Crypto World

The new oil? Inside the effort to turn AI computing power into a tradeable commodity

For decades, companies have turned to futures markets to manage uncertainty. Airlines hedge fuel costs. Farmers hedge crops. Manufacturers hedge metals.

Now a startup wants to bring that same financial machinery to artificial intelligence.

Silicon Data, a company that tracks pricing across cloud providers and GPU marketplaces, has partnered with CME Group to launch what could become the world’s first futures contracts tied to the computational power needed to run AI, allowing companies to hedge against fluctuations in the cost to train and run AI models. The contracts are still awaiting regulatory approval.

Early signs suggest investor interest is quickly emerging. Within days of Silicon Data’s announcement with CME Group, asset managers including ProShares and Rex Shares filed proposals for exchange-traded funds tied to the proposed contracts, including leveraged and inverse products.

Founder and CEO Carmen Li believes the market could eventually rival some of the world’s largest commodity markets.

“I think it will be larger” than oil futures, Li said in an interview, adding that energy demand tied to running artificial intelligence will eventually surpass all other energy uses, combined.

Like jet fuel

The idea stems from a simple observation: AI companies increasingly depend on compute in the same way airlines depend on jet fuel.

Most companies don’t own the high-end graphics processing units, or GPUs, that power modern AI systems. Instead, they rent access through cloud providers and a growing ecosystem of so-called neoclouds. As demand for AI infrastructure surges, the cost of that compute can fluctuate, making it difficult for businesses to forecast expenses.

“Right now we’re at a high point of uncertainty,” said Seoyoung Kim, a finance professor at Santa Clara University. “A lot of people don’t know how much computing power they’ll need in the next year, and a lot of suppliers of that computing power right now don’t know how many GPUs and to what capacity they should order and the manufacturers, like Nvidia, they don’t know how much they should produce.”

Silicon Data has built a series of GPU price indexes that track the hourly rental cost of specific chips across providers. The company hopes those benchmarks can serve as the foundation for a futures market, much as West Texas Intermediate crude oil underpins energy derivatives.

Like any futures market, compute contracts will need both buyers and sellers. Companies worried about rising compute costs would seek protection from higher prices, while providers with large amounts of capacity could hedge against the risk of prices falling.

Silicon Data’s benchmarks have already begun appearing in high-profile corporate disclosures. SpaceX, for example, referenced the company’s GPU rental-rate data in its prospectus to go public.

Speculators coming in

Not everyone in the market would be looking to hedge risk. As with other futures markets, compute contracts would also draw speculators — traders with no direct need for GPU capacity but a view on where compute prices are headed.

Proponents argue that speculators play an important role in building liquidity and improving price discovery. Critics counter that speculation can amplify volatility and disconnect prices from underlying demand.

“Speculators are a very important piece of the ecosystem as well,” Li said. “You need natural hedgers. You need market makers. You need speculators. They have opinion. They want to express their opinion, which is perfectly fine.”

The Harvard MBA said traders who believe they have insight into future supply-and-demand dynamics should be able to express those views through the market, helping establish prices for the broader industry.

The ProShares and Rex Shares filings for ETFs are contingent on regulatory approval of the futures market. Still, they suggest some investors already view AI compute as a potentially tradable asset class rather than simply a technology input.

Benchmarking AI compute cost

Unlike a barrel of oil, AI compute is not a standardized physical commodity. Silicon Data said there are more than 50 different configurations of Nvidia’s H100 chip alone, with prices varying based on processors, memory, networking, utilization rates and data center location.

For the proposed futures market to work, traders need confidence that a single benchmark can accurately represent those variations.

“What we do is normalize the prices coming to our platform every day to a base H100 case,” Li said. “It’s a very complicated normalization step, even before the index calculation step.”

Kim, the Santa Clara finance professor, noted that standardization has always been a challenge for futures markets. Corn futures, for example, specify the exact grade of corn that can be delivered under a contract. Compute markets face a similar task: defining precisely what buyers and sellers are trading.

“The CFTC is going to want to know exactly what the product is,” Kim said. Contract specifications, settlement procedures and benchmark construction are all likely to face scrutiny before the market can launch, she said.

— CNBC’s Charlotte Morabito contributed to this story.

Securitize expanded its regulated US platform after its capital subsidiary registered with the SEC, while SECZ shares fell nearly 10% on Monday.

Summary

- Securitize Capital’s SEC investment adviser registration became effective July 22, federal records show.

- The registration adds disclosure, compliance, recordkeeping and examination requirements under US securities law.

- Securitize manages more than $5 billion in assets, including BlackRock’s $2.6 billion BUIDL fund.

- SECZ fell nearly 10% to $6.76, reducing Securitize’s market value to about $1 billion.

Securitize Capital becomes an SEC-registered adviser

Securitize said Monday that its subsidiary, Securitize Capital LLC, has registered with the US Securities and Exchange Commission as an investment adviser.

The registration became effective on July 22, according to the SEC’s Investment Adviser Public Disclosure database. The Miami-based business had operated as an exempt reporting adviser in Florida since March 2023.

That earlier status generally restricted the unit to advising venture capital funds or private funds with less than $150 million in US assets under management. Full registration removes those limits but brings additional disclosure, compliance, recordkeeping and examination duties under the Investment Advisers Act of 1940.

