Crypto World

Polymarket’s 5-cent signal was the only thing that got the Netanyahu rumors right

The rumor followed a familiar wartime script. Iran’s Islamic Revolutionary Guard Corps claimed it had struck Benjamin Netanyahu’s office. Then came the forged screenshots — fake posts from the Israeli prime minister’s official account announcing he was dead. Then came the AI furore over a low-resolution freeze-frame from a press conference that, at the right angle, appeared to show Netanyahu’s right hand sporting six fingers, leading contrarian commentators to take victory laps.

Conservative influencer Candace Owens amplified the claims loudly on X, demanding to know where Netanyahu was and why his office was “releasing and deleting fake AI videos.” Iran’s Tasnim News Agency — run by the Islamic Revolutionary Guard Corps — published an article titled “New Video of Netanyahu Proves Fake,” cataloguing alleged clear signs that a subsequent coffee shop clip, posted by Netanyahu’s own account to debunk the rumors, was itself generated by artificial intelligence. The conspiracy had become self-sealing; every refutation was recast as fresh evidence.

But while the fact-checkers scrambled and the podcasters speculated, one data source offered a clean, immediate signal. On Polymarket, the world’s largest crypto prediction market, the contract for “Netanyahu out by March 31” was trading at around 4 to 5 cents, implying a roughly 4 to 5% probability of him leaving office before the end of the month. The market didn’t move. For anyone paying attention to that number, the entire conspiracy theory collapsed in a single glance.

A record-breaking backdrop

To understand why the Netanyahu conspiracy took hold when it did, you need to understand the information environment it emerged from.

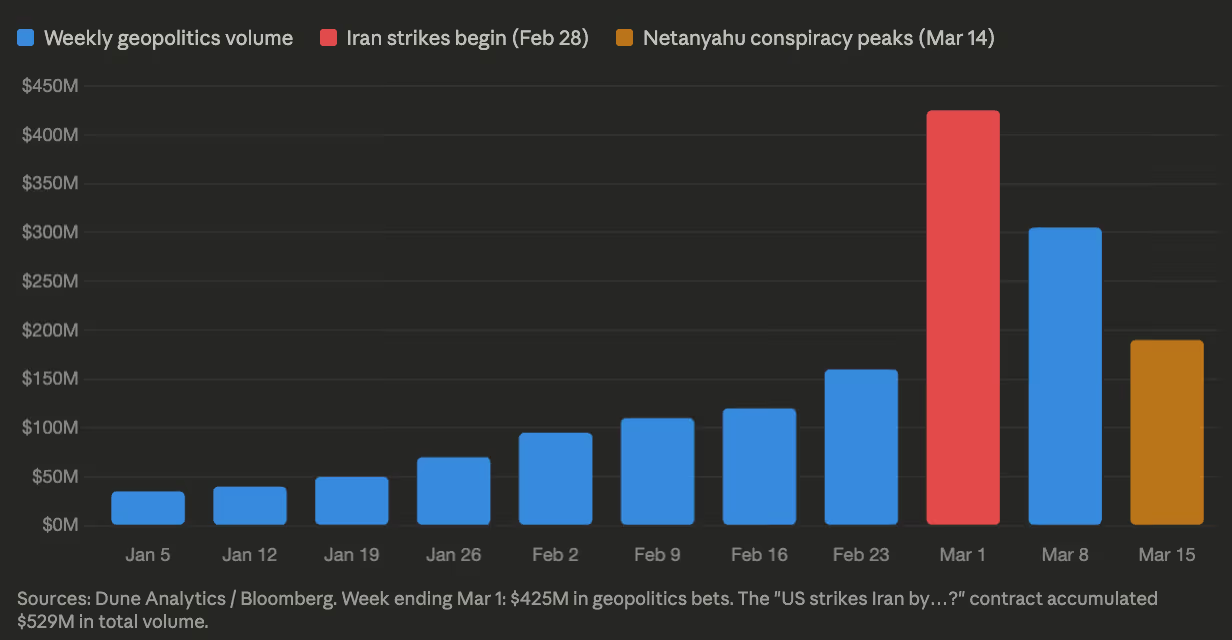

Since the U.S. and Israel launched strikes on Iran on Feb. 28, Polymarket has been transformed into something closer to a real-time geopolitical intelligence terminal. In the week ending March 1, bettors placed $425 million in geopolitics wagers on the platform alone — up from $163 million the prior week — with total platform wagering hitting a record $2.4 billion. The “US strikes Iran by…?” contract accumulated $529 million in total volume, making it one of the largest single markets Polymarket has ever hosted and the fourth-largest in its entire “Politics” category.

It is a remarkable trajectory for a platform that processed $73 million in total trading volume in 2023 and was pushed offshore by a CFTC settlement a year later. By 2025, Polymarket had processed approximately $22 billion in notional trading volume across the year — a figure that underscores how quickly the platform has moved from crypto curiosity to mainstream financial infrastructure.

This is no longer a crypto curiosity. In October 2025, the Intercontinental Exchange, parent company of the New York Stock Exchange, invested $2 billion into Polymarket at a $9 billion valuation, and launched a “Polymarket Signals and Sentiment” tool that feeds real-time prediction market data directly to Wall Street trading desks. When the Iran war began, equity and oil futures markets were closed for the weekend. Polymarket was not.

The market as instant truth machine

Prediction markets don’t have death contracts in the conventional sense. What Polymarket offers instead are “politician out by X date” markets, which resolve “Yes” if a leader resigns, is removed, or steps down. They don’t directly price the probability of death. But in a context where the conspiracy theory is that Netanyahu has been killed and the government is conducting a cover-up, these contracts function as a powerful proxy.

The logic is simple. A leader who has died or been incapacitated cannot indefinitely run a country from office. Eventually, a resignation, a removal or a credible leak would surface. And if any of that happened, the payout on a “Yes” share at 5 cents would be enormous: a $1 payout on a 5-cent share is a 20-to-1 return.

One trader was willing to make that bet at scale. A single Polymarket account placed $151,000 on Netanyahu being out before March 31, accumulating nearly 3.8 million shares at 4.7 cents each. If correct, the position would pay out $3.8 million. It is currently underwater by roughly $26,000.

That number is the ceiling of rational conviction in the conspiracy. At the height of the online hysteria, the most aggressive speculator on record was willing to stake $150,000 on the theory — implying he knew the odds were long. The market as a whole put the probability at around 5%. Social media said it was certain. The money said otherwise.

“Whether a politician is in or out of office is a very economically meaningful outcome for a lot of people,” said Aaron Brogan, a managing attorney at Brogan Law who has advised on prediction market regulation. “These are exactly the kinds of markets that event contract rules were designed to accommodate.”

