Crypto World

Nio surges 9% after releasing first flagship EV in more than two years

Chinese electric car company Nio announced May 27, 2026, that former NBA player Yao Ming (R) would be a representative for the brand as it launches the ES9 SUV, a car that CEO William Li Bin (L) touted as the largest SUV in China.

Lintao Zhang | Getty Images News | Getty Images

BEIJING — Chinese electric car company Nio is trying to raise the bar for premium vehicles in a fiercely competitive market.

The U.S.-listed stock surged 9% Wednesday, sending shares further into the green for 2026, after Nio officially launched its ES9 SUV with prices as low as 390,000 yuan ($57,470) when paying for battery power on a separate, monthly basis.

It reflects the ongoing race to the bottom in China’s electric car market, despite Beijing’s efforts to curb excessive competition, often called involution.

When Nio launched its flagship ET9 sedan in late 2023, prices started at 800,000 yuan. But before deliveries started in the first quarter of 2025, consumer electronics company Xiaomi had launched its first electric car — at 215,900 yuan.

With the new ES9, which Nio claims is the largest SUV in China, deliveries start Thursday.

CEO William Li showed off an array of features at a launch event in Beijing, from advanced driver-assist systems that can respond to road signs, to passenger seats with wood-colored tables that unfold similarly to those on an airplane. The ES9 also supports an in-car water boiler that lets passengers brew tea.

Nio signed on several brand promoters, including Robin Zeng, the CEO of CATL, the industry’s battery giant, who affirmed in a marketing video that about 2,000 of his employees had bought Nio cars.

Nio

Li also emphasized how the ES9 proactively protects passengers with “smart safety” systems that can detect and minimize impact from dangerous scenarios, and got China’s state broadcaster CCTV to livestream a crash test and other safety features.

Nio delivered 83,465 cars in the first quarter, nearly twice as many as a year ago, but a 33% drop from the fourth quarter. The figure also includes vehicles from Nio’s lower-priced brands Onvo and Firefly, which the company launched in the last two years to remain competitive in China’s sluggish consumer market.

Tesla‘s Model Y was the top-selling SUV in China last month by deliveries, according to industry data site China AutoHome. Elon Musk’s automaker last week received Beijing’s approval to launch driver assist in the country after years of waiting.

Nio’s ES8 ranked 10th in April deliveries across both electric and traditional gasoline-powered cars.

Foreign automakers are also revamping competition in China’s premium market at lower prices.

Audi on May 8 started presales for its E7X electric SUV with prices starting at 289,800 yuan, and is set to officially launch the car Friday morning. The car is the second model under the German automaker’s new China-focused brand, co-developed with Shanghai’s SAIC, that replaces the four-rings logo with the AUDI letters.

The US Commodity Futures Trading Commission (CFTC) has proposed new rules for prediction markets, signaling that sports event contracts are generally not contrary to the public interest even though federal law classifies them as “gaming.”

Released on Wednesday, the proposal distinguishes sports event contracts from games of pure chance, saying markets based on final scores and win-loss records can aid price discovery. Contracts tied to player injuries, officiating decisions or other outcomes that could encourage manipulation, however, are unlikely to meet the public interest test.

The proposal also clarifies that election contracts are not considered “gaming” under the relevant federal laws. Reuters reported this could further ease regulatory uncertainty for platforms such as Kalshi and Polymarket, which rose to prominence during the 2024 US presidential election as traders increasingly turned to prediction markets to gauge the race’s outcome.

The draft rules are open for public comment for 45 days and could help define the future regulatory framework for US prediction markets.

Gary Kalbaugh, a partner at Cahill Gordon & Reindel LLP in New York, said the proposal is principles-based rather than a blanket approval, noting that each contract would still be subject to a case-by-case public interest analysis.

“‘Gaming’ is defined more broadly than anticipated and sweeps in sports events,” Kalbaugh wrote on Wednesday. “Contracts settling on aggregate outcomes (final scores, win-loss, season stats) are presumptively permissible.”

Source: Gary Kalbaugh

Related: Anchorage backs Treasury’s GENIUS AML rules, seeks secondary-market sanctions clarity

Increased regulatory clarity comes as prediction markets see adoption surge

The proposed rules come as prediction markets — described as an “asset class” in the draft — continue to gain momentum, with Kalshi and Polymarket reaching multibillion-dollar valuations amid rising investor and institutional interest.

Both companies have expanded their ties to traditional financial markets. Kalshi recently partnered with Nasdaq to launch a new category of prediction markets that allows users to forecast the future valuations of private companies ahead of their initial public offerings.

Polymarket, meanwhile, has partnered with Dow Jones to integrate real-time prediction market data into its media brands, including The Wall Street Journal.

“The prediction markets continue to become more mainstream, with newly formed partnerships with news organizations and more firms moving quickly into this space,” said Melinda Roth, a professor of sports law and corporate finance at Georgetown University Law Center. “As these markets continue to grow, the unanswered question is if event contracts are financial instruments or are they simply gambling.”

