Crypto World

Nvidia Partners with Groq on New Inference Platform as OpenAI Seeks Speed

Key Points

- A fresh inference computing platform is in development at Nvidia to accelerate AI model execution for OpenAI and similar enterprises.

- Groq, a chip startup, will supply the processor for this platform, which Nvidia plans to unveil at its upcoming GTC conference in San Jose.

- Performance issues with Nvidia’s existing hardware have left OpenAI dissatisfied, particularly for development-related workloads.

- A massive $20 billion licensing agreement between Nvidia and Groq halted OpenAI’s independent negotiations with the startup.

- Last September, Nvidia pledged up to $100 billion toward OpenAI in exchange for equity ownership.

According to a Wall Street Journal article released Friday, Nvidia is creating a specialized processor designed to enhance the speed and efficiency of AI inference operations.

When AI systems like ChatGPT answer user questions, they’re performing inference computing. This differs substantially from training operations, where Nvidia has maintained market leadership for years.

Nvidia’s GTC developer conference in San Jose next month will serve as the launch venue for this platform. At its core sits a processor manufactured by emerging company Groq.

Neither Reuters nor Nvidia provided immediate confirmation of these details. OpenAI similarly remained silent when asked for comment.

The context surrounding this development is significant. Earlier this month, Reuters revealed that OpenAI has expressed frustration over performance limitations in Nvidia’s current hardware lineup—particularly when handling software development queries and facilitating AI-to-AI interactions.

OpenAI is pursuing hardware solutions capable of managing approximately 10% of its inference workload. Nvidia appears determined to retain this business.

The Hunt for Enhanced Processing Power

Prior to Nvidia’s intervention, OpenAI had initiated discussions with two chip manufacturers—Cerebras and Groq—seeking superior inference processing capabilities.

Those negotiations ended abruptly. Nvidia secured Groq through a $20 billion licensing arrangement, eliminating OpenAI’s option to work directly with the startup.

This represents a calculated strategic maneuver. By acquiring Groq’s technology through licensing, Nvidia simultaneously blocked a potential competitor from reaching OpenAI while gaining access to Groq’s chip innovations for its own infrastructure.

The Deeper Financial Connection

The commercial ties between Nvidia and OpenAI extend well beyond hardware procurement.

Last September, Nvidia announced plans to commit up to $100 billion to OpenAI. This arrangement provided Nvidia with ownership shares in the AI developer while furnishing OpenAI with resources to acquire cutting-edge processors.

Nvidia now occupies dual roles as both hardware vendor and financial stakeholder—a strategic position that creates powerful incentives to maintain control over OpenAI’s chip requirements.

On February 27, the day prior to this news emerging, NVDA stock declined 4.16%.

Should the inference platform receive official confirmation at next month’s GTC event, it would mark Nvidia’s targeted answer to mounting demands from clients requiring faster, purpose-built AI processing capabilities.

Groq’s inclusion in the platform architecture indicates Nvidia’s readiness to forge startup partnerships rather than engage in pure competition—particularly when such collaborations prevent competitors from accessing major clients.

Nvidia’s GTC developer conference is scheduled for San Jose next month, where the company is anticipated to formalize this announcement.

Jamie Dimon, chief executive officer of JPMorgan Chase & Co., right, departs the US Capitol in Washington, DC, US, on Wednesday, Feb. 25, 2026.

Graeme Sloan | Bloomberg | Getty Images

JPMorgan Chase CEO Jamie Dimon said Tuesday that while artificial intelligence tools could eventually help companies defend themselves from cyberattacks, they are first making them more vulnerable.

Dimon said that JPMorgan was testing Anthropic’s latest model — the Mythos preview announced by the AI firm last week — as part of its broader effort to reap the benefits of AI while protecting against bad actors wielding the same technology.

“AI’s made it worse, it’s made it harder,” Dimon told analysts on the bank’s earnings call Tuesday morning. “It does create additional vulnerabilities, and maybe down the road, better ways to strengthen yourself too.”

When asked by a reporter about Mythos, Dimon seemed to refer to Anthropic’s warning that the model had already found thousands of vulnerabilities in corporate software.

“I think you read exactly what is it,” Dimon said. “It shows a lot more vulnerabilities need to be fixed.”

The remarks reveal how artificial intelligence, a technology welcomed by corporations as a productivity boon, has also morphed into a serious threat by giving bad actors new ways to hack into technology systems. Last week, Treasury Secretary Scott Bessent summoned bank CEOs to a meeting to discuss the risks posed by Mythos.

JPMorgan, the world’s largest bank by market cap, has for years invested heavily to stay ahead of threats, with dedicated teams and constant coordination with government agencies, Dimon said.

“We spend a lot of money. We’ve got top experts. We’re in constant contact with the government,” he said. “It’s a full-time job, and we’re doing it all the time.”

‘Attack mode’

Still, the CEO warned that risks extend beyond any single institution, given the interconnected nature of the financial system.

“That doesn’t mean everything that banks rely on is that well protected,” Dimon said. “Banks… are attached to exchanges and all these other things that create other layers of risk.”

JPMorgan Chief Financial Officer Jeremy Barnum said the industry has long been aware that AI cuts both ways in cybersecurity.

