Crypto World

Provenance Blockchain TVL Hits All-Time High of $1.2 Billion

HELOC provider Figure Markets accounts for the network’s entire TVL.

The Provenance blockchain hit a new milestone on Wed. Feb. 11, as its total value locked (TVL) climbed to an all-time high of $1.2 billion.

This marks a 7% increase in TVL over the past 24 hours, and a roughly 570% jump since early November 2025, when TVL stood at about $179.9 million, according to DeFiLlama data.

Notably, Figure Markets is currently the only protocol tracked on Provenance by DeFiLlama, meaning the network’s entire TVL is essentially tied to Figure’s activity. Figure Markets is described as a decentralized custody platform, which offers spot trading, crypto-backed lending, and yield-bearing assets.

DeFiLlama data shows Figure Markets’ TVL at approximately $1.22 billion, with about $301 million currently borrowed. The protocol has generated roughly $3.84 million in annualized fees and revenue, while 30-day decentralized exchange volume stands at approximately $2.08 billion.

Figure Technologies, the entity behind Figure Markets and Provenance, currently leads in the tokenized private credit space, accounting for $15 billion of the market’s $20 billion active loans, per RWAxyz. The company is also the largest non-bank home equity line of credit (HELOC) originator in the U.S.

Meanwhile, Provenance’s native token, HASH, was the second-best performing token on the day, rising about 8% in 24 hours to trade near $0.018, according to CoinGecko. Figure’s HELOC token is currently trading at $1.02, down 1% on the day.

Provenance’s TVL increase comes amid renewed attention towards tokenized real-world assets (RWAs), which have grown 14% over the past month to a distributed asset value of over $24.7 billion.

Experts are Divided

Still, not everyone views the milestone as a structural breakthrough. Brian Huang, co-founder of Glider, told The Defiant that tokenizing assets on a standalone or siloed blockchain does not necessarily increase their utility.

“Assets aren’t any more useful on chain than offchain unless they have composability. Provenance has no composability,” Huang said. “Overall, I wouldn’t read into the $1.2 billion in assets. In the long term, tokenization will favor open protocols like Ethereum and Solana.”

Danny Nelson, Research Analyst at Bitwise Asset Management, took a different viewpoint, calling Provenance’s business “very real.”

“It’s the secret sauce fueling Figure Markets’ rise to become the largest non-bank home equity loan (HELOC) business in the U.S,” Nelson said. “Figure Markets purpose built Provenance Chain to handle its HELOCs.”

He explained that Figure represents all loan-related paperwork, contracts, and finances as tokens on the blockchain. “There, it can process everything much faster than a traditional lending business can,” Nelson added. “Figure is cutting the costs of creating each loan, and speeding up its processing, by handling the entire loan lifecycle on Provenance.”

Provenance’s growth follows a January announcement from Figure launching the On-Chain Public Equity Network (OPEN) on Provenance. The move allowed companies to list their equity natively on-chain.

“Unlike other tokenization efforts, OPEN equities are blockchain-registered, not a tokenized version of Depository Trust and Clearing Corporation (DTCC) securities,” the announcement reads.

Figure said its own stock will be the first public equity trading natively on the blockchain, with market makers including Jump Trading preparing to support the platform.

The Defiant reached out to Figure and Provenance for comment, but has not heard back at the time of publishing.

In the United States, victims of the $4 billion crypto Ponzi scam OneCoin are finally receiving compensation.

On April 13, the US Department of Justice said that $40 million in assets are available to anyone who purchased OneCoin between 2014 and 2019 and experienced a net loss.

This program marks a milestone for OneCoin victims, most of whom had no recourse to get back what they lost, until now. Victims in the UK attempted a class action suit in 2024, but it fell apart when litigation funding was terminated.

Few crypto schemes were as prominent as OneCoin, in terms of scale and the international intrigue that followed. Founders and associates have been imprisoned or killed, while the ringleader is still on the lam.

The Wild West of early crypto was often defined by schemes and eccentric characters, the effects of which, in the case of OneCoin, are still felt today.

OneCoin’s founding and legal troubles

In 2014, cryptocurrency was still a niche internet phenomenon. The Bitcoin white paper was only six years old, and general knowledge of cryptocurrencies and blockchain tech was limited. Still, interest in the new asset class was rising among retail investors.

From August to December 2014, Ruja Ignatova and Karl Sebastian Greenwood founded OneCoin. Initial promotions began in Europe, and soon entities popped up in Bulgaria, Dubai and Belize.

OneCoin’s structure was convoluted. Investors needed to buy packages of tokens that would allow them to “mine” OneCoin. There were several different price entry points for packages, with almost no upper limit. The most expensive, according to CoinMarketCap, was 225,000 euros.

Promoters, meanwhile, could earn commissions by bringing new investors into the program. This allowed the project to expand rapidly.

While marketed as a cryptocurrency, it was not decentralized. The coin itself was hosted on the centralized servers of OneCoin Ltd. The coins were not available for public trading and owners could only trade nominal amounts in a closed system.

The project seemed fairly suspect from the outset, but fear of missing out, as well as the massive audiences drawn by Ignatova at seemingly above-board conferences, were enough to convince many.

Throughout 2015, the project grew across the globe in Europe, Asia, Africa and Latin America. Repeating the familiar MLM playbook, promoters emphasized urgency, and the immediacy of an impending explosion in value and crypto adoption.

Regulators began to catch on by late 2015. Bulgaria’s Financial Supervision Commission issued a warning about OneCoin, after which the company ceased all operations in the country.

By 2016, several other national financial regulators also had OneCoin on their lists. By year’s end, Norway, Bulgaria, Finland, Sweden and Latvia were all investigating the project. The Hungarian central bank called it a pyramid scheme.

In December, Italian authorities defined OneCoin as an illegal pyramid scheme and demanded it cease activities in the country. China began investigating the project and even arrested some investors.

Regulation efforts ramped up again in 2017. Germany, Thailand, Belize and Vietnam all issued cease-and-desist orders or declared OneCoin illegal. In India, undercover police arrested 18 organizers of a OneCoin event that attempted to bring in new investors. Indian authorities went so far as to charge Ignatova herself in July.

By the year’s end, things had reached a breaking point. Investors were concerned about delays in a supposed exchange that would allow them to cash out their coins. This was supposedly going to be addressed at an October meeting of OneCoin organizers in Lisbon, Portugal.

But Ignatova didn’t show. According to a BBC investigation, she boarded a Ryanair flight from Sofia to Athens, Greece on Oct. 25, 2017. No one has seen her since.

Arrests, murders and Crypto Queen on the run

In early 2018, investigators moved in on the project. At the request of prosecutors in Germany, Bulgarian police raided the OneCoin offices in Sofia. The raid, which according to the Sofia Globe also included German police and Europol, seized servers and material evidence.

