Crypto World

How to Optimize Company Operational Costs: A Manual on Modern Payment Ecosystems

Recent business landscape shifts have forced companies to rethink financial management. Remote work, global teams, scattered suppliers — all demand fast, cheap, transparent settlements. Traditional banking works, sure, but often feels like shipping packages by postal carriage in the drone era. That’s why businesses increasingly seek alternatives enabling settlements without intermediaries and currency conversions within minutes.

This piece isn’t about financial miracles or tech wonders. Rather, it’s about building smart payment infrastructure, cutting fees, speeding operations while staying legally compliant. We’ll examine real tools (from classic methods to cutting-edge solutions) and identify where hidden costs lurk.

Anatomy of Corporate Payment Expenses

When Airbnb was gaining momentum, the company faced a challenge: paying hosts across 190+ countries. Bank transfers took 3–7% commission plus several days. The solution became a proprietary payment system — a path later echoed by modern crypto solutions for business, though not every company can afford or justify such investment.

Typical cost structure looks like this: payment system fees (1.5-3.5%), currency conversion (another 2-4% on unfavorable rates), interbank charges ($15 to $50 per SWIFT), internal processing costs (accounting salaries, software). Annually, an average company with €10M turnover might spend up to €350K just on transactional expenses.

Stripe published a 2023 study showing businesses underestimate real payment costs by 40-60%. Hidden expenses include chargebacks, fraud, human error during manual entry, cash flow delays. One mistaken $100K payment can paralyze a department for a week.

Classic Banking: Where Money Gets Lost

Picture a Polish IT company paying contractors in the US, India, and Portugal. Through SWIFT, transfers take 3-5 days, passing through 2-3 correspondent banks, each taking $25-40. Exchange rates set by banks with their own markup. Result: from $5,000 sent, the recipient gets $4,820. The rest vanishes in fees.

An alternative — systems like Wise (formerly TransferWise) — use local accounts to simulate international transfers. Instead of physically moving money across borders, the company sends zloty to Wise’s Polish account, while the recipient gets dollars from their US account. Fees drop to 0.4-1%, timing to one day.

Revolut Business went further, offering multi-currency accounts holding 28 currencies simultaneously. For companies with constant multi-currency settlements, this means buying euros or dollars during favorable rates, not when payment’s due.

Yet classic systems have limits. Payments to certain countries (Argentina, Nigeria, partially Turkey) remain complicated due to currency controls. Weekends and holidays paralyze SWIFT. Most importantly, even modern neobanks still operate within fiat system limitations.

Cryptocurrency Rails: When Speed Matters

When Tesla announced accepting Bitcoin, that was more PR than business strategy. But there are spheres where cryptocurrencies solved real pain points. GameStop launched an NFT marketplace in 2022 not for hype, but to monetize digital assets without intermediaries.

Practical applications run deeper than they appear. Companies use stablecoins (USDT, USDC) for rapid international settlements. Transferring $100K in USDC between Berlin and Toronto takes 15 minutes and costs $2-5, regardless of amount. Particularly relevant for e-commerce: stores can accept payments globally without configuring local payment gateways in each country.

Ripple (XRP) was specifically created for banks — JPMorgan, Santander and others test it for interbank settlements. Settlement speed: 3-5 seconds versus 3-5 days with SWIFT, fees: fractions of a cent. Mass adoption hasn’t happened yet due to regulatory uncertainty.

Businesses need to understand: cryptocurrencies aren’t fiat money replacements, but additional tools. Bitcoin or Ethereum volatility makes them unsuitable for daily settlements without instant conversion. Yet for payments to freelancers in countries with limited banking (Venezuela, Zimbabwe), sometimes it’s the only option.

Multi-Chain Solutions and Their Role

Previously, transferring between different blockchains was a quest: exchange Bitcoin for Ethereum through an exchange, withdraw to wallet, wait for confirmations. Modern cross-chain crypto swaps like those offered by LetsExchange have automated this process, allowing direct asset exchanges between different networks without centralized intermediaries.

Thorchain, Cosmos, and Polkadot built infrastructure for blockchain interaction. Practical business benefit: accept payments in one cryptocurrency, make payouts in another, optimizing fees. For instance, receive USDT on Tron network (fee $1), swap to USDC on Polygon (fee $0.01), and withdraw through Ethereum when gas is cheaper.

Uniswap V3 allows companies to independently provide liquidity and earn from exchange commissions. Some fintechs use this as an additional revenue source: account balances work instead of just sitting idle.

Important nuance — regulatory. The European MiCA (Markets in Crypto-Assets) will take full effect from late 2024, establishing clear rules for crypto business. Companies should consult lawyers before implementing crypto products.

Automation and API Integrations

Shopify processes billions annually, and the key to efficiency is complete automation. Each payment automatically reconciles with invoices, splits between seller and platform, reserves for possible returns. Human intervention only occurs when problems arise.

Modern payment gateways provide APIs for integration with ERP systems (SAP, Oracle), CRM (Salesforce), and accounting (QuickBooks, Xero). This eliminates manual data entry — the main error source. When a client pays an invoice, the record automatically enters accounting, updates inventory, triggers shipping processes.

Plaid built an entire business on connecting financial systems. Through their API, apps can check balances, initiate payments, reconcile transactions without logging into each bank separately. For companies with dozens of accounts across different banks, this proves critical.

Artificial intelligence began analyzing payment patterns. Algorithms detect anomalies (unexpected large payments, new recipients), warn about possible fraud, forecast cash flow. Visa and Mastercard use ML models to block fraudulent transactions before completion.

Geographic Peculiarities and Local Methods

What works in the US can fail in Asia. WeChat Pay and Alipay control 94% of China’s online payment market. Western companies entering the Chinese market must integrate these systems, though they fundamentally differ from familiar card payments.

Latin America lives on Pix (Brazil) and Mercado Pago (Argentina, Mexico). Pix — a state instant transfer system launched by Brazil’s Central Bank in 2020. Within three years, 140+ million users registered. Transactions are free, instant, work 24/7. For business, this means zero fees on receiving payments.

Africa built a unique mobile money ecosystem. M-Pesa (Kenya, Tanzania) processes more transactions than Western Union worldwide. People pay utilities, receive salaries, take microloans — all through SMS, without bank accounts. International companies adapt systems to such realities.

Even within Europe, differences are significant. Germans dislike credit cards, preferring SEPA transfers and cash. Netherlands lives on iDEAL (direct bank payments). Scandinavia nearly abandoned cash. Global strategy must account for local specifics.

Security and Compliance: Invisible Costs

Equifax lost data on 147 million clients in 2017 through an unpatched vulnerability. Compensation cost $1.4 billion. Security investments seem like expenses until you become a hack victim.

PCI DSS (Payment Card Industry Data Security Standard) — minimum requirements for companies processing card data. Certification costs $5K to $500K depending on volumes. But the alternative is worse: data breach fines reach $100K plus card acceptance bans.

KYC (Know Your Customer) and AML (Anti-Money Laundering) — not just bureaucracy. For violations, the European Banking Authority fines millions of euros. HSBC paid $1.9 billion in 2012 for AML requirement breaches. Compliance automation through services like Onfido or Jumio saves money long-term.

Two-factor authentication, biometrics, card data tokenization — standards that became cheaper in recent years. Google Authenticator is free but reduces hack risk by 96%. Tokenization replaces real card numbers with one-time codes — if intercepted, they’re worthless.

Practical Steps Toward Optimization

Auditing current systems is the first task. How much does each transaction type cost? What’s average speed? How much time does accounting spend on reconciliation? Buffer reduced payment processing time from 40 hours monthly to 2 hours simply by switching from manual transfers to automated systems.

Provider diversification reduces risks. If the main payment gateway crashes (Visa and Mastercard had outages in 2018 and 2022), backup picks up the load. Plus you can switch between providers depending on fees for specific regions.

Fee negotiations work. Payment systems are willing to lower commissions for stable clients with predictable volume. One European marketplace reduced acquiring from 2.8% to 1.9% simply by showing annual statistics and inviting competing offers.

Team training investments pay off. Finance professionals need to understand the difference between SEPA Instant and SEPA Credit, know when to use cryptocurrencies versus traditional rails. Shopify Academy teaches payment basics for free — such resources are available to everyone.

Future of Payment Systems

Central banks are launching their own digital currencies (CBDC). Bahamian Sand Dollar has operated since 2020, Chinese digital yuan tests in millions of transactions, ECB plans digital euro by 2028. For business, this could mean instant settlements without intermediaries at all — payment goes directly from company account to recipient’s Central Bank account.

Open Banking forces banks to share data through APIs. In the EU, this is already reality thanks to PSD2. Result — apps like Revolut or N26 can show balances from all banks, initiate payments, build analytics. Traditional bank monopoly crumbles.

Quantum computers threaten modern encryption. IBM and Google work on post-quantum cryptography. Companies should monitor developments — in 5-10 years, entire security infrastructure will need updating.

Embedded finance makes financial services part of non-financial products. Uber doesn’t just call taxis but also credits drivers. Shopify issues business loans to sellers based on sales. Tesla allows buying electric cars on credit without banks. The blurring of lines between fintech and regular business will only intensify.

Cutting Costs Without Disruption

Operational payment costs aren’t fixed. Every company can reduce them by 20-40% without radical changes. An audit, choosing the right tools, and constant optimization suffice. The financial world changes rapidly, but basic principles remain: transparency, speed, security, and reasonable cost. The rest is finding balance between innovation and stability.

