Crypto World

KOSPI Falls 8%, Triggers Circuit Breakers, as Big Tech Selloff Hits Asia

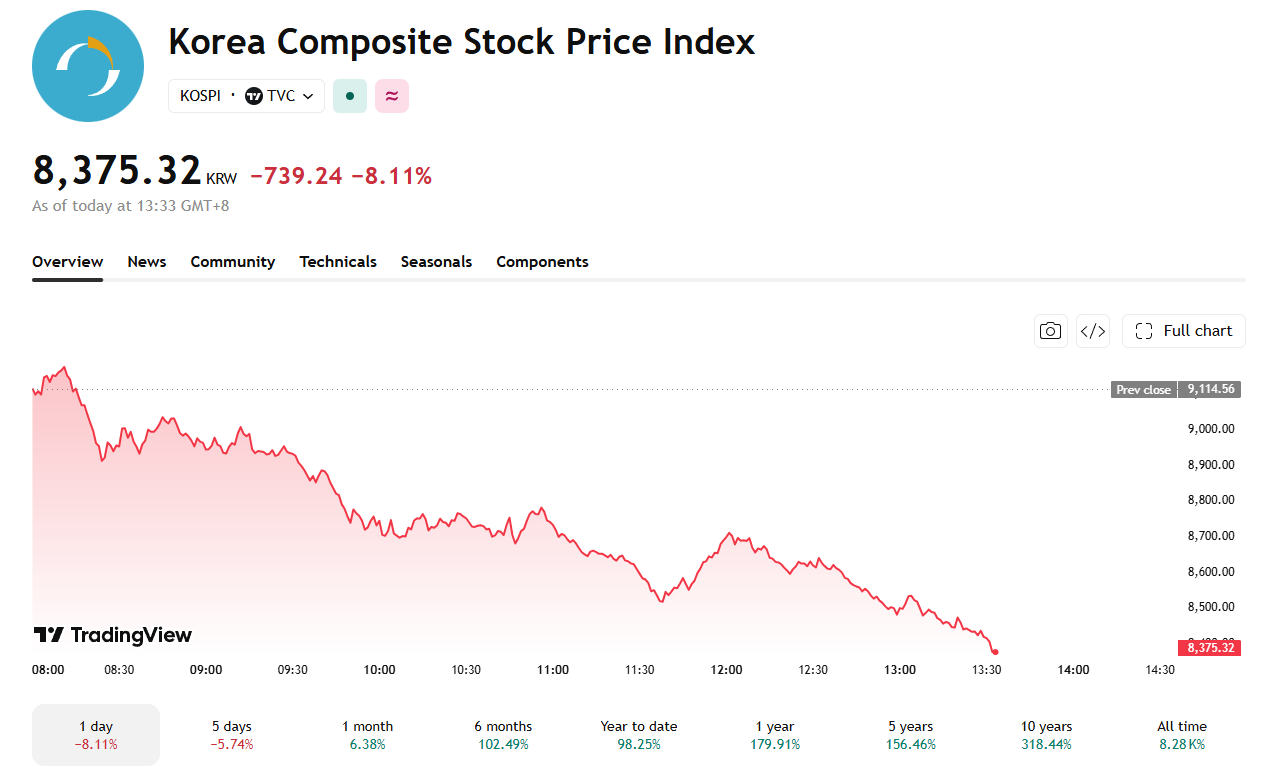

South Korea’s KOSPI crashed more than 8% on June 23, triggering circuit breakers twice, as Japan’s Nikkei 225 broke an eight-session winning streak in a broad selloff driven by US technology stocks.

The moves extended a turbulent stretch for Asian equities as Tuesday’s tech-driven reversal erased early gains across the region. Benchmarks in Taiwan, South Korea, and Japan had each climbed at least 40% this year, making the concentrated semiconductor trade the most exposed when US megacap sentiment shifted.

Circuit Breakers Triggered as KOSPI Freefall Deepens

The KOSPI opened at 9,083.54, down 0.34% from the prior close, then collapsed through the 9,000, 8,900, and 8,800 levels and all the way down to 8,500 in rapid succession. The Korea Exchange triggered a sell-side circuit breaker at 11:40 a.m., then activated a first-stage circuit breaker around 2:40 p.m. as the index sank to 8,375.31, an 8.11% decline on the day.

Wall Street set the tone. Alphabet fell 4.99% after two high-profile AI researchers left the company for rivals. SpaceX shed 16%, its third straight losing session, after the company announced a large investment-grade bond offering that rattled confidence in AI capital spending.

In Tokyo, the Nikkei 225 snapped its recent record run, and is also in freefall, down almost 3% at the time of publishing.

Samsung and SK Hynix Lead Seoul’s Losses

Foreign investors are at the source of the collapse, as there has been net selling in KOSPI shares. Samsung Electronics fell 8.77% to 322,500 won. The drop extended a historic session from the prior day, when Samsung lost the top KOSPI market-cap position to SK Hynix for the first time in 26 years. SK Hynix itself fell a massive 11.55 % to 2.582 million won, despite Micron surging 6.82% overnight.