“These tools can make it easier to find vulnerabilities, but then also potentially be deployed by bad actors in attack mode,” Barnum said on the earnings call. Recent advances from Anthropic and others have simply intensified an existing trend, he said.

Dimon also said that while advanced AI tools are important, old-school cybersecurity practices remain essential.

“A lot of it is hygiene… how do you protect your data? How do you protect your networks, your routers, your hardware, changing your passcode?” he said. “Doing all those things right dramatically reduces the risk.”

Goldman Sachs CEO David Solomon said Monday during an earnings call that his bank was testing Mythos, though he declined to comment further.

Blockchain investigator ZachXBT has linked a fake Ledger Live app to over 50 victims, who have lost a total of $9.5 million worth of crypto between them.

He traced stolen funds to KuCoin deposit addresses and called out the crypto exchange via Telegram and X.

Over 150 addresses tied to a known money laundering service were reportedly used to deposit stolen funds to the exchange.

App Store honeypot

Garrett Dutton of the band G. Love & Special Sauce initially drew attention to the fake wallet app, previously available on Apple’s App Store, when he took to X on Saturday to lament losing his retirement fund “in an instant.”

Dutton’s thread explains that he lost 5.9 bitcoin (BTC),worth approximately $440,000, after being “tricked” into entering his seed phrase into the app.

Read more: Thai police want Interpol to track alleged KuCoin money launderer

Around 12 hours after Dutton’s post, ZachXBT flagged nine transaction IDs which the sleuth claims show Dutton’s BTC being “laundered” via crypto exchange KuCoin.

Two days later, ZachXBT published a follow-up community alert to his Investigations Telegram group. It linked the fake app to “$9.5M stolen from 50+ suspected victims between April 7–13 across Bitcoin, EVM, Tron, Solana, & Ripple.”

The top three victims reportedly lost a combined total of $7.25 million in various cryptocurrencies.

KuCoin under fire

ZachXBT’s Telegram post also tied over 150 KuCoin deposit addresses to money laundering service AudiA6.

He also called out KuCoin on X, where he highlighted both these fake Ledger Live app-linked thefts and the recent Bitcoin Depot loss, accusing the exchange of allowing money launderers to “operate freely.”

Read more: Bitcoin Depot didn’t spot 50 BTC hack for three days, report

The exchange eventually replied to ZachXBT’s list of theft addresses in the Dutton case, 48 hours after it was posted. Other on-chain investigators have flagged addresses allegedly linked to scams who have deposited significant sums to KuCoin over recent weeks.

Just over two years ago, KuCoin and two of its founders were charged with flouting U.S. anti-money laundering laws.

Protos reached out to KuCoin, but it did not respond immediately, we will update this piece if we hear back.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Crypto World

White House Signals Breakthrough on ‘Clarity Act’: Federal Stablecoin Floor Nears Reality

Patrick Witt, executive director of the President’s Council of Advisors for Digital Assets and the White House’s chief crypto adviser, said on Monday that negotiations on the Digital Asset Market Clarity Act have advanced well beyond the stablecoin yield impasse, with multiple outstanding issues being resolved in parallel behind the scenes.

The signal is the clearest indication yet that a federal regulatory floor for payment stablecoins is within legislative reach.

The question isn’t whether the White House wants this bill passed. It clearly does. The question is whether the Senate Banking Committee can hold a markup hearing before the political window closes, analysts warn that missing a May 2026 advancement deadline risks pushing the entire legislative effort past the November midterms.

- Yield Compromise Holding: A bipartisan deal on stablecoin yield – the primary bank-industry flashpoint – is intact, per Witt, who called it a “must-have” precondition for tackling remaining issues.

- Secondary Issues Closing: DeFi illicit finance protections and restrictions on senior government officials profiting from crypto – a Democratic demand targeting President Trump – are both reportedly near resolution.

- Senate Banking Committee Markup Pending: The Clarity Act requires a committee markup before reaching a full Senate floor vote; that hearing was derailed in January 2026 by bank lobbyist objections and has not been rescheduled.

- Federal Reserve Role Contested: A core negotiating tension remains over whether the Fed retains veto power over state-chartered stablecoin issuers – a provision that would materially affect whether issuers like Circle’s USDC gain direct access to federal payment infrastructure.

- Banking Sector Split: The American Bankers Association responded critically Monday to a White House economic report downplaying yield-bearing stablecoin risks to bank deposits – signaling the industry remains internally divided.

- Midterm Clock Running: Sen. Bill Hagerty and Sen. Cynthia Lummis have flagged a late-April markup target; failure risks post-election delay until 2027.

- Watch: Updated stablecoin yield legislative text expected after Easter recess following final industry-bank talks.

Discover: Best Crypto Presales to Watch Amid Stablecoin Regulatory Clarity

What the Clarity Act Federal Floor Actually Changes for Stablecoin Issuers and Market Infrastructure

The core structural shift embedded in the Clarity Act is the establishment of a federal minimum standard , a regulatory floor, that all payment stablecoin issuers must meet regardless of their state charter status.

Before this framework, issuers operated under a patchwork of state money transmission licenses with no unified federal reserve, capital, or transparency requirements.