Bitget CEO Gracy Chen says a $1t single‑day US stock wipeout is accelerating a global macro risk reset, while lower leverage helps Bitcoin act more like a neutral portfolio allocation than a pure risk punt.

Summary

- Over $1 trillion was wiped from US stocks in a single day as risk assets sold off.

- Bitget CEO Gracy Chen says the slide has accelerated a global “reassessment of macro risks.”

- Bitcoin’s smaller drawdown and lower leverage hint at growing status as a neutral allocation.

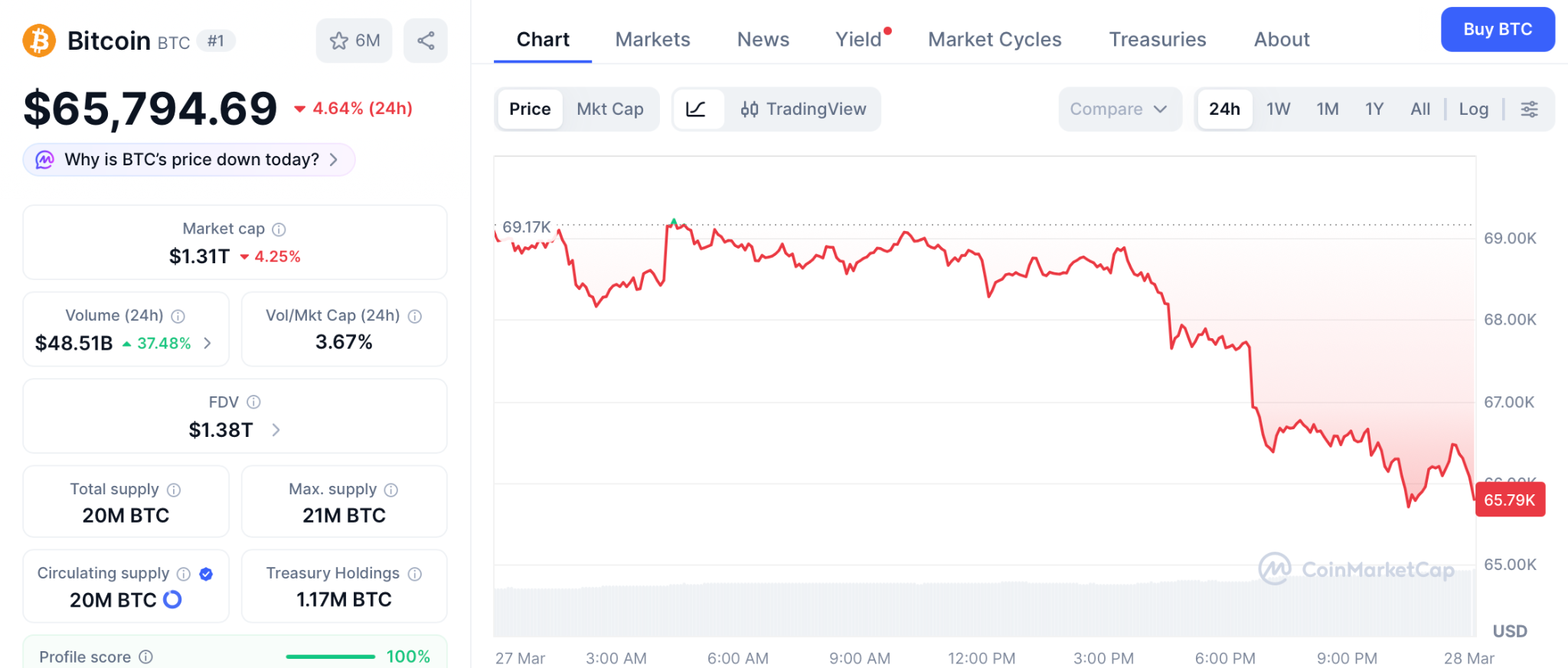

In the wake of a sharp US equity selloff that erased more than $1 trillion in market value in a single session, Bitget CEO Gracy Chen says the rout is forcing investors to reprice macro risk at a much faster clip while Bitcoin (BTC) is starting to behave more like a neutral, portfolio-level allocation than a pure risk-on punt. According to ChainCatcher, the CEO’s remarks are the latest on top of a broader drawdown that has already knocked trillions off US benchmarks since President Donald Trump’s second-term tariff agenda reignited inflation fears and hit tech-heavy names. As of Friday morning, Bitcoin was trading around $66,500, down roughly 4% on the day but still outpacing major stock indices on a relative basis.

Gracy Chen: $1t US stock selloff shows Bitcoin becoming neutral allocation

Chen argued that the current move is less about idiosyncratic crypto stress and more about global portfolios digesting a new regime of higher energy prices, stickier inflation, and geopolitical conflict spilling over into capital allocation decisions. “This round of adjustment reflects that global markets are reassessing macro risks at a faster pace,” she said, adding that as oil spikes again, “the impact of geopolitical changes is no longer limited to the energy market but is beginning to more directly affect global capital allocation.” The comment comes as strategists at Bloomberg and elsewhere flag how renewed tariff salvos and conflict risk have turned the post-2024 equity boom into what one Bloomberg analysis called a “$1 trillion wreckage,” even as Bitcoin’s institutional scaffolding has largely held.

Despite warning that Bitcoin will “still maintain high volatility in the short term,” Chen highlighted that the asset’s behavior this week has been “relatively robust” compared with previous episodes when risk appetite collapsed. She pointed to a sharp reduction in derivatives leverage as a key reason: “The overall leverage in the crypto market has significantly decreased, thereby limiting the scale of forced liquidations that typically amplify downward pressure during market stress.” That fits with recent flows data showing Bitcoin spot ETFs have seen bouts of outflows but not the kind of capitulation that marked prior crashes, while Bitget’s own protection and risk systems have been tightened as volatility climbed.

For Chen, the resilience is sending a signal about how Bitcoin is being used. “In an increasingly fragmented macro environment, Bitcoin is starting to be viewed by some portfolios as a more neutral allocation choice,” she said. That echoes her earlier comments that recent drawdowns are “tightly linked to the macro cycle,” with investors rotating between crypto, equities, and gold as they navigate Trump’s tariff-led policy shock and rising odds of a US recession. According to a recent crypto.news story, US markets have wiped out $9.6 trillion in value since Trump’s second inauguration, even as Bitcoin has repeatedly bounced after single-day drops of 1%–5%, underlining its evolving role in a world where macro risk is now the dominant driver of asset prices.

In earlier coverage, crypto.news detailed how a previous wave of selling erased $1.1 trillion from digital assets in just 41 days as leverage cascades intensified the downside, a backdrop that makes today’s more orderly drawdown stand out. Another recent story examined how the same tariff and inflation shock that hit tech stocks has rippled through crypto, while a separate report tracked how Bitcoin’s price has stayed comparatively resilient even as US equity indices flirt with bear-market territory. For live market data on Bitcoin, readers can follow its price page on crypto.news, alongside dedicated pages for other major assets involved in these rotations, including Ethereum, XRP, Solana, and Dogecoin.

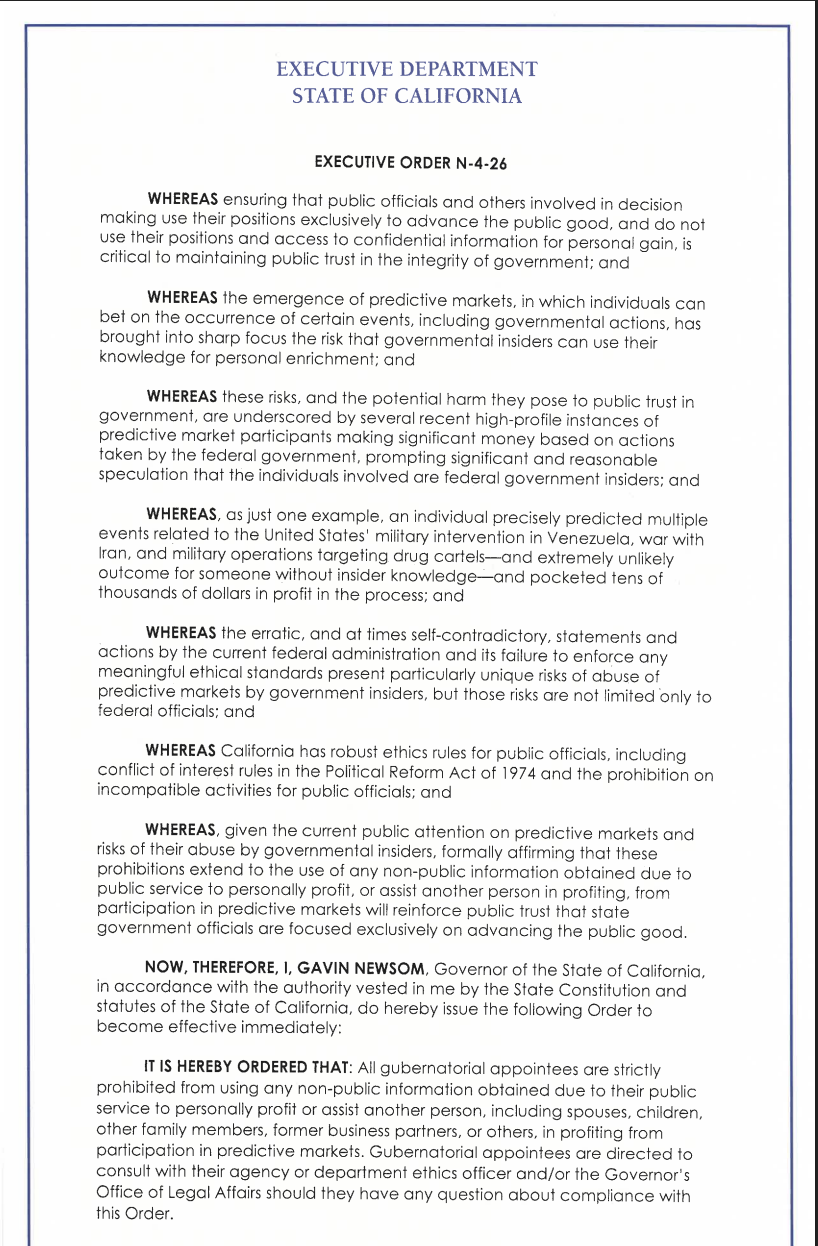

California Governor Gavin Newsom signed an executive order on Friday, expanding rules to curb public servants and those close to them from benefiting from insider trading on prediction markets tied to political or economic events they can influence or are privy to.

