Crypto World

Meta (META) Launches Arena App to Enter Crowded Prediction Market Space

Quick Overview

- Meta is building “Arena,” a forecasting platform enabling users to predict outcomes using points rather than actual currency.

- The platform will encompass political events, sporting matches, cultural happenings, and global news, functioning as a standalone product separate from Instagram and Facebook.

- CEO Mark Zuckerberg has designated Arena as a high-level internal initiative, despite its experimental classification.

- The company previously launched and discontinued a comparable service named Forecast between 2020 and 2022.

- While prediction markets continue expanding rapidly, they’re encountering heightened regulatory oversight concerning gaming regulations and potential market manipulation.

Meta, the organization behind Facebook, is constructing a mobile application named Arena designed as a forecasting platform. The service will enable participants to predict results of actual events spanning electoral contests, athletic competitions, and cultural phenomena. The New York Times reported details from two informed employees, noting the application will employ a points mechanism instead of monetary transactions.

Founder and CEO Mark Zuckerberg personally directed Arena’s creation, according to sources. The New York Times’ contacts characterized the initiative as simultaneously experimental and strategically significant for the corporation.

Arena will operate as an independent entity distinct from Meta’s current portfolio, which includes Facebook and Instagram. This standalone approach differs from Meta’s typical strategy of incorporating new capabilities into established platforms.

A Second Attempt at Forecasting

This represents Meta’s second venture into prediction platforms. In 2020, the company introduced Forecast, allowing participants to make predictions about current affairs and developments during the Covid-19 outbreak. The service was discontinued in 2022.

Meta has previously explored cryptocurrency and financial technology initiatives. The company unveiled Libra, a digital currency project, in 2019, which became Diem before being abandoned in 2022. Recently, Meta introduced USDC payment options for content creators in Colombia and the Philippines.

Should Arena launch successfully, it would enter direct competition with established platforms including Polymarket and Kalshi, both experiencing substantial growth. Polymarket attracted significant attention throughout the 2024 presidential election cycle, processing billions in transaction volume. With Meta recording 3.56 billion daily active participants across its ecosystem by March 2026, Arena could access an enormous existing user base.

Additional major technology companies have entered the forecasting sector. Coinbase and Kraken have investigated opportunities in this market, while Robinhood has launched event contracts connected to political developments and economic indicators.

Regulatory Challenges Intensify

The forecasting platform sector faces mounting legal challenges across the United States. The Commodity Futures Trading Commission continues disputes with state-level authorities regarding whether specific event contracts constitute illegal gambling activities.

Congress is evaluating proposed legislation addressing insider trading concerns on forecasting platforms. These efforts intensified following allegations against U.S. soldier Gannon Ken Van Dyke, who reportedly earned over $400,000 through a Polymarket position related to Venezuelan President Nicolás Maduro’s potential capture. Van Dyke’s trial is scheduled for December 2026.

Meta hasn’t announced a definitive launch timeline for Arena, nor has the company dismissed the possibility of incorporating real-money wagering features in the future.

Crypto World

Forgotten coin litecoin (LTC) could surprise everyone before its next halving: Crypto Daily

Traders may want to keep an eye on in the coming weeks and months. One of the earliest altcoins, LTC may see bullish price action, potentially outperforming the broader market, including bitcoin .

Here’s why.

Litecoin’s fourth reward halving is due around July 27, 2027 when the payment will drop by 50% to 3.125 LTC. Litecoin has a peculiar tendency to bottom out anywhere between six to 12 months before the event.

The evidence is there.

LTC bottomed in late June 2022 at around $40, just over a year before the third halving on Aug. 2, 2023. In the intervening period, it rallied to as high as $114 by July 2023, only to pull back to $80 in the lead-up to the event. In November 2022, the month that crypto exchange FTX collapsed and pulled down the wider market, litecoin actually rose more than 40%.

A similar pattern played out before the first two halvings. In each case, LTC bottomed out months beforehand, rallied and then dropped back a bit into the event. (Check the Daily Signal)

If history holds true, that means litecoin could find a bottom any time now.

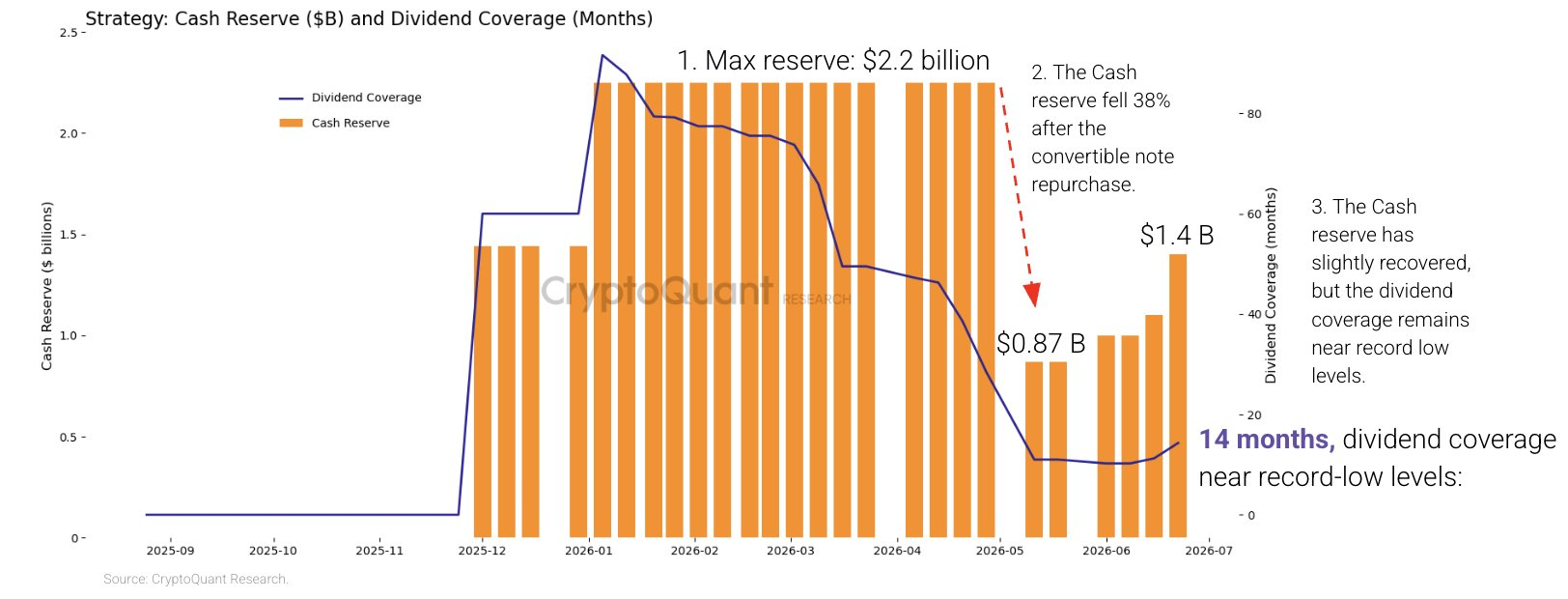

After Strategy’s dividend coverage fell to 14 months from seven years, CryptoQuant thinks the company led by Michael Saylor should pause Bitcoin purchases and focus on replenishing its cash reserve that’s down 38% year-to-date.