That ambiguity has been the primary barrier preventing institutional adoption at scale for settlement and cash management.

Under the proposed framework, issuers would be required to maintain 1:1 reserve backing with high-quality liquid assets, meet federal safety-and-soundness standards, and comply with AML and illicit finance controls, including, critically, new DeFi-specific protections that Witt confirmed are still being finalized.

— JackTheRippler © (@RippleXrpie) April 13, 2026

HUGE NEWS:

HUGE NEWS:

The CLARITY ACT will be presented to the Banking Committee THIS WEEK, confirmed by Senator Bill Hagerty.

Regulatory clarity is coming in 2026! pic.twitter.com/d9yl8CGiVY

The DeFi provisions are not cosmetic. They determine whether decentralized protocols that route stablecoin liquidity face issuer-level compliance obligations or are treated as distinct actors, a distinction that shapes the entire secondary market architecture for USDC and its competitors.

The Federal Reserve dimension carries the highest institutional stakes.

Negotiations are reportedly centering on whether the Fed retains override authority over state-regulated issuers, a mechanism that would function as a systemic risk check but would also effectively give the central bank leverage over which issuers can access federal payment rails.

For Circle, that access would reduce counterparty risk at the settlement layer and open institutional corridors currently closed to non-bank entities.

Deputy Treasury Secretary Scott Bessent has publicly urged rapid spring 2026 passage, citing midterm urgency, a signal that Treasury views this not as incremental cleanup but as foundational market infrastructure legislation.

The stablecoin yield compromise, reached between key senators from both parties, addresses what banks had framed as an existential threat to their deposit base.

Bank of America CEO Brian Moynihan warned in February that trillions in deposits could migrate to yield-bearing stablecoins if Congress authorized interest-like returns.

Witt proposed language at ETHDenver in February limiting stablecoin rewards to “activities or transactions” rather than balances, with violations penalized up to $500,000 per day, a formulation that appears to have formed the basis of the current bipartisan compromise.

This dynamic mirrors what’s unfolding in Japan’s reclassification of crypto as a financial instrument, where the core legislative tension also centered on where digital assets fit within existing banking and payment system hierarchies.

Discover: Best Crypto Exchanges for Stablecoin Trading and Settlement

The post White House Signals Breakthrough on ‘Clarity Act’: Federal Stablecoin Floor Nears Reality appeared first on Cryptonews.