“Becoming an SEC-registered investment adviser is an important step in the continued expansion of Securitize’s platform,” co-founder and CEO Carlos Domingo said.

“Asset managers and institutional investors want to work with partners that understand both the opportunity of tokenization and the obligations that come with operating in regulated markets.”

The company noted that registration does not represent an SEC endorsement or indicate a particular level of skill or training.

SEC status expands Securitize’s US regulatory stack

Securitize Capital’s registration completes a broader group of regulated services covering the issuance, management and trading of tokenized securities.

Securitize Markets operates as an SEC-registered broker-dealer and runs an SEC-regulated alternative trading system. Other affiliates provide transfer-agent and fund-administration services. FINRA also approved Securitize Markets in May to custody tokenized securities and support atomic settlement.

The expanded structure could allow Securitize to work more closely with asset managers building onchain vaults, lending products and other portfolio strategies. The company reported more than $5 billion in assets under management as of July across products linked to BlackRock, Apollo, BNY, Hamilton Lane, KKR and VanEck.

BlackRock’s BUIDL tokenized Treasury fund accounts for about $2.6 billion of that total.

The registration follows SEC Commissioner Hester Peirce’s July 22 warning that managing certain vaults and lending strategies may create investment adviser obligations. Peirce urged businesses operating within the securities market to engage with the regulator while developing compliant onchain products.

SECZ falls despite Citi’s bullish price target

SECZ shares fell over 10% during Monday trading to about $6.76, giving Securitize a market capitalization of slightly under $1 billion per data from Yahoo Finance. The decline extended the stock’s losses since its New York Stock Exchange debut earlier in July.

Citi analyst Peter Christiansen separately initiated coverage with a Buy rating and a $10 price target. The target represented about 34% upside from Friday’s closing price of $7.47.

Christiansen described Securitize as important infrastructure for real-world asset tokenization but identified several risks. These included the company’s reliance on BlackRock’s BUIDL fund, exposure to interest-rate changes and uncertainty over the development of higher-margin transaction revenue.

Securitize pushes IPOs and public stocks onchain

Securitize entered public markets on July 2 through a merger with Cantor Equity Partners II that generated about $400 million in gross proceeds. It also tokenized its own SECZ shares on the listing date.

Cantor and Securitize later announced a July 15 partnership designed to incorporate blockchain infrastructure into IPOs and follow-on stock offerings. Cantor will provide capital-markets and trading services, while Securitize will manage the issuance, distribution and servicing of tokenized securities.

Unlike products that create blockchain representations of stocks already trading on exchanges, the arrangement would place onchain infrastructure within the original securities issuance process.

Hanwha Group has also emerged as Securitize’s largest shareholder. SEC filings show that the South Korean conglomerate controls 15.69 million shares through affiliated entities and investment vehicles, equal to a 9.6% stake.

Securitize is also working with the NYSE on infrastructure for the exchange’s planned tokenized securities platform. The adviser registration gives the company another regulated US entity as it expands from issuing tokenized funds into portfolio management and public-market settlement.

