Crypto World

Hyperliquid draws FCA warning while ICE explores its model

Hyperliquid has been flagged by the UK Financial Conduct Authority, bringing regulatory scrutiny to one of the largest crypto perpetual futures venues.

Summary

- UK FCA warned that Hyperliquid and Hyper Foundation may be offering financial services without authorization.

- ICE CEO Jeffrey Sprecher said the NYSE parent is studying Hyperliquid’s perpetual futures model.

- Hyperliquid generated $255 million in revenue by May 20, while HYPE gained 101% year to date.

According to a notice published by the UK Financial Conduct Authority on May 21, Hyperliquid, Hyper Foundation, the protocol’s application, and related social media channels may be offering or promoting financial services and products in the United Kingdom without authorization.

The regulator stated that consumers should avoid dealing with the platform and warned that firms operating without approval may not provide the protections available through regulated financial services.

The FCA’s warning arrived as cryptocurrency perpetual futures, commonly known as perps, attract increasing attention from regulators, exchanges, and trading firms.

Unlike traditional futures contracts, perpetual futures have no expiration date and rely on recurring funding payments to keep prices aligned with spot markets.

At the same time, major operators of regulated exchanges have begun discussing whether similar products could gain a larger foothold in traditional financial markets.

Traditional exchanges are studying perpetual futures

Speaking at Piper Sandler’s Global Exchange & Fintech conference on June 4, CME Group Chief Executive Terry Duffy criticized the Commodity Futures Trading Commission’s decision to allow regulated crypto perpetual futures in the U.S.

Duffy argued that the highly leveraged products introduce risks that many market participants may underestimate. He said perpetual futures can allow traders to maintain positions indefinitely while using leverage that may reach 50 times the deposited capital.

According to Duffy, automatic liquidation mechanisms and funding-rate costs could expose retail investors to significant losses if they do not fully understand how the products function.

Describing the market as increasingly driven by speculation, Duffy questioned whether the new contracts serve the long-term interests of investors.

While CME’s chief executive voiced concerns, Intercontinental Exchange Chief Executive Jeffrey Sprecher took a different approach. During remarks made last week, Sprecher said the parent company of the New York Stock Exchange was studying Hyperliquid’s model and discussing with regulators why traditional venues could not offer comparable products.

Those comments emerged as regulated crypto perpetual futures began entering the U.S. market. On May 29, the CFTC approved the first regulated crypto perpetual futures products for U.S. participants, opening a market that had previously been dominated by offshore platforms.

U.S. firms move into a market long led by offshore venues

Following the regulatory approval, prediction market operator Kalshi launched Bitcoin perpetual futures and introduced Ethereum perpetual futures on June 4.

According to regulatory filings, another 11 cryptocurrency perpetual futures contracts, including products tied to Solana and Dogecoin, remain under review.

Elsewhere in the sector, Coinbase Financial Markets received regulatory guidance allowing eligible institutional clients in the United States to access perpetual futures and options listed on Deribit, the derivatives exchange acquired by Coinbase in 2025.

Kraken has also announced plans to offer regulated Bitcoin perpetual futures through Bitnomial Exchange, a regulated platform acquired by parent company Payward earlier this year.

Against that backdrop, Hyperliquid remains one of the largest decentralized venues for perpetual futures trading.

The platform’s scale has made it increasingly difficult for regulators and traditional exchanges to ignore. By May 20, Hyperliquid had generated $255 million in revenue for the year, according to reported figures, while the HYPE token had gained 101% over the same period.

Pi Network’s PI token fell to a new all-time low near $0.126 on June 5, 2026, capping a slide that has erased more than 30% of its value in a month and confirmed a bearish breakdown traders had been watching for weeks.

Summary

- Pi Network fell to a new all-time low near $0.126 after a month-long decline that erased more than 30% of its value.

- More than 163 million PI tokens are set to enter circulation in June, adding supply pressure as demand remains weak and market liquidity stays thin.

- New ecosystem initiatives, including a developer center and four games from CiDi Games, have yet to generate enough demand to offset the ongoing token unlocks.

At roughly $0.13, the token carries a market cap around $1.36 billion and sits near rank #58, a long way from the excitement that surrounded its Open Mainnet launch and exchange listings.

The immediate triggers are clear and specific. More than 163 million PI (PI) tokens are scheduled to unlock and enter circulation this month, averaging over 5 million per day, with the single largest release of nearly 16 million PI due on June 11. That fresh supply is landing into thin liquidity and a brutal market-wide selloff that has dragged Bitcoin below $62,000 and wiped out over $1.6 billion in leveraged positions.

The question every PI holder is now asking is whether the unlocks push the token below $0.10. This piece breaks down why Pi hit a new low, the supply problem at the heart of it, the one bright spot, and what would have to change.

How Pi got here

The path to a new all-time low was not sudden. It was a steady erosion that accelerated into a breakdown.

Pi Network surged to around $0.296 in March 2026, riding enthusiasm around its exchange listings and the broader attention its unusually large user base attracted. That was the peak. From there the token entered a persistent downtrend, retreating through the spring as the initial excitement faded and selling pressure built. By late May it was trading near $0.15, already its lowest level since February, and below all its major moving averages, a sign that bears had taken firm control of the trend.

The technical structure then broke. For weeks, Pi had been trading inside a falling wedge pattern on the daily chart, with buyers repeatedly failing to reclaim resistance in the $0.18 to $0.20 region. When they failed one final time, sellers forced a decisive breakdown below the lower boundary of the wedge and below the critical support band around $0.129 to $0.131. That breakdown is what pushed PI into price discovery on the downside, opening the door to the fresh record low near $0.126 reached on June 5.

The drop also has to be understood against the backdrop of the broader market. This was not a Pi-specific collapse happening in isolation. Bitcoin briefly fell to an intraday low near $61,550 on June 4, Ethereum dropped below $1,800, and the CoinGlass data showed more than $1.6 billion in leveraged positions liquidated across crypto. That kind of market-wide capitulation crushes appetite for speculative altcoins, and Pi, as one of the more speculative large-cap names, felt it acutely. But the market selloff is only the accelerant. The core problem is structural, and it is about supply.

The supply problem at the heart of it

The single most important factor in Pi’s decline is its token unlock schedule, and the math is unforgiving.

Pi Network has a token release schedule that steadily moves locked tokens into circulation, and June is a heavy month. Data from PiScan shows more than 163 million PI scheduled to enter circulation over the next 30 days, with daily unlocks averaging over 5 million tokens. The largest single-day release, nearly 16 million PI, is expected on June 11. Every one of those tokens is new supply hitting the market, and supply that arrives faster than demand grows pushes price down by simple arithmetic.

This is the deep structural challenge Pi faces, and it is not new, just intensifying. The token’s design front-loads a large amount of supply entering circulation over time, and for that not to crush the price, there has to be commensurate demand: new buyers, real usage, genuine utility pulling tokens out of circulation as fast as the schedule puts them in. Right now, that demand is not there. Liquidity is thin, the broader market is in retreat, and there is no flood of new buyers stepping in to absorb the unlocks. The result is a persistent imbalance where new supply consistently outweighs new demand, and the price grinds lower.

The timing makes it worse. The June unlocks, and especially the June 11 release, are landing precisely when market liquidity is at its weakest and risk appetite at its lowest. In a strong bull market, an ecosystem might absorb 163 million new tokens without much trouble, because demand is rising fast enough to soak them up. In a fearful, illiquid market, the same supply becomes a heavy weight. This is why analysts are openly discussing whether PI breaks below $0.10: it is not a wild bearish fantasy; it is a straightforward read of supply outrunning demand at the worst possible moment.

The one bright spot

It would be incomplete to describe Pi purely as a supply-driven collapse, because there is genuine development activity worth noting, even if it has not yet moved the price.

The most concrete recent positive is on the ecosystem side. CiDi Games launched a Developer Center alongside four new games, explicitly designed to attract builders and users into the Pi ecosystem. The pitch to developers is straightforward: plug into Pi’s large community, access built-in revenue streams, and integrate through a ready software development kit. The ambition, in CiDi’s framing, is to become the infrastructure for games inside Pi. The network also completed a mandatory protocol upgrade, with node operators required to move to the latest version to stay connected, a sign of ongoing technical maintenance.

