Crypto World

Strategy’s Saylor Signals BTC Buy Ahead of 2x Monthly Dividend Vote

Strategy, the bitcoin treasury vehicle led by executive chairman Michael Saylor, signaled additional activity in its BTC holdings on Sunday as it nears a pivotal STRC dividend vote. Saylor posted on X a bubble chart tracking Strategy’s Bitcoin purchases over nearly six years, hinting that “a good time to add more dots.” The post came ahead of a shareholder meeting where investors will decide whether STRC dividends shift from a monthly cadence to semi-monthly payouts.

CEO Phong Le amplified the message, noting that Strategy’s objective is to increase net Bitcoin and Bitcoin per share over time, and that rumors should be treated cautiously until the vote concludes.

Strategy continues to hold a sizable Bitcoin treasury—843,706 BTC with an average cost of about $75,701 per BTC. Bitcoin itself traded around $62,153 at the time of writing, after a roughly 16.6% decline over the past week, according to CoinMarketCap data.

Last week, Strategy announced it had repurchased some corporate debt, temporarily pausing further BTC accumulation and stirring market fears that financing buybacks could require selling BTC.

Key takeaways

- A signal of renewed BTC purchases from Saylor ahead of STRC news, continuing a pattern of public cues ahead of Strategy’s acquisitions.

- The proposed STRC dividend change would move to semi-monthly payments; passage hinges on 50% of all 85 million STRC shares outstanding as of April 17, 2026.

- BTC’s recent price action has been negative, with Strategy’s 843,706 BTC holding carrying an implied cost basis around $75,701 per coin.

- Debt repurchase last week paused BTC accumulation and raises questions about liquidity and future capital allocation plans.

- Retail investor proxy voting participation remains historically low relative to institutions, potentially shaping the outcome of the proposal.

Strategic signals behind the vote and the BTC thesis

Michael Saylor’s public signaling has become part of Strategy’s cadence ahead of material BTC moves. The executive chairman’s social posts, often accompanied by data visualizations from StrategyTracker, historically precede the company’s latest crypto purchases and help frame market expectations around Strategy’s ever-expanding bitcoin pool. Strategy remains one of the most prominent publicly traded holders of Bitcoin, with a reported 843,706 BTC on its balance sheet and an average acquisition cost near $75,701 per BTC. In the current price environment, Bitcoin traded around $62,153, illustrating the gap between the cost basis of Strategy’s holdings and prevailing market prices.

The context matters for investors evaluating the potential impact of further acquisitions on Strategy’s per-share Bitcoin exposure and on the liquidity characteristics of STRC—an issue that has gained additional attention as the company navigates a broader sell-off in crypto markets.

Dividend cadence change: voting mechanics and what’s at stake

The key decision for Strategy shareholders is a proposed adjustment to STRC dividend payments, shifting from a monthly to a semi-monthly schedule. The company argues that more frequent distributions would reduce reinvestment lag, improve liquidity and market efficiency, and contribute to greater price stability. The amendment requires the support of 50% of all STRC shares outstanding, which stood at 85 million as of April 17, 2026, meaning roughly 42.5 million votes would be needed for passage.

The outcome is expected to be determined at Monday’s Strategy shareholder meeting. Cointelegraph requested turnout data from proxy solicitor Alliance Advisors, but did not receive an immediate response. As a practical matter, retail participation in proxy voting has historically lagged institutional engagement; a Harvard Law School Forum on Corporate Governance note from November highlighted that retail holders vote on about 29% of their shares, compared with roughly 77% for institutional holders.

What changes if the measure passes and what to watch next

Proponents contend that semi-monthly distributions would bolster liquidity, shorten reinvestment lags, and theoretically enhance the Sharpe ratio by providing more entry and exit points for investors. Strategy leadership has framed the change as part of a disciplined, time-scaled approach to increasing bitcoin exposure over time while maintaining stability for STRC holders. The company suggested that the new cadence would begin in June, with the first semi-monthly payout expected in July, a detail referenced by Saylor at the Synergy26 conference for registered investment advisors.

Beyond the vote, investors will be watching for any new BTC purchases or other capital allocation moves that could influence Strategy’s cost basis and the dynamic between its bitcoin treasury and STRC’s market performance. The latest signals from Saylor and StrategyTracker emphasize that corporate actions remain intertwined with the company’s long-running strategy of expanding bitcoin ownership while navigating the implications of debt management and liquidity planning.

As the voting process unfolds, readers should keep an eye on turnout figures and any updates on Strategy’s Bitcoin accumulation plans, which could have material implications for both STRC holders and the broader narrative around publicly traded Bitcoin treasury vehicles.

HTX, the crypto exchange linked to Justin Sun, has delisted the USD1 stablecoin issued by World Liberty Financial (WLFI) after asserting that WLFI froze HTX on-chain addresses in a sanctions-related review. In its update, HTX said WLFI’s project team unilaterally imposed a freeze on specific HTX on-chain addresses, restricting the on-chain circulation of WLFI assets tied to those addresses. As a result, HTX stopped accepting deposits or conversions of USD1 and announced a 1:1 conversion of USD1 holdings into Tether (USDT), with exact timing and procedures to be announced later. The exchange also suspended trading pairs involving USD1 or WLFI and stated it would pursue safeguards for user assets through potential legal remedies.

HTX’s decision arrives amid heightened regulatory pressure on crypto platforms in Europe and beyond. In late May, the United Kingdom designated HTX (formerly Huobi Global) under sanctions criteria, citing “reasonable grounds to suspect” that the exchange had supported Russia’s government through financial services. HTX has maintained that the sanctioned entity is Huobi Global S.A., distinct from the online HTX exchange, and that the UK designation should not impact HTX’s platform or user funds. The delisting underscores how sanction compliance and complex corporate structures can translate into rapid on-chain and trading frictions for users.

Key takeaways

- HTX delists World Liberty Financial’s USD1 stablecoin and halts USD1-related deposits, conversions, and several trading pairs, citing a WLFI-initiated address freeze.

- USD1 holdings on HTX will be converted 1:1 into USDT, with further timing details to be announced separately.

- HTX accuses WLFI of freezing addresses without adequate notice, contractual basis, or due process, and says it may pursue legal remedies to protect users.

- UK sanctions on HTX in May 2024 highlight the broader regulatory backdrop facing exchanges linked to high-profile personalities and political figures, though HTX asserts the sanctioned entity is distinct from the live exchange.

- Public cross-lawsuits frame a tense web: Justin Sun has previously sued WLFI over token freezes, while WLFI alleged defamation in a separate filing—illustrating how reputational and legal battles intersect with stability and compliance issues.