Why the odds are hard to fake

The 2024 US election cycle offered a masterclass in prediction market efficiency — and the limits of efforts to dismiss its signals. When Polymarket showed Donald Trump trading at a substantial premium over Kamala Harris, critics cried manipulation. A French trader, they alleged, had artificially pumped Trump’s odds using multiple accounts for political purposes.

The experts weren’t buying it. As Flip Pidot, co-founder of American Civics Exchange, told CoinDesk at the time: a true manipulator trying to move the price would simply pile in blindly and let themselves get filled at worsening prices. The French trader did the opposite — splitting orders strategically across accounts to minimize slippage. That is what profit-seeking looks like, not propaganda.

The deeper reason manipulation struggles to stick is expected value arbitrage. If a price is artificially depressed or inflated, profit-hungry traders pile in to exploit the gap until it closes. Cross-market arbitrage reinforces this: Polymarket prices in real time against Kalshi, Betfair, and others. If odds drift meaningfully out of line across platforms, traders immediately sell the higher price and buy the lower one, synchronizing markets toward a consensus.

Harry Crane, a statistics professor at Rutgers University who studies prediction markets, sees the Netanyahu episode as a near-perfect illustration of this dynamic. “These markets are an antidote to propaganda precisely because their resolution rules anchor outcomes to verifiable sources rather than narrative,” he told CoinDesk. “I understand why governments want to limit them — not because of concerns over leaking classified information, but because verifiable price signals are harder to control.”

That framing maps directly onto the Netanyahu conspiracy. The people claiming he was dead were doing structurally the same thing as those who cried Polymarket was rigged in 2024: attacking the signal rather than engaging with it.

What the market is actually pricing — and what it isn’t

Crane is careful about the limits of the signal, and his caveat is worth sitting with.

“The market is only pricing the probability that Netanyahu is verifiably out of office under these rules,” he said. The resolution criteria state that the contract resolves “Yes” if Netanyahu announces his resignation or is otherwise removed from office, confirmed by official sources or a consensus of credible reporting. If a government concealed a leader’s death so completely that no credible source ever confirmed it, the market could resolve “No” — faithfully, correctly under its own rules, and yet without capturing the underlying reality.

That dynamic was playing out in real time. Domer — a well-known prediction market trader who goes by ImJustKen online — was publicly holding a No position on Netanyahu leaving office before March 31. Not because he was certain Netanyahu was alive, but because he didn’t believe a departure would ever be confirmed under the market’s resolution criteria, even if it occurred. He was pricing the verification gap, not the conspiracy itself.

But that caveat reveals something important about the conspiracy itself. The Netanyahu death rumor only holds together if you believe in a cover-up so total — encompassing Israeli officials, international media, independent fact-checkers, and Netanyahu’s own social media accounts simultaneously — that no verifiable evidence would ever surface. At that point, the conspiracy has become unfalsifiable by design. An unfalsifiable claim is one no rational actor should stake capital on.

This is the key distinction from traditional fact-checking. A fact-checker requires institutional credibility, research time, and editorial process — all of which conspiracy theories are engineered to preemptively undermine. A Polymarket price requires none of that. It requires only that someone, somewhere, believes the opposite enough to put real money on it. When no one does, that is its own kind of proof.

The contrast case: Khamenei

The clearest evidence that these markets work as a truth signal — and not merely as a null result — is what happened with the Khamenei contract.

When Iranian Supreme Leader Ali Khamenei was killed in the February 28 strikes, the “Khamenei out as Supreme Leader by March 31” contract on Polymarket behaved exactly as you would expect from an efficient market. It had hovered between 25% and 50% through January and February as tensions built, pricing genuine uncertainty about an escalating conflict. Then, when Iranian state TV confirmed his death, it spiked vertically to 100%. The contract drew $45 million in volume. The top trader made $757,000 on a yes bet. Four others cleared six figures.

The Netanyahu market did not do this. It stubbornly remained below 5 cents throughout the conspiracy cycle. The crowd that correctly priced Khamenei’s death — and got paid for it — looked at the Netanyahu claims and declined to move.

The regulatory storm gathering overhead

The informational value of these markets is being stress-tested at exactly the moment when political pressure against them is reaching its peak.

When Khamenei was killed, Kalshi — Polymarket’s CFTC-regulated rival — invoked a “death carveout” buried in its contract terms, settling its Khamenei positions at the last traded price before his death: roughly 39.5 cents rather than the full dollar. Polymarket, which carries no such carveout, paid out in full. A $54 million class action lawsuit against Kalshi followed.

The inconsistency in Kalshi’s approach has been pointed out sharply. In late 2024, Kalshi had run a market on whether a 100-year-old Jimmy Carter would attend Trump’s inauguration. When Carter died before it took place, Kalshi settled that contract to “No” — resolving a market directly via death, without invoking any carveout. As Crane has noted, the application of its death carveout appears to have been selective: they settle on death, just not when it’s expensive.

Kalshi disputes the characterization. “Our rules were clear from the beginning, we never changed them, and we settled based on the rules,” a spokesperson said. The company added that it reimbursed all fees and net losses out of pocket following the Khamenei settlement — “to the tune of millions of dollars” — ensuring no user lost money on the market. “Kalshi is a peer-to-peer exchange and does not profit from user losses. We have no incentive not to pay out our users, but we need to follow the rules of the exchange and the rule of law.”

On the legislative push, the company struck a conciliatory tone. “Kalshi already bans insider trading and markets directly tied to death and war,” a spokesperson said. “As a US-based exchange, we support regulators and policymakers from both sides of the aisle in their efforts to keep these markets safe and responsible in America.”

Kalshi declined to comment on record about the consistency of the death carveout as applied to the Khamenei contract versus the Carter market, or on the current status of the class action lawsuit.

Six Democratic senators, led by Adam Schiff, have written to the CFTC demanding a categorical ban on contracts that “resolve upon or closely correlate to an individual’s death.” Separately, senators Merkley and Klobuchar have introduced the End Prediction Market Corruption Act, which would bar the president, vice president, members of Congress, and their immediate families from trading event contracts, and impose fines and profit clawbacks for violations — citing the well-timed wagers on US strikes and Iranian leadership changes that netted some traders hundreds of thousands of dollars.

Blockchain analytics firm Bubblemaps identified six newly created wallets that collectively netted $1.2 million betting on the timing of US strikes on Iran, with accounts funded within 24 hours of the attack. One trader turned roughly $60,000 into nearly $500,000.

Brogan is skeptical that the legislative push has the momentum to land. “This is largely Democratic senators using the legislative process to generate political capital,” he said. “The conditions under which that legislation actually passes are where something really calamitous happens — some kind of market collapse or scandal that forces politicians to make an example of the industry. Without that, I don’t think there’s sufficient political capital to move it.”

