Crypto World

Tether Gold Expands to BNB Chain as Tokenized Gold Market Approaches $5 Billion

The integration connects the dominant gold-backed token to BNB Chain’s RWA ecosystem amid a volatile stretch for spot gold prices.

Tether announced Wednesday that its tokenized gold product, XAU₮, is now available on BNB Chain, expanding the token’s reach to the third-largest decentralized finance (DeFi) ecosystem by total value locked (TVL).

Each XAU₮ token represents one fine troy ounce of physical gold held in Swiss vaults as a London Good Delivery bar. The token is issued by TG Commodities under El Salvador’s Digital Asset Issuance Law.

The move comes at a turbulent moment for gold markets. Spot gold is trading at roughly $4,400 per ounce, well below its all-time high of approximately $5,589 hit in January but still sharply higher year-over-year. Gold surged 64% in 2025, its largest annual gain in 40 years, as investors piled into safe-haven assets amid geopolitical tensions and trade uncertainty.

That rally fueled explosive growth in tokenized gold. The sector crossed $4 billion in market value in January, though the sector remains dominated by just two products, XAU₮ and PAXG, which control more than 95% of the market.

BNB Chain’s RWA Play

The expansion positions BNB Chain to capture more real-world asset activity.

Nina Rong, executive director of growth at BNB Chain, said the integration “extends what is already the second-largest RWA ecosystem by TVL” and gives users “a trusted, gold-backed asset they can use across DeFi without friction.”

Tether also said it has integrated XAU₮ via the USDT0 network, a cross-chain infrastructure layer that enables unified liquidity across blockchains.

Growing Competition

The listing comes as the tokenized gold sector faces growing scrutiny over its concentrated structure. The World Gold Council recently proposed shared infrastructure for tokenized gold products, arguing that the high barriers to entry, including the need to independently build custody relationships, compliance pipelines, audit frameworks, and redemption logistics, limit competition and hamper fungibility.

New entrants are also challenging the duopoly. In January, DeFi protocol Theo launched a yield-bearing tokenized gold product called thGOLD, designed to generate returns on idle gold exposure, something neither XAU₮ nor PAXG currently offers natively.

“People understand gold. They trust it because it has held value for millennia,” said Tether CEO Paolo Ardoino. “With XAU₮, we are not changing what gold is; we are making it usable in a modern financial system.”

A viral warning from economist Peter St. Onge has spotlighted how an 89–10 Senate housing bill quietly folds in a temporary CBDC ban and reshapes the path for the CLARITY Act.

Summary

- Economist Peter St. Onge’s post warning that a CBDC provision is buried inside a must-pass housing bill drew nearly 196,000 views on X in under three hours.

- The U.S. Senate passed the 21st Century ROAD to Housing Act on March 12 with an 89–10 vote, embedding a ban on Federal Reserve-issued digital dollars through 2031.

- The bill must still pass the House, where Republican lawmakers are pushing for a permanent CBDC ban rather than the temporary prohibition in the Senate version.

A viral alarm from Heritage Foundation economist Peter St. Onge is reigniting one of crypto’s most contested political fights in Congress: the prospect of a U.S. central bank digital currency. In a post on X that amassed 195,700 views and 3,600 likes by the afternoon of March 26, @profstonge warned that “Congress is trying to sneak a CBDC into their must-pass housing bill,” adding that such a currency “would replace the US dollar with a government-controlled crypto-token that 80% of voters reject.”

The bill in question, the 21st Century ROAD to Housing Act, passed the Senate on March 12 by an overwhelming 89–10 margin. As reported by Yahoo Finance, the legislation is primarily a sweeping housing reform package crafted by Senate Banking Committee Chairman Tim Scott and Senator Elizabeth Warren, covering everything from FHA loan limits to institutional investor restrictions on single-family homes. Buried within it, however, is Title X — a provision that bars the Federal Reserve and its regional banks from issuing or creating a digital dollar, or any asset substantially resembling one, through 2031.

The inclusion was not accidental. According to Unchained Crypto, House conservatives pushed to embed anti-CBDC language into the legislation as a condition of broader bipartisan compromise, a strategy that allowed digital currency policy to advance without requiring a standalone crypto bill. The White House signaled support for the measure, with advisors recommending the president sign it if presented in its current form.

The CBDC Provision Dividing Washington

The debate cuts across party lines in ways that complicate easy narratives. While the Senate version imposes a ban through 2031, some House Republicans are pushing for a permanent prohibition, arguing that a time-limited restriction simply kicks the problem down the road. At the same time, critics on the left have argued the provision has no place in a housing bill and could muddy what should be a straightforward affordability package.

Wall Street commentator @WallStreetMav added another layer of skepticism in a separate post on X that drew 92,000 views, writing that “Republicans aren’t banning CBDCs, they’re redesigning them. Same surveillance, same control, just routed through banks so Wall Street gets its cut.” The post, which framed the compromise as a “revenue-sharing agreement” rather than genuine reform, accumulated 873 likes and 357 retweets within hours.

The housing bill CBDC fight arrives alongside a parallel battle over the CLARITY Act, the digital asset market structure legislation that has stalled in the Senate over a separate stalemate on stablecoin yield. Coinbase withdrew support for an earlier CLARITY Act draft after proposed language would have banned passive yield on stablecoins — a provision the exchange said was worse than the status quo. Senator Cynthia Lummis has since said sticking points on stablecoin yield and DeFi provisions are “largely reached,” framing April 2026 as a critical legislative window.

A Temporary Ban or a Political Signal?

For CBDC opponents, the housing bill provision is less about the technical details of digital currency design and more about drawing a political line before midterm elections. As Ledger Insights noted, the ban expires at the end of 2030 — after Trump leaves office — leaving the door open for a future administration. The Federal Reserve, for its part, has consistently maintained it would not launch a digital dollar without explicit congressional authorization, framing its existing research as exploratory rather than developmental.

Whether the CBDC provision survives a House-Senate conference process remains uncertain. House leaders have already indicated they are unlikely to accept the Senate version of the housing bill as written and may seek to renegotiate key provisions — including how long, and how broadly, any CBDC ban applies. As crypto.news previously reported, the Senate vote drew rare cross-aisle alignment, but that consensus may face pressure once negotiations with the House begin in earnest.

NYSE CPO Jon Herrick says blockchain should plug into existing rails like central clearing, as ICE’s OKX deal and SEC moves on tokenized stocks redraw market structure.

Summary

- NYSE Chief Product Officer Jon Herrick said at the New York Digital Assets Summit on March 26 that the exchange’s strategy centers on blockchain “interoperability” with existing market infrastructure, not wholesale replacement of it.

- Herrick emphasized that legacy mechanisms like central clearing retain irreplaceable risk management value and predicted the boundary between traditional and tokenized assets could disappear within the next decade.

- The comments land weeks after NYSE parent Intercontinental Exchange (ICE) made a strategic investment in crypto exchange OKX at a $25 billion valuation, with plans to offer NYSE tokenized equities to OKX’s 120 million users.

NYSE Chief Product Officer Jon Herrick on March 26 told the audience at the New York Digital Assets Summit that the world’s largest stock exchange has no intention of tearing down its existing market infrastructure to make way for blockchain — it intends to wire the two together. According to CoinDesk, Herrick said the NYSE is pursuing interoperability, exploring the application of tokenized assets within the current system, including real-time or near-real-time settlement and extended trading hours.