Strategy’s dividend obligations have nearly quadrupled to $1.2 billion, as the company issued substantial new STRC preferred stock, which carries an 11.5% yield.

“They should pause Bitcoin purchases, rebuild cash reserves, and adopt a systematic framework for purchase timing,” wrote the market data analytics provider’s CEO Ki Young Ju in a Wednesday X post, adding that the biggest public Bitcoin treasury holder should also create a “disciplined selling framework” for the next bull market.

Strategy’s cash reserve fell 38% after the company repurchased $1.5 billion of its 2029 senior notes at a discount, Cointelegraph reported on May 26. Those coffers have since recovered to $1.4 billion after it sold $335.5 million in MSTR shares, which added $300 million to its US dollar reserve on Monday, although it is near a record-low of 14 months’ of funds available to pay dividends.

STRC preferred shares hit by BTC correction

Strategy’s income-generating preferred stock, STRC, fell to $82.50 last week, a record 17.5% below its $100 par value. CryptoQuant’s report attributed it to the Bitcoin bear market correction and the “simultaneous depletion” of its cash reserve.

STRC is one of Strategy’s main mechanisms to fund its Bitcoin accumulation. Trading below par limits Strategy’s ability to raise funds through STRC sales. It may also force the company to increase its nominal dividend rate to attract buyers and protect STRC’s price.

The company said it plans to “continue replenishing” its USD reserve to “support the credit quality of its Digital Credit securities,” according to a Monday X post.

Cointelegraph’s request for comment on Strategy’s plans to replenish the cash reserve and whether this could help STRC’s price recover was not immediately replied to by the company.

Strategy cash reserve and dividend coverage in months. Source: CryptoQuant

No obligation to sell Bitcoin to support STRC price

CryptoQuant said Strategy is not “obligated” to sell Bitcoin to maintain STRC’s price, as the company can also deploy other tools to defend the stock, such as raising the current 11.5% dividend yield or issuing MSTR stock to “signal its ability to continue paying dividends,” adding:

“However, the path back to $100 is not straightforward.[…] Rebuilding the cash reserve to ~$2.8 billion (24 months of coverage) is a necessary condition for STRC to recover.”

Strategy’s Bitcoin holdings only provide a “limited emergency cushion,” as the company is sitting on about $10.6 billion in unrealized losses, meaning that a forced BTC sale at current rates would “crystallize large losses and destroy shareholder value,” CryptoQuant said.

Related: Capital B shareholders approve up to $120B in financing capacity for Bitcoin strategy

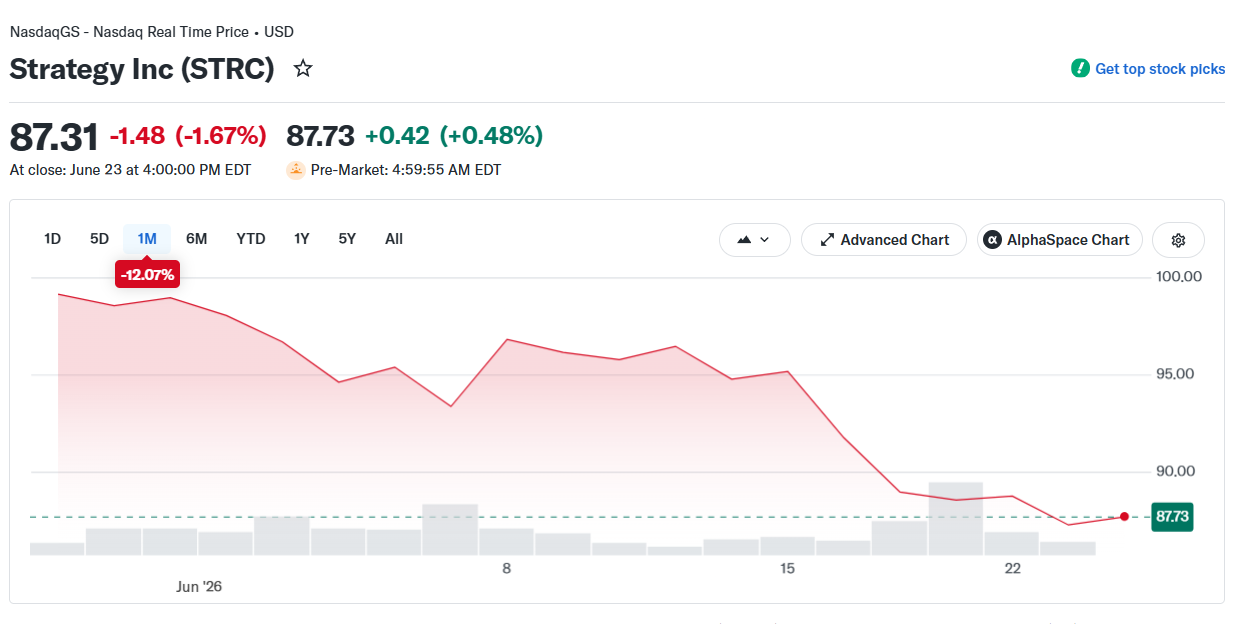

Ahead of Wednesday’s Nasdaq market open, STRC shares were little changed after closing at $87.31 on Tuesday. That extended the preferred stock’s 12% decline in the past month, according to Yahoo Finance data.

STRC/USD, 1-month chart. Source: Yahoo Finance

CryptoQuant’s head of research, Julio Moreno, attributed STRC’s decline to a “deterioration in Strategy’s fundamentals,” including its falling dividend cash coverage caused by the depletion of its cash reserve and a fourfold increase in STRC’s annualized dividend obligations so far in 2026.

Magazine: Bitcoin, the ‘canary in the coal mine,’ XRP transaction demand falls 91.5%: Market Moves

London, United Kingdom, June 24th, 2026, Chainwire

OpenPayd, a leading provider of financial infrastructure, has secured authorisation under the EU’s Markets in Crypto-Assets (MiCA) framework, strengthening its ability to deliver regulated stablecoin infrastructure across Europe.

The milestone comes one year after OpenPayd launched its stablecoin infrastructure, enabling businesses to move and manage fiat and digital assets through a single platform. Since launch, adoption has expanded across treasury, settlement and cross-border payment use cases as businesses increasingly seek regulated pathways into the digital asset economy. Today, OpenPayd processes more than $240 billion in annualised volume for over 1,100 businesses globally, including Kraken, eToro, OKX and B2C2.

