Crypto World

Lending Pool Heist: Are Trump Crypto Insiders Setting Up To Crash DOLO Crypto?

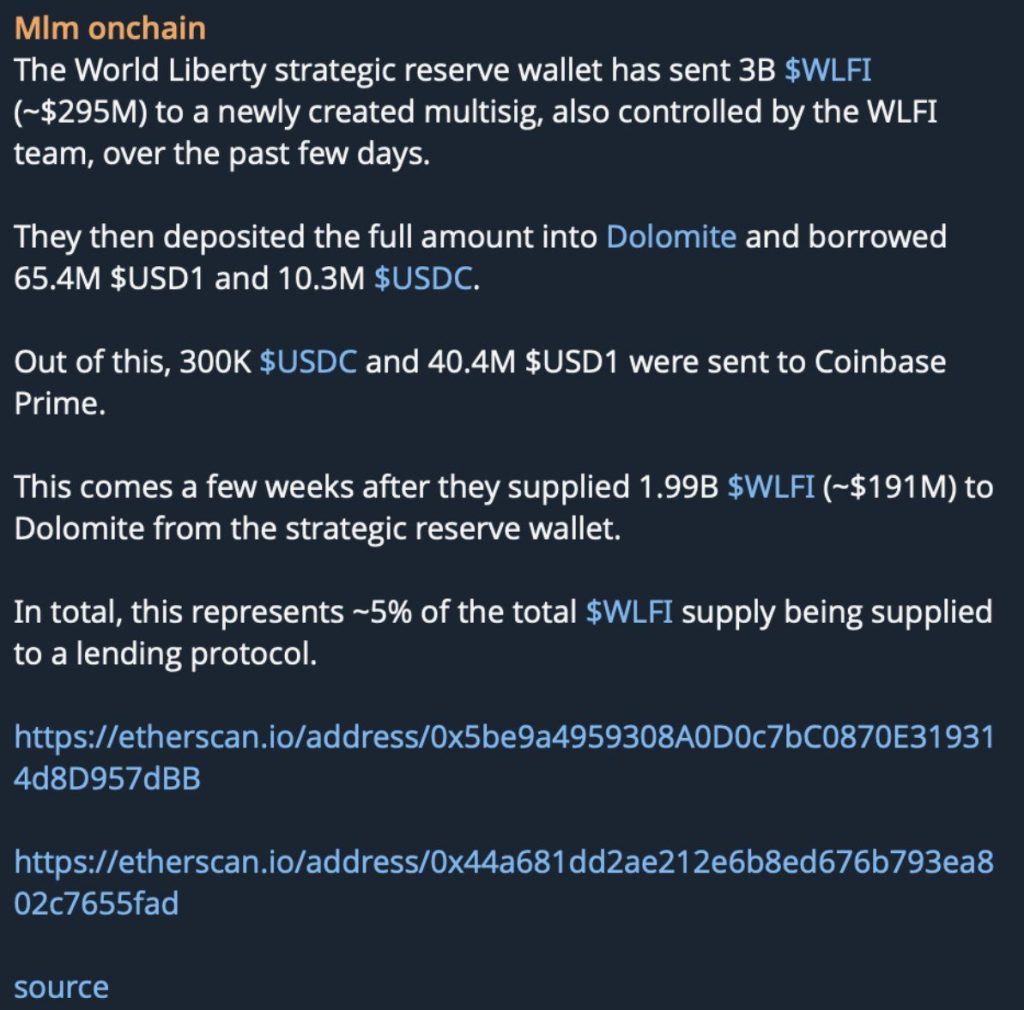

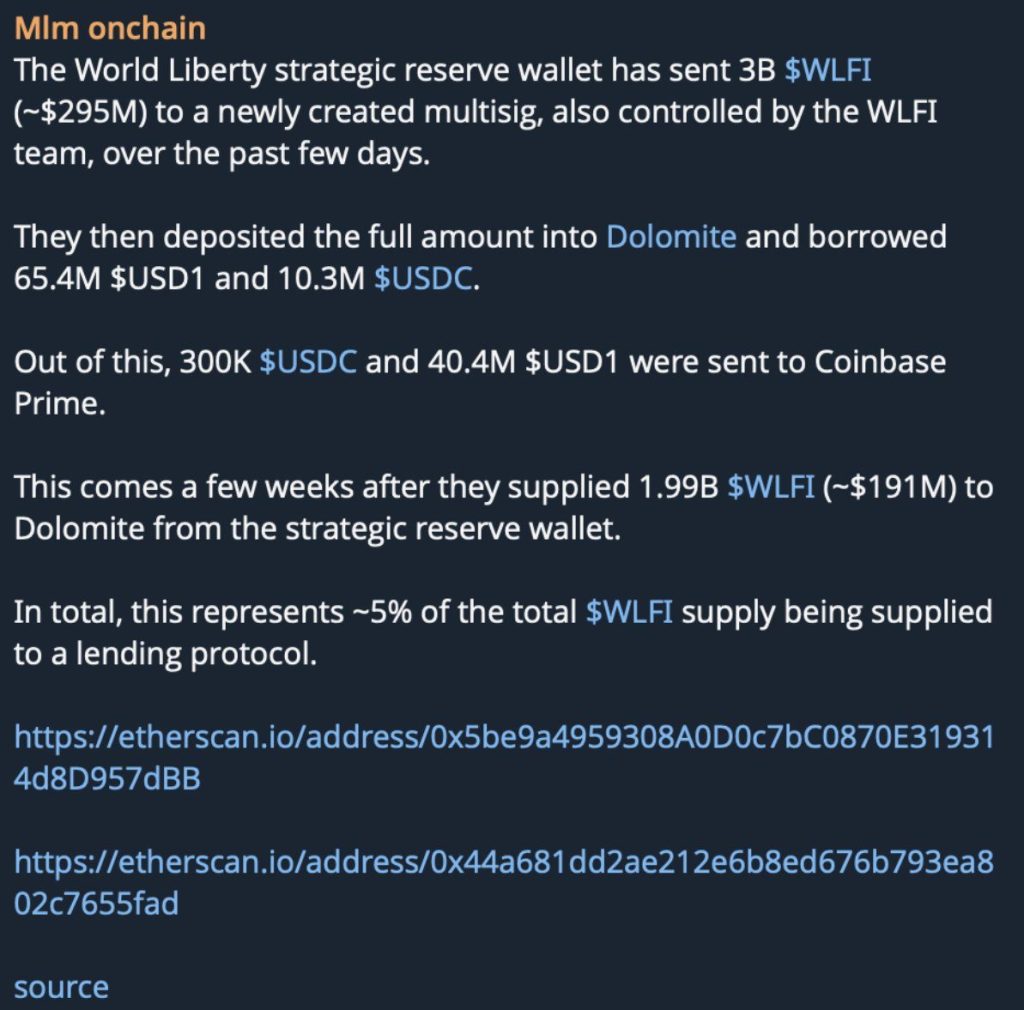

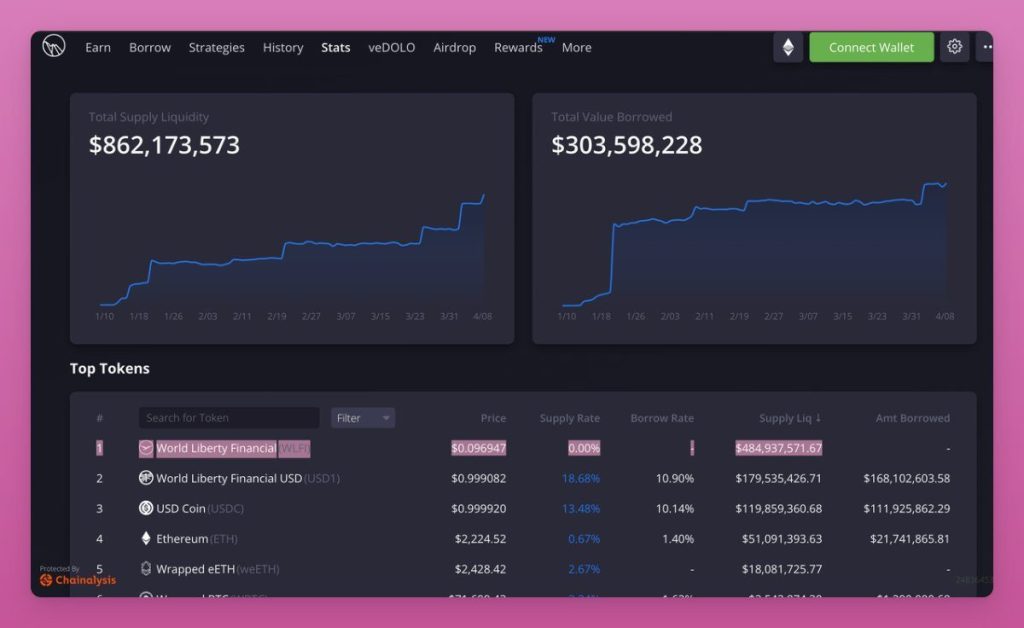

Are Trump crypto insiders back at it again? $484 million in Trump WLFI crypto tokens deposited on Dolomite Protocol. Borrowed against for USDC. And a governance token with almost no real market depth sits as the collateral backstop.

If this unwinds, Dolomite lenders don’t get a haircut; they get wiped.

DeFi analyst Ignas flagged the pattern on X, identifying the leverage structure as a potential systemic threat to Dolomite’s lending pools. The on-chain footprint is already public. The question isn’t whether the risk exists – it’s whether lenders understand what they’re sitting inside.

- The Deposit: Approximately $484M in $WLFI tokens has been deposited into Dolomite Protocol as collateral.

- The Mechanism: That collateral is being used to borrow USDC – extracting real stablecoin value against a token with minimal on-chain liquidity.

- The Bad Debt Risk: If $WLFI price drops sharply, collateral value falls below outstanding USDC debt, leaving Dolomite lenders with unrecoverable DeFi bad debt.

- The Yield Trap: USDC lending APY on Dolomite has spiked to 13.5% – attractive on the surface, but potentially unredeemable if a bank run triggers on bad debt confirmation.

- The Political Trigger: Analysts tie the likely $WLFI dump window to the fading political utility of the token post-cycle – a timeline tied directly to the Trump orbit’s exit incentives.

- What to Watch: DOLO’s $15M market cap makes it acutely vulnerable to protocol insolvency fears; any public confirmation of bad debt could detonate the token in hours.

Explore: The best pre-launch token sales with asymmetric upside potential

How the $484M Trump WLFI Crypto Leverage Play Actually Works – and Where It Breaks

The structure is direct and that’s what makes it dangerous. Entities linked to World Liberty Financial deposited $484M worth of WLFI into Dolomite Protocol, using those tokens as collateral to borrow USDC.

On paper, it looks like a standard DeFi leverage position. In practice, it’s a liquidity time bomb.

WLFI is a governance token. It has politically generated demand and almost no organic secondary market depth.