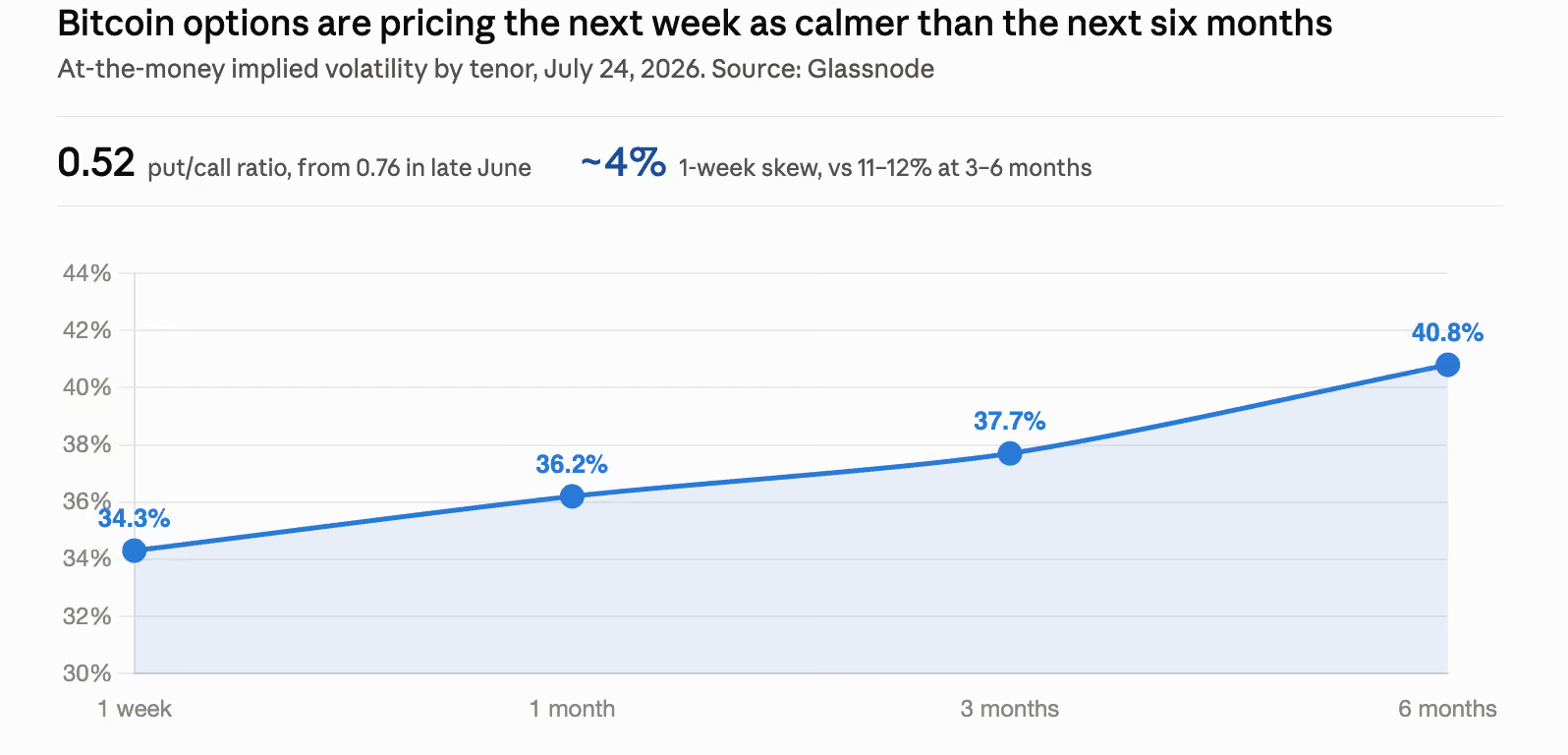

Bitcoin’s options market has turned notably less defensive over the past month, unwinding the downside protection traders built up in June just as the Federal Reserve prepares to meet.

The put/call ratio on open interest, which measures how much of the market is positioned in puts, contracts that pay off when the price falls, against calls, which pay off when it rises, has dropped to roughly 0.52 from about 0.76 in late June, according to Glassnode.

Calls are gaining share, the pattern of traders stepping back from hedging rather than adding to it. Recently, large traders have been accumulating $70,000 strike calls and bull call spreads, signaling expectations of upside in the spot price.

The 25-delta skew, the premium traders pay for downside protection relative to equivalent upside exposure, has fallen to around 4% at the one-week tenor while three- and six-month contracts hold at 11% to 12%. That indicates traders are still paying for insurance against something going wrong later this year, but have largely stopped paying for it this week.

On Friday, a clever startup manufactured a viral media story about a Brazilian rancher securing a $19,600 loan by tokenizing 10 cows.

However, omitted from the subsequent wall-to-wall media coverage was some very inconvenient context, such as the rancher’s seat on the board of a state-backed ranching fund, his massive herd, and plentiful access to traditional, real estate-based financing.

When the story hit social media on Friday, crypto influencers applauded blockchain technologies extending credit to a farmer in need.

Unfortunately, this feel-good story falls apart under the slightest scrutiny.

Firstly, the rancher’s expansive, multi-generational real estate exceeds 1.3 square miles, and as of the most recent estimates, had over 500 cows alongside other operations.

Even if the herd size hasn’t grown, the 10 animals in Friday’s announcement represent a mere 4% of the dairy’s more than 240 lactating cows.

Secondly, trade press profiles identify the operator of the farm, Fazenda Engenho Velho, as civil engineer João Guilherme Brenner whose family has owned the land for generations.

Unlike many farmers and ranchers who rent their land, his family owns its land outright and, as such, has access to conventional, real estate-based financing.

A president, director, and seven-figure rancher

In 2022, a magazine interview documented the rancher’s election as president of Paraná’s Holstein breeders association and his appointment to the board of directors of the Brazilian state’s livestock development fund.

His 10 Holstein cows in Imbituva, Paraná secured a credit note this week, worth roughly $19,700.

Despite that loan of 1% the value of his dairy’s land, press outlets gushed about “one of Brazil’s first uses of tokenized livestock as loan collateral.”

Press coverage soared past a million views through posts about tokenization ostensibly allowing farmers to access financial lifelines.

For context, Paraná’s agriculture department prices farmland of the Imbituva municipality at 23,200 to 126,900 Brazilian reais (BRL) per hectare across every soil classification except its worst.

Anywhere within that price range, Guilherme Brenner’s 360 hectares are worth millions of US dollars.

Read more: 28,000 crypto wallets pledged $560M for SpaceX shares they didn’t get

The headlines look great

It’s not surprising to learn that the media cycle benefited a startup. Cowmed, an agtech that spearheaded both tokenized cattle deals, structured the stunt alongside a receivables fund, Target Fundo de Investimento em Direitos Creditórios.

In 2024, a similar yet separate company, tokenization startup Simple Token, set the goal of using tokenized livestock to unlock 200 million BRL worth of loans by the end of 2026, in partnership with Cowmed.

With less than six months left, actual disclosed credit across the lifetime of both companies’ tokenized livestock efforts is 99% short of their goal, although the privately held companies aren’t required to make public disclosures.

Cowmed has raised over $1 million across several rounds of financing since 2017. Its latest publicly accessible financing was a crowdfunding campaign that closed 5.9 million BRL at a valuation of $6.2 million.