The MiCA authorisation enables OpenPayd to operate as a regulated crypto-asset service provider (CASP) under a unified European regulatory framework, allowing the company to provide regulated crypto-asset services to clients across the EEA through a single licence.

Through the authorisation, OpenPayd can offer regulated digital asset services including fiat-to-stablecoin on and off-ramping, custody, wallet infrastructure and global stablecoin transfers across major blockchain networks. Through a single API, businesses can seamlessly move and manage money across both traditional financial rails and digital assets.

Iana Dimitrova, CEO of OpenPayd, said, “Stablecoins are rapidly becoming part of mainstream financial infrastructure. MiCA is a major step forward for Europe because it gives businesses the assurance to leverage digital asset technology to improve their payments and treasury and to grow.

At OpenPayd, we are building the universal financial infrastructure for the digital economy. This authorisation strengthens our ability to help businesses move and manage money globally through a single platform that seamlessly connects traditional finance and digital assets.”

The MiCA approval forms part of OpenPayd’s broader investment in regulatory infrastructure and global connectivity across both fiat and digital asset services. Together with its existing regulatory permissions and banking network, OpenPayd is building one of the industry’s most comprehensive regulated infrastructures for global money movement.

About OpenPayd

OpenPayd is building the universal financial infrastructure for the digital economy. Founded in 2018 by Dr. Ozan Ozerk, its rails-agnostic platform enables businesses to move and manage money globally – across fiat and digital assets – through a single, powerful API. OpenPayd provides embedded accounts, FX, domestic and international payments, Open Banking, and stablecoin on/off ramps – delivering interoperability between traditional finance and digital assets. With one of the most comprehensive banking networks in the market, OpenPayd enables real-time money movement, everywhere.

Trusted by global brands including eToro, Kraken, OKX, and B2C2, OpenPayd processes more than $240 billion in annual volumes for over 1100 businesses. It is the infrastructure layer powering the next generation of financial services.

Contact

OpenPayd

press@openpayd.com

A Wall Street Journal investigation has found that roughly $1.9 million in bets displayed across more than 1,100 creator videos promoting Polymarket were not real, exposing a fake-engagement campaign at the world's largest prediction market as it pursues U.S. regulatory approval and institutional… Read the full story at The Defiant

The crypto market remained sluggish and weak on Wednesday as bitcoin and ether (ETH) fell less than 0.4% since midnight UTC and the CoinDesk 20 Index (CD20) lost 0.9%, with 18 of its constituents declining.

The lack of a meaningful bounce will be the largest concern, especially as U.S. equity futures began to recover from Tuesday’s tech selloff.

A portion of the altcoin market outperformed its peers, with jupiter (JUP) and monero (XMR) posting gains of between 2% and 4% to suggest investor appetite is still alive despite bearish market conditions.

Bitcoin now needs to avoid slipping back below the psychological level of support at $60,000, which would trigger a return to a trading range not seen since late 2024 with $52,000 emerging as a key level to the downside.

Derivatives positioning

- Trading has slowed in the derivatives market, with volume down 27% to $141 billion int the past 24 hours, while open interest has increased by 2% to $106 billion. Liquidations tallied $158 million, the lowest in two weeks.

- BTC futures open interest (OI) is holding steady at around 730K BTC for the eighth straight day, signaling consolidation at current levels.

- ETH futures are showing renewed action. OI rose to 14.3 million ETH, the most in two weeks and up from a recent low of 13.74 million.

- The increase occurred as the spot price fell from roughly $1,780 to $1,650 over the past two days, a combination that typically indicates traders shorting into the rally. While funding rates hold slightly positive, showing some demand for bull exposure, 24-hour cumulative volume delta (CVD) is negative, a sign that bears are leading price action through market orders rather than passive limit orders.

- SOL futures are busier than ever, with OI at a lifetime high of 77.68 million tokens. But both funding rates and 24-hour OI-adjusted CVD are negative, meaning the action is being driven by fresh shorts, or bearish bets, on the token.

- In contrast, ZEC’s market is cooling fast, with OI retreating to 2 million tokens from near 2.55 million tokens last month.

- Broadly speaking, bears appear to be leading price action in most of the top 25 tokens, as is evident from negative OI-adjusted CVDs for the second straight day.

- Bitcoin’s 30-day implied volatility index (BVIV) has cooled to 43% from nearly 48% on Tuesday. Ether’s volatility index displays a similar pattern.

- On Deribit, the one-week skew widened to 10.9 vol points in favor of puts from roughly 7 points a day ago, a clear sign of intensifying downside concerns. The one-month skew also expanded.

- Block flows on Paradigm featured a straddle strategy involving call and put options at the $62,000 strike, both expiring July 3. A straddle buyer bets on elevated volatility.

Token talk

- While monero and jupiter performed well as Wednesday dawned, the same cannot be said for the likes of ethena (ENA), pump (PUMP) and stellar (XLM), all of which tumbled between 2.2% and 3.5% since midnight UTC.

- Ethena has now lost more than 90% of its value since touching a record high of $0.87 last September. The yield-generating DeFi platform is suffering from a strategy that depends on bullish market conditions, including positive funding rates.

- Similar drawdowns have been seen across veteran tokens such as and , which failed to reach their respective 2021 heights in the recent bull market, effectively trading in a macro downtrend since then.

- The U.S. Dollar Index (DXY) continued to set new ground on Wednesday and is now challenging its May 2025 high. A strengthening dollar is typically seen as a negative for risk assets, including altcoins, because it suggests investors feel safer in cash.

Ripple keeps winning. A five-second cross-border Treasury settlement with JPMorgan and Mastercard, ten major deals this year, an IPO the chief executive keeps hinting at. XRP keeps trading near a dollar and change. The gap between the company and the token is the entire story.

Summary

- Ripple’s institutional wins are real, but they do not always create XRP demand.

- The JPMorgan Treasury settlement used RLUSD, not XRP, as the cash leg.

- Ripple equity and XRP remain separate assets with different value drivers.

- XRP needs utility to become token demand before the price can break its range.

In June 2026, Ripple completed something that should have been a milestone for its token. Working with JPMorgan, Mastercard, and Ondo Finance, it settled the redemption of a tokenized United States Treasury fund across borders and across banks on the XRP Ledger, and the blockchain leg finalized in under five seconds, against the one to three business days the same transaction takes on traditional rails.

The participants were real, the speed was real, and the headline wrote itself: Wall Street is settling Treasuries on Ripple’s blockchain. And yet XRP, the token, barely moved, and where it did move it often fell.

The asset spent most of 2026 trading in a narrow band near a dollar and change, while news exactly like this piled up around it. That disconnect, a company stacking institutional wins while its token goes nowhere, is one of the most instructive puzzles in crypto.

The answer is more revealing than either the bulls or the bears usually admit.

