Crypto World

Polish President Vetoes Crypto Bill for Third Time ahead of MiCA Deadline

Polish President Karol Nawrocki vetoed a cryptocurrency regulatory bill for the third time, which sought to implement Europe’s Markets in Crypto Assets Regulation (MiCA) in the country.

Nawrocki said Thursday he supports regulating the cryptocurrency market but argued that the government incorporated only one of 16 key amendments proposed by his office. He said that the text was nearly identical to the previous two drafts he refused.

The third veto of the bill delays Poland’s alignment with the EU-wide regulatory framework just weeks before the end of MiCA’s transitional period on July 1. Following the end of the grace period, crypto asset service providers will be required to hold a MiCA license or stop servicing EU clients.

Poland is currently the only EU member state without a domestic MiCA implementation. Following the July 1 deadline, Poland-based crypto asset service providers without a MiCA license may lose the legal basis to serve EU customers.

Related: MiCA architect says EU should prioritize tokenization over DeFi rules

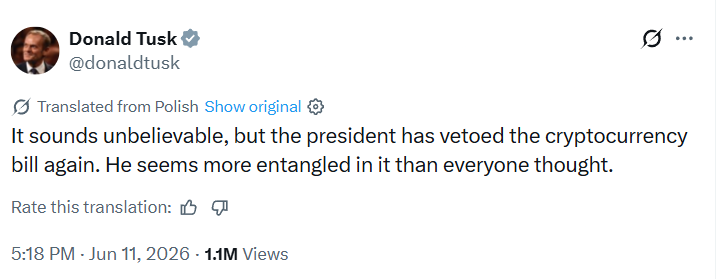

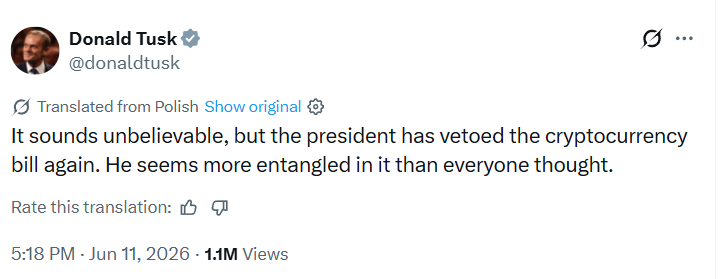

Polish Prime Minister Donald Tusk slammed the veto in a Thursday X post, writing: “It sounds unbelievable, but the president has vetoed the cryptocurrency bill again. He seems more entangled in it than everyone thought.”

Source: Donald Tusk

Political deadlock deepens over crypto bill

The decision adds to Poland’s political standoff on how the country should oversee crypto assets. It comes nearly two months after Poland’s parliament failed to reverse the second veto issued by President Nawrocki.

Lawmakers fell short of the 263 votes needed to override the veto in an April vote on the bill, which is backed by Tusk’s government and seeks to align Poland with MiCA.

Nawrocki has reportedly defended his opposition by citing concerns about excessive regulation, limited transparency and the potential burden on small businesses.

Government officials warned that delays leave consumers and businesses exposed to fraud and abuse.

The third veto comes as scrutiny of Poland’s crypto sector intensifies. Prosecutors are investigating one of Poland’s largest crypto exchanges, Zondacrypto, for suspected fraud and money laundering involving 2,000 customers with alleged links to Russian organized crime.

Zonda CEO Przemysław Kral has denied accusations of misappropriating funds.

Magazine: Crypto wanted to overthrow banks, now it’s becoming them in stablecoin fight

On 30 July, Amazon.com reported its financial results for the second quarter of 2026, significantly exceeding market expectations. Revenue rose 20% year-on-year to $200.6 billion, compared with the consensus forecast of around $196.5 billion. The main growth driver was the AWS cloud business, where sales increased by 37% — the fastest growth rate in 18 quarters — while the segment’s operating profit surged to $16.6 billion. Total operating profit climbed 43% to $27.5 billion. Net income reached $62.6 billion, or $5.75 per share, although a substantial portion came from a $53.4 billion non-operating gain related to the revaluation of Amazon’s stake in Anthropic. Advertising revenue also increased by 26% year-on-year.

Amazon Technical Analysis

On the four-hour AMZN chart, a downtrend developed after the stock peaked near $278 in May. The decline towards $226 at the end of June was followed by a corrective recovery along an ascending trendline connecting higher lows until mid-July, when the price approached resistance around $258, where the red resistance level is currently located. A break below this trendline signalled that the correction had run out of momentum, after which the price returned to the current market profile range, settling between the POC zone at $244.5 and the lower profile boundary at $232.5. Below this area lies the green support level at $226.5.

Should the current rebound continue and the price break above the POC zone, it is likely to face two further obstacles: the upper profile boundary at $249 and the red resistance level at $258. It is also worth noting that the RSI + MAs indicator currently shows readings of 46, 36 and 43. The indicator suggests that the slower moving average has yet to move below the parity zone, while the RSI has already recovered from oversold territory.

