Crypto World

Inside Coinbase’s push to bring prediction markets on chain and on venue

Coinbase is folding regulated prediction markets into its “everything exchange” vision, using The Clearing Company to clear on‑chain event contracts beside crypto and stocks.

Summary

- Coinbase is moving prediction markets from a Kalshi integration toward an on‑chain, in‑house stack after acquiring The Clearing Company, aiming to keep them inside a regulated perimeter.

- In Europe, financial‑underlying prediction markets fall under MiFID while politics and sports are pushed into fragmented national gambling regimes, leaving most current on‑chain volume in regulatory limbo.

- Coinbase is already experimenting with cross‑margining via perpetual futures and sees long‑term scope to extend collateral efficiency across prediction markets, crypto, and tokenized assets on a single venue.

Coinbase’s push to become an “everything exchange” will increasingly run through regulated prediction markets rather than just spot crypto, according to Côme Prost‑Boucle, the exchange’s head of international listings, speaking with crypto.news at ETHGlobal Cannes on March 31.

For Prost‑Boucle, prediction markets are not a novelty bolt‑on. They sit at the core of Coinbase’s plan to become what he calls an “everything exchange.” “The whole strategy is pretty simple,” he told crypto.news.

“We want to build the everything exchange with Coinbase, meaning that we want to bring under one regulated umbrella all of the asset classes that you can imagine and offer this to both our retail customers and our institutional customers.”

Coinbase leading the way to become an ‘Everything Exchange’

That umbrella now stretches beyond spot crypto into derivatives, options, tokenized stocks and equities, token sales and, crucially, event‑based contracts that let users trade on future outcomes. “We have this whole breadth of different products that we’re bringing into one umbrella, which is Coinbase,” he said. “Our goal is to push this to as many users as possible across the world, and the reaction has been pretty tremendous so far.”

Coinbase’s debut in prediction markets was deliberately conservative. The initial launch in the U.S. leaned on Kalshi, the CFTC‑regulated event‑contract venue, giving the product an immediate regulatory backbone but also clear constraints on geography and design.

“The first iteration of the product is available in the US and in a couple of regions, but for instance, it’s not available in Europe because of lack of regulatory clarity,” Prost‑Boucle said. That version effectively pipes Kalshi’s markets into the Coinbase interface, letting users trade small‑ticket contracts on elections, sports, macro data and other real‑world events while staying inside a U.S. event‑contract framework.

The second phase is more aggressive. In December, Coinbase agreed to acquire The Clearing Company, a specialist prediction‑market clearing startup with roots in the existing event‑contract ecosystem.

Prost‑Boucle referred to it in the interview as “a company called The Clearing House,” but the strategic intent is clear. “The goal is for us to bring these capacities internally so that we can develop this product on chain and we can develop with the DNA that we have to bring all asset classes on chain,” he said. In effect, Coinbase is moving from renting regulated rails to owning the clearing and risk stack, and then pushing more of the lifecycle on‑chain while staying within the event‑contract perimeter. That stands in contrast to crypto‑native venues such as Polymarket, which prioritizes unconstrained on‑chain liquidity first and only later began to grapple with regulatory structure.

Prediction markets dominate conversation at ETHGlobal

If prediction markets are to sit alongside crypto, derivatives and tokenized stocks in a single app, collateral efficiency will determine whether users actually route meaningful size through Coinbase. Here, Prost‑Boucle says institutional desks are already applying pressure. “That’s also something that institutional clients have been pushing for,” he noted when asked about cross‑margining prediction markets with other Coinbase products. “We’re currently doing cross‑margining for our perpetual futures product, and that’s something that our institutional clients have been craving,” he added, pointing to demand for “always‑on exposure possibilities, weekend hedging, all of this that perpetual futures have as internal features.” The logical goal is to have a single collateral pool backing BTC perpetuals, tokenized equity and a portfolio of geopolitical or macro event contracts, rather than trapping capital in isolated silos across venues. “At the moment we’re working on this product,” he said of cross‑margining, “but I think that’s a good vision for us in the longer term—to have cross‑margining across the different asset classes, I guess.”

The main structural obstacle to that vision is Europe. “Prediction markets in the EU are pretty difficult to apprehend because there’s no unified regulatory framework,” Prost‑Boucle said. “It all depends on what you have as an underlying asset.” He draws a sharp line that mirrors emerging legal commentary: a contract on the future price of Bitcoin is treated as a financial derivative under MiFID, while a contract on an election or football match is pushed into gambling. “If the contract lies on a financial underlying asset, that would be regulated by MiFID,” he explained. “But all of the other classes, where currently all of the volumes are—on politics, on sports, this would be regulated under gambling laws in Europe.”

That split leaves most of today’s on‑chain volume—heavily skewed toward politics and sports—in regulatory limbo from the perspective of a regulated exchange. Any operator that wants to offer political or sports markets across the bloc has to navigate a patchwork of national gambling regimes, each with its own licensing, consumer rules and, in some cases, state monopolies. “It means you would have to go for every single European gambling law, because there is no unified regulatory framework,” Prost‑Boucle said. “These laws are pretty national, they’re quite country‑specific and they’re quite hard to get.” Despite that, he is not writing off the region. “I guess we’re still hopeful that at some point we’re going to have regulatory clarity on prediction markets and a better structure in Europe that enables this type of contract to flourish as well,” he said.

Beyond trading revenues, Coinbase clearly sees prediction markets as an information layer that competes with polling, research, and even traditional media. Prost‑Boucle points to cases in the U.S. where broadcasters are already embedding live market odds, such as CNBC, CNN, the Dow Jones and other media recently integrating Polymarket odds into the ‘traditional’ newscycle.

That, in turn, brings the problem of truth into focus. Once markets start pricing geopolitics, conflicts, and leadership changes, disputes over what actually happened can become payout disputes. That means oracles used to resolve contracts may be facing increasing scrutiny from not only bettors, but also regulators.

Prost‑Boucle argues that most of the damage begins with poor contract design. “It’s crucial when you enter a contract to look at what the event criteria are,” he said. “Obviously you want to diversify sources of truth and have kind of fixed criteria to make sure there is no ambiguity when an event like this happens,” he added. Asked whether AI agents could help by aggregating across outlets and delivering a consolidated verdict, he is open but cautious. “Potentially, AI could be helping with sorting out across different sources‑of‑truth venues and making sure that we have a consolidated view and a fixed view that is not biased by any specific media or even a group of people,” he said.

