Crypto World

Robinhood wins bigger Wall Street bets as $135 price target emerges

Robinhood shares have climbed more than 6% after multiple Wall Street firms reaffirmed bullish ratings and projected further upside as the brokerage expands its global business and AI offerings.

Summary

- Robinhood shares rose over 6% as Wall Street firms reiterated Buy ratings and projected upside to $135.

- Analysts cited global expansion, AI-powered products, and crypto initiatives as key drivers of future growth.

- Robinhood expanded into Canada, the UK, and Singapore while launching its blockchain and AI trading features.

According to recent research notes from Piper Sandler, BTIG, and Mizuho, confidence in Robinhood’s long-term growth story has strengthened even after the stock’s strong rally. According to Yahoo Finance data, shares briefly traded above $115 after the Wall Street opening bell, extending their monthly gain to about 31% as investors responded to a series of new product launches and international expansion plans.

Piper Sandler maintained its Buy rating and kept a $135 price target on Robinhood, suggesting the stock still has room to appreciate. BTIG also reiterated its Buy recommendation with a $125 target. Meanwhile, Mizuho raised its target price to $130 from $115 while maintaining a Buy rating, making it one of the latest firms to increase expectations for the brokerage.

Global expansion continues to support Robinhood’s growth story

Mizuho’s latest research note argued that Robinhood could become the first true “hyperscaler” among online brokerage platforms. The firm pointed to Robinhood’s base of more than 27 million funded accounts, its easy-to-use trading platform, and its popularity among younger investors as reasons for its positive outlook.

The brokerage also believes Robinhood’s opportunity extends well beyond the United States. According to Mizuho, the company is expected to deepen its presence across Europe before eventually expanding further into Asian markets.

Recent announcements from Robinhood have added support to that outlook. The company said it now serves more than 1 million funded customers in Europe while confirming plans to launch Robinhood Crypto in the UK as part of its regional expansion.

Outside Europe, Robinhood officially introduced its crypto platform in Canada with zero trading fees for the first 90 days. The company also disclosed that it had secured a brokerage license in Singapore, giving it another foothold in the Asian market.

AI products and blockchain strategy attract fresh investor attention

Alongside its international rollout, Robinhood has continued expanding its technology offerings. The company recently introduced Robinhood Chain, a blockchain network designed to support AI-assisted token swaps, liquidity discovery, and access to tokenized real-world assets.

The blockchain launch followed the rollout of Robinhood’s Agentic trading tools, which use artificial intelligence to help users analyze markets and manage investments. According to the company, those AI-native features have gained traction among traders since their introduction.

The combination of blockchain infrastructure, AI-powered products, and expansion into new markets has coincided with stronger optimism from Wall Street analysts. Their latest forecasts suggest these initiatives could open additional revenue streams while helping Robinhood diversify beyond its traditional retail brokerage business.

Even with analysts maintaining bullish targets, short-term trading could still be affected by broader market volatility. For now, however, brokerage firms including Piper Sandler, BTIG, and Mizuho continue to argue that Robinhood’s international expansion, growing crypto business, and investment in AI technology provide a favorable foundation for further growth in the months ahead.

After several failed attempts to extend its recovery, Ethereum is beginning to show signs of exhaustion beneath the major100-day MA. The latest rejection from this zone has weakened short-term momentum and increases the probability of a broader pullback if key support levels fail to hold.

Ethereum Price Analysis: The Daily Chart

On the daily timeframe, ETH’s outlook is gradually shifting toward a bearish bias after multiple failed attempts to reclaim the 100-day moving average. The repeated rejection from this dynamic resistance around $1.95K, combined with the emergence of bearish daily candles, suggests buyers are losing momentum.

Meanwhile, Ethereum continues to struggle with the descending channel, with the upper boundary represented by the white trendline serving as the most critical support.

If sellers manage to push the price back inside this channel, it would confirm a bearish continuation and likely trigger a deeper decline toward the $1.56K to $1.64K demand zone. On the upside, bulls must first reclaim the $1.88K to $1.91K resistance area before attempting another move toward the 100-day MA near $1.95K.

ETH/USDT 4-Hour Chart

The 4-hour chart has turned more bearish after Ethereum broke below its ascending trendline, signaling that buyers have lost short-term control. This breakdown shifts the focus toward lower support levels unless bulls can quickly reclaim the broken structure.

The first support now lies within the $1.85K to $1.87K demand zone, where price is currently attempting to stabilize. Losing this area would likely accelerate the decline toward the next major demand zone between $1.75K and $1.79K.

On the other hand, the $1.88K to $1.91K supply zone has become the primary threshold for buyers. A successful reclaim of this region would invalidate the immediate bearish scenario and could allow Ethereum to challenge the descending resistance and the 100-day moving average once again.