Meanwhile, Halter, Cowmed’s competitor and maker of electronic fences and cattle collars, closed a $220 million round in March of this year at a $2 billion valuation.

In comparison, Cowmed could certainly use to catch up. It is probably quite happy about Friday’s virality.

Cowmed’s business is far more modest than its competitors. It charges roughly $5 per collar per month and reported less than $3.6 million in revenue last year.

Tokenized cows are no better than non-tokenized cows

In summary, for a loan worth less than $20,000, Cowmed earned a global marketing campaign with over a million views that would have cost many multiples of that from paid advertising.

The use of blockchain in the stunt added no discernable value beyond the addition of buzzwords for media. The arrangement relies on trust in one rancher, one collar maker, one tokenization provider, and one lender.

There’s no decentralization to speak of beyond trust in corporate executives.

For years, cattle have collateralized loans to ranchers. Moreover, wireless tracking of animal collars has existed without blockchain technologies for over a decade.

For this Brazilian rancher, traditional databases could have tracked his cows just as well as any blockchain.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

The U.S. Commodity Futures Trading Commission has asked a federal court to expedite its ruling against Minnesota before the state’s prediction-market ban takes effect on Aug. 1.

Summary

- Minnesota’s ban takes effect Aug. 1, leaving the court only days to decide on injunctive relief.

- Kalshi and Polymarket joined the CFTC’s request for a temporary administrative stay.

- The CFTC may seek emergency appellate relief if the district court does not act promptly.

- Industry groups argue that one federal framework should govern regulated event contracts across the United States.

CFTC presses court as Aug. 1 deadline approaches

The CFTC requested expedited handling of its motion for a preliminary injunction, according to its latest court filing. The regulator said a decision is needed before Minnesota’s new law takes effect later this week.

Minnesota Governor Tim Walz signed the measure in May. It makes creating, operating, facilitating, or advertising a prediction market in the state a criminal offense.

The CFTC sued Minnesota on May 19, arguing that the state law interferes with the federal derivatives framework established under the Commodity Exchange Act. The agency asked the court to block enforcement while the wider legal dispute proceeds.

A hearing has already taken place, but the judge has not ruled on the preliminary injunction request. The Commission said it would treat the motion as constructively denied if the court neither issues a decision nor temporarily stays the law by July 28.

In that event, the regulator plans to seek interim relief from the federal appeals court.

Kalshi and Polymarket join request for temporary stay

Kalshi and Polymarket have filed separate challenges seeking to stop Minnesota from enforcing the ban. Both platforms joined the request for a temporary administrative stay while the court considers their preliminary injunction motions.

The companies also indicated that they would treat their motions as constructively denied if the court does not act by the stated deadline. They could then pursue relief at the appellate level alongside the CFTC.

The dispute centers on whether event contracts offered through federally regulated exchanges fall exclusively under the CFTC’s authority or may also be restricted through state gambling laws.

Minnesota considers prediction markets a form of gambling that can expose residents to addiction and financial harm. CFTC Chair Michael Selig has taken the opposing position, arguing that Minnesota’s law would turn federally regulated operators and participants into felons.

For U.S. users, the ruling could determine whether access to prediction markets depends on their state of residence. A decision favoring Minnesota may also encourage other states to pursue direct bans or enforce gambling rules against event-contract platforms.

CFTC tightens oversight of event-contract filings

The court fight does not mean the CFTC supports unrestricted prediction markets. The agency has also increased its scrutiny of how registered exchanges introduce new event contracts.

As crypto.news previously reported, the CFTC issued its second warning of the year on July 24 over broad, template-style self-certification filings. Its Division of Market Oversight instructed exchanges to provide contract-specific terms, settlement procedures, data sources and compliance analysis.

Designated contract markets may still use self-certification to list qualifying contracts without waiting for advance Commission approval. However, the regulator said one filing cannot cover an open-ended range of contract variations unless it includes enough detail for each product.

The advisory shows that the federal-state dispute concerns regulatory authority rather than whether prediction markets should operate without oversight. The CFTC maintains that federally registered platforms must follow the Commodity Exchange Act and the agency’s rules, including product-level disclosure requirements.

Federal prediction-market framework gains support

The Minnesota case comes as the CFTC considers broader rules for event contracts. Its proposal would guide reviews of contracts linked to gaming, war, terrorism, assassination and conduct that violates federal or state law.

The public comment period closed on July 27. Hyperliquid Policy Center and Multicoin Capital submitted a joint filing supporting written federal standards.

The groups argued that exchange-traded contracts differ from traditional wagers because participants trade with each other rather than against a bookmaker.

“A bet with a bookmaker is a wager against the house: the house sets the odds and wins when you lose. An exchange-traded contract is a trade between two willing participants at a market price, and the venue’s business is matching that trade for a fee, whichever side wins.”

Hyperliquid Policy Center and Multicoin said forcing registered platforms to comply with 50 separate state gambling regimes would fragment the federal market structure. Minnesota maintains that states retain authority to protect residents from products they view as unlicensed gambling.

The immediate question now rests with the federal court. A ruling or temporary stay before Aug. 1 would preserve current access while the litigation continues, while no action could send the CFTC, Kalshi and Polymarket directly to the appeals court.