That means the $484M figure is a valuation on-paper, not $484M that can actually be liquidated into the open market without collapsing the token’s price by 60%, 70%, or more in a single session.

The collateral isn’t real in any liquidation scenario that matters.

When collateral value drops below the outstanding USDC borrow, and with WLFI’s liquidity profile, the threshold is not far, Dolomite’s liquidation engine cannot recover the debt.

No buyer exists at the price needed to make lenders whole. That’s the DeFi bad debt scenario: the USDC is gone, the collateral is worthless at scale, and the protocol is left insolvent in all but name.

Ignas’s alert on X specifically called out the borrow pressure dynamics, USDC lending rates on Dolomite have already spiked to 13.5% as the protocol attempts to attract fresh liquidity to service the growing borrow demand.

That rate spike is not a yield opportunity. It’s a distress signal. Similar warning patterns preceded the Stabble protocol’s 62% TVL collapse on Solana, where liquidity pressure built silently before the exit hit.

The math on DOLO exposure is brutal at this scale. A $15M market cap token absorbing a protocol-wide insolvency event involving nine figures of bad debt doesn’t survive the news cycle intact.

What DOLO Lenders Are Actually Facing – The Bad Debt Exposure Quantified

DOLO sits at approximately $15M in market cap. That number matters because it tells you exactly how much bad news the token can absorb before the math becomes unsurvivable.

Dolomite does not appear to operate a protocol-level insurance fund sufficient to cover a nine-figure bad debt event. There is no backstop that absorbs $484M in underwater collateral.

IYKYK.

New USDC incentives from @worldlibertyfi are now live on Dolomite.$USDC

→ 14.02% APY

→ 6.52% WLFI

→ 0.59% oDOLO https://t.co/in1nMNXWjz pic.twitter.com/mfgtv5mhu7— Dolomite

(@Dolomite_io) April 7, 2026

The 13.5% USDC APY that Dolomite is currently advertising to new depositors is the yield trap Ignas explicitly warned about.

Depositors chasing that rate are walking into a pool that may not be redeemable at par if the borrow position unwinds badly. This is the same dynamic that burned depositors in DeFi platform controversies where advertised yields masked structural insolvency risk.

If bad debt is confirmed on-chain – whether through a WLFI price collapse or a forced liquidation event – DOLO’s reaction will be immediate. A $15M cap token doesn’t need institutional selling pressure to crater. Retail panic alone is sufficient at that size.

Discover: The Best Crypto Presales Live Right Now

The post Lending Pool Heist: Are Trump Crypto Insiders Setting Up To Crash DOLO Crypto? appeared first on Cryptonews.

Cryptocurrency exchanges are taking a growing market share from traditional finance (TradFi) trading venues through tokenized commodities products, but the mainstream adoption of tokenized precious metals remains limited by pricing and liquidity issues.

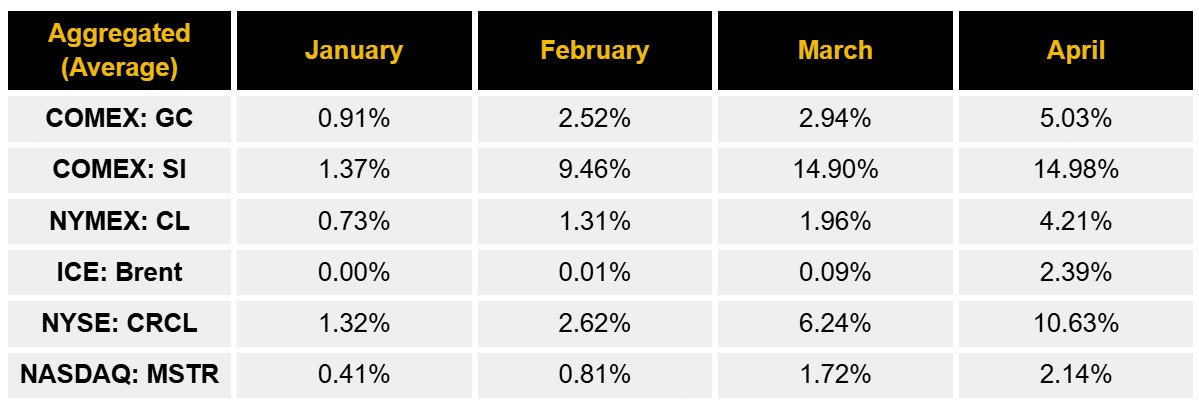

Silver perpetuals have reached about 40% of the equivalent volume of the Comex Silver (SI) Contract at their peak, the world’s largest silver futures market, which accounts for over 70% of global exchange-traded silver futures volume, according to a Thursday report from Binance Research.

During March and April, tokenized silver accounted for 14.90% and 14.98% of the Comex’s volume, respectively, up from just 1.37% in January.

The growth suggests crypto exchanges are capturing more demand for round-the-clock exposure to traditional assets, particularly in metals-linked perpetuals, but analysts at Kaiko said liquidity depth and price formation still pose major obstacles to wider adoption among traditional investors.

Crypto TradFi perps need reliable pricing, strong liquidity

Tokenized commodities offer 24/7 trading, which can create vulnerabilities compared to TradFi gold and silver futures, where the holiday and weekend close create “natural circuit breakers that actually protect market quality,” Kaiko research analyst Laurens Fraussen told Cointelegraph.

This exposes tokenized commodities to degraded order book debt, widened spreads and less reference pricing from closed traditional venues.