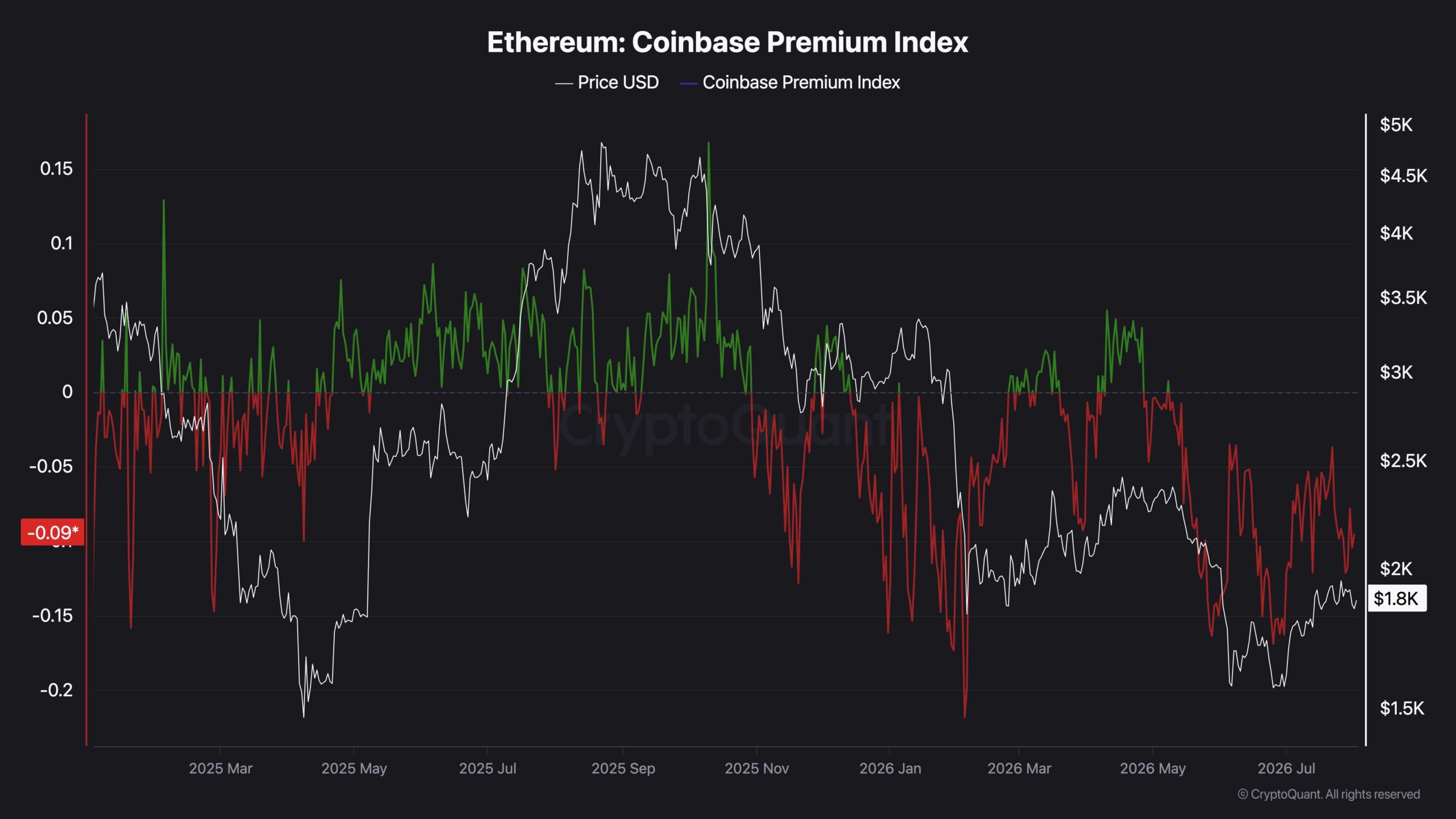

Sentiment Analysis

The Coinbase Premium Index remains in negative territory, indicating that Ethereum continues to trade at a discount on Coinbase relative to other major exchanges. This persistent negative premium suggests buying pressure from U.S.-based institutional participants remains relatively weak despite the recent recovery.

Historically, sustained positive readings have accompanied stronger bullish phases, whereas prolonged negative values often reflect cautious institutional sentiment. Until the premium returns to positive territory and remains there consistently, the current rebound may struggle to develop into a sustained uptrend, leaving Ethereum vulnerable to additional downside pressure if technical support levels begin to fail.

The post Ethereum Price Analysis: ETH’s Double Rejection at $2K Spells More Trouble Ahead appeared first on CryptoPotato.

Ripple’s XRP remains under steady selling pressure as the latest rebound attempts continue to lose momentum. The recent price action suggests sellers are maintaining control, while buyers are once again being forced to defend a critical support area.

Ripple Price Analysis: The Daily Chart

The daily chart shows little improvement compared to the previous analysis. The asset continues to trade beneath the descending resistance trendline while remaining well below the major moving averages, preserving the broader bearish market structure.

The latest candles indicate that sellers remain in control after another failed recovery attempt, pushing the price back toward the key demand zone around $1.01 to $1.04. This support has repeatedly prevented a deeper decline over the past several weeks, making it the most important level to monitor.

As long as XRP remains below the descending trendline and the main resistance between $1.24 and $1.29, the broader outlook favors continued weakness. A decisive breakdown below the $1.01 to $1.04 support zone would likely accelerate the decline toward the next major support around $0.89.

XRP/USDT 4-Hour Chart

On the 4-hour timeframe, rather than recovering from support, XRP has continued to print lower highs and lower lows while remaining capped by the descending resistance trendline.

The recent rejection near $1.09 was followed by another decline toward the $1.01 to $1.04 demand zone, showing that buyers have yet to regain control. This area remains the last significant short-term defense for the bulls.

If this support fails, the bearish momentum is likely to intensify and extend the decline toward lower levels. Conversely, buyers would first need to reclaim the descending trendline before any meaningful recovery toward the $1.24 to $1.29 resistance zone could be considered. Until then, rallies are likely to face selling pressure and remain corrective in nature.

The post XRP Price Analysis: Is a Drop Below $1 Inevitable as Sellers Stay in Control? appeared first on CryptoPotato.

Bitcoin continues to trade without a decisive directional bias as both buyers and sellers defend key technical levels. Until one side forces a confirmed breakout, the current environment is likely to remain dominated by range-bound price action and short-term liquidity grabs.

Bitcoin Price Analysis: The Daily Chart

The daily chart suggests Bitcoin is still locked in a prolonged consolidation phase between the major support around $57.8K to $60.2K and the primary resistance at $66.2K to $66.8K. Despite several attempts by both buyers and sellers, neither side has managed to establish a sustained trend beyond these boundaries.

This type of market structure typically favors liquidity sweeps and stop hunts around local highs and lows before a genuine directional move develops. As long as the asset remains trapped between these two zones, traders should expect continued choppy price action rather than a sustained trend.

