Crypto World

I’d rather go broke than contribute to KYC’s grip on society

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

Today’s traditional banking system has become too comfortable in encouraging society to overshare while underdelivering on security guarantees. Never has a financial system demanded such a sacrifice of an individual’s personal data. KYC requires legal identity, biometric data, address history, and device fingerprints, which are all bundled together and stored indefinitely by third parties.

Summary

- KYC turned privacy into collateral damage: Banks demand passports, biometrics, and device data — then store it in breach-prone databases that individuals can never truly reclaim.

- Finance has shifted from neutral infrastructure to permissioned gatekeeper: Access can be frozen, revoked, or denied — turning participation into a conditional privilege.

- Zero-knowledge tech offers a third path: Prove eligibility without surrendering identity, enabling transparency for systems and privacy for individuals.

Once that information leaves an individual’s control, it can be copied, breached, and sold to anyone. Even when companies act in good faith, the data itself becomes a liability. You cannot replace a passport the same way you can replace a lock. If we lose control of our fingerprint, address, and name, then who do we become if not a prisoner to an interdependent hive mind of capital structures that feed off the intelligence of the masses? For those who value privacy and autonomy, KYC isn’t a quality of life feature; it’s subconscious theft.

KYC: The irreversible surrender

KYC is often justified in the name of safety, but centralised safety is still a centralised risk. Large databases of sensitive information become magnets for attackers, insiders, and state actors alike. Recent incidents include Coinbase insiders exploiting customer data for extortion and Finastra, a software provider to 45 of the world’s largest 50 banks, losing 400gb of sensitive information in a data breach orchestrated by cyber criminals. History shows that no system is immune to breach, and no regulatory framework ever prevents exponential growth. What begins as ‘just for withdrawals’ quietly expands into continuous monitoring, indefinite retention, and mandatory sharing. Over time, the database itself becomes the weakest point in the system, and it rigs the world around you.

Neutrality in banking is dead

Last year, UK high street bank Lloyds was found to have used banking data from 30,000 of its own staff members to influence pay talks. This sort of treachery doesn’t just expose a dysfunctional system; it confirms that data will be used against individuals in plain sight. Blind consent can come at serious personal cost, whether implicit or explicit, and the reason it’s so alluring is that the consequence of failure rarely falls on the institution that collected the data; it falls on the individual whose lives become harder in ways that cannot be reversed.

There is also a deeper shift that happens once identity becomes a prerequisite for participation. KYC does not simply verify who someone is; it establishes permission. Someone decides who gets access, under what conditions, and with what ongoing oversight. Finance stops being neutral infrastructure and becomes a system of gates.

That change matters. A financial system built on permission inevitably reflects the values, incentives, and pressures of those who control it; accounts can be frozen, and access can be revoked. Geopolitical tensions rising across the globe, coupled with stricter KYC demands, mean that over 850 million people will soon, if not already, be excluded from digital banking systems altogether, not because they are criminals, but because they lack stable documents, stable addresses, or stable geopolitical status. For much of the world, financial access isn’t a right, but a merely temporary privilege.

This is why the claim that privacy is only for people who have something to hide has always been a toxic lie. Privacy is not about hiding wrongdoing, it is about preserving what makes each individual who they are, and protecting them from a world becoming evermore comfortable with surveillance. A society where all economic activity becomes an extension of your CV isn’t safe; it’s a surveillance state.

Privacy needs transparency to succeed

The challenge has never been choosing between privacy and transparency, but learning how to build systems that honour both equally. Transparency is essential for systems to function well. We need visibility into flows, patterns, and outcomes to detect abuse, improve infrastructure, and govern responsibly. While transparency requires visibility and authentication to be effective, it doesn’t need to see everything; it can still see movements, trends, and anomalies as a silhouette.

The rise of cryptography in recent years has seen significant breakthroughs in financial privacy technology. Zero-knowledge encryption layer 1 ecosystems such as Zcash (ZEC) and Monero (XMR) are surging as many firms are now weighing up the impact of becoming hardened by Zcash, bringing the relationship between privacy and transparency into sharper focus, as many search for a societal alternative to the normalisation of KYC practices.

Zero-knowledge encryption’s strongest asset is that it allows the general population to prove eligibility without revealing identity; selective disclosure that limits what is shared to what is strictly necessary; and user-held credentials that remove the need for centralised databases altogether. Transactions can be tracked under persistent, pseudonymous identifiers that allow systems to learn and adapt without tying activity to real-world identity. A participant can be recognised as the same actor over time, allowing for accountability, analytics, and improvement, without creating a permanent identity honeypot.

Things must get uglier before they’ll get better

Although the market is moving positively toward privacy in a world that feels more dangerous by the day, zero-knowledge encryption is still a long way from becoming the norm. This means anyone who values their privacy in 2026 will have to endure exclusion, loss, and uncertainty if they are not willing to comply with the alternative.

Every web3 breakthrough is inherently still a long-term experiment, one that intersects painfully with both financial traditionalism and conservative politics. New organisational forms are rarely elegant at the beginning, and unregulated early-stage blunders often spook the political establishment. Corporations, democracies, and public markets all went through ugly, unstable phases before they matured; decentralised systems will too.

Mistakes will be made, and scandals will happen, but infrastructure hardens over time, and what feels like a hefty compromise today becomes tomorrow’s default, and today’s gold standard will become tomorrow’s scandal. Once zero-knowledge practices are normalised, they will not contract, but expand.

After all, being at the tip of the spear means you can strike the heart first, and in time, when the world sees that the traditional banks have sold everyone’s souls down the river, the right people will be forced to pay attention.

Crypto World

LayerZero, Canton, and Zero Blockchain Are Building the Rails for Institutional Cross-Chain Value

TLDR:

- LayerZero has integrated 165+ chains and processed over $200B in volume, creating deep operational lock-in for builders.

- Canton Network processes $8T in monthly RWAs and $350B daily in Treasury repo, with LayerZero as its only live interoperability rail.

- On-chain data shows coordinated ZRO accumulation between $1.30–$2.00, with sizing patterns inconsistent with typical retail behavior.

- Activating the fee switch on $150B in annualized volume would shift ZRO’s valuation from pure optionality to measurable cash flow.

LayerZero, Canton Network, and Zero Blockchain are drawing attention as a potential interoperability stack in the crypto space.

Analysts and on-chain observers are tracking how these three protocols connect crypto-native messaging, institutional liquidity, and execution infrastructure.

The arrangement positions ZRO as a central asset across gas, staking, and value capture functions. Early accumulation patterns and institutional backing are adding weight to the narrative.

Institutional Rails and Network Lock-In

LayerZero has integrated over 165 chains and processed more than $200 billion in cross-chain volume. That scale creates what researchers describe as “infra gravity.” Once an application builds on a messaging layer, migration becomes operationally expensive.