Legacy commodities offerings avoid these issues through centralized clearing, consolidated liquidity, standardized contracts and “coordinated operating hours that prevent liquidity deserts,” Fraussen said, adding that crypto needs “better chain abstraction and unified liquidity aggregation” to compete with TradFi.

Related: NYSE taps Securitize for 24/7 tokenized securities platform

Despite the infrastructure concerns, tokenized gold perps have surpassed the gold futures trading volumes of several regional commodity exchanges, a trend seeing monthly acceleration, according to Binance Research.

Binance Research also said gold perpetuals outpaced several regional commodity exchanges in March, reaching 401% compared to gold futures trading on the Japanese energy commodities futures exchange TOCOM, 228% of India’s Multi Commodity Exchange (MCX) and 216% of the Dubai Gold & Commodities Exchange (DGCX).

Binance attributed part of this growth to “market-moving events” that routinely occur on weekends, which would leave investors exposed to gap risks through traditional venues operating under regular trading hours.

Magazine: Can Robinhood or Kraken’s tokenized stocks ever be truly decentralized?

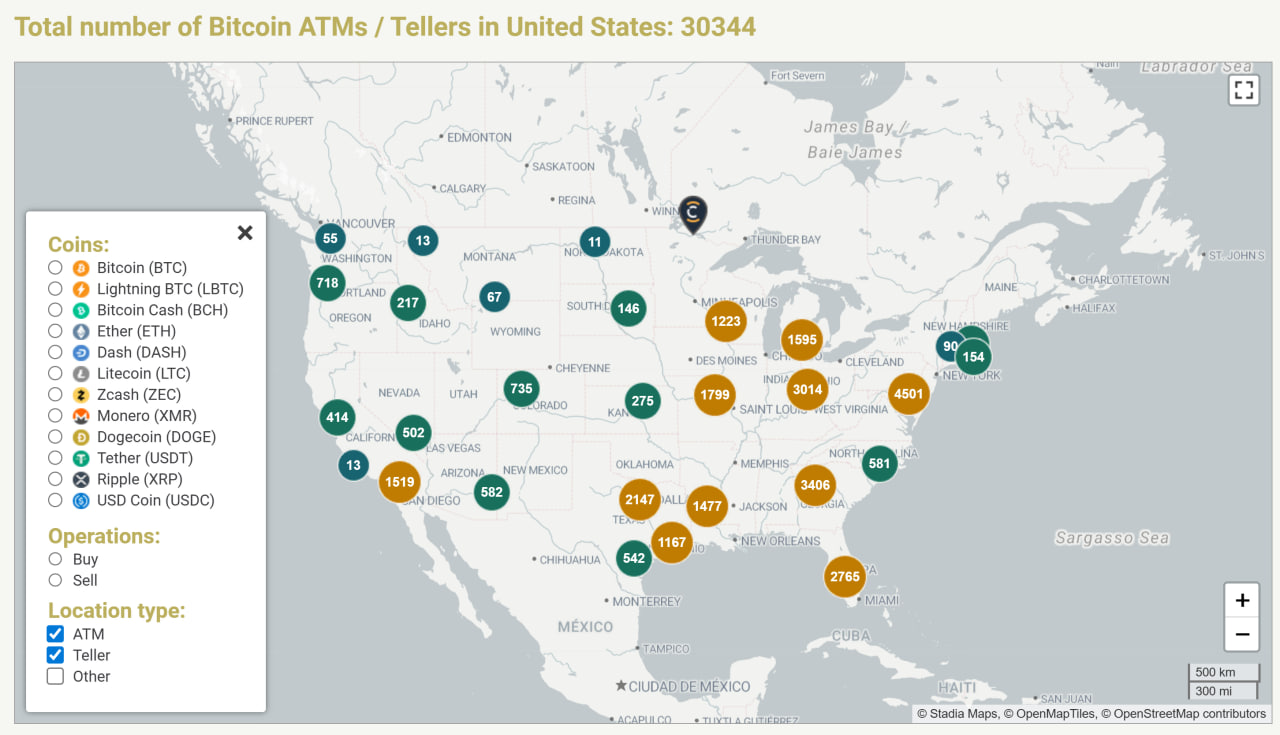

Crypto ATM operator Bitcoin Depot revealed that it lost about 50.9 Bitcoin, worth roughly $3.7 million, after a hacker gained access to some of its internal systems.

The breach happened on March 23 after the attacker took control of credentials linked to Bitcoin Depot’s corporate Bitcoin (BTC) wallets, according to a Monday filing with the US Securities and Exchange Commission. The company said that customer accounts, platforms and personal data were not affected.

Bitcoin Depot added that the attack has not had a major impact on daily operations, and said it has insurance that may cover some of the losses. “As the investigation of the incident is ongoing, the full scope, nature and impact of the incident are not yet completely known,” the filing states.

Shares of Bitcoin Depot jumped sharply on Wednesday, closing at $2.74, up $0.37 or 15.61% on the day, with additional gains in pre-market trading pushing the price to $2.90, a further 5.84% increase, according to data by Yahoo! Finance.

Related: Bitcoin Depot enters Hong Kong as part of Asia expansion

Bitcoin Depot under pressure

Bitcoin Depot has been facing growing legal and regulatory pressure across several US states. The company recently had its money transmission license suspended in Connecticut, along with a temporary cease-and-desist order, with regulators citing violations such as high fees and failure to fully refund scam victims.

The company has also faced a lawsuit from Massachusetts alleging overcharging and facilitating scams, and paid $1.9 million in Maine to compensate affected users.

In June 2024, Bitcoin Depot also experienced a data breach that exposed the personal information of 26,732 customers. The breach was linked to an external system, and authorities cleared the company to issue notifications only after the probe concluded in June 2025.