A confirmed breakout above the $66.2K to $66.8K resistance could trigger another leg toward the higher resistance around $72K to $74K. Conversely, losing the $57.8K to $60.2K demand zone would invalidate the current consolidation and expose Bitcoin to a deeper correction.

BTC/USDT 4-Hour Chart

On the 4-hour timeframe, Bitcoin is trading inside an even tighter range within the broader daily consolidation. Buyers continue defending the support region at $61.8K to $62.2K, while sellers repeatedly cap rallies below the resistance around $64.9K to $65.6K.

Holding above the buyers’ defense could allow another recovery attempt toward the upper boundary of this range. However, the recent sequence of lower highs indicates that sellers still hold a slight advantage, making a breakdown below the $61.8K to $62.2K support zone the more likely scenario if buying momentum continues to weaken. Such a move could accelerate selling pressure toward the lower boundary of the broader daily range.

Sentiment Analysis

The two-week liquidation heatmap shows a notable concentration of liquidity just beneath Bitcoin’s recent lows. This suggests futures market participants have been actively defending that area, with buyers stepping in to absorb selling pressure whenever the price approaches the lower liquidity cluster.

At the same time, a substantial pool of liquidity remains above the market around the $66K to $67K region, indicating that both sides still have attractive liquidation targets. As long as Bitcoin remains inside its broader consolidation, the price is likely to continue oscillating between these liquidity zones before a decisive breakout determines the next major trend.

The post Bitcoin Price Analysis: Will the Next Liquidity Sweep Push BTC Below $60K? appeared first on CryptoPotato.

A Canadian entrepreneur lost more than $1.6 million in Bitcoin (BTC) from a Coldcard hardware wallet in under seven minutes, part of a wave that may total 1,367.05 BTC.

The case exposes an uncomfortable truth about self-custody: doing everything right may not be enough.

How One Holder Lost 18 BTC in Seven Minutes

Cold storage means keeping private keys on a device that never touches the internet. Jonathan Goodman followed that principle carefully, storing his Coldcard in a safety deposit box.

His 18.25 BTC sat in wallets secured across multiple safes. He never shared his seed phrase and kept every device isolated from online exposure.

None of it mattered on July 29, 2026. Between 9:36 and 9:43 that evening, every wallet he controlled was emptied.

Follow us on X to get the latest news as it happens.

Goodman first heard about a broader problem while at his cottage.

Assuming it would not affect him, he checked the balances in the Wasabi wallet software and found a series of red withdrawal transactions.

The vulnerability traces back to 2021. A flaw in the code that generates seed phrases left certain devices exposed, and attackers allegedly used artificial intelligence to brute-force the affected seed phrases.

He is filing reports with the police and the Ontario Securities Commission. Recovery hopes remain slim, though he wrote that the hardest part was having done everything right.

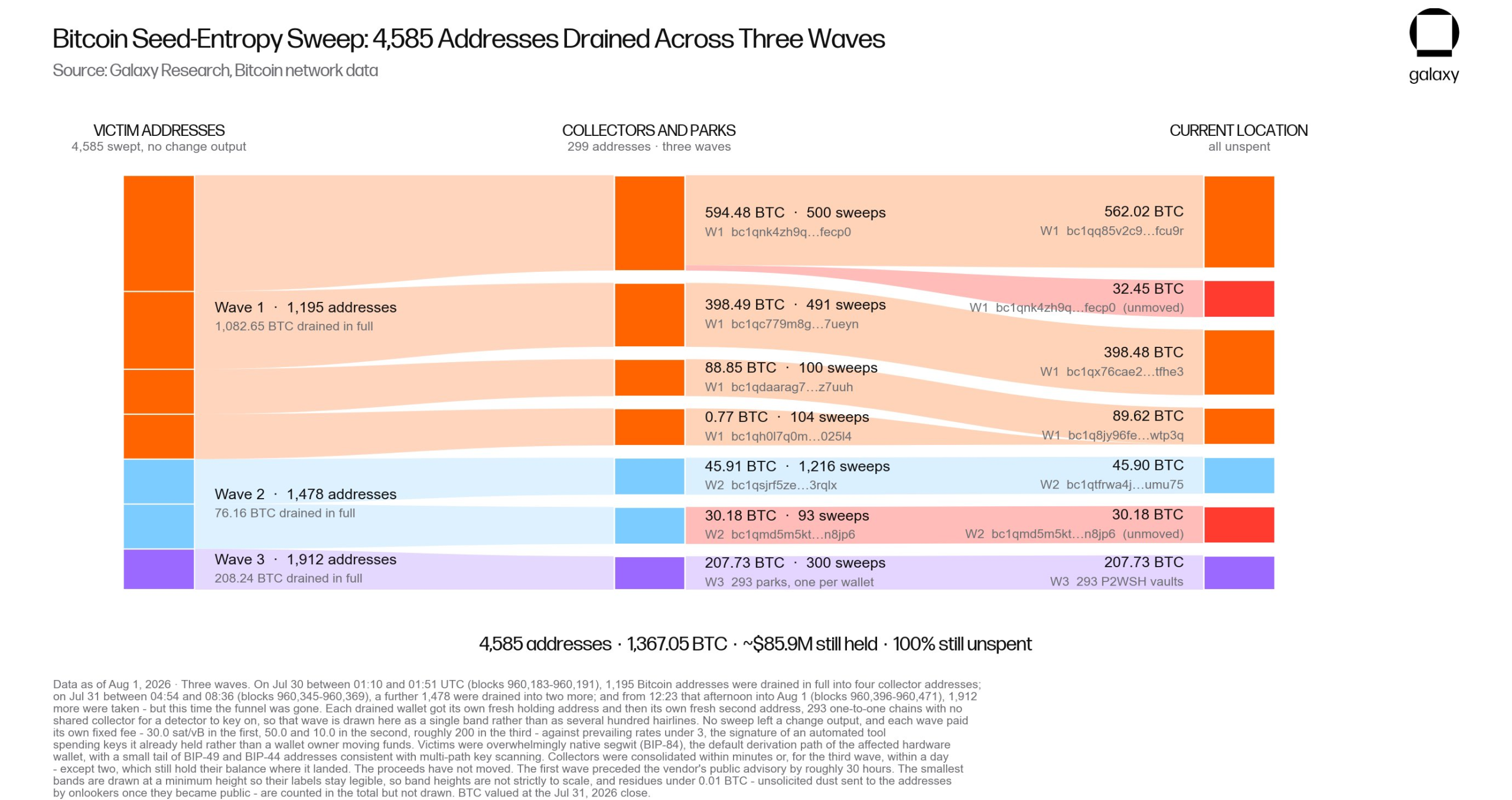

The scale extends far beyond one victim. Galaxy Research identified three suspected attack waves targeting addresses generated by Coldcard devices.

