Crypto World

Strategy calls its new bitcoin funding tool an ‘iPhone’ moment but analysts warn of hidden risks

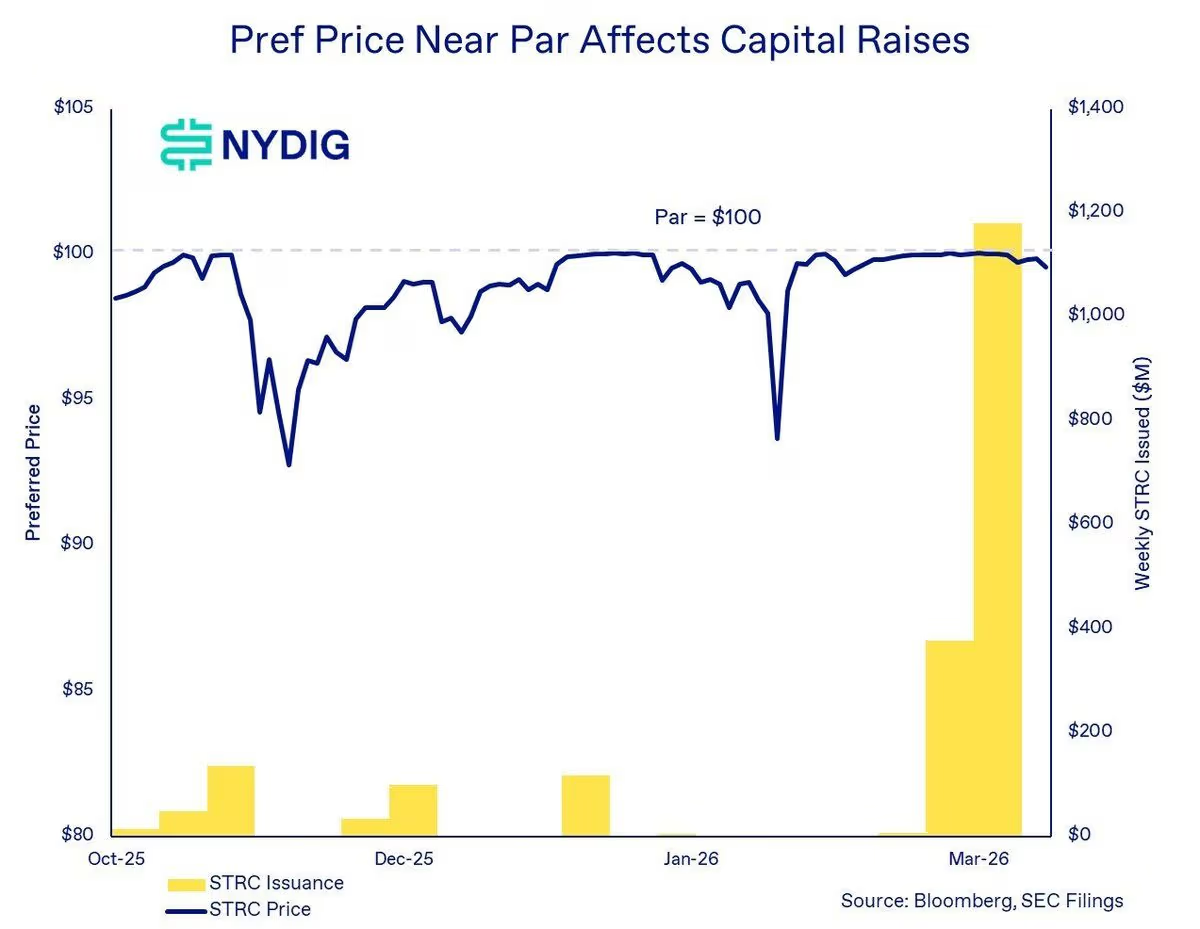

Strategy (MSTR), the leading corporate holder of bitcoin, has described the launch of its Perpetual Stretch Preferred Stock (STRC) as the firm’s “iPhone moment,” and despite its support in BTC accumulation, risks remain.

Before digging into these risks, it’s worth noting that while the focus is on STRC, specifically over its larger liquidity and adoption, they also apply to similar preferred offerings, including another bitcoin treasury company, Strive’s preferred offering, SATA.

These instruments are “not well understood through the lens of traditional credit or equity,” and instead require a different analytical framework, said NYDIG’s Global Head of Research Greg Cipolaro in a note.

By design, STRC targets a steady $100 share price, using a variable monthly dividend to keep trading near that level. The approach has already supported multi-billion dollar issuance and the acquisition of more than 50,000 bitcoin, according to STRC.live data.