HTX delisting: how the dispute unfolded and what changes for users

In an official post, HTX stated that WLFI’s team “unilaterally imposed a freeze on specific HTX on-chain addresses based on sanctions compliance reviews.” The consequence, according to HTX, is a restriction on the on-chain circulation of WLFI assets associated with those addresses. To protect users, HTX decided to delist USD1 and to convert existing USD1 holdings into USDT at a 1:1 ratio. The exchange emphasized that the exact timing and mechanics of the conversion would be announced separately, but the immediate effect is a pause on deposits and conversions of USD1, as well as the suspension of WLFI/USDT, USD1/USDT, BTC/USD1 and ETH/USD1 trading pairs.

HTX’s statement also criticized WLFI for acting without sufficient prior communication, adequate contractual or legal grounds, or transparent disclosure. The exchange signaled that it would explore legal avenues to safeguard user rights and assets, indicating a possible broader legal battle should WLFI stand by the freezing action. This move reflects a broader tension inside the crypto liquidity ecosystem: sanctions compliance can collide with user rights and the integrity of on-chain assets, pushing platforms to make rapid, user-visible changes to stablecoins and trading liquidity.

Regulatory backdrop: sanctions, statements, and the path forward

The UK’s sanction action against HTX in May 2024 serves as a backdrop to HTX’s decision to delist USD1. The British government cited “reasonable grounds to suspect” that HTX had supported Russia’s government through financial services. HTX has asserted that Huobi Global S.A., the entity named in the designation, is a distinct corporate entity from the online HTX exchange. The company argued that such a designation should not automatically impact its platform or its users, yet the incident adds pressure on exchanges to maintain compliance while preserving user assets and liquidity.

World Liberty Financial has not publicly confirmed whether it froze HTX addresses. WLFI’s public statements, however, have underscored a stance on sanctions compliance. On X, WLFI stated that “in light of recent sanctions updates, World Liberty Financial maintains risk-based sanctions compliance controls.” The project has yet to provide detailed commentary on the HTX matter, and Cointelegraph notes that it contacted WLFI for comment. The lack of immediate public disclosure from WLFI leaves a gap in understanding the full scope of the address freezes and their rationale, complicating the assessment of responsibility and due process in the process.

Beyond this specific incident, the broader dispute intersects with ongoing personal and legal frictions between Justin Sun and WLFI. Sun, a crypto entrepreneur associated with HTX and serving on the exchange’s global advisory board, has previously pursued civil action against WLFI, alleging that WLFI froze his tokens and threatened to burn them “without any proper justification.” WLFI later countered with a defamation lawsuit against Sun, alleging false statements about WLFI’s token sale practices and alleged prohibited transfers. These overlapping lawsuits highlight how reputational and contractual disputes can evolve alongside regulatory actions, potentially impacting liquidity, market perception, and user confidence in affiliated platforms.

Market impact and investor perspective: what this means for users and builders

While the immediate action centers on USD1 and related WLFI assets, the episode raises several questions for investors, traders, and developers building on or around WLFI-linked instruments. First, the incident underscores the fragility of stablecoins and on-chain assets when sanction screens intersect with exchange-level enforcement. A unilateral address freeze, followed by asset delistings, can squeeze liquidity and complicate exit possibilities for users who hold instruments pegged to WLFI or USD1. Traders who previously relied on USD1 liquidity on HTX will need to adapt to convert liquidity into USDT, potentially widening spreads between WLFI-related pairs and other stablecoins until liquidity rebalances elsewhere.

Second, the episode illustrates how jurisdictional sanctions risk translates into operational risk for exchanges. HTX’s readiness to delist and convert holdings signals a risk-management approach aimed at protecting users, but it also introduces uncertainty for users who may have been holding USD1 or WLFI assets across multiple venues. The UK sanction action against HTX, while contested in terms of its impact on the online platform, contributes to a broader environment in which exchanges must balance regulatory compliance with user rights and asset usability.

For builders and auditors, the situation highlights the importance of transparent governance and clear communications around sanctions-driven actions. As WLFI and HTX navigate legal actions and potential regulatory clarifications, projects issuing on-chain tokens tied to financial instruments will benefit from robust dispute-resolution mechanisms, explicit on-chain freeze procedures, and predictable paths for user redress when asset freezes occur. The absence of a standardized framework for addressing such freezes can increase confusion and erode trust during already volatile periods in the crypto market.

What comes next: unresolved questions and watchpoints

Key questions remain about how WLFI will address HTX’s allegations of improper freezing, whether WLFI will provide detailed disclosures about the affected addresses, and how the conversion process from USD1 to USDT will unfold in terms of timing, fees, and eligibility. The UK sanction action against HTX adds a layer of regulatory scrutiny that may influence how other exchanges approach similar scenarios, especially when there are concerns about the delineation between sanctioned entities and live platforms. As the legal dispute between Sun and WLFI develops, readers should monitor whether additional lawsuits emerge and how courts interpret sanctions compliance, due process, and the protection of user assets in cross-border crypto arrangements.

For now, users of HTX holding USD1 or WLFI-linked assets should stay alert to further notices from HTX regarding conversion timelines, deposit options, and new trading restrictions. As WLFI responds and regulators weigh next steps, the market will be watching closely for the emergence of any precedent that could shape how stabilizers and sanction screening interact with on-chain asset flows in the months ahead.

Sources: HTX official post on X; UK sanctions update on HTX; World Liberty Financial statements on X; prior reporting on Justin Sun’s suits against WLFI and WLFI’s defamation suit against Sun.

Yuga Labs has completed a whitehat rescue operation after an exploit in Flooring Protocol placed several high-value NFTs at risk.

Summary

- Yuga Labs rescued 68 NFTs after Flooring Protocol’s exploit exposed high-value collections to theft.

- The saved assets included BAYC, MAYC, CryptoPunks, Azuki, Moonbird, Doodles and other NFTs.

- Flooring Protocol’s architect said aggressive bit-level code helped hide the vulnerability from security reviews.

Yuga Labs CEO Michael Figge said the assets are now in the company’s custody. The rescued NFTs include 29 Bored Apes, 4 Mutant Apes, 1 BAKC, 2 CryptoPunks, 1 Azuki, 2 Elementals, 26 Captains, 1 Moonbird and 2 Doodles.

Yuga Labs moves after Flooring Protocol exploit

Figge said Yuga Labs acted after an exploit hit Flooring Protocol earlier on June 8. Some collections had already been raided before the team found a related risk path.

“We’ve just finished a whitehat operation on an exploit discovered in Flooring Protocol,” Figge said.

The rescue involved Yuga Labs’ blockchain lead, known as 0xQuit, and security researcher Coffee. Figge said GrailsOTC fronted the funds and NFTs needed to move exposed assets away from vulnerable pools.

The company said it will work with Flooring Protocol developers to return the assets once a fix is ready.

Bug created near-unlimited token balance

0xQuit said the exploit allowed a small amount of WETH to create a near-infinite fpToken balance. Attackers could then drain Flooring pools and redeem the underlying NFTs.

The issue came from packed ownership and indexing logic. According to 0xQuit, a malicious token ID could make ownership checks pass while later accounting showed a different result.

