has repeatedly fallen to near-record lows during the course of Bitcoin’s latest 50% drawdown from $126,080, set in October. Market sentiment has risen cautiously over the last 10 days, with Bitcoin up more than 7% since tanking to a near two-year low of $58,190 on June 25.

Many analysts blamed that drop on Strategy — the largest corporate Bitcoin holder — after its top perpetual preferred stock offering, Stretch (STRC), broke from its $100 par value to below $75, raising fears that its dividend model was unsustainable.

Related: Crypto Biz: Bitcoin maximalism meets the realities of capital markets

On Thursday, Bitwise chief investment officer Matt Hougan said the STRC incident squeezed out excess leverage and likely moved the market one step closer to a bottom.

“As the market continues to sort things out, I’m convinced the bottom is closer than ever — and that we will enter a new bull market in the fall.”

Don’t wait for the bottom, analyst says

Swan Bitcoin analyst Adam Livingston noted that Bitcoin is currently trading only 16% above the realized price — the network’s aggregate on-chain cost basis — a level that has historically coincided with strong forward returns of 41% at six months and 81% at 12 months.

Livingston acknowledged that buying Bitcoin right now “feels awful,” but that’s precisely why it’s trading at a discount, he argued.

“Waiting for ‘the bottom’ is a wonderful plan with one flaw. The bottom never announces itself,” Livingston said, recommending investors buy now rather than overpay at the top.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Senator Kirsten Gillibrand, a leading US lawmaker involved in negotiations on digital-asset market regulation, has proposed a new ethics rule aimed at preventing elected officials—and the president and their spouse—from issuing or backing their own tokens. The push comes as renewed scrutiny continues around conflicts of interest in the crypto space.

In a notice released on Friday, Gillibrand said Congress should consider legislation that would bar elected officials and their spouses from “issuing or sponsoring their own digital assets.” Her proposal specifically covers the US president and their spouse, while not clarifying whether the restriction would also apply to other family members or, for example, the vice president’s office.

Key takeaways

- Senator Kirsten Gillibrand is calling for a ban on elected officials and their spouses issuing or sponsoring their own digital assets.

- The draft she outlined would cover the president and the president’s spouse, according to her Friday statement.

- The proposal targets concerns about self-dealing and insider influence in crypto-related policy.

- Gillibrand’s ethics push ties into broader legislative negotiations around the Digital Asset Market Clarity (CLARITY) Act, where ethics issues have contributed to delays.

- The new restriction does not explicitly extend to other relatives, even as other criticisms have focused on family involvement in crypto-linked activities.

A targeted ethics rule aimed at token issuance

Gillibrand framed her proposal as a practical safeguard for a sector still working toward consistent federal rules. In her comments, she argued that officials and their spouses should not be able to issue memecoins, emphasizing the risk that personal financial incentives could undermine consumer protections and efforts to combat illicit activity.

Her statement links the ethics concern directly to conflicts of interest: she said “self-dealing” should not be allowed to weaken the policy work required to strengthen safeguards and expand financial access. Gillibrand also pointed to the broader public interest in ensuring enforcement and rulemaking are not distorted by insider advantages.

The senator’s notice also suggested that any workable solution must be broad enough to address the integrity of the legislative process, particularly when lawmakers have influence over market structure and consumer-facing rules.

How this connects to the CLARITY Act negotiations

Gillibrand is not introducing the idea in isolation. She is also among the lawmakers negotiating the Digital Asset Market Clarity (CLARITY) Act in the Senate—a bill that has reportedly faced delays linked to ethics concerns, tokenization questions, and how stablecoin incentives would be handled.

According to earlier reporting, Gillibrand expected the chamber to vote on the CLARITY Act by the Senate’s August state work period, but said no one would support the bill without addressing ethics concerns. Her reasoning centered on the possibility that elected officials could “get rich” from crypto markets due to their insider status.

That legislative backdrop helps explain why a narrower proposal about memecoin issuance by officials and spouses could still be politically important: it would target a concrete scenario—token sponsorship or issuance by those with rulemaking power—rather than leaving ethics questions as a vague debate.

Earlier coverage from Cointelegraph noted that lawmakers were wrestling with ethical and structural concerns in the broader package, including issues related to tokenization and stablecoin-linked rewards.

