Crypto World

If one trader can force the outcome of a prediction market, it shouldn’t be tradable

As platforms such as Polymarket gain mainstream visibility during U.S. election cycles and major geopolitical events, their prices are increasingly cited as real-time signals of truth. The pitch is seductive: let people put money behind beliefs, and the market will converge on reality faster than polls or pundits. But that promise collapses when a contract creates a financial incentive for someone to change the very outcome it claims to measure.

The problem is not volatility. It is design.

When a forecast becomes a plan

The most extreme example is the assassination market, a contract that pays if a named individual dies by a certain date. Most major platforms do not list anything so explicit. They do not have to. The vulnerability does not require a literal bounty.

It only requires an outcome that a single actor can realistically influence.

Consider a sports-adjacent case: a prop market on whether there will be a pitch invasion during the Super Bowl. A trader takes a large position on “yes,” then runs onto the field. It is not hypothetical. It has happened. That is not a prediction. It is execution.

The same logic extends well beyond sports. Any market that can be resolved by one person taking one action, filing one document, placing one call, triggering one disruption or staging one stunt embeds an incentive to interfere. The contract becomes a script. The trader becomes the author.

In those cases, the platform is not aggregating dispersed information about the world. It is pricing the cost of manipulating it.

Political and event markets carry a higher risk

This vulnerability is not evenly distributed across the prediction universe. It concentrates on thinly traded, event-based or ambiguously resolved contracts. Political and cultural markets are especially exposed because they often hinge on discrete milestones that can be nudged at relatively low cost.

A rumor can be seeded. A minor official can be pressured. A statement can be staged. A chaotic but contained incident can be manufactured. Even when no one follows through, the mere existence of a payout changes incentives.

Retail traders understand this instinctively. They know a market can be correct for the wrong reasons. If participants begin to suspect that outcomes are being engineered, or that thin liquidity allows whales to push prices for narrative effect, the platform stops being a credibility engine and starts looking like a casino with a news overlay.

Trust erodes quietly, then all at once. No serious capital operates in markets where outcomes can be cheaply forced.

“All markets are manipulable” misses the point

The standard defense is that manipulation exists everywhere. Match fixing happens in sports. Insider trading happens in equities. No market is pure.

That confuses possibility with feasibility.

The real question is whether a single participant can realistically manipulate the outcome they are betting on. In professional sports, results depend on dozens of actors under intense scrutiny. Manipulation is possible but costly and distributed.

In a thin event contract tied to a minor trigger, one determined actor may be enough. If the cost of interference is lower than the potential payout, the platform has created a perverse incentive loop.

Discouraging manipulation is not the same as designing against it.

Sports as a structural template

Sports markets are not morally superior. They are structurally harder to corrupt at the individual level. High visibility, layered governance, and complex multi-actor outcomes raise the cost of forcing a result.

That structure should be the template.

It is product integrity

Prediction platforms that want long-term retail trust and eventual institutional respect need a bright-line rule: do not list markets whose outcomes can be cheaply forced by a single participant, and do not list contracts that function as bounties on harm.

If a contract’s payout can reasonably finance the action required to satisfy it, the design is flawed. If resolution depends on ambiguous or easily staged events, the listing should not exist. Engagement metrics are not a substitute for credibility.

The first scandal will define the category

As prediction markets gain visibility in politics and geopolitics, the risks are no longer abstract. The first credible allegation that a contract was based on non-public information, or that an outcome was directly engineered for profit, will not be treated as an isolated incident. It will be framed as proof that these platforms monetize interference with real-world events.

That framing matters. Institutional allocators will not deploy capital into venues where the informational edge may be classified. Skeptical lawmakers will not parse the difference between open-source signal aggregation and private advantage. They will regulate the category as a whole.

The choice is simple. Either platforms impose listing standards that exclude easily enforceable or easily exploitable contracts, or those standards will be imposed externally.

Prediction markets claim to surface the truth. To do that, they must ensure their contracts measure the world rather than reward those who try to rewrite it.

If they fail to draw that line themselves, someone else will draw it for them.

Crypto World

Attacker exploits Resolv USR stablecoin to mint 80 million tokens, cashes out $25M: Resolv Labs

An attacker has successfully exploited the Resolv USR stablecoin protocol, minting 80 million tokens and withdrawing at least $25 million before the depeg.

An attacker has exploited Resolv Labs’ USR stablecoin to mint 80 million tokens, causing the stablecoin to depeg from its $1 peg. The attacker has reportedly cashed out at least $25 million from the exploit, marking a significant security breach for the protocol.

The incident represents a critical failure in Resolv Labs’ token minting controls and represents a major loss for USR holders and the protocol. Stablecoin exploits of this magnitude underscore ongoing risks in DeFi protocols, particularly around access controls and minting mechanisms.

