Crypto World

Peter Thiel-Backed Stock Crashes 50% After ‘Superhuman Sports’ Dream Collapsed

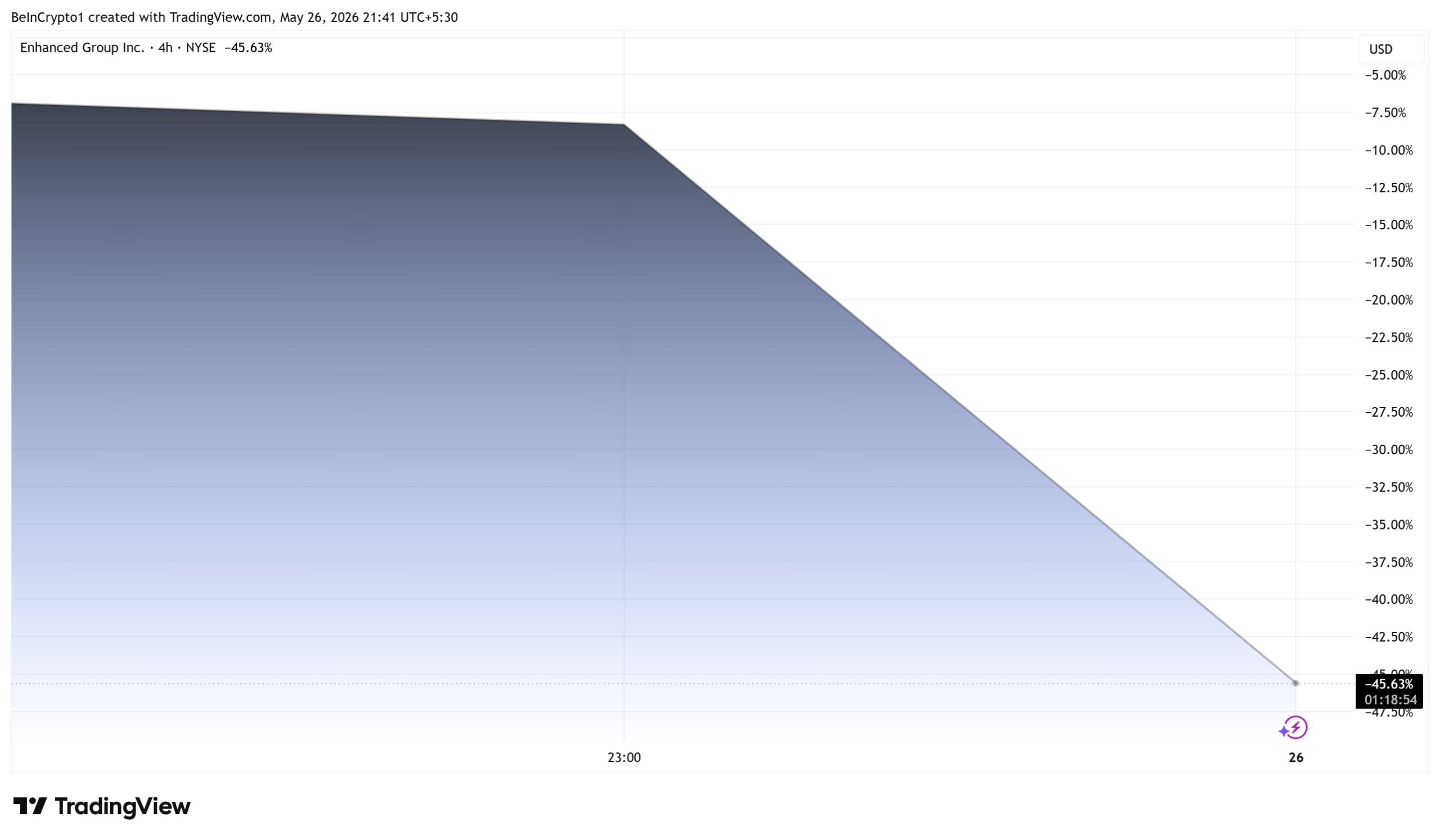

Shares of Enhanced Group (ENHA), the company behind the Peter Thiel-backed Enhanced Games, fell by as much as half on Tuesday after a six-hour Las Vegas debut produced only one unofficial world record.

The startup went public this month at a $1.2 billion valuation and has now shed hundreds of millions in market value over the past three weeks.

Vegas Debut Delivers One Record

The Enhanced Games held a single-night competition on May 24 at Resorts World Las Vegas, paying out a $25 million purse.

Roughly 42 athletes competed, with the company’s own monitoring data showing 91% used testosterone, 79% used human growth hormone, and 62% used stimulants like Adderall & modafinil ahead of the event.

“Peter Thiel and Donald Trump Jr. spent millions to create a steroid Olympics. They promised to “redefine human limits” and put up $25M in prize money…the whole pitch was that drugs would shatter the limits of clean sport. Instead, they proved the gap between juiced and clean…the only thing they actually proved was how good the clean athletes already are. You think the Enhanced Games exposed anything or just embarrassed themselves?” one researcher posed.

Only one unofficial world record fell. Greek swimmer Kristian Gkolomeev clocked 20.81 seconds in the men’s 50-meter freestyle, beating Cameron McEvoy’s 20.88-second mark and earning a $1 million bonus.

Sprinter Fred Kerley, who had predicted Usain Bolt’s 9.58-second 100-meter mark would be “destroyed,” won in 9.97 seconds, a time that would not have qualified for the Paris Olympics final.

Clean athletes, including Olympic gold medalist Hunter Armstrong, took three events outright.

Silicon Valley Loses to Biology

After closing at $5.36 on Friday, ENHA opened near $2.67 on Tuesday, a roughly 50% intraday slide that wiped out close to $800 million in market value.

Market cap has fallen from $981 million on May 7 to roughly $655 million.

Follow us on X to get the latest news as it happens

The setup echoes another recent venture-backed spectacle. A week earlier, Figure AI staged a 10-hour “Man vs. Machine” contest in which a human intern beat its F.03 humanoid robot 12,924 packages to 12,732.

When a single live-streamed proof point misses, the equity story tends to unravel in hours, not quarters.

With backers like tech investor Peter Thiel historically quick to rotate out of stalling bets, ENHA’s path to a second event now depends on public-market patience.

The post Peter Thiel-Backed Stock Crashes 50% After ‘Superhuman Sports’ Dream Collapsed appeared first on BeInCrypto.

Franklin Templeton has filed with the US Securities and Exchange Commission (SEC) to launch two exchange-traded funds designed to turn dividend income from US stocks into Bitcoin exposure. The proposal, disclosed in a June 18 SEC filing, targets investors who want a rules-based path to add Bitcoin exposure without abandoning an equity allocation.