Summary

Strong earnings provide a fundamental catalyst for a continuation of the current rebound, although the RSI + MAs oscillator has yet to generate a clear signal. In the coming days, further guidance from management on AI infrastructure capital expenditure, along with the market’s reaction to earnings reports from other technology giants, could determine the stock’s next move.

Buy and sell stocks of the world’s biggest publicly-listed companies with CFDs on FXOpen’s trading platform. Open your FXOpen account now or learn more about trading share CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Quantum Solutions sold 1,000 ETH for $1.903 million on July 30 through its consolidated subsidiary, GPT Pals Studio Limited.

Summary

- 1,000 ETH sale raised $1.903 million as Quantum Solutions redirected funds toward AI data centers.

- 4,375 ETH authorization permits another 2,471 tokens to be potentially sold through October 30, 2026.

- 4,764.80 ETH remain, while 3,050 tokens stay pledged as collateral to a Singapore-based financial lender.

The Tokyo-listed company plans to redirect the proceeds toward its AI Infrastructure Data Center business. The sale reduced the group’s Ethereum balance to 4,764.80 ETH and is expected to produce a loss of about ¥17 million in the second quarter of the fiscal year ending February 2027.

The company also raised the maximum amount authorized for sale from 1,875 ETH to 4,375 ETH. After two disposals totaling 1,904 ETH, Quantum may sell another 2,471 ETH before October 30. Any further transactions will depend on funding needs, market conditions and progress in its AIDC plans.

Quantum Solutions expands its ETH sale authority

The revised ceiling adds 2,500 ETH to the earlier authorization adopted on June 4. Quantum said the change gives it more flexibility to fund data-center usage agreements, GPU equipment, launch preparations and related operating costs. The filing states that the increase “does not constitute a decision to immediately sell” the entire authorized amount.

Quantum’s first sale occurred on June 16, when GPT Pals sold 904 ETH at $1,777.07 each for about $1.606 million. That transaction left the group with 5,764.80 ETH and generated an expected ¥18 million loss based on its revalued carrying price.

The latest sale creates a ¥17 million loss

GPT Pals received a net $1,903 per ETH in the July transaction. Quantum had marked the assets at $2,003.97 each on May 31, leaving a $100.97 difference per token. The company therefore expects a $100,970 realized loss, equal to roughly ¥17 million at its stated exchange rate.

That accounting loss is not measured against the original historical purchase price. Quantum uses fair-value accounting and records valuation changes at each quarter-end. When it sells ETH, it compares the sale price with the latest carrying value under its moving-average method.

Most remaining ETH is tied to loan collateral

Of the 4,764.80 ETH left after the sale, 3,050 ETH remains pledged to a Singapore-based financial services company as collateral for an earlier borrowing. Only 1,714.80 ETH sits in GPT Pals’ crypto trading account, according to the filing.

The remaining authorization exceeds that unpledged balance by 756.20 ETH. This means Quantum would likely need to release or replace some collateral, acquire more ETH or use another arrangement before selling the full additional 2,471 ETH. The company has not said that it will take any of those steps.

Quantum’s top Japanese treasury ranking is disputed

The two sales have cut Quantum’s ETH holdings by about 28.6% from the 6,668.80 ETH reported before the June disposal. As previously reported, Quantum became one of the leading listed Ethereum treasury companies after rapidly adding ETH in late 2025.

Its current Japanese ranking is less clear. BitcoinTreasuries.net lists Def Consulting with 4,976 ETH as of June 30, which would place Quantum behind it. However, CoinGecko currently lists Def Consulting at 4,571 ETH. The conflicting tracker figures mean the claim that Quantum remains Japan’s largest listed Ethereum holder cannot be treated as settled without a newer company disclosure.

moreover, FG Nexus also reduced its Ethereum treasury in June as losses widened. Meanwhile, larger holders including BitMine and SharpLink continued accumulating, showing that corporate Ethereum strategies have moved in different directions during the market downturn.

Quantum said it will disclose any further sales requiring public notice. The next formal checkpoint is its second-quarter results, scheduled around October 10 on the company’s investor calendar. Investors will then see the recognized sale losses, updated ETH holdings and any further AIDC spending before the authorization expires on October 30.