Analysts at Bernstein say prediction markets are seeing growing institutional adoption as investors seek alternative macro-hedging tools through binary-outcome contracts.

Magazine: How to fix suspected insider trading on Polymarket and Kalshi

The European Union has advanced a sanctions package aimed at Russia that extends restrictions to the crypto sector. The 21st set of measures would ban transactions on 11 crypto platforms as part of a broader effort to cut off channels that could enable evasion of the bloc’s restrictions amid Moscow’s war in Ukraine.

In statements on X, Kaja Kallas, vice president of the European Commission and the EU’s foreign policy chief, described the proposal as widening the sanctions regime beyond banks and energy revenues to include crypto firms and other actors outside the bloc. The Commission has not publicly named the 11 platforms under consideration. European Commission President Ursula von der Leyen later framed the package as targeting 31 additional Russian banks and 20 third-country entities, including crypto platforms and oil traders, to curb activity that assists sanctioned individuals or supports attempts to circumvent EU measures.

Key takeaways

- The EU’s 21st sanctions package would ban transactions on 11 crypto platforms, extending sanctions enforcement into the crypto sector and aiming to close gaps used to bypass restrictions.

- The package expands the roster of designated entities to include 31 Russian banks and 20 third-country actors, among them crypto platforms and oil traders, strengthening cross-border enforcement.

- The Commission has not publicly identified the 11 platforms; designation details are expected through formal channels as the package progresses.

- The move follows parallel actions by other jurisdictions, notably the United Kingdom’s sanctions on HTX Global S.A. for alleged support to Russia-linked financial networks, illustrating a trend toward coordinated sanctions pressure on crypto service providers.

- For the crypto industry, the proposal signals heightened regulatory scrutiny, expanding AML/KYC obligations, licensing considerations, and sanctions-screening requirements for EU-pressured operations and counterparties, with potential implications for cross-border liquidity and service provision.

EU expands sanctions to crypto platforms

The EU’s latest sanctions package represents a deliberate step to align digital-asset oversight with traditional financial controls. By extending bans to crypto platforms, the bloc seeks to deprive sanctioned actors of avenues to move funds, access counterparties, or conduct transactions that could contravene existing restrictions. The measures are framed as part of a broader effort to prevent sanctions evasion, with officials arguing that crypto entities outside the EU have, in some cases, facilitated or facilitated access to sanctioned networks.

While the Commission has not named the 11 platforms, the move signals a willingness to apply sanctions pressure at the point of transactional interaction in the crypto markets, not solely on traditional banking rails. The approach reflects ongoing EU policy objectives to bring crypto activity under comprehensive compliance, monitoring, and enforcement standards, particularly in relation to anti-money-laundering (AML) and countering the financing of terrorism (CFT) regimes. In parallel, the EU continues to advance its broader crypto policy agenda, including MiCA and related initiatives intended to provide a harmonized regulatory framework for crypto service providers and market participants across member states.

The designation of entities beyond Russia’s banking sector—such as crypto platforms and oil traders—illustrates the EU’s intent to curb holistic support networks that may enable evasion of asset freezes or sanctions. The lack of immediate public disclosure about the specific platforms under review underscores the procedural nature of sanctions designations, which typically unfold through formal regulations and subsequent compliance guidance.

Compliance, licensing, and enforcement implications

The expansion to crypto platforms is likely to alter the compliance landscape for firms with either EU operations or counterparties connected to EU markets. Crypto exchanges, wallet providers, custodians, and other service operators could face heightened obligations, including rigorous sanctions screening, enhanced due diligence, and stricter transaction monitoring. For banks and financial institutions engaged with crypto entities, the package adds a further layer of risk assessment and regulatory oversight, reinforcing the need for robust know-your-customer (KYC) processes and AML controls in line with EU and global standards.

From a licensing perspective, the EU’s approach may intersect with MiCA provisions and ongoing efforts to clarify the regulatory status of various crypto activities. While MiCA primarily governs the licensing, governance, and disclosure requirements for crypto-asset service providers, the sanctions context adds an external compliance constraint that firms must incorporate into risk management, treasury operations, and cross-border settlement arrangements. Operators seeking or holding EU licenses may also face stricter reporting requirements, heightened scrutiny of third-country ties, and more frequent audits or investigations related to sanctions compliance.

For market participants outside the EU, the development raises considerations about access to EU markets and the ability to service EU customers while complying with potentially expanding restrictions on sanctioned entities. The scope of the designations—particularly if linked to third-country platforms—could influence international cooperation on sanctions enforcement, including data sharing, screening standards, and any mutual recognition arrangements that affect cross-border enforcement efforts. Moreover, the move could drive crypto firms to reassess their counterparties and routing options to avoid inadvertently facilitating sanctioned activity, even if unintentional.