The funds—titled the Franklin US Equity Bitcoin DRIP Index ETF and Franklin US Innovation Bitcoin DRIP Index ETF—would follow indexes that reinvest dividends from selected US stocks into a predetermined Bitcoin allocation. According to the filing, the initial allocation framework would place 5% into Bitcoin exposure and 95% into equities, with the index methodology governing how that balance is maintained over time.

Key takeaways

- Franklin Templeton filed for two dividend-reinvestment ETFs that convert stock dividends into Bitcoin exposure through proprietary index rules.

- The proposed funds would start with a 5% Bitcoin exposure and 95% US equities allocation, then keep that target within limits through periodic rebalancing.

- Bitcoin exposure could be gained through multiple instruments, including Bitcoin exchange-traded products, futures, options, and Bitcoin-backed depositary receipts, as described in the SEC filing.

- The “Equity” fund would track a broad US large-cap benchmark, while the “Innovation” version would focus on the 100 largest non-financial companies listed on Nasdaq.

- The filing arrives as at least several issuers continue experimenting with Bitcoin strategies beyond traditional spot ETF wrappers, amid reported softness in US spot ETF flows.

How Franklin Templeton’s “DRIP into Bitcoin” approach would work

In its SEC filing, Franklin Templeton describes two ETFs that use a Dividend Reinvestment Plan (DRIP) concept—but with the reinvestment redirected toward Bitcoin exposure. The indexes underlying each fund would systematically direct regular and special dividends from the equity holdings into Bitcoin within the index’s allocation framework.

Per the filing, the funds would launch with the same starting mix: 5% Bitcoin exposure and 95% US equities. The mechanism is intended to create a structured way to accumulate Bitcoin exposure over time as dividends are generated by the equity portfolio.

The SEC filing also outlines how the funds would maintain the allocation. It states that the indexes would be rebalanced quarterly to keep the Bitcoin allocation inside predefined boundaries, and that the indexes would be reconstituted semiannually.

Where the Bitcoin exposure could come from

One of the more practical details in the filing is how the funds plan to access Bitcoin exposure. Rather than relying on a single instrument, Franklin Templeton indicates that the proposed ETFs could gain Bitcoin exposure using a range of options. These include:

- Bitcoin exchange-traded products

- Bitcoin futures contracts

- Bitcoin options

- Bitcoin-backed depositary receipts

In addition, the filing states that the funds may hold certain Bitcoin-related investments through a wholly owned Cayman Islands subsidiary. The inclusion of a subsidiary structure signals that the issuer is planning for operational flexibility in how it sources or holds the relevant Bitcoin-linked instruments.

Two equity universes, one Bitcoin reinvestment rule

The two proposed ETFs differ in the equity set used to generate dividend income, even though both would follow the same dividend-to-Bitcoin investment concept.

According to the filing, the Franklin US Equity Bitcoin DRIP Index ETF would track an index built around a US large-cap equity benchmark. The Franklin US Innovation Bitcoin DRIP Index ETF, meanwhile, would track an index composed of the 100 largest non-financial companies listed on Nasdaq.

Both funds would be passive index ETFs tracking proprietary VettaFi indexes. Franklin Templeton’s filing also indicates that those indexes would be managed with quarterly rebalancing and semiannual reconstitution, meaning the reinvestment-to-Bitcoin process would remain rule-bound even as the underlying equity constituents potentially change.

Why this filing matters as issuers test income-focused Bitcoin products

Franklin Templeton’s proposal adds to a growing trend among asset managers: developing Bitcoin strategies designed to generate or enhance returns through structured rules, including income-focused methods. The filing comes after other major players explored Bitcoin-related products aimed at harvesting yield characteristics rather than relying solely on spot price appreciation.

Earlier this year, BlackRock filed for the iShares Bitcoin Premium Income ETF, which would use an options strategy tied to Bitcoin and its spot ETF to pursue additional returns. In April, Goldman Sachs outlined plans for a Bitcoin income ETF that would invest in spot Bitcoin exchange-traded products and sell call options against those holdings—aimed at generating yield while reducing sensitivity to price swings. Hamilton ETFs also moved toward a covered-call-style approach in Canada with a proposed leveraged Bitcoin income fund, as described in earlier reporting.

At the same time, the filing appears amid concerns about the near-term demand picture for US spot Bitcoin ETFs. CoinShares data cited that spot products have seen persistent outflows—though the source provided in the text points to SoSoValue, noting six consecutive weeks of net outflows between May 15 and June 18.

That backdrop helps explain why dividend-reinvestment mechanics could be appealing. By funneling cash generated from equity holdings into Bitcoin exposure on an ongoing basis, the strategy may offer a different “behavioral” path into Bitcoin—one anchored to equity dividends and disciplined index rules, rather than investor timing decisions alone.

What to watch next

Investors should watch how the SEC evaluates the proposed index methodology, particularly the practical implementation of Bitcoin exposure via futures, options, or Bitcoin-linked instruments, and whether the issuer specifies any additional constraints as part of the review. If approved, the funds would represent another step in Bitcoin ETF design—shifting the conversation from “spot access” to “systematic, income-linked allocation.”

Hsiao-Wei Wang has stepped down as co-executive director and board member of the Ethereum Foundation, effective immediately.

Summary

- Wang said her sabbatical helped her decide to leave Ethereum Foundation leadership effective immediately.

- Her exit follows Tomasz Stańczak’s February departure and Bastian Aue’s interim leadership appointment this year.

- Ethereum Foundation still funds protocol research as Glamsterdam and wider roadmap work continue this year.

She announced the decision on X after returning from a sabbatical. Wang said the break gave her time to review her priorities and the next phase of her life. She said she came to feel it was the “right moment” to step back from her formal role.

She thanked Bastian Aue for guiding the transition while she was away. Wang did not announce a new job or project, but said she expects to spend more time closer to home. She also said she remains a member of the Ethereum community.

Buterin credits Wang’s research and community work

Ethereum co-founder Vitalik Buterin also responded to Wang’s exit, saying she had been a “steadfast contributor” to the Ethereum ecosystem for a decade. He recalled her early role in the Ethereum research community and said she helped make research and consensus work more organized.

Buterin also pointed to Wang’s work outside protocol research. He said she helped build a strong Ethereum community in Taipei through people and events. He added that Wang handled her foundation leadership role “skillfully and gracefully” during a difficult period for Ethereum and the wider industry.

His comments add context to Wang’s departure by placing her work across both technical coordination and community building. Wang has not announced her next role, but Buterin said he looks forward to her next steps.

Exit follows earlier leadership change

Wang’s exit comes months after another change at the top of the Ethereum Foundation. In February, Tomasz Stańczak stepped down as co-executive director, and the board appointed Aue as interim co-executive director.

The Ethereum Foundation said at the time that Aue had deep knowledge of its structure and values. It also said he had worked with Wang and Stańczak on decisions across grants, enterprise work, and operations.

Wang and Stańczak had been named co-executive directors in March 2025. The foundation said then that Wang brought seven years of research experience, including work tied to the Beacon Chain and Ethereum’s wider research process. The appointment created a dual-leadership model after Aya Miyaguchi moved into the president role.