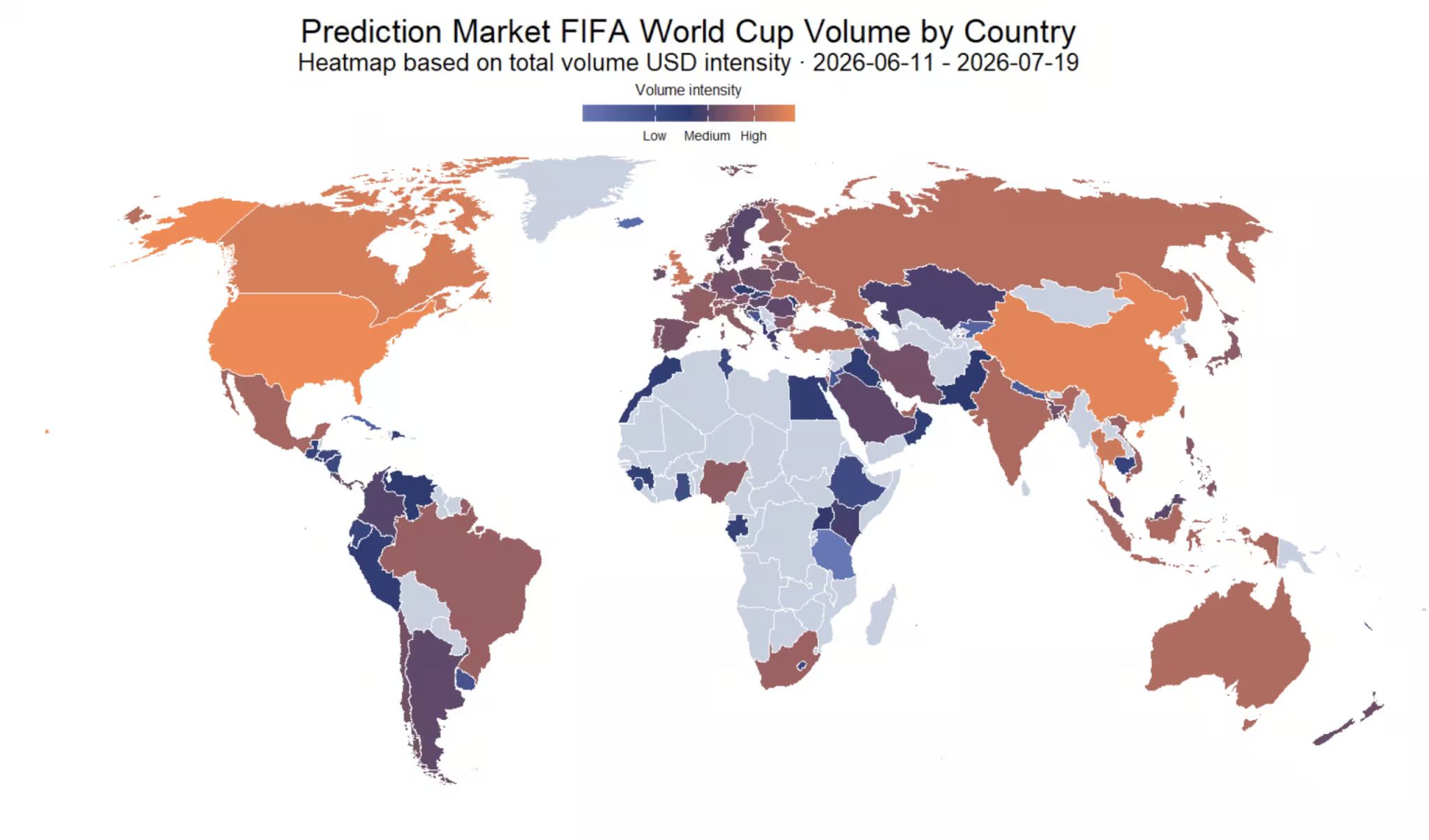

The 2026 FIFA World Cup generated $20 billion in blockchain prediction-market volume from January through the tournament’s end, Chainalysis reported on July 30.

Summary

- $20 billion in prediction-market volume accumulated from January through the World Cup’s five-week tournament period.

- 400,000 wallets generated $5.7 billion during the tournament, representing 63% of prediction-market activity by volume.

- $24 million in FIFA Collect trades supported ticket access for more than 100,000 fans worldwide.

The analytics firm said more than 400,000 wallets participated, while $5.7 billion was traded during the five-week event.The report also tracked $24 million in stablecoin-powered trading through FIFA Collect, the football body’s official digital collectibles platform. The data show how betting, collectibles and ticket access converged on public blockchain infrastructure during the tournament.

World Cup prediction markets dominated onchain activity

World Cup-related markets accounted for about 63% of all prediction-market volume during the competition. Daily activity began near $50 million in January, exceeded $100 million during busy pre-tournament periods and moved toward $250 million after matches began on June 11.

Volume topped $300 million on the final, when Spain defeated Argentina, Chainalysis said. The $20 billion total covers trading from January, including qualifying and pre-tournament markets. It should not be read as betting conducted only during the tournament.

The figures fit a broader expansion in event contracts. Binance Research separately reported that monthly prediction-market notional volume rose 86% from January to $51.6 billion in June. It said Kalshi and Polymarket represented 92% of June’s total, although its market-wide measurement differs from Chainalysis’ World Cup-specific dataset.

U.S. and China led globally attributed volume

Chainalysis attributed the most activity to the U.S. and China, followed by Canada, Thailand and the United Kingdom. Participation came from every continent except Antarctica.

However, the firm cautioned that its proprietary geolocation method “may carry uncertainty” when VPNs, mixers or privacy tools obscure wallet locations. The rankings therefore represent Chainalysis’ attribution, not verified residence data for every participant.

However, World Cup demand pushed daily prediction-market volume sharply higher during June. In addition, Kalshi gained tournament exposure through ADI Predictstreet, FIFA’s official prediction-market partner.

Chainalysis identified about 3,700 participating wallets with traceable illicit interaction histories, representing less than 1% of the total. It reported at least $5.4 million flowing from Huobi or HTX into wallets that later used World Cup markets. Scam-linked wallets accounted for about $2 million, while stolen-fund exposure exceeded $800,000.

