Crypto World

Palantir (PLTR) Stock Under Scrutiny as UK Lawmakers Demand NHS Contract Exit

Key Takeaways

- British parliamentary report identifies Palantir dependency as an “unacceptable point of weakness” for national security

- Lawmakers highlight the £330 million ($444 million) NHS data platform agreement as creating dangerous vendor dependency

- Report references Peter Thiel’s political connections and Palantir’s defense sector involvement as incompatible with British principles

- Parliamentary committee recommends activating the 2027 contract exit provision and pursuing domestic alternatives

- Palantir’s British leadership dismissed cancellation calls as “frankly irresponsible”

British lawmakers have issued a sharp rebuke of Palantir’s expanding presence in UK government operations, expressing alarm that reliance on the American data analytics company creates vulnerabilities around sensitive public information.

Palantir Technologies Inc., PLTR

On Wednesday, the Commons Science, Innovation and Technology Committee released a comprehensive 70-page assessment that highlighted Palantir as a concerning case study of excessive dependence on a limited group of American technology vendors. The assessment characterized this dependency as an “unacceptable point of weakness.”

Shares of Palantir (PLTR) drew attention after the parliamentary report emerged, as market participants monitored potential implications from mounting political opposition in a strategically important overseas market.

Central to the committee’s concerns is Palantir’s seven-year National Health Service arrangement valued at £330 million. Secured in 2023, the agreement aims to consolidate healthcare information from throughout the NHS into a unified system enabling medical professionals to make more informed, timely decisions.

According to NHS officials, the partnership has produced “huge benefits for patients,” including accelerated cancer identification and the treatment of thousands of additional patients monthly.

Lawmakers Push for 2027 Contract Termination

Despite these reported advantages, the parliamentary committee is pressing the government to invoke a contractual exit provision available in 2027. The recommendation includes transitioning to a British-based solution or developing an internal capability.

Beyond technical considerations, MPs expressed concerns about aspects of Palantir’s profile and leadership. The assessment referenced co-founder Peter Thiel’s relationships with Donald Trump and his previous critiques of public healthcare systems. Additionally, the report noted Palantir’s contracts providing technology to American defense and immigration enforcement agencies.

The committee concluded these factors constitute a “clear mismatch with UK values” and cautioned that Britain’s digital modernization objectives could be “derailed at any time by a decision taken outside our shores.”

Committee chair Dame Chi Onwurah stated the UK faces serious exposure and advocated for technological independence in essential public service domains.

Company Defends NHS Partnership

Louis Mosley, Palantir’s UK chief executive, responded swiftly to the criticism. In a BBC radio interview, he noted the committee itself had recognized the NHS contract’s positive performance, making termination calls “frankly irresponsible.”

Mosley emphasized that Palantir secured the agreement through a transparent, competitive procurement procedure, and that NHS data governance remains entirely with the health service.

Foxglove, a British advocacy organization that has actively opposed Palantir’s NHS participation, praised the parliamentary findings and urged complete contract termination.

The committee’s assessment also criticized broader government digital initiatives, characterizing the administration’s £45 billion annual savings target through digitalization as “worryingly optimistic.”

Additional recommendations included designating a cabinet-level minister specifically responsible for overseeing digital transformation efforts.

The UK government’s Department of Health and Social Care had not issued a statement in response to the report at press time.

Ripple keeps winning. A five-second cross-border Treasury settlement with JPMorgan and Mastercard, ten major deals this year, an IPO the chief executive keeps hinting at. XRP keeps trading near a dollar and change. The gap between the company and the token is the entire story.

Summary

- Ripple’s institutional wins are real, but they do not always create XRP demand.

- The JPMorgan Treasury settlement used RLUSD, not XRP, as the cash leg.

- Ripple equity and XRP remain separate assets with different value drivers.

- XRP needs utility to become token demand before the price can break its range.

In June 2026, Ripple completed something that should have been a milestone for its token. Working with JPMorgan, Mastercard, and Ondo Finance, it settled the redemption of a tokenized United States Treasury fund across borders and across banks on the XRP Ledger, and the blockchain leg finalized in under five seconds, against the one to three business days the same transaction takes on traditional rails.

The participants were real, the speed was real, and the headline wrote itself: Wall Street is settling Treasuries on Ripple’s blockchain. And yet XRP, the token, barely moved, and where it did move it often fell.

The asset spent most of 2026 trading in a narrow band near a dollar and change, while news exactly like this piled up around it. That disconnect, a company stacking institutional wins while its token goes nowhere, is one of the most instructive puzzles in crypto.

The answer is more revealing than either the bulls or the bears usually admit.

This piece takes the puzzle apart. It covers the settlement that did not move the token and the detail the headlines skipped, the structural separation between Ripple the company and XRP the asset, the supply overhang that quietly weighs on the price, the genuine catalysts XRP does have, and why those catalysts keep getting priced as maybes.

The aim is to explain, without spin in either direction, why good news for Ripple so often fails to become good news for XRP, and what would actually have to change for the token to break out of its range.

The win that did not move the token

The June settlement was not a small thing. For years the tokenization story has been mostly demonstrations on private chains, so a live, cross-border, cross-bank redemption of a real tokenized Treasury on a public ledger, with JPMorgan’s settlement platform delivering dollars to Ripple’s bank in Singapore in the same flow, is a credibility win for the XRP Ledger.

It connected one of the largest settlement institutions in the world to a public blockchain, outside normal banking hours, in seconds. As a proof that the rails work, it was about as strong as these announcements get.

That is the settlement broken down in detail. The transaction matters because it shows that regulated institutions are willing to test the XRP Ledger for real-world asset settlement.

The market’s reaction told a different story. XRP did not rally on the news in any durable way, and on the day of an earlier version of the same pilot it actually fell almost 5%, erasing a brief pop.

This was not an anomaly. It fit a pattern that has defined XRP through 2026, where Ripple partnership headlines arrive, the token spikes briefly or not at all, and then drifts back down.

Traders have a weary phrase for it: every Ripple deal seems to be followed by the XRP price dropping. When a genuinely impressive institutional milestone produces a shrug or a selloff, the explanation is rarely that the milestone was fake.

It is usually that the milestone has less to do with the token than the headline implies.

The detail the headlines skipped: XRP was barely in the trade

Here is the part that reframes everything. In that landmark Treasury settlement, XRP the asset did almost no work.

The bridging and settlement were done with RLUSD, Ripple’s dollar-pegged stablecoin, not with XRP. The tokenized Treasury, Ondo’s product, was redeemed by exchanging it for RLUSD, and XRP appeared only as the tiny network fee that every XRP Ledger transaction pays.

Those fees are fractions of a cent on a trade moving far larger sums. The asset that the headlines attached to the news was, in the actual mechanics, a bystander.

This is not an accident or an oversight; it is by design, and the reason matters. Institutional settlement needs a stable, audited, dollar-denominated instrument, because no treasurer is going to settle a Treasury redemption in an asset that can swing 10% in a day.

RLUSD is built for exactly that role: dollar-pegged, backed by cash and Treasuries, and regulated. XRP’s price volatility rules it out of the settlement leg by definition, which is why Ripple deliberately built the product to use RLUSD as the cash leg.

That is the RLUSD that did the settlement work. It is useful precisely because it is not supposed to move.

So when Ripple wins an institutional settlement deal, the direct beneficiary is the XRP Ledger as infrastructure and RLUSD as the settlement token, while XRP the asset captures only the minuscule fee. The headline says XRP.

The transaction says RLUSD. The price reflects the transaction.

Ripple the company versus XRP the token

Step back and the deeper issue comes into focus: Ripple the company and XRP the token are not the same thing, and the market has started pricing them separately.

Ripple is a private company that sells software and payment services, signs deals with banks, holds a large treasury, and may one day go public. XRP is a cryptocurrency that trades on its own supply and demand.

Owning XRP does not make you a shareholder in Ripple, does not entitle you to its profits, and does not give you a claim on its corporate success. The two are linked by association and by Ripple’s large XRP holdings, but they are distinct assets with distinct drivers.

This is why the IPO chatter, which intensified after chief executive Brad Garlinghouse called the moment real ahead of a company event, is more complicated than it sounds for token holders. An initial public offering would let people buy Ripple equity, and it would reward Ripple’s shareholders.