He also draws a clear distinction between Polymarket’s legal exposure and Kalshi’s. “The restrictions Kalshi faces are not directly applicable to Polymarket,” Brogan said. Polymarket is not a CFTC-regulated US exchange — a status that stems from a 2021 settlement that pushed it offshore and barred US users from accessing it directly. That remains its largest single legal exposure, Brogan noted, though he pointed out that the Trump administration has shown little appetite for pursuing the kind of action the Biden administration explored against Polymarket CEO Shayne Coplan in early 2025.

Crane, for his part, is unambiguous about what would be lost if the legislative push succeeded. “These markets have genuine informational value and can counter propaganda,” he said. “That’s the case study here — a market involving war and the fate of a political leader doing exactly what its critics say it shouldn’t exist to do.”

There is also a state-level front opening up. Arizona recently charged Kalshi with operating an illegal gambling operation — part of a broader conflict between states that regulate and tax traditional gambling markets and federally-overseen prediction markets that sit outside their control. “The question that ultimately matters is whether federal law will preempt state law on this,” Brogan said. “There are courts hearing that question right now.”

What the crowd gets right — and what it can’t fix

None of this is to say prediction markets are infallible. Crane notes that nearly 25% of Polymarket’s historical volume has been attributed to wash trading — artificial activity generated by users trying to position themselves for a potential token airdrop — a figure that Columbia University researchers found peaked at around 60% in December 2024 before falling sharply. Wash trading inflates headline volume without necessarily biasing prices, but it is a legitimate caveat to the “wisdom of crowds” narrative.

The more fundamental limitation is what Crane identified in his answer to the manipulation question: a sufficiently coordinated disinformation campaign could, in theory, move a market — especially a smaller one. The Netanyahu “out by March 31” contract had enough liquidity to make that expensive, but not impossible.

What prediction markets cannot do is replace the underlying information infrastructure they depend on. They resolve against credible sources. If those sources are corrupted or silent — as Iranian state media clearly was throughout this episode — the market’s signal is only as good as the resolution criteria it is anchored to.

But in the Netanyahu case, that is precisely where the conspiracy fell apart. The rumor required a cover-up so comprehensive that no Israeli official, no international journalist, no independent fact-checker, and no market trader with real money on the line would ever find confirmation. The market priced that scenario at 5 cents. It was right.

When Candace Owens was demanding to know where Bibi was, Polymarket already had an answer. It just costs a few pennies to read it.

TLDR:

- Bitcoin shows its longest decoupling from equities since 2020 amid ongoing macro uncertainty.

- A major liquidation event erased months of open interest in a single trading session.

- While equities held firm, Bitcoin continued to decline due to market-specific pressures.

- Correlation shifts reveal changing dynamics between crypto and traditional financial markets.

Bitcoin has entered its longest period of divergence from the S&P 500 since 2020, following a sharp market disruption.

While equities maintained strength during this period, Bitcoin continued its decline, reflecting a shift in correlation patterns between crypto and traditional markets.

The separation became more visible after October, when both markets began moving in different directions. Bitcoin lost momentum, while equities remained near their highs.

This divergence has now persisted for several months, marking a rare phase in recent market cycles.

Liquidation Event Reshapes Market Structure

Market data shows that Bitcoin’s recent decline began after a large liquidation event on October 10. Nearly 70,000 BTC in open interest was wiped out within a single session. This reset brought derivatives exposure back to levels last seen in April 2025.

The sudden unwind erased more than six months of accumulated positions. As a result, market structure weakened, leading to sustained selling pressure. Bitcoin failed to recover alongside equities, marking a clear break from earlier synchronized movements.

A tweet from Darkfost noted that Bitcoin entered a bear phase during this period. At the same time, the S&P 500 continued to perform, creating a visible gap between the two markets. This separation has now extended longer than any similar period seen since 2020.

In addition, the removal of leveraged positions reduced short-term upward momentum. Traders became more cautious, while liquidity conditions tightened. As a result, Bitcoin struggled to regain strength even during brief market rebounds.

Correlation Breakdown Signals Market Shift

Historically, Bitcoin and equities have shown periods of strong alignment, especially during liquidity-driven cycles. However, the current phase reflects a breakdown in that relationship. Correlation levels have dropped toward neutral or negative territory in recent months.

Bitcoin’s continued decline has been linked to broader geopolitical tensions affecting global markets. Even so, equities remained resilient for most of this period. This contrast reinforced the ongoing divergence between the two asset classes.

The divergence suggests that crypto markets reacted earlier to tightening conditions. While equities showed delayed weakness, Bitcoin had already adjusted through price corrections. This pattern aligns with previous cycles where crypto moved ahead of traditional assets.

At the same time, Bitcoin’s higher volatility has made it more sensitive to sudden shocks. The recent liquidation event amplified this effect, accelerating downside movement. Meanwhile, equities absorbed similar pressures more gradually and with less volatility.

As the correlation weakens, market participants continue to monitor whether alignment will return or divergence will persist. Current conditions suggest that both assets are responding differently to evolving macroeconomic pressures.

Crypto World

US Senators and White House Reach Tentative Deal to End Bank-Crypto Stablecoin Yield Clash

TLDR:

- Senators Tillis and Alsobrooks reached a White House-backed agreement in principle on stablecoin yield language.

- The deal proposes barring yield payments on passive balances to address bank concerns over deposit flight.

- White House adviser Patrick Witt called the agreement a major milestone toward passing the CLARITY Act.

- The agreement still requires vetting from banking and crypto industry groups before any final deal is confirmed.

Stablecoin regulation in the United States may be edging closer to a major breakthrough. Key senators and White House officials have reached a tentative agreement on crypto legislative language.

The deal addresses a long-standing clash between banks and digital asset firms over yield payments. Sen. Thom Tillis (R-N.C.) and Sen. Angela Alsobrooks (D-Md.) spearheaded the agreement. Their deal could unlock a path forward for landmark crypto legislation stalled since January.

Senators Bridge Partisan Divide Over Stablecoin Yield

The central dispute in this legislation has been about yield payments to stablecoin holders. Banks and Wall Street groups raised concerns about widespread deposit flight from traditional accounts.

They argued that stablecoin yield rewards could pull customers away from conventional banking products. The clash had been keeping the crypto bill stalled in the Senate Banking Committee since January.

Both Tillis and Alsobrooks acknowledged those banking concerns throughout the negotiation process. Alsobrooks confirmed the two senators have reached a deal, stating, “Sen. Tillis and I do have an agreement in principle.”

She added that the deal seeks to “protect innovation” while also giving lawmakers the opportunity to “prevent widespread deposit flight.” Her comments came during a Friday interview following talks with White House officials.

The new language is expected to target yield payments made on a passive balance. Alsobrooks confirmed the proposal will seek to bar yield payments “on a passive balance,” though full details remain undisclosed.