Why does this matter? Because the only durable fix for Pi’s supply problem is real demand, and real demand comes from actual usage. If the ecosystem develops applications that people use, and those applications create genuine reasons to hold and spend PI, then the network starts generating the organic demand needed to absorb the unlocks. Gaming is a plausible vector for that, since games can drive frequent, real transactions rather than pure speculation. A developer center and new games are exactly the kind of foundational ecosystem-building that, if it succeeds, could eventually change the demand side of the equation.

The honest caveat is the size of the gap between this and what the price needs. Four new games and a developer center are early-stage ecosystem development. They are not, today, generating anywhere near the transaction volume or token demand required to offset 163 million in monthly unlocks. The bright spot is real, but it operates on a timeline of months and years, while the supply pressure is hitting right now. For the ecosystem activity to matter to the price, it has to scale dramatically, and that has not happened yet.

What would have to change

Pi’s near-term path and its longer-term prospects are different questions, and it helps to separate them.

In the near term, the price is caught between the unlock schedule and the broader market, and neither is in Pi’s favor right now. The immediate technical question is whether the $0.126 to $0.131 zone holds or breaks.

A decisive break below it, especially around the June 11 unlock, would put PI firmly in downside price discovery with $0.10 as the obvious psychological target. A broader market stabilization, by contrast, would relieve some of the pressure mechanically, since much of the recent drop came from the market-wide selloff rather than Pi alone.

So in the short run, watching Bitcoin and the overall risk environment tells you a lot about where PI goes, because a fearful market amplifies the unlock damage and a recovering one cushions it.

In the longer term, the question is entirely about whether demand can catch up to supply. This is the structural test Pi has to pass. The unlock schedule will keep putting tokens into circulation regardless of price. For the token to find a durable floor and eventually recover, the ecosystem has to generate enough genuine usage and demand to absorb that supply, ideally pulling tokens out of circulation through real economic activity faster than the schedule adds them.

The CiDi Games developer push is a step in that direction, but it needs to multiply many times over. Tier 1 exchange access, which has been a persistent topic for Pi, would also help by broadening the buyer base, though it is not a substitute for organic demand.

The community itself is split on what comes next, which is honest given the uncertainty. Some traders see the slump as a clear warning and a reason for caution, pointing to $0.10 as a real risk if selling continues. Others frame it as a buy-the-dip opportunity for long-term believers, urging patience and focus on whether the network can build real utility through the downturn. Even Pi’s supporters concede the move is a reality check.

The fairest summary is that Pi is a project with an unusually large user base and a genuine supply problem, and its future depends on whether it can convert that user base into the kind of real, on-chain demand that makes the relentless token unlocks survivable. Until that conversion happens at scale, the supply keeps coming, and the price keeps feeling it.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 5, 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

They were born from the same code and the same founder, and now they are competing for a slice of what could become the largest market in finance.

Summary

- XRP and Stellar share the same origin but now compete through very different institutional strategies.

- XRP leads in payments, ODL volume, regulatory clarity, and ETF access.

- Stellar owns the bigger tokenization headline after DTCC chose it for tokenized securities infrastructure.

- Both tokens still face the same value-capture problem: network adoption does not automatically create token demand.

XRP and Stellar both trace back to Jed McCaleb, who co-founded Ripple and then left to create Stellar in 2014. A decade later, the two networks are the leading crypto contenders to become the settlement infrastructure for tokenized real-world assets, a market that bulls size at up to $114 trillion as stocks, bonds, funds, and Treasuries move on-chain.

In 2026 each landed a defining win. XRP has the CLARITY Act advancing through the Senate, spot ETFs with $1.41 billion in cumulative inflows, and live cross-border payment volume that generates direct token demand today. Stellar secured the single biggest institutional endorsement any of these tokens has received: a deal with the DTCC, the backbone of US securities settlement, to bring tokenized stocks, ETFs, and Treasuries directly onto its network. So who wins?

The honest answer is that they are winning different races, and the question that actually matters for investors is which catalyst pays off first. This piece compares them head to head across payments, tokenization, regulation, and token value capture, and lays out how to think about the contest.

Same roots, different bets

The shared origin story matters because it explains why these two networks are so similar and yet have diverged so sharply in strategy.

Jed McCaleb co-founded Ripple and helped create the technology that became the XRP Ledger. In 2014 he left after disagreements over direction and founded Stellar, building a network with deep technical similarities: both are fast, cheap, energy-light payment ledgers with native tokens, both use a consensus model rather than mining, and both were designed from the start for moving value across borders rather than running complex smart contracts. If you squint, XRP and Stellar are siblings, which is exactly what they are.

The divergence is in who they decided to serve. Ripple aimed XRP and the XRP Ledger squarely at banks and large financial institutions, building enterprise infrastructure, pursuing regulatory clarity through litigation and legislation, and selling directly to the commercial cross-border payments market. Stellar, through the nonprofit Stellar Development Foundation, leaned toward financial inclusion, emerging-market access, and partnerships with issuers and institutions willing to build on open infrastructure, with a stronger emphasis on stablecoins and asset issuance than on being the bridge currency itself.

Those different bets set up the 2026 contest. XRP went deep on commercial payments and US regulatory legitimacy. Stellar went deep on becoming a neutral issuance platform that established financial institutions could use to put real-world assets on-chain. Both strategies are now paying off, but in different arenas, which is why declaring a single winner misunderstands the race.

The payments race: XRP is ahead

On the original battleground, cross-border payments, XRP is winning on the metrics that exist today.

Ripple’s On-Demand Liquidity network has real, growing volume. Cumulative Ripple Payments volume crossed $95 billion as of January 2026, the network spans more than 70 currency corridors, and it covers an estimated 80 percent of major global remittance routes. The heaviest volume runs through corridors like Japan, the Philippines, and Mexico, where legacy banking costs are high and demand for fast, cheap remittances is constant. Crucially for the token, ODL builds direct XRP demand into every transaction it touches, because the model uses XRP as the bridge asset converted on each side of a payment. ODL volume is projected to grow 30 to 50 percent in 2026.

Stellar competes in payments too, with a long history in remittances and a partnership with MoneyGram that put it on the map for cash-to-crypto access. But it has not matched XRP’s commercial depth in bank-facing cross-border settlement, and its token does not capture payment flows the way XRP’s ODL does, because Stellar’s model leans more on stablecoins moving across the network than on the native token serving as the universal bridge.

So in payments, the scoreboard favors XRP: more volume, more corridors, deeper bank relationships, and a token-demand mechanism wired directly into the payment flow. If the tokenization race never materialized and the contest were purely about moving money across borders, XRP would be the clear leader. But the tokenization race is materializing, and that is where Stellar landed the bigger blow.

The tokenization race: Stellar’s DTCC bombshell

In tokenized securities, the infrastructure for putting stocks, bonds, and funds on-chain, Stellar secured the endorsement that reframes the entire competition.

The DTCC, the Depository Trust and Clearing Corporation, is the unglamorous but enormously powerful backbone of US securities settlement, the entity through which a vast share of American stock and bond trades clear. Its plan to bring tokenized stocks, ETFs, and Treasuries directly onto Stellar is, by a wide margin, the most significant institutional validation any payment-focused token has received. This is not a fintech startup or a single bank running a pilot. It is the central plumbing of US capital markets choosing Stellar as a venue for tokenized assets. For a network competing to become RWA settlement infrastructure, there is no bigger reference customer.

Stellar’s broader RWA credentials reinforce it. Franklin Templeton’s tokenized money-market fund has operated on Stellar, giving it a track record with a major traditional asset manager, and over a billion dollars in real-world assets had been tokenized on the network heading into 2026. The DTCC deal sits on top of that foundation as the marquee endorsement.