GENIUS Act history and memecoin conflict concerns

Gillibrand’s latest proposal also aligns with a moment in the development of stablecoin regulation. During consideration of the Guiding and Establishing National Innovation for US Stablecoins Act (GENIUS Act) in 2025, she said that senators had removed provisions specifically targeting Trump’s connections to the crypto industry, including the president’s memecoin Official Trump.

At the time, Gillibrand said the memecoin was likely “illegal based on current law,” but she acknowledged that fully addressing Trump’s ethics problems would require a “very long and detailed bill.” Trump later signed the GENIUS Act into law in July 2025.

That history highlights a recurring tension in Washington’s approach to crypto ethics: even when lawmakers see potential conflicts, crafting a solution that both clears legal scrutiny and achieves political consensus can be difficult. Gillibrand’s new initiative appears designed to shorten that distance by creating a rule that directly restricts token issuance or sponsorship by officials and their spouses.

Trump’s response and the wider conflict-of-interest debate

The proposal arrives amid continued debate over whether crypto profits by political figures create improper influence. This week, Cointelegraph reported that Trump said he earned about $1.4 billion from crypto ventures in 2025, the same year he took office.

According to Cointelegraph’s earlier reporting, Trump also asserted there was “nothing illegal” and “nothing wrong” with profiting from investments as president, while not directly answering questions about perceived conflicts of interest. The underlying concern for critics is not only whether transactions are legally permissible, but whether they erode trust in policymaking when an official’s financial exposure is tied to the regulatory outcomes.

Gillibrand’s proposal also stops short of explicitly extending the ban to all relatives. While she focused on elected officials and spouses, other criticisms have targeted the role of Trump’s sons in crypto-adjacent ventures, including World Liberty Financial and American Bitcoin, as reported in the article’s discussion of prior controversy.

That gap may matter for supporters of stricter rules: if spouses and officials are barred, critics may still ask how regulators should treat token sponsorship that is effectively enabled through broader family involvement, especially where family-linked businesses or holdings can influence perception—even if not always statutory ethics triggers.

As the CLARITY and stablecoin-related policy agendas continue to evolve, the key question for investors, builders, and market participants is whether ethics restrictions become part of a final legislative package—or remain a recurring obstacle that slows major crypto bills. Watch closely for whether Gillibrand’s proposal gains bipartisan traction, and whether negotiators are willing to translate ethics objections into enforceable rules rather than leaving them to case-by-case scrutiny.

Irish authorities have recovered another 500 BTC from wallets tied to convicted drug trafficker Clifton Collins.

Summary

- Irish authorities recovered another 500 BTC, raising total seized funds from Collins wallets to 1,500 BTC.

- Arkham data shows roughly 4,500 BTC still tied to dormant wallets linked to the case.

- Europol’s cybercrime unit helped investigators access wallets once believed unreachable due to lost private keys.

The Criminal Assets Bureau said in a Facebook statement that the latest seizure was made with support from Europol’s European Cybercrime Centre.

The latest recovery brings CAB’s total in the Collins case to 1,500 BTC. The bureau said the Bitcoin was identified as proceeds of crime. It marks the third 500 BTC recovery from the same wider wallet cluster this year, after earlier seizures in March and May.

Case traces back to lost private keys

The Collins case became known because the Bitcoin was long believed to be out of reach. The Irish Times reported in 2020 that Collins bought most of the coins in late 2011 and early 2012 using proceeds from cannabis sales. He later split more than 6,000 BTC across 12 wallets, with 500 BTC in each wallet.

According to that report, Collins printed the private keys on paper and hid them in the aluminum cap of a fishing rod case at a rented home in County Galway. The property was later cleared after his arrest, and the fishing gear was believed to have been taken to a dump. The keys were then viewed as lost.

Europol support remains central

Europol has helped Irish investigators in the wallet recovery work. The Irish Times reported in March that CAB accessed the first 500 BTC wallet with support from Europol’s European Cybercrime Centre. Garda Headquarters said at the time that Europol provided “highly complex technical expertise and decryption resources” for the operation.

As previously reported, Irish authorities first accessed a lost Bitcoin wallet tied to Collins in March. That wallet held 500 BTC and was part of the same 6,000 BTC stash. The recovery was notable because the funds had been viewed as locked for years.