Those waves involved 4,585 source addresses and drained 1,367.05 BTC, worth roughly $88.6 million at the time of reporting.

What Galaxy Research Found in the Attack Data

Galaxy Research head Alex Thorn indicates that the attacks appear to be ongoing. He urged users who have not moved funds from potentially vulnerable setups to act immediately.

The first two waves showed similar transaction patterns and may share a common operator, though that remains unconfirmed. The third differed significantly, suggesting either updated tools or a separate actor exploiting the same key space.

The stolen Bitcoin remains in attacker-controlled addresses, with no further movement. Drained holdings had sat dormant for an average of 3.18 years, suggesting most victims were long-term holders rather than institutions.

Galaxy stressed an important caveat. Its findings rely solely on on-chain data and have not definitively confirmed insufficient randomness in the generation of the affected addresses.

“…this is a blow to bitcoin self-custody and we need to do better as a community: with security, with education, and with being realistic about complexity, expectations, and recommendations we make to friends, family, and the public…,” Alex Thorn said.

Analyst Shanaka Anslem Perera highlighted a deeper irony in Coldcard’s own documentation. The manual describes its default seed-generation method as the one it trusts most, while labeling it as low risk to users.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

Alternatives exist within the same device. Users can combine hardware output with dice rolls, or rely on dice alone, which the manual says removes all trust in the hardware. Most users likely followed the default path. That is precisely the method Galaxy Research now links to the losses.

The conceptual tension runs deeper. Reproducibility, prized for verifying firmware, becomes a liability in secret generation, since both weak and strong seeds produce valid 24-word phrases that appear identical.

Devices marketed under a “Don’t Trust, Verify” ethos can still harbor entropy flaws, leaving no visible trace. Affected users should assess their setups and migrate funds where necessary.

The post $1.6 Million Drained in a Blink: User Recounts His Dramatic Coldcard Wallet Hack appeared first on BeInCrypto.