Related: Australia’s financial watchdog may gain power to ban crypto ATMs

US cities move to ban crypto ATMs

US cities are increasing pressure on crypto ATMs as concerns over fraud grow. Stillwater, Minnesota, has banned crypto ATMs after residents lost large sums to scams, while Spokane, Washington, introduced a citywide ban in June, calling the kiosks a “preferred tool for scammers” following a spike in fraud cases.

Haverhill, Massachusetts, is also considering banning crypto ATMs, with a proposed ordinance citing fraud and money laundering risks that would require all machines to be removed within 60 days if approved.

Magazine: Bitcoin may take 7 years to upgrade to post-quantum — BIP-360 co-author

Banks are approaching stablecoins cautiously despite rapid market growth, reflecting early-stage strategy and rising structural concerns, according to a report by S&P Global Market Intelligence.

According to the Wednesday report, the question is no longer whether stablecoins will endure, but how they will reshape business models, infrastructure and revenue, For banks, the trade-offs are sharp, spanning deposit risk, modernization costs and new competition.

A wait-and-see stance still dominates. S&P Global’s Q1 2026 U.S. Bank Outlook survey found just 7% of 100 mostly smaller institutions are developing frameworks, with none actively piloting, underscoring how exploratory strategies remain.

“Most financial institutions remain early and cautious,” said Jordan McKee, director of fintech research at S&P Global Market Intelligence, in emailed comments. “Our survey of U.S. banks shows that stablecoin strategy is still largely exploratory, with limited internal development and no active pilots among smaller institutions.”

Stablecoins, digital tokens pegged to assets like fiat currencies or commodities, have become a core layer for payments and settlement in crypto, widely used in trading and cross-border flows. The market is dominated by Tether’s USDT, followed by Circle Internet’s (CRCL) USDC.

The stablecoin market has grown rapidly into a roughly $300 billion-plus sector, with total market capitalization surpassing $316 billion in early 2026 after nearly doubling since 2023, according to multiple data sources.

Transaction volumes have also surged into the tens of trillions annually, underscoring rising use in trading, payments and cross-border transfers, while forecasts point to continued expansion, potentially reaching $500 billion or more in the near term as institutional adoption accelerates.

Pressure is building. The report pointed to growing concern over deposit cannibalization and customer migration, alongside a surge in stablecoin mentions on earnings calls following the GENIUS Act’s passage in July 2025.

Competition is also intensifying. S&P Global highlighted a wave of nonbanks pursuing charters to house stablecoin issuance, custody and settlement within regulated entities, positioning themselves as credible alternatives.

Banks are also wary of yield-like incentives in stablecoin ecosystems that could compete with deposits, even as direct interest payments remain restricted.

Responses will diverge. S&P Global analysts expect large, global banks to explore issuing tokenized deposits or bank-backed digital assets, while regional and midsize lenders focus on facilitating access via fiat on- and off-ramps. Regardless of strategy, banks will remain key gateways between fiat and stablecoin networks, but doing so will require significant upgrades to legacy systems ill-suited for real-time digital asset activity.

Cross-border banks face the strongest push to modernize as payments shift to multi-rail systems combining traditional, real-time and tokenized networks. Interoperability and wallet infrastructure will be critical, with large banks building multi-network connectivity and smaller firms leaning on fintech partners. Secure custody and embedded compliance are expected to become standard, the report added.

Read more: Stablecoin rewards restrictions can slow but not stop Circle’s USDC, says Citigroup

BitMEX has released its Q1 2026 derivatives report, highlighting a sharp rise in trading activity for traditional finance perpetual swaps (TradFi Perps), driven by increased demand for tokenised commodities and equities.

According to the report, TradFi perpetual swaps grew from 0.03% of total crypto derivatives volume in December 2025 to 1.72% by the end of Q1 2026, reaching $30.7 billion in weekly trading volume. This expansion was supported by new product launches across prominent exchanges and macroeconomic events, including increased volatility in commodities markets.

“Q1 marked a clear inflection point for TradFi perpetuals, with volume growth driven by real market demand for 24/7 access to commodities and equities,” said Stephan Lutz, CEO at BitMEX. “What we’re seeing is the early formation of a structurally different market, one that removes the constraints of traditional trading hours and introduces new forms of price discovery and liquidity.”

BitMEX has introduced a range of TradFi perpetual products as part of this shift, expanding its derivatives offering to provide continuous access to commodities and equity markets.

The report identifies commodities as the primary growth driver, with trading volume increasing more than 65,000% during the quarter. Precious metals such as silver and gold led early momentum, while crude oil trading accelerated in March amid geopolitical tensions, reaching $6.9 billion in weekly volume.

Equity perpetuals also saw significant growth, rising more than 900% to $4.9 billion in weekly volume. Activity was concentrated in crypto-adjacent equities and major technology stocks, reflecting continued convergence between digital asset markets and traditional finance instruments.

The report further notes structural differences between perpetual swaps and traditional Contracts for Difference (CFD), particularly in areas such as transparent price discovery, peer-to-peer execution, and continuous market access.

Unlike CFD-based models offered by some platforms, these products enable direct market participation, with pricing determined by underlying market dynamics rather than broker-led mechanisms. These characteristics have contributed to increased participation from both retail and professional traders.

Market expansion was also shaped by exchange-level developments. BitMEX recorded more than 1,300% growth over the 90-day period while Binance captured a significant share of new volume following its entry into the category.