The position is a meaningful signal. NYSE is the most systemically significant equities venue on the planet, and Herrick’s framing — blockchain layered onto existing rails, not substituted for them — reflects how the exchange is navigating the practical and regulatory constraints of one of the most tightly supervised industries in finance. He noted that existing mechanisms such as central clearing still carry irreplaceable risk management value and should be preserved, even as the exchange pushes deeper into tokenization. As previously reported by crypto.news, the NYSE is already building a 24/7 blockchain-based trading venue for tokenized stocks and ETFs, pending SEC approval. The platform is designed to combine NYSE’s Pillar order-matching engine with blockchain-based post-trade settlement funded by stablecoins.

Herrick predicted that the boundary between traditional and tokenized assets may gradually dissolve over the next decade — a timeline that aligns with where institutional momentum is visibly heading. Morgan Stanley, as detailed in a previous crypto.news story, plans to enable tokenized stock settlement on its internal alternative trading system in the second half of 2026, while Nasdaq has already filed with the SEC to support tokenized equities on its public exchange.

ICE doubles down with OKX investment

The strategic backdrop to Herrick’s remarks is considerable. Earlier this month, ICE — NYSE’s parent company — made a strategic investment in OKX, valuing the crypto exchange at $25 billion and securing a board seat, as covered in a previous crypto.news story. Under the partnership, subject to regulatory approval, OKX’s 120 million users would gain access to ICE’s U.S. futures markets and NYSE tokenized equities. “Our strategic relationship with OKX will expand global retail access to ICE’s pre-eminent regulated markets and accelerate our plans to offer on-chain infrastructure and tokenized assets to U.S. investors,” said Jeffrey C. Sprecher, Chair and CEO of ICE, at the time of the announcement.

A market structure being redrawn

The tokenized equity market reached a market cap of roughly $800 million and $1.8 billion in monthly volume as of early 2026, still nascent by Wall Street standards but growing fast. The regulatory environment has also shifted: the SEC granted the DTCC a three-year window in late 2025 to custody tokenized securities, effectively clearing a path for broker-dealers to connect to on-chain settlement without abandoning the existing market structure.

Herrick’s interoperability-first philosophy — bridging old and new rather than replacing one with the other — may well prove to be the dominant model for how legacy exchanges absorb blockchain over the decade ahead.

U.S. Representative Maxine Waters, the ranking Democrat on the House Financial Services Committee, is questioning the limited “master account” obtained by crypto exchange Kraken from the Federal Reserve Bank of Kansas City, which she said raises potential consumer-protection issues and questions about the approval process.

Waters, who is likely to return to the chairman seat on the committee if the Democrats regain a House majority in this year’s elections (set at an 84% chance in current bets on Polymarket), sent a Thursday letter to the president of the Kansas City arm of the Fed system, Jeff Schmid. She suggested that the unusual approval for a “limited purpose account” at Kraken, which allows the firm to become the first to win direct access to Federal Reserve payment services, is on unclear legal footing.

“The announcement raises questions about the approval because neither statute nor the Federal Reserve Board’s Account Access Guidelines refer to a ‘limited purpose account’ type,” she wrote in the letter. “Accordingly, I write to request that you clarify the terms of Kraken’s account access approval and provide additional information regarding the process and considerations informing the approval.”

The new account granted the U.S. firm full-fledged access to the same payment rails that much of the traditional financial system operates on. Several crypto-native firms have sought that access but are still awaiting approval, keeping a close eye on a separate effort at the Federal Reserve Board in Washington to write rules that could govern a “skinny” master account for such businesses. That process is still in the early stages.

When the Kansas City Fed was asked to comment on Waters’ queries, a spokesman said the bank has “received the letter and will review it.”

The regional bank in Kansas City — one of the 12 such banks nationwide — announced earlier this month that Kraken would get the long-sought-after access. Schmid said at the time that his bank was trying to maintain a system that “supports a level competitive field and reinforces the stability and resilience that has underpinned the Federal Reserve’s payment system offerings throughout its history.”

Read More: Court closes Custodia fight with Federal Reserve just as Fed opens master-account door

The crypto exchange has previously been in the crosshairs of Japanese regulators for offering products and services without the proper registration.

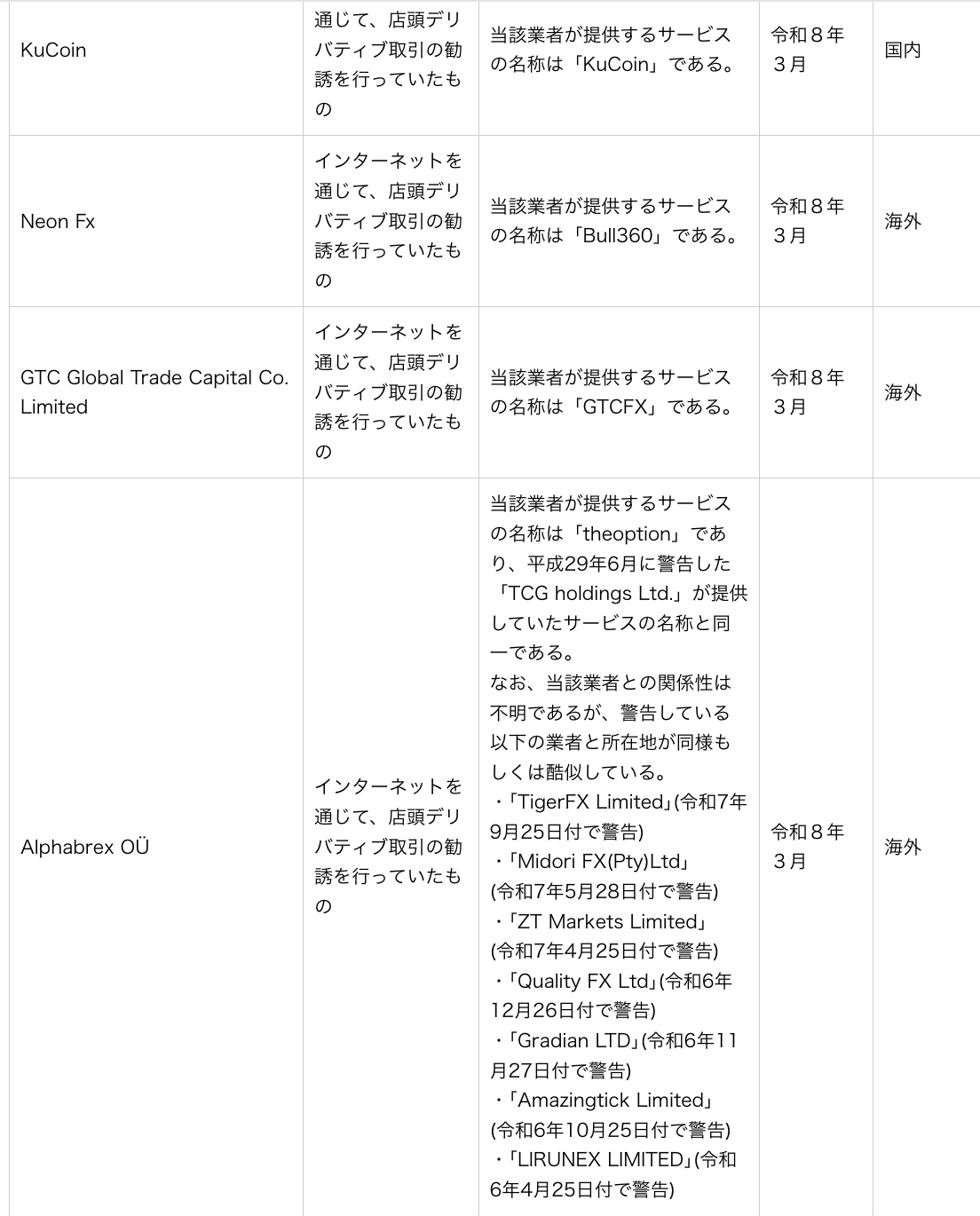

Japan’s watchdog overseeing many activities for cryptocurrency exchanges, has issued warning letters to companies including KuCoin for conducting certain operations without registering, according to a Thursday update from the Financial Services Agency (FSA).