It would not, by itself, pay anything to XRP holders, who own a separate asset.

That is the IPO question for token holders. The most realistic answer is that any benefit would be indirect unless Ripple deliberately created a program for XRP holders, and no such program exists.

Garlinghouse’s strongest argument is an indirect one, and it has genuine merit: because Ripple remains the largest single holder of XRP, the company has a built-in incentive to drive the token’s value, and its partnerships and integrations do plausibly increase XRP’s long-term utility and demand.

That alignment is real. But it is indirect, a rising tide the company hopes to create, not a dividend it pays, and a holder who treats a possible IPO as a direct reward is counting on a maybe attached to a maybe.

The market’s persistent refusal to rally Ripple’s wins into XRP’s price is, in effect, the market enforcing this distinction.

The supply overhang nobody wants to discuss

There is also a more mechanical weight on the token, and it sits on the supply side.

Ripple holds an enormous quantity of XRP in escrow, a locked reserve it releases on a schedule, and that release is a structural source of new supply hitting the market. Each month Ripple can release up to one billion XRP from escrow, then re-locks most of it, but the net amount that actually reaches circulation still runs into the hundreds of millions of tokens monthly.

That is a steady stream of potential selling pressure built into the token’s design.

The significance is that it sets a high bar for any bullish supply story. Some XRP optimists point to the tiny fees burned on each ledger transaction as a deflationary force, but at current transaction volumes the burn is a rounding error next to the escrow releases.

For fee burn to tighten supply in any meaningful way, on-chain activity would have to grow by orders of magnitude, enough to offset hundreds of millions of newly released tokens every month. A single institutional settlement test does not move that needle.

So even when Ripple announces real adoption, a holder has to weigh it against a supply schedule that keeps running on its long-set path. The demand side has to climb a down escalator, and one impressive pilot does not change the speed of the steps.

What XRP actually has going for it

None of this means XRP is a lost cause, and a fair account has to give the bull case its due, because the token’s position has improved in ways that are concrete.

The years-long legal cloud has lifted. The Securities and Exchange Commission’s case against Ripple ended in 2025 with the courts’ finding that XRP sold on public exchanges was not a security, and a later joint classification treated XRP as a digital commodity, giving the token more regulatory clarity than almost any other asset of its size.

That clarity is real and durable, even if it rests partly on interpretation rather than statute.

The institutional door has also opened. Spot XRP exchange-traded funds launched in late 2025 from a roster of established issuers and pulled in well over a billion dollars in assets, with major institutions appearing among the disclosed holders.

That is where XRP demand is actually coming from. ETF flows are not enough by themselves to erase the supply overhang, but they are measurable demand in a way that partnership headlines are not.

Ripple’s stablecoin, RLUSD, crossed a billion dollars in market value in under a year and is being woven into real settlement and card products. Ripple has also kept expanding its payments footprint, including a Bitso partnership around a regulated MXN-backed stablecoin on XRPL and a Flutterwave investment aimed at expanding RLUSD settlement across African payment corridors.

Those are not trivial supports. They show Ripple pushing both sides of its strategy: the ledger as institutional settlement infrastructure and stablecoins as the cash leg that enterprises actually want to use.

The single biggest potential catalyst is legislative. If the CLARITY Act passes and writes XRP’s digital-commodity status into federal law, analysts have projected several billion dollars of additional XRP ETF inflows.

That is the catalyst that could codify XRP’s status. It is the one event that could turn today’s regulatory interpretation into statutory certainty.

These are the ingredients of a genuine bull case, and they explain why XRP has held a floor rather than collapsing, even as it refuses to break out.

Why the catalysts keep getting priced as maybes

So the puzzle resolves into a simpler observation: XRP has real catalysts, but the market keeps pricing them as possibilities instead of facts, and there is a logic to that caution.

A proof-of-concept settlement is priced as a proof of concept until it becomes recurring volume. An ETF is priced on the flows it actually attracts, not the flows it might.

A legislative catalyst is priced on the probability of passage, which for the CLARITY Act has hovered well short of certainty as the bill grinds through the Senate. Each of these is a maybe, and a token sitting on a stack of maybes trades like a token sitting on a stack of maybes: range-bound, reactive, and quick to sell the news.

The pattern of selling Ripple’s wins is the market expressing exactly this. When XRP spiked after its legal victory in 2025, long-term holders used the burst of volume to sell, and the token settled back into its range.

Every subsequent partnership has met a version of the same response, because the partnerships, however real, have not yet produced measurable, sustained demand for the token itself.

The market is not being irrational. It is distinguishing between infrastructure adoption, which benefits Ripple and the ledger, and token demand, which is what actually moves XRP, and it is waiting for proof that the first turns into the second.

What the chart has been saying all year

If you want a blunt summary of everything above, look at what XRP’s price actually did around its biggest catalysts, because the chart has been telling the story in plain language.

When Ripple’s long legal fight with the Securities and Exchange Commission finally ended in 2025, XRP spiked hard, touching levels far above where it trades now, and then it faded. Long-term holders used the surge of volume and attention to sell into strength, and the token drifted back down through the rest of the year and settled into the narrow range it has occupied for months.

Each subsequent institutional headline produced a smaller version of the same shape: a brief pop, a fade, a return to the range. The 200-day moving average, a common gauge of the longer trend, has sat well above the price for much of the year, which is a technical way of saying the market has been in a patient holding pattern, neither convinced enough to break out nor scared enough to break down.

A second signal is easy to overlook because it points the other way. While Ripple was landing marquee partnerships, the payments company MoneyGram, once one of Ripple’s most-cited real-world users, moved its on-chain settlement work toward a rival blockchain.

One defection does not undo a year of deals, and the strategic damage may be small, but it punctures the simplest version of the bull narrative, the one where every institution that touches Ripple stays forever and compounds XRP demand.

Adoption is not monotonic. Partners arrive and partners leave, and the network effect that XRP optimists count on is more contested than the announcement cadence suggests.

The chart reflects this ambivalence honestly: a market that has seen real progress and real setbacks, and has priced the token as a thing that might work out, with the proof still pending.

The lesson in the price action is the same lesson the mechanics teach. Markets are forward-looking, and they will pay up in advance for catalysts they believe will convert into demand.

XRP’s refusal to sustain its rallies is the market saying, repeatedly, that it does not yet see the conversion, that the partnerships and pilots have not become the recurring, token-level demand that would justify a rerating.

That is not a permanent verdict. It is a standing challenge, and the chart will be the first place the answer shows up, long before any press release confirms it.

The bigger pattern: when the network wins and the token waits

XRP’s predicament is not unique, and seeing it as one case of a broader pattern makes the whole situation less mysterious.

Across crypto, there is a recurring gap between the success of a network and the price of the token attached to it. A blockchain can attract real usage, real institutions, and real volume while its native token languishes, because adoption of the infrastructure and demand for the token are two different things that only sometimes move together.

A network captures value for its token when using the network requires buying, holding, or burning that token in volume large enough to matter against its supply. When the network can be used without much of the token changing hands, the usage and the price decouple, and the token becomes a spectator to its own success.

XRP sits squarely in that trap. The XRP Ledger is being adopted for serious settlement work, but those settlements lean on RLUSD as the cash leg and use only a sliver of XRP as a fee.

So the network’s growth does not pull much demand through to the token. This is the same dynamic that has frustrated holders of other infrastructure tokens whose chains saw heavy use that never translated into proportional token demand.

The token is not useless; it secures the ledger, pays the fees, and provides liquidity. But the volume of XRP that the network’s growth actually requires is small relative to the token’s large and steadily expanding supply, and that imbalance is the core of the disappointment.

The market is not failing to notice Ripple’s progress. It is noticing, correctly, that the progress runs largely through rails that do not require much XRP.

Understanding this reframes what a holder is really betting on. To own XRP in expectation of price appreciation is to bet not merely that Ripple succeeds, but that Ripple’s success comes to require XRP itself in growing quantities, through settlement volume, ecosystem use, and demand that finally outpaces the escrow supply.

That is a more specific and more demanding bet than simply believing in the company, and it is the bet the market keeps declining to front-run.

The network can keep winning for years while the token waits, and the waiting ends only when usage and token demand finally converge. Until they do, the gap that has defined XRP through 2026 is less a puzzle than a predictable feature of how value accrues, or fails to accrue, to a token whose network can succeed without it.

