Crypto World

Singapore court grants $3M to Terraform UST collapse victims

Singapore court has awarded more than $3 million in damages to 40 investors after finding Terraform Labs and co-founder Do Kwon liable for fraudulent misrepresentations tied to the 2022 TerraUSD collapse.

Summary

- Singapore court awarded more than $3 million to 40 investors after finding Terraform Labs and Do Kwon liable for fraudulent UST claims.

- The ruling followed earlier court findings and used a revised UST valuation that increased compensation for eligible claimants.

- Terraform’s legal troubles continue as bankruptcy proceedings and other lawsuits linked to the 2022 Terra collapse remain ongoing.

According to the June 29 judgment from the Singapore International Commercial Court (SICC), the award concludes the second tranche of a representative fraud action brought by 275 investors who sought compensation for losses suffered during the collapse of the TerraUSD (UST) algorithmic stablecoin in May 2022.

The latest ruling follows the court’s first-tranche decision in 2025, which found that Terraform Labs Pte Ltd and Do Kwon made actionable fraudulent representations. It also incorporates guidance from the Singapore Court of Appeal’s March 2026 decision, which revised the method for calculating damages by adopting a higher cut off value of about $0.60485 per UST.

Court finds investors relied on false UST claims

In its ruling, the SICC found that Terraform and Kwon falsely represented UST as a stablecoin capable of reliably maintaining its one dollar peg through its algorithm, reserves, and LUNA-based arbitrage mechanism. According to the court, those statements appeared on Terraform’s website, white papers, and public communications despite being false or made with reckless disregard for their accuracy.

The court held that some investors relied on those claims when buying or continuing to hold UST, leading to financial losses after the stablecoin lost its peg. Damages were therefore calculated on a reliance basis for holdings up to May 12, 2022, while losses after that date were treated as too speculative for compensation.

The Court of Appeal’s earlier decision to increase the UST cut off valuation resulted in higher compensation for eligible claimants than under the original damages model.

Bankruptcy cases continue as legal pressure grows

The Singapore judgment adds to Terraform’s expanding legal challenges after the company entered Chapter 11 bankruptcy proceedings in the United States. Claims reconciliation for creditors is ongoing, and any further recoveries for investors are expected to depend largely on distributions from the bankruptcy estate, alongside the outcome of other pending litigation.

Earlier this year, Terraform’s court-appointed bankruptcy administrator also sued market maker Jane Street, alleging the firm used confidential information and manipulated markets to profit during the Terra ecosystem’s collapse. Jane Street denied the allegations, calling the lawsuit an attempt to extract money and maintaining that Terra investor losses resulted from fraud committed by Terraform’s own management.

Do Kwon, who was sentenced to 15 years in prison after pleading guilty to fraud charges in the United States, also continues to face criminal proceedings in South Korea alongside other legal actions connected to the collapse.

According to the SICC ruling and related court proceedings, the case adds to a series of legal actions examining how crypto projects communicated risks to investors before major failures. The court’s findings may also influence future representative actions involving digital asset projects, while regulators in several jurisdictions continue to push for stronger disclosure standards for stablecoin and decentralised finance products.

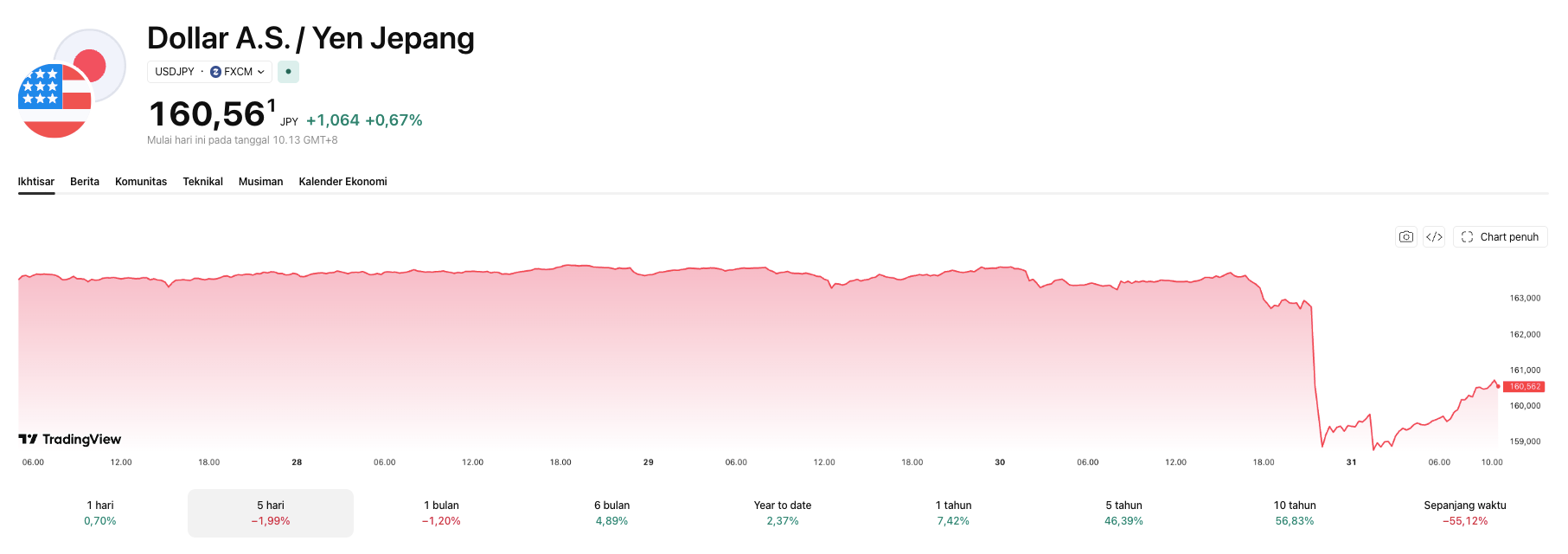

The Bank of Japan is set to hold its policy rate at 1% on Friday. Confirmed currency intervention sent the Japanese Yen (JPY) surging against the US Dollar (USD) before partly reversing.

A market source told Reuters that Japan carried out yen-buying, dollar-selling intervention overnight. The move pulled the currency off a 40-year low in its biggest single-day jump since January 2023.

A Yen Rally Already Fading

USD/JPY tumbled from above 163 to below 158 on Thursday. The pair then climbed back to 160.175 in early Friday trading as the intervention effect began to fade.

Still, the reversal shows how quickly currency moves can unwind without follow-through signals from the central bank itself.

Rodrigo Catril, senior FX strategist at National Australia Bank, said the timing suited Japan’s weaker dollar and calmer risk sentiment.

“If you want to kind of intervene, it’s probably quite a good time.”

Rodrigo Catril, National Australia Bank

The Bank of Japan raised its policy rate to 1% in June, the highest level in 31 years. Analysts expect Friday’s meeting to hold that rate while striking a hawkish tone. A Reuters poll points to another hike, to 1.25%, by year-end.