Ethereum work continues across teams

Wang used her message to point to the Ethereum community beyond the foundation. She said Ethereum has always been “bigger than any one role” and credited builders, researchers, educators, node operators, validators, and users.

As previously reported by crypto.news, the Ethereum Foundation has continued to fund protocol and infrastructure work. Its Q1 2026 grants supported Geth, Erigon, Lighthouse, validator security tools, zero-knowledge research, and public infrastructure.

Crypto.news also reported that the foundation has faced other staff changes in 2026. The Protocol Cluster transition included exits or sabbaticals involving Barnabé Monnot, Tim Beiko, and Alex Stokes, while new leads took over key areas. That transition came as core teams kept work moving across scaling, security, and client development.

Roadmap remains under watch

The leadership change lands as Ethereum developers prepare for major roadmap work. Crypto.news earlier reported that the Glamsterdam upgrade focuses on Enshrined Proposer-Builder Separation and Block-Level Access Lists.

Those changes aim to make block building more transparent and help clients process data more efficiently. Ethereum teams are also tracking gas repricing, Layer 1 scaling, privacy, and future security work.

The change also comes as the foundation narrows its role. Crypto.news recently reported Vitalik Buterin’s view that the Ethereum Foundation should act as one node in the wider Ethereum system, not as Ethereum’s parent or permanent steward.

Custodia Bank and Vantage Bank have unveiled a tokenized payments model that has combined bank deposits and stablecoins into a single asset, with plans to make the network available to banks and customers in the fourth quarter of 2026.

Summary

- Custodia and Vantage Bank have proposed a token that functions as a bank deposit inside the Hazel network and as a stablecoin when transferred outside it.

- The Ethereum based system has been running since March and is being tested by participating banks ahead of a planned launch in late 2026.

- The proposal comes as banks seek blockchain payment solutions that keep customer deposits within the banking system amid rising stablecoin adoption.

According to a white paper published on June 18, the proposed token changes its legal and operational form depending on where it is held. Inside the Hazel banking network, it functions as a bank deposit issued by a participating institution. Once transferred to external users or platforms outside the consortium, it becomes a stablecoin backed by cash and short-term U.S. Treasury securities.

Custodia and Vantage said the system has been operating on Ethereum since March and is currently undergoing testing with participating banks ahead of a planned launch later this year. The companies said Hazel is designed to support tokenized deposits, stablecoins and other blockchain-based financial assets through shared banking infrastructure.

Rather than requiring banks to overhaul existing systems, the white paper stated that Hazel operates alongside current core banking software, payment rails and ledger infrastructure. Participating institutions can continue using their existing systems while offering blockchain-based payment services.

The proposal arrives as banks search for ways to enter tokenized payments while retaining customer deposits within the regulated banking sector. Custodia and Vantage said the platform is intended for institutions of all sizes, including community banks and credit unions, allowing them to participate in digital asset payments without moving deposits to third-party stablecoin issuers.

Banks advance tokenized deposit plans

Across the banking sector, financial institutions have increasingly explored tokenized deposits as an alternative to traditional stablecoin models.

Earlier this month, The Wall Street Journal reported that The Clearing House, whose owners include JPMorgan Chase, Bank of America and Citigroup, is preparing a tokenized deposit network that could launch in the first half of 2027. According to the report, the system would allow banks to settle payments using blockchain-based representations of customer deposits.

At the same time, banking groups have opposed proposals that would permit stablecoin issuers to offer yield-bearing products. JPMorgan CEO Jamie Dimon recently said banks would continue challenging provisions in the CLARITY Act, a U.S. crypto market structure bill that he argued could allow crypto firms to compete for deposits without obtaining bank charters.

DefiLlama data shows the stablecoin sector has grown to roughly $315 billion from about $251 billion a year earlier, underscoring the increasing role of blockchain-based dollar assets in payments and settlement activity.

For Custodia, the Hazel initiative also arrives after years of regulatory disputes over access to the traditional banking system. In March, the U.S. Court of Appeals for the Tenth Circuit declined to revive the bank’s challenge against the Federal Reserve after regulators denied its application for a master account.

Custodia had argued that direct access to Federal Reserve payment infrastructure would allow it to provide settlement services without relying on intermediary banks, while regulators cited concerns related to its crypto-focused business model.

Ethereum trades near $1,696 as ETF outflows, Fed caution, weak whale activity and rare RSI signals shape the next ETH price move.

Yuma, one of Bittensor’s largest contributors and the network’s third-largest validator, has published a detailed critique of the proposed “Root Reborn” upgrade, arguing that the design introduces governance, regulatory, and market structure risks that outweigh its potential benefits.

Summary

- Yuma has opposed Bittensor’s proposed Root Reborn upgrade, warning that it could introduce conflicts of interest, regulatory concerns, and new risks for stakers.

- The proposal would allow validators to allocate root staking rewards across subnet tokens instead of automatically converting rewards into TAO.

- Yuma said subnets backed by validator allocations could benefit from additional demand, but called for more testing, risk analysis, and a formal upgrade roadmap before deployment.

The proposal, currently under review and not yet active on mainnet, would overhaul how root staking rewards are handled. Under the existing system, root dividends are effectively paid by automatically converting subnet alpha emissions back into TAO. The new design would stop those automatic sales.

Instead, validators would set allocation weights across subnets. Root emissions would then be deployed into validator-selected baskets of subnet tokens, with stakers receiving redeemable claims on those positions rather than direct TAO rewards.

The proposal states that the change would reduce automatic sell pressure on subnet assets and make validator allocation decisions a more important part of the network economy. It would also introduce new tools to track validator basket net asset value, subnet allocations, staker liabilities, and network-wide basket performance.

Yuma said the proposal changes the role of validators from infrastructure operators into active allocators of capital.

“In its current form, the Root Reborn proposal carries substantial unmitigated risk that outweighs its benefits,” the validator group wrote.

Yuma warns of conflicts and regulatory exposure

Yuma argued that validators would gain significant influence over capital flows inside the Bittensor ecosystem, creating incentives that may not always align with the interests of delegators.

The group said validators could direct allocations toward subnets in which they already hold positions or accept external incentives from subnet operators seeking additional capital. Yuma compared the structure to the lessons of the LIBOR scandal, where a small group of participants held influence over key financial benchmarks.

“Moral hazard is acute,” Yuma wrote, adding that validators should be expected to maximize their own financial returns.

The organization also questioned whether validator performance could be measured effectively under the proposed system. It said validators would not control redemption timing, making it difficult to maintain target portfolio allocations as users enter and exit positions.

Over time, Yuma argued, new emissions would represent an increasingly small portion of large validator baskets, limiting a validator’s ability to materially influence performance through future allocation decisions.

The report also raised concerns about regulatory treatment. Yuma said validators currently direct blockchain emissions, but Root Reborn would place them in a position where they actively determine subnet token exposure for delegators.