The specifics are still being worked through as lawmakers prepare to share the language with industry stakeholders.

Tillis echoed a cautiously optimistic tone when speaking about the progress made. “In working with the White House, I think we have an agreement,” he said in a separate interview.

He noted that the next step is to vet the language with industry, describing them as “a party to an ultimate deal.” He added that he feels “like we’re in a good place” with where negotiations currently stand.

White House Endorses Deal as Industry Review Awaits

The White House played an active role in brokering the tentative stablecoin agreement. Patrick Witt, a top White House crypto policy adviser, publicly addressed the development on X.

He credited both Tillis and Alsobrooks “for bridging the partisan divide to tackle a difficult issue.” His public comments came shortly after the story of the agreement was first published.

Witt also acknowledged in his post that more work remains before the bill is finalized. He wrote that there is “more work to be done to close out this and other outstanding issues.”

Despite that, he described the development as “a major milestone toward passing the CLARITY Act.” That bill has been held up in part due to the ongoing bank-crypto yield dispute.

Still, the agreement does not guarantee automatic support from the banking and crypto industries. Both sectors will need to review the final language before giving any formal endorsement.

Industry groups on both sides have strong interests in the outcome of this legislation. Any final version of the bill will need broad backing from both sectors to pass.

The coming weeks will be critical in determining whether the CLARITY Act can advance. Senators and White House officials will continue working to address any remaining sticking points. A finalized agreement could clear the way for a vote in the Senate Banking Committee.

TLDR:

- Whale unrealized profit ratios remain between 1 and 1.5, showing balanced market positioning without excess pressure

- Historical data links low whale profit zones with accumulation phases and the start of upward price trends

- No spike above 3 suggests Ethereum has not reached overheated conditions seen in past cycle peaks

- Current structure supports gradual price growth rather than sharp rallies or immediate market reversals

Ethereum’s long-term market structure shows a steady recovery, with whale profitability pointing to a developing uptrend rather than a peak phase.

Data tracking price movements and unrealized profit ratios suggest that the market remains balanced, with no strong signs of distribution pressure.

The chart, covering 2016 through early 2026, aligns Ethereum’s price with the profitability of whale wallets. Large holders across multiple tiers appear to have returned to profit, a condition historically linked to early-cycle growth.

Whale Profitability Returns as Market Stabilizes

Ethereum’s price cycles have consistently moved alongside whale profit ratios. During previous bull runs, profit levels surged above 3, followed by sharp corrections. In contrast, bear market phases pushed ratios closer to zero, marking accumulation zones.

The current range sits between 1 and 1.5, which reflects moderate profitability. This level has previously appeared during transition periods between accumulation and expansion phases. As a result, the market structure appears stable rather than overheated.

A recent tweet by analyst CW noted that wallets holding over 100,000 ETH have moved back into profit. The tweet stated that past transitions from loss to profit often marked the beginning of upward trends. That pattern now appears to be forming again.

At the same time, earlier cycles show similar behavior. In 2019 and 2020, whale profitability remained low before gradually rising. Those phases later led to sustained price growth. The current setup mirrors those earlier conditions without showing excess momentum.

Mid-Cycle Structure Supports Gradual Price Movement

Ethereum’s present structure reflects a mid-cycle phase rather than a late-stage rally. Profit ratios have not reached extreme levels, which reduces the likelihood of immediate large-scale selling by major holders.

During the 2021 peak, profit ratios climbed above 3.5 as prices approached all-time highs. That environment encouraged distribution as whales secured gains. The absence of such levels today suggests a different market stage.

Price action between $2,000 and $3,000 aligns with this moderate profitability range. The market appears to be building strength gradually, instead of accelerating into a sharp rally. This behavior often precedes more extended upward movement.

The lack of rapid spikes in whale profit indicates steady accumulation or holding patterns. When combined with historical data, this condition has often led to continued price expansion over time.

If profit ratios begin rising toward 2.5 or higher, the market could enter a stronger growth phase. However, a sudden move above 3 would require close monitoring, as past cycles show such levels near turning points.

As of this writing, the structure remains balanced. Whale profitability supports a developing trend without signaling overheating. As a result, Ethereum appears positioned within an early growth phase rather than nearing a cycle peak.

TLDR:

- Every Pi Network DApp must lock Pi Coin as collateral before minting its own custom token.

- More DApps launching on Pi Network means more Pi Coin gets locked, reducing circulating supply over time.

- Pi Coin is being positioned as base money for the ecosystem, similar to how the USD functions globally.

- Pi traded at $0.1981 with a 3.45% price gain in 24 hours, reflecting growing market interest.

Pi Network is drawing attention as decentralized applications continue building on its blockchain. Each DApp introduces its own token economy, yet all remain anchored to Pi Coin as base collateral.

DApp Tokens on Pi Network Serve Distinct Economic Roles

Pi Network hosts a growing number of decentralized applications across gaming, e-commerce, and finance sectors. Each application operates its own token to manage incentives within its specific user base.

Gaming apps distribute reward tokens to active players on the platform. Shopping platforms issue loyalty points and digital vouchers to their customers.

Running all DApp activity exclusively on Pi Coin would create tokenomics management challenges. Custom tokens give each application the freedom to structure its own economy independently.

This separation allows developers to innovate without disrupting the broader Pi Network supply. The design supports diverse use cases while keeping Pi Coin’s central role intact.

According to a post by @fireside_pi on X, the Pi Core Team follows a clear strategic direction. “Each DApp runs its own mini-economy, needs its own token for flexibility,” the post stated.

This structure mirrors how layers in traditional financial systems operate. Base assets provide collateral while upper layers handle specialized transactions.

The token model benefits developers and users across the ecosystem simultaneously. Developers gain flexibility in designing reward systems suited to their platforms.

Users receive access to airdrops, staking opportunities, and platform-specific incentives. Pi Coin remains the foundational asset supporting every transaction layer above it.

Pi Coin Scarcity Increases as DApp Collateral Requirements Grow

Every DApp launching on Pi Network must lock an equivalent amount of Pi Coin as collateral. This mechanism directly reduces the circulating supply of Pi Coin over time.

As more applications succeed and expand, more Pi Coin gets permanently locked away. A shrinking supply combined with steady demand supports upward price pressure.

The @fireside_pi post described this as Pi Network’s path toward becoming base money for billions. “More DApps launching and succeeding means more Pi gets locked forever,” the post noted.

The comparison drawn is to how the US dollar serves as a global reserve currency. Pi Coin is positioned to fill that same foundational role within its own ecosystem.

At the time of writing, Pi Network’s price stood at $0.1981 per coin. The 24-hour trading volume reached $37,665,490, reflecting active market participation.

Pi recorded a 3.45% price increase over the past 24 hours. However, the seven-day performance showed a marginal decline of 0.03%.

