Crypto World

Nine Wallets Earned $2.4M With 98% Win Rate on Polymarket Military Bets: Bubblemaps

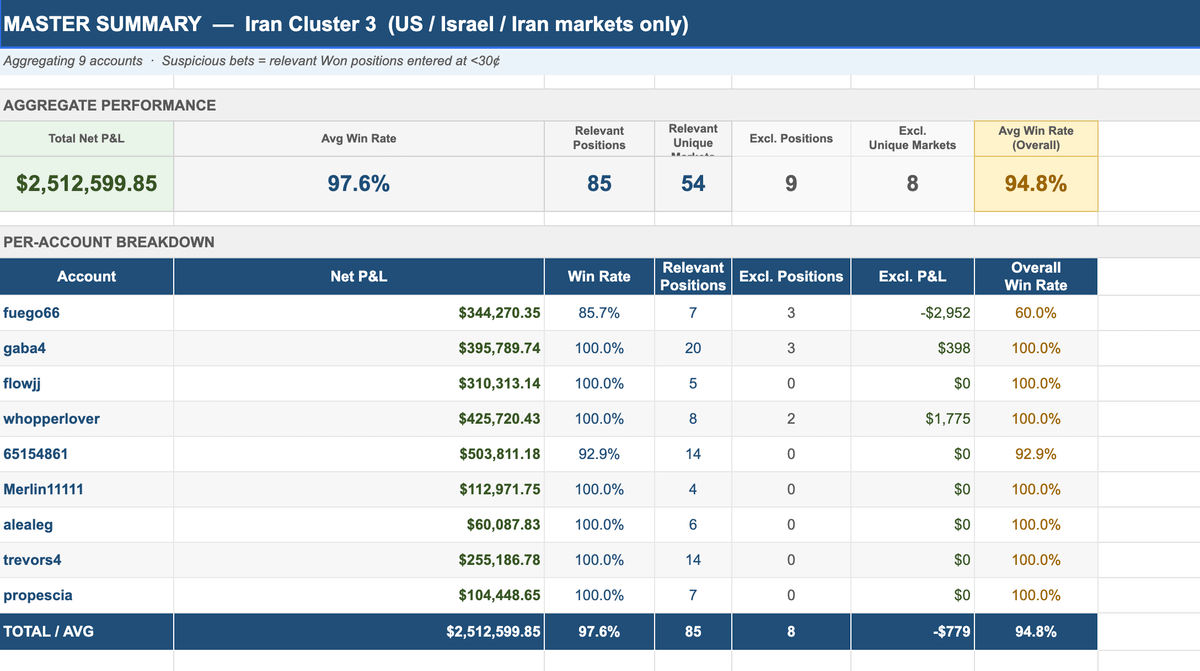

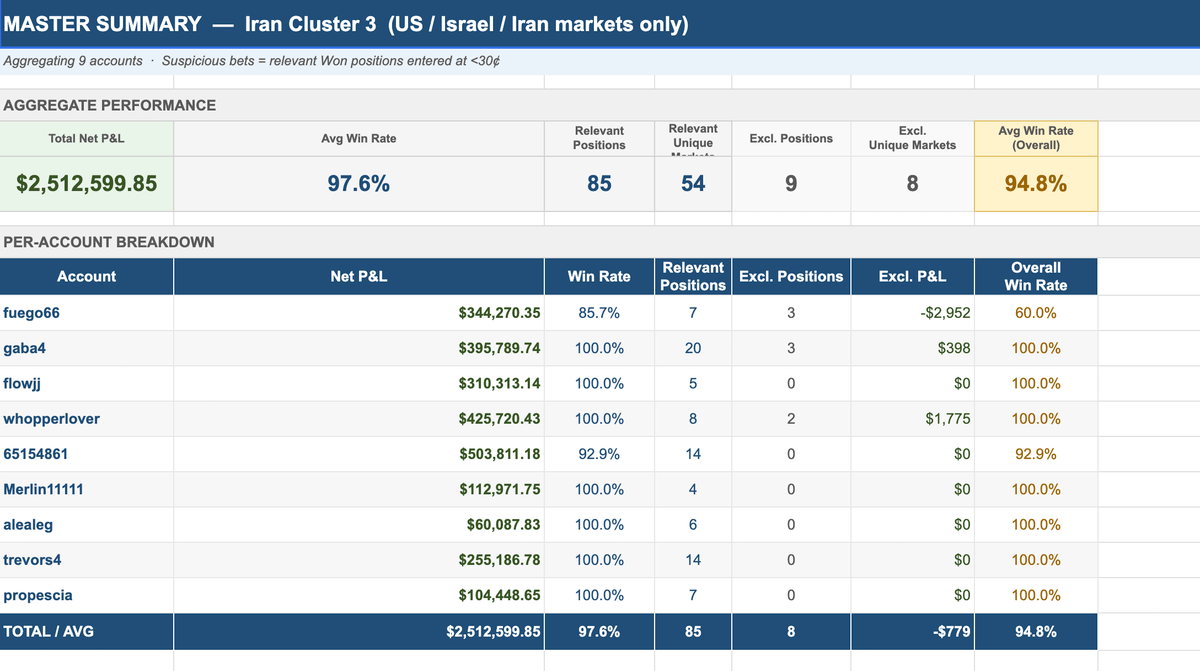

Blockchain data platform Bubblemaps said it identified a cluster of Polymarket wallets that collectively earned $2.4 million with a 98% win rate on contracts tied to US military operations.

Nine wallets placed all their major bets just before major military developments, including the Feb. 28 attack on Iran, the killing of Iranian Supreme Leader Ayatollah Ali Khamenei and the US-Iran ceasefire agreement, Bubblemaps wrote in a Monday X post.

The accounts were all funded through centralized cryptocurrency exchanges in a tight timeframe and made some minor losing bets on Feb. 20, which likely served to “avoid attention,” according to Bubblemaps. Four of them each made around $400,000 in profit on their bets that the US would strike Iran on Feb. 28.

The investigation highlights the growing insider trading concerns tied to decentralized prediction markets such as Polymarket and Kalshi. It aimed at curbing insider trading on prediction markets.

Source: Bubblemaps

While the data platform doesn’t have definitive proof that the accounts belonged to insiders, the onchain trail is “symptomatic of someone with an unfair informational advantage,” Nicolas Vaiman, the CEO of Bubblemaps, told Cointelegraph. He added:

“We cannot say with certainty that this was an attempt to hide, but it is suspicious that funds were routed through CEXs and third-party services before funding new Polymarket accounts, effectively covering their tracks.”

US lawmakers seek stricter regulations on war-related prediction market contracts

US lawmakers have previously proposed new laws to fight the growing insider trading concerns tied to military contracts on prediction markets.

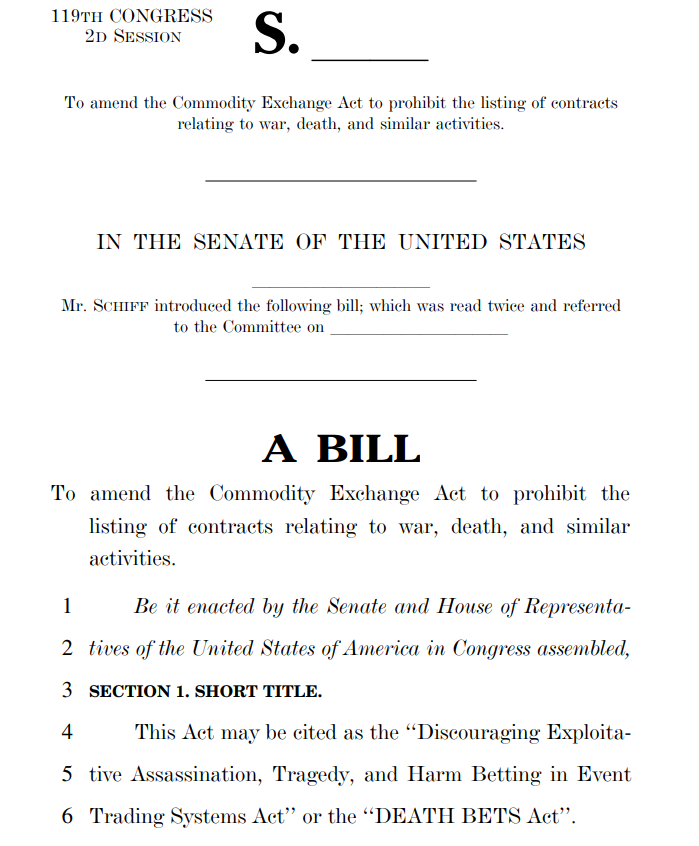

On March 10, US Democratic Party Senator Adam Schiff introduced the DEATH BETS Act, which seeks to ban federally regulated prediction markets from listing contracts tied to war, terrorism, assassination and individual deaths.