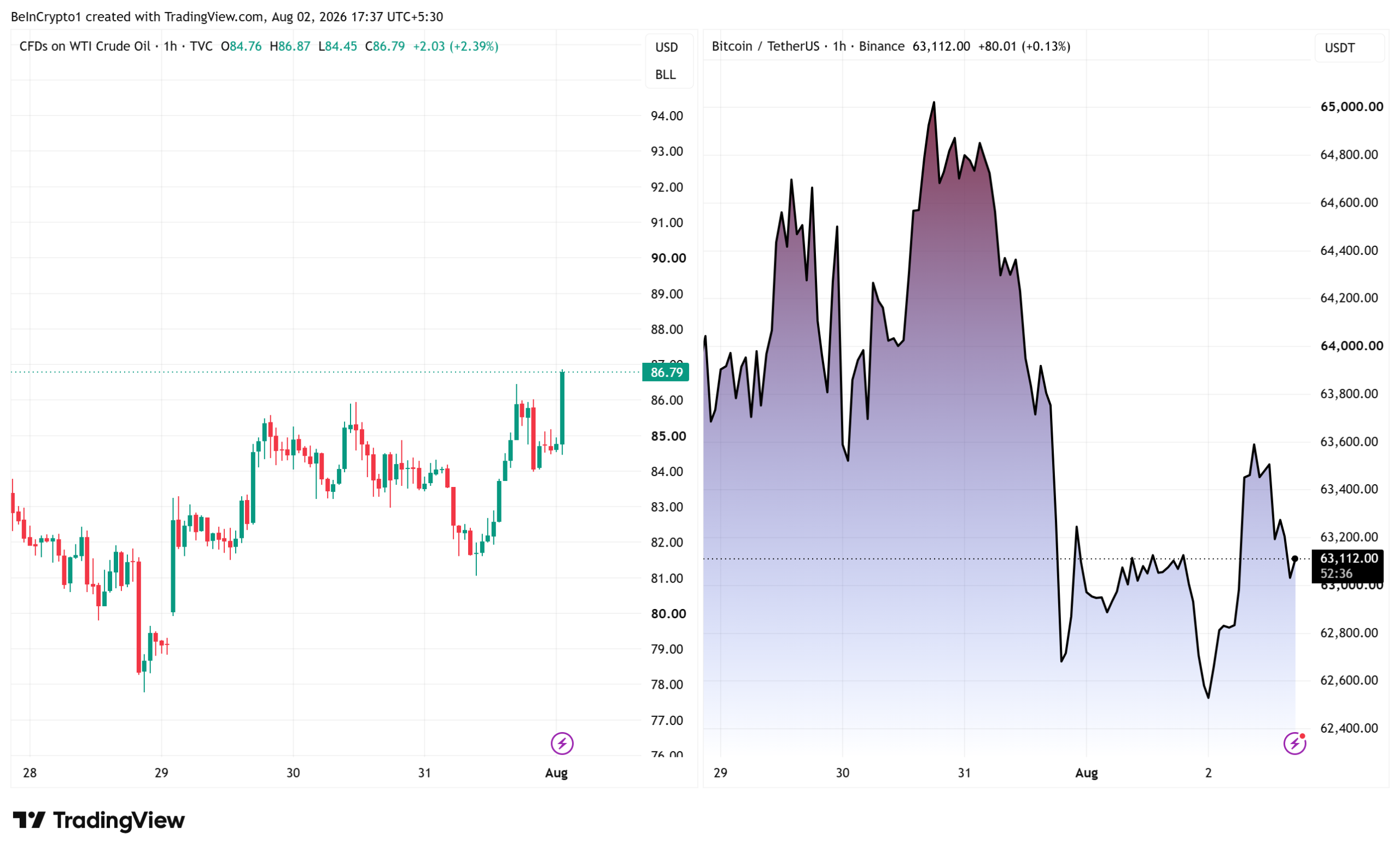

Iran has denied President Donald Trump’s claim that a deal exists to reopen the Strait of Hormuz, the world’s busiest oil route. Oil jumped on the denial.

Bitcoin (BTC) barely moved. That gap says a lot about what crypto traders now choose to ignore.

Trump Says a Hormuz Deal Exists. Iran Says It Does Not

Trump posted on Truth Social early Sunday. He said he had canceled a planned strike on Iran.

He wrote that Iran and its neighbors asked him to hold off. The reason, he said, was that “the perimeters of a deal has been agreed to.”

That deal would open the Strait of Hormuz right away. It would also end Iran’s nuclear threat.

Iran answered within hours. Fars News Agency quoted a source close to the nuclear talks.

“There is no agreement regarding the reopening of the Strait of Hormuz, and the news published about it is false,” Fars News Agency, via CGTN.

Follow us on X to get the latest news as it happens

Iran’s acting defense minister, Seyyed Majid Ibn Al-Reza, called Trump’s words psychological warfare. Fars International called Trump’s terms a wish list.

None of this is new. An earlier pause in strikes in late July also went nowhere.

Talks did happen, though. Qatari mediators met Iran’s foreign minister, Abbas Araghchi, and US envoy Steve Witkoff on Saturday. Saudi Crown Prince Mohammed bin Salman urged Trump to cool things down.

Why Oil Jumped and Bitcoin Did Not

Start with the map. The Strait of Hormuz is a narrow sea lane between Iran and Oman.

About 20 million barrels of oil passed through it every day in 2024, EIA data shows. That is roughly a fifth of the oil the world uses.

Here is the problem. Only about 2.6 million barrels a day can go around it, through pipelines in Saudi Arabia and the UAE.

The rest has nowhere else to go. That is why one denial can move a market this big.

WTI crude, the US benchmark, closed at $84.67 on Friday. It then rose about 2.4% to trade near $86.79.

The denial also puts an official forecast in doubt. On July 7, the EIA cut its Brent crude forecast for this quarter by $27 a barrel, to $74. It cited the June US-Iran deal and busier traffic through the strait.

That June deal has since fallen apart. Analysts tracking Hormuz reopening timelines now expect the route to stay restricted into 2027.

Bitcoin did almost nothing. It added 0.08% in 24 hours and sat near $63,063.

It also trades about 50% below its record of $126,080, set on October 6, 2025. The muted Bitcoin price reaction suggests traders now ignore headlines that change nothing on the water.

What Happens Next

Oil matters to crypto for one reason. It feeds inflation.

June proved the link. US energy prices fell 5.7% that month, the steepest drop since April 2020.

The BLS said energy did most of the work. Headline prices fell 0.4% over the month. Annual inflation cooled to 3.5% from 4.2%.

Energy is still expensive over a full year, however. Gasoline is up 26.7%.

So a lasting jump in oil would undo that progress. That makes Federal Reserve rate cuts harder to justify. Rate cuts are what assets like Bitcoin want.

The next check comes August 12, when the BLS publishes July inflation.

Until ships can sail through Hormuz freely, oil keeps its war premium. Bitcoin keeps waiting.

The post Iran Denies Trump’s Hormuz Deal, Oil Jumps but Bitcoin Watches appeared first on BeInCrypto.

South Koreans sent $367 million more in stablecoins out of the country than they brought back in June. It was the 18th month in a row that money left.

The Financial Supervisory Service (FSS) handed those numbers to lawmaker Lee Jong-wook. The streak started in January 2025. Traders are chasing something they cannot get at home.

Why South Korea’s Stablecoin Outflows Keep Widening

Five exchanges handle almost all local crypto trading. They are Upbit, Bithumb, Coinone, Korbit, and Gopax.

In June, they sent roughly $1.8 billion in stablecoins to foreign platforms. About $1.44 billion came back. The gap was $367 million.

Local media reported that across the whole second quarter, close to $1.1 billion left.

Follow us on X to get the latest news as it happens

The size is what caught the attention of lawmakers. Koreans bought about $470 million of foreign shares in June, according to the Korea Securities Depository. The stablecoin outflow matched 77.6% of that figure.

A year earlier, the ratio sat near 20%. Crypto money now leaves the country almost as fast as stock money.

The trend held even as the local market shrank. Seoul confirmed a 22% crypto tax for 2027, and domestic trading volume fell nearly 55% in the first half.

One caveat belongs here. The FSS counts only the five licensed exchanges, so coins sent to private wallets first never show up.

What Foreign Exchanges Offer That Seoul Cannot

Korean platforms mostly offer plain spot trading. That is the whole problem.

Foreign venues offer far more.

- Crypto derivatives with heavy leverage

- Dollar-based real world assets (RWAs)

- Decentralized Finance (DeFi) protocols

- Staking rewards

Some also list Samsung Electronics, SK Hynix, and Hyundai Motor as tradable contracts. Leverage on those can run into the tens of times. A stablecoin transfer is the cheapest way in.

The same hunger shows up in regulated markets. Koreans put a net $1.28 billion into foreign leveraged exchange-traded funds (ETFs) in June. That was more than triple the May total.

