Crypto World

Michael Saylor unveils Bitcoin’s four tribes as the market tumbles

Following bitcoin’s worst week in two years, Strategy(MSTR) Executive Chairman Michael Saylor published a framework on X, arguing that the Bitcoin community is evolving into four distinct ideological camps.

Rather than viewing these groups as competitors, he presents them as complementary forces that will collectively shape bitcoin’s future.

The first group, Bitcoin Maximalists, sees Bitcoin as the ultimate monetary breakthrough. They believe bitcoin has already solved the problem of digital scarcity and offers superior property rights, protection from inflation, and economic empowerment. Their focus is conviction: bitcoin is not one crypto asset among many, but the dominant digital monetary network.

The second group, Bitcoin Capitalists, views Bitcoin as a form of digital capital that should be integrated into the global economy. They support corporate treasury adoption, institutional custody, bitcoin-backed securities, lending markets, and broader financial infrastructure. Their goal is to expand bitcoin’s reach by embedding it into existing economic systems rather than replacing them.

The third group, Bitcoin Technologists, focuses on improving the protocol. They argue that Bitcoin must continue to evolve to address challenges in scalability, privacy, usability, security, and future threats such as quantum computing. While they support innovation, Saylor notes that changes to bitcoin’s base layer must be approached cautiously to avoid unintended consequences.

The fourth group, Bitcoin Fundamentalists, prioritize protecting bitcoin’s original principles: decentralization, self-custody, immutability, censorship resistance, and individual sovereignty. They are wary of excessive institutional influence, financialization, and protocol changes that could compromise Bitcoin’s core characteristics.

Saylor’s central argument is that Bitcoin needs all four perspectives. Maximalists provide conviction, Capitalists drive adoption, Technologists ensure long-term resilience, and Fundamentalists safeguard the protocol’s integrity. Saylor argues that Bitcoin’s most successful path lies in a balance among these four forces.

Sam Bankman-Fried’s X account posted, “Another great quarter for stocks.” The message came despite his ongoing 25-year prison sentence for the FTX fraud.

A prison-approved proxy sent the post, since Bankman-Fried has no direct internet access behind bars. The timing lined up with the close of the stock market’s best quarter since 2020.

Stocks Close Out Their Best Quarter Since 2020

The Dow, S&P 500, and Nasdaq each closed higher on June 30. The S&P 500 gained 0.8%, and the Nasdaq rose 1.5%. Both posted their best quarterly performance since 2020.

The gains held even as the Middle East conflict weighed on broader sentiment. The Dow logged its biggest quarterly jump since 2022. Meanwhile, technology stocks led the advance, with a semiconductor index gaining 3.9% on the day.

The rally extends a longer trend. Stocks have outpaced Bitcoin over the past five years. A $1,000 stake in the S&P 500 from 2021 is now worth more than the same bet on the token.

Traditional markets grabbed other headlines this week too. SpaceX’s Nasdaq 100 debut is set for July 7. It marks the fastest index inclusion on record.

A quarter-end rally followed cooling jobs data and an Iran ceasefire. Together, they pushed indexes to fresh highs into the close.

SBF´s Pardon Play From Behind Bars

Market watchers view the tweet as part of a broader image campaign. Bankman-Fried wants to reposition himself as a market-savvy voice in traditional finance. That framing beats being remembered as the architect of an $8 billion collapse.

The framing lines up with his legal strategy. Bankman-Fried filed for a presidential pardon through the Justice Department in early June. Trump, however, has repeatedly ruled out clemency for him.

That bid faces long odds. A federal appeals court upheld his conviction and sentence earlier in June. Judges rejected claims that the trial judge excluded key evidence. The post follows the same playbook, aiming to reshape his image while his appeal continues.

FTX Token FTT Pumps, Then Crashes Back

Automated trading bots reacted within minutes to SBF’s X post. The FTX token, FTT, briefly jumped by as much as 11%. It then erased the entire move just as fast.

FTT now trades near $0.23, still far below its 2021 all-time high near $84. The token sits just above its multi-year low of $0.22, reached in early June.

Total FTT trading volume remains thin compared to major tokens. The swift reversal suggests thin liquidity, not renewed conviction, drove the spike.

Bankman-Fried’s proxy may keep posting market commentary. Whether it works depends on how much credibility, not just attention, the effort can still buy him.

The post Sam Bankman-Fried is Posting Market Takes From Prison Now appeared first on BeInCrypto.

Crypto World

Europe is closing the door on offshore crypto, but it’s leaving the riskiest window open

ESMA itself said in a February statement that firms with derivatives marketed as “perpetual futures” are likely to fall under the existing product-intervention measures on contracts for difference (CFDs). The commercial name, ESMA said, is irrelevant. Even voluntary negative-balance protection does not alter the analysis. If a perp meets the CFD definition, all CFD rules apply: leverage limits, a mandatory risk warning, margin close-out, negative balance protection and a ban on trading incentives. Those restrictions are a heavy burden on licensed derivatives providers in Europe.The offshore market is teeming with sharksA European investor can open an account at Hyperliquid, the largest decentralized perp trading platform, and take Bitcoin exposure with 50x leverage. Other platforms, like Aster, offer up to 200x leverage on bitcoin. Neither platform is authorized under MiCA or the Markets in Financial Instruments Directive (MiFID), which covers derivatives trading in the EU. There’s no loss limit that the EU can enforce, no key information document, no bonus ban, and no close-out rule, and they’re available to anyone with a self-custody wallet and a few minutes of free time.

And without those protections, retail investors almost always lose: when ESMA and national regulators reviewed the data in 2018, 74% to 89% of retail investment accounts lose money on CFDs across EU jurisdictions, with average losses per client ranging from €1,600 to €29,000.

Crypto World

Palantir (PLTR) Stock Gains Momentum on Nvidia AI Deal and Presidential Stake Disclosure

Key Highlights

- Shares climbed 2.42% in premarket sessions Wednesday, trading at $119.49

- The data analytics firm unveiled a sovereign AI collaboration with Nvidia targeting U.S. federal agencies

- Palantir broadened its existing partnership with Surf Air Mobility to fast-track SurfOS platform development

- Financial disclosures showed President Trump maintains a minimum $1 million position in the company

- Year-to-date performance shows PLTR down approximately 30% and trading beneath key technical indicators

Palantir Technologies (PLTR) experienced a 2.42% uptick during Wednesday’s premarket session, reaching $119.49, following Tuesday’s announcement of strategic partnerships and the revelation of a notable investor in its shareholder registry.

Palantir Technologies Inc., PLTR

The data analytics specialist has struggled throughout 2026, shedding approximately 30% of its value year-to-date, making any bullish developments particularly significant for investors.

The primary catalyst came from a sovereign AI collaboration announcement with Nvidia. This strategic alliance aims to deploy an intelligent infrastructure combining Nvidia’s AI capabilities and Nemotron open-source models within protected, sovereign computing environments—specifically designed for federal government operations and essential infrastructure systems.

The partnership merges Nvidia’s AI platform with Palantir’s comprehensive suite including AIP, Ontology, Foundry, and Apollo technologies.

According to Palantir CEO Alex Karp, this integration will “allow the U.S. government to unleash the full power of LLMs while removing the underlying security risks.” Nvidia’s CEO Jensen Huang characterized the partnership as evidence of “how open models can strengthen America’s leadership in AI.”

Aviation Partnership Receives Boost

The secondary development involved strengthening Palantir’s commercial relationship with Surf Air Mobility. The company pledged additional engineering talent and market development support to accelerate SurfOS evolution, which operates on the AIP and Foundry infrastructure.