DEATH BETS Act. Source: Schiff.senate.gov

The bill came shortly after six Polymarket traders netted $1 million by betting on the US strike against Iran.

Separately, in late March, California Governor Gavin Newsom signed an executive order to curb public servants from insider trading on prediction markets tied to political or economic events they can influence.

Related: CFTC no-action letter eases event contract reporting rules

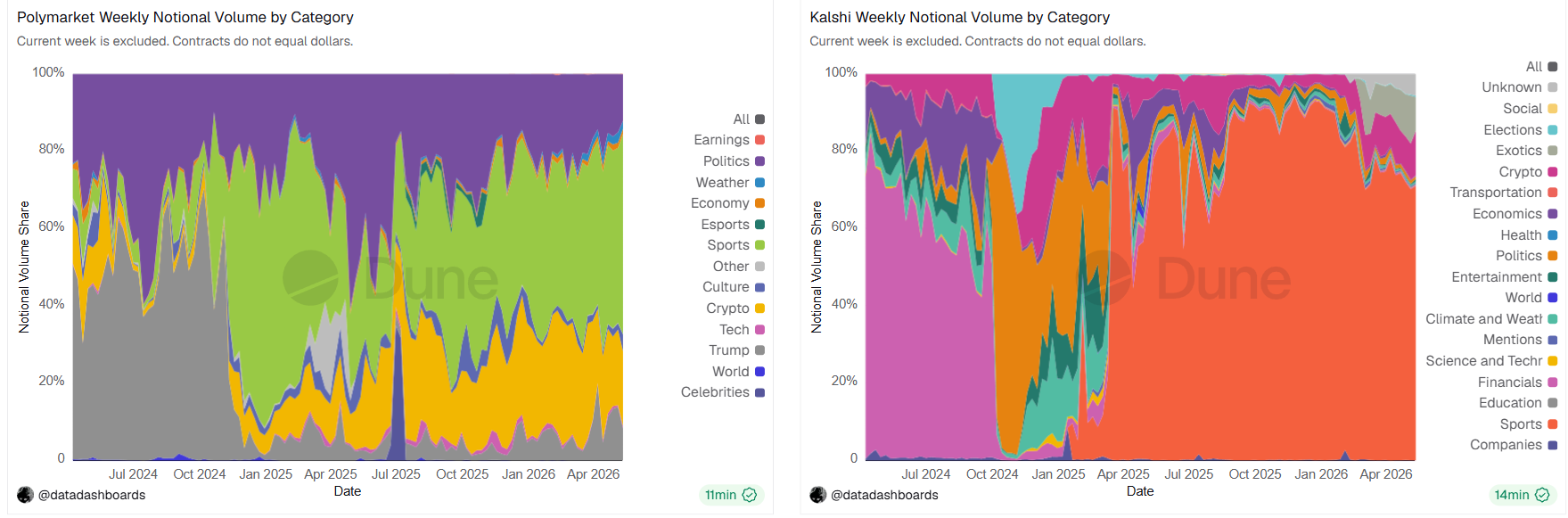

Polymarket, Kalshi, notional volume per category, weekly. Source: Dune

Politics-related contracts are currently the third-largest category on Polymarket, accounting for 12% of notional trading volume, and the fifth-largest on Kalshi, where they account for 0.7% of weekly trading volume, according to Dune data.

Magazine: Inside a 30,000 phone bot farm stealing crypto airdrops from real users

BitGo has appointed Angela Ang as Managing Director of APAC and President of BitGo Singapore.

Summary

- Angela Ang will lead BitGo’s APAC growth after prior roles at MAS and TRM Labs.

- BitGo Singapore remains central to the firm’s regulated digital asset infrastructure push across Asia Pacific.

- The appointment follows BitGo’s dtcpay partnership and wider demand for compliant crypto custody services regionally.

The digital asset infrastructure company said in an announcement that Ang cleared all regulatory and fit-and-proper requirements before taking the role.

Ang will lead business growth, market development and operating infrastructure across Asia-Pacific. Her mandate focuses on expanding institutional access to regulated digital asset services, including custody, wallets, trading, financing, settlement, staking and stablecoin infrastructure.

The hire comes as banks, payment firms and crypto platforms place more weight on regulated service providers. BitGo is presenting the appointment as part of its effort to serve institutions that need secure access to digital assets within clear compliance rules.

Regulatory background shapes appointment

Ang joins BitGo from TRM Labs, where she served as Head of APAC Public Policy and Strategic Partnerships. She was part of the blockchain intelligence firm’s founding APAC team and helped support its regional growth.

Before TRM Labs, Ang spent more than a decade at the Monetary Authority of Singapore. BitGo said she led the team that built and operated Singapore’s payments and crypto licensing framework. That background gives BitGo a leader with direct experience in regulation, policy and institutional market building.

Singapore stays central to BitGo strategy

Singapore will remain the base for BitGo’s APAC strategy. BitGo Singapore is regulated by the Monetary Authority of Singapore as a Major Payment Institution. The company said the appointment reflects its continued investment in Singapore and the wider region.

Jody Mettler, BitGo’s Chief Operating Officer and President of BitGo Bank & Trust, said Ang’s experience covers “regulation, market infrastructure, and commercial growth.” He said those areas are relevant as institutions seek trusted partners that can meet the standards of a regulated financial system.

Angela Ang said BitGo has built its reputation around “security, compliance, resilience, and trust.” She added that Singapore has one of the world’s respected digital asset frameworks and that APAC is entering a new phase of institutional market development.

APAC growth follows recent partnerships

The appointment comes as BitGo pushes deeper into regulated infrastructure across Asia. As crypto.news reported earlier, BitGo Singapore’s dtcpay deal focused on custody, settlement, security and payment network support for digital asset markets.

According to an earlier crypto.news report, BitGo’s Moon partnership added support for Bitcoin-linked prepaid card products across Asia. Moon selected BitGo Singapore as the infrastructure layer for the products, which were set to reach Hong Kong retail stores and online buyers.

BitGo also continues to expand beyond Asia. crypto.news previously reported that BitGo weighed an IPO after assets under custody rose to $100 billion in the first half of 2025. The company later became a public company and now trades under the BTGO ticker.

The new APAC role gives BitGo a senior regional leader as institutions look for compliant crypto services. For Singapore, the appointment also shows how former regulators are moving into digital asset firms as the market shifts toward licensed infrastructure.

The appointment places BitGo’s regional growth under a leader with regulatory and commercial experience. It also shows that BitGo wants APAC expansion to move through licensed services, local expertise and institutional-grade infrastructure.

Crypto World

Eldora Opens On-Chain Access to 280+ Tokenized US Equities for Investors Across 85+ Countries, Launches $20,000 Trading Campaign

The on-chain investment platform lets retail investors in Asia-Pacific buy real, 1:1-backed tokenized US stocks, including SpaceX, Nvidia, Apple, and Tesla — alongside a 5.3% T-Bill yield and institutional DeFi lending — through a single dashboard and a single KYC, with no brokerage account required.

Eldora, an on-chain investment platform, announced the expansion of its tokenized US equity marketplace to 280+ assets and the launch of a $20,000 Trading Campaign, opening in early June 2026 — the platform’s largest community initiative to date.

For most retail investors across Asia-Pacific, owning shares in Nvidia or Apple has never been straightforward. It has meant navigating foreign brokerage registration, funding dollar-denominated accounts, paying high conversion fees, and accepting settlement windows that close on weekends and holidays.

Eldora addresses this with tokenized US equities — blockchain-based representations of real, US-listed securities backed 1:1 by shares held in regulated custody through Dinari, a transfer agent registered with the US Securities and Exchange Commission. The platform now lists 280+ tokenized US stocks and ETFs, including SpaceX ($SPCX), Nvidia ($NVDA), Apple ($AAPL), Tesla ($TSLA), Johnson & Johnson ($JNJ), and the iShares Russell 2000 ETF ($IWM), available 24 hours a day across Ethereum, BNB Chain, Polygon, Arbitrum, and Base.