Switching providers for marginal fee savings means reworking compliance systems, risk models, and liquidity routing. That dependency is where network effects become structural rather than speculative.

Canton Network adds a different dimension to this stack. It connects over 800 institutional firms, including Goldman Sachs and J.P. Morgan. The network processes roughly $8 trillion in real-world assets monthly and around $350 billion in U.S.

Treasury repo volume daily. LayerZero is currently the only interoperability rail operating inside that environment. That positioning means the cross-domain liquidity rails for institutions are already in place.

Researcher Nick Research noted on X: “LayerZero is the only interoperability rail live inside that environment. It means if institutional liquidity ever needs to move cross-domain, the rails are already chosen.”

That framing points to a first-mover advantage that is operational rather than theoretical. The integration is live, not pending.

Zero Blockchain rounds out the stack as an execution layer. Its backers include Citadel Securities and the DTCC. Those are not venture bets on technology — they are strategic positions from firms that process real financial volume. The thesis is that interoperability with proper execution controls is where value capture actually concentrates.

On-Chain Signals and the Fee Switch

On-chain data has started reflecting accumulation behavior ahead of any major narrative shift. Clusters of wallets funded through Coinbase Prime accumulated tens of millions in ZRO between $1.30 and $2.00.

The buying patterns showed identical sizing and tight timing, which does not match typical retail activity. Long-duration holders including a16z and ARK have also taken multi-year positions in the asset.

The fee switch is the mechanism that would make this shift visible at the protocol level. Currently, LayerZero routes approximately $150 billion in annualized cross-chain volume with no protocol revenue.

Once fees activate, the valuation framework moves from optionality toward cash flow. That transition tends to reprice assets quickly when it happens on top of an embedded network.

Nick Research summarized the stack plainly: “LayerZero is the messaging layer → Canton is the institutional liquidity pool → Zero is where that liquidity can actually settle and scale.”

The value capture relative to how far network effects have already progressed remains the core observation driving current interest.

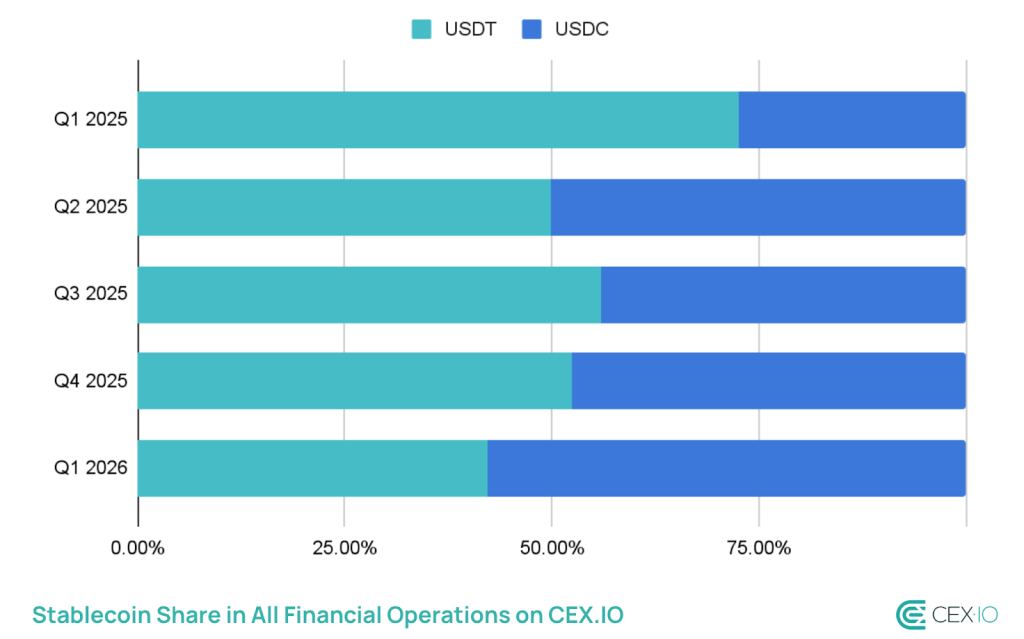

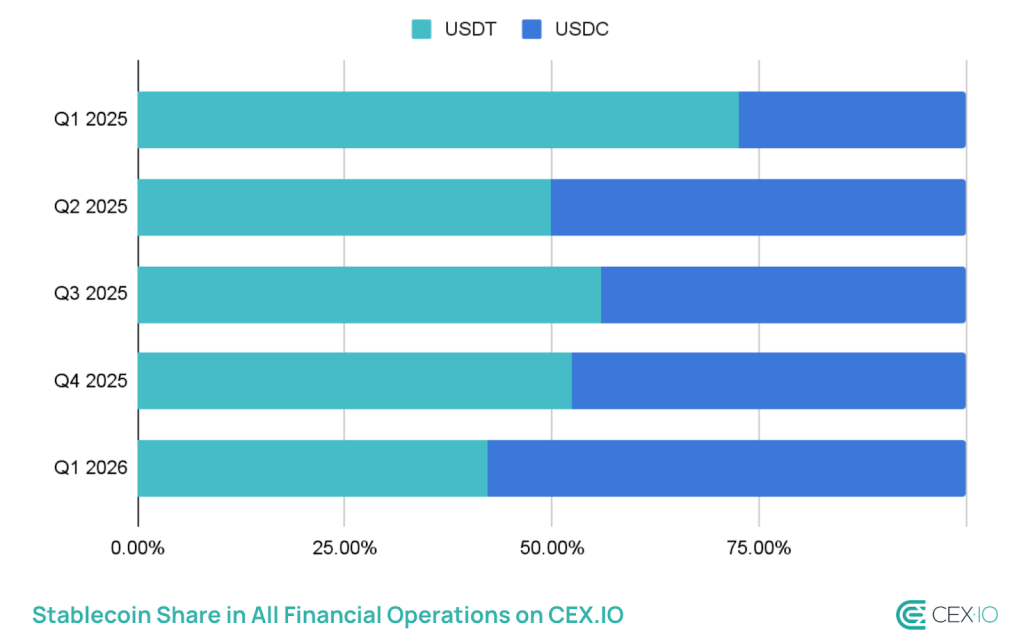

Total stablecoin supply reached a record $315 billion in Q1 2026, rising roughly $8 billion quarter-over-quarter even as the broader crypto market contracted.

The headline figure masks a sharper story underneath: USDC is taking ground from USDT, and the gap is closing faster than most market participants expected.

USDC supply surged 220% since late 2023 to approximately $78 billion, driven by institutional B2B settlement, payroll infrastructure, and programmatic payment rails built by Visa and Stripe.

