Crypto World

RHEA Finance Integrates TRON to Expand Cross-Chain DeFi Access

TLDR:

- RHEA Finance integrates TRON, giving 370 million users access to cross-chain liquidity via one wallet.

- NEAR Intents and Chain Signatures power seamless cross-chain execution without extra wallets or bridges.

- TRON processes over $20 billion daily and holds $85 billion in USDT, making it a key DeFi target.

- Intent-based architecture lets users state financial goals while solvers handle all cross-chain execution.

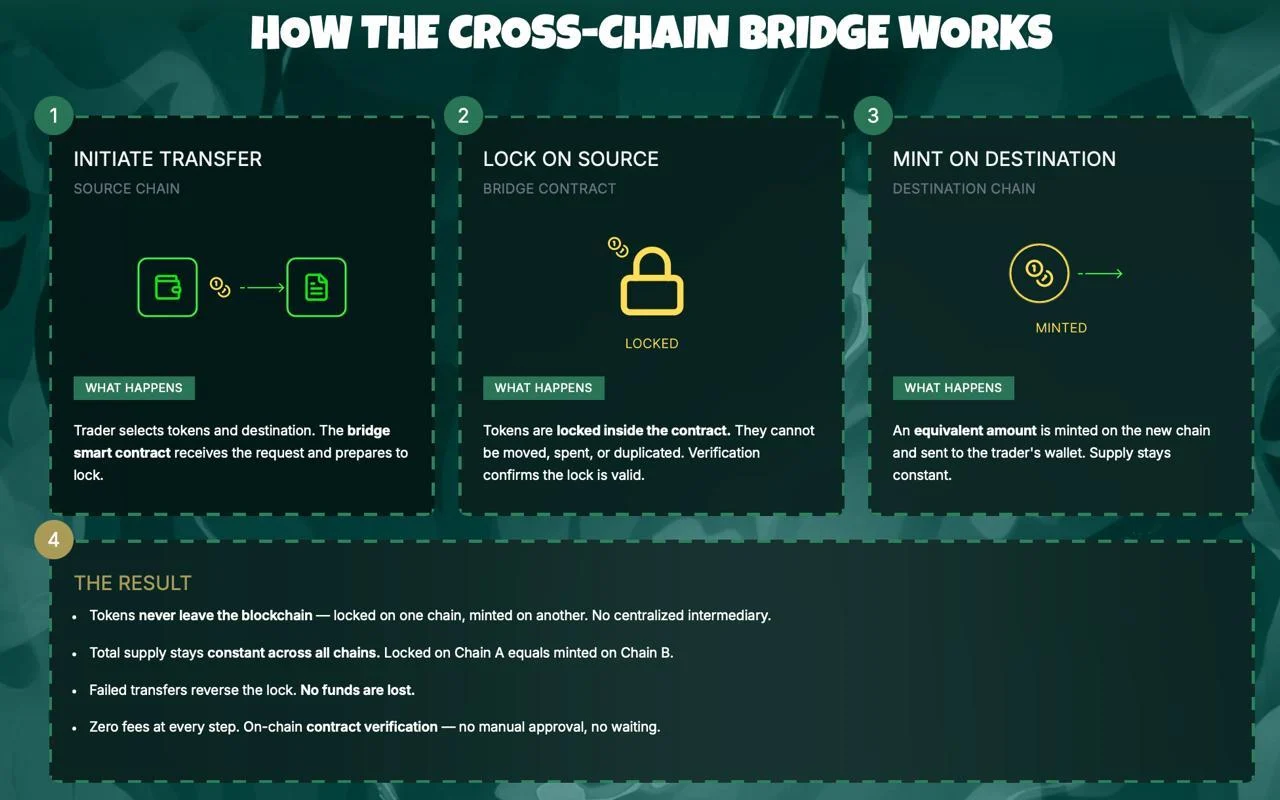

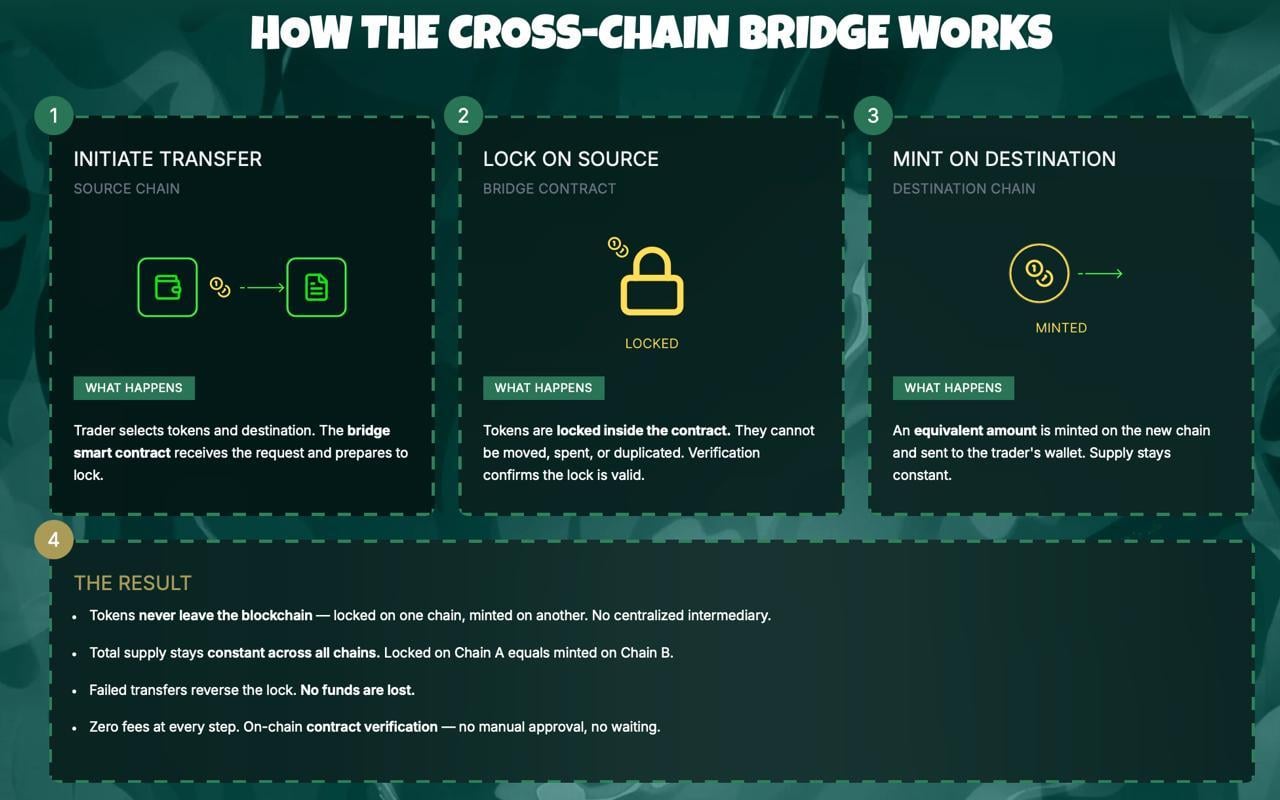

RHEA Finance has announced its integration with the TRON network, extending chain abstracted liquidity to one of blockchain’s most active ecosystems.