In July, co-founder Greenwood was arrested on charges of money laundering and fraud in Thailand, where he would await extradition back to the United States.

Ignatova’s own lawyer, Mark S. Scott, was convicted of conspiracy to commit money laundering and conspiracy to commit bank fraud due to his connections and activities at OneCoin. He would be disbarred a few years later.

OneCoin stayed in the headlines for the next couple of years as developments continued to unfold. In July 2020, two project promoters, Oscar Brito Ibarra and Ignacio Ibarra, were kidnapped and murdered in Mexico. Local media reported that local cartels, which were increasingly becoming interested in cryptocurrencies, could have been involved.

In 2020, entertainment media in Hollywood reported that Kate Winslet would star in a movie about OneCoin. To date, it hasn’t started production.

While Greenwood’s case proceeded in the United States, the Federal Bureau of Investigation put Ignatova on its Ten Most Wanted fugitives list in June 2023.

In September, Greenwood was sentenced to 20 years in prison and ordered to pay $300 million in damages. He pleaded guilty to charges of fraud and money laundering. His sentence was a marked reduction from the initial 60 years sought by the prosecution.

In 2024, the DoJ arrested and charged William Morro for bank fraud in connection with OneCoin. Morro moved some $35 million in OneCoin funds between banks in China and Hong Kong, and $6 million between Hong Kong and the US. Morro surrendered himself to authorities and pleaded guilty to one count of conspiracy to commit bank fraud.

In the latest news, the DoJ announced on Monday that $40 million in assets are available to compensate investors who bought OneCoin between 2014 and 2019 and recorded a net loss.

By the time everything was said and done, some 3.5 million people had lost money to the crypto scheme. Authorities estimate that organizers ultimately made away with $4 billion in user funds.

Ignatova remains at large and on the Ten Most Wanted list. The FBI is offering a $5 million reward for info leading to her arrest and/or conviction.

Magazine: Bitcoin will not hit $1M by 2030, says veteran trader Peter Brandt

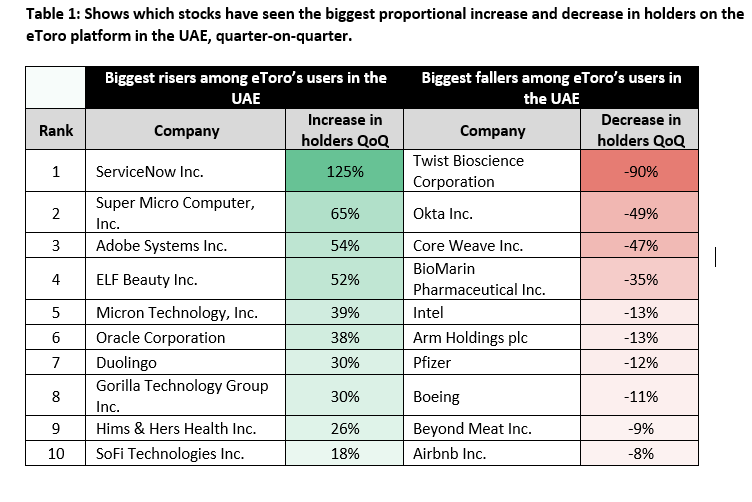

United Arab Emirates investors are leaning into the artificial intelligence sell-off rather than running from it, despite the regional conflict testing the Gulf’s ambitions to become a global hub for AI and digital assets.

New eToro data shared with Cointelegraph on Wednesday show users in the UAE boosted holdings of software and AI infrastructure names whose share prices fell sharply in the first quarter, suggesting they used the downturn to “buy the dip” rather than broadly de-risk.

The pattern suggests UAE investors are staying exposed to long-term AI and digital-infrastructure themes even as the conflict raises fresh risks for data centers, logistics and cross-border technology build-outs in the Gulf. An April 13 report from Deutsche Bank said the shock is more likely to sharpen rather than derail demand for AI, cybersecurity and sovereign digital infrastructure in the region.

Related: Bitcoin falls to lower support as analysts say markets are ignoring key Iran issue

Josh Gilbert, market analyst at eToro, told Cointelegraph that UAE investors became more selective over where they took risk in Q1, and investor behavior was driven by long-term themes rather than a risk-off mindset.

He said the clearest signal was across AI infrastructure and software names, pointing to ServiceNow (+125%), Super Micro Computer (+65%), Adobe (+54%) and Oracle (+38%), which all saw significant increases despite market pressure.

On the crypto side, he said that Strategy Inc. remained the eighth-most-held stock, indicating continued exposure to crypto-linked equities.

War puts Gulf AI ambitions under pressure

The resilience comes as the US-Israeli conflict with Iran has exposed new risks for Gulf tech infrastructure. Deutsche Bank cited reported strikes on Amazon Web Services data centers in the UAE and Bahrain and threats against the planned 1GW Stargate campus in Abu Dhabi.

Gilbert said the conflict was driving volatility, with sharp oil price swings that can ultimately affect tech valuations. Maintaining core exposure to diversified mega-cap tech while rotating within the sector suggests a more nuanced, risk-aware approach, he said.

Deutsche also highlighted that the Gulf, and the UAE in particular, is unlikely to abandon the AI race. The region benefits from cheap energy, an unusually dense pipeline of data center projects, and sovereign wealth funds that control about $5 trillion worldwide in 2025, with Abu Dhabi vehicles among the most aggressive backers of global AI deals, the report said.

Crypto companies stay open as conflict remains

On the ground in Dubai, crypto players say the conflict has slowed but not derailed the city’s hub ambitions. HashKey MENA’s managing director, Ben El-Baz, told Cointelegraph that operations remained “broadly functional,” helped by cloud-based trading and custody systems less dependent on a physical location, even though remote work and travel disruptions were unavoidable.

Related: BTC recovery fragile, Iran war fallout to ‘dominate’ markets in 2026: Analyst

Other companies, including Binance, also continued normal operations, despite reports to the contrary. A Binance spokesperson told Cointelegraph employees were given the option of temporary relocation as a precautionary measure, but the “vast majority” chose to remain, while major conferences such as Token2049 were postponed.

Dubai-based investment firm, Ento Capital, says the conflict is “refining” rather than derailing the GCC story. Senior executive officer Hayssam El Masri told Cointelegraph that investors have shifted from “confidence-driven to risk aware,” but are generally not exiting the region. War-tested resilience and ongoing investment in AI, cloud and crypto infrastructure may ultimately strengthen the GCC’s long-term positioning, he said.

Regulators bet clear rules will anchor capital

Dubai’s Virtual Assets Regulatory Authority (VARA) has continued to roll out its activity-based framework throughout the turmoil, including detailed guidance on token issuance and formal rules for crypto derivatives.