For now, Coinbase’s approach is less about chasing the wildest version of prediction markets and more about proving they can live inside the same rule‑set as everything else on the platform: keep them in a regulated perimeter, pull clearing and risk in‑house via The Clearing Company, and wire the whole thing into a broader multi‑asset venue where collateral actually earns its keep across products. As Brian Armstrong has put it in other contexts, Coinbase wants to be “the most trusted bridge” into the crypto economy, and in that frame, everything else—from MiFID hair‑splitting in Brussels to the next generation of AI‑driven oracles—is just another set of constraints to engineer around, not a reason to sit out a market.

US Federal Reserve Governor Michael Barr said Tuesday that clearer US stablecoin rules could speed the market’s growth, but warned that regulators still need to address money laundering risks, bank run risks and consumer safeguards as they implement the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act.

Speaking at a Federalist Society event on stablecoin regulation, Barr said the law provides “needed clarity” for issuers, but that “a great deal will depend on how federal and state regulators implement the statute.”

Barr said stablecoins are still used mainly for crypto trading and as a US dollar store of value in some foreign markets, though they could also lower remittance costs, speed up trade finance processing and help firms manage treasury operations. He also highlighted the risk of bad actors buying stablecoins in secondary markets without identity checks, and said issuers may be tempted to stretch for yield in reserve assets in ways that undermine confidence during stress.

Barr’s speech also cast the stablecoin debate in historical terms. He said private money has a “long and painful history” when safeguards are weak, pointing to the Free Banking Era in the US, the Panic of 1907, money market fund stress during the global financial crisis and COVID-19 shock, and more recent stablecoin valuation pressure as reasons to be cautious about any asset marketed as redeemable at par on demand.

Barr’s remarks come as US agencies move from legislation to rule-writing. The US Treasury Department opened a second round of public comment on implementing the GENIUS Act in September 2025, saying the law must be translated into rules that both encourage innovation and address illicit finance, consumer protections and financial stability risks.

Fed Vice Chair for Supervision Michelle Bowman told lawmakers in February that banking regulators were already working on capital and liquidity rules for stablecoin issuers, and Federal Deposit Insurance Corporation chair Travis Hill said in March that the agency does not expect stablecoins to receive deposit insurance under the law.

Related: Who gets the yield? CLARITY Act becomes fight over onchain dollars

Barr warns GENIUS Act rollout will test stablecoin safeguards

Barr’s speech signals where the implementation fights may land. He flagged reserve asset rules, regulatory arbitrage, the scope of issuer activities beyond issuance, capital and liquidity requirements, Anti-Money Laundering (AML) checks and consumer protection standards as the key issues still to be settled.

The GENIUS Act, signed into law on July 18, 2025, created a federal framework for payment stablecoins in the United States. The law requires issuers to maintain one-to-one backing with reserve assets such as US dollars and Treasury bills, and is expected to take effect 18 months after signing or 120 days after final agency rules are completed.

Magazine: How crypto laws changed in 2025 — and how they’ll change in 2026

Crypto World

tZERO and Stobox Sign MOU to Connect Tokenized Securities with Regulated Trading Markets

TLDR:

- tZERO and Stobox signed an MOU to connect tokenization infrastructure with regulated secondary market access.

- Stobox holds a VASP license in Europe and supports compliant exempt securities offerings across the United States.

- tZERO operates a regulated broker-dealer and ATS providing custody, trading, and settlement for digital asset securities.

- Both firms plan to explore expanded opportunities as Stobox grows its global footprint in tokenized asset markets.

tZERO and Stobox have signed a Memorandum of Understanding to align their capabilities in primary issuance and regulated trading.

The partnership connects tokenization infrastructure with compliant brokerage and secondary market environments.

As tokenized securities grow in demand, issuers need solutions beyond basic issuance. This collaboration targets distribution, investor access, and liquidity in a structured and regulated manner.

Bridging Tokenization Infrastructure and Regulated Markets

tZERO operates a regulated broker-dealer and alternative trading system, known as an ATS. Its infrastructure supports issuance, custody, trading, and settlement of digital asset securities.

The company provides institutional-grade access to blockchain-powered financial markets. This positions it as a key link between tokenization technology and regulated capital markets.

Stobox, on the other hand, focuses on structuring and issuing compliant digital securities. It supports exempt offerings in the United States under applicable regulations.

In Europe, it operates under a Virtual Asset Service Provider license. Its platform prepares tokenized assets for interaction with broader financial ecosystems.

The MOU reflects both companies’ focus on building end-to-end solutions for the digital securities market. Issuers today require a connected path from asset structuring to compliant trading environments.

The partnership directly addresses that gap in the market. It allows both firms to operate in a more compliant and coordinated manner.

tZERO CEO Alan Konevsky stated the company’s goal clearly. “Our infrastructure solutions and partner network seek to deliver integrated market solutions that bridge tokenization technology services to compliant issuance, distribution, trading, and custody,” he said.

Konevsky added that closer alignment across these nodes supports the next phase of market development.

Expanding Regulated Access for Digital Securities

Ross Shemeliak, Co-Founder of Stobox, noted the broader shift taking place across the industry. “Digital securities need a clear path from issuance to market access,” he said.

This reflects the growing demand for more structured and regulated infrastructure in the tokenized asset space. The partnership moves in that direction with a shared framework for collaboration.

Both companies intend to explore further opportunities as the relationship develops. Stobox is advancing its global footprint, and tZERO sees fintech platforms as a key target segment.

Together, they aim to support issuers operating across different markets and jurisdictions. Each organization, however, will continue to operate independently within its own scope.

The tokenized securities market continues to attract attention from institutional and retail participants alike. Access to secondary market liquidity remains one of the main challenges for issuers.

Partnerships like this one work to remove those barriers through regulated and compliant channels. The market is moving toward more interconnected infrastructure, and this MOU reflects that direction.

