Crypto World

Stablecoin Crypto Supply Hits $315B in Q1 as USDC Gains, USDT Slips

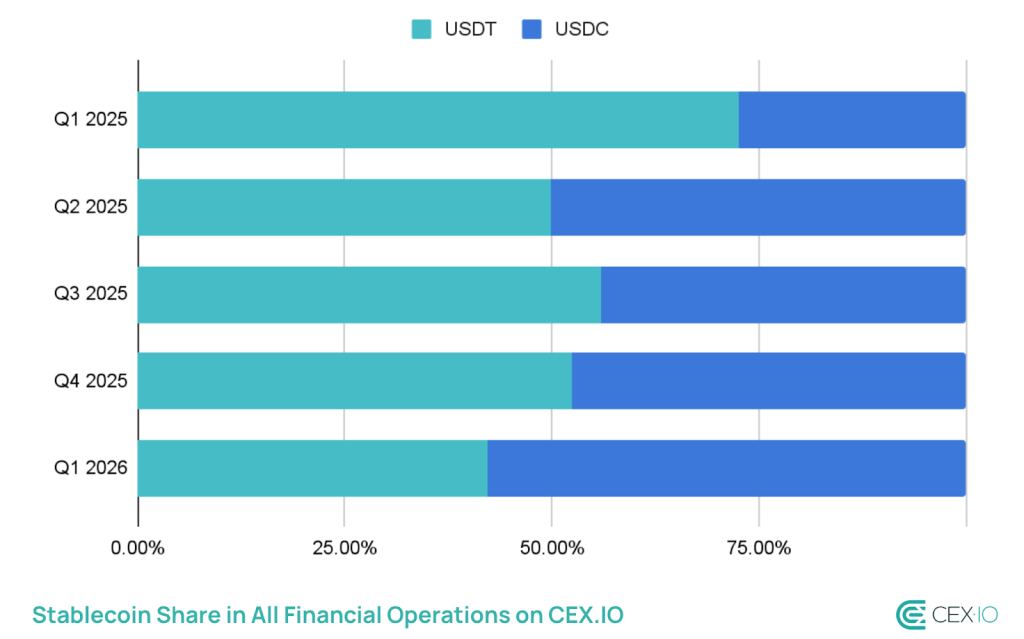

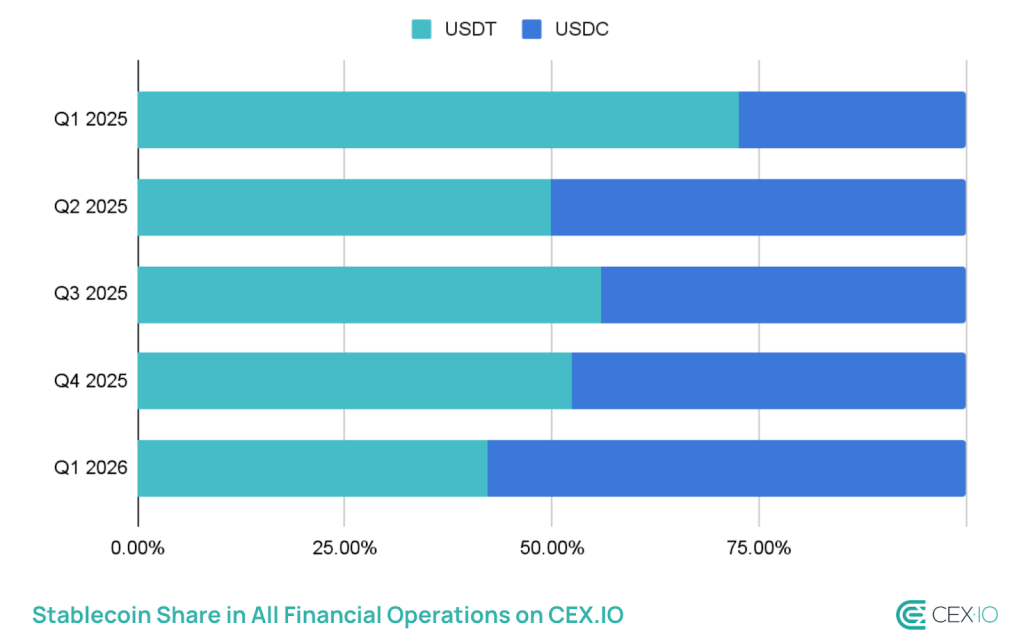

Total stablecoin supply reached a record $315 billion in Q1 2026, rising roughly $8 billion quarter-over-quarter even as the broader crypto market contracted.

The headline figure masks a sharper story underneath: USDC is taking ground from USDT, and the gap is closing faster than most market participants expected.

USDC supply surged 220% since late 2023 to approximately $78 billion, driven by institutional B2B settlement, payroll infrastructure, and programmatic payment rails built by Visa and Stripe.

USDT, still the dominant issuer by raw supply, saw its share slip – a divergence CEX.IO flagged as one of the quarter’s defining market dynamics.

- Total stablecoin supply hit a record $315B in Q1 2026, up ~$8B QoQ – the slowest growth since Q4 2023, but still expansion during a market contraction.