Sean McHugh, VARA’s head of market assurance, told Cointelegraph that in periods of stress, serious market participants do not seek “the lightest-touch jurisdiction, they look for the clearest one,” adding that Dubai’s combination of transparent licensing, visible supervision and active enforcement is meant to persuade institutions to treat the emirate as a strategic base rather than an opportunistic punt.

Magazine: Bitcoin will not hit $1M by 2030, says veteran trader Peter Brandt

Crypto World

Wolfe Research Highlights Meta (META), Uber (UBER), DoorDash (DASH), and Shopify (SHOP) as Prime Internet Stock Opportunities

Key Highlights

- Wolfe Research identifies Meta, Uber, DoorDash, and Shopify as premier large-cap internet investment opportunities

- Internet mega-cap equities currently trade significantly beneath their three-year median valuation levels

- TD Cowen maintains Buy recommendation on Meta with $820 target, highlighting AI-powered advertising expansion

- Uber initiated autonomous robotaxi services in Dubai and announced Blacklane acquisition plans

- DoorDash faces revised price targets following driver fuel subsidy introduction, though Buy ratings persist

Wolfe Research has spotlighted Meta, Uber, DoorDash, and Shopify as premier large-cap internet investment selections. According to the firm, compelling valuations have emerged following a widespread sector correction.

Internet mega-cap companies currently trade approximately three turns beneath their three-year historical median valuations. Large-cap counterparts similarly demonstrate significant discounts relative to historical benchmarks.

Despite this valuation compression, Wolfe Research emphasizes that underlying business fundamentals continue to show strength. The firm’s strategy centers on identifying companies positioned for positive earnings revisions, margin enhancement, and durability against macroeconomic headwinds.

Meta Platforms

Wolfe Research maintains an Outperform rating on Meta with an $800 price objective. The stock has lagged the S&P 500 by 12 percentage points following its January quarterly results.

The research firm anticipates first-quarter revenue will surpass analyst projections by a low-single-digit percentage. Looking ahead to Q2, Wolfe projects management will provide revenue guidance of $61 billion, exceeding the Street’s $60 billion estimate.

Artificial intelligence enhancements through platforms including Lattice, GEM, and Andromeda are anticipated to fuel this expansion. The rollout of the Muse Spark large language model represents a significant growth catalyst.

TD Cowen similarly maintains a Buy stance with an $820 target price. The firm’s first-quarter projections for revenue and operating income stand 1% and 6% above consensus figures, respectively.

Meta’s revenue increased 22% year-over-year to $201 billion, accompanied by an 82% gross profit margin. The company is slated to report earnings on April 29.

Regarding regulatory developments, the European Commission is preparing to mandate that Meta reverse its policy limiting competing AI chatbots on WhatsApp.

Uber Technologies

Wolfe Research assigns Uber an Outperform rating with a $90 price target. The stock has trailed the S&P 500 by two percentage points since reporting February earnings.

First-quarter bookings are projected to exceed estimates by a low-single-digit margin. Second-quarter guidance is anticipated to align with or surpass consensus expectations.

Uber recently announced plans to acquire Blacklane, a premium global chauffeur service. Additionally, the company is evaluating a potential controlling interest in Kakao Mobility.

The ride-hailing leader has introduced fully autonomous robotaxi services in Dubai, accessible through its application. Analysts also identify more substantial share repurchase programs as a potential value driver in the latter half of 2026.

DoorDash

Wolfe Research rates DoorDash Outperform with a $195 price objective. Shares have underperformed the S&P 500 by 12 percentage points since February.

The firm projects first-quarter gross order value and EBITDA will exceed analyst estimates. Proprietary survey research indicates DoorDash is capturing additional market share within grocery delivery services.

Multiple analysts, including the team at BTIG, have adjusted price targets downward due to expenses associated with a recently implemented driver fuel subsidy initiative. However, all firms preserved Buy or Outperform recommendations.

Shopify

Wolfe Research previously downgraded Shopify when shares traded near $165. The firm now considers the current $112 price level an attractive entry point.

First-quarter metrics including gross merchandise volume, revenue, and operating income are all projected to surpass Street expectations. Newly launched products such as Shop Campaigns, Audience, and Sidekick, combined with an expanding Google partnership, are identified as primary growth engines.

Wells Fargo and Deutsche Bank have reduced their price targets while maintaining constructive ratings. Piper Sandler reaffirmed an Overweight rating, emphasizing a robust revenue growth trajectory.

BitMEX Research has proposed a ‘quantum canary fund’ mechanism for Bitcoin that would trigger a coin freeze only if a quantum computing threat is demonstrably real, positioning the idea as a direct counter to BIP-361’s preemptive forced-migration approach.

The proposal lands in the middle of an active governance fight over how Bitcoin should respond to quantum risk, and whether protocol-level coercion is ever justified to protect user funds.

The question isn’t whether quantum computers will eventually threaten ECDSA signatures. It’s who gets to decide when that threat is actionable, and what the protocol is allowed to do about it.

- Proposal: BitMEX Research has put forward a quantum canary fund as an alternative mechanism for protecting Bitcoin against quantum computing threats.

- Trigger condition: The canary fund activates a coin freeze only if a verified quantum threat materializes – not preemptively, unlike BIP-361’s phased approach.

- Canary mechanics: A designated address uses a Nothing-Up-My-Sleeve Number (NUMS) system to generate a provably unknown private key, monitored on-chain via soft fork for signs of quantum exploitation.

- Safety window: A 50,000-block delay – roughly 345 days – follows any canary trigger before a full freeze activates, giving legitimate holders time to migrate.

- What it responds to: BIP-361, merged into the Bitcoin Improvement Proposal repository on April 15, 2026, proposes banning sends to quantum-vulnerable addresses within three years and freezing legacy coin spends within five years of activation.

- Trade-off acknowledged: BitMEX concedes the canary mechanism adds complexity and introduces its own risks, but argues it is preferable to BIP-361’s disruption of Bitcoin’s immutability guarantees.

- Community fault line: Jameson Lopp’s BIP-361 drew sharp criticism for preemptively restricting legitimate funds; Adam Back has advocated optional upgrades over mandatory freezes.

- Watch: Whether BitMEX formalizes the canary fund as a counter-BIP and whether it draws engagement on the Bitcoin developer mailing list – that activity will signal whether this proposal moves from concept to contention.

Discover: The best pre-launch token sales

How the Canary Fund Mechanism Actually Works – and What It Doesn’t Protect

The canary fund concept centers on a specially constructed Bitcoin address whose private key is provably unknown to anyone.

Using a Nothing-Up-My-Sleeve Number (NUMS) system, the address is generated on the elliptic curve in a way that no party, including its creators, can control.