The Fed’s Hold Adds Pressure

The Federal Reserve also held rates steady Wednesday, its fifth straight pause. Traders questioned the central bank’s resolve on inflation, weakening the dollar broadly. That adds pressure on Kazuo Ueda, the Governor of the Bank of Japan (BOJ), to sound convincingly hawkish.

The US Dollar Index (DXY) fell 0.7% in the previous session, Reuters reported. The index was on pace for a 1.5% weekly drop.

That broader dollar weakness narrows the gap between the Fed’s benchmark rate and the BoJ’s 1% level. Traders use that spread to fund the yen carry trade, borrowing cheap yen to buy higher-yielding dollar assets.

The strategy only works if the rate gap holds and the yen doesn’t strengthen too quickly. A narrower gap or a stronger yen could unwind those trades fast, adding another reason to watch Ueda’s tone closely.

The post BoJ Holds Rates at 1%: Will Japan’s Yen Intervention Hold? appeared first on BeInCrypto.

Senate Minority Leader Chuck Schumer has introduced legislation aimed at creating a dedicated US anti-corruption bureau, arguing that existing oversight is not designed to stop presidents from profiting while in office—an accusation he ties directly to President Donald Trump’s cryptocurrency-related investments.

Schumer’s proposal, the Anti-Corruption Bureau Creation Act, would establish a new federal agency with authority to “investigate, enforce, and prevent executive branch corruption,” according to a Thursday announcement from Schumer’s office. The bill also seeks to consolidate key ethics and enforcement bodies under one roof—an approach lawmakers supporting the measure say could strengthen accountability more than the current “patchwork” of watchdogs.

Key takeaways

- Schumer’s bill would create a new federal anti-corruption bureau with investigative, enforcement, and preventive powers focused on executive branch conduct.

- The legislation points to reported Trump earnings from investments, including cryptocurrency exposure, as part of a broader argument for tighter safeguards.

- The proposed bureau would incorporate the Federal Election Commission, the Office of Government Ethics, and the Office of Special Counsel into a single structure.

- Supporters are also pushing the measure alongside continued negotiations over the Senate’s crypto market-structure effort, the CLARITY Act, which still lacks a scheduled vote.

- Even if the bureau legislation clears Congress, Trump could veto it; overriding a veto would require a two-thirds majority in both chambers.

A new enforcement model pitched as a response to crypto-related conflicts

In a statement released with the bill introduction, Schumer said he had introduced the Anti-Corruption Bureau Creation Act to address executive branch corruption more directly. The proposal is built around Congress’ findings—stated in the bill text—that Trump disclosed earning more than $2 billion from investments in 2025, including $1.4 billion associated with cryptocurrency, and that his family holds more than $1 billion in a crypto fund tied to foreign governments.

Schumer framed the new agency as having “real teeth,” emphasizing that it would include enforcement authority rather than acting only as a monitor. He also said the bureau would be staffed by a bipartisan group of seven members confirmed by the Senate.

To address remedies for wrongdoing, the bill includes mechanisms allowing private citizens and state authorities to pursue recovery of funds that Schumer described as stolen from Americans “through corruption.”

“This new bureau is one where these institutions work in symbiosis, strengthening each other and eliminating barriers between them which often got in the way,” Schumer said. “It replaces a broken patchwork of watchdogs, none of which were built for this moment, with one, powerful anti-corruption agency, ready to act anywhere, anytime corruption strikes.”

White House pushes back on conflict claims tied to investment accounts

The anti-corruption push arrives amid persistent Democratic criticism of Trump’s involvement in the crypto industry while in office. Schumer’s office noted concerns that have also hovered over the Senate’s broader crypto policy effort, the Digital Asset Market Clarity (CLARITY) Act.

While the White House agreed to certain ethics provisions in CLARITY, many lawmakers have argued those changes do not adequately address potential conflicts of interest.

In a statement to Cointelegraph, White House Principal Deputy Press Secretary Anna Kelly reiterated the administration’s position that there were “no conflicts of interest” related to Trump’s investments. Kelly said the investments were “held in fully discretionary accounts managed by independent third-party financial institutions.”

Consolidating ethics and enforcement under one “roof”

A notable feature of Schumer’s bill is its plan to reorganize parts of the federal oversight landscape. The proposal would place the US Federal Election Commission, the Office of Government Ethics, and the Office of Special Counsel “under one roof” within the new bureau.

The intent, as described in Schumer’s remarks, is to reduce the friction between agencies and streamline action when corruption is alleged—an argument he made by contrasting the proposed bureau with what he characterized as outdated or mismatched oversight structures.

Schumer introduced the bill with cosponsors Andy Kim, Alex Padilla, and Jeff Merkley.

What’s happening with the Senate’s CLARITY Act remains uncertain

Schumer’s anti-corruption initiative is moving alongside a separate, more technical fight in the Senate: whether and when the CLARITY Act will advance.

The article notes that the Senate has just over a week before lawmakers break for a month-long state work period. That calendar pressure is heightening uncertainty for pending legislation, including CLARITY, especially as lawmakers face the prospect of competing priorities ahead of the 2026 midterms.

As of Thursday, the Senate had not scheduled a vote on the CLARITY Act, despite encouragement from some Republican lawmakers and industry figures. Former Securities and Exchange Commission official John Reed Stark said the situation is difficult to predict, describing “enormous drama” surrounding the bill and stating that experts he spoke with could not confidently forecast what would happen that week.

Industry leaders have also signaled confidence while acknowledging timing risks. Coinbase CEO Brian Armstrong said the bill was at the “one-yard line,” while Senator Cynthia Lummis continued pushing for a vote, according to posts cited in the report.

Legislative math: momentum doesn’t eliminate veto risk

Even if Schumer’s anti-corruption bureau legislation gains traction, it still faces major hurdles. The bill would require Republican support in both chambers to pass, with the party holding only a slim majority in the Senate. If it clears the Senate and House before 2028, President Trump could still veto the legislation.

Overriding a presidential veto would require a two-thirds majority in both the House and Senate, leaving the outcome dependent on whether Democrats can sustain enough cross-party backing.

For crypto watchers, the near-term focus is likely to split: whether the Senate can find a path forward on the CLARITY Act before its schedule runs out, and whether Schumer’s anti-corruption bureau proposal gains enough bipartisan traction to survive both legislative and veto thresholds—especially given the ongoing dispute over how (or whether) current ethics arrangements address potential conflicts tied to crypto.

Samsung SDS has identified stablecoin infrastructure as the first major collaboration area under its investment in Dunamu, outlining plans to combine blockchain, AI and cloud technologies as part of its digital asset strategy.

Summary

- Samsung SDS said its investment in Dunamu is part of a strategy to build digital asset infrastructure rather than a financial investment.

- The company is discussing stablecoin infrastructure, AI powered payments and virtual asset financial systems with Dunamu.

- Samsung SDS reported 17% cloud revenue growth and a 75% jump in external cloud business during the second quarter.