Built on NEAR Protocol’s intent-based architecture, the cross-chain DEX and lending protocol now enables TRON users to trade, lend, and borrow across multiple chains.

Users can do this without bridges, extra wallets, or technical knowledge of underlying chain mechanics.

TRON Users Gain Seamless Multi-Chain Access

The integration is powered by NEAR Intents and NEAR Chain Signatures. Together, these tools allow TRON users to express financial goals, such as lending USDT or swapping TRX. A decentralized solver network then handles execution across supported blockchains automatically.

Users sign transactions using only their existing TRON wallet through the RHEA PassKey experience. This removes the need for NEAR, EVM, or any additional wallet setup. The process is designed to be straightforward and accessible to users of all experience levels.

TRON has built a strong presence in global stablecoin payments over the years. The network holds over $85 billion in circulating USDT supply and supports more than 370 million user accounts.

Additionally, TRON processes over $20 billion in daily transfer volume, making it a natural fit for cross-chain DeFi.

RHEA Finance aggregates liquidity across multiple blockchains through its core architecture. By adding TRON, the platform extends its infrastructure to a vast and active user base. Assets can now move between blockchains without fragmentation or added complexity.

Intent-Based Architecture Addresses Long-Standing DeFi Challenges

NEAR Protocol Co-Founder and RHEA Finance advisor Illia Polosukhin spoke directly to the value of the integration. “With RHEA’s TRON integration, the massive user base of TRON gains access to broad cross-chain liquidity through a single wallet,” he said.

He further noted, “This is the power of NEAR Intents and chain abstraction. The user states their intent and it just works, no need to think about infrastructure.”

TRON DAO Community Spokesperson Sam Elfarra also weighed in on the development. “RHEA Finance’s integration represents a meaningful step in further driving cross-chain DeFi accessibility to TRON’s global user base,” Elfarra stated.

He added that users can now transact across ecosystems without leaving TRON, enhancing interoperability across the broader Web3 landscape.

The integration directly addresses fragmented liquidity and complex bridging workflows in DeFi. It also removes the persistent need for multiple wallets when operating across chains. Users simply express their desired outcome, and the infrastructure manages execution on the backend.

Native settlement workflows are designed to keep collateral and proceeds within the TRON ecosystem. This approach maintains the security and familiarity that existing TRON users expect.

As blockchain interoperability grows, intent-based systems like this show how decentralized finance can scale to meet the needs of a global user base.

Crypto World

Sports betting should be regulated as a financial product, not gambling, aspiring prediction market provider says

MIAMI BEACH, Fla. — Sports betting should be regulated as a federal financial product rather than a state-licensed casino product, two panelists said Thursday.

Appearing at Consensus Miami 2026, Jacob Fortinsky, co-founder and CEO of sports betting platform Novig, said the legacy sportsbook model is structurally broken because it treats winning bettors as cheaters.

“Sports betting is really the only industry in the country that regularly limits and bans their power users,” Fortinsky said. He framed sports event contracts as binary financial instruments that “for so long have been treated as a gambling product and instead should really be treated as a financial product.” Globally, he said, sports betting is “a $2 trillion asset class still dominated by these legacy casinos.”

Adam Mastrelli, founder of 57 Maiden, a firm that builds AI-driven trading strategies for prediction markets, validated the critique with personal experience.

“My partner and I got kicked off of two big sportsbooks within two months of trading because we were sharp,” he said, It’s like “LeBron James getting kicked out of the NBA for being too good,” he added.

Mastrelli said the team turned to Novig, which he said charges no fees and allows traders to create synthetic positions.

Mastrelli said his firm’s edge decayed quickly, and of 154 proposed trading strategies, only three currently run profitably.

“This edge will go away,” he said, “so if you can build systems that can keep up with that edge and that alpha… then it becomes really, really intriguing.” His most profitable season, he said, was the WNBA.

Fortinsky said Novig is on track to transition this summer from a sweepstakes model live in 35 states to a federal DCM framework that will let it operate in all 50 states. An earlier attempt to be regulated at the state level in Colorado, he said, was a wake-up call. “Regulators told us essentially you’re naive if you think we care about consumer protection or innovation or market efficiency. We really just care about our tax revenue,” he said.

The federal-state fight, Fortinsky added, is “going to get to the Supreme Court in the next two or three years,” with 15 pending lawsuits between the Commodity Futures Trading Commission, Kalshi, Robinhood and various states. Within prediction markets, he argued sports is “counterintuitively actually the safest vertical,” given the bigger insider-trading and manipulation concerns around political and event-driven contracts.

Mastrelli, who said he avoids offshore platforms entirely, compared prediction markets to equities exchanges: “When I see a robust equities market now, this is AQR against SIG. It doesn’t go away.”

The Linux bug nicknamed Copy Fail is drawing heightened attention from cybersecurity authorities, government agencies and the crypto sector. Described as a local privilege-escalation flaw, Copy Fail could let an attacker with basic user access gain full root control on affected systems. The issue has earned a place in the Cybersecurity and Infrastructure Security Agency’s Known Exploited Vulnerabilities catalog, signaling a high-priority risk for organizations worldwide. Given how deeply Linux underpins crypto infrastructure—from exchanges and custody platforms to validators and node operators—a kernel-level vulnerability of this kind threatens to ripple through the ecosystem even though the flaw does not target blockchain protocols directly.

Security researchers from Xint.io and Theori identified Copy Fail, which hinges on a logic error in how the Linux kernel handles memory operations within its cryptographic subsystems. In pragmatic terms, a regular user could manipulate the kernel’s page cache—the temporary storage the system uses to speed up file I/O—to escalate privileges. What makes this flaw particularly alarming is how accessible the exploit appears to be: a compact Python script can trigger the vulnerability with only modest modifications, enabling root access on many Linux installations. Researcher Miguel Angel Duran has highlighted that the exploit can be demonstrated with roughly 10 lines of Python code on affected machines.

Key takeaways

- Copy Fail (CVE-2026-31431) is a local privilege-escalation vulnerability affecting many mainstream Linux distributions released since 2017, not a remote-exploit against blockchain protocols.

- A working proof-of-concept exploit is publicly available, increasing the risk of rapid exploitation after the initial foothold.

- The flaw stems from how the kernel manages its page cache during memory operations, allowing basic users to gain root control on vulnerable systems.

- Crypto infrastructure—validators, nodes, exchanges, custody services and cloud-based trading—could face indirect but serious consequences if attackers compromise underlying Linux servers.

Copy Fail: how the exploit works and why it matters for crypto

Root access in a Linux server equates to the “master key” to the machine. With it, an attacker can install or remove software, view or exfiltrate sensitive data and reconfigure protections, potentially turning off monitoring tools or altering security settings. Copy Fail exploits a flaw in the kernel’s handling of the page cache, a fast-access memory area used to accelerate file operations. By manipulating cached data under specific conditions, an attacker can bypass intended permission checks and elevate privileges.