Crypto World

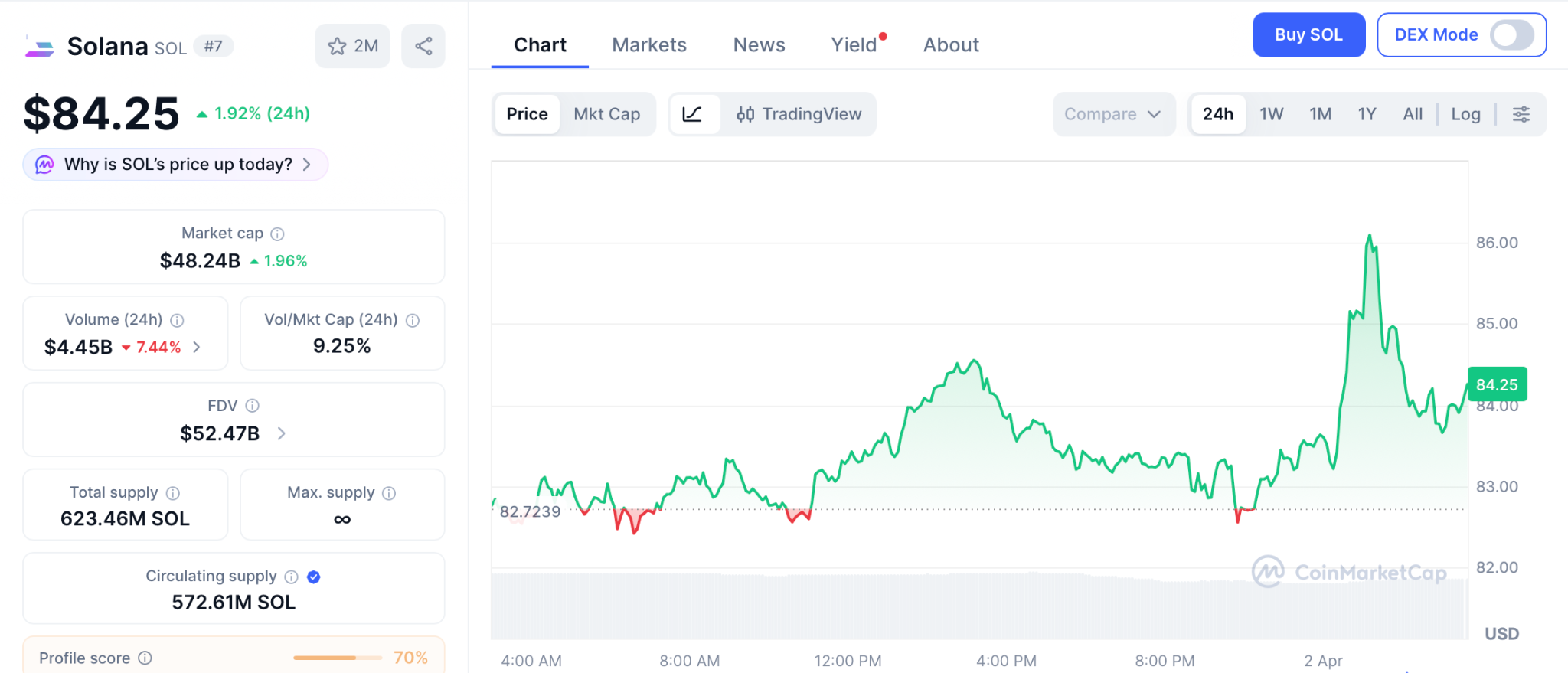

Solana Price Holds $84.25 as Memecoin DEX Volume Hits $87.8 Billion While Pepeto Presale Fills Past $8 Million

The solana price sits at $84.25 with memecoin weekly DEX volume reaching $87.8 billion in March, more than double from August 2025. Pepeto combines meme energy with real exchange tools, offering both working products and growth potential that separates it from tokens running on pure speculation. The right investment in crypto at the right time can change a life.

PEPE exploded from a presale price and the people who acted early made the biggest returns they will ever see. The same pattern is visible before the crowd confirms it, and more than $8 million entering Pepeto during fear answers why wallets keep buying without waiting.

Solana memecoin weekly DEX volume reached $87.8 billion in the last week of March, up from $40.5 billion in August 2025, according to CoinPedia.

DeFi total value locked grew 12% in March despite the correction. BeInCrypto confirmed the solana price recovery is also shaped by the SUI 42.94 million token unlock on April 1 and Firedancer validator development pushing past one million TPS in testing, adding infrastructure depth to the Solana ecosystem.

Where Working Products and Growth Potential Beat Pure Speculation

Why Pepeto Combines Meme Energy With Exchange Tools the Solana Price Cannot Offer

Pepeto combines meme energy with real exchange tools, offering both working products and growth potential that pure speculation cannot match. The cofounder who built the original Pepe coin to $11 billion designed this platform with a former Binance expert, giving holders staking returns at 189% APY, multi chain access through the bridge across Ethereum, BNB Chain, and Solana, and wallet growth confirmed by $8 million in presale capital at $0.000000186 while fear sat at 8 on the index.

The risk scorer screens every contract before capital enters, keeping scam tokens away. PepetoSwap handles zero fee trades. An independent SolidProof review confirmed every contract, and the 420 trillion supply matches what took PEPE to $11 billion with zero products.

PEPE exploded from a presale price and the people who acted early made the biggest returns they will ever see. The same pattern is visible with Pepeto before the crowd confirms it.

Analysts project 100x from presale to Binance listing, and more than $8 million entering during fear answers why everyone keeps buying: they see what the listing delivers while SOL grinds through recovery.

Solana Price Prediction: Targets, Levels, and DEX Volume Impact for 2026

SOL trades at $84.25 on April 1 according to CoinMarketCap, recovering as memecoin DEX volume doubled to $87.8 billion. DeFi TVL grew 12% in March, and Firedancer validators pushed past one million TPS in testing.

Support sits at $75 with resistance at $95 to $100. SOL ETFs launched in Q3 2025 and attracted the most sustained inflows among alt ETFs during Q1. Analyst year end targets range from $150 to $250.

From $84.25, reaching $250 gives 200% over months, a solid return that depends on sustained DeFi growth and favorable macro conditions. The solana price gives 200% over quarters while the presale compresses 100x into one listing.

The Solana Price Pattern Is the Same One, and the Right Investment at the Right Time Changes Everything

The right investment in crypto at the right time can change a life. PEPE exploded from a presale price and proved it. The same pattern is visible before the crowd confirms it with Pepeto. The Pepeto official website shows more than $8 million from wallets that already see what the Binance listing delivers.

Entering this presale while the solana price recovers and DEX volume keeps growing is how that same signal gets acted on, and letting it pass while the crowd waits for confirmation could be the one missed moment where exchange tools outperform everything that runs on meme volume alone.

Visit Pepeto before this presale stage closes and the Binance listing opens at a price nobody inside today will ever pay.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the solana price on April 1 2026?

SOL trades at $84.25 with memecoin DEX volume at $87.8 billion and DeFi TVL up 12%. Analyst year end targets range from $150 to $250.

How does the solana price affect presale entries?

Growing DEX volume means more trades captured. The Pepeto official website shows an exchange platform positioned for that volume once the Binance listing arrives.