Ted Mabrey, Global Head of Commercial at Palantir, stated the platform presents “a clear opportunity to build and define the central operating system for the future of aviation and air mobility.”

Presidential Investment Creates Market Buzz

Contributing to Wednesday’s price action was President Trump’s most recent financial disclosure, submitted to the U.S. Office of Government Ethics on Tuesday.

The documentation reveals Trump maintains a minimum $1 million stake in Palantir, alongside positions exceeding $5 million each in Apple and Nvidia. The complete filing discloses 418 publicly traded equity holdings.

While not representing a dominant portfolio allocation, having a sitting U.S. president publicly identified as an investor typically generates market interest.

Regarding operational performance, Palantir delivered Q1 revenue of $1.63 billion, exceeding analyst consensus estimates of $1.54 billion. The organization maintains profitability, carries zero debt, and continues producing robust free cash flow.

Nonetheless, technical indicators paint a challenging picture. PLTR currently trades 6.7% beneath its 20-day moving average, 11.8% below its 50-day average, and 24.6% under its 200-day moving average. A bearish death cross pattern—occurring when the 50-day SMA drops below the 200-day—materialized in February.

‘Big Short’ investor Michael Burry maintains a documented short position against PLTR, along with similar bets against Tesla and Nvidia.

Analyst sentiment reflects a Moderate Buy rating overall, though bearish perspectives emphasize valuation concerns and potential vulnerabilities related to specific U.K. government contracts.

Both the presidential disclosure and Nvidia partnership were documented Tuesday. PLTR traded at $119.49 during Wednesday’s premarket hours, representing a 2.42% advance.

That transition has also reshaped the Ethereum Foundation itself.

Earlier this year, the foundation published a renewed mandate emphasizing Ethereum’s core values: including credible neutrality, self-sovereignty and open infrastructure, while reducing its involvement in some implementation-focused initiatives. Combined with ongoing budget constraints, the shift has resulted in restructuring across the organization.

Dietrichs views those changes less as a crisis than an overdue evolution. “It’s more a transition period,” he said. “Ethereum is now much more intentionally, proactively reorienting itself to be ready for this new time period.”

Filling in the gaps

But as the turmoil started to unveil itself at the EF, many have started to wonder whether EthLabs would replace it. Dietrichs sees that rather than competing with the foundation, EthLabs intends to complement it. “We’re deliberately positioning ourselves to fill the gaps that the Ethereum Foundation now deliberately leaves,” Dietrichs said. “We’re not trying to create a competing vision for Ethereum.”

Those gaps, he argues, center on adoption-oriented engineering work, like improving Ethereum’s scalability, strengthening layer-1 performance, advancing interoperability, and identifying the technical barriers preventing broader institutional use.

“The gap we see is this more practical, adoption-oriented work, making Ethereum, practically useful for the real world,” he said. EthLabs plans to continue work its founders previously led within the foundation, including layer-1 scaling research, while expanding into areas like interoperability and engagement with financial institutions exploring blockchain infrastructure.

Alt season is the phase when altcoins outrun Bitcoin and portfolios go vertical. Traders have waited more than 260 days for the latest one. Here is what it is, how to measure it, and why it keeps failing to show up.

Summary

- Alt season, or altcoin season, is a sustained period when most altcoins outperform Bitcoin, often producing the largest percentage gains of a market cycle.

- It is measured by the Altcoin Season Index, which tracks how many of the top 100 altcoins beat Bitcoin over 90 days; above 75 is alt season, below 25 is Bitcoin season, and the index sits near 43 in mid-2026.

- The classic pattern is a rotation: Bitcoin rises first, then consolidates, and capital flows out into large-cap alts, then mid-caps, then small-caps.

- The reason alt season keeps not arriving in 2026 is a mix of a bearish Bitcoin far below its record, high Bitcoin dominance, and the ETF wall, where institutional money is locked into Bitcoin through regulated funds instead of rotating into alts.

- The index is reactionary, confirming an alt season only after it has begun, which is why chasing it late and rotating prematurely are the two most common and costly mistakes.

Alt season is the crypto market’s most anticipated and most argued-about phase. It is the stretch of a cycle when the thousands of coins that are not Bitcoin suddenly outrun it, and portfolios that spent months going nowhere go vertical. Traders wait for it, debate whether it has started, and often miss it. As of mid-2026, the wait has stretched past 260 days since the last confirmed alt season, long enough that some question whether the phenomenon still works the way it used to. This guide explains what alt season actually is, how it is measured, the rotation that drives it, and, most usefully right now, why it keeps failing to arrive.

What alt season is

An altcoin is any cryptocurrency other than Bitcoin, from large names like Ethereum, Solana, and XRP down to thousands of small tokens. Alt season is the phase of a market cycle when these altcoins, as a group, significantly outperform Bitcoin over a sustained stretch, typically weeks to a few months. During one, it is common for many altcoins to double or triple while Bitcoin moves sideways or rises more slowly, and the best-performing names can post gains of several hundred percent.

The defining feature is relative performance, not just rising prices. Altcoins can go up while Bitcoin also goes up; what makes it an alt season is that they go up more. Capital that had concentrated in Bitcoin spreads outward into the rest of the market, lifting a broad range of tokens and shifting attention, liquidity, and speculation toward new narratives and projects. It is the part of the cycle that produces the outsized returns crypto is famous for, and also the sharpest reversals when it ends.

Alt season is the counterpart to Bitcoin season, the phase when Bitcoin leads and altcoins lag. The market cycles between the two, and knowing which phase you are in is one of the most useful pieces of context a crypto participant can have, because the same portfolio behaves very differently depending on which is in force.

The Altcoin Season Index

The most-cited way to judge the phase is the Altcoin Season Index, a tool that turns the question into a single number. It measures how many of the top 100 altcoins, excluding stablecoins, have outperformed Bitcoin over the previous 90 days, and expresses that as a score from 0 to 100. The thresholds are simple: a reading above 75 signals a confirmed alt season, meaning at least three quarters of the leading altcoins beat Bitcoin over the window. A reading below 25 signals Bitcoin season, where altcoins are broadly lagging. Anything between 25 and 75 is a mixed or neutral market where no clear rotation has taken hold.

As of mid-2026, the index sits around 43, up sharply from June lows near 11 to 12 but still well short of the 75 needed to confirm rotation. That reading tells a precise story: altcoins have gained some strength off the bottom, with more of them starting to beat Bitcoin, but the market remains in neutral territory, leaning toward Bitcoin, not in an alt season. The jump from the low teens to the low 40s shows early signs of life without confirmation.

The index has one important weakness that every user should understand. It is built on a trailing 90-day window, which makes it a lagging, reactionary measure. By the time it climbs above 75 and confirms an alt season, much of the move has already happened, so the confirmation arrives after the best entry points have passed. The index is excellent for describing where the market has been and poor at predicting where it is going next.

Bitcoin dominance and the rotation

The companion metric is Bitcoin dominance, often written BTC.D, which is Bitcoin’s share of the total crypto market capitalization. When dominance is high, Bitcoin holds most of the market’s value; when it falls, value is shifting into altcoins. Traders watch dominance closely because a sustained decline is one of the clearest signs that capital is rotating out of Bitcoin and into the rest of the market, the essence of an alt season.