USDT, still the dominant issuer by raw supply, saw its share slip – a divergence CEX.IO flagged as one of the quarter’s defining market dynamics.

- Total stablecoin supply hit a record $315B in Q1 2026, up ~$8B QoQ – the slowest growth since Q4 2023, but still expansion during a market contraction.

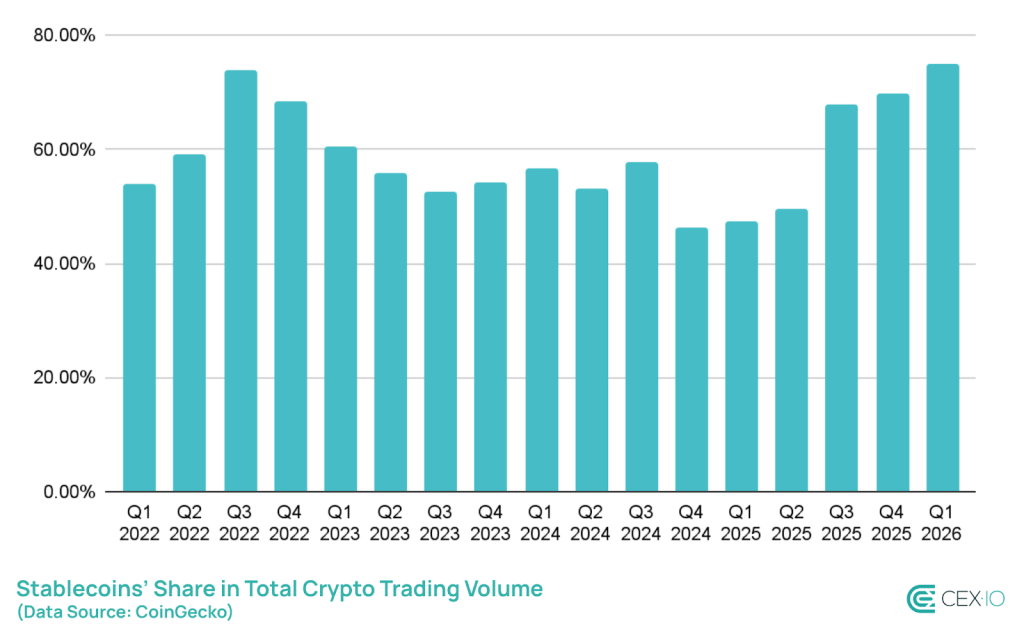

- Stablecoins accounted for 75% of total crypto trading volume in Q1 – the highest share on record.

- Total stablecoin transaction volume topped $28 trillion, exceeding Visa and Mastercard combined.

- USDC supply surged 220% since late 2023 to ~$78B; USDT’s market share slipped amid the divergence.

- Retail-sized transfers fell 16% – the steepest drop on record – while bots drove approximately 76% of all stablecoin transaction volume.

- Yield-bearing stablecoins now represent a $3.7 billion subsector, introducing new fragmentation and regulatory risk.

Discover: The best crypto to diversify your portfolio during market turbulence

Stablecoins also captured 75% of total crypto trading volume in Q1 – the highest share on record – while total transaction volume topped $28 trillion, a figure that now regularly exceeds those of major payment networks like Visa and Mastercard combined. Growth rate slowing is real; demand evaporating is not.

USDC Gain Is a Regulatory Story, Not Just a Market Share Story

The USDC surge is not organic retail adoption. CEX.IO’s data points to institutional programmatic money – B2B corridors, payroll settlement, treasury management, as the primary driver.

USDC’s transaction velocity hit 90x with an average transfer size of $557, a profile consistent with frequent, smaller institutional transactions rather than whale moves.

Circle’s positioning ahead of potential U.S. stablecoin legislation has been deliberate. With the Clarity for Payment Stablecoins Act still under debate and regulatory frameworks for digital assets evolving in Washington, regulated issuers like Circle have a structural advantage in onboarding compliance-sensitive institutional capital. That distinction matters – it’s not market share gained on yield or liquidity depth alone.

Analysts reviewing the quarter described the shift bluntly: “This isn’t retail adoption; it’s institutional programmatic money.” The number that confirms it is USDC’s average transfer size of $557 – dwarfed in absolute terms by USDT’s larger individual trades, but indicative of high-frequency, automated institutional flows that mirror broader tokenization and institutional adoption trends reshaping digital asset infrastructure.

If U.S. stablecoin legislation passes with provisions favoring regulated, audited issuers, USDC’s gain becomes structural. If it stalls, the competitive edge narrows and USDT’s entrenched liquidity depth reasserts dominance.

USDT Still Leads – But the Competitive Moat Is Narrowing

USDT remains the largest stablecoin by supply and the dominant liquidity instrument across emerging market corridors and Tron-based DeFi.

Its concentration on Tron, where low fees drive retail and cross-border transfer volume, gives it a user base that USDC’s Ethereum-centric institutional footprint doesn’t directly compete with. Yet.

The Q1 slip in USDT’s market share comes alongside the steepest recorded drop in retail-sized transfers – down 16% – which cuts at one of USDT’s core use cases.

Simultaneously, bots now account for approximately 76% of all stablecoin transaction volume, meaning the organic retail demand that historically anchored USDT’s dominance in high-frequency small-value transfers is contracting.

CEX.IO flagged this as evidence of “a more sophisticated, but potentially less organic, market structure.”

Tether’s response has been limited to quarterly reserve attestations and geographic expansion rather than product-level innovation. That’s a defensible posture while it holds network effects.

It becomes a liability if institutional capital flows continue rotating into regulated instruments and USDC’s programmatic integrations deepen across Western payment infrastructure.

Watch Circle’s May attestation and Tether’s Q2 report for whether the supply divergence widens. If USDC crosses $90 billion while USDT stagnates, this quarter’s share shift stops looking like a blip and starts looking like a trend.

The $315 billion total supply figure tells you stablecoins are the market’s load-bearing layer. The USDC/USDT split tells you who’s building on top of it.

Explore: The best pre-launch token sales with asymmetric upside potential

The post Stablecoin Crypto Supply Hits $315B in Q1 as USDC Gains, USDT Slips appeared first on Cryptonews.

SpaceX has submitted a confidential draft registration to the U.S. Securities and Exchange Commission, targeting a $1.75 trillion valuation and a raise of up to $75 billion — what would be the largest initial public offering in financial history.