The critical caveat is timing. DTCC’s production testing does not begin until July 2026, and broader availability is not targeted until 2027. So the token-demand implications are still months, possibly more than a year, away. A landmark announcement is not the same as live volume, and Stellar’s win is currently a promise of future activity rather than present flow. That timing gap is the single most important qualifier on the Stellar bull case, and it is why the race is not over despite the size of the endorsement.

The regulatory and ETF race: XRP’s structural edge

Beyond payments and tokenization, two more factors tilt the near-term contest, and both favor XRP.

The first is regulation. The CLARITY Act passed the Senate Banking Committee on May 14 and, if it becomes law, would permanently write XRP’s commodity classification into federal statute. This matters more than it might sound. The March 17 SEC-CFTC interpretive ruling already gave XRP commodity status, but an agency ruling can be reversed by the next administration, whereas a law cannot. Codified commodity status would remove the last major regulatory blocker for US banks adopting XRP-based ODL and for the broadest range of XRP ETF products. XRP has spent years and a landmark lawsuit earning regulatory clarity, and it is closer to locking it in permanently than any comparable token.

The second is ETF access. Spot XRP ETFs have already drawn $1.41 billion in cumulative inflows, giving institutions a regulated, familiar channel to gain XRP exposure. That infrastructure exists today and is accumulating capital, even if the flows have not moved the price dramatically. Stellar does not have a comparable ETF presence, so XRP holds a structural advantage in institutional accessibility through regulated wrappers.

Put the near-term factors together and XRP leads on three of four fronts: payments volume, regulatory clarity, and ETF access, with Stellar leading decisively on the tokenization endorsement. That scoreboard explains why XRP is the larger, more liquid, more institutionally embedded asset today. But it also sets up the deeper question that determines the long-run winner, and on that question both tokens share the same vulnerability.

The problem both share: value capture

Here is the twist that complicates any simple “who wins” verdict. Both XRP and Stellar face the same fundamental challenge, and it is the one that has kept both tokens’ prices subdued despite their adoption wins.

For XRP, the problem is that banks can use the XRP Ledger without necessarily buying the token. Tokenized assets and stablecoins can sit on and move across the ledger while the activity requires only a fraction of a cent of XRP for transaction fees, not meaningful token purchases. The ledger thrives while the token waits.

For Stellar, the problem is structurally identical and arguably worse in the tokenization context. When the DTCC or Franklin Templeton issues tokenized securities on Stellar, the operation does not require holding XLM beyond trivial transaction costs. The network gets the prestigious business and the settlement volume; the token captures very little of it directly. A tokenized Treasury settling on Stellar generates network activity, but it does not create the kind of XLM buy pressure that would move the price the way the endorsement’s size suggests it should.

This is the shared trap of payment-and-settlement tokens: the more successful they are as neutral infrastructure that institutions adopt without friction, the less those institutions need to touch the native token. XRP’s ODL bridge mechanism is actually the stronger of the two value-capture stories, because it does require buying XRP for each bridged payment, which is why XRP’s payments lead matters for the token specifically and not just for the ledger. Stellar’s tokenization win is larger in prestige but weaker in direct token demand, because tokenized-asset issuance on Stellar does not inherently require XLM. So the race has a paradox at its core: the win that is bigger for the network (Stellar’s DTCC deal) may be smaller for the token, while the win that is more modest in headline terms (XRP’s growing ODL volume) is more directly tied to token demand.

So who actually wins?

The cleanest way to answer is to separate the question into the parts that have different answers, because “who wins” depends entirely on what you are measuring and over what horizon.

On commercial cross-border payments right now, XRP wins. It has the volume, the corridors, the bank relationships, and a token-demand mechanism built into the payment flow. This is a present-tense lead backed by real numbers.

On tokenized securities infrastructure over the long run, Stellar has the stronger position after the DTCC endorsement, the single biggest institutional validation in the space. But this is a future-tense lead, with production testing starting in July 2026 and broad availability not until 2027, so it is a bet on a payoff that has not arrived.

On near-term catalysts and token accessibility, XRP wins, with the CLARITY Act advancing, codified commodity status within reach, and $1.41 billion already in ETFs. The factors most likely to move a token price in the next year favor XRP.

On the deepest question, which token actually captures the value its network creates, neither has solved it, and XRP’s ODL bridge gives it a modest structural edge because that specific mechanism requires buying the token.

The practical synthesis for an investor is that the more important question is not “which is better” but “which catalyst arrives first.” XRP’s catalysts, CLARITY passage, continued ETF accumulation, and ODL growth, are nearer-term and more directly tied to token demand. Stellar’s catalyst, the DTCC tokenization rollout, is larger in scale but further out and less directly tied to XLM demand. An investor who wants exposure to the tokenization thesis with a payoff that could land sooner and flow to the token leans XRP. An investor willing to wait years for what could be the bigger institutional prize, and who believes Stellar will eventually solve the value-capture gap, leans XLM. Both are betting on the same enormous market. They are just betting on different paths into it, on different timelines, with different odds that the token rather than just the network gets paid. That, not a single winner, is the real shape of the $114 trillion race.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 5, 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

Crypto World

Crypto Market Reset Wipes Out $500 Billion in Just 25 Days with Bitcoin Leading Mass Sell-Off

Key Insights

- More than $500 billion were wiped out from the cryptocurrency market over 25 days as the sell-off became even more intense on major cryptocurrencies.

- More than $400 billion worth of market value was wiped out by Bitcoin as it dropped towards $61,000.

- Meme coins and growth coins registered even higher sell-offs as risk-on sentiment waned

Trigger for the Massive Crypto Market Contraction

The Crypto Market Reset is becoming very strong after a loss of over $500 billion in the digital assets space within the span of just 25 days. Almost all segments of the crypto industry suffered massive declines during this period, where even Bitcoin, Ethereum, major altcoins, and meme tokens saw significant losses.

The market sentiment changed very fast, prompting investors to switch to a defensive mode due to rising volatility and lack of liquidity. From a market correction phase, it escalated into a widespread sell-off trend that caused one of the biggest market contractions in recent months.

Based on data mentioned in social updates, there was a decline of over $500 billion in the value of digital assets in just 25 days as money started moving away from risky assets. This is primarily due to the cautious stance taken by investors amidst uncertain macroeconomic conditions.

Bitcoin Represents the Largest Proportion of the Losses

Bitcoin was identified as the greatest driver of the market correction. According to media reports, losses incurred by the main cryptocurrency amounted to over $400 billion as its price declined back to the $61,000 mark.

Data from market heatmaps indicated that Bitcoin was one of the worst performers. Given that Bitcoin is the largest crypto by market cap, its downturn negatively affected the whole crypto space.

The fall in Bitcoin’s price made investors less confident, which resulted in lower interest in risky crypto projects. Market participants started prioritizing capital preservation amid growing uncertainty.

While historically being a strong and resilient currency, the latest market correction demonstrated Bitcoin’s vulnerability amid unfavorable market conditions.

Downtrend Continues for Ethereum and Leading Altcoins

There was also selling pressure in Ethereum, one of the largest digital assets. Ethereum declined by about 33.6%, indicating a continuation of the downtrend.

Other top-ranked altcoins also showed severe drops in value. Solana saw an average drop of more than 55%, whereas XRP and Avalanche saw considerable declines amid investors’ efforts to avoid risk in the crypto market.

Cardano became another leading cryptocurrency to see a severe loss in value during the period, with an approximate 71.5% decline. Chainlink saw another notable decline of around 43%.

From these numbers, one can see a market-wide tendency rather than developments specific to each blockchain ecosystem. In particular, market factors seem to be more important than individual project news.

Growth Tokens and Meme Coins Suffer from Greater Adjustments

This correction was much more pronounced for growth tokens and speculative coins. Cryptocurrencies that were earlier highly in demand faced some of the most pronounced corrections.

In particular, Sui lost nearly 75.7% of its value, becoming one of the worst-performing assets. The same happened with Aptos, Kaspa, Render, and other growth projects.

Meme coins were not spared by this market readjustment either. For instance, Dogecoin shed over 53% of its value, whereas Shiba Inu, Bonk, and Pepe saw substantial decreases as well. Typically in bull markets, meme coins are among the best performers; however, during bear periods, the corrections are much deeper.