The U.K. designated Huobi Global on May 26 under its Russia sanctions regime and clarified that HTX falls within those restrictions through ownership. The European Union later added HTX to a transaction-ban list, with the measure scheduled to apply from August 23.

These findings measure earlier wallet interactions and fund flows. They do not prove that each flagged wallet committed an offense through its World Cup trades.

FIFA Collect connected digital assets with tickets

FIFA Collect let users trade digital collectibles and obtain rights connected to match tickets. FIFA says more than 100,000 fans gained stadium access through its Right-to-Ticket products. Chainalysis traced $24 million in payments to a key FIFA Collect smart-contract wallet from May 2025 through the tournament.

The firm estimated that FIFA received at least $6 million from secondary transactions after applying the platform’s 5% share. It found negligible direct illicit exposure among FIFA Collect users, which “may be a result of FIFA’s robust KYC practices,” according to Chainalysis. That explanation is an assessment, not a controlled test.

As crypto.news reported, FIFA moved its collectibles platform to a purpose-built, Avalanche-based blockchain in 2025. The next test is whether ticket-linked collectibles and prediction-market users remain active after the World Cup. Regulators and platforms will also face pressure to strengthen sanctions screening, market surveillance and settlement controls as event-contract volumes expand.

Crypto markets barely registered one of the sharpest equity rallies of the year on Friday, with bitcoin holding near $64,300 while South Korean stocks staged a record rebound from the selloff that dominated the past two weeks.

The majors were close to unchanged. Ether traded at $1,907, XRP at $1.08, solana at $74 and dogecoin at $0.07, with roughly $27 billion changing hands in bitcoin and $7 billion in ether. BNB was the exception, up 3% on the day to $590 and the only major holding a meaningful weekly gain. Bitcoin spiked to $65,300 in early Asian hours before giving it back within an hour.

The weekly picture stays soft. Hyperliquid’s HYPE is down 5% over seven sessions, solana and XRP are each off 3%, and bitcoin has lost 2%. Ether and dogecoin are up 1%.

Equities went the other way, hard. The Kospi surged as much as 17%, rebounding from a three-day rout that had taken the index more than 40% below its June peak. Samsung and SK Hynix both jumped more than 23%, and Taiwan Semiconductor rose 10%, making chipmakers the biggest contributors to a broad Asian advance.

The 2026 FIFA World Cup generated $20 billion in prediction market volume, with the US and China contributing the largest country-level flows, according to new Chainalysis research published Thursday.

More than 400,000 wallets placed on-chain bets on the tournament. World Cup markets accounted for roughly 63% of all prediction market activity during the event.

World Cup Betting Volumes Peaked at the Final

Chainalysis tracked World Cup betting from January 2026. Markets were already producing nearly $50 million in daily volume months before kickoff. Daily activity jumped to around $250 million once the tournament opened on June 11.

The final, in which Spain defeated Argentina, drove over $300 million in wagers. Novelty markets also attracted heavy flows. A single market asked whether Cristiano Ronaldo would cry after his last campaign, generating $49 million.

Bettors fared unusually well. Chainalysis found 55% of participants ended the tournament in profit, and 79% of those winners were experienced prediction market users.

The report mapped tournament betting flows by country between June 11 and July 19. The heatmap shows that the US and China generated the highest attributable volumes worldwide.

Canada, Thailand, and the UK also ranked among the top contributors. Australia, Brazil, Russia, and India also saw heavy activity, while much of Africa showed little or no attributable volume.

Follow us on X to get the latest news as it happens

Sanctioned Exchange Funds Reached Betting Wallets

Not all the money was “clean.” Chainalysis identified roughly 3,700 wallets, under 1% of bettors, with illicit transaction histories.

The largest single source was Huobi/HTX, which sent at least $5.4 million into World Cup betting wallets. The UK sanctioned the exchange in May over alleged Russian sanctions evasion, and the EU followed in July. Scam-linked wallets added around $2 million.

Meanwhile, FIFA’s own on-chain experiment stayed largely clean. Chainalysis identified a key FIFA Collect wallet on Avalanche that received $24 million from NFT collectors between May 2025 and the tournament’s end.

The firm said that strict identity checks may explain the negligible level of illicit exposure. On-chain flows indicate FIFA collected at least $6 million from secondary sales.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post US and China Led $20 Billion World Cup Prediction Market Boom, Chainalysis Says appeared first on BeInCrypto.