That created what he called “ghost ownership.” After that, an unchecked balance update caused an underflow and gave the attacker a much larger balance than intended.

Once the balance wrapped, the attacker could push token prices near zero and extract liquidity from the pool.

Flooring Protocol warns against new deposits

Flooring Protocol’s 0xFreeLunch said the exploit affected FloorProtocol V2 and BitmapPunks. Both projects used contracts where fungible tokens were pegged 1:1 to NFTs locked in the contract.

“Despite multiple rounds of security reviews,” he said, an attacker found a vulnerability that allowed excess fungible tokens to be minted and redeemed for NFTs.

He said the same vector also hit BitmapPunks and drained liquidity pools supplied by the team. He added that the attack surface was larger than the first attacker appeared to know.

0xQuit warned users not to deposit any more NFTs into Flooring Protocol, saying newly deposited assets could become vulnerable.

More than $500k in NFTs secured

0xQuit said the rescued NFTs were worth more than $500,000. He also said the exploit was not fully resolved because attackers still held some NFTs.

The incident adds to Flooring Protocol’s history of security concerns. Earlier related reports noted that the protocol was previously hit in an NFT exploit worth about $1.5 million.

Flooring Protocol’s architect said he takes responsibility for the contract design. He said the vulnerability came from gas-saving bit-level code that escaped earlier security reviews.

He also said the team is tracing extracted assets and working with security teams and exchanges.

Separately, as crypto.news reported, BAYC NFTs have remained a target for theft. In May 2024, an NFT trader lost three Bored Apes worth over $145,000 in a phishing attack linked to Pink Drainer.

BTC, ETH, XRP and others pulled back from their overnight highs as Iran-Israel tensions and oil rally triggered risk aversion in Asian stocks.

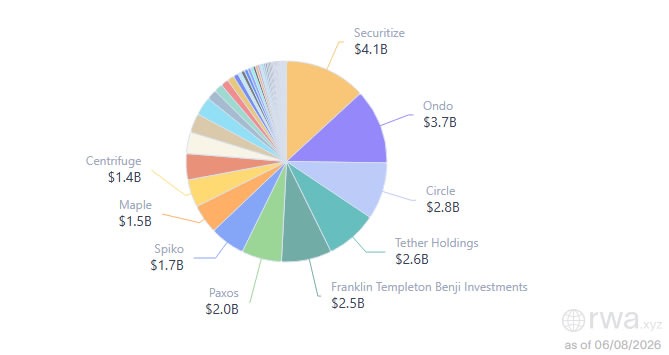

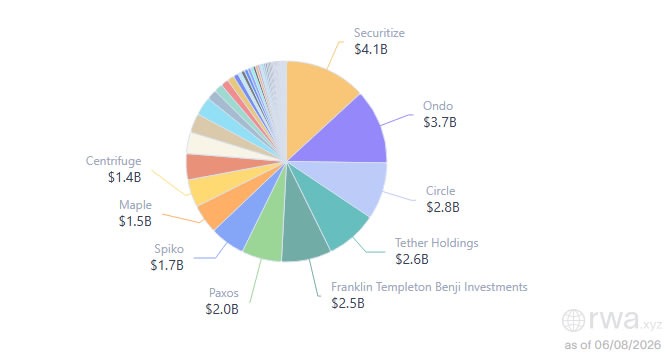

Real-world asset tokenization platform Securitize is one step closer to going public via a special acquisition company (SPAC) merger, after one of its filings was approved by the US Securities and Exchange Commission.

The regulator approved the Form S-4 registration statement from Cantor Equity Partners II, a publicly traded special purpose acquisition company (SPAC) sponsored by an affiliate of Cantor Fitzgerald, and Securitize on Friday.

Carlos Domingo, co-founder and CEO of Securitize, said the move marks “another important milestone for Securitize and for the broader institutional adoption of tokenization.”

Shareholders are set to vote on June 29, and if approved, the combined company will list on the New York Stock Exchange as Securitize Corp, or “SECZ,” giving investors access to one of the largest real-world asset tokenization companies in the world.

Securitize has $4 billion in assets under management and offers tokenized funds in partnership with leading asset managers, including Apollo, BlackRock, BNY, VanEck and others. The firm reported a first-quarter revenue of $19.5 million, up 39% from the prior-year period.

The NYSE signed a memorandum of understanding with Securitize in March as part of a broader effort to develop blockchain-based stock trading infrastructure for Wall Street.

Securitize is the largest tokenization platform by market share. Source: RWA.xyz

Tokenized RWA onchain value up 220% in 12 months

Tokenized real-world assets such as equities and US Treasuries have seen strong momentum recently, despite the broader crypto bear market.

Related: SEC makes digital assets strategic priority through 2030

Total RWA value on-chain hit a record high of $32 billion in May, excluding stablecoins, following an increase of around 220% over the previous 12 months.

Almost half of the assets on-chain are tokenized US Treasuries, while around 16% are tokenized commodities, according to RWA.xyz. Tokenized stocks represent a small market share with just 4.8% or $1.5 billion.

Ethereum and layer-2 networks remain the market leaders for tokenization, with more than 60% dominance combined.

Magazine: Korea probes Polymarket users, crypto PACs sweep primaries: Hodler’s Digest

Something strange happened in early June 2026. The crypto market shed roughly $250 billion in 72 hours, with Bitcoin and Ethereum both suffering double-digit losses, in one of the most violent deleveraging events in recent memory.

Summary

- Crypto lost roughly $250B in 72 hours while major U.S. stock indices remained near record highs.

- More than $5.4B in leveraged longs were liquidated over five days, strengthening the leverage-shakeout explanation.

- Crypto-specific leverage, ETF outflows, sentiment, and forced selling explain the crash better than an equity-market decline.

- The decoupling shows crypto remains vulnerable to internal market mechanics despite growing institutional integration.

And while crypto burned, the traditional financial markets it is supposed to move with did not flinch. Major U.S. stock indices continued trading near their all-time highs, showing zero signs of the systemic stress you would expect if a genuine risk-off wave were sweeping global markets. This divergence is the most analytically interesting feature of the entire selloff, and it has split observers into camps.

Some see proof of manipulation, others a pure crypto-specific liquidity shakeout, and others a warning that crypto is front-running a macroeconomic turn that equities have not yet priced. The one explanation that does not fit the evidence is the simplest one everyone reaches for: that crypto crashed because the broader market did. It did not, because the broader market did not crash. This piece works through what the decoupling actually means, why it happened, and what it tells you about what crypto has become.

The divergence, precisely

Start with the two facts that do not fit the usual story, because their coexistence is the whole puzzle.

Fact one: crypto suffered a severe, fast collapse. Roughly $250 billion evaporated from the total digital asset market capitalization in 72 hours. Bitcoin fell from the $70,000s toward $61,000, Ethereum dropped under $1,800 and touched lower, and major altcoins fell double digits, with Solana, Cardano, and others down sharply. Over a billion dollars in leveraged positions were liquidated in cascades. By any measure, this was a genuine crypto crisis, not a routine pullback.

