Crypto World

Is XRP complementing the banking network or replacing it?

For years the XRP community has promised that XRP would flip SWIFT, the messaging network behind global banking. In 2026 the reality is stranger than the slogan. SWIFT is building its own blockchain ledger that pointedly leaves XRP out, even as XRP gets wired into SWIFT through a side door.

Summary

- The long-running claim that XRP will replace SWIFT has given way to a more complicated 2026 reality in which the two systems both compete and connect.

- SWIFT is a messaging network used by more than 11,000 institutions to move trillions of dollars a day, and it completed its migration to the ISO 20022 data standard in late 2025 and is now building its own blockchain shared ledger.

- That SWIFT ledger deliberately excludes public-network assets like XRP, keeping settlement in tokenized bank deposits, which undercuts the idea that XRP becomes the settlement rail.

- At the same time, a SWIFT integration with the payments firm Thunes gives banks optional access to Ripple’s liquidity products, including XRP as a bridge asset, so XRP is wired in as an option rather than a requirement.

- Ripple itself has hedged by pushing its RLUSD stablecoin as speed without volatility, pointing toward a future where XRP is one optional liquidity leg in a fragmented, interoperable system rather than the network that replaces SWIFT.

The single most durable promise in the XRP community is that XRP will one day replace SWIFT, the messaging network that sits behind nearly every international bank transfer on earth. It is a powerful story, the idea that a fast, cheap digital asset will sweep away a slow, decades-old system and capture the enormous value flowing through global payments, and it has motivated XRP holders for years. The trouble is that the story has always blurred two very different things: SWIFT, which is a messaging system that tells banks how to move money, and XRP, which is an asset that can actually move value.

In 2026, the relationship between the two has become more interesting and more complicated than the slogan suggests. SWIFT is not standing still, having finished a major data-standard overhaul and begun building its own blockchain ledger. Ripple, for its part, has quietly softened its rhetoric from replacing SWIFT to complementing it, and has hedged its own bets by leaning into a dollar stablecoin alongside XRP. The blunt replacement narrative no longer fits the facts.

What makes the question genuinely worth examining now is that both systems are making concrete moves that reveal how they actually see each other. SWIFT has built a blockchain ledger that deliberately leaves XRP out, a telling choice. Yet through a separate integration, XRP has been wired into SWIFT as an optional liquidity tool, an equally telling choice in the other direction.

The result is neither the clean replacement the bulls predicted nor the irrelevance the skeptics expected, but something messier: a fragmented, interoperable landscape in which XRP is one option among several, available but not required. This piece works through what SWIFT actually is and what Ripple actually built, the reality behind the ISO 20022 hype, SWIFT’s own blockchain project and why it excludes XRP, the side door through which XRP gets connected anyway, Ripple’s pivot toward its stablecoin, and an honest verdict on whether XRP is complementing the banking network or replacing it. The answer matters because so much of the XRP investment case rests on which of those two things is true.

What SWIFT actually is, and is not

To judge the rivalry clearly, you have to be precise about what SWIFT does, because the replacement narrative often gets this wrong. SWIFT is not a payment system that moves money; it is a messaging network that moves instructions about money. When a bank in one country needs to send funds to a bank in another, SWIFT carries the standardized message that says, in effect, pay this amount to this account.

The actual money moves separately, through the banks’ own accounts and the correspondent banking system. More than eleven thousand financial institutions use SWIFT, and the value of payments it helps coordinate runs into trillions of dollars every day, which makes it the central nervous system of cross-border finance. It is, above all, a trusted standard and a network, deeply embedded in how banks talk to one another.

The weaknesses the replacement narrative points to are real, but they live in the settlement layer beneath SWIFT, not strictly in SWIFT itself. Because a cross-border payment often hops through a chain of correspondent banks, each holding pre-funded accounts in various currencies and each taking a fee and adding delay, the traditional process can take one to three business days and is closed on weekends and holidays. A payment from Japan to Brazil might pass through three or four intermediaries before arriving.

SWIFT has worked to improve this. Its gpi service, launched in 2017, sped things up so that a large share of payments now credit within thirty minutes and effectively all within a day, with tracking along the way. But gpi modernized the messaging and tracking without changing the underlying correspondent-banking architecture, which still relies on pre-funded accounts and intermediaries. So SWIFT is best understood as the messaging and standards layer of a settlement system whose plumbing is slow, and the question is whether a blockchain alternative can replace that plumbing, the messaging layer, or both.

What Ripple actually built

Ripple’s pitch is aimed squarely at the settlement plumbing, and understanding its core product clarifies where XRP fits. Ripple is a blockchain financial-technology company built around the XRP Ledger, and its enterprise network, historically called RippleNet, lets financial institutions send payments to one another more directly than the correspondent system allows.

The mechanism that actually involves XRP is called On-Demand Liquidity, or ODL, and it is the heart of the XRP value proposition. Instead of a bank pre-funding accounts in every destination country, ODL converts the sending currency into XRP on a crypto exchange, moves that XRP across the XRP Ledger in three to five seconds, and converts it into the destination currency on the other side. The XRP acts as a bridge asset, a momentary carrier of value between two currencies, which removes the need for the expensive pre-funded accounts that slow the traditional system.

The advantages are concrete. An XRP Ledger transaction settles in seconds rather than days, costs a fraction of a cent, and runs around the clock, including weekends, with the network having processed billions of transactions cumulatively and supported tens of billions of dollars in liquidity volume. For a bank or payment provider, ODL promises to free up the capital that would otherwise sit idle in pre-funded foreign accounts, while settling far faster.

This is the genuine innovation behind the XRP thesis: not a new messaging standard, but a new way to handle the settlement leg, using a digital asset as a bridge so value can move without the correspondent-banking overhead. Whether this complements SWIFT or replaces it depends on whether banks adopt the bridge for the settlement leg while keeping SWIFT for messaging, or whether something more wholesale occurs. And as the rest of this piece shows, the 2026 evidence points firmly toward the former.

The ISO 20022 reality check

No discussion of Ripple versus SWIFT is complete without addressing ISO 20022, because few topics generate more confusion and hype in the XRP community. ISO 20022 is a global standard for the format of financial messages, replacing older, less structured message types with a richer format that carries far more data, such as detailed remittance information, compliance data, and structured identifiers.

It improves automation, transparency, and anti-money-laundering monitoring, and it has become the common language toward which the world’s major payment systems are migrating. SWIFT completed its full migration to ISO 20022 in November 2025, ending the long coexistence with legacy message types, a genuine milestone for global finance.

Here is where the confusion sets in. A persistent claim in XRP circles holds that XRP is ISO 20022 compliant in a way that guarantees it a central role once banks adopt the standard. The reality is more limited. Ripple did join the ISO 20022 standards body, becoming one of the first blockchain firms to do so, and RippleNet is built to send and receive ISO 20022 messages, which lets it interoperate cleanly with banks using the standard.