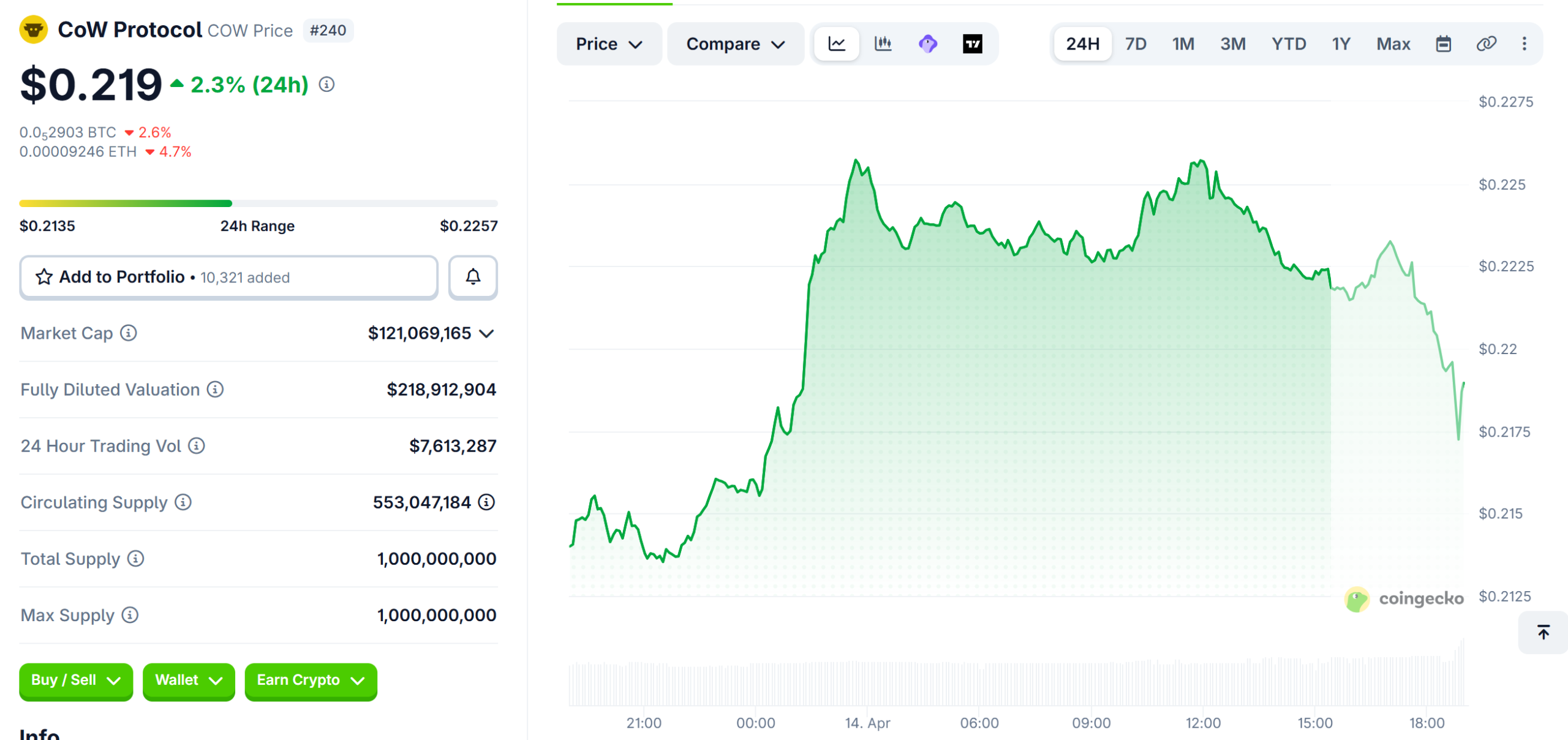

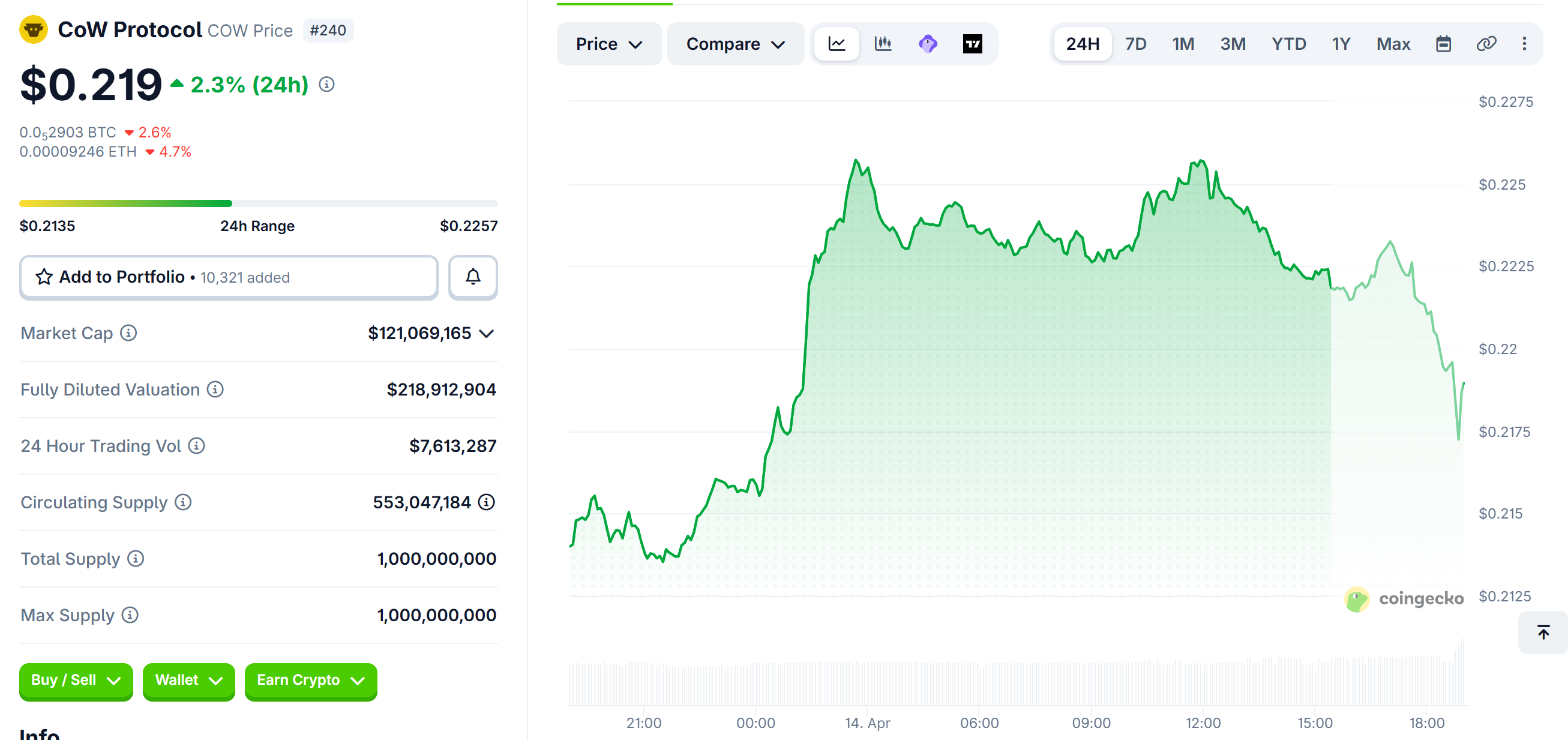

CoW Swap has warned users to stay away from its frontend at swap.cow.fi after Web3 security firm Blockaid detected malicious activity on the cow.fi domain.

The team is actively investigating the issue, which may involve a compromise that tricks users into signing harmful transactions designed to drain their wallets.