Fact two: traditional markets were calm. While crypto bled, major U.S. stock indices continued to trade near their historical highs. There was no equity crash, no credit-market stress, no spike in the volatility indices that signal genuine financial fear, no flight to safety of the kind that accompanies real systemic risk-off events. The stock market, in other words, behaved as though nothing was wrong, because from its perspective nothing was.

This coexistence breaks the explanation most people reach for instinctively. When crypto falls hard, the reflexive assumption is “risk assets are selling off” or “the macro environment turned.” But that explanation requires the broader risk-asset complex to be selling off too, and it was not. Stocks, the largest and most liquid risk-asset class, sat near record highs throughout. So whatever drove crypto down, it was not a general flight from risk that swept everything, because everything did not get swept. The crypto crash was, to a striking degree, a crypto event. Understanding why requires looking at what is specific to crypto, and that is where the real explanations live.

Explanation one: the leverage shakeout

The most concrete and well-supported explanation is that this was a crypto-native liquidity event, driven by the leverage that exists inside crypto markets and almost nowhere else at the same intensity.

Crypto markets carry leverage that traditional markets do not permit at the same scale. Retail and professional traders alike can take positions many times their capital through perpetual futures and other derivatives, and during the calm, rising stretch before the crash, that leverage accumulated. Funding rates ran hot, open interest swelled, and the market filled with crowded long positions, each carrying a liquidation price not far below the current level. This built a structure that was fragile in a way the stock market simply was not, because equities do not carry the same density of leveraged, auto-liquidating positions.

When the price started falling, that structure did what it always does: it cascaded. Falling prices hit the first cluster of liquidation points, forcing automatic selling, which pushed prices lower, hitting the next cluster, in a self-reinforcing chain that ran far faster than any human could react. More than $5.4 billion in leveraged long positions was reportedly liquidated over five days, with daily losses peaking above $400 million on June 4. This is a purely internal crypto mechanism. It does not require the stock market to do anything, because it is generated entirely by the leverage structure inside crypto itself. A leverage shakeout of this kind can crater crypto while equities sit untouched, precisely because the fragility lives in crypto’s own plumbing.

This explanation fits the divergence perfectly. If the crash were driven by a leverage cascade unique to crypto’s market structure, you would expect exactly what happened: a violent crypto collapse with no corresponding move in traditional markets, because the mechanism is endogenous to crypto. The $250 billion did not flee to safety in bonds or cash in a way that would show up in traditional markets; much of it simply evaporated as leveraged positions were wiped out and forced selling drove prices down. The shakeout interpretation says the crash was real but mechanical, a deleveraging event that cleaned out excess instead of delivering a verdict on crypto’s value or a reaction to the outside world.

Explanation two: the manipulation theory

The decoupling has also fueled a louder, more conspiratorial explanation, and while it deserves skepticism, it deserves a fair hearing because the divergence is what gives it oxygen.

The manipulation argument runs roughly as follows: the crypto market is smaller, less regulated, and more concentrated than traditional markets, which makes it more susceptible to deliberate price manipulation by large players. The fact that crypto crashed in isolation, without any corresponding macro event in traditional markets, is read by proponents as evidence that the move was engineered, that large actors deliberately triggered cascades to liquidate over-leveraged retail positions, hunt stop-losses, and accumulate at lower prices. The thinness of weekend and off-hours crypto liquidity, the concentration of derivatives activity on a handful of venues, and the documented history of manipulation in crypto’s past all feed the suspicion.

There is a legitimate kernel here that should not be dismissed entirely. Crypto markets really are more manipulable than deep, regulated equity markets, liquidation cascades can in fact be triggered and exploited by large players who can see where stop-losses and liquidation points cluster, and the practice of pushing price into liquidation zones to harvest forced selling is a real phenomenon, not pure fantasy. To that extent, “manipulation” in the narrow sense of large players exploiting the leverage structure is plausibly part of what happened.

But the strong version of the theory, that the entire crash was a coordinated engineering operation, overreaches and should be treated with caution. The selloff has ample non-conspiratorial explanation: record ETF outflows, a hawkish Fed outlook, genuine geopolitical risk from U.S.-Iran tensions, the Saylor sale denting sentiment, and the leverage cascade. When sufficient ordinary forces explain an event, attributing it to deliberate manipulation requires extraordinary evidence that proponents generally do not provide.

The divergence from stocks does not prove manipulation; it is equally well explained by the leverage shakeout, which is mechanical, not orchestrated. The honest position is that exploitation of the leverage structure by large players is real and probably occurred at the margins, while the grand-conspiracy version is an understandable but unsupported leap that the decoupling alone cannot justify.

Explanation three: crypto is front-running something

The third explanation is the most unsettling, and it takes the decoupling as a warning, not a quirk: that crypto, as a faster and more sentiment-driven market, is pricing in a macroeconomic turn that equities have not yet acknowledged.

The logic rests on crypto’s nature as a leading-edge risk asset. Crypto trades 24/7, is dominated by retail and fast-moving capital, and responds to sentiment shifts faster than the slower, institution-heavy equity markets. In this framing, the forces weighing on crypto, the hawkish Fed outlook with markets pricing a high probability of zero rate cuts, the geopolitical risk from Middle East tensions, and the capital rotation toward the AI trade, are real macroeconomic headwinds.

The capital-rotation argument has gained additional support from claims that money has moved toward private AI investments such as SpaceX and Anthropic. In this reading, Bitcoin is not falling because equities are weak; it is falling partly because the strongest speculative capital is chasing opportunities elsewhere.

Crypto is simply reacting to the macro forces first. The stock market, on this view, is complacent, sitting near record highs while ignoring the same risks that crypto is already pricing, and the divergence is a sign that crypto is the canary rather than the anomaly.

If this is correct, the implication is serious: it would mean the crypto crash is an early warning that equities are due for their own repricing, and that the calm in traditional markets is temporary. There is historical precedent for risk assets at the speculative edge turning before the broader market, and crypto’s sensitivity to liquidity conditions makes it a plausible early indicator of tightening financial conditions that have not yet hit stocks. The strong jobs report that crushed rate-cut hopes is exactly the kind of macro shift that would eventually pressure equities too, and crypto may simply have reacted to it faster and harder.

The counterargument is that crypto has a long history of crashing on its own for its own reasons without predicting anything about equities, and that treating every crypto selloff as a macro omen is a pattern that mostly generates false alarms. Crypto’s higher volatility and internal leverage mean it moves more for endogenous reasons, so a crypto crash is far more often just a crypto crash than a leading indicator of a stock market turn.

The front-running thesis is plausible and worth taking seriously precisely because the macro headwinds are genuine, but it is also the kind of narrative that feels compelling in the moment and is usually wrong about timing. The truthful assessment is that crypto could be front-running a macro turn, but the base rate for “crypto crash predicts stock crash” is low, so this explanation should be held as a real possibility rather than a confident forecast.