That is a real advantage for Ripple’s network. But the XRP token itself is not ISO 20022 certified, because ISO 20022 standardizes messaging formats and does not certify cryptocurrencies or blockchains at all. The standard governs how payment information is structured, not which asset settles a payment. So while RippleNet’s compliance gives Ripple a seat at the table and makes integration easier, the idea that ISO 20022 anoints XRP as the chosen settlement asset is a misreading.

The standard raises the bar for every payment solution, traditional or crypto, and SWIFT, as the established messaging hub that helped shape the standard, arguably benefits at least as much as Ripple does. ISO 20022 is a prerequisite for interoperability, not a victory for any single token.

SWIFT is not standing still

The replacement narrative tends to picture SWIFT as a static, aging incumbent waiting to be disrupted, but the 2026 reality is that SWIFT is actively building its own path into the blockchain era. After completing the ISO 20022 migration, SWIFT moved on to a more ambitious project: a blockchain-based shared ledger designed to enable round-the-clock cross-border settlement. Having run trials since 2025 with a group of more than forty banks, SWIFT completed the design phase of this ledger in early 2026 and began building its first working version, with the aim of processing real transactions before the end of the year.

The ledger is permissioned and compatible with common smart-contract tooling, and it is tied closely to the ISO 20022 messaging SWIFT already runs, so banks can plug into it through SWIFT’s trusted infrastructure instead of adopting an entirely new public blockchain.

Crucially, SWIFT has been explicit that this is about extending its existing role, not handing the rails to a competitor or issuing new money. Its chief innovation officer framed the effort as preserving settlement in central-bank money, commercial-bank money, or tokenized deposits, while adding the ability to lock in commitments, execute complex cross-border transactions atomically, and share a single auditable record across networks. In other words, SWIFT wants to keep value inside the regulated banking system while gaining the speed and programmability of a blockchain.

To get there, it has been stress-testing nearly every digital-asset rail available, running trials with major banks on tokenized deposits, tokenized bonds, and stablecoins, including a March 2026 interoperability trial that tested several stablecoins. The picture this paints is not of an incumbent asleep at the wheel, but of a network methodically absorbing blockchain technology into its own infrastructure, on its own terms, while keeping its central position as the orchestrator of global banking. That ambition sets up the most consequential detail for XRP holders.

The detail XRP holders cannot ignore

If SWIFT is building its own blockchain ledger, the obvious question for the XRP thesis is whether XRP is part of it, and the answer, pointedly, is no. SWIFT’s shared-ledger project is designed around tokenized bank deposits in currencies such as dollars, euros, and Canadian dollars, transferred between banks under the same regulations that govern wires, and it deliberately avoids public-network assets like XRP.

The design principle is that no value should escape regulated accounts, so reaching a public-ledger asset would require an additional step outside the system’s perimeter, a step the project intentionally does not take. SWIFT’s ledger is permissioned and built for the control and auditability that central banks and supervisors demand, which is precisely the opposite of XRP’s open, public network.

This is a genuinely important development that much of the bullish commentary glosses over. If banks get the round-the-clock, blockchain-based settlement they want from SWIFT’s own ledger, using tokenized deposits they already trust and within the regulated perimeter they are comfortable with, then a significant part of the problem ODL was meant to solve gets solved without XRP. SWIFT is, in effect, building a competitor to the settlement innovation that underpins the XRP thesis, and building it in a way that keeps XRP out by design.

For an XRP holder, this should temper any expectation that banks will inevitably route settlement through XRP simply because blockchain is faster. The institutions have a path to blockchain settlement that does not touch XRP at all, offered by the network they already use and trust. That does not mean XRP is shut out of the banking system entirely, because there is a side door, but it does mean the headline rail SWIFT is building is, by deliberate choice, an XRP-free one.

The side door: how XRP gets wired in anyway

The story has another turn, because even as SWIFT’s own ledger excludes XRP, XRP has been connected to SWIFT through a separate channel, and understanding this optionality is essential to an honest verdict. Through an integration involving the payments firm Thunes, the more than eleven thousand banks on the SWIFT network gain optional access to Ripple’s liquidity products, including XRP as a bridge asset.

The routing works in sequence: a company sends a payment via SWIFT, SWIFT can route it through Thunes, Thunes offers access to Ripple’s ODL infrastructure, and XRP settles that leg. The critical word in that sequence is optional. No step forces a bank to use XRP; the connection makes XRP available as one liquidity choice among others, not a mandated part of the flow.

This optionality is structurally meaningful, but it is a double-edged thing for XRP holders, and the distinction matters enormously for how to read the narrative. On one hand, being wired into SWIFT, even optionally, gives XRP distribution at a scale it could never reach through Ripple’s direct partnerships alone, putting an XRP settlement option in front of thousands of institutions. On the other hand, optional access creates demand optionality, not guaranteed volume.

The banks can use the XRP rail, but nothing compels them to, and many will default to the rails and assets they already know. So the SWIFT connection is real and potentially valuable, but it is a long way from the mandatory, network-wide adoption the replacement narrative imagined. The accurate way to hold it is that XRP now has a foot in the door of the world’s dominant banking network, as one option a bank can choose, while SWIFT simultaneously builds its own settlement ledger that bypasses XRP. Both things are true at once, which is exactly why the simple replace-or-die framing fails.

Ripple’s own pivot tells the story

Perhaps the clearest signal about whether XRP is replacing SWIFT comes from Ripple itself, which has been quietly repositioning in a way that speaks volumes. Alongside its push for XRP-based settlement, Ripple has been aggressively advancing its dollar-pegged stablecoin, RLUSD, and the rationale reveals how Ripple now sees the landscape.

RLUSD is fully reserved with cash and short-term government securities, audited regularly, and positioned as enterprise-grade infrastructure that offers the speed of blockchain rails without the price volatility of XRP. In effect, Ripple is offering banks and payment firms stablecoin-as-a-service: a way to get fast, programmable settlement while holding a stable dollar value instead of a fluctuating token. This directly complements SWIFT’s own tokenized-deposit strategy instead of trying to overthrow it.

The significance of this pivot is hard to overstate for the replacement debate. A company that truly believed XRP was on the verge of replacing SWIFT and capturing all that settlement value would have little reason to build a competing stablecoin product that settles without XRP. Ripple is hedging, building rails that work whether or not banks choose XRP, because it understands that enterprises often want stability over a bridge asset and that the future is more likely to be a fragmented mix of instruments than a single winner.

This is the same complementary posture Garlinghouse has signaled in softening from earlier replace-SWIFT rhetoric toward language about Ripple complementing existing systems. Ripple, in other words, has read the room. It is positioning itself as a provider of modern settlement infrastructure, of which XRP is one component and RLUSD is another, instead of betting everything on XRP displacing the incumbent network. When the company most invested in XRP’s success diversifies away from pure-XRP settlement, holders should take note of what that says about the realistic ceiling of the replacement thesis.