The collateral-based token model places Pi Coin at the center of all ecosystem value. Every new DApp that scales adds locking pressure on the available Pi supply.

This creates a direct structural relationship between ecosystem growth and Pi Coin’s scarcity. Holders of Pi Coin stand to benefit as the network continues to expand.

Crypto World

Jerome Powell Honored With Paul Volcker Public Integrity Award at ASPA Annual Conference

TLDR:

- Jerome Powell received the Paul Volcker Public Integrity Award at the ASPA Annual Conference via video.

- Powell called Volcker the greatest public servant in economics, citing his non-partisan service under four presidents.

- Volcker held firm against political pressure in the 1980s, ultimately defeating double-digit inflation through high interest rates.

- Powell closed with a defining line: integrity is the foundation of every public servant’s lasting legacy and credibility.

Jerome Powell, Federal Reserve Chair, received the Paul Volcker Public Integrity Award at the ASPA Annual Conference.

Powell accepted the honor via a pre-recorded video, expressing deep gratitude for the recognition. He drew on Volcker’s legacy to reflect on core principles of public service.

His remarks centered on independence, integrity, and the courage to resist short-term pressures. The ceremony honored Powell’s commitment to non-partisan central banking leadership.

Powell Draws on Volcker’s Record of Non-Partisan Service

Jerome Powell described Paul Volcker as a towering figure in economics and central banking. He called Volcker “perhaps our greatest public servant in the economic arena.”

Volcker served at the Treasury under Presidents Kennedy, Johnson, and Nixon before leading the Federal Reserve. He chaired the Fed from 1979 to 1987, nominated by Carter and reappointed by Reagan.

Powell noted that non-political, non-partisan service forms the bedrock of the Federal Reserve. No one embodies that virtue more fully than Paul Volcker, he added.

Such service allows public institutions to earn lasting trust from leaders across both parties. Moreover, it gives those institutions the credibility needed to act in the broader public interest.

Volcker’s record of serving multiple presidents without compromising his principles stood out throughout Powell’s remarks.

That kind of commitment, Powell argued, defines what true public integrity means. It also shows how non-partisan dedication can produce results that outlast any single administration. Trust built steadily over time creates the space needed for bold and necessary decisions.

Powell further stated that “independence and integrity are inseparable.” He explained that public servants need independence to do what is right.

Integrity, in turn, ensures that independence is used wisely and not for personal gain. Together, these qualities define the standard Volcker set across his entire career.

Volcker’s Inflation Battle as a Lesson in Long-Term Leadership

Volcker’s defining test came during the double-digit inflation crisis of the early 1980s. Unemployment climbed above 9 percent, and critics loudly called for a change of course.

Yet Volcker held firm, committed to bringing inflation down through sustained high interest rates. His decision was painful in the short term but ultimately restored price stability.

Powell referenced a speech Volcker delivered at the Economic Club of Chicago on May 19, 1982. Speaking with unemployment above 9 percent, Volcker acknowledged “the pain of wringing out inflation through high interest rates.”

He also outlined the prospect of “a return to price stability, and with it a much brighter future.” That vision, Powell noted, ultimately proved correct.

Volcker’s resolve helped launch what economists now call the Great Moderation. This was a prolonged period of low inflation and steady, consistent economic growth.

Powell gave Volcker considerable credit for that outcome. Resisting short-term pressure, he argued, can yield lasting benefits for the broader economy.

Powell closed by quoting directly from his own acceptance remarks: “In the end, our integrity is all we have.” He framed Volcker’s career as the clearest living example of that principle.

Each public servant, he said, should look back and know they did the right thing. That standard, Powell argued, remains the truest measure of a life in public service.

The U.S. securities and commodities watchdogs have jointly published guidance that for the first time attempts a formal taxonomy for digital assets. Market observers welcomed the move as a material shift away from the prior Gensler-era posture, with Galaxy Digital’s Alex Thorn framing it as a step toward pragmatic regulation even as it stops short of giving permanent, court-binding rules.

The SEC guidance, issued this week, lays out a five-category framework for digital assets: digital commodities, digital collectibles like NFTs, digital tools, stablecoins, and tokenized securities. The document describes how these assets may fit under existing laws and where each category might draw regulatory lines. The fact sheet accompanying the guidance highlights the five buckets and how they align with the agency’s broader remit, while the linked materials emphasize that the interpretation is aimed at clarifying how the law applies rather than rewriting it.

The distinction matters enormously under the Administrative Procedure Act. A legislative rule or substantive rule goes through notice-and-comment rule-making, has the force and effect of law, and binds both the agency and regulated parties. The interpretive rule, by contrast, is exempt from those procedures and does not carry the same binding force for courts or firms.

In practical terms, the interpretive rule signals that the agencies are prioritizing clarity over breadth in the near term. It is not a binding mandate that courts must enforce; rather, it sets out how regulators currently interpret existing statutes and how they might apply them to different digital-asset structures. For the crypto industry, that creates a more predictable operating environment over the next several quarters, even as the longer-term regulatory architecture remains to be finalized.

Galaxy’s Thorn emphasized that while the interpretive stance provides meaningful guidance for the next 30 months, the broader path to stable, enduring regulation hinges on Congress codifying the CLARITY Act into law. The CLARITY framework is designed to codify market structure principles for crypto assets, but has stalled in recent months amid disagreements over stablecoin yield, open-source software protections, and other DeFi-related provisions. Thorn noted that while the new interpretive rule reduces immediate regulatory risk, a formal law would lock in a durable framework for decades to come.

The CLARITY Act stalls, but whispers of a possible deal surface

The push to pass a comprehensive crypto-market-structure bill faces political headwinds. In January 2025, industry insiders and lawmakers raised concerns that the CLARITY Act would hamper DeFi development through broad reporting and KYC requirements, and could restrict stablecoin operations. The industry’s pushback centered on provisions seen as disproportionate or technically onerous for decentralized finance and open-source tooling, even as they sought clearer guardrails against fraud and market manipulation. A recent Politico live update reported that a tentative agreement between the White House and lawmakers is being pursued to move the bill forward, though many specifics remain under wraps.

Public reporting on the deal suggests discussions include a potential ban on stablecoin yield from passive balances, a point highlighted by Senator Angela Alsoboorks as part of the ongoing negotiations. The broader question remains: can legislators craft a framework that satisfies consumer protections and financial stability concerns without stifling innovation in DeFi and open-source crypto tooling? Coverage from Cointelegraph notes that any final agreement will need careful balancing of these competing priorities, with industry observers watching for hidden provisions that could alter DeFi, custody, and settlement rights for participants across the ecosystem.