Summary

- SpaceX filed confidentially with the SEC on April 1, 2026, targeting a June Nasdaq listing at up to $1.75 trillion

- The proposed $75 billion raise would more than double Saudi Aramco’s 2019 record of $29 billion and triple Alibaba’s $22 billion U.S. IPO record

- Starlink’s 9.2 million subscribers and approximately $16 billion in 2025 revenue anchor the valuation, alongside the February 2026 merger with Musk’s xAI

The filing, internally codenamed “Project Apex,” was first reported by Bloomberg and confirmed independently by CNBC and Reuters. SpaceX has not publicly commented. A confidential filing allows a company to submit its financials to the SEC for regulatory review before making them public — a standard step before a roadshow.

According to CNBC, 21 banks have been lined up to manage the offering, with Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, and Morgan Stanley holding senior bookrunner roles. SpaceX is also exploring a dual-class share structure to preserve insider voting control and plans to allocate up to 30% of shares to retail investors — roughly three times the typical norm.

At $1.75 trillion, SpaceX would rank above every S&P 500 company except Nvidia, Apple, Alphabet, Microsoft, and Amazon.

The valuation rests primarily on Starlink, SpaceX’s satellite internet division. The service ended 2025 with 9.2 million subscribers across 150 countries, generating approximately $16 billion in annual revenue, with projections pointing toward $22 billion by year-end 2026. SpaceX merged with Musk’s AI venture xAI in February 2026, folding the Grok chatbot and social network X into a single entity that Musk valued at $1.25 trillion at the time. The company has accumulated more than $24.4 billion in federal government contracts since 2008, spanning NASA, the Air Force, and Space Force, according to FedScout.

Musk’s Path to Trillionaire Status

Musk owns approximately 44% of SpaceX. His current net worth sits at roughly $823 billion, according to Forbes. A successful listing at the target valuation would push him toward becoming the first individual in history to surpass $1 trillion — and the first person to simultaneously lead two separate trillion-dollar publicly traded companies. Tesla currently carries a market cap of approximately $1.4 trillion.

The filing positions SpaceX ahead of OpenAI and Anthropic, which are both reportedly weighing public offerings before year’s end. If all three proceed, Bloomberg has described 2026 as potentially the most consequential year for technology IPOs since the dot-com era.

The SpaceX name has long been exploited in crypto markets through impersonation scams — a pattern documented across multiple platforms and token launches — though the IPO itself represents an altogether different category of market event. It arrives at a moment of intensifying institutional appetite for new financial products, a trend visible across crypto ETF launches and alternative asset offerings that Wall Street is moving quickly to capture.