Sources: ResolvLabs on X, PeckShieldAlert on X

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

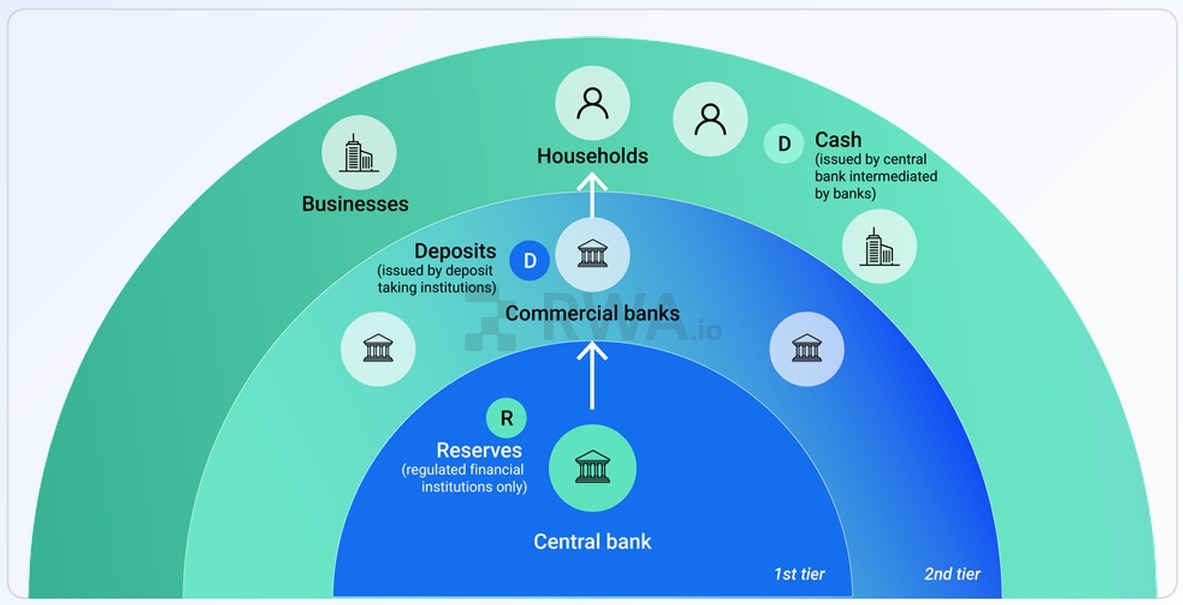

Banks are exploring tokenized deposits as they test ways to move commercial bank money onto blockchain-based payment and settlement infrastructure, according to a new report from real-world asset data platform RWA.io

The report, which was authored by RWA.io with contributions from industry participants including UK Finance, Citi, BNY, JPMorgan’s Kinexys, Standard Chartered, ABN Amro and Digital Asset, argues that tokenized deposits are emerging alongside stablecoins and central bank digital currencies as part of a broader onchain cash stack.

Tokenized deposits are digital representations of traditional bank deposits on blockchain or other distributed ledger infrastructure. Unlike many stablecoins, they are direct liabilities of the issuing bank and sit within existing banking frameworks, including deposit insurance, capital requirements, and Anti-Money Laundering and Know Your Customer rules.

The report points to a growing set of bank pilots and deployments in Europe. In January, Lloyds Banking Group and Archax said they completed the UK’s first public blockchain transaction using tokenized deposits on the Canton Network, while UK Finance’s Great British Tokenised Deposit pilot is testing person-to-person marketplace payments, remortgaging and digital-asset settlement through mid-2026.

The broader push reflects how banks are trying to preserve their role in payments, treasury and deposit-taking as digital cash instruments multiply.

Tokenized deposits as a middle ground in the stablecoin, CBDC debate

UK Finance said in the report that tokenized deposits will play a vital role in a future “multi-money” world. The industry group said tokenized deposits will complement other forms of digital money, “including privately and potentially publicly issued monies.”

Related: BNY launches tokenized deposits amid TradFi rush into blockchain and crypto

Marko Vidrih, the co-founder and chief operating officer at RWA.io said that while much of the attention in digital money focuses on stablecoins or central bank digital currencies (CBDCs), the global financial system still runs on commercial bank money.

“Bringing that money onto digital rails will underpin the next generation of digital finance,” Vidrih said. “For that reason, it is important to understand how tokenized deposits fit within the broader digital money ecosystem alongside stablecoins and CBDCs.”

ECB advances digital euro work, builds tokenized money rails

The European policy backdrop is moving in parallel. The European Central Bank is advancing work on a digital euro as US dollar-backed stablecoins continue to dominate digital asset markets and cross-border transactions.

The ECB recently opened applications for experts to contribute to workstreams focused on how a digital euro would function across ATMs, payment terminals and acceptance infrastructure. The ECB has also said it aims to begin a 12-month pilot for the digital euro in the second half of 2027.

In March, the European Central Bank unveiled Appia, its long-term plan for how tokenized financial markets in Europe could work using central bank money. A key part of that plan is Pontes, a new settlement mechanism designed to let blockchain-based financial platforms connect to the Eurosystem’s existing payment infrastructure.

That existing infrastructure is known as TARGET Services, which already processes large-value euro payments, securities settlement and instant payments across Europe. The ECB said Pontes is scheduled to launch in the third quarter of 2026, while feedback gathered through Appia’s consultation process will help shape the wider framework for Europe’s tokenized financial system.

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

The 2026 split between gold and Bitcoin is being read through the lens of two distinct buyer groups, according to Stephen Coltman, head of macro at 21Shares, a provider of crypto exchange-traded products. While gold has benefited from a sustained wave of central-bank purchases, Bitcoin remains largely a retail asset, with ownership concentrated among individuals rather than institutions. Coltman framed the dynamic as a macro-driven divergence that could persist as fundamentals evolve.

Physical gold has a greater geopolitical strategic role currently, as the asset of choice for state actors who want to store wealth in a way that is protected from rival powers. This has meant that it has traded with greater sensitivity to deteriorating international relations.