Audiera (BEAT), Ondo (ONDO), and Ethena (ENA) lead the TOP 3 altcoins to watch in the last week of July 2026 after posting weekly gains of 50%, 17%, and 14.4%.

Each token now approaches a decisive technical level. BEAT tests $4, ONDO eyes $0.46 after an accumulation breakout, and ENA challenges a downtrend that has capped its price since October 2025.

Token

Weekly Gain

Current Price

Key Level to Watch

Setup

Audiera (BEAT)

+50%

$3.78

$3.98 resistance (0.236 Fib)

Post-cup-and-handle recovery

Ondo (ONDO)

+17%

$0.41

$0.46 target (above 0.786 Fib)

Breakout from accumulation

Ethena (ENA)

+14.4%

$0.0898

$0.13 resistance

Trendline breakout attempt

Audiera (BEAT) Tests the $4 Barrier After a 50% Weekly Surge

BEAT posted the strongest weekly performance of the three, and momentum has carried into today. The token trades near $3.78 after adding 6% in the past 24 hours, per BeInCrypto market data.

The weekly chart shows a cup and handle formation that developed between January and May 2026. After the May breakout, the price reached the pattern’s $4 target in roughly three weeks.

The rally later extended to a record high of $11.44 on MEXC in June. BEAT then corrected to the 0.5 Fibonacci retracement support at $1.22, where buyers stepped in.

That bounce now faces the 0.236 Fibonacci level at $3.98, the most important resistance on the chart. Meanwhile, the Relative Strength Index (RSI) sits at 62, below overbought territory but rising. However, analysts have flagged supply-related risks after the token’s parabolic rise, so a rejection here could trigger a sharp downside.

A weekly close above $3.98 could reopen the path to price discovery. A rejection would keep $1.22 in focus as the key support.

ONDO Breaks Out of Accumulation With $0.46 in Sight

ONDO gained 17% last week and trades at $0.41, up 6% in 24 hours. The token spent January through early May inside an accumulation zone between $0.25 and $0.29 before breaking out on heavy volume.

More recently, the price bounced off the 0.382 Fibonacci retracement at $0.29. It then broke through the 0.618 Fibonacci resistance at $0.37, a level that may now act as support.

The next target sits right above the 0.786 Fibonacci at $0.44, within the resistance zone near $0.46. That would represent a gain of roughly 12% from current levels.

Volume tells a supportive story. The spike recorded between May and June is declining, yet activity remains elevated compared with the accumulation phase. In contrast, the RSI stays neutral at 55 while trending higher, suggesting the move still has room before overheating.

ENA Rounds Out the Altcoins to Watch With a Trendline Breakout

ENA, the third pick among this week’s altcoins to watch, climbed around 14.4% last week. The token trades at $0.0898, up almost 6% in 24 hours.

The weekly chart suggests ENA is breaking out from a descending resistance trendline in place since the October 2025 peak. The token also shrugged off its July token unlocks, which added over 40 million ENA to circulation without triggering a sell-off.

Resistance remains layered above. The first hurdle sits around $0.13, just above the 0.236 Fibonacci at $0.113, roughly 26% higher. Beyond that, the 0.618 Fibonacci at $0.25 and the 0.786 Fibonacci at $0.35 mark the next major barriers.

Volume has been decreasing since the June peak, which may signal a phase of accumulation. Meanwhile, the RSI has recovered to the neutral zone at 38 after months of oversold readings.

Holding the support zone near $0.07 remains essential for the bullish case. A confirmed weekly close above the trendline could target $0.13, while a breakdown below $0.07 would invalidate the recovery.

The post TOP 3 Altcoins to Watch in Last Week of July 2026 appeared first on BeInCrypto.

The Tom Lee-chaired Bitmine Immersion Technologies continues to expand its Ethereum treasury, adding almost 10,000 ETH over the past week.

This purchase was slightly larger than the one from the previous week, but it’s still significantly lower than many completed just a month ago. Recall that the former BTC miner bought over 52,000 ETH in June.

Another 9,946 ETH Scooped

The press release shared by the company outlined the impressive streak, noting that the firm has acquired some portion of ETH for well over a year. In fact, this accumulation spree began when it launched the Ethereum Treasury Strategy on June 30, 2025, and has continued to this day.

The purchase of the 9,946 ETH in the past week brought Bitmine’s total holdings to 5,787,414 ETH, worth well over $11 billion at current prices. However, it still remains deep in the red since its average buying price is nearly twice as high.

Bitmine said it continues with its main goal to bring its total stash to 5% of Ethereum’s total supply. It has now come to less than 0.2% of that target, but it keeps demonstrating that the firm remains committed to accumulating Ethereum despite already controlling nearly one in every 20 ETH in existence.

Chairman Tom Lee is still bullish on the industry and Ethereum in particular, pointing to the strengthening of the ETH/BTC pair and the recent technical momentum. The largest altcoin has outperformed the market over the past few days, posting another 5% surge daily and hitting a 2-month peak at almost $2,000. Lee believes $2,000 and $2,500 are ETH’s main obstacles on the path to a major recovery.

Staking Continues

In times when the actual number of validators who want to unstake their ETH tokens has gone down to practically zero, Bitmine doubled down on its strategy to put almost all of its stash to work. The firm revealed that more than 4.9 million tokens have been staked through its institutional platform, MAVAN.