What the decoupling actually tells us

Stepping back, the most durable lesson of the divergence is not which explanation wins but what the decoupling reveals about crypto’s nature in 2026.

For years, the dominant narrative was that crypto had become “just another risk asset,” moving in lockstep with tech stocks and the Nasdaq, its independence eroded by institutional adoption and ETF integration. The June selloff complicates that story. A market that crashes $250 billion while stocks sit at record highs is not moving in lockstep with anything.

The decoupling demonstrates that crypto retains a distinct market structure, driven by internal forces, leverage cascades, ETF flows, sentiment shifts, and crypto-specific catalysts like the Saylor sale, that can override its correlation with traditional markets entirely. Crypto is correlated with equities until it is not, and the moments when the correlation breaks are revealing: they show that crypto’s own plumbing, especially its leverage, can dominate everything else.

This cuts in a counterintuitive direction for the maturation narrative. The institutionalization of crypto through ETFs was supposed to make it more stable and more tightly integrated with traditional finance. But the June crash shows that integration is partial and conditional. ETF flows became a major driver, yes, but the underlying market still carries the leverage and sentiment-driven fragility that produces violent, isolated moves.

Crypto in 2026 is a hybrid: institutionalized enough that ETF flows move it, but still crypto-native enough that a leverage cascade can crater it while the institutions’ other holdings sit calm. The decoupling is the proof that the old crypto market structure did not disappear under the institutional veneer; it is still there underneath, capable of taking over.

The practical takeaway for anyone trying to read crypto is to resist the reflexive “risk-off” explanation when crypto falls in isolation. When crypto crashes and stocks do not, the cause is almost certainly something internal to crypto, leverage, flows, or a specific catalyst, rather than a broad macro event, because a broad macro event would show up in stocks too.

The June 2026 crash was, on the best available evidence, primarily a crypto-native leverage shakeout, amplified by ETF outflows and a hostile macro backdrop, with large players plausibly exploiting the cascade at the margins and a live but unproven possibility that crypto is front-running a turn equities have not priced.

What it was not is a simple case of crypto following the stock market down, because the stock market did not go down. That single fact, crypto crashing alone while equities held their highs, is the most important thing the selloff revealed, and it says crypto is still its own animal, integrated with traditional finance but not yet tamed by it.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

For the first time, the United States housing system is preparing to count your Bitcoin as a real asset when you apply for a mortgage, without making you sell it first.

Summary

- Fannie Mae and Freddie Mac are moving toward recognizing verified crypto holdings in mortgage risk assessments.

- Eligible borrowers may keep their Bitcoin instead of selling it and triggering a potentially taxable transaction.

- Crypto is initially expected to count as mortgage reserves, not replace the cash required for closing costs.

- Exchange custody, valuation haircuts, and limits on crypto reserves remain important restrictions for borrowers.

The shift traces to a directive from Federal Housing Finance Agency Director William Pulte, who ordered Fannie Mae and Freddie Mac, the government-sponsored enterprises that guarantee the majority of America’s roughly 51 million mortgages, to prepare proposals for treating cryptocurrency as an asset in single-family mortgage risk assessments.

The key phrase is “without conversion to U.S. dollars.” Until now, a borrower with a hundred thousand dollars in Bitcoin had to liquidate it, triggering a taxable event and surrendering future upside, before a lender would count a cent of it. Under the new framework moving through implementation in 2026, verified crypto holdings could strengthen a mortgage application while the borrower keeps the coins. It has been called a revolutionary moment that could change homeownership forever.

It is also narrower, more conditional, and more complicated than the headlines suggest. This piece explains what the order actually does, how it would work in practice, the catches that matter, and what it really means for crypto holders who want to buy a home.

What the order actually says

Start with the precise language, because the details define both the promise and the limits.

The directive came from William Pulte, Director of the Federal Housing Finance Agency, the regulator that oversees Fannie Mae and Freddie Mac and that also installed Pulte as chairman of both companies’ boards. The order instructs each enterprise to “prepare a proposal for consideration of cryptocurrency as an asset for reserves in their respective single-family mortgage loan risk assessments, without conversion of said cryptocurrency to U.S. dollars.” Pulte framed it in explicitly political terms, tying it to President Trump’s stated goal of making the United States “the crypto capital of the world,” and adding that he wanted “people who own cryptocurrency to be able to buy homes like everyone else.”

The significance starts with who Fannie Mae and Freddie Mac are. These two government-sponsored enterprises do not lend directly to homebuyers. Instead, they buy mortgages from the lenders who originate them, bundle those loans into securities, and guarantee payments to investors, which provides the liquidity that keeps the mortgage market functioning. Because they guarantee the majority of U.S. mortgages, their underwriting rules effectively set the standard for what the entire conventional mortgage market will accept. When Fannie and Freddie change what counts as a qualifying asset, lenders across the country follow, because loans have to conform to GSE guidelines to be sold to them. So a change at this level is not a niche product tweak. It is a change to the rules of the largest mortgage market on earth.

The order marks the first formal step toward integrating digital assets into the GSEs’ underwriting frameworks. That framing, “first formal step,” is important and easy to lose in the excitement. This is a directive to prepare proposals, the opening move in a process, not a finished, live mortgage product on day one. By 2026 that process has advanced from the initial order into implementation, with the enterprises drafting guidelines and some lenders beginning to experiment, but it is an evolving framework rather than a switch that flipped overnight.

What actually changed: the “no conversion” breakthrough

To understand why this matters, you have to understand the old rule it replaces, because the entire significance is in one specific change.

Under the pre-existing guidelines, cryptocurrency was effectively invisible to mortgage underwriting unless it stopped being cryptocurrency. Fannie Mae’s selling guide required that any virtual currency a borrower wanted to use for qualifying, whether for the down payment, closing costs, or asset reserves, had to be liquidated into U.S. dollars first. The dollars then had to be “sourced and seasoned,” meaning documented as sitting in a bank account for a period of time, before they counted. In practical terms, your Bitcoin counted for nothing to a mortgage application until you sold it and parked the proceeds in a bank.

That requirement carried real costs that went beyond inconvenience. Selling crypto to qualify for a mortgage triggers a taxable event, potentially generating capital gains taxes on appreciated holdings. It forces the holder to surrender any future upside on assets they believed in enough to accumulate. And it exposes them to timing risk, having to sell at whatever the market price happens to be when they apply. For a crypto holder, the old rule said, in effect: you can use this wealth to buy a home, but only by giving up being a crypto holder.

The new framework changes exactly this. Under the directive, verified crypto holdings can be counted as reserves without conversion to dollars. The borrower keeps the coins, avoids the taxable sale, retains the upside, and still gets credit for the assets in the underwriting calculation. This is the breakthrough, and it is meaningful: it recognizes cryptocurrency as a legitimate store of wealth that can sit on a borrower’s financial statement the way stocks, bonds, and retirement accounts do, rather than treating it as something that has to be cashed out to be real. For someone whose net worth is substantially in Bitcoin or Ethereum, that is the difference between their wealth helping them qualify and being invisible.