At its core, STRC works by adjusting yield to steer price. If shares trade above $100, the company can trim the dividend to cool demand. If shares fall below that level, it can raise dividends to attract buyers. Keeping the price anchored lets the firm issue new shares near par, bringing in capital that is then deployed to buy bitcoin.

The novel financial instrument has been a success so far. Not only has it allowed Strategy to buy more than $3.5 billion worth of bitcoin, but it has also attracted institutions that have added STRC to their balance sheets.

In practice, the product resembles a money market fund with a floating yield of 11.5%, far above U.S. Treasuries. The appeal hinges on the steady $100 price tag coupled with high yields.

When conditions are favorable, NYDIG’s Cipolaro wrote, the mechanism creates a powerful feedback loop. The loop, in which STRC trades near par, enables the firm to raise capital, deploy proceeds to buy more bitcoin, expand the asset base, and sustain investor confidence. That confidence sustains additional issuance.

“As long as preferreds remain anchored near par, equity trades above the NAV, and capital markets stay open, the flywheel drives ongoing bitcoin demand,” Cipolaro wrote in the note.

Still, not everything’s rosy.

BitMEX Research has written in a note titled “A bit of Stretch” that it sees the risks related to the product as “substantially greater than those related to short duration U.S. treasuries.”

Where the risks actually sit

Bullish investors often point out that STRC is well-capitalized and could easily cover dividend payments, given Strategy’s massive 761,068 BTC war chest and more than $2.2 billion in cash reserves. That’s around 50 years of covered dividend payments, while the company can still lower STRC’s dividend over time to further the coverage. On top of that, there are monetization options for the company’s massive bitcoin stash, which could further dividend payments.

The risks, however, aren’t based on dividend coverage at all, according to NYDIG’s Cipolaro.

“The appropriate way to assess risk in STRC and SATA is through the lens of governance and subordination rather than focusing solely on payment risk,” he wrote.

The mechanism STRC uses also creates a stress path. If bitcoin drops and confidence in Strategy’s balance sheet weakens, STRC could slip below par.

To defend the price, the company would need to raise the dividend. Higher payouts increase cash obligations, which can, in turn, worry investors and push the price lower. That feedback loop is a familiar one in credit markets.

In a standard corporate setting, that cycle can end in forced asset sales. Companies may have to sell core holdings to meet rising obligations, locking in losses at the worst time. For Strategy, that would mean selling BTC into a falling market. However, Strategy’s Michael Saylor has repeatedly said he won’t sell the company’s bitcoin stack.

The STRC terms, however, give the company another option. The target price is not a binding promise. If conditions turn, Strategy can reduce the dividend rather than increase it.

According to BitMEX Research’s reading of the SEC filings related to STRC, Strategy can “at its absolute discretion, lower the dividend rate by up to 25 bps a month, no matter what else is happening.”

Unpaid dividends can, in addition, accrue without triggering default or forcing asset sales. As BitMEX Research put it, instruments like these were “written by the company for the company.”

Read more: Strategy’s latest massive bitcoin purchase offers insight into its evolving funding model

Built to bend, not break

That flexibility shifts what would happen to STRC in cases of a crisis.

Instead of a company caught in a squeeze, the pressure moves to the security holders. If the dividend is reduced, the yield becomes less attractive, and the market price can fall to reflect the new reality.

NYDIG’s Cipolaro made it clear in his note that the structure “can remain solvent while still delivering suboptimal outcomes for preferred holders due to the loss of confidence and funding access.” The risk isn’t a default on its dividend, but rather the loss of its attractiveness.

Strategy’s legacy software business does not cover those payments on its own. The model depends on continued issuance or balance sheet management tied to its bitcoin holdings.

The binding constraint is not income generation, but the combination of continued access to capital markets and sufficient asset coverage,” NYDIG’s Cipolaro wrote. The setup invites comparisons to structures that rely on new inflows to support payouts.

The difference here is that payouts are not fixed. If demand slows, the company can lower the dividend instead of maintaining a rate it cannot sustain. That feature helps protect the issuer but weakens the claim for investors seeking stability and income.

“When the music stops, if things become challenging for MSTR, instead of selling bitcoin, MSTR could just abandon the narrative that STRC is targeting stability,” BitMEX Research wrote. “This feels very favourable for MSTR and the dividend payments are therefore quite sustainable and affordable, in our view.”

Breaking the mechanism

Market impact will depend on how long the $100 anchor holds.

As long as demand for yield products remains strong and bitcoin sentiment is supportive, STRC can keep channeling funds into the company’s treasury strategy.