“Validators are no longer simply providing a neutral technological service due to the requirement to also set weights for subnet token rewards,” the group wrote.

Proposal seeks to reduce sell pressure on subnet assets

Supporters of the proposal have presented the upgrade as a mechanism to keep more value inside the subnet economy.

A summary accompanying the Subtensor pull request stated that root yield would move away from automatic subnet token sales and toward reinvestment across validator-selected subnets. The proposal described the change as a way to make validator selection depend on capital allocation decisions rather than primarily on fees or staking yields.

The proposal also said delegators would gain additional transparency through dashboard tools that display basket composition, net asset value, and outstanding liabilities owed to stakers.

Yuma acknowledged that subnets receiving validator allocations could benefit from increased demand and stronger token prices. The group wrote that subnets awarded meaningful weights would likely experience net-positive price effects, while subnets receiving little or no allocation could see neutral outcomes.

At the same time, Yuma warned that the structure could encourage lobbying efforts by subnet operators seeking validator support. The report said new projects may face greater barriers to entry if relationships with validators become an important factor in attracting capital.

The validator group also identified operational risks. Its report cited escrow concentration in a single coldkey, redemption dynamics that could create losses for late redeemers during periods of heavy withdrawals, repeated slippage costs from basket rebalancing, and execution challenges if network activity scales significantly.

Yuma urged the OpenTensor Foundation and network stakeholders to consider alternative approaches that allow stakers to express subnet preferences directly through opt-in mechanisms rather than concentrating allocation decisions among validators.

The group also called for a published upgrade roadmap, a defined release process, additional testing, and formal risk evaluation before any implementation proceeds.

The debate arrives days after Bittensor attracted renewed market attention following comments from Grayscale Head of Research Zach Pandl, who argued that recent U.S. restrictions on Anthropic’s advanced AI models could strengthen demand for decentralized AI networks. Pandl wrote that investors may increasingly look toward alternatives such as Bittensor as access to frontier AI systems becomes subject to centralized controls.

TAO (TAO) climbed roughly 30% within 12 hours after those developments, as per previous coverage on crypto.news. However, as of press time, TAO is down over 6% as traders weigh the recent concerns around the Root Rebor proposal.

AllUnity has launched SEKAU, a Swedish krona-backed stablecoin issued under the European Union’s Markets in Crypto-Assets Regulation.

Summary

- SEKAU is backed 1:1 by Swedish krona reserves and structured as a MiCA e-money token.

- AllUnity launched SEKAU across Ethereum, Solana, Base, Tempo and Polygon for institutional settlement use cases.

- The rollout expands AllUnity’s EURAU and CHFAU strategy as Europe builds regulated local stablecoins markets.

In a Friday announcement, the company said the token is structured as an e-money token and backed 1:1 by Swedish krona reserves.

The launch gives Sweden a regulated private stablecoin linked to its national currency. AllUnity said SEKAU targets institutional settlement, cross-border payments, treasury flows, and digital asset market use.

The company said SEKAU is fully reserved and supported by segregated fiat reserves. Holders also have a statutory right of redemption at par value under MiCA rules, according to AllUnity’s legal notice.

Banking partners support reserves

Banking Circle will act as the designated reserve and transaction bank for SEKAU. AllUnity said Banking Circle will hold and manage the fiat reserves backing the Swedish krona stablecoin.

Marginalen Bank is also supporting the rollout as a banking partner. Trust Anchor Group will provide digital asset infrastructure and integration support for broader access to SEKAU.

AllUnity CEO Alexander Höptner said the launch gives the Swedish krona “a native place in the digital economy.” He said the token can support instant settlement, programmable money, and cross-border payments.

Token launches on five networks

SEKAU debuts on Ethereum, Solana, Base, Tempo, and Polygon. AllUnity said the multi-chain rollout is designed to improve access, liquidity, and use across several blockchain ecosystems.

The company also plans to expand SEKAU to more networks later in 2026. The stablecoin will initially be available through the AllUnity Business Mint Account for onboarded institutional clients.

AllUnity said those clients can mint and redeem SEKAU through the platform. The company also said expansion to centralized and decentralized trading venues is already underway.

AllUnity expands European stablecoin lineup

The SEKAU launch extends AllUnity’s multi-currency stablecoin strategy. The company already operates EURAU, a euro-backed stablecoin, and CHFAU, a Swiss franc-backed stablecoin.

As previously reported by crypto.news, AllUnity planned a June launch for SEKAU after earlier announcing its Swedish krona stablecoin push. That report noted that dollar-backed stablecoins still dominate global supply, leaving limited room for regulated non-dollar options.

The Riksbank said earlier this year that stablecoins linked to one national currency are regulated like e-money under MiCA. It also said there were no stablecoins in Swedish kronor at that time.

Crypto.news earlier reported that European banks and companies are moving from research to rollout in stablecoins. MiCA has given issuers a clearer rulebook, while payment demand has pushed projects tied to euro, Swiss franc, and now Swedish krona settlement.

SEKAU does not replace Sweden’s e-krona research. A central bank digital currency would be public money issued by the Riksbank, while SEKAU is private money issued by a regulated company.

For AllUnity, the launch adds a third currency to its regulated stablecoin portfolio. For Europe, it adds another local-currency option at a time when banks, fintechs, and crypto firms are building payment tools under MiCA.

Hong Kong’s market operator and central bank have begun testing a wholesale central bank digital currency for derivatives trading, expanding the use of digital money within the city’s financial infrastructure.

Summary

- HKEX and the HKMA have launched a pilot to test e-HKD for derivatives margin payments during after-hours trading.

- The trial could allow clearing participants to transfer margin funds outside regular banking hours using a wholesale CBDC.

- The initiative extends Hong Kong’s wholesale e-HKD strategy into a live capital markets use case after authorities prioritized institutional adoption.

A joint announcement from Hong Kong Exchanges and Clearing (HKEX) and the Hong Kong Monetary Authority (HKMA) said the pilot will explore whether e-HKD can support advance margin payments for the after-hours trading (AHT) session in Hong Kong’s derivatives market.

Under the proposal, clearing participants would be able to use e-HKD, a wholesale central bank digital currency designed to operate around the clock, to transfer margin outside regular banking hours. HKEX and the HKMA said the arrangement would strengthen risk management during the after-hours session while preserving existing operational processes.

The initiative targets a longstanding limitation in the current system. At present, clearing participants must submit advance margin deposit requests to HKFE Clearing Corporation Limited by 3 p.m. if they want those funds recognized for the following after-hours trading session.

HKEX said it has invited clearing participants under HKFE Clearing Corporation to join real-value trial transactions on a voluntary basis. The exchange added that any wider rollout would depend on regulatory approvals, market preparedness and other operational considerations.