The exploit is not a remote attack. A target must already be reachable—via phishing, compromised credentials or another initial access vector—before privilege escalation can occur. Once foothold is established, the attacker can expand control across the host and, in the context of crypto operations, threaten custodial wallets, hot nodes, and trading or node-management infrastructure.

The crypto industry’s dependence on Linux is wide-ranging. Validators and full nodes rely on Linux-based servers; mining operations and pools run on Linux ecosystems; centralized and decentralized exchanges depend on Linux-driven backend stacks; custodial services and wallet infrastructure are Linux-backed; and cloud-based trading systems often sit upon Linux infrastructure. A kernel vulnerability that enables rapid, broad privilege escalation thus carries outsized risk for operational continuity and key security.

Public commentary and analyses emphasize several factors that compound the risk: the flaw affects a broad set of distributions, a working PoC is publicly available, and the vulnerability has persisted in kernels going back to 2017. As security firms and researchers underscore, once exploit code circulates, threat actors can quickly identify unpatched hosts for exploitation. The timing also matters: disclosures arrive as the cybersecurity community increasingly examines how artificial intelligence can accelerate vulnerability discovery and weaponization.

AI, vulnerability discovery and crypto’s exposure

The Copy Fail disclosure arrives amid a broader push to incorporate artificial intelligence into vulnerability research. Initiatives like Project Glasswing, backed by a coalition including Amazon Web Services, Anthropic, Google, Microsoft and the Linux Foundation, highlight a trend where AI tooling is rapidly improving at identifying and instrumenting weaknesses in code. Anthropic and others have argued that modern AI models can outperform humans in spotting exploitable bugs within complex software, potentially accelerating both offense and defense in cybersecurity.

For the crypto sector, the intersection of AI-driven vulnerability discovery and kernel-level flaws raises red flags. Crypto systems—built on layered open-source technologies and deployed across heterogeneous infrastructures—can be particularly susceptible to AI-enhanced attack patterns. If adversaries combine initial access with quick privilege escalation on Linux-based servers, the knock-on effects could include compromised validators, tainted node operators and disrupted service for exchanges and custodians.

In practical terms, even if a direct blockchain protocol breach is unlikely, the integrity of the underlying systems powering the crypto economy remains a critical concern. Large exchanges and custodial platforms operate at scale on Linux-centric stacks, and a successful, widespread kernel exploit could lead to downtime, credential leakage or wallet exposure—outcomes that would reverberate through trading and settlement services globally.

Defense in depth: practical steps for organizations and users

Addressing Copy Fail requires a coordinated mix of rapid patching, access control and proactive monitoring. The guidance emerging from security briefs points to a structured response for different actors in the crypto ecosystem:

For cryptocurrency organizations and infrastructure teams

- Implement and verify official kernel and system patches as soon as they are released by upstream vendors and distribution maintainers.

- Limit local user accounts and permissions; enforce the principle of least privilege across all Linux hosts.

- Regularly audit cloud instances, virtual machines and physical servers for unusual privilege-escalation activity.

- Improve monitoring for anomalous authentication attempts and privilege escalations; implement robust SSH hardening and key management.

- Review container orchestration, cloud IAM policies and network segmentation to minimize blast radius if a host is compromised.

For everyday crypto users

- Keep operating systems and essential software up to date with the latest security patches.

- Avoid unverified software sources and crypto tooling; prefer hardware wallets for significant holdings.

- Enable MFA wherever possible and isolate high-value wallet activity from routinely used devices.

For node runners, validators and developers

- Prioritize prompt kernel and security updates; subscribe to relevant security bulletins and advisories.

- Audit container environments, orchestration tools and cloud permissions for over-privileged configurations.

- Enforce the minimum viable privileges for administrators and ensure robust change controls around critical systems.

What to watch next and why it matters

The Copy Fail disclosure reinforces a broader truth: the security of crypto systems is as much about the integrity of the operating environment as it is about protocols, keys and consensus. While the vulnerability does not directly attack blockchain networks, its potential to destabilize the servers and services that support crypto ecosystems makes urgent patching and hardening essential. As AI-driven tools reshape vulnerability discovery, readers should expect rapid cycles of disclosure and remediation, making timely updates and vigilant security hygiene more important than ever for exchanges, validators and users alike.

Looking ahead, market participants should monitor how major Linux distributions respond, the pace of patch deployment across exchanges and custodians, and any changes in incident response practices within the crypto infrastructure community. If threat actors begin exploiting Copy Fail at scale, the next few quarters could test the resilience of large-grade crypto operations and highlight the ongoing need for defense-in-depth in both software supply chains and operational security. For now, the focus remains clear: patch early, monitor closely and assume that privileged access, once obtained, can rapidly cascade unless defenses hold firm.

Sources and related context include official sector advisories and technical analyses from security researchers and industry researchers, with updates referenced from CISA’s KEV catalog and reporting on the Copy Fail vulnerability, public PoCs, and AI-assisted vulnerability research initiatives.

The Senate Banking Committee will meet on Thursday, May 14, to consider the Digital Asset Market Clarity Act of 2025, putting the crypto market structure bill back on the calendar after a January postponement.

The notice follows months of talks over regulatory jurisdiction, consumer protections, developer protections and stablecoin rewards. CoinDesk reported last week that crypto firms had backed a stablecoin yield compromise meant to unlock the bill.

Cody Carbone, CEO of The Digital Chamber, said the notice marks “a major step” toward clarity for more than 70 million Americans who use cryptocurrencies..

Blockchain Association CEO Summer Mersinger called the markup notice “an important step toward establishing clear rules for digital asset markets.”

“This work reflects months of serious engagement on difficult questions, from SEC-CFTC jurisdiction to consumer protection and developer protections,” Mersinger said. “Clear statutes are what American consumers, businesses, and innovators deserve.”

Kristin Smith, president of the Solana Policy Institute, called the markup “a make or break moment for American leadership in financial markets.” Miller Whitehouse-Levine, the group’s CEO, said the date is “the first step” toward giving builders and financial institutions certainty to build onchain in the U.S.

Ji Hun Kim, CEO of the Crypto Council for Innovation, said “the momentum is real, and the time is now.” The markup, he said, brings the U.S. closer to a framework that safeguards consumers, gives investors clear disclosures, protects developers and supports responsible innovation.

The markup gives Senate Banking another shot at moving the bill before the White House’s July 4 target for Clarity Act passage.

Though the crypto industry is cheering the hearing date, the banking industry said it still has concerns.

A joint letter addressed to Senate Banking Committee leaders Tim Scott and Elizabeth Warren from a coalition of banking trade associations said that they still had some concerns with the bill, proposing edits to the text of the legislation.