This piece takes the puzzle apart. It covers the settlement that did not move the token and the detail the headlines skipped, the structural separation between Ripple the company and XRP the asset, the supply overhang that quietly weighs on the price, the genuine catalysts XRP does have, and why those catalysts keep getting priced as maybes.

The aim is to explain, without spin in either direction, why good news for Ripple so often fails to become good news for XRP, and what would actually have to change for the token to break out of its range.

The win that did not move the token

The June settlement was not a small thing. For years the tokenization story has been mostly demonstrations on private chains, so a live, cross-border, cross-bank redemption of a real tokenized Treasury on a public ledger, with JPMorgan’s settlement platform delivering dollars to Ripple’s bank in Singapore in the same flow, is a credibility win for the XRP Ledger.

It connected one of the largest settlement institutions in the world to a public blockchain, outside normal banking hours, in seconds. As a proof that the rails work, it was about as strong as these announcements get.

That is the settlement broken down in detail. The transaction matters because it shows that regulated institutions are willing to test the XRP Ledger for real-world asset settlement.

The market’s reaction told a different story. XRP did not rally on the news in any durable way, and on the day of an earlier version of the same pilot it actually fell almost 5%, erasing a brief pop.

This was not an anomaly. It fit a pattern that has defined XRP through 2026, where Ripple partnership headlines arrive, the token spikes briefly or not at all, and then drifts back down.

Traders have a weary phrase for it: every Ripple deal seems to be followed by the XRP price dropping. When a genuinely impressive institutional milestone produces a shrug or a selloff, the explanation is rarely that the milestone was fake.

It is usually that the milestone has less to do with the token than the headline implies.

The detail the headlines skipped: XRP was barely in the trade

Here is the part that reframes everything. In that landmark Treasury settlement, XRP the asset did almost no work.

The bridging and settlement were done with RLUSD, Ripple’s dollar-pegged stablecoin, not with XRP. The tokenized Treasury, Ondo’s product, was redeemed by exchanging it for RLUSD, and XRP appeared only as the tiny network fee that every XRP Ledger transaction pays.

Those fees are fractions of a cent on a trade moving far larger sums. The asset that the headlines attached to the news was, in the actual mechanics, a bystander.

This is not an accident or an oversight; it is by design, and the reason matters. Institutional settlement needs a stable, audited, dollar-denominated instrument, because no treasurer is going to settle a Treasury redemption in an asset that can swing 10% in a day.

RLUSD is built for exactly that role: dollar-pegged, backed by cash and Treasuries, and regulated. XRP’s price volatility rules it out of the settlement leg by definition, which is why Ripple deliberately built the product to use RLUSD as the cash leg.

That is the RLUSD that did the settlement work. It is useful precisely because it is not supposed to move.

So when Ripple wins an institutional settlement deal, the direct beneficiary is the XRP Ledger as infrastructure and RLUSD as the settlement token, while XRP the asset captures only the minuscule fee. The headline says XRP.

The transaction says RLUSD. The price reflects the transaction.

Ripple the company versus XRP the token

Step back and the deeper issue comes into focus: Ripple the company and XRP the token are not the same thing, and the market has started pricing them separately.

Ripple is a private company that sells software and payment services, signs deals with banks, holds a large treasury, and may one day go public. XRP is a cryptocurrency that trades on its own supply and demand.

Owning XRP does not make you a shareholder in Ripple, does not entitle you to its profits, and does not give you a claim on its corporate success. The two are linked by association and by Ripple’s large XRP holdings, but they are distinct assets with distinct drivers.

This is why the IPO chatter, which intensified after chief executive Brad Garlinghouse called the moment real ahead of a company event, is more complicated than it sounds for token holders. An initial public offering would let people buy Ripple equity, and it would reward Ripple’s shareholders.

It would not, by itself, pay anything to XRP holders, who own a separate asset.

That is the IPO question for token holders. The most realistic answer is that any benefit would be indirect unless Ripple deliberately created a program for XRP holders, and no such program exists.

Garlinghouse’s strongest argument is an indirect one, and it has genuine merit: because Ripple remains the largest single holder of XRP, the company has a built-in incentive to drive the token’s value, and its partnerships and integrations do plausibly increase XRP’s long-term utility and demand.

That alignment is real. But it is indirect, a rising tide the company hopes to create, not a dividend it pays, and a holder who treats a possible IPO as a direct reward is counting on a maybe attached to a maybe.

The market’s persistent refusal to rally Ripple’s wins into XRP’s price is, in effect, the market enforcing this distinction.

The supply overhang nobody wants to discuss

There is also a more mechanical weight on the token, and it sits on the supply side.

Ripple holds an enormous quantity of XRP in escrow, a locked reserve it releases on a schedule, and that release is a structural source of new supply hitting the market. Each month Ripple can release up to one billion XRP from escrow, then re-locks most of it, but the net amount that actually reaches circulation still runs into the hundreds of millions of tokens monthly.

That is a steady stream of potential selling pressure built into the token’s design.

The significance is that it sets a high bar for any bullish supply story. Some XRP optimists point to the tiny fees burned on each ledger transaction as a deflationary force, but at current transaction volumes the burn is a rounding error next to the escrow releases.

For fee burn to tighten supply in any meaningful way, on-chain activity would have to grow by orders of magnitude, enough to offset hundreds of millions of newly released tokens every month. A single institutional settlement test does not move that needle.

So even when Ripple announces real adoption, a holder has to weigh it against a supply schedule that keeps running on its long-set path. The demand side has to climb a down escalator, and one impressive pilot does not change the speed of the steps.

What XRP actually has going for it

None of this means XRP is a lost cause, and a fair account has to give the bull case its due, because the token’s position has improved in ways that are concrete.

The years-long legal cloud has lifted. The Securities and Exchange Commission’s case against Ripple ended in 2025 with the courts’ finding that XRP sold on public exchanges was not a security, and a later joint classification treated XRP as a digital commodity, giving the token more regulatory clarity than almost any other asset of its size.

That clarity is real and durable, even if it rests partly on interpretation rather than statute.

The institutional door has also opened. Spot XRP exchange-traded funds launched in late 2025 from a roster of established issuers and pulled in well over a billion dollars in assets, with major institutions appearing among the disclosed holders.

That is where XRP demand is actually coming from. ETF flows are not enough by themselves to erase the supply overhang, but they are measurable demand in a way that partnership headlines are not.

Ripple’s stablecoin, RLUSD, crossed a billion dollars in market value in under a year and is being woven into real settlement and card products. Ripple has also kept expanding its payments footprint, including a Bitso partnership around a regulated MXN-backed stablecoin on XRPL and a Flutterwave investment aimed at expanding RLUSD settlement across African payment corridors.

Those are not trivial supports. They show Ripple pushing both sides of its strategy: the ledger as institutional settlement infrastructure and stablecoins as the cash leg that enterprises actually want to use.

The single biggest potential catalyst is legislative. If the CLARITY Act passes and writes XRP’s digital-commodity status into federal law, analysts have projected several billion dollars of additional XRP ETF inflows.