The order prohibits “gubernatorial appointees,” public officials appointed to office by the governor of the state, from using “confidential or non-public information” gleaned from performing their duties to profit from related prediction markets.

Newsom’s executive order also extends the prohibition to include spouses, family members or former business partners of the appointed officials from using non-public information to profit. “Public service should not be a get-rich-quick scheme,” Newsom said. He added:

“At a time when Trump’s Washington is riddled with ethical failures and insider profiteering, California is drawing a bright line: If you serve the public as a political appointee, you serve the public — period. We’re not going to tolerate this kind of corruption in California.”

An announcement from Newsom’s office listed several instances of political insiders using non-public information to profit from prediction markets, including six suspected political insiders who profited from US strikes on Iran.

Newsom’s office also cited another case of suspected insider trading, which occurred in January, after one Polymarket trader netted $410,000 betting that the US would arrest former Venezuelan leader Nicolás Maduro hours before his capture.

Prediction markets have come under scrutiny from US lawmakers, who argue that political insiders are using the platforms to unfairly benefit from their positions and are potentially threatening national security by wagering on sensitive events like war and elections.

Related: Detroit set to enter Michigan‘s battle against Coinbase prediction markets

US lawmakers accelerate prediction market crackdown after insider allegations surface

Texas Congressman Greg Casar and Connecticut Senator Chris Murphy introduced the “Banning Event Trading on Sensitive Operations and Federal Functions (BETS OFF) Act” in March 2026 in response to the prediction market insider trading allegations.

The bill seeks to prohibit government insiders from using prediction platforms to profit from markets tied to war or death.

US Representative Adrian Smith and Representative Nikki Budzinski also introduced similar legislation in March, titled the “Preventing Real-time Exploitation and Deceptive Insider Congressional Trading (PREDICT) Act.”

The legislative proposal prohibits the US President, lawmakers and other high-ranking government officials from betting on prediction markets.

Magazine: Train AI agents to make better predictions… for token rewards

Bittensor’s TAO is consolidating near $328 after a triple‑digit AI‑sector rally, with rich valuations, hot RSIs and a new golden‑cross fractal all flagging room for a 40% corrective dump toward $200 if profit‑taking accelerates.

Summary

- Bittensor’s TAO is trading near $327.81 after a 4.47% daily rebound, but remains down over 17% on the week following a sharp correction from recent highs.

- TAO’s volumes and RSIs show the token coming off an overheated, triple‑digit monthly rally, with 24‑hour turnover equal to nearly one‑fifth of its circulating supply and multi‑timeframe momentum still elevated.

- Rising whale participation and a broader AI‑token surge have driven Bittensor’s upside, but fresh fractal and golden‑cross analysis now flag the risk of a 40% drawdown if profit‑taking accelerates.

Bittensor’s (TAO) native token TAO, a leading AI and big‑data asset, is changing hands around $327.81 today, up 4.47% over the last 24 hours but still lower by 17.67% on the week as the market digests a violent, sector‑wide swing in artificial intelligence narratives. With a market capitalization of about $3.53 billion and 24‑hour trading volume of $622.80 million, TAO currently ranks among the largest AI‑linked crypto assets, reflecting both strong speculative interest and deep two‑sided liquidity.

TAO slips 17% after parabolic AI rally, fractals flag 40% downside risk

The token underpins Bittensor, a decentralized AI network that rewards machine‑learning models for contributing useful inference, effectively positioning TAO as both a governance and incentive asset at the center of an on‑chain AI compute marketplace.

Over the past month, TAO’s price has climbed more than 100%, with 7‑day, 14‑day and 30‑day gains of 21.68%, 58.38% and 105.14% respectively, before this week’s pullback. On the flow side, roughly 1.79 million TAO — equal to 18.68% of circulating supply — has traded in the last 24 hours, underscoring unusually intense activity relative to its size. Momentum remains elevated rather than exhausted: intraday RSI sits near 62, while the 7‑day RSI is around 58, signaling continued bullish bias without a full reset into oversold territory. This follows earlier spikes in whale participation and open interest that helped propel TAO’s breakout above $200 in early March, when large holders aggressively accumulated during the initial phase of the rally.

Bittensor’s TAO pauses near $328 as golden‑cross fractal warns of deeper pullback

However, the same parabolic structure that lifted Bittensor is now flashing caution. CoinMarketCap’s latest AI‑token update notes that TAO surged roughly 160% into a golden cross on March 26, and historical fractal analysis of prior crosses indicates average corrections of about 40% within five to six weeks, implying potential downside toward the $200 region if the pattern repeats. That warning comes against the backdrop of a broader AI‑crypto basket that recently advanced more than 10% in a single day, as the sector’s combined capitalization expanded sharply on March 25. In other words, while Bittensor remains a bellwether for on‑chain AI and continues to trade with strong liquidity and active whale interest, its current technical setup suggests the market is transitioning from euphoria to a more fragile phase where profit‑taking, not fresh capital, may dominate the next move.

Crypto World

BlockDAG News 2026: Stripe Acquires Bridge for $1B While Pepeto Targets Life Changing Returns as BTC and LINK Slide

The average American car payment is $740 a month stretching six years on vehicles losing value every day. Stripe just acquired stablecoin startup Bridge for over $1 billion, proving owning crypto infrastructure is where the money flows.

The blockdag news shows slow price targets, but a $5,000 Pepeto entry is targeting the kind of returns that pay off the car, the loan, and the interest from one position. More than $8 million raised with an exchange already serving traders, and analysts project 100x as the Binance listing approaches.

Stripe acquired stablecoin startup Bridge for over $1 billion, then purchased wallet provider Privy and billing platform Metronome to assemble a full stack payment ecosystem according to FinTech Weekly.

As one analyst noted, owning the rails means you stop paying rent on someone else’s blockchain.

According to CoinDesk, the stablecoin infrastructure race is accelerating as the CLARITY Act framework takes shape, and the BDAG outlook falls far short of the capital pouring into verified exchange entries right now.

The Best Entries and Where the BlockDAG News Conversation Falls Short

Pepeto: The Verified Exchange Where $5K Today Targets the Returns That Clear Car Payments Permanently

Every new token that launches creates a new risk for investors, and as the market expands the volume of dangerous contracts keeps increasing. Pepeto is the verified exchange where a $5,000 entry today targets the returns that clear $740 monthly car payments permanently, and the BDAG forecast shows a project still struggling with supply unlocks while this exchange is already running and attracting whale capital.

The exchange’s contract scanner becomes more valuable as the ecosystem grows, checking every project automatically before the reader’s money goes near it and explaining what it found in plain language.

PepetoSwap handles every trade without taking any commission so portfolios stay intact, the blockchain connector moves tokens across networks at zero transfer cost, and a SolidProof audit confirmed every contract. The mind behind the original Pepe coin, which climbed to $11 billion on meme power with zero products backing it, engineered this exchange alongside a Binance infrastructure veteran.

In the months ahead, the BDAG headlines will fade and the crypto news will eventually cover the success stories made by Pepeto, the exchange seeing demand, and the returns earned, but by then the entry is gone. Analysts project 100x from the current entry at $0.000000186, and 192% APY staking expands every wallet’s position as the Binance listing nears. Rounds close faster every week, the presale is still accepting entries, and a 2026 portfolio with Pepeto is most likely the strongest decision any investor carrying $740 monthly car payments can make right now.

Bitcoin (BTC)

BTC trades at $65,794 per CoinMarketCap, down 5.6% on the week after the $14 billion options expiry triggered mass selling. MARA sold 15,133 BTC just to manage debt, and a recovery to $75,000 delivers 11% over months, a slow rebuilding play, while the presale entry targets 100x from one listing event the miners selling BTC are watching others position for.

MARA sold 15,133 BTC just to manage debt, and a recovery to $75,000 delivers 11% over months, a slow rebuilding play, while the presale entry targets 100x from one listing event the miners selling BTC are watching others position for.

Chainlink (LINK)

LINK sits at $8.66 per CoinMarketCap, grinding 83% below its $52.70 all time high after six consecutive red monthly candles.

A break above $9.74 targets $11 for a 27% move, and while the BDAG conversation keeps the project visible, presale entries are where the life changing returns live and Pepeto offers exactly that math.

The BlockDAG News Will Fade but the Wallets Inside Pepeto Are Building the Returns the Market Will Cover

Stripe just spent over $1 billion to own stablecoin rails, and American families spend $740 a month on car payments stretching six years.