On the other hand, Bitcoin’s practical appeal centers on everyday users seeking resilience amid financial stress. Coltman notes that BTC has significant appeal as an alternative lifeline when local banking infrastructure falters or access to the traditional financial system is constrained, a feature that becomes particularly salient during crises. This contrast helps explain why gold and Bitcoin can diverge at the same time, even as investors watch both assets for different kinds of hedging and exposure.

Coltman also highlighted the inverse correlation between BTC and gold, suggesting that investors may benefit from holding both assets to tap into their respective strengths—gold as a strategic reserve and Bitcoin as a mobile, permissionless financial option during disruptions.

Macro forces through most of the last few years pushed gold to a record run, with the precious metal climbing toward near $5,600 per ounce in January 2026. Yet heightened volatility and swift drawdowns pulled prices back to roughly $4,497 per ounce, renewing the debate about gold’s role as a store of value and how it will fare against Bitcoin in the medium term.

Key takeaways

- Gold’s rally has been driven predominantly by central-bank purchasing, while Bitcoin remains more retail-led in ownership and demand.

- The BTC–gold relationship tends to move inversely, suggesting a potential diversification benefit for investors who allocate to both assets.

- January 2026 saw gold scaling multi-decade highs near $5,600/oz, followed by a retreat to around $4,500/oz amid renewed volatility.

- Analysts diverge on the long-term leadership: some see BTC outperforming gold over the next few years, while others argue gold’s reserve-asset status strengthens its staying power.

Two camps on future dominance: BTC versus gold

Among market observers, the tug-of-war between Bitcoin and gold persists as a central theme for the years ahead. Macro economist Lyn Alden contends that Bitcoin is likely to outperform gold over the next three years, arguing that the existing rally in gold could face diminishing returns in the next cycle. As Alden put it in discussions cited in coverage around these views, the pendulum typically swings between the two assets, and heavy gains for gold could temper BTC’s upside in the near term.

But not everyone sees Bitcoin eclipsing gold. Ray Dalio, the famed hedge-fund veteran, maintains that BTC will not replace gold as a store of value. He points to Bitcoin’s exposure to risk-on dynamics and its correlation with technology equities, whereas gold carries entrenched status as a reserve asset within the global banking system. The debate underscores a broader question: which asset better preserves wealth across regimes of stress and monetary policy shifts?

Geopolitics, crises, and the case for 24/7 access

The 2026 period has also underscored the practical differences between the two assets during real-world events. Coltman cited episodes such as the Iran-related conflict, where financial infrastructure and market access in some regions faced disruption. In such moments, the appeal of a global, 24/7 settlement layer—Bitcoin—appears to offer continuity when traditional financial rails are strained. That sense of resilience helps explain why BTC can behave differently from gold in the same geopolitical environment.

The dynamic is not purely academic. In times of stress, gold’s geopolitical role as a state-aligned wealth store remains a stabilizing force for many investors who seek a traditional hedge within a framework of central-bank policy and international relations. Yet Bitcoin’s ability to function as a borderless, permissionless asset during crises adds a complementary edge for those who want an alternative pathway to financial access when banks and payments networks are disrupted.

What to watch next

As macro and geopolitical headwinds evolve, the balance between gold and Bitcoin will hinge on central-bank action, inflation dynamics, and how effectively both assets penetrate different investor cohorts. For traders and portfolio builders, monitoring central-bank balance-sheet trends, currency stability in stressed regions, and the pace of retail adoption for Bitcoin will be essential to gauge which asset gains resilience in the next phase of the cycle. The core tension—whether gold’s reserve role or Bitcoin’s crisis-resilience will lead—remains unresolved, but the ongoing dialogue among analysts signals that both assets will continue to play meaningful, albeit distinct, roles in diversified crypto and traditional portfolios.

Investors should stay alert to shifting macro signals and geopolitical developments, as these factors will continue to shape how gold and Bitcoin interact in 2026 and beyond. The landscape remains uncertain, but the case for a dual exposure—benefiting from the unique strengths of each asset—appears to be a persistent theme for informed market participants.

TLDR:

- Bitmine holds 4.6 million ETH, with 3 million actively staked and generating around $180 million annually.

- Ethereum’s 2.8% staking yield cuts the cost gap, meaning Lee needs only 8–9% more to match Saylor’s offer.

- Bitmine has been acquiring over 60,000 ETH weekly, building a low cost basis ahead of any product launch.

- Unlike Bitcoin, Ethereum’s native protocol yield subsidizes the dividend structure, making the flywheel self-reinforcing.

ETH Stretch may be the next big institutional product to emerge in the crypto market. Bitmine, led by strategist Tom Lee, currently holds 4.6 million ETH.

That figure represents nearly 4% of Ethereum’s total circulating supply. Of that holding, 3 million ETH is actively staked, generating around $180 million per year in protocol rewards.

Analyst Axel Bitblaze recently argued that Lee has the infrastructure to launch a Stretch-style fixed-yield product on this existing base.

Ethereum Staking Yield Creates a Structural Cost Advantage

Michael Saylor’s Stretch product offers a fixed 11.5% yield, with all proceeds going into Bitcoin. This buying pressure has pushed hundreds of millions into BTC each week.

Many credit this as a key reason Bitcoin held above $69,000. Without this demand, some analysts suggest prices would sit near $50,000.

Tom Lee, however, already runs a yield engine that Saylor does not have. Bitmine’s staked ETH generates about 2.8% annually from Ethereum’s protocol.

That income covers part of any fixed dividend Lee would need to pay out. Lee would only need to generate an additional 8–9% to match Saylor’s offer.