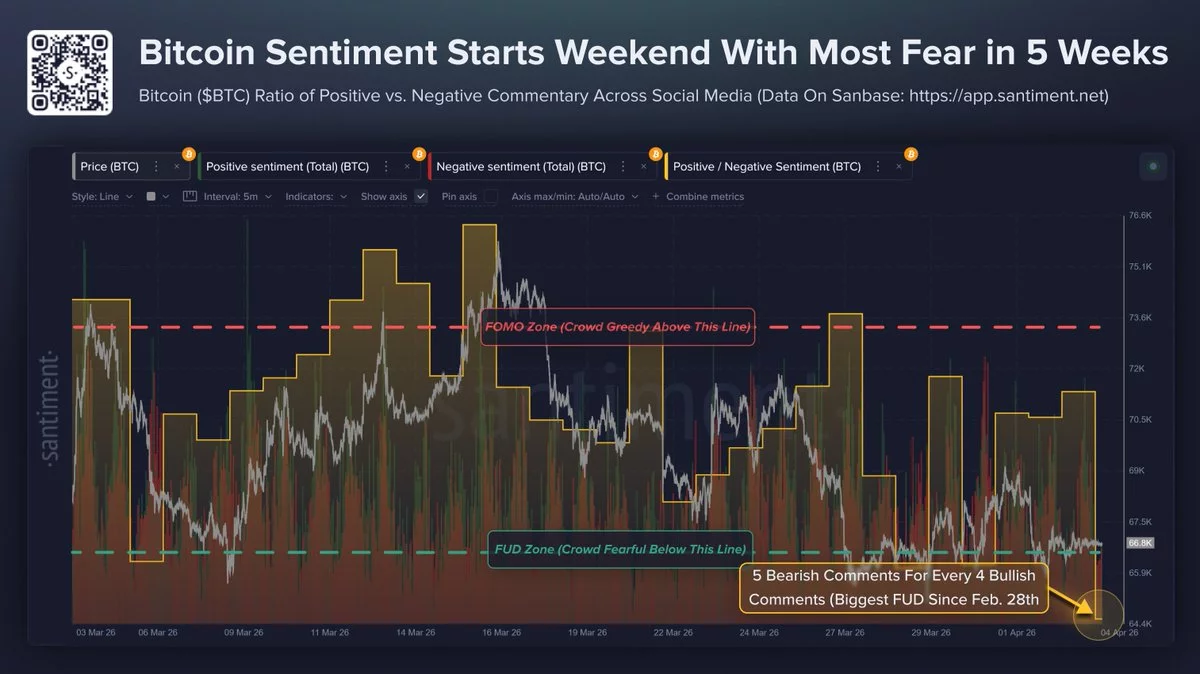

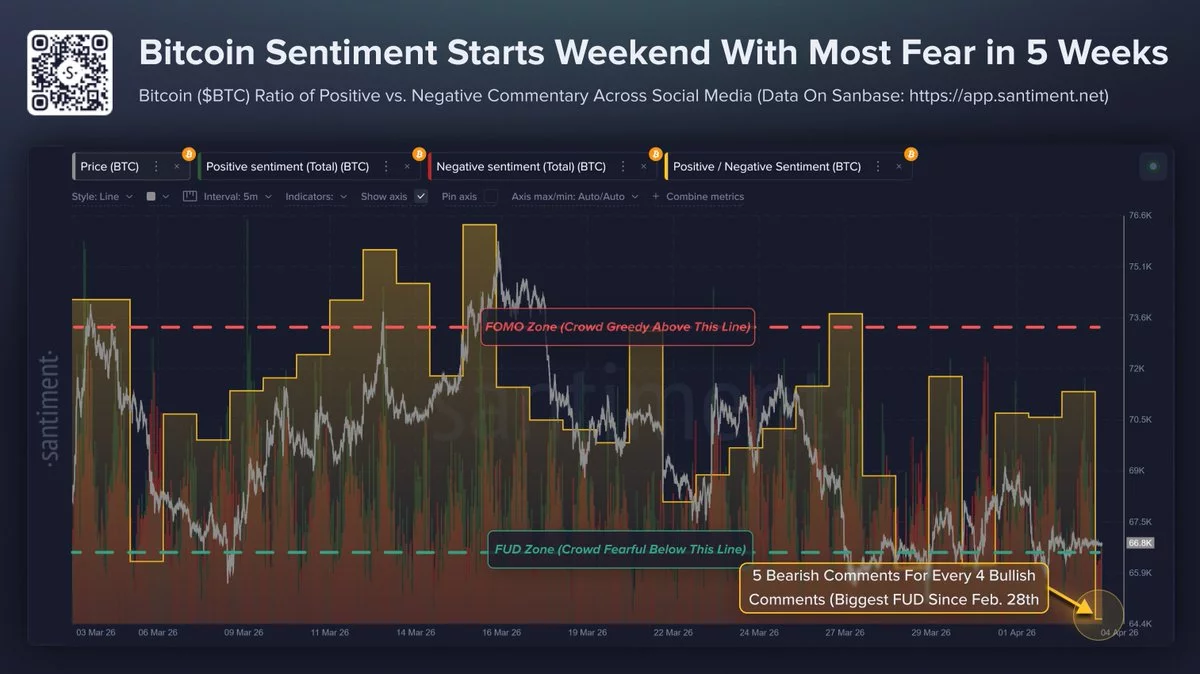

Bitcoin price slipped toward its lowest levels of 2026 on April 4 as social sentiment also weakened.

Summary

- Bitcoin traded near $66,800 as Santiment showed bearish discussion reached its highest level since late February 2026.

- Retail traders turned cautious as spot demand weakened, while leverage remained elevated during Bitcoin’s latest pullback.

- Institutional buyers stayed active as ETFs, Strategy, and Metaplanet kept adding Bitcoin despite weak sentiment.

Data from Santiment showed bearish Bitcoin commentary rising across X, Reddit, and Telegram while the asset traded near $66,800.

Santiment said Bitcoin recorded its highest level of bearish discussion since February 28. The platform found that positive comments fell to 0.81 for every bearish comment, showing that negative talk now leads online discussion.

The shift came as crypto market volatility stayed high and pushed Bitcoin below the $70,000 mark. The data also showed that traders posted about five bearish comments for every four bullish ones across major social platforms.

Retail traders appeared more cautious as Bitcoin pulled back to one of its weakest levels this year. The drop in price and the rise in negative commentary pointed to growing fear, uncertainty, and doubt in the broader market.

Spot demand is weakening while leverage stays elevated. That suggests that buyers in the spot market have slowed down, even as leveraged positions remain active and add pressure during volatile trading sessions.

Institutions continue to buy

While retail sentiment weakened, institutional demand remained more stable. Bitcoin ETFs continued to attract attention, and corporate holders such as Strategy and Metaplanet kept adding exposure despite the latest market decline.

This contrast showed a clear split in market behavior. Smaller traders reacted to price weakness and online sentiment, while larger players focused on longer-term positioning during the current pullback.

As crypto.news recently reported, exchange supply keeps falling, but macro risks still cloud the setup. Lower exchange balances often suggest reduced selling supply, but broader economic pressure still affects market direction.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Elon Musk’s X is rolling out a security feature that will automatically lock any account that mentions cryptocurrency for the first time — requiring additional verification before posting resumes — a direct response to a wave of account hijacking campaigns exploiting social trust to promote scam tokens.

Summary

- X Head of Product Nikita Bier confirmed the auto-lock feature, saying it targets the financial incentive behind crypto phishing attacks on the platform

- The measure follows a surge in account hijacking incidents, including the April 1 compromise of Predictfully founder Benjamin White’s account, which was used to push scam content and extort $4,000 from the real owner

- Bier estimates the feature should eliminate 99% of the incentive behind current phishing operations and called out Google for failing to block phishing emails at the Gmail level

The auto-lock triggers on an account’s first-ever cryptocurrency-related post. Once triggered, the account is locked, and the user must complete verification before regaining access. Bier described it as targeting the core attack vector: hackers gain account access through phishing emails, lock out the original owner, and use the account’s established follower trust to promote fraudulent tokens, fake giveaways, and memecoins.

“This should kill 99% of the incentive,” Bier wrote in response to a user’s account of how they lost control of their profile to a phishing attack disguised as a copyright violation notice. The attacker had used a pixel-perfect fake login page to harvest the user’s credentials and two-factor authentication codes before locking them out and beginning scam promotion.

What This Targets

Crypto-linked account hijacking on X has been a documented and persistent problem since the platform’s days as Twitter. The auto-lock builds on earlier platform efforts to eliminate mention-spam campaigns and coordinated account behavior used in crypto promotions. Long-term users who have never posted about cryptocurrency will face verification on their first such post, while legitimate accounts, Bier indicated, can regain access quickly through the process.

Bier also publicly criticized Google for allowing phishing emails to reach users through Gmail. “Google isn’t doing shit to stop the phishing,” he wrote — framing the auto-lock as a platform-level workaround to a vulnerability upstream that X cannot directly control.

The U.S. Federal Trade Commission has documented how social media crypto scams have surged into a multi-billion dollar problem, with victims often unable to recover funds given the irreversibility of on-chain transfers. This structural reality is what makes hijacked accounts with established follower trust so valuable to attackers — and what the auto-lock directly targets by severing the link between account access and immediate monetization via crypto promotion.

Limitations

Critics have flagged that the measure only intervenes after an account has already been compromised via phishing. If email providers do not better filter phishing emails upstream, the attack chain remains intact. The feature could also create friction for legitimate first-time crypto posts from established accounts, though Bier indicated the verification process will be brief for genuine users.

As broader crypto hack and phishing losses have shown improvement in recent months — with February 2026 recording the lowest monthly total since March 2025 — the $285 million Drift Protocol exploit this week is a sharp reminder that headline risk remains high. X’s new feature addresses one specific and high-volume attack vector within a much larger ecosystem of crypto-linked fraud.

Crypto has spent years obsessing over speed, fees and scalability. Now it may have to confront a more existential question: what happens when its core security breaks?

That question is moving from theory to urgency. Quantum computers, machines that use the principles of quantum physics to process information in fundamentally different ways than today’s computers, could eventually solve the kinds of mathematical problems that underpin modern encryption.

Discussions around post-quantum cryptography have intensified across the industry in recent weeks, especially after new research from Google and academic collaborators suggested that such systems could one day break widely used encryption, potentially cracking systems like Bitcoin’s in minutes rather than years.

While Bitcoin developers scramble to find a solution and Ethereum prepares for the event, Solana is trying to get ahead of that scenario.

Cryptography firm Project Eleven has teamed up with the Solana Foundation to experiment with post-quantum security, technology designed to withstand quantum attacks that could render today’s cryptography obsolete. The early work is already surfacing a difficult reality: making Solana quantum-safe may come at the expense of the performance that defines it.