Complement or replace: the honest verdict

So where does this leave the question at the heart of the matter? The honest verdict is that XRP is complementing the banking network far more than replacing it, and that the 2026 evidence has largely retired the clean replacement narrative. The landscape that is actually forming is not winner-takes-all but fragmented and interoperable, a world in which several systems coexist and connect instead of one sweeping the others away.

SWIFT retains its position as the standards-setter and messaging hub of global finance, and it is extending that position into blockchain on its own terms, with a settlement ledger that keeps value inside the regulated banking system and deliberately excludes XRP. Ripple, meanwhile, controls a suite of modern settlement tools, including the XRP Ledger, the optional XRP bridge liquidity now reachable through SWIFT, and the RLUSD stablecoin, and it is selling all of them into a market that increasingly wants choice instead of a single rail.

Within that landscape, XRP’s realistic role is as one optional liquidity leg among many, valuable where it is chosen but never mandated, available to thousands of institutions through the SWIFT connection yet competing against tokenized deposits, stablecoins, and SWIFT’s own XRP-free ledger for each transaction. That is a meaningful role, and it is not nothing: a foot in the door of global banking, with genuine speed and cost advantages, is a real asset. But it is a long way from the world the slogan promised, in which XRP becomes the settlement rail of international finance and captures the value flowing across it.

For holders, the practical takeaway is to replace the binary replace-or-die framing with a more accurate one. XRP’s banking future is about optionality and adoption rates: how often institutions actually choose the XRP rail when given the option, and whether ODL volume grows enough to matter against the token’s large supply. The replacement dream made XRP a bet on inevitability. The complementary reality makes it a bet on competition, in which XRP must win each transaction against capable rivals, including the incumbent it was supposed to replace. That is a more sober thesis, but it is the one the facts now support.

Frequently Asked Questions

Is XRP going to replace SWIFT?

The 2026 evidence strongly suggests no, at least not in the wholesale way the community long predicted. SWIFT is a messaging network used by over eleven thousand institutions, and instead of being swept away, it has modernized, completing its ISO 20022 data-standard migration and building its own blockchain settlement ledger. That ledger deliberately excludes XRP, keeping value in tokenized bank deposits. XRP has been connected to SWIFT optionally through a Thunes integration, giving banks access to XRP as one liquidity choice, but participation is not required. The realistic picture is XRP complementing the banking network as one optional settlement tool, not replacing the network that coordinates global payments.

What is the difference between SWIFT and Ripple?

SWIFT is a messaging network that carries standardized instructions about payments between banks; it does not move the money itself, which travels separately through correspondent banking. Ripple is a blockchain company whose On-Demand Liquidity product actually moves value, converting a sending currency into XRP, moving it across the XRP Ledger in seconds, and converting it to the destination currency, which removes the need for pre-funded accounts. So SWIFT is primarily the messaging and standards layer, while Ripple targets the settlement layer beneath it. They operate at different points in the payment process, which is part of why they can complement each other instead of being pure substitutes.

Is XRP ISO 20022 compliant?

This is widely misunderstood. RippleNet, Ripple’s payment network, is built to handle ISO 20022 messages and Ripple joined the standards body, which helps its network interoperate with banks adopting the standard. But the XRP token itself is not ISO 20022 certified, because ISO 20022 is a messaging-format standard that does not certify cryptocurrencies or blockchains at all. It governs how payment data is structured, not which asset settles a payment. So the popular claim that ISO 20022 guarantees XRP a central role is a misreading. The standard raises the bar for all payment solutions and arguably benefits SWIFT, the established messaging hub, at least as much as it benefits Ripple.

Does SWIFT’s blockchain ledger use XRP?

No, and this is one of the most important developments for XRP holders. SWIFT’s blockchain shared ledger, which moved into its building phase in 2026, is designed around tokenized bank deposits and deliberately avoids public-network assets like XRP. It is permissioned, keeps value inside regulated accounts, and is built for the control and auditability central banks require. This means SWIFT is creating a path to round-the-clock blockchain settlement that does not involve XRP, solving much of the problem ODL was meant to address without the token. Banks wanting blockchain settlement have an XRP-free option from the network they already trust, which meaningfully tempers the case for inevitable XRP adoption.

How does XRP connect to SWIFT then?

Through a separate integration involving the payments firm Thunes. The arrangement gives the more than eleven thousand banks on SWIFT optional access to Ripple’s liquidity products, including XRP as a bridge asset. A payment can route from SWIFT through Thunes to Ripple’s ODL infrastructure, where XRP settles the leg. The key point is that this access is optional, not mandated. It gives XRP exposure to a vast network of institutions, which is truly valuable for distribution, but it creates demand optionality instead of guaranteed volume, since banks can choose the XRP rail but are never forced to use it over the alternatives available to them.

What does this mean for XRP’s value?

It reframes the XRP thesis from inevitability to competition. The replacement narrative implied XRP would automatically capture global settlement value; the complementary reality means XRP is one optional liquidity tool that must win each transaction against tokenized deposits, stablecoins, including Ripple’s own RLUSD, and SWIFT’s XRP-free ledger. XRP retains real advantages in speed, cost, and round-the-clock settlement, and its optional presence on SWIFT gives it broad distribution. But its value will depend on how often institutions actually choose the XRP rail and whether that volume grows enough to matter against XRP’s large supply, instead of on a wholesale replacement of SWIFT that the current evidence does not support.

This article is information, not investment advice. Details of SWIFT’s and Ripple’s products, integrations, and strategies reflect reporting available as of June 27, 2026, and can change. The competitive landscape in cross-border payments is evolving quickly. Nothing here is a recommendation to buy or sell XRP or any asset. Verify current details from primary sources and consider your own circumstances before making any decision.