According to the agency’s latest list of entities “conducting financial instruments business without registration,” the FSA said platforms KuCoin, NeonFX, theoption, and GTCFX received a March notice for “soliciting over-the-counter (OTC) derivatives trading via the internet.” Of the four platforms, the FSA listed KuCoin, which is headquartered in the Seychelles, as offering services to Japanese residents, while the others have an international user base.

The FSA issued a similar warning to KuCoin and other exchanges, including Bybit, in November 2024 for offering products and services to Japanese residents without proper registration. In February 2025, the financial watchdog sent requests to Apple and Google for the companies to suspend downloads of KuCoin’s app.

Japan has a high concentration of crypto users. The FSA reported in February 2025 that there were more than 12 million accounts among a population of about 123 million. The country ranked 19th in Chainalysis’s 2025 Global Crypto Adoption Index.

Cointelegraph reached out to KuCoin for comment, but had not received a response at the time of publication.

Related: Austria’s regulator slaps new business ban on KuCoin’s EU exchange

The FSA’s notice comes as the financial watchdog prepares to shift Japan’s legal framework from the country’s Payment Services Act to the Financial Instruments and Exchange Act. The change would significantly alter reporting requirements for initial exchange offerings and token issuers, and provide regulators with greater enforcement authority over unregistered platforms.

Japan’s PM denies involvement in memecoin project

Sanae Takaichi, who has served as the prime minister of Japan since October 2025, publicly denied connections to the “Sanae token” earlier this month after the project grew to a market value of about $28 million before falling sharply. The FSA was reportedly considering an investigation into the matter.

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

Crypto World

Ethereum Price Prediction Turns Bullish Long Term as Pepeto Presents Strongest Odds Before the Binance Listing

Large wallets are stacking ETH at a pace that took the market off guard, with buying address balances going vertical while the Fear and Greed Index hits 10, the lowest reading in 16 months. While the new trend looks good for the ethereum price prediction on a longer timeline, it could take a while before retail sees any returns from it.

This is why smaller entries and presales are growing in popularity. Pepeto is the exchange that raised more than $8 million, but the Binance listing approaching presents a much shorter path to returns when compared to waiting for ETH to clear resistance. Analysts project 100x to 300x, and the entry is still open.

The Fear and Greed Index dropped to 10 on March 26, the worst reading in 16 months, while ETH open interest climbed to multimonth highs as DeFi and AI tokens outperformed BTC, according to CoinDesk.

Bitcoin settled at $68,350 with spot ETF outflows hitting $124 million on March 25, the fifth straight day of redemptions, according to The Block.

The ETH outlook benefits from whale buying during fear, but the exchange already at presale pricing with a Binance listing confirmed is where the compressed returns live before trading opens.

Where the ETH Whale Buying Meets Presale Returns Before the Listing Window Closes

Pepeto

There is no guarantee ETH makes a massive move any time soon. This is exactly why Pepeto and the presale entry present such a valuable opportunity for traders who want control over their timing.

Analysts project 100x to 300x from the current entry, which at $0.000000186 could be the return that changes your position for the rest of the cycle. The exchange pulled in more than $8 million while the correction raged. The risk scorer checks every contract before your capital touches it, PepetoSwap keeps your full position intact at zero fees, and the cross chain bridge moves tokens at zero cost.

Since you can rely on the exchange for daily trading with 193% APY staking compounding early positions while stages fill faster, the adoption path is clear. The SolidProof audit verified every contract, and the developer who created the original Pepe coin reaching $11 billion with the same 420 trillion supply built the exchange alongside a former Binance expert.

Pepeto delivers the ETH forecast crowd a faster answer because the initial move from the listing could be massive, but the exchange itself and the daily use behind it will stay active for years.

Ethereum Price Prediction: Can ETH Clear $2,200 and Start the Run to $2,600?

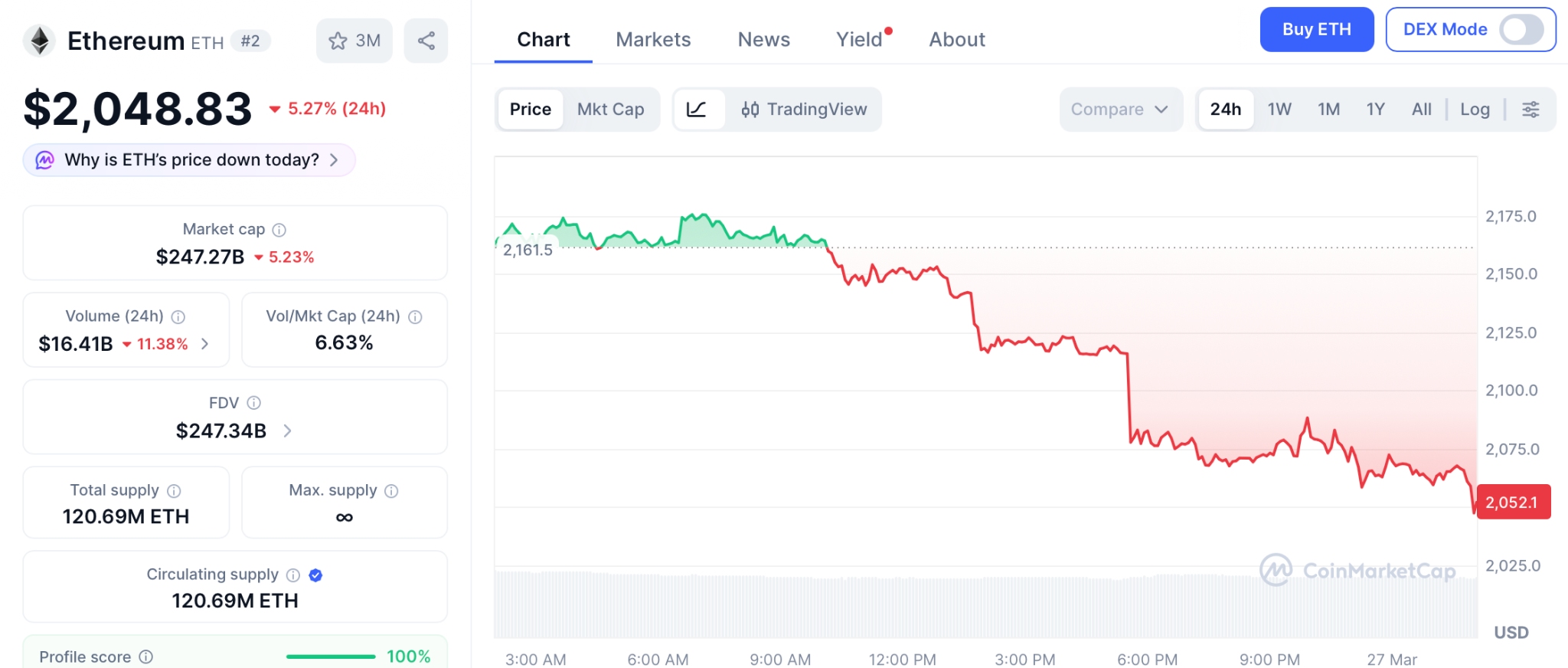

Ethereum trades at $2,048 as of March 27 hovering above $2,000 support with open interest at multimonth highs, according to CoinMarketCap.