Dormant wallets still hold large value

As crypto.news reported in May, the seizure later reached 1,000 BTC after CAB and Europol secured a second 500 BTC wallet. At the time, Arkham said another 500 BTC had moved from the Collins-linked entity after years of inactivity.

The latest move raises the total known recovery to 1,500 BTC. Onchain data from Arkham still tags wallets linked to Collins and shows remaining activity tied to the entity. Lookonchain also said in a July 2 post on X that another 500 BTC had been deposited to Coinbase Prime, while about 4,500 BTC remained in wallets linked to the case.

Recovery keeps case under scrutiny

The Collins case remains one of Ireland’s best-known crypto crime recoveries because the funds were tied to old private-key storage and years of inactivity. Each wallet recovery reduces the amount still considered dormant, but a large balance remains under watch by onchain analysts.

The case also shows how law enforcement agencies are using technical support and blockchain tracking in asset recovery. CAB has not fully explained how investigators gained access to the latest wallet. For now, the confirmed recoveries show that Bitcoin once viewed as lost may still be reachable when agencies combine legal seizures, cybercrime support, and onchain tracing.

The U.S. Securities and Exchange Commission (SEC) is studying a more orderly process for ETF approvals as the agency faces a sharp rise in new product filings.

Summary

- SEC officials want a clearer ETF process as crypto and prediction market filings increase sharply.

- Confidential filings could protect ETF issuers from copycats before new products become public.

- Prediction market ETFs remain under review while regulators seek feedback on novel fund structures.

Bloomberg ETF analyst Eric Balchunas said in a post on X that SEC Investment Management Division official Brian Daly said the agency receives about 200 ETF applications each month.

Daly made the comments during a Trillions interview with Balchunas and Joel Weber. According to Balchunas, Daly said the SEC “did a bad job with crypto” and wants to rebuild trust through an “orderly process” for novel products, including prediction market ETFs.

Confidential filings under review

Balchunas said in a second post on X that the SEC is also considering confidential ETF filings. The idea would allow some issuers to file products privately before their applications become public. That could protect early ideas and reduce copycat filings.

The SEC raised a similar issue in its public review of novel ETFs. As crypto.news reported, the agency asked whether ETF filings should stay confidential for part of the 75-day review period before becoming public. The agency said this could give applicants more room to develop products without rushing incomplete filings into the market.

Prediction market ETFs remain paused

The review comes while prediction market ETFs remain under SEC scrutiny. As crypto.news reported, the SEC delayed several prediction market ETF proposals while seeking public input on how event-based funds should be regulated. Bitwise, Roundhill Investments, and GraniteShares had filed products tied to elections and other event contracts.

The SEC’s official June 30 request asks for feedback on ETFs that invest in innovative assets or use novel strategies. SEC Chair Paul Atkins said ETF innovation depends on a “consistent, transparent, and efficient regulatory framework.” Daly also said ETF assets grew from $4 trillion in 2019 to more than $12 trillion at the end of 2025.

Crypto ETFs add to the filing wave

The agency’s review also matters for crypto funds. As previously reported, the SEC approved the T. Rowe Price Active Crypto ETF, a multi-asset product that may hold Bitcoin, Ethereum, XRP, Solana, Dogecoin, Shiba Inu, and other assets. That approval showed how crypto products are moving beyond single-asset funds.

Other issuers are also testing the new ETF path. Bitwise filed an S-1 for a spot SUI ETF, while the SEC’s generic listing standards have shortened parts of the approval process for qualifying products. The rising number of applications has made process questions more urgent.

The SEC is also reviewing wider digital asset rules. Previously, crypto.news reported that Atkins backed a limited innovation exemption for tokenized securities. That work sits beside the ETF review as the agency tries to support new products while keeping investor disclosures clear.

For ETF issuers, confidential filings could change how new products reach the market. For investors, the main question is whether the SEC can speed up reviews without weakening oversight. The current review shows the agency is trying to avoid another uneven approval cycle as crypto, tokenization, and prediction markets enter the ETF market.

CACEIS, the custody banking arm of Crédit Agricole, is in exclusive talks to acquire French crypto investment platform Meria, according to a BlockStories report.

Summary

- CACEIS is reportedly targeting Meria to expand beyond crypto custody into brokerage and staking services.