That, in turn, reinforces Strategy’s position as a major public holder of bitcoin. NYDIG has shown that bitcoin’s price stability is what enables the economic viability of at-the-market issuance of these products.

STRC and Striv’es SATA have seen their prices drop below par during periods of sharp bitcoin price declines, the firm’s research found. When that happens, “issuance becomes uneconomic, limiting the ability to raise capital and slowing the flywheel.”

The risk shows up when conditions change. A prolonged drop in BTC’s price or a shift in rates could test the price mechanism. If the dividend is cut to preserve cash, STRC could trade well below par. Losses would be borne by investors who treated the shares as a near-cash substitute.

“It resembles being short a put on bitcoin asset coverage, earning yield in exchange for bearing downside risk if bitcoin declines and erodes the asset cushion,” NYDIG offered as a frame for institutional investors. “Unlike a standard option, however, there is no fixed strike or maturity, and outcomes are path-dependent and shaped by management discretion.”

The broader significance is the template itself.

STRC blends equity features with bond-like behavior and a built-in adjustment lever. It offers a new path for companies to raise capital tied to volatile assets without locking in fixed obligations.

For now, these instruments have done their job: attract capital and support further bitcoin accumulation. The open question is how it behaves under stress and who absorbs the cost when the trade no longer looks stable.

The interpretation of that scenario isn’t great, but not for MSTR, “it’s the investors who may feel somewhat aggrieved when the music stops,” BitMEX concluded.

Read more: Strategy’s credit risk falls as preferred equity value surpasses convertible debt

Kenya is moving closer to formalizing oversight of its digital asset sector after completing public consultations on proposed rules for crypto firms.

On April 11, the National Treasury announced that it had concluded stakeholder submissions on the draft Virtual Asset Service Providers (VASP) regulations. This step advances the framework needed to implement the country’s 2025 law governing crypto-related businesses.

Kenya Drafts Stricter Rules for Crypto Firms

The rules will establish licensing requirements and supervisory standards for companies dealing in cryptocurrencies, tokenized assets, and stablecoins.

The proposed regime outlines entry thresholds for operators, including ownership suitability tests, capital requirements, and governance standards. It also establishes obligations related to risk management and anti-money laundering compliance.

The Kenyan authorities are also seeking to impose stricter consumer safeguards. This would include mandatory disclosures, transparent pricing, and protections for crypto client funds.

The framework introduces market conduct provisions aimed at curbing manipulation and insider activity, while requiring due diligence for asset listings and ongoing monitoring of trading activity. Firms would also be subject to periodic reporting, audits, and cybersecurity standards under a system combining on-site and off-site supervision.

The central bank and capital markets authorities are expected to share oversight of the crypto sector.

Kenya’s push to formalize oversight aligns with a broader global shift among regulators to define sectoral rules while preserving space for innovation.

The Treasury said the next phase will involve reviewing feedback and refining the draft before finalizing the regulations. The outcome is expected to shape how firms enter and operate in one of Africa’s more mature fintech markets.

“Kenya is building a trusted framework that balances innovation with financial stability,” the financial agency stated.

The consultation process comes as digital asset use expands rapidly across Africa. According to Ripple, the continent faces high transaction costs, delays in cross-border transfers, and limited access to stable foreign currencies.

As a result, people on the continent have shown increased reliance on crypto-based tools for settlement and savings.

Due to this, Sub-Saharan Africa has emerged as one of the fastest-growing crypto markets, with transaction volumes rising sharply over the past year.

The post Kenya Moves Closer to Regulating Crypto Firms With VASP Framework appeared first on BeInCrypto.

Crypto World

Trump token sees whale accumulation ahead of Mar-a-Lago gala; senators raise questions over event

Large investors are accumulating the TRUMP memecoin ahead of an upcoming gala hosted by President Donald Trump at Mar-a-Lago on April 28, even as the token trades near record lows and the impending event faces political scrutiny.

Data tracked by blockchain sleuth Lookonchain shows notable whale buying through centralized exchanges. One whale, “8DHkza,” withdrew 850,488 $TRUMP tokens (worth approximately $2.4 million) from Bybit over the past two days. Another address, “7EtuAt,” withdrew 105,754 tokens (around $298,000) from Binance 17 hours ago and currently holds 1.13 million tokens, valued at roughly $3.2 million.

Outflows from exchanges are said to represent investor intention to take direct custody of coins and hold the same for long-term. Hence, outflows are taken to indicate accumulation and potentially reduce immediate sell-side liquidity in the market.

The accumulation comes ahead of an invitation-only luncheon reportedly limited to the top 297 TRUMP token holders, with the top 29 receiving exclusive VIP access to Donald Trump.