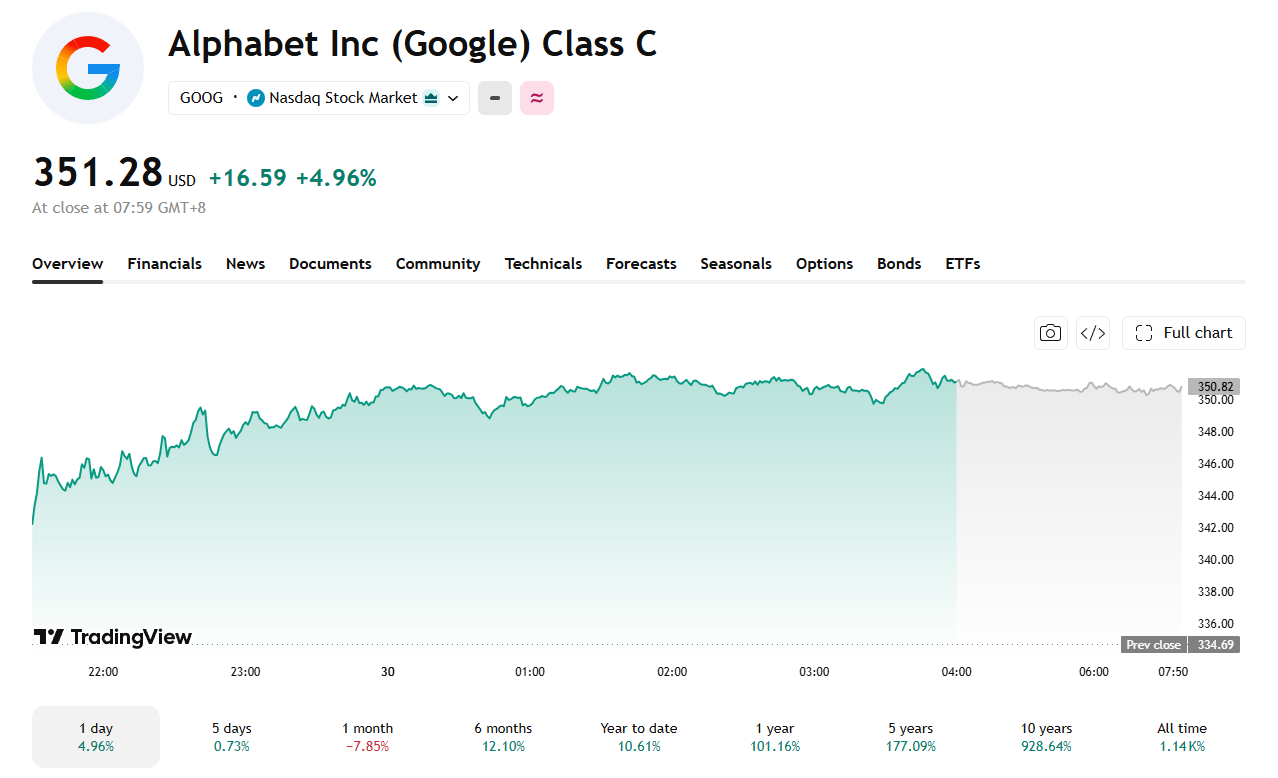

The Dow Jones Industrial Average (DJIA) closed above 52,000 for the first time on Monday, June 29, powered by Alphabet’s blue-chip debut and a broad rally in semiconductor stocks.

The index gained 306.63 points, or 0.59%, to finish at 52,182.74. The S&P 500 rose 1.18% to 7,440.43, and the Nasdaq Composite surged 2.07% to 25,820.14.

Alphabet’s Dow Debut Lifts Sentiment

Alphabet (GOOGL) climbed nearly 5% on its first session as a Dow member after replacing Verizon in the index. The addition carries more symbolic weight than mechanical impact, as the stock already sits in the S&P 500 and Nasdaq 100, limiting forced fund buying from the change.

Despite Monday’s pop, Alphabet is still on pace for its worst month since February of last year, with six of the past seven weeks ending in negative territory. Investor concerns center on AI execution, with Nvidia chip stock flows drawing renewed attention across the sector as compute access tightens.

Semis and Geopolitics Drive the Broader Move

The VanEck Semiconductor ETF gained more than 3%, led by Astera Labs, KLA, and Applied Materials, which rose roughly 16%, 12%, and 11%, respectively.

Macro relief also played a role. The US and Iran agreed to pause hostilities and allow commercial vessels to transit the Strait of Hormuz freely.

Brent and West Texas Intermediate climbed slightly, as traders weighed whether the ceasefire would hold. BeInCrypto previously covered how Iran’s oil ceasefire deals move crude and downstream inflation expectations.

Whether the rally extends into a shortened week ahead of the July 4 holiday will depend on whether the Iran ceasefire holds and if semiconductor momentum carries through.

The post Dow Closes Above 52,000 for First Time as Alphabet Debuts appeared first on BeInCrypto.

U.S. spot bitcoin ETFs lost a net $231 million on Monday, with BlackRock’s IBIT accounting for $300 million of outflows that other funds partly offset, including $50 million into ARKB and $35 million into GBTC, per SoSoValue data.

The outflow lands as risk appetite elsewhere is surging. Wall Street’s technology rally spread into Asia on Tuesday, with the MSCI Asia Pacific index up 1% on the year’s final trading day after a semiconductor rebound helped the S&P 500 snap a five-session losing streak. The Asian benchmark is on track for its biggest quarterly gain in almost 17 years.

South Korea’s Kospi, which crashed 10% in a single session earlier this month, climbed 2.1% to extend its lead as the world’s best-performing major benchmark this year. Samsung is up more than 100% this quarter, and SK Hynix has gained almost 240% since April. The yen slid to its weakest level against the dollar since 1986, a sign investors are funding the AI trade by borrowing in yen.

Bitcoin ETFs are not participating in that capital rotation, however. The same AI infrastructure spending fueling record quarters in Seoul and Tokyo is the trade competing for the dollars that might otherwise flow into bitcoin, a dynamic that has run through the month’s coverage of SpaceX, Anthropic and the chip sector.

Key Highlights

- BitMine acquired 27,084 ETH in the past week, marking its fourth-smallest weekly accumulation this year, pushing total reserves to 5.7 million ETH.

- US-based spot Ethereum ETFs experienced their seventh consecutive week of net redemptions, shedding $273.3 million in the steepest weekly decline since January.

- Sharplink re-entered the market after an eight-month hiatus, acquiring 39,196 ETH valued at $62.4 million across three consecutive days.

- Ethereum has declined approximately 50% year-to-date and approaches the possibility of recording three consecutive quarterly losses.

- Derivatives markets reveal $4.09 billion in short positions compared to $1.31 billion in long positions, highlighting prevailing bearish sentiment among traders.

Ethereum’s market value hovers around $1,580 as the blockchain network contends with diminishing corporate accumulation and persistent outflows from investment vehicles. The cryptocurrency has found it difficult to maintain critical price thresholds throughout June.

BitMine Immersion, holding the distinction of being the largest institutional ETH holder, acquired 27,084 ETH during the previous week. This transaction elevated the company’s aggregate holdings to 5.7 million ETH, representing approximately $9.22 billion in value. The purchase volume represents one of the company’s most modest weekly acquisitions this year.

Simultaneously, BitMine allocated 160,480 ETH to its staking infrastructure. The firm’s staked portfolio now encompasses 4.879 million ETH, producing approximately $211 million in annual staking rewards.

BitMine Chairman Thomas Lee attributed the reduced acquisition pace to end-of-quarter “window dressing” activities. He observed that market participants frequently reduce exposure to underperforming assets during quarterly closings, regardless of positive fundamental developments.