What would actually break the range

If you want to know when XRP might finally move, the framework above tells you where to look, and it is not the next partnership headline.

The thing that breaks the range is the conversion of utility into token demand: settlement volume large enough that fees and ecosystem use begin to matter against the escrow supply, ETF flows that compound instead of trickle, and a regulatory catalyst like the CLARITY Act actually crossing the line and pulling institutional money off the sidelines.

Those forces aligning, not any one of them alone, is the strongest version of the XRP thesis.

Until then, the disconnect is likely to persist, and understanding why is the most valuable thing a holder can take from the past year. Ripple is winning, genuinely and repeatedly, in the institutional arena it has targeted for a decade.

But Ripple’s wins flow first to Ripple the company, to the XRP Ledger as a piece of infrastructure, and to RLUSD as a settlement instrument, and only indirectly, slowly, and conditionally to XRP the token.

A holder who watches the partnerships and wonders why the price will not follow has been watching the wrong variable. The variable that matters is whether all that institutional adoption ever turns into durable demand for XRP itself, and so far, the market has decided it has not seen enough proof.

The deal with JPMorgan was a milestone. It was just a milestone for the ledger, not yet for the coin.

Frequently asked questions

What did Ripple and JPMorgan actually do?

Ripple, JPMorgan, Mastercard, and Ondo Finance completed the first cross-border, cross-bank redemption of a tokenized United States Treasury fund on the XRP Ledger. Ondo’s tokenized Treasury product was redeemed on the ledger while Mastercard’s network and JPMorgan’s settlement platform delivered dollars to Ripple’s bank in Singapore, with the blockchain leg settling in under five seconds versus one to three business days on traditional rails. It is a real milestone for tokenized settlement and for the XRP Ledger as infrastructure.

Why did XRP not go up after the JPMorgan deal?

Because XRP the asset was barely involved in the transaction. The settlement used RLUSD, Ripple’s dollar-pegged stablecoin, as the cash leg, while XRP appeared only as the tiny network fee. Institutional settlement needs a stable, audited dollar instrument, and XRP’s price volatility rules it out of that role by design. So the deal benefited the XRP Ledger and RLUSD far more than XRP, which is why the token did not rally and, on an earlier version of the pilot, actually fell.

Is XRP the same as owning a stake in Ripple?

No. Ripple is a private company, and XRP is a separate cryptocurrency. Owning XRP does not make you a Ripple shareholder, does not entitle you to its profits, and would not give you a claim in a Ripple IPO. The two are linked because Ripple is the largest holder of XRP and its business can increase the token’s utility over time, but that benefit is indirect. A Ripple IPO would reward Ripple’s equity holders, not XRP holders directly.

Why is XRP stuck in a range?

A mix of supply and demand factors. On the supply side, Ripple releases large amounts of XRP from escrow each month, a steady source of selling pressure that small fee burns cannot offset at current volumes. On the demand side, Ripple’s institutional wins have not yet produced sustained demand for the token itself, so the market prices each partnership, ETF, and legislative catalyst as a maybe instead of a confirmed driver, leaving XRP range-bound and quick to sell the news.

What could actually push XRP higher?

The conversion of utility into real token demand. That means settlement volume large enough that ecosystem use begins to matter against the escrow supply, ETF flows that compound instead of merely trickling, and a regulatory catalyst such as the CLARITY Act passing and writing XRP’s digital-commodity status into federal law, which analysts project could draw billions in additional ETF inflows. Those forces aligning together, not any single headline, is the strongest case for a breakout.

Does XRP have a real bull case at all?

Yes. XRP has more regulatory clarity than almost any major token after the SEC case ended and a later classification treated it as a digital commodity. Spot XRP ETFs launched in late 2025 and gathered over a billion dollars, with major institutions among the holders, and RLUSD crossed a billion dollars in market value quickly. The CLARITY Act could codify XRP’s status and unlock further ETF demand. These are genuine supports, which is why XRP has held a floor, even as it waits for adoption to translate into token demand.

This article is information, not investment advice. Prices, partnership details, and corporate and legislative plans change quickly and reflect reporting available as of June 24, 2026. Verify current data with official sources before relying on anything described here.