Han Ji-young of Kiwoom Securities noted that the Magnificent Seven weakness and rising Treasury yields weighed on growth stocks, while falling oil prices tied to US-Iran ceasefire talks could partially cushion the rate burden.

The post KOSPI Falls 8%, Triggers Circuit Breakers, as Big Tech Selloff Hits Asia appeared first on BeInCrypto.

US-listed spot Bitcoin exchange-traded funds (ETFs) finished July in the green despite a late-month wave of selling and BTC price volatility.

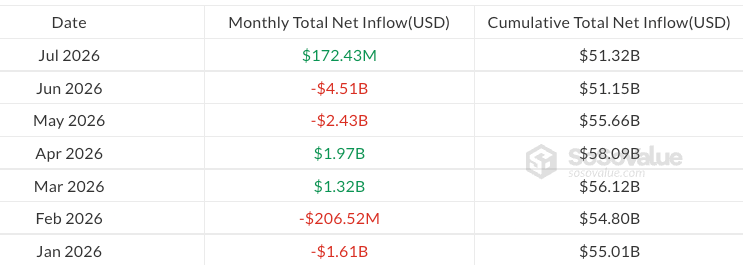

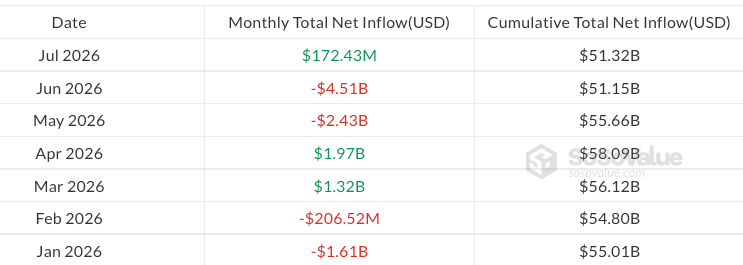

Bitcoin ETFs attracted a modest $172.4 million in net inflows in July, reversing two consecutive months of outflows, according to SoSoValue data.

The monthly inflows came despite a volatile end to July, as the funds logged a $265.4 million net outflow on Friday, marking their largest daily withdrawal since July 13.

July’s return to positive territory improved Bitcoin ETF flows after nearly $7 billion in combined outflows over the previous two months, including the largest monthly outflow of 2026 in June at $4.5 billion. However, the weak finish showed investors remained cautious heading into August.

Bitcoin ETFs remain negative in 2026 with $5.29 billion in outflows

Despite a modest net inflow in July, US-listed spot Bitcoin ETFs have recorded around $5.3 billion in net outflows year to date.

March, April and July were the only positive months of 2026, bringing in a combined $3.46 billion in inflows, while January, February, May and June posted outflows totaling about $8.75 billion.

Monthly spot Bitcoin ETF flows in 2026. Source: SoSoValue

The products have still attracted $51.32 billion in cumulative net inflows since launch, while total net assets stood at $76.29 billion at the end of July.

Related: Bitcoin price sinks to 2-week lows as US stocks fail to copy Asia rebound

Weekly flows turned negative at the end of the month after three consecutive weeks of inflows, with Bitcoin ETFs recording a $61.53 million outflow for the week ending July 31.

Ether ETFs end July with four-week inflow streak

While Bitcoin ETFs faced renewed selling pressure at the end of July, some altcoin ETFs maintained steadier inflows.

Ether ETFs stood out, posting four consecutive weeks of inflows and ending the month with a $365.2 million net inflow, according to SoSoValue.

The inflows marked the second month of positive flows for Ether ETFs year to date after April’s $356 million inflow. Despite the recovery, the products remained about $1.1 billion in net outflows year to date.

XRP ETFs also maintained steady demand, recording $27.3 million in July inflows and marking their fifth positive month of 2026. The products have recorded about $343 million in net inflows year to date, making them one of the stronger-performing crypto ETF categories this year.

Magazine: A quantum roadmap would push Bitcoin much higher: Charles Edwards

The XRP Ledger wants to let banks pay network costs for their users. If validators agree, people could use the ledger without ever buying XRP.

Jazzi Cooper, head of product at RippleX, said the xrpld 3.3.0 release should arrive next week. It carries five proposed changes. One is called Sponsored Fees and Reserves.

Why Using the XRP Ledger Costs XRP Today

Every account on the ledger locks up 1 XRP. That amount cannot be spent or moved. Each extra item an account holds, such as a trustline, locks another 0.2 XRP.

Every transaction also burns a small fee. So a new user has to buy XRP first. Only then can they do anything else.

The upgrade changes who pays. A bank, issuer, or platform can cover both the fee and the locked amount. Users still hold their own accounts and keys.

Cooper called that requirement one of the biggest barriers for new users, and for institutional tokenization on XRPL.

“Users continue to own their accounts and keys, while removing one of the biggest onboarding hurdles: requiring every participant to acquire and manage XRP before they can interact with the network,” Cooper said.

Follow us on X to get the latest news as it happens

What It Means for XRP Demand

XRP trades near $1.06. It is down 1.3% on the day and about 64% lower than a year ago. Its market cap sits at $66.5 billion.

The locked XRP does not vanish under this plan. It simply moves. Sponsors would hold it instead of millions of small users.