In addition, funding rate disparities across exchanges created arbitrage opportunities. The report highlights cases where traders could capture yield through cross-exchange positioning, with some spreads exceeding 100% annualised returns under specific conditions.

Looking ahead, BitMEX expects continued growth in TradFi perpetual markets, supported by broader asset listings across Forex, commodities, and more, increasing institutional awareness, and ongoing demand for 24/7 trading access. The report suggests that weekly trading volumes could approach $100 billion as additional asset classes enter the market.

The full report can be found on BitMEX’s blog.

About BitMEX

BitMEX is the OG crypto derivatives exchange, providing professional crypto traders with a platform that caters to their needs with low latency, deep crypto native and especially BTC liquidity, and unmatched reliability.

Since its founding, no cryptocurrency has been lost through intrusion or hacking, allowing BitMEX users to trade with confidence that their funds are secure and that they have access to the products and tools required to be profitable.

The post BitMEX Report Finds 500%+ Increase in Tokenised Commodities and Equity Perpetuals appeared first on BeInCrypto.

BitMEX co-founder Arthur Hayes has publicly challenged reports that Iran is collecting Bitcoin (BTC) tolls from oil tankers transiting the Strait of Hormuz.

His skepticism echoes a growing chorus of crypto voices questioning whether Tehran’s crypto toll demands have any on-chain substance behind them.

Iran’s Crypto Toll Demand Meets Blockchain Skepticism

The controversy stems from a report on Bitcoin tolls at the Strait of Hormuz. According to Hamid Hosseini, spokesperson for Iran’s Oil, Gas and Petrochemical Products Exporters’ Union, laden tankers must email cargo details to Iranian authorities.

They then receive a toll assessment of roughly $1 per barrel of oil on board.

Payments must be made in cryptocurrency or Chinese yuan. BTC was explicitly cited as an accepted option. Fully loaded supertankers could face fees of up to $2 million, roughly 281 BTC at recent prices.

The payment window is reportedly just seconds long, designed to make funds difficult to trace or seize under Western sanctions.

The Islamic Revolutionary Guard Corps (IRGC) enforces compliance, with non-compliant vessels risking denial of passage.

Hayes responded on X with a pointed challenge.

“I’ll believe Iran is charging a toll in $BTC when I see a tx linked to a vessel’s toll payment. Otherwise, it’s just the IRGC trolling the western filthy fiat financial system,” Hayes challenged in a post.

Strait Remains Blocked as Doubts Mount

Despite a two-week US-Iran ceasefire, shipping data shows minimal tanker traffic. According to reports citing intelligence firm Kpler, no oil or gas tankers have passed through since the ceasefire took effect.

Hundreds of vessels remain waiting, and the waterway that normally handles roughly 135 ships per day remains largely restricted.

Earlier Bloomberg reporting indicated some vessels had paid tolls in yuan or stablecoins like Tether (USDT) for IRGC-escorted passage before the ceasefire.

However, no BTC-specific payments have been verified on-chain.

Other renowned accounts amplify the skepticism, citing “geopolitical shitposting” as the reason the story transcends BTC-only to any crypto or yuan within minutes.

Meanwhile, a Mossad-linked commentary account raised an additional wrinkle. It claimed Iran listed the Trump-linked USD1 token as an accepted payment method, framing the move as a potential geopolitical provocation.

What Comes Next

BTC surged roughly 5% on the initial reports, signaling that markets treated the news as a bullish adoption signal.

Yet the EU has publicly stated that freedom of navigation must be ensured without any payment or toll.

If a verifiable on-chain transaction surfaces linking BTC to a specific vessel’s toll, it would represent one of the largest real-world sovereign uses of Bitcoin for energy-related payments.

Until that proof appears, Hayes and much of the crypto community remain unconvinced.

The post Arthur Hayes Calls Iran’s Bluff: Show Me the Bitcoin or It’s Just IRGC Theater appeared first on BeInCrypto.

Bitcoin Depot Inc. reportedly failed to spot a data breach that resulted in the loss of over 50 bitcoins (BTC) worth $3.7 million for three days.

The BTC ATM operator disclosed the loss of 50.9 BTC in an SEC filing earlier this week, stating that the attacker gained access to its IT systems and its digital asset settlement accounts on March 23.

This, it says, allowed them to move the BTC from company-controlled wallets.

However, according to subsequent research from onchain sleuth ZachXBT, the breach actually occurred three days earlier on March 20.

“On April 6, 2026 Bitcoin Depot disclosed in an SEC 8K filing it uncovered an incident on March 23, 2026 which resulted in 50.9 BTC ($3.6M) stolen,” wrote Zach on Telegram.

“However the report did not include theft addresses so I manually traced out the incident onchain and found 19 high confidence theft addresses from March 20.

“This means it took three days for Bitcoin Depot to notice the funds were missing from its business.”

Read more: Inside the $280M Drift hack: weeks of setup, minutes to drain

Zach continued, “A delta of 3.55 BTC (54.45 BTC total) vs 50.9 BTC reported was found indicating other employee personal accounts may have also been impacted.

“54 BTC ($3.7M) flowed to KuCoin, a crypto exchange increasingly used by illicit actors.

“At the time of my post the theft addresses still have not been reported in any compliance tools I use.”

According to the SEC filing, Bitcoin Depot is continuing to investigate the nature and scope of the incident with the assistance of unnamed “third-party specialists.”

It also says it’s “working with its outside cybersecurity experts to further reinforce its information technology systems and to prevent future unauthorized access.”

It also reassures users that no customer personally identifiable information was accessed, but does add that the “investigation remains ongoing.”