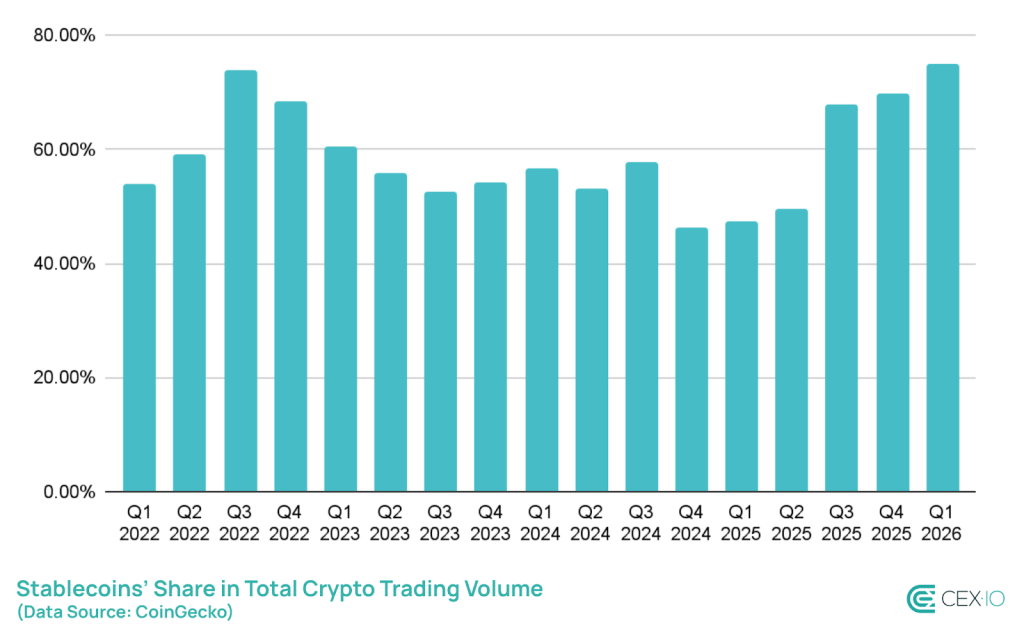

- Stablecoins accounted for 75% of total crypto trading volume in Q1 – the highest share on record.

- Total stablecoin transaction volume topped $28 trillion, exceeding Visa and Mastercard combined.

- USDC supply surged 220% since late 2023 to ~$78B; USDT’s market share slipped amid the divergence.

- Retail-sized transfers fell 16% – the steepest drop on record – while bots drove approximately 76% of all stablecoin transaction volume.

- Yield-bearing stablecoins now represent a $3.7 billion subsector, introducing new fragmentation and regulatory risk.

Discover: The best crypto to diversify your portfolio during market turbulence

Stablecoins also captured 75% of total crypto trading volume in Q1 – the highest share on record – while total transaction volume topped $28 trillion, a figure that now regularly exceeds those of major payment networks like Visa and Mastercard combined. Growth rate slowing is real; demand evaporating is not.

USDC Gain Is a Regulatory Story, Not Just a Market Share Story

The USDC surge is not organic retail adoption. CEX.IO’s data points to institutional programmatic money – B2B corridors, payroll settlement, treasury management, as the primary driver.

USDC’s transaction velocity hit 90x with an average transfer size of $557, a profile consistent with frequent, smaller institutional transactions rather than whale moves.

Circle’s positioning ahead of potential U.S. stablecoin legislation has been deliberate. With the Clarity for Payment Stablecoins Act still under debate and regulatory frameworks for digital assets evolving in Washington, regulated issuers like Circle have a structural advantage in onboarding compliance-sensitive institutional capital. That distinction matters – it’s not market share gained on yield or liquidity depth alone.

Analysts reviewing the quarter described the shift bluntly: “This isn’t retail adoption; it’s institutional programmatic money.” The number that confirms it is USDC’s average transfer size of $557 – dwarfed in absolute terms by USDT’s larger individual trades, but indicative of high-frequency, automated institutional flows that mirror broader tokenization and institutional adoption trends reshaping digital asset infrastructure.

If U.S. stablecoin legislation passes with provisions favoring regulated, audited issuers, USDC’s gain becomes structural. If it stalls, the competitive edge narrows and USDT’s entrenched liquidity depth reasserts dominance.

USDT Still Leads – But the Competitive Moat Is Narrowing

USDT remains the largest stablecoin by supply and the dominant liquidity instrument across emerging market corridors and Tron-based DeFi.

Its concentration on Tron, where low fees drive retail and cross-border transfer volume, gives it a user base that USDC’s Ethereum-centric institutional footprint doesn’t directly compete with. Yet.

The Q1 slip in USDT’s market share comes alongside the steepest recorded drop in retail-sized transfers – down 16% – which cuts at one of USDT’s core use cases.

Simultaneously, bots now account for approximately 76% of all stablecoin transaction volume, meaning the organic retail demand that historically anchored USDT’s dominance in high-frequency small-value transfers is contracting.

CEX.IO flagged this as evidence of “a more sophisticated, but potentially less organic, market structure.”

Tether’s response has been limited to quarterly reserve attestations and geographic expansion rather than product-level innovation. That’s a defensible posture while it holds network effects.

It becomes a liability if institutional capital flows continue rotating into regulated instruments and USDC’s programmatic integrations deepen across Western payment infrastructure.

Watch Circle’s May attestation and Tether’s Q2 report for whether the supply divergence widens. If USDC crosses $90 billion while USDT stagnates, this quarter’s share shift stops looking like a blip and starts looking like a trend.

The $315 billion total supply figure tells you stablecoins are the market’s load-bearing layer. The USDC/USDT split tells you who’s building on top of it.

Explore: The best pre-launch token sales with asymmetric upside potential

The post Stablecoin Crypto Supply Hits $315B in Q1 as USDC Gains, USDT Slips appeared first on Cryptonews.

Ripple CEO Brad Garlinghouse has been named the 2026 Business Leader of the Year by the Harvard Business School Association of Northern California.

Summary

- Brad Garlinghouse received Harvard’s 2026 Business Leader of the Year award in San Francisco this week.

- Harvard praised Garlinghouse for scaling Ripple while keeping focus on the company’s long-term business vision.

- Ripple expanded through major acquisitions, global licenses, and XRP ETF momentum after its SEC battle.

The award was presented during a dinner at the Julia Morgan Ballroom in San Francisco. The Harvard Business School Association of Northern California has given the award since 1969. Past recipients include Amazon CEO Andy Jassy, former Cisco CEO John Chambers, and Intel co-founder Gordon Moore.

Harvard Business School Professor David B. Yoffie praised Garlinghouse’s leadership at Ripple. He pointed to the CEO’s work in building the company while keeping its core business direction in place.