In practice, that effort has meant moving beyond theory and into live testing. Project Eleven has worked with the Solana ecosystem to model how the network would behave if its current cryptography were replaced, including deploying a test environment using quantum-resistant signatures — the digital keys that authorize transactions. The goal is not just to prove the technology works, but to understand what breaks when it’s pushed to scale.

The early results show a clear tradeoff.

The new, quantum-safe “signatures” that approve transactions are much larger and heavier than those used today, roughly 20 to 40 times larger, Project Eleven CEO Alex Pruden, who founded the project, after years in crypto and venture capital, brings a mix of military and industry experience to the problem, told CoinDesk. That means the network can handle far fewer transactions at once. In testing, a version of Solana using this new cryptography ran about 90% slower than it does today, Pruden said.

That tradeoff cuts directly at the heart of Solana’s design. The blockchain has built its reputation on high throughput and low latency, positioning itself as one of the fastest networks in crypto. But post-quantum cryptography — while more secure against future threats — comes with heavier data and computational requirements, making it harder to maintain those speeds.

‘Pick any wallet’

Solana may also face a more immediate structural challenge than its peers.

Unlike Bitcoin and Ethereum, where wallet addresses are typically derived from hashed public keys, Solana exposes public keys directly. That difference matters in a quantum scenario. “In Solana, 100% of the network is vulnerable,” Pruden said.

“A quantum computer could pick any wallet and immediately start trying to recover the private key.”

Pruden, a former Army Green Beret, first became interested in Bitcoin while deployed in the Middle East, later worked at Coinbase and joined Andreessen Horowitz’s venture team on its first fund. He then became an early leader at privacy-focused blockchain Aleo before launching Project Eleven, a firm focused on preparing digital assets for what he calls “Q-day,” the moment quantum computers can break today’s cryptography.

Some developers in the Solana ecosystem, meanwhile, are looking at simpler, more immediate fixes. One example is something called ‘Winternitz Vaults’, which uses a different kind of cryptography that’s believed to be safer against quantum attacks. Instead of changing the entire network, these tools focus on protecting individual wallets, giving users a way to secure their funds now while bigger, system-wide upgrades are still being figured out.

Despite those hurdles, Solana has moved faster than much of the industry in at least one respect: experimentation. “There’s something tangible,” Pruden said. “We actually have a testnet with post-quantum signatures.” He added that the Solana Foundation “deserves credit for at least engaging and wanting to do the work.”

Across crypto, that level of engagement remains rare. While some ecosystems, most notably Ethereum, have begun discussing long-term migration paths, concrete implementation has been limited.

The broader challenge is not just technical, but social: upgrading cryptography in decentralized systems requires coordination across developers, validators, applications and users, all of whom must move in sequence.

For Pruden, the risk is that the industry waits too long to begin that process. “This is a tomorrow problem — until it’s today’s problem,” he said. “And then it takes four years to fix.”

Read more: Here’s how bitcoin, Ethereum and other networks are preparing for the looming quantum threat

Crypto World

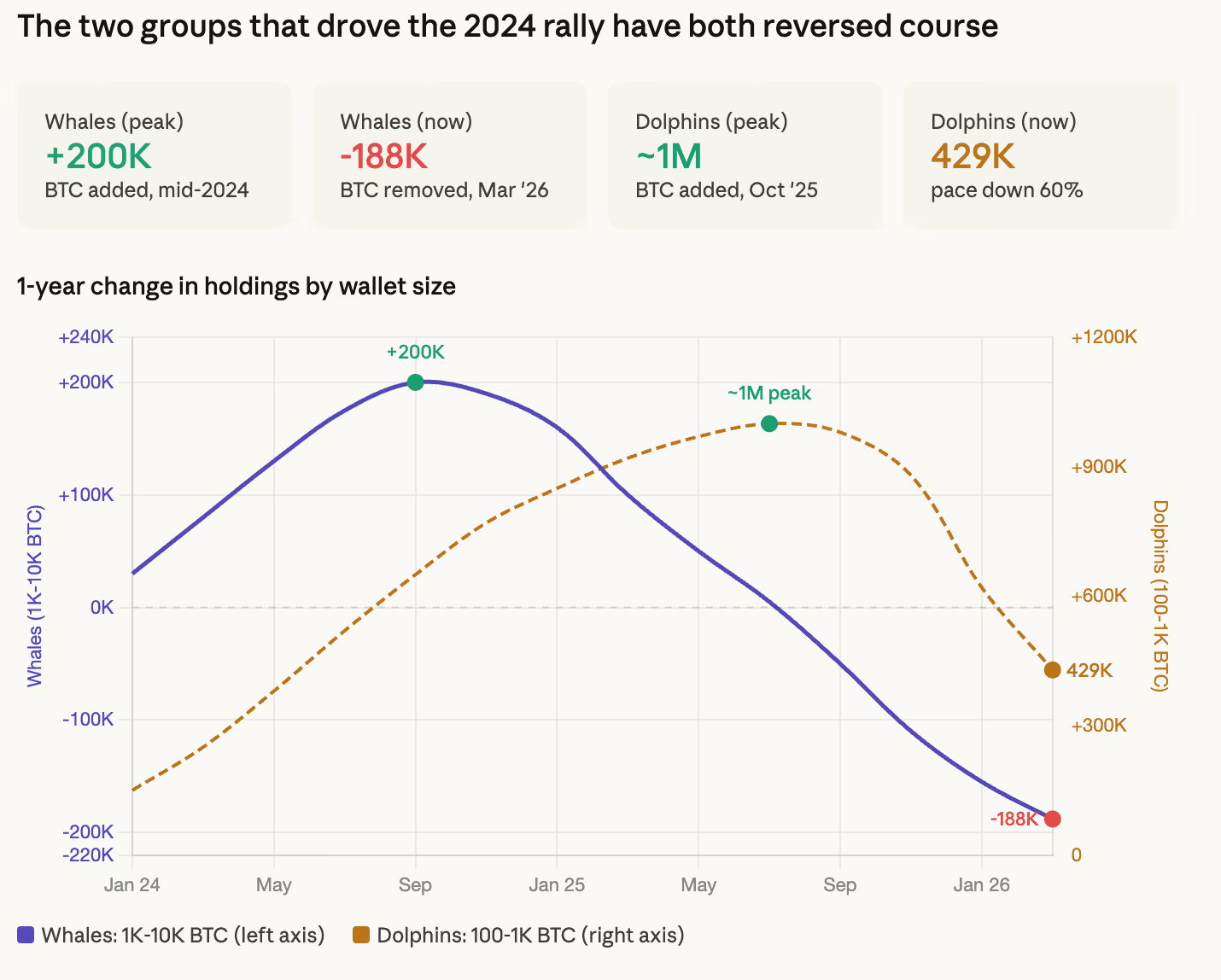

Bitcoin whales are selling the most aggressively on record while ETFs and Strategy keep buying

The most visible bitcoin buyers in the world are buying at near-record pace. It is not enough.