- Meria’s MiCA license gives the French platform stronger regulatory access across Europe’s crypto market.

- The talks show banks are buying crypto-native firms as MiCA raises compliance pressure across Europe.

The deal has not been formally announced by either company.

Meria, formerly known as Just Mining, was co-founded by Owen Simonin, known online as Hasheur. The company serves about 150,000 users and manages roughly €350 million in assets under management, according to the report. Its main services include crypto brokerage and staking products.

A bank push into crypto services

CACEIS already has a digital asset business line focused on custody. The company says its crypto services target asset managers, institutional investors, and other clients seeking regulated access to digital assets. Its parent group, Crédit Agricole, is one of France’s largest banking groups.

CACEIS also holds French and European crypto permissions. The AMF’s public record says CACEIS Bank has been authorized to provide crypto-asset services under MiCA through the Article 60 notification route. That allows the group to offer services such as custody, order reception, and transfer of crypto-assets.

Meria adds retail reach and staking

A Meria deal would give CACEIS access to a crypto-native platform with a retail user base and staking expertise. BlockStories reported that staking is one of the activities of interest to CACEIS, as Meria serves both retail and institutional clients in that area.

The reported talks come shortly after Meria received MiCA CASP authorization in France. A market intelligence listing shows Meria SAS as a France-based MiCA Crypto-Asset Service Provider authorized by the AMF on June 22. That timing gives the platform added value as Europe’s new licensing regime takes full effect.

MiCA changes the deal market

The talks reflect a wider shift in Europe’s crypto market. The MiCA transition period ended on July 1, forcing many crypto firms to secure CASP licenses or stop serving users under the old national regimes.

MiCA gives licensed firms a European passport, but it also raises compliance costs. As previously reported, France and other EU markets have seen a divide between firms that secured authorization and those still working through the process. That gap may push banks and larger regulated firms to buy licensed crypto platforms instead of building everything internally.

Banks move closer to regulated crypto

The reported Meria talks also fit a broader pattern of regulated finance moving into digital assets. As crypto.news reported, Coinbase opened its Luxembourg MiCA hub as the EU deadline approached. The exchange used Luxembourg as its base for serving customers across the bloc under one licensing setup.

Other firms have taken similar steps. As reported by crypto.news, Ripple moved closer to full MiCA compliance through Luxembourg CASP approval, while B2C2 secured MiCA approval to expand regulated crypto trading across Europe.

The National Organization of Black Law Enforcement Executives has endorsed the Digital Asset Market Clarity Act, giving the crypto market structure bill its first formal public backing from a major law enforcement group.

Summary

- NOBLE became the first major law enforcement group to formally back the CLARITY Act.

- The endorsement challenges warnings from police and prosecutor groups over Section 604 language.

- The bill still needs Senate floor time and 60 votes before reaching final passage.

Journalist Eleanor Terrett reported the endorsement in a July 2 post on X, citing a letter sent to Senate leaders John Thune and Chuck Schumer.

NOBLE National President Reneé Hall signed the letter. According to Terrett, the group said the bill “contains several provisions” that could give law enforcement new tools while keeping existing criminal authorities in place. The endorsement arrives as Senate talks continue over crime, oversight, and developer protections in the bill.

Endorsement breaks from other groups

NOBLE’s position differs from earlier warnings by several police and prosecutor groups. Four U.S. law enforcement organizations raised concerns that Section 604 may weaken crypto crime investigations. Their concerns centered on the Blockchain Regulatory Certainty Act language inside the CLARITY Act.

Section 604 would protect some non-custodial developers and software providers from automatic money transmitter treatment. Critics argue that the language may make it harder to trace illicit finance in decentralized systems. Supporters say the section protects software builders who do not control user funds and should not be treated like banks or brokers.

DOJ pushback adds to debate

The debate widened after the Department of Justice pushed back on claims that the bill would create broad enforcement gaps. As crypto.news reported, the DOJ challenged law enforcement claims and said criticism of the bill’s crime-fighting language was not accurate.

NOBLE’s letter now gives supporters another argument as they seek Senate votes. The group said the bill does not change federal criminal tools used in money laundering, unlicensed money transmission, conspiracy, sanctions, and other cases. That point directly addresses one of the main objections raised by other law enforcement groups.