That is the catalyst that could codify XRP’s status. It is the one event that could turn today’s regulatory interpretation into statutory certainty.

These are the ingredients of a genuine bull case, and they explain why XRP has held a floor rather than collapsing, even as it refuses to break out.

Why the catalysts keep getting priced as maybes

So the puzzle resolves into a simpler observation: XRP has real catalysts, but the market keeps pricing them as possibilities instead of facts, and there is a logic to that caution.

A proof-of-concept settlement is priced as a proof of concept until it becomes recurring volume. An ETF is priced on the flows it actually attracts, not the flows it might.

A legislative catalyst is priced on the probability of passage, which for the CLARITY Act has hovered well short of certainty as the bill grinds through the Senate. Each of these is a maybe, and a token sitting on a stack of maybes trades like a token sitting on a stack of maybes: range-bound, reactive, and quick to sell the news.

The pattern of selling Ripple’s wins is the market expressing exactly this. When XRP spiked after its legal victory in 2025, long-term holders used the burst of volume to sell, and the token settled back into its range.

Every subsequent partnership has met a version of the same response, because the partnerships, however real, have not yet produced measurable, sustained demand for the token itself.

The market is not being irrational. It is distinguishing between infrastructure adoption, which benefits Ripple and the ledger, and token demand, which is what actually moves XRP, and it is waiting for proof that the first turns into the second.

What the chart has been saying all year

If you want a blunt summary of everything above, look at what XRP’s price actually did around its biggest catalysts, because the chart has been telling the story in plain language.

When Ripple’s long legal fight with the Securities and Exchange Commission finally ended in 2025, XRP spiked hard, touching levels far above where it trades now, and then it faded. Long-term holders used the surge of volume and attention to sell into strength, and the token drifted back down through the rest of the year and settled into the narrow range it has occupied for months.

Each subsequent institutional headline produced a smaller version of the same shape: a brief pop, a fade, a return to the range. The 200-day moving average, a common gauge of the longer trend, has sat well above the price for much of the year, which is a technical way of saying the market has been in a patient holding pattern, neither convinced enough to break out nor scared enough to break down.

A second signal is easy to overlook because it points the other way. While Ripple was landing marquee partnerships, the payments company MoneyGram, once one of Ripple’s most-cited real-world users, moved its on-chain settlement work toward a rival blockchain.

One defection does not undo a year of deals, and the strategic damage may be small, but it punctures the simplest version of the bull narrative, the one where every institution that touches Ripple stays forever and compounds XRP demand.

Adoption is not monotonic. Partners arrive and partners leave, and the network effect that XRP optimists count on is more contested than the announcement cadence suggests.

The chart reflects this ambivalence honestly: a market that has seen real progress and real setbacks, and has priced the token as a thing that might work out, with the proof still pending.

The lesson in the price action is the same lesson the mechanics teach. Markets are forward-looking, and they will pay up in advance for catalysts they believe will convert into demand.

XRP’s refusal to sustain its rallies is the market saying, repeatedly, that it does not yet see the conversion, that the partnerships and pilots have not become the recurring, token-level demand that would justify a rerating.

That is not a permanent verdict. It is a standing challenge, and the chart will be the first place the answer shows up, long before any press release confirms it.

The bigger pattern: when the network wins and the token waits

XRP’s predicament is not unique, and seeing it as one case of a broader pattern makes the whole situation less mysterious.

Across crypto, there is a recurring gap between the success of a network and the price of the token attached to it. A blockchain can attract real usage, real institutions, and real volume while its native token languishes, because adoption of the infrastructure and demand for the token are two different things that only sometimes move together.

A network captures value for its token when using the network requires buying, holding, or burning that token in volume large enough to matter against its supply. When the network can be used without much of the token changing hands, the usage and the price decouple, and the token becomes a spectator to its own success.

XRP sits squarely in that trap. The XRP Ledger is being adopted for serious settlement work, but those settlements lean on RLUSD as the cash leg and use only a sliver of XRP as a fee.

So the network’s growth does not pull much demand through to the token. This is the same dynamic that has frustrated holders of other infrastructure tokens whose chains saw heavy use that never translated into proportional token demand.

The token is not useless; it secures the ledger, pays the fees, and provides liquidity. But the volume of XRP that the network’s growth actually requires is small relative to the token’s large and steadily expanding supply, and that imbalance is the core of the disappointment.

The market is not failing to notice Ripple’s progress. It is noticing, correctly, that the progress runs largely through rails that do not require much XRP.

Understanding this reframes what a holder is really betting on. To own XRP in expectation of price appreciation is to bet not merely that Ripple succeeds, but that Ripple’s success comes to require XRP itself in growing quantities, through settlement volume, ecosystem use, and demand that finally outpaces the escrow supply.

That is a more specific and more demanding bet than simply believing in the company, and it is the bet the market keeps declining to front-run.

The network can keep winning for years while the token waits, and the waiting ends only when usage and token demand finally converge. Until they do, the gap that has defined XRP through 2026 is less a puzzle than a predictable feature of how value accrues, or fails to accrue, to a token whose network can succeed without it.

What would actually break the range

If you want to know when XRP might finally move, the framework above tells you where to look, and it is not the next partnership headline.

The thing that breaks the range is the conversion of utility into token demand: settlement volume large enough that fees and ecosystem use begin to matter against the escrow supply, ETF flows that compound instead of trickle, and a regulatory catalyst like the CLARITY Act actually crossing the line and pulling institutional money off the sidelines.

Those forces aligning, not any one of them alone, is the strongest version of the XRP thesis.

Until then, the disconnect is likely to persist, and understanding why is the most valuable thing a holder can take from the past year. Ripple is winning, genuinely and repeatedly, in the institutional arena it has targeted for a decade.

But Ripple’s wins flow first to Ripple the company, to the XRP Ledger as a piece of infrastructure, and to RLUSD as a settlement instrument, and only indirectly, slowly, and conditionally to XRP the token.

A holder who watches the partnerships and wonders why the price will not follow has been watching the wrong variable. The variable that matters is whether all that institutional adoption ever turns into durable demand for XRP itself, and so far, the market has decided it has not seen enough proof.

The deal with JPMorgan was a milestone. It was just a milestone for the ledger, not yet for the coin.

Frequently asked questions

What did Ripple and JPMorgan actually do?

Ripple, JPMorgan, Mastercard, and Ondo Finance completed the first cross-border, cross-bank redemption of a tokenized United States Treasury fund on the XRP Ledger. Ondo’s tokenized Treasury product was redeemed on the ledger while Mastercard’s network and JPMorgan’s settlement platform delivered dollars to Ripple’s bank in Singapore, with the blockchain leg settling in under five seconds versus one to three business days on traditional rails. It is a real milestone for tokenized settlement and for the XRP Ledger as infrastructure.