- The company plans to expand its AI infrastructure from 110 MW today to more than 800 MW by 2031.

According to Samsung SDS during its second-quarter earnings conference call on Wednesday, the company has been discussing stablecoin infrastructure, AI-powered next-generation payments and virtual asset financial system integration with Dunamu, the operator of South Korea’s largest cryptocurrency exchange Upbit.

Samsung SDS has outlined how its Dunamu investment will be used

Samsung SDS President Lee Joon-hee said the company’s stake in Dunamu was made to enter the digital asset infrastructure business rather than as a financial investment. He said Samsung SDS intends to combine Dunamu’s blockchain operating experience with its own IT services, artificial intelligence, cloud computing and cybersecurity capabilities to strengthen digital financial infrastructure.

Lee added that the companies are considering business opportunities spanning stablecoin infrastructure, AI-based payment systems and system integration services built around virtual assets. According to Samsung SDS, discussions are continuing as both sides work toward developing concrete business models.

The comments provide the clearest description yet of Samsung SDS’s plans after it invested in Dunamu earlier this year.

In May, Samsung Securities, Samsung SDS and Samsung Card agreed to acquire a combined 4% stake in Dunamu for 612.8 billion won, or about $408 million, by purchasing 1.39 million shares from Kakao-linked entities. Samsung SDS acquired a 1% stake, while Samsung Securities purchased 2% and Samsung Card acquired the remaining 1%.

At the time, Samsung SDS said it planned to combine its AI, cloud, security and data management services with Dunamu’s blockchain expertise, while Dunamu said it expected cooperation on blockchain investment products, payment infrastructure and AI-related blockchain applications.

Stablecoin plans extend Samsung’s digital asset push

The latest comments come less than a week after Samsung Electronics disclosed plans to bring stablecoin support to Samsung Wallet.

During the Galaxy Unpacked event on July 24, Samsung Electronics said the wallet application will support stablecoins alongside payments, rewards and digital assets, although it did not disclose launch dates, supported tokens, blockchain networks or regional availability.

Product manager Lee Dinham said at the event that Samsung Wallet would expand beyond conventional payment functions to include stablecoins, allowing users to transfer digital value directly from compatible Galaxy devices.

Together, the wallet announcement and Samsung SDS’s latest remarks indicate that Samsung’s digital asset initiatives now extend from consumer payment products to the infrastructure supporting blockchain-based financial services.

The direction also differs from Samsung’s response to Open Standard’s proposed OUSD stablecoin consortium earlier this month. According to South Korean newspaper Chosun, Samsung said it had not held formal consultations with Open Standard and did not know what role it was expected to play after being listed as a founding consortium member. Dunamu, Shinhan Bank and K-Bank also told the newspaper they were still reviewing the proposal and had not approved participation.

Cloud growth has supported Samsung SDS results

Samsung SDS disclosed alongside the conference call that second-quarter revenue increased 5.9% year over year to 3.7178 trillion won, while operating profit rose 0.7% to 231.8 billion won. Net profit climbed 4.6% to 184.1 billion won.

IT services revenue reached 1.7625 trillion won, up 5% from a year earlier.

Cloud operations remained the fastest-growing segment. Revenue from the cloud business increased 17% to 779.4 billion won, while external cloud business revenue jumped 75% year over year.

According to Samsung SDS, cloud service provider revenue grew 24% as demand for Samsung Cloud Platform increased and GPU-as-a-Service deployments expanded across public-sector and enterprise customers. Cloud management services revenue also rose 17%, supported by AI transformation projects in the financial sector and enterprise resource planning deployments within South Korea’s shipbuilding industry.

AI infrastructure expansion will also support blockchain services

Alongside its blockchain plans, Samsung SDS said it continues expanding AI infrastructure and enterprise AI offerings.

The company said it was recently selected as a core operator under South Korea’s government-backed GPU infrastructure program and launched an NPU-as-a-Service product based on FuriosaAI’s Renegade neural processing chip. It has also secured AI-related projects with Woori Bank and the Export-Import Bank of Korea while maintaining partnerships with OpenAI, Anthropic and Google Cloud for generative AI services.

Samsung SDS currently operates about 110 megawatts of AI infrastructure and plans to expand capacity to 230 megawatts by 2029. According to the company, that figure is expected to exceed 800 megawatts by 2031 when design, construction and operational projects are included.

The infrastructure buildout accompanies Samsung SDS’s strategy of pairing its cloud and AI capabilities with Dunamu’s blockchain platform as the companies continue discussions around stablecoin infrastructure, digital asset payment systems and virtual asset financial technology services.

The Bank of Korea has successfully completed live cross-border payment tests using tokenized central bank reserves under the Bank for International Settlements-led Project Agora, processing transactions across six currencies and multiple payment scenarios.

Summary

- Bank of Korea completed live Project Agora payment tests using tokenized reserve funds across six currencies.

- South Korean banks tested cross border settlements including a 20 million won transfer using tokenized reserves.

- The trial linked Project Hangang with the BIS platform to validate real world payment workflows.

- The central bank plans additional Project Agora tests covering more payment scenarios and transaction types.

According to the Bank of Korea, the central bank participated in the latest round of Project Agora real transaction testing alongside 27 other central banks and private financial institutions, confirming that the platform’s core functions and operating processes worked reliably in an environment designed to mirror real-world payment operations.

The exercise covered the Korean won, U.S. dollar, euro, British pound, Swiss franc and Japanese yen. South Korea’s participating commercial banks included KB Kookmin Bank, NongHyup Bank, Shinhan Bank, Woori Bank and Hana Bank.

Participating institutions processed transactions worth about 800,000 Swiss francs across 17 payment scenarios.

The Bank of Korea said the tests successfully handled several cross-border payment use cases, including single- and dual-currency settlements between companies and banks, payment-versus-payment foreign exchange settlements and fund transfers within the same financial group.

Project Agora has linked tokenized reserves with cross-border payments

For its domestic test, the Bank of Korea worked with NongHyup Bank and Shinhan Bank to transfer 20 million won between the two lenders using tokenized reserve funds. According to the central bank, it received payment instructions from both banks before issuing, transferring, and redeeming tokenized reserves on the Project Agora platform.

The process also included a manual connection between Project Hangang, the Bank of Korea’s wholesale central bank digital currency platform, and the central bank’s existing financial network to validate interoperability during the transaction.

Separately, KB Kookmin Bank became the first South Korean commercial bank to complete a deposit token payment test with an overseas lender after conducting a yen-based settlement trial with Japan’s MUFG Bank. The bank said the results would support its participation in future phases of Project Agora.

The Bank of Korea said additional live transaction tests would follow as the project expands to cover payment types and operational scenarios that were not included in the latest exercise.

Project Hangang has supported South Korea’s digital payment plans

The latest cross-border testing builds on South Korea’s efforts to extend Project Hangang beyond institutional pilots and into commercial payment infrastructure.