A soft fork marks this address for on-chain monitoring, turning it into a live tripwire: if funds ever move from it, that movement proves a quantum computer has cracked ECDSA in practice, not just in theory.

That is not the same as quantum-proofing Bitcoin. The canary fund does not upgrade any existing wallet, does not migrate any exposed public keys, and does not protect coins that were already at risk the moment their public keys appeared on-chain.

What it does is delay the most disruptive protocol intervention, a coin freeze – until there is verifiable on-chain evidence that the threat is real and active.

The 50,000-block safety window built into the proposal (approximately 345 days) is deliberately structured as an incentive, not just a grace period.

BitMEX’s reasoning: if a quantum-capable actor can crack the canary address, competitors with similar capabilities would face the same temptation across thousands of exposed addresses.

The race-to-claim dynamic theoretically surfaces the threat before it propagates silently. The complexity cost is real – the canary system requires soft fork coordination, on-chain monitoring infrastructure, and a community-wide consensus on what constitutes a valid trigger. BitMEX acknowledges this openly.

Discover: The best crypto to diversify your portfolio with

The Governance Debate the Canary Fund Sits Inside

BIP-361, authored by Jameson Lopp and merged into the Bitcoin Improvement Proposal repository on April 15, 2026, represents the most structured protocol-level response to quantum risk currently in circulation.

Its Phase A bans new sends to quantum-vulnerable addresses three years after activation. Phase B, two years later, invalidates all legacy signatures, freezing any unmigrated coins outright.

A speculative Phase C proposes zero-knowledge proofs linked to seed phrases for limited recovery, though feasibility remains unresolved.

The backlash was immediate and predictable. Critics argued BIP-361 violates Bitcoin’s core property-rights guarantees by preemptively restricting funds that have not been compromised.

Adam Back’s position, that Bitcoin must prepare for quantum risk through optional upgrades rather than coercive protocol changes, reflects the dominant skeptic view. The quantum security debate has been intensifying alongside broader market attention to Bitcoin’s long-term cryptographic assumptions.

BitMEX’s canary fund attempts a third path: evidence-based intervention rather than precautionary freezing.

It preserves the status quo until the threat becomes empirically demonstrable, which satisfies the ‘your keys, your coins’ objection, until the canary trips, nothing changes.

The trade-off is that it provides no protection during the window between when a quantum adversary first achieves cryptographic capability and when they choose to trigger the canary.

That gap could be exploited silently. The question isn’t whether the canary fund is philosophically cleaner than BIP-361. It’s whether ‘wait for proof’ is an acceptable risk posture given that Google and Caltech research suggests quantum breakthroughs may arrive ahead of prior estimates. Other major blockchains, including Tron, are already building out quantum roadmaps without waiting for on-chain confirmation of a threat.

The post BitMEX Proposes ‘Canary Fund’ Alternative in Bitcoin Quantum-Security Debate appeared first on Cryptonews.

The U.S. Department of Justice unveiled a concrete restitution track for victims of the OneCoin scheme, revealing roughly $40 million in assets that may be available to investors who purchased OneCoin between 2014 and 2019 and suffered net losses. The development represents a rare, tangible path to recovery for millions of individuals from a case that has hovered between notoriety and conviction for years. By contrast, earlier global efforts, including a 2024 UK class action, faltered when funding for litigation was terminated, underscoring the uneven landscape of redress in cross-border crypto fraud cases.

OneCoin’s rise and fall remains a archetype of the era’s crypto Wild West: ambitious promises, a centralized “coin” that lacked a true decentralized backbone, and an expansive network built on multi-level marketing tactics. Regulators worldwide began circling the project as concerns about its structure and viability intensified from 2015 onward. The case later spiraled into a long-running criminal saga, with arrests, prosecutions, and a global pursuit of the ringleaders that continues to shape how authorities approach similar schemes today.

Key takeaways

- The DoJ says about $40 million in OneCoin-related assets are available to compensate eligible victims who bought OneCoin between 2014 and 2019 with net losses.

- Estimates put the total amount of money lost to OneCoin at roughly $4 billion across the 3.5 million people affected, based on prosecutors’ assessments.

- OneCoin operated as a centralized program rather than a true cryptocurrency, with coins hosted on OneCoin Ltd. servers and trade limited to a closed system rather than public markets.

- Promoters earned commissions for recruiting other investors, a hallmark of the MLM-style expansion that aided the scheme’s rapid global reach.

- Key prosecutions and indictments over the years include the sentencing of co-founder Karl Sebastian Greenwood, the ongoing status of founder Ruja Ignatova on the FBI’s Ten Most Wanted list, and recent charges against William Morro in 2024.

A restitution path emerges after a long regulatory chase

According to the Department of Justice, specific assets are now earmarked to compensate victims who bought OneCoin during the defined window and who sustained net losses. The DoJ’s announcement in mid-April signposts a procedural checkpoint in a case that has stretched over nearly a decade, with investigators detailing a schema that drew in millions of dollars and investors across multiple continents.

What makes this development notable is the volume of potential relief relative to the scale of loss. While $40 million will not restore all victims’ losses, it offers a recognized mechanism for recovery within a case where most individuals had little or no recourse for restitution in the past. The DoJ statement aligns with broader enforcement aims: to recover assets from criminal activity and distribute them to those who were harmed, even when the perpetrators have fled or faced lengthy sentences.

OneCoin’s architecture and the regulatory crackdown that followed

To understand why restitution remains such a pressing issue, it helps to revisit OneCoin’s mechanics. Launched in 2014 by Ruja Ignatova and Karl Sebastian Greenwood, the project promoted a “cryptocurrency” that relied on centralized servers and a tiered packaging system. Investors purchased tokenized “packages” that purportedly allowed them to mine OneCoin, with a spectrum of entry points, including some of substantial price. However, unlike genuine cryptocurrencies, OneCoin was not truly decentralized and did not offer public trading on an open exchange. Ownership and transfers occurred within a closed ecosystem controlled by OneCoin Ltd., leaving little chance for real market liquidity or independent verification of value.

The regulatory response was swift and global. By late 2015, Bulgaria’s Financial Supervision Commission issued a warning, and operations in the country ceased. Across Europe and beyond, regulators in countries including Norway, Finland, Sweden, Latvia, and Hungary weighed in with cautions and actions that labeled OneCoin a potential pyramid scheme. Italy formally categorized OneCoin as illegal and halted promotional activities, while China initiated investigations and detained some investors. In 2017, Germany, Thailand, Belize, and Vietnam issued cease-and-desist orders or declared OneCoin unlawful. In India, undercover police arrested organizers of an OneCoin event; Ignatova herself faced charges in connection with the scheme.