That cuts both ways. Everyday users lose their main reason to buy XRP. But a platform signing up thousands of accounts would need far more of it.

Past upgrades offer little guide. Permissioned Domains went live in February with more than 91% validator support. A smaller update followed in May. Neither moved the price much, and ledger use has grown while XRP fell.

2 of the 5 Changes Failed Before

Confidential MPT hides Multi-Purpose Token (MPT) balances from public view. Auditors can still check them when needed. Dynamic MPT lets issuers decide upfront which token settings they may change later.

The last two are second attempts. Batch groups up to eight transactions so they all succeed or all fail. It was pulled in February. Pranamya Keshkamat and Cantina AI’s tool Apex found a flaw that let attackers spend from other people’s accounts.

Permission Delegation was switched off in September 2025. A developer known as tequ reported that it charged fees before checking signatures. Neither ever reached the live network, so no money was lost.

Validators now decide. Each change needs 80% support for two straight weeks. Batch has been rejected once already.

The post XRP Ledger Upgrade Could Make Owning XRP Optional: Will Demand Fall? appeared first on BeInCrypto.

Moneyflip CEO Marcos Arturo Kleiman Tronllan faces a federal murder-for-hire charge after allegedly paying undercover agents $40,000 to kidnap and kill a businessman over an unpaid debt.

Summary

- Kleiman allegedly agreed to pay $40,000 to kidnap and murder a Mexican businessman.

- Prosecutors said the final payments included $5,000 in cash and about 25,000 USDT.

- Undercover agents previously had Kleiman convert approximately $750,000 into cryptocurrency.

- The federal charge carries up to 10 years in prison and a $250,000 fine.

Moneyflip CEO arrested in Miami

Homeland Security Investigations agents arrested Kleiman in Miami on July 30 in connection with a federal complaint filed in San Diego.

Kleiman, 40, is a Mexican citizen and lawful permanent resident of the United States. He previously lived and worked in San Diego, according to the U.S. Attorney’s Office for the Southern District of California.

Moneyflip is a registered money services business offering cross-border currency exchange services. Kleiman previously operated the company as MXN Financial LLC before it changed its name to Moneyflip LLC in 2025.

Investigators began examining Kleiman while investigating currency exchange businesses in San Diego and Imperial counties. Authorities suspected that he used cross-border transactions to avoid Bank Secrecy Act reporting requirements and launder proceeds from drug sales.

The complaint contains allegations rather than proven facts. Kleiman is presumed innocent unless convicted.

Undercover agents converted $750K into crypto

Undercover HSI agents approached Kleiman in February and asked him to convert U.S. dollars into cryptocurrency. The agents allegedly told him that the money came from drug sales.

Prosecutors said Kleiman created an email account and shared its password with the agents. The parties allegedly communicated through unsent draft emails to avoid transmitting messages directly.

Kleiman then allegedly converted approximately $750,000 into cryptocurrency and arranged for the assets to be transferred to an undercover agent’s wallet. Authorities said he charged a 10% fee.

“Kleiman converted approximately $750,000 of United States currency into cryptocurrency and caused the transmission of those crypto coins into an undercover federal agent’s wallet,” prosecutors said.

During those discussions, Kleiman allegedly asked whether the agents could recover a debt from a Mexican businessman and kill him. Prosecutors said he agreed to pay $40,000 for the kidnapping and murder, including two $5,000 advance deposits.

Agents staged murder before 25,000 USDT payment

Kleiman allegedly arranged for a third party to deliver the first $5,000 deposit to an undercover agent in San Diego in May. Prosecutors said he later paid another $5,000 deposit after an agent requested money to reserve the purported killers.

On July 28, the undercover agents showed Kleiman three photographs and a video that falsely depicted the businessman as having been captured, tortured and killed. No murder occurred as part of the operation.

Authorities said Kleiman responded that the agents could count on him to complete the payment. On July 29, he allegedly delivered another $5,000 in cash and transferred approximately 25,000 USDT to an undercover cryptocurrency wallet.

USDT is a dollar-pegged stablecoin issued by Tether. Unlike cash, transfers made through public blockchain networks can leave transaction records that investigators may use alongside messages, surveillance, and other financial evidence.

Federal charge carries a 10-year maximum sentence

Kleiman faces one count of murder-for-hire under Title 18, Section 1958(a) of the U.S. Code. The charge carries a maximum sentence of 10 years in federal prison and a fine of up to $250,000.

The case is being prosecuted by Assistant U.S. Attorneys Michael Deshong and Christopher Beeler. HSI led the investigation with support from the U.S. Postal Inspection Service, Drug Enforcement Administration, Customs and Border Protection, IRS Criminal Investigation, and local law enforcement agencies.

Money services businesses that exchange or transmit convertible virtual currencies may fall under federal Bank Secrecy Act requirements. Registration as a money services business does not represent government approval of a company or its activities.

George Santos said he would attend the 2026 State of the Union. He was also betting on Kalshi that he would skip it. Regulators have now fined him $35,000.

He made $17,570 on that bet. He kept the money for about five months. Now he has to give all of it back.

He Bet Against Himself, and Won

Kalshi is a US exchange where people trade contracts on real events. Federal derivatives rules cover it, not state gambling rules.