“Programmable ownership, real-world yield, and decentralized credit markets are converging into a single on-chain financial stack. Eldora is building the access layer for that transition.”

— Theophane Rame, Founder & CEO, Eldora

Tokenized Equities, T-Bill Yield, and DeFi Lending — One Login

According to Dinari’s custody framework, each token on Eldora represents a beneficial interest in the underlying US-listed security — not a derivative, not a synthetic contract. A single KYC verification unlocks all platform products across all five supported blockchains simultaneously: tokenized equities, a T-Bill yield product at 5.3% APY (as of June 2026) on idle stablecoin capital, and institutional DeFi lending aggregated from AAVE (127+ asset reserves), Maple Finance (Syrup USDC at 4.45% APY, $1.4 billion in total assets), and Morpho.

Investors can use tokenized equity positions as collateral within the platform’s DeFi lending stack, enabling yield generation on stock holdings without liquidating positions.

Ghost Portfolio and Observatory: Eliminating the Onboarding Barrier

Ghost Portfolio, launched in June 2026, allows first-time users to build and monitor a complete simulated portfolio — across tokenized stocks, T-Bill yield, and DeFi lending — using real market data, before connecting a wallet or submitting identity documents. Simulated allocations convert directly into live positions upon completion of KYC. Ghost Portfolio lets the platform make the case before asking for a passport.

The Eldora Observatory provides a free, login-optional market intelligence dashboard aggregating live Bloomberg and CNBC feeds, CNN Fear & Greed index data, real-time asset prices across equities, crypto, commodities, and forex, and AI-generated market commentary.

$20,000 Trading Campaign in June 2026

The $20,000 Trading Campaign runs for 12 weeks beginning in early June 2026. Rewards are distributed from the pool based on verified platform activity — trading tokenized equities, deploying capital into yield and DeFi lending strategies, inviting friends via referral, and engaging with Ghost Portfolio or Observatory — with real-time standings published on Eldora’s public Leaderboard. Ghost Portfolio participants may accumulate campaign standing before committing real capital, providing a genuinely low-risk entry point for investors new to on-chain investing.

Access tokenized US stocks, T-Bill yield, and institutional DeFi lending from anywhere in APAC → app.eldora.do

Platform Traction and Market Context

The platform’s early traction reflects the scale of the problem it is targeting. Eldora has surpassed 10,000 active users across 85+ countries, backed by a community of more than 20,000 members across X, Discord, and Telegram. The Discover marketplace lists 280+ tokenized US equities and ETFs — all live and tradable — across 12+ active integrations including Dinari, Maple Finance, AAVE, and Morpho.

The real-world asset tokenization market surpassed $24.9 billion globally in early 2026, up 289% year on year, with tokenized stocks the fastest-growing individual asset category. Institutional participation has accelerated, with J.P. Morgan projecting the tokenized securities market could reach between $4 trillion and $16 trillion by 2030.

About Eldora

Eldora is an on-chain investment platform that provides access to tokenized US equities, Treasury bill yield products, and decentralized lending markets through a unified dashboard and a single KYC framework. The platform aggregates infrastructure from Dinari (SEC-registered transfer agent), Maple Finance, AAVE, and Morpho, and is available across Ethereum, Base, Polygon, Arbitrum, and BNB Chain. Eldora is incorporated in Zurich, Switzerland and serves a global user base across 85+ countries.

Website: Web: eldora.network & App: app.eldora.do

The post Eldora Opens On-Chain Access to 280+ Tokenized US Equities for Investors Across 85+ Countries, Launches $20,000 Trading Campaign appeared first on BeInCrypto.

Block, the financial services company led by Jack Dorsey, says it has launched “Builderbot,” an AI-native set of engineering tools designed to handle a meaningful portion of production software changes. The company claims the system can carry out roughly 15% of all production code changes at Block, positioning the rollout as a step beyond traditional AI coding assistants.

In describing Builderbot, Block frames the development as a practical shift: AI systems are moving from suggesting code to coordinating work that can be merged and shipped, while engineers retain responsibility for higher-level judgment and product decisions. Block also linked the announcement to its broader AI push that coincided with a major workforce reduction earlier this year.

Key takeaways

- Block says Builderbot can execute around 15% of its production code changes, turning AI from “assistive” into “operational” in day-to-day engineering.

- The company estimates Builderbot performs over 200,000 operations per day and merges about 1,500 pull requests per week.

- Builderbot is presented as an orchestration layer that coordinates multiple AI agents across Block’s full codebase rather than a single repository.

- Block attributes faster delivery—moving items from backlog to live—on the order of days rather than months, with humans still focused on key decisions.

- The rollout adds new context to Block’s February decision to cut about 40% of staff, which Dorsey said was driven by accelerating AI adoption.

Builderbot aims to bridge AI coding and real engineering

Block introduced Builderbot as a “missing layer” between AI coding tools and how software teams actually operate at scale, according to Brad Axen, head of AI capabilities at the company. Block’s internal metrics, as presented in its announcement, suggest the system is not limited to drafting snippets or generating isolated changes.

Axen said that tasks that previously took months could be completed in days with Builderbot, reflecting an emphasis on throughput and execution speed rather than experimentation alone. The company also claims Builderbot can perform more than 200,000 operations per day and merges approximately 1,500 pull requests per week, figures intended to show tangible productivity impact.

For investors and builders watching AI deployment, the key question is whether these systems can reliably translate intent into production-ready code—without overwhelming reviewers or compromising quality. Block’s decision to describe measurable operational metrics suggests it is aiming to make the case that AI-generated work can fit existing engineering workflows, including review and merging processes.

An orchestration approach across Block’s entire codebase

A central feature of the system, Block says, is that Builderbot understands the broader environment in which software runs. The company describes Builderbot as an orchestration layer that coordinates multiple AI agents across its full codebase—covering services, APIs, and internal conventions—rather than restricting agents to a single repository.

Block contrasts this with the typical approach of coding assistants that operate within one codebase boundary. In its example, an engineer working on Cash App could use Builderbot to make changes in a Square service they have never worked on, because the system allegedly already knows how that service is built and how it fits into Block’s overall architecture.

This matters because production scaling isn’t only about generating more code; it is about making changes that are consistent with system rules, dependencies, and deployment practices. If Builderbot genuinely has awareness of cross-service relationships, it could reduce the “handoff friction” that often slows teams down when changes span multiple systems.

Block adds that the practical outcome is faster iteration: an idea can move from backlog to being available to “millions of customers” in days instead of months, while engineers focus on judgment and product taste rather than repetitive scaffolding.

AI acceleration and workforce restructuring context

Block’s announcement does not arrive in isolation. The company also connected Builderbot to its earlier restructuring, noting that its February layoffs—40% of staff—were attributed by Jack Dorsey to the rapid acceleration of AI at Block.

That linkage highlights a tension that many companies in this space are grappling with: faster engineering cycles can reduce certain forms of manual work, even as firms argue that human roles shift toward oversight, product direction, and quality decisions. Block’s description of engineers remaining responsible for judgment and taste suggests it is positioning Builderbot as augmentation rather than a complete replacement.

Still, the practical question for employees and outside observers remains how responsibilities are redistributed. Metrics like merged pull requests and daily operations can indicate scale, but they don’t alone reveal how the human workload changes—whether review becomes faster, whether engineers spend more time on higher-level design, or whether roles are reduced in practice.

The broader shift toward AI-written code at major tech firms

Block is not the only company exploring AI agents for software development. Other large organizations have publicly discussed how automation is affecting coding and engineering output.

Earlier reporting highlighted that Spotify engineers have used a background coding agent called Honk, which runs a version of a Claude model through Anthropic’s Agent SDK. Separately, Spotify Co-CEO Gustav Söderström said on a February earnings call that the best developers “have not written a single line of code since December,” underscoring how far the conversation has shifted from assistance to execution.

At Google, CEO Sundar Pichai said in April that three-quarters of new code is AI-generated, pointing to a scale where AI output is shaping day-to-day development. Microsoft’s Satya Nadella also described, in 2025, that the company uses AI to write between 20% and 30% of code powering its software, again positioning AI as a meaningful part of the production process rather than a side tool.

Taken together, these examples place Block’s Builderbot announcement in a larger trend: CEOs and engineering leaders are increasingly measuring AI productivity in terms of code volume and delivery timelines. For the crypto industry, this matters indirectly—many crypto projects rely on fast-moving engineering teams, and the same automation patterns could influence how quickly core infrastructure is iterated, audited, and updated.