The saga continued into the 2018–2020 period with high-profile law-enforcement actions: Bulgarian and German authorities raided OneCoin offices; Greenwood was arrested in Thailand in 2018 to face charges; Ignatova’s legal and public profile grew as investigations advanced. A US case culminated in 2023 with Greenwood receiving a 20-year prison sentence and an order to pay about $300 million in damages for fraud and money laundering. The FBI designated Ignatova as one of its Ten Most Wanted Fugitives in 2023, underscoring the unresolved status of the founder’s whereabouts. Meanwhile, public focus on the scheme persisted as DoJ actions broadened to address money flows and related offenses.

Prosecutions, fugitives, and the ongoing enforcement narrative

Greenwood’s 2023 sentencing highlighted the scale of the fraud and the legal consequences for organizers. The court’s decision to impose a 20-year term reflected the gravity of charges including money laundering and fraud, though it was notably shorter than the initial 60-year sentence sought by prosecutors. A parallel line of enforcement continued into 2024, with DoJ actions against William Morro, who moved substantial OneCoin funds across banking corridors in Asia and the United States and subsequently pleaded guilty to conspiracy to commit bank fraud. Morro’s case illustrated how prosecutors pursued cross-border financial movements linked to OneCoin’s operations.

Ignatova remains at large, with the FBI offering a substantial reward—up to $5 million—for information leading to her arrest or conviction. The ongoing status of Ignatova hangs over the broader OneCoin narrative and serves as a reminder of the difficulties regulators face when high-profile operators evade capture across multiple jurisdictions.

What the restitution development means for the market and stakeholders

For victims and their advocates, the new asset pool offers a semblance of closure after years of uncertainty. It also signals a continued appetite among U.S. authorities to pursue asset recovery in cases involving cross-border crypto-adjacent fraud, even when the underlying assets were never truly decentralized currencies. For investors and builders in the broader crypto space, the OneCoin case underscores several enduring risk factors: the appeal of high-yield promises paired with opaque compliance profiles, the reliance on recruitment-driven growth, and the dangers of conflating MLM incentives with genuine asset innovation.

On the regulatory front, OneCoin’s arc contributes to a growing sense that authorities will pursue both criminal prosecutions and civil forfeiture where possible, particularly in schemes that blend traditional fraud with crypto elements. The UK’s failed 2024 class action also illustrates the complexities of cross-border litigation funding and the practical limits of collective redress in transnational crypto cases. As restitution progresses, readers should watch how the DoJ formulates distribution criteria, how many victims ultimately receive payments, and whether more assets are identified for recovery in related proceedings.

For traders and developers, the OneCoin saga offers a cautionary reminder: the crypto market thrives on credible, transparent structures and verifiable liquidity. Where those features are absent, enforcement and restitution can lag, but they remain on the radar of prosecutors and regulators with a growing toolkit for recovering proceeds and protecting the public.

Looking ahead, readers should monitor updates from the Department of Justice regarding the distribution process for the $40 million pool, any additional forfeiture actions tied to OneCoin, and continuing efforts to locate Ruja Ignatova. As the investigative and judicial processes unfold, the case will continue to shape how authorities approach similar schemes and how victims seek redress in a landscape where borders and technologies intersect.

Tether is leading a $150M recovery initiative for Drift Protocol; the plan will also shift the perp DEX’s primary settlement asset to USDT on Solana.

Tether announced a strategic collaboration with Drift Protocol on Thursday, April 16, to support user recovery and facilitate the platform’s relaunch following the exploit earlier this month.

The recovery plan is backed by up to $150 million in combined support, including up to $127.5 million from Tether, according to the announcement from the firm. The structure links funding to trading activity on Drift’s platform, enabling user balance restoration as the exchange resumes operations and generates revenue.

As the Defiant reported previously, the perpetual futures DEX was hacked for over $270 million in crypto on April 1. An April 5 postmortem from Drift revealed that the attack was the result of a complex social engineering and corporate infiltration scheme that began at least six months before the exploit occurred. Per Drift’s report, independent, nonprofit on-chain security group SEAL 911 found that the exploit was likely carried out by a North Korean state-affiliated group.

USDT Settlement

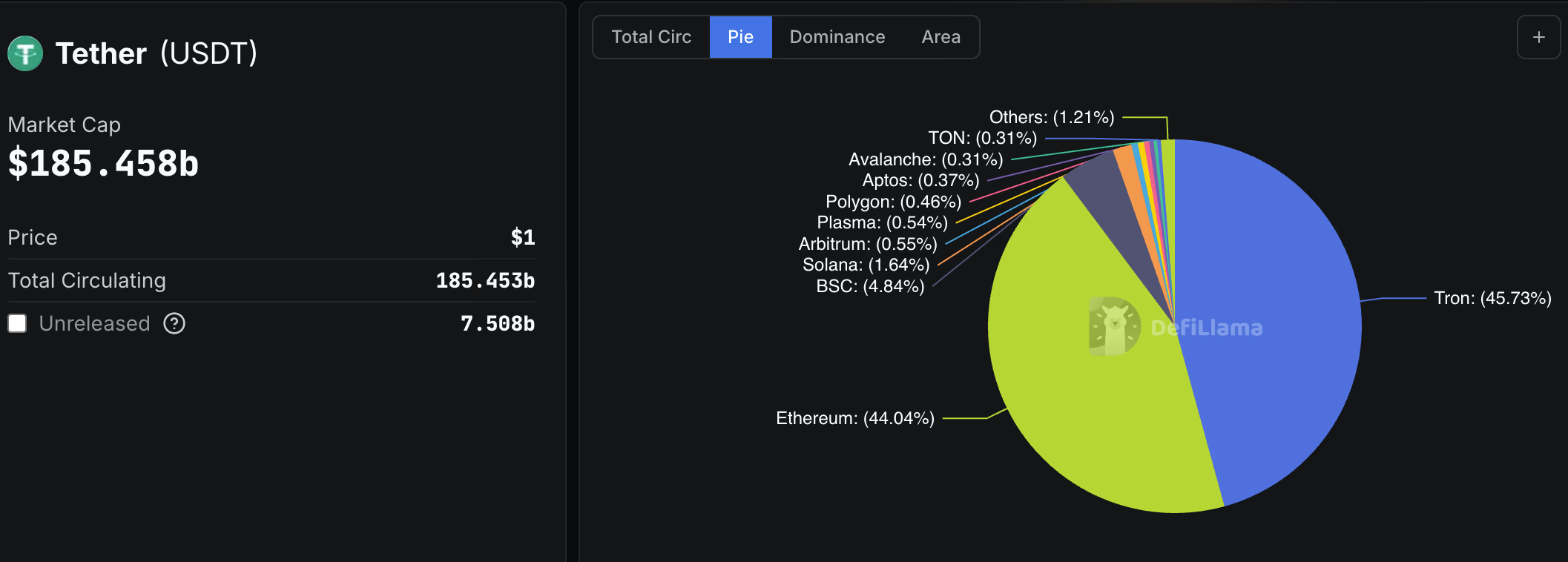

As part of the relaunch, Drift will transition its settlement asset from USDC to USDT, bringing its over 128,000 users and 35 ecosystem teams, including Gauntlet, Neutral, and M1, onto USDT-based trading on Solana, per the announcement. The move positions USDT as a primary settlement asset on what was Solana’s largest perp DEX.