Seeking Stability Despite Continuing Uncertainty

Although a select few assets proved somewhat immune to the decline, there was only a limited degree of positive results seen across the market as a whole. The general heatmap continued to indicate weakness across the board, reflecting the conservative nature of recent trading activity.

The resetting of the crypto market demonstrates just how volatile the space can be. Having witnessed over $500 billion wiped out in less than a month, attention will now be focused on the performance of Bitcoin and other major cryptocurrencies to see if stability is achieved. Liquidity and macroeconomic developments will continue to be the key determinants of crypto market performance in the coming weeks.

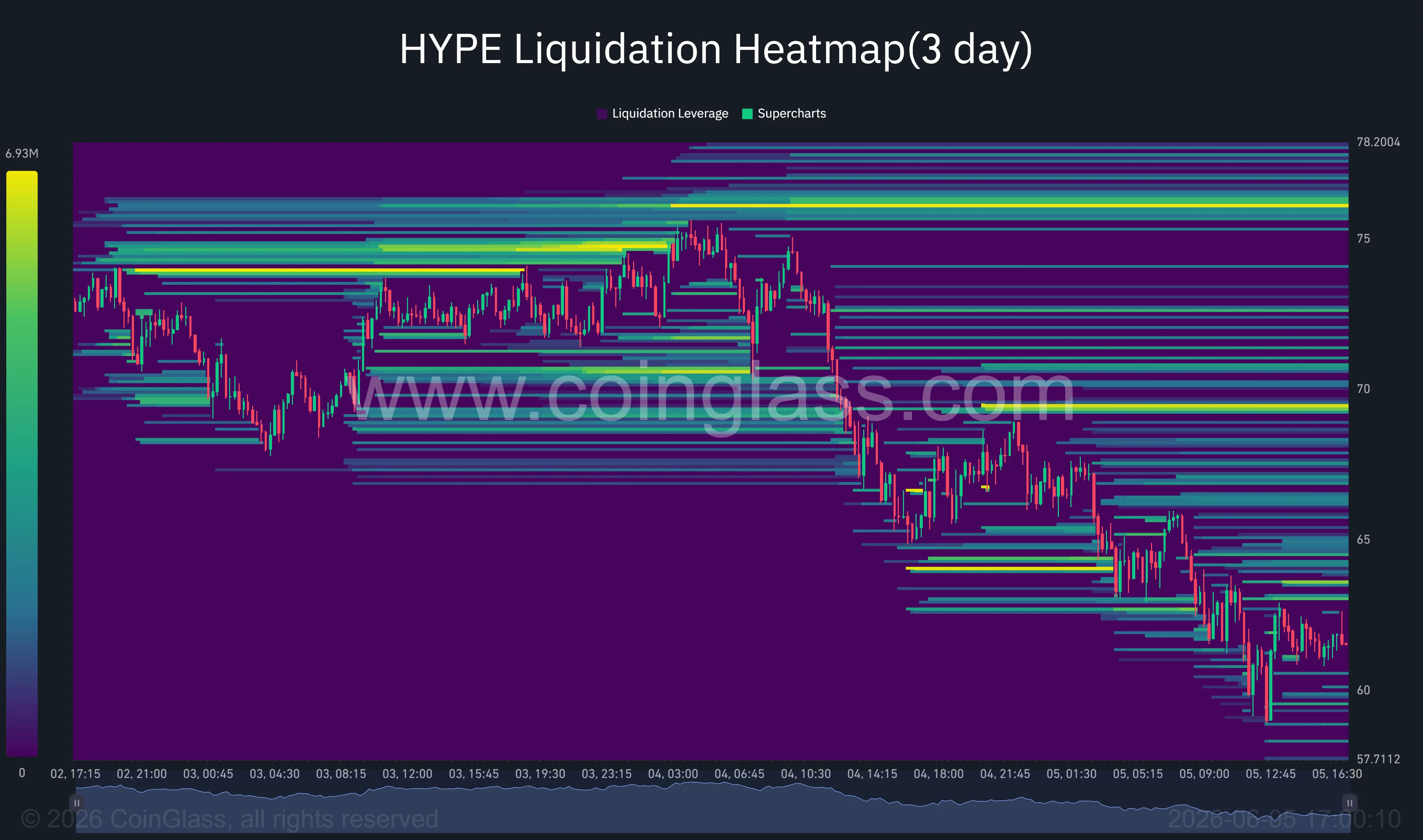

Hyperliquid has fallen sharply from its record high after a whale-led selloff triggered a wave of liquidations and pushed momentum indicators into their weakest position since the token’s breakout rally began.

Summary

- Hyperliquid fell from a record high of $75.48 to near $62 after Arthur Hayes sold his entire $18 million HYPE position, triggering a wave of profit-taking and liquidations.

- HYPE’s daily MACD has printed its first bearish crossover since May, while key support levels at $55 and $50 have come into focus if selling pressure continues.

- Despite the selloff, a16z-linked wallets accumulated more than $15 million worth of HYPE, lifting their 2026 holdings to roughly 6.9 million tokens.

According to data from crypto.news, Hyperliquid (HYPE) price was trading near $62 on Friday, June 5, after plunging from an all-time high of $75.48 just a day earlier. The token briefly touched the $58 area before buyers stepped in, though sentiment remains fragile following the abrupt exit of several prominent market participants.

The immediate bearish catalyst came from BitMEX co-founder Arthur Hayes, who liquidated his entire HYPE position worth roughly $18 million, as reported by crypto.news on June 4.

On-chain data tracked by Onchain Lens showed Hayes sold approximately 247,334 HYPE tokens. Other prominent traders, including Andrew Kang and Andreas Brekken, were also linked to sizable reductions in exposure. The concentrated selling overwhelmed spot demand and triggered a decline that wiped more than 17% off HYPE’s value within hours.

The selloff came only months after Hayes publicly projected a $150 price target for HYPE and placed a $100,000 charity wager on the token outperforming other large-cap cryptocurrencies.

Following the exit, Hayes pointed to a combination of macroeconomic headwinds, including rising oil prices driven by Middle East tensions, liquidity demand from several major AI-related IPOs, and the risk of a broader downturn in financial markets later this year.

Despite closing his position, Hayes maintained a bullish long-term outlook for HYPE. In a June X post, he wrote:

“Btw just because I dumped my entire $HYPE bag, doesn’t mean I still don’t have faith $HYPE will best $SOL by year end. Sometimes you gotta go down to go up.”

Additional pressure emerged from derivatives markets. Lookonchain reported that loracle.hl, a whale trader who previously lost $46.46 million shorting HYPE, had flipped long and was facing another unrealized loss of more than $840,000 during the latest selloff. The trade underscored how quickly leverage has been punished on both sides of the market as volatility intensified.

Technical structure places $55 and $50 in focus

The daily chart shows that HYPE has retreated into a key Fibonacci support region after failing to hold above the recent breakout zone. The token is currently trading between the 0.786 retracement level near $63.9 and the 0.618 level near $54.6, measured from the January low around $20.4 to the June peak near $75.7.

A breakdown below the 0.618 retracement could expose the midpoint support near $48.1, bringing the psychologically important $50 level into view. The area between $54 and $55 now represents the first major support cluster bulls need to defend.

Momentum indicators have also deteriorated. The daily MACD has produced its first bearish crossover since the rally accelerated in May, while the histogram has turned negative.

At the same time, the Relative Strength Index has dropped from overbought territory above 70 to roughly 54, showing that buyers have lost control of short-term momentum.

CoinGlass liquidation heatmaps identify another critical zone. Dense concentrations of leveraged positions remain stacked between $60 and $64, while larger liquidity pools sit around $58 and below. A decisive move through those levels could trigger another round of forced selling and increase downside volatility.

Institutional accumulation continues beneath the selloff

Not all capital has been leaving the ecosystem. As reported by crypto.news earlier, wallets linked to venture capital firm Andreessen Horowitz accumulated an additional 224,100 HYPE tokens worth more than $15 million during the selloff.