In mid-2026, Bitcoin dominance sits in the mid-to-high 50s, and analysts have flagged a sustained break below 55%, and ideally lower, as the threshold that would signal a real, broad rotation. Above that level, Bitcoin is still absorbing the market’s capital, and altcoins struggle to get sustained traction. The mechanism links dominance to the index: falling dominance means altcoins are gaining share, which shows up as more of them outperforming Bitcoin, which lifts the Altcoin Season Index. The two metrics describe the same rotation from different angles.

The reason dominance matters so much is that it captures the flow of money, not just price. An altcoin can rise in dollar terms while Bitcoin rises faster, in which case dominance climbs and it is still Bitcoin season despite green candles everywhere. Only when altcoins outpace Bitcoin does dominance fall and rotation begin. That is why seasoned traders watch dominance alongside price: it strips out the illusion that a rising market is automatically an alt season.

The four phases of the cycle

Alt season does not appear at random; it tends to arrive at a specific point in a repeating cycle with four rough phases. The first is accumulation, when prices stabilize near the bottom of a downturn and early buyers quietly build positions while sentiment is still poor. The second is the Bitcoin-led rally, when fresh capital enters the market and flows first into Bitcoin, the primary on-ramp, pushing it up and often to new highs while altcoins lag.

The third phase is where alt season lives. After Bitcoin rallies hard and then consolidates, moving sideways, holders who have made gains start looking for higher returns elsewhere and rotate capital into altcoins. This rotation is usually sequential instead of simultaneous: money moves first into large-cap alts like Ethereum, then into mid-caps, and finally into small-cap and speculative tokens as risk appetite grows. The fourth phase is the top and unwind, when euphoria peaks, the last speculative money piles into the smallest and riskiest coins, and the cycle eventually reverses into a downturn.

Understanding this sequence explains why alt season has a prerequisite that is often missed: it typically follows a Bitcoin rally to new highs and a consolidation. Without Bitcoin first leading and then pausing, there is no pool of Bitcoin gains to rotate, and no stable backdrop for capital to move out along the risk curve. The phase is not just a mood; it is a specific stage that depends on what came before it.

Why alt season keeps not arriving in 2026

This is the question on every trader’s mind, and the answer is a convergence of factors instead of a single cause. The first is the most basic: alt season usually follows a Bitcoin rally to new highs and a consolidation, and in 2026 Bitcoin has done the opposite. It sits far below its record, in a bearish, drawn-out drawdown, so the precondition of a fresh Bitcoin high that seeds rotation has simply not been met. There are no large Bitcoin gains sitting around waiting to rotate into alts when Bitcoin itself is down.

The second factor is dominance. Bitcoin dominance has stayed elevated in the mid-to-high 50s, above the threshold analysts see as necessary for broad rotation, which means capital keeps concentrating in Bitcoin instead of spreading out. The third, and the most structurally interesting, is the ETF wall. Spot Bitcoin exchange-traded funds have pulled enormous institutional capital into Bitcoin through regulated products, but that money is largely confined to Bitcoin. Unlike the retail flows of past cycles, which moved freely from Bitcoin into thousands of altcoins, institutional capital that enters through a Bitcoin ETF tends to stay in Bitcoin, because those investors gain crypto exposure through the fund and do not rotate down the risk curve into individual tokens. The channel that once carried money from Bitcoin into alts is partly blocked.

There is a fourth factor: selectivity. Even where rotation is happening, it is narrative-driven and concentrated instead of broad. Institutional participation has made the market more discerning, so money managers favor altcoins with clear fundamentals, regulatory standing, and liquidity, while thousands of microcap tokens with no product and no revenue are left behind. The result is that even partial rotations lift a handful of sectors, real-world assets, AI infrastructure, blue-chip DeFi, instead of the whole market. A rising tide that once floated every boat now floats a chosen few, which is why the broad, everything-pumps alt season of past cycles keeps failing to materialize.

Historical alt seasons

The past shows what a real alt season looks like, and how the forces behind them change. The first major one ran through 2017 and into early 2018, driven by the initial coin offering boom. Hundreds of new projects raised money by issuing tokens directly to retail investors, flooding the market with new assets and speculators, and Bitcoin dominance collapsed from around 86% in late 2017 to under 40% at the start of 2018 as money poured into altcoins. It ended in a deep, prolonged bear market that erased most of the gains.

The second ran through 2020 and 2021, powered by different narratives: decentralized finance protocols, non-fungible tokens, new layer-one blockchains, and eventually meme coins. Capital rotated from Bitcoin into DeFi, then NFTs, then competing smart-contract chains, producing enormous gains across sectors. Institutional investors began entering crypto during this cycle, making the market larger but also beginning the shift toward the selectivity now visible in 2026.

The contrast between those cycles and the present is the whole lesson. Both past alt seasons ran on free-flowing retail capital that moved easily from Bitcoin into a wide field of tokens. The 2026 market has more institutional money, more regulation, and the ETF wall, all of which channel capital differently. The historical pattern is not broken, but the plumbing has changed, which is why the same triggers produce a weaker and more selective response than they once did.

The conditions that would trigger one

If alt season is late instead of dead, what would actually bring it? Analysts point to a set of conditions that, when several align, have historically preceded rotation within a quarter. The first and most important is Bitcoin making a new high and then consolidating, which creates both the gains and the stable backdrop that seed rotation. Until Bitcoin recovers and leads, the sequence cannot begin.

The second is a sustained break in Bitcoin dominance below the mid-50s, confirming that capital is genuinely leaving Bitcoin for alts instead of just lifting the whole market together. The third is expanding liquidity, often from central-bank rate cuts, because looser financial conditions push investors toward higher-risk, higher-beta assets, and altcoins are the highest-beta assets in crypto. The fourth is the Altcoin Season Index sustaining a move above roughly 40 to 50 with momentum, showing that outperformance is broadening instead of flickering.

The practical approach that follows from this is to watch the conditions converge instead of guessing a date. When three or more are present at once, the odds of rotation rise sharply. Until then, the index sitting in neutral is telling you plainly that this is not yet alt season, and the traders who override that signal to get in early are usually the ones left holding underperforming tokens while Bitcoin does the work.

The traps to avoid

Alt season is where fortunes are made and lost, and the losses usually come from two predictable mistakes. The first is chasing it late. Because the index is reactionary, by the time it confirms an alt season above 75, the largest and easiest gains have already happened, and entering then means buying near the top of a fast-moving, overextended market. The window is typically two to five months, and the last stretch is the most dangerous, when the smallest and riskiest coins spike and then collapse hardest.

The second mistake is rotating prematurely, moving fully into altcoins before Bitcoin has confirmed a new high and led the cycle. Every past alt season was preceded by Bitcoin leading first, so rotating early means holding depreciating altcoins while Bitcoin outperforms, the opposite of the intended trade. The index sitting in Bitcoin season or neutral is an explicit signal that the rotation has not started, and ignoring it to position early is a common and expensive error.

The deeper trap is treating alt season as a guaranteed event rather than a probability. It is not an on-off switch that must flip in every cycle; it is a phase that depends on conditions, and those conditions can fail to line up, as 2026 shows. The disciplined approach is to track the index and dominance daily, watch for the trigger conditions to converge, and add altcoin exposure selectively and gradually once the signals confirm, instead of betting the portfolio on a rotation that the data has not yet endorsed.

Where the money rotates first

If a rotation does begin, it does not lift every token at once, and knowing the order helps separate a real broadening from a narrow bounce. The sequence tends to follow the risk curve. Capital leaves Bitcoin first for the largest, most liquid altcoin, historically Ethereum, because it is the safest step out along the curve and the easiest for large money to enter. A sustained move in the ETH/BTC ratio is often read as the opening signal that rotation has started at the top of the market.