A CryptoQuant weekly report showed overall 30-day apparent demand at negative 63,000 BTC as of late March, meaning the broader market is selling far faster than institutions can absorb. ETF purchases hit approximately 50,000 BTC in the rolling 30-day window, the highest since October 2025. Strategy’s accumulation held steady at roughly 44,000 BTC. Together, the two largest institutional channels absorbed about 94,000 BTC in March.

If institutions bought 94,000 BTC and net demand is still negative 63,000, the rest of the market — such as retail, older whales, miners, funds — sold approximately 157,000 BTC in the same period.

At least four other independent indicators are pointing in the same direction.

The whale reversal

Large holders, wallets with 1,000 to 10,000 BTC, have turned from the market’s biggest buyers into its biggest sellers on a scale CryptoQuant describes as one of the most aggressive distribution cycles on record.

A year ago, these wallets were collectively adding 200,000 bitcoin to their holdings. Today they are collectively removing 188,000. That is a nearly 400,000 BTC swing from accumulation to distribution in roughly 18 months.

Mid-tier holders, wallets with 100 to 1,000 BTC, are still technically accumulating but the pace has collapsed more than 60% since October 2025, from nearly 1 million BTC in annual additions to 429,000. They haven’t stopped buying. They’ve dramatically slowed down.

The realized price compression

Bitcoin’s spot price at in the $67,000-$68000 range sits 21% above its realized price of $54,286, the average cost basis of every coin on the network weighted by its last transaction. That means the average holder is still in profit, which historically means the market has not bottomed, as CoinDesk noted earlier in the week.

In 2022, the signal that marked the actual cycle low was spot falling below realized price. Bitcoin traded under its aggregate cost basis from June through October of that year, and the deepest point, roughly 15% below realized, coincided almost exactly with the low near $15,500.

The current setup is not that. But the gap is closing fast. In late 2024, when bitcoin traded above $119,000, the premium to realized price was roughly 120%. That has compressed to 21% in about 15 months, one of the fastest approaches to the realized price line outside of outright crashes.

The sentiment disconnect

The Fear and Greed Index has been stuck between 8 and 14 for the past month, deep in extreme fear territory. Yet bitcoin ETFs drew over $1 billion in net inflows in March.

That combination of extreme fear alongside strong institutional buying is unusual. It means the flows are not translating into broader confidence, but that institutions are buying into a market that the rest of the participants do not want to be in.

The widely-followed Coinbase Premium Index reinforces this. The metric, which measures whether bitcoin trades at a premium or discount on Coinbase relative to other exchanges and serves as a proxy for U.S. institutional appetite, has been persistently negative since bitcoin’s all-time high above $126,000 in early October 2025. Even with prices in the $65,000 to $70,000 range, American buyers have not stepped back in at scale.

The war pattern

The behavioral explanation for the demand drain is visible in the price action of the past five weeks. Bitcoin has spent the entire Iran conflict grinding between $65,000 and $73,000, selling on every escalation headline, rallying on every de-escalation headline, and ending up roughly where it started. Monday’s 4% equity rally on ceasefire optimism gave back by Wednesday after Trump’s address promised to hit Iran “extremely hard.”

The pattern of hope, headline, reversal repeats with such regularity that the dominant strategy has become not to have a position at all. That shows up in the demand data as gradual withdrawal rather than panic selling.

The drawdown is compressing, not ending

The current drawdown from October’s all-time high above $126,000 is roughly 47%, significantly less severe than the 84% to 87% crashes that followed the 2013 and 2017 peaks. Fidelity Digital Assets analyst Zack Wainwright noted in late March that bitcoin’s growth is becoming “less impulsive,” with a reduced probability of extreme downside events as the asset matures.

“Bitcoin’s drawdowns compressing to about 50% is a sign of a maturing market structure,” said Jason Fernandes, co-founder and market analyst at AdLunam. “As liquidity deepens and institutional participation increases, volatility naturally compresses on both the upside and the downside.

The drawdown compression framing matters for the demand data. If bitcoin is maturing into an asset where 50% corrections replace 85% crashes, then the current contraction may not resolve with the violent capitulation flush that marked previous cycle bottoms.

What could change this

Two catalysts sit on the near-term horizon.

Morgan Stanley received approval this week for a bitcoin ETF charging just 14 basis points, 11 below the category average. The product opens access to 16,000 financial advisors managing $6.2 trillion, a channel that has not previously had direct bitcoin ETF exposure.

Strategy’s STRC preferred equity product saw hundreds of millions in inflows around its recent ex-dividend date, providing the funding mechanism for its 44,000 BTC monthly accumulation. If that repeats and accelerates each month, it adds a new source of sustained buying pressure.

However, it would remain a single company running a leveraged bitcoin strategy.

CryptoQuant’s own report identifies a potential short-term bounce toward $71,500 to $81,200 if the Iran conflict de-escalates, corresponding to the Lower Band and Trader On-chain Realized Price resistance zones.

These two metrics track the average cost basis of short-term and active traders respectively, and that have historically acted as ceilings during bear market rallies. Bitcoin currently trades below both.

The read across all five data sources is that bitcoin’s demand structure is thinning from the inside.

That does not mean the current range floor breaks, but that the floor depends entirely on whether ETFs, Strategy, and the new Morgan Stanley channel can continue absorbing what the rest of the market is trying to get rid of.

Cambodia has moved closer to tougher action against scam centers linked to crypto fraud and other online crimes.

Summary

- Cambodia’s Senate approved a draft bill targeting scam compounds tied to crypto and online fraud.

- The bill sets prison terms, fines, and tougher penalties for gangs or multiple victims involved.

- The measure now awaits royal approval as Cambodia faces pressure over regional scam centers globally.

The country’s Senate approved a draft law that would impose prison terms and fines on people involved, marking a new step in its response to scam compounds.

Cambodia’s Senate said it unanimously approved the draft law on Friday, with all 58 senators voting in favor. The bill now awaits the king’s approval before it can take effect.

Reports said the proposed law would impose prison terms of two to five years and fines of up to $125,000 for certain offenses. Those penalties could double if the crimes involve a gang or affect several victims.

The Senate said the draft law would create criminal rules to address gaps in current legislation. It described the measure as part of a wider effort to respond to fraud carried out through technology systems.

In its notice, the Senate said the law would help tackle risks to social security, the economy, and public order. The notice added that the measure aimed to improve cooperation in the fight against fraud and protect Cambodia’s reputation. It said the draft law would help “fill the gaps and deficiencies in the current law” and improve efforts against fraud.