However, TRUMP continues to trade at record lows near $2.80, down 0.2% on a 24-hour basis and over 1% in seven days. The token came under pressure this week after CoinDesk reported the Trump-linked crypto venture World Liberty Financial’s controversial lending strategy on the Dolomite DeFi platform.

Meanwhile, U.S. lawmakers have stepped up scrutiny of the Mar-a-Lago event. Senators Elizabeth Warren, Adam Schiff, and Richard Blumenthal have sent a letter to Fight Fight Fight LLC, a Delaware-based entity run by Trump associate Bill Zanker, requesting documents and information on whether Trump played a role in planning, promoting, or financially benefiting from the gathering. Fight Fight Fight LLC TRUMP memecoin in partnership with entities affiliated with Donald Trump.

“It is essential that Congress fully understand the extent to which President Trump and his family are profiting off of his cryptocurrency ventures,” the senators said, adding that “Congress must also take steps to prohibit and prevent these egregious conflicts of interest.”

The probe introduces an additional layer of uncertainty for the token, as regulatory and political risks intersect with already weak price action.

The United States government must pass the CLARITY Act, which aims to provide the crypto industry with clearer regulatory oversight, soon, or risk waiting almost another four years to move the industry forward, according to US Senator Cynthia Lummis.

“This is our last chance to pass the Clarity Act until at least 2030,” Lummis, a well-known crypto advocate, said in an X post on Friday.

“We can’t afford to surrender America’s financial future,” she added. The comments come as crypto industry participants begin to worry that the bill’s chances of passing this year are narrowing, with US midterm elections in November potentially changing congressional priorities and slowing momentum on the highly anticipated crypto legislation.

The former White House AI and crypto czar, David Sacks, also chimed in on Thursday with a similar view to Lummis.

“The time to act is now. Senate Banking, and then the full Senate, should pass market structure. I’m confident that they will. And then President Trump will sign this landmark bill into law,” Sacks said.

Consumers and entrepreneurs both “win” from the CLARITY Act

Many industry participants have argued that the passage of legislation aimed at clarifying which regulators oversee parts of the crypto industry could lead to greater innovation in the US and potentially increase demand for crypto assets among retail investors.

A16z Crypto managing partner Chris Dixon reiterated that view in a post, saying that “when rules are defined, both consumers and entrepreneurs win.”

A wide range of sectors in the crypto industry expect the move to be positive.

Web3 gaming giant Immutable founder Robbie Ferguson said just days before, on April 3, that “the CLARITY Act will make the last decade of growth in gaming look like a joke.”

On Friday, Coinbase CEO Brian Armstrong, who withdrew the crypto exchange’s support for the Digital Asset Market Clarity Act in January, said “it’s time” for the legislation to pass after months of delays.

Meanwhile, Coinbase chief legal officer Paul Grewal said on April 2 that the CLARITY Act could be nearing a markup hearing in the US Senate Banking Committee. However, he noted that progress hinges on resolving disagreements over stablecoin yield.

Related: CFTC unveils innovation task force members in crypto clarity push

Regulators are also voicing their support for the legislation.

US Securities and Exchange Commission (SEC) Chairman Paul Atkins said in a post on the same day that, “It’s time for Congress to future-proof against rogue regulators & advance comprehensive market structure legislation to President Trump’s desk.”

Magazine: Bitcoin quantum-safe without upgrade? CZ’s 2031 crypto vision: Hodler’s Digest, April 5 – 11

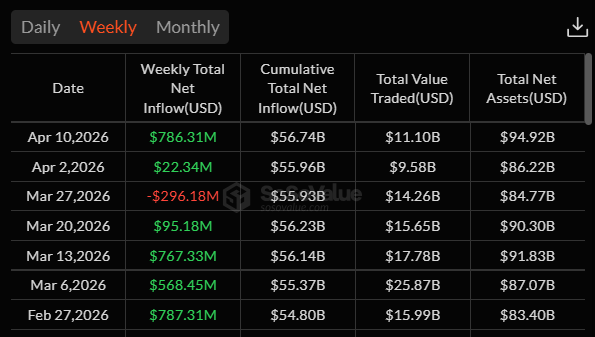

US spot Bitcoin exchange-traded funds (ETFs) posted their strongest weekly inflow since February last week, drawing more than $786 million.

Data from SoSoValue showed that the US-listed funds’ performance last week narrowly trailed the roughly $787.31 million recorded during the last week of February.

BlackRock and Morgan Stanley’s New MSBT Fund Drive Interest

The inflows followed a softer stretch for the products amid broader market volatility and geopolitical tension, which weighed on risk appetite.