Is Pepeto a better entry than SOL right now?

SOL targets 200% over months. Pepeto targets 100x from presale to Binance listing with cross chain tools and the architect of the original PEPE.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Bitmine Immersion Technologies purchased 71,179 Ethereum – worth approximately $147 million – last week, its largest single-week buy of 2026 and the fifth consecutive week of sustained crypto accumulation.

Combined with the 238,244 ETH acquired over the prior four weeks, Bitmine has now stacked roughly 309,423 ETH in just over a month – and the supply mechanics behind that pace are worth examining precisely.

Chairman Tom Lee is not being subtle about the thesis. The question the market hasn’t fully answered yet: is Bitmine absorbing sell pressure fast enough to move price – or is ETH’s 22% YTD decline signaling that even $147M weekly buys aren’t enough to flip sentiment on their own?

Key Takeaways:

- Bitmine acquired 71,179 ETH (~$147M) last week – its largest weekly purchase of 2026, bringing its five-week total to 309,423 ETH.

- Total holdings now sit near 4.73 million ETH (~3.92% of supply), valued at approximately $10.5 billion – exceeding Bitmine’s $9.34 billion market cap.

- 3.14 million ETH are currently staked, generating $180M in annualized yield at a 2.81% seven-day rate – with $272M projected once MAVAN staking launches.

- Tom Lee ties the crypto winter’s end directly to oil market stabilization – citing crypto’s inverse correlation to oil as currently at its highest level in a year.

Discover: The best pre-launch token sales

Five Weeks of Crypto Buying, What 309,000 Ethereum Actually Does to Liquid Supply

Bitmine confirmed the purchase via an official post on X, with on-chain data corroborating the 71,179 ETH acquisition – up from 65,341 ETH the prior week on March 23, marking a clear escalation in weekly pace. Of its total ~4.73 million ETH holdings, 3.14 million are already staked, effectively removing them from liquid circulation entirely.

That’s a meaningful supply withdrawal at a moment when institutional staking demand is accelerating across the board.

Lee framed the strategy explicitly on Monday: “Bitmine has maintained the increased pace of ETH buys in each of the past four weeks, as our base case is ETH is in the final stages of the ‘mini-crypto winter.’” He added that the macro unlock condition is specific – “the crypto winter likely ends when the upside risk to oil prices peaks,” pointing to the highest crypto-oil inverse correlation in the past year as the key read.

StrategicEthReserve currently tracks 67 large ETH treasury holders. Bitmine leads by a wide margin – SharpLink Gaming sits second with 863,000 ETH, Ether Machine third with 496,000.

The gap between first and second place alone is more than 3.8 million tokens. That concentration matters: Bitmine is absorbing a structurally significant portion of available sell-side flow, but broader institutional outflows elsewhere are still creating headwinds that individual corporate treasury buying struggles to fully offset.

Ethereum Price Prediction: Can Bitmine’s Accumulation Force a Repricing Above $2,200?

ETH is currently trading near $2,065, down roughly 22% year-to-date despite Bitmine’s aggressive weekly purchases.

Key resistance sits at $2,200 – a level ETH has failed to reclaim since the October crash – while near-term support holds around $1,980, a zone that has absorbed two recent liquidation events. RSI on the daily chart is hovering near 42, not yet oversold but showing no clear momentum reversal signal.

This whole move hinges on oil and whether that pressure finally cools off, because if it does, that is the kind of macro relief that can unlock risk assets, and with Bitmine steadily buying large chunks of ETH every week, supply keeps getting tighter in the background, which gives price a real shot at reclaiming $2,200 and pushing toward $2,500 if momentum follows.

Right now though it still feels stuck in the middle, with tensions and oil volatility hanging around, keeping ETH boxed between roughly $1,980 and $2,150 while Bitmine keeps accumulating but cannot fully break price out on its own, so you get a grind instead of a clean trend.

The risk is that this demand story fades before it fully plays out, because if inflows stay weak and Bitmine slows down as it gets closer to its supply target, that removes the main buying pressure, and without it, ETH can slip back toward $1,800 where the next real support sits.

The supply mechanics are shifting materially – but ETH’s price hasn’t priced in five weeks of $100M+ weekly buying. That disconnect is either a lagging signal or a warning that demand needs a macro catalyst, not just a corporate treasury, to resolve.

Discover: The best crypto to diversify your portfolio with

The post Bitmine Scoops $147M in Ethereum Crypto, Extends Five-Week Buying Streak appeared first on Cryptonews.

XRP price is trading at $1.32, down 2.5% in the last 24 hours, as the asset attempts to stabilize after five consecutive months of losses, which is also being boosted by Franklin Templeton’s prediction.

XRP has been grinding through a consolidation phase following its post-election peak, with analysts identifying $1.27 as the critical bear-market support floor. Meanwhile, Nvidia continues absorbing AI spending cycle uncertainty and export restriction headlines, compressing its multiple. Both assets are under pressure. Both carry asymmetric upside arguments. The difference is risk profile, time horizon, and, crucially, where each asset sits in its own cycle.

Can Ripple’s token outperform a battered Nvidia in a market where macro pressure is squeezing both crypto and tech stocks simultaneously? The answer depends almost entirely on which technical level comes next.

Discover: The best crypto to diversify your portfolio with

XRP Price Prediction: Break $1.76, or Will Bears Defend the $1.50 Resistance Wall?

XRP is currently consolidating in the $1.29–$1.39 range, with momentum turning tentatively positive after a multi-month downtrend. Five red months have left the asset searching for a directional catalyst, but the technical structure isn’t broken yet.

Key levels to watch:

- Support: $1.27 bear-market floor. A close below this level invalidates the recovery thesis.

- First resistance: $1.51, where sellers have repeatedly stepped in.

- Bull target: $1.76–$1.80, a zone where approximately 1.85 billion XRP has accumulated, making it the critical decision point for any sustained rally.

In good condition, XRP holds $1.27, clears $1.51 on volume, and targets the $1.76–$1.85 range this year, consistent with moderate AI-model forecasts projecting $1.60–$1.85. Or, it would range-bound chop between $1.29 and $1.51 as the market awaits a macro trigger. But a breakdown below $1.27 opens a retest of deeper support, invalidating the consolidation-recovery narrative entirely.

More aggressive analyst targets require a fundamental shift in institutional adoption and liquidity conditions that isn’t reflected in current price action. For now, $1.51 is the wall that matters.