The ethereum price prediction depends on clearing $2,100 and the 50 day SMA near $2,200, which opens a run to $2,600 with $3,000 as the stretch target. The setup falls apart if ETH loses $2,000, locking the price between $1,750 and $2,100.

Whale buying addresses going vertical during the correction signals conviction, and Fear and Greed at 10 historically resolves with a sharp recovery 40% of the time. The ETH forecast is structurally bullish for 2026, but the path from $2,048 to $3,000 is a 40% move over many months, not the 100x to 300x the presale compresses into one listing event.

Ethereum Price Prediction Confirms This Is the Second Chance to Be Early and the Reader Can See It Clearly

The ethereum price prediction may not offer fast movement in the short term despite the high probability that a future rally is building underneath. You are waiting for external catalysts to move the chart while the Fear and Greed Index sits at its lowest point in over a year. In contrast, Pepeto already has everything needed to break out on its own terms with more than $8 million raised and a Binance listing confirmed.

The listing date is when the 100x to 300x projections from analysts play out. Last cycle made millionaires out of the wallets that moved first, and this is that same moment with a confirmed listing approaching. The Pepeto official website is where being early this time means you collect what the rest of the cycle talks about.

Click To Visit Pepeto Website To Enter The Presale

FAQs:

What does the ETH buying data mean for the ethereum price prediction?

Whales stacking ETH during fear reduces sell pressure over time and historically precedes big moves, but clearing $2,200 and the 50 day SMA at $2,200 is the trigger.

How does Pepeto compare to the ethereum price prediction timeline?

ETH’s bull case depends on macro conditions clearing resistance gradually. The Pepeto official website is where 100x to 300x from one listing is still at presale pricing with a confirmed date.

What levels does the ethereum price prediction need to break for a rally?

ETH must clear $2,100 and the 50 day SMA at $2,200 to open $2,600 with $3,000 as the stretch target, while losing $2,000 locks it in a range.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

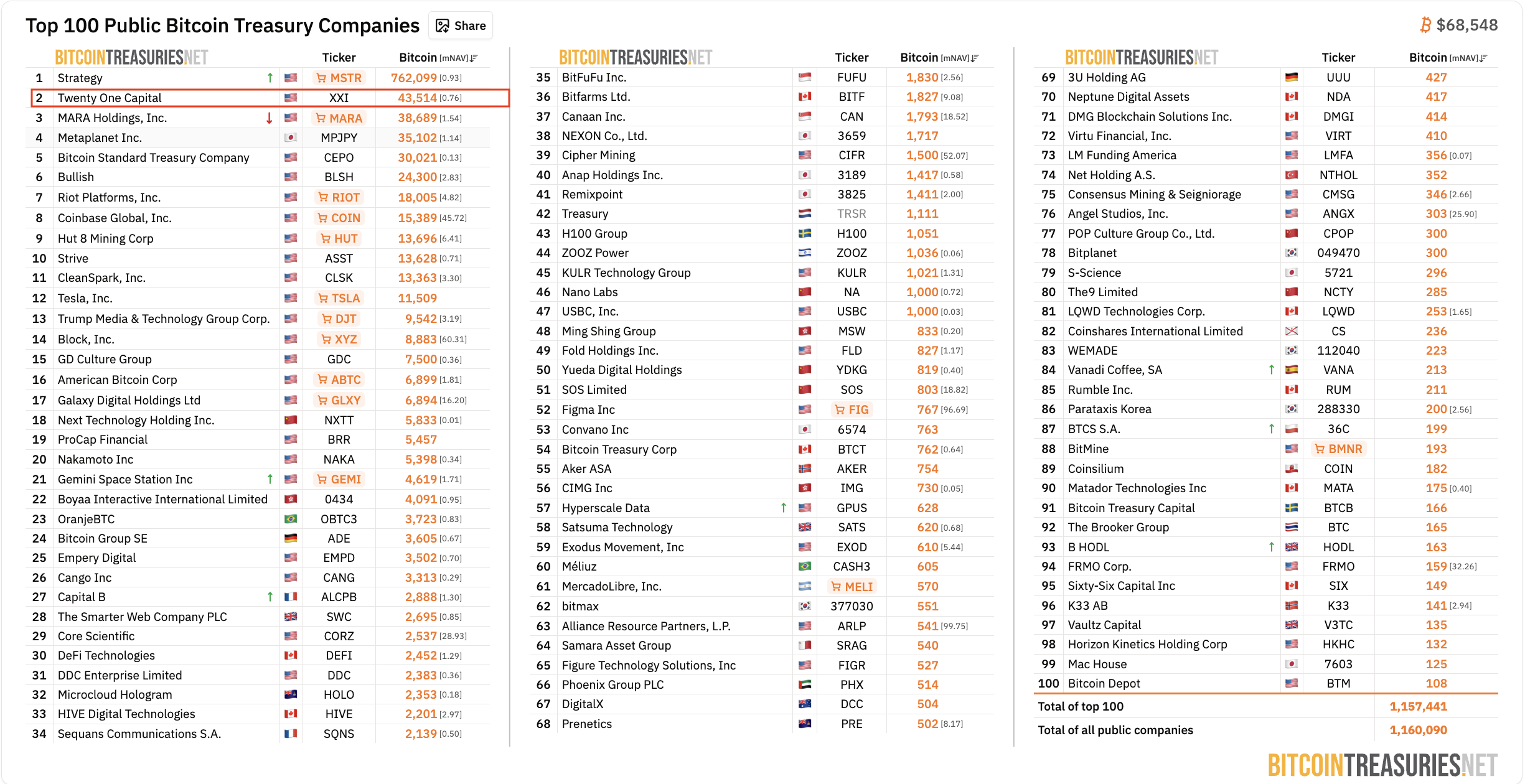

Jack Mallers’ Twenty One Capital is now the second-largest publicly traded Bitcoin treasury by BTC holdings, after miner MARA sold off a portion of its holdings and fell to the number three spot.

The newly formed Bitcoin (BTC) treasury company holds 43,514 BTC in its corporate treasury, valued at over $2.9 billion using the market price at the time of this writing, according to data from BitcoinTreasuries.

Twenty One Capital was publicly listed late last year following its business combination with Cantor Equity Partners, a special purpose acquisition company. Now trading under the ticker XXI, the NYSE-listed shares are down more than 25% year to date.

MARA sold 15,133 BTC, valued at about $1.1 billion, throughout March 2026. The next largest publicly traded Bitcoin holder is Japanese BTC treasury company Metaplanet with 35,100. Bitcoin Treasuries analyst Tyler Rowe in a note Thursday said:

“For the industry, it’s a cautionary signal. MARA borrowed aggressively to stack sats during the bull run and is now selling Bitcoin at a loss to service that debt. This is the precise scenario critics of debt-fueled treasury strategies have warned about.”

This aggressive borrowing is in “sharp contrast” to the business model popularized by BTC treasury company Strategy, which treats BTC as “perpetual digital credit,” using it as collateral to continually finance BTC acquisitions.

“Can miners sustainably operate as Bitcoin treasury companies without the capital markets infrastructure Saylor spent five years building,” Rowe said in the note shared with Cointelegraph.