“By exploring the use of CBDC, we aim to provide a more flexible and timely payment option outside of regular business hours, and address longstanding operational pain points in the industry. This project reflects the shared commitment of HKEX and the HKMA to embracing innovation, strengthening the resilience of our markets and reinforcing Hong Kong’s position as a leading international financial centre.” – Vanessa Lau, Chief Operating Officer at HKEX.

Meanwhile, Howard Lee, Deputy Chief Executive of the HKMA, said the pilot would test a wholesale CBDC application in a live market environment.

Wholesale CBDC strategy moves into live market testing

The latest trial builds on the HKMA’s decision to prioritize institutional applications for e-HKD after completing the second phase of its digital currency pilot program in 2025.

At the time, the HKMA concluded that e-HKD and tokenized bank deposits could support programmable and cost-effective transactions across financial services. Trial participants included banks, technology firms and financial institutions that tested digital money in practical use cases.

Authorities later said institutional demand for e-HKD exceeded interest from retail users. The central bank subsequently shifted its focus toward wholesale deployment, including tokenized financial markets and trade settlement applications.

The new HKEX pilot provides one of the clearest examples yet of that strategy. Rather than testing consumer payments, the project places e-HKD within Hong Kong’s derivatives market and uses it to support margin funding during trading activity that continues after banks have closed.

Sonic Labs’ latest governance shake-up has spilled into the market, with the network’s native utility token, S, sliding shortly after the firm announced the resignation of three high-profile board members. According to the report, the departures include Michael Kong, David Richardson, and Andre Cronje, who had previously played key roles across Sonic’s predecessor ecosystem and the project’s technology.

On Friday, the S token traded around 0.031, down 5% over 24 hours. The same announcement also named new top leadership—Matt Visser as chief executive officer and Kosta Kourkoumelis as chief operating officer—while describing the changes as part of a broader effort to respond to community criticism and a long-running decline in the token’s value since the Sonic upgrade.

Key takeaways

- Sonic Labs confirmed board resignations from Michael Kong, David Richardson, and Andre Cronje, shortly before new executives were named.

- The S token fell to about 0.031 on Friday, reflecting immediate market sensitivity to governance changes.

- Sonic Labs attributed leadership transitions to a shift away from business decision-making by the departing board members.

- The company linked the overhaul to community dissatisfaction and a prolonged decline in S since the network upgrade.

- Sonic Labs said it will pursue more transparent governance and establish a dedicated risk and compliance committee.

Board resignations and a rapid leadership reconfiguration

Sonic Labs said that the resignations reflect an orderly handover from long-time builders who helped shape the organization. In a statement attributed to Andre Cronje’s prior communication regarding his resignation, Sonic Labs framed the departing executives as remaining invested in Sonic’s long-term success, while stepping back from ongoing business decisions.

The report lists the three resigning figures as:

- Michael Kong, described as a former CEO of the Fantom Foundation and director at Sonic Labs.

- David Richardson, who served as executive chairman of Sonic Labs.

- Andre Cronje, previously chief technology officer.

Sonic Labs also announced new leadership appointments to steer the organization forward. Matt Visser was named chief executive officer, and Kosta Kourkoumelis was appointed chief operating officer. The reshuffle suggests Sonic Labs intends to pair the board-level changes with day-to-day management restructuring, rather than treating the resignations as purely administrative.

Why the token is reacting now

The immediate drop in the S token comes at a moment when Sonic Labs has been under scrutiny for both performance and sentiment. The article states that S has fallen 97% since launching in January 2025 as part of a network upgrade, and that this decline has occurred alongside a “prolonged decline” in the token and growing community dissatisfaction.

In its own remarks about the situation, Sonic Labs reportedly acknowledged negative price action and weaker community sentiment, emphasizing that it would not treat the downturn as a temporary optics problem. The reported message—“We are not going to open with a victory lap. The token is down. Community sentiment is down. We see both clearly, we are not spinning it”—signals that the company views current market mood as a governance and communication challenge, not just a trading-cycle issue.

For investors and traders, the practical takeaway is that Sonic Labs appears to be responding to a credibility gap. Even when token fundamentals don’t change overnight, governance shifts can affect perceived execution risk—especially for protocols that rely on continued developer confidence and stable institutional oversight.

Governance reforms: transparency, communication, and compliance

The article notes that Sonic Labs is overhauling its leadership and governance structure. Sonic Labs said the changes include a commitment to more transparent governance and clear communication about project updates. It also highlighted plans to create a dedicated risk and compliance committee, a move that may be aimed at strengthening internal controls as the network continues to mature.

The reorientation is important because Sonic is described as an EVM-compatible layer-1 that positions itself around speed, including claims of 10,000 transactions per second and subsecond finality. Where performance claims meet reality depends on consistent execution and sustained coordination among leadership, developers, and stakeholders. Governance reform—especially involving risk and compliance—can help reduce uncertainty for users and ecosystem partners, even if it doesn’t immediately reverse token price momentum.

From Fantom to Sonic: a major technical shift still unfolding

The background to this governance update is Sonic’s origin story. Sonic Labs is described as the successor to the Fantom Foundation, founded in 2018. The network’s rebrand from Fantom to Sonic is characterized as a major structural and technical upgrade, including the replacement of the legacy Fantom Opera network.

That context matters because the S token launched as part of the Sonic upgrade in January 2025. When a protocol undergoes a migration and replatforming event, it often takes time for liquidity, ecosystem incentives, and community alignment to stabilize. The article’s claim that S has declined 97% since launch suggests that, at least so far, the market has judged the post-upgrade execution and traction against expectations.

At the same time, Sonic Labs’ stated focus on transparent governance and better project communication indicates it sees the present moment as a pivot point—an opportunity to rebuild alignment after leadership changes and community complaints intensified.

Elsewhere in the broader crypto sector, the article also references a leadership departure at the Ethereum Foundation, where co-executive director Hsiao-Wei Wang reportedly stepped down on Thursday, following a year that included layoffs and departures. While the Ethereum Foundation event is separate from Sonic’s day-to-day operations, it underscores a wider theme: institutional governance in crypto continues to experience personnel volatility, which can influence sentiment across the industry.

What to watch next for Sonic and S

Following the board resignations and the new CEO and COO appointments, investors will likely watch whether Sonic Labs can translate governance promises—particularly around transparent decision-making, clearer project updates, and a risk/compliance framework—into measurable progress on ecosystem delivery. The key question is whether improved accountability can stabilize community sentiment and, over time, narrow the gap between Sonic’s stated roadmap and market expectations.

HIVE Digital Technologies shares rose after the company announced a $220 million, three-year GPU cloud contract with Bell Canada and Cohere.

Summary

- HIVE’s BUZZ HPC signed a $220 million three-year AI cloud contract with Bell and Cohere.

- The deal covers 2,304 Nvidia Grace Blackwell GPUs at Bell’s Merritt facility in Canada directly.

- crypto.news earlier reported HIVE’s AI shift, falling Bitcoin holdings, and growing HPC revenue this year.