For readers tracking this space, the next signals to watch are whether systems like Builderbot can maintain reliability as they scale, how quality controls evolve with higher AI throughput, and whether other companies follow Block’s lead in publishing comparable operational metrics rather than only high-level claims.

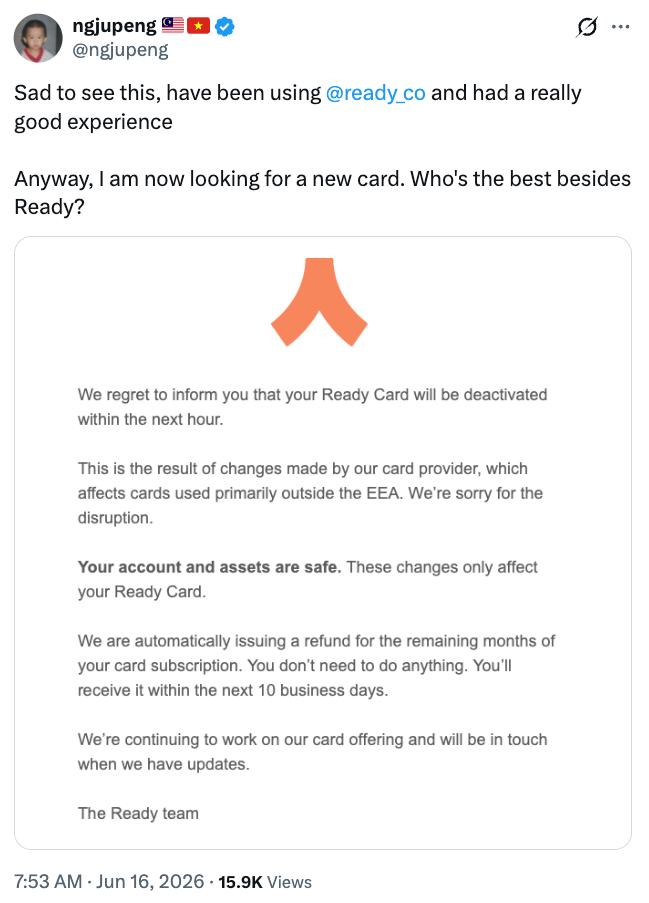

Ready, a self-custodial crypto wallet and payments company, has reportedly restricted card access for users outside the European Economic Area, according to multiple user reports.

Ready has restricted USDC card functionality for users outside the European Economic Area following a change in its card provider, according to notices shared by users on social media.

Several users shared screenshots of an in-app notice from Ready stating: “Your Ready Card will be deactivated within the next hour,” citing changes affecting users “primarily outside the EEA.”

The reported changes left some users questioning how quickly access to crypto-linked payment cards can be restricted when providers change.

Users question speed of restriction and communication

Several users criticized the short notice period before the changes took effect, saying they lost access to the card within hours.

One user, who uses the X handle TapSatoshi, said in a post that they were frustrated with the company’s product roadmap, citing delayed features such as Apple Pay support and prioritizing the addition of a “Rewards” section.

Source: ngjupeng

Screenshots of Ready’s message also stated that users would receive automatic refunds for any remaining subscription period within 10 business days.

It remains unclear which company will serve as the new card provider for the Ready Card or what prompted the change. The previous issuer-side partner linked to the program was Kulipa, according to publicly available documentation.

Related: BitGo courts crypto firms awaiting MiCA approval amid Binance licensing concerns

Cointelegraph contacted Ready for comment regarding the issue but did not receive a response by publication time.

USDC at the center of the Ready Card

Formerly known as Argent, Ready is a wallet built for the Starknet ecosystem, an Ethereum layer-2 scaling network using zero-knowledge rollups.

While Ready’s wallet supports multiple crypto assets, including Bitcoin (BTC) and Ether (ETH), the Ready Card is primarily built around USDC, which users spend directly from their wallet balance at checkout.

Source: Ready

According to Ready documentation, the system checks a user’s USDC balance in real time when a purchase is made and processes the transaction through Mastercard’s payment network, converting crypto into fiat at the point of sale. The card issuer acts as the bridge between the self-custodial wallet and traditional payment rails.

This structure allows users to retain full control of their assets in the wallet, while the card only provides a spending layer on top of those funds. If card access is restricted, users can still hold and transfer USDC onchain without interruption.

Magazine: The end of anon? AI could unmask crypto’s hidden identities

CME Group CEO Terrence Duffy announced Wednesday that the exchange operator will file a federal lawsuit against the CFTC, targeting the regulator’s late-May approval of bitcoin perps for prediction-market platform Kalshi, the first regulated U.S. listing of perpetual futures.

Duffy’s central argument, made on CNBC’s Fast Money, is that the products the CFTC approved as futures are legally swaps under the Dodd-Frank Act, and that the agency overstepped its authority in fast-tracking them without adequate review.

The stakes extend well beyond Kalshi. Duffy stated on air that CME holds exclusive licensing agreements with every major benchmark provider whose indexes underpin crypto derivatives pricing.

If perpetual futures are reclassified as swaps in court, any platform offering them would need to route through CME’s licensing framework regardless of how their products are labeled, a structural outcome that would effectively block Kalshi, Coinbase, and Kraken from operating U.S. perp markets outside CME’s terms.

CFTC Chair Michael Selig defended the approval earlier the same week, telling CNBC it was “time to approve regulated futures contracts that have no expiration date,” while a CFTC spokesperson dismissed the threatened lawsuit as frivolous.

The broader regulatory context matters here. Legislators are simultaneously debating the scope of CFTC jurisdiction over crypto through vehicles like the CLARITY Act currently moving through the Senate, which would formalize CFTC authority over digital commodity derivatives – making the outcome of CME’s lawsuit directly relevant to how that legislative framework gets applied in practice.

Discover: The Best Token Presales

CME Duffy Core Argument: Why Perpetual Futures Are Swaps Under Dodd-Frank

The legal framing is specific and worth unpacking. The Dodd-Frank Act draws a hard line between futures and swaps in the Commodity Exchange Act: a futures contract involves delivery or cash settlement at a defined expiration date, while a swap involves two parties continuously exchanging payments based on an underlying reference rate.

Perpetual futures have no expiration date. Instead, they use a funding-rate mechanism, periodic payments between long and short holders, to keep the contract price anchored to spot. That mechanism, Duffy argues, is structurally identical to a swap under the statute.

Duffy stated the case plainly in his CNBC appearance: “Under the Dodd-Frank Act, it clearly defines what a swap is and what a future is, and when there’s two parties exchanging payments to each other, that’s deemed a swap.

So, if anything, these products that he supposedly approved as futures are not futures, they would be swaps, and if they’re swaps, and let’s say, as you know, there are different requirements in order to participate in the swap market.”

The classification carries real consequences: swaps participants face stricter eligibility requirements, higher capital thresholds, and different reporting obligations than futures market participants.

CME’s second front is procedural. Market lawyers quoted in early coverage expect the lawsuit to include an Administrative Procedure Act challenge, arguing the CFTC relied on expedited self-certification and abbreviated review for what the agency itself has described as a novel and complex product class,without the full notice-and-comment rulemaking that complexity typically demands.

Duffy reinforced the procedural critique directly, accusing the CFTC of describing a 24/7 trading release as a formal rule when it was not, saying he believed “to an extent” the agency was misrepresenting facts.

Discover: The Best Crypto to Diversify Your Portfolio

CFTC Chair Selig Calls the Lawsuit Frivolous: Here’s the Regulator’s Case

Selig’s position is that the CFTC has clear statutory authority to approve futures contracts on commodity indexes, and that a well-structured perpetual futures contract, with a defined reference rate, margining requirements, and daily settlement, qualifies as exactly that.

The agency’s framing sidesteps the no-expiry objection by pointing to the daily settlement mechanic as functionally equivalent to the roll that occurs in dated futures, satisfying the Commodity Exchange Act’s “future delivery” requirement at least in economic terms.

Whether that construction holds up to the Dodd-Frank swap definition in federal court is the central legal question the case will force into the open.

The CFTC also has a political tailwind: the current regulatory posture across Washington has been broadly pro-crypto-access, and fast-tracking onshore perp listings aligns with the administration’s stated goal of pulling derivatives volume back from offshore, unregulated venues.

Derivatives lawyers quoted across coverage have noted that the case could function as a test of the entire CFTC product-approval framework for crypto, putting the futures-swap boundary under the kind of federal-court scrutiny it has never faced in the context of crypto derivatives specifically.