Bitblaze noted on X that this cost structure allows Lee to undercut Stretch on yield expenses. That margin could make the product more attractive to institutional capital.

Wall Street typically responds well to yield products with stronger cost profiles. Staking income is a meaningful competitive edge in this space.

Additionally, Bitmine has been buying over 60,000 ETH per week in current market conditions. The firm’s cost basis remains low, and Ethereum sentiment is broadly negative.

Those two factors create a favorable window for any product announcement. A low cost basis combined with native yield strengthens the overall case considerably.

The Ethereum Flywheel and Its Reflexivity Potential

The mechanics of an ETH Stretch product follow a clear and self-reinforcing loop. Every dollar raised would go toward buying more ETH on the open market.

More ETH purchased means more ETH available for staking. More staked ETH then generates additional protocol rewards to help fund the dividend.

This cycle differs from Saylor’s model in one key respect: Ethereum has native yield. Bitcoin has no protocol income, yet the BTC Stretch flywheel has still gained traction.

Ethereum’s staking rewards subsidize the structure from the start. That makes the feedback loop cheaper to run and easier to grow.

Bitblaze argued that Saylor’s flywheel works despite Bitcoin having no yield. Lee’s version, by contrast, would run on Ethereum’s own protocol income.

That distinction changes the product economics entirely. A yield-backed demand engine does not rely solely on price appreciation. It draws strength directly from the Ethereum protocol itself.

Should Lee announce such a product while sentiment is low, the price response could be rapid. Institutional capital targeting yield would flow in, driving ETH demand higher.

Higher ETH prices improve staking returns in dollar terms, attracting still more capital. That loop, once active, tends to accelerate.

Crypto World

Ethereum Price Prediction: ETH Price Could Reach $2,500 as BNB Weakens and Pepeto Shows the Utility Gains That Matter

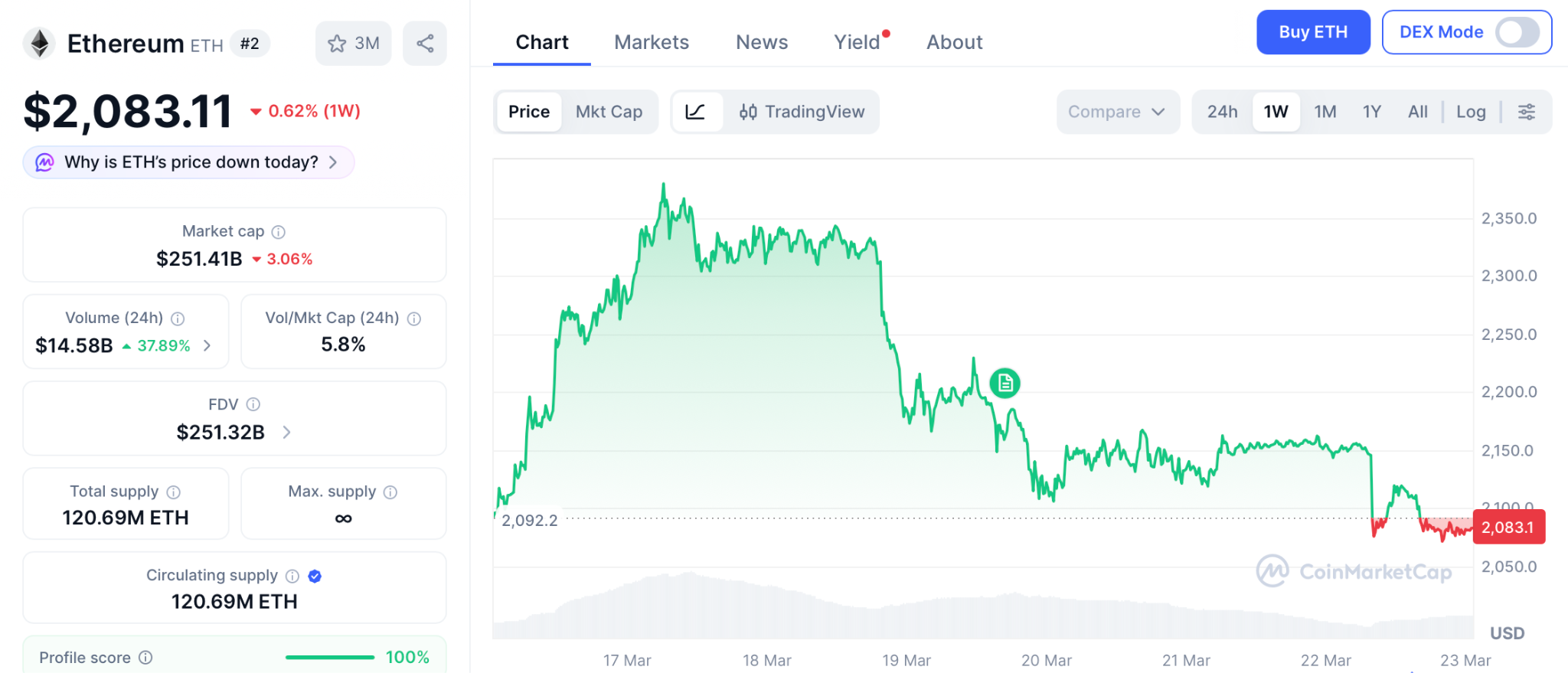

BlackRock launched the iShares Staked Ethereum Trust on March 12, and the fund pulled in $254 million in its first week, making it the fastest growing crypto ETF this quarter.