The contract was simple. It asked who would show up at the State of the Union. Santos traded it between February 12 and February 25.

While he held those bets, he posted about his plans on X. The US Commodity Futures Trading Commission (CFTC) says those posts were misleading. Its order came out Friday.

Prices then moved his way. He walked away with $17,569.98. He now owes that back, plus a $17,500 fine.

He is also banned from trading for three years. He admitted nothing.

This is not his first problem. Congress expelled Santos in 2023. Trump commuted his fraud sentence last year.

Kalshi Caught It in Seconds

No regulator spotted this first. The exchange did, and so did other traders. Kalshi CEO Tarek Mansour described how fast it happened.

“within seconds it was flagged by our system. We opened investigations and within minutes we had like a hundred whistleblower complaints,” Axios reported, citing Tarek Mansour, Kalshi CEO.

That speed is the real story here. On a stock exchange, staff dig through records weeks later. On these markets, the people holding the other side notice immediately.

They have every reason to look. Their own money is at stake. Most Kalshi traders lose as it is, so they watch each other closely.

Regulators are circling too. In February, the CFTC said it would go after insider trading and manipulation on markets like these. Former officials had warned about weak oversight earlier.

Kalshi has since punished three congressional candidates who bet on their own races. A White House teleprompter operator lost his job in July. Reports said he won over $100,000 betting on Trump’s speeches.

Santos Says He Did Nothing Wrong

His lawyer, Joseph W. Murray, says the deal proves nothing.

“Mr. Santos has settled without admitting any of the Commission’s allegations, findings, or conclusions,” Joseph W. Murray, via MS NOW.

Kalshi is running its own case against him as well. If it collects any money, it says it will try to repay the traders he beat.

The timing is awkward, though. New York sued the company on the same day. The state calls it illegal gambling and wants up to $36 billion.

Kalshi says it is a regulated exchange, not a casino. It is fighting that case while chasing a $40 billion valuation.

Catching Santos in seconds may be the best argument it has.

The post George Santos Kalshi Bet Cost Him $35,000: Who Caught Him First? appeared first on BeInCrypto.

A Hong Kong woman reportedly lost around $3.3 million after an online romantic partner directed her to a fraudulent cryptocurrency investment platform.

Summary

- 25 romance-linked investment scams were reported in Hong Kong between July 24 and 30.

- Combined losses from the cases approached nearly $9 million, according to local police statistics.

- One victim saw supposed returns of more than 800% before the platform blocked withdrawals.

- Hong Kong also recorded a 92.1% rise in online employment scams during early 2025.

Crypto romance scams cost victims nearly $9M

Hong Kong authorities recorded 25 investment fraud cases involving online romantic relationships during the week ending July 30, according to police statistics cited by Binance Square News.

The reported losses totaled nearly HK$70 million, or roughly $9 million. One case accounted for more than a third of that amount.

A 50-year-old insurance professional reportedly met a person online who presented himself as a car dealer. After establishing a romantic relationship, the person persuaded her to invest in virtual currencies through an unfamiliar platform.

The victim continued transferring money after the platform displayed rising account balances. By last month, it claimed that her portfolio had generated returns exceeding 800%.

However, the platform denied her withdrawal request. The purported romantic partner and an alleged investment adviser then stopped responding, leaving the woman with cumulative losses exceeding HK$26 million or around $3.3 million.

Authorities did not disclose which cryptocurrencies were involved or whether any of the transferred funds had been recovered.

Fake profits kept the victim investing

The case follows a common pattern in relationship-based cryptocurrency fraud. Scammers first build trust through dating applications, social media or messaging services before introducing an investment opportunity.

Victims are then directed to trading websites or applications controlled by the fraudsters. These platforms may display fabricated profits, allow a small initial withdrawal, or encourage victims to increase their deposits.

The scheme typically becomes apparent when a victim attempts to withdraw a larger amount. Operators may block the transaction or demand additional payments described as taxes, processing charges or penalties.

Hong Kong police urged investors to treat investment recommendations from newly established online contacts with caution. Warning signs include guaranteed returns, unusually high profits and requests to transfer funds through an unfamiliar platform.

The FBI describes the same method, saying criminals control the supposed investments and often steal all funds deposited by victims.

Hong Kong employment scams also surged

The romance cases add to a wider increase in online fraud affecting Hong Kong residents.

Police recorded 2,148 online employment scams between January and May 2025, up 92.1% from the same period a year earlier, according to figures reported by the South China Morning Post and HRD Asia.

Reported losses increased from HK$260 million to HK$480 million, an 89% rise. Authorities registered 621 cases in May alone, with 60% originating on WhatsApp and another 22% on Telegram.

Investigators attributed much of the increase to “click farming” schemes. Fraudsters initially pay participants small commissions for completing simple online tasks, such as following social media accounts or purchasing products to inflate a seller’s activity.

After gaining trust, scammers ask victims to commit larger sums for higher-paying assignments. Withdrawal attempts are then rejected, with operators claiming the victim made an error or damaged a company system and must pay a penalty.