Commentators in the ongoing regulatory classification disputes around the Clarity Act have drawn direct parallels to this case, noting that definitional line-drawing by agencies has repeatedly ended up in litigation.

The post CME Move To Sue CFTC Over Crypto Perpetual Futures: Here’s Why appeared first on Cryptonews.

The British pound remains under pressure following weaker-than-expected inflation data, which has reinforced expectations of further monetary easing by the Bank of England. Investors are staying cautious ahead of today’s policy meetings of both the UK central bank and the Swiss National Bank, which is affecting both GBP/USD and GBP/CHF.

The latest data published yesterday showed a slowdown in inflationary pressures in the UK. The annual consumer price index remained at 2.8%, while monthly price growth came in at just 0.2% compared with expectations of 0.4%. Core inflation also came in below forecasts, easing to 2.6% versus expectations of 2.7%. Additional signs of cooling price pressures came from a slowdown in the retail price index and weaker dynamics across several producer price indicators.

The easing of inflation pressures has increased expectations that the Bank of England could continue its gradual policy easing in the coming months. Although no change in interest rates is widely expected today, markets will focus on the accompanying statement, the voting split within the Monetary Policy Committee, and guidance on future policy steps.

GBP/USD

Yesterday, following Jerome Powell’s press conference, the pair fell sharply, renewing its recent low at 1.3300. If the 1.3300–1.3330 range, which has contained the pair’s decline for more than a month, turns into resistance, further downside towards 1.3180–1.3200 may follow. A break of the bearish scenario would require a sustained move above 1.3330.

Key events for GBP/USD:

- today at 09:00 (GMT+3): UK unemployment rate;

- today at 09:00 (GMT+3): UK average earnings (including bonuses);

- today at 15:30 (GMT+3): US Philadelphia Fed manufacturing index.

GBP/CHF

The GBP/CHF pair is showing a relatively modest decline. Price has found support at 1.0600 and is consolidating within the 1.0600–1.0650 range. A breakout from this range would provide clearer direction for the next move. A sustained move above 1.0650 could trigger a retest of the recent high at 1.0700, while a break below the lower boundary could lead to a deeper corrective decline.

Key events for GBP/CHF:

- today at 10:30 (GMT+3): Swiss National Bank interest rate decision;

- today at 11:30 (GMT+3): Swiss National Bank press conference;

- today at 14:00 (GMT+3): Bank of England interest rate decision.

Thus, the key drivers for GBP/USD and GBP/CHF today will be the Bank of England and Swiss National Bank decisions. Following weaker-than-expected inflation data, the market will be looking for confirmation of the UK central bank’s policy stance, while any shifts in expectations for future monetary policy could significantly influence GBP price action in the coming days.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Key Highlights

- Starting June 17, Aster will allocate 99% of all platform fees toward purchasing ASTER tokens from the open market.

- Every token buyback triggers an equivalent burn from reserve supplies, generating a dual 198% deflationary mechanism.

- The initiative aims to reduce ASTER’s total supply from 8 billion down to 3 billion tokens through systematic burns.

- Tokens acquired through buybacks flow directly to veASTER stakers through the platform’s Loyalty Rewards system.

- ASTER pierced the $0.65 resistance barrier and is now testing the $0.81 threshold.

On June 17, 2026, Aster unveiled a transformative tokenomics restructuring that propelled its native ASTER token upward by more than 20% within 24 hours.

The mechanism behind this surge is clear-cut: virtually all daily platform revenue—99% to be exact—will now fuel direct ASTER token purchases from secondary markets.

These buyback operations run automatically through a time-weighted average pricing mechanism, with all transactions recorded on-chain for full transparency. The protocol has made public the dedicated wallet address (0xa0edBaBcb48034e368de286b49F9603C7AfA1b60) to enable community verification of all purchases.

In a unique twist, each ASTER token repurchased from the market triggers the permanent destruction of an equivalent token amount from the project’s reserve wallet, beginning with team-allocated holdings.

This dual-action approach creates what the protocol terms a “198% combined deflationary pressure,” simultaneously reducing circulating supply through market removal and total supply through permanent burns.

Aggressive Supply Contraction Plan

Token burns occur every two weeks and will persist until the maximum supply contracts from its current 8 billion to a final target of 3 billion ASTER.

As of the June 17 implementation date, the total supply registered at roughly 7.82 billion tokens, while circulating supply hovered between 2.68 and 2.70 billion.

Every ASTER token acquired via buybacks enters the Loyalty Rewards distribution pool. Each reward cycle features a baseline allocation of 300,000 ASTER tokens, supplemented by all tokens purchased during that period’s buyback operations, then distributed proportionally to veASTER holders according to their lock-up weights.

Additional buying pressure stems from Aster Spot’s listing mechanism. Each permissionless token listing carries a 50,000 USDT listing fee, with 100% of these proceeds channeled into the same buyback infrastructure.

Market Reaction and Technical Analysis

ASTER peaked near $0.80 immediately following the announcement before encountering profit-taking activity. At last check, the token traded around $0.74, representing a roughly 13% daily gain.

Examining the daily timeframe, ASTER successfully breached the $0.65 price level that had served as a ceiling since April.

The Relative Strength Index climbed beyond 65, while the MACD indicator generated a bullish signal with expanding green histogram bars.

The critical resistance zone now lies at $0.81, a level that has previously rejected multiple advance attempts. A decisive break above this barrier would push ASTER into price ranges unseen since the final months of 2025.

Should the price retrace, the former resistance at $0.65 is expected to provide support.

This enhanced program represents a significant evolution from earlier iterations that directed between 70–80% of platform fees toward buybacks, now capturing nearly total revenue for token economics optimization.

Fidelity Investments has launched a money market fund aimed at stablecoin issuers and institutional investors seeking to meet reserve requirements under the GENIUS Act.

Summary

- Fidelity has launched a money market fund designed to help stablecoin issuers meet reserve requirements under the GENIUS Act.

- The new Fidelity Reserves Digital Fund will invest in cash, short term U.S. Treasuries, and other eligible assets permitted under federal stablecoin rules.

- Fidelity joins State Street in targeting the stablecoin reserve management market as institutions prepare for expected growth in digital dollar issuance.

Fidelity said on Thursday that the new Fidelity Reserves Digital Fund will invest in cash, short-term U.S. Treasury securities, overnight repurchase agreements backed by Treasuries, and government money market funds that qualify under the federal stablecoin framework.

The launch places Fidelity among a growing group of traditional financial firms offering products tailored to stablecoin reserve management. State Street introduced a similar product this week through its State Street Stablecoin Reserves Money Market Fund, which was also designed for issuers operating under the GENIUS Act.

Robin Foley, Fidelity’s head of fixed income, said the firm’s experience in fixed income and money markets positions it to provide a compliant reserve management solution for stablecoin issuers under the new legislation.

Fidelity expands stablecoin strategy

The new fund adds to Fidelity’s stablecoin business, which expanded earlier this year with the introduction of the Fidelity Digital Dollar, or FIDD.

At the time, Fidelity Digital Assets said the U.S. dollar-backed stablecoin would serve both retail and institutional investors and would be supported by Fidelity’s reserve management infrastructure. Mike O’Reilly, president of Fidelity Digital Assets, said the company had spent years researching stablecoins and viewed regulatory clarity as an important step for adoption.

The GENIUS Act established the first federal framework for payment stablecoins in the United States. Among its requirements, issuers must maintain reserves in cash, short-dated Treasury securities, and certain government money market funds.

Fidelity said the Fidelity Reserves Digital Fund will hold Treasury bills, notes, and bonds with maturities of 93 days or less. The portfolio will also include cash balances and overnight repurchase agreements secured by Treasury securities.

Asset managers target stablecoin reserves market

Asset managers have begun introducing products that align with the reserve standards established under the new law.

State Street said this week that its reserve fund was created to help issuers satisfy GENIUS Act requirements. State Street Bank and Trust Company and Anchorage Digital joined the launch as initial backers.

State Street Chief Executive Officer Yie-Hsin Hung said the legislation established a framework for how stablecoin reserves can be invested. Anchorage Digital Chief Executive Officer Nathan McCauley said reserve management would become increasingly important as stablecoin usage expands.

Industry projections cited by State Street estimate that global stablecoin issuance could reach between $1.9 trillion and $4 trillion by 2030. If those forecasts materialize, issuers would need to place a substantially larger volume of reserve assets into highly liquid investments permitted under the law.