SoSoValue data shows that the flow pattern was uneven through the week. The funds opened with a sharp $471.32 million intake on Monday, then slipped into outflows midweek before recovering on Thursday and Friday.

The turnaround left the group with its best weekly result in nearly two months and suggested buyers returned as Bitcoin regained momentum.

BlackRock’s iShares Bitcoin Trust remained the main driver of demand. The fund brought in about $612 million during the week, accounting for almost four-fifths of total net inflows across the category.

The concentration underscored how heavily new institutional allocations continue to favor the largest and most liquid product in the market.

Meanwhile, Morgan Stanley’s newly launched MSBT fund added another point of interest for the market. The fund raised roughly $46 million over its first three trading days, giving investors a fresh entry point as demand across the ETF group picked up again.

Its early flows were modest compared with BlackRock’s scale, but the launch carries broader significance because of Morgan Stanley’s distribution reach. The bank’s network of roughly 16,000 financial advisers oversees trillions of dollars in client assets, giving it access to a channel few Bitcoin ETF issuers can match.

The improvement in fund flows came alongside a strong week for the underlying asset. Bitcoin climbed from around $67,000 to above $70,000 during the period and was trading near $73,411 by the end of the week, a gain of about 9%.

The move marked one of the token’s strongest weekly advances in recent months and helped restore momentum after a period of weaker price action.

The post US Bitcoin ETFs Log Biggest Weekly Inflow Since February appeared first on BeInCrypto.

Polymarket betting markets reportedly appeared inside Google News results alongside established news publishers before disappearing.

A Google spokesperson told The Verge that the platform’s appearance in News was an error. “This site briefly appeared in Google News in error, and it is no longer surfacing in News,” spokesperson Ned Adriance reportedly said.

Before removal, Polymarket links were shown directly beneath mainstream outlets when users searched event-driven queries. In one example cited by Futurism, a search for “will ships transit the strait” related to the Strait of Hormuz returned a Polymarket market predicting outcomes on vessel passage alongside reporting from Reuters and The Guardian.

In a Sunday search conducted by Cointelegraph, the same query did not surface any Polymarket results.

Related: Three Polymarket traders made timely bets on US-Iran ceasefire

Polymarket and Kalshi pursue media partnerships

Last year, Google partnered with both Polymarket and rival Kalshi to integrate their data into Google Finance.

In June, Elon Musk’s X also announced a partnership with Polymarket, naming it as its official prediction market partner. The deal aimed to integrate the betting-based forecasting service into the social media platform.

Furthermore, in October, MetaMask said it would integrate Polymarket as part of its push to expand beyond a crypto wallet into a broader “democratized finance” gateway. The same month, World App, the digital wallet and identity platform from Sam Altman’s World project, also added the Polymarket app.

Related: Prediction market users await Artemis II mission splashdown

Small portion of Polymarket traders make a profit

As Cointelegraph reported, only a tiny fraction of Polymarket traders manage to generate consistent high monthly income, according to new data shared by crypto analyst Andrey Sergeenkov. While around 1% of traders have crossed $5,000 in profits in a single month, only 0.015% were able to sustain that level for four consecutive months.

The findings also show that just 0.033% of wallets have exceeded $100,000 in total profits, with some of these likely belonging to professional traders rather than retail users. Despite growing hype around prediction markets as a fast-rising crypto use case, the data suggests most participants struggle to maintain consistent profitability over time.

Magazine: Bitcoin’s ‘biggest bull catalyst’ would be Saylor’s liquidation — Santiment founder

Crypto exchange activity slowed in the first quarter of 2026 after the market cooled from its earlier peak.

Summary

- Crypto exchange trading volume fell sharply in Q1 2026 as market participation weakened after the cycle peak.

- Perpetual futures dominated March activity, with volume reaching four times the level of spot trading.

- Binance held the top position in spot and derivatives despite rising competition from secondary exchanges.

CryptoQuant data showed lower participation across centralized venues, while Binance kept the lead in both spot and derivatives trading.

Centralized exchange trading volume dropped about 48% from the October 2025 peak. The figure fell to $4.3 trillion in March 2026, its lowest level since October 2024.

The pullback showed lower participation from traders and investors after the earlier market run. Activity narrowed toward the biggest exchanges, as users favored liquid venues during periods of price movement.

Perpetual futures remained the main source of trading activity during the quarter. Perpetual volume rose to $3.5 trillion in March, while spot volume stood at $0.8 trillion.

That gap showed how strongly derivatives shaped market structure in Q1. Perpetual volume reached four times spot volume in March, and cumulative perpetual trading hit $4.5 trillion this year.