Some market observers note the change signals the capitulation of crypto treasury and mining companies amid a challenging business environment, worsened by the crypto bear market that started in October 2025 and declining share prices.

Related: Sweden’s H100 eyes Europe’s No. 2 Bitcoin treasury with 3,500 BTC deal

Analysts forecast the decline of the crypto treasury space in 2025

In June 2025, venture capital firm Breed said that only a few crypto treasury companies would survive the “death spiral” of contracting market net asset values (mNAVs) by maintaining a price premium that would allow these companies to secure more financing.

As access to cheap financing options disappears, companies trading at or below their net asset value would have to sell their BTC holdings to meet debt obligations, according to Breed.

Companies that treat their crypto holdings as a speculative bet, rather than a long-term play, were likely to capitulate between cycles, Deng Chao, CEO of asset manager HashKey Capital, told Cointelegraph.

At the same time, crypto treasury companies with a disciplined treasury strategy would last through multiple cycles, he said.

Magazine: Bitcoin’s ‘biggest bull catalyst’ would be Saylor’s liquidation: Santiment founder

TLDR:

- Dragonfly’s Qureshi compares today’s AI agents to the 1964 mouse, warning adoption will take far longer than expected.

- OpenClaw remains buggy and unreliable for financial tasks as models operate outside their training distribution today.

- The x402 protocol processes only around one million dollars daily, confirming the market is still in its tinkering phase.

- Qureshi expects a new model generation within months, but says reaching the early majority will still take several more years.

Agentic payments are gaining momentum as a talking point across crypto and fintech circles globally. Yet a senior voice from one of crypto’s most recognized investment firms is urging caution on timelines.

Haseeb Qureshi, a managing partner at Dragonfly Capital, recently shared what he called his “most bearish take” on the subject.

While he believes agents will eventually reshape how money moves, he argues the technology remains far from ready for mainstream use.

Dragonfly’s Qureshi Points to History as a Cautionary Benchmark

Qureshi grounded his warning in a well-known piece of technology history. He referenced the computer mouse, which was first invented in 1964, as a parallel to today’s AI agents.

That invention clearly pointed toward mass personal computing, yet widespread adoption took many additional years. His point is that spotting a transformative technology early does not mean it arrives on schedule.

OpenClaw sits at the center of his current skepticism about agentic readiness. The Dragonfly executive described the tool as buggy, complicated, and unfit for managing real financial assets.

It regularly makes poor decisions and, in his words, “goes bankrupt doing stupid shit.” These are not minor rough edges — they reflect a structural gap between agent capability and real-world task demands.

The core problem, according to Qureshi, is that current models are handling tasks well outside their training distribution. That mismatch produces the erratic and unreliable behavior users routinely encounter.

No major lab has yet applied reinforcement learning directly to OpenClaw interaction traces. However, those traces carry strong training signal that labs have not yet tapped.

Once a lab trains purpose-built models on agentic task data, a major performance improvement is expected. Every major AI laboratory is working toward this, Qureshi noted, because the commercial prize is clearly visible.

That model release will likely arrive within months, not years. Still, even that milestone will only mark the close of the tinkering era, not the start of mass adoption.

Live Payment Data Backs the Dragonfly Partner’s Cautious Stance

Qureshi pointed to real protocol data to support his position on where the market currently stands. The x402 protocol is processing roughly one million dollars in daily volume at present.

The Machine Payment Protocol is recording even smaller figures than that. Together, those numbers confirm the current user base consists almost entirely of early experimenters.

The Dragonfly executive also drew on a widely cited framing from investor Chris Dixon. The idea is that what technically curious people do on weekends today, the broader public will be doing within ten years.

That pattern has played out consistently across major technology waves, from the internet to mobile. Agentic payments appear to be sitting at the very beginning of that same cycle.

Qureshi mapped out the full adoption curve to give context to what comes next. After the tinkering phase closes, the market enters early adopter territory, which itself will take time to mature.

The early majority follows that, and then comes the late majority and eventual late adopters. Each phase carries its own timeline, and none of them collapse quickly.

For now, the Dragonfly partner sees agents as a long-term story that the industry should not rush. The technology direction is clear, and the destination is not in question.

What remains uncertain is how long each phase of adoption will actually take. That uncertainty, he argues, is precisely what crypto has a habit of underestimating.

Representative Stephen Lynch voiced concerns about the direction of the SEC under Donald Trump, citing dropped investigations and enforcement actions on crypto companies.

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

We began our new Outset Data Pulse analysis expecting 12 years of headline data to confirm a familiar belief in crypto: that news moves markets, and that faster headlines give you an edge.

But what the findings showed instead was more unsettling: most of the time, price seems to move first, and the headline comes later to explain it.

That’s not to say that “news doesn’t matter.” It’s closer to saying we’ve been treating it as the trigger when it often behaves more like the explanation after the move. And it’s easy to see why that belief survived for so long.

Anyone who spends enough time around crypto starts to notice the same thing: something moves, the news feed lights up, and then the dots get connected. When Bitcoin dumps or soars, coverage multiplies. When a major decision hits, whether it’s an ETF approval, an exchange collapse, or a legal victory, headlines also explode.

But the part of that belief which really matters – the part that turns news into a tradable edge – is directional. If headlines genuinely cause price movement, then reading faster makes you earlier. If price movement causes headlines, then reading faster mostly just makes you better informed about what already happened.

That was the real question here: not whether news exists in the sequence, but whether it consistently comes early enough to matter in the way traders often assume.