The BDAG news cycle keeps attention on a project with slow price targets, but in the months ahead the crypto news will cover the success stories made by Pepeto, the exchange seeing demand, and the returns that changed portfolios, and by then the entry is gone.

The Pepeto official website is still accepting entries, and a 2026 portfolio with Pepeto before the Binance listing is the decision that separates the families still making car payments from the ones who cleared every balance from one position.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What does the blockdag news mean for investors searching for better entries?

The blockdag news shows slow price targets while Pepeto’s verified exchange targets 100x from one Binance listing event, and the presale entry clears car payments from one position.

What is the latest blockdag news investors should watch?

The blockdag news cycle keeps the project visible, but the Pepeto official website is where the 100x entry with a verified exchange and Binance listing is still open.

Does the blockdag news matter for 2026 portfolios?

The blockdag news provides context for existing holders, but Pepeto’s presale with the Pepe builder and Binance listing targets the returns that change the reader’s financial life.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Coinbase and Better Home & Finance have operationalized the first conforming crypto-backed mortgage in U.S. history, allowing borrowers to pledge Bitcoin or USDC as collateral for a Fannie Mae-backed home loan without liquidating their positions.

The product plugs directly into the $12 trillion U.S. residential mortgage market, not as a niche private offering, but as a GSE-conforming instrument backed by the same federal infrastructure that underwrites more than half of American home purchases.

The surface headline is historic. The mechanism underneath it is where the real trade-off lives. BTC is discounted to 40% of market value for collateral purposes; USDC is discounted to 80%. A borrower pledging $100,000 in Bitcoin receives $40,000 in usable down payment credit, a haircut that makes the math work for the GSEs but demands significant overcollateralization from the borrower.

The question this article answers: what does it actually take to use crypto to buy a house under this framework, and what does the product’s existence signal about where institutional mortgage infrastructure is heading?

- Policy Trigger: FHFA Director Bill Pulte directed Fannie Mae and Freddie Mac on June 25, 2025, to develop crypto-as-asset underwriting guidelines, providing the regulatory foundation for this product.

- Haircut Mechanism: BTC is valued at 40% of market price; USDC at 80%. A $100,000 BTC position yields $40,000 in qualifying collateral.

- First Mover: Coinbase and Better Home & Finance are executing the first conforming loan under this structure; lender Newrez has since launched its own parallel crypto-backed program.

- Scope Limitation: Only assets held on U.S.-regulated exchanges with AML compliance and a 60-day holding history qualify — cold wallets, DeFi positions, and staked assets are excluded.

Discover: The best crypto presales gaining institutional momentum right now

How the Loan Structure Actually Works

The product is structured as two instruments layered together: a primary conforming Fannie Mae-backed mortgage and a second mortgage covering the down payment, secured by pledged crypto collateral. Coinbase holds the pledged assets in custody; borrowers do not transfer ownership, but the collateral is encumbered for the loan’s duration.

Get your house and keep your crypto. — Coinbase

Crypto-backed mortgages are here – increasing access to homeownership for millions of Americans.

Buy a home without converting your portfolio by using BTC or USDC as collateral for your down payment.

Offered by Better, powered by Coinbase. pic.twitter.com/9hfL3fVty5

(@coinbase) March 26, 2026

(@coinbase) March 26, 2026

The haircut is the defining constraint. To generate $80,000 in qualifying down payment credit using Bitcoin at the 40% valuation rate, a borrower must pledge $200,000 in BTC.

USDC’s 80% rate is more capital-efficient; $100,000 in USDC yields $80,000 in usable collateral, but still demands a meaningful overcollateralization buffer.

Fannie Mae’s volatility haircut framework is designed precisely to absorb the asset class’s price swings without triggering forced liquidations on the borrower side.

There are no margin calls. Collateral is not at risk from short-term price drops. The crypto position becomes actionable for the lender only after 60 or more days of delinquency, aligning with standard foreclosure timelines and deliberately decoupling the mortgage’s credit risk from crypto’s daily volatility.

Eligible assets must be held on a U.S.-regulated exchange with full AML compliance and a minimum 60-day documented holding history. Cold wallets are excluded. DeFi positions do not qualify. Staked assets are out. The framework is narrow by design; it trades flexibility for GSE compatibility, which is the only pathway to conforming status.

The policy architecture behind this traces directly to FHFA Director Pulte’s June 25, 2025, directive ordering Fannie Mae and Freddie Mac to develop formal underwriting guidelines for digital assets. Phase 1 framework proposals covering volatility treatment and documentation standards are currently under FHFA review, with a 6-to-12-month timeline before the rollout of Phase 2 criteria.

Discover: The best crypto presales gaining institutional momentum right now

The post Coinbase Powers First Crypto-Backed Conforming Mortgages appeared first on Cryptonews.

Avalanche’s AVAX is grinding sideways around $9, testing key support as a bullish “digital commodity” ruling, Animoca partnership and cheaper subnets collide with thin liquidity and stubborn overhead supply.

Summary

- Avalanche’s AVAX is trading close to $9.07 today, roughly flat on the day but struggling to hold above the $9.00–$9.50 support zone after a multi‑month drawdown.

- The token, a layer‑1 smart contract platform, carries a market cap in the low‑single‑digit billions and remains under pressure despite recent regulatory clarity and high‑profile partnerships aimed at driving institutional and real‑world asset adoption.

- Technical indicators show mixed momentum, with AVAX hovering near oversold territory on higher time frames while intraday moves remain range‑bound, framing the current price action as a possible basing attempt rather than a confirmed reversal.

Avalanche’s (AVAX) native token AVAX, the core asset of the Avalanche layer‑1 smart contract network, is trading around $9.07 today, marking a sideways session that leaves the token pinned just above critical support in the $9.00–$9.50 band.

After starting 2026 near $12.31 and sliding to an average closing level near $10.14, AVAX has posted a double‑digit percentage decline year‑to‑date, underperforming several rival smart contract platforms as broader altcoin liquidity thins out. The asset underlies a high‑throughput, subnet‑based ecosystem designed to host DeFi, gaming and real‑world asset (RWA) applications, positioning AVAX squarely in the L1 and RWA‑adjacent category in the current market structure.

AVAX tests $9–$9.50 floor as institutional RWA story outruns spot demand

In terms of immediate trading dynamics, recent analysis pegs AVAX consolidating between roughly $8.66 and $10.20, with short‑term forecasts calling for only a modest 2.95% upside toward $9.53 over the coming days if support holds. Technical dashboards show RSI cycling in the neutral‑to‑slightly‑oversold range depending on timeframe, and prior attempts to sustain a breakout above the $10 psychological level have faded quickly, underscoring the presence of persistent overhead supply. That pattern is consistent with a market where retail participation has retreated sharply following a 94% decline from all‑time highs, leaving price heavily dependent on selective institutional flows rather than broad speculative enthusiasm.

Fundamentally, Avalanche has logged several milestones that should, in theory, support AVAX over the medium term. On March 17, 2026, U.S. regulators formally classified AVAX as a “digital commodity,” aligning it with Bitcoin and Ethereum from a legal standpoint and potentially smoothing the way for regulated products and deeper institutional involvement. Days later, Web3 heavyweight Animoca Brands disclosed an investment and strategic partnership with Ava Labs aimed at growing Avalanche’s footprint in Asia and the Middle East, including targeted deployments in RWA, digital identity and entertainment. On the technology side, the November 2025 Granite mainnet upgrade and prior Octane hard fork dramatically cut fees, improved cross‑chain messaging and introduced biometric‑friendly cryptography, making it cheaper and simpler to launch subnets and onboard mainstream users.

Yet price remains stuck in a tight range because this fundamental progress has not fully translated into sustained spot demand for AVAX. Analysts note that real‑world asset TVL on Avalanche has pushed above $1.3 billion, with institutional pilots from major financial firms, but these flows are gradual rather than explosive, and many treasuries hedge or amortize their AVAX exposure. As a result, the current tape looks like a classic disconnect: structurally bullish long‑term narrative, but near‑term price dictated by whether $9.00 can hold in the face of lingering risk‑off sentiment across non‑Bitcoin, non‑Ethereum large‑caps.

LayerZero has become the first interoperability protocol live on the Canton Crypto Network, the institutional blockchain backed by Goldman Sachs, Microsoft, and DTCC, enabling regulated financial institutions to route tokenized assets across more than 165 public blockchains while preserving compliance standards.

This is kind of Wall Street’s tokenization infrastructure opening a direct channel to the entirety of onchain liquidity.

- Integration Scope: LayerZero is now live on Canton Network, connecting its $100 billion ecosystem to Canton’s institutional rails and enabling cross-chain access to 165+ public blockchains.

- Institutional Signal: Canton already processes more than $350 billion in daily U.S. Treasury repo volume; testing participants include Goldman Sachs, BNP Paribas, Tradeweb, and Citadel Securities.

- Market Implication: Nearly 400 ecosystem participants on Canton now have a credible path to cross-chain tokenized asset deployment — a structural liquidity unlock for institutional RWA markets.

Discover: The best crypto presales gaining institutional momentum right now

Routing $350 Billion in Daily Repo Volume Across 165 Chains

Canton crypto core infrastructure, built by Digital Asset on the DAML smart contract language, already handles serious institutional volume. Broadridge’s distributed ledger repo platform processes between $300 billion and $400 billion in daily U.S. Treasury repo transactions through Canton — establishing it as operating infrastructure, not a proof-of-concept.