Key Takeaways

- Nvidia achieved $215.9 billion in fiscal 2026 revenue, marking a 65% year-over-year surge

- The Data Center division at Nvidia delivered $193.7 billion throughout the fiscal year

- AMD’s full-year 2025 revenue reached $34.6 billion, with Data Center sales climbing 32% to $16.6 billion

- Nvidia’s Data Center business exceeds AMD’s by more than 11-fold

- Export restrictions on AMD’s MI308 GPU resulted in $440 million in charges

The artificial intelligence chip sector features two heavyweight competitors in Nvidia and AMD, yet recent financial disclosures reveal a significant gap in their operational scale.

For fiscal 2026, Nvidia announced revenue totaling $215.9 billion. This represented a 65% jump compared to the previous fiscal period. The company maintained a gross margin of 71.1%.

The fourth quarter performance alone delivered $68.1 billion in top-line results. Within that timeframe, Data Center operations contributed $62.3 billion.

Across the entire year, Nvidia’s Data Center division produced $193.7 billion in revenue. This segment has evolved into the company’s primary engine, fueled predominantly by artificial intelligence infrastructure investments from major cloud providers and tech giants.

Nvidia’s business model extends beyond silicon. The company provides an integrated ecosystem encompassing accelerators, networking equipment, complete systems, and proprietary software platforms. This comprehensive approach creates significant switching barriers for enterprise customers.

The primary vulnerability for Nvidia lies in customer concentration. A substantial portion of revenue derives from a narrow window of heavy capital expenditure by hyperscale data center operators. Any deceleration in this investment wave could materially impact financial performance.

AMD’s Financial Performance

AMD disclosed full-year 2025 revenue of $34.6 billion. The Data Center division contributed $16.6 billion, representing 32% growth versus 2024. This expansion was fueled by EPYC server CPU sales and Instinct AI accelerator deployments.

Advanced Micro Devices, Inc., AMD

During the fourth quarter, AMD reported a 54% gross margin alongside $1.8 billion in operating income and $1.5 billion in net income.

While these figures demonstrate strength, Nvidia’s yearly Data Center revenue still dwarfs AMD’s by more than 11 times. This disparity underscores how nascent AMD’s position remains in the AI infrastructure landscape.

AMD doesn’t require dominance over Nvidia to achieve substantial growth. Even modest market share gains in server processors and AI accelerators can generate significant revenue increases.

However, challenges persist. AMD absorbed approximately $440 million in charges throughout fiscal 2025 stemming from U.S. export restrictions affecting its MI308 data-center GPU.

This development highlights both regulatory exposure and the difficulty of eroding Nvidia’s entrenched market leadership.

Wall Street Perspective

Analyst sentiment favors both stocks, though Nvidia commands stronger conviction. MarketBeat data shows 54 analysts following Nvidia with a Buy consensus. The breakdown includes 48 buy ratings, 4 strong buys, and 2 hold ratings. The consensus 12-month price target stands at $275.25.

AMD draws attention from 40 analysts with a Moderate Buy rating. This comprises 1 strong buy, 31 buys, and 8 holds. The average price target reaches $296.44.

Nvidia’s more bullish consensus rating mirrors its commanding market position and superior profit margins.

Interestingly, AMD’s average price target of $296.44 exceeds Nvidia’s $275.25 target. This implies analysts perceive greater potential appreciation from AMD’s current valuation, despite Nvidia’s superior operational metrics.

More than $3 trillion in digital assets could eventually become vulnerable to theft within the next four to seven years, according to a new report from Project Eleven.

Project Eleven focuses on post-quantum security and migration for digital assets and recently announced a collaboration with the Solana Foundation to prepare its network against the threat of quantum computing.

“The digital asset industry holds over $3 trillion in aggregate value, and virtually all of it is secured by the same class of cryptographic primitive: elliptic curve digital signatures,” which are vulnerable to quantum computing attacks, the report said.

But it is not only crypto that is at stake here. The report states that the same public-key cryptography security used by bitcoin, ether and stablecoins also underpins banking systems, cloud infrastructure, authentication networks and military communications.

The 110-page report by Project Eleven, whose CEO Alex Pruden was on stage at Consensus Miami 2026, also states that sufficiently powerful quantum computers could use Shor’s algorithm to derive private keys from public keys, allowing attackers to forge signatures and take over control of wallets and digital accounts secured by the elliptic curve cryptography.

This means blockchains, banking infrastructure, cloud systems, military comms and other digital identity systems are also vulnerable, not just bitcoin, ethereum, stablecoins, and other blockchains, the report emphasizes.

Project Eleven says a “Q-Day” scenario, the arrival of cryptographically relevant quantum computer cable of breaking widely used public-key cryptography, could be as early as 2030, no later than 2033.

“Our analysis suggests that, based on current trends, Q-Day is more likely to occur than not by 2033, and potentially even as soon as 2030,” the report reads. “The window for the world to migrate to post-quantum cryptography is narrowing.”

And here is why it is becoming so complicated, the report explains: large systems often take between five to more than 10 years to migrate, depending on how complex their networks are.

Another difficult challenge is how the transition actually takes place, as migrating all quantum vulnerable systems and blockchains to secure networks involves a process that requires a coordinated, simultaneous transition from all users, exchanges, custodians, wallet providers and miners.

Read more: To freeze or not to freeze: Satoshi and the $440 billion in bitcoin threatened by quantum computing

“The gap is not technical,” the report says. “The gap is entirely coordination, urgency, and willingness to accept the costs of migration.”

When it comes to Bitcoin, things get even more complicated because upgrades historically move slowly and often become politically contentious.

“The Bitcoin SegWit upgrade — a relatively modest change compared to PQC migration — took over two years from proposal to activation (2015-2017) and triggered a contentious chain split,” the report recalled.

Read more: What the Fork? Why Bitcoin Tech Changes Impact Price

“The distributed nature of blockchain networks means that migration to post-quantum cryptography may take the better part of a decade, longer than other centralized systems.”

Pruden, who authored the report along with CTO Conor Deegan, warned that Bitcoin’s migration to post-quantum cryptography could prove even harder than Taproot because it would require coordinated action across users, exchanges, custodians and miners. He also said he personally leaned toward “recycling” the 5.6 million to 6.9 million vulnerable BTC tokens, worth up to roughly $500 billion at current prices back into the bitcoin’s supply curve rather than allowing a quantum attacker to eventually sweep them.

The report by Pruden’s Project Eleven ultimately acknowledges that the issue creates tension between bitcoin’s fixed-supply ethos and its commitment to property rights.

Read more: Bitcoin’s quantum debate splits as Adam Back pushes optional upgrades over forced freeze

1. Copy Fail: The Linux vulnerability affecting crypto infrastructure security

A recently uncovered security flaw in Linux is drawing concern from cybersecurity specialists, government agencies and the cryptocurrency sector. Codenamed “Copy Fail,” the vulnerability affects many popular Linux distributions released since 2017.

Under specific circumstances, the flaw could let attackers escalate privileges and gain full root control of affected machines. The Cybersecurity and Infrastructure Security Agency (CISA) has added the issue to its Known Exploited Vulnerabilities catalog, highlighting the serious threat it poses to organizations worldwide.