As previously reported, the Ministry of Science and ICT and the Korea Internet & Security Agency launched a 9.6 billion won program earlier this month to connect Project Hangang with the country’s existing payment network. The initiative is led by the Korea Financial Telecommunications and Clearings Institute and includes nine commercial banks, payment gateway providers and large merchants testing deposit token payments for everyday retail transactions.

Instead of replacing existing payment terminals, the project allows banks to issue deposit token wallets while merchants continue using current point-of-sale systems. Government agencies also plan to test deposit tokens for public-sector payments before integrating the technology with South Korea’s digital public finance platform.

The Bank of Korea has consistently distinguished deposit tokens from stablecoins. Deposit tokens represent commercial bank deposits issued through a wholesale CBDC framework operated by the central bank, while stablecoins are separate digital assets backed by reserve assets under their own regulatory model.

Bank of Korea has continued to prioritize CBDCs alongside Project Agora

The successful testing also follows Governor Shin Hyun-song’s digital finance agenda announced after he took office in April.

In his inaugural speech, Shin said the Bank of Korea would continue expanding Project Hangang while participating in international initiatives such as Project Agora to strengthen cross-border payment infrastructure and support the Korean won in digital finance.

Although lawmakers have continued drafting stablecoin legislation under the proposed Digital Asset Basic Act, Shin’s speech focused on wholesale CBDCs and tokenized bank deposits rather than privately issued stablecoins.

His earlier work at the Bank for International Settlements argued that multiple privately issued stablecoins could fragment payment systems, though later reports indicated he had become more open to stablecoins operating alongside CBDCs under an appropriate framework.

South Korea has advanced stablecoin legislation separately

While the central bank continues testing tokenized reserves and deposit tokens, lawmakers and financial regulators have been developing a separate legal framework for stablecoins.

The Financial Services Commission recently told the National Assembly that it intends to consolidate ten pending digital asset proposals into a single Digital Asset Basic Act covering stablecoin issuance, exchanges, disclosures, governance and operational resilience. The regulator has not published a final draft or announced a submission date.

Separately, a policy report published by Hashed Open Research and the Solana Policy Institute recommended introducing interim licensing guidance for won-backed stablecoins before the full legislation is completed. Participants at the June symposium cited in the report argued that temporary rules could help regulated businesses prepare for stablecoin issuance and payment services while lawmakers continue negotiating the final framework.

The Bank of Korea has maintained that banks should play a leading role in any future stablecoin model because of monetary policy, foreign exchange and financial stability considerations. Ownership rules for stablecoin issuers, however, remain under discussion, with lawmakers and regulators continuing consultations before the proposed legislation moves forward.

Bitget Wallet will launch Assetback on Aug. 1, allowing eligible card users to convert purchase rewards automatically into Bitcoin, tokenized gold, U.S. equity tokens, an exchange-traded fund token or USDC.

Summary

- Seven reward assets include Bitcoin, tokenized gold, three U.S. stocks, an ETF, and USDC options.

- Eligible cardholders receive 2% base rewards, while qualifying users can unlock 3% during booster periods.

- Rewards become redeemable seven days after transactions and require at least one USDC before withdrawal.

The company said users can select one of seven assets: BTC, Tether Gold, tokenized Nvidia, Tesla and Alphabet shares, an S&P 500 product, or USDC. Rewards will be generated from qualifying purchases made with the Bitget Wallet Card.

Bitget Wallet replaces cash rewards with seven assets

Assetback provides a 2% base reward for cardholders. New users and customers who meet a monthly spending threshold can receive up to 3% through a booster tier. Once unlocked, the higher rate applies during that calendar month and the next one.

Users may change their selected reward asset once each month. USDC rewards are credited to the card balance, while other rewards can be moved to a rewards account after reaching at least one USDC in accumulated value. Redemption becomes available seven days after the underlying transaction.

However, the advertised rate does not apply to every payment. Bitget Wallet says monthly caps, merchant-category exclusions and risk reviews apply. Refunded, reversed or cancelled transactions do not qualify. The model also replaces the card’s previous zero-fee rewards program, so users should review regional fees and limits.

Tokenized stocks provide exposure, not standard shares

The stock and ETF rewards will use xStocks, which issues blockchain tokens backed by securities held in custody. Available choices include Nvidia, Tesla, Alphabet and an S&P 500-linked product. xStocks says each token is backed one-for-one by underlying securities.

However, tokenized equities are not identical to holding shares through a conventional brokerage account. Rights, redemption access, trading availability and investor protections depend on the issuer, platform and user’s location. Bitget Wallet also describes the rewards as available only to eligible users.

As previously reported, Bitget Wallet added more than 130 xStocks products in May, allowing users to access tokenized equities through its self-custodial application. In related coverage, crypto.news explained how tokenized stocks work, including issuer, custody, liquidity and regulatory risks.

Card access still depends on each user’s region

Bitget Wallet says the card serves markets across Europe, Asia and Latin America, with availability also expanding in Africa. Its official card page states that cards may operate through Visa or Mastercard depending on the regional issuing partner. The product supports Apple Pay and Google Pay in eligible markets.

The card converts selected crypto assets to fiat when users pay merchants. Official terms state that customers must complete identity checks and live in supported jurisdictions. The terms also permit applicable conversion, foreign-exchange and other charges, meaning Assetback should not be treated as a guaranteed net return.

Bitget Wallet says it has more than 100 million users and that spending through its card nearly tripled during the first half of 2026. It also cited monthly crypto-card payment volume of $656 million in May, up from $271 million one year earlier. Those figures are company-provided and have not been independently audited.

The Aug. 1 rollout will test actual demand

Users will need Bitget Wallet app version 9.5.3 or later to access the updated card. After selecting an asset, eligible cashback will be converted automatically, creating small recurring purchases rather than requiring a separate trade after every card payment.Bitget Wallet describes the process as applying “dollar-cost averaging” to routine spending. That is a company characterization, not a promise that the selected assets will gain value. Bitcoin, tokenized gold and equity-linked products can rise or fall after rewards are credited.

There is no verified market reaction because Bitget Wallet is not publicly traded and the announcement does not introduce a new token. The next measurable updates will be redemption activity, reward volumes and whether regional cardholders adopt non-cash rewards after Aug. 1.