The latest purchase increased a16z-linked holdings to roughly 6.90 million HYPE acquired in 2026, representing an estimated position worth more than $322 million. The buying activity contrasts sharply with the profit-taking seen from traders and whales near the highs.

Fundamentals also remain supportive for the token. Hyperliquid continues generating some of the highest revenues in crypto, while approximately 99% of protocol fees are directed toward programmatic HYPE buybacks.

The decentralized exchange has steadily increased its share of perpetual futures trading volume, giving the token a revenue stream that few competitors can match.

However, several risks could still challenge the bullish case. Further weakness in Bitcoin (BTC), escalating geopolitical tensions, additional whale distributions, or a sustained break below the $55 support area could accelerate losses toward $50.

For now, traders appear focused on whether HYPE can reclaim the $64 region and invalidate the bearish MACD crossover before sellers target the next major support zone.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

While the crypto world fixates on price charts and the broader market bleeds, the most consequential fight for crypto’s future is happening in Senate offices and on conference stages, and it pits two of the most powerful men in finance against each other.

Summary

- Garlinghouse and Dimon represent the wider battle between crypto firms and traditional banks.

- The CLARITY Act fight centers on whether stablecoins can offer yield-like rewards.

- Banks fear yield-bearing stablecoins could drain deposits and weaken their funding base.

- A compromise could let crypto claim regulatory clarity while banks keep stablecoin yield restricted.

On one side is Brad Garlinghouse, the CEO of Ripple, who has spent years and a landmark SEC lawsuit pushing for US crypto legislation and who put the odds of the CLARITY Act passing at 80 percent. On the other is Jamie Dimon, the CEO of JPMorgan, America’s largest bank, who has said flatly that he is not satisfied with the bill as written and warned that banks “will not accept it that way.”

The CLARITY Act is the crypto industry’s most important legislative priority, the bill that would finally define the legal status of digital assets in the US. Whether it passes, and what it looks like if it does, comes down in large part to a power struggle between the crypto industry that wants it and the banking industry that fears what it would unleash. This piece lays out who these two men are, what they are actually fighting over, why the fight matters far beyond their companies, and how it is likely to resolve.

The two men and what they represent

To understand the fight, you have to understand that Garlinghouse and Dimon are not just two executives with different opinions. Each represents an entire industry’s interests, and their clash is a proxy for the larger war between crypto and traditional banking.

Brad Garlinghouse has been the public face of crypto’s fight for US regulatory legitimacy. As CEO of Ripple, he led the company through a multi-year SEC lawsuit over whether XRP was an unregistered security, a case that became a rallying point for the entire industry. Ripple’s partial victory established important precedent, and Garlinghouse emerged as one of the most prominent advocates for clear federal crypto rules. He has been openly bullish on the CLARITY Act, at one point putting the odds of passage by a spring deadline at 80 percent, and Ripple has built an end-to-end institutional infrastructure betting that regulatory clarity will bring banks on-chain. Garlinghouse represents the crypto industry’s core argument: give us clear rules, and we will build the future of finance inside the US rather than offshore.

Jamie Dimon represents the incumbent. As CEO of JPMorgan Chase for nearly two decades, he runs the largest bank in the United States and is arguably the most influential voice in traditional finance. Dimon has a long and complicated history with crypto, having once called Bitcoin a fraud before his bank built blockchain infrastructure and began offering crypto services. But on the CLARITY Act, his position is sharp and clear: he is not satisfied with the current text, he has criticized specific provisions, and he has warned that the banking industry will not accept the bill as written. When Dimon speaks on financial regulation, senators listen, because the banking lobby is one of the most powerful forces in Washington and JPMorgan sits at its center.

So this is not a personality spat. It is the crypto industry’s chief evangelist versus the banking industry’s most powerful figure, fighting over a bill that would redraw the boundary between their two worlds. The specifics of what they are fighting over reveal exactly what is at stake.

What they’re actually fighting over

The core of the dispute is not the whole bill. It is one provision: whether stablecoins can pay yield. That single question is where the crypto and banking interests collide most directly, and it is the issue Dimon keeps returning to.

A stablecoin that pays yield, effectively interest on the balance you hold, is a powerful product. For crypto firms, it would be a way to attract enormous deposits by offering returns that compete with or beat traditional savings accounts. For banks, that is precisely the nightmare. Banks fund their entire business on deposits, the cheap money customers park with them, which they lend out at higher rates. If yield-bearing stablecoins can pull those deposits out of the banking system and into crypto-issued dollar tokens, banks lose their cheapest funding source. Dimon’s objection is, at its heart, a defense of the bank deposit base against a new competitor.

The CLARITY Act’s drafters tried to thread this needle with a compromise. The text that emerged would prohibit stablecoin yield that is the “functional or economic equivalent” of what banks offer on deposits, while allowing “bona fide” transactions and certain activity-based rewards. In other words, crypto firms could keep some reward programs but could not simply pay interest on balances the way a bank does. This compromise, negotiated with White House involvement and shepherded by Senators Thom Tillis and Angela Alsobrooks, was meant to give each side something.

It satisfied no one fully, which is why the fight continues. Dimon criticized the framework anyway, taking aim at Coinbase CEO Brian Armstrong in the process, and argued the draft could fail because it lets crypto firms offer interest-like products without being regulated like banks, while doing too little on anti-money-laundering rules and consumer protections. From the banking side, members of the American Bankers Association reportedly flooded Senate offices with more than 8,000 letters arguing the compromise was too friendly to crypto. From the crypto side, the worry is the opposite: that the restrictions go too far and neuter one of the most promising stablecoin products. Garlinghouse, by contrast, has taken a pragmatic line, suggesting Ripple is positioned to thrive regardless of exactly how the yield question resolves because the company is so far ahead on infrastructure. That posture, confident and adaptable, contrasts sharply with Dimon’s defensive opposition, and it captures the difference between a challenger who wants the game to start and an incumbent who fears the new rules.

Why this fight matters beyond the two companies

It would be easy to dismiss this as a clash between one crypto company and one bank. That would badly understate what is riding on it, because the outcome shapes the regulatory environment for the entire digital-asset industry and, by extension, the price trajectory of major tokens.

The CLARITY Act is widely viewed as crypto’s single most important legislative priority. It would establish the first comprehensive federal framework for digital assets, finally resolving whether tokens fall under the SEC or the CFTC and replacing years of regulation-by-enforcement with clear rules for issuers, exchanges, and investors. For XRP specifically, passage would write its commodity classification permanently into law, green-lighting US banks to adopt XRP-based settlement and opening the door to a fuller range of ETF products. For the broader industry, regulatory certainty is the thing that institutional capital has been waiting for, the unlock that could bring sidelined money into the market and keep crypto businesses operating in the US rather than fleeing to friendlier jurisdictions.

That is why the Garlinghouse-Dimon fight is so consequential. The stablecoin-yield provision is not a side issue that can be quietly resolved; it is the sticking point that could sink the entire bill or delay it past the point of passage. If Dimon and the banking lobby succeed in either blocking the bill or forcing yield restrictions so tight that the compromise collapses, crypto loses its most important legislative win in a year when the market is already weak. If Garlinghouse and the crypto industry prevail and the bill passes in a form they can live with, it could be the catalyst that reframes the second half of 2026. The fight between two CEOs is, in effect, a fight over whether the entire industry gets its regulatory foundation this cycle.

There is also a deeper irony worth naming. JPMorgan’s own analysts have warned that the CLARITY Act is running out of time before the midterm elections, even as JPMorgan’s own CEO is part of why it is stalling. The bank is simultaneously diagnosing the bill’s poor odds and contributing to them. That tension captures how traditional finance approaches crypto in 2026: building crypto infrastructure and offering crypto services with one hand while lobbying to constrain the rules with the other. Dimon is not anti-crypto in the way he once was. He is pro-bank, and where crypto threatens banks, he fights it.

The twist: the banks might win even if the bill passes

Here is the part that makes the fight more subtle than a simple win-or-lose contest, and it is the detail most coverage misses. Even if the CLARITY Act passes and crypto claims victory, the banking industry may get the substantive outcome it actually wants.