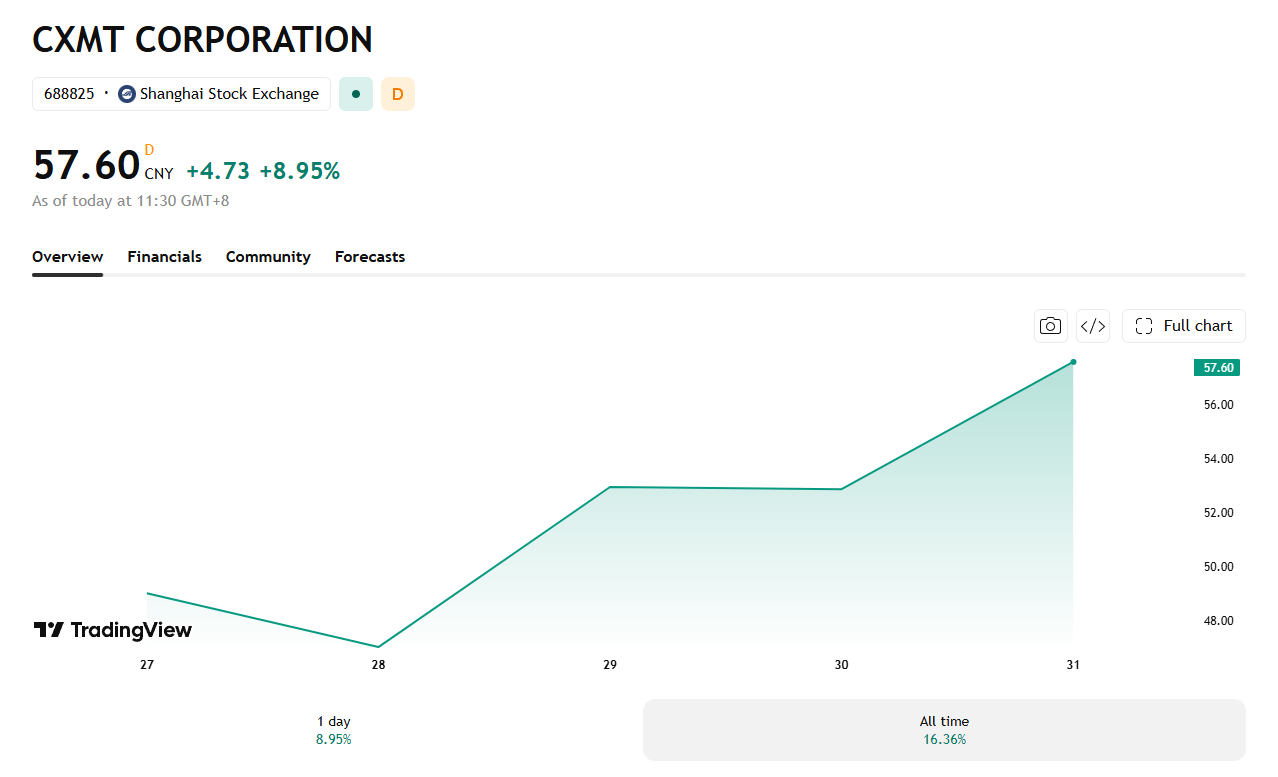

CXMT Corp (688825) jumped 8.95% on Friday to close at 57.60 yuan (about $8.51), extending its rally through a fifth trading day on the Shanghai Stock Exchange.

The Chinese memory chipmaker has grown continuously in the few days since its record initial public offering (IPO) last week, pushing its market capitalization to roughly 3.54 trillion yuan, or about $523 billion.

Why CXMT Keeps Climbing

CXMT, short for ChangXin Memory Technologies, listed on Shanghai’s STAR Market on July 27. Shares surged as much as 466% on opening day. The move briefly pushed CXMT past Industrial and Commercial Bank of China to become mainland China’s most valuable listed company.

The IPO raised 57.92 billion yuan, or about $8.6 billion. CXMT plans to use the funds to expand production and close the technology gap with foreign rivals.

Two forces are driving investor demand. Beijing wants chip self-sufficiency as Washington restricts China’s access to advanced semiconductor equipment.

At the same time, a global shortage of dynamic random-access memory (DRAM), the chips that let devices and AI models store and process data, has manufacturers redirecting supply toward AI data centers.

What CXMT Actually Makes

CXMT was founded in 2016 and is based in Hefei. The company holds roughly 7.7% of the global DRAM market, making it the world’s fourth-largest producer. Samsung Electronics, SK Hynix, and Micron Technology control the other 90% between them.

CXMT mainly builds mainstream memory chips for phones, laptops, and servers. It still trails rivals in High Bandwidth Memory (HBM), the advanced chip type that feeds AI data centers directly. Counterpoint Research director MS Hwang said CXMT aims to start supplying HBM within China by 2027.

Dell, HP, and Apple have reportedly started testing CXMT’s chips as they look to diversify away from Korean and American suppliers. Price is the main draw. But the deal carries risk.

The Pentagon has added CXMT to a list of firms it links to the Chinese military, a designation the company denies. Apple is separately lobbying Washington for clearance to use Chinese-made memory.

CXMT’s rise lands amid what industry watchers call “RAMageddon,” a consumer device memory squeeze that has already boosted Apple’s smartphone pricing power and rattled chip stocks from Seoul to Wall Street.

Analysts remain split on how much relief CXMT can deliver. That means any pricing benefit for everyday devices probably won’t arrive soon, even as the AI chip race keeps accelerating.

The post CXMT Stock Jumps Another 9%: What the Chipmaker Means for the AI Race appeared first on BeInCrypto.

U.S. Senate Minority Leader Chuck Schumer introduced the Anti-Corruption Bureau Creation Act on July 30, proposing a federal agency with authority to investigate and pursue executive-branch corruption.