Compared to Nvidia, XRP offers higher volatility and no earnings floor, but also no valuation ceiling tied to GPU shipment cycles. The same asymmetry argument applies across major altcoins, and traders rotating out of tech are increasingly running the numbers.

Discover: The best pre-launch token sales

Bitcoin Hyper Eyes Early-Mover Upside While XRP Battles Key Resistance

XRP’s recovery looks plausible, but at a $70B+ market cap, even a move to $1.85 represents modest percentage gains for new capital entering now. Traders who want crypto-native upside without waiting for Fibonacci levels to clear are scanning earlier-stage infrastructure plays. That’s where the risk-reward math gets interesting.

Bitcoin Hyper ($HYPER) is currently in presale at $0.0136778, having raised $32 million, a figure that signals serious market interest at this stage. The project positions itself as the first-ever Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, targeting sub-second finality and smart contract execution that reportedly outpaces Solana.

The architecture addresses Bitcoin’s three core constraints, slow transactions, high fees, and zero programmability, while preserving Bitcoin’s underlying security and trust model. A Decentralized Canonical Bridge handles BTC transfers natively. High-APY staking bonus is also live for early participants.

Those who want to research Bitcoin Hyper further can review the full technical documentation before the presale window closes.

This article is for informational purposes only and does not constitute financial advice. Crypto markets are volatile — always do your own research before investing.

The post XRP Price Prediction: Is Ripple a Better Investment Than Nvidia Now? appeared first on Cryptonews.

Algorand price shot up over 20% on Wednesday, becoming the best performer among the leading 100 crypto assets by market cap.

Summary

- Algorand price surged over 20% to an eight-week high of $0.105, rebounding sharply after recently hitting an all-time low.

- The rally followed its mention in a Google Quantum AI paper highlighting its post-quantum cryptography efforts, boosting investor visibility.

- Rising futures open interest and a bullish technical breakout above key moving averages point to strengthening upside momentum.

According to data from crypto.news, Algorand (ALGO) price hit an 8-week high of $0.105 on Wednesday while bringing its market cap to over $936 million. The move follows just two days after the token hit an all-time low.

The main catalyst that drove the Algorand price rebound today is its citation by Google Quantum AI in a recent paper focused on the threats major blockchains face from quantum computing. Notably, the project was mentioned over 32 times in the document, ranking just after Bitcoin and Ethereum for its proactive stance on post-quantum cryptography.

In contrast, some of the top crypto projects, such as Solana and XRP, were mentioned nearly half as often, while Hedera and Avalanche received zero mentions in the report.

Being cited in one of the most prestigious research papers gave Algorand a big boost in visibility and enhanced its technical appeal to investors who felt they got a massive discount from the token hitting its lowest level since inception.

A recent major development that has also supported its gains today includes Algorand’s integration into the Swiss retail bank PostFinance, which enabled its 2.5 million customers to directly trade and hold ALGO using their existing accounts.

Demand from derivative traders has also buoyed the token price. Data from CoinGlass shows that the open interest dedicated to Algorand futures rose 55% over the past day to $58.9 million.

Meanwhile, its weighted funding rate has shifted to a positive reading, suggesting that long position holders were paying short traders to maintain their positions, which is widely seen as a bullish signal for the market.

On the daily chart, Algorand price has broken out of a descending parallel channel pattern, a major bearish structure that had been capping gains since the beginning of this year.

Algorand price has crossed over the 20-day, 50-day, and 100-day SMA back-to-back over the past two days, a sign that short-term momentum is turning aggressively bullish. Furthermore, the supertrend indicators, which traders use to gauge market direction, remain in the green, suggesting the path of least resistance is currently to the upside.

For now, $0.138, which marks the 200-day SMA, is the most important resistance level that traders would be keeping a close watch on. A break above that could signal a long-term trend reversal and open the door for a much larger recovery toward previous yearly highs.

However, if Algorand price falls below the 50-day SMA at $0.088, it would invalidate the current breakout and likely lead to a retest of the recent all-time lows.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

NOW DeFi launches quantum cloud mining as Bitcoin consolidates and XRP liquidity rises.

Summary

- Bitcoin and XRP consolidation increases risks for spot holders, driving demand for alternative yield strategies.

- NOW DeFi launches “quantum computing cloud mining” to deliver automated returns without relying on market direction.

- The platform converts crypto into cloud hashrate, enabling passive income without hardware or active trading.

As Bitcoin (BTC) enters a high-level, wide-ranging consolidation zone driven by global macroeconomic factors, and Ripple (XRP) sees increasing liquidity in cross-border payments, the crypto asset market is undergoing a new paradigm shift.

For the massive number of spot holders, the time cost of “holding and waiting for a pump” and the risks of market pullbacks are rising sharply.

Against this backdrop, NOW DeFi, the world’s leading automated wealth ecosystem, officially announced today the full launch of its highly anticipated “Quantum Computing Cloud Mining” architecture.

By introducing exponentially advanced quantum computing power, NOW DeFi has successfully broken through the profit bottlenecks of traditional spot holding, providing global crypto investors with a brand-new path to ignore market bulls and bears, offering stable hashrate dividends of up to $20,000 per day.

In-depth market analysis: The “profit vacuum” for spot holders

According to Q1 on-chain data and technical analysis (TA), both BTC and XRP exhibit strong “supply lock-up” characteristics. However, during volatile price wicks, retail investors’ spot holdings are highly susceptible to paper losses.

The vast majority of investors’ crypto assets remain in a “dormant” state, unable to generate compound interest while enduring immense psychological pressure from constantly monitoring charts. Furthermore, traditional DeFi staking yields have plummeted, leaving the market in urgent need of a high-return alternative backed by strong technical barriers.

NOW DeFi’s disruptive innovation: How does quantum computing generate yield?

To address this industry pain point, NOW DeFi integrates cutting-edge quantum computing with high-frequency node verification technology. The core advantage of quantum hashrate lies in its ability to process massive hash collisions and cross-market arbitrage models in mere milliseconds.

NOW DeFi “fragments” this top-tier computing power into cloud-based contracts. Holders of BTC, XRP, and other mainstream assets simply need to convert their assets into NOW DeFi’s hashrate fuel to earn 100% fully automated hashrate outputs — requiring zero hardware investment or market monitoring.