Staking 85% of its total holdings means that the firm’s seven-day staking yield of 2.65% (annualized) projects annual revenue of approximately $254 million. The company plans to allocate its entire ETH fortune to staking, which would increase the number to roughly $300 million.

The post Tom Lee’s Bitmine Keeps Buying Ethereum, Treasury Nears 5.8 Million ETH appeared first on CryptoPotato.

The cuts come as the crypto industry grapples with a prolonged downturn. After three consecutive quarters of declines, the total cryptocurrency market capitalization fell to around $2.1 trillion at the end of the second quarter, while trading volumes weakened and retail participation slowed amid higher interest rates, geopolitical uncertainty and persistent outflows from crypto exchange-traded fund (ETF).

U.S. spot bitcoin ETFs recorded a combined $6.9 billion of net outflows in May and June. While flows have recovered in July, including a six-day streak of inflows, the rebound remains modest relative to the withdrawals seen during the broader market downturn.

Uphold stressed that it is not closing its U.K. operations or any of its international offices, adding that all locations remain fully staffed and operational.

The firm’s enterprise platform enables banks, fintechs and broker-dealers to integrate digital asset services for their own customers, an area the company said is seeing rapid growth.

The momentum in that business, combined with weaker retail demand, made the restructuring necessary as it shifts personnel and investment toward enterprise products. Further growth announcements are expected in the coming months, the company said.

The firm remains bullish on the long-term outlook for the retail market. “In 2026, we’re expanding our popular consumer app into a multi-asset, blockchain-enabled financial companion,” McLoughlin said. “By year end, the app will offer US stocks, tokenized securities, asset-backed lending, credit cards, prediction markets and enhanced DeFi yield opportunities on assets including XRP,” he added.

Binance Futures launched three USDT-settled perpetual contracts tied to the ProShares Bitcoin ETF and two long-duration U.S. Treasury products on July 27.

Summary

- Binance introduced BITOUSDT, TMFUSDT, and TBTUSDT perpetual contracts in five-minute intervals.

- All three products support up to 25x leverage and remain available for trading around the clock.

- Orders require a minimum notional value of 5 USDT, with funding settled every eight hours.

- The contracts expand Binance’s tokenized traditional finance offering, but regional access restrictions still apply.

Binance Futures adds three ETF-linked contracts

Binance Futures began rolling out the three USDⓈ-M perpetual contracts at 13:30 UTC, according to a July 27 exchange announcement.

TMFUSDT opened first, followed by TBTUSDT at 13:35 UTC and BITOUSDT at 13:40 UTC. Each contract uses USDT as its settlement asset and allows traders to take long or short positions without an expiration date.

TMFUSDT tracks the Direxion Daily 20+ Year Treasury Bull 3X ETF. The underlying fund seeks to deliver three times the daily performance of the ICE U.S. Treasury 20+ Year Bond Index.

TBTUSDT follows the ProShares UltraShort 20+ Year Treasury ETF, which targets twice the inverse daily performance of its long-duration Treasury benchmark. This means the underlying ETF generally benefits when long-term U.S. Treasury bond prices decline.

BITOUSDT is linked to the ProShares Bitcoin ETF, or BITO. The U.S.-listed fund provides Bitcoin exposure primarily through futures contracts rather than holding Bitcoin directly.

New contracts offer leverage of up to 25x

Binance set the maximum leverage for each contract at 25x. The minimum order size is 0.01 units, while every order must carry a notional value of at least 5 USDT.

Funding payments will take place every eight hours, with the funding rate capped between negative 2% and positive 2%. Binance set the base interest rate used in the funding calculation at 0%.

The contracts also support Multi-Assets Mode. Eligible traders can use several supported assets as margin instead of relying only on the contract’s settlement currency.

However, Binance said its funding-interval adjustment mechanism will not apply to the three products. Their funding cycle will remain at eight hours even when the rate reaches its upper or lower limit or when no funding payment is required.

Trading will remain available 24 hours a day, seven days a week. That differs from the underlying U.S.-listed ETFs, which trade during defined exchange sessions.

Binance may later change the products’ leverage limits, funding rates, tick sizes and margin requirements in response to market conditions.

ETF derivatives support Binance’s super app strategy

The launch expands Binance’s presence in tokenized traditional finance by giving crypto traders exposure to Bitcoin futures and opposing views on long-duration U.S. government bonds through one derivatives platform.

Crypto.news reported earlier in July that Binance is working to develop a broader financial “super app” built around trading, payments, stablecoins and investment products.

Shunyet Jan, Binance’s head of spot trading and derivatives, said trading remains central to the platform but no longer represents its entire target market.

“We’re trying to not just be a crypto exchange, but be a super app that involves payment.”

The new perpetual contracts fit that strategy by bringing references to established U.S. investment products into Binance’s round-the-clock trading environment. They also let users trade interest-rate and Bitcoin themes without buying shares of the underlying ETFs.

What the contracts mean for US traders

Although the three contracts reference ETFs listed on NYSE Arca, Binance warned that the products may not be available in every region. A U.S.-listed underlying asset does not automatically make its Binance-linked perpetual contract available to U.S. customers.