The deal adds another step to HIVE’s move from pure Bitcoin mining into high-performance AI computing.

The company said its BUZZ High Performance Computing unit will provide the GPU cloud layer for the project. The deployment will use 2,304 Nvidia Grace Blackwell GPUs at Bell’s AI Fabric facility in Merritt, British Columbia.

Bell and Cohere anchor Canadian AI stack

The infrastructure will support Cohere’s enterprise AI models for Canadian government and corporate customers. HIVE said the compute layer will stay on Canadian soil, matching Canada’s push for domestic AI systems and local control of data.

Bell AI Fabric will provide the data centre and network services. Cohere will use the platform for foundation models and enterprise AI tools, while Hypertec will supply Canadian-built hardware for the cluster.

Bell AI Fabric executive Michel Richer said Canada has “the talent and innovation to lead in AI.” Cohere’s Michael Pelosi said enterprise and government AI buyers need to know “where those models run” and how data stays protected.

Bitcoin miner deepens AI pivot

The contract strengthens HIVE’s shift away from relying only on Bitcoin mining revenue. The company has been building an AI and high-performance computing business under BUZZ HPC as miners search for new uses for power, cooling, and data centre capacity.

The project is expected to go live from late 2026 to early 2027. Reports said the contract could add about $70 million in annual recurring revenue. That would lift HIVE’s contracted high-performance computing revenue target above $100 million when combined with its existing run rate.

As previously reported by crypto.news, HIVE’s high-performance computing revenue rose 94% to $19.5 million in fiscal 2026. Crypto.news also reported that BUZZ HPC had reached $35 million in contracted recurring revenue before the new Canada deal.

Miners race for AI revenue

HIVE is not the only Bitcoin miner turning to AI infrastructure. Crypto.news earlier reported that IREN, Bitdeer, and other mining-linked firms are converting data centre capacity for AI and cloud computing customers.

The shift reflects a wider trend across the mining sector. Miners already own power contracts, cooling systems, technical teams, and facilities that can support GPU workloads. Those assets can help them serve AI customers when mining margins fall.

HIVE has also outlined a larger AI plan in Canada. Crypto.news previously reported that the company announced a proposed Toronto AI “super factory” with 320 megawatts of capacity and more than 100,000 GPUs.

The Bell and Cohere contract gives HIVE a clearer commercial case for that strategy. It also gives the company a major AI customer relationship as demand for sovereign cloud infrastructure grows in Canada.

The bill is on the calendar, the House has promised to move fast, and the committee fight is over. Everything now comes down to a single number: whether Senate leadership can find seven Democratic votes before the August recess. Here is the math that decides crypto’s biggest law.

Summary

- The CLARITY Act is now eligible for a Senate floor vote without further committee action.

- The House has signaled it will move quickly if the Senate passes the bill before recess.

- The bill needs at least seven Democratic votes to clear the Senate’s 60-vote threshold.

- The August recess is the deadline that could decide whether the bill passes or stalls.

As of mid-June 2026, the CLARITY Act, the most comprehensive crypto market-structure bill ever to advance in the United States, has reached the stage where only one thing stands between it and becoming law: votes. On June 1, the bill was formally placed on the Senate Legislative Calendar as Calendar No. 423, making it eligible for a full floor vote without any further committee action.

A vote can now happen at any time the Senate’s leadership chooses to schedule one. On June 18, the chairman of the House Agriculture Committee’s digital-assets subcommittee, Dusty Johnson, signaled that the House would act swiftly to pass the bill if the Senate takes it up before the August recess, removing the other procedural uncertainty.

The committee fights are over. Its text is on the floor. The House is ready to move. What remains is arithmetic.

That arithmetic is specific and unforgiving. The CLARITY Act needs 60 votes to overcome a Senate filibuster, Republicans hold roughly 53 seats, and only two Democrats, Ruben Gallego and Angela Alsobrooks, are on record supporting it from the May committee vote.

Both Democrats gave explicit warnings that their committee support did not guarantee a vote for final passage. That leaves a gap of at least seven Democratic votes that Senate leadership must find before the recess, and finding them is now the entire story.

This piece lays out how the bill reached this point, exactly what the vote math requires, where the seven Democrats might come from and what they want, why the August recess is a hard deadline, and what the whole thing means for a crypto market that has waited all year on this single bill. Everything now turns on seven votes.

How the bill got here

To understand why the math is all that is left, it helps to see how much has already been cleared, because the bill has traveled a long road to reach the floor.

The bill began in the House, which passed its version in July 2025 by a decisive bipartisan margin of 294 to 134, drawing more than 70 Democratic votes and the most comprehensive crypto regulatory framework ever to clear a chamber of Congress. That House passage handed the Senate a finished framework for dividing crypto oversight between the Securities and Exchange Commission and the Commodity Futures Trading Commission.

The Senate, as it tends to do, declined to simply take the House text and began building its own version through 2025, with discussion drafts and committee work stretching across the year. That process was slow and contentious, reflecting the genuine disagreements over how to regulate a new asset class, but it moved steadily toward a Senate bill.

The decisive committee moment landed on May 14, 2026, when the Senate Banking Committee advanced the bill by a vote of 15 to 9, with all thirteen Republicans joined by two Democrats, Gallego and Alsobrooks. Markets celebrated, with Bitcoin rallying toward $82,000 and XRP breaking above $1.50 on the news.

Then the qualification in the vote sank in: both Democratic supporters stated openly that their committee votes should not be read as commitments to support final passage on the Senate floor. On June 1, the bill was placed on the Senate Legislative Calendar as Calendar No. 423, formally eligible for a floor vote without further committee action.

Every committee stage, markup, and text-merging is now behind the bill. That is why the remaining question is no longer about process but about whether the votes exist on the floor.

The vote math, exactly

Now the arithmetic itself, because it is the whole game, and it is worth stating with precision instead of in the vague terms most coverage uses.

Like most significant legislation, the bill must overcome a filibuster to pass the Senate, which requires 60 votes, not a simple majority of 51. Republicans hold roughly 53 seats, so even with every Republican voting yes, the bill falls short of 60 by about seven votes, which must come from Democrats.

From the May committee vote, exactly two Democrats are publicly on record in favor, Gallego and Alsobrooks, and both attached explicit caveats that their committee support was not a promise of a floor vote for final passage. So the math is stark: starting from the two known Democratic supporters, Senate leadership needs to find at least seven more Democratic votes, and may need to first reconfirm the two it thinks it has, to reach the 60-vote threshold.

Every analysis of the bill’s prospects reduces to this question of whether those seven-plus Democratic votes can be assembled.

This is why the situation is best understood as pure vote-counting, not as a question of momentum or process. Its procedural path is clear, the House is committed to moving quickly, and the Republican votes are essentially in hand, which strips away every variable except the one that matters: the Democratic vote count.