Stablecoins, which are typically pegged to the U.S. dollar, currently account for roughly $320 billion in market value and are widely used for trading, payments, and cross-border transfers.

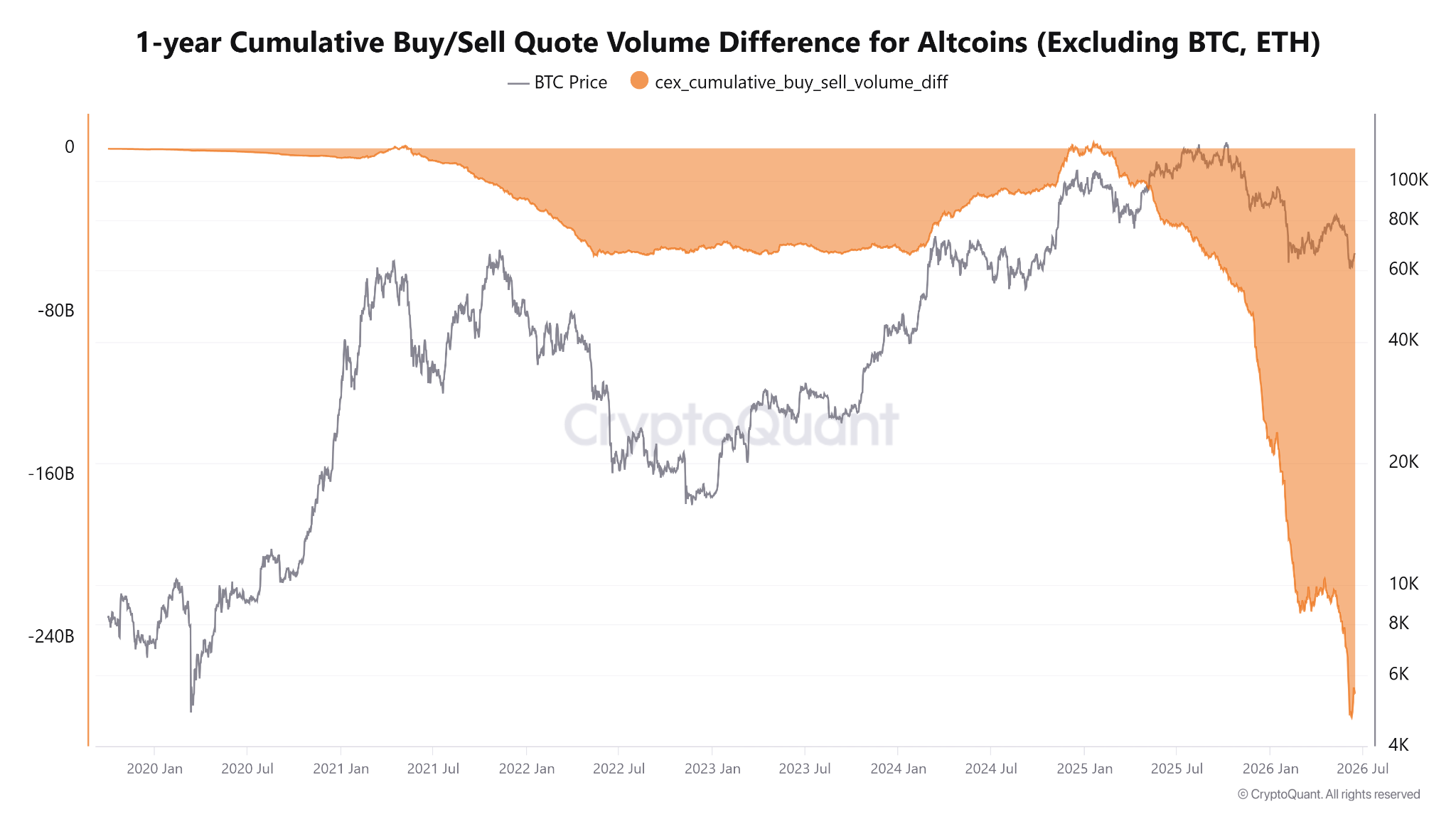

Altcoin markets (excluding Ether (ETH)) recently saw $266 billion in net selling volume on centralized exchanges, the deepest reading since the metric began tracking spot demand in 2020.

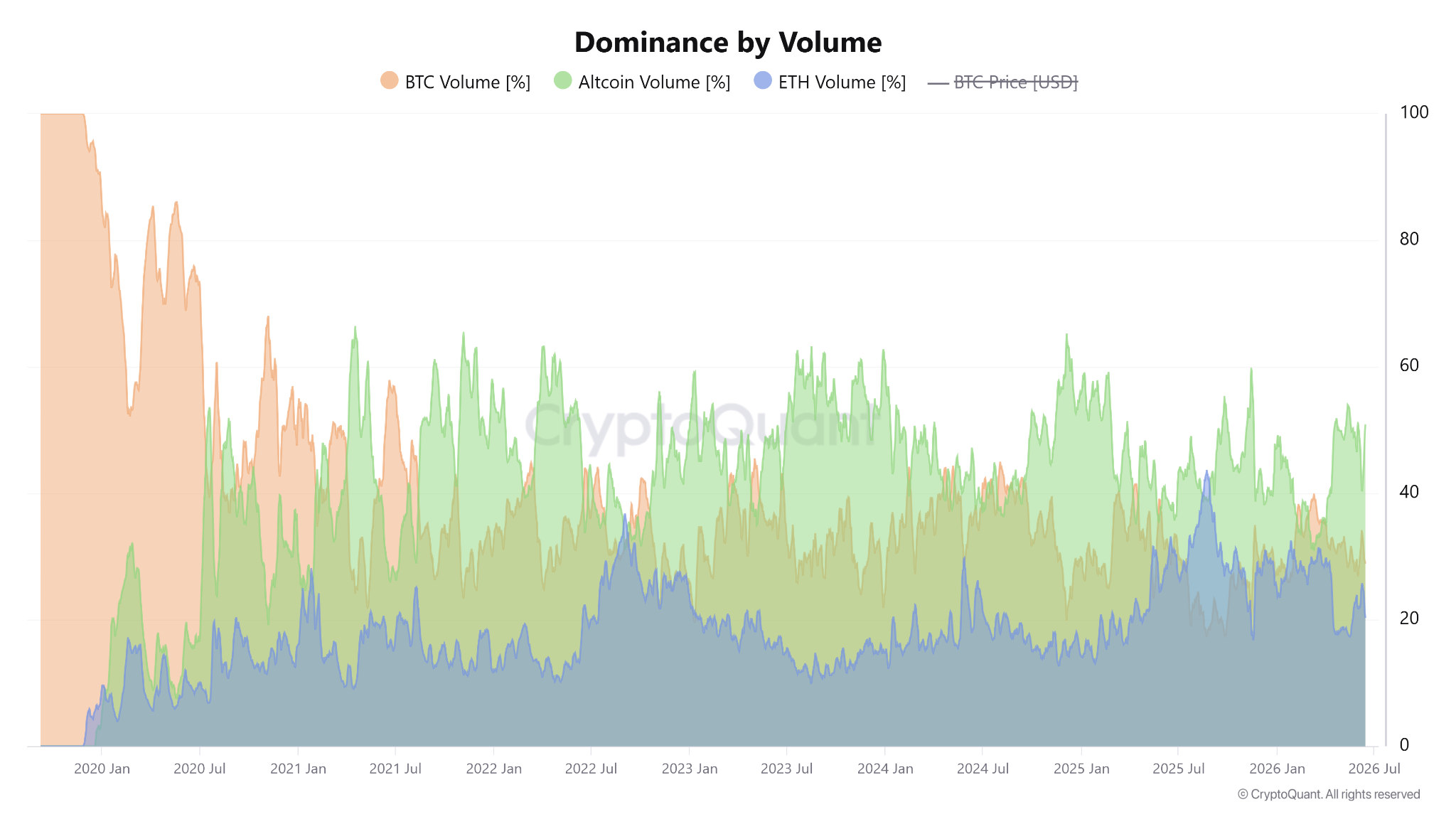

Altcoins accounted for 51% of Binance futures trading volume on June 16, compared with 28.85% for Bitcoin and 20.20% for Ether, positioning the exchange as a leader in derivatives activity in 2026.

The divergence between record selling and dominant trading activity points to capital rotating within crypto and also into alternative exchange products.