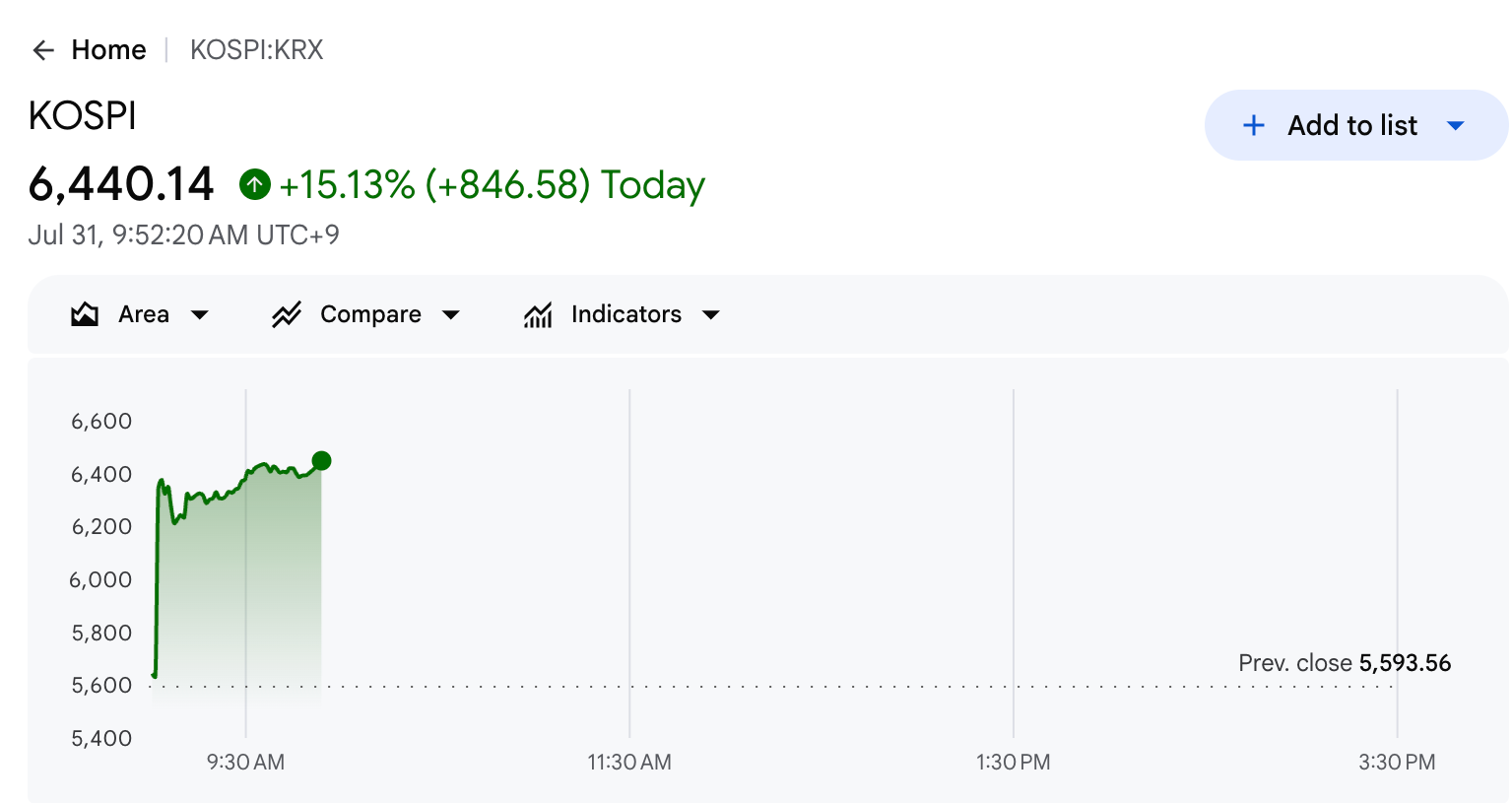

South Korea’s KOSPI index surged by double digits on Friday morning. The rebound follows back-to-back circuit breakers on Tuesday and Wednesday, as well as sharp monthly losses.

Stronger-than-expected cloud results from Microsoft and Amazon revived confidence in AI spending, sparking a chip rally across Seoul and Tokyo.

KOSPI Rebound Triggers Buy-Side Sidecar in Seoul

According to Google Finance, KOSPI stood at 6,440.14, up 15.13% at press time. The index gained 846.58 points from Thursday’s close of 5,593.56 by 10:30 a.m. local time.

Follow us on X to get the latest news as it happens

A buy-side sidecar was triggered at 9:06 a.m., suspending program trading for five minutes. The KOSDAQ saw a similar curb after touching an intraday high of 693.81. At press time, it was up by 8.91%.

The rally was carried by index heavyweights. SK Hynix jumped 27.69% to 1,688,000 won, while Samsung Electronics climbed 21.74% to 252,000 won.

The bounce comes after days of turmoil. Circuit breakers halted both markets on July 28 and 29, forcing an emergency government meeting after 864.5 trillion won evaporated in two sessions.

Before this session, July ranked as the market’s worst crash ever, with the KOSPI down over 33% for the month.

US Cloud Earnings Reignite the AI Trade

The catalyst came from Wall Street overnight. Microsoft rallied 16% Thursday after Azure growth beat forecasts, and Amazon jumped over 9% in extended trading on stronger-than-expected second-quarter revenue.

The Nasdaq climbed 2.78%, and the S&P 500 added 1.66%. Meanwhile, the Philadelphia semiconductor index soared 8.2%, and the iShares Semiconductor ETF (SOXX) gained more than 8%.

The rally spilled into Tokyo. Advantest surged 17.92%, and Tokyo Electron climbed 9.67%. SoftBank Group rose 15.12%. Japan’s Nikkei 225 added 5.35%, and the broader Topix gained 2.32%.

Whether the rebound holds is the next test. Even after Friday’s surge, the KOSPI trades roughly 31% below its June record of 9,385.59.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post KOSPI Snaps Back 15% as Asia’s AI Chip Rally Returns appeared first on BeInCrypto.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

The latest Duel.com referral code, DUEL5, offers new users access to instant rakeback rewards and enhanced RTP benefits on eligible Duel Originals.

Summary

- Duel.com updated its DUEL5 referral code, offering new users 50% instant rakeback and access to 100% RTP Duel Originals.

- New Duel.com users can unlock 50% instant rakeback and permanent 100% RTP Duel Originals with the DUEL5 referral code.

- DUEL5 referral code gives Duel.com players permanent rakeback and Duel Originals rewards.

Looking for the latest Duel.com referral code? The current working code is DUEL5. New players who enter DUEL5 during registration unlock 50% instant rakeback on eligible casino games and gain permanent access to 100% RTP Duel Originals, making it one of the most valuable long-term offers available on the platform.

Unlike traditional welcome bonuses that expire after a wagering requirement is met, the DUEL5 referral code improves your account permanently. Every eligible wager earns instant rakeback, while Duel’s in-house Originals are designed to operate at a full 100% return to player (RTP), meaning there is no built-in house edge within the stated limits of those games.

Launched in July 2025 by Nevis-registered Immortal Snail LLC, Duel.com is the crypto casino created by Ossi “Monarch” Ketola, founder of the well-known CS skin betting platform CSGOEmpire. Today, Duel offers more than 5,000 casino games, live dealers, Duel Originals, and a full cryptocurrency sportsbook.

What is the Duel.com referral code?

The current Duel.com referral code is: DUEL5

Entering DUEL5 during registration permanently activates:

- 50% instant rakeback on eligible casino wagers.

- Access to Duel Originals with 100% RTP.

- Leaderboard eligibility with daily and monthly prize pools.

- Rewards that continue for as long as the account remains active.