TLDR

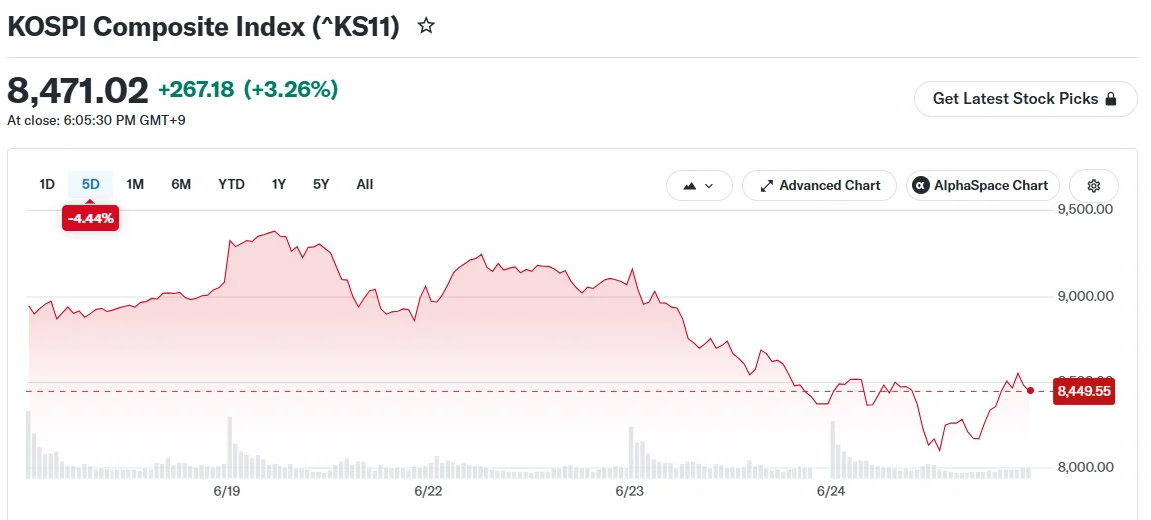

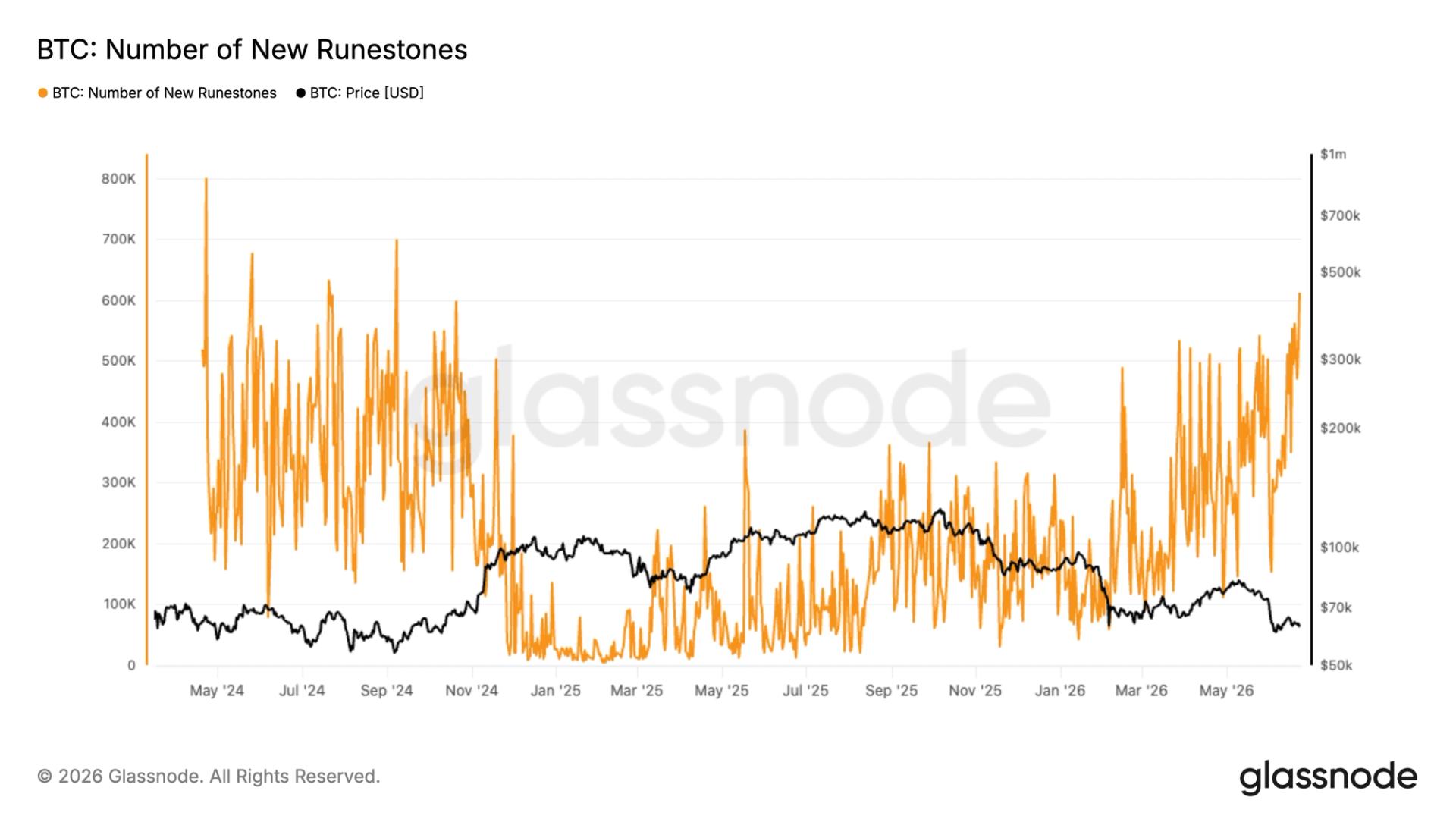

- The KOSPI index rallied between 3.3% and 4.6% during Wednesday’s trading after Tuesday’s devastating 10% decline

- Samsung Electronics jumped as much as 10% following reports of a $5.8 billion share repurchase program

- SK Hynix gained 1% to 3.4% amid news of upcoming American Depositary Receipts listing in the United States

- The previous day’s selloff stemmed from MSCI’s developed market rejection and concerns over AI sector momentum

- The KOSPI still holds its position as the globe’s top-performing major index with nearly 100% gains this year

South Korea’s equity markets delivered an impressive comeback on Wednesday following one of the most severe single-session declines witnessed in years. The KOSPI benchmark surged 3.3% to settle at 8,471 points, after touching highs of 4.6% during intraday trading.

This impressive recovery arrived merely 24 hours after the index experienced a devastating nearly 10% collapse on Tuesday, erasing substantial market capitalization from technology and semiconductor companies.

Samsung Electronics spearheaded Wednesday’s revival, jumping between 7% and 10% throughout the trading day. The dramatic increase followed reports from Yonhap indicating Samsung’s preparation for a share repurchase program valued at approximately 90 trillion won, equivalent to about $5.8 billion.

SK Hynix similarly bounced back, climbing between 1% and 3.4%. News emerged that the memory chip manufacturer was advancing plans to establish American Depositary Receipts listing in the United States, a strategic initiative expected to draw considerable foreign capital.

Both technology giants had experienced devastating losses exceeding 12% during Tuesday’s trading, meaning Wednesday’s rally represented only a partial restoration of lost value.

What Sparked Tuesday’s Market Collapse

Multiple catalysts converged to pummel South Korean equities on Tuesday. The primary trigger was MSCI’s announcement rejecting South Korea’s petition for reclassification to developed market status, a prestigious upgrade the nation had actively pursued.

Uncertainty surrounding the artificial intelligence sector also contributed significantly. Reports indicated SK Hynix might be reconsidering its emphasis on high-bandwidth memory products — critical components for AI processors — potentially pivoting toward conventional memory solutions. This speculation alarmed investors heavily positioned in AI-related semiconductor stocks.

Leveraged exchange-traded products intensified the downturn. As valuations declined, market participants rapidly liquidated these instruments, creating a cascading effect that magnified losses. South Korea’s chief financial regulator publicly acknowledged concerns regarding the recent authorization of such ETFs only weeks earlier.

Regional Markets Show Divergent Performance

Broader Asian equity markets displayed mixed results on Wednesday. Japan’s Nikkei 225 retreated 0.9%. Taiwan’s Taiex declined 2.2%, with semiconductor giant TSMC finishing 4% lower.

Hong Kong’s Hang Seng advanced up to 1%, defying the broader regional weakness.

Market observers highlighted that the recent instability demonstrates how interconnected Asia’s leading exchanges have become with global artificial intelligence sentiment.

Chris Weston, head of research at Pepperstone, noted the technology sector correction partially reflected profit-taking activity as investors reassessed risk-reward dynamics, particularly in heavily concentrated AI and memory chip positions.

Michael Wan, an analyst at MUFG, maintained an optimistic long-term perspective for the industry. He characterized the current volatility as preliminary fluctuations within what he identified as a transformational technological evolution.

Notwithstanding the dramatic two-day volatility, the KOSPI continues to maintain its status as 2026’s best-performing major global equity index, boasting gains approaching 100% year-to-date.

South Korea is folding its token securities work into a broader government push to modernize capital markets, as regulators plan faster settlement, longer trading hours and additional technology upgrades. The Financial Services Commission (FSC) said it has launched a capital market infrastructure review involving multiple agencies and market operators, with tokenized securities to be handled through a separate public-private track before being aligned with the wider reform agenda.

On Tuesday, the FSC announced the start of its capital market infrastructure review meeting, aimed at coordinating reforms across government bodies. The regulator said the token securities agenda will be discussed through a dedicated public-private council and later connected to the larger initiative—an approach that effectively keeps the legislative and technical details for tokenized assets on a separate timetable while still targeting system-level integration.

Key takeaways

- The FSC has begun a cross-government capital market infrastructure review that will coordinate reforms such as faster settlement and expanded trading access.

- Token securities will remain governed through a separate public-private council for now, before being linked to the broader infrastructure roadmap.

- Plans include a roadmap to shorten the securities settlement cycle (targeted for October) and a Korea Securities Depository (KSD) settlement system for over-the-counter trades in unlisted shares and certain fractional investment products by the end of 2026.

- South Korea’s token securities framework was enabled by January amendments recognizing blockchain-based distributed ledgers as securities registries, with a scheduled effective date in February 2027.

- Samsung SDS has been contracted to build a token securities management platform connecting KSD’s existing electronic securities account system with blockchain-based data, with completion targeted for February 2027.

A broader modernization plan, with token securities kept in a parallel track

The FSC’s move places tokenized securities within a wider overhaul of South Korea’s financial market plumbing rather than treating them as a standalone experiment. The regulator said the capital market infrastructure review is intended to coordinate reforms across agencies and market participants, while token securities discussions will continue through a public-private council.

In commentary on the initiative, FSC Vice Chairman Kwon Dae-young said the effort is guided by four policy priorities: trust, shareholder protection, innovation and market access. That framing matters for investors and market operators because tokenized securities regulation is likely to live or die on whether new systems can be reconciled with existing investor-protection and reporting standards.

Settlement speed and KSD systems point to “mainstreaming” tokenization

While token securities have their own legal timeline, the infrastructure review includes operational upgrades that could influence how quickly blockchain-based assets can be used alongside conventional market workflows. According to the FSC, the reform package includes a roadmap to shorten the securities settlement cycle, expected by October. The regulator also described a KSD system for settling over-the-counter (OTC) trades in unlisted shares and fractional investment products, targeted for completion by the end of 2026.

If delivered as scheduled, those milestones would help reduce one of the practical frictions around securities tokenization: integration with established settlement and custody processes. For market participants, shortening settlement cycles and building depository-linked infrastructure could make tokenized products easier to operationalize, since the reporting and settlement logic would be more closely aligned with the processes investors already understand.

Token securities law already passed—implementation is now the focus for 2027

South Korea’s token securities effort predates the latest infrastructure review. In January, the National Assembly approved amendments that recognize blockchain-based distributed ledgers as valid securities registries and allow the issuance and circulation of token securities.

The FSC said the resulting framework is scheduled to take effect in February 2027. That start date depends on regulators finalizing subordinate rules and supporting infrastructure. The FSC also indicated that, at the second meeting of its public-private token securities council in May, it was targeting July for the release of proposed subordinate regulations and guidelines.