Senate clock remains tight

The endorsement comes as the bill faces a narrow window in the Senate. The CLARITY Act’s path depends on a pre-August vote because the chamber has limited floor time before recess. If the bill misses that window, its realistic path could move into 2027.

The bill also needs 60 votes on the Senate floor. As previously reported, the Senate math requires Democratic support because Republicans cannot pass the measure alone. That makes law enforcement concerns important, especially for senators focused on illicit finance, consumer protection, and national security.

Industry keeps pressure on lawmakers

Industry groups are also pressing senators to act. Stand With Crypto urged supporters in a July 2 post on X to call for a vote when the Senate returns from recess on July 13. The group argued that delay could push builders, jobs, and capital outside the U.S.

Every day without clear rules, innovation drifts overseas.

When the Senate is back from recess on July 13, Senators can vote YES on the Clarity Act to keep American builders, jobs, and capital here at home instead of heading abroad.

The window is narrow. Tell your Senators to… — Stand With Crypto🛡️ (@standwithcrypto) July 2, 2026

The CLARITY Act would create a market structure framework for digital assets and define roles for the SEC and CFTC. The bill would classify digital assets, set registration paths, and add compliance rules for crypto firms.

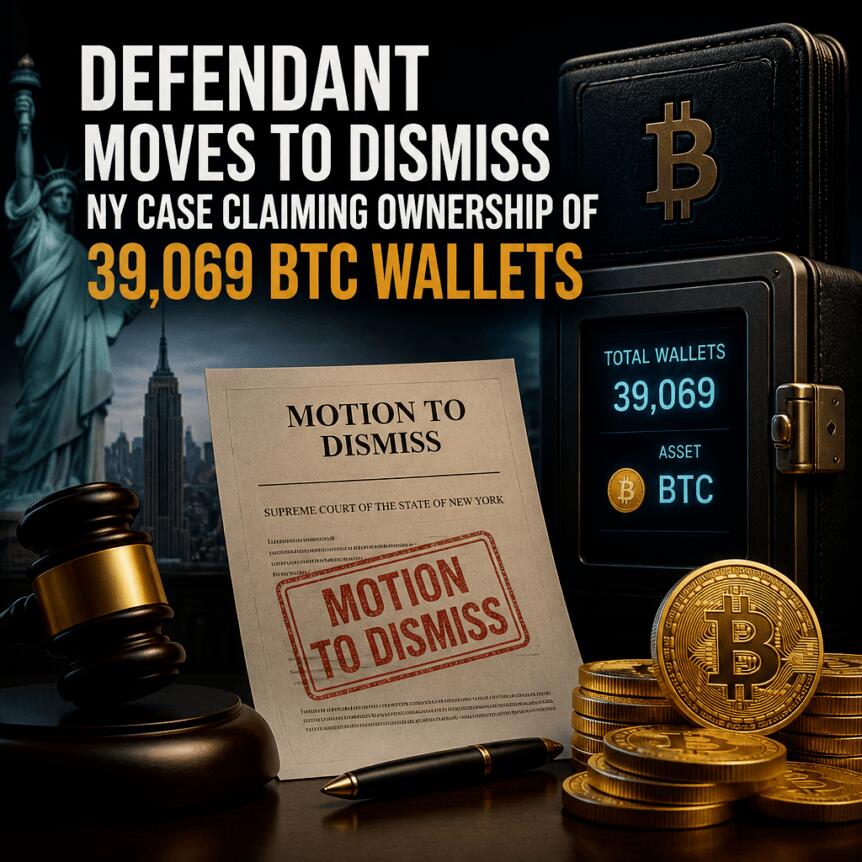

A pseudonymous defendant has asked a New York court to dismiss a lawsuit seeking ownership of 39,069 dormant Bitcoin addresses, arguing that Bitcoin addresses are simply public data and cannot be sued under the state’s jurisdictional rules.

In a motion filed Thursday, the defendant—using the name “John Doe 33”—contends that the plaintiff’s theory of “finding” and claiming abandoned property fails because a Bitcoin address is not a legal person or entity. The filing also challenges the effort to treat on-chain addresses as recoverable under New York lost-property law.