Industry observers view the potential deal as a litmus test for how aggressively regulators and lawmakers intend to police the sector while still enabling mainstream crypto adoption. The unfolding talks underscore a broader tension: the desire for a predictable, codified regime versus the organic, global nature of decentralized technologies. As policymakers debate stablecoin yield limits, disclosure standards, and on-chain compliance tools, market participants are parsing what a new law would mean for issuance, trading venues, and developer incentives alike.

What comes next for regulation and market structure

Today’s guidance represents a significant milestone in regulatory clarity, but it is not the final destination. Investors and builders now have a clearer benchmark for evaluating where a given asset sits within the SEC-CFTC taxonomy, and how existing securities and commodities laws might apply. Yet crucial questions remain about how the CLARITY Act will shape the long-term architecture of the crypto market, particularly in the DeFi space, where permissionless innovation has been a defining feature of the sector’s growth.

In practical terms, the new interpretive rule affords the industry a clearer window for planning and compliance over the next couple of years, while lawmakers push for a more permanent framework. This separation—clarity in the near term, codified law in the longer term—could help reduce the kind of regulatory guesswork that has previously unsettled projects, exchanges, and users. Still, until the CLARITY Act is enacted, firms must operate with the underlying statutes in mind and be prepared for future amendments that could reshape how tokens are treated, how disclosures are required, and how on-chain activity is monitored.

As the regulatory conversation evolves, observers will watch for signs of how the White House and Congress resolve key points of contention, including stablecoins, developer protections, and the balance between consumer safeguards and innovation-friendly policy. The next few months should yield a clearer picture of whether a bipartisan framework can emerge that satisfies financial-stability concerns while preserving the open, collaborative ethos that underpins much of the crypto ecosystem.

Readers should keep an eye on official updates to the CLARITY Act and related regulatory proposals, as well as the ongoing enforcement posture from the SEC and CFTC. The coming months will likely reveal whether the interpretive guidance suffices as a transitional tool or if a broader legislative settlement becomes indispensable for sustainable growth in the digital-asset economy.