For the crypto industry, the implications go well beyond a standard software bug. Linux powers much of the underlying infrastructure for exchanges, blockchain validators, custody solutions and node operations. As a result, an operating system-level vulnerability could create significant disruptions across large parts of the cryptocurrency ecosystem.

2. What is “Copy Fail”?

“Copy Fail” refers to a local privilege-escalation vulnerability in the Linux kernel, identified by security researchers at Xint.io and Theori.

In simple terms, it allows an attacker who already has basic user-level access on a Linux system to elevate their permissions to full administrator or root control. The bug stems from a logical error in how the kernel handles certain memory operations within its cryptographic components. Specifically, a regular user can influence the page cache, the kernel’s temporary storage for frequently accessed file data, to gain higher privileges.

What stands out about this vulnerability is how easy it is to exploit. A compact Python script, requiring minimal changes, can reliably trigger the issue across a wide range of Linux setups.

According to researcher Miguel Angel Duran, it only requires roughly 10 lines of Python code to gain root access on affected machines.

3. Why this vulnerability stands out as particularly risky

Linux security issues range from highly complex attacks that require chained exploits to simpler ones that need just the right conditions. “Copy Fail” has drawn significant attention because it requires relatively little effort after an initial foothold.

Key factors contributing to the vulnerability include:

- It affects most mainstream Linux distributions.

- A working proof-of-concept exploit is publicly available.

- The issue has existed in kernels going back to 2017.

This mix makes the vulnerability more concerning. Once exploit code circulates online, threat actors can quickly scan for and target unpatched systems.

The fact that such a critical flaw stayed hidden for years underscores how even well-established open-source projects can contain subtle vulnerabilities in their foundational code.

Did you know? The Bitcoin white paper was released in 2008, but Linux dates back to 1991. That means much of today’s crypto infrastructure is built on software foundations older than many blockchain developers themselves.

4. How the “Copy Fail” exploit works

It is important to first understand what full “root” control means on a Linux server. Root access is essentially the highest level of authority over the machine.

With it, an attacker could:

- Add, update or delete any software

- View or steal confidential files and keys

- Modify critical system settings

- Access stored wallets, private keys or authentication credentials if they are present on the affected system

- Turn off firewalls, monitoring tools or other defenses

The exploit takes advantage of how the Linux kernel manages its page cache. The system uses a small, fast memory area to speed up file reading and writing. By abusing how the kernel handles cached file data, an attacker can trick the kernel into granting higher privileges than intended.

Crucially, this is not a remote attack that can be launched from anywhere on the internet. The attacker first needs some form of access to the target machine. For instance, they could gain access through a compromised user account, a vulnerable web app or phishing. Once they have that initial foothold, the attacker can quickly escalate their permissions to full root control.

5. Why this matters for the cryptocurrency industry

Linux is widely used across cloud, server and blockchain node infrastructure, making it important to many crypto operations.

Core parts of the crypto ecosystem run on it, including:

- Blockchain validators and full nodes

- Mining farms and pools

- Centralized and decentralized cryptocurrency exchanges

- Custodial services and hot/cold wallet infrastructure

- Cloud-based trading and liquidity systems

Because of this deep dependence, a kernel-level vulnerability like “Copy Fail” can create indirect but serious exposure across the crypto world. If attackers successfully exploit it on vulnerable servers, the possible consequences include:

- Stealing private keys or administrative credentials

- Compromising validator nodes to disrupt operations or support broader network attacks

- Draining funds from hosted wallets

- Causing widespread downtime or launching ransomware

- Exposing user data stored on affected systems

While the vulnerability does not attack blockchain protocols directly, breaching the underlying servers that support them can still lead to major financial losses, reputational damage and operational disruption.

Did you know? Major crypto exchanges rely on large-scale cloud, server and Kubernetes infrastructure to process trading activity, run blockchain nodes and support market-data operations around the clock. Coinbase, for example, has publicly described infrastructure tied to blockchain nodes, trading engines, staking nodes and Linux production environments.

6. Why initial access still poses a major threat in crypto environments

Some users downplay this vulnerability because it requires a certain level of existing access to the target system. However, most real-world cyberattacks unfold in multiple phases rather than striking all at once.

A typical attack sequence looks like this:

- Attackers first break in using phishing campaigns, leaked passwords or infected applications.

- They secure a basic foothold with ordinary user-level rights.

- They then use flaws like “Copy Fail” to quickly escalate to full administrator privileges.

- From there, they expand their reach across the network.

This pattern is especially dangerous in the cryptocurrency space, where exchanges, node operators and development teams are prime targets for phishing and credential theft. What starts as a minor breach can quickly escalate into a full takeover when reliable privilege-escalation tools are available.

7. Why security teams are particularly concerned

CISA’s decision to include “Copy Fail” in its Known Exploited Vulnerabilities (KEV) catalog signals that the flaw is viewed as a high-priority risk.

Red flags include the public release of working exploit code. As soon as proof-of-concept scripts become widely available, threat actors begin automated scans to look for unpatched systems to target.

Many organizations, particularly in finance and crypto infrastructure, also tend to delay kernel updates. They prioritize system stability and avoid potential downtime or compatibility issues. However, this approach can leave systems exposed for longer during critical vulnerability windows, giving attackers more time to strike.

Did you know? In simple terms, “root access” is like having the master key to an entire building. Once attackers gain it, they can potentially control nearly every process running on the system, change protected files and interfere with core security settings.

8. The AI connection: Why this vulnerability could signal bigger challenges ahead

Copy Fail was disclosed at a time when the cybersecurity world is increasingly focused on the role of artificial intelligence in vulnerability discovery.

The timing coincides with the introduction of Project Glasswing, a collaborative effort backed by leading tech organizations such as Amazon Web Services, Anthropic, Google, Microsoft and the Linux Foundation. Participants in the project have highlighted how rapidly advancing AI tools are becoming better at identifying and weaponizing weaknesses in code.

Anthropic has stressed that cutting-edge AI models are already outperforming many human experts when it comes to finding exploitable bugs in complex software. The company says these systems could greatly speed up both offensive and defensive cybersecurity work.

For the cryptocurrency industry, this trend is particularly concerning. Crypto systems are high-value targets for hackers and are often built on layered open-source technologies, making them potentially more exposed as AI-driven attack methods evolve.

9. What this means for everyday crypto users

For most individual crypto holders, the direct risk from this specific Linux issue remains low. Everyday users are unlikely to be personally singled out.

That said, indirect effects could still reach users through:

- Breaches or downtime at major exchanges

- Compromised custodial platforms holding user funds

- Attacks on blockchain validators or node providers

- Disruptions to wallet services or trading infrastructure

Self-custody users should take note if they:

- Run their own Linux-based blockchain nodes

- Operate personal validators or staking setups

- Maintain crypto-related tools or servers on Linux

Ultimately, this situation highlights an important reality: Strong crypto security is not just about secure smart contracts or consensus mechanisms. It also depends heavily on keeping the underlying operating systems, servers and supporting infrastructure up to date and protected.