Cross-border action and broader policy context

The EU action follows a widening pattern of cross-border sanctions enforcement against crypto platforms and related entities. In the United Kingdom, authorities imposed sanctions in May on HTX Global S.A., the Panamanian entity behind HTX, on grounds of suspected support for Russia-linked financial networks. UK officials asserted reasonable grounds to suspect that HTX facilitated financial services and funds connected to sanctioned actors via intermediaries such as A7 Limited Liability Company and Grantex, with HTX denying direct ties to the sanctioned entity. This alignment of steps across major jurisdictions highlights how sanctions policy is increasingly threading through crypto markets, regardless of national borders.

Analysts have cautioned that broad exchange-level tainting can have mixed effects on the integrity of tracing illicit flows. On one hand, expanding the sanctions net to cover crypto platforms reduces the channels through which sanctioned actors can maneuver funds. On the other hand, overly broad or opaque designation efforts risk freezing legitimate users or impeding legitimate compliance tools, potentially hindering the ability of investigators to track illicit money flows. Industry researchers have raised concerns about the potential chilling effects on the legitimate crypto ecosystem if enforcement tools are not carefully calibrated to distinguish sanctioned actors from compliant users and compliant service providers.

Background data cited in industry observations show how flows can intersect with sanctioned networks. A Global Ledger analysis noted substantial high-risk activity linked to HTX and related entities, illustrating the scale at which exchanges can interact with high-risk corridors. Such findings underscore the practical challenges that regulators face in maintaining a balance between restricting illicit activity and preserving legitimate access to financial services and lawful movement of value. In this context, the EU’s designation process will be closely watched by financial institutions, exchanges, and compliance teams as they adapt to evolving risk profiles and enforcement expectations.

From a policy standpoint, the EU’s move sits within a broader trajectory of tightening crypto regulatory oversight in the context of EU financial-market integration, consumer protections, and the international stance on sanctions enforcement. For institutions, this means integrating sanctions screening with crypto-asset risk assessments, aligning corporate policies with EU-level guidance, and ensuring that cross-border operations stay within the boundaries of designated entities and restricted channels. In parallel, ongoing policy debates surrounding MiCA and future rulemakings around stablecoins, tokenization, and banking access for crypto firms will influence how sanctions risk interacts with broader market structure and regulatory alignment.

Closing perspective

As the EU clarifies which crypto platforms will be subject to transaction bans, regulators will also weigh the designations’ scope, potential enforcement challenges, and compatibility with broader EU crypto policy objectives. The next steps will likely include formal designation announcements, accompanying guidance for market participants, and possible legal challenges from affected firms. Given the regional and international regulatory momentum, institutions should prepare for intensified due diligence, updated compliance playbooks, and closer attention to MiCA-related licensing pathways as sanctions designations unfold and cross-border cooperation evolves.

The U.S. Commodity Futures Trading Commission has floated a formal rule framework for prediction markets, signaling a cautious but potentially meaningful path toward legitimizing event-based contracts. In the agency’s proposed rules, sports event contracts are not regarded as inherently contrary to the public interest even though federal law classifies gaming as a broad category. The move suggests a nuanced stance: markets that reflect final scores or win-loss records could aid price discovery, while contracts tied to injuries, officiating decisions, or other elements that could invite manipulation are less likely to pass what the CFTC calls a public-interest test.

The CFTC’s draft, released this week, distinguishes sports event contracts from games of pure chance and argues that markets built on verifiable outcomes can contribute to market transparency and price formation. By contrast, contracts that hinge on subjective or manipulable outcomes may fail the test of public interest and could face stricter scrutiny or rejection. The agency’s approach signals a recognition that not all outcome-based contracts are the same, and that the underlying mechanics—how outcomes are determined and settled—will matter as much as the event itself.

The proposal has immediate regulatory implications for platforms that have gained traction in the U.S. prediction-market space, notably Kalshi and Polymarket. Reuters reported that election-focused contracts—central to both platforms during the 2024 U.S. presidential race—are not considered “gaming” under current federal law, a distinction that could ease regulatory uncertainty for such ventures as they expand beyond political bets. The draft rules are open for public comment for 45 days, allowing participants, policymakers, and investors to weigh in before any formal adoption.

The prospect of clearer, principles-based guidance comes at a moment when prediction markets are aggressively positioning themselves as a new, alternative layer of financial information. The industry has already begun to carve out a niche as a form of macro-hedging and data-driven forecasting, attracting interest from traditional finance and media alike.

Gary Kalbaugh, a partner at Cahill Gordon & Reindel LLP, welcomed the proposal’s direction but cautioned that it remains principles-based rather than an outright green light. In his view, each contract would still undergo a case-by-case public-interest analysis under the framework. “Gaming” is defined more broadly than some expect and could sweep in sports events, he noted, yet contracts settling on aggregate outcomes—such as final scores, win-loss records, or season statistics—appear presumptively permissible under the new approach.