The bulk of USDT’s over $185.4 billion circulating supply is currently on Ethereum and TRON, with both chains holding about 45% of the stablecoin’s market cap. About $3 billion in USDT is currently on Solana, making it the fourth-largest chain by USDT market cap, following BNB Smart Chain (BSC).

Tether CEO Paolo Ardoino said in today’s announcement that the investment and collaboration reflect confidence in Drift’s role in DeFi, and emphasized aligning recovery with real activity and long-term growth.

The DRIFT token rallied over 14% today on the news to ab0out $0.05, after falling sharply after the exploit. The token remains down 98% from its all-time high of $2.60 set in November 2024, per CoinGecko data.

Earlier this week, Tether launched its own wallet app, a multichain, self-custodial wallet that supports USDT, USAT, XAUT, and Bitcoin.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

BitMEX, one of the safest crypto exchanges, announced today the launch of the TradFi Trade and Earn Campaign for users who trade its TradFi derivatives contracts, available for trading 24/7. The campaign allows traders to win their share of a 50,000 USDT prize pool by completing a series of trading missions.

BitMEX currently offers a range of TradFi products, including perpetual swaps on global stocks, indices, commodities, and forex. Unlike other platforms, its TradFi derivatives are available 24/7, allowing users to access markets outside of traditional hours. The campaign will run from 16 April 2026 at 12:00 PM (UTC) to 16 May 2026 at 11:59 PM (UTC). Users can participate at any time during the campaign period.

Rewards will be distributed across 3 categories:

- The Beginner’s Boost: New traders can claim $5 in trading credits by trading TradFi Perps on BitMEX.

- Get Paid to Trade: By achieving trading volume tiers, all participants can claim up to $500 in trading credits.

- Get Paid to Post: Any participant that trades TradFi Perps over the weekend and shares proof of their trades to their X accounts can claim $5 in trading credits.

To participate in the TradFi Trade and Earn campaign, traders must be fully verified on BitMEX. Competition details and registration can be found here. For more details on BitMEX TradFi Perps, visit this page.

About BitMEX

BitMEX is the OG crypto derivatives exchange, providing professional crypto traders with a platform that caters to their needs through low latency, deep crypto native liquidity and unmatched reliability.

Since its founding, no cryptocurrency has been lost through intrusion or hacking, allowing BitMEX users to trade safely in the knowledge that their funds are secure. So too that they have access to the products and tools they require to be profitable.

BitMEX was also one of the first exchanges to publish their on-chain Proof of Reserves and Proof of Liabilities data. The exchange continues to publish this data twice a week – proving assurance that they safely store and segregate the funds they are entrusted with.

For more information on BitMEX, please visit the BitMEX Blog or www.bitmex.com, and follow Telegram, Twitter, Discord, and its online communities. For further inquiries, please contact press@bitmex.com.

The post BitMEX Launches the 24/7 TradFi Campaign Featuring a 50,000 USDT Prize Pool appeared first on BeInCrypto.