Why did XRP not go up after the JPMorgan deal?

Because XRP the asset was barely involved in the transaction. The settlement used RLUSD, Ripple’s dollar-pegged stablecoin, as the cash leg, while XRP appeared only as the tiny network fee. Institutional settlement needs a stable, audited dollar instrument, and XRP’s price volatility rules it out of that role by design. So the deal benefited the XRP Ledger and RLUSD far more than XRP, which is why the token did not rally and, on an earlier version of the pilot, actually fell.

Is XRP the same as owning a stake in Ripple?

No. Ripple is a private company, and XRP is a separate cryptocurrency. Owning XRP does not make you a Ripple shareholder, does not entitle you to its profits, and would not give you a claim in a Ripple IPO. The two are linked because Ripple is the largest holder of XRP and its business can increase the token’s utility over time, but that benefit is indirect. A Ripple IPO would reward Ripple’s equity holders, not XRP holders directly.

Why is XRP stuck in a range?

A mix of supply and demand factors. On the supply side, Ripple releases large amounts of XRP from escrow each month, a steady source of selling pressure that small fee burns cannot offset at current volumes. On the demand side, Ripple’s institutional wins have not yet produced sustained demand for the token itself, so the market prices each partnership, ETF, and legislative catalyst as a maybe instead of a confirmed driver, leaving XRP range-bound and quick to sell the news.

What could actually push XRP higher?

The conversion of utility into real token demand. That means settlement volume large enough that ecosystem use begins to matter against the escrow supply, ETF flows that compound instead of merely trickling, and a regulatory catalyst such as the CLARITY Act passing and writing XRP’s digital-commodity status into federal law, which analysts project could draw billions in additional ETF inflows. Those forces aligning together, not any single headline, is the strongest case for a breakout.

Does XRP have a real bull case at all?

Yes. XRP has more regulatory clarity than almost any major token after the SEC case ended and a later classification treated it as a digital commodity. Spot XRP ETFs launched in late 2025 and gathered over a billion dollars, with major institutions among the holders, and RLUSD crossed a billion dollars in market value quickly. The CLARITY Act could codify XRP’s status and unlock further ETF demand. These are genuine supports, which is why XRP has held a floor, even as it waits for adoption to translate into token demand.

This article is information, not investment advice. Prices, partnership details, and corporate and legislative plans change quickly and reflect reporting available as of June 24, 2026. Verify current data with official sources before relying on anything described here.

TLDR

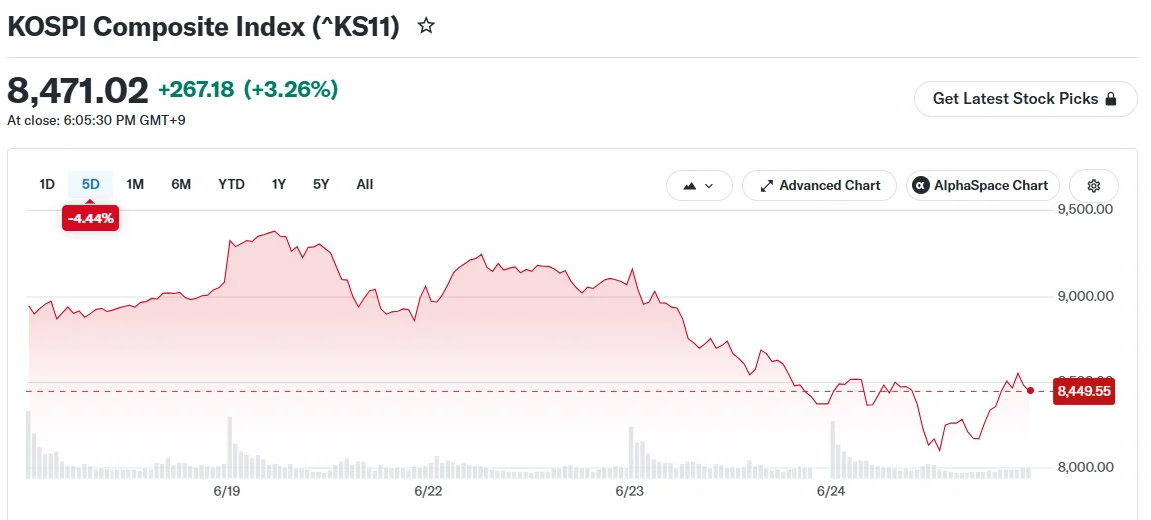

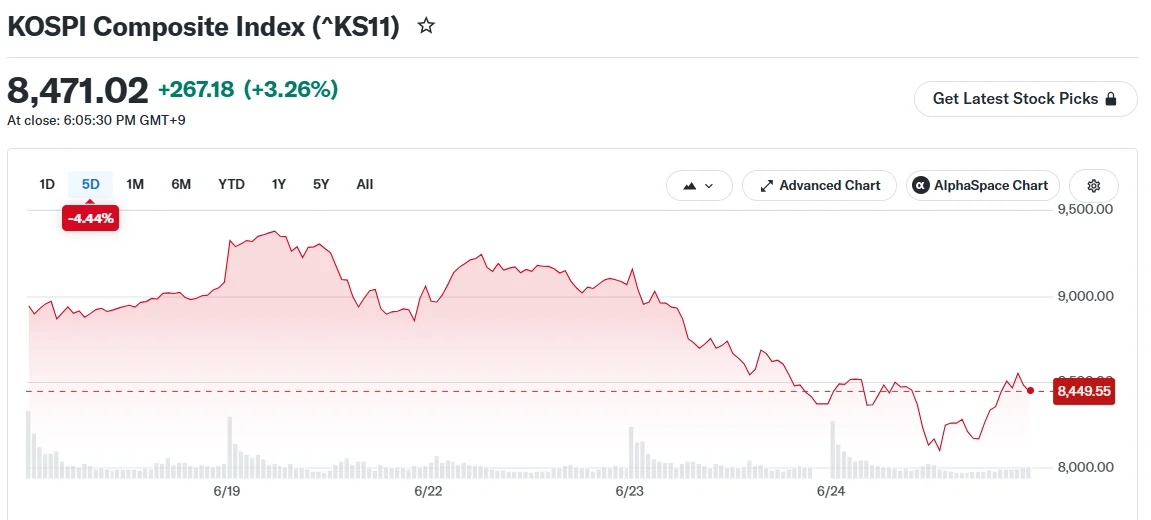

- The KOSPI index rallied between 3.3% and 4.6% during Wednesday’s trading after Tuesday’s devastating 10% decline

- Samsung Electronics jumped as much as 10% following reports of a $5.8 billion share repurchase program

- SK Hynix gained 1% to 3.4% amid news of upcoming American Depositary Receipts listing in the United States

- The previous day’s selloff stemmed from MSCI’s developed market rejection and concerns over AI sector momentum

- The KOSPI still holds its position as the globe’s top-performing major index with nearly 100% gains this year

South Korea’s equity markets delivered an impressive comeback on Wednesday following one of the most severe single-session declines witnessed in years. The KOSPI benchmark surged 3.3% to settle at 8,471 points, after touching highs of 4.6% during intraday trading.