The rise in derivatives activity also picked up during the relief rally in the third week of March. Binance recorded the largest 24-hour open interest increase for both Bitcoin and Ethereum by mid-March.

Bitcoin open interest on Binance rose by $829 million in 24 hours, while Ethereum open interest increased by $1.6 billion. Across exchanges, Bitcoin and Ethereum perpetual futures open interest climbed to $23 billion and $16 billion.

Binance keeps lead in derivatives trading

Binance led the perpetual futures market with a 40% share and $1.4 trillion in monthly volume. OKX followed with 19%, while Bybit held 13%.

The data showed that most open interest growth flowed to Binance during the March rebound. Other exchanges, including Gate and Bybit, also posted gains, but none matched Binance’s scale.

Binance remained the largest spot trading venue in March. The exchange recorded $248 billion in spot volume and controlled 32% of the market.

That share was down from 37% in October 2025, but Binance still held a lead well ahead of rivals. MEXC and Bybit followed with 9% and 7%, while Gate and Crypto.com posted growth without changing the broader market order.

North Korea’s six-month infiltration campaign at Drift rattled a crypto industry already reeling from billion-dollar exploits.

But as the news settled, a bigger question came into focus: why does North Korea keep coming back to crypto in the first place, and why does its approach look so different from every other state-backed hacking operation on the planet?

The short answer, according to security experts, is that crypto helps give the regime a revenue stream and keep them afloat.

“North Korea doesn’t have the luxury of patience,” said Dave Schwed, chief operating officer at SVRN and the founder of the cybersecurity masters program at Yeshiva University. “They’re under comprehensive international sanctions and they need hard currency to fund weapons programs. The UN and multiple intelligence agencies have confirmed that crypto theft is a primary funding mechanism for their nuclear and ballistic missile development.”

That urgency explains a dynamic that has long puzzled investigators: why North Korean hackers carry out large-scale, traceable heists on public blockchains instead of quietly using crypto to evade sanctions the way other state actors do.

The answer, Schwed argues, is structural. Russia still has an economy: oil, gas, commodity exports, and trading partners willing to use workarounds. It needs crypto as a payment rail, but not for much else. Iran, too, has goods to move — sanctioned oil, proxy financing networks, willing intermediaries across the Middle East. North Korea has almost nothing left to sell.

“Their exports are almost entirely sanctioned. They don’t have a functioning economy that needs a payment rail. They need direct revenue,” Schwed said. “Crypto theft gives them immediate access to liquid value, globally, without needing a counterparty willing to do business with them.”

That distinction — crypto as infrastructure versus crypto as a target — is what separates North Korea not just from Russia, but from Iran as well. While Russia routes money through crypto to work around sanctions, and Iran uses it to fund proxy networks across the Middle East, North Korea is running something closer to a state-sponsored heist operation.

“Their targets are exchanges, wallet providers, DeFi protocols and the individual engineers and founders who have signing authority or infrastructure access,” said Alexander Urbelis, chief information security officer at ENS Labs and a professor of cybersecurity at King’s College London. “The victim is whoever holds the keys or access to the infrastructure that holds the keys.”

Russia and Iran, by comparison, treat crypto as incidental, a means to broader geopolitical ends.

“Russia targets elections, energy infrastructure and government systems. Iran goes after dissidents and regional adversaries,” Urbelis said. “When either of them touches crypto, it’s to move money, not to steal it from the ecosystem.”

That singular focus has pushed North Korean operatives to adopt tactics more commonly associated with intelligence agencies than criminal hackers: months-long relationship building, fabricated identities and supply chain infiltration.

The Drift campaign is only the most recent example.

“You’re not defending against a phishing email from a random scammer,” Urbelis said. “You’re defending against someone who spent six months building a relationship specifically to compromise one person who has the access you need to protect.”

Crypto’s own architecture makes it a uniquely attractive hunting ground. In traditional finance, even successful hacks run into friction in the form of compliance checks, correspondent bank checks, settlement delays and the possibility of reversing fraudulent transfers. When North Korea’s hackers pulled off the Bangladesh Bank robbery in 2016, the heist took days to process and most of the funds were eventually recovered or blocked. In crypto, none of those safeguards exist at the protocol level.

“Once a transaction is signed and confirmed, it’s final,” Urbelis said. The Bybit exploit earlier last year moved $1.5 billion in roughly 30 minutes, a pace and scale that would be nearly impossible in the traditional banking system.

That finality fundamentally changes the security calculus. In banking, a reasonable defense can be built across prevention, detection and response, because there’s always a window to freeze funds or reverse a wire. In crypto, that window barely exists, which means stopping an attack before it happens isn’t just preferable — it’s essentially the only option.