Yoffie said Garlinghouse showed an “extraordinary ability to scale a complex platform while maintaining a steadfast commitment to his core vision.” The comment came as Garlinghouse marked 11 years at Ripple.

Garlinghouse’s path at Ripple

Garlinghouse joined Ripple in April 2015 as chief operating officer after earlier executive roles at AOL and Yahoo. He later became CEO in 2016 after co-founder Chris Larsen brought him into the company.

Before joining Ripple, Garlinghouse had reportedly considered a role at Uber. He later became one of the most visible executives in the crypto sector, especially during Ripple’s long legal dispute with the SEC.

Ripple expands after legal battle

Ripple has continued to grow after its legal fight with the SEC. Garlinghouse has also become a leading voice in calls for clearer crypto rules in the United States.

Over the past year, Ripple completed large acquisitions, including GTreasury for $1 billion and Hidden Road for $1.25 billion. The company later rebranded Hidden Road as Ripple Prime, a clearing platform focused on institutional finance.

Ripple also secured key licenses in global markets, including an Electronic Money Institution license in the United Kingdom. The company has also benefited from growing interest in XRP products after XRP spot ETFs launched last year.

The Harvard award adds another public milestone for Garlinghouse as Ripple expands its role in crypto payments, custody, stablecoins, and institutional markets.

TLDR:

- Galaxy Digital CEO Mike Novogratz expects the CLARITY Act to reach Trump’s desk for signing by June 2026.

- Galaxy’s Alex Thorn puts the odds of the CLARITY Act passing in 2026 at 50%, citing Senate delays as a key risk.

- Senator Cynthia Lummis warned that failing to pass the CLARITY Act now could delay reform until at least 2030.

- The CLARITY Act could unlock U.S. financial market access for an estimated 5.5 billion people across the globe.

The CLARITY Act remains one of the most closely watched pieces of legislation in the crypto space. Galaxy Digital CEO Mike Novogratz stated the bill will likely be finalized in May.

He expects President Trump to sign it into law in June. The bill aims to give the U.S. crypto industry a clearer regulatory framework.

Its passage could open American financial markets to over 5.5 billion people worldwide who currently lack access.

CLARITY Act Timeline Draws Both Confidence and Caution

Novogratz shared his outlook during a podcast with SkyBridge Capital founder Anthony Scaramucci. He said the bill would go to committee in the first week of May.

He added that it would be signed shortly after by President Trump. His comments came after a disappointing week for the industry. The Senate Banking Committee did not schedule a markup hearing as many had anticipated.

The CEO emphasized the bill’s broad political appeal. He said it is “wildly important” for both Democrats and Republicans to see it through.

This bipartisan support has been a consistent talking point among industry advocates. However, that support has not yet translated into a clear legislative path forward.

The CLARITY Act passed the House in July 2025 with backing from both parties. Yet ongoing disputes have slowed its progress through the Senate.

A major sticking point involves stablecoin yields. The banking sector has raised concerns that such yields could undermine their competitive position in the market.

U.S. Senator Cynthia Lummis issued a stark warning on April 10. She posted on X: “This is our last chance to pass the Clarity Act until at least 2030.

We can’t afford to surrender America’s financial future.” Her statement added urgency to an already pressured legislative calendar heading into May.

Industry Analysts See Mixed Odds for CLARITY Act in 2026

Galaxy Digital’s head of firmwide research, Alex Thorn, offered a more measured view. He put the current odds of the CLARITY Act passing in 2026 at 50%.

Thorn shared this estimate in an X post earlier in the week. He also released a detailed research report outlining the legislative risks involved.

Thorn had expected the Senate Banking, Housing, and Urban Affairs Committee to announce a markup hearing. That announcement was anticipated for the last week of April.

It did not happen as expected. He warned that if the markup process slips past mid-May, the odds of passage will drop sharply.

Novogratz, meanwhile, pointed to the broader economic case for the legislation. He noted that large institutions like SpaceX and Google could be tokenized and sold to global investors.

He also said a crypto wallet on a smartphone would allow people in countries like Bhutan, Botswana, Bolivia, and Paraguay to participate in the U.S. economy. That vision, he argued, is central to the bill’s purpose.

The CLARITY Act carries weight beyond the crypto market alone. A number of firms left the U.S. during the Biden administration due to regulatory uncertainty.

Clearer rules could bring those firms back and attract new ones. Whether Congress acts in time remains the central question heading into May.

Snagging a Markets in Crypto Assets (MiCA) license to operate in Europe is great, but, alone, it won’t be enough to turn a profit, according to Ben Zhou, the CEO of Bybit, one of the largest cryptocurrency trading platforms.

MiCA doesn’t cover the full range of products, such as derivatives and tokenized assets, needed to be profitable, Zhou said in an interview. For those, companies also need a MiFID II (Markets in Financial Instruments Directive) license and an Electronic Money Institution (EMI) license.

“With the current MiCA framework, you can only do fiat-to-crypto, crypto-to-crypto,” Zhou said. “There are many elements of a profitable business you cannot do, so even as a MiCA holder — unless you’re Kraken or BItpanda or Bitvivo, who are already making money because they have multiple licenses.”

Even Bybit, the world’s second-largest cryptocurrency exchange by trading volume, is some way off from breaking even in Europe, Zhou said. That timeline depends on when the firm acquires the other licenses it needs.

“We don’t make money under the current MiCA license. But we’re able to afford it because we’re a big entity. For us, it’s a long-term investment,” Zhou said. “It could be five years away, but I think that is a bit long. I would assume we are probably going to be profitable within two years.”

Market consolidation is coming

A MiCA license issued by one country allows a crypto-asset service provider to operate across the European Economic Area (EEA): all 27 members of the European Union, as well as Norway, Iceland and Liechtenstein.