Key takeaways

- The CFTC’s proposal frames prediction markets as an asset class that can be lawful if contracts are structured to support price discovery, with sports-based bets treated differently from high-risk, manipulable outcomes.

- Election contracts are not classified as gaming under current federal law, a distinction that could reduce regulatory friction for platforms like Kalshi and Polymarket.

- A 45-day public comment window will shape how regulators, market participants, and lawmakers view the framework and its potential adoption across the U.S. market.

- The rules are intended to be principles-based and contract-specific, meaning a one-size-fits-all approval is unlikely; a case-by-case assessment will determine permissibility.

- Early adoption signs point to growing mainstream interest in prediction markets, with platform partnerships and rising valuations illustrating ongoing institutional engagement.

Regulatory architecture and what changes

The draft marks a shift toward a more nuanced regulatory posture, separating sports-event contracts—where outcomes are typically final and verifiable—from forms of betting that hinge on chance or subjective judgments. In the agency’s view, contracts tied to objective results such as final game outcomes or season stats can contribute to price discovery. This is a departure from a blanket presumption of illegality and implies a more flexible framework that could accommodate a range of contract designs while maintaining guardrails against manipulation or deception.

Analysts and legal experts have underscored that the architecture hinges on case-by-case evaluation under a public-interest standard. The Kalbaugh assessment highlights that the framework’s principles-based nature will require careful scrutiny of each contract’s settlement mechanics, data integrity, and potential for gaming the system. As the CFTC’s proposal invites stakeholder feedback, observers will likely probe how the agency will weigh the balancing act between innovation and investor protection in real-world markets.

Momentum, partnerships, and institutional interest

Even as the regulatory dialogue evolves, the industry’s momentum persists. Prediction markets have increasingly been described as an asset class in their own right, attracting multibillion-dollar valuations for pioneering platforms such as Kalshi and Polymarket. These firms have tapped traditional financial markets to extend their reach and legitimacy. Kalshi has aligned with Nasdaq to launch new categories that enable users to forecast private company valuations ahead of initial public offerings, signaling a bridge between private-market signaling and public market dynamics. Polymarket has pursued a different path, partnering with Dow Jones to weave real-time prediction-market data into its media partnerships, including The Wall Street Journal. The goal appears twofold: deepen market liquidity and provide journalists and investors with data-driven narrative tools that reflect consensus forecasts across a spectrum of events.

Experts see these trends as indicative of broader adoption rather than episodic hype. Georgetown University Law Center professor Melinda Roth noted that prediction markets are becoming more mainstream as partnerships with media and financial institutions expand. The question, she said, is whether event contracts function as recognizable financial instruments or whether they remain closer to speculative bets. Bernstein & Co. has likewise highlighted growing institutional interest, framing prediction markets as potential macro-hedging tools offering binary-outcome payoffs that can diversify risk in a portfolio of macro bets.

For readers watching the regulatory horizon, the combination of clarified rules and expanding market activity creates a nuanced landscape. The CFTC’s proposed framework could lower friction for compliant platforms while preserving guardrails to deter manipulation and abuse. It also underscores a longer arc of regulatory maturation: as the market scales, lawmakers and regulators will be watching how prediction markets interact with traditional financial markets, consumer protection standards, and market integrity mechanisms.

What to watch next

With the public-comment window now open, the next several weeks will reveal how stakeholders respond to the CFTC’s approach. Key questions include how the agency will define and monitor data integrity, what types of contract settlements will be deemed manipulable, and how such markets will interact with existing securities and gaming laws. Investors and users should monitor whether the final rules—potentially refined after public input—create clearer pathways for platform operators to design compliant, price-discovery-focused contracts while guarding against exploitative tactics.

As prediction markets move from an experimental niche to a more integrated part of the financial information ecosystem, readers should stay attuned to how platforms adapt their product designs, data feeds, and regulatory risk management practices. The unfolding framework could shape not only how participants trade today, but how developers, researchers, and media partners leverage these markets to gauge sentiment, forecast events, and inform decision-making in a rapidly evolving landscape.

Solana DEX Raydium confirmed Wednesday that an attacker drained approximately $1.34 million from its legacy AMM V3 program, a deprecated contract phased out in 2021, with current users unaffected and full compensation coming from the protocol treasury. Raydium core contributor Infra disclosed the… Read the full story at The Defiant

Amazon has secured a $17.5 billion delayed draw term loan facility from Citibank and other banks.

Summary

- Amazon secured a $17.5 billion delayed draw term loan facility from Citibank and other banks.

- The company said the loan proceeds will support general corporate purposes, including investments and debt repayment.

- Bloomberg linked the financing to Amazon’s AI spending plans, including infrastructure costs and AI company investments.

The company disclosed the senior unsecured agreement in a June 10 filing with the Securities and Exchange Commission. The financing gives Amazon extra borrowing capacity for corporate needs, capital spending, and debt repayment.