This impressive recovery arrived merely 24 hours after the index experienced a devastating nearly 10% collapse on Tuesday, erasing substantial market capitalization from technology and semiconductor companies.

Samsung Electronics spearheaded Wednesday’s revival, jumping between 7% and 10% throughout the trading day. The dramatic increase followed reports from Yonhap indicating Samsung’s preparation for a share repurchase program valued at approximately 90 trillion won, equivalent to about $5.8 billion.

SK Hynix similarly bounced back, climbing between 1% and 3.4%. News emerged that the memory chip manufacturer was advancing plans to establish American Depositary Receipts listing in the United States, a strategic initiative expected to draw considerable foreign capital.

Both technology giants had experienced devastating losses exceeding 12% during Tuesday’s trading, meaning Wednesday’s rally represented only a partial restoration of lost value.

What Sparked Tuesday’s Market Collapse

Multiple catalysts converged to pummel South Korean equities on Tuesday. The primary trigger was MSCI’s announcement rejecting South Korea’s petition for reclassification to developed market status, a prestigious upgrade the nation had actively pursued.

Uncertainty surrounding the artificial intelligence sector also contributed significantly. Reports indicated SK Hynix might be reconsidering its emphasis on high-bandwidth memory products — critical components for AI processors — potentially pivoting toward conventional memory solutions. This speculation alarmed investors heavily positioned in AI-related semiconductor stocks.

Leveraged exchange-traded products intensified the downturn. As valuations declined, market participants rapidly liquidated these instruments, creating a cascading effect that magnified losses. South Korea’s chief financial regulator publicly acknowledged concerns regarding the recent authorization of such ETFs only weeks earlier.

Regional Markets Show Divergent Performance

Broader Asian equity markets displayed mixed results on Wednesday. Japan’s Nikkei 225 retreated 0.9%. Taiwan’s Taiex declined 2.2%, with semiconductor giant TSMC finishing 4% lower.

Hong Kong’s Hang Seng advanced up to 1%, defying the broader regional weakness.

Market observers highlighted that the recent instability demonstrates how interconnected Asia’s leading exchanges have become with global artificial intelligence sentiment.

Chris Weston, head of research at Pepperstone, noted the technology sector correction partially reflected profit-taking activity as investors reassessed risk-reward dynamics, particularly in heavily concentrated AI and memory chip positions.

Michael Wan, an analyst at MUFG, maintained an optimistic long-term perspective for the industry. He characterized the current volatility as preliminary fluctuations within what he identified as a transformational technological evolution.

Notwithstanding the dramatic two-day volatility, the KOSPI continues to maintain its status as 2026’s best-performing major global equity index, boasting gains approaching 100% year-to-date.

South Korea is folding its token securities work into a broader government push to modernize capital markets, as regulators plan faster settlement, longer trading hours and additional technology upgrades. The Financial Services Commission (FSC) said it has launched a capital market infrastructure review involving multiple agencies and market operators, with tokenized securities to be handled through a separate public-private track before being aligned with the wider reform agenda.

On Tuesday, the FSC announced the start of its capital market infrastructure review meeting, aimed at coordinating reforms across government bodies. The regulator said the token securities agenda will be discussed through a dedicated public-private council and later connected to the larger initiative—an approach that effectively keeps the legislative and technical details for tokenized assets on a separate timetable while still targeting system-level integration.

Key takeaways

- The FSC has begun a cross-government capital market infrastructure review that will coordinate reforms such as faster settlement and expanded trading access.

- Token securities will remain governed through a separate public-private council for now, before being linked to the broader infrastructure roadmap.

- Plans include a roadmap to shorten the securities settlement cycle (targeted for October) and a Korea Securities Depository (KSD) settlement system for over-the-counter trades in unlisted shares and certain fractional investment products by the end of 2026.

- South Korea’s token securities framework was enabled by January amendments recognizing blockchain-based distributed ledgers as securities registries, with a scheduled effective date in February 2027.

- Samsung SDS has been contracted to build a token securities management platform connecting KSD’s existing electronic securities account system with blockchain-based data, with completion targeted for February 2027.

A broader modernization plan, with token securities kept in a parallel track

The FSC’s move places tokenized securities within a wider overhaul of South Korea’s financial market plumbing rather than treating them as a standalone experiment. The regulator said the capital market infrastructure review is intended to coordinate reforms across agencies and market participants, while token securities discussions will continue through a public-private council.

In commentary on the initiative, FSC Vice Chairman Kwon Dae-young said the effort is guided by four policy priorities: trust, shareholder protection, innovation and market access. That framing matters for investors and market operators because tokenized securities regulation is likely to live or die on whether new systems can be reconciled with existing investor-protection and reporting standards.

Settlement speed and KSD systems point to “mainstreaming” tokenization

While token securities have their own legal timeline, the infrastructure review includes operational upgrades that could influence how quickly blockchain-based assets can be used alongside conventional market workflows. According to the FSC, the reform package includes a roadmap to shorten the securities settlement cycle, expected by October. The regulator also described a KSD system for settling over-the-counter (OTC) trades in unlisted shares and fractional investment products, targeted for completion by the end of 2026.

If delivered as scheduled, those milestones would help reduce one of the practical frictions around securities tokenization: integration with established settlement and custody processes. For market participants, shortening settlement cycles and building depository-linked infrastructure could make tokenized products easier to operationalize, since the reporting and settlement logic would be more closely aligned with the processes investors already understand.

Token securities law already passed—implementation is now the focus for 2027

South Korea’s token securities effort predates the latest infrastructure review. In January, the National Assembly approved amendments that recognize blockchain-based distributed ledgers as valid securities registries and allow the issuance and circulation of token securities.

The FSC said the resulting framework is scheduled to take effect in February 2027. That start date depends on regulators finalizing subordinate rules and supporting infrastructure. The FSC also indicated that, at the second meeting of its public-private token securities council in May, it was targeting July for the release of proposed subordinate regulations and guidelines.

For builders and compliance teams, this is a critical distinction: the high-level legal permission is already in place, but detailed operational requirements—such as how tokenized securities records are maintained, verified and integrated into existing securities infrastructure—will be shaped by the subordinate regulations released later in the process.

Infrastructure work underway: KSD platform integration targeted for February 2027

Technical infrastructure is already moving forward. In May, Samsung SDS said it had won a Korea Securities Depository (KSD) contract to build a token securities management platform. The goal, as described at the time, is to connect KSD’s existing electronic securities account system with blockchain-based data.

Samsung SDS said it aims to complete the platform by February 2027, aligning the technical readiness with the broader token securities framework effective date. According to the FSC, detailed token securities plans will continue to be developed and discussed by the public-private council before being connected to the wider capital market infrastructure review.