Now is a critical juncture for many small to medium-sized crypto companies in Europe, because the MiCA grandfathering period closes at the end of June. That means firms must have obtained MiCA authorization to operate across the region by July 1 — a cut-off point that is widely expected to be the death knell for many smaller crypto firms.

“There’s going to be market consolidation,” Zhou said. “That’s why these guys are shutting down. Because even if they know they could afford MiCA, they’re like, ‘WTF, I need [MiFID, EMI] to make money, and I need to make a whole lot of investment in compliance infrastructure to be able to be profitable?’”

MiCA itself is undergoing change, with some country regulators calling for tighter, more centralized control and granting increased oversight to bodies such as the European Securities and Markets Authority (ESMA). And when it comes to structured products, ESMA recently reminded crypto firms offering perpetual futures that some of these products may fall outside the rules.

Zhou said Bybit chose a stringent regulator in Austria’s FMA, a decision he said will pay dividends down the line. Each country interprets MiCA differently, he said: “Some countries interpret it as a way to attract new business; some want heavy regulation. So you actually have different levels of strictness.”

As for bringing ESMA into the mix, Bybit is neutral, Zhou said.

“There are talks about a more level playing field,” he said. “But there could be disadvantages. Because when you have a local regulator they are easy to get to. If we have any issues, we just send an email and go to FMA in Vienna. But if everyone’s in Paris, then you have to line up. There are more CASPs, increased bureaucracy, decreased efficiency.”

Crypto World

Could Pepeto Be the Best Crypto to Buy in 2026 While BTC Tests $80K and ETH Holds Above $2,300?

The crypto market just flipped into greed territory for the first time in weeks, and the Fear and Greed Index hitting 60 has every trader asking which token carries the biggest returns from here.

Finding the best crypto to buy in 2026 means looking past coins that already ran and finding entries that still carry distance between where they sit and where they go.

BTC is testing $80,000 with $996 million in weekly ETF inflows, and a presale launched by the mind behind the first Pepe token has gathered more than $9.5 million from wallets that verified the live tools before sending capital.

Bitcoin touched $79,388 on April 22 before pulling back to $77,800 as profit taking hit altcoins harder than the leader.

Weekly ETF inflows reached $996 million with Bitcoin products leading the charge according to 24/7 Wall Street, and growing expectations around the CLARITY Act markup in the Senate added a regulatory tailwind that the market had not priced in.

The rally is real, but the question now is whether the best returns from here come from large caps or from entries that have not hit the open market yet.

Tokens Positioned for the Next Leg of the Recovery

Pepeto

While the market watches BTC test resistance, the best crypto to buy in 2026 might be sitting in a presale most traders have not found yet. Pepeto is a marketplace that turns meme coin trading into a verified ecosystem where every tool runs live and every contract carries a SolidProof audit. It was built by the cofounder who created the original Pepe coin, with 420 trillion supply matching the same token structure that went from zero to billions the first time.

The risk scorer scans contracts for warning signs before capital gets committed, catching scams that move faster than news so the wallet stays protected during fast rotations that follow big BTC moves. PepetoSwap handles zero fee trades across tokens, keeping the full value of each position inside the wallet instead of leaking to platform charges.

178% APY staking layers returns above the presale position, and the expected Binance listing draws closer while that reward compounds. The presale sits at $0.000000186, and more than $9.5 million has been gathered from wallets that ran through the live platform before committing.

The 100x target from one expected Binance debut holds because presale to exchange is the window where every previous crypto fortune started, and the wallets buying now join that group before the crowd pays full price. Visit Pepeto to check the tools live.

Ethereum (ETH)

ETH trades near $2,316 according to CoinMarketCap, holding above $2,300 while BTC leads the rally.

The network still dominates smart contract development with over 31,000 active developers, but ETH needs to reclaim $2,800 before the recovery pattern confirms.

From $2,400 the path to the $4,800 peak is a 2x, solid for a portfolio anchor but far from the multiplier math that presale entries carry ahead of a listing event.