Investment Fund Redemptions Accelerate

US spot Ethereum exchange-traded funds registered their seventh straight week of negative net flows. These investment vehicles experienced redemptions totaling $273.3 million over the past week, representing the most substantial weekly decline since January, based on SoSoValue tracking data.

BlackRock’s iShares Ethereum Trust experienced the largest redemptions among ETF providers. The trend demonstrates retail and institutional fund investors reducing allocations while certain corporate treasuries maintain their accumulation strategies.

This divergence has generated an atypical market dynamic. Corporate balance sheet strategies continued adding ETH exposure while traditional fund investors redirected capital to alternative investments.

Sharplink, another prominent institutional ETH holder, re-initiated purchases following an eight-month dormant period. Blockchain analytics from Lookonchain documented the company’s acquisition of 39,196 ETH valued at $62.4 million through three separate transactions during the previous week.

Arkham Intelligence data identified the initial purchase batch through FalconX on Thursday. Sharplink executed additional transactions on Friday, complemented by substantial over-the-counter trades throughout the weekend.

As of June 21, Sharplink maintained holdings of 876,285 ETH, establishing its position as the second-largest public corporate ETH holder after BitMine. The company has not publicly addressed the rationale behind resuming its accumulation strategy.

Quarter-End Performance and Derivatives Market Positioning

Ethereum has experienced a decline approaching 50% since the beginning of January. This downturn temporarily allowed Tether’s USDt stablecoin to surpass ETH in overall market capitalization during the past week.

Cryptocurrency analyst Max Crypto highlighted in a social media post that ETH approaches the possibility of recording three consecutive quarterly losses for the first time in its history. He characterized this pattern as a structural concern extending beyond temporary price volatility, prompting market observers to monitor whether the asset can prevent a fourth consecutive negative quarter.

Derivatives market information from CW indicated that high-leverage short positions on ETH totaled $4.09 billion. Long positions registered $1.31 billion on the identical platform, suggesting that speculative traders anticipate continued downward price movement.

From a technical perspective, ETH trades beneath its 20-day, 50-day, and 100-day Exponential Moving Averages, which range between $1,670 and $2,004. The Relative Strength Index currently registers 35, while the Stochastic indicator stands at 26, both metrics indicating persistent downward momentum with minimal signals of reversal.

Market analyst Daan Crypto Trades remarked on social platform X that Ethereum has been unable to successfully recapture previous support zones. He indicated that a recovery above $1,750 would represent the initial indication of bullish strength on extended timeframes, whereas a breach below the current $1,500 support level, which has provided a floor on two prior occasions, could trigger a decline toward April 2025 price lows.

Near-term resistance levels for ETH are positioned at $1,626, followed by additional barriers at $1,670 and $1,741. Support zones are established near $1,524, with a secondary support foundation at $1,404.

Key Takeaways

- XRP currently hovers around $1.05, maintaining stability above the critical $1 threshold following a June 25 dip to $1.01—the lowest level in 19 months.

- Tokens flowing out of exchanges increased dramatically, jumping from 40.7 million to approximately 123 million XRP within days, suggesting potential accumulation by holders.

- Spot XRP ETFs recorded their eighth consecutive week of positive inflows, bringing total cumulative inflows to approximately $1.47 billion.

- Network engagement surged with daily active addresses climbing 72% over a two-week period, moving from 23,000 to nearly 39,500.

- Derivatives open interest contracted sharply from 1.3 billion to under 150 million, indicating a significant deleveraging event.

XRP maintains its position around the $1.05 level following a challenging June performance. The digital asset touched approximately $1.01 on June 25, marking its lowest valuation in 19 months, yet purchasing pressure has successfully defended the psychologically important $1.00 threshold in subsequent trading sessions.

While price action has remained subdued, the underlying XRP Ledger has demonstrated notable vitality. The blockchain recorded 4,941 newly created wallets within a 24-hour window, representing the most significant single-day expansion in wallet creation observed over the past three months.

Concurrently, daily active addresses have experienced substantial growth. The metric expanded from approximately 23,000 on June 14 to nearly 39,500 by June 27, reflecting a 72% increase within a fortnight.

Token Movement and Institutional Capital Flow

Blockchain analytics reveal an accelerating trend of tokens being withdrawn from centralized exchanges. The exchange net position change metric shifted from roughly 40.7 million XRP on June 22 to approximately 123 million XRP several days afterward, representing an increase of nearly 200%.

Such withdrawal patterns typically indicate that holders are moving assets into self-custody rather than positioning for immediate sales. Meanwhile, institutional appetite for XRP exposure continues unabated.

Spot XRP exchange-traded funds have maintained positive net inflows for eight consecutive weeks. Total cumulative inflows now approach $1.47 billion, with an additional $22.99 million recorded during the week ending June 26.

Notably, on June 26, XRP-focused ETFs attracted $15.6 million in capital while bitcoin-based products experienced $444.5 million in withdrawals and ethereum funds recorded $12.9 million in outflows.

The derivatives market has undergone significant consolidation. Open interest across primary trading venues declined from a peak exceeding 1.3 billion to beneath 150 million, eliminating substantial speculative positioning that accumulated during XRP’s previous upward movement.

Market intelligence firm Santiment Intelligence highlighted this divergence between price weakness and growing network participation in a recent analysis. The firm observed that new wallet creation and optimistic market sentiment are materializing even as price threatens the $1 level, with sentiment analysis revealing 3.7 positive comments for each negative one—the highest ratio in three months.

Critical Technical Zones Under Observation

XRP has remained confined within a descending price channel throughout the past year. The 20-period exponential moving average, which tracks near-term momentum, currently aligns with the upper boundary of this channel in the $1.18 to $1.22 range.

This region also coincides with a Fibonacci retracement level at $1.178 and a concentration of approximately 22.8 million XRP in cost basis distribution between $1.18 and $1.19. An additional 27.4 million XRP are positioned between $1.21 and $1.22.

These price zones represent areas where previous purchasers may attempt to exit positions at breakeven, establishing resistance. A decisive move above $1.18 followed by $1.22 would push XRP beyond its established downtrend into more neutral technical territory.

For downside protection, immediate support is established near $1.02. A violation of this level could potentially trigger a decline toward $0.87, according to Fibonacci extension analysis.

In the near term, market participants are monitoring $1.06 as initial resistance, followed by the $1.09 to $1.10 zone where previous recovery attempts have encountered selling pressure. A sustained move above $1.20 would represent the first meaningful indication of a potential trend reversal.

The 4-hour relative strength index has recovered to 46 after entering oversold territory, though it remains below the neutral 50 threshold. Price action recently consolidated within a $1.03 to $1.06 range, with peak trading volume occurring on June 29 at 17:00 UTC when 86.5 million XRP were exchanged.