Binance.US operates as a separate U.S.-only company with its own governance. Its chief executive, Stephen Gregory, recently said the platform aims to reclaim 20% of the U.S. crypto trading market after a two-year period of regulatory pressure.

Binance.com’s new futures contracts therefore should not be confused with a Binance.US product launch. U.S. traders must consider platform eligibility and local derivatives rules before attempting to access similar leveraged products.

The launch also comes days after Binance placed Across Protocol, Lisk and Stacks under its Monitoring Tag on July 24. Those tokens remain tradable, but Binance is reviewing their volatility, liquidity, development activity and operational risk more closely.

Bitcoin is heading into the final stretch of July under the pressure of shifting US macro expectations, with traders focused on two near-term catalysts: the Federal Reserve’s latest policy decision and new inflation data that could influence rate expectations. At the same time, market participants are watching whether the usual ties between crypto and traditional risk assets are returning or fading—an issue that has become more relevant as equities show signs of wobbling.

With US bond yields elevated and oil reacting to geopolitical developments, the next few days could determine whether Bitcoin’s relatively tight trading behavior turns into a decisive breakout—or a renewed pullback. On-chain signals add another layer: CryptoQuant reports that BTC whale inflows to Binance have cooled materially since mid-June.

Key takeaways

- FedWatch data from CME Group assigns a roughly one-in-three chance of a July hike, while pointing to higher odds for September.

- Markets will get a fresh read on inflation Thursday via the June PCE report, which IMEN expects to moderate to 3.7% year over year.

- Bitcoin’s correlation with major equity indices appears weak on higher timeframes, but geopolitical and macro shocks could re-link the markets.

- CryptoQuant data shows BTC inflows from whales to Binance have fallen as much as 44% since June 12, with retail inflows declining less sharply.

- Technically, Bitcoin is testing a widely watched 50-month trend level, where sell-side activity could determine whether the range holds.

Fed and inflation headline risk returns to the front of crypto

The immediate driver for risk assets remains the US interest-rate outlook. Attention is centered on the Federal Open Market Committee’s decision set for Wednesday, July 29, chaired by Kevin Warsh. Expectations around further tightening have remained volatile, with geopolitical tensions and persistent inflation concerns keeping the possibility of additional rate hikes on the table.

According to CME Group’s FedWatch Tool, the probability of a hike at the upcoming meeting is about 31%, while odds for a September increase are higher—around 50%.

Those expectations were not static. Earlier Monday, oil prices fell about 8% after developments involving the US and Iran paused strikes, according to the article’s reporting. That shift was reflected in Fed pricing as rate-hike odds moved from 37.4% to 33.7%.

Beyond the headline odds, traders are also tracking bond-market signals. Mosaic Asset Company noted in its “The Market Mosaic” newsletter that the 30-year Treasury yield is testing a breakout level. The firm referenced how, in May, the 30-year yield saw a false move above the 5% resistance area that had held since late 2023. A stronger long-end move can still matter for broader financial conditions—even if the long end plays a smaller direct role in funding the government than it once did.

PCE may offer clues on whether inflation is cooling fast enough

Inflation data is the other pillar for the week. On Thursday, markets will focus on the June Personal Consumption Expenditures (PCE) index, with the prior month’s reading described as a three-year high at 4.1% year over year. The report’s importance for crypto lies in how quickly traders can reprice the probability of Fed actions once the inflation trajectory becomes clearer.

The Bureau of Economic Analysis is expected to publish the June PCE numbers (as referenced in the article). IMEN, in an X post cited by the report, predicted that June PCE inflation would come in moderately below May, forecasting 3.7% year over year.

That kind of move could help explain the market’s recent sensitivity. The article notes that June’s PCE release coincided with Bitcoin dipping to macro lows around $58,000, underscoring how inflation surprises can quickly ripple through risk sentiment.

Bitcoin’s equity link looks muted—but not immune

One of the more notable themes from the reporting is that Bitcoin’s correlation with major equity benchmarks has appeared unusually weak on longer timeframes. TradingView data referenced in the article suggests the daily correlation between BTC/USD and the S&P 500—using a 20-week loopback window—is “practically absent,” at levels not seen since March. Against the Nasdaq Composite, the correlation coefficient is reported around 0.11, last observed in mid-February.

That matters because it implies Bitcoin may be trading more on its own set of drivers than pure equity beta. However, the report cautions that bearish macro or geopolitical developments can still force correlations back into view, especially when markets are repricing discount rates.

Equities themselves are not providing a clean tailwind. US corporate earnings have reportedly continued to exceed expectations, but the article points to historically elevated valuations as a reason rallies may struggle to absorb further shocks. It also highlights that several major tech names saw notable drawdowns in the prior week, with “Magnificent 7” losses totaling about 5.3% through Friday, after earlier sell-offs tied to $GOOGL and $TSLA.

Even so, the Kobeissi Letter cited in the article argued that margins and earnings beats remain strong across the S&P 500 so far, and that AI is supporting earnings growth. Investors should recognize the tension here: solid earnings can reduce the immediate pressure, but higher rates can still cap multiples and undermine market breadth.

From exchange flows to BTC price levels: what to watch next

Alongside macro risk, crypto-specific positioning is also under scrutiny. CryptoQuant’s analysis—quoted in the article—focuses on BTC transfer flows to Binance. The firm reports that whale inflows to Binance have dropped by as much as 44% since June 12, while retail inflows have fallen 22%.