Loan commitments run through Sept. 30

According to Amazon’s SEC filing, bank commitments under the facility expire on Sept. 30. Amazon can draw funds before that date, unless it borrows the full amount earlier. Any loan drawn under the facility will mature three years from the borrowing date. Citibank N.A. serves as the administrative agent for the agreement.

Amazon described the borrowing purpose in narrow terms. “Borrowing under the DDTL Facility will be used for general corporate purposes,” the company said. The filing did not assign proceeds to any single project. However, the structure lets Amazon access funds as business needs arise.

According to a report by Bloomberg, an Amazon spokesperson gave more details on those purposes. The spokesperson said proceeds may support investments, fund capital expenditures, and repay debt.

AI spending forms part of the funding backdrop

The new loan could help Amazon fund artificial intelligence investments. The report linked the facility to Amazon’s technology infrastructure plans.

Amazon has said it plans about $200 billion in AI infrastructure and other capital expenditures this year. Bloomberg cited that figure in its report as well as Amazon’s investments in AI companies. Amazon is expected to invest up to $50 billion in OpenAI.

The report said Amazon has already invested $10 billion in Anthropic. It also said another $15 billion investment in Anthropic may follow. Amazon also continues spending on cloud, data centers, and computing capacity. Amazon did not name any AI project in the SEC filing.

Debt sales add context to financing

Amazon sold 14 billion Canadian dollars of high-grade bonds on June 8. The sale equaled about $10 billion, according to the report. Since March, Amazon has sold bonds in euros, U.S. dollars, and Swiss francs, Bloomberg reported. The Canadian dollar sale came before the loan disclosure.

The company has not said the loan replaces any specific bond sale. It has also not disclosed any drawdown under the facility. The DDTL Credit Agreement includes customary representations, warranties, covenants, and default events, according to Amazon. The filing said it does not contain financial covenants.If a default event occurs, Amazon would have applicable grace periods.

If unresolved or unwaived, unpaid amounts may become immediately due. The filing said lenders may terminate commitments after an unresolved default event. Amazon named the firms as full-service financial institutions with multiple business lines. Their activities may include trading, commercial banking, investment banking, advisory, investment management, research, hedging, brokerage, and market making.

TLDR:

- Binance holds $41.2B in USDT, but the ERC-20 book is at the 23.5th percentile of its 30-day range.

- Combined 30-day USDT netflows across ERC-20 and TRC-20 at Binance total approximately -$1.27 billion.

- The MA7 flipped to +$120M on June 5 before cooling to neutral by June 8, signaling deceleration.

- KuCoin and Bitget show TRC-20 accumulation, but their $465M reserve limits the signal’s market impact.

Bitcoin stablecoin liquidity on Binance continues to weaken in June 2026, pointing to market consolidation rather than a fresh recovery.

The exchange holds roughly $41.2 billion in USDT across ERC-20 and TRC-20 chains, yet the reserve has been declining steadily.

On-chain data shows the ERC-20 book has shed 2.3% over the past 30 days, sitting at only the 23.5th percentile of its 30-day range — well below accumulation territory.

Outflow Intensity Peaked in Late May

Combined 30-day netflows across both chains total approximately -$1.27 billion, marking a broad retreat of capital from the exchange.

Late May registered the most extreme outflow intensity of the current cycle, with the seven-day moving average of ERC-20 netflows dropping to -$215 million — a reading flagged as a strong capital exit signal.

The pace of distribution shifted in early June, though the direction remains negative. The MA7 flipped briefly to +$120 million on June 5 before cooling back to neutral by June 8, suggesting deceleration rather than reversal.

According to CryptoQuant analyst Crazzyblockk, this is a key distinction: “Until Binance’s USDT reserve reclaims its 30-day average with sustained positive daily flows, the liquidity foundation for a BTC recovery remains incomplete.”

The reserve remains nearly 12.4% below its December 2025 peak of $43.9 billion. Capital that exited during the correction has not returned, and the 30-day average has yet to be reclaimed. These conditions make it difficult to argue that a genuine recovery cycle is underway.

The broader exchange picture adds further context to the data. OKX, Bybit, and Bitfinex are all in mild distribution on a 30-day basis, reinforcing the pattern seen at Binance.

Smaller Exchanges Accumulate, But Signal Remains Limited

KuCoin and Bitget are showing accumulation on the TRC-20 chain in early June, which stands in contrast to the dominant outflow trend. However, their combined reserve of approximately $465 million limits the structural weight of this signal.

For a signal to carry meaningful market impact, it must originate from exchanges that hold a significant share of total stablecoin liquidity.

At current levels, KuCoin and Bitget together represent a fraction of what Binance alone holds, making their accumulation a minor counterpoint rather than a market-shifting force.

Bitcoin traded in the low $60,000 range through early June, and stablecoin flows suggest the market is stabilizing rather than reloading.

The distinction matters: stabilization reflects reduced selling pressure, whereas reloading implies fresh capital entering in preparation for an upside move.