Because referral codes cannot be added after an account is created, new users should enter DUEL5 during the sign-up process.

How to sign up on Duel.com with referral code DUEL5

- Go to the official Duel.com website.

The first and most important step to the genuine platform. New players can either use the trusted link or type Duel.com directly into their browser. Stay vigilant against phishing scams — plenty of fake sites try to pass themselves off as the real Duel online casino. - Click the Register button.

This can be found in the top-right corner of the website. Once it is clicked, a pop-up window will open containing the registration form.

- Create a username and password.

Both fields are required. The username is public, showing up in Castle Roulette chat and on leaderboards, so pick something you are happy being seen under. Use a password unique to this account, and turn on two-factor authentication in settings before making a deposit. A crypto balance has no bank behind it to reverse an unauthorized withdrawal.

Track live Castle Roulette results

For those who regularly play Castle Roulette, it’s worth keeping an eye on recent results using the DuelRewards.io Castle Roulette Tracker. Available at Duel Castle Roulette website, the tracker records every completed spin in real time, making it easy to review recent history without manually logging outcomes.

The tracker displays live Castle Roulette results, recent multiplier history, streaks, droughts, and historical statistics, giving players a clear overview of how the game has unfolded over time. Whether you’re checking which multipliers have appeared recently or reviewing previous sessions, everything is available in one place.

Because Castle Roulette is a provably fair game, each spin is generated independently of the last. This means no tracker can predict future results or increase your chances of winning. Instead, the DuelRewards.io tracker is designed as an informational tool, allowing players to monitor live data, analyze historical results, and follow the game’s activity as it happens.

For those who are already using the DUEL5 referral code to unlock 50% instant rakeback and 100% RTP Duel Originals, pairing it with the DuelRewards.ioCastle Roulette Tracker gives them a convenient way to stay up to date with every Castle Roulette spin while they play.

- Decide whether to add an email.

Email is optional here, part of Duel’s no-KYC approach. Tick the Email box to reveal the field. Adding one gives you an account recovery path. Skipping it keeps things more private, but recovery becomes much harder if you lose access.

- Tick the Referral code box and enter DUEL5.

This is the step that decides whether you get the offer. Ticking the checkbox below the email option reveals an input field. Type DUEL5 in manually, and read it back before you move on. Duel will not add a code after registration, so missing this field permanently forfeits the rakeback and 100% RTP on that account.

- Accept the Terms & Conditions and click Create Account.

Worth an actual read rather than a reflex tick, particularly the restricted-jurisdiction list and the withdrawal terms.

- Deposit and start playing.

Duel is crypto-only, accepting BTC, ETH, USDT, SOL, LTC, and more than 10 other assets, with deposits usually confirming within minutes. Rakeback accrues from your first wager and credits as bets settle, and the Duel Originals section is where the 100% RTP applies.

What does DUEL5 unlock?

Most crypto casinos focus on offering large one-time deposit bonuses that often come with high wagering requirements. Duel takes a different approach by rewarding every qualifying wager instead.

50% instant rakeback

With DUEL5, half of the house edge is returned instantly on eligible games including many slots, live dealer tables, and game shows.

Unlike a traditional casino bonus:

- There are no wagering requirements.

- Rewards are credited automatically.

- Rakeback is available immediately after eligible wagers settle.

- There is no expiry on the benefit.

For players who wager regularly, ongoing rakeback can provide significantly more long-term value than a one-time welcome bonus.

100% RTP Duel originals

One of Duel’s biggest selling points is its collection of Duel Originals.

Games including Crash, Dice, Mines, Plinko, Blackjack, and Castle Roulette are designed to operate at 100% RTP, meaning there is no built-in house edge within the game’s published mechanics.

Castle Roulette has become one of the platform’s signature games, featuring multipliers from 2x up to 48x alongside provably fair verification, allowing players to independently verify every completed round.

Duel.com referral codes for 2026

| Code | Benefit | Wagering | Expiry |

| DUEL5 | 50% instant rakeback + 100% RTP on Duel Originals | None | Permanent |

Rather than rewarding only your first deposit, DUEL5 continues providing value every time you play.

Is the Duel.com referral code worth using?

For players planning to use Duel regularly, DUEL5 is one of the platform’s strongest available sign-up offers because it provides permanent benefits instead of temporary promotional credits.

Instead of relying on a single welcome bonus, the referral code continually reduces the effective cost of eligible wagering through instant rakeback while also unlocking Duel Originals that operate at 100% RTP.

Important things to know

While the referral code improves the value of your account, gambling always involves risk. A game with 100% RTP does not guarantee profit, and short-term results remain unpredictable.

Duel currently accepts cryptocurrency only, with support for assets including BTC, ETH, SOL, USDT, and others.

The platform is licensed by the Anjouan Gaming Authority. Availability varies by jurisdiction, and users should ensure Duel is legal where they live before registering. Duel’s terms also state that attempting to access restricted regions through a VPN may result in account action.

Bottom line

If you’re searching for the latest Duel.com referral code, DUEL5 is the current working code for new players.

By entering DUEL5 during registration, you permanently activate 50% instant rakeback, gain access to 100% RTP Duel Originals, and qualify for Duel’s leaderboard rewards. Unlike most casino promotions, these benefits aren’t tied to a one-time deposit or lengthy wagering requirement, making DUEL5 one of the most valuable long-term offers currently available on Duel.com.

FAQ

What is the Duel.com referral code?

The current working Duel.com referral code is DUEL5. New players can enter it during registration to unlock 50% instant rakeback and permanent access to 100% RTP Duel Originals.

What does the DUEL5 referral code give you?

DUEL5 permanently enables 50% instant rakeback on eligible casino wagers, access to Duel Originals with 100% RTP, and qualification for Duel leaderboard promotions.

Can I add the Duel referral code after signing up?

No. The referral code must be entered when creating your account and cannot normally be added later.

Does 100% RTP mean I cannot lose?

No. A game operating at 100% RTP removes the theoretical house edge over the long run but does not eliminate short-term variance, so individual sessions can still result in losses.

Does Duel.com accept fiat currency?