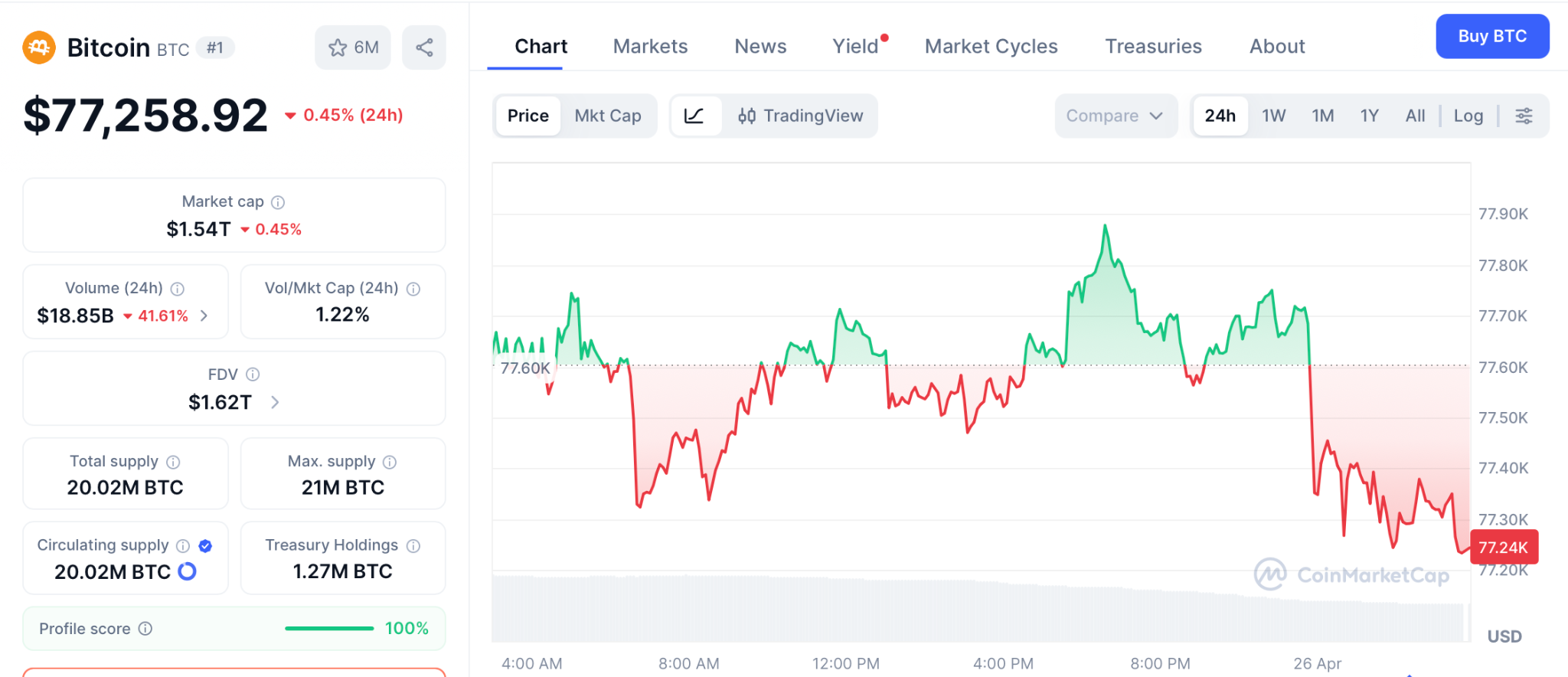

Bitcoin (BTC)

BTC sits near $77,258 according to CoinMarketCap, testing the $80,000 level that has acted as resistance since the pullback from the October 2025 peak of $126,000. Weekly ETF inflows at $996 million show institutional demand is real, and the CLARITY Act could open the door to bigger allocations.

The math from $77,258 to a new high above $126,000 is a 1.6x, strong by traditional standards but modest compared to presale entries that carry 100x projections from a single listing event.

Conclusion

Will BTC break $80,000? The signals point toward higher levels as ETF demand and regulation clarity build across the market. But the signals for Pepeto point at something beyond a market recovery, they point at the same setup that produced every early buyer success story in crypto.

Every cycle creates winners who entered during fear and collected wealth during recovery, and the expected Binance listing will separate the wallets that entered from everyone who reads about them afterward.

Entering the Pepeto official website enow is how those wallets plan to be on the right side of that line when trading opens.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the best crypto to buy in 2026 right now?

BTC and ETH carry strength, but presale entries like Pepeto offer the distance between current price and listing that large caps cannot match.

Why are traders choosing Pepeto over large caps?

A SolidProof audit, zero fee trading, and an expected Binance listing at presale pricing explain why more than $9.5 million entered the Pepeto official website.

Will BTC reach $100,000 this year?

That is a real possibility if ETF inflows continue and the CLARITY Act passes, but the timeline depends on broader market conditions.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

The Ethereum Foundation has moved to unwind part of its staking position shortly after nearing its stated goal of 70,000 staked ETH.

On Saturday, the Ethereum Foundation unstaked 17,035.326 ETH, worth roughly $40 million, according to Arkham data. The move involved depositing wrapped staked ETH (wstETH) into Lido’s unstETH contract, with ETH expected to be returned once the withdrawal queue completes.

In Ethereum, unstaking is the process of withdrawing ETH that was previously locked to help secure the network through validators. When ETH is staked, it’s deposited into the Ethereum Beacon Chain, where it remains locked while earning rewards. To unstake, a withdrawal request is initiated, and the funds enter a queue period after which the funds are released.

The Ethereum Foundation has not yet revealed why it unstaked 17,000 ETH, prompting some users to speculate it could be preparing to sell. “The biggest seller of ETH continues to be the people who created ETH,” one user wrote.

Related: Another DeFi protocol hacked as Sui-based Volo hit by $3.5M exploit

Ethereum Foundation nears 70K staked ETH goal

The EF started staking ETH after updating its policy in June 2025. At the time, the foundation said that staking and decentralized finance participation would help fund protocol research, development and ecosystem grants.

Since February, the foundation has steadily expanded its position, staking 2,016 ETH initially, followed by 22,517 ETH in March. Earlier this month, the foundation staked more than 45,000 ETH in a series of transactions, bringing the total to around 69,500 ETH, just shy of its internal 70,000 ETH staking target.

However, concerns remain over governance risks. Ethereum co-founder Vitalik Buterin has cautioned that large-scale staking by the foundation could complicate neutrality during potential contentious hard forks, where competing chains may emerge.

Related: Ethereum Risks 10% Dip Versus Bitcoin Despite ETH Staking Milestone

DeFi protocols unite to back rsETH

As Cointelegraph reported, decentralized finance protocols have joined forces to stabilize rsETH after a $293 million exploit on the Kelp restaking platform triggered market disruption. The incident involved hackers stealing over 116,000 restaked ETH tokens and using them as collateral to borrow funds, leaving roughly $195 million in bad debt on Aave and straining the broader DeFi lending market.

Backers have pledged over 43,500 ETH (around $101 million) in a coordinated “DeFi United” effort led by Aave, with participation from Lido DAO, Golem Foundation and major contributions from EtherFi Foundation and Mantle.

Magazine: Ethereum’s Fusaka fork explained for dummies: What the hell is PeerDAS?

TLDR:

- Open Interest spiked sharply in April, signaling crowded and unstable positioning across Bitcoin derivatives markets.

- Negative funding rates during the rally confirm shorts are being squeezed out, not that bulls are leading organically.

- Perp CVD is rising while Spot CVD stays flat, proving the current move lacks genuine spot market buying support.

- Bitcoin must hold above $80,000 to target $85,000 — a breakdown below that level reopens significant downside pressure.

Bitcoin short squeeze activity is currently driving prices higher in the cryptocurrency market. The Consumer Price Index rose again recently, pointing to sticky inflation that shows no clear resolution.