Seoul did try to compete. Korea listed its first single-stock leverage ETFs on May 27. Less than a month later, FSS Governor Lee Chan-jin publicly criticized them.

A bigger fix is on the way. Four agencies published a plan on July 19 to legalize won-backed stablecoins. A separate bill would treat crypto as national wealth.

The Leverage Unwind Sitting Behind the Numbers

The regulator’s worry proved well founded. Fourteen leveraged ETFs track Samsung and SK Hynix. Their assets shrank from about $10.7 billion at the end of June to $6.3 billion by July 13.

Margin loans fell too. Korean brokerages held roughly $21.8 billion on July 30, down about $4.4 billion since June 24.

The Kobeissi Letter says $67 billion has drained from margin accounts across Korea, China, and Taiwan. BeInCrypto could not confirm that total.

The KOSPI lost 22.19% in July, its worst month since 1997. Then it jumped 17.91% on July 31, a record single day.

Economist Steve Hanke blames global fatigue with AI hype. That rebound, led by a 29.95% gain in SK Hynix, cuts against the idea. Asia’s unwinding AI trade has swung just as hard in Tokyo.

The stablecoin figures tell a steadier story. Korean money is not hiding. It is relocating, much as it did when Korean investors cashed out late last year.

Lee sits on the National Assembly’s finance committee for the People Power Party. He wants the government to act.

“As the ‘coin move’ from domestic to overseas spreads, funds are flowing abroad, and investors are being defenseless against high-risk derivatives on foreign exchanges,” local media reported, citing Lee.

Seoul can close the exits or widen the menu at home. That choice decides what month 19 looks like.

The post South Koreans are Sending Stablecoins to Foreign Exchanges at Record Rate appeared first on BeInCrypto.

Everything under one login

Round-the-clock trading is one part of the plans exchanges have for traditional assets. Coinbase and Binance want customers to trade crypto, stocks and other products through one account, a model both have described as an “everything exchange” or financial super app.

Coinbase is preparing to offer U.K. customers equities and derivatives alongside crypto after securing investment-services authorization from the Financial Conduct Authority under rules based on the Markets in Financial Instruments Directive, or MiFID.

The authorization allows Coinbase to offer traditional shares to retail customers and crypto, equity and commodity perps to eligible institutional and advanced traders, the company said.

“Perpetual futures are a core focus of what Coinbase is trying to bring to market,” said Keith Grose, U.K. CEO at Coinbase, in an interview with CoinDesk. “We’re really focused on being the ‘everything exchange.’”

Grose said the longer-term plan is to bring spot crypto, perpetual futures, traditional equities, and eventually tokenized versions of other assets into one place. That could allow customers to use positions across different markets as collateral or borrow against their equities.

Using stocks as collateral

Binance is testing another part of the model by allowing some high-net-worth clients to use tokenized stock positions as collateral for other trades.

“We recognize you could have Nvidia or SpaceX stock, a tokenized version,” Jan said. “You could actually have a tokenized stock put on our exchange, and we’ll use that as collateral for you to trade something else. It could be a crypto derivative.”

Trump Media-linked wallets transferred 2,628 Bitcoin, valued at about $165 million, to Crypto.com on Aug. 2, according to on-chain analysts Lookonchain.

Summary

- 2,628 BTC moved to Crypto.com, but no company filing has confirmed an outright sale yet.

- Trump Media reported 9,542.16 BTC in March, including 4,260.73 BTC pledged as secured convertible-note collateral.

- Lookonchain estimates realized and unrealized Bitcoin losses at $555 million after seven months of transfers.

The movement reportedly reduced the wallets’ remaining balance to about 4,261 BTC.Lookonchain described the movement as another sale and estimated that Trump Media had disposed of 7,281 BTC over seven months. However, neither Trump Media nor an SEC filing had confirmed the latest coins were sold as of Aug. 2. An exchange deposit can precede a sale, custody change, collateral arrangement or another internal transaction.

Trump Media transfer is not a confirmed sale

Lookonchain said the company originally acquired 11,542 BTC for about $1.37 billion, averaging $118,522 per coin. Its post stated, “It looks like Trump Media sold another 2,628 BTC,” wording that reflects uncertainty about the final transaction.

EmberCN separately traced the 2,628 BTC to Crypto.com and estimated that the linked wallets had transferred out about 7,281 BTC. The Arkham entity page identified two recent movements totaling roughly 2,628 BTC, including transfers of about 2,429 BTC and 198.9 BTC.

Source: Akham

Remaining Bitcoin nearly matches pledged collateral

Trump Media’s latest quarterly filing provides the strongest company-confirmed baseline. The company reported 9,542.16 BTC at March 31, with a cost basis of $1.131 billion and a fair value of $647.1 million. It recorded no change in the number of coins during the first quarter.

The SEC filing also said 4,260.73 BTC served as collateral for convertible notes and could not be withdrawn or distributed unless indenture requirements were met. The restrictions are scheduled to end no later than May 29, 2028.

The reported post-transfer balance of about 4,261 BTC almost exactly matches that pledged amount. This suggests the tracked wallets may now mainly contain restricted collateral, but the on-chain labels do not prove the accounting or legal status of each coin.

The $555M loss remains an outside estimate

Lookonchain calculated that the 7,281 BTC left the linked wallets at an average price of $74,855, generating about $545 million. It then estimated Trump Media’s combined realized and unrealized Bitcoin loss at approximately $555 million.

Those figures are not company-confirmed. The calculation assumes exchange transfers became sales near the observed market prices. It also combines estimated losses on transferred coins with the paper loss on the remaining balance. Trump Media’s March filing confirmed a lower fair value, but said the company had not realized material digital-asset losses at that reporting date.

Trump Media transferred 2,650 BTC worth about $205 million to Crypto.com on May 22. The coins remained in an exchange-linked wallet when that report was published, showing why a transfer should not automatically be reported as a completed sale.