For builders and compliance teams, this is a critical distinction: the high-level legal permission is already in place, but detailed operational requirements—such as how tokenized securities records are maintained, verified and integrated into existing securities infrastructure—will be shaped by the subordinate regulations released later in the process.

Infrastructure work underway: KSD platform integration targeted for February 2027

Technical infrastructure is already moving forward. In May, Samsung SDS said it had won a Korea Securities Depository (KSD) contract to build a token securities management platform. The goal, as described at the time, is to connect KSD’s existing electronic securities account system with blockchain-based data.

Samsung SDS said it aims to complete the platform by February 2027, aligning the technical readiness with the broader token securities framework effective date. According to the FSC, detailed token securities plans will continue to be developed and discussed by the public-private council before being connected to the wider capital market infrastructure review.

This coordination step is likely to affect how smoothly tokenized securities transition from a legal concept into a production-ready market feature. Integrating with the depository’s existing account systems is particularly important because depositories are central to ownership records, settlement workflows and operational continuity—areas where regulators generally seek reliability and auditability.

For market participants, the key near-term items to watch are the October settlement-cycle roadmap and the end-2026 KSD OTC settlement system timeline, alongside the July release of subordinate regulations from the token securities public-private council. The sequence of these milestones will offer the clearest signal on how quickly South Korea can move from permission to practical, depository-linked tokenization at scale.

Anthropic’s Mythos artificial intelligence (AI) model reportedly needed only hours to find certain security vulnerabilities in highly sensitive US government computer systems during an intelligence test, a US official told the Associated Press.

Still, that speed does not mean it could exploit them in the same window, the official said, speaking anonymously to discuss the sensitive matter.

Anthropic Mythos Mapped the Weak Spots in Secure Government Systems

The official said the testing was conducted under Project Glasswing. Anthropic opted against a public release for Mythos.

Instead, it granted a select group of more than 50 technology firms early access to the unreleased model, allowing them to identify and remediate critical software vulnerabilities.

Senator Mark Warner of Virginia referenced the tests on June 11. He spoke before the Senate Committee on Banking, Housing, and Urban Affairs.

“This tool broke into almost all of our classified systems, not in weeks but in hours,” he said.

Warner attributed the account to the head of the National Security Agency (NSA) and US Cyber Command, Gen. Joshua Rudd.

Follow us on X to get the latest news as it happens

Mythos already carries a track record of finding flaws. The UK’s AISI (AI Security Institute) tested Mythos Preview on expert-level capture-the-flag challenges. The model succeeded 73% of them. No model had cleared that bar before April 2025.

In April, Mozilla credited the AI model with surfacing 271 vulnerabilities in Firefox. The browser maker patched them in Firefox 150.

Anthropic then launched Claude Fable 5 in early June. It billed the model as a general release version of its Mythos tier, with added safeguards.

The opening was brief. On June 12, the US government issued an export control directive citing national security. The order required the firm to bar every foreign national from Fable 5 and Mythos 5.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Anthropic Mythos Found Cracks in the Government’s Most Guarded Systems appeared first on BeInCrypto.

Key takeaways

- Risk sentiment across financial markets remained fragile following conflicting statements from US and Iranian officials.

- XRP risks dropping below $1.0 if the bearish trend persists.

Ripple’s XRP remained under pressure on Wednesday, trading below $1.10 and maintaining a broader bearish outlook.

The remittance-focused cryptocurrency failed to extend an early-week recovery attempt as investors reacted to renewed geopolitical uncertainty surrounding negotiations between the United States and Iran.

Mixed US-Iran signals fuel market uncertainty

Risk sentiment across financial markets remained fragile following conflicting statements from US and Iranian officials after the first round of peace negotiations held in Switzerland.

US Vice President JD Vance said late Monday that Iran had agreed to allow inspectors from the International Atomic Energy Agency (IAEA) back into the country. However, Iranian authorities disputed the claim, insisting that Tehran had made no additional commitments during the discussions.

Iran’s chief negotiator, Mohammad Bagher Ghalibaf, stated that the United States had agreed to release approximately $12 billion in frozen Iranian assets.

Meanwhile, Donald Trump warned reporters that Washington would take further action if Iran failed to comply with the terms of any agreement.

The conflicting messages have contributed to risk-off sentiment across cryptocurrency markets, limiting demand for digital assets and reinforcing bearish pressure on XRP.

Investor sentiment across the cryptocurrency market remains weak despite a slight improvement in confidence levels.

The Crypto Fear & Greed Index registered a reading of 23 on Monday, remaining firmly in “Extreme Fear” territory. While the index improved marginally from 20 recorded a day earlier, market participants continue to adopt a cautious stance amid macroeconomic and geopolitical uncertainties.

The subdued sentiment suggests that traders remain reluctant to aggressively accumulate risk assets, increasing the likelihood that short-term rallies could face selling pressure.

XRP price forecast: Bears continue to control the trend

From a technical perspective, XRP continues to exhibit a bearish structure on the daily timeframe.

The token is trading well below its key Exponential Moving Averages (EMAs), including the 50-day EMA at $1.25, the 100-day EMA at $1.35, and the 200-day EMA at $1.56.

XRP also remains below the middle Bollinger Band near $1.15, reinforcing the current downward bias.

Momentum indicators further support the cautious outlook. The Relative Strength Index (RSI) sits around 38, signaling weak bearish momentum without yet reaching oversold conditions.

Meanwhile, the Moving Average Convergence Divergence (MACD) histogram remains slightly positive around the zero line, indicating tentative stabilization rather than a decisive trend reversal.

For XRP to regain bullish momentum, buyers must overcome several important resistance zones.

The first hurdle lies at the Bollinger Band midpoint near $1.15, followed by resistance at the upper Bollinger Band around $1.22.

Beyond that, the 50-day EMA at $1.25 and a descending trendline near $1.28 create a significant supply zone. Additional resistance levels are located at the 100-day EMA around $1.35 and the 200-day EMA near $1.56.

A successful break above these barriers would be required to shift the broader market structure back toward a bullish outlook.

On the downside, XRP’s immediate support is located near the lower Bollinger Band at $1.07.

A decisive breakdown below this level could accelerate selling pressure and expose the token to a retest of the recent support zone around $1.05.

Should bearish momentum intensify further, traders may look toward the psychologically important $1.00 level as the next major area of demand.

Until buyers reclaim key resistance levels, XRP remains susceptible to additional downside risk in the near term.

Bitcoin’s price action is looking increasingly like it has followed the blueprint of prior market cycles, according to new technical research circulating this week. One analyst argues BTC is “compressed” below a longer-term adoption structure, while another set of estimates suggests the current bear-market leg may be only partly finished—and could face renewed pressure around August if key monthly levels fail.

Together, the commentary points to a market that may not be “broken,” but is still working through historical patterns that have often dictated the next directional shift for BTC over multi-month horizons.

Key takeaways

- Analyst David Eng says Bitcoin remains cyclical, tracking both a 400-day clock and a longer four-year “adoption structure” trend line.

- Eng’s framework places a four-year fair-value target near $76,400, implying BTC is trading below that level and therefore “compressed.”

- Rekt Capital estimates the ongoing bear market is about 71% complete, based on historical analogs.

- Rekt Capital is watching the 50-month EMA near $63,900; a monthly close around $62,000 would be treated as a possible breakdown signal.

- If July improves but fails to hold, Rekt Capital warns August could negate any upside and bring further downside continuation.

Two-cycle timing: “not broken,” but compressed

In a Wednesday post on X, analyst David Eng described Bitcoin’s behavior as running on “two clocks.” The shorter cycle, he said, is linked to a 400-day simple moving average (SMA), while the longer cycle filters out “noise” and highlights a structure tied to adoption over multi-year periods.

Eng pointed to the 400-day SMA as a recurring support level during previous bull markets, noting that this cycle has not seen daily candle closes below the average, echoing how prior runs behaved. On the four-year time frame, he argued a cleaner uptrend becomes visible, with price shifting above and below the trend line depending on where the market is in its cycle.

The practical takeaway from Eng’s thesis is that Bitcoin repeatedly stretches away from the longer-term adoption structure and then reverts toward it—rather than moving in a straight line. In his view, that means the current conditions reflect compression beneath the structure instead of a structural failure.