While the ethereum price prediction shows a path toward $2,500, Pepeto is drawing attention with exchange infrastructure already live, more than $8 million raised, and a Binance listing approaching. The wallets entering now are targeting returns the ethereum price prediction needs the full cycle to deliver.

Ethereum Price Prediction Gains Support After BlackRock Staked ETF Pulls $254 Million in One Week

BlackRock launched ETHB on March 12 on Nasdaq, staking 70% to 95% of its Ethereum holdings and paying investors roughly 82% of staking rewards through monthly payouts, according to CoinDesk.

The fund reached $254 million in assets within seven days, according to Decrypt. Goldman Sachs reported over $1 billion in Ethereum ETF holdings, and Larry Fink called blockchain infrastructure necessary at Davos this year.

The ethereum price prediction has institutional money behind it, but from $2,083 the path to $2,500 is a 20% move that takes patience.

Ethereum Price Prediction and the Presale Offering Returns ETH Cannot Match

Pepeto

As rug pulls grow more common, the cost of entering a project without checking its contracts keeps rising. Every cycle, traders lose more capital to scams that grow harder to detect with each new method. Doing your own research takes hours most people do not have, and it still misses the risks buried in smart contract code.

Pepeto was designed to end that problem before your money is at risk. The exchange is already running while the presale fills. The risk scorer examines every contract for hidden traps and scam patterns, giving you a clear answer in seconds instead of hours of digging through code, so you act with confidence instead of guessing.

The cofounder who took the original Pepe coin to $11 billion with nothing is now building an exchange with zero fee trading, cross chain transfers at zero cost through the bridge, and a SolidProof audit completed before the presale opened. A former Binance expert is on the dev team, 195% APY staking compounds in wallets that positioned early, and the presale has crossed more than $8 million with the Binance listing approaching.

At $0.000000186 with the same 420 trillion supply that reached $11 billion under Pepe, matching that market cap is over 150x, and Pepeto has the exchange infrastructure Pepe never built. The wallets filling the presale are taking the entry that disappears the moment trading begins, and the holders who are not inside yet are the ones who will spend this cycle wishing they had moved.

Ethereum Price Prediction: Can ETH Reach $2,500 With BlackRock Leading Institutional Demand?

ETH trades near $2,083 as of March 22, holding above the $2,000 support that formed a floor since mid February, according to CoinMarketCap.

BlackRock’s ETHA holds $6.5 billion and the new staked ETHB already sits at $254 million after one week. Resistance levels form at $2,235 and $2,380, and if both break cleanly the next ethereum price prediction target is $2,500.

Losing $2,000 could trigger a pullback toward $1,800. Even the bullish $2,500 scenario is a 20% move from current prices, a return that requires months of positive conditions and institutional follow through.

BNB

BNB trades near $631 as of March 22, steady despite the broader correction, according to CoinMarketCap. The Binance ecosystem keeps BNB supported, but from $631 the token needs to reclaim $720 before any meaningful run begins.

A 2x requires BNB above $1,200, a level it has never held. Neither the ethereum price prediction nor BNB delivers the distance a presale to exchange listing compresses into the moment trading opens.

Ethereum Price Prediction Points to $2,500 but the Presale Entry Points to Where Wealth Was Built

The ethereum price prediction has BlackRock behind it, the staked ETF is pulling institutional money, and the $2,500 target is realistic. But the smart money wallets filling Pepeto at presale pricing are building positions that expect returns ETH from $2,090 takes years to match.

The crypto news will cover this moment after the Binance listing, and the only question is whether you lock in your position on the Pepeto official website today or pay a higher price later from wallets that moved while you were still reading about ETH.

BlackRock is staking ETH for 3% yield. The wallets inside Pepeto are targeting 150x, decide which return fits this cycle.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the ethereum price prediction for today?

The ethereum price prediction targets $2,500 if ETH holds above $2,000 support. Investors seeking faster returns are looking at Pepeto, where matching Pepe’s market cap is over 150x from presale.

Why is Pepeto trending alongside the ethereum price prediction?

Pepeto has become the presale drawing the most capital because it combines a working exchange with the same supply that took Pepe to $11 billion, positioning it for returns ETH cannot match from $2,083.

How does the ethereum price prediction compare with early presales like Pepeto?

The Pepeto official website offers a presale where the Binance listing compresses the return window into days, while the ethereum price prediction from $2,083 to $2,500 is a 20% move requiring months.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

TLDR:

- Trump issues 48-hour ultimatum demanding Iran reopen the Strait or face power plant strikes.

- Iran warns of full closure of the Strait and retaliation against regional energy infrastructure.

- Tanker traffic dropped 90%, increasing concerns over global oil supply and market stability.

- Iranian officials list potential targets, including Israel and US-linked energy assets.

Iran war live Trump Strait of Hormuz tensions intensified after a 48-hour ultimatum triggered threats of energy infrastructure attacks, raising risks of wider regional escalation and disruption to global oil transit routes.

Trump Issues 48-Hour Ultimatum

The United States has issued a direct warning to Tehran. In his statement, President Donald Trump demanded that Iran fully reopen the Strait within 48 hours.

He threatened attacks on major Iranian power plants if the demand is ignored. The ultimatum highlighted the strategic significance of the Strait of Hormuz, through which a significant portion of global oil shipments pass.

Tanker traffic has already fallen by nearly 90% in recent weeks, raising concerns about energy supply disruptions worldwide.