Core hashrate contract matrix: A wealth path from retail to institutional

To meet the needs of investors of all sizes, NOW DeFi has unveiled its latest quantum hashrate yield model. Data shows that top strategic investors can achieve explosive wealth growth through compound interest and high-frequency hashrate clusters:

Strategy Level

Entry Threshold(USD)

Strategic Cycle(Days)

Est. Total Strategic Yield(USD)

Strategy Positioning

Entry-Level Quantum

$100

2

$8

Algorithm trial, ultra-short-term arbitrage

Standard Quantum

$1,500

10

$235.5

Mid-term trend capture, compound growth

Advanced Quantum

$5,000

15

$1,215

Deep learning-driven, long/short hedging

Elite Quantum

$25,000

25

$11,250

Institutional execution logic, high-frequency arbitrage

Quantum Strategy

$90,000

20

$36,000

Top-tier hashrate cluster, full market coverage

(For more strategy details and real-time dynamic data, please visit the official website)

How to earn passive income via NOW DeFi’s quantum hashrate?

NOW DeFi was designed to make cutting-edge quantum technology accessible to everyone. Eliminating tedious hardware configurations and complex trading models, any investor can unlock exponential wealth growth in just four simple steps:

- Register and claim a welcome bonus: Instantly receive a $22 welcome bonus. Register today to claim a cash reward and start the passive income journey with zero risk.

- Select and Activate a Hashrate Contract: Choose a quantum hashrate package that suits a particular capital size. Once a strategy package is purchased, the system takes over immediately.

- 100% Fully Automated Yield: Say goodbye to staring at plunging charts. Without any market monitoring, profits will be automatically and accurately credited every 24 hours.

- Ultimate Liquidity and Flexible Withdrawals: Take full control of wealth. Once the account balance reaches $100, it can be withdrawn directly to a crypto wallet or reinvested to unlock exponential compound interest. Absolutely transparent, with zero hidden fees, no maintenance fees, and no surprise charges—100% of the money you earn belongs to you.

About NOW DeFi: The ultimate consensus for global safe-haven capital

NOW DeFi provides an elite-level automated wealth accumulation ecosystem, with the core vision of helping global investors stop losses in the spot market and achieve maximum returns with complete peace of mind. In the unpredictable crypto market, NOW DeFi has built a powerful global safe-haven consensus:

- Global Safe-Haven Consensus: Trusted by over 10 million smart investors across more than 198 countries and regions who have successfully broken free from market volatility.

- Fortress-Like Security: Equipped with industry-leading dual-layer protection from McAfee® and Cloudflare®, allowing you to sleep soundly knowing your funds are secured by military-grade encryption.

- Seamless Multi-Asset Support: Offers unparalleled flexibility with direct settlement in top digital assets, including XRP, BTC, ETH, SOL, DOGE, USDC, USDT, BNB, and BCH.

Conclusion and action guide: Seize the early-adopter dividends of the quantum era

The ultimate goal of technical analysis is to guide trading. In 2026, as crypto market trends become increasingly complex, stopping senseless gambling in the spot market and shifting assets to the highly certain quantum hashrate track has become the consensus among smart investors.

For more information, please visit the official NOW DeFi website and download the application.

Email: [email protected]

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Australia has passed legislation that will bring many digital asset platforms and tokenised custody platforms under the country’s financial services licensing regime.

The Corporations Amendment (Digital Assets Framework) Bill 2025 has now cleared both houses of the Australian Parliament, according to parliamentary records, marking the biggest step yet in Canberra’s push to create a dedicated regulatory framework for digital assets.

Introduced in November 2025, the bill amends the Corporations Act and ASIC Act to regulate digital asset platforms and tokenised custody platforms, with the stated aim of improving consumer protection, market integrity and regulatory certainty.

The bill now awaits royal assent, the final step before becoming law. It is set to take effect 12 months after assent, with an additional transition period for businesses to comply.

The bill requires crypto operators, including exchanges and custody platforms, to obtain an Australian Financial Services Licence (AFSL) from the Australian Securities and Investments Commission (ASIC), the country’s financial regulator.

The Digital Economy Council of Australia (DECA), an industry group representing Australia’s digital economy, praised the development in a statement on LinkedIn.

“For the first time, we have a legislative framework that directly addresses digital asset platforms and it provides long-awaited clarity for businesses, investors and regulators, and marks a shift from uncertainty toward implementation,” DECA said.

Related: Australia fines local Binance unit $6.9M over client onboarding failures

Addendum clarifies treatment of MPC and crypto custody under new law

Jazz Ozvald, former assistant director of digital asset policy at the Commonwealth Treasury, took to LinkedIn to express delight at the milestone in passing the bill.

He noted that the government also tabled an Addendum to the Explanatory Memorandum, which includes additional detail about how the bill is intended to apply where digital tokens are factually controlled through multi-party computation (MPC).

MPC is a cryptographic technology used to secure crypto wallets by splitting control between multiple parties, so no single person has full control. Transactions can only be approved when enough parties work together, making it harder for funds to be stolen or misused.

Related: Google targets 2029 post-quantum migration as threats draw nearer

The addendum says that the law only applies to platforms that actually hold crypto for customers, rather than just providing technology that helps control it, even in shared-control setups like MPC.

Magazine: Nobody knows if quantum secure cryptography will even work

SpaceX, Elon Musk’s aerospace powerhouse, has reportedly filed confidentially for an initial public offering with the U.S. Securities and Exchange Commission. The move, described by Bloomberg as citing people familiar with the matter, positions the company for what could be one of the largest public listings in U.S. history and signals a potential shift in how a private space and AI conglomerate marshals capital for its next phase.

According to Bloomberg’s reporting, the IPO could be timed for a June close, should the process move forward as planned. While details remain shielded behind confidentiality, insiders told Bloomberg that the offering could value SpaceX well above $1.75 trillion and could raise as much as $75 billion, a scale that would dwarf many prior debutings and reimagine the company’s public-market footprint.

The listing could feature a dual-class share structure designed to preserve control for insiders, including SpaceX founder Elon Musk, even as public investors participate. In line with such structures, the offering is expected to allocate up to 30% of shares for individual investors, according to the coverage.

On the banking and advisory front, the process is anticipated to involve a cadre of Wall Street firms, with Bank of America, Goldman Sachs, JPMorgan Chase, Morgan Stanley and Citigroup commonly cited as likely participants in steering SpaceX through its transition to a public company.

Beyond the IPO chatter, SpaceX’s crypto footprint remains a recurring point of interest. The company is widely reported to hold a substantial Bitcoin position—8,285 BTC on its balance sheet, valued at more than $565 million at current prices. Notably, SpaceX moved its Bitcoin to a new wallet address in October, fueling speculation about whether the company intends to maintain a long-term crypto strategy or adjust holdings in response to market conditions.