The pickup began about 18 months ago, before MiCA’s first rules took effect, she said. Stablecoin regulations began applying about a year ago, and crypto-asset service providers have been working through a transition period before the July 1, 2026, deadline. After that date, firms relying on legacy national regimes will no longer be able to provide MiCA-regulated services in the EU.

The inquiries come from entrepreneurs frustrated by bureaucracy and regulatory burdens in Europe.

“They’re not just some random guys,” she said. “They’re former founders or current founders, somebody with multiple exits, somebody with years of experience in crypto.”

The deadline is already reshaping the competitive landscape. Binance, the world’s largest cryptocurrency exchange by trading volume, withdrew its MiCA application in Greece last week and notified EU users it would suspend some services while seeking another regulatory route. The company said it remains committed to Europe.

“Our ambitions in Europe remain the same, and we are confident we will secure a MiCA licence in the coming months,” Binance said in a statement to CoinDesk on Thursday.

Rivals are trying to capitalize. OKX and Coinbase (COIN) announced bonuses of up to 8% of total deposits and transfers for new users the following day.

Sovereign wealth funds are reportedly increasing exposure to spot Bitcoin, a development MidChains CEO Basil Al Askari said may reflect growing institutional interest at current price levels. Speaking on Cointelegraph’s “Chain Reaction” podcast on Monday, Al Askari said he could confirm at least one—and potentially two—in the coming weeks—sovereign wealth funds accumulating spot Bitcoin.

While retail participation has slowed, Al Askari pointed to stronger momentum from institutions and corporates, arguing that the present price environment is functioning as an “entry level” for larger funds that can wait through long accumulation cycles.

Key takeaways

- MidChains CEO Basil Al Askari says one, possibly two, sovereign wealth funds are accumulating spot Bitcoin, potentially in the coming weeks.

- Al Askari frames the current price level as attractive “entry level” positioning for mega funds with long time horizons.

- He expects the effect on markets to be gradual rather than a rapid cascade, but sees it as a clear signal to other institutions.

- Coinbase institutional strategy head John D’Agostino earlier said institutional buyers view the dip as an opportunity, particularly among UAE family offices and sovereign-linked investors.

- Despite spot Bitcoin ETF outflows in the U.S., corporate treasuries—especially Strategy—continue adding to BTC holdings.

Sovereign funds add spot Bitcoin exposure

Al Askari’s remarks center on state-backed capital moving into Bitcoin at a time when retail demand appears to be cooling. A sovereign wealth fund is typically a government-owned investment pool funded by national reserves, so the implication is less about short-term trading and more about long-term allocation decisions.

To help contextualize the scale of that player base, the article notes sovereign wealth funds collectively control more than $13 trillion globally, citing Visual Capitalist. Al Askari described these allocations as experiments for institutions that may have been waiting for a more compelling price to begin building positions.

Importantly for investors, he argued that this type of activity is unlikely to trigger an immediate, dramatic repricing. Instead, it can act as a confidence signal—encouraging other institutions that view larger funds as leaders to “start to get involved.”

Why a “long horizon” matters for Bitcoin supply dynamics

Al Askari suggested the strategic value of such accumulation lies in Bitcoin becoming “more and more scarce” over time as larger holders with longer investment horizons lock in supply. In his view, the key mechanism is not just who buys, but how long they plan to hold.

That distinction matters because it reframes the narrative from near-term momentum to liquidity and available float over extended periods. If more institutional capital transitions from sporadic exposure to sustained accumulation, the market’s effective supply can tighten gradually—potentially influencing volatility and depth even when short-term flows look mixed.

“I do think this is what will happen, is that over the longer term period, we’ll start to see Bitcoin becoming more and more scarce as a result of larger holders with much longer time horizons on their holding periods as far as looking at investments.”

ETFs see U.S. outflows even as corporate treasuries buy

The broader picture is mixed across investor segments. According to the source, sustained U.S. spot Bitcoin ETF outflows have totaled more than $4.1 billion so far this month, referencing Cointelegraph coverage of ETF flow performance and noting that Bitcoin ETF outflows are exceeding that threshold.

At the same time, corporate treasuries—particularly Strategy—continue accumulating. The article states that Strategy has scooped up 3,657 BTC this month, pointing to Cointelegraph reporting on the company’s reserve purchases.

This divergence—ETF outflows on one side and corporate accumulation on the other—can be read as a shift in where new demand is showing up. When exchange-traded product flows weaken but corporate balance-sheet demand persists, it suggests the marginal buyer may be changing rather than demand disappearing altogether.

Institutional “discount buying” and sovereign-linked appetite

Coinbase’s head of institutional strategy, John D’Agostino, previously weighed in on how institutional investors interpret the current market. In a CNBC interview earlier this month, D’Agostino said the “dip” is being welcomed by institutional investors, adding that he had just returned from the Middle East and observed that UAE family offices and sovereign-linked investors were not unhappy to buy at a discount.

The remarks underscore a practical reality for large-scale allocation: for patient capital, drawdowns can improve entry terms and reduce the risk of buying at potentially overextended levels. For traders, it also highlights that short-term market declines may not deter longer-term participants—especially those able to execute steadily rather than chase trends.

Known sovereign examples: Mubadala and Bhutan

The source highlights specific sovereign-related examples to illustrate the pattern. It notes that Abu Dhabi’s Mubadala Investment Company invested $437 million in BTC via BlackRock’s iShares Bitcoin Trust (IBIT) shares in February 2025. It also points to Bhutan’s Druk Holding and Investments as an early and more direct sovereign holder, while stating that the company has been selling some BTC this year, referencing Cointelegraph coverage of those sales.

Taken together, these examples point to a broader institutional learning curve: sovereign entities have already tested mechanisms for gaining Bitcoin exposure, and the current phase may be characterized by more deliberate scaling and timing—potentially shifting from ETF vehicles toward spot accumulation, as Al Askari suggested.

For readers, the next thing to watch is whether ETF outflows remain elevated as corporate and sovereign-related buyers continue adding, and whether Al Askari’s “one, possibly two” additional sovereign funds materialize publicly in the weeks ahead. That will help clarify whether this is a one-off window for discounted entries—or the start of a more durable institutional accumulation cycle.

Crypto exchange users in Australia will soon face stricter rules on all transfers as the country’s travel rule is set to come into force on Wednesday, aligning it with similar rules in the EU, US and UK.

From July, all crypto sent and received on locally-regulated crypto exchanges will require users to provide additional information, such as the name of the person the crypto is being sent to or received from, and the name of the platform.

Gabby Lewis, the head of fraud and financial crime at Swyftx, told Cointelegraph that for most exchange users, “the impact should be very limited. They’ll provide the required details once, and then these will be saved for future use.”