How it would actually work

The mechanics matter, because the order does not make crypto equivalent to cash, and the conditions attached shape who actually benefits.

The most important practical point is the role crypto plays. The directive is about counting cryptocurrency as reserves, the financial cushion lenders want to see proving a borrower can keep paying the mortgage if their income is interrupted. This is distinct from using crypto directly for the down payment or closing costs, which still generally requires actual dollars that have to be sourced and seasoned. So the realistic near-term picture is not “pay for your house in Bitcoin.” It is “your Bitcoin holdings strengthen your financial profile and reserve position, helping you qualify, while you still need dollars for the actual cash to close.” That is a real benefit, especially for self-employed or crypto-wealthy borrowers whose assets are strong but whose documented income or liquid cash might otherwise fall short, but it is narrower than the headline implies.

Three conditions attach to which crypto counts. First, only assets on regulated exchanges qualify: the crypto must be evidenced and stored on a U.S.-regulated centralized exchange subject to applicable laws, so holdings on platforms like Coinbase count while other arrangements may not. Second, risk-based adjustments apply: because crypto is volatile, the GSEs are directed to apply additional risk mitigation, which in practice means haircuts. Where stocks might get a modest discount to account for market swings, crypto could face a much larger buffer, so a hundred thousand dollars in Bitcoin might be counted as only sixty or seventy thousand in reserves. Third, limits on the share of reserves: the proposals are directed to limit the portion of total reserves that can be composed of cryptocurrency, so a borrower cannot rely on crypto alone.

The honest framing, as some mortgage analysts have noted, is that even in the best case crypto is unlikely to be treated more favorably than stocks and bonds, and probably a bit less favorably given the volatility haircuts. It will not be easier than the treatment of traditional securities, and that makes sense, because it would be strange to give a volatile asset better treatment than a stable one. The realistic outcome is that crypto becomes a recognized but discounted asset class in underwriting, counted with wider guardrails than traditional holdings, which is still a major step up from being counted at zero.

The self-custody controversy

The condition that crypto must sit on a regulated exchange has provoked the sharpest criticism, and it exposes a genuine philosophical tension at the heart of the order.

The requirement is that eligible crypto be stored on a U.S.-regulated centralized exchange. The logic is verification: regulators and lenders want to be able to confirm the borrower actually owns the assets, and holdings on a regulated, KYC-compliant exchange are easy to verify through statements and account records. From an underwriting standpoint, that is a reasonable instinct. Lenders need documentary proof of assets, and a regulated exchange provides a familiar paper trail.

But it cuts against one of cryptocurrency’s foundational principles, and self-custody advocates have pushed back hard. Nick Neuman, CEO of the self-custody provider Casa, called the exchange requirement a mistake, arguing that self-custody is fundamentally about property rights, which are a core American value. His technical point is that the verification concern is solvable without forcing custody onto exchanges: thanks to cryptography, it is trivial to prove that assets held in self-custody are owned by a given individual, through cryptographic signatures that demonstrate control of the wallet without surrendering it. In other words, the order assumes that only exchange-held assets can be verified, when in fact self-custodied assets can be verified too, just by a different method that the framework does not yet accommodate.

The criticism matters beyond ideology, because a large share of serious, long-term crypto holders deliberately self-custody precisely to avoid exchange risk, the lesson hammered home by years of exchange failures. The exchange-only requirement therefore excludes exactly the cohort most committed to crypto as a long-term store of wealth, the people most likely to have substantial holdings they have held for years. It is a meaningful gap, and the hope among advocates is that the framework evolves to recognize cryptographic proof of self-custodied holdings, allowing the housing system to be forward-thinking enough to accommodate how committed holders actually store their assets. For now, though, the rule rewards keeping your crypto on an exchange, which sits in tension with the security practices the crypto community spent years promoting.

What it really means for crypto holders

Pulling it together, the order is significant, but its significance is best understood by separating what it does from what the headlines imply.

What it does, concretely: it establishes for the first time that the U.S. conventional mortgage system will recognize cryptocurrency as a legitimate asset class in underwriting, counted without forcing a sale. For a crypto holder applying for a mortgage, that means holdings on a regulated exchange can strengthen the reserve position and overall financial profile, improving the odds of qualifying, without the tax hit and lost upside of liquidating. For borrowers whose wealth is concentrated in crypto, which includes many in the industry, that removes a real barrier that previously made their assets invisible to lenders. It is a legitimization milestone, crypto taking a seat at the table alongside stocks and bonds in one of the most conservative corners of American finance.

What it does not do: it does not let you buy a house with Bitcoin in the literal sense, it does not treat crypto as favorably as cash or even as favorably as stocks, it does not count self-custodied holdings, and it did not happen all at once. The realistic version is that crypto becomes a recognized but heavily caveated asset for reserves, subject to volatility haircuts, exchange-custody requirements, and limits on what share of reserves it can comprise. The transformation is real but incremental, an opening of the door rather than a wide-open entrance.

The broader meaning is the most durable point. This is part of a wider 2026 trend of cryptocurrency being woven into the traditional U.S. financial system, alongside the spot ETFs, the advancing regulatory frameworks, and the growing institutional infrastructure. Having the entities that guarantee over half of U.S. mortgages prepare to count crypto as an asset is a profound signal of legitimization, regardless of how narrow the initial mechanics are. It says the housing system, perhaps the most important wealth-building institution in American life, now considers cryptocurrency a form of wealth worth recognizing. For a holder, the practical advice is to temper the excitement with the details: keep records, understand that exchange custody is currently required, expect volatility haircuts, and recognize that crypto will strengthen an application rather than replace the need for documented income and actual dollars to close. The door is opening. It is just opening at the measured pace that the most conservative part of the financial system always moves, and that it is opening at all is the real story.

This article is for informational purposes and does not constitute financial, investment, tax, or mortgage advice. Cryptocurrency markets are highly volatile and mortgage rules vary by lender and circumstance. The figures and analysis described reflect data available as of June 2026. Always do your own research and consult with qualified financial and mortgage professionals before making decisions.

HTX has delisted USD1, the stablecoin issued by Trump-linked World Liberty Financial, after the exchange said WLFI froze certain on-chain addresses linked to the platform.

Summary

- HTX removed USD1 after wallet addresses linked to the exchange were frozen.

- World Liberty Financial cited sanctions compliance controls.

- HTX said user USD1 balances will convert to USDT at a 1:1 rate.

- The move adds to Justin Sun’s dispute with the Trump-linked crypto project.

The exchange, associated with crypto entrepreneur Justin Sun, said the freeze limited the movement of assets tied to those addresses. HTX said it removed USD1 to protect user assets and reduce trading risk.