— Fundraising Digest (@CryptoRank_VCs) March 26, 2026

Goldman Sachs‑backed Canton Chain taps LayerZero

Goldman Sachs‑backed Canton Chain taps LayerZero

"@CantonNetwork has already built the rails for traditional finance, processing more than $350 billion in daily U.S. Treasury repo volume"

– Bryan Pellegrino, CEO @LayerZero_Core

This move is a step toward… pic.twitter.com/6IJqAaukMs

The LayerZero integration now sits on top of those rails. LayerZero Labs CEO Bryan Pellegrino framed the division of labor precisely: “Canton has already built the rails for traditional finance, processing more than $350 billion in daily U.S. Treasury repo volume. LayerZero’s job is to make sure those assets are available in every global market, across blockchains.”

The distinction matters technically. LayerZero does not operate as a traditional bridge, it is designed to make any token or application natively compatible with any blockchain, avoiding the custodial risk that has plagued earlier cross-chain solutions. For Canton’s compliance-focused participants, that architecture matters as much as the connectivity itself.

Testing has already involved Goldman Sachs, BNP Paribas, DRW, QCP, Liberty City Ventures, and Tradeweb, the same institutions that underwrote Digital Asset’s $135 million funding round in June 2025, led by DRW Venture Capital and Tradeweb Markets with participation from Circle Ventures and Citadel Securities.

Discover: The best presale crypto projects launching on cross-chain infrastructure right now

The post Goldman Sachs-Backed Canton Crypto Chain Adds LayerZero Interoperability appeared first on Cryptonews.

The US Treasury Department announced Thursday, March 26, that Donald Trump will become the first sitting president to have his signature appear on the US dollar, a move officials say is intended to commemorate America’s 250th anniversary.

The decision raised immediate questions about the notes’ future once the current administration leaves office. While US law guarantees all issued currency remains legal tender indefinitely, a future administration could quietly stop printing them.

Trump is Breaking a 165 Year Economic Tradition

Treasury Secretary Scott Bessent’s signature will appear alongside Trump’s, beginning with $100 bills in June, with other denominations to follow. In a press release, Bessent framed the decision as recognition of the administration’s economic record.

“There is no more powerful way to recognize the historic achievements of our great country and President Donald J. Trump than US dollar bills bearing his name, and it is only appropriate that this historic currency be issued at the Semiquincentennial,” he said.

Treasurer Brandon Beach echoed the sentiment, describing Trump as “the architect of America’s Golden Age economic revival.”

“Printing his signature on the American currency is not only appropriate, but also well deserved,” Beach said.

The announcement marked a significant departure from longstanding practice.

Since 1861, US banknotes have carried only the signatures of the Treasury Secretary and the Treasurer. The current bills in circulation bear the signatures of former Secretary Janet Yellen and former Treasurer Lynn Malerba.

The reaction was swift. California Governor Gavin Newsom was among the first to respond, posting to X:

“Now Americans will know exactly who to blame as they’re paying more for groceries, gas, rent, and health care.”

The decision represented the latest in a series of moves by the Trump administration to attach the president’s name to American institutions.

A Broader Naming Campaign

Last December, the administration renamed the United States Institute of Peace after Trump, placing his name on the organization’s headquarters following a prolonged dispute over control of the institute.

Roughly two weeks later, the Kennedy Center added Trump’s name to the performing arts complex. Congress had originally designated the venue as a living memorial to former President John F. Kennedy.

By December 22, the pattern extended to war equipment.

Trump announced plans for the Navy to develop a new class of large surface battleships, which the administration said would meet the demands of modern maritime conflict. Sky News reported at the time that a senior administration official had confirmed the fleet would be known as “Trump Class” battleships.

Unlike renaming a building or rebranding a battleship, removing a president’s signature from the US dollar is not simply a matter of political will. Any future administration seeking to undo it will face considerable logistical and legislative hurdles.

What the Next US President Can and Cannot Do

Under the Legal Tender Act, all currency issued by the United States government remains valid and redeemable at face value indefinitely.

No president, treasury secretary, or act of the executive branch can unilaterally invalidate notes already in circulation. While Congress holds constitutional authority over legal tender, no administration would willingly risk the economic disruption the process entails.

The practical path available to a future administration is narrower. It would involve instructing the Bureau of Engraving and Printing to stop producing notes bearing Trump’s signature. New currency would then be issued, quietly reverting to the previous norm.

No legislation would need to be passed. The existing notes would simply fade from circulation on their own as newly printed dollars replace them.

That process, however, will take time. Depending on how many notes are printed before any future administration changes course, Trump-signed currency could remain in widespread use for the foreseeable future.

The post Donald Trump is Leaving His Forced Legacy On the US Dollar Bill appeared first on BeInCrypto.

Zcash’s ZEC is consolidating near $235–$240 after a sharp February selloff, with a $25m ZODL raise, Foundry’s new mining pool and rising shielded use turning it into a 2026 privacy‑trade leader.

Summary

- Zcash’s ZEC is trading near $235–$240 after a mid‑March surge of over 20% in a single day, extending a multi‑week recovery from February’s steep drawdown.

- The privacy‑focused coin has seen daily volumes in the hundreds of millions of dollars during the latest upswing, as traders respond to fresh venture funding, new mining infrastructure and improving technical momentum.

- Sector‑wide interest in privacy assets has picked up in 2026, with ZEC outpacing many peers as on‑chain shielded usage rises and developers accelerate work on new wallets and consensus upgrades.

Zcash’s (ZEC) native token ZEC, one of the longest‑running privacy coins in the market, is holding near the $235–$240 range this week after a volatile first quarter that saw it sell off sharply in February before rebounding on strong March news flow.

Data from BestCryptoChecker shows ZEC’s price dropped about 20.93% in February 2026, falling from $302.80 to close the month at $239.41, underscoring how aggressively the asset had been de‑risked before the latest move higher. The token, which uses zero‑knowledge proofs to enable shielded transactions and is categorized as a privacy and payments coin, has now re‑emerged as a focal point in the renewed 2026 privacy narrative.

ZEC extends rebound as $25m ZODL raise and Foundry mining pool revive Zcash story

Momentum turned decisively in March. On March 16, ZEC posted a 23.26% daily gain to trade around $285.35, with market capitalization at roughly $4.74 billion and 24‑hour trading volume reaching $583 million, according to MEXC’s tracking. CoinMarketCap’s Zcash dashboard later highlighted that ZEC broke above $235 on March 25 on “strong volumes” following a major ecosystem funding announcement, extending a weekly gain above 10% on elevated spot turnover. While some shorter‑term RSI screens still flag periods of selling pressure on lower timeframes, 14‑day readings near the low‑to‑mid‑50s indicate neither extreme euphoria nor deep exhaustion, leaving room for trend continuation if demand persists.

Behind the tape, a series of structural developments has reframed the Zcash story for 2026. The Zcash Open Development Lab (ZODL), a new core development entity formed after the breakup of the Electric Coin Company’s engineering team, closed a funding round of more than $25 million on March 25 from backers including Paradigm, a16z crypto and Coinbase Ventures, with capital earmarked for expanding the Zodl wallet and other privacy‑first tools. CoinMarketCap also reports that Foundry Digital, the largest Bitcoin mining pool, plans to launch an institutional‑grade ZEC mining pool in April 2026, marking its first move beyond Bitcoin and signaling growing confidence in Zcash’s long‑term viability. Additional roadmap items, including the CashZ wallet launch, consensus protocol upgrades and continued ZODL‑led ecosystem expansion, underline an effort to modernize infrastructure and make shielded transactions more accessible, potentially deepening ZEC’s role as a base layer for private finance.

Beyond Zcash itself, privacy coins as a group have begun to stage a comeback in 2026, with MEXC noting that ZEC and peers have delivered double‑digit daily moves as regulatory clarity around “digital commodities” and renewed interest in zero‑knowledge technology shift attention back to privacy‑preserving chains. That broader context matters: while some traders still see scope for a deeper correction toward the $100–$150 range based on ZEC’s longer‑term breakdown from much higher levels, recent funding, infrastructure and usage data have opened the door to a sustained repricing if the privacy trade continues to attract both retail and institutional capital.