The part where the data got harder to argue with

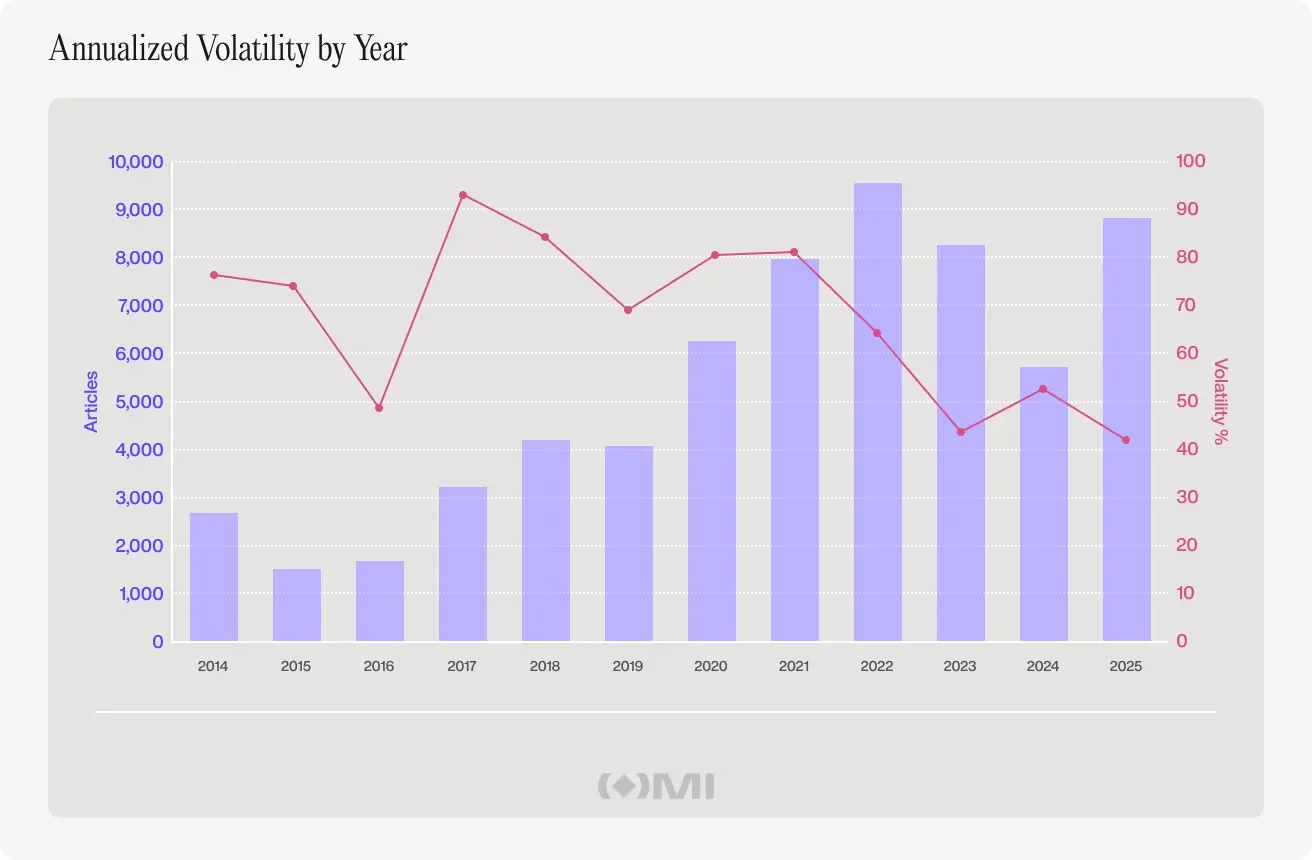

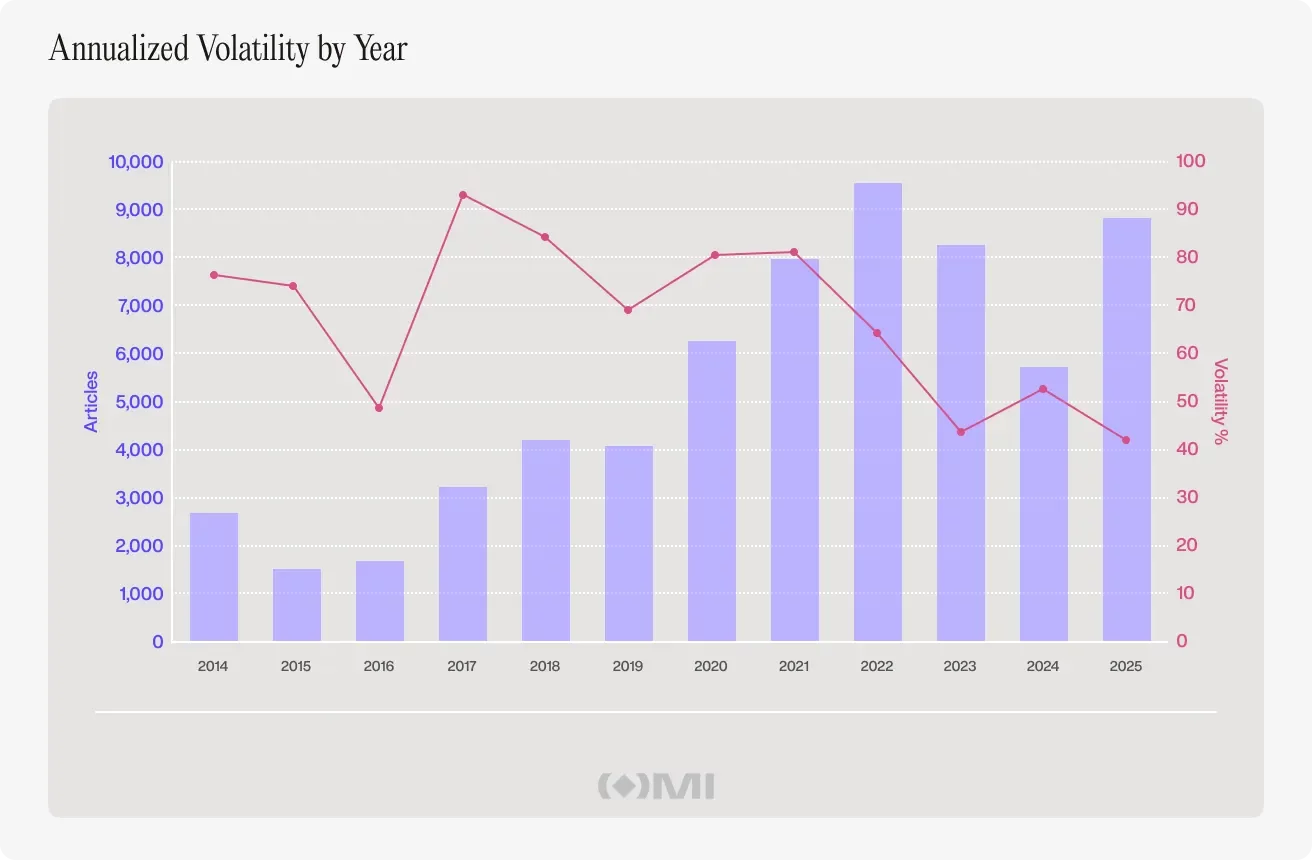

The core dataset powering this Outset Data Pulse report includes 63,926 CoinDesk headlines spanning January 1, 2014 through December 30, 2025, matched to daily Bitcoin closing prices from the TradingView composite index.

That gave us 4,381 days where both a closing price and a headline count were available – enough to test the relationship from several angles, including causality, price behavior around major news spikes, headline sentiment, and topic clustering on the busiest coverage days.

It is also broad enough to cover nearly every “surely news mattered there” event worth testing, including bull and bear cycles, the FTX implosion, the COVID crash, and the start of the spot Bitcoin ETF era.

News volume didn’t forecast price

One of the first things we looked at was whether yesterday’s information helps forecast today’s movement.

We inspected five time horizons, from one day out through five days out. What kept standing out was that the news did not predict Bitcoin’s price across those lags.

Then there’s the kind of number you can’t really argue with because it’s too small to appear important: the correlation between daily changes in article volume and daily Bitcoin returns was 0.019, which means only 0.04% of daily price action was explained. For practical purposes, this is effectively zero.

The longer-term picture points in the same direction. Year by year, article volume and Bitcoin volatility moved on very different rhythms, with no stable relationship between heavier coverage and more explosive price behavior.

That doesn’t mean news and volatility never overlap. They obviously do. But over time, the relationship stays too loose and inconsistent to treat headline volume as a dependable signal on its own.

Price started showing up before the coverage

We also looked in the reverse direction: whether price moves tended to show up before headline volume did, and the most interesting pattern appeared around a two-day lag.

But the part that felt closest to actual market experience was looking at the 50 biggest news days and tracking Bitcoin’s price three days before and three days after each spike.

What stood out was the shape of the move. In the three days before a major coverage spike, Bitcoin’s price was already elevated, around 1% above the event-day baseline. Then after the spike, price drifted down by roughly 0.8% by day three.

That is not a “news moves markets” narrative. It’s a “markets move, then news catches up” story. And once you see that shape, you start noticing how many famous crypto moments feel like they rhyme with it.