10. How to stay protected

“Copy Fail” is a reminder of how quickly underlying operational vulnerabilities can escalate into major security threats in the digital space. The positive side is that most of these risks are manageable. Organizations and users can significantly reduce their exposure by applying security updates promptly, enforcing stricter access controls and maintaining strong overall cybersecurity practices.

For cryptocurrency organizations and infrastructure teams

Companies running Linux-based systems should prioritize these steps:

- Deploy official security patches as soon as they become available

- Minimize and strictly control local user accounts and permissions

- Regularly audit cloud instances, virtual machines and physical servers

- Set up strong monitoring for unusual privilege-escalation attempts

- Strengthen SSH access, key-based authentication and overall login security

For everyday crypto users

Individual holders can lower their exposure by:

- Keeping operating systems and software fully updated

- Avoiding downloads from unverified sources or unofficial crypto tools

- Using hardware wallets for significant holdings

- Enabling multi-factor authentication (MFA) wherever possible

- Isolating high-value wallet activities from everyday computers and browsers

For node runners, validators and developers

Those managing blockchain nodes or development environments should:

- Apply kernel and system updates without delay

- Closely follow Linux security bulletins and advisories

- Review container setups, orchestration tools and cloud permissions

- Limit full administrator rights to the bare minimum

Crypto World

XRP Price Prediction Strengthens After Ripple, JPMorgan, Mastercard Settle First Cross Border Tokenized Treasury on XRP Ledger: Pepeto Holds the Bigger Multiple

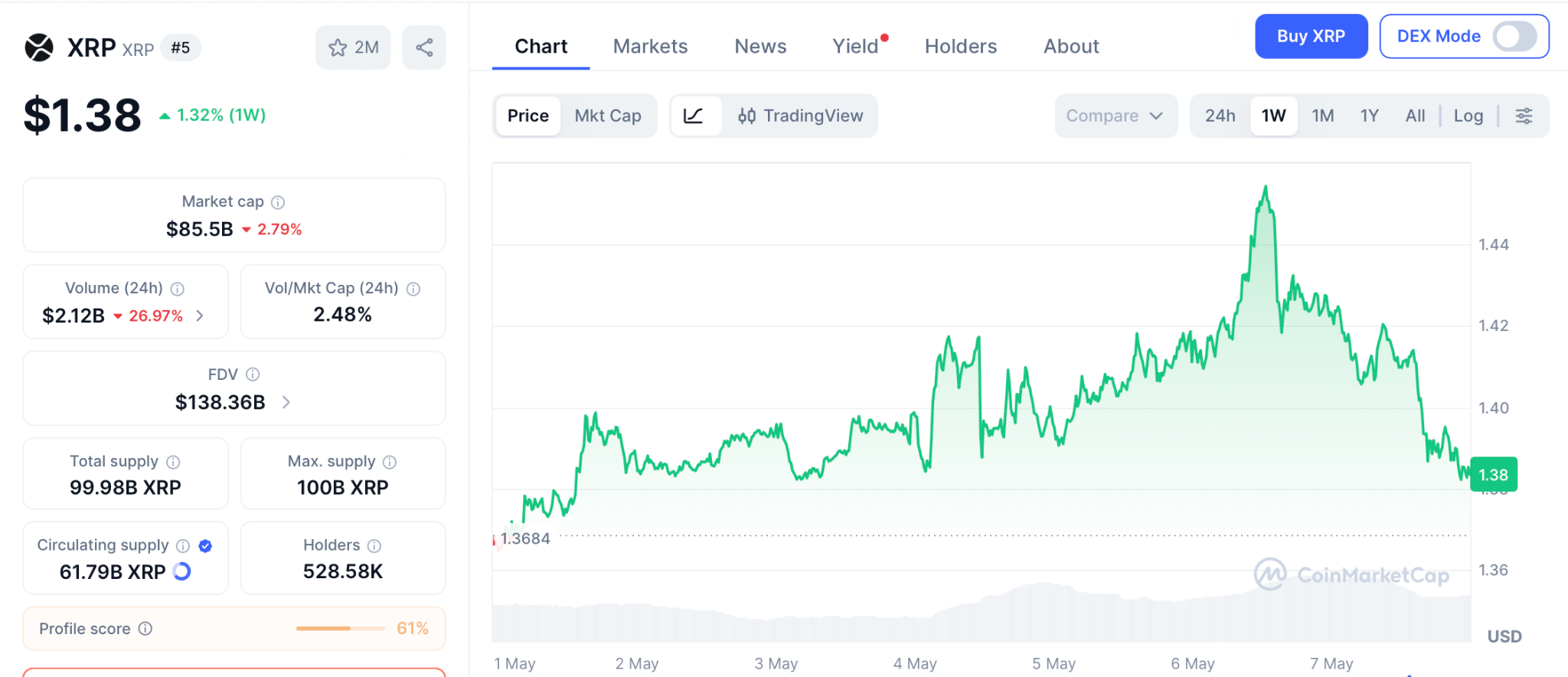

The XRP price prediction picked up serious momentum after Ripple, JPMorgan, Mastercard, and Ondo Finance completed the first cross border, cross bank redemption of a tokenized US Treasury fund on the XRP Ledger, as reported by CoinDesk. The pilot settled in under five seconds outside normal banking windows, plugging a public blockchain into JPMorgan’s $3 trillion Kinexys settlement platform.

This is the kind of plumbing that turns XRP from a payments narrative into live institutional infrastructure, with JPMorgan delivering US dollars to Ripple’s Singapore bank in the same flow that cleared the asset side on XRPL.

XRP trades at $1.38 today after a 2.34% pullback. While XRP price watchers track whether $1.45 breaks first, Pepeto is drawing capital from wallets that know presale entries reprice the moment a Binance listing arrives. With $9.86 million already raised at $0.0000001869, the math is too clean to ignore.

XRP Price Prediction Gets a Major Boost as Tokenized Treasury Settlement Lands Live on XRPL

The Ondo OUSG redemption used the XRP Ledger as the asset rail, with Mastercard’s MTN routing instructions and JPMorgan delivering dollars across borders. The pilot is the first time a public blockchain and global banking infrastructure handled a cross border tokenized fund redemption as one continuous flow.

XRPL adoption keeps building. RLUSD handled the bridging while a fraction of XRP paid the network fee, which proves what XRP holders always pointed at: when banks plug in, the network underneath gets repriced.

But the XRP price barely moved on the news, up just 1% before pulling back, because an $80 billion network gets revalued slowly.

XRP Price Prediction Versus the Pepeto Setup at Presale Entry

Smart capital does not chase the headline coin. It looks for the next setup that mirrors what worked, and Pepeto is that setup right now, lining up with projects that delivered three figure returns within twelve months of hitting Binance.

The exchange is already live, with three pieces shipping today instead of sitting in a roadmap. PepetoSwap clears swaps on Ethereum, BNB Chain, and Solana at zero cost so the position lands intact, and the cross chain bridge ships tokens between networks without taking a cut. The contract scanner sits in front of every wallet approval and reads the code first, catching risky approvals at the door instead of after the loss.