Truth API launch adds separate regulatory scrutiny

The Bitcoin movement followed Trump Media’s Aug. 1 launch date for Truth API, a paid service providing institutional customers with low-latency access to influential Truth Social posts. The company said the product delivers posts in milliseconds and could create a recurring revenue stream. Its revenue expectations remain forward-looking claims.

U.S. Senators Adam Schiff and Elizabeth Warren asked the SEC to investigate whether the service could violate federal securities laws. Their letter raised concerns that paying firms could receive market-moving presidential posts faster than ordinary users. The request is not an SEC finding, and the agency had not publicly announced an enforcement action.

Crypto.news reported that Trump Media posted a $405.9 million first-quarter net loss, partly reflecting unrealized markdowns across Bitcoin, Cronos and securities.

The company’s next quarterly filing should clarify whether the May and August transfers were sales, custody movements or transactions linked to hedging and financing arrangements. No verified Bitcoin or DJT price movement can be attributed solely to the Aug. 2 transfer.

Bitcoin Improvement Proposal 110 can no longer reach its 55% voluntary miner threshold during the current difficulty period, according to blockchain signaling data and an Aug. 1 analysis from Strategy Executive Chairman Michael Saylor.

Summary

- 28 signaling blocks appeared among 1,108, leaving BIP-110 at 2.53% support as of Aug. 2.

- Saylor said all 24 initial signals came from DATUM miners sharing rewards through OCEAN’s system.

- Mandatory signaling starts at block 961,632, when enforcing nodes reject every non-signaling block as invalid.

Strategy’s official website identifies Saylor as the company’s executive chairman. At block 960,561, Saylor counted 24 signaling blocks among 946, equal to 2.54%. He said every signal came from miners using DATUM while sharing rewards through OCEAN, with none identified outside that system. By 11:13 UTC on Aug. 2, the public BIP-110 monitor had advanced to block 960,723 and counted 28 signals among 1,108 blocks, or 2.53%. Only 908 blocks remained.

BIP-110 cannot reach voluntary lock-in

The proposal needs 1,109 signaling blocks within one 2,016-block difficulty period to lock in voluntarily. Even if every remaining block in the current period signals, the total could reach only 936. Saylor therefore said the threshold was “mathematically unreachable” and argued that the observed count was “not miner consensus.”

The latest monitor supports that arithmetic. However, it does not independently establish Saylor’s attribution of every signaling miner. His pool claim applied to the 24 blocks examined at block 960,561. The monitor confirms that the overall rate remained almost unchanged after four additional signals appeared.

BIP-110 would restrict Bitcoin transaction data

BIP-110, formally called the Reduced Data Temporary Softfork, proposes seven temporary consensus restrictions. These include limiting most new output scripts to 34 bytes, capping OP_RETURN outputs at 83 bytes, restricting certain data pushes to 256 bytes and temporarily limiting several Taproot features. Outputs created before activation would remain exempt.

Supporters say the one-year rules would reduce arbitrary data storage and keep Bitcoin focused on monetary activity. Critics, including Saylor and Blockstream co-founder Adam Back, argue that consensus rules should not determine which currently valid transaction structures deserve block space. As previously reported, Saylor said fee markets and individual node policies offer a safer response to disputed data use.

Saylor questions OCEAN and DATUM’s role

Saylor also alleged that OCEAN made BIP-110 signaling the default on an existing endpoint. He called the initiative a “vertically integrated marketing campaign for Knots and OCEAN/DATUM.” That description represents his interpretation rather than a finding by an independent technical body.

The official BIP-110 installation guide directs users toward Bitcoin Knots and includes instructions for pointing rented hashpower at a DATUM node. OCEAN’s DATUM documentation says miners create block templates through their local nodes, while the pool coordinates reward splits instead of constructing mining work. Those documents confirm the technical relationship, but they do not independently establish Saylor’s claim about promotional intent.

Mandatory signaling becomes the next test

The current voluntary period ends at block 961,631. From block 961,632 through 963,647, software enforcing BIP-110 is designed to reject every block that does not signal bit 4. The proposal would then lock in at block 963,648 and activate at block 965,664, when its transaction restrictions would begin for 52,416 blocks.

Saylor warned that any 100% signaling reading during the mandatory window would reflect the software rule rather than a fresh vote of support. Foundry USA Pool has separately asked its mining customers to vote on whether the pool should signal, with its voting window scheduled to close near block 961,632. No verified result was publicly available by Aug. 2.

The next decisive evidence will come from major mining pools, exchanges, wallets and node operators before the mandatory period starts. Low voluntary signaling does not automatically cancel BIP-110 because its deployment includes mandatory signaling. However, enforcing nodes could follow a minority chain if most hashpower continues mining non-signaling blocks. Saylor and Back warned that enforcing the proposal without broad agreement could divide the network.

Bitcoin has seen a spike in very small transfers—moves of less than 1 BTC—that match the intensity last observed around the collapse of FTX. The renewed activity comes as researchers continue to track a suspected Coldcard wallet-related hack, underscoring how quickly users are reacting when self-custody tools appear compromised.

According to CryptoQuant head of research Julio Moreno, Friday recorded the highest daily level of sub-1 BTC transfers since November 2022, with 39,600 BTC moved. The total was just 300 BTC below 39,900 BTC transferred on Nov. 16, 2022, shortly after FTX filed for bankruptcy. Moreno framed the comparison as a sign of urgency and said users appear to be “taking action.”

Key takeaways

- Daily Bitcoin transfers below 1 BTC hit their highest level since November 2022, totaling 39,600 BTC, per CryptoQuant’s Julio Moreno.

- Galaxy Research says the suspected Coldcard incident caused estimated losses of 1,367 BTC across 4,585 addresses, after identifying a further 207.7 BTC taken in an additional wave.

- Galaxy’s Alex Thorn warned that the attack was still ongoing and urged affected users to move funds immediately from Coldcard-generated addresses.

- The incident is reigniting debate over whether self-custody is safer than relying on third-party platforms, with executives arguing the impact differs across user approaches.