The rules are set to bring Australia in line with other countries that have implemented the travel rule for years, which the Financial Action Task Force, an international policy-making body, first extended to crypto in 2019.

Crypto users have long expressed concern that the rule would impact the anonymity of the technology and the risks of data linking crypto transfers to personal information being leaked.

However, Lewis said that the “travel rule isn’t crypto-specific. It already applies across financial services and has been implemented in areas including Singapore, the United States, New Zealand and the UK. Australia is now following suit.”

The rule aims to prevent money laundering, terrorist financing and scams by increasing the traceability of crypto transfers. It will be enforced by the Australian Transaction Reports and Analysis Centre (AUSTRAC), the country’s financial intelligence agency.

Transfers from a regulated crypto exchange to a self-custodial address, such as a cold storage wallet, will also prompt a user to verify and declare that they are the owner of that address.

“We’re generally talking about a quick confirmation that the wallet is theirs,” Lewis said. “The additional steps mainly come into force for transfers that involve another party or another exchange.”

Australia’s travel rule has no minimum value threshold, meaning a transfer of any size will require an exchange to gather information, aligning it with countries including France, the Netherlands and Japan that have no minimum.

Source: Sam Green

Other countries have set minimum reporting thresholds, such as the US, which only collects information on transfers starting at $3,000.

Some crypto exchanges operating in Australia have already begun to implement the travel rule, such as Kraken, which started on March 31, and CoinJar, which started on Tuesday.

Related: Australia passes digital asset bill bringing crypto platforms under licensing

Crypto users online have recently given mixed reactions to the rule, which the Australian parliament passed into law in 2024.

“With these new rules, you can forget about sending crypto anonymously,” a Reddit user wrote earlier this month.

“New travel rule is insane,” another Reddit user wrote earlier in June. “Thinking of moving everything to cold storage instead now.”

In response, one Reddit user said that “the regulated platforms were never anonymous.”

“This is less of a problem than you’re making it out to be unless you’re involved in activities the authorities would be interested in already,” another user wrote.

Magazine: Crypto scammers face death, Aussie CGT makes Asian hubs attractive: Asia Express

Self-exiled Chinese billionaire Miles Guo has been sentenced to 30 years in a U.S. prison after being convicted in a fraud scheme that prosecutors said stole more than $1 billion from investors through multiple ventures, including cryptocurrency.

Summary

- Miles Guo was sentenced to 30 years in a U.S. prison and ordered to forfeit $889 million after his fraud conviction.

- Prosecutors said the scheme raised more than $1 billion from investors through multiple ventures, including the Himalaya Exchange and Himalaya Coin.

- The sentencing comes as crypto related financial crime continues to face tighter enforcement in both the United States and China.

According to multiple media reports, U.S. District Judge Analisa Torres handed down the sentence on Monday and ordered Guo, also known as Guo Wengui, to forfeit $889 million in restitution.

The sentencing follows a July 2024 jury verdict that found Guo guilty on nine fraud and conspiracy charges after prosecutors accused him of raising money from hundreds of thousands of online followers through false investment promises tied to businesses under his control.

Crypto scheme formed part of fraud case

Federal prosecutors had alleged that Guo attracted investors by presenting himself as a critic of the Chinese Communist Party after fleeing China more than a decade ago, while using that reputation to promote fraudulent investment opportunities.

According to the U.S. Department of Justice, one of those ventures was the Himalaya Exchange, a cryptocurrency ecosystem that collected more than $262 million from victims. The department said Guo later spent investor funds on luxury assets, including a mansion and high end vehicles.

Earlier court filings from the DOJ said Guo orchestrated a scheme that defrauded thousands of investors of more than $1 billion after his arrest in March 2023.

At the sentencing hearing, the Associated Press reported that Guo told the court he came to the United States “to destroy the CCP.” AP also reported that Judge Torres said Guo had preyed on supporters seeking democracy in China and had continued to deny causing financial harm.

SEC case remains part of wider enforcement action

Separate from the criminal prosecution, the U.S. Securities and Exchange Commission charged Guo and his financial adviser, William Je, in March 2023 over an alleged fraud that raised hundreds of millions of dollars through an unregistered crypto asset known as H Coin, or Himalaya Coin.

According to the SEC complaint, Guo falsely claimed the token was backed by gold and assured investors they would be reimbursed for any losses. The regulator also accused Guo and Je of diverting investor funds to finance luxury purchases, including a mansion and a Ferrari, while seeking permanent injunctions, civil penalties and the recovery of alleged illegal gains.

The SEC and DOJ announced their actions on the same day in March 2023, with the Justice Department filing a 12-count indictment that included securities fraud, wire fraud, investment fraud and money laundering charges against Guo. William Je was also charged with obstruction of justice, while authorities said they seized about $634 million held across 21 bank accounts linked to the investigation.

Guo is also known for his association with former Donald Trump strategist Steve Bannon. In 2020, the pair announced the New Federal State of China initiative, describing it as an effort to overthrow the Chinese government.

Elsewhere, Chinese authorities have also stepped up enforcement against cryptocurrency-related financial crimes.

China’s Supreme People’s Procuratorate said on June 25 that prosecutors had charged more than 1,200 people for drug related money laundering cases between January 2025 and May 2026, including schemes involving cryptocurrencies.

The disclosure came as China announced a death sentence for a convicted drug trafficker found to have laundered more than 48 million yuan, or about $7 million, through cryptocurrency as part of a cross-border narcotics operation.

The US Supreme Court ruled 5-4 on June 29 that President Donald Trump cannot remove Federal Reserve Governor Lisa Cook, for now. Still, the decision preserves the Fed’s independence at the worst possible time for Bitcoin.

The ruling locks in a hawkish Fed that has already eliminated rate cut expectations for 2026 and put hikes back on the table. High rates keep pressure on zero-yield assets like Bitcoin, and Monday’s decision removes one of the few near-term paths to a more dovish board.

A Hawkish Fed Just Got More Secure

Cook’s survival matters for rate policy. Trump wanted her gone so he could, instead, install a governor more open to rate cuts. The court blocked that move.

The timing stings for crypto markets. The June Federal Open Market Committee meeting eliminated rate cut projections for 2026 entirely and put hikes back on the table. Bitcoin ETF outflows continued through June as investors rotated away from zero-yield assets.

BTC dropped below $60,000 on Monday, meaning it is now down more than 50% from its all-time high.

Monday’s ruling locks in the Warsh-led, hawkish Fed, at least until lower courts resolve the underlying case. Trump cannot sidestep that by firing governors at will.

“This was never about mortgage documents … It was an attempt to remove me on a manufactured pretext because I refused to bow to political pressure.”

— Lisa Cook, Federal Reserve Governor, statement

What Case Does Trump Have Against Cook?