From there, money tends to move down the size ladder. After large-caps like Ethereum absorb the first wave, capital flows into mid-cap tokens with proven products and liquidity, then finally into small-cap and speculative names as risk appetite grows and traders chase higher percentage gains. This is why the late stage of an alt season is the wildest: the smallest and least proven coins move last and hardest, which is also why they fall the fastest when the phase ends. The order is a rough gauge of how far a rotation has traveled.

Sector leadership matters as much as size. In any given cycle, rotation concentrates in a few narratives instead of spreading evenly, and the leading sectors change from cycle to cycle. In 2026 the candidates most often cited include layer-two scaling networks, real-world asset tokenization, blockchain infrastructure for artificial intelligence, and blue-chip decentralized finance. Meme coins typically peak last and crash hardest, which makes their surge a late-stage signal more than an early one. Watching which sectors lead tells you what the market is actually rewarding, not just that alts are moving.

The selectivity point returns here with force. Because institutional capital favors tokens with fundamentals, liquidity, and regulatory standing, a modern rotation can lift a handful of quality names while thousands of microcaps stay flat, which looks nothing like the everything-pumps seasons of the past. A trader watching only a favorite microcap might conclude alt season never came, while large-cap and sector leaders quietly outperformed. Judging rotation by the leaders and the index, not by one held bag, gives a truer read.

The practical use of all this is sequencing your own attention. Track the ETH/BTC ratio for the first sign that money is stepping out of Bitcoin, watch whether strength broadens from large-caps into mid-caps as confirmation, and treat a frenzy in the smallest coins as a late-cycle warning instead of an invitation. Rotation is a process with an order, and reading that order is more useful than waiting for a single index number to flip.

Frequently Asked Questions

What is alt season in crypto?

Alt season, or altcoin season, is a sustained phase of the market cycle when most altcoins, meaning cryptocurrencies other than Bitcoin, significantly outperform Bitcoin. During one, many altcoins can double or triple while Bitcoin moves sideways or rises more slowly. It is defined by relative performance, altcoins gaining more than Bitcoin, and it produces some of the largest percentage returns of a cycle.

How is alt season measured?

The main tool is the Altcoin Season Index, which tracks how many of the top 100 altcoins, excluding stablecoins, outperformed Bitcoin over the previous 90 days, scored from 0 to 100. Above 75 confirms an alt season, below 25 signals Bitcoin season, and 25 to 75 is neutral. Traders also watch Bitcoin dominance, since a sustained decline signals capital rotating from Bitcoin into altcoins.

What is Bitcoin dominance and why does it matter?

Bitcoin dominance is Bitcoin’s share of the total crypto market capitalization. High dominance means Bitcoin holds most of the market’s value; a falling reading means capital is shifting into altcoins. A sustained break below the mid-50s is often flagged as the threshold for a real, broad rotation. Dominance captures the flow of money, so it can reveal Bitcoin season even when altcoin prices are rising.

Why has alt season not arrived in 2026?

Several factors have converged. Bitcoin is far below its record in a bearish drawdown, so the usual precondition of a fresh Bitcoin high has not been met. Dominance has stayed elevated. And the ETF wall keeps institutional money locked in Bitcoin through regulated funds instead of rotating into alts. Rotation that does occur is selective and narrative-driven instead of broad.

What is the ETF wall?

The ETF wall describes how spot Bitcoin exchange-traded funds pull large institutional capital into Bitcoin but largely keep it there. Unlike past cycles where retail money moved freely from Bitcoin into thousands of altcoins, investors who gain exposure through a Bitcoin ETF tend to stay in Bitcoin rather than rotating into individual tokens. This partly blocks the channel that historically carried money into alts.

What would trigger an alt season?

Analysts point to a set of conditions that, when several align, have preceded rotation: Bitcoin making a new high and consolidating, a sustained break in Bitcoin dominance below the mid-50s, expanding liquidity such as from rate cuts, and the Altcoin Season Index sustaining above roughly 40 to 50 with momentum. When three or more appear together, the odds of rotation within a quarter rise sharply.

Is the Altcoin Season Index a good timing tool?

Only partly. The index is built on a trailing 90-day window, which makes it reactionary. By the time it confirms an alt season above 75, much of the move has already happened, so it describes where the market has been better than where it is going. It is useful for context, but relying on it to time entries usually means arriving late, after the easiest gains have passed.

What mistakes do traders make around alt season?

The two most common are chasing it late, buying after the index confirms and the biggest gains are gone, and rotating prematurely, moving into altcoins before Bitcoin has led and confirmed a new high, which leaves them holding underperforming tokens while Bitcoin rises. A third is treating alt season as guaranteed rather than a conditional phase that can fail to arrive, as 2026 has shown.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and market cycles are unpredictable. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures such as the Altcoin Season Index and Bitcoin dominance are accurate as of July 1, 2026, and will change.

“A MiCA license is not something you can buy because you have money and power,” he said. “It is making sure every process is fully transparent.”

Still, Fazel acknowledged the new rules will be hardest on startups because obtaining and maintaining a license requires significant capital.

“If there’s one segment I feel bad for, it’s startups,” he said. “Innovation may suffer for companies that don’t have enough capital.”

A level playing field

For licensed exchanges, another question remains: whether regulators can enforce the new rules against firms operating outside the European Union.

Dr. Lin Han, founder and CEO of Gate Group, said licensed exchanges have spent years preparing for MiCA, but the framework only works if everyone follows it.

“Everybody needs to follow the rule,” Han said. “Then we can compete on better service for users.”

The European Securities and Markets Authority (ESMA) has said firms serving EU clients without MiCA authorization are breaching EU law and should stop offering those services. It has also warned firms not to rely on “reverse solicitation” to continue serving European customers and has encouraged measures such as geo-blocking to prevent access.

Han questioned whether regulators have the resources to prevent unlicensed platforms from continuing to operate from overseas.

Binance has been hit with a £150 million ($200 million) lawsuit, accusing it of offering illegal derivative products, just one day before the exchange is due to exit EU markets.

Almost 1,700 British investors joined together to file the lawsuit in London’s High Court yesterday, claiming it offered risky derivative products without permission from the UK’s financial regulator, the FCA.

Investors claim to have lost tens of thousands, and in some cases millions, on derivatives offered between 2019 and 2020 while the exchange was under the leadership of its former CEO and founder, Changpeng Zhao.

A KP Law partner told the Financial Times, “Our clients are ordinary people, many of whom committed significant savings and who have suffered real financial harm. We are determined to hold Binance and its founder, Changpeng Zhao, to account.”

The exchange said it will “defend against these claims through the appropriate legal process in due course. Binance remains committed to its obligations to users and to operating in accordance with applicable law.”

Defendants in the lawsuit include Zhao, Binance’s Cayman Islands entity, the UAE-registered Nest Exchange, and unknown persons operating the Binance Trading Platform.

Time’s up for Binance in the EU

The lawsuit was filed just one day before Binance has to remove its operations from EU territories today, due to its failure to secure a license under the bloc’s Markets in Crypto-Assets Regulation (MiCA).

Binance had originally been earmarked to secure a license from Greece and believed it was compliant with MiCA regulations. It then withdrew its application on June 26 and claimed it would pursue a different EU member state.

According to The Block’s Gareth Jenkinson, European Central Bank President, Christine Lagarde, “directly ordered Greece to reject Binance’s MiCA license application.”

Jenkinson’s undisclosed source claimed Binance had “essentially been given the green light by Greece’s regulator, before the ECB stepped in.”