US crypto fraud losses reached $7.2B

Similar investment schemes remain a major threat to US users. Cryptocurrency investment fraud produced $7.2 billion in reported US losses during 2025, making it the country’s largest category of financial loss reported to the FBI’s Internet Crime Complaint Center.

The FBI’s 2025 report said scammers commonly approach victims through social media, dating platforms and unsolicited messages before moving conversations to private messaging services.

US authorities advise victims to stop sending money immediately and preserve wallet addresses, transaction hashes, platform domains and communications. The FBI also warns against paying supposed recovery services, which may operate a second scam targeting people who have already lost funds.

Hong Kong police similarly advised users not to lower their financial safeguards because of emotional attachment or trust. Investors should independently verify platforms and avoid offers promising guaranteed or abnormally high returns.

One of the most recognizable and well-known figures in the cryptocurrency space has displayed a somewhat controversial approach to his Ethereum investments over the past few months.

The most recent data shared by Lookonchain doubled down on his sporadic approach, as he had realized another loss.

The analytics resource informed that the former BitMEX CEO deposited nearly 2,365 ETH into Cumberland and Galaxy Digital earlier today, and received 4.3 million USDC in return.

According to the analysts, this meant that his selling price was at $1,821 given the asset’s retreat over the past few days from a multi-month peak of $1,980.

Hayes secured a sizeable loss of $241,000 (or 5.3%) on this trade because he went on an accumulation spree during the aforementioned ascent from ETH. As previously reported, he bought 7,213 ETH for $13.87 million at an average price of $1,923.

Arthur Hayes(@CryptoHayes) bought high and sold low again!

Over the past 2 hours, he deposited 2,364.38 $ETH into Cumberland and Galaxy Digital, receiving 4.3M $USDC in return.

His selling price was $1,821, resulting in a loss of $241K (-5.3%).

He had previously bought 7,213… pic.twitter.com/4AVZpjANZD

— Lookonchain (@lookonchain) August 1, 2026

What’s interesting here is that this is not the first time Hayes has lost on ETH by buying high only to sell low weeks later. His previous major ETH trade was several weeks ago, when he accumulated at prices well over $1,900 again after the token jumped to $1,950.

Once it started to nosedive, though, Hayes was quick to sell off his stash at an average price of under $1,700. Thus, he incurred another major loss in just weeks, while ETH’s price rebounded shortly after.

The post Arthur Hayes Does It Again: Buys ETH High, Sells It Low appeared first on CryptoPotato.