Trump’s statement did not clarify whether nuclear-linked power plants, such as Bushehr, would be included in the strike. This uncertainty added to regional tension, as the potential for collateral damage remains high.

“If Iran doesn’t FULLY OPEN the Strait, the US will hit major power plants first,” Trump’s statement read, reflecting the firm deadline.

Iran Warns of Retaliation and Regional Impact

Iranian officials outlined a detailed response as spokesperson Ebrahim Zolfaghari confirmed that the Strait remains partially open under controlled access. He however, warned that any strike on power plants would trigger immediate retaliation.

Iran indicated that a full closure of the Strait would follow any attack, with reopening dependent on reconstruction of damaged infrastructure.

Officials also listed potential regional targets, including power plants in Israel, companies with American shareholders, and energy infrastructure in countries hosting US bases.

Iran’s parliament speaker, Mohammad Bagher Ghalibaf, further emphasized the scale of potential consequences. He warned that attacks on Iranian infrastructure could lead to the irreversible destruction of energy networks across the Gulf, maintaining elevated oil prices for an extended period.

Previous demonstrations of Iran’s reach, such as the strike on Qatar’s Ras Laffan LNG terminal, showed the country’s capability to disrupt regional energy systems.

Regional and international actors are monitoring the situation closely, highlighting the strategic and economic stakes.

Iran war live Trump Strait of Hormuz tensions remain critical as the 48-hour deadline approaches, with both sides maintaining firm positions and regional stability at stake.

The divergence between gold and Bitcoin (BTC) in 2026 can be explained by two distinct segments of buyers, according to Stephen Coltman, head of macro at crypto exchange-traded product (ETP) provider 21Shares.

Gold’s rally over the last three years has been primarily fueled by central bank buying, while Bitcoin is more widely held by individuals than financial institutions, Coltman told Cointelegraph. He said:

“Physical gold has a greater geopolitical strategic role currently, as the asset of choice for state actors who want to store wealth in a way that is protected from rival powers. This has meant that it has traded with greater sensitivity to deteriorating international relations.”

However, BTC has more utility for individuals who may use it as an alternative “lifeline” when local banking infrastructure fails during times of crisis, and accessing the traditional financial system is not possible.

“Shortly after the conflict started, both the Dubai and Abu Dhabi exchanges were shut down following missile and drone strikes from Iran,” which, he said, is a “stark reminder” of how valuable 24/7 access is in wartime situations or other emergencies.

Coltman told Cointelegraph that the inverse correlation between BTC and gold means that investors should hold both to benefit from each asset’s unique properties.

Ongoing macroeconomic and geopolitical shocks over the last several years drove gold to an all-time high of nearly $5,600 per ounce in January 2026.

However, heightened volatility dragged the precious metal back down to about $4,497 per ounce, leading to renewed debate among analysts about gold’s role as a store of value asset, and how it will perform against Bitcoin in the coming years.

Related: Bitcoin vs gold shows potential bottom signals as BTC bulls defend $70K

Financial analysts are split on gold versus BTC dominance

Bitcoin is likely to outperform gold over the next three years, according to macroeconomist Lyn Alden.

“It’s usually a pendulum between the two. If gold has gone up as much as it did, the entire diminishing return story per cycle is going to be erased in the coming one, too,” Alden said.

However, former hedge fund manager Ray Dalio expects that BTC will never replace gold as a store-of-value asset because it still trades like a risk-on asset with correlation to technology stocks, while gold is entrenched as a reserve asset in the banking system.

Magazine: Is China hoarding gold so yuan becomes global reserve instead of USD?

Crypto World

Hyperliquid Surpasses 218,000 Active Traders as Crude Oil Perpetuals Hit $300 Million Open Interest

TLDR:

- Hyperliquid’s active perpetual traders reached 218,340, marking a fresh local high with a 2.14% 24-hour gain.

- Crude oil perpetuals crossed $300M in open interest, overtaking every crypto and equity pair on Hyperliquid.

- Hyperliquid’s HIP-3 markets surpassed $1.43B in total open interest as platform activity hit an all-time high.

- Real-world assets including commodities, stocks, ETFs, and FX now account for roughly 30% of platform volume.

Hyperliquid is recording fresh activity highs across its perpetual trading platform in 2025. Active perpetual traders have reached 218,340, marking a new local high with a 24-hour gain of 2.14%.

Simultaneously, crude oil perpetuals on the platform have crossed $300 million in open interest. This figure places crude oil above every crypto and equity pair on the exchange.

Together, these numbers reflect a platform experiencing steady and measurable expansion this year.

Hyperliquid Trader Activity Recovers and Pushes Into New Territory

Hyperliquid’s active trader count has followed a notable recovery path over recent months. The platform peaked around November before pulling back sharply into January, dropping to roughly 150,000 active traders. That kind of reset typically stalls momentum on most trading platforms.

However, Hyperliquid began climbing again from late January onward. Since then, participation has moved steadily higher, reclaiming previous levels along the way. The platform has now pushed past its earlier highs into fresh territory.

According to data shared by Hyperliquid Hub on X, the platform went from around 127,000 traders in August to over 218,000 today.

That represents a broad expansion in user activity within less than a year. The growth has been gradual rather than driven by a single spike.

The post further noted a reinforcing dynamic: more traders bring more liquidity, which tightens spreads and improves execution.

Better execution, in turn, draws additional traders to the platform. This cycle has been building steadily through 2025 and continues to gain traction.