Despite this, Bitcoin is pushing into a key resistance zone. Analysts note this is not a one-way market. Mixed scenarios and liquidity moves are expected as conflicting signals continue to play out across the market.

Open Interest Spike Points to Crowded and Fragile Market Conditions

Open Interest in Bitcoin’s derivatives market spiked sharply during April. Market analyst Boris of @Fundingvest described the rapid buildup as aggressive and unhealthy positioning.

Such a surge indicates that positions are becoming deeply crowded. This overcrowding makes the current price move unstable and exposed to sudden and sharp reversals.

After the OI spike, funding rates remained negative even as prices climbed. Negative funding during a price rally is a direct indication of crowded short positioning.

In response, the market pushed prices higher, forcing short sellers to cover their positions. This pattern reflects a textbook short squeeze playing out within the derivatives segment.

Meanwhile, Perpetual CVD has been driving prices higher throughout this period. Spot CVD, however, remained largely flat during the same time frame.

Boris pointed out that this divergence makes the analysis straightforward. The current rally is derivative-driven and lacks support from genuine spot market buying activity.

Without spot market backing, the sustainability of this rally remains questionable. Price increases unsupported by spot buyers tend to be temporary. The liquidity built through the short squeeze may later be used against new long positions. This sets up the next key risk forming in the market.

Long Trap Risk Builds as Shorts Exit and New Longs Enter

As shorts exit under pressure, longs are now beginning to take their place. Boris flagged this transition as a possible setup for a long trap in the coming weeks.

A long trap forms when buyers enter aggressively near highs, only to face a sharp reversal. This cycle is a recurring pattern in Bitcoin’s derivatives-driven market.

Bitcoin’s price structure is also forming a minor Higher High and Higher Low sequence. On the surface, this HH-HL pattern carries a mild bullish reading.

However, Boris outlined two clear scenarios based on where price holds from here. A failure to maintain above $80,000 would open the door to further downside pressure.

Conversely, holding above $80,000 could push Bitcoin toward the next target near $85,000. The $80K level is therefore acting as the market’s key line in the sand.

Traders monitoring this structure will seek confirmation of either a breakdown or continuation. The outcome around this price level may define Bitcoin’s short-term trajectory.

CPI data continues to add uncertainty to an already complicated macro setup. Sticky inflation does not offer a clear directional signal for Bitcoin.

With the current derivatives positioning, the market remains exposed to sharp moves in either direction. Caution and active risk management remain essential for all market participants.

Adam Back, inventor of Hashcash and a pioneering figure in Bitcoin’s early development, has dismantled the new Satoshi Nakamoto documentary by challenging its core technical assumptions about Bitcoin mining patterns and coin ownership.

Back’s detailed response on X points to critical flaws in how the documentary interprets early mining data and the so-called Patoshi pattern used to estimate Satoshi’s holdings.

The Patoshi Pattern Problem

The documentary relies heavily on the Patoshi pattern, a statistical analysis of Bitcoin block timestamps that researchers claim can identify blocks mined by Satoshi. The analysis suggests Satoshi controlled 500,000 to 1 million Bitcoin by mining roughly 20-40% of blocks in Bitcoin’s first year.

Back argues that this analysis is fundamentally unreliable.

“Clearly there were many other miners (60-80% of hashrate or more even in the first year),” Back wrote.

As the Bitcoin network grew and more participants joined, the pattern became increasingly ambiguous and impossible to verify with certainty.

It has been suggested that as miner participation increased over time, attribution became increasingly unclear, with the Patoshi pattern potentially blending into background noise. This implies the documentary may overstate how precisely early mining activity can be linked to specific actors.

The Flawed “Never Sold” Assumption About Satoshi

The documentary’s central claim rests on the assumption that Satoshi never sold a single Bitcoin, which they argue proves the creator is dead.

This narrative hinges on the belief that a living Satoshi would have spent or sold coins given the extraordinary price appreciation from $0 to $100,000 per Bitcoin.

Back challenges this logic directly. He questions whether the Patoshi pattern can actually prove that Satoshi holds all those coins unsold. Even if the pattern correctly identifies Satoshi’s early mining, it does not prove that those specific coins remain untouched.

“If Satoshi sold any, he could have sold from more recent, more ambiguous coins first,” Back argued.

In other words, Satoshi could have strategically liquidated coins from the ambiguous later mining period when the Patoshi pattern becomes unreliable, and attribution becomes impossible.

Timeline Inconsistencies and Technical Flaws

Back also flagged the documentary’s sloppy handling of timeline evidence. He referenced earlier work by Jameson Lopp showing that Hal Finney was running a marathon at the exact moment Satoshi was sending test transactions on the Bitcoin network, a direct contradiction that disqualifies Finney from the theory.

Back described the documentary’s approach as suffering from “Gell-Mann amnesia,” a term referring to the tendency to dismiss contradictory evidence that emerges after an initial theory is proposed. When the Finney timeline objection was raised, the filmmakers simply shifted their claim to include Len Sassaman without addressing why their original evidence failed.

Additionally, the documentary dismisses EU timezone residents based on forum post analysis, then later pivots to naming Sassaman despite these timezone inconsistencies, Back noted.

This pattern suggests the documentary started with a conclusion. It then worked backward to find supporting evidence rather than following evidence to a conclusion.

The C++ and Windows Problems

Back also highlighted the devastating objection raised by Cam and Len Sassaman’s widow. Sassaman did not know C++ and had never owned a Windows machine. Bitcoin’s original code is written in C++, creating a critical technical barrier.

Additionally, Sassaman was a vocal Bitcoin critic during his lifetime, making his secret role as co-creator highly implausible.

What This Means for the Satoshi Mystery

Back’s analysis does not definitively solve the Satoshi mystery, but it does demolish the documentary’s theory piece by piece. His core argument is that early Bitcoin mining data is too ambiguous. The “never sold coins” assumption is unfounded. It cannot support firm conclusions about Satoshi’s identity.