What Happened to CoW Swap’s Frontend

Blockaid, which provides transaction screening for major wallets and DeFi platforms, flagged the cow.fi domain after its dApp scanning engine identified suspicious behavior.

CoW Swap confirmed the alert shortly after, urging users to avoid interacting with the site entirely while the investigation continues.

“We are currently experiencing an issue with the CoW Swap frontend (https://swap.cow.fi). While we are investigating, please DO NOT use CoW Swap,” they wrote.

The CoW Protocol (COW) token, which trades at roughly $0.22 with a market cap near $120 million, has not yet seen a significant sell-off in response.

However, the risk to users who interact with the compromised frontend remains high.

Frontend attacks do not target smart contracts directly. Instead, they alter the interface users see, potentially injecting malicious transaction requests that appear legitimate.

Users who sign these transactions may unknowingly grant attackers access to their funds.

How Users Should Protect Themselves

CoW Swap advised all users to disconnect wallets from the platform and review any recent transactions for suspicious approvals.

Revoking token approvals through tools like Revoke.cash or Etherscan’s approval checker is a critical first step.

This is not the first time CoW Swap has faced security challenges. In 2023, an exploiter drained over $180,000 from the protocol’s settlement contract, though user funds were not directly affected in that incident.

Frontend compromises have become an increasingly common attack vector in DeFi. The 2025 Bybit hack, which exploited Safe Wallet’s frontend infrastructure, resulted in $1.5 billion in losses and underscored how even trusted interfaces can become entry points for attackers.

Users should wait for an official all-clear from the CoW Swap team before reconnecting wallets or resuming activity on the platform.

The post CoW Swap Warns Users to Avoid Frontend After Blockaid Flags Malicious Activity appeared first on BeInCrypto.

Nexo, a digital assets wealth platform for crypto holders, has been named the Official Regional Digital Asset Partner of the Argentina Football Association (AFA), marking a major step in the company’s South American expansion ahead of the 2026 FIFA World Cup.

The AFA x Nexo partnership positions Nexo alongside one of the most celebrated national teams in global football, reinforcing its ambitions in Latin America, where the company has recently strengthened its footprint through the acquisition of local platform Buenbit and the establishment of a regional hub in Buenos Aires.

Federico Ogue, CEO at Buenbit by Nexo, emphasized the alignment between the two organizations: “Argentina’s national team represents the highest level of sporting excellence, built on talent, conviction, and an unrelenting will to win. At Nexo, we share that standard. As we grow our presence in Argentina and across South America, partnering with AFA is a statement of commitment to this region and the clients we serve here.”

Strategic Expansion Meets Global Football Excellence

The agreement was formally unveiled during a high-profile signing ceremony in Buenos Aires, attended by executives, media, and invited guests. The event marks the official start of a collaboration that blends digital finance innovation with elite sports branding on a global stage.

Leandro Petersen, Chief Commercial & Marketing Officer of AFA, highlighted the broader significance of the partnership: “We are excited to announce a new partnership with a strong global reach that aligns with the Argentine Football Association’s international growth strategy, which we have been building in recent years through agreements with leading companies in innovation and technology.”

He also added: “Nexo’s arrival as the Official Digital Assets Partner of the Argentine National Team reflects not only the growth of our brand globally, but also the growing interest of international companies in partnering with Argentine soccer and one of the world’s most prominent national teams.”

Petersen also drew parallels between business and sport performance: “Success in elite sports, just as in business, is based on a clear strategy, discipline, and the ability to perform at the highest level when it matters most.”

The partnership comes at a pivotal time, with Argentina entering the upcoming World Cup cycle as defending champions and competing across North American venues, further amplifying global visibility for both AFA and Nexo.

Discover: The best pre-launch token sales

Nexo Argentina Partnership is not the Only one this World Cup

Far from a single sponsorship, the 2026 tournament is emerging as one of the most crypto-integrated sporting events in history. FIFA has already signed a landmark deal with blockchain-powered prediction platform ADI Predictstreet as an official partner, enabling fans worldwide to engage with matches through data-driven prediction markets built on crypto.

Introducing @Predictstreet — ADI Chain (@ADIChain_) April 2, 2026

The Official Prediction Market Partner of the @FIFAWorldCup 2026

More than 5 billion fans will watch the World Cup.

ADI Predictstreet was built to reach every single one of them.

The first consumer-facing ecosystem project on ADI Chain is going… pic.twitter.com/oYJpD2eElv

This follows FIFA’s Web3 push, including the development of its own blockchain ecosystem for digital collectibles and fan engagement.

Even fan access and monetization are being reshaped by blockchain rails. FIFA has experimented with NFT-based ticketing and digital ownership models in the lead-up to 2026, blending collectibles with access rights and creating new commercial layers around the tournament experience.

Want to be at the FIFA World Cup 2026 — FIFA Collect (@FIFACollect) March 9, 2026

?

Here's how to get there with an RTT

1⃣ Sign in/Sign up your FIFA Collect account

2⃣ Browse RTT listings & choose your match

4⃣ Buy or make an offer

5⃣ Be there.