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Canary Capital has filed registration with the SEC for a Pepe ETF, marking what appears to be the first attempt to create and ETF for the “blue-chip” memecoin in the U.S.

Canary Capital filed a registration with the U.S. Securities and Exchange Commission for what appears to be the first U.S. spot Pepe ETF on Wednesday, April 8, 2026. The filing represents a formal submission to the SEC for a potential exchange-traded product tied to the Pepe memecoin.

The move comes amid growing institutional interest in cryptocurrency-based ETF products. If approved, the ETF would provide regulated exposure to Pepe, the fourth-largest memecoin by market capitalization.

Sources: SEC

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

CoreWeave (CRWV) and Meta (META) have broadened their existing partnership, originally valued at up to $14.2 billion, with a new agreement worth around $21 billion.

As part of the deal, CoreWeave will supply dedicated cloud capacity to Meta through 2032, helping power the development and rollout of its AI technologies.

The infrastructure will span multiple locations and feature early deployments of NVIDIA’s (NVDA) Vera Rubin platform, aimed at boosting efficiency, reliability, and scale.

The NVIDIA Vera Rubin platform is the next-generation AI supercomputing architecture is expected to mark a massive shift from simple “Generative AI” to “Agentic AI,” whereby AI becomes more proactive in executing steps towards its goals rather than relying on human prompts.

A key focus of the CoreWeave-Meta agreement is inference, reflecting the industry’s shift toward running AI systems continuously rather than just training them.

“This is another example that leading companies are choosing CoreWeave’s AI cloud to run their most demanding workloads,” said CEO Michael Intrator.

The deal signals that large tech companies are increasingly securing long-term compute resources to support AI-driven services. Shares of CoreWeave rose 3% in pre-market trading on Thursday.

Read More: Mark Zuckerberg’s Meta is planning stablecoin comeback in the second half of this year

Meta Platforms is stepping up its presence in the fast-moving social commerce space, introducing new tools that connect creators, artificial intelligence, and advertising more closely to actual purchases, particularly across Instagram and Reels.

Summary

- Meta Platforms is rolling out new tools that let brands turn Instagram Reels into shoppable content by linking product catalogs with creators.

- The company is expanding AI-driven ad tools, including automated video creation and product optimisation, improving conversions and lowering acquisition costs.

- Meta is also preparing new AI models, including Muse Spark, as it scales its ecosystem across WhatsApp, Facebook, and Instagram to stay competitive.

The latest rollout signals a shift from passive product discovery toward a system where engagement can translate more directly into measurable sales outcomes.

A key part of the strategy centres on expanding the role of creators in the shopping journey. Businesses across 22 countries, including India, will soon be able to share product catalogues with creators, enabling them to tag and link items directly within Reels content. The change effectively turns creator posts into shoppable storefronts, narrowing the gap between entertainment and commerce.

Meta said its creator marketplace now includes more than 1.5 million discoverable creators. New filters within Ads Manager allow brands to identify suitable partners with more precision, improving campaign alignment.

“This makes it easier than ever for businesses to quickly identify creators who are a good match for their goals and likely to perform well in their partnership ads campaigns,” the company said.

“Partnership Ads has moved influencer marketing from a brand-building line item to a marketing channel tied to outcomes,” said Vikas Chawla, pointing to the growing ability to measure creator-led performance.

Meta is also increasing its focus on Reels as a space where users are more likely to engage with ads. The company has expanded its “Reels Trending Ads” into categories such as business, finance, travel, and entertainment, placing brands alongside content that is already drawing strong engagement.

“We’re now part of conversations consumers are already having… the performance uplift has been hard to ignore,” said Sadhvi Dhawan.

At the same time, artificial intelligence is becoming a central component of Meta’s commerce stack alongside creators.

The company is extending its Advantage+ suite with generative AI tools that automate video production, voiceovers, and translations. These tools are designed to lower the effort needed to produce localised, high-volume ad creatives.

Meta is also testing a feature called “product set optimisation,” which allows advertisers to prioritise specific products within larger catalogues. Early results show a 17% drop in cost per purchase for promoted items.

Automated catalog video tools are also gaining traction. These tools convert static listings into video ads and are delivering up to 20% more conversions per dollar, further improving campaign efficiency.

Meta prepares new AI models as competition intensifies

Alongside its commerce push, Meta is advancing its artificial intelligence roadmap with plans to release its first models developed under Alexandr Wang. Some versions are expected to be offered under an open-source license.

Meta has long stood out among major U.S. tech firms for allowing developers to modify its frontier models. However, rising competition in AI is prompting questions over whether that level of openness will continue.

The company continues to emphasise its distribution advantage. By embedding AI tools across platforms such as WhatsApp, Facebook, and Instagram, Meta can reach billions of users globally, often without direct cost. That scale remains difficult for rivals to match and forms a key part of its strategy to close the gap with competitors.

Meta has also introduced Muse Spark, its first model from the Meta Superintelligence Labs unit. The system is positioned as a step toward “personal superintelligence” capable of reasoning, using tools, and coordinating multiple agents on behalf of users.

A core feature of Muse Spark is its “Contemplating” mode, which runs several agents in parallel before producing a response. Meta describes it as an answer to advanced reasoning systems such as those seen in models like Gemini Deep Think and GPT Pro.

The company’s push into AI has also involved internal restructuring. Reports indicate that Meta has cut hundreds of roles as it redirects resources toward priority engineering projects tied to its AI ambitions.