And while banks operate under decades of regulatory guidance and audit requirements, many crypto projects are still improvising — often prioritizing speed and innovation over governance and controls.

That gap creates an environment where even sophisticated teams can be vulnerable, particularly to the kind of long-term infiltration tactics North Korea has been refining.

“This is the hardest operational security problem in crypto right now,” Urbelis said of the challenge of vetting against sophisticated fake identities and third-party intermediaries. “I don’t think the industry has solved it.”

Read more: How North Korea’s 6-month long secret espionage program has crypto community rethinking security

Donald Trump is facing fresh scrutiny as crypto tokens tied to his name and family trade near record lows.

Summary

- TRUMP fell about 90% from its peak as renewed scrutiny hit Trump-linked crypto projects again this week.

- WLFI dropped to a fresh all-time low as criticism of Trump family crypto ties intensified.

- Senators pressed Bill Zanker for details after Trump announced an April 25 gala for token holders.

The pressure has grown after a new gala for token holders raised new questions from Democratic lawmakers.

The Official Trump token, known as TRUMP, fell to an all-time low of about $2.73 in March 2026. It later traded near $2.86, according to CoinGecko data.

The token has dropped about 90% from its January 2025 peak above $73. The decline has kept attention on Trump-backed crypto ventures as traders track whether the project can regain momentum.

World Liberty Financial’s governance token, WLFI, also fell sharply. The token dropped to about $0.07 on Saturday, marking a new all-time low.

WLFI is down nearly 75% from its September 2025 high of about $0.31. The slide has added to pressure on projects linked to Trump and his family.

Criticism grows around Trump crypto ventures

The price declines drew criticism from market observers and legal scholars. Professor Tonya Evans responded to the sell-off with a sharp rebuke of Trump’s role in crypto.

“We thought Sam Bankman-Fried or Gary Gensler were the worst things to happen to the crypto industry, and they were horrible,” Evans said.

She added that “turns out, it was the guy who surrounds himself with sycophants, siphons every bit of value he can for himself, and then expeditiously bankrupts companies and casinos without consequence.”

Her comments came as debate over Trump’s crypto activity returned to the center of public discussion. Critics have focused on whether token-linked events create a financial path to political access.

April gala draws Senate attention

President Trump recently announced another gala for token holders, scheduled for April 25. The event has drawn criticism from Democratic senators who said the plan raises questions about access and fundraising.

Senators Elizabeth Warren, Richard Blumenthal and Adam Schiff sent a letter to Bill Zanker, the memecoin’s creator, seeking details about the event, according to Politico. They said organizers were “dangling access” to Trump while requiring attendees to hold TRUMP tokens, a structure they said could benefit Trump and his family through increased token demand.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Arthur Hayes, co-founder of BitMEX, has added to his Hyperliquid (HYPE) position, purchasing 26,022 tokens worth approximately $1.1 million.

The buy, flagged by on-chain tracker Lookonchain, marks his first HYPE accumulation in roughly three months, signaling renewed confidence in the token.

Why Arthur Hayes Is Doubling Down on Hyperliquid

With this latest addition, his total holdings now stand at 247,334 HYPE, valued at approximately $10.44 million. The position is sitting on unrealized gains of 27.22%, equivalent to around $2.23 million in profit.

This reflects a strong return on his initial investment despite broader market volatility in the crypto space. The renewed accumulation follows Hayes’s public declaration on April 8.

Follow us on X to get the latest news as it happens

Hayes has maintained a $150 price target for the token by August 2026, roughly a 266% increase from current levels. The executive pointed to Hyperliquid’s revenue model as a key driver.

The platform returns 97% of its trading fees to buy back and burn HYPE from the open market, creating a deflationary loop that ties token value directly to platform usage.

Meanwhile, the acquisition comes as institutional interest in HYPE is also rising. Bitwise filed an amended registration statement with the SEC, adding the ticker BHYP and a 0.67% management fee.

Bloomberg analyst Eric Balchunas said such additions typically signal a fund may launch soon. Last month, Grayscale submitted its own S-1 application to list the Grayscale HYPE ETF on Nasdaq under the ticker GHYP.

A potential ETF approval could open the door to significant institutional capital inflows into HYPE, potentially driving broader adoption and renewed price momentum for the token.

HYPE has been one of the strongest large-cap performers over the past year, gaining roughly 176% according to CoinGecko data. However, it has not escaped broader market pressure.

The token slipped approximately 2% in the past 24 hours to around $40.91 as the US and Iran failed to reach an agreement.