Key takeaways

- The motion argues that Bitcoin addresses are data strings that cannot be the subject of a lawsuit, rather than legal entities that courts can exercise jurisdiction over.

- The plaintiffs’ lost-property claim is framed as legally defective because the addresses were always publicly visible on the blockchain.

- Even if ownership were determined, recovering the Bitcoin would still require access to the corresponding private keys.

- Blockchain-linked reporting cited in the case suggests the defendant may control a long-dormant wallet holding roughly 5,000 BTC.

Why the court fight centers on “addresses” rather than keys

The lawsuit, filed in May by plaintiff “Noah Doe” along with two Wyoming-based LLCs identified as ABC Company and XYZ Company, targets what it describes as abandoned Bitcoin associated with 39,069 dormant addresses. The plaintiffs allege the Bitcoin tied to those addresses is abandoned property, which they reported to the New York Police Department before asserting claims under New York lost-property law.

In the motion to dismiss, John Doe 33 argues the complaint is legally defective for a threshold reason: Bitcoin addresses are not “persons” or legal entities and therefore cannot be sued. The filing further claims that the plaintiffs cannot establish that an address was “found,” as required by lost-property concepts, because the relevant address information has been publicly viewable on the blockchain since the coins were received.

For investors and builders, the procedural dispute matters because it goes beyond a single wallet list. It asks whether traditional legal frameworks for identifying owners and claiming property can map onto the blockchain’s structure—where addresses are public identifiers and control is enforced through private keys rather than through legal status.

The alleged “abandoned” wallets include famous names

The complaint lists 39,069 Bitcoin addresses that include wallets widely associated with well-known Bitcoin labels, such as addresses attributed to Bitcoin creator Satoshi Nakamoto and to the Mt. Gox hacker. The addresses collectively are reported—via an estimate attributed to Sani, founder of Bitcoin analytics platform Timechain Index—to hold roughly 3.7 million BTC, valued at about $234 billion at the time of that estimate.

That scale is a key reason the case has attracted attention. A ruling could influence how courts treat claims that attempt to convert blockchain identifiers into claimable “property” within existing state laws.

At the same time, the filing acknowledges a practical hurdle that remains independent of any jurisdictional debate: even if the court were to rule on ownership of the assets associated with the addresses, the plaintiffs would still need the private keys to move any Bitcoin. Without those keys, the Bitcoin remains inaccessible regardless of how a court characterizes ownership or abandonment.

Defendant says they control a long-dormant wallet

Separate from the legal arguments, the motion’s credibility is bolstered—at least in part—by blockchain data cited in public commentary. According to an X post on Friday by Alex Thorn, head of research at Galaxy Digital, blockchain information suggests John Doe 33 controls a wallet that received 5,000 BTC in April 2014 and has remained untouched for more than 12 years.

Thorn indicated the wallet’s current value is above $300 million at prevailing market prices, and he characterized the defendant as a “real holder” with meaningful standing rather than a bystander who could be targeted without any real ability to defend the claim.

Thorn also wrote that the filing helped avoid what had been described as a “near-certain” default judgment, while simultaneously challenging jurisdictional and statutory defects raised by the plaintiffs’ approach.

Dormancy data underscores why recovery questions persist

Beyond the specific defendants and plaintiffs, the broader question of what happens to lost or inaccessible Bitcoin continues to drive legal scrutiny. Bitbo data cited in the reporting indicates that about 3.5 million BTC, valued around $215 billion, have been dormant for at least 10 years, while another 6.6 million coins—worth roughly $406 billion—have been dormant for over five years.

Those figures highlight a persistent imbalance in how on-chain “time” translates to legal rights. Blockchain dormancy may signal lost control, but it does not automatically yield a mechanism for third parties to access private keys. This case, therefore, tests whether legal systems can bridge the gap between public address records and the cryptographic controls that govern ownership in practice.

For readers tracking regulation and legal precedent in crypto, the important development is not only who named which addresses, but how courts handle the mismatch between legal concepts like “found property” and the blockchain reality that addresses are public labels—while control is determined privately.

As the New York case progresses, the key questions to watch are whether the court agrees that addresses cannot be sued as entities, and—if the case survives procedural challenges—what standard it may apply to abandonment and recoverability when private keys are necessary to access any funds.