In the same blog post referenced by the article, contributor Amr Taha wrote that retail inflows are roughly twice whale inflows, leaving a gap of $3.9 billion. The interpretation offered is that the composition of transfers has shifted: retail participants are currently more active than whales in sending BTC to exchanges.

That distinction matters because exchange inflows can influence sell-side readiness, though it does not automatically translate into immediate selling. Still, Taha frames the FOMC meeting as a “major macro catalyst” that could test whether this divergence between retail and whale behavior persists or starts to converge.

The report also points to signs of active redistribution at Binance, noting single-day withdrawals of over 9,000 BTC last week, as previously covered by Cointelegraph.

On the market chart, Bitcoin’s near-term behavior remains range-bound. After the Sunday weekly close, the article says BTC reached a local high of $65,680 on Bitstamp, but it remains engaged in a familiar contest with the 50-month exponential moving average trend line. Trader and analyst Rekt Capital is cited warning that sell-side pressure appears to be building at this resistance area.

Rekt Capital’s view, as quoted, is that if seller volume dominates while Bitcoin is held at resistance, rejection becomes more likely. The analysis also references the 200-week simple moving average, describing price as “sandwiched” between the 200-week SMA and the 50-month EMA—setting up a scenario where continued compression could eventually force a volatility expansion.

For traders and long-term observers alike, the next key questions revolve around whether macro data and the Fed decision reinforce current risk pricing or trigger a sharper repricing. If PCE and post-FOMC guidance confirm a higher-for-longer path, Bitcoin’s exchange-flow shifts and its resistance-area compression may matter more than usual; if inflation cools meaningfully, the market could regain room to break out of its current “boring” range.

Crypto World

CME launches single stock futures enabling investors to trade SpaceX, Micron and others 23 hours a day

Sopa Images | Lightrocket | Getty Images

Investors looking to wager on stocks such as SpaceX and Micron Technology now have a new tool: single-stock futures that trade for nearly 24 hours a day.

CME Group on Monday launched cash-settled single-stock futures on 55 U.S. equities, along with micro-sized contracts on 22 names, marking the exchange’s push into a market designed to let investors take leveraged long or short positions around the clock.

The contracts trade on CME’s Globex platform from Sunday evening through Friday afternoon, with a one-hour daily maintenance break, enabling investors to respond to earnings and other market-moving events outside regular U.S. stock market hours.

The lineup includes futures tied to SpaceX, one of Wall Street’s most closely watched recent IPOs, as well as Micron Technology, Nvidia, Tesla and Apple. Standard contracts represent 100 shares of the underlying stock, while micro contracts represent 10 shares.

“Retail brokers have characterized the launch as the year’s largest retail growth catalyst, with more than 35 retail partners targeting day one/week one readiness,” Morgan Stanley analyst Michael Cyprys said in a note.

CME said the products are designed to offer a simpler way to express bullish or bearish views than options. Unlike options, single-stock futures do not involve time decay or changing implied volatility, while requiring only a fraction of the capital needed because they are traded on margin. The contracts are cash settled, with final settlement based on the stock’s official closing price at expiration. They do not represent ownership in the companies.

The exchange said it may expand the lineup beyond the initial 55 stocks based on customer demand and its listing standards.

Exchange stocks like CME have come under pressure this year as perpetual futures emerging on overseas exchanges are seen as a rising threat to the traditional trading businesses even though most are currently not legal in the U.S.

CME, YTD

Kalshi and Coinbase were given the greenlight this year by the CFTC to offer cryptocurreny related ‘perps’, which are futures contracts without an expiration date. The regulatory move was seen as foreshadowing a wider approval for these types of products on equities. The overseas equity perps were in the spotlight ahead of the SpaceX IPO with international platforms like Hyperliquid offering perpetual futures in the Elon Musk space company ahead of its official debut.

Securitize gains SEC adviser status as SECZ falls 10%

‘Tracker’ Officially Returns in 3 Months

How Callaway rebuilt its golf ball and why the Chrome Tour X settled in my bag

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World6 days ago

Crypto World6 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat6 days ago

NewsBeat6 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech17 hours ago

Tech17 hours agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Tech7 days ago

Tech7 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech7 days ago

Tech7 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

Business6 days ago

Business6 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment6 days ago

Entertainment6 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Crypto World5 days ago

Crypto World5 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics7 hours ago

Politics7 hours agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

NewsBeat7 days ago

NewsBeat7 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Sports21 hours ago

Sports21 hours agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Sports4 days ago

Sports4 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

News Videos4 days ago

News Videos4 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Fashion4 days ago

Fashion4 days ago16 Dresses for the High Summer Event

-

Politics1 day ago

Politics1 day agoSpain sweeps the board at 2026 World Cup with individual awards

-

Crypto World7 days ago

Crypto World7 days agoAndrew Cuomo joins OKX board as crypto exchange expands in U.S.

-

Entertainment3 days ago

Entertainment3 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

News Videos21 hours ago

News Videos21 hours agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Crypto World1 day ago

Crypto World1 day agoXRP Ledger adds $2.6B as RWA inflows rank second

You must be logged in to post a comment Login