No. Duel currently operates as a cryptocurrency-only platform and supports several major digital assets for deposits and withdrawals.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

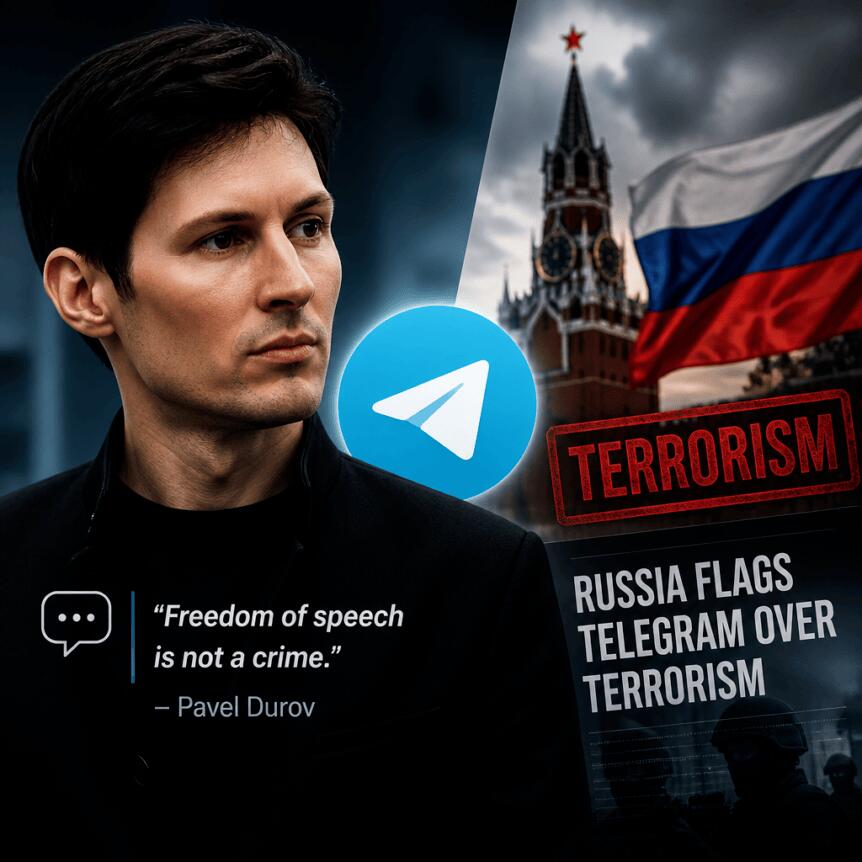

Telegram founder Pavel Durov has responded to Russia’s latest legal actions by accusing authorities of trying to impose mass surveillance and censorship on the messaging platform, while also claiming the state has moved to restrict his ability to publish online.

Speaking in a Telegram post on Thursday—one day after Russia announced new charges—Durov said Russian authorities labeled him a “terrorist” following his refusal to comply with government demands related to monitoring and restricting content on Telegram.

Key takeaways

- Durov says Russia designated him a “terrorist” after he resisted demands tied to mass surveillance and censorship of Telegram.

- He also claims Russian authorities barred him from publishing information on the internet.

- Russia’s Federal Security Service alleges Telegram failed to remove channels linked to terrorist groups and Ukrainian intelligence services.

- The Russian case follows a separate, ongoing investigation in France tied to accusations that Telegram inadequately moderates illegal content and does not sufficiently respond to law enforcement requests.

- Additional legal pressure is reportedly building in Australia through court proceedings over alleged failures to remove terrorism-related content.

Russia escalates allegations against Durov

According to the timeline reported earlier by Cointelegraph, the comments came a day after Russia’s Federal Security Service (FSB) accused Durov of facilitating terrorist activity. The FSB’s allegation centers on a claim that Telegram did not remove channels used by terrorist organizations and by what Russia described as Ukrainian intelligence services.

Durov’s response on Telegram frames the situation as part of a broader conflict over how governments seek control of online communication. He told Telegram users that Russia had also blocked him from “publishing information on the Internet,” and added that authorities appeared to be “confused about who can ban whom from the Internet.”

How the Russian investigation started

The current escalation builds on a criminal investigation Russia launched in February, as previously detailed by Cointelegraph. At the time, regulators accused Telegram of leaving nearly 155,000 channels, chats, and bots online despite Telegram’s position that such content did not violate relevant Russian law.

The investigation was tied to a wide range of alleged violations, including rules covering extremist material, terrorism, drug trafficking, and other illicit activity categories—suggesting that Russian authorities are treating Telegram’s moderation and compliance as a central issue rather than targeting isolated incidents.

Broader legal challenges in Europe and beyond

While Russia’s charges are the latest development, Durov’s legal problems extend beyond the country. Cointelegraph previously reported that Durov was arrested in France in August 2024 and remains under judicial investigation over allegations that Telegram facilitated criminal activity by failing to adequately moderate illegal content and respond to law enforcement requests.

Durov has denied wrongdoing, saying French authorities did not follow due process in efforts to obtain information from Telegram. His arrest also sparked an organized public push from the TON community, which—according to Cointelegraph—raised more than 9 million signatures on an open letter urging French authorities to release him.

The case has also involved changes to how restrictions on his movement were handled. Cointelegraph reported that French authorities allowed Durov to return temporarily to Dubai in March 2025, before lifting travel restrictions entirely later in 2025.

New pressure reported in Australia

Alongside Europe and Russia, Telegram is facing further legal scrutiny in Australia. Cointelegraph reported that Australian regulators this week launched court proceedings alleging Telegram failed to remove terrorism-related content.

For Telegram and Durov, these separate legal tracks underscore a recurring theme in cross-border platform enforcement: different jurisdictions are asking the same underlying question—how much responsibility a messaging provider should bear for removing content and supporting law enforcement access.

Durov’s privacy-and-surveillance messaging

Durov has portrayed himself as a defender of free speech and digital privacy, using recent statements to argue that compliance efforts can drift into broader surveillance. Cointelegraph noted that in April he warned the European Union’s proposed age-verification app could open the door to wider online monitoring.

That same month, Cointelegraph also reported that Durov linked alleged tax data leaks to a wave of crypto-related kidnappings in France, and said Telegram would leave the country rather than grant authorities access to users’ private messages.

In the current dispute with Russia, his public framing follows the same pattern: he positions government demands as attempts to expand control over messaging infrastructure rather than as targeted enforcement of specific legal obligations.

As Russia’s case develops and other jurisdictions—such as France and Australia—pursue their own enforcement actions, investors and builders in crypto-adjacent ecosystems may want to watch for any tangible changes in platform moderation, legal compliance requirements, and cross-border cooperation that could affect how TON and Telegram-related services operate in practice.

The Hong Kong Securities and Futures Commission has issued a restriction notice freezing assets worth up to HK$125.247 million in a client account at Futu Securities International Limited as part of an ongoing investigation into suspected IPO share manipulation.

Summary

- Hong Kong’s SFC has frozen HK$125.2 million linked to a suspected IPO share manipulation scheme.

- The restriction applies to a client account at Futu, while the brokerage itself is not under investigation.

- Futu must obtain the SFC’s approval before handling the restricted assets and report any related instructions.

- The investigation remains ongoing as the regulator seeks to protect investors and the public interest.

According to the Hong Kong Securities and Futures Commission (SFC), the restriction applies to assets held by a certain entity suspected of participating in a fraudulent scheme designed to create a false or misleading appearance of demand for shares in an initial public offering.

The regulator said Futu is not the subject of its investigation and stressed that the restriction notice will not affect the brokerage or any of its other clients. The action targets a specific customer account and prevents the assets from being moved while the investigation continues.

SFC has restricted access to the assets

Under the notice, Futu must not dispose of, transfer, process, or otherwise deal with the assets held in the affected customer account without first obtaining written consent from the SFC. The restriction covers assets up to HK$125,247,000.