The case against Cook centers on allegations from FHFA Director Bill Pulte, who accused her of mortgage fraud in August 2025. Pulte claims Cook listed two properties, one in Michigan and one in Georgia, as primary residences within weeks of each other in 2021, notably before she joined the Fed board.

Cook’s attorney called the claim baseless, saying it rests on a single ambiguous reference in one mortgage document.

Cook and her allies argue that the timing reveals the real motive. Trump moved to fire her after months of pressuring the Fed to cut rates faster, and Cook had voted to hold rates steady. Ultimately, the court said no to the firing.

Yet, the fact that this case reached the Supreme Court at all is proof of concept. As Trump’s appointment of Warsh showed, political pressure on the Fed does not require firing anyone. It just requires choosing the right chair.

The post Supreme Court Blocks Trump From Firing Governor Leaving Bitcoin with Hawkish Fed appeared first on BeInCrypto.

For years, crypto wallets have served as the gateway to decentralized finance (DeFi). They allow users to store digital assets, sign transactions, and interact with blockchain applications. While these functions remain essential, the next generation of wallets is evolving into something much more powerful: intelligent financial agents capable of managing digital assets autonomously, making informed decisions, and optimizing financial strategies.

This transformation marks a major milestone in the evolution of Web3, where artificial intelligence (AI) and blockchain technology converge to create smarter, more efficient financial systems.

The Evolution of Crypto Wallets

The earliest cryptocurrency wallets were simple tools designed to store private keys securely. As blockchain ecosystems matured, wallets expanded their capabilities by supporting decentralized applications (dApps), NFT management, staking, cross-chain transactions, and token swaps.

Despite these improvements, users still perform most tasks manually. Finding the best yield, monitoring market conditions, rebalancing portfolios, and protecting assets from emerging risks require continuous attention and technical knowledge. Intelligent financial agents aim to eliminate much of this complexity.

What Are Intelligent Financial Agents?

An intelligent financial agent is an AI-powered software system that operates on behalf of a user while respecting predefined rules and permissions. Instead of simply executing commands, these agents analyze blockchain data, evaluate market opportunities, and carry out financial actions automatically.

Unlike traditional automated trading bots that follow rigid instructions, intelligent agents continuously learn from changing market conditions and adapt their strategies based on user preferences and objectives.

For example, an intelligent agent could:

- Monitor multiple DeFi protocols for the highest risk-adjusted yields.

- Automatically rebalance a crypto portfolio.

- Pay recurring blockchain subscriptions.

- Execute cross-chain transfers at the lowest possible cost.

- Protect funds by moving assets away from protocols experiencing security concerns.

- Optimize tax reporting and transaction records.

The wallet becomes more than storage—it becomes an active financial assistant.

How AI Enhances On-Chain Decision Making

Artificial intelligence excels at processing enormous amounts of information far faster than humans. Blockchain networks generate vast streams of real-time data, including liquidity movements, governance proposals, protocol upgrades, transaction volumes, and market sentiment.

AI agents can analyze these data sources simultaneously to identify trends and opportunities that would be difficult for individuals to detect manually.

Rather than asking:

“Which lending protocol currently offers the best return?”

Users may simply instruct:

“Maximize my yield while keeping portfolio risk low.”

The intelligent agent can evaluate multiple protocols, compare risks, execute transactions, and continue monitoring performance after deployment.

Automation Beyond Trading

Many people associate AI in crypto with automated trading, but intelligent financial agents have much broader applications.

They can simplify everyday blockchain interactions by:

- Managing staking positions automatically.

- Claiming and compounding rewards.

- Voting in decentralized governance according to user preferences.

- Managing NFT collections.

- Scheduling recurring payments.

- Executing payroll for decentralized organizations.

- Monitoring wallet security continuously.

This allows users to focus on strategy instead of repetitive operational tasks.

Personalized Financial Management

One of the greatest strengths of intelligent financial agents is personalization.

Every investor has different goals, risk tolerance, liquidity needs, and investment horizons. AI agents can build customized strategies based on these individual preferences.

For example:

- Conservative users may prioritize capital preservation.

- Income-focused investors may maximize staking rewards.

- Active traders may seek short-term opportunities.

- Long-term holders may automate dollar-cost averaging.

Instead of offering generic financial advice, intelligent agents continuously adapt to each user’s evolving objectives.

Challenges and Risks

Despite their promise, intelligent financial agents introduce new challenges.

Security remains the highest priority. Permitting AI systems to manage digital assets requires robust safeguards, including permissioned execution, transaction limits, multi-signature approvals, and transparent audit trails.

Privacy is equally important. AI systems handling sensitive financial information must protect user data while maintaining decentralization whenever possible.

There are also regulatory considerations. As autonomous financial software becomes more sophisticated, governments and regulators will likely develop new frameworks governing AI-driven financial services.

The Future of Autonomous Finance

The long-term vision extends beyond individual wallets.

Future decentralized ecosystems may consist of networks of AI agents collaborating. One agent could negotiate loans, another could optimize liquidity, while another manages governance participation—all operating under user-defined objectives.

In this environment, financial management becomes increasingly autonomous, efficient, and accessible.

Rather than replacing human decision-making, intelligent financial agents serve as trusted assistants that help users navigate increasingly complex decentralized ecosystems with greater confidence.

Conclusion

The transition from traditional crypto wallets to intelligent financial agents represents one of the most exciting developments in Web3. By combining blockchain’s transparency with AI’s analytical capabilities, users can move beyond manual asset management toward autonomous, personalized financial assistance.

As these technologies continue to mature, wallets will no longer function solely as secure storage for digital assets. They will evolve into intelligent companions capable of monitoring markets, executing complex financial strategies, managing risk, and helping users achieve their financial goals with minimal friction.

The future of decentralized finance isn’t just about owning digital assets—it’s about empowering intelligent systems to help manage them responsibly, securely, and efficiently.

REQUEST AN ARTICLE

All 9 Live-Action Batman Actors, Ranked

BITCOIN!!!!!! NOW!!!!!!!!!!!!!!!!!!!!!!!!!!!!

Changes are proposed for some Hamilton primary school catchment areas

-

Sports7 days ago

Sports7 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics4 days ago

Politics4 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics4 days ago

Politics4 days agoPotential 2028er World Cup attendee leaderboard

-

News Videos2 days ago

News Videos2 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Business4 days ago

Business4 days agoAsia stock markets slide as tech shares slump

-

Tech4 days ago

Tech4 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World6 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 days ago

Crypto World5 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World3 days ago

Crypto World3 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business6 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World3 days ago

Crypto World3 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports3 days ago

Sports3 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech2 days ago

Tech2 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World4 days ago

Crypto World4 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World4 days ago

Crypto World4 days agoRTX holders must register wallets before token distribution begins

-

Crypto World5 days ago

Crypto World5 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

You must be logged in to post a comment Login