Until Binance’s USDT reserve consistently posts positive daily flows and climbs back above its 30-day average, the liquidity conditions for a sustained BTC price recovery remain thin. The data, as it stands, supports a consolidation scenario — not a recovery.

TLDR:

- SpaceX debuted at $2T and 100x revenue, dwarfing Apple’s sub-$2B IPO — a valuation gap analyst calls alarming

- Insiders hold 95% of SpaceX shares, with 93% becoming sellable by November via a compressed unlock schedule

- Retail and institutional selling to fund IPO participation is draining liquidity from the broader US stock market

- SpaceX posted $4.3B in Q1 2026 losses; cumulative losses hit $41.3B, data most retail investors overlook

The US stock market is flashing warning signs not seen since the dot-com collapse. A veteran market analyst with 13 years of experience is sounding the alarm over the current IPO boom, calling it the biggest red flag of his career.

At the center of the warning is SpaceX, going public at $2 trillion and 100x revenue. That compares to Apple’s IPO at under $2 billion and 15x revenue — a contrast that exposes how extreme current valuations have become.

Insider Structure and Unlock Timeline Set the Stage for a Selloff

The SpaceX IPO is not designed to reward new buyers. Fidelity dropped its minimum investment from $500,000 to $2,000, and SpaceX allocated 30% of shares to retail participants. Millions of new buyers were brought in just before the listing.

Insiders, however, control 95% of all shares. That represents approximately $1.66 trillion in privately held stock sitting above the market. Retail buyers are entering at peak prices while those holding the bulk of shares prepare to sell.

The unlock schedule makes the threat concrete. A 60-day lockup triggers a 20% release once the stock climbs 30%. From day 70, recurring 7% tranches unlock across days 90, 105, 120, and 135. Another 28% follows Q3 earnings.

By November, roughly 93% of insider shares become sellable. That volume hitting the market over a compressed window is a direct threat to the broader US stock market, not just SpaceX’s price.

Capital Rotation Is Already Draining the Broader Market

Institutions are not waiting. They are already shortening index inclusion timelines, selling current holdings, and raising cash ahead of forced buying tied to new listings. That repositioning creates selling pressure across existing equities right now.

Retail investors are doing the same, liquidating portfolios to fund IPO participation. The analyst draws a direct parallel to the late 1990s dot-com era, when capital rotation out of existing stocks into new listings preceded a broad market crash.

SpaceX reported $4.3 billion in losses in Q1 2026 alone. Cumulative losses stand at $41.3 billion. Most retail participants never reach that data, buried deep inside a 300-page prospectus. That information gap consistently favors insiders over new buyers.

Anthropic and OpenAI carry the same structural problem. Both trade at valuations inflated by circular investment flows involving Nvidia.

Neither has reached profitability, and current pricing requires earnings growth that analysts say is unlikely to materialize.

The analyst’s conclusion is straightforward: capital flowing into these IPOs exits the US stock market, and that exit pressure is building fast.

Robinhood Securities has received approval to serve as an IPO underwriter, CEO Vlad Tenev announced Tuesday, moving the brokerage from a distribution role into the group of firms that help bring companies public alongside Wall Street banks. Tenev posted the announcement on X Tuesday, writing that… Read the full story at The Defiant

[PRESS RELEASE – New York, United States, June 10th, 2026]

Shotgun.fun, a new trading terminal, launches today with a model that returns every fee back to the trader, ending an industry standard that has quietly extracted billions.

Every trade ever placed has made someone else money: not the market and not the protocol, but the terminal sitting between traders and execution. The fee paid on every buy, every sell, and every limit order became the status quo. Shotgun’s the paradigm shift.

Shotgun.fun is a high-performance trading terminal that returns up to 100% of trading fees to traders. Cashback starts at 50%, already higher than any other trading terminal offering, and scales with volume. Tiers are built to unlock fast. Getting to 100% is not an out-of-reach theoretical ceiling, it’s the destination.

The terminal is fully non-custodial, secured through Turnkey, ensuring keys are encrypted and accessible only to the user.

Shotgun arrives fully loaded:

- Trenches displays new launches, graduating tokens, and fresh migrations in real time, ahead of broader market visibility.

- Trader Discovery helps users find the best traders in the space and copy their moves in real time.

- Instant Trade adds one-click trading directly on the chart, no distractions.

- Limit Orders enable autopilot trading from buying the dip to stop loss, take profit, and trailing stop loss.

- Multi-Wallet Management helps users bring all their wallets into a single interface. Full control, zero friction.

- Portfolio captures full historical performance of every wallet, every token, every profit and loss.

Insiders have extracted hundreds of millions from everyday traders across recent token launches. Shotgun aims to even the playing field by shining a light on insider wallets, helping users view their trades and copy their moves in real time.

Shotgun also comes packed with a referral program that offers up to 50% revenue share across five layers of referrals, meaning users earn when their referrals trade.