Market structure and access to private holdings are also on the radar as SpaceX eyes broader investor participation. Trading venues and tokenization platforms have been examining opportunities to offer tokenized shares or similar vehicles for high-profile private companies, including SpaceX and other AI leaders. Robinhood and Kraken, among others, have discussed how retail investors might gain access to nonpublic companies through blockchain-based tokenized instruments, a development Robinhood’s CEO has described as potentially widening participation even as high-profile private tech firms pursue public-market exits.

Key takeaways

- SpaceX reportedly filed confidentially for an SEC IPO, with a possible June timeline and a valuation above $1.75 trillion; potential raise up to $75 billion.

- The deal could use a dual-class structure preserving insider voting control, with up to 30% of shares reserved for individual investors.

- Major banks—Bank of America, Goldman Sachs, JPMorgan Chase, Morgan Stanley and Citigroup—expected to advise on the transition to a public company.

- SpaceX reportedly maintains 8,285 BTC (worth over $565 million) on its balance sheet, with a October wallet move prompting questions about long-term crypto strategy.

- Tokenized private-share concepts are circulating in crypto markets, with Robinhood and Kraken cited as exploring access to SpaceX, OpenAI and other nonpublic firms for retail investors.

- In the AI space, SpaceX’s acquisition of xAI places it in a broader race with OpenAI and other private AI labs; OpenAI recently closed a funding round with about $122 billion in committed capital, lifting its implied valuation toward the hundreds of billions, and Bloomberg notes potential IPO activity for both OpenAI (as early as 2026) and Anthropic (potentially as soon as October).

Context: SpaceX’s AI ambitions and the public market timing

The reported IPO comes on the heels of SpaceX’s February move to acquire xAI, Elon Musk’s AI venture, signaling a ramp-up in the company’s participation in the fast-evolving AI ecosystem. The combination of aerospace prowess and AI development positions SpaceX to leverage a broader technology and capital-market narrative as investors assess how private companies transition to public ownership.

OpenAI, the creator of ChatGPT, has been central to the AI funding landscape. Bloomberg notes that OpenAI concluded its latest funding round with about $122 billion in committed capital, driving its estimated value higher—a point underscoring the growing parallel between AI capital intensity and public-market appetites. The firm has been widely discussed as a potential IPO candidate in 2026, a signal to market participants that large AI players could become regulars on public exchanges in the coming years. Anthropic, another important name in the field, is also reported to be weighing a public listing, with Bloomberg indicating a possible listing as soon as October of this year.

As SpaceX contemplates a potential public listing, retail and institutional investors alike are watching how the company would balance the demands of a public-filed governance framework with its private-market strategies and multi-vertical ambitions. The prospect of a dual-class structure remains a point of contention for some market observers, given how it concentrates voting power among insiders even as it enables faster strategic execution and longer-term investment horizons.

For crypto-market observers, the overlap between SPAC-like tokenization concepts and traditional IPOs adds another layer of consideration. Tokenized shares and blockchain-based participation could, in theory, broaden access to a private giant like SpaceX for retail buyers who traditionally have had limited entry points. While these products are still gaining regulatory clarity and market traction, the ongoing interest from platforms such as Robinhood and Kraken indicates a broader industry push to bridge private-market participation with public-market liquidity via tokenization tools.

What this means for investors and the AI ecosystem

If SpaceX proceeds with an IPO in the proposed size and structure, it would be among the largest listings in U.S. history and would place the company at a valuation tier previously seen with mega-cap tech and consumer platforms. For investors, the potential blend of aerospace breadth and AI stakes could create a diversified exposure within a single name, while the dual-class voting framework could shape how quickly and how decisively SpaceX can execute long-term strategy in a volatile market environment.

From a broader market perspective, the convergence of SpaceX’s public-market ambitions with the AI arms race highlights a trend where tech giants are building vertical integrations across space, transportation, and artificial intelligence. OpenAI’s and Anthropic’s public-market trajectories, while not guaranteed, add a tailwind to this narrative, suggesting that the next wave of big listings could include private AI labs alongside more diversified technology conglomerates. Investors should watch regulatory developments, the timing and terms of any anchor shareholders, and how SpaceX plans to balance public reporting requirements with its rapid, multi-domain execution plan.

Whether or not the SpaceX IPO materializes on schedule, the reporting underscores a larger dynamic: the market’s willingness to value private, highly strategic technology entities at multi-trillion-dollar levels and to explore new models of ownership and participation, including tokenized access to private-equity-like positions. For crypto markets, the ongoing dialogue around tokenization, crypto holdings, and public-market access remains a live space to watch as these conversations intersect with traditional capital-raising mechanisms.

Readers should monitor upcoming disclosures and investor briefings, which Bloomberg notes SpaceX has signaled will occur later this month. How the market perceives SpaceX’s balance between leadership in aerospace and AI, and how the company navigates governance, capital structure, and crypto exposure, will likely shape the scope of future public-market activity among technology-first, asset-light conglomerates.

As the IPO discourse unfolds, investors and builders will need to weigh not only the size of the offering but also the governance implications, the strategic roadmap for AI initiatives, and the evolving role of crypto in corporate treasury strategies. The next steps—from regulatory filings to investor roadshows—will reveal how SpaceX intends to translate its private-market momentum into a lasting public-market narrative.

Stay tuned for updates on next steps, regulatory milestones, and any refinements to SpaceX’s proposed capital structure as the market awaits a potential landmark listing that could redefine the contours of big-tech and AI investing.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

AI crypto trading bots reshape investing as automation replaces manual execution and emotional decision-making.

Summary

- AI crypto trading bots simplify investing by automating strategies and removing the need for constant monitoring.

- SaintQuant targets beginners with pre-configured strategies and no coding or complex setup required.

- Its fully automated system offers a hands-off approach for users seeking simple, consistent crypto trading.

The rise of AI trading bot crypto solutions has transformed how people approach cryptocurrency trading. What once required deep technical knowledge, constant monitoring, and emotional discipline can now be handled by intelligent automation.

Today, both beginners and experienced traders are exploring automated crypto trading platforms to improve efficiency and reduce manual effort. But key questions remain:

- Do AI trading bots work?

- Can you build one without coding?

- Is there a free crypto trading bot worth trying?

In this guide, we’ll break down everything that is needed to know — from how these bots work to how to choose the best platform — while sharing practical insights to help anyone get started.

What is an AI trading bot in crypto?