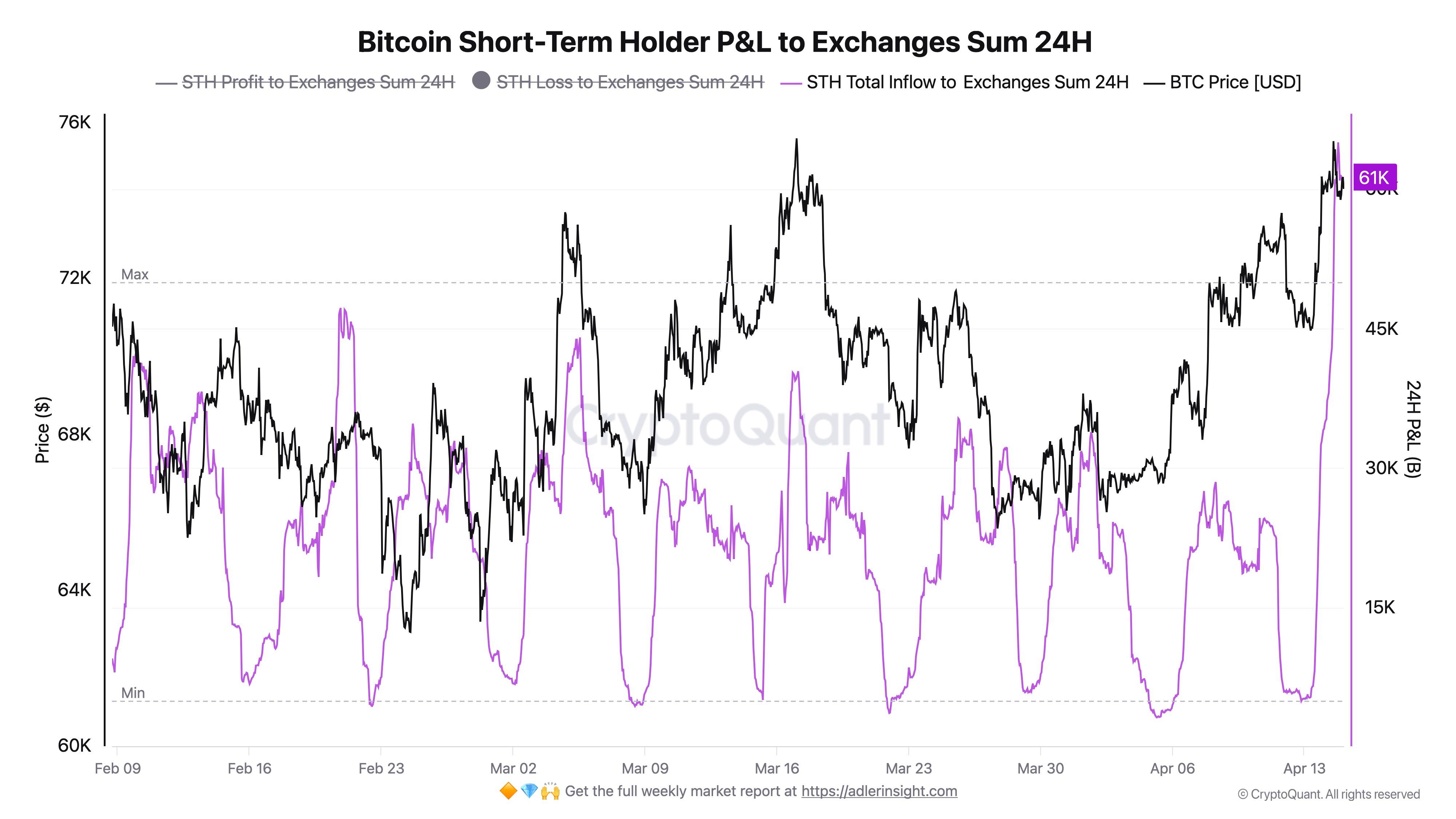

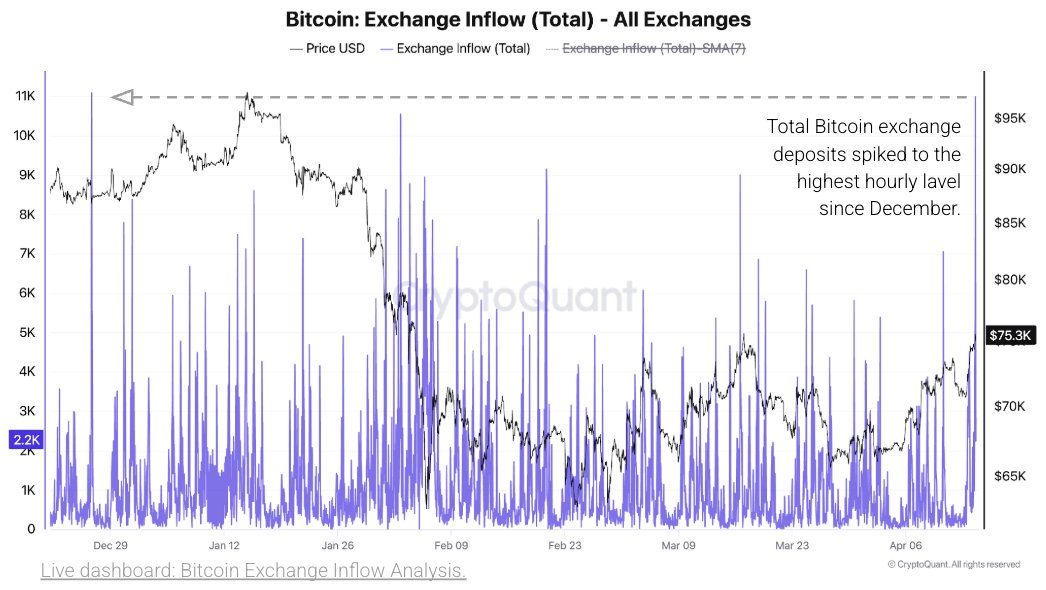

Bitcoin’s (BTC) price trajectory has largely been positive since the US-Iran war, though it has also been volatile. On April 14, BTC briefly climbed above $76,000, its highest price level since early February.

Realized profits hit $1.14 billion during the spike, one of the year’s largest single-day readings. However, the gains failed to hold.

Similarly, BTC’s surge over $75,000 yesterday was met with resistance again. The price adjusted to $74,656 as of press time.

But what is hindering Bitcoin’s rally? According to on-chain signals, it’s short-term holders.

Why Short-Term Holders Are Capping Bitcoin’s Rally

Analyst Darkfost noted that Short-Term Holders (STHs) significantly ramped up exchange flows as BTC tested $75,000 on April 15. Within 24 hours, more than 65,000 BTC moved to exchanges, with 61,000 BTC sent in profit.

“For now, any price increase is being treated as an opportunity to exit the market, whether in profit or at a loss.Yesterday, profits dominated, with 61,000 BTC sent to exchanges in profit. At this stage, STHs remain highly reactive to price movements,” the analyst wrote.

Follow us on X to get the latest news as it happens

On-chain analytics firm CryptoQuant identified the Traders’ On-Chain Realized Price at $76,800 as a key resistance level. This metric reflects the average cost basis of short-term traders and has historically capped relief rallies, including the January 2026 bounce.

As BTC tested $76,000 earlier this week, hourly exchange inflows rose to approximately 11,000 BTC. This marked the highest reading since late December 2025. According to CryptoQuant, this is,

“A historically reliable warning signal of near-term selling pressure, as holders move coins to exchanges in preparation for potential distribution at key resistance zones.”

The average exchange deposit jumped to 2.25 BTC, the highest daily reading since July 2024. Large individual transfers exceeding 1,000 BTC to Binance drove the increase.

Moreover, the share of large deposits as a percentage of total exchange inflows surged from below 10% to above 40% within days around the $76,000 level.

“Daily realized profits remain at approximately $500 million—below the $1 billion threshold that historically marks a significant profit realization spike in bear markets—suggesting that profit-taking has not yet peaked. If Bitcoin sustains near $76K or rallies further toward the $76.8K Traders’ Realized Price, realized profits could accelerate sharply, adding further near-term selling pressure,” the analysis added.

Glassnode’s weekly report reinforced this view. The 30-day EMA of the Realized Profit/Loss Ratio is 1.16, indicating that investors are broadly selling into strength.

The firm identified the True Market Mean at $78,100 as the critical level for any sustained recovery. A move above that threshold would require the market to absorb the current wave of profit-taking on a sustained basis, something that would demand a significant catalyst, according to the report.

With short-term holders treating every rally as an exit opportunity and institutional participation still rebuilding, Bitcoin faces a clear supply overhang that must be absorbed before any structural trend change can develop.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Bitcoin’s Biggest Problem Right Now Isn’t the Market, It’s Its Own Holders appeared first on BeInCrypto.

Crypto World

Drift gets $148 million rescue fund and Tether will replace Circle’s USDC for settlement after massive exploit

Drift Protocol, the victim of a recent North Korean exploit, plans to relaunch with Tether’s USDT as its settlement layer after securing a proposed funding package of up to $147.5 million from the stablecoin issuer and partners, the companies said on Thursday.

The deal includes up to $127.5 million from Tether and $20 million from the other partners, structured to support user recovery following Drift’s April 1 exploit and to reboot the platform as a USDT-based perpetual futures exchange on Solana. Previously, the platform used Circle’s stablecoin USDC as its settlement layer.

The rescue package combines a revenue-linked credit facility, ecosystem grants and loans to market makers. A portion of trading revenue, alongside committed capital, will be directed to a recovery pool aimed at covering roughly $295 million in user losses over time.

The funding comes after a North Korea-linked group infiltrated Drift Protocol, posing as a quantitative trading firm for about six months before carrying out an exploit that was more than $270 million on April 1. Drift’s governance token, DRIFT, has lost about 70% of its value since the exploit.