Eng also calculated that the four-year trend line currently implies a “fair price” around $76,400. He framed BTC as undervalued by roughly 20% relative to that estimate. In addition, Eng referenced Bitcoin’s Power Law trajectory, suggesting it is now entering territory approaching $135,000—an observation he used to reinforce the idea that the broader cycle framework remains intact.

“It is compressed below its adoption structure.”

When monthly closes matter: the 50-month EMA test

While Eng focused on longer-horizon cycle structure, another analyst—Rekt Capital—has been looking at how bear-market history typically evolves after key moving averages are challenged. In his latest commentary, Rekt Capital put the current downtrend at around 71% complete, referencing his own historical comparison work.

A central part of that monitoring centers on Bitcoin’s 50-month exponential moving average (EMA), which he described as currently sitting near $63,900. For traders, the distinction between an intramonth move and a confirmed monthly close is important: Rekt Capital’s scenario depends on what the market does at the month’s end.

He suggested that if the June monthly close resembles a trade around $62,000, it would “confirm the breakdown” from the 50-month EMA. In his framing, a subsequent month that turns positive could then potentially convert the 50-month average into new resistance—turning a former support reference into a ceiling.

“August would cancel out July and send Bitcoin into downside continuation.”

Why a “compressed” market can still signal tension

Eng’s “compressed” characterization and Rekt Capital’s caution about possible continuation are not necessarily contradictory. Eng’s framework emphasizes that Bitcoin can remain cyclical even when it is trading below a longer-term adoption structure; the compression can persist as the market works through transitional phases of the cycle. Rekt Capital, meanwhile, is concerned with the near-to-medium-term path that often determines whether a bear market grinds lower before eventually bottoming.

That overlap matters for investors because it highlights two different risk windows. In Eng’s view, BTC is still reverting toward the longer-term framework; in Rekt Capital’s view, the next steps depend on whether the market successfully holds key moving-average terrain—particularly around the 50-month EMA region.

For traders, this creates a practical monitoring checklist: not just where BTC trades intraday, but whether monthly closes confirm or negate moving-average breakdown narratives. If the market does not follow through on a breakdown, the downside thesis weakens; if it does, historical patterns may reassert themselves on the timeline Rekt Capital laid out.

What to watch next

The key near-term variable is how BTC behaves around the cited monthly level dynamics—especially whether June’s end-of-month close confirms weakness relative to the 50-month EMA, and whether any July strength can persist or gets reversed in the way Rekt Capital expects for August. Beyond that, Eng’s longer-cycle “fair value” reference around $76,400 may become a useful benchmark for assessing whether compression is merely a pause or the start of a broader repricing.

For centuries, banks have acted as the primary gatekeepers of lending. Whether individuals needed a mortgage, businesses required capital, or entrepreneurs sought funding, traditional financial institutions controlled access to credit. However, advances in blockchain technology and decentralized finance (DeFi) are challenging this model by enabling lending without banks.

As digital assets, smart contracts, and decentralized networks continue to evolve, a new financial ecosystem is emerging—one where borrowing and lending can occur directly between participants without relying on centralized intermediaries. This shift has the potential to reshape global finance and expand access to capital on an unprecedented scale.

How Traditional Lending Works

In the conventional banking system, financial institutions perform several critical functions:

- Evaluating borrower creditworthiness

- Managing deposits

- Issuing loans

- Collecting repayments

- Earning profits through interest spreads

While this system has supported economic growth for decades, it also presents challenges:

- Lengthy approval processes

- Geographic limitations

- High operational costs

- Limited access for the unbanked

- Dependence on centralized decision-makers

Millions of people around the world remain excluded from traditional credit systems despite having the ability and willingness to repay loans.

The Rise of Decentralized Lending

Decentralized lending platforms leverage blockchain technology and smart contracts to automate the lending process. Instead of relying on banks, these systems allow users to supply liquidity and earn interest while borrowers access capital directly from decentralized pools.

Smart contracts automatically handle:

- Loan issuance

- Collateral management

- Interest calculations

- Liquidation processes

- Repayment tracking

Because these functions are executed by code, many administrative costs and inefficiencies can be reduced.

Key Advantages of Bankless Lending

1. Global Accessibility

Anyone with an internet connection and a compatible wallet can participate in decentralized lending markets. Geographic restrictions and banking infrastructure become less relevant.

This opens opportunities for:

- Emerging economies

- Remote communities

- Freelancers

- Digital entrepreneurs

- Underbanked populations

2. Faster Loan Processing

Traditional loans often require extensive documentation and approval periods.

Blockchain-based lending can provide access to funds within minutes through automated smart contracts, significantly improving efficiency.

3. Greater Transparency

Every transaction is recorded on a public blockchain, allowing users to verify:

- Interest rates

- Available liquidity

- Loan terms

- Platform activity

Transparency reduces information asymmetry and increases trust in the system.

4. Continuous Market Availability

Unlike banks that operate during specific hours, decentralized lending markets function 24 hours a day, seven days a week.

Borrowers and lenders can interact at any time without waiting for business hours or regional banking schedules.

5. Reduced Intermediary Costs

By removing multiple layers of administration and oversight, decentralized systems can potentially offer more competitive rates for both borrowers and lenders.

The Evolution Beyond Collateralized Loans

Most current decentralized lending systems require borrowers to provide collateral worth more than the loan itself. While effective for risk management, this model limits accessibility.

The future may introduce more sophisticated approaches:

On-Chain Credit Scoring

Blockchain activity can serve as an alternative credit history.

Factors may include:

- Transaction history

- Wallet longevity

- Repayment behavior

- Governance participation

- Asset management patterns

These data points could help establish digital reputations and unlock undercollateralized lending opportunities.

Decentralized Identity Systems

Emerging identity frameworks aim to allow users to prove trustworthiness while maintaining privacy.

This could create portable credit profiles that work across multiple platforms and ecosystems.

AI-Powered Risk Assessment

Artificial intelligence may eventually analyze vast amounts of on-chain and off-chain data to evaluate borrower risk more accurately.

AI-driven models could improve:

- Loan pricing

- Default prediction

- Portfolio management

- Capital allocation

Real-World Assets and Lending

One of the most promising developments is the integration of real-world assets into blockchain-based lending systems.

Assets such as:

- Real estate

- Government bonds

- Corporate debt

- Invoices

- Commodities

can potentially be represented digitally and used as collateral.

This could significantly expand the size of decentralized lending markets by connecting blockchain liquidity with traditional economic assets.

Challenges That Must Be Solved

Despite its promise, bankless lending still faces several obstacles.

Regulatory Uncertainty

Governments worldwide continue to develop frameworks for digital assets and decentralized financial services.

Clear regulations will be important for large-scale adoption.

Smart Contract Risks

Software vulnerabilities can expose users to losses if protocols are not properly audited and secured.

Security remains a critical priority.

Market Volatility

Digital asset prices can fluctuate rapidly, affecting collateral values and increasing liquidation risks.

More stable collateral options may help mitigate this challenge.

User Experience

Many lending platforms remain difficult for newcomers to understand.

Simpler interfaces and better educational resources will be necessary for mainstream participation.

What the Future May Look Like

The future of lending may not involve a complete replacement of banks but rather a transformation of how credit is created and distributed.

We may see:

- Hybrid financial systems combining traditional and decentralized infrastructure

- AI-assisted lending markets

- Global digital credit networks

- Tokenized real-world collateral

- Instant settlement and loan execution

- Portable blockchain-based credit identities

In this environment, access to capital could become more open, efficient, and borderless than ever before.

Conclusion

Lending without banks represents one of the most significant innovations emerging from blockchain technology. By leveraging smart contracts, decentralized networks, digital identity systems, and tokenized assets, the financial industry is moving toward a future where credit can flow more freely and efficiently.

While challenges related to regulation, security, and adoption remain, the long-term trend points toward increasingly decentralized lending ecosystems. As technology matures, bankless lending could become a powerful complement—or even an alternative—to traditional financial services, creating new opportunities for borrowers and lenders around the world.