Meanwhile, decentralized exchange activity is contracting across the board. Total DEX spot volume fell 23.9% to $212 billion in March, the lowest monthly figure since October 2024.

Monthly perpetual DEX volumes dropped to $699 billion in March, down from a peak of $1.369 trillion in October 2025, according to DefiLlama data. Hyperliquid still leads the perp segment, but the five-month downtrend raises questions about whether fee-driven buybacks can sustain their pace if trading activity continues to cool.

Whether ETF approvals and sustained whale accumulation can offset that macro softening remains the key question for HYPE holders heading into Q2.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Arthur Hayes Buys $1.1 Million in HYPE After 3-Month Break appeared first on BeInCrypto.

Bitcoin gave up its late-week gains on April 12 after the United States and Iran failed to secure a permanent peace agreement.

Summary

- Bitcoin fell sharply after US-Iran peace talks failed to produce a permanent agreement over the weekend.

- Ethereum, XRP, BNB and Solana declined as the wider crypto market turned lower today.

- RAVE rose another 40% and extended gains above 1,000% despite the broader market pullback.

The pullback ended a steady rise that started after both sides announced a two-week ceasefire, and it pushed most major altcoins lower.

Bitcoin started the week with gains after reports said the United States and Iran had opened ceasefire talks. The asset moved from about $67,000 to $70,000 before fresh doubts around the talks brought back volatility.

The price then climbed again after President Donald Trump announced a ceasefire on Tuesday. Bitcoin rose above $72,000 and later moved close to $73,000 as traders responded to easing geopolitical stress and fresh market speculation around the Strait of Hormuz.

Bitcoin kept rising into the weekend as peace talks in Pakistan approached. The asset reached nearly $74,000 late on April 11, extending the recovery that followed the ceasefire news.

That move ended early on April 12. Bitcoin fell by more than $2,000 within minutes after Vice President JD Vance said both sides had failed to reach a lasting agreement. At the time of reporting, Bitcoin traded near $71,500, down 1.5% on the day.

Ethereum, XRP and Solana move lower

Most large-cap altcoins also posted losses after Bitcoin reversed. Ethereum fell about 1% but stayed above $2,200, while XRP slipped to $1.33 after a similar daily decline.

BNB dropped below the $600 level, and Solana lost more than 2%. HYPE, Cardano and Bitcoin Cash each fell by more than 3%, while Polkadot and RAIN posted deeper losses during the broader market pullback.

RaveDAO’s native token moved against the wider market trend and rose another 40% on the day. The token has gained more than 1,000% since last Sunday and has entered the top 100 altcoins by market value.

The total crypto market cap fell by more than $30 billion and dropped to $2.51 trillion. Bitcoin’s market cap stood at about $1.43 trillion, while its market dominance remained above 57%.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Israeli strike kills infant girl in south Lebanon during father’s funeral

Kenya Moves Closer to Regulating Crypto Firms With VASP Framework

Boxing: Why Tyson Fury and Anthony Joshua are still on different pages

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

Achieving financial freedom isn’t permission to abandon your purpose on earth. #worldwide

Moneyview Personal Loan App | How To Apply Money View Loan | Moneyview Personal Loan Telugu 2026

How Small Actions Change Financial Struggles | A Simple Economics Story

-

Business6 days ago

Business6 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Politics2 days ago

Politics2 days agoUS brings back mandatory military draft registration

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Veronica Beard

-

Tech5 days ago

Tech5 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Fashion6 days ago

Fashion6 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Sports2 days ago

Sports2 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion5 days ago

Fashion5 days agoLet’s Discuss: DEI in 2026

-

Crypto World3 days ago

Crypto World3 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business2 days ago

Business2 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Crypto World4 days ago

Crypto World4 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics2 days ago

Politics2 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Business2 days ago

Business2 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Business19 hours ago

Business19 hours agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Tech6 days ago

Tech6 days agoItalian court says Netflix must refund customers up to $576 over price hikes

-

Tech6 days ago

Tech6 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

-

Tech6 days ago

Tech6 days agoSamsung just gave up on its own Messages app

-

Tech6 days ago

Tech6 days agoHaier is betting big that your next TV purchase will be one of these

-

Tech6 days ago

Tech6 days agoThe Xiaomi 17 Ultra has some impressive add-ons that make snapping photos really fun

-

Politics2 days ago

Politics2 days agoLBC Presenter Mocks Trump Over Iran War Failures

-

Tech6 days ago

Tech6 days agoSave $130 on the Samsung Galaxy Watch 8 Classic: rotating bezel, sleep coaching, and running coach for $369

You must be logged in to post a comment Login