Summary

- Seven Senate-confirmed members would lead the proposed bureau, with subpoena, enforcement and reporting powers nationwide.

- Trump’s certified disclosure entries totaled over $1.4 billion across crypto-related ventures during calendar year 2025.

- Four Democratic senators sponsor the bill; its launch materials named no Republican cosponsor on Friday.

Senators Andy Kim, Alex Padilla and Jeff Merkley joined Schumer as original cosponsors.The bill cites President Donald Trump’s 2025 financial disclosure and says he received at least $2 billion from investments and business interests, including more than $1.4 billion connected to crypto ventures. The proposal does not itself establish that any disclosed income resulted from illegal conduct.

The crypto figure represents an aggregation of entries in the disclosure, rather than a single total calculated by the Office of Government Ethics. The filing reports income and transaction amounts, not the net profit that would appear on a tax return.

Anti-Corruption Bureau would combine three watchdogs

Schumer’s proposal would place the Federal Election Commission, Office of Government Ethics and Office of Special Counsel inside one independent bureau. A seven-member board confirmed by the Senate would oversee investigations, subpoenas, enforcement actions and public reporting.

The legislation would also allow state attorneys general and private plaintiffs to seek recovery of funds allegedly obtained through corruption. Its official summary describes disgorgement, treble damages and awards for successful plaintiffs. It also proposes a self-financing Freedom From Influence Fund.

A three-judge division of the U.S. Court of Appeals for the D.C. Circuit could appoint temporary board members when vacancies threaten the bureau’s operation. The provision is intended to prevent a president or Senate from disabling the agency by leaving seats vacant.

Trump’s crypto income came from several ventures

Trump’s certified disclosure lists $635.1 million in royalties from Celebration Coins. It also records hundreds of millions of dollars from World Liberty Financial token sales, equity transactions and crypto wallets, plus $196.9 million tied to a stablecoin-related holding company. Together, the listed crypto-related entries exceed $1.4 billion.

Those figures describe disclosed revenue and proceeds, not necessarily Trump’s personal after-tax earnings. As previously reported, the filing showed that crypto generated more income than Trump’s resorts and other property businesses during 2025.

The bill separately states that Trump’s family held more than $1 billion in a crypto fund connected to foreign governments. It references a reported United Arab Emirates-backed investment in World Liberty Financial. These are legislative findings and allegations, not a court judgment that corruption occurred.

White House rejects conflict-of-interest claims

White House Principal Deputy Press Secretary Anna Kelly said Trump’s investments were held in fully discretionary accounts managed by independent third-party financial institutions. She maintained there were “no conflicts of interest.” Trump has also said he does not manage his personal finances while serving as president.

Schumer described the existing federal oversight system as a “broken patchwork” and argued that its agencies were not designed to address current executive-branch conduct. The White House disputes the premise that Trump’s business income creates an unlawful conflict.

The bill faces a difficult path through Congress

The publicly released full bill text still displayed a placeholder instead of a Senate bill number on July 31. The launch announcement listed four Democratic sponsors and no Republican cosponsor. The measure must clear both chambers before reaching Trump, who could veto it.

The proposal also enters a wider debate over the Digital Asset Market Clarity Act. Senator Cynthia Lummis released updated Senate text on July 22 after the bill passed the Banking Committee by a 15–9 vote. Senator Elizabeth Warren argued that its current ethics provisions would not adequately restrict presidential crypto interests, while supporters continued to seek a bipartisan agreement.

Crypto.news reported that the CLARITY Act still faced disputes over ethics and banking provisions as supporters pressed for a vote. The Senate is scheduled to reconvene on Aug. 3, but no timetable has been announced for Schumer’s anti-corruption bill. Its next steps could include formal numbering, committee referral and hearings before any floor consideration.

Wintermute says the next phase of altcoin momentum may look different from past cycles: fewer tokens could attract sustained inflows as institutional desks concentrate their activity into a narrower basket of assets. In a first-half 2026 OTC flow report, the market maker found that institutional counterparties accounted for the vast majority of spot trading activity on its desk—an outcome that, if mirrored across the broader market, would likely make “altseason” less broad and more selective.

The shift also appears to include a timing mismatch. Wintermute reports that institutional participation tends to fade quickly after a token’s price and volume spike, while retail activity typically stays elevated for longer—suggesting any future rallies could be more short-lived and restricted to the tokens institutions already favor.

Key takeaways

- Wintermute’s first-half 2026 OTC data shows institutional counterparties generated 72% of spot flow across all tokens on its desk—the highest share recorded—up from 61% in H2 2025 and 59% in H1 2025.

- Liquidity and attention are concentrating in the “short list” of assets institutions choose, while activity in the market’s smaller “long tail” weakens.

- The number of unique tokens traded by institutional counterparties rose only 24% from H1 2024 to H1 2026, versus 76% growth for retail clients.

- Institutional activity after a price-and-volume surge typically cools within about one day, while retail activity remains elevated for around three days.