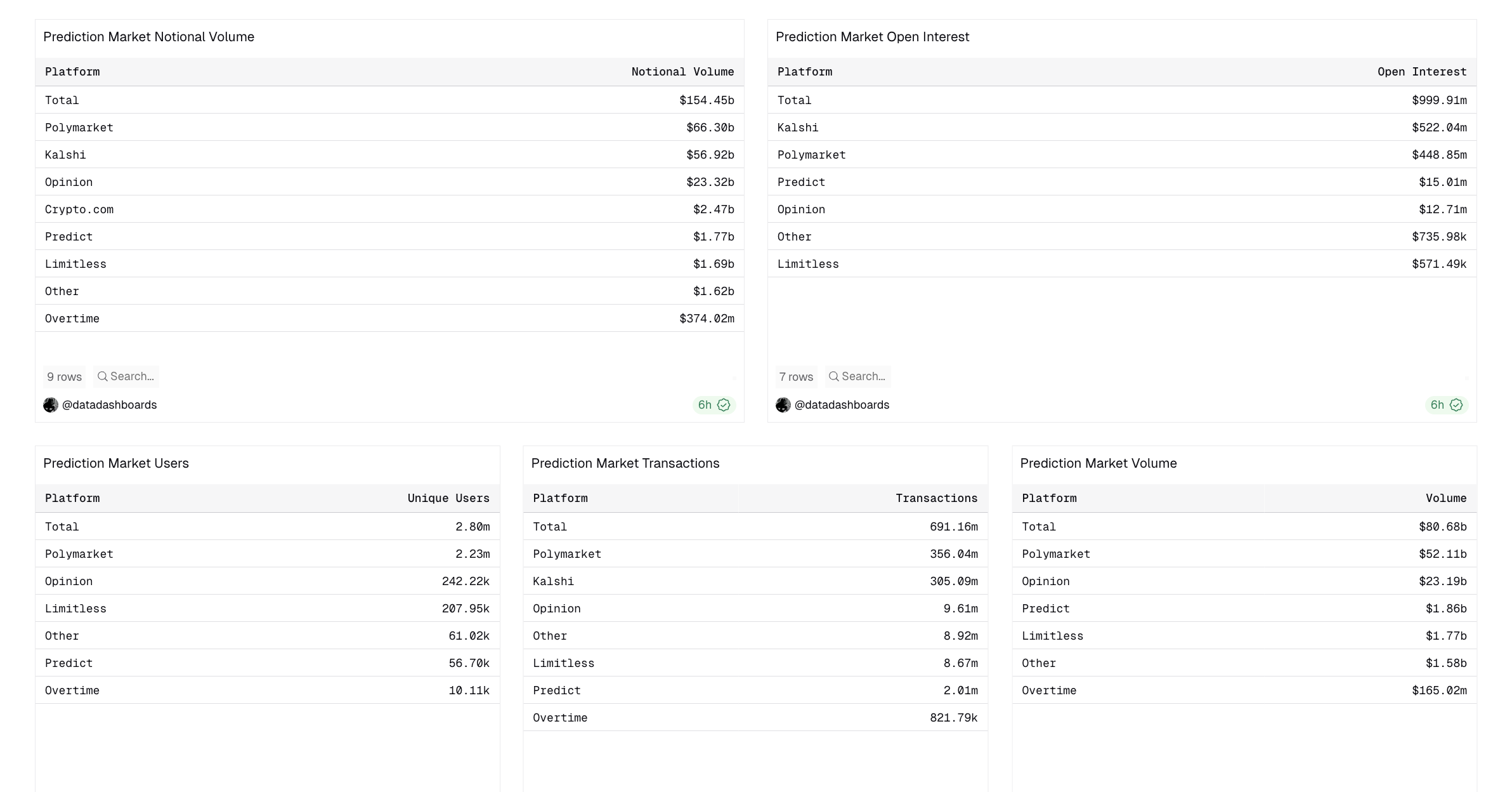

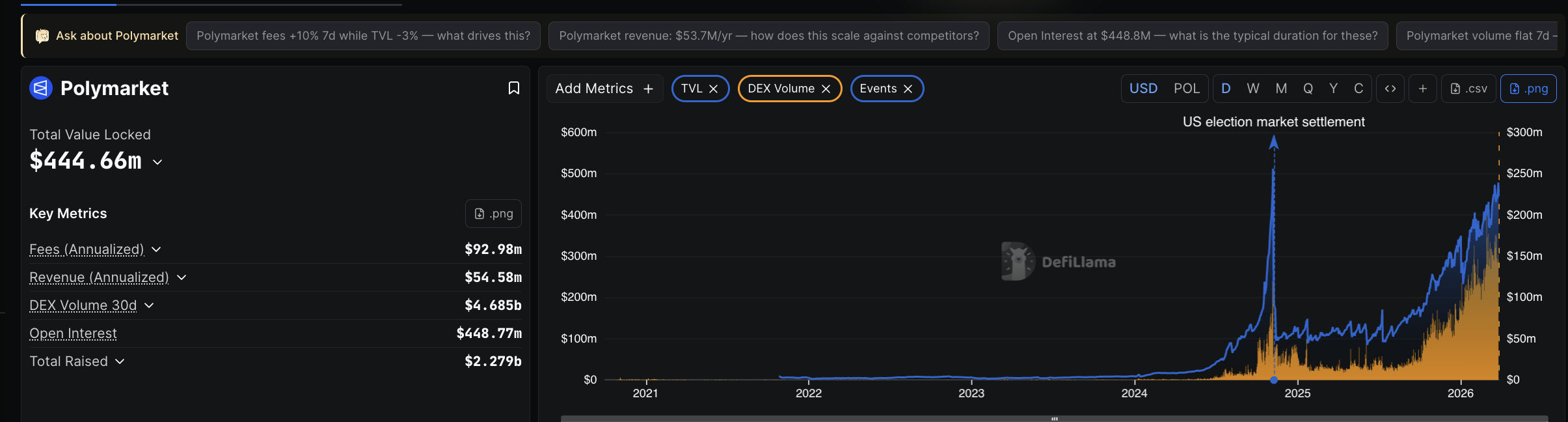

Prediction markets have processed more than $154 billion in total volume, with daily trading on Polymarket alone often exceeding $300 million.

That scale forces a more important question. These platforms no longer look like niche betting venues. They increasingly resemble something closer to retail trading.

This analysis uses on-chain data, primarily from Polymarket—the largest platform by users and transactions in a market dominated by a Polymarket–Kalshi duopoly—to test that shift directly.

$10 Trades Are Defining the Market

Across four dimensions, who participates, how they behave, how capital moves, and at what scale, the volume growth pattern tells a consistent story.

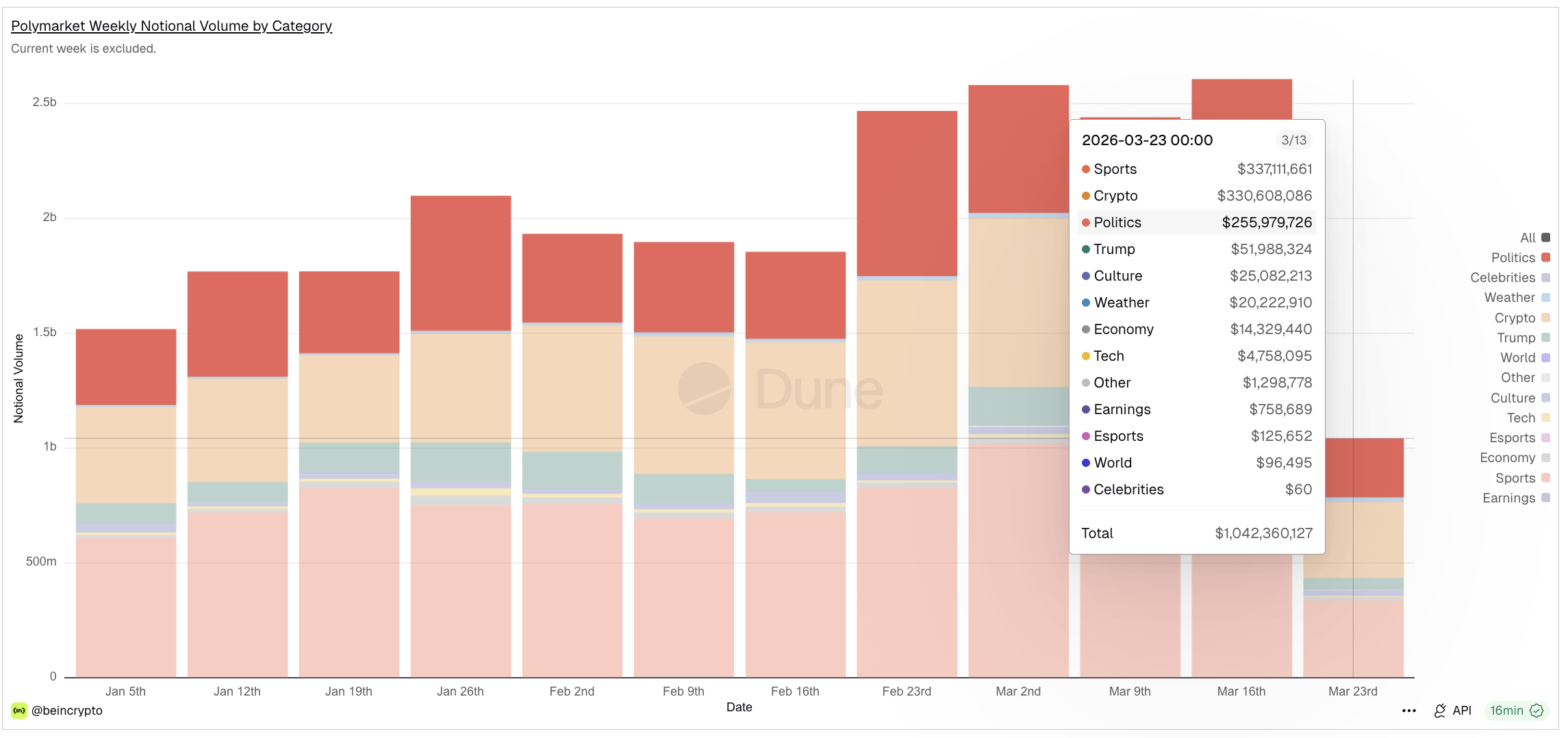

And the category mix reinforces the framing: crypto and politics (excluding sports) now lead weekly volume on Polymarket, with the economy and earnings categories growing alongside them. These are not traditional gambling categories. They are finance-adjacent verticals.

Notably, sports event contracts are already being offered as CFTC-regulated financial products by Kalshi and distributed through Robinhood’s Predictions Hub, placing them alongside stocks, options, and crypto within the same brokerage interface.