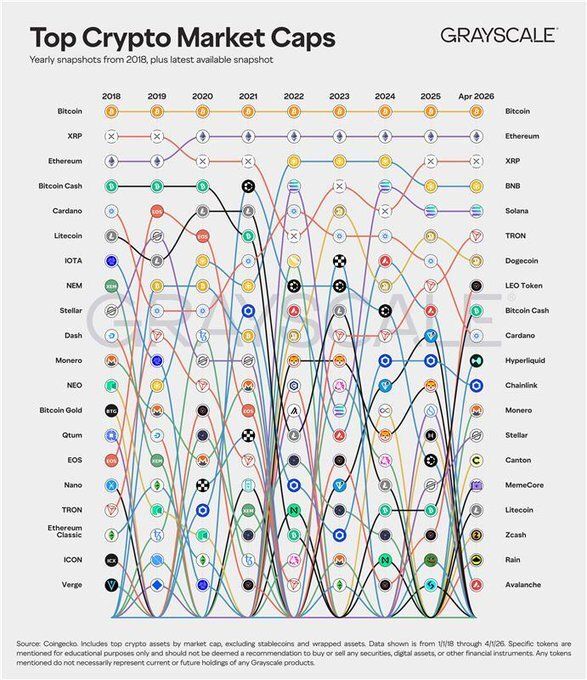

A chart tracking the top 15 cryptocurrencies by market cap every year since 2018 shows a clear pattern. Bitcoin never moves from the number one position.

Most altcoins that once competed for top rankings have either fallen sharply or disappeared entirely.

Bitcoin Holds Number One Across Every Cycle

Bitcoin maintains the top position every single year from 2018 to 2026. The crypto market goes through multiple bear markets, regulatory crackdowns in major economies, and waves of new competitors during this period.

Bitcoin’s ranking does not change. It remains at number one while the rest of the top 15 reshuffles around it.

Ethereum and XRP: The Only Cryptos That Keep Up

Ethereum has held second place consistently since 2018, maintaining its position as the dominant smart contract platform. No competitor manages to overtake it despite years of challengers entering the market.

XRP shows more volatility but never drops out of the top 10. It moves from second place in 2018 to third in 2026, surviving a multi-year SEC lawsuit that would have ended most projects. Out of the original 20 cryptos tracked in 2018, only Bitcoin, Ethereum, and XRP maintain top positions.

The Cryptos That Vanished and the Newcomers That Replaced Them

Half of the cryptos that appeared in the 2018 top 15 have completely disappeared from the top 20 by 2026. IOTA, NEM, Dash, NEO, Qtum, EOS, Bitcoin Gold, Nano, Verge, and Ethereum Classic were once considered serious projects. Investors debated which one would become the next

Ethereum. EOS raised $4 billion in its ICO. Dash was marketed as digital cash for the world. Today, none of them rank among the top 20.

The replacements show an equally notable shift. Solana climbs from obscurity to the top five. Dogecoin, created as a joke, now sits in the top ten. Hyperliquid did not even exist in 2018 and now competes with decade-old names.

Higher Means Stable, Lower Means Volatile

The chart shows a pattern: the higher the ranking, the more stable the position. Bitcoin at number one never moves. Ethereum at number two barely shifts. XRP fluctuates within the top 10 but stays there.

Below the top 10, the volatility increases. Projects jump ten positions up or drop out of the rankings entirely within a single cycle. Most of the 2018 top 15 that vanished came from positions six through fifteen.

What This Means for Crypto Rankings

The chart illustrates the volatility that defines crypto beyond price swings. Rankings shift. Projects that dominate one cycle can disappear in the next. Market cap positions that seem secure can evaporate within a few years.

The data covers eight years. In that time, only three cryptos maintain their top positions. Ten disappear from the top 20 entirely. The rest drop but survive somewhere lower in the rankings. For a market often described as high-risk, the data shows where that risk plays out: not just in price, but in relevance.

The post Bitcoin Stays on Top for 8 Years: Most Cryptos Vanished appeared first on BeInCrypto.

American Airlines raises checked bag fees, trims economy perks amid soaring fuel prices

Crypto Exchanges Vie for TradFi Commodities Market, Pricing Gaps Remain

20 photos we love from the Masters Par-3 Contest

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

Which 2 would you pick? #finance #investmenttips #investmentadvice #investmentforbeginners #trader

google pay pocket money kya hai | how to use google pay pocket money | gpay pocket money new update

WARNING: Bitcoin is 11 Days Away from a MASSIVE Move! (ETH, XRP, SOL, AVAX)

-

NewsBeat7 days ago

NewsBeat7 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business7 days ago

Business7 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business5 days ago

Business5 days agoExpert Picks for Every Need

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports5 days ago

Sports5 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech2 days ago

Tech2 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business4 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Fashion3 days ago

Fashion3 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Fashion2 days ago

Fashion2 days agoLet’s Discuss: DEI in 2026

-

Tech7 days ago

Tech7 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Politics6 days ago

Wings Over Scotland | The quality of mercy

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Fashion7 days ago

Fashion7 days agoStatement Sunglasses: The Accessory Shaping Modern Fashion

-

Crypto World23 hours ago

Crypto World23 hours agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics6 days ago

Politics6 days agoEast Jerusalem Palestinian families eviction orders

-

Fashion7 days ago

Fashion7 days agoFor Love & Lemons’ Spring 2026 Line is for the Romantics

-

Sports7 days ago

Sports7 days agoWhich German players will make final cut?

-

Politics6 days ago

Politics6 days agoWhy so many children are now classified as ‘disabled’

-

Fashion7 days ago

Fashion7 days agoCoffee Break: Santa Croce Tote

You must be logged in to post a comment Login