Read more: Binance probed by DoJ, files lawsuit against WSJ

Zhao claimed in an interview with Jenkinson that two EU countries were vying for Binance’s application until political forces intervened.

Despite the setback, Binance Head of Europe and the UK, Gillian Lynch, boldly claimed, “Binance is not leaving Europe.”

Binance CEO Richard Teng also said the company is committed to securing a license “in the coming months.”

However, it appears Binance has failed to find another welcoming EU country in time for the July 1 MiCA deadline, which it’s had six years to prepare for.

The exchange has stressed that any impacted users will still have access to withdraw their funds.

Teng added today, “Please know that we are working hard behind the scenes, including in close engagement with regulators, to navigate this transition responsibly and to continue serving our users in the best way possible.”

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

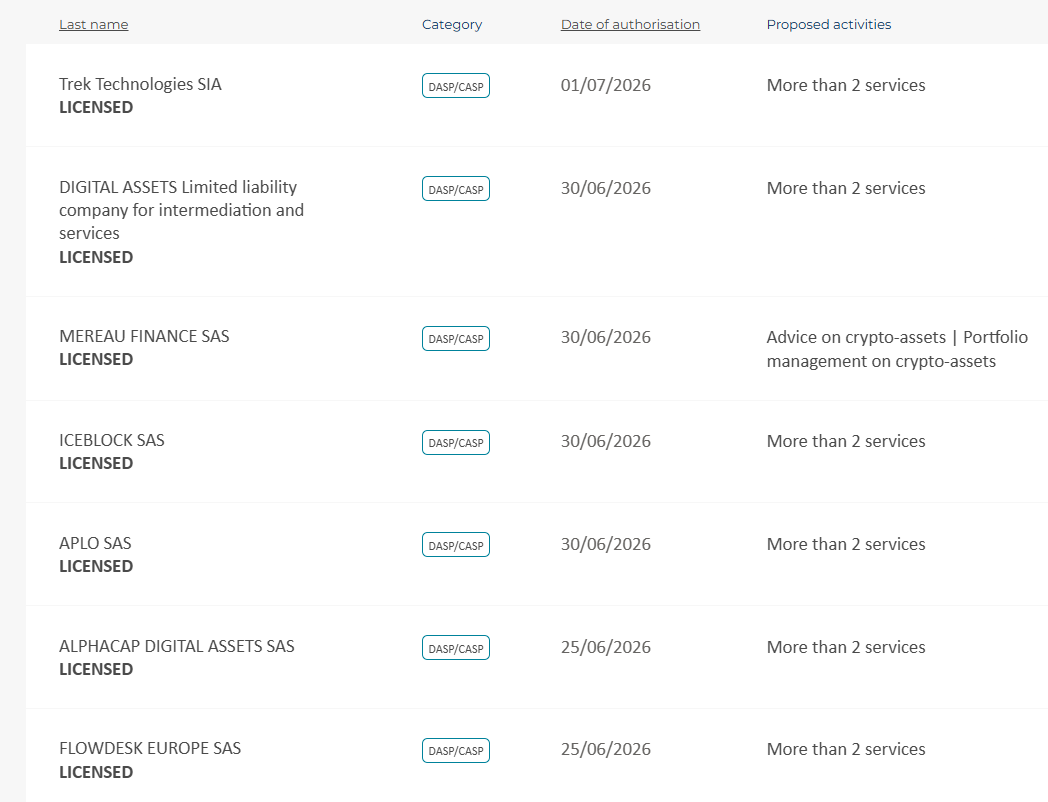

A slew of last-minute licenses were issued to cryptocurrency companies in Europe as Wednesday marked the end of the transitional period under the Markets in Crypto-Assets Regulation (MiCA).

Four companies were authorized in Italy this week, including asset management platform Hodlie, crypto exchange Young Platform, trading platform CryptoSmart and crypto service provider Hercle, bringing Italy’s total to eight authorized crypto asset service providers (CASPs), according to a Tuesday announcement from the Bank of Italy. The central bank said the country’s financial regulator, Consob, approved the licenses in coordination with it.

The French financial markets regulator, Autorité des marchés financiers (AMF), also added three new companies on Tuesday, including crypto investment platform Mereau Finance, blockchain infrastructure provider Iceblock and crypto service provider Aplo, bringing the total number of licensed CASPs to 31.

In Malta, digital asset prime broker FalconX announced Monday that it had received a MiCA license, while Venga announced on Wednesday that it had received CASP authorization from Spain.

The licenses were issued during the final stretch of MiCA’s 18-month transitional period, which ended on Wednesday. By Friday, the European Securities and Markets Authority’s (ESMA) interim register showed 244 authorized CASPs across the European Union and European Economic Area.

France’s whitelist includes newly licensed CASPs. Source: AMF

Related: Polish president vetoes crypto bill for third time ahead of MiCA deadline