The most revealing signal is not how much money flows through prediction markets. It is who is placing the trades.

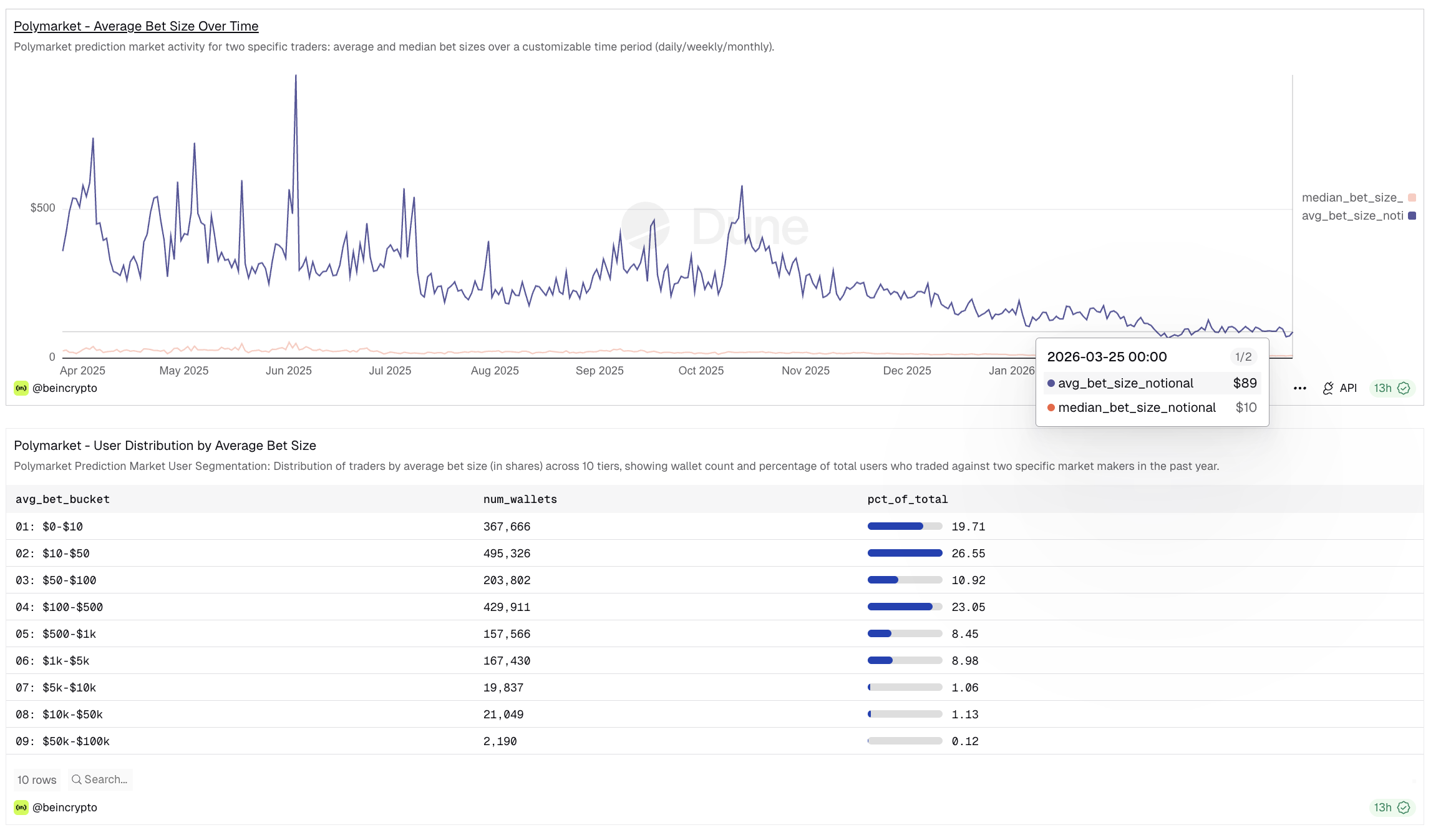

On Polymarket, the median bet size is $10, according to BeInCrypto’s exclusive dashboard. The average sits at $89, but that figure is pulled upward by a thin tail of large participants.

The underlying distribution paints a clearer picture: roughly 20% of all wallets trade in the $0 to $10 range, another 27% fall between $10 and $50, and about 11% sit in the $50 to $100 bracket.

In total, over 57% of users trade for less than $100, and more than 80% trade for less than $500.

This is not a market shaped by whales. It is a market built on small, individual participants deploying modest amounts. The pattern mirrors what defined the rise of retail stock trading.

Robinhood, for comparison, reported a median account size of $240, with the average around $5,000, according to CEO Vlad Tenev in 2021. The structural similarity is hard to miss: prediction markets are attracting the same class of small participants that reshaped equities over the past five years.

Users are Acting Like Traders, Not Bettors

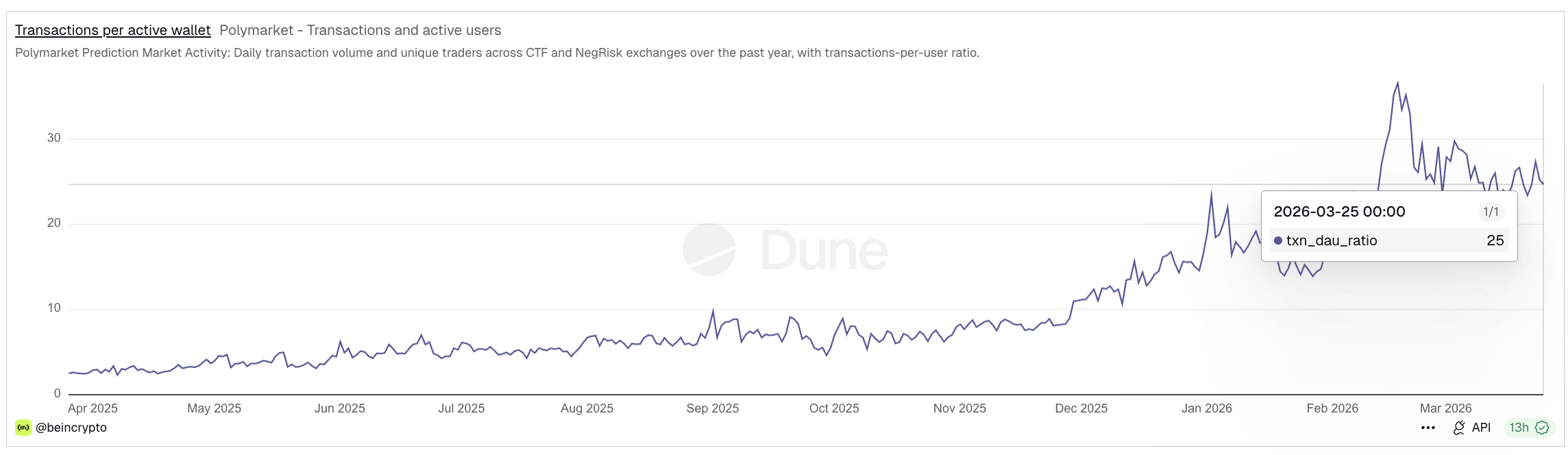

Participation alone does not distinguish a financial platform from a betting one. Frequency of interaction does.

A bettor places a wager and waits. A trader enters positions, adjusts exposure, exits, and re-enters. The transactions-per-active-user ratio captures this distinction directly.

On Polymarket, this ratio currently stands at approximately 25 transactions per daily active user, meaning the average active participant executes 25 trades per day. Earlier this year, the figure peaked near 37.

For context, through most of mid-2025, the ratio hovered between 3 and 5. The structural jump beginning in late 2025 represents a clear behavioral shift: users are no longer placing single predictions and walking away. They are actively managing positions across multiple markets.

This pattern has a direct parallel in crypto markets. A Kaiko research report on Binance found that the exchange processed 61.9 million trades against $20 billion in spot volume on a single snapshot day in December 2025, implying small average trade sizes and frequent execution across its 300 million registered accounts.

High-frequency, small-size trading is the behavioral signature of retail finance, whether the underlying asset is a stock, a token, or a prediction contract.

Capital Is Constantly in Motion

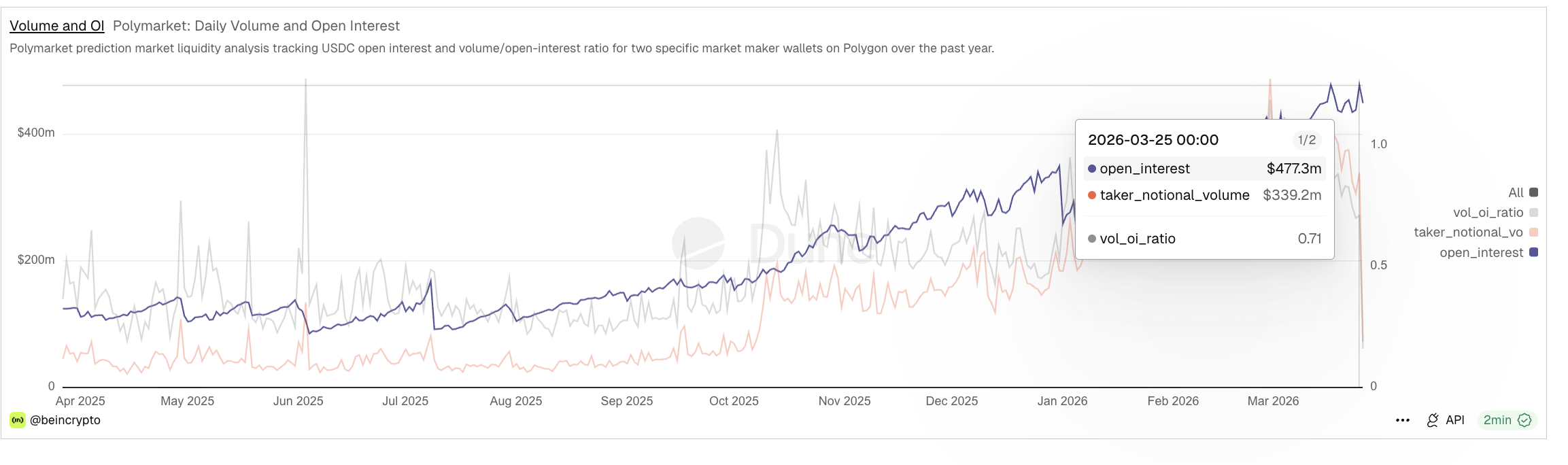

If users behave like traders, the capital dynamics should confirm it. They do. Polymarket currently holds approximately $445 million in total value locked, while open interest stands at roughly $477 million.