Altcoin trading stays active despite outflows

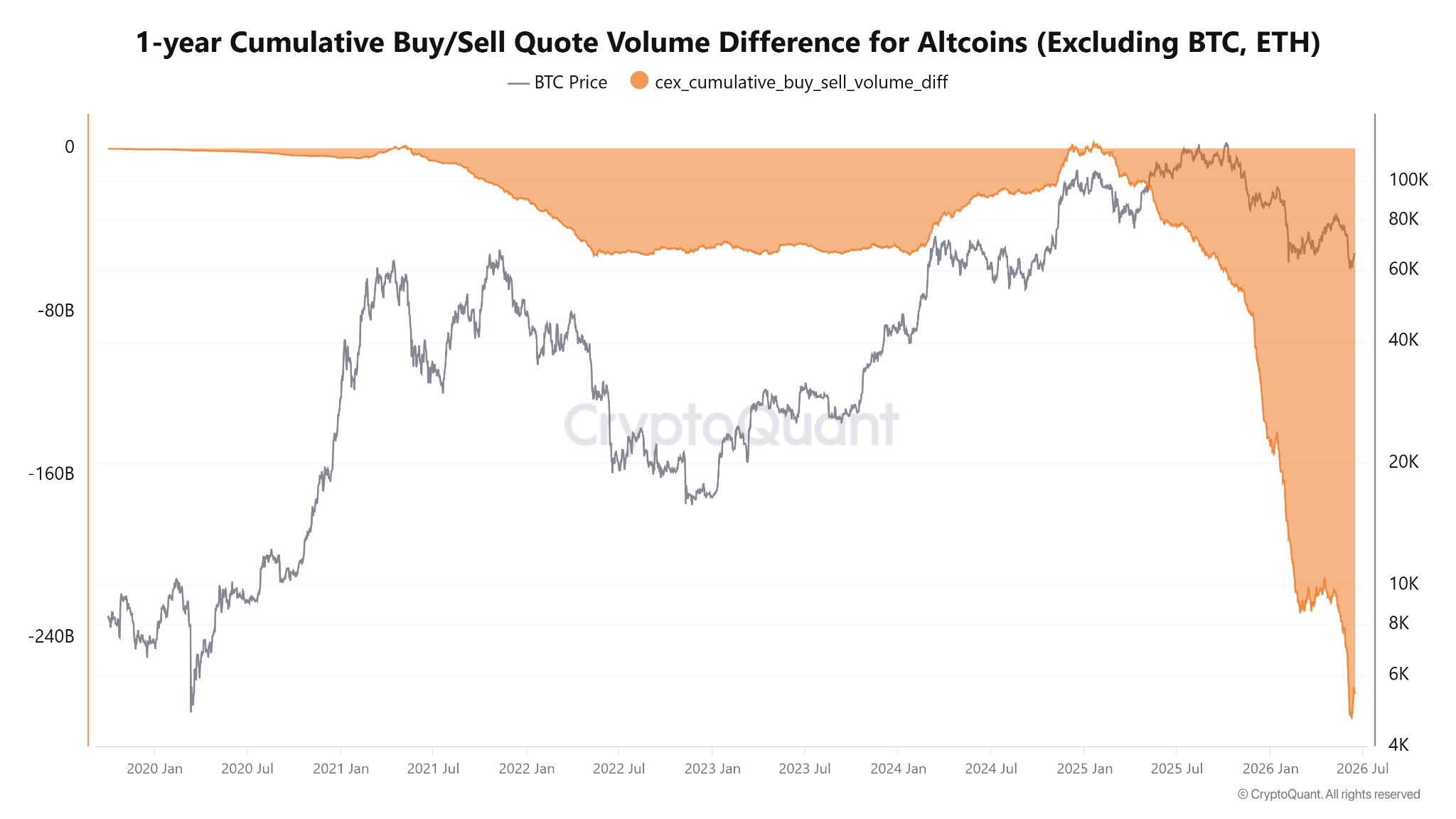

Crypto analyst IT Tech noted that the one-year cumulative buy-sell difference for altcoins, excluding Bitcoin (BTC) and Ether (ETH), dropped to -$266 billion on June 16.

One-year cumulative buy-sell volume for altcoins. Source: CryptoQuant

The current readings show that selling pressure has outweighed buying demand for an extended period, pushing the cumulative balance to a new low.

However, altcoin trading activity tells a different story. Data shows altcoins accounted for 51% of daily futures trading volume on June 16, compared with 28.85% for Bitcoin and 20.20% for Ether. Altcoins have led exchange trading volumes for most of 2025, aside from a brief period in February when Bitcoin overtook the sector.

Volume dominance between BTC, ETH, and altcoins. Source: CryptoQuant

The combination of elevated futures trading activity and deeply negative spot demand points to capital recycling within the altcoin market rather than fresh spot inflows. This shows investors continuing to trade altcoins, although aggregate spot purchases have not kept pace with the selling volume.

Related: BitGo courts crypto firms awaiting MiCA approval amid Binance licensing concerns

Crypto liquidity shifts beyond altcoins

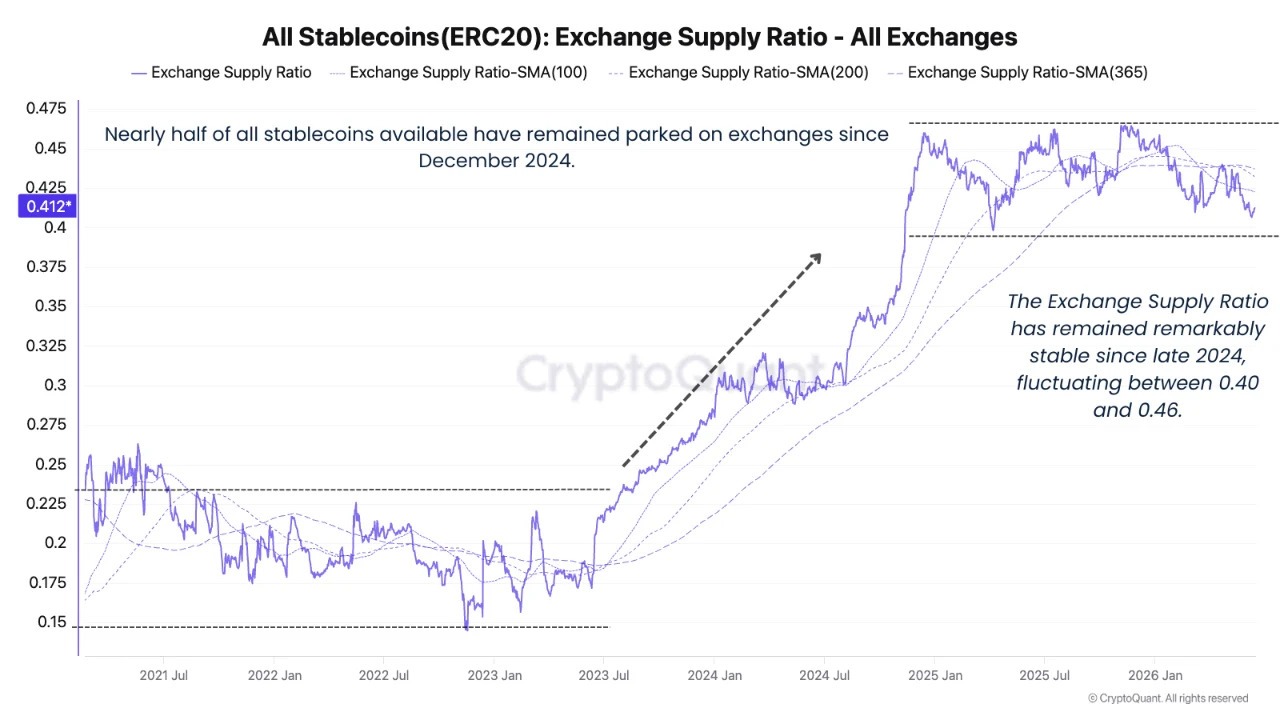

Market analyst MorenoDV indicated that exchange stablecoin balances have changed little since December 2024. The exchange supply ratio for ERC-20 stablecoins has fluctuated between 0.40 and 0.46, meaning roughly 40% to 46% of circulating stablecoins have stayed on exchanges for more than a year.