A bill that needs seven crossover votes in a polarized Senate is neither doomed nor assured. It sits in the deeply uncertain middle where the outcome depends on negotiation, on what the wavering Democrats can be offered, and on whether leadership can hold a coalition together through a floor vote.

That bicameral commitment from the House, the promise to act swiftly if the Senate delivers, means the House will compress its own timeline to nothing. The only remaining constraint on the bill becoming law before the recess is whether Senate leadership can produce those seven or more Democratic votes.

The whole thing has narrowed to that single number.

Where the seven votes come from, and what they want

Those seven votes are not abstract; they are specific senators with specific concerns, and understanding what they want explains both why the votes are gettable and why they are hard.

Democrats who might provide the needed votes are, broadly, the more moderate and crypto-open members of the caucus, including some of the twelve Democrats who published their own crypto framework in 2025, signaling a willingness to legislate on the issue if their conditions were met. These are not implacable opponents.

They are senators who want a market-structure bill but want it on terms they can defend, which means their votes are available at a price, and the negotiation is about what that price is. Their central sticking points have been consistent: conflict-of-interest and ethics language, provisions addressing the previous administration’s crypto dealings, rules on stablecoin yield, illicit-finance and anti-money-laundering provisions, and protections for decentralized finance.

A Democrat is far more likely to vote yes if the bill addresses the ethics concerns and the consumer and illicit-finance safeguards they have emphasized. They are far less likely if it does not.

This is where the path to seven votes runs through specific amendments. The most-discussed route to Democratic support has been adding ethics and conflict-of-interest language by amendment on the floor, which several Democrats have signaled would move them toward yes, along with satisfactory resolution of the stablecoin-yield and illicit-finance questions.

That is why the provisions blocking Democratic votes matter so much. The bill is not stuck because members cannot describe the problem; it is stuck because each fix can alienate a different part of the coalition.

The challenge is that amendments that win Democratic votes can cost Republican ones, and the bill has to thread a version that holds essentially all 53 Republicans while adding seven Democrats. That balance is real and difficult because the two sides want different things.

Some provisions have already been fought over and trimmed in committee, leaving them in the awkward position of being too weak for one side and too strong for the other. The seven votes exist in principle, among the moderate Democrats who want a bill, but assembling them requires a negotiated text that satisfies their conditions without losing the Republican base.

That negotiation is the hard, uncertain work now underway on the floor.

Why the August recess is a hard deadline

Its timing is not arbitrary, and the August recess functions as a genuine cliff that shapes everything, which is why the next several weeks matter so much.

The Senate runs on a calendar with limited floor time, and the August recess is a hard break that removes weeks of legislative days. The White House set a target of signing the bill on or around July 4, and while that specific date is ambitious, the broader deadline is the recess.

If the Senate does not pass the bill before it leaves for August, the realistic path narrows considerably. This is partly a matter of momentum, since a bill that misses its window can lose the political energy that carries it, and partly a matter of the calendar beyond the recess, which is where the deeper danger lies.

After the summer comes the runway toward the November midterm elections, and legislating becomes harder as an election approaches. Both parties become less willing to hand the other a win and more focused on campaigning than on compromise.

What makes the recess deadline consequential is the midterm dimension, which makes the recess deadline more than merely inconvenient. If the bill slips past August and into the fall, it collides with the midterm calendar, and a crypto market-structure bill that does not pass before the election faces the risk of stalling entirely.

That could force the bill to confront a potentially less favorable Congress in 2027, depending on how the elections reshape the chamber. A delay, in other words, is not just a delay; it is a step toward the bill possibly dying and having to restart in a new and uncertain political environment.

That is the downside if the votes fall short. The period between now and the August recess is the decisive window, and the seven-vote math has to be solved in weeks rather than months.

The bill is closer to law than any market-structure bill in American history. It is also, if it misses this window, closer to a familiar death, and the recess is the line between those two outcomes.

What it means for crypto and XRP

Its fate matters enormously for the crypto market, and for XRP in particular, because CLARITY would resolve the single biggest overhang on the asset class.

For crypto broadly, CLARITY would provide the federal framework that the industry has wanted for years, defining how digital assets are regulated, dividing oversight between the SEC and CFTC, and replacing regulatory uncertainty with statutory clarity. That certainty is the precondition for the deeper institutional adoption that has been held back by the lack of clear rules, because large institutions managing fiduciary money need defined legal treatment before they commit at scale.

For XRP specifically, the stakes are even sharper, because CLARITY would codify XRP’s status as a digital commodity into federal law, a classification that, unlike an agency-level determination, cannot be reversed by a future administration with a memo. That permanence is what institutions have been waiting for.

It is also what passage would do for XRP. Analysts at Standard Chartered and JPMorgan have projected that XRP exchange-traded funds could draw $4 billion to $8 billion in inflows if the bill passes, several times what they have attracted so far.

The bill also matters beyond the ETF channel. It speaks directly to the utility waiting on the law, including tokenized settlement and institutional infrastructure that can only scale when the legal framework is clear enough for large firms to use.

This is why the seven-vote math is not just a legislative curiosity but a direct input into the crypto market’s near-term path. A passage before the recess would remove the overhang, codify XRP’s status permanently, and potentially unlock the institutional inflows that have waited on legal certainty, a clearly bullish outcome for XRP and the broader market.

A failure to pass before the recess, with the midterm risk that follows, would leave the uncertainty in place, disappoint a market that has priced in significant odds of passage, and potentially trigger the sell-the-delay reaction that catalysts denied tend to produce.

The market has been pricing meaningful odds of 2026 passage, around 70% by some prediction-market measures, which means a meaningful disappointment is possible if the votes do not materialize. Everything the crypto market is hoping for from CLARITY now depends on whether seven Democrats can be found before August.

That makes the vote math the most important variable in the asset class right now.

What it means for investors

For anyone watching crypto or XRP, the situation translates into a clear framework for what to track and how to think about the binary ahead.

The key variable to watch is no longer whether the bill advances procedurally, which it has, but whether the Democratic votes materialize. That means the signals that matter are reports of negotiations over the ethics, stablecoin-yield, and illicit-finance provisions, statements from moderate Democrats about their willingness to support the bill, and any move by Senate leadership to actually schedule a floor vote.

The August recess is the deadline that frames the whole thing, so the calendar matters as much as the content. The closer the recess approaches without a vote, the more the downside scenario gains weight.

An investor following XRP or the broader market should read the bill’s prospects through this lens, watching the vote count and the calendar instead of the procedural milestones that are already behind it. They should also watch the supply setup into the vote, because XRP’s ability to respond to a legislative catalyst depends not only on the headline, but on whether flows are strong enough to overcome supply pressure.

The realistic framing is that the outcome is starkly binary and deeply uncertain, sitting in the middle range where seven crossover votes in a polarized Senate could go either way. Passage before the recess would be a major positive catalyst, particularly for XRP given the permanence it would grant.