The near-parity between these two figures carries a specific implication: virtually all deposited capital is actively deployed in live positions rather than sitting idle. This is not passive liquidity. It is working capital.

The volume-to-open-interest ratio reinforces the point. With daily taker volume around $339 million and open interest at $477 million, the ratio is 0.71. Capital is not just deployed. It is rotating.

Positions are being opened, closed, and re-entered at a pace that suggests continuous portfolio management rather than static, event-dependent exposure. A low vol-OI ratio would have suggested more betting-like activity.

In a traditional betting market, capital tends to lock in and wait for resolution. Here, it circulates. That distinction is material: it signals a system in which participants treat capital as a tool for ongoing risk adjustment, not a one-time stake in a single outcome.

This Is No Longer Event-Driven Growth

The behavioral and capital patterns described above would be noteworthy even at modest volumes. But they are not operating at modest volumes.

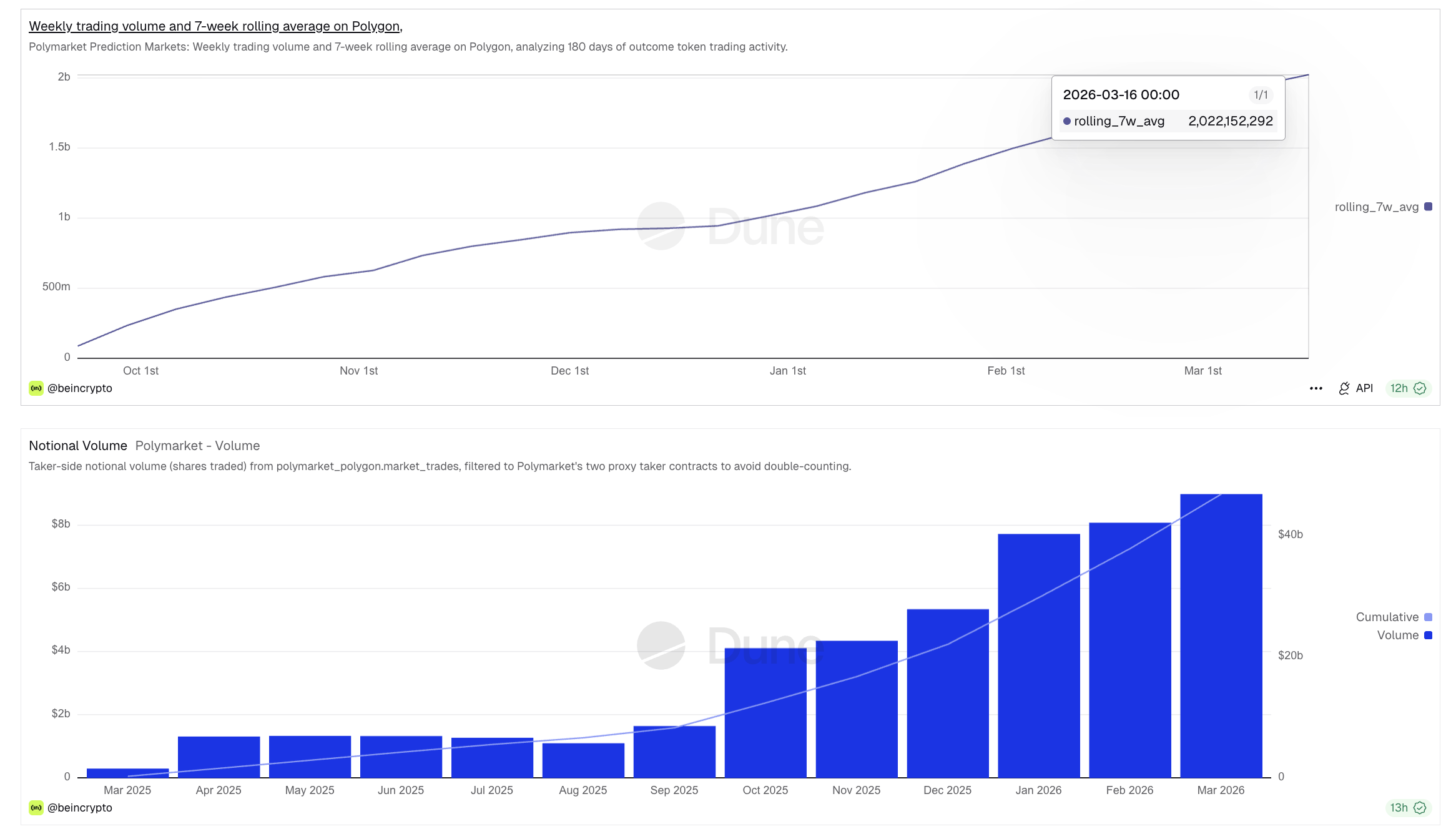

Polymarket’s weekly notional volume has consistently exceeded $1 billion through Q1 2026, with recent weeks surpassing $2.5 billion. The 7-week rolling average has crossed $2 billion.

Monthly volumes have climbed from around $1 billion in mid-2025 to over $8 billion by March 2026. The growth trajectory is not driven by any single event cycle.

Volume is diversifying across categories: sports, crypto, and politics. Each contributed substantially in the most recent weekly data, with economy, weather, and culture adding further breadth.

This diversification is what separates structural growth from event-driven spikes. A presidential election creates a temporary surge.

Sustained, multi-category volume growth across sports, crypto, macro, and culture points to a user base that engages with prediction markets regularly, not just occasionally, as a typical retail habit.

What the Prediction Markets’ Data Says

Each dimension reinforces the next in a single causal chain. The majority of participants are small, retail-sized users. Those users trade frequently, not once, but dozens of times per session.

The capital they deploy is almost entirely active, rotating through positions rather than sitting idle. And this behavior is occurring at billions of dollars in monthly volume, across a broadening set of categories.

When small users dominate participation, execute frequent trades, and keep capital constantly in play at scale, the system begins to resemble a retail financial market rather than a betting platform.

Prediction markets are no longer just mechanisms for forecasting outcomes. They are changing into retail trading systems for real-world events, platforms where participants express views, manage risk, and deploy capital with a frequency and discipline that mirrors stock markets.

The post Prediction Markets Now Behave Like Stock Trading Platforms appeared first on BeInCrypto.

Kenny Smith nixes UNC job talk, calls for long-term commitment from next coach

Turns Out That Advertisers Not Wanting To Fund Neo-Nazi-Adjacent Content Isn’t An Antitrust Violation

Washington DC area airports face ground stops over odor at air traffic control tower

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Mine Bitcoin 5X Cheaper Without Rigs? How to Stake HNO Coin #bitcoinmining #Crypto #Altcoin #shorts

Business Studies Class 12: Financial Markets One Shot NCERT Revision | CBSE 2026

COCKROACHES in the Financial System! (Private Credit)

-

NewsBeat3 days ago

NewsBeat3 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

Crypto World6 days ago

Crypto World6 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

News Videos2 days ago

News Videos2 days agoParliament publishes latest register of MPs’ financial interests

-

Sports5 days ago

Sports5 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

Sports4 days ago

Sports4 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Business5 days ago

Business5 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Tech5 days ago

Tech5 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Tech5 days ago

Tech5 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

News Videos4 days ago

News Videos4 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

Tech6 days ago

Tech6 days agoToday’s NYT Connections Hints, Answers for March 22 #1015

-

Business1 day ago

Business1 day agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Business6 days ago

Business6 days agoWill Duke Basketball Win It All? Duke Basketball Enters Second Round as Third Favorite to Claim NCAA Title

-

Sports5 days ago

Sports5 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who hit 12 Derby-Oaks Doubles enters picks

-

NewsBeat5 days ago

NewsBeat5 days agoUpdate on Wisbech river crash as search for teenage boy enters fifth day

-

Entertainment4 days ago

Entertainment4 days agoCynthia Bailey Dishes on ‘RHOA’ Season 17, Discusses Kandi

-

Tech4 days ago

Tech4 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

NewsBeat2 days ago

NewsBeat2 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

NewsBeat7 days ago

NewsBeat7 days agoThe 3 airlines that have entered insolvency in 2026 so far

-

Tech6 days ago

Tech6 days agoSteamOS update adds support for Steam Machine and other non-Valve hardware

You must be logged in to post a comment Login