Shotgun is led by Miguel Loures and Pedro Maurício, the founding team behind Pulsar Finance, a portfolio manager backed by Delphi Ventures that grew to more than one million users before being acquired by Terraform Labs. The team has been building in this space since 2020.

“Until now, traders have been treated as the product, not as users,” said Miguel Loures, founder of Shotgun. “We built Shotgun to give the power back to the people.”

Shotgun launches with support for Solana, with more blockchains and agentic trading coming soon.

About Shotgun

Shotgun.fun is a non-custodial trading terminal built for traders. Up to 100% cashback, enterprise-grade execution, and a full suite of tools built for speed, instinct, and being first.

More information available at:

Website: https://shotgun.fun/

Twitter/X: https://x.com/shotgundotfun

The post Shotgun.fun Launches as the First Trading Terminal With 100% Cashback appeared first on CryptoPotato.

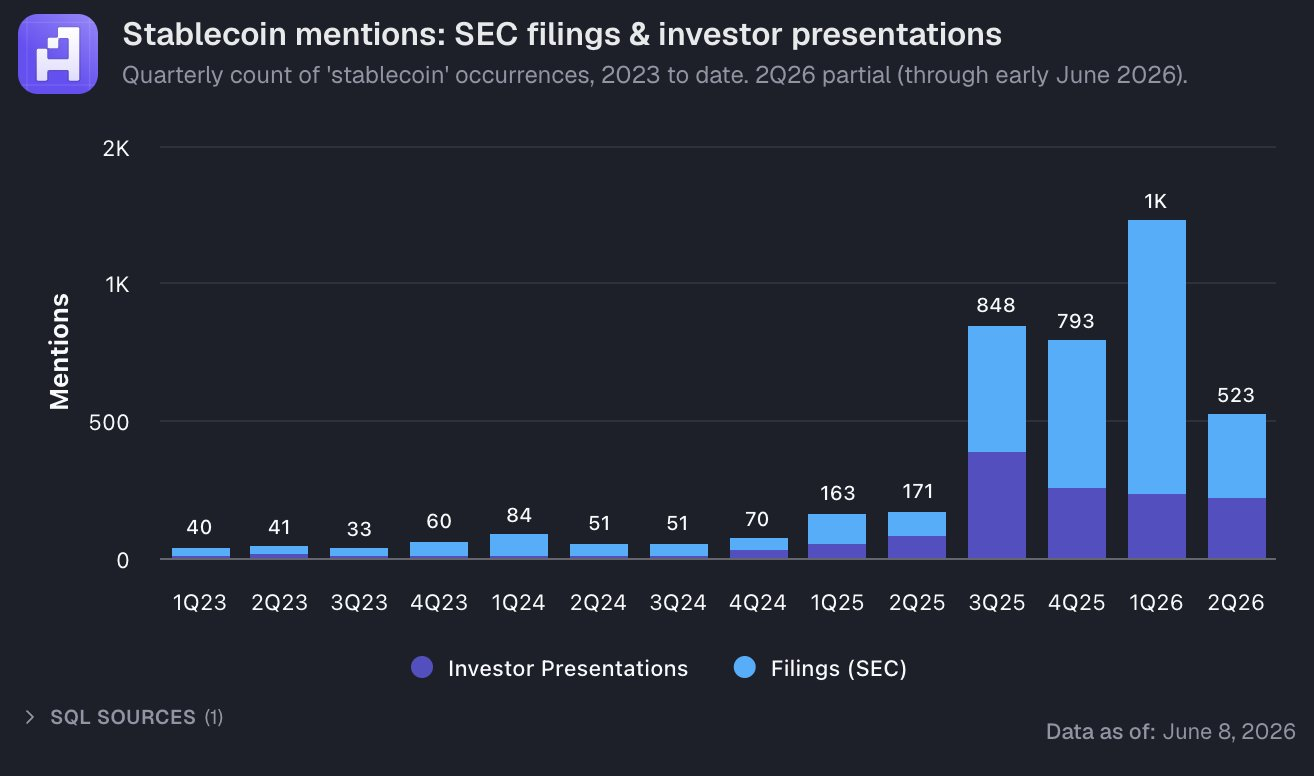

Bitwise CIO Matt Hougan says financial advisors remain interested in crypto but now care more about stablecoins and tokenization than Bitcoin. He drew the conclusion after speaking with more than 40 advisors in a single day of sales calls.

Data from analytics firm Artemis points the same way. Stablecoin mentions in SEC filings and investor presentations peaked at roughly 1,000 in the first quarter of 2026, the firm reports.

Stablecoins and Tokenization Take Center Stage

Hougan described the conversations in a memo published on June 10. Reportedly, he met eight advisory teams on Monday, his busiest single day since joining Bitwise eight years ago.

Engaging those advisors on Bitcoin proved difficult, he admitted, even at prices near $60,000 that he considers attractive for long-term investors.

Instead, conversations kept returning to payments, capital markets, and tokenized assets.