Institutional desks are pulling OTC liquidity toward a smaller set of tokens

Wintermute’s OTC flow report points to a structural change in how capital is deployed across the altcoin market. According to Wintermute, institutional counterparties drove 72% of spot flow across all tokens handled on its OTC desk in the first half of 2026—its highest recorded level. That compares with 61% in the second half of 2025 and 59% in the first half of the previous year.

While institutional participation has been rising, Wintermute’s interpretation matters for traders and investors: when the majority of activity is concentrated among a smaller group of counterparties and assets, rallies can become narrower. The firm said liquidity is increasingly clustering in tokens institutions favor, while the broader “long tail” of smaller tokens sees less consistent engagement.

That concentration effect is reinforced by the growth rates in token participation. Wintermute found that from H1 2024 to H1 2026, the number of unique tokens traded by institutional counterparties increased by 24%, whereas retail clients increased their number of unique traded tokens by 76% over the same span. In practical terms, the data suggests that retail participants explore a wider range of assets, while institutional flow remains comparatively disciplined.

Faster institutional pullbacks after spikes could reshape altcoin rally dynamics

Another detail in Wintermute’s report relates to how quickly activity cools after a token experiences a surge. The firm found that institutional activity following spikes in a token’s price and volume faded after roughly one day. Retail behavior differed: Wintermute says retail activity typically stays elevated for about three days after similar surges.

If these patterns extend beyond Wintermute’s OTC venue, they can influence how traders structure exposure during altcoin moves. Short-lived institutional participation can mean that order flow—and therefore liquidity—does not remain supportive for as long as it may have in earlier cycles when broader rotation into many assets sustained momentum.

For market participants, the implication is straightforward: rallies may require faster decision-making and more asset-selective positioning, because the “institutional bid” may not persist the way it once did across a wide swath of tokens.

Other data points suggest “altseason” rotation is narrowing across venues

Wintermute’s proprietary OTC findings add to a growing set of signals that capital is clustering around fewer altcoins. On June 20, CryptoQuant CEO Ki Young Ju said the “traditional rotation of Bitcoin profits” into smaller assets had “basically disappeared.” CryptoQuant data referenced by Young Ju suggested that trading volume in Bitcoin-denominated altcoin pairs was near its weakest level since 2021.

Meanwhile, CryptoQuant’s CEO also pointed to market cap concentration. The 10 largest non-stablecoin altcoins accounted for about 80.5% of the non-Bitcoin, non-stablecoin market’s capitalization—another indicator that the market’s center of gravity is increasingly tilted toward the biggest names in the category.

Exchange-level data has also suggested a similar pattern. In July 2025, Kaiko reported that the ten largest altcoins made up 63% of altcoin trading volume, up from roughly 50% several months earlier as activity in smaller tokens weakened. Together with Wintermute’s OTC numbers, the message across different datasets is consistent: liquidity and trading interest are drifting toward the same smaller group of assets.

Market debate: broad rallies vs. selective sector moves

The question now facing investors is whether this concentration will permanently reduce the breadth of future altcoin runs—or simply change their shape. DWF Labs managing partner Andrei Grachev has argued that broad altcoin rallies are giving way to more selective sector activity. In March 2025, Grachev said too many tokens were competing for limited capital, while institutional investors remained focused on Bitcoin, Ether, and tokenized real-world assets.

This framing aligns with the mechanics Wintermute describes: if institutions are more concentrated, and their participation fades quickly after price and volume spikes, “rotation” may become less of a market-wide wave and more of a series of targeted moves. In such an environment, tokens outside the institutional comfort zone may struggle to attract sustained liquidity, even if retail interest remains visible for a brief period.

It also highlights a potential tension between retail and institutional behavior. Retail participation appears to spread across more tokens and remain elevated longer after bursts. But if institutional desks dominate overall spot flow on major venues and OTC desks, retail-led excitement may not be enough to maintain broad-based momentum without follow-through from larger pools of capital.

For readers, the key watch items are whether institutional concentration continues to increase beyond H1 2026, and whether the “one-day” institutional fade and “three-day” retail persistence become stable patterns across more tokens and more trading conditions. If they do, the definition of “altseason” may shift from a widespread rotation into many names to a narrower, faster-moving set of trades that reflect where liquidity is actually concentrated.

Roughly 594 bitcoin, worth about $38 million, was swept out of around 500 separate wallets between 01:31 and 01:56 UTC on Friday in an attack traced to a flaw in how Coldcard hardware wallets generated their keys.

The theft moved 1,324 chunks of bitcoin across 500 transactions inside a three-block window, with 562 BTC then consolidated into a single address that has not moved.

Every drained wallet was single-signature and each held more than 0.15 BTC. Many had been dormant for years and the coins spanned 2021 to 2026, matching the flaw’s age almost exactly.

Coldcard is a hardware wallet built by Canadian firm Coinkite, a small standalone device that stores bitcoin keys offline, away from internet-connected computers. Mk2, Mk3, Mk4, Q and Mk5 are successive generations of that product, released over several years the way a phone maker ships numbered models.

Exposure depends on the firmware the device was running at the moment the wallet was first created, not on when the hardware was bought.

A wallet’s seed, the secret phrase controlling the funds, is meant to be drawn at random from a pool so vast that guessing is hopeless.