Go to the Marketplace  https://t.co/JtpS3Pz4nn pic.twitter.com/Mxb8WCRhvV

https://t.co/JtpS3Pz4nn pic.twitter.com/Mxb8WCRhvV

Discover: The best crypto to diversify your portfolio with

The post Nexo Named Official Digital Asset Partner of Argentina Ahead of 2026 FIFA World Cup appeared first on Cryptonews.

Foundry Digital’s newly launched Zcash (ZEC) mining pool captured approximately 29% of the network’s total hashrate within a month of going live, a rate of consolidation that rivals what ViaBTC, the prior dominant pool, took considerably longer to establish.

The pool went public in April 2026 after Foundry announced the initiative on March 11, onboarding institutional miners ahead of the public launch.

The speed of that hashrate capture is the signal worth examining. Foundry didn’t inch into Zcash mining, it arrived and immediately held roughly the same share that ViaBTC had built as the incumbent leader, sitting at around 30% of network hashrate before Foundry’s entry.

- Hashrate Capture: Foundry’s Zcash pool seized ~29% of network hashrate within one month of launch, per company data and the new Zcashinfo.com block explorer.

- Zcash Network Context: Zcash’s total hashrate had risen from 8.1 GSol/s to 13.8 GSol/s since early September 2025 before Foundry’s entry, with ViaBTC previously holding ~30% dominance.

- Pool Structure: The pool uses a PPLNS payout model, distributes rewards via transparent ZEC addresses, enforces KYC/AML checks, and requires no minimum hashrate, a deliberate institutional access design.

- Compliance Infrastructure: Foundry’s pool mirrors the SOC 1 Type 2 and SOC 2 Type 2 compliance framework of Foundry USA Pool, its dominant Bitcoin mining operation.

- Zcashinfo.com Launch: Foundry released a dedicated Zcash block explorer alongside the pool, providing real-time hashrate distribution, pool rankings, and mining difficulty tracking.

- What to Watch: Whether Foundry’s share continues climbing past 30% – the threshold at which centralization risk becomes a live network security debate – is the next data point that matters.

Discover: How sovereign and institutional actors are reshaping proof-of-work network economics

What Does 29% Hashrate Capture in One Month Actually Mean for Zcash Network Security?

A single pool controlling 29% of a PoW network’s hashrate is not inherently dangerous, but it concentrates block production risk in ways that demand monitoring.

At 29%, Foundry cannot unilaterally execute a 51% attack, but it is close enough to the threshold that any further organic growth changes that calculus.

The fact that ViaBTC was already sitting at ~30% before Foundry launched means the network now has two pools each holding roughly three-tenths of total hashrate. That’s a different concentration structure than existed six months ago.

Foundry Zcash Pool is officially live! Since our announcement last month, we've seen rapid hashrate growth reaching ~30% of network hashrate. Institutional miners have been looking for compliant, purpose-built $ZEC infrastructure, and we're proud to deliver it.

Additionally,… pic.twitter.com/GOXyKrqhhH— Foundry (@FoundryServices) April 13, 2026

Foundry CEO Mike Colyer framed the launch as an infrastructure gap play: Zcash has “matured into an institutional-grade asset, but the mining infrastructure supporting it hasn’t kept pace.”

The data supports the premise that Zcash’s hashrate growth from 8.1 GSol/s to 13.8 GSol/s since September 2025 reflects expanding miner interest that the existing pool infrastructure wasn’t built to absorb at an institutional scale.

What Foundry has built operationally is notable for its compliance architecture. The pool’s PPLNS payout model, mandatory KYC/AML checks, SOC 1 and SOC 2 audit equivalency, and 24/7 U.S.-based support aren’t features designed for hobbyist miners.

No minimum hashrate requirement means the access floor is low, but the compliance overhead signals this is targeting miners who need defensible regulatory positioning, the same institutional cohort driving volume on Foundry USA Pool in Bitcoin.

Zooko Wilcox, Zcash founder and now Chief Product Officer at Shielded Labs, directly addressed the centralization angle: “This will spread out the Zcash mining hashpower from its current concentration in a single pool, and hopefully it will bring in new Zcash miners who trust Foundry to operate a high-quality service.”

That framing treats Foundry’s entry as a decentralization event relative to ViaBTC’s prior dominance. Whether it remains that depends on where Foundry’s share stabilizes. If it climbs past 35%, the narrative flips.

The data shows rapid institutional onboarding. That implies pre-existing demand from miners who were waiting for a compliant U.S.-based option, not that Foundry manufactured the hashrate from scratch.

The post Foundry Captures 29% of Zcash Hashrate Within a Month of Pool Launch appeared first on Cryptonews.

Bitget, the world’s largest Universal Exchange (UEX), today launched CFD Copy Trading, expanding access to traditional financial markets and allowing users to automatically follow professional traders across forex, commodities, and indices directly from the Bitget platform.

The launch follows strong growth in Bitget’s CFD business, which recently surpassed $6 billion in single-day trading volume as users responded to heightened volatility across global markets. Recent price movements in gold, oil, major currency pairs, and equity indices have drawn increased participation from crypto-native traders seeking broader market exposure as macro conditions become more interconnected.