The reason lies in what happens to capital if passive stablecoin yield is restricted, as the current draft intends. JPMorgan’s own analysts have pointed out that effective restrictions on passive stablecoin yield would push idle crypto cash toward alternatives: tokenized Treasuries, digital money-market funds, and tokenized deposits. Those are products that flow back toward regulated, bank-friendly, Treasury-backed instruments rather than into yield-bearing stablecoins issued by crypto-native firms. In other words, the yield restriction that Dimon is fighting for does not just protect bank deposits; it channels crypto capital into the kinds of products banks and traditional asset managers control.

So the real outcome of the fight may not be a clean crypto win or a clean banking win. It may be a bill that passes with the crypto industry celebrating the regulatory clarity it has wanted for years, while the banking industry quietly secures the provision that matters most to it, the one that keeps yield-bearing stablecoins from becoming a deposit-draining competitor. Garlinghouse gets his framework. Dimon gets his protection. The headline reads as a crypto victory, and the fine print reads as a banking victory, and both can plausibly claim they won.

This is why the fight is worth watching even though almost no one is watching it. The price charts that dominate attention are downstream of exactly this kind of regulatory detail. Whether stablecoins can pay yield determines where billions of dollars of crypto capital flows, which products win, and which industry captures the next phase of on-chain finance. Two CEOs are fighting over a single provision, and the resolution of that fight will shape the structure of the digital-asset economy for years, regardless of what Bitcoin does next week.

How it likely resolves

Pulling the threads together, the most probable path is messier than either side would prefer, and it runs through the same calendar pressure squeezing everything else in crypto policy.

The bill cleared the Senate Banking Committee but still needs 60 votes in the full Senate, reconciliation with the House version, and a presidential signature, all before a midterm-election calendar that effectively empties Washington in August and turns attention to campaigns thereafter. That leaves a narrow window, and the stablecoin-yield fight between the Garlinghouse and Dimon camps is the most likely thing to consume the time the bill does not have. The crypto investment firm Galaxy has put the odds of passage this year at roughly 50-50 or lower, with the uncertainty coming not from any single issue but from the number of unresolved questions that must be settled in sequence under severe time pressure.

The realistic outcomes are three. The bill passes this summer in a form built on the existing yield compromise, handing crypto its regulatory framework while preserving the restrictions banks want, the “both sides claim victory” scenario. The bill slips past the August recess and dies for the year, a loss for Garlinghouse and the crypto industry and a quiet win for Dimon and the banks who benefit from continued delay. Or it limps into a post-election lame-duck session with diminished odds. Each path runs directly through the yield fight, which is why this single provision, and the two men championing the opposing sides of it, holds outsized power over the whole effort.

For anyone trying to track crypto’s regulatory future, the signal to watch is not the daily token price but the movement on stablecoin yield. If Garlinghouse’s pragmatic confidence proves justified and the compromise holds, expect a bill and a potential market catalyst. If Dimon’s opposition hardens and the banking lobby keeps the pressure on, expect delay and disappointment. The fight nobody is watching is the one that determines whether crypto gets the foundation it has been building toward, and the two men at its center are fighting not just for their companies but for which industry writes the rules of on-chain finance. That is a fight worth watching, even when the charts are screaming for attention.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 5, 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

Crypto World

Polymarket allegedly paid influencers at least $350,000 for undisclosed promotions: report

Polymarket has paid at least $350,000 to social media influencers over a 14-month period, with many of those creators later promoting the prediction market platform on X without clearly disclosing a paid relationship, according to a POLITICO investigation based on PayPal transaction records.

Summary

- POLITICO reported that Polymarket’s chief marketing officer sent at least $350,000 to influencers, many of whom later promoted the platform on X without clear paid partnership disclosures.

- More than 490 Polymarket-related posts were identified across paid creators during a 14-month period, according to POLITICO’s review of payment records and social media activity.

- The report arrives as Polymarket faces growing scrutiny in multiple jurisdictions, including a user investigation in South Korea and ongoing regulatory attention in the United States.

According to POLITICO, the payments were sent by Polymarket chief marketing officer Matthew Modabber through a personal PayPal account between January 2025 and February 2026.

The publication reported that Modabber transferred more than $2.5 million to over 800 people during that period, while records reviewed by reporters identified at least 20 influencers who later posted about Polymarket hundreds of times on social media.

Among those who reportedly received payments were conservative influencer Alex LoRusso, political commentator Brian Krassenstein, former collegiate swimmer and Fox News contributor Riley Gaines, and several other online personalities with large followings across the political spectrum.

A Polymarket spokesperson told POLITICO that working with content creators forms part of the company’s normal business practices and said the platform regularly collaborates with independent organizations, partners, and creators to support its mission of providing market-based insights.

The spokesperson declined to discuss the company’s disclosure policies, the use of Modabber’s personal PayPal account, or whether the payments were reported as business expenses.

Influencer campaign grows alongside Polymarket’s expansion

Records reviewed by POLITICO showed that at least 20 creators who received money from Modabber posted about Polymarket on X after the payments began. The publication counted more than 490 posts mentioning the platform during the review period and reported that none included disclosures identifying them as paid promotions.

Federal Trade Commission guidance requires influencers to disclose material connections when endorsing products or services. Speaking to POLITICO, former FTC deputy general counsel Robin Moore said the activity described in the report appeared to be the type of arrangement that generally should be disclosed.

Several creators promoted major Polymarket developments after receiving payments, according to the report. Following the launch of a Department of Government Efficiency dashboard in February 2025, influencer Eric Daugherty described the release as a breaking development to his audience. Riley Gaines and media personality Elijah Schaffer also shared posts praising the feature, POLITICO reported.

Later in June, after Polymarket announced a partnership with Elon Musk’s artificial intelligence company xAI, multiple paid influencers published supportive posts within hours of each other, according to POLITICO’s review of social media activity.

One influencer who spoke anonymously to the publication said Polymarket occasionally supplied suggested posts and directed creators toward specific markets or announcements that it wanted promoted.

Meanwhile, Shane Ginsberg, founder of the social media marketing company Street Poller, reportedly received at least $77,000 from Modabber. POLITICO reported that Ginsberg’s network of creators produced man-on-the-street videos promoting Polymarket during the run-up to the 2024 U.S. presidential election, with some creators displaying Polymarket branding even when the platform itself was not directly mentioned.

Regulatory scrutiny continues to build

The marketing campaign has emerged as Polymarket faces increasing legal and regulatory attention in several jurisdictions.

Separately, South Korean authorities have recently opened what Chosun Biz described as the country’s first known investigation into domestic Polymarket users. The Gangwon Provincial Police Agency is examining whether participation on the platform violated South Korea’s gambling laws, with investigators reportedly considering whether user activity falls under provisions of the Criminal Act governing gambling offenses.

Regulators and prosecutors in South Korea have recently shown a willingness to apply existing laws to blockchain-based activities. As previously reported, prosecutors charged several individuals linked to the CATFI meme coin rug pull in a case described by Digital Asset as the country’s first prosecution involving a decentralized exchange under the Virtual Asset User Protection Act.

Pressure has also increased in the United States. In May, the U.S. Department of Justice charged Google software engineer Michele Spagnuolo with commodities fraud, wire fraud, and money laundering after alleging he used confidential company information to profit from prediction market contracts on Polymarket tied to Google’s annual search rankings. Prosecutors said the activity generated roughly $1.2 million in profit.

At the same time, the Commodity Futures Trading Commission filed a parallel civil complaint and reiterated that insider trading laws apply to prediction markets. Enforcement Director David Miller said the agency remains focused on preventing the misuse of nonpublic information in markets under its jurisdiction.

Questions around Polymarket’s market operations have also drawn criticism from traders. Last week, a disputed market asking whether Strategy would sell Bitcoin before May 31 concluded with a “No” outcome after a final UMA review, despite a regulatory filing showing that Strategy had sold 32 Bitcoin during the final week of May.

The resolution sparked complaints from several traders and prompted renewed debate over how prediction markets should handle disputed outcomes and post-trade rule clarifications.