REQUEST AN ARTICLE

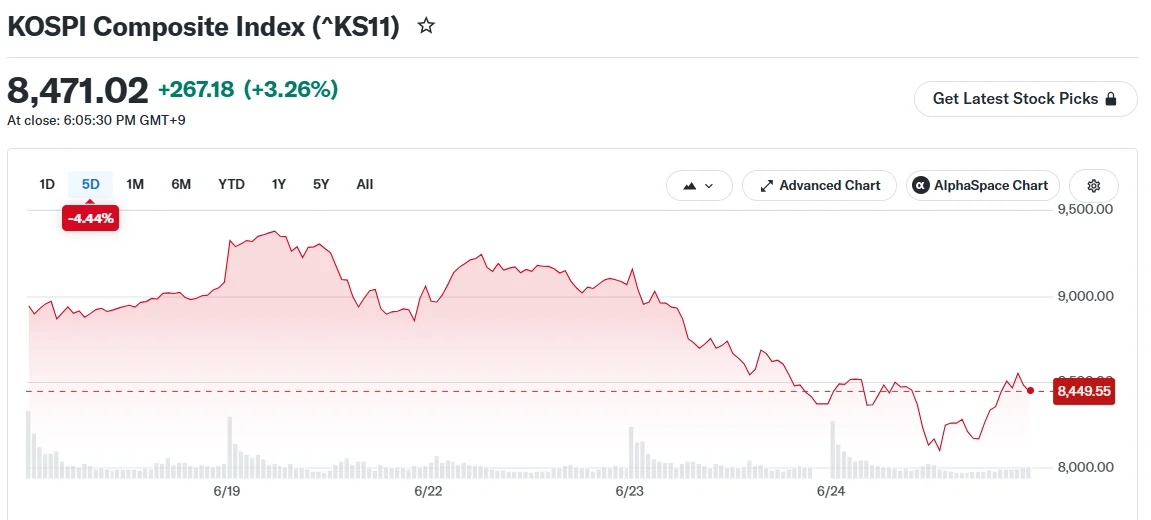

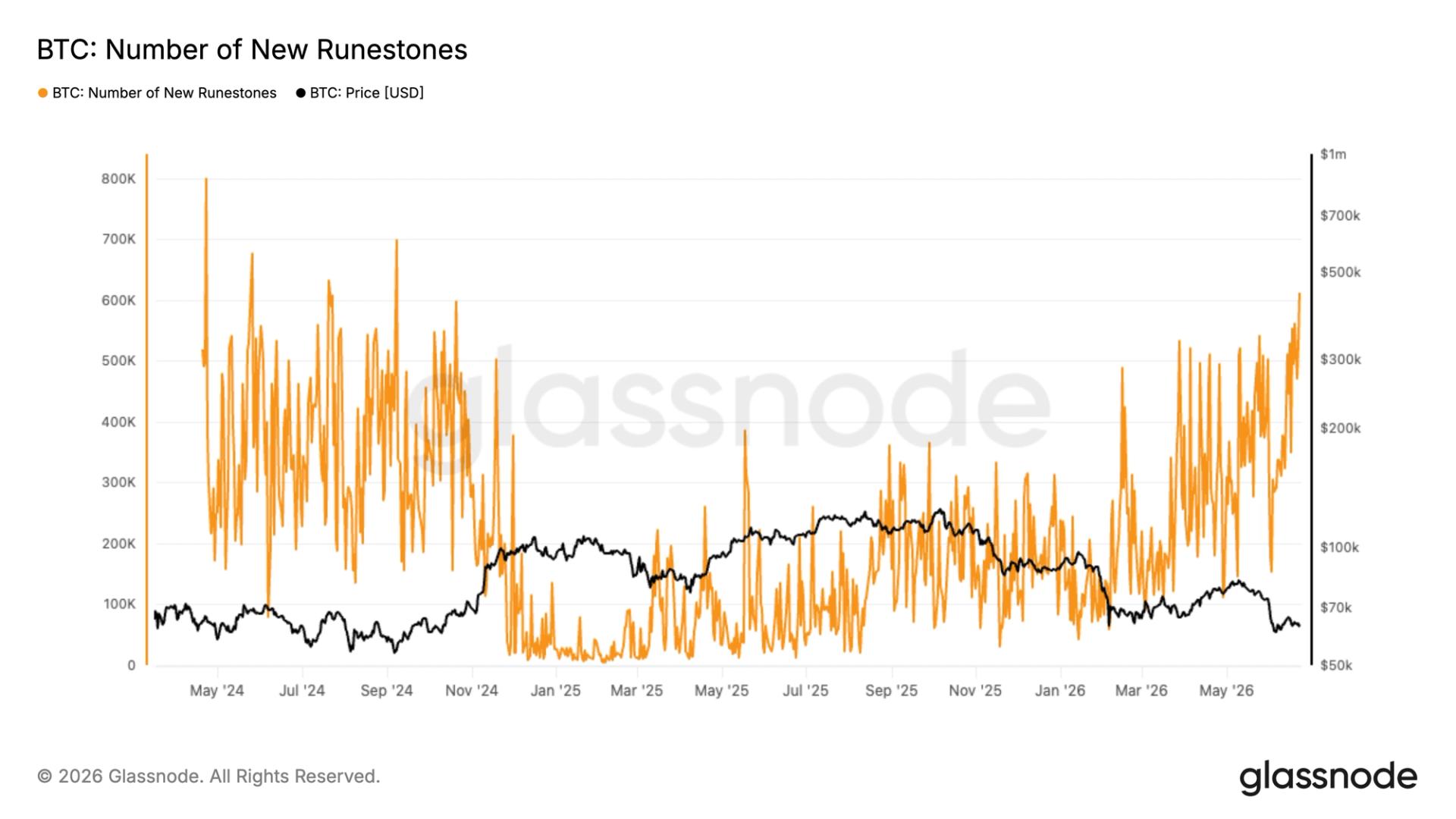

Bitcoin’s onchain activity is surging despite the asset remaining deep in a bear market.

The number of Bitcoin transactions recently climbed above 820,000 per day, according to Glassnode data. The increase comes as bitcoin trades around $62,000, roughly 50% below its October all time high, a period when network activity would typically be expected to weaken.

The transaction count is the highest since April 23 2024, the immediate aftermath of the last halving event and debut of the Runes protocol, a Bitcoin fungible token standard, which brought with it a considerable spike in transaction fees.

Similar to how ERC-20 tokens operate on Ethereum, Runes allow users to create and transfer fungible assets directly on Bitcoin.

Runes appears once again to be driving a rush in Bitcoin activity, with transactions carrying Rune protocol messages, known as Runestones, surging above 600,000 per day, also marking a two-year high, Glassnode data show.

The euro remains under pressure following weak macroeconomic data from the euro area and fresh signals that the European Central Bank is prepared to maintain a more accommodative monetary policy stance. Data released yesterday pointed to a deterioration in business activity across the eurozone’s largest economies. Weak readings from Germany and France heightened concerns about the pace of the region’s economic recovery.

Additional pressure came from comments by ECB President Christine Lagarde, which markets interpreted as more dovish than recent remarks from Federal Reserve officials. As a result, investors continue to scale back expectations for further policy tightening by the ECB.

Market participants will also focus today on Germany’s Ifo Business Climate Index. Forecasts suggest the headline index may rise to 85.6 from 84.9 previously, while the Expectations Index is expected to increase to 85.0 from 83.8. Although an improvement in business sentiment could provide temporary support for the euro, investors are likely to assess the data against the broader backdrop of slowing economic activity across the euro area. Even if the figures improve, markets may view them as insufficient to alter the prevailing picture of economic cooling.

EUR/USD

Yesterday, sellers managed to break key support at 1.1400, pushing the pair to a fresh low for the year. A sustained move below 1.1400 could pave the way for a further decline towards the next support zone at 1.1310–1.1280. A move back above 1.1400–1.1420 would be the first indication that bearish pressure is easing.

Key events for EUR/USD:

- Today at 11:00 (GMT+3): Germany Ifo Business Climate Index;

- Today at 12:00 (GMT+3): speech by Bundesbank President Joachim Nagel;

- Today at 17:00 (GMT+3): US New Home Sales.