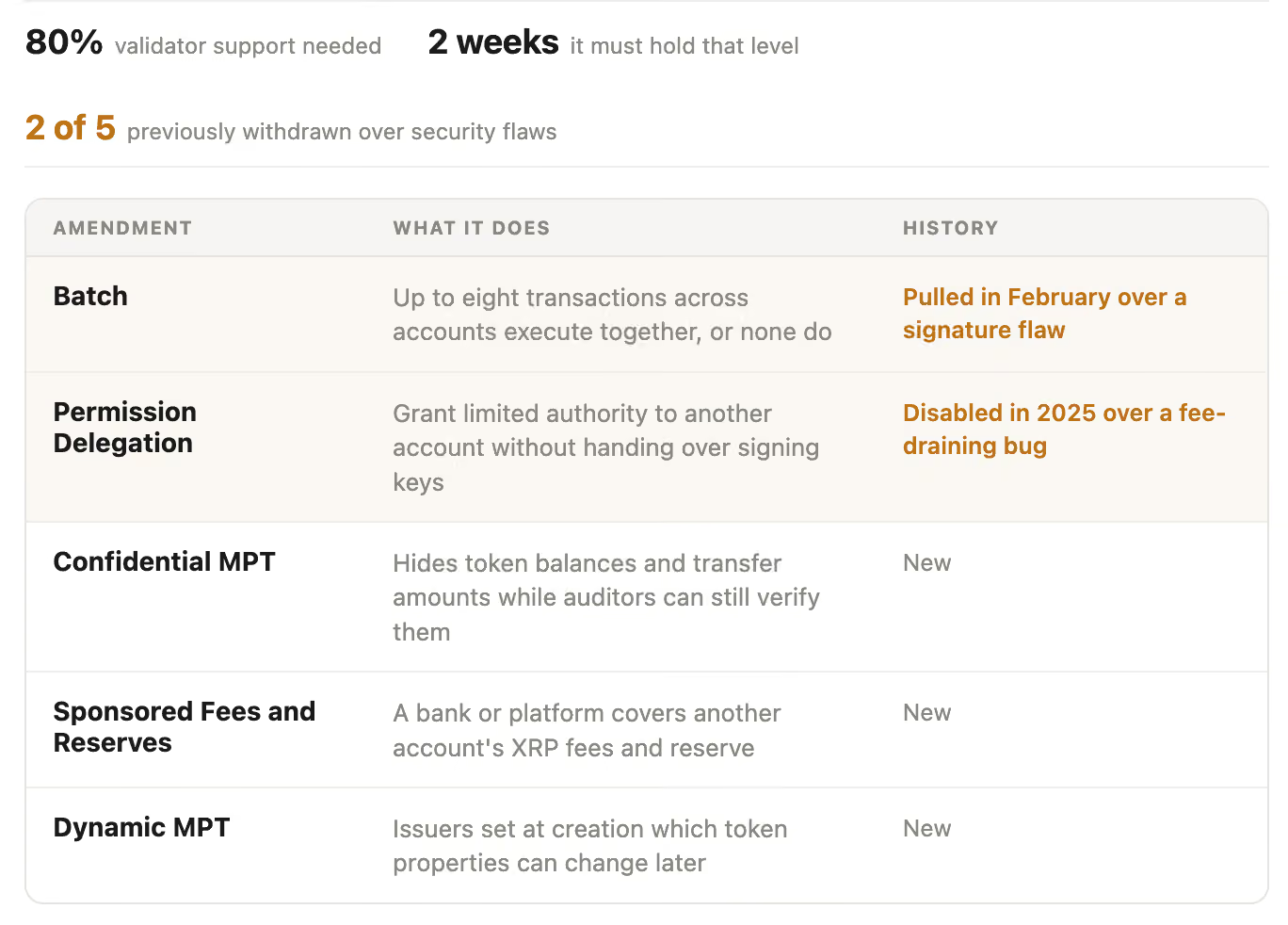

XRP Ledger developers are preparing five proposed amendments for the upcoming xrpld 3.3.0 release, targeting privacy, atomic settlement, and easier institutional onboarding.

Summary

- Five proposed amendments are expected to accompany the xrpld 3.3.0 software release.

- Confidential MPT would support private token balances and transfer amounts using cryptographic proofs.

- Batch transactions would enable delivery-versus-payment and atomic settlement across multiple accounts.

- Amendments require validator approval before they can activate on the XRP Ledger.

XRP Ledger v3.3.0 targets institutional transactions

Jazzi Cooper, head of product at RippleX, outlined the proposed changes in a post on X. The xrpld 3.3.0 release is anticipated next week, although releasing the software will not immediately activate its amendments.

“XRPL has already proven it can support tokenized assets at scale. Now it’s time to put these assets to use: global transfers, trading, collateralizing, and settling,” Cooper said.

She added that the five amendments would move the network closer to supporting those activities. The proposals cover confidential token transactions, transaction batching, delegated permissions, sponsored costs, and adjustable token properties.

Each amendment must pass through the XRP Ledger’s validator-governed approval process. Amendments affecting transaction processing generally need at least 80% support from trusted validators for two consecutive weeks before taking effect.

The upgrade follows the activation of fixCleanup3_2_0 on July 29. XRPScan data showed that the amendment received support from 30 of 35 participating trusted validators, equivalent to 85.71%.

Its activation made version 3.2.0 the minimum software release compatible with the updated mainnet rules. Nodes running version 3.1.0 or earlier became amendment-blocked and could no longer follow validated ledgers correctly.

Confidential MPT would add token privacy

Confidential MPT would add native privacy features for Multi-Purpose Tokens on XRPL. The proposal uses elliptic-curve encryption and zero-knowledge proofs to conceal token balances and transfer amounts while allowing authorized verification.

Issuers and holders could keep transaction data private from the public while granting access to a designated third party, such as an auditor or regulator. The arrangement is intended to balance commercial confidentiality with institutional reporting and compliance requirements.

“For financial institutions, privacy is often a prerequisite for using public blockchain infrastructure,” Cooper said.

The proposal could be relevant to US-regulated institutions evaluating public blockchains for tokenized assets. Banks, broker-dealers and asset managers often need transaction confidentiality while retaining records that can be reviewed by auditors or regulators.

However, the amendment would represent a network-level technical function, not regulatory approval for any specific financial product or activity.

Batch and delegated permissions support settlement

The proposed Batch amendment would allow transactions involving multiple accounts to execute atomically within one ledger. Either every part of the batch would succeed, or the entire operation would fail.

The structure can support delivery-versus-payment, where the transfer of an asset and its corresponding payment occur together. It could also reduce settlement risk in more complicated workflows involving several accounts or assets.

Permission Delegation would allow an account holder to grant narrowly defined transaction permissions without transferring control of the account’s signing authority. An institution could therefore authorize a treasury or operations team to perform specific tasks while keeping its issuance keys under separate control.

Sponsored Fees and Reserves would address another onboarding issue by allowing a bank, issuer, or platform to cover transaction fees and account reserves for users.

“Users continue to own their accounts and keys, while removing one of the biggest onboarding hurdles: requiring every participant to acquire and manage XRP before they can interact with the network,” Cooper said.

Dynamic MPT would make issued tokens adjustable

Dynamic MPT, the fifth proposed amendment, would let issuers modify selected token properties after issuance. Adjustable fields could include transfer fees, metadata, and other predefined features.

Issuers currently may need to create a replacement token when important terms require changes. Dynamic MPT is intended to provide limited flexibility without requiring an entirely new issuance, although the final amendment specifications will determine which properties can be changed.

The proposed features arrive as XRPL records increased tokenized real-world asset activity. RWA.xyz data showed that the network added approximately $2.6 billion in RWA value during the six months through July 26, excluding stablecoins.

That ranked XRPL second among tracked networks for net RWA inflows, behind BNB Chain at about $3 billion and ahead of Stellar at roughly $2.1 billion. XRPL’s combined distributed and represented RWA value reached approximately $4.38 billion.