Market rout and leverage unwind

Cryptocurrency markets registered a sharp drawdown this week as bitcoin fell from near $74,000 to an intraday low around $61,556, a roughly 17% decline over four trading days. The move coincided with more than $4.4 billion in liquidations across derivatives markets, with long positions bearing the bulk of the losses.

Ether slid below $2,000 during the same period, and trading dynamics on major exchanges signaled a pullback in institutional participation: the Coinbase premium — the price gap between Coinbase and Binance — has been negative and widening, an indicator market participants often read as weaker U.S. institutional bid.

Traders and analysts pointed to a combination of macro and market‑micro factors. Heightened geopolitical tensions involving the U.S. and Iran appeared to sap risk appetite, while speculative capital rotated toward AI equities that were perceived to offer clearer near‑term earnings. On-chain metrics also showed that many recent buyers were underwater, intensifying forced selling in a leveraged market.

Gnosis Pay exploit underscores middleware risk

On June 1, users of Gnosis Pay — a service that links noncustodial Safe wallets to Visa‑branded payment cards — experienced an exploit traced to a vulnerability in the Zodiac Delay Module, a third‑party component used in Safe’s modular stack. Gnosis co‑founder Martin Koppelmann publicly urged affected users to withdraw certain assets, and the Gnosis team subsequently said it would cover user losses related to the incident.

The event follows a similar pattern seen in other recent incidents, where core wallet frameworks remain intact but ancillary modules introduce attack surfaces. A week earlier, a separate incident involving a third‑party Safe module known as the Squid exploit drained about $3.2 million from dozens of Safe wallets. Together, these failures highlight the security tradeoffs introduced by composable middleware: integrating external modules accelerates feature development but multiplies dependency and review surfaces.

For products that bridge on‑chain wallets to off‑ramp rails like Visa, the incidents illustrate the technical and operational complexity of safely extending noncustodial keys into payments ecosystems. The events have already reignited debate among custodial and self‑custody proponents about which custody models best balance user convenience and systemic risk.

Zcash halt and verification key updates after minting vulnerability

Zcash experienced a separate disruption when security researcher Taylor Hornby disclosed a flaw in the Orchard shielded protocol circuit that, according to the researcher, could enable undetected minting of ZEC. The disclosure precipitated an emergency response from the Zcash team, including temporarily disabling Orchard, coordinating a soft fork, and deploying verification key updates via a hard fork within days.

Price action responded violently: ZEC lost more than 40% in a 24‑hour window as market confidence in supply integrity deteriorated. Observers have noted that Zcash’s Turnstile Accounting — the system for tracking shielded pool balances — may not readily reveal whether counterfeit coins were minted and migrated within normal outflow bounds. That uncertainty, rather than any single technical fix, is what markets appear to be pricing.

Notably, the researcher reported using contemporary AI tooling during analysis, a reflection of how machine‑assisted code review is lowering the marginal cost of uncovering complex cryptographic or protocol vulnerabilities. That capability increases both the speed at which bugs are found and the urgency of rapid, coordinated protocol responses.

Regulatory pressure: MiCA transitional deadline looms

Adding to market strains, the EU’s Markets in Crypto‑Assets (MiCA) transitional period expires on July 1, 2026. MiCA entered into force on December 30, 2024, and member states were given up to 18 months to transpose its provisions into national law. Some jurisdictions accelerated that timeline — for example, the Netherlands implemented a shortened window — but the July 1 date is the common regulatory boundary for operating without authorization across the bloc.

The practical implication for users and service providers is concrete: crypto‑asset service providers serving European customers without MiCA authorization risk being out of compliance and could be forced to restrict services or accounts. Industry participants have urged users to verify the regulatory status of their platforms and consider self‑custody options where appropriate.

Implications and what to watch

Three themes emerge from recent events. First, leverage and concentrated derivative positions amplify price moves — liquidations remain a primary driver of short‑term volatility. Second, the architecture of Web3 services matters: composability accelerates innovation but introduces operational dependencies that are progressively becoming the focal point for attackers. Third, regulatory transitions such as MiCA impose timeline‑driven operational risk for centralized platforms offering services to European users.

For market participants, the near term will be shaped by how exchanges, protocol teams, and third‑party module developers respond to these failures: faster disclosure, coordinated emergency upgrades, and improved security auditing can restore confidence, but they are not panaceas. Users concerned about counterparty or platform risk should review custody arrangements and confirm whether their providers have regulatory authorization if they operate in the EU.

Finally, the Zcash episode underscores a broader point: supply integrity is fundamental to token value. Even when teams patch vulnerabilities quickly, the reputational shock can trigger sustained repricing as participants reassess trust in protocol assumptions.

We will continue to monitor price action, on‑chain flows, and follow‑up technical disclosures related to these incidents.

Disclaimer: This article is for informational purposes and does not constitute investment or legal advice. Readers should verify technical claims and consult professionals before acting.

Morgan Stanley Wealth Management has expanded its crypto offering by enabling eligible clients to convert digital asset holdings into spot crypto exchange-traded products through a new referral arrangement with Galaxy Digital.

Summary

- Morgan Stanley clients can now lend Bitcoin, Ether, and Solana to Galaxy Digital in exchange for shares in spot crypto investment products.

- Galaxy has reduced the minimum lending transaction size for Morgan Stanley referred clients to $5 million from $25 million.

According to a Friday announcement, high-net-worth Morgan Stanley clients can lend cryptocurrencies including bitcoin, ether, and Solana to Galaxy Digital and receive shares in spot crypto investment products in return, including the recently launched Morgan Stanley Bitcoin Trust.

The companies said the process allows investors to move crypto exposure into regulated investment vehicles without selling their digital assets first. The announcement added that the structure could reduce in-kind crypto-to-ETP onboarding times by as much as 75%.

Explaining the rationale behind the arrangement, Alison Nest, Head of Investment Solutions Products at Morgan Stanley, said the bank has been active in decentralized finance and views the referral capability with Galaxy as a way to help wealth management clients integrate digital assets into their portfolios through an institutional framework.

Nest said the arrangement creates a connection between traditional finance and decentralized finance while giving investors additional ways to diversify their holdings.

Morgan Stanley deepens digital asset push

The latest initiative arrives as Morgan Stanley continues to add new crypto-related products and services across its wealth management and brokerage businesses.

Earlier this year, the bank launched the Morgan Stanley Bitcoin Trust, a spot Bitcoin exchange-traded fund that completed its first month without recording a day of net redemptions, according to previous company disclosures.

Recent regulatory filings have also shown the bank expanding beyond Bitcoin products. In May, Morgan Stanley disclosed holdings in the Volatility Shares XRP ETF and the Grayscale XRP ETF, adding XRP-linked investment products to a crypto portfolio that already included Bitcoin and Ethereum exposure.

At roughly the same time, the firm submitted an updated registration statement for the Morgan Stanley Solana Trust, a proposed spot Solana ETF that would hold SOL directly and stake part of its assets through third-party providers. According to the filing, staking rewards generated from those holdings would contribute to the fund’s overall returns.

Crypto access has also extended to Morgan Stanley’s brokerage business. Through a pilot program launched on E*Trade in May, the bank began offering Bitcoin, Ether, and Solana trading through infrastructure provided by Zerohash.

Morgan Stanley executives said at the time that the initiative formed part of a strategy to keep clients within the firm’s investment ecosystem.

Leadership changes have accompanied the expansion. Amy Oldenburg, a longtime Morgan Stanley executive, was appointed earlier this year to lead the firm’s first dedicated digital asset strategy role.

Galaxy expands institutional services

For Galaxy Digital, the partnership adds another institutional channel to its lending and asset management business.

According to company figures, Galaxy generated $505 million in adjusted gross profit during 2025 from its trading, lending, asset management, and staking services division.

Only days before announcing the Morgan Stanley referral arrangement, Galaxy also introduced an institutional over-the-counter prediction market trading desk, adding another service aimed at professional investors.

The U.S. House Ways and Means Committee has released seven crypto tax discussion drafts that would introduce new rules for decentralized finance lending, stablecoin payments, staking rewards, and other digital asset transactions ahead of a June 9 congressional hearing.