The debate reveals how difficult it is to prove Satoshi’s identity solely through technical forensics. Even the most sophisticated pattern analysis loses precision over time as the number of network participants grows and mining becomes more distributed.

Other candidates, like Nick Szabo, gained renewed discussion following the documentary’s failure. Some researchers suggest the mystery may never be solved unless Satoshi voluntarily reveals themselves or new evidence surfaces.

The post Adam Back Challenges the Biggest Claim About Satoshi’s Bitcoin Holdings appeared first on BeInCrypto.

The Ethereum Foundation has unstaked 17,035.326 ETH, worth about $40 million, shortly after moving close to its 70,000 ETH staking target.

Summary

- Ethereum Foundation unstaked 17,035 ETH worth $40 million after nearing its 70,000 ETH staking target.

- The foundation deposited wstETH into Lido’s unstETH contract and awaits ETH after withdrawal queue completion.

- Market users questioned a possible sale, but the foundation has not explained the transaction yet.

Arkham data showed the transaction on Saturday. The foundation deposited wrapped staked ETH into Lido’s unstETH contract. The ETH will return after the withdrawal queue completes, based on Ethereum’s normal unstaking process.

The Ethereum Foundation began staking ETH after changing its policy in June 2025. The group said staking and DeFi activity would help fund protocol research, development, and ecosystem grants.

Since February, the foundation has increased its staked ETH balance. It started with 2,016 ETH, added 22,517 ETH in March, and later staked more than 45,000 ETH this month.

Those transactions lifted its total staked ETH to about 69,500 ETH. The figure placed the foundation close to its stated 70,000 ETH staking goal before the latest withdrawal.

Unstaking raises market questions

The Ethereum Foundation has not explained why it unstaked over 17,000 ETH. The lack of a public reason led some market users to question whether the ETH could move to exchanges or be sold.

One user wrote, “The biggest seller of ETH continues to be the people who created ETH.” The comment reflected market concern, though no official statement has linked the unstaking move to a sale.

In Ethereum, staking locks ETH to help secure the network through validators. Unstaking starts a withdrawal request, places funds in a queue, and releases ETH after the waiting period ends.

DeFi recovery efforts continue after rsETH exploit

The move also comes as DeFi protocols work to support rsETH after a large Kelp restaking exploit. The incident involved more than 116,000 restaked ETH tokens and left bad debt across lending markets.

Aave has led a DeFi United recovery effort with support from Lido DAO, Golem Foundation, EtherFi Foundation, and Mantle. Backers have pledged more than 43,500 ETH, worth about $101 million, to help stabilize rsETH.

Ethereum co-founder Vitalik Buterin has also warned about risks tied to large foundation staking. He said heavy staking by the foundation could create governance concerns during disputed hard forks.

TLDR:

- Bitcoin surged to $79,447 on April 22 as futures Open Interest expanded by nearly $3 billion.

- Spot Bitcoin ETFs recorded a net outflow of $1.845 billion on the same day BTC hit its peak.

- Open Interest fell from $27.56B to $25.26B between April 22 and 24, confirming position unwinding.

- Dual pressure from spot ETF outflows and futures closures explains why Bitcoin stalled at $79,447.

Bitcoin’s April 22 price surge to nearly $79,447 has drawn renewed scrutiny from on-chain analysts. Data reviewed by CryptoQuant verified analyst Carmelo Alemán points to futures market activity, not spot buying, as the primary driver of the move.

Spot Bitcoin ETFs recorded a net outflow of $1.845 billion on the same day prices peaked. The pattern challenges the narrative that institutional spot demand powered the rally.

Futures Expansion Drove Bitcoin’s Short Squeeze Above $79,000

Open Interest in Bitcoin futures expanded by nearly $3 billion on April 22. That expansion preceded the intraday high of $79,447 recorded that day.

Analysts often associate large OI increases with aggressive positioning in derivatives markets. In this case, the data points to a short squeeze as the mechanism behind the price move.

A short squeeze occurs when rising prices force traders holding short positions to close them. That closing process generates additional buying pressure, pushing prices even higher.

However, this type of rally lacks the organic demand needed to sustain the move. Without spot buyers absorbing supply, the price eventually loses momentum.

The ETF outflow figure of $1.845 billion on April 22 adds weight to that reading. Institutional money was not flowing into spot Bitcoin products during the rally.

Instead, capital was moving out of those vehicles at a notable pace. That divergence between futures activity and spot flows is a critical detail in understanding the move.

Alemán’s analysis concludes that the rally was led by derivatives, not by underlying spot demand. The timing of the ETF outflows, occurring near the peak of the move, further supports that conclusion. The combination of futures-driven price action and simultaneous spot selling created a fragile top.

Open Interest Decline After April 22 Confirmed Position Unwinding

After Bitcoin peaked, Open Interest began to fall sharply in the sessions that followed. OI dropped from $27.56 billion on April 22 to $26.10 billion on April 23, a reduction of $1.46 billion.

It then fell again to $25.26 billion by April 24, shedding another $839 million. Price followed that decline, moving toward the $77,400 area.

By April 25, OI had only decreased by around $230 million, and price movement was minimal. The largest price drops matched the periods of heaviest futures unwinding. That correlation reinforces the view that derivatives positioning was central to the move in both directions.

The dual pressure of spot ETF outflows and futures position closures explains why Bitcoin failed to hold above $79,447. Neither force was acting in isolation. Together, they removed the buying support needed to sustain the rally.

The data available through April 25 remained incomplete, though the trend was already clear. The sequence, futures expansion, short squeeze, ETF outflows, then OI contraction, tells a consistent story. Bitcoin’s April rally was a derivatives event, not a spot-driven breakout.

Crypto World

Coinbase’s John D’Agostino says crypto platform stands alone as industry’s full-service prime broker

Coinbase (COIN) has quietly crossed a threshold that Wall Street would recognize immediately: it has become, by its own definition, the only full-service prime brokerage in crypto.