Canary Capital renewed its marketing push for the Canary HBAR ETF on July 30, describing HBR as the first U.S. spot exchange-traded product holding Hedera’s native token.

Summary

- 704.3 million HBAR backed Canary’s fund, with net assets near $47.8 million on July 30.

- 5.18 million HBR shares were outstanding after Canary added fifty thousand shares in latest update.

- HBR’s 0.95% sponsor fee accompanied a 37.32% year-to-date market-price decline recorded through July 29, 2026.

The post was not a new launch announcement. HBR began trading on Nasdaq on Oct. 28, 2025, after its registration became effective with the U.S. Securities and Exchange Commission.

The latest fund data gives a clearer view of its current scale. HBR held 704.35 million HBAR and reported about $47.8 million in net assets on July 30. The product had 5.18 million shares outstanding and charged a 0.95% sponsor fee.

Canary HBAR ETF now holds 704 million HBAR

Canary’s official fund page shows that HBAR represented effectively all the trust’s assets, apart from about $30 in cash and other items. The 704.35 million-token position was valued at approximately $47.8 million using the administrator’s stated price. HBR provides price exposure through brokerage accounts without requiring investors to manage private keys.

Shares outstanding increased from 5.13 million on July 28 to 5.18 million on July 29. That 50,000-share increase was the latest reported expansion in the fund’s share count. It does not, by itself, establish the identity or strategy of the investors behind the creation.

Additionally, HBR recorded $989,000 in net inflows on July 2, its largest single-day inflow since May 15. The fund then listed roughly $49.14 million in net assets, showing that its asset value can move even when new shares enter because HBAR’s market price also changes.

Latest filing shows losses despite share growth

HBR’s first-quarter SEC filing showed 4.2 million shares outstanding and $50.34 million in net assets on March 31. The trust created 740,000 shares and recorded no redemptions during the quarter. However, HBAR depreciated 17.8% during the period, and the fund reported a $10.58 million decrease in net assets from operations.

More recent performance data remained weak. Canary listed HBR’s market-price return at negative 37.32% for 2026 through July 29 and negative 63.32% since inception. Its net asset value return was negative 36.48% year-to-date.

In the latest market data available early July 31, HBR traded near $9.33, while HBAR changed hands around $0.0727. Those figures show current pricing only and do not prove that Canary’s July 30 post caused any market move.

Enterprise and tokenization claims need context

Canary said HBR gives registered access to a network governed by organizations including Google and IBM. The Hedera Council says its members run network nodes, vote on governance matters and approve technology updates. Its structure uses equal voting rights and term limits.

The asset manager also called HBR “built for the next wave of real-world asset tokenization.” That is a forward-looking marketing claim rather than a verified forecast. One related development has already occurred: Archax tokenized the HBR ETF on Hedera and completed an after-hours transaction on Nov. 27, 2025, according to a Hedera case study.

That blockchain transaction did not change how ordinary Nasdaq investors buy and sell HBR shares. It instead demonstrated a separate tokenized representation handled through regulated market infrastructure.

What investors should watch next

HBR is structured as a single-asset trust, not an investment company registered under the Investment Company Act of 1940. Canary warns that the product is not diversified and that investors could lose their entire principal. The trust currently lists BitGo Trust Company and Coinbase Custody Trust Company as its digital-asset custodians.

Investors will next look for the quarterly SEC filing covering the period ended June 30. That report will provide fuller figures for share creations, redemptions, expenses and changes in the trust’s HBAR position. Until then, daily holdings, share counts and net assets provide the most current official measures of fund activity.

HBR’s history also matters when assessing Canary’s new promotion. In related coverage, crypto.news reported on the fund’s path to launch in October 2025. The July post therefore renews attention around an existing product rather than introducing a new U.S. HBAR ETF.

Amazon Analysis: Strong Earnings Coincide with a Breakout from the Correction

Elly De La Cruz sparks Reds’ walk-off win over Pirates

Hospital parking hike in Essex only adds stress, patients say

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Brooks Brothers

-

Sports4 days ago

Sports4 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business1 day ago

Business1 day agoWhy Trees Belong on the Risk Register

-

Tech4 days ago

Tech4 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World5 days ago

Crypto World5 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics4 days ago

Politics4 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Entertainment7 days ago

Entertainment7 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

Politics3 days ago

Politics3 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos4 days ago

News Videos4 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Business2 days ago

Business2 days agoMajor shareholder moves on Canyon

-

Crypto World5 days ago

Crypto World5 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

News Videos18 hours ago

News Videos18 hours agoBitcoin Enters the 3rd Stage of the Bear Market

-

Politics5 days ago

Politics5 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Entertainment2 days ago

Entertainment2 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Entertainment5 days ago

Entertainment5 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

Crypto World2 days ago

Crypto World2 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech6 days ago

Tech6 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

News Videos2 days ago

News Videos2 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics14 hours ago

Politics14 hours agoLuke Littler’s dominance sparks GOAT debate

-

Tech3 days ago

Tech3 days agoNew macOS Sequoia & Sonoma security updates for older Macs

You must be logged in to post a comment Login