A miss, and the midterm risk that follows, would be a real disappointment for a market that has priced in significant passage odds. An investor should size any position tied to this catalyst to the reality that it is a coin-flip-adjacent legislative bet, not a near-certainty.

They should be wary both of assuming passage and of assuming failure, because the seven-vote math is truly unresolved. None of this is investment advice; it is a frame for the single most important legislative variable in crypto, reduced now to whether a handful of senators can be brought to yes before summer ends.

Seven votes from history

The CLARITY Act stands closer to becoming law than any crypto market-structure bill ever has. The House passed it, the Senate Banking Committee advanced it, it sits on the Senate floor calendar eligible for a vote, and the House has promised to move swiftly the moment the Senate acts.

Every procedural obstacle that can be cleared has been cleared. That is why the bill’s fate no longer turns on process or momentum but on a single, specific number: the seven-plus Democratic votes that Senate leadership must find to reach 60 and break a filibuster, beyond the two committee supporters who have warned their support is not yet a promise.

Those votes exist in principle, among the moderate Democrats who want a market-structure bill on terms they can defend. But assembling them requires a negotiated text that adds ethics and consumer protections enough to win seven Democrats without losing any of the 53 Republicans, a balance that is real work and deeply uncertain.

The August recess is the deadline, with the midterm calendar beyond it threatening to turn any delay into a possible death and a 2027 restart before a less favorable Congress. For crypto and especially for XRP, whose commodity status CLARITY would permanently codify and whose ETF inflows could multiply on passage, everything now rides on this arithmetic.

The bill is one good negotiation from a historic law and one missed window from a familiar grave. The difference between those outcomes is seven votes.

That is all that is left, and it is everything.

Frequently asked questions

What is the current status of the CLARITY Act?

As of mid-June 2026, the CLARITY Act has cleared the Senate Banking Committee, 15-9 on May 14, and was placed on the Senate Legislative Calendar as Calendar No. 423 on June 1. That makes it eligible for a full Senate floor vote at any time without further committee action. The House passed its version in July 2025 and, per a June 18 signal from a House Agriculture subcommittee chairman, would move swiftly to finalize the bill if the Senate passes it before the August recess.

Why does the CLARITY Act need seven Democratic votes?

The bill must overcome a Senate filibuster, which requires 60 votes. Republicans hold roughly 53 seats, so even with all of them voting yes, the bill falls about seven votes short and must draw them from Democrats. Only two Democrats, Ruben Gallego and Angela Alsobrooks, are on record supporting it from the committee vote, and both warned that their committee support did not guarantee a floor vote. So leadership must find at least seven more Democratic votes.

What do the wavering Democrats want in the bill?

The main sticking points are conflict-of-interest and ethics language, including provisions on the prior administration’s crypto dealings, rules on stablecoin yield, illicit-finance and anti-money-laundering provisions, and protections for decentralized finance. Moderate Democrats who want a bill are more likely to vote yes if these concerns are addressed by amendment. The difficulty is that amendments winning Democratic votes can cost Republican ones, so the text must satisfy seven Democrats without losing the Republican base.

Why is the August recess a hard deadline?

The Senate has limited floor time, and the August recess removes weeks of legislative days. The White House targeted a July 4 signing, but the real deadline is the recess: if the bill does not pass before it, the path narrows sharply. Beyond the recess looms the November midterm calendar, which makes legislating harder and risks stalling the bill entirely, potentially forcing a restart before a less favorable Congress in 2027. A delay is a step toward possible death.

What would CLARITY mean for XRP?

CLARITY would codify XRP’s status as a digital commodity into federal law, a classification that, unlike an agency determination, cannot be reversed by a future administration. That permanence is what institutions have waited for before committing at scale. Analysts at Standard Chartered and JPMorgan have projected XRP ETFs could draw $4 billion to $8 billion in inflows if the bill passes, several times what they have attracted so far, making passage a potentially major catalyst for XRP.

How likely is the CLARITY Act to pass in 2026?

It is deeply uncertain. Prediction markets have priced 2026 passage around 70%, but the outcome reduces to whether seven-plus Democratic votes can be assembled before the August recess, a coin-flip-adjacent question in a polarized Senate. The bill is closer to law than any market-structure bill in history, with every procedural step cleared, but seven crossover votes are neither assured nor doomed. The result depends on floor negotiations over ethics and consumer provisions in the coming weeks.

As of June 19, 2026. Legislative situations change rapidly; verify the current status before relying on this analysis. This article is information, not investment or legal advice.

Why people in the world’s most populous country are choosing to have fewer children

SpaceX’s Strength in Space, Connectivity Supports Initial Credit Ratings, Firms Say

Sharon Osbourne’s Hospital Trip Sparks New Concern

-

Business6 days ago

Business6 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Crypto World5 days ago

Crypto World5 days agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Crypto World7 days ago

Crypto World7 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Fashion10 hours ago

Fashion10 hours agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment5 days ago

Entertainment5 days agoMatt Damon’s Viral Sci-Fi Thriller Has Taken Over HBO Max

-

Business5 days ago

Business5 days agoAnthropic staff to meet White House officials next week, Axios reports

-

Tech5 days ago

Tech5 days agoAs AI companies race to go public, who else is along for the ride?

-

Crypto World5 days ago

Crypto World5 days agoBitcoin could crash to $48,000, if this historical pattern is triggered

-

NewsBeat5 days ago

NewsBeat5 days agoWarning of disruption as Cardiff Crossrail works to start

-

Politics5 days ago

Politics5 days ago“Israel’s” ban on ICRC visits ruled illegal, but Knesset moves to stop them permanently

-

Entertainment6 days ago

Entertainment6 days agoDeion Sanders Shares Powerful Post After Viral Advice To Deiondra

-

News Videos5 days ago

News Videos5 days agoFinancial Accounting | Last Day Revision Strategy and Booster | CMA Inter – June 2026

-

NewsBeat5 days ago

NewsBeat5 days agoTributes to former deputy head teacher at Cambridge school among death and funeral notices

-

NewsBeat5 days ago

NewsBeat5 days agowhat doctors are seeing in ebike crashes

-

Entertainment5 days ago

Entertainment5 days agoKate Middleton Glare Goes Viral After Kids Booed At Royal Event

-

Crypto World5 days ago

Crypto World5 days agoXRP ETFs Outperform As Bitcoin And Ethereum Funds Extend Outflow Trend

-

Crypto World6 days ago

Crypto World6 days agoMarket Preview: SpaceX (SPCX) IPO Record, Federal Reserve Meeting, and Iran Nuclear Agreement

-

Tech5 days ago

Tech5 days agoOver 400 Arch Linux packages compromised to push rootkit, infostealer

-

Business5 days ago

Business5 days agoInvesco Quality Income Fund Q1 2026 Commentary

-

Entertainment7 days ago

Entertainment7 days ago44 Years Later, This Is the Greatest Star Trek Quote in Sci-Fi History

You must be logged in to post a comment Login