Even the biggest headlines didn’t behave like clean signals

These are the kinds of moments we all remember because they felt like turning points for crypto. For example, the U.S. Securities and Exchange Commission approved the spot Bitcoin ETF on January 11, 2024. CoinDesk published 51 articles that day while Bitcoin dropped 7.67% the next day and was down 10% by day three.

Compare that with December 4, 2023, when speculation was running hot but nothing had been confirmed. CoinDesk published 81 articles, and Bitcoin rose 5% the next day.

The same inconsistency showed up elsewhere: after the FTX collapse produced the busiest news day in the dataset, Bitcoin barely moved, while the January 2017 break back above $1,000 was followed by an 11% drop the next day and nearly 20% within three.

Across the ten biggest news events in the dataset, price reactions never settled into a usable pattern – some produced strong gains, others sharp losses, and many no clear follow-through at all.

That inconsistency matters because it’s what breaks the tradability story. If “news moves markets” were a stable indicator at the daily level, the largest news spikes would be where you’d expect the relationship to show up most clearly, certainly not where it dissolves into randomness.

We tried sentiment too

At that point, the obvious pushback is that volume is noisy, but sentiment might still hold the edge. Surely, bullish vs bearish headlines should matter, right?

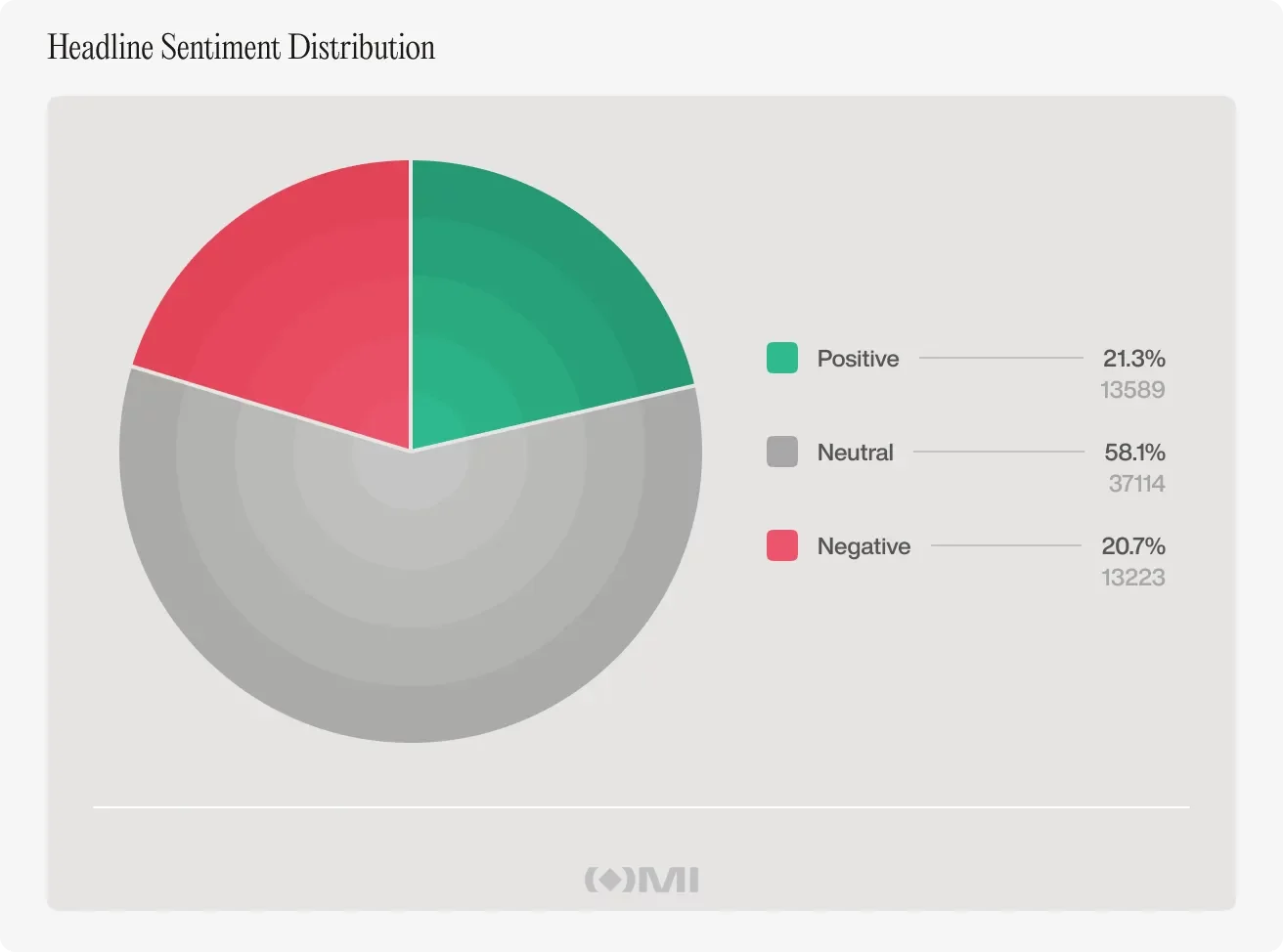

So every headline was run through FinBERT, a financial-language sentiment model. It labeled each headline as positive, negative, or neutral. It also averaged sentiment across each day.

The dataset’s distribution was nearly perfectly balanced, with 58% neutral, 21% positive, and 21% negative. The part that matters for trading is the next step: did daily headline tone correlate with daily returns?

The reported correlation was 0.07, with sentiment explaining about 0.5% of price movement. Again, this is close to nothing for anyone trying to systemically time entries. Worse (or maybe more revealing), the relationship wasn’t stable. In rolling three-month windows, the correlation flipped between positive and negative with no consistent pattern.

There’s also something that feels obvious once you say it out loud: headline sentiment can end up ‘grading’ language that is already racing to price. A headline like “Bitcoin falls below $70,000” gets a negative score, but the fall is already in the same day’s price data.

So we’re back in the same place: the headline is describing the move, not front-running it.

The reframing that made everything make sense

None of what we have seen so far lands in the “ignore news” category. That’s not true, and it’s not useful.

The more hopeful shift is this: by the time a headline hits a major publication, the information has often already moved through faster channels. This includes order flow, on-chain data, social layers, insider networks, and other forms of positioning and interpretation that don’t wait for editorial cycles.

That’s the line that changes how we read the market. The media isn’t where the signal starts. It’s where the signal becomes legible. Headlines are pretty much the “last mile,” representing the moment when a move that has already begun gets named, packaged, debated, and turned into a story people can repeat.

What this changes

Reading faster doesn’t necessarily make you earlier. The market absorbs information before the newsroom has even agreed on the framing. Headlines are often better at telling us what just happened than what happens next. That’s not an insult to journalism. It’s a statement about timing.

And using media as a timing tool can put you behind the market, because the thing you’re reacting to may already be reflected in flows and positioning by the time you are ready to move.

Even the report puts it plainly: headlines are not a clean signal feed. On peak-coverage days, about 61% of headlines fell into broad industry noise – partnerships, fundraising, product launches, stablecoin developments, NFT and gaming updates – with no obvious link to Bitcoin’s next move. Even regulation, the strongest plausible category, still failed to produce a reliable signal at the daily level.

One of the stranger findings was that even Bitcoin halving did not emerge as a distinct cluster on extreme-news days, suggesting that some of Bitcoin’s most important forces do not operate through the daily headline cycle at all.

Where we have to be honest about the exceptions

News could matter at much shorter timeframes, specifically minutes rather than days. A breaking headline can still move the market in the moment, even if that effect gets muted once you zoom out to daily closing prices.