While that growth has largely been driven by experienced traders able to react quickly to macroeconomic signals, access remains uneven for everyday users who do not actively track market developments or trade across multiple asset classes. CFD Copy Trading is designed to reduce that barrier by allowing users to mirror the strategies of top-performing traders starting from 50 USDT, using the same copy trading framework already familiar across Bitget’s futures and spot products.

“More users are paying attention to macro movements because the opportunity set has widened beyond crypto alone,” said Gracy Chen, CEO of Bitget. “What matters now is making that access practical. Copy trading lowers the execution barrier for users who want exposure to global markets without needing to build that expertise from scratch.”

The product is built on Bitget’s MT5-integrated CFD infrastructure and introduces several mechanisms designed to improve execution and transparency for both traders and followers. MT5 account creation and withdrawal processing are completed in under three seconds through a fully automated backend process, reducing friction at onboarding and settlement. Bitget also applies a High-Water Mark profit-sharing model, under which expert traders only receive profit share when a follower’s account reaches a new net profit high after fully recovering prior losses. This means traders are rewarded only when followers have reached net profitability, aligning incentives more directly across both sides of the strategy.

Performance data including ROI, follower count, and profit-sharing figures refresh hourly, replacing the delayed reporting model still common across much of the market. Profit-sharing settlements are processed daily, and eligible traders can receive up to 30% in profit share, with VIP structures also allowing restricted access portfolios for invited followers.

The launch also expands Bitget’s broader Universal Exchange strategy, which is built around giving users access to multiple asset classes under a single account structure. Through USDT-based margin, users can move between crypto, commodities, forex, and indices without transferring funds between external brokers or converting capital across separate platforms. For crypto users, CFD Copy Trading creates a simpler entry point into traditional financial markets. For experienced MT5 and forex traders, it also creates a new entry point into Bitget’s broader ecosystem, where traditional and digital asset markets increasingly overlap within a single trading environment.

To know more about CFD copy trading, please visit here.

About Bitget

Bitget is the world’s largest Universal Exchange (UEX), serving over 125 million users and offering access to over 2M crypto tokens, 100+ tokenized stocks, ETFs, commodities, FX, and precious metals such as gold. The ecosystem is committed to helping users trade smarter with its AI agent, which co-pilots trade execution. Bitget is driving crypto adoption through strategic partnerships with LALIGA and MotoGP™. Aligned with its global impact strategy, Bitget has joined hands with UNICEF to support blockchain education for 1.1 million people by 2027. Bitget currently leads in the tokenized TradFi market, providing the industry’s lowest fees and highest liquidity across 150 regions worldwide.

For more information, visit: Website | Twitter | Telegram | LinkedIn | Discord

Risk Warning: Digital asset prices are subject to fluctuation and may experience significant volatility. Investors are advised to only allocate funds they can afford to lose. The value of any investment may be impacted, and there is a possibility that financial objectives may not be met, nor the principal investment recovered. Independent financial advice should always be sought, and personal financial experience and standing carefully considered. Past performance is not a reliable indicator of future results. Bitget accepts no liability for any potential losses incurred. Nothing contained herein should be construed as financial advice. For further information, please refer to our Terms of Use.

The post Bitget Launches CFD Copy Trading as Demand for Cross-Market Exposure Accelerates appeared first on BeInCrypto.

Crypto World

Nvidia Stock Extends Winning Streak Ahead Of Two Key Reports| Investor’s Business Daily

Nvidia (NVDA) extended gains Tuesday even as the broader stock market fluctuated following the U.S. imposition of a blockade on ships in the Strait of Hormuz after peace talks between the U.S. and Iran failed. Shares are on track for matching their longest string of advances made on Nov. 14, 2023, when they marked 10 consecutive wins. Is Nvidia stock…

Gate, one of the leading global digital asset exchanges, today announced a significant milestone in its ongoing strategic partnership with FC Internazionale Milano. Starting from April 2026, the Gate brand identity has officially debuted as the Official Sleeve Partner for the Inter U23 team, further solidifying the bond between the two organizations and their shared commitment to innovation and future growth by supporting the next generation of professional football talent.

Expanding a Legacy: From 2024 to the Future

The journey between Gate and Inter began in 2024, when Gate first joined the Nerazzurri family as a key partner. Over the past two years, this collaboration has flourished through shared values of excellence and community engagement. Building on this solid foundation, Gate expanded its sponsorship in 2026 to include the newly established Inter U23 squad, marking a new chapter in this high-profile sports-tech alliance.

Empowering the Next Generation

The Inter U23 team serves as a vital bridge between the youth academy and the professional elite level. By securing the sleeve sponsorship at this strategic juncture in 2026, Gate underscores its dedication to “Growth and Potential”—values that are central to both the crypto industry and professional football. The Gate logo will accompany these high-potential young players on the pitch as they embark on new chapters in their professional careers.

Dr. Han, the founder and CEO of Gate, said:

Gate has consistently been committed to empowering users worldwide through the power of technology and innovation. Since our partnership began in 2024, we have witnessed the incredible spirit and resilience of Inter. Supporting the U23s is a natural progression for Gate, as we believe in empowering the next generation of talent. Debuting on the sleeve symbolizes our passion for nurturing future stars and growing alongside the club.”