Validator operators will be able to review the amendments as their specifications become available. Activation will depend on whether each proposal independently secures the required consensus after xrpld 3.3.0 is released.

Validators (entities that supply their resources to run and maintain a network) were advised to reject it, and an emergency server release marked it unsupported to prevent activation. No funds were lost, because it never reached the main network.

Permission Delegation, which lets an institution grant another account narrowly scoped authority without handing over full signing power, was disclosed as vulnerable in September 2025 and disabled.

The bug allowed one account to charge transaction fees to another and potentially drain its balance. The ledger’s documentation has listed both amendments as obsolete since, to be replaced by revised versions.

The other three are new. Confidential MPT combines zero-knowledge proofs, which let someone prove a statement is true without revealing the underlying data, with elliptic-curve encryption, so that balances and transfer amounts on Multi-Purpose

Tokens stay private while auditors or regulators can still verify them when required.

Sponsored Fees and Reserves lets a bank or platform cover another account’s XRP fees and reserve requirement, removing the need for every user to acquire XRP before transacting.

Lastly, Dynamic MPT lets an issuer specify at creation which token properties can be changed later, avoiding a full migration to a new token when fees or metadata need updating.

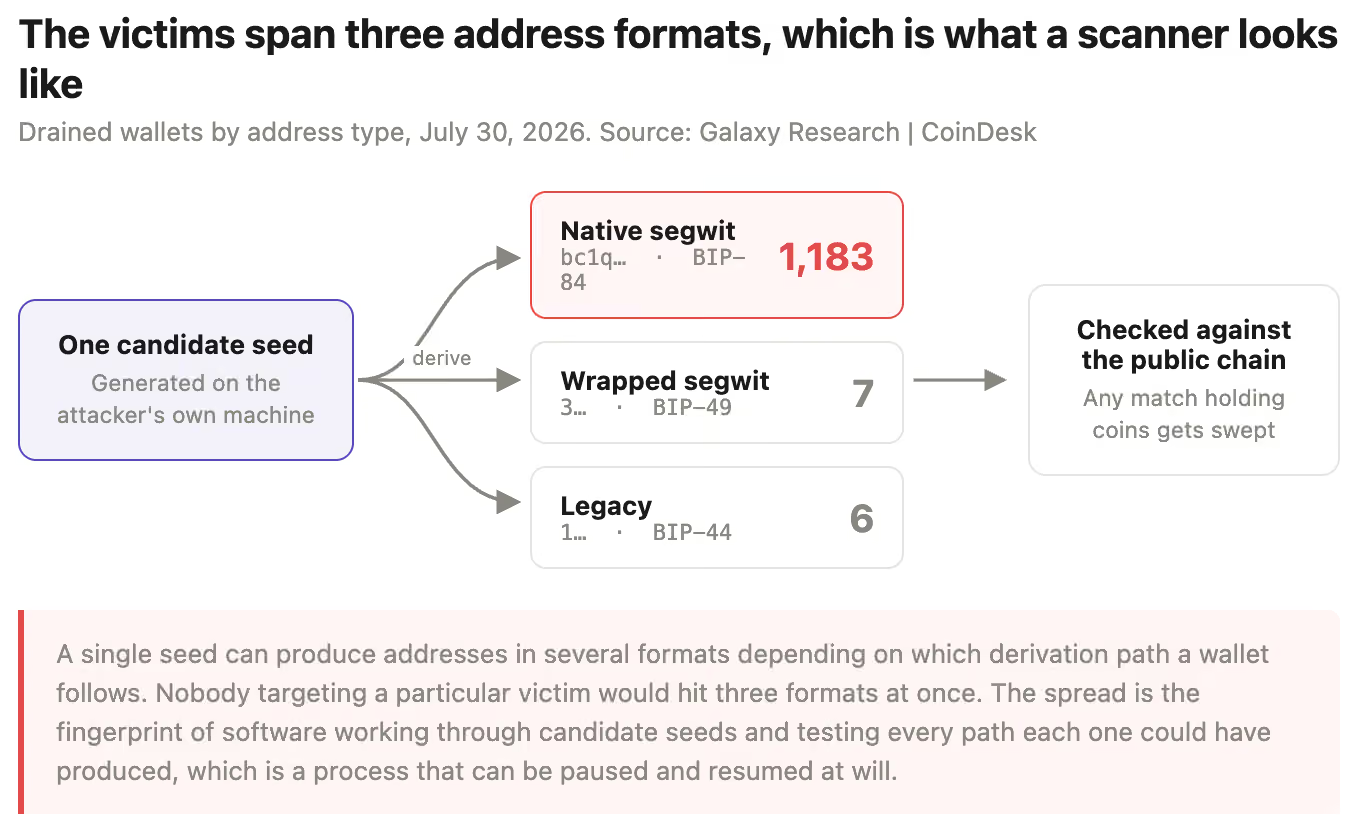

Every step of that runs on the attacker’s machine. The victim’s device is not involved at any point and could be powered off in a safe on another continent.