Crypto World

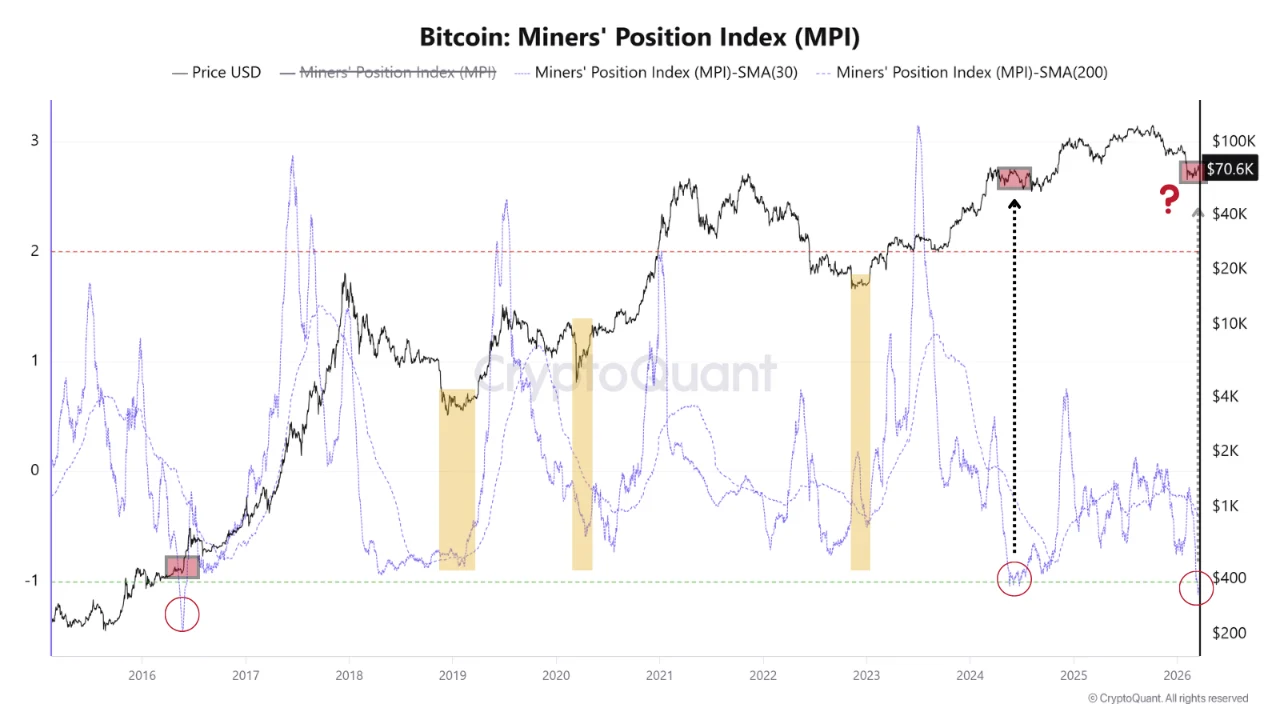

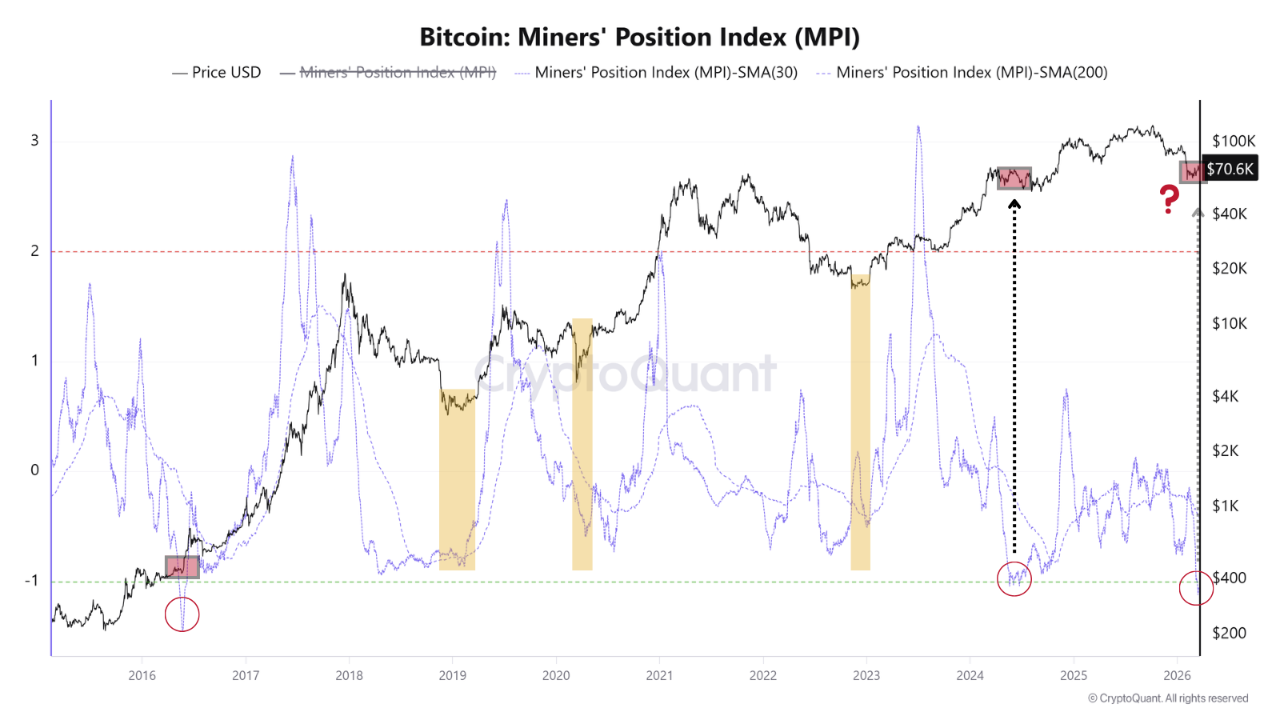

Bitcoin Miners’ Position Index Hits Historic Low: Strength Signal or Early Warning Sign?

TLDR:

- Bitcoin Miners’ Position Index has dropped to -1.04, marking one of the lowest readings in its recorded history.

- Extreme low MPI reflects minimal miner selling pressure, suggesting miners may be holding rewards in anticipation of higher prices.

- Historically, Bitcoin price recoveries emerged as MPI rose from depressed levels, not at the moment it hit its floor.

- Low MPI removes a key structural headwind, but sustained price movement still depends on demand-side confirmation signals.

Bitcoin’s Miners’ Position Index (MPI) has fallen to -1.04, one of the lowest readings ever recorded in its history. This is only the third time the 30-day moving average has neared the -1 threshold.

At this level, miners are sending far fewer coins than their one-year average reflects. The sharp drop in outflows raises a critical question across the market: does extreme miner inactivity signal quiet accumulation and strength ahead, or does it mask a deeper structural warning?

The Case for Hidden Strength Behind Miner Inactivity

When miners hold block rewards rather than move them to exchanges, sell pressure from one of Bitcoin’s most consistent natural sellers drops sharply.

The Miners’ Position Index measures outflows against a one-year historical average, and a reading of -1.04 places current miner behavior near the bottom of its entire recorded range. That level of restraint does not happen frequently.

Analyst MorenoDV_ noted the reading publicly, describing it as one of the lowest MPI prints in Bitcoin’s history. He pointed out this is only the third time the 30-day moving average has approached the -1 mark.

Source: Cryptoquant

According to his analysis, miners appear to be either accumulating block rewards or anticipating higher prices ahead.

From a supply perspective, reduced miner distribution removes a persistent structural headwind. Miners have long represented a consistent source of selling in the market, given their need to cover operational costs. When that flow dries up at this scale, available sell-side supply contracts meaningfully.

That contraction does not guarantee price appreciation on its own. However, it does create conditions where demand-side forces face less resistance.

In that context, extreme miner inactivity can reasonably be read as a quiet form of market strength rather than passive behavior.

The Silent Warning Embedded in Extreme Low MPI Readings

Historical patterns complicate any straightforward bullish reading of extreme low MPI levels. Most Bitcoin cyclical price lows did not form precisely at the moment MPI hit its floor.

Instead, price recoveries tended to emerge as the metric began rising from those depressed levels, not while it sat at the bottom.

Extreme low MPI readings have also historically coincided with periods of miner stress, compressed margins, and macro uncertainty.

That context matters. Inactivity at this scale can reflect miners unable or unwilling to sell, rather than miners confidently holding in anticipation of gains.

MorenoDV_ acknowledged this nuance directly in his analysis. He noted that the absence of miner selling alone cannot sustain upward momentum without clear demand expansion.

Spot flows, ETF inflows, and derivatives positioning all remain necessary catalysts that MPI does not capture.

The signal becomes more actionable when MPI begins recovering from these lows alongside improving market conditions.

Until that recovery takes shape, extreme miner inactivity sits in an ambiguous space. It reduces one headwind, but it does not confirm the demand-side engagement needed to drive a sustained directional move.

TLDR:

- OpenAI plans to nearly double its workforce from 4,500 to 8,000 employees by the close of 2026.

- Most new hires will be deployed across product development, engineering, research, and sales divisions.

- OpenAI is recruiting “technical ambassadorship” specialists to help businesses maximize its AI tools.

- A $110 billion funding round valued OpenAI at $840 billion, backing its large-scale hiring strategy.

OpenAI is reportedly planning to nearly double its workforce from 4,500 to 8,000 employees by end of 2026. The Financial Times published this report on Saturday, citing two people with knowledge of the matter.The company did not respond to a request for comment by press time.

The expansion plan targets product development, engineering, research, and sales teams. This move comes as the company continues to scale its commercial operations across global markets.

A Focused Hiring Push Across Product, Engineering, and Sales

The company plans to direct most of the new hires toward product development, engineering, research, and sales. These four areas form the core of its technical and business growth strategy.

The ChatGPT maker operates as one of the most closely watched artificial intelligence firms globally. The Financial Times report, citing insiders, notes that the hiring plan is structured around these key functions.

The company is also stepping up recruitment for “technical ambassadorship” specialists. According to the FT report, these professionals are aimed at “helping businesses make better use of its tools.” This growing role reflects a broader push toward enterprise-level client support and integration.

The ChatGPT maker recently completed a $110 billion funding round that included Big Tech companies and SoftBank’s Masayoshi Son.

That round valued the company at $840 billion, making it one of the highest-valued private companies in the world. The capital raised provides the company with the financial resources needed to sustain large-scale hiring into 2026.

Internal Code Red and Market Competition Accelerate OpenAI’s Expansion

OpenAI CEO Sam Altman reportedly issued an internal “code red” directive in early December last year. The order paused non-core projects and redirected teams toward accelerating product development timelines.

This came as a direct response to Google’s release of Gemini 3, which intensified AI competition.

The code red move showed how seriously the company responds to competitive pressure in the AI sector. Redirecting internal resources and pausing non-essential work reflects a clear change in operational priorities.

It also signals that the company treats speed of delivery as a core part of its market strategy. This approach appears to be shaping how the company plans to scale operations in 2026.

SoftBank’s Masayoshi Son joined the $110 billion round alongside several major Big Tech investors. His participation, combined with broader tech involvement, pushed the valuation to “$840 billion,” as reported by Reuters.

With that financial base secured, OpenAI is well-placed to meet its workforce targets before the end of 2026.