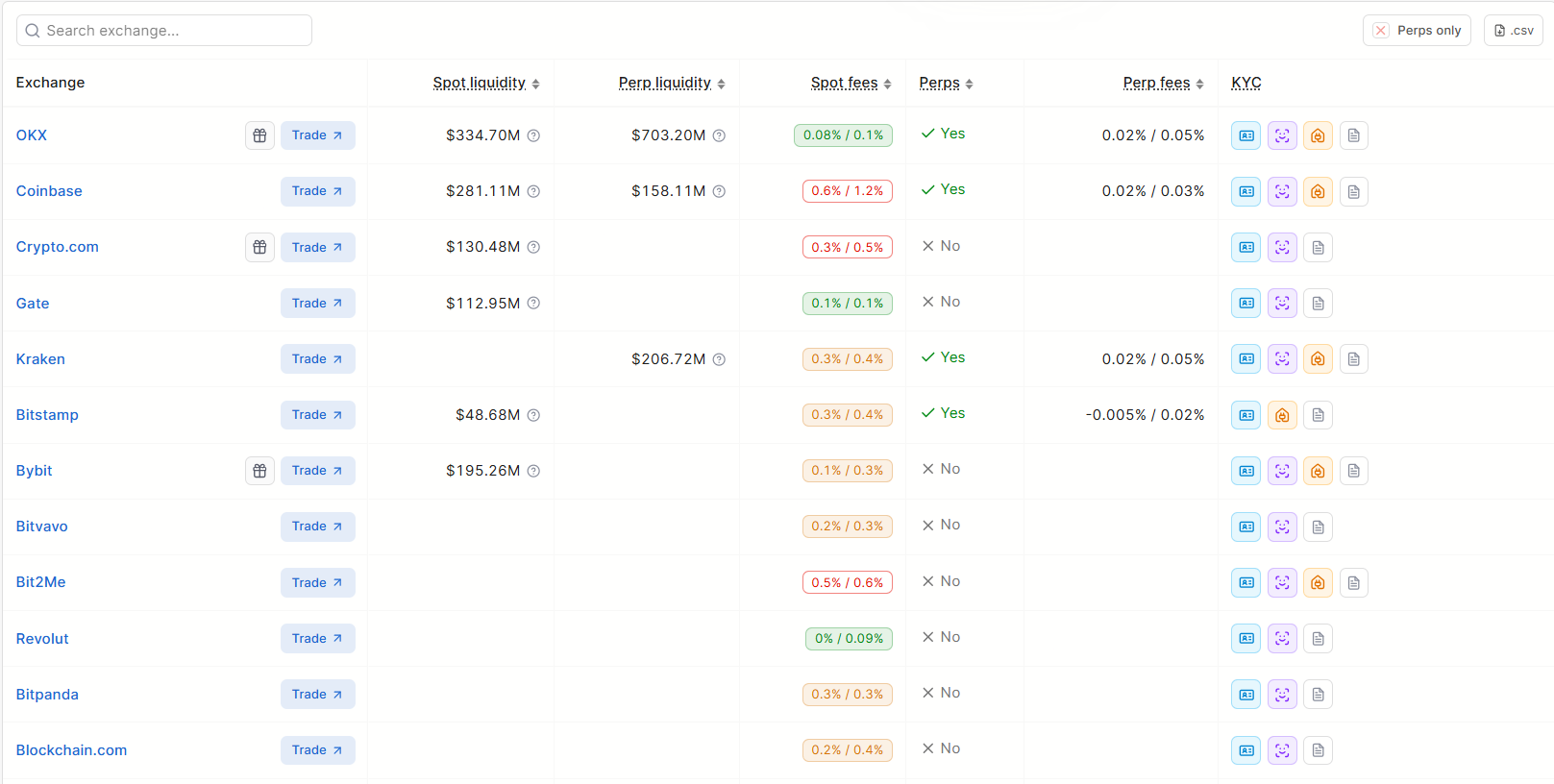

Largest MiCA-authorized exchanges emerge as transition ends

Binance, the world’s largest crypto exchange by trading volume, remains unlicensed under MiCA. The exchange applied for authorization in Greece but later withdrew its application, saying it will seek authorization in another member state.

Greece is among the EU member states that have yet to issue a MiCA license.

On June 23, the European Securities and Markets Authority (ESMA) said crypto service providers that remain unauthorized by the deadline must take “immediate” steps to wind down their EU activities.

With Binance remaining unlicensed under MiCA, the largest MiCA-authorized exchanges by spot orderbook liquidity include OKX, Coinbase, Bybit, Crypto.com, Gate and Bitstamp, according to DefiLlama data.

MiCA-regulated cryptocurrency exchanges in Europe. Source: DefiLlama

Magazine: Crypto wanted to overthrow banks, now it’s becoming them in stablecoin fight

The assumption is simple: Ripple goes public, XRP moons. The reality is that Ripple equity and the XRP token are different assets, and the channels connecting them are weaker than the hype suggests.

Summary

- Ripple remains private with no S-1 on file, but a $750 million buyback fixed its valuation near $50 billion and private secondary shares have surged to about $136.90, keeping IPO speculation loud.

- Ripple equity and the XRP token are legally separate: owning XRP gives no claim on the company, and a public listing would not hand shareholders or token holders any automatic link between the two.

- The plausible transmission channels are sentiment, Ripple’s escrow and sell behavior, institutional validation, and value accrual, and each is weaker or more two-sided than the “IPO equals XRP moon” story assumes.

- There is a real counter-case that an IPO could pull capital away from XRP, by giving investors who want Ripple exposure a way to buy the stock instead of the token.

- The evidence so far is mixed: XRP briefly re-coupled to Ripple’s rising private valuation, yet the token is still down about 26% on the year, which points to weak, not strong, transmission.

The reflex in the XRP community is automatic. Ripple goes public, the story goes, and XRP rockets alongside it. The logic feels obvious, because Ripple and XRP are wrapped together in the same brand, the same headlines, and the same decade of shared history. But an initial public offering sells shares in a company, and XRP is a token that confers no ownership of that company.

Whether a Ripple listing would actually move the token is not a matter of sentiment or loyalty. It is a question of mechanism: through what channels, if any, would value flow from a Ripple equity event into the XRP price? This piece examines those channels one by one, and finds them thinner than the hype implies. The XRP holder payout question has already become a separate community obsession, but the XRP holder payout question is not the same as a price-transmission mechanism.

The starting point: Ripple equity and XRP are different assets

Everything begins with a distinction the excitement tends to blur. Ripple Labs is a private company. XRP is a digital asset that trades on public exchanges. There is no mechanism that entitles an XRP holder to Ripple shares, dividends, or any slice of the company’s profits, and a public listing would not create one.

If Ripple lists tomorrow, an XRP holder owns exactly what they owned the day before: a token, not a piece of the business. The one concrete link runs the other direction. Ripple is itself one of the largest holders of XRP, with tens of billions of tokens held in escrow that it releases on a schedule and uses, in part, to fund operations. So the company’s relationship to the token is that of a giant holder and periodic seller, not a value conduit that passes equity gains down to token holders.

That asymmetry matters for the whole analysis. When people say an IPO would help XRP, they are really claiming that something about Ripple becoming public would change demand for, or supply of, the token. The rest of this piece tests each version of that claim. Until then, Ripple equity and XRP should be treated as related but legally separate assets, not two versions of the same exposure.

Channel one: sentiment and attention

The first and most immediate channel is psychological. An IPO would be a media event, a wave of coverage, analyst notes, and credibility that reframes Ripple from a litigation-scarred crypto firm into a public company vetted by underwriters and public markets. In a market where attention is a real driver of price, that halo could spill onto XRP, lifting the token on narrative even without any mechanical connection. That is the channel the community understands instinctively, because XRP has always traded partly on Ripple headlines.

There is some evidence this channel is live. When Ripple’s private secondary shares surged, one analysis linked the move to XRP briefly re-coupling with the company’s rising valuation, as the market started treating the private-share price near $136.90 as a fundamental signal for the token. That is the sentiment channel working in real time: a Ripple equity data point moving XRP through association rather than mechanics. It is also why where XRP could go from here depends partly on whether traders treat corporate news as a catalyst or just another temporary headline.

The limit is that sentiment is fickle and shallow. It can lift a token into an event and drop it just as fast afterward, and it does not build the sustained demand that holds a price up. A narrative bump around an IPO is plausible. A durable re-rating on sentiment alone is not, which is why this channel, while real, is the weakest foundation for a lasting move.

Channel two: Ripple’s escrow and sell behavior

The most underappreciated channel runs through Ripple’s own balance sheet. Because Ripple holds a vast XRP escrow and sells tokens to help fund itself, anything that changes the company’s need to sell XRP changes the supply hitting the market. This is where an IPO could actually matter mechanically. A successful listing would raise cash and give Ripple a public currency, its own stock, to fund acquisitions and operations.

A cash-rich, publicly funded Ripple might lean less on programmatic XRP sales, easing a source of sell pressure that has weighed on the token for years. That is a genuine, if indirect, bullish path. Less selling from the single largest holder is a supply-side positive that does not depend on sentiment. It is the most concrete way an IPO could help XRP.

The two-sided catch is disclosure. Going public subjects Ripple to far heavier reporting requirements, which means the escrow, the sales, and the token’s role in Ripple’s finances would face new scrutiny from public-market investors and regulators. Greater transparency could reassure the market, or it could surface uncomfortable details about how much the company depends on token sales, which would cut the other way. The escrow channel is the strongest mechanical link, but its direction is not guaranteed.

Channel three: institutional access and validation

The third channel is legitimacy. A public Ripple would sit inside the regulated financial system in a way it does not today, and that validation could radiate outward to the whole XRP ecosystem. The backdrop already leans this way: XRP was recognized as a commodity in March, and seven spot XRP exchange-traded funds are trading with roughly $1.43 billion in cumulative inflows. A high-profile Ripple listing would add another layer of institutional acceptance, potentially making allocators more comfortable holding XRP through regulated products.