John D’Agostino, head of strategy at Coinbase Institutional, said the definition of a prime broker still follows a familiar Wall Street checklist: trading, custody, financing, derivatives and cross-margining. In crypto, he added, there’s an extra layer, staking. “If you can do all of those at scale, you’re a prime,” he said.

In equities and fixed income, only a handful of firms, Goldman Sachs (GS), Morgan Stanley (MS) and Bank of America (BAC), truly qualify as full-service primes, D’Agostino said. Smaller brokers can support funds, but they don’t offer the full stack. “A $100 million hedge fund isn’t getting everything from the top tier. They’re piecing it together,” he said. “The big primes do everything.”

Crypto, until recently, worked the same way, just more fragmented. Funds stitched together custody from one provider, derivatives from another, financing elsewhere. “You can synthetically replicate a prime by patching services together,” D’Agostino said. “But Coinbase is the only one doing all of it natively.”

Coinbase is the largest U.S.-based cryptocurrency exchange and a major provider of infrastructure for institutional investors, offering trading, custody and financing services through its Coinbase Institutional unit.

Its flagship platform, Coinbase Prime, bundles these functions into a single system, allowing hedge funds and asset managers to trade, store and finance digital assets under one roof. Prime holds over $350 billion in assets under custody, about 12% of the total crypto market cap, and serves as custodian for more than 80% of U.S. bitcoin and ether ETF assets.

The firm has become a key bridge between traditional finance and crypto markets, serving as custodian for a significant share of U.S. bitcoin and ether (ETH) exchange-traded fund (ETF) assets and operating under a growing regulatory framework, including oversight from New York regulators

Crypto prime brokers provide institutional clients with a bundled suite of services designed to mirror traditional offerings in markets like equities and FX. They help funds manage counterparty risk and access liquidity across fragmented venues. Prominent players include Coinbase Prime, Galaxy Digital (GLXY), FalconX and Anchorage Digital.

Cross-margining

The final piece fell into place in March with the rollout of cross-margining between spot and derivatives positions, allowing market makers and institutional traders to reduce capital requirements by as much as 10% to 20%. “That was the last pillar,” D’Agostino said. “Now we’re a prime by any standard, substitute crypto for any asset class.”

Coinbase’s institutional platform processes roughly $236 billion in quarterly trading volume and supports more than 470 assets across 20-plus blockchains.

Beyond trading and custody, Coinbase runs a $1 billion lending book and what D’Agostino describes as the industry’s largest listed derivatives footprint through its Deribit integration. Its staking business spans 10 to 20 tokens at institutional scale, including dedicated products through Coinbase Asset Management.

“Those are the core components. There are firms doing well in custody, others in derivatives, others in lending,” he said. “No one is solving all of those problems in one place.”

That gap has persisted in part because of crypto’s relative size. At roughly 3% to 5% of global equities and fixed income markets, it remains too small for major banks to fully commit.

D’Agostino instead expects banks and incumbents to partner. “Buy, build or rent,” he said. “Banks will rent. It’s cheaper and smarter to rent the best brand than build a so-so version.”

Longer term, that calculus could change if crypto grows to 20% or 30% of global markets. “Then you’ll see full-scale competition,” D’Agostino said. “But that’s years away.”

For now, the bigger threat isn’t Wall Street, it’s startups. “I’m less concerned about JPMorgan than I am about the next Brian Armstrong,” he added.

Read more: Coinbase, Bybit said to be working together on tokenization, custody and distribution of U.S. stocks

Soaring US stocks face pivotal week of tech-led earnings, Fed meeting

Brad Garlinghouse wins top Harvard business leadership award

Cavaliers vs. Raptors prediction, odds, spread, time: 2026 NBA playoff picks for Sunday

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business7 days ago

Business7 days agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread – Corporette.com

-

Entertainment7 days ago

NBA Analyst Charles Barkley Chimes in on Ice Spice McDonald’s Fiasco

-

Crypto World18 hours ago

Hyperliquid $HYPE Rally Builds Momentum as AI Sector Enters Prove-It Phase

-

Politics6 days ago

Politics6 days agoGary Stevenson delivers timely reminder to register to vote as deadline TODAY

-

Crypto World6 days ago

Bank of Hawai’i (BOH) Q1 2026: Net Income Drops to $57.4M as Net Interest Margin Expands

-

Politics4 days ago

Politics4 days agoMaking troops accountable for war crimes threatens US alliance, ex-SAS colonel warns

-

Politics4 days ago

Politics4 days agoDisabled people challenge government SEND proposals over segregation concerns

-

Business4 days ago

Business4 days agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Politics4 days ago

Politics4 days agoZack Polanski responds to home secretary’s taser threat

-

Politics4 days ago

Politics4 days agoStarmer handler McSweeney to be dragged from shadows by Foreign Affairs Committee

-

Politics4 days ago

Wings Over Scotland | How To Get Away With Crimes

-

Crypto World5 days ago

Crypto World5 days agoFive Value Stocks with Recovery Potential in 2026: PayPal (PYPL), Nike (NKE), and More

-

Crypto World5 days ago

Crypto World5 days agoNew York sues Coinbase, Gemini over prediction market offerings

-

Politics4 days ago

Politics4 days ago‘Iran is still a nuclear threat’

-

Sports3 days ago

Sports3 days agoTim Bradley names the current best in the world: “Better than Inoue and Usyk”

-

Business4 days ago

Business4 days agoHCL Tech share price tank over 9% after weak Q4. JPMorgan, HSBC & 3 others cut target price

-

Crypto World5 days ago

Crypto World5 days agoCrypto’s great hope in Senate’s Clarity Act still has a path to survive tight calendar

-

NewsBeat5 hours ago

NewsBeat5 hours agoLK Bennett closes all stores after entering administration

-

Business4 days ago

Business4 days agoThe Job Benefits Most Men Don’t Know to Negotiate

You must be logged in to post a comment Login