Crude Oil Perpetuals Lead Platform as Real-World Assets Drive Volume

Crude oil perpetuals have emerged as the largest market on Hyperliquid by open interest. The $300 million figure surpasses all crypto and equity pairs currently listed on the exchange. This development was reported by Delphi Digital and reflects a shift in what traders are engaging with.

Real-world assets, including commodities, stocks, ETFs, and foreign exchange pairs, now account for approximately 30% of overall platform volume.

That share represents a meaningful portion of activity. The growth of non-crypto markets on the platform has been a defining trend this year.

Hyperliquid’s HIP-3 markets have also crossed $1.43 billion in total open interest across all listed pairs. Active traders reached a new all-time high alongside this open interest figure. Both metrics moved higher together, suggesting broad participation rather than concentrated positioning.

The expansion into real-world assets marks a broader shift in how the platform is being used. Traders are no longer limited to crypto pairs when using Hyperliquid. The platform’s range of markets has grown, and so has the volume flowing through them.

Bitcoin (BTC) traded just below the $69,000 mark as traders braced for a pivotal weekly candle close, with prices hovering near the long-term line around $68,300. After a weekend slide, the setup underscores a tug-of-war between a fragile near-term outlook and the possibility of a contrarian move, even as analysts debate the significance of a fresh technical signal.

Historically, the 200-week exponential moving average has anchored multi-year cycles, but this year its reliability has been questioned. Cointelegraph has noted that the long-term EMA has failed to act as a clear support in 2026, complicating investor expectations for a durable bottom or renewed upside. As BTC approached the $68,300 region, traders watched to see whether the weekly close would restore any confidence in the metric or amplify the lingering bearish bias.

Key takeaways

-

Bitcoin remained under $69,000, testing the 200-week EMA near $68,300 as a critical reference point for the weekly close.

-

Market psychology tilted toward caution, with substantial liquidations signaling risk-off dynamics over the past 24 hours.

-

A fresh bullish tempo appeared with a golden cross developing between the 21-day and 50-day moving averages, but durability remains uncertain.

-

Analysts split on the path forward: some warn of continued macro downside even as near-term momentum offers a potential relief rally.

Weekend test of the long-term line

Trading data show BTC price action around the 200-week trend line, a level that has historically framed major cycles even as the asset wobbled through the weekend. The immediate vicinity of $68,300 serves as a focal point for whether bulls can sustain a bid above entrenched resistance or if sellers reassert control as the weekly close approaches.

Extended downside pressure in the days leading into the close produced notable liquidations across the market. CoinGlass reported that more than $300 million in long positions were liquidated, with roughly $100 million in shorts also liquidating in the same window. The liquidation profile underscores a risk-off environment in which traders are shrinking risk exposure into key technical junctures.

From a chart perspective, BTC’s motion around the 200-week EMA has reinvigorated debate about whether this line can again offer a meaningful foothold. In a broader 2026 context, some analysts have warned that the EMA’s traditional role as a durable support may be waning, complicating the interpretation of daily moves around this level.

Liquidity pressure and trader sentiment

The weekend action underscored a broader mood among market participants: risk appetite remains fragile as macro uncertainties persist. With a large portion of the futures market liquidated into the close, traders may adopt a cautious stance, awaiting a clearer directional cue from the weekly close and any subsequent macro catalysts.

In such a regime, the key question is whether the counter-move, if it occurs, can sustain momentum beyond a relief rally. The balance between safe-haven flows and renewed appetite for risk will likely define BTC’s trajectory over the coming sessions, particularly as market participants await more concrete signals from on-chain data, derivatives activity, and broader market liquidity conditions.

Momentum flicker: the Golden Cross and what it may imply

On the technical front, a visible positive signal emerged as the 21-day simple moving average crossed above the 50-day moving average, a formation often interpreted as a short-term momentum cue. Proponents of the setup cautioned that the cross could herald a temporary lift, though they emphasized that durability would hinge on subsequent price action.

Keith Alan, cofounder of trading resource Material Indicators, commented on the potential implications, saying the Golden Cross “will likely deliver some short term bullish momentum. Must watch to see if it develops into something durable.” He added a more cautious note, reflecting the prevailing sentiment: “For now…the range game continues.”

These near-term signals come after March saw two “death crosses” on BTC’s daily chart, a pattern historically associated with renewed downside pressure. The market’s interpretation of a Golden Cross in the current environment remains mixed: a possible spark for a bounce, but no guarantee of a sustained breakout without follow-through from higher timeframes.

Bearish undertones persist in higher timeframes

Several well-known traders have stressed that longer-horizon momentum remains skewed to the downside. A prominent analyst reiterated a bearish thesis for the macro cycle, highlighting ongoing fragility in higher timeframes despite any short-term bullish cues. The tension between near-term momentum signals and longer-term risk remains a defining feature of the BTC narrative as the market approaches another pivotal weekly close.

“There are still 0 signs of bear market exhaustion on HTF. No divs, no bear PA exhaustion, no momentum loss, etc.” He also noted a continued outlook for lower prices, saying, “I still have high confidence in seeing 50k and likely a bit lower.”

That sentiment sits alongside reminders from earlier periods that the market can swing on a few data points, even as long-run structural factors weigh on price discovery. The debate over whether BTC can muster a sustained recovery or slide toward new macro-driven lows remains unresolved, with bulls awaiting confirmation from price action and bears watching for any renewed downside momentum.