Crypto World

Bitcoin options signal extreme fear as downside protection premium hits new all-time high, says VanEck

Bitcoin traders are paying record prices for downside protection, according to VanEck’s mid-March 2026 Bitcoin ChainCheck, a sign that investors remain defensive even as spot prices begin to stabilize.

In the report, senior VanEck analysts said bitcoin’s 30-day average price fell 19% from the prior period, while realized volatility dropped from about 80 to just above 50.

Futures funding rates also eased to 2.7% from 4.1%, suggesting leveraged speculation has cooled.

Options markets show investors are as cautious as it gets. VanEck said the put/call open interest ratio averaged 0.77 and peaked at 0.84, the highest level since June 2021, when China cracked down on bitcoin mining.

Traders spent about $685 million on put options over the past 30 days, while call premiums fell 12% to about $562 million, the report adds. Relative to spot volume, put premiums reached roughly 4 basis points, an all-time high in VanEck’s data.

“Relative to spot volume, put premiums reached an all-time high of roughly 4 basis points, roughly 3x the levels seen in mid-2022 following the Terra/Luna stablecoin collapse and the Ethereum staking liquidity crisis,” the report reads.

That means investors are paying up for insurance against further losses.

VanEck said that kind of fear has often marked turning points rather than fresh breakdowns. The firm found that, in the past six years, similar options that skewed readings were followed by average bitcoin gains of 13% over 90 days and 133% over 360 days.

The report also points out onchain activity has remained weak while miner selling remains contained.

TLDR:

- Tether holds $141B in U.S. Treasury exposure, ranking it 17th among all global government debt holders.

- The GENIUS Act legally requires stablecoin issuers to back every token with T-bills or dollar equivalents.

- China cut $86B in Treasury holdings as Japan signals drawdown, opening demand gaps stablecoins now fill.

- Apollo projects the stablecoin market could hit $2 trillion by 2028, potentially surpassing Japan’s Treasury position.

Stablecoins have quietly become a structural component of U.S. monetary policy. Tether and Circle now hold over $160 billion in U.S. Treasury securities combined.

That total places both companies above sovereign nations, including South Korea, Germany, and Saudi Arabia. A decade ago, neither existed in any meaningful financial capacity. Today, they rank among the most consistent buyers of American government debt on the planet.

The GENIUS Act Turned Stablecoin Reserves Into a Treasury Buying Mandate

The GENIUS Act, signed into law last year, reshaped how stablecoin issuers manage their reserves. The legislation requires each stablecoin token to be backed 1:1 with verified reserves.

Those reserves must be held in U.S. dollars, Treasury bills, or short-duration equivalent instruments. Congress did not only regulate stablecoins as it also created a legal mandate to buy Treasuries at scale.

Tether currently holds $141 billion in total U.S. Treasury exposure under this structure. Of that amount, $122 billion is held directly in T-bills.

The remaining portion is parked in overnight reverse repurchase agreements. That positions Tether as the 17th largest holder of U.S. government debt worldwide.

Circle’s USDC adds another $24.5 billion in Treasury reserves to the broader picture. About 93% of Circle’s total reserves sit in overnight repos and short-term government securities.

As TFTC noted on X, “Congress didn’t just regulate stablecoins. It created a legal mandate to buy Treasuries at scale.” Together, both issuers have become a growing class of captive Treasury buyers.

Tether also reported $10 billion in profit through the first three quarters of 2025. That result surpassed Bank of America’s earnings for the same period.

It also nearly matched figures posted by both Goldman Sachs and Morgan Stanley. Tether reached that level with a workforce of approximately 300 employees.

Stablecoins Fill the Demand Gap as Traditional Foreign Buyers Pull Back

China reduced its Treasury holdings by $86 billion over the past year. Its current position has fallen to the lowest level recorded since 2008.

Japan, the largest foreign holder at $1.2 trillion, is also signaling a slow drawdown. The traditional foreign buyer base for U.S. government debt is gradually narrowing.

Stablecoins are absorbing a share of that demand in real time. Every dollar minted as USDT or USDC creates automatic buying pressure for U.S. government securities.

The dollar also gets distributed globally through crypto payment rails. This mechanism extends dollar dominance without relying on traditional diplomatic or military tools.

Apollo estimates the stablecoin sector could reach $2 trillion by 2028. At that scale, stablecoin issuers would hold more Treasuries than Japan currently does.

TFTC stated that “the U.S. government now has a structural incentive to grow the stablecoin market.” That incentive is now embedded directly into federal legislation.

The growth of stablecoins serves both crypto markets and the broader U.S. fiscal structure. Each new token minted adds to Treasury demand in a measurable and automatic way.

This dynamic was not present in any meaningful form just five years ago. Stablecoins now function as one of the most reliable buyers of American sovereign debt.

Is Hubert Davis out at UNC? Tar Heels boosters lose faith after historic loss

Apple’s foldable iPhone is coming… not just when you thought

XRP REPRICING IS COMING! – XRP AS A PETRO-BRIDGE – THE PRICE OF XRP IS UNPREDICTABLE – XRP NEWS

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

XRP REPRICING IS COMING! – XRP AS A PETRO-BRIDGE – THE PRICE OF XRP IS UNPREDICTABLE – XRP NEWS

The Freaky Truth About XRP…(Over?)

The “Financial Blockage” That Almost No One Talks About – Your Relationship to What You Want

-

Tech6 days ago

Tech6 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Fashion1 day ago

Fashion1 day agoWeekend Open Thread: Adidas – Corporette.com

-

Politics1 day ago

Politics1 day agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Tech4 days ago

Tech4 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

News Videos3 days ago

News Videos3 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Business6 days ago

Business6 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Crypto World21 hours ago

Crypto World21 hours agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Business5 days ago

Business5 days agoAustralian shares drop as Iran war enters third week

-

Crypto World5 days ago

Crypto World5 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Politics3 days ago

Politics3 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Fashion5 days ago

Fashion5 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

Tech2 days ago

Tech2 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Crypto World3 days ago

Crypto World3 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

Politics4 days ago

Politics4 days agoReal-time pollution monitoring calls after boy nearly dies

-

NewsBeat3 days ago

NewsBeat3 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

Business5 days ago

Business5 days agoMeta planning major layoffs as AI spending and automation reshape workforce

-

News Videos3 days ago

News Videos3 days agoPARLIAMENT OF MALAWI – PAC MEETING WITH REGISTRAR OF FINANCIAL ON AMARYLLIS HOTEL – INQUIRY LIVE

-

Politics6 days ago

Politics6 days ago9 Stylish Leather Jackets Perfect For Spring 2026

-

Crypto World6 days ago

U.S. Oil Companies Post Record Profits as Oil Prices Break $100

-

Entertainment5 days ago

Oscars reunite Rob Reiner supergroup of 17 stars for emotional tribute: Here's who appeared on stage

You must be logged in to post a comment Login