The regulator also instructed the brokerage to immediately notify it if it receives any instructions relating to the restricted assets. In addition, Futu must not assist, encourage, or cause another party to deal with those assets unless the regulator has given prior written approval.

Explaining the decision, the SFC said issuing the restriction notice is desirable in the interests of investors and the public. The investigation into the suspected scheme remains ongoing.

According to the regulator, the restriction notice was issued under Sections 204 and 205 of Hong Kong’s Securities and Futures Ordinance.

Futu has not been accused of wrongdoing

While the restriction notice involves an account maintained at Futu Securities International (Hong Kong) Limited, the SFC made it clear that the brokerage itself is not under investigation.

The regulator also stated that the order will not affect the firm’s day-to-day business or the accounts of its remaining customers.

Futu is licensed under Hong Kong’s Securities and Futures Ordinance to conduct multiple regulated activities, including securities dealing, futures contracts dealing, leveraged foreign exchange trading, advising on securities, advising on futures contracts, providing automated trading services, and asset management.

The latest regulatory action therefore relates only to the suspected conduct of a single client entity rather than the firm’s licensed operations.

Although the regulator disclosed the value of the restricted assets and the suspected nature of the scheme, it did not identify the customer entity involved or provide further details about the alleged conduct.

No enforcement action has been announced against Futu, and the SFC has not indicated when its investigation may conclude.

For now, the restriction notice remains in effect, preventing the affected assets from being handled without regulatory approval while investigators continue examining the suspected attempt to create artificial demand for IPO shares.

Futu has expanded its crypto services in Hong Kong

The restriction notice comes after Futu expanded its digital asset business under Hong Kong’s regulated virtual asset framework.

In June 2026, the brokerage received approval from the SFC to expand its Type 1 licensed activities, allowing eligible clients to use securities-backed financing for virtual asset trading. The approval made Futu the first brokerage in Hong Kong to provide financing for cryptocurrency transactions backed by traditional securities.

Under that arrangement, qualified investors became able to use securities held in conventional margin accounts as collateral to obtain financing for crypto trades, removing an earlier limitation that prevented such credit facilities from being used for digital asset transactions.

The approval followed another crypto-related rollout completed in May 2025, when Futu launched deposit services for Bitcoin, Ethereum, and Tether. Eligible investors were allowed to deposit those digital assets through the firm’s trading platform and trade them alongside Hong Kong, U.S., and Japanese stocks, exchange-traded funds, options, bonds, and other investment products from a single account.

At the time, Futu said the service allowed users to move more easily between virtual assets and traditional financial products through the same trading interface. The brokerage had already introduced cryptocurrency trading in 2024 after securing regulatory approval to offer virtual asset services to retail and professional investors.

Hong Kong authorities have continued expanding the city’s regulatory framework for digital assets through new licensing proposals covering virtual asset advisory and portfolio management services, alongside the existing oversight of trading platforms, custody providers, and stablecoin issuers.

OpenAI cut prices on two GPT-5.6 models on July 30, slashing Luna by 80% and Terra by 20%, as businesses grow more cautious about ballooning AI bills.

The cuts land three weeks after GPT-5.6’s launch. They reflect mounting pressure from cost-conscious enterprises. Cheaper Chinese rivals, including Moonshot AI’s Kimi K3 and Z.ai’s GLM-5.2, add to that pressure.

A Pricing Squeeze With High Stakes

Luna’s input price fell to 20 cents per million tokens from $1. Its output price dropped to $1.20 from $6. Terra’s rates fell to $2 and $12 per million tokens, down from $2.50 and $15. Sol, OpenAI’s flagship model, kept its price.

The discounts follow years of unrestrained corporate AI spending. Workers called the trend tokenmaxxing, using AI freely without tracking cost. Finance teams now want clearer returns before approving new AI budgets.

Cutting Costs to Make Money?

OpenAI framed the move as an efficiency gain, not a defensive one. Open AI explained:

“Our strategy remains focused on advancing both capability and efficiency so each generation of intelligence can accomplish more work at a lower cost.”

The timing still matters. Chinese AI models gained ground on Anthropic and OpenAI this year. They undercut both labs on cost. Anthropic’s mid-tier Claude Sonnet 4.6 still costs more per token than the discounted Terra.

Analysts say cheaper pricing could lift usage of OpenAI’s and Anthropic’s models. It could also thin the margins investors watch as both companies pursue anticipated initial public offerings. Winning cost-sensitive customers and proving profitability to future shareholders pull in opposite directions.

IPO Pressure Mounting

Cutting prices could cut both ways for OpenAI’s IPO ambitions. Wider adoption strengthens the growth story bankers will pitch to investors. Usage and revenue growth tend to matter more than near-term margins in a pre-IPO narrative, and locking in cost-sensitive enterprise customers now, before they defect to cheaper Chinese rivals, protects the market share on which any IPO valuation depends.

It also lets the company point to efficiency gains (lower cost per task) as evidence that their technology is maturing rather than just getting more expensive to run.

However, IPO investors will eventually want to see a credible path to profitability, and shrinking per-token revenue on already thin-margin inference businesses makes that path harder to show on a prospectus.

If Terra’s and Luna’s usage doesn’t grow enough to offset the lower prices, the cuts show up as reduced revenue rather than reduced cost, exactly the kind of number that gets picked apart in IPO due diligence.

Whether the discounts ease that tension or simply delay it stays unclear for now. OpenAI’s next earnings update, once usage data from Terra and Luna appears, should offer an early answer.

The post Amid Rising AI Costs and IPOs, OpenAI Slashes Prices for Customers appeared first on BeInCrypto.

Stassi Schroeder Rethinks SI Return After Brutal Online Comments

Ferragamo’s Fall 2026 Campaign Focuses on Footwear

The Biggest Losers I’ve Ever Had On Financial Audit

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Brooks Brothers

-

Sports4 days ago

Sports4 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business1 day ago

Business1 day agoWhy Trees Belong on the Risk Register

-

Tech4 days ago

Tech4 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World5 days ago

Crypto World5 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics4 days ago

Politics4 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Entertainment7 days ago

Entertainment7 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

Politics3 days ago

Politics3 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos4 days ago

News Videos4 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Sports7 days ago

Sports7 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Fashion7 days ago

Fashion7 days ago16 Dresses for the High Summer Event

-

Business2 days ago

Business2 days agoMajor shareholder moves on Canyon

-

Crypto World5 days ago

Crypto World5 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Politics5 days ago

Politics5 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

News Videos15 hours ago

News Videos15 hours agoBitcoin Enters the 3rd Stage of the Bear Market

-

Entertainment2 days ago

Entertainment2 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Entertainment5 days ago

Entertainment5 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

Tech6 days ago

Tech6 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

Crypto World2 days ago

Crypto World2 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

News Videos2 days ago

News Videos2 days agoClaude: Build Financial Dashboards in Minutes (2026)

You must be logged in to post a comment Login