Chris Larsen has reportedly backed a derivatives startup founded by the son of US Senator Kirsten Gillibrand as lawmakers continue negotiating the CLARITY Act, a crypto market structure bill expected to shape the industry’s regulatory framework.

Summary

- Chris Larsen reportedly invested in a startup founded by Senator Kirsten Gillibrand’s son as CLARITY Act negotiations continue.

- The reported investment comes while lawmakers debate ethics rules tied to the crypto market structure bill.

- Senate Republicans are seeking Democratic support to pass the CLARITY Act before the legislative window narrows.

According to a Thursday report by Politico, Ripple co-founder and executive chair Chris Larsen was among the investors supporting the American Perpetuals Exchange Corp. (APEC), a derivatives platform founded by Theodore Gillibrand. The report said the company raised roughly $30 million, with most individual investors contributing between $5,000 and $10,000, though Larsen’s exact investment amount was not disclosed.

The reported investment comes while Senator Gillibrand remains involved in Senate negotiations over ethics provisions tied to the Digital Asset Market Clarity (CLARITY) Act. The proposed legislation is expected to affect digital asset companies operating in the United States, including Ripple.

Larsen remains closely watched by the XRP community

Separately, Larsen has remained under close observation by XRP investors because of his large cryptocurrency holdings and past wallet activity. Blockchain data previously showed wallets linked to the Ripple executive becoming active before notable political and market events.

Crypto.news reported in May that Larsen controls an estimated 2.58 billion XRP across eight wallets tracked on XRPScan, making him one of the largest known individual XRP holders. The publication also noted that dormant wallets linked to Larsen resumed activity in January 2025, transferring more than $109 million worth of XRP to exchanges including Coinbase, Bitstamp and Bybit.

Later, blockchain investigator ZachXBT reported that Larsen-linked addresses moved another 50 million XRP, with roughly $140 million eventually reaching exchanges while XRP traded near record highs.

In the meantime, Democratic lawmakers have continued pressing Republicans to include stronger ethics language in the CLARITY Act, citing President Donald Trump’s connections to the cryptocurrency industry.

The Senate has only a limited window to complete work on the CLARITY Act before lawmakers leave Washington again. Following the Independence Day recess, senators are scheduled to return on July 13 before another month-long state work period begins in August, narrowing the available time to pass the legislation before the US election period is expected to slow congressional activity.

Republican lawmakers, who hold a narrow Senate majority, have indicated they expect the bill to pass the chamber during July. Senator Cynthia Lummis said in June that negotiations were still covering ethics provisions, decentralized finance, and illicit finance issues. Because the legislation requires 60 votes in the Senate, Republican lawmakers will need Democratic support for the measure to advance.

XRP: “WE’RE ABOUT TO GET FILTHY RICH” Popular Analyst Claims -Report

50-day ‘summer of play’ event given go-ahead at popular National Trust estate

Soda, Coffee, and Cava Won the First Half. Snacks and Pizza Struggled.

-

Tech6 days ago

Tech6 days agoClaude Code turned every engineer into three. Now companies need more product thinkers

-

Tech6 days ago

Tech6 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Fashion10 hours ago

Fashion10 hours agoWeekend Open Thread: High Hopes

-

Crypto World4 days ago

Crypto World4 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics16 hours ago

Politics16 hours agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

News Videos5 days ago

News Videos5 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech4 days ago

Tech4 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Crypto World6 days ago

Crypto World6 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business4 days ago

Business4 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World7 days ago

Crypto World7 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Tech7 days ago

Tech7 days agoRussian hackers now target Signal backup recovery keys

-

Business4 days ago

Business4 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Sports3 days ago

Sports3 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

NewsBeat3 days ago

NewsBeat3 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

-

Tech6 days ago

Tech6 days agoSilicon Valley paid to kill AI regulation, now it wants the rules back

-

Crypto World2 days ago

Crypto World2 days agoBinance stock trading tops $1B in first month after launch

-

Tech7 days ago

Tech7 days agoOpenAI mulls delaying IPO over valuation concerns

-

Crypto World2 days ago

Crypto World2 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

NewsBeat2 days ago

NewsBeat2 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

News Videos4 days ago

News Videos4 days agoHow to Build INSANE Live Financial Dashboards With Claude

You must be logged in to post a comment Login