The argument is that validation compounds. Each step that moves XRP from contested asset toward accepted infrastructure lowers the barrier for the next institution, and a Ripple IPO would be a large step. In a world where the token already has ETF access, a public parent company strengthens the case that the ecosystem is durable. That is also why XRP’s regulatory status matters more than the IPO hype itself: institutions care less about community excitement than about whether the asset can be held cleanly under durable rules.

The weakness is that validation of the company is not the same as demand for the token. Institutions can conclude that Ripple is a fine investment and express that view by buying the stock, which does nothing for XRP. Legitimacy is a soft tailwind, helpful at the margin, but it does not force anyone to buy the token. For a durable move, validation has to become measurable token demand, not just a better story around the issuer.

Channel four: the value-accrual problem

This is the channel that breaks the simple story, and it is the most important. For an IPO to lift XRP durably, Ripple’s commercial success has to translate into demand for the token. But Ripple’s business and XRP’s value are only loosely coupled. Many of Ripple’s bank and payment partners use its software without touching XRP at all, and the company earns revenue from services, licensing, and acquisitions that do not route through the token.

Ripple can thrive as a company while XRP stagnates, because the token’s value depends on settlement usage and demand for XRP itself, instead of on Ripple’s profit and loss. This value-accrual gap explained is the reason a Ripple IPO is not the guaranteed catalyst holders imagine. An IPO rewards equity holders for the company’s success. It does not, by itself, create the on-chain demand that would lift the token.

Unless a listing changes how much XRP is actually used to move value, the mechanical link from Ripple’s public-market performance to the XRP price is faint. The token needs its own demand story, and the IPO does not write one. It may make Ripple more visible, more credible, and more valuable. None of that automatically makes XRP more scarce or more necessary.

The counter-case: an IPO could hurt XRP

The overlooked possibility is that a Ripple listing works against the token. For years, buying XRP was one of the only ways for a public investor to express a view on Ripple’s success. An IPO removes that constraint by offering the pure play: if you want exposure to Ripple, you buy the stock, which actually owns the business, the revenue, and the growth. The token, which owns none of that, becomes the inferior vehicle for a Ripple bet.

That substitution could siphon capital and attention away from XRP toward the equity. Some of the speculative demand that flowed into the token as a Ripple proxy would rationally rotate into shares once shares exist. In this reading, the IPO does not transmit value to XRP at all. It competes with it.

The very event the community treats as the catalyst could turn out to be a drain, redirecting the Ripple trade into a security that leaves the token behind. That does not mean XRP must fall on a Ripple IPO. It means the direction is not obvious, because the listing creates both a halo effect and a substitute asset. The market would have to decide whether XRP remains the best way to trade Ripple’s ecosystem once Ripple stock exists.

What the evidence shows so far

The cleanest test available is how XRP has behaved as Ripple’s private valuation has climbed. The answer is telling. Ripple’s secondary shares surged to about $136.90 and its valuation was fixed near $50 billion, and while XRP did briefly re-couple to that move on sentiment, the token still trades near $1, down roughly 26% on the year. If the transmission were strong, a 376% surge in Ripple’s private-share price should have dragged XRP sharply higher.

It did not. The token acknowledged the news and kept falling with the broader market. That is the empirical verdict: transmission exists, but it is weak. Ripple getting more valuable has not made XRP more valuable in any durable way, which is exactly what the value-accrual analysis predicts.

An actual IPO would be a bigger event than a private-share revaluation, so the sentiment bump could be larger. But the underlying mechanics that limited the private-market spillover would still apply to a public one. The stock would price Ripple’s business, while XRP would still need regulatory clarity, ETF flows, settlement usage, and broader market support. The link is real enough for traders to chase, but not strong enough to treat as automatic.

What would actually move XRP

If the IPO is a weak lever, what is a strong one? The catalysts that genuinely drive XRP are the ones that change token demand or supply directly. Regulatory outcomes rank first: whether crypto market-structure legislation codifies XRP’s status cleanly, which affects how freely institutions can hold it. ETF flows rank second, because sustained inflows into the seven XRP funds are real, measurable demand for the token.

Settlement usage ranks third: whether XRP is actually used to move value at scale, against the escrow supply that keeps entering the market. That is where XRP fits in settlement becomes more important than the IPO narrative. XRP needs recurring use as a bridge asset or liquidity tool, not just Ripple’s name in public-market headlines. And the direction of Bitcoin and the broader market ranks alongside all of them, since XRP rarely fights the tape.

Against those, a Ripple IPO sits at the edge of the picture. It could add a sentiment bump, it could ease Ripple’s XRP selling, and it could burnish the ecosystem’s legitimacy. Each is a real but modest channel, and at least one plausible effect points the wrong way. The honest conclusion is that a Ripple IPO would be a meaningful corporate event that most likely moves XRP far less than the community expects, and possibly not in the direction they assume.

The Coinbase and Circle precedent

The clearest way to test the transmission question is to look at crypto-adjacent companies that already trade publicly, because they show what happens when a company and the tokens around it are separated on public markets. Coinbase is the obvious case. Its stock gives investors exposure to the exchange’s revenue, which rises and falls with trading volume, but owning the stock is not the same as owning the assets that trade on it. When crypto rallies, Coinbase revenue tends to rise, so there is a loose correlation, yet the stock and the broader token market frequently move apart, because the equity is priced on the business and the tokens are priced on their own supply and demand.

Circle offers a sharper version of the lesson. Circle issues the USDC stablecoin, but USDC is a dollar-pegged token that does not float, so Circle equity captures the value of the issuing business, the reserves, the yield, the growth, while the token itself is designed to stay at a dollar. The company can be worth a great deal while the token it issues, by construction, accrues none of that equity value. That is the extreme illustration of the point: a token and its issuer’s stock can be almost entirely decoupled.

XRP sits somewhere between these cases. It is not a dollar peg, so it can appreciate, but it is also not an equity claim on Ripple, so it does not capture the company’s growth the way shares would. Even when Ripple-linked infrastructure appears in real capital-markets events, such as stablecoin settlement using RLUSD on the XRP Ledger, the immediate value still tends to accrue to the rails, the issuer, or the company before it accrues to XRP itself. The precedent from public crypto companies is that the market prices the business and the token separately, and a listing that rewards the equity does not automatically reward the associated token.

A Ripple IPO would most likely follow the same script, with the stock absorbing the value of the business while XRP continues to trade on its own drivers. That does not make the IPO irrelevant. It makes it indirect. The market would finally have a clean way to buy Ripple, and that could clarify how much demand for XRP was really token demand versus company-proxy demand all along.

What a realistic IPO scenario looks like for XRP

It helps to walk through how an actual Ripple listing would probably play out for the token, stage by stage, because the timeline reveals where the modest effects concentrate. In the announcement phase, when Ripple confirms an S-1 or a date, expect a sentiment spike: headlines, community excitement, and a short-term bid in XRP as traders position for the event. This is the sentiment channel firing, and it could produce a sharp but shallow move that fades as the news is absorbed.

In the run-up to the listing, attention would build, and XRP could trade with elevated volatility as speculation swings between the “IPO lifts XRP” and “IPO competes with XRP” theses. Some capital that had been using XRP as a Ripple proxy might already begin rotating toward the anticipated equity, capping the token’s upside even amid the excitement. The listing itself would be an equity event: shares price, the stock trades, and the value of Ripple’s business gets marked by the market. XRP would react mostly to the tone, a strong debut lifting sentiment, a weak one dampening it, rather than to any mechanical flow.