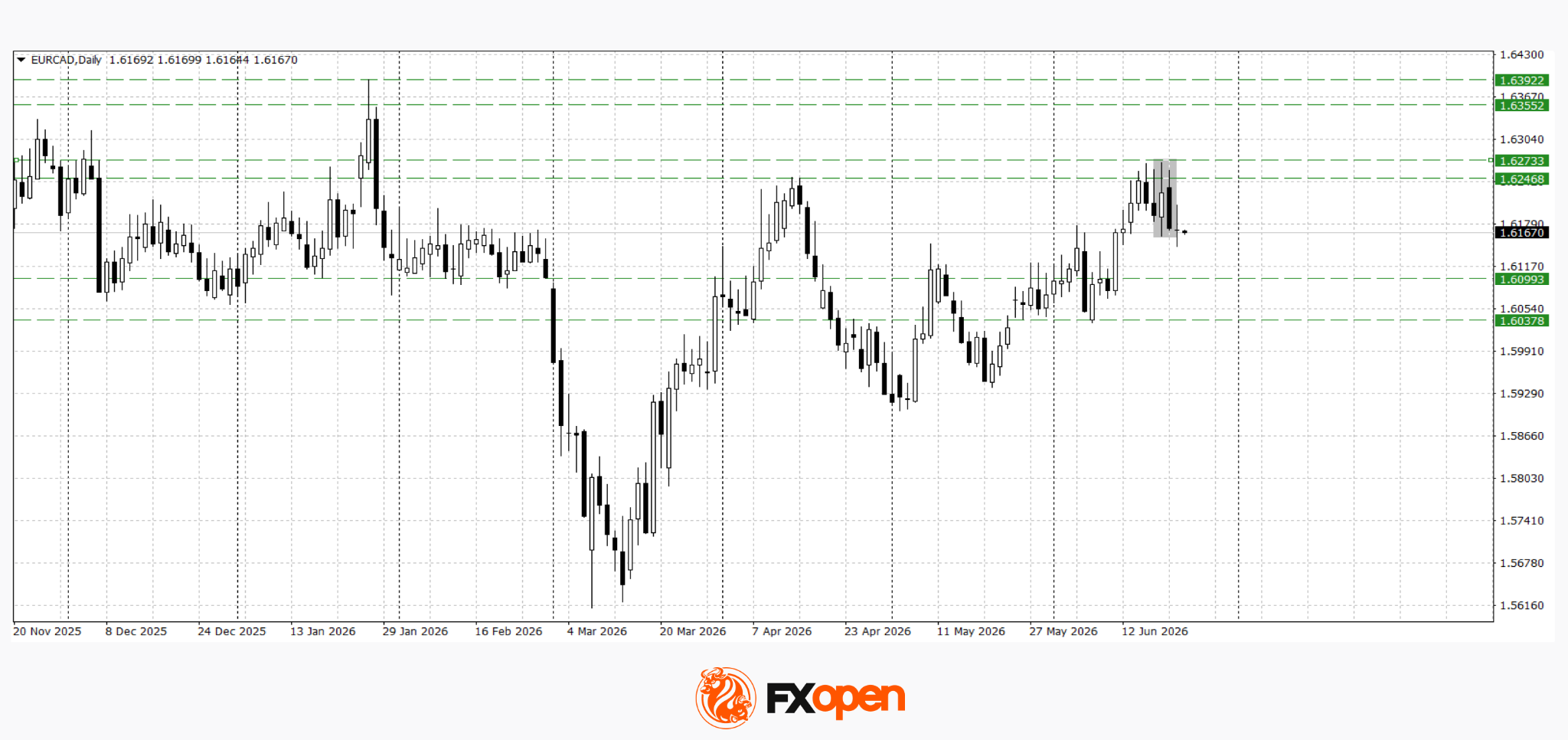

EUR/CAD

EUR/CAD has retreated from this year’s highs near 1.6200. Technical analysis suggests the pair may decline towards the 1.6100–1.6030 area, as a bearish engulfing pattern has formed on the daily timeframe. Conversely, a break above resistance at 1.6270 could trigger a resumption of the uptrend towards 1.6350–1.6400.

Key events for EUR/CAD:

- Today at 14:15 (GMT+3): speech by Bank of Canada Senior Deputy Governor Carolyn Rogers;

- Today at 15:30 (GMT+3): Canadian Manufacturing Sales;

- Today at 17:30 (GMT+3): US Crude Oil Inventories.

Overall, pressure on the euro persists amid weak eurozone data and diverging monetary policy expectations between the ECB and the Federal Reserve. If the German data fail to improve investor sentiment, both EUR/USD and EUR/CAD may extend their declines. At the same time, stronger European data or a weaker US dollar could trigger a corrective recovery in the single currency.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Strobe Finance, the only native decentralized lending protocol on the XRP Ledger’s EVM Sidechain, has announced that it is winding down and has given users until July 13 to repay their loans.

The users also have until July 20 to withdraw their deposits before the front end closes permanently.

That shutdown will leave the XRPL EVM Sidechain without a functioning lending market and has raised pointed questions about whether the network can support retail-focused DeFi projects at all.

What Happened, and What Users Need to Know

In a post on X published late Tuesday, the Strobe team bluntly laid out their reason for shutting down. According to them, while the project launched with enough funding to reach mainnet, it had not been able to secure additional support through grants, angel investors, or venture capital. And as total value locked (TVL) fell, the fees the protocol was earning were eventually not enough to cover monthly running costs.

The team also noted that the price of XRP had dipped by about 60% from the level it had been at when Strobe launched, making the funding gap even worse. Furthermore, the XRPL EVM Sidechain, which had been central to Strobe’s original design, is no longer a primary focus within the wider Ripple ecosystem.

“Throughout all of this, our team has contributed hundreds of hours, unpaid, to keep Strobe running,” they wrote. “We have done so gladly, but it is no longer sustainable.”

For those still using the protocol, the timeline is tight, as new deposits and borrowings have been disabled as of the announcement. In addition, anyone with an open loan has been asked to repay it before July 13, when Strobe will start liquidating unpaid positions to protect lenders as liquidity drains out. And since standard liquidation fees will apply, the team pointed out that repaying voluntarily is the better option.

From July 13 to July 20, the app will remain open for withdrawals only, and after the 20th, users will have to interact directly with Strobe smart contracts, which the project said it will publish a step-by-step guide for, although it stressed that using the app before that date would be far simpler.

“To put it plainly: out before 13 July is best; out before 20 July is essential,” it stated.

A Niche That No One Else Filled

There have been some disappointed reactions from several community members, including crypto commentator Shen, who wrote on X that Strobe was “a genuinely unique product within the XRP ecosystem” that had brought decentralized lending to the XRPL mainnet through the EVM Sidechain.

“If innovative products with no local ecosystem competition can’t survive on the XRPL long-term, what kind of projects can?” they asked.

They also called for major changes in how the chain supports retail-focused projects.

Another commentator, Krippenreiter, said they had lent money through the protocol and called its closure “really really bad.”

Ripple itself has been pushing the XRPL in a different direction. Earlier this month, it launched an AI starter kit that positioned XRP and its RLUSD stablecoin as tools for autonomous payment applications and machine-to-machine transactions. That institutional and developer-focused pitch is a long way from the retail lending product that Strobe was trying to build.

The post Important Ripple (XRP) Deadline Concerning Many Users appeared first on CryptoPotato.

Portsmouth residents warned about one common habit that puts you at risk of online theft

Ripple wins with JPMorgan, so why is XRP still stuck?

The 10 Most Suspenseful Movies of All Time, Ranked

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment4 days ago

Entertainment4 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Tech2 days ago

Tech2 days agoMicrosoft accidentally kills epic Outlook email threads

-

Sports16 hours ago

Sports16 hours agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Business4 days ago

Business4 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Crypto World8 hours ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 hours ago

Crypto World5 hours agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Politics6 days ago

Politics6 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Business10 hours ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business4 days ago

Business4 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Politics4 days ago

Politics4 days agoAndy Burnham and the meaning of Makerfield

-

Tech6 days ago

Tech6 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

Crypto World4 days ago

Crypto World4 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World4 days ago

Crypto World4 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

NewsBeat5 days ago

NewsBeat5 days agoKeir Starmer Allies Question His Chances For No 10

-

Crypto World4 days ago

Crypto World4 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Tech2 days ago

Tech2 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Tech3 days ago

Tech3 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Business5 days ago

Business5 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

-

Sports5 days ago

Sports5 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

You must be logged in to post a comment Login