HTX removes USD1 after wallet freeze

HTX said World Liberty Financial “unilaterally imposed a freeze” on specific HTX on-chain addresses following sanctions compliance checks.

The exchange said the action restricted circulation of some WLFI-linked assets. It also said the freeze came without enough prior communication, clear legal basis, or due process.

HTX has suspended USD1 deposits and conversion services. It also halted trading for WLFI/USDT, USD1/USDT, BTC/USD1, and ETH/USD1 pairs.

The exchange said eligible USD1 balances will be converted into Tether’s USDT at a 1:1 rate. HTX said more details on timing will be shared separately.

World Liberty cites sanctions controls

World Liberty Financial has not publicly confirmed whether it froze HTX-linked addresses.

The project posted on X that “in light of recent sanctions updates, World Liberty Financial maintains risk-based sanctions compliance controls.”

The dispute follows UK sanctions announced on May 26 against Huobi Global S.A., formerly linked to the HTX brand. UK authorities said they had grounds to suspect the entity supported Russia through financial services.

HTX rejected the link to its current online exchange. It said Huobi Global S.A. is separate from the operating HTX platform and should not affect users.

Justin Sun dispute adds pressure

The USD1 delisting adds another layer to the public fight between Justin Sun and World Liberty Financial.

As previously reported by crypto.news, Sun and World Liberty have been locked in a legal dispute after WLFI froze Sun’s tokens. Sun sued the project in April, claiming his assets were frozen and threatened without proper reason.

World Liberty later sued Sun for defamation. The project claimed he made false statements and broke WLFI token sale rules through alleged transfers, short-selling, and straw purchases.

Sun has been linked to HTX and has served on its global advisory board. The exchange has said it may seek legal remedies to protect user rights.

USD1 faces fresh trust test

USD1’s removal from HTX comes at a difficult time for stablecoin issuers and crypto exchanges. The case shows how compliance actions can quickly affect token access, trading pairs, and user balances.

The stablecoin had gained attention because of its link to World Liberty Financial, a project tied to U.S. President Donald Trump and his family. Donald Trump, Donald Trump Jr., Eric Trump, and Barron Trump are listed as advisers.

HTX said its main goal is to protect users while asking WLFI to reverse the freeze. For now, USD1 trading on HTX remains suspended, and users must wait for the exchange’s conversion update.

US lawmakers are urging Congress to confront AI-driven job losses, warning that automation could displace workers as layoff data and blunt warnings from bank chiefs intensify pressure.

Senators Elizabeth Warren and Bernie Sanders led the latest calls.

Warren and Sanders Push Washington for Protections

Warren said Congress cannot wait years to measure layoffs before acting, arguing workers need protection now.

Follow us on X to get the latest news as it happens

Sanders went further, blaming industry money for the stalemate.

“Is Congress doing anything to help the millions of workers who could lose their jobs to AI and robotics? No. They’re intimidated by the hundreds of millions the AI industry is pouring into super PACs. We must ban super PACs and crack down on corruption,” he said.

The concern crosses party lines. Republican Senator Josh Hawley has put jobs at the center of his warnings about AI. He cited an Economist report that nearly one in five US workers expect AI or automation to take their jobs.

Hawley argued that such fear should not be brushed aside with promises of long-term gains.

“That anxiety deserves to be taken seriously, not glossed over with promises of long-term benefits. It’s true that the economy is not zero-sum—automation of human labor in some domains might open up opportunities in others,” he wrote.

AI Layoffs Rise as Banks Signal Deeper Cuts

The warnings come as new data showed AI behind 38,579 US job cuts in May, the highest monthly total since tracking began. For the year, employers have tied 87,714 cuts to AI. That total already tops the 54,836 blamed on the technology in all of 2025.

The pressure now reaches various sectors. JPMorgan’s Jamie Dimon has said AI will eliminate jobs, and Citigroup’s Jane Fraser expects some roles to become unnecessary.

According to Debasish Patnaik of QuantumBlack AI unit, banks are reducing junior analyst classes by as much as two-thirds.

BeInCrypto reported that Standard Chartered plans to cut more than 15% of corporate function roles by 2030 as AI use rises. Meanwhile, customer service also sits directly in the path now.

Not everyone shares the alarm. Andreessen Horowitz partner David George has rejected the AI job apocalypse as a myth. Economist Tyler Cowen makes a similar case.

He says AI lets small teams accomplish far more than before. That shift, he argues, should spawn more companies, projects, and nonprofits.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post AI Job Displacement Concerns Pushes US Senators to Demand Action appeared first on BeInCrypto.

Bitcoin spent Sunday evening, June 7, trading as a real-time diplomatic scoreboard. Israel struck sites in south Beirut linked to Hezbollah, the Iran-backed militant group active in Lebanon, killing two people and injuring at least 20.

Iran’s Islamic Revolutionary Guard Corps (IRGC) retaliated with what it called “warning strikes,” saying Israel should stand down or face a broader wave. Bitcoin reacted immediately, slipping from $62,000 to $61,200, before the move reversed. Then Trump responded, moving the markets.

Trump Overrules Netanyahu on the Iran Timeline

In an interview on Sunday evening, Trump left no room for ambiguity. “I call the shots. I call all the shots. He doesn’t call the shots,” Trump said, referring to Israeli Prime Minister Benjamin Netanyahu.

On the same evening, Trump said Netanyahu “won’t have any choice” but to accept whatever agreement Washington reaches with Iran.

He confirmed he called Netanyahu directly to urge him not to retaliate, said he was “not happy” with Israel’s strikes, and noted the attacks were not coordinated with the US.

Trump added that the deal was “almost complete” and expected to be announced at the start of the new business week.

When Trump’s diplomatic momentum last moved Bitcoin above $74,000, the market has consistently treated his deal-making language as a near-term price catalyst.

What the Bitcoin Iran Spike Actually Means

Bitcoin is trading roughly $20,000 below its mid-May peak of $82,000, with geopolitical pressure and rising Fed hike expectations driving almost the entire decline.

Sunday’s 5% spike in response to Trump’s remarks showed the market reading his language as different from previous peace optimism.

This time, it feels less like a ceasefire rumor and more like a direct statement that the US president intends to conclude this deal, with or without Israel’s cooperation.

The recovery from the $82,000 high tracks almost exactly with the collapse in ceasefire confidence since mid-May.

If Trump delivers more towards a peace deal on Monday, June 8, the price move so far could be the preview. As BeInCrypto’s coverage of previous ceasefire rallies showed, confirmed deals move Bitcoin significantly further than the diplomacy itself.

Trump has set his own deadline. The market will open on Monday, watching whether he delivers.

The post Bitcoin Price Jumped 5% as Trump Tells Israel “I Call the Shots” appeared first on BeInCrypto.

Bitcoin pulled back from Sunday highs as renewed military conflict between Iran and Israel sent Asian stocks, including South Korea’s Kospi index, sharply lower.

The leading cryptocurrency by market value traded at around $62,900 at 4:00 UTC, having hit a high of $63,776 late Sunday, according to data source CoinDesk.