In the aftermath, the durable question resurfaces: does anything about a public Ripple change token demand or supply? If a cash-rich Ripple eases its XRP selling, that supply relief could support the token over time, the most concrete lasting benefit. If investors conclude the stock is the better Ripple bet, capital could keep rotating out of XRP into shares. The realistic net is a sentiment-driven spike around the event that mostly fades, a possible modest supply-side benefit if Ripple sells less XRP, and an ongoing competitive pull from the equity.

That is a meaningful corporate story with a muted and two-sided token effect, which is a long way from the moonshot the community pictures. The IPO could matter. It just would not erase the legal separation between the company and the token. XRP would still need its own demand engine.

Frequently asked questions

Does owning XRP give you a stake in Ripple?

No. XRP is a digital token that trades on public exchanges and confers no ownership of Ripple Labs, no shares, no dividends, and no claim on the company’s profits. Ripple the company and XRP the token are legally separate. A Ripple IPO would sell shares in the business, and holding XRP would give you no automatic right to those shares or their gains.

Has Ripple actually filed to go public?

Not as of late June 2026. Ripple remains private with no S-1 on file and no confirmed date, and executives have repeatedly downplayed the urgency of a listing. The speculation is driven by signals such as a $750 million share buyback that fixed the valuation near $50 billion and a surge in private secondary shares to about $136.90, not by an official filing. That distinction matters because IPO speculation can move sentiment long before any legal filing exists.

Could a Ripple IPO raise the XRP price?

It could, through weak and indirect channels. A listing could lift XRP on sentiment, could ease sell pressure if a cash-rich public Ripple relies less on XRP sales, and could add legitimacy to the ecosystem. None of these is a mechanical guarantee, and the evidence so far shows only faint transmission from Ripple’s rising valuation to the token. The stronger catalysts are still regulatory clarity, ETF flows, and actual XRP settlement usage.

How could an IPO hurt XRP?

By offering a substitute. An IPO would let investors who want Ripple exposure buy the stock, which actually owns the business, instead of the token, which does not. Some speculative capital that flowed into XRP as a Ripple proxy could rotate into the equity once it exists, redirecting demand away from the token rather than toward it. That is why a Ripple IPO is not automatically bullish for XRP.

What is the value-accrual problem?

It is the gap between Ripple’s success and XRP’s value. Many Ripple partners use its software without touching XRP, and much of its revenue does not route through the token. So Ripple can prosper as a company while XRP stagnates, because the token’s value depends on settlement usage and its own demand, not on Ripple’s profit and loss. This is why an IPO is not a guaranteed catalyst.

Did XRP move when Ripple’s private valuation rose?

Briefly and weakly. When Ripple’s secondary shares surged to about $136.90, one analysis linked it to XRP re-coupling with the valuation on sentiment. But XRP still trades near $1, down about 26% on the year, so a large rise in Ripple’s private-share price did not drag the token durably higher. That points to weak transmission between the two.

What actually drives the XRP price?

The strongest drivers are regulatory clarity on XRP’s status, sustained ETF inflows into the seven spot XRP funds, real settlement usage against the escrow supply, and the direction of Bitcoin and the broader market. These change token demand or supply directly. A Ripple IPO sits at the edge of that list, a modest and two-sided factor instead of a primary catalyst. The event may affect attention, but attention is not the same as recurring demand.

Would Ripple sell more or less XRP after an IPO?

Possibly less, which would be the most concrete bullish channel. A listing would raise cash and give Ripple a public stock to fund operations and deals, potentially reducing its need to sell XRP from escrow. The offsetting risk is that going public brings heavier disclosure of the escrow and token sales, which could reassure or unsettle the market depending on what it reveals. The direction depends on what the filings show and whether Ripple actually changes its sell behavior.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and corporate plans such as an IPO are speculative and can change. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures are accurate as of July 1, 2026, and will change.

Ripple has joined the OpenUSD (OUSD) consortium as a launch integration partner, placing itself inside a stablecoin initiative backed by more than 140 companies across payments, banking, fintech, and crypto.

However, according to crypto analyst WrathofKahneman, there’s a catch: OpenUSD will be launching on Solana, Stellar, Base, and Polygon, but not on the XRP Ledger, which has left traders asking what Ripple will actually get out of the deal and whether XRP could benefit at all.

Ripple Joins OpenUSD as Questions Swirl Around XRP

In a July 1 thread on X, WrathofKahneman described OpenUSD as a consortium-backed dollar stablecoin designed to solve pain points for businesses by enabling free minting and redemption and removing volume limits. It will also distribute reserve earnings to partners after deducting management fees.

According to Open Standard, the independent entity that will govern the token, OpenUSD, will go live later this year, with Visa, Mastercard, Stripe, Coinbase, BlackRock, Google, and Bybit among the companies backing it.

The analyst argued that the project is in part an anti-USDC play engineered by Stripe. Recall that Stripe bought Bridge earlier this year specifically for its OCC bank charter, and per WratheofKahneman, OpenUSD will let Stripe “get out from under Circle by creating neutral infrastructure and shared economics.”

They think that positioning makes OpenUSD dangerous for Circle’s margins, since a stablecoin where every partner feels like a co-owner is a hard thing to compete against with a traditional single-issuer model.

As for Ripple, the industry observer doesn’t think the company had much choice.

“Ripple doesn’t want to be absent from a massive payments-stablecoin consortium, even if OpenUSD is not issued on XRPL, because they sell payments infra,” they wrote.

They also noted that Ripple’s business would be fine, even if it lost some RLUSD profit to the new stablecoin. And speaking of RLUSD, the analyst said there is only a small overlap, given that OpenUSD is built for the broader economy, while RLUSD is primarily used for settlements within Ripple’s own stack.

On XRP, WrathofKahneman was a bit more uncertain, suggesting that the worth of the Ripple token requires value coming into the ledger, and it may only be affected if OpenUSD is eventually issued on XRPL.

“It would only help,” they explained. “But this is a big ‘if’ and likely why Ripple got in the consortium even if not yet issuing.”

The market watcher also flagged the presence of Coinbase in the group despite its deep USDC ties, saying it showed platforms are hedging against getting boxed into a single stablecoin economy.

Competition Moving Toward Shared Infrastructure

OUSD is entering a market where stablecoin issuers and payment firms are increasingly competing over infrastructure instead of individual tokens.

For instance, earlier this month, Mastercard expanded support for several stablecoins, including RLUSD and USDC, across networks such as XRPL, Ethereum, Solana, Arbitrum, and Base. According to the company, the move was to position itself as a neutral infrastructure provider rather than backing one issuer.

The post Ripple’s OpenUSD Move: Payment Infrastructure Push or XRP Value Catalyst? appeared first on CryptoPotato.

Kathleen Krüger takes over as Hamburg’s head of sport

Playstation To Stop Producing Physical Discs In 2028

TRUMP: AMERICA WILL BUY XRP IN MASS??! HUGE XRP BOMBSHELL!!!

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World2 days ago

Crypto World2 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics6 days ago

Politics6 days agoPotential 2028er World Cup attendee leaderboard

-

Business5 days ago

Business5 days agoAsia stock markets slide as tech shares slump

-

News Videos3 days ago

News Videos3 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech6 days ago

Tech6 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business1 day ago

Business1 day agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World4 days ago

Crypto World4 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports5 days ago

Sports5 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech4 days ago

Tech4 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech4 days ago

Tech4 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World5 days ago

Crypto World5 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World5 days ago

Crypto World5 days agoRTX holders must register wallets before token distribution begins

-

Crypto World6 days ago

Crypto World6 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

-

Tech2 days ago

Tech2 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Business2 days ago

Business2 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

You must be logged in to post a comment Login