What readers should watch next

The immediate focus for BTC markets is the weekly candle close and how price behaves in the aftermath. If the price can hold above key support near the 200-week EMA and demonstrate follow-through above near-term moving averages, a cautious upside tilt could emerge. Conversely, failure to defend the region around $68,000–$68,300 may invite renewed selling pressure and retesting of lower support bands.

Investors should also monitor liquidity patterns and derivatives activity as they often foreshadow the next directional move. In addition, traders will be paying close attention to any shifts in macro sentiment or changes in the risk-on/risk-off appetite that can influence Bitcoin’s risk premium and its correlation with broader markets.

This ongoing narrative—between a fragile near-term bounce and the weight of higher-timeframe bears—will likely shape price action in the weeks ahead. As always, readers are advised to conduct their own research and consider how these developments fit their risk tolerance and investment horizon.

TLDR:

- BTC dominance has been ranging between 58% and 60% for months and is now approaching the critical 58% range low.

- Analyst CryptoCandy24x expects a rotation back to 60% or higher if BTC dominance holds firmly above the 58% boundary.

A CME gap at 70.1K remains unfilled, with analysts watching for a potential rejection that could push Bitcoin toward 66K. - Analyst maintains a short position, warning that Bitcoin’s structure stays bearish while price trades below the 71.4K level.

BTC dominance is nearing the 58% range low as Bitcoin’s price holds around $67,922, drawing attention from analysts across the market.

The metric has been cycling between 58% and 60% for months, and its latest move toward the lower boundary is happening alongside a key CME gap sitting at 70.1K.

Traders are now watching both developments closely, as the outcome of each could shape Bitcoin’s short-term price direction in the days ahead.

BTC Dominance Tests Critical Support at 58%

BTC dominance has been trapped in a defined range between 58% and 60% for several months. The metric has repeatedly rotated from the range high to the range low without breaking in either direction.

This prolonged consolidation has kept traders on alert for any sign of a decisive move. The current approach toward 58% is now putting that lower boundary under renewed pressure.

Analyst @cryptocandy24x noted that BTC dominance is once again approaching the range low near 58%. According to the analyst, if the current momentum holds, a rotation back toward the 60% range high is possible in the coming days.

However, this outlook only remains valid as long as BTC dominance holds above the 58% level. A confirmed breakdown below that mark would shift the bias in a different direction entirely.

A hold at 58% would suggest Bitcoin is maintaining its market share against altcoins. If dominance bounces from this level, it would align with the analyst’s expectation of a return toward 60% or higher.

On the other hand, a drop below 58% could signal growing altcoin strength across the broader market. The next few sessions will be telling as to which scenario plays out.

CME Gap at 70.1K Adds Pressure to Bitcoin’s Short-Term Outlook

While BTC dominance tests its range low, Bitcoin’s price is also facing a notable technical setup overhead. The CME closed at 70.1K, leaving a gap below the close that the market has yet to address.

Gaps of this nature have historically shown a strong tendency to get filled at some point. This makes the 70.1K level a significant reference point for traders planning their next moves.

Analyst @KillaXBT provided an update on how Bitcoin’s structure is developing around these key levels. The analyst noted that a push toward the CME gap, followed by a rejection, could lead to a retest of the 66K level next week.

KillaXBT also confirmed that the broader structure remains bearish while Bitcoin stays below 71.4K. The analyst noted they remain short and are tracking how price reacts at these zones.

A gap fill at 70.1K followed by a strong rejection would add more weight to the bearish case currently building. Traders are therefore watching for entry signals around that level ahead of any potential downside continuation.

The 66K area, meanwhile, stands as the next key support zone if selling pressure resumes. Until Bitcoin reclaims 71.4K, the market structure continues to favor the downside.

If you want to have good governance, you cannot be in a yes-sir mode: Sashidhar Jagdishan

Attacker exploits Resolv USR stablecoin to mint 80 million tokens, cashes out $25M: Resolv Labs

Koneru Humpy Withdraws From FIDE Women’s Candidates Tournament Owing To West Asia Conflict

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics2 days ago

Politics2 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Tech5 days ago

Tech5 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Crypto World1 day ago

Crypto World1 day agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World2 days ago

Crypto World2 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

News Videos4 days ago

News Videos4 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World1 day ago

Crypto World1 day agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Business7 days ago

Business7 days agoAustralian shares drop as Iran war enters third week

-

Crypto World7 days ago

Crypto World7 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Politics5 days ago

Politics5 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Fashion7 days ago

Fashion7 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

Tech3 days ago

Tech3 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Politics5 days ago

Politics5 days agoReal-time pollution monitoring calls after boy nearly dies

-

Crypto World4 days ago

Crypto World4 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

NewsBeat4 days ago

NewsBeat4 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

Business6 days ago

Business6 days agoMeta planning major layoffs as AI spending and automation reshape workforce

-

News Videos4 days ago

News Videos4 days agoPARLIAMENT OF MALAWI – PAC MEETING WITH REGISTRAR OF FINANCIAL ON AMARYLLIS HOTEL – INQUIRY LIVE

-

Business8 hours ago

Business8 hours agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Entertainment7 days ago

Oscars reunite Rob Reiner supergroup of 17 stars for emotional tribute: Here's who appeared on stage

-

Business4 days ago

Business4 days agoWho Was Alex Pretti? 5 Key Facts About the ICU Nurse Killed by Federal Agents in Minneapolis

You must be logged in to post a comment Login