About Gate

Gate, founded in 2013 by Dr. Han, is one of the world’s earliest cryptocurrency exchanges. The platform serves over 51 million users with 4,500+ digital assets and pioneered the industry’s first 100% proof-of-reserves. Beyond core trading services, Gate’s ecosystem includes Gate Wallet, Gate Ventures, and other innovative solutions.

For more information, please visit: Website | X | Telegram | LinkedIn| Instagram | YouTube

Disclaimer:

This content does not constitute an offer, solicitation, or recommendation. You should always seek independent professional advice before making investment decisions. Note that Gate may restrict or prohibit certain services in specific jurisdictions. For more information, please read the User Agreement.

The post Gate Deepens Partnership with Inter , Officially Becoming Sleeve Sponsor for Inter U23 appeared first on BeInCrypto.

- The US DOJ opens claims process for OneCoin victims.

- Over $40 million in seized funds are available for distribution.

- Deadline for filing claims set for June 30, 2026.

The US Department of Justice has launched a formal compensation claims portal for victims of the OneCoin scheme, marking a new phase in one of the largest crypto-related fraud cases ever uncovered.

The move comes years after the collapse of OneCoin, a project that attracted millions of investors worldwide with promises of high returns from a digital currency that was later exposed as fraudulent.

Many people from different countries were left with significant financial losses after the scheme unravelled, leading to extensive criminal investigations and asset seizures across multiple jurisdictions.

Now, with a dedicated compensation process in place, the focus has shifted toward distributing recovered funds back to those who were harmed.

The scale of the OneCoin fraud and how it unfolded

OneCoin operated between 2014 and 2019, presenting itself as a revolutionary cryptocurrency investment opportunity.

It was heavily promoted through aggressive marketing campaigns and a wide network of recruiters who encouraged individuals to buy into what was described as a fast-growing digital asset.

However, authorities later determined that OneCoin did not function like a real cryptocurrency. Instead of operating on a transparent blockchain network, it relied on centralised systems controlled by the people behind the project.

Despite this, it continued to attract investors globally, but it ultimately crashed in 2019, leading to losses believed to reach into the billions of dollars.

Estimates of total losses vary, but the figure is commonly placed at around $4 billion, with some assessments suggesting even higher exposure when accounting for global investor participation.

The scale of the fraud made it one of the most significant financial fraud investigations tied to the digital asset space.

Over time, law enforcement agencies were able to trace and seize assets linked to individuals involved in the scheme, and these recovered funds form the basis of the compensation program announced by the US Department of Justice.

How the compensation claims process will work

The newly launched claims portal is designed to allow victims of OneCoin to formally submit requests for compensation.

The process is structured as a remission program, which means that money recovered from seized assets will be redistributed to eligible victims based on verified losses.

To qualify, individuals must show that they invested in OneCoin during the operational period between 2014 and 2019. They must also demonstrate a net financial loss.

This means that any funds previously withdrawn or recovered will be deducted from the total amount claimed to determine eligibility.

Notably, the total pool of available funds for distribution currently stands at over $40 million.

While this is a significant amount, it represents only a small fraction of the overall losses suffered by investors globally.

As a result, any payouts are expected to be partial and distributed proportionally among approved claimants.

The deadline for submitting claims has been set for June 30, 2026. After this date, no new applications will be accepted, and the distribution process will move forward based on verified submissions.

For many affected investors, the opening of a claims process offers a long-awaited opportunity to recover at least part of their lost funds.

Although the available compensation is limited compared to total losses, it represents a formal acknowledgement of harm and an effort to return seized assets to their rightful owners.

Most XRP Holders Are Missing the Real Opportunity

Anand Rathi Share & Stock Brokers Q4 Results: Profit more than doubles to Rs 41 crore despite market crash

Anthropic Mythos reveals ‘more vulnerabilities’ for cyberattacks

-

Politics4 days ago

Politics4 days agoUS brings back mandatory military draft registration

-

Sports4 days ago

Sports4 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Veronica Beard

-

Tech7 days ago

Tech7 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Politics4 days ago

Politics4 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Politics2 days ago

Politics2 days agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World5 days ago

Crypto World5 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business4 days ago

Business4 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Crypto World23 hours ago

Crypto World23 hours agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Crypto World19 hours ago

Crypto World19 hours agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

Crypto World6 days ago

Crypto World6 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

NewsBeat2 days ago

NewsBeat2 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Business4 days ago

Business4 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Business3 days ago

Business3 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Politics4 days ago

Politics4 days agoLBC Presenter Mocks Trump Over Iran War Failures

-

Crypto World4 days ago

Crypto World4 days agoFederal judge blocks Arizona from bringing criminal charges against Kalshi

-

Tech5 days ago

Tech5 days agoA version of Windows 10 released a decade ago is now eligible for additional security patches

-

NewsBeat2 days ago

NewsBeat2 days agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Business4 days ago

Business4 days agoIMF retains floor for precautionary balances at SDR 20 billion

-

NewsBeat8 hours ago

NewsBeat8 hours agoTrump and Pope Leo: Behind their disagreement over Iran war

You must be logged in to post a comment Login