The track record turns presale conviction into actual returns. The original Pepe cofounder who pushed a meme launch from zero to $11 billion on a 420 trillion supply leads the build, while a former Binance executive runs the listing path, so the people steering this presale already know how to land a meme token on a tier one exchange.

SolidProof audited the codebase before any dollar entered, $9.86M is locked in, 175% APY staking compounds every position daily, and at $0.0000001869 the entry sits where it does only until the Binance listing flips trading live.

XRP Price Forecast: Where Does XRP Go From $1.38?

XRP trades at $1.38 today per CoinMarketCap, sitting above the $1.40 breakout zone with $1.45 to $1.47 capping upside. The XRP price prediction for 2026 targets $2.80 per Standard Chartered, roughly a 2x from here, with $8 in play if the CLARITY Act passes this summer.

XRP ETF inflows have continued and the JPMorgan settlement deepens institutional confidence, but the move from $1.38 to $2.80 plays out over months, and 2x is not the 100x a presale to listing event delivers.

Conclusion

The XRP price prediction for 2026 keeps strengthening as Ripple, JPMorgan, and Mastercard tie XRPL into live institutional banking, but the early days of XRP returns ended a long time ago. Picture the trader who watched Shiba Inu trade at fractions of a cent and said the entry would be there next month.

Picture the wallet that found Dogecoin in the early rounds and waited one more week before locking in. From $1.38, even the most bullish XRP targets pay a fraction of what those entries delivered, and the same window is open right now on a project that has not seen its first Binance candle.

No other 2026 project combines the Pepe cofounder track record, a working exchange with audited tools, and meme coin energy at presale pricing. The Pepeto page is where this entry stays open until the listing flips live, and once that switch is thrown the wallets reading and waiting are the ones who read about it next month and ask what they were doing today.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the XRP price prediction for 2026 after the JPMorgan tokenized treasury settlement?

XRP trades at $1.38 with Standard Chartered targeting $2.80 in the moderate case and $8 if the CLARITY Act passes the Senate. Pepeto at presale targets 100x from one Binance listing.

Why is Pepeto considered the strongest crypto presale right now?

Pepeto is the presale exchange combining zero fee swaps, a cross chain bridge, and an AI risk scanner at $0.0000001869, with $9.86M raised and SolidProof audit complete. The XRP price prediction shows 2x while Pepeto targets 100x on listing day.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Executives from MoonPay, Ripple, and Paxos said at Consensus Miami 2026 that stablecoin regulation has accelerated institutional adoption but that major infrastructure and privacy gaps still block mainstream use.

Summary

- MoonPay VP Richard Harrison said the GENIUS Act gave firms a regulatory permission slip, accelerating traditional finance entry into stablecoins.

- Ripple SVP Jack McDonald argued that institutional adoption depends on regulated products, trusted custody, and utility beyond market capitalisation.

- Paxos engineer Brent Perrault warned that unresolved privacy issues on public blockchains remain a significant barrier to enterprise-scale stablecoin payments.

Top executives at three of the most active stablecoin companies told the Consensus Miami 2026 audience on May 8 that new US regulation has fundamentally changed the competitive landscape for dollar-pegged tokens, bringing traditional financial institutions into a market that was previously difficult for them to enter. The shift, however, has exposed a new set of problems the industry has yet to solve.

Richard Harrison, MoonPay’s vice president of banking and payment partnerships, said the passage of the GENIUS Act gave firms across traditional finance a regulatory framework to operate within. “What GENIUS brought us was clarity,” Harrison told the panel, noting that traditional finance firms are now entering stablecoins at a faster pace because compliance is easier to evaluate.

Harrison compared the current state of stablecoin adoption to electric vehicles: the core product works, but mass-market take-up depends entirely on the supporting infrastructure. “How do you use stablecoin to pay your rent?” he said. “How do you use it to buy a cup of coffee?”

Institutional demand versus real-world usability

Jack McDonald, Ripple’s senior vice president for stablecoins, told the panel that institutional clients are focused less on market capitalisation and more on practical details: regulatory compliance, custody security, and whether stablecoins can do something useful beyond trading.

McDonald said Ripple continues to concentrate on treasury operations, collateral management, and cross-border payment settlement as the primary enterprise use cases, arguing that utility must drive adoption rather than speculative interest.

Harrison added that stablecoins currently represent a relatively small share of global remittance flows, though he projected the figure could reach around 10% of the market over the next five years as payment rails improve and more merchants integrate digital dollar services.

Stablecoin-based cross-border transfers already settle near-instantly at fees below one dollar, compared with traditional banking fees that can exceed 6%.

Brent Perrault, a senior staff software engineer at Paxos, said privacy remains the sector’s most persistent unresolved problem. Public blockchains expose transaction amounts and the flow of funds, which creates compliance and confidentiality concerns for businesses handling sensitive financial data.

Perrault warned that partial privacy solutions are insufficient because users inevitably move between private and public blockchain environments. He said competitive differentiation among stablecoin issuers is now increasingly driven by trust, distribution partnerships, and user incentives rather than technical specification alone.

Distribution gaps and what comes next

Perrault pointed to PayPal USD’s growth and Charles Schwab’s use of Paxos infrastructure as evidence that demand from established financial institutions is real and expanding beyond crypto-native firms.

The challenge, he said, is that even well-capitalised issuers with strong compliance records face significant friction when trying to connect stablecoin rails to the everyday payment systems consumers and businesses already use.

The panel’s comments at Consensus Miami came as the CLARITY Act moves toward its Senate Banking Committee markup on May 14. As crypto.news reported, five major banking trade groups rejected the Tillis-Alsobrooks stablecoin compromise language just days before the vote.

The executives at Consensus did not directly address the markup, but their remarks underscored why the regulatory outcome matters to companies building stablecoin payment products at scale.

The stablecoin market currently sits at approximately 317 billion dollars in total value. Western Union announced its USDPT stablecoin on Solana earlier in May, with issuance through Anchorage Digital.

That entry reflects exactly the dynamic Harrison described: regulation has lowered the barrier, but the infrastructure needed to make stablecoins work in everyday consumer contexts is still being built.

Swiss campaigners will drop a bid to get the Swiss National Bank (SNB) to hold bitcoin in its reserves after collecting only about half of the 100,000 signatures needed to trigger a national referendum.

The initiative sought to change Switzerland’s constitution so the SNB would hold bitcoin alongside gold and foreign-currency reserves. The group had 18 months to gather signatures and push for the country’s direct democracy to vote on the subject.

The Federal Chancellery listed the proposal as an amendment to the country’s Federal Constitution, requiring part of the SNB’s monetary reserves to be held in gold and bitcoin. The text did not specify an allocation.

The campaign had framed bitcoin as a neutral reserve asset and a hedge against exposure to dollar- and euro-denominated holdings. Supporters said those currencies make up roughly three-quarters of the SNB’s foreign-currency reserves, according to Reuters.

The SNB had already rejected the idea last year, when it opposed adding bitcoin to its reserves over concerns surrounding the cryptocurrency’s liquidity and volatility.

