Crypto World

The real race isn’t Bitcoin vs. Ethereum. It’s the US vs. China on digital money

While crypto Twitter argues about Bitcoin versus Ethereum, two superpowers are quietly running a different race. The United States is using dollar-backed stablecoins to extend the dollar’s reach into every corner of the digital economy. China is using its e-CNY and the mBridge platform to build an alternative settlement system that bypasses the dollar entirely. The outcome will shape the next century of global finance. And almost nobody outside policy circles is paying attention.

Summary

- The United States has used dollar-backed stablecoins and the GENIUS Act to expand the dollar’s role across global digital payments and crypto networks.

- China has accelerated cross-border use of the eCNY through mBridge and new interest-bearing wallet policies tied to its state-controlled digital currency system.

- Despite de-dollarization efforts from BRICS nations, dollar-pegged stablecoins still dominate global digital settlement activity and reinforce demand for U.S. dollar assets.

The argument that misses the actual fight

Open any crypto publication this year, and you will find some version of the same debate. Bitcoin maximalists versus Ethereum supporters. Solana versus Ethereum. Layer ones versus layer twos. The tribal warfare is loud, it is entertaining, and it is mostly beside the point.

While that argument fills the timelines, a different and far more consequential race is being run by people who do not post memes. The United States Treasury and the People’s Bank of China are competing to define what money looks like for the next century. They are doing it in plain sight, in policy documents and central bank press releases, with two completely different theories of the case.

The American theory: extend the dollar’s reach into every digital corner of the global economy by privatizing it, regulating it, and shipping it on open networks. The Chinese theory: build a sovereign digital currency under direct state control, and link it together with friendly central banks into a parallel settlement system that does not need American rails at all.

This is the real race. It will decide whether the global financial system of the 2030s and 2040s stays dollar-denominated and U.S.-administered, or whether it splits into competing blocs with different reserve assets, different settlement rails, and different rules. The stakes are not the price of a token. They are the architecture of money itself.

What the United States is actually doing

The American strategy is easier to miss because it is being run by the private sector with regulatory blessing rather than by a central bank. But the strategy is explicit, and it has been spelled out at the highest levels of the U.S. Treasury.

The instrument is the stablecoin. The framework is the GENIUS Act, signed into law in July 2025. The thesis was stated bluntly by Treasury Secretary Scott Bessent: stablecoins are a way to “extend the dollar’s reach” in decentralized finance and cross-border payments. Crypto commentator Arthur Hayes has put it more starkly. Stablecoins, in his framing, work as on-ramps that redirect offshore liquidity into U.S. Treasury bills. Every USDT or USDC in circulation requires reserves, and those reserves sit mostly in dollar-denominated assets. Tether alone now holds roughly $113 billion in U.S. Treasuries as of Q1 2026. The stablecoin sector, in aggregate, has become one of the largest non-sovereign buyers of U.S. government debt.

This is not an accident. It is the strategy. By making it easy, legal, and trusted to hold a dollar-pegged token on any blockchain in the world, the United States has effectively privatized dollar issuance and shipped it through global crypto networks. A small-business owner in Lagos who takes payment in USDT, a remittance recipient in Manila who saves in USDC, and a Lebanese citizen who holds stablecoins because the local currency is collapsing are each, without knowing it, deepening dollar penetration into their local economies. They are also indirectly financing the U.S. Treasury market.

The numbers are now large. Fiat-backed stablecoin supply crossed $319 billion in April 2026. Adjusted transaction volume hit $10.9 trillion in 2025, with some estimates putting total settlement volume past $33 trillion, more than Visa. Roughly ninety-nine percent of fiat-backed stablecoin value is pegged to the dollar. The euro, the yuan, the yen, and every other currency together account for the remaining one percent. In digital money, the dollar is not winning. It has, so far, lapped the field.

The genius of this approach, from the U.S. perspective, is that it works without the political baggage of a U.S. central bank digital currency. There is no Federal Reserve digital dollar to argue about. There is no surveillance state implication. There is only a regulated private sector building products that happen to pour offshore savings into U.S. debt and pull the global digital economy toward dollar-denominated settlement. The state does not have to build the rails. It just has to make them legal and trusted.