This coordination step is likely to affect how smoothly tokenized securities transition from a legal concept into a production-ready market feature. Integrating with the depository’s existing account systems is particularly important because depositories are central to ownership records, settlement workflows and operational continuity—areas where regulators generally seek reliability and auditability.

For market participants, the key near-term items to watch are the October settlement-cycle roadmap and the end-2026 KSD OTC settlement system timeline, alongside the July release of subordinate regulations from the token securities public-private council. The sequence of these milestones will offer the clearest signal on how quickly South Korea can move from permission to practical, depository-linked tokenization at scale.

Anthropic’s Mythos artificial intelligence (AI) model reportedly needed only hours to find certain security vulnerabilities in highly sensitive US government computer systems during an intelligence test, a US official told the Associated Press.

Still, that speed does not mean it could exploit them in the same window, the official said, speaking anonymously to discuss the sensitive matter.

Anthropic Mythos Mapped the Weak Spots in Secure Government Systems

The official said the testing was conducted under Project Glasswing. Anthropic opted against a public release for Mythos.

Instead, it granted a select group of more than 50 technology firms early access to the unreleased model, allowing them to identify and remediate critical software vulnerabilities.

Senator Mark Warner of Virginia referenced the tests on June 11. He spoke before the Senate Committee on Banking, Housing, and Urban Affairs.

“This tool broke into almost all of our classified systems, not in weeks but in hours,” he said.

Warner attributed the account to the head of the National Security Agency (NSA) and US Cyber Command, Gen. Joshua Rudd.

Follow us on X to get the latest news as it happens

Mythos already carries a track record of finding flaws. The UK’s AISI (AI Security Institute) tested Mythos Preview on expert-level capture-the-flag challenges. The model succeeded 73% of them. No model had cleared that bar before April 2025.

In April, Mozilla credited the AI model with surfacing 271 vulnerabilities in Firefox. The browser maker patched them in Firefox 150.

Anthropic then launched Claude Fable 5 in early June. It billed the model as a general release version of its Mythos tier, with added safeguards.

The opening was brief. On June 12, the US government issued an export control directive citing national security. The order required the firm to bar every foreign national from Fable 5 and Mythos 5.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Anthropic Mythos Found Cracks in the Government’s Most Guarded Systems appeared first on BeInCrypto.

Key takeaways

- Risk sentiment across financial markets remained fragile following conflicting statements from US and Iranian officials.

- XRP risks dropping below $1.0 if the bearish trend persists.

Ripple’s XRP remained under pressure on Wednesday, trading below $1.10 and maintaining a broader bearish outlook.

The remittance-focused cryptocurrency failed to extend an early-week recovery attempt as investors reacted to renewed geopolitical uncertainty surrounding negotiations between the United States and Iran.

Mixed US-Iran signals fuel market uncertainty

Risk sentiment across financial markets remained fragile following conflicting statements from US and Iranian officials after the first round of peace negotiations held in Switzerland.

US Vice President JD Vance said late Monday that Iran had agreed to allow inspectors from the International Atomic Energy Agency (IAEA) back into the country. However, Iranian authorities disputed the claim, insisting that Tehran had made no additional commitments during the discussions.

Iran’s chief negotiator, Mohammad Bagher Ghalibaf, stated that the United States had agreed to release approximately $12 billion in frozen Iranian assets.

Meanwhile, Donald Trump warned reporters that Washington would take further action if Iran failed to comply with the terms of any agreement.

The conflicting messages have contributed to risk-off sentiment across cryptocurrency markets, limiting demand for digital assets and reinforcing bearish pressure on XRP.

Investor sentiment across the cryptocurrency market remains weak despite a slight improvement in confidence levels.

The Crypto Fear & Greed Index registered a reading of 23 on Monday, remaining firmly in “Extreme Fear” territory. While the index improved marginally from 20 recorded a day earlier, market participants continue to adopt a cautious stance amid macroeconomic and geopolitical uncertainties.

The subdued sentiment suggests that traders remain reluctant to aggressively accumulate risk assets, increasing the likelihood that short-term rallies could face selling pressure.

XRP price forecast: Bears continue to control the trend

From a technical perspective, XRP continues to exhibit a bearish structure on the daily timeframe.

The token is trading well below its key Exponential Moving Averages (EMAs), including the 50-day EMA at $1.25, the 100-day EMA at $1.35, and the 200-day EMA at $1.56.

XRP also remains below the middle Bollinger Band near $1.15, reinforcing the current downward bias.

Momentum indicators further support the cautious outlook. The Relative Strength Index (RSI) sits around 38, signaling weak bearish momentum without yet reaching oversold conditions.

Meanwhile, the Moving Average Convergence Divergence (MACD) histogram remains slightly positive around the zero line, indicating tentative stabilization rather than a decisive trend reversal.

For XRP to regain bullish momentum, buyers must overcome several important resistance zones.

The first hurdle lies at the Bollinger Band midpoint near $1.15, followed by resistance at the upper Bollinger Band around $1.22.

Beyond that, the 50-day EMA at $1.25 and a descending trendline near $1.28 create a significant supply zone. Additional resistance levels are located at the 100-day EMA around $1.35 and the 200-day EMA near $1.56.

A successful break above these barriers would be required to shift the broader market structure back toward a bullish outlook.

On the downside, XRP’s immediate support is located near the lower Bollinger Band at $1.07.

A decisive breakdown below this level could accelerate selling pressure and expose the token to a retest of the recent support zone around $1.05.

Should bearish momentum intensify further, traders may look toward the psychologically important $1.00 level as the next major area of demand.

Until buyers reclaim key resistance levels, XRP remains susceptible to additional downside risk in the near term.

Raining Money – A Sensory Activation For Infinite Wealth

Environment Agency monitoring River Ouse for ammonia

Fortune 500: 5 Ideal Dividend Buys With 2 “Safer” Industry Leaders

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment4 days ago

Entertainment4 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Tech2 days ago

Tech2 days agoMicrosoft accidentally kills epic Outlook email threads

-

Sports17 hours ago

Sports17 hours agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Business4 days ago

Business4 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Crypto World8 hours ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 hours ago

Crypto World5 hours agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Politics6 days ago

Politics6 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Business11 hours ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business4 days ago

Business4 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Politics4 days ago

Politics4 days agoAndy Burnham and the meaning of Makerfield

-

Tech6 days ago

Tech6 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

Crypto World4 days ago

Crypto World4 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World4 days ago

Crypto World4 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

NewsBeat5 days ago

NewsBeat5 days agoKeir Starmer Allies Question His Chances For No 10

-

Crypto World4 days ago

Crypto World4 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Tech2 days ago

Tech2 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Tech3 days ago

Tech3 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Business6 days ago

Business6 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

-

Sports5 days ago

Sports5 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

You must be logged in to post a comment Login