Hougan tied the shift to two forces:

- The fiat debasement trade has faded, with gold trading about 20% below its all-time high by his account,

- Stablecoin talk from SEC Chair Paul Atkins and BlackRock CEO Larry Fink has become constant on financial television.

Follow us on X to get the latest news as it happens

“If you think financial advisors are the marginal net buyer of crypto in the next cycle, the first place money would flow might be into stablecoin- and tokenization-linked investments,” Hougan wrote in the memo.

He expects that flow to favor tokenization rails such as Ethereum (ETH) and Solana (SOL), plus stablecoin-linked equities Circle (CRCL) and Coinbase (COIN).

The pattern would echo earlier cycles, he argued, including the spot ETF progress that pulled crypto out of its 2022 collapse.

Peak Attention or a New Adoption Phase

Artemis adds a measurable signal to the anecdotes, showing stablecoin references in corporate disclosures hit their highest recorded level in Q1 2026.

Regulation helps explain the timing. On February 19, SEC staff said broker-dealers may apply a 2% capital haircut to payment stablecoins, treating them as near-cash.

That guidance builds on the GENIUS Act, the 2025 law that created a federal category for payment stablecoins.

Usage data tells a similar story. A Fireblocks report based on a March 2025 survey of 295 finance executives found 49% of institutions already use stablecoins for payments.

The combination cuts two ways:

- Advisor curiosity suggests fresh capital could flow into stablecoin and tokenization plays first.

- Peaking mentions, however, may indicate the theme is already crowded in corporate communications, with stocks, gold, and Treasuries moving on-chain in practice rather than in pitch decks.

Tokenized real-world assets similarly defied last year’s downturn.

Hougan frames advisors, a group managing more than $175 trillion by Investment Adviser Association figures, as the new investor class that could end the 2026 downturn.

Therefore, their engagement matters more than usual after his earlier crypto winter call proved prescient.

The first-quarter mention peak marking saturation or the start of an implementation phase may become clearer as second-quarter filings arrive.

In the meantime, advisor demand gives the market a concrete adoption signal to track.

The post Bitwise Memo Uncovers Key Insight From 40 Financial Advisors appeared first on BeInCrypto.

Ipswich Town: Manager Kieran McKenna resigns after promotion to Premier League

Uber sues New York City over ’reckless’ driver protection law

CFTC Proposes Prediction Market Rules Favoring Sports Contracts

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Evereve – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoJensen Huang Approves Samsung, SK Hynix, and Micron for NVIDIA (NVDA) HBM4 Memory Supply

-

Crypto World3 days ago

Crypto World3 days agoAnatomy of the June crypto crash: Fed, Iran, Saylor

-

Entertainment4 days ago

Entertainment4 days agoThe Best Mystery Series of All Time Is Surging on Streaming 30 Years After It Ended

-

NewsBeat3 days ago

NewsBeat3 days agoAlexander Zverev wins the French Open to finally earn a 1st Grand Slam title

-

Tech5 days ago

Tech5 days agoSuspicious Polyfill login prompts pop up on Toshiba, Muji websites

-

Crypto World4 days ago

Senator Cynthia Lummis Calls CLARITY Act the Most Consequential Financial Legislation of This Generation

-

Tech6 days ago

Tech6 days agoMicrosoft launches MXC, an OS-level sandbox for AI agents, with OpenAI and Nvidia already on board

-

Tech4 days ago

Tech4 days agoMicrosoft unveils seven homegrown AI models in new bid for ‘long term self-sufficiency’

-

Business6 days ago

Business6 days ago(VIDEO) Justin Bieber Delivers Surprise Happy Birthday Serenade to Diners at Los Angeles Mexican Restaurant

-

Business4 days ago

Business4 days agoThe Pain Points Taking a Fragile Tech Rally Down a Notch

-

Crypto World3 days ago

Crypto World3 days agoEli Lilly (LLY) Stock Surges 4% Following Breakthrough Sleep Apnea Trial Results

-

Crypto World6 days ago

LBank Surpasses 25 Million Users Worldwide as AFA Partnership Continues to Drive Global Growth

-

Tech5 days ago

Tech5 days agoVon der Leyen’s AI envoy pick draws conflict-of-interest fire

-

Crypto World3 days ago

Crypto World3 days agoTrump’s AI Ownership Plan Could Benefit Anthropic at OpenAI’s Expense

-

Tech5 days ago

Tech5 days agoMeta steals a tactic from Tesla and builds data centers in tents

-

Sports1 day ago

Sports1 day agoBangladesh beat Australia after 20 years in ODIs, register only their second win over six-time world champions | Cricket News

-

Business3 days ago

Business3 days agoHigh Stakes for Wembanyama as New York Pushes for 3-0 Lead

-

Tech5 days ago

Tech5 days agoHackers now exploit SolarWinds Serv-U flaw to crash servers

-

Tech3 days ago

Tech3 days agoNotion restores access to Anthropic after service disruption

You must be logged in to post a comment Login