Stablecoins (ERC20) exchange supply ratios. Source: CryptoQuant

During the same period, Bitcoin experienced price swings exceeding 50%, trading between $60,000 and $120,000. Binance held between 25% and 30% of the total stablecoin supply, accounting for more than half of exchange-held reserves. This indicates liquidity has stayed available, but capital deployment has become increasingly selective.

Part of the capital appears to be targeting traditional asset products offered by crypto exchanges. According to CryptoQuant, metals futures volume peaked at nearly $500 billion in March 2026, as gold and silver prices reached record highs. The trading activity in pre-IPO perpetual products expanded to $715 million in May and $2 billion in June, up from just $2 million in March.

Binance processed $10.3 billion in pre-IPO perpetual volume in June, roughly 20 times higher than the entire month of May, while controlling about 83% of the segment. Growth in metals, oil, equities, and pre-IPO contracts highlights how exchange users are increasingly allocating liquidity across a wider range of assets, with Binance continuing to hold the largest concentration of deployable stablecoin capital.

Related: Hyperliquid open interest surges 32% in week: Is $80 HYPE next?

Michelle Bond, the wife of former FTX executive Ryan Salame, will move forward to trial on illicit campaign finance-related charges after a Manhattan federal judge rejected an attempt to throw out the indictment. The decision, issued by U.S. District Judge George Daniels on Wednesday, hinged on whether prosecutors promised Bond immunity in exchange for Salame’s guilty plea.

Daniels denied Bond’s motion to dismiss, concluding there was “no ambiguity” in the written plea agreement and that prosecutors never promised Bond would be cleared. The ruling is expected to be among the final steps in the cluster of criminal cases stemming from FTX’s collapse in 2022, one of the most consequential events in the history of the crypto industry.

Key takeaways

- Judge George Daniels ruled that the plea agreement did not grant Michelle Bond immunity and that prosecutors made no binding promise to avoid her prosecution.

- The court found the government’s position was “undisput[ably]” supported by evidence that immunity was not offered when Ryan Salame pleaded guilty.

- Bond’s indictment centers on allegations that she used FTX-linked funds to bankroll her 2022 congressional campaign.

- Bond faces four separate campaign-finance counts, each carrying up to five years in prison.

No immunity in the plea paperwork

Bond asked the court to dismiss the indictment by arguing that prosecutors made assurances during a 2023 meeting. According to Bond, then–Manhattan U.S. Attorney Danielle Sassoon told her and Salame’s attorney that if Salame pleaded guilty, prosecutors would “conclude” investigative matters related to Ryan Salame but not those related to Bond.

In his decision, Daniels rejected that argument by emphasizing the “four corners” of the plea agreement—meaning the terms that were actually set in writing. The judge wrote that there was “no ambiguity” in the agreement and found that “all parties, including the defendants and their counsel” understood that the government had not promised Bond immunity when Salame entered his guilty plea.

Daniels also pointed to testimony from Bond’s former lawyer, Gina Parlovecchio, indicating that she did not view Sassoon’s statement as a promise at the time it was made. The judge concluded the evidence showed the government did not bargain for Bond’s non-prosecution in return for Salame’s plea.

How FTX money allegedly flowed into a 2022 campaign

Prosecutors’ allegations trace the case to Bond’s failed attempt to win a House seat in 2022. In an earlier filing made by the government and reported in August 2024, prosecutors said that after Bond launched her congressional run, Salame arranged a consulting arrangement between Bond and FTX, under which Bond was paid $400,000.

According to the government, Bond then used those funds to illegally support her campaign, along with additional money—prosecutors allege Salame wired her hundreds of thousands of dollars between June and August 2022. Prosecutors further claimed Bond tried to obscure the source of payments and made false statements to both a congressional committee and the Federal Election Commission.

Bond’s defense has argued that the government’s earlier assurances about the scope of prosecution should matter. But Daniels’ ruling makes clear that, at least under current findings, the court does not accept that any side discussions overrode the written plea terms.

Where the case fits in the broader FTX fallout

FTX’s collapse in 2022 sent shockwaves through crypto markets and triggered a long-running set of criminal investigations and prosecutions. The Salame-related matter has already reached a sentencing milestone: Salame, who served as co-CEO of FTX’s Bahamian subsidiary, FTX Digital Markets, was sentenced to seven and a half years in prison in May 2024.

That sentence followed a guilty plea by Salame to conspiring to make illegal political contributions and to operating an illegal money transmitter. Bond’s case is closely connected to those same allegations, but it targets her alleged role in financing and concealing campaign support tied to FTX.

The judge’s ruling is therefore significant not just for Bond, but for the pace of closing out FTX-linked prosecutions. If upheld through further proceedings, it would keep the focus on Bond’s indictment and move the case closer to trial.

Charges and potential exposure

Bond is facing four criminal counts connected to campaign finance and donation-related conduct. The charges listed in the indictment include conspiracy to cause unlawful political contributions; causing and receiving a straw donor contribution; causing and accepting excessive campaign contributions; and an unlawful corporate contribution.

Each of the four counts carries a statutory maximum sentence of up to five years in prison. The case turns largely on whether the alleged payments and related campaign activity violated U.S. campaign finance laws, and whether Bond’s attempts to conceal the funding sources or make related statements crossed criminal lines.

With Judge Daniels denying the motion to dismiss, Bond will now have to litigate the merits of the government’s allegations rather than seeking relief based on alleged immunity promises tied to Salame’s plea.

For observers watching the final chapters of the FTX criminal saga, the key next development is how Bond responds at trial or in any subsequent motion practice—particularly given the judge’s emphasis on the written plea agreement and what communications were or were not treated as binding promises.

Diodes Incorporated: My Best Pick For The Semis Rally

BitGo hires ex-MAS regulator to power APAC crypto push

Craig Melvin stuns Bowen Yang and Matt Rogers with hatred of peanut butter: 'They perverted the peanut!'

Blockchain.com files with SEC for U.S. IPO

Israel says it has killed new Hamas military leader in Gaza City airstrikes

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

How to Build Wealth – Financial Expert Reveals his 15 Yrs Journey ft. @pattufreefincal

THIS IS NO JOKE!!?? XRP JUST WENT LIVE WORLD WIDE?! (SWITCH FLIPPED)

Save First, Spend Later | Warren Buffett Best Financial Advice in Tamil #Shorts | Life Lines Tamil

-

Business4 days ago

Business4 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World7 days ago

Crypto World7 days agoOppenheimer backs SpaceX as $70 billion retail frenzy builds

-

Crypto World7 days ago

Crypto World7 days agoMarkets Rally as SpaceX IPO Looms Amid Iran Tensions and Inflation Surge

-

Crypto World3 days ago

Crypto World3 days agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Crypto World5 days ago

Crypto World5 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Tech5 days ago

Tech5 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Tech6 days ago

Tech6 days agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

NewsBeat6 days ago

NewsBeat6 days agoEl Nino has formed in the Pacific and could set records, forecasters say

-

Tech7 days ago

Tech7 days agoDutton Ranch star claims they ‘didn’t see any disruption’ on set following Chad Feehan’s exit from Yellowstone spinoff fueled by Taylor Sheridan clash rumors

-

Politics7 days ago

Politics7 days agoPolitics Home | Healey Resignation Is “Colossal Failure Of Government”, Says Former Labour Defence Secretary

-

Entertainment7 days ago

Entertainment7 days agoDonnie Wahlberg & More Heat Up Las Vegas at Circa’s Barry’s Downtown Prime

-

Sports7 days ago

Sports7 days agoFirst Time Since 1971: Australia Register Historic Low In ODI Cricket

-

Tech7 days ago

Tech7 days agoOpendoor Ends India Operations, Fueling a Bigger Conversation About AI and Outsourcing

-

Politics7 days ago

Politics7 days agoBelfast burns, while Met chief points finger at Iran and Russia

-

NewsBeat6 days ago

NewsBeat6 days agoFBI searches office of Ohio voter registration group

-

Business7 days ago

Business7 days agoAT&T: Verizon's 27% Outperformance Sets Up A Solid Entry Point

-

Tech6 days ago

Tech6 days agoAnthropic is spending $150M to embed 1,000 AI fellows inside nonprofits. No degree required.

-

Politics7 days ago

Politics7 days agoModi thanks Trump for wishes as US attacks Indian seafarers

-

Entertainment6 days ago

Entertainment6 days ago‘The Pitt’s Fan-Favorite Doctor Confirms Noah Wyle Gave His Blessing to Return [Exclusive]

You must be logged in to post a comment Login