Bitcoin miner TeraWulf posted a net loss of $427 million in the first quarter of 2026, up from the $61.4 million loss recorded in the same period a year earlier.

Total revenue for the quarter came in at $34 million, with high-performance computing (HPC) lease revenue accounting for $21 million, roughly 60% of the total and a 117% jump from the prior quarter, according to a Friday announcement. Bitcoin mining revenue fell 50% to around $13 million.

The HPC revenue was driven by 60 megawatts of operational critical IT capacity at Lake Mariner, one of North America’s largest HPC campuses, leased to Core42. TeraWulf is also coordinating infrastructure delivery with Fluidstack and Google, with additional capacity buildings on track for delivery in 2026. The company ended the quarter with approximately $3.1 billion in cash.

“Our capital structure is designed to align long-term financing with contracted cash flows, supporting disciplined growth while maintaining financial flexibility,” chief financial officer Patrick Fleury said.

Related: CoreWeave shows how crypto-era infrastructure quietly became AI’s backbone

TeraWulf accelerates AI transition

In October last year, TeraWulf announced a 25-year lease deal with Fluidstack, backed by Google, worth around $9.5 billion in contracted revenues, an expansion of an earlier 10-year commitment. The miner is also building out a national pipeline of power-advantaged sites, including a newly acquired 480 MW site in Hawesville, Kentucky, a 300 MW project in Lansing, New York, and a 210 MW site in Morgantown, Maryland, with potential to scale to 1 gigawatt.

“We are building a power-advantaged platform that we believe is increasingly differentiated in a market constrained by access to power,” CEO Paul Prager said, noting that the company’s Abernathy joint venture, a 168 MW HPC project under a 25-year lease, remains on track for delivery in the fourth quarter of 2026.

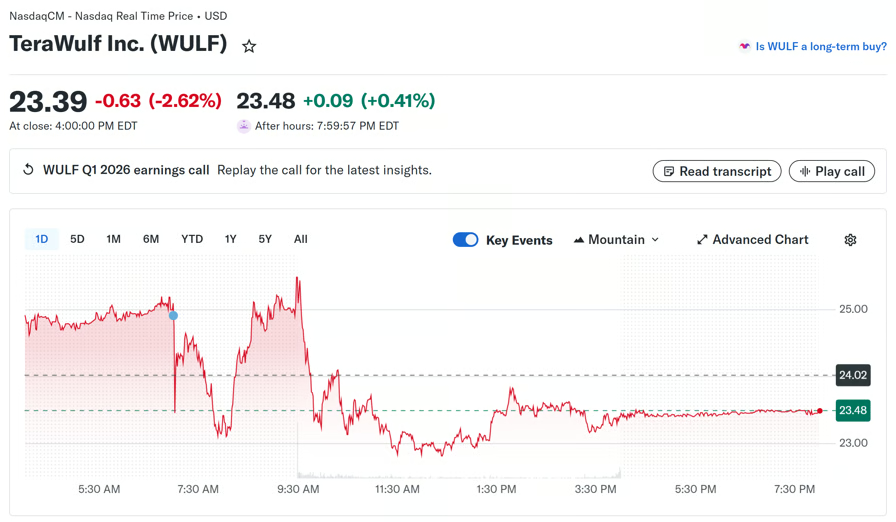

Shares of WULF closed the day down 2.6%, though the stock has gained more than 105% since the start of the year and is up over 30% in the past month.

TeraWulf shares decline. Source: Yahoo! Finance

Related: Bitcoin Miner Bitdeer Liquidates Entire BTC Treasury, Holdings Fall to Zero

Riot’s data center business generates $33 million in revenue

As Cointelegraph reported, Riot Platforms posted $167.2 million in revenue for the first quarter of 2026, with its newly launched data center business contributing $33.2 million, helping offset a decline in Bitcoin mining revenue, which fell to $111.9 million from $142.9 million a year earlier.

Bitcoin miners are pivoting to AI infrastructure as shrinking margins push the industry toward more predictable revenue, with Core Scientific, MARA Holdings, Hive, Hut 8 and Iren converting mining facilities into data centers or acquiring AI compute assets.

Magazine: Bitcoin will not hit $1M by 2030, says veteran trader Peter Brandt

Reason for Man City case delay suggested as ex-Premier League chief says ‘I question that’

Applied Materials Stock: Supplying Intel Comes With Its Perks (NASDAQ:AMAT)

Sports betting should be regulated as a financial product, not gambling, aspiring prediction market provider says

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

I Don’t Follow. I Rule #mafia #lifestyle #luxury #money #rich #mindset #millionaire #billionaire #fy

Cryptocurrency Spotlight for Beginners: A Clear Step into Crypto

Quanto devi GUADAGNARE per COMPRARE una BMW M3 2026 #money #bmw #finance #car #salary

-

Crypto World1 day ago

Crypto World1 day agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

NewsBeat6 days ago

NewsBeat6 days agoChannel 5 – All Creatures Great and Small series 7 new post

-

Crypto World2 days ago

Crypto World2 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

Tech5 days ago

Tech5 days agoImage AI models now drive app growth, beating chatbot upgrades

-

News Videos6 days ago

News Videos6 days agoAP Dhillon – Old Money (Official Audio)

-

Fashion23 hours ago

Fashion23 hours agoWeekend Open Thread: Marianne Dress

-

NewsBeat2 days ago

NewsBeat2 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Sports7 days ago

Sports7 days agoFive killed in Texas plane crash identified as Amarillo pickleball players

-

Entertainment7 days ago

New Netflix Movies in May 2026 — My Top 3 Picks to Stream

-

Entertainment7 days ago

Anna Nicole Smith’s Daughter Attends 2026 Kentucky Derby

-

Crypto World7 days ago

Pi Network Mandates Protocol 23 Upgrade for All Mainnet Nodes Before May 15 Deadline

-

Crypto World7 days ago

Crypto World7 days agoBitcoin mining equities rise in 2026 as BTC lags behind

-

Entertainment7 days ago

Entertainment7 days agoMelissa Joan Hart and More Stars Attend 2026 Kentucky Derby

-

Business5 hours ago

Business5 hours agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Entertainment7 days ago

Venus Williams’ Best Met Gala Looks Over the Years

-

Business6 days ago

Business6 days agoLuka Doncic Injury Update: Doncic’s Hamstring Recovery Slows Lakers’ Hopes Against Thunder: Can He Run Yet?

-

Entertainment7 days ago

Entertainment7 days agoNetflix’s 10-Part Miniseries Based on a True Story Is a Perfect Weekend Binge

-

Sports6 days ago

Sports6 days agoIs Man United v Liverpool on TV? Channel, streaming and how to watch Premier League fixture

-

Entertainment7 days ago

“Storage Wars” star Darrell Sheets' ex-wife breaks silence on his death

-

Business7 days ago

Business7 days agoKuwait International Airport Resumes Operations After Closure as Regional Tensions Ease in 2026

You must be logged in to post a comment Login