Summary

- House Ways and Means Committee has released seven crypto tax discussion drafts covering DeFi lending, stablecoins, staking, mining, and wash-sale rules.

- Proposed measures could introduce tax relief for certain stablecoin payments while extending anti-abuse and wash-sale rules to digital assets.

- The proposals will be discussed at a June 9 congressional hearing as lawmakers consider changes to U.S. crypto tax policy.

According to crypto journalist Eleanor Terrett, the discussion package breaks crypto tax policy into a series of standalone proposals covering areas such as stablecoins, mining, staking, DeFi lending, wash-sale rules, charitable donations, and a voluntary disclosure program for taxpayers with unresolved crypto reporting issues.

The proposals arrive as lawmakers increase their focus on how digital assets should be taxed in the United States. Several of the subjects included in the drafts were previously grouped together under greater legislative efforts, including the bipartisan Digital Asset Protection, Accountability, Regulation, Innovation, Taxation, and Yields Act, known as the PARITY Act, and separate legislation introduced by Senator Cynthia Lummis.

DeFi lending and stablecoin transactions move into focus

Among the most closely watched provisions are those affecting decentralized finance activity. Terrett said the discussion drafts address DeFi lending, an area that has faced years of uncertainty over how transactions should be treated under U.S. tax law.

The package also includes provisions related to stablecoin payments. Under one proposal, compliant stablecoins could qualify for a de minimis treatment on small gains and losses generated through everyday transactions.

The measure would allow certain low-value payments to receive different tax treatment from speculative crypto trades. At the same time, lawmakers continue to examine how stablecoins should be treated within the tax system.

As reported by crypto.news earlier, the bipartisan PARITY Act proposed a deemed-basis rule for regulated dollar-pegged payment stablecoins. According to Representative Steven Horsford’s office, the provision would treat digital dollars used as payment instruments more like cash for tax purposes while including safeguards against trading and arbitrage abuse.

Several anti-abuse measures also appear in the new discussion drafts. Terrett said the proposals would extend wash-sale and constructive-sale rules to crypto transactions, bringing digital assets closer to the framework already applied to traditional financial markets.

Mining and staking rules remain under review

Tax treatment of mining and staking rewards remains another major topic within the package. According to Terrett, the discussion drafts include provisions addressing both activities alongside charitable contributions and reporting requirements.

Related legislative efforts have already sought changes in this area. Under the PARITY Act introduced by Representatives Horsford, Max Miller, Suzan DelBene, and Mike Carey in May, taxpayers would be allowed to elect when staking and mining rewards become taxable. Horsford’s office said the proposal is designed to address the so-called phantom income issue faced by some participants.

Earlier coverage also noted that 18 bipartisan lawmakers urged the Internal Revenue Service to revisit its 2023 staking guidance before the 2026 tax year.

Attention now turns to the Ways and Means Committee hearing scheduled for June 9, where the discussion drafts are expected to play a central role. Terrett said the proposals will likely feature prominently during the proceedings as lawmakers evaluate potential changes to crypto taxation.

Outside the tax debate, Congress continues to consider other digital asset legislation. The CLARITY Act is advancing through the legislative process, while Representative Nick Begich recently introduced the American Reserves Modernization Act, a bill that would pursue budget-neutral methods of increasing U.S. Bitcoin reserve holdings rather than requiring the government to purchase up to 1 million BTC over five years.

Cardano is getting attention again, but not the kind holders usually want.

ADA fell to around $0.16 on Thursday, down nearly 30% over the past seven days and more than 75% over the past year, CoinDesk data show. The token briefly traded below $0.16, its lowest level since December 2020, extending a drawdown that has turned Cardano from one of crypto’s largest retail communities into one of the market’s clearest stress cases.

The latest selling followed comments from founder Charles Hoskinson, who said he was “taking a break” after warning that Cardano could face a “wave of failures” across its ecosystem. His remarks came after TapTools, a Cardano analytics platform, said it would shut down after four years, and after the community voted against funding Cardano’s 2026 Summit in Singapore.

The market reaction has now spread beyond price.

Santiment said ADA’s social dominance reached about 0.52%, a 2026 high, meaning more than one in every 190 crypto-related discussions across tracked social channels focused on Cardano.

Daily active addresses also climbed to 28,459, the highest level in four months, suggesting users are moving funds, checking positions or interacting with the network during the selloff.

Such a kind of activity can be read two ways.

The bullish version is that Cardano’s base has not disappeared. ADA still has one of crypto’s louder communities, and activity rising into a selloff can show holders are engaged rather than checked out.

However, another read is that attention is being pulled in by distress. Project shutdowns, funding fights and the founder stepping back are not the kind of catalysts that usually bring durable bids. Retail loyalty can keep a token relevant, but it cannot replace ecosystem growth, new capital or working applications.

That is the test now. ADA is cheap by old cycle standards, but cheap alone is not a catalyst. Cardano needs evidence that projects can survive, treasury funding can be deployed and users have reasons to do more than defend the chain online.

Pi Network just hit a new all-time low

Polo G’s Girlfriend Announces Pregnancy In Heartwarming Video

I Asked 4 AI Excel Tools to Build a Financial Model. Only One Passed

-

Business4 days ago

Business4 days agoJade Biosciences, Inc. (JBIO) Discusses Positive Interim Results From JADE101 Phase I Healthy Volunteer Study and Development Plans Transcript

-

Tech7 days ago

Tech7 days agoSpaceX just won a second Golden Dome contract. This one is $4.16 billion.

-

Sports3 days ago

Sports3 days agoFrench Open 2026 results: Alexander Zverev beats Rafael Jodar and will play Jakub Mensik in semi-finals

-

Business7 days ago

Business7 days agoIs the Spurs Phenom Already Better Than Prime Diesel?

-

Tech4 days ago

Tech4 days agoCryZENx Releases Fresh Playable Content Deep Inside Jabu-Jabu for His Ocarina of Time Remake

-

Fashion10 hours ago

Fashion10 hours agoWeekend Open Thread: Evereve – Corporette.com

-

Politics7 days ago

Politics7 days agoThe House | Inside Andy Burnham’s Makerfield Campaign: “Nobody Thinks This Is In The Bag”

-

Crypto World19 hours ago

LBank Surpasses 25 Million Users Worldwide as AFA Partnership Continues to Drive Global Growth

-

Business3 days ago

Business3 days agoTrump Taps Housing Chief Bill Pulte as Acting Intelligence Director After Gabbard Exit

-

Entertainment7 days ago

Entertainment7 days agoOne of the Greatest Sitcoms of All Time Shoots Up Apple TV’s Charts 11 Years Later

-

Business7 days ago

Business7 days agoDemand Conditions Improve In Chemicals Sector In April 2026

-

NewsBeat7 days ago

NewsBeat7 days agoEverything you need to know as Cambridge’s Strawberry Fair returns after cancelled year

-

Crypto World4 days ago

Crypto World4 days agoSeagate (STX) Stock Surges to Record High on AI Boom and Legal Settlement

-

NewsBeat3 days ago

NewsBeat3 days agoRepublicans balk at Trump’s attempt to appoint a MAGA enforcer to lead National Intelligence

-

Entertainment7 days ago

Entertainment7 days agoBritney Spears Shares Troubling Update After Hard Year

-

Crypto World3 days ago

Crypto World3 days agoEU AI Data Center Project Faces Delays as Funding Gaps Grow

-

Business3 days ago

Business3 days agoAehr Test Systems Stock Soars 17% Amid Surging AI Demand and Conference Spotlight

-

Tech7 days ago

Tech7 days agoIntel and 3DGS back a $3.3bn glass-substrate plant in India’s Odisha

-

Tech7 days ago

Tech7 days agoAcer’s Swift Air 14 is a peppy MacBook Neo rival with some cool upgrades and a $699 ask

-

Tech7 days ago

Tech7 days agoKnox County, TN Rolls Back ‘Roots’ Book Ban After Backlash

You must be logged in to post a comment Login