At the same time, longer and slower narrative shifts, the kind that build over weeks, may still influence price in ways this approach can’t fully capture.

There are limits to this too: one publication, even a highly trusted one, does not represent the whole information universe. Crypto’s fastest information often travels through social platforms and private channels that this dataset can’t track. Also, some patterns may only show up in specific conditions, not in the cleaner daily relationships these tests can pick up.

So we’re not left with a simple “news is useless” mantra. Rather, we’re left with something more actionable: most of the time, the headline is the market becoming explainable, not the market beginning to move.

Bitcoin’s on-chain picture remains centered on profitability dynamics, with the total supply in profit holding near a historically significant zone. As of Thursday, CryptoQuant data show about 60.6% of BTC supply in profit, placing the market in a band (roughly 50% to 60%) that has repeatedly framed cycles and potential accumulation phases. The metric briefly dipped to 50.8% on Feb. 5—the lowest since Jan. 2, 2023—leaving a sizable portion of holders at or near breakeven and at a potential loss.

Historical echoes are often cited by traders when profitability enters this range. In January 2023, BTC traded around $16,682 with profitability near 51%, just before a pronounced rally that CryptoQuant’s analysis notes as mirroring a pattern later seen in a multi-hundred percent upmove. A separate moment in March 2020 saw the total supply in profit slip below 50% as BTC hovered near $6,500, ahead of a bull run that pushed prices toward $69,000 in 2021. While past patterns can offer context, they do not guarantee future outcomes; profitability alone does not pinpoint price bottoms, but it does sketch zones where long-term accrual has been strong and selling pressure historically eased.

Key takeaways

- Bitcoin’s supply in profit stands around 60.6%, a level within the 50–60% zone historically linked to market-cycle resets and renewed accumulation.

- Long-term holder profitability remains meaningful: the long-term holder net unrealized profit/loss (LTH-NUPL) sits near 0.40, suggesting holders remain in profit even as overall profitability tightens.

- Institutional and corporate participation has grown, with entities holding roughly 15.8% of circulating BTC (about 3,319,677 BTC), potentially dampening short-term price sensitivity to swings.

- Short-term holder (STH) inflows to Binance have fallen to about 25,000 BTC on March 25, indicating less reactive selling from newer market participants.

- Valuation-based on-chain signals (MVRV, NUPL, Puell) are flashing zones associated with stress for retail demand but not definitive bottoms, highlighting a balance of risk and upside potential ahead.

Profitability baselines and market structure

The 50–60% profitability corridor has been a recurring feature across several cycles. When a large share of supply sits in profit, unrealized gains on the network compress, which can reduce the incentive for holders to sell into weakness. In this framework, the market’s current 60.6% profitability suggests a still-robust share of the supply that could weather minor downturns without triggering acute downside selling pressure. Yet the same metric also shows that a meaningful number of investors remain in the red or near break-even, underscoring the persistence of volatility and the potential for renewed demand when risk appetite shifts.

Crucially, the composition of who owns BTC is shifting. The rise of corporate entities and exchange-traded products (ETFs) as significant holders means a portion of the market is increasingly dominated by entities with longer time horizons and lower sensitivity to short-term price swings. In aggregate, these participants are estimated to control around 15.8% of the circulating supply, or roughly 3.32 million BTC. This dynamic tends to flatten peak-forcing selloffs that can accompany prolonged drawdowns, contributing to a market where profitability compression does not necessarily translate into a wave of distressed selling from veteran investors alike.

On-chain signals and market stress zones

Beyond aggregate profitability, on-chain flow metrics add nuance to the picture. Short-term holder activity has shown a meaningful contraction in selling pressure on BTC. CryptoQuant data indicate STH inflows to Binance dropped to near 25,000 BTC on March 25, a low not seen during the February sell-off, according to comments from market analysts. Such a drop points to a cooling in reactive selling from newer market participants and a potential for steadier price action if selling pressure remains subdued.

Meanwhile, traditional valuation models that analysts watch—market-value to realized-value (MVRV), NUPL, and Puell Multiple—continue to illuminate where stress is most likely to surface. Analysts have observed that when MVRV falls below 1, NUPL slips under -0.2, or Puell Multiple approaches 0.35, those periods have historically coincided with heightened retail stress or undervalued conditions. While these indicators do not guarantee a local bottom, they map out zones where downside risk has often been bounded by prior upside potential, offering traders a probabilistic framework for assessing risk-reward dynamics in the near term.

Taken together, the current on-chain configuration suggests a market moving away from the kind of acute, long-term holder distress that punctuated bear markets in 2015, 2018, and 2022. The divergence between a modestly higher supply-in-profit reading and steady LTH-NUPL points to a market that could see renewed accumulation without triggering uniform, forceful capitulation among long-term investors. In other words, the landscape is shifting toward an ownership mix that may support more measured corrections rather than sharp, cyclical lows.

Related: Bitcoin in ‘later stages’ of bear market: Watch these BTC price levels

What readers should watch next

For traders and investors, the key questions revolve around whether the current on-chain balance can sustain a move higher without retesting lows. The persistence of a sizable profit pool coupled with a growing share of BTC held by institutions could support a gradual re-accumulation narrative, even if price swings remain volatile. Markets will likely respond to macro developments, policy signals, and shifts in risk appetite as much as to on-chain metrics.

Next steps to monitor include: the trajectory of MVRV, NUPL, and Puell readings as BTC moves through key price zones; any shifts in the distribution of BTC held by corporates and ETFs; and observed changes in STH and overall exchange flows that could presage larger moves in supply held by retail participants. While on-chain data cannot predict exact bottoms, it continues to offer a granular view of where investors are positioned and how that positioning might shape the path of least resistance for Bitcoin in the months ahead.

Plans for a new cinema in Ripon submitted to council

Who knew Lord Sugar is a table tennis fan?

Congress sneaks CBDC into housing bill, economist warns 80% of voters opposed

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

NEW YORK’S Governor ERUPTS After $7 Trillion Vanguard Builds Its Next Financial Center in Texas!

Divine Financial Breakthrough #Prayer #FinancialBlessing #ChristianMotivation #Faith #Breakthrough

Crypto Setup Looks TERRIFYING! – But It’s Not What You Think!!

-

Crypto World6 days ago

Crypto World6 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

NewsBeat2 days ago

NewsBeat2 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics6 days ago

Politics6 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Crypto World5 days ago

Crypto World5 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Tech7 days ago

Tech7 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

News Videos21 hours ago

News Videos21 hours agoParliament publishes latest register of MPs’ financial interests

-

Sports3 days ago

Sports3 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

Sports3 days ago

Sports3 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Business4 days ago

Business4 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Tech4 days ago

Tech4 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Sports6 days ago

Sports6 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who nailed 12 Derby-Oaks Doubles enters picks

-

Tech4 days ago

Tech4 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

Tech5 days ago

Tech5 days agoToday’s NYT Connections Hints, Answers for March 22 #1015

-

Business6 days ago

Columbia Sportswear enters $500 million credit agreement with JPMorgan Chase

-

News Videos3 days ago

News Videos3 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

Business5 days ago

Business5 days agoWill Duke Basketball Win It All? Duke Basketball Enters Second Round as Third Favorite to Claim NCAA Title

-

Sports4 days ago

Sports4 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who hit 12 Derby-Oaks Doubles enters picks

-

Crypto World6 days ago

Crypto World6 days agoSmall-cap Russell 2000 enters correction territory

You must be logged in to post a comment Login