Galaxy’s breakdown shows the process running. Of the drained wallets, 1,183 used the modern native segwit address format, seven used an older standard and six an older one still. Nobody targets a specific victim across three address formats at once.

That is systematic enumeration, checking each candidate seed against every path it might have produced. The operator can widen the search, refine it and return whenever they choose.

Galaxy warned further waves are likely if owners do not move their funds.

Nor can an owner determine whether they are exposed. There is no test to run against your own wallet that reveals whether your seed sits inside the reproducible range.

Attack might not be fully finished

Coinkite, Coldcard’s maker, has warned Mk3 owners and says its newer devices are unaffected, while Block’s report places the Mk2, Mk4, Q and Mk5 in scope as well. Until that is resolved, anyone who generated a seed on the affected firmware has to assume the worst rather than verify it.

The attacker did make one mistake, however.

Block’s Clay Garrett said on X that the operator used a paid account at a “well-known blockchain data provider” to query the source addresses during the sweeps, and that the provider’s internal logs matched the suspected workflow with what he called extraordinary specificity, down to the number, timing and sequence of requests.

Bitcoin tried but failed at $65,000 on several occasions in the past week, and there are now multiple and different signals suggesting that another leg down is on the cards.

From war escalation to ETF withdrawals, let’s dive in.

Macro Factors

Let’s start with the Wednesday developments on US soil when the central bank decided to leave interest rates unchanged. At first glance, this doesn’t sound too bearish, right? After all, the alternative was to hike them, and there was a real possibility.

However, history shows that essentially all recent FOMC meetings, no matter what the outcome was, have been followed by a BTC price correction. Popular analysts have caught this rather negative pattern, which materialized with a $3,000 price decline over the past few days.

On the plus side, we can argue that the Friday correction to a 2-week low of $62,400 has priced in that almost mandatory post-FOMC retracement.

But there’s another macro factor that tends to harm risk-on assets like bitcoin: the war in the Middle East. Tension escalated over the past 24 hours, which included Iran reportedly striking tankers under US escort in the Strait of Hormuz.

Subsequent reports from the WSJ claimed that Trump has ordered a fresh attack on Iran to get it to surrender. According to CBS News, the US plans to attack Iranian energy assets, and this substantial escalation is expected to begin over the weekend.

Internal Reasons

The first in this section comes from the ETF behavior. The financial vehicles had a solid three-week run in which they attracted over $200 million in net inflows. However, the tides turned once again last week, with $61.53 million in net outflows. Friday was the day that changed the course, as investors pulled out over $265 million to reverse the $233 million in net inflows on Thursday.

Lastly, let’s explore a technical tool. Ali Martinez warned that the TD Sequential, a metric used to determine whether the underlying asset might reverse its price trend soon, has flashed a major sell signal on the 3-day chart.

The analyst added that this red sign comes as August begins, which has historically been associated with BTC pullbacks.

“History doesn’t have to repeat, but it’s a setup worth watching,” he added.

One for the Bulls

Let’s not begin the month only with negativity and review the opposite side of the coin. Michaël van de Poppe noted earlier that BTC could be primed for a major rebound due to its historical connection with the Nasdaq and South Korea’s KOSPI. Both major indices skyrocketed at the end of the business week, with KOSPI notching a massive 18% surge.

“The last time this happened, Bitcoin rallied to $83,000,” said van de Poppe. His expectation contrasts Ali Martinez’s warning for a weak start to August.

An enormous bounce on the Nasdaq and therefore a massive weekly candle, just as $KOSPI has bounced upwards.

I repeat, the last time this happened, #Bitcoin rallied to $83,000.

I would expect to see a strong start of August coming week for #Bitcoin as a response to the current… https://t.co/EJF8PcmOSI

— Michaël van de Poppe (@CryptoMichNL) July 31, 2026

The post BTC Price Warning: 4 Reasons Bitcoin Could Drop Further Next Week appeared first on CryptoPotato.

Bunnie Xo Prepared To Make Surprising Pivot After Jelly Roll Split

Enterprise cloud infrastructure uptake shows no sign of slowing

Chief Financial Disaster Episode 1.#funny #comedy #couple #marriage #relationship

-

Sports5 days ago

Sports5 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business2 days ago

Business2 days agoWhy Trees Belong on the Risk Register

-

Fashion14 hours ago

Fashion14 hours agoWeekend Open Thread: Wit & Wisdom

-

Politics10 hours ago

Politics10 hours agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Tech5 days ago

Tech5 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World7 days ago

Crypto World7 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics5 days ago

Politics5 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Politics4 days ago

Politics4 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos5 days ago

News Videos5 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Entertainment4 days ago

Entertainment4 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Crypto World6 days ago

Crypto World6 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Business3 days ago

Business3 days agoMajor shareholder moves on Canyon

-

Politics6 days ago

Politics6 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

News Videos2 days ago

News Videos2 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World1 hour ago

XRP Ledger v3.3.0 brings five institutional features

-

Entertainment6 days ago

Entertainment6 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

Crypto World3 days ago

Crypto World3 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech4 days ago

Tech4 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos3 days ago

News Videos3 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics2 days ago

Politics2 days agoLuke Littler’s dominance sparks GOAT debate

You must be logged in to post a comment Login