Small-transfer surge echoes the post-FTX era

While large market moves often capture headlines, the current data point focuses on behavior at the granularity of everyday wallet operations: sub-1 BTC transfers. Moreno’s analysis suggests the market is seeing a level of small withdrawals not observed since the period following FTX’s bankruptcy filing.

The comparison matters because it points to reflexive user behavior—moving funds in smaller increments—rather than a single, coordinated “whale” action. In the wake of FTX, exchange-related uncertainty drove users toward faster, more defensive moves. Here, the catalyst is different: ongoing concerns tied to Coldcard-generated addresses.

Moreno’s observation that these transfers had not occurred at similar daily intensity since the FTX collapse suggests that the Coldcard incident may be triggering a comparable sense of immediate risk. That doesn’t prove equivalence in scale or cause, but it does show that user reaction can look similar even when the underlying event is distinct.

Galaxy Research details additional theft wave

Galaxy Research, part of Galaxy Digital, reported Saturday that it had identified another attack wave tied to the suspected Coldcard hack. In that wave, an additional 207.7 BTC was drained—valued at roughly $13.2 million at the time Galaxy cited.

Including the newly identified activity, Galaxy estimated total losses of 1,367 BTC, affecting 4,585 addresses. Galaxy’s reporting suggests the incident is not a single moment of exploitation, but an ongoing process where both victims and attacker infrastructure continue to emerge as investigators refine their tracking.

Galaxy also points readers to a Coldcard-focused tracking resource, “Coldcard Watch,” as part of the broader transparency around wallet activity connected to the suspected incident.

“Still ongoing” warnings push users toward immediate withdrawal

Alex Thorn, Galaxy Digital’s head of firmwide research, said in an X post on Sunday that the attack remained active. Thorn urged users to move funds from Coldcard-generated addresses immediately if they had not already done so.

Thorn added that his team continues to identify both new victim addresses and attacker addresses. He also noted that reports from users have helped investigators and authorities track stolen funds, reinforcing a practical implication for readers: in incidents where on-chain patterns are evolving, user-provided information can accelerate investigative work.

The warning is also a reminder that self-custody isn’t only about holding assets—it’s about operational readiness. When wallet-generated addresses are implicated, the “time to react” becomes part of the security model, whether users follow best practices or not.

Self-custody debate returns as commentators argue “failure” vs “risk control”

The suspected Coldcard hack has again pulled the conversation toward the long-running fault line in crypto security: self-custody versus third-party custody. Self-custody is a foundational principle in Bitcoin, emphasizing user control without dependence on intermediaries. Yet security incidents involving consumer-grade tools can complicate the narrative and raise fresh questions about usability and safety.

Nick Neuman, CEO of Bitcoin security company Casa, pushed back against claims that “self-custody is over.” He argued that because self-custody is distributed, users have time to respond as threats are identified. Neuman also estimated that potentially 10 times more Bitcoin was protected through self-custody than was stolen and identified so far in the attack.

That position reframes the debate from whether an incident can occur at all to how the system responds once the risk becomes visible. In Neuman’s view, the existence of ongoing victims does not negate the defensive advantage that self-custody can provide—especially when users monitor, verify, and act on warnings.

Others took the issue in a different direction. Eric Balchunas, a senior ETF analyst at Bloomberg, argued via X that Bitcoin exchange-traded funds may offer a safer and more convenient alternative for many users, pointing to the longer operating history of ETFs.

In contrast, critics of that argument say the Coldcard episode reflects a failure of a specific wallet provider or implementation rather than a fundamental breakdown of self-custody itself. The tension here is important for readers to recognize: “self-custody” is not a single technology—it’s a set of practices and tools—so incidents can be interpreted as either systemic or localized depending on what readers believe broke down.

What to watch next

With Galaxy saying the attack is still unfolding and continuing to identify new victim and attacker addresses, the next key signal will be whether transfer patterns and wallet-specific indicators stabilize as users move funds. For investors and builders, the bigger question is how quickly the broader community can validate affected addresses and coordinate response—because in cases like this, speed is part of the security outcome.

The Best Financial Strategies by Income: $40k, $75k, $100k+

Fishing lake up for sale in pretty Cambridgeshire village

Capital Power: Picking Up Stock After A Dividend Hike (TSX:CPX:CA)

Renter of Home in Anne Heche Crash Denies Settlement With Son

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Weekend Open Thread: Staud – Corporette.com

The Best Financial Strategies by Income: $40k, $75k, $100k+

Power of money||#shorts #ytshorts #sigma #motivational #trendingshorts #trending #inspire

Crypto Trading For Beginners | Bitcoin Trading for Beginners | Crypto Trading kaise kare | App India

-

Sports7 days ago

Sports7 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business4 days ago

Business4 days agoWhy Trees Belong on the Risk Register

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Wit & Wisdom

-

Tech7 days ago

Tech7 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Politics2 days ago

Politics2 days agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Politics6 days ago

Politics6 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World24 hours ago

Crypto World24 hours agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics5 days ago

Politics5 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Entertainment5 days ago

Entertainment5 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

News Videos7 days ago

News Videos7 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Business4 days ago

Business4 days agoMajor shareholder moves on Canyon

-

News Videos3 days ago

News Videos3 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World1 day ago

Crypto World1 day agoXRP Ledger v3.3.0 brings five institutional features

-

Crypto World5 days ago

Crypto World5 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech6 days ago

Tech6 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos5 days ago

News Videos5 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics3 days ago

Politics3 days agoLuke Littler’s dominance sparks GOAT debate

-

Sports3 days ago

Sports3 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Business5 days ago

Business5 days agoJohnson & Johnson agrees to $5.5B settlement over talc cancer claims

-

Crypto World5 hours ago

Crypto World5 hours agoCrypto PAC spending tops $2M in Michigan House race

You must be logged in to post a comment Login