An AI trading bot is a software program that uses artificial intelligence to analyze market data and execute trades automatically. Unlike traditional bots that follow fixed rules, AI-powered bots adapt to changing market conditions using:

- Machine learning algorithms

- Predictive analytics

- Real-time data processing

These bots are widely used in:

- Crypto trading online for automated execution

- Portfolio management

- Arbitrage opportunities across exchanges

In essence, an AI-powered Bitcoin bot acts as a 24/7 trading assistant, capable of making decisions faster than any human trader.

Do AI trading bots work? (Realistic expectations)

The short answer: Yes — but with limitations.

Advantages

- 24/7 trading without downtime

- Emotion-free decisions, reducing impulsive trades

- Fast execution in volatile markets

Limitations

- No guarantee of profits

- Performance depends on strategy quality

- Vulnerable to extreme market conditions

AI trading bots work best when used as tools to enhance strategy, not as “set-and-forget money machines.”

How to build an AI Crypto trading bot without coding, and are there free options?

One of the biggest myths in crypto trading is that there’s no need for programming skills to use automation. Fortunately, that’s no longer true.

Simple no-code setup process

For those wondering how to build an AI crypto trading bot without coding, here’s a simplified path:

- Choose a platform

- Select pre-built AI strategies

- Configure risk settings

- Backtest strategies

- Deploy live trading

Modern platforms now provide intuitive dashboards, making the process accessible even to complete beginners.

Tools that make it easy

- Plug-and-play platforms

- Strategy marketplaces

- Managed cryptocurrency trading services

These tools eliminate complexity and allow users to focus on outcomes rather than technical setup.

Is there a free crypto trading bot?

Yes — but most “free” options come with trade-offs.

What “Free” Usually Means:

- Limited features

- Trial-based access

- Restricted performance tools

Hidden Costs to Consider:

- Exchange fees

- Spread and slippage

- Paid upgrades for full functionality

Real example: Try before committing

Some platforms offer a better alternative through trial-based access to premium features.

For instance, SaintQuant provides a beginner-friendly experience with:

This allows users to experience a real automated crypto trading platform — not just a limited demo.

When free bots make sense

Free or trial bots are ideal for:

- Beginners exploring AI trading bots

- Testing strategies safely

- Learning how automation works in real markets

Key takeaway

There is no need for coding skills or a large upfront investment to start using an AI trading bot crypto solution. With no-code tools and trial offers, entry barriers are lower than ever.

Best AI trading bot crypto platforms (expert insights)

Choosing the right platform is critical. Based on usability, features, and accessibility, here are some top options:

1. SaintQuant – Simplified AI Trading for passive income

SaintQuant stands out as a beginner-focused platform designed for simplicity and efficiency.

Key Features:

- Pre-configured AI trading strategies

- No coding or complex setup required

- Fully automated trading system

Advantages:

- Ideal for beginners and passive investors

- Quick onboarding process

- Focus on consistent, automated performance

If you’re looking for a hands-off automated bitcoin trading platform, SaintQuant offers one of the easiest entry points.

2. Cryptohopper – Advanced customization

Cryptohopper is a well-known platform offering:

- Strategy customization

- Signal marketplace

- Advanced trading tools

Pros:

Cons:

- Steeper learning curve for beginners

3. Other AI trading bots worth considering

There are also various:

- Bots for sale in strategy marketplaces

- Hybrid platforms combining AI and manual controls

When evaluating options, always prioritize:

- Security

- Exchange integration

- Transparency

Key features to look for in the best AI trading bot

When choosing the best AI trading bot crypto, consider:

- Automation quality

- Backtesting capabilities

- Risk management tools

- Exchange compatibility

- Performance transparency

These features determine whether a bot is truly effective or just hype.

Risks and best practices

Even the best bots require responsible usage.

Best Practices:

- Start with a small capital

- Diversify strategies

- Monitor performance regularly

- Use secure API configurations

Avoid relying entirely on automation—human oversight still matters.

AI trading bots vs manual trading

| Factor | AI Trading Bots | Manual Trading |

| Speed | Instant execution | Slower |

| Emotion | Emotion-free | Emotion-driven |

| Control | Less direct control | Full control |

Best approach: combine both for optimal results.

Future of AI in crypto trading

The future of AI trading bots is promising, with trends including:

- Integration with DeFi ecosystems

- More advanced predictive models

- Increased adoption among retail investors

As technology evolves, automation will likely become a standard part of crypto trading online.

Conclusion

AI trading bots are reshaping the crypto landscape by making trading more accessible, efficient, and data-driven.

- They work — but require smart usage

- They can be built and deployed without coding

- Free and trial options make it easy to start

Platforms like SaintQuant are helping bridge the gap for beginners, offering a streamlined way to enter the world of automated trading.

If you’re new, start small, experiment with strategies, and gradually scale your involvement. With the right approach, AI-powered cryptocurrency trading services can become a valuable part of your investment toolkit.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Chiefs GM Brett Veach silent on invite to Travis Kelce, Taylor Swift’s wedding

Artemis II Mission Launches Successfully

Bonus time! #finance #economy

![Why A Major Bitcoin Bounce Is Imminent [Data]](https://wordupnews.com/wp-content/uploads/2026/04/1775098099_maxresdefault-80x80.jpg)

-

Business6 days ago

Business6 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Tech6 days ago

Tech6 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

NewsBeat5 days ago

NewsBeat5 days agoThe Story hosts event on Durham’s historic registers

-

Sports5 days ago

Sports5 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment3 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment4 days ago

Entertainment4 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World2 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech3 days ago

Tech3 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World7 hours ago

Crypto World7 hours agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Sports1 day ago

Sports1 day agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech2 days ago

Tech2 days agoEE TV is using AI to help you find something to watch

-

Tech2 days ago

Tech2 days agoApple will hide your email address from apps and websites, but not cops

-

Tech2 days ago

Tech2 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech2 days ago

Tech2 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Fashion6 days ago

Fashion6 days agoEn Vogue in Brown Leather and Tailored Neutrals by Atelier Savoir, Styled by J Bolin

-

Politics2 days ago

Politics2 days agoShould Trump Be Scared Strait?

-

Crypto World2 days ago

Crypto World2 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Fashion6 days ago

Fashion6 days agoWhat Are Your Favorite T-Shirts for the Weekend?

-

Fashion5 days ago

Fashion5 days agoWeekly News Update, 3.27.26 – Corporette.com

-

Crypto World1 day ago

Crypto World1 day agoBitcoin enters the public bond market as Moody’s gives a first-of-its-kind crypto deal a rating

You must be logged in to post a comment Login