WTI crude oil futures jumped over 3% to $93.50 as Iran and Israel traded airstrikes, ending the recent fragile ceasefire that had calmed energy markets. U.S. President Donald Trump called for restraint and said he has requested Israeli Prime Minister Benjamin Netanyahu “not to retaliate”.

“I am going to call Bibi right now and tell him not to retaliate,” he told Axios in a telephonic interview. “Israel had its strike and Iran had its strike. We don’t need another one.”

Still, Asian equity markets took a beating, with South Korea’s KOSPI falling over 6.8%, prompting a temporary trade halt amid volatile conditions. Japan’s Nikkei index also fell over 3%.

The latest spike in oil prices could only add to the upward momentum in the U.S. Treasury yields, which surged Friday following the release of the blowout monthly U.S. jobs report. Hardening of Treasury yields typically boosts demand for the dollar and dollar equivalents and weighs over riskier assets like cryptocurrencies.

Bitcoin has already taken a beating for several reasons, including Strategy’s BTC sale, the AI stock frenzy, and the exodus of capital from spot bitcoin ETFs. Prices fell nearly 14% last week, briefly penetrating the $60,000 mark.

Volatility could remain high this week as geopolitical tensions, coupled with key data releases such as U.S. inflation and major IPOs like SpaceX and Anthropic, are likely to influence liquidity dynamics.

Robin Van Persie sacked by Feyenoord after just 16 months in charge

All the Trailers From Xbox Games Showcase 2026

Monaco Grand Prix: Harry Benjamin’s driver ratings as Kimi Antonelli wins again

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Evereve – Corporette.com

-

Business6 days ago

Business6 days agoJade Biosciences, Inc. (JBIO) Discusses Positive Interim Results From JADE101 Phase I Healthy Volunteer Study and Development Plans Transcript

-

Crypto World3 days ago

Crypto World3 days agoJensen Huang Approves Samsung, SK Hynix, and Micron for NVIDIA (NVDA) HBM4 Memory Supply

-

Sports5 days ago

Sports5 days agoFrench Open 2026 results: Alexander Zverev beats Rafael Jodar and will play Jakub Mensik in semi-finals

-

Tech6 days ago

Tech6 days agoCryZENx Releases Fresh Playable Content Deep Inside Jabu-Jabu for His Ocarina of Time Remake

-

Business5 days ago

Business5 days agoTrump Taps Housing Chief Bill Pulte as Acting Intelligence Director After Gabbard Exit

-

Business1 day ago

Business1 day agoThe Pain Points Taking a Fragile Tech Rally Down a Notch

-

Crypto World3 days ago

LBank Surpasses 25 Million Users Worldwide as AFA Partnership Continues to Drive Global Growth

-

NewsBeat5 days ago

NewsBeat5 days agoRepublicans balk at Trump’s attempt to appoint a MAGA enforcer to lead National Intelligence

-

Tech3 days ago

Tech3 days agoRCS Messages Between iPhone and Android Get End-to-End Encryption With iOS 26.5

-

Crypto World6 days ago

Crypto World6 days agoSeagate (STX) Stock Surges to Record High on AI Boom and Legal Settlement

-

Tech3 days ago

Tech3 days agoMicrosoft launches MXC, an OS-level sandbox for AI agents, with OpenAI and Nvidia already on board

-

Tech3 days ago

Tech3 days agoMeta steals a tactic from Tesla and builds data centers in tents

-

Crypto World5 days ago

Crypto World5 days agoEU AI Data Center Project Faces Delays as Funding Gaps Grow

-

Entertainment5 days ago

Entertainment5 days agoDid The Mandalorian And Grogu Already Ruin The Next Star Wars Movie?

-

Business5 days ago

Business5 days agoAehr Test Systems Stock Soars 17% Amid Surging AI Demand and Conference Spotlight

-

Crypto World3 days ago

Crypto World3 days agoMerlin (MRLN) Stock Soars 32% on Major USSOCOM Autonomy Milestone

-

Business6 days ago

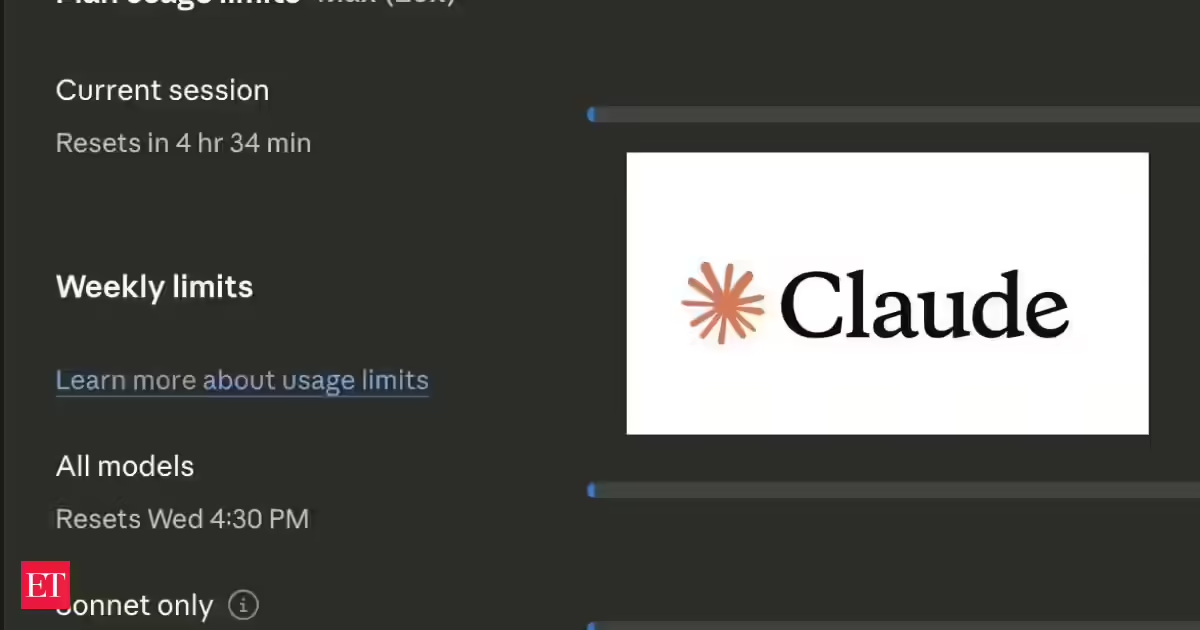

Business6 days agoClaude AI Down Today Reason: Why Anthropic’s AI is not working today? What’s the latest quota update

-

Business1 day ago

Business1 day agoCryptos Could Be Casualties of SpaceX IPO as Bitcoin Hits Lowest Price Since 2024

-

Tech5 days ago

Tech5 days agoInstagram will stop bombarding teens with the same kind of obsessively unhealthy content

You must be logged in to post a comment Login