Circle came under fire from the crypto community for its seeming unwillingness to halt the money transfer after the exploit. The attacker moved about $232 million in USDC from Solana to Ethereum using Circle’s cross-chain transfer protocol. Some critics, including blockchain investigator ZachXBT, said Circle could have moved faster to blacklist wallets and freeze funds to prevent (or at least slow down) the attacker from moving the assets.

However, Circle’s didn’t take any such actions due to legal risks.

Its CEO, Jeremy Allaire, later said that his company freezes USDC wallets only when directed by law enforcement or courts, not in real time during hacks. The approach reflects Circle’s broader strategy to align closely with regulators and institutions.

Its rival, USDT, meanwhile, is more nimble at freezing funds. The stablecoin issuer has repeatedly frozen assets linked to hacks or other illicit activities previously.

Drift is the largest decentralized perpetual futures exchange on Solana, with more than 175,000 users and roughly $150 billion in cumulative trading volume. Founded in 2021, it offers perpetuals, spot trading, lending, borrowing and cross-margin trading.

Stablecoin war

Competition in stablecoins is intensifying as exchanges, fintechs, and traditional financial institutions race to control the on-ramps, liquidity, and settlement layers that underpin digital asset markets.

Circle’s USDC has been steadily chipping away at Tether’s long-standing dominance of the stablecoin market, gaining share on the back of regulatory alignment and growing institutional use.

While USDT still leads by a wide margin, according to CoinDesk data, with roughly $185.5 billion in supply versus about $78.6 billion for USDC, Circle’s transaction volume outpaced Tether’s in recent months as its market share expanded.

With the new funding package, Tether also plans to fund fee reductions and user incentives tied to Drift’s transition to USDT, while extending liquidity support to designated market makers to bolster trading depth at relaunch.

Drift said the move positions USDT at the center of its trading infrastructure while providing a pathway to restore user funds and resume operations.

Read more: How a Solana feature designed for convenience let attackers drain more than $270 million from Drift

HIVE Digital is raising $75m in 0% exchangeable notes to fund GPUs and data centers as it pivots from pure bitcoin mining toward AI cloud and eyes a TSX up‑listing.

Summary

- HIVE Digital plans a $75m private placement of 0% exchangeable senior notes due 2031.

- Proceeds will fund GPU purchases, AI data center expansion and capped call hedging.

- The miner has TSX conditional approval after posting record $93.1m quarterly revenue.

HIVE Digital Technologies is raising $75 million via a private offering of 0% exchangeable senior notes due 2031, doubling down on artificial intelligence infrastructure and data centers as it prepares to move its listing to the Toronto Stock Exchange.

The notes will be issued by HIVE Bermuda 2026 Ltd., a wholly owned subsidiary, to qualified investors in a deal that also includes a 13‑day option for an additional $15 million of paper.

According to HIVE, net proceeds will fund “general corporate purposes and capital investment, including the purchase of graphics processing units and data center expansion,” as the company accelerates its pivot from pure bitcoin mining toward high‑performance computing and AI workloads.

The securities will not bear regular interest and can be exchanged into cash, HIVE common shares, or a mix of both once final pricing and the initial exchange rate are set, giving investors equity‑linked upside without conventional coupons.

To offset potential dilution from the exchangeable notes, HIVE “intends to fund capped call transactions using cash on hand,” a structure designed to cap the effective conversion price and reduce pressure on common shareholders if the stock rallies.

The company said part of the net proceeds may be used to reimburse the issuer for those capped call costs, linking the financing directly to equity‑protection mechanics.

HIVE also disclosed it has received conditional approval to list its common shares on the Toronto Stock Exchange, with trading expected to transition from the TSX Venture Exchange around April 30, subject to meeting TSX requirements by June 30, 2026. The miner’s shares closed at $2.47 on Nasdaq on Wednesday, with roughly $42 million in volume, compared with an average of about $24.6 million.

The financing push follows what HIVE called “record” quarterly results in its fiscal third quarter ended Dec. 31, 2025, where it reported $93.1 million in revenue, up 219% year‑over‑year and 7% quarter‑over‑quarter. The company still posted a net loss of $91.3 million, driven by accelerated depreciation tied to its Paraguay expansion and non‑cash revaluation adjustments, underscoring the capital‑intensive nature of its shift beyond bitcoin mining.

In March, HIVE announced it would progressively “phase down” ASIC‑based bitcoin mining at its Boden facility in Sweden amid tax disputes with local authorities while upgrading the site into a Tier‑III high‑performance computing data center. The firm has already launched its first GPU cluster in Asunción, Paraguay, where its BUZZ AI Cloud platform is processing early large language model training workloads, signaling how quickly the business is re‑orienting toward AI cloud services.

In previous crypto.news coverage of miners diversifying into high‑performance computing, reporters highlighted how firms are seeking to smooth bitcoin cycle risk by monetizing GPU compute for AI and enterprise clients, a trend HIVE’s latest financing appears designed to accelerate.

Other crypto.news reporting on miners’ capital markets moves and AI pivots has tracked a similar shift, including pieces on public miners’ debt raises and data‑center conversions in North America.

12 Years Later, OneCoin Crypto Ponzi Legacy Continues

Padres C Freddy Fermin hit by foul ball but avoids concussion

Israel’s Lebanon house demolitions are part of an explicitly genocidal doctrine

-

Politics6 days ago

Politics6 days agoUS brings back mandatory military draft registration

-

Sports6 days ago

Sports6 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Veronica Beard

-

Politics6 days ago

Politics6 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Politics4 days ago

Politics4 days agoWorld Cup exit makes Italy enter crisis mode

-

Business6 days ago

Business6 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Crypto World3 days ago

Crypto World3 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Crypto World3 days ago

Crypto World3 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos1 day ago

News Videos1 day agoSecure crypto trading starts with an FIU-registered

-

NewsBeat4 days ago

NewsBeat4 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Business5 days ago

Business5 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Business6 days ago

Business6 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Politics6 days ago

Politics6 days agoLBC Presenter Mocks Trump Over Iran War Failures

-

Crypto World6 days ago

Crypto World6 days agoFederal judge blocks Arizona from bringing criminal charges against Kalshi

-

NewsBeat2 days ago

NewsBeat2 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Crypto World2 days ago

Crypto World2 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

NewsBeat4 days ago

NewsBeat4 days agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Tech7 days ago

Tech7 days agoA version of Windows 10 released a decade ago is now eligible for additional security patches

-

Business6 days ago

Business6 days agoIMF retains floor for precautionary balances at SDR 20 billion

-

Business6 days ago

Business6 days agoFormer Liverpool CEO eviscerates FIFA for World Cup ticket pricing

You must be logged in to post a comment Login