In addition, the bill moved forward after criticism from foreign governments and international bodies over scam activity in Southeast Asia. A 2025 report from the US State Department said Cambodia’s government had often treated scam cases as labor disputes and had not prosecuted owners or operators of suspected scam compounds.

The timing also followed action from the United Kingdom, which sanctioned operators of a Cambodia-based scam center. Cambodia also extradited to China the leader of a criminal syndicate with reported links to scam compounds. Before the Senate vote, the National Assembly approved the bill on March 30 with all 112 members voting in support.

Scam centers remain under scrutiny

Reports from the region have described scam compounds as closed sites where workers may face control, threats, and abuse. A 2024 UN report on a compound in the Philippines said some workers were trafficked, held against their will, and exposed to violence.

The report said many of these sites operate like self-contained facilities. It stated that the people inside are “basically fenced off from the outside world,” with access to restaurants, dormitories, and other services that reduce the need to leave. Cambodia’s proposed law now places fresh attention on how the country plans to address such operations.

Bitcoin (BTC) traded near $67,000 over the weekend after a week of sharp swings. The broader crypto market also stayed steady, while Pi Network’s PI token held above $0.17 after days of losses.

Summary

- Bitcoin traded around $67,000 as weekend volatility faded and the broader crypto market stayed subdued.

- Pi Network’s PI token stabilized above $0.17 after recent losses, ending its sharp downward trend.

- VeChain climbed 9% daily while HASH dropped 10%, marking the strongest altcoin moves reported today.

Bitcoin showed limited movement over the past 24 hours and remained close to the $67,000 level. Its price action followed a volatile week in which the asset moved between $66,000 and $68,000 before rising to $69,200 on Wednesday.

That move reversed after fresh market pressure, sending Bitcoin down to $65,700 later the same day. Since then, the asset has traded in a narrow range. At press time, Bitcoin’s market capitalization stood at about $1.34 trillion, while its market dominance remained near 56.2%.

Most large-cap altcoins posted small changes during the same period. Ethereum held near $2,050 after a slight daily loss, while XRP remained above $1.30. BNB, Solana, TRX, and Cardano all recorded gains of less than 1%.

The biggest moves among larger altcoins came from a smaller group of assets. RAIN fell more than 6% and dropped below $0.0075. HBAR, PEPE, UNI, and SHIB also traded lower. In contrast, Ethereum Classic rose 3.5% to $8.30 and stood out from the broader market.

PI token steadies after recent drop

Pi Network’s PI token showed signs of stability after a recent downward move. The token traded above $0.17, marking a pause in the decline that had drawn attention across the altcoin market.

Elsewhere, HASH posted the sharpest daily loss among the mentioned tokens, falling 10% over the past 24 hours. VeChain moved in the opposite direction and gained 9% on the day, helping it return to the top 100 altcoins by market value.

Meanwhile, the total crypto market value changed little over the day and remained just below $2.4 trillion. That flat reading matched the quiet performance seen across Bitcoin and most major altcoins during the weekend session.

Market activity also stayed muted despite recent macro and geopolitical headlines that had raised expectations of stronger price swings earlier in the week.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

HypurrFi has warned users not to interact with its website or lending app after reporting a possible domain hijacking.

Summary

- HypurrFi warned users to avoid its app after reporting a possible domain compromise Friday.

- The team said user funds remain safe while it investigates the suspected hijacking incident.

- Frontend attacks remain a crypto risk because compromised domains can trick users into signing transactions.

The incident has raised fresh concern over frontend attacks in decentralized finance, even when onchain systems remain intact.

HypurrFi said it is investigating a possible compromise involving its domain. The team asked users to avoid the website and the lending protocol until it shares a new update.

Founder androolloyd posted on X, “Do NOT USE THE HYPURR .FI domain, it is compromised.” The team later repeated that warning and told users not to interact with the app until further notice.

HypurrFi also said there is no current sign of risk to user funds. It added that its social media accounts remain under team control during the investigation.

The warning focused on the website and user access point rather than the protocol’s core contracts. That distinction is common in cases where attackers target frontend systems instead of onchain code.

HypurrFi operates as a DeFi lending and borrowing protocol on HyperEVM. HyperEVM is the EVM-compatible network linked to Hyperliquid’s trading ecosystem.

The protocol has about $30 million in total value locked, based on DefiLlama data. That made the warning more urgent for users who may still try to access the platform through the compromised domain.

The team did not provide details on how the hijacking may have happened. It also did not say when the site would return to normal use.

For now, the main message from the project remains clear. Users should avoid the domain and wait for an official notice before reconnecting wallets or signing any transaction requests.

Domain hijacking remains a known crypto risk

Domain hijacking has become a recurring issue across the crypto sector. These attacks often target a project’s website and user interface instead of its smart contracts.

Once attackers control a domain, they can place wallet drainers or other malicious prompts on the site. This method can affect users even when the underlying protocol has passed security reviews.

A similar case affected the BONKfun domain last month. That incident added to a growing list of attacks that use fake or compromised frontends to reach users.

Smart Money Wallet Tips for Financial Growth

‘We’re not going anywhere’: Belfast coffee shop burglary ‘fourth incident in just a few weeks’

5 Relatively Secure And Cheap Dividend Stocks, Yields Up To 8% (April 2026)

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Smart Money Wallet Tips for Financial Growth

#money #discipline #inspirationalquotes #selfimprovement #motivationalquotes #motivation #automobile

Don’t make the same financial mistake that I did! #costofliving #smartmoney #makemoneyfromhome

-

NewsBeat2 days ago

NewsBeat2 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business2 days ago

Business2 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion18 hours ago

Fashion18 hours agoWeekend Open Thread: Spanx – Corporette.com

-

Entertainment5 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World3 days ago

Crypto World3 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech5 days ago

Tech5 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World4 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Entertainment7 days ago

Entertainment7 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Tech5 days ago

Tech5 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Tech4 days ago

Tech4 days agoEE TV is using AI to help you find something to watch

-

Sports4 days ago

Sports4 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Business2 days ago

Business2 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Fashion6 days ago

Fashion6 days agoAmazon Sundays: Soft Spring Layers

-

Tech6 days ago

Tech6 days agoElon Musk’s last co-founder reportedly leaves xAI

-

Fashion5 days ago

Fashion5 days agoThe Best Spring Trends of 2026

-

Tech4 days ago

Tech4 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Politics5 days ago

Politics5 days agoShould Trump Be Scared Strait?

-

Tech5 days ago

Tech5 days agoApple will hide your email address from apps and websites, but not cops

-

Crypto World5 days ago

Crypto World5 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech4 days ago

Tech4 days agoFlipsnack and the shift toward motion-first business content with living visuals

You must be logged in to post a comment Login