The GENIUS Act is the legal scaffolding. It defines payment stablecoins as a distinct regulated category, requires one-to-one reserve backing in high-quality liquid assets, opens issuance to banks under OCC supervision, and creates a U.S.-supervised path that competes structurally with foreign stablecoins. Tether’s planned U.S. domestic stablecoin launch fits this pattern. So does the Trump administration’s USD1 stablecoin, marketed openly as a “digital dollar for the world.” The U.S. is not building one digital dollar. It is building an entire ecosystem of them, each privately issued, each pushing toward the same outcome.

What China is actually doing

China is running a different play, executed by the state directly and aimed at a different goal.

The e-CNY, the digital yuan, is the world’s largest live central bank digital currency. By late 2025, cumulative transaction value had crossed $2.3 trillion. Twenty-nine pilot cities have integrated it into public transit and retail. 180 million wallets have been created. Domestic adoption still trails Alipay and WeChat Pay, but the gap is closing, and on January 1, 2026, the People’s Bank of China made a structural change that rewrote the asset’s economic logic.

Until that date, the e-CNY was classified as M0, basically digital cash, and could not earn interest. From January 1, 2026, banks are permitted to pay interest on verified digital yuan wallets, and the e-CNY is treated as a deposit-like instrument with commercial banks as counterparties. The currency is now covered by China’s national deposit insurance. In plain language: the e-CNY went from a digital substitute for paper money to a digital substitute for a bank account. The incentive to hold it just got dramatically larger.

That domestic change is half the story. The other half is happening across borders.

Project mBridge, the cross-border CBDC platform jointly developed by the People’s Bank of China, the Bank for International Settlements, and the central banks of Thailand, the UAE, and Hong Kong, processed over $55 billion in transactions by late 2025. The e-CNY accounts for more than 95 percent of mBridge settlement volume. Cross-border e-CNY activity overall reached roughly $2.38 trillion by November 2025, an 800 percent expansion since 2023. China launched its e-CNY International Operation Center in Shanghai in September 2025. Pan Gongsheng, the PBOC governor, has explicitly framed the goal as building “a more multi-polar monetary system less vulnerable to politicization.” It is a polite way of saying: a system the United States cannot weaponize.

The expansion is mapped. The PBOC’s 2026 work plan includes new cross-border pilots with Singapore, Thailand, Hong Kong, the UAE, and Saudi Arabia. A retail e-CNY pilot is now operating in Laos, where Chinese tourists can scan QR codes at participating local merchants and settle directly in digital yuan. The 15th Five-Year Plan (2026-2030) explicitly mandates active participation in international digital-currency governance. A new e-CNY measurement, management, and ecosystem framework took effect on January 1, 2026.

The pattern is consistent. China is building a digital settlement system that is sovereign, state-controlled, interest-bearing, and designed to operate at the edges of its trade and political alliances. It does not need to displace the dollar globally. It needs to offer a credible alternative for the share of the world economy that already does business inside China’s orbit, or that wants the option not to depend on U.S. payment infrastructure. That is a smaller target than “replace the dollar,” and a much more achievable one.

The paradox at the heart of the race

Here is where the story gets interesting, and where most coverage gets it wrong.

The de-dollarization push has not been a clean fight. The BRICS bloc, now expanded with Indonesia and partner status for nations from Belarus to Vietnam, represents close to forty percent of global GDP by purchasing power parity. Russia and China settle around ninety percent of their bilateral trade in rubles and yuan. The dollar’s share of BRICS trade has fallen from 79 percent in 2022 to 58 percent by mid-2025. BRICS Pay and mBridge are building a real alternative payment infrastructure. The political will to escape the dollar is the strongest it has been in decades.

And yet the dollar’s overall position has, on the most important metrics, strengthened.

The Bank for International Settlements’ 2025 Triennial Survey, the most authoritative measure of global currency usage, found the dollar was on one side of 89.2 percent of all foreign exchange transactions in April 2025, up from 88.4 percent in 2022. The renminbi’s share rose to 8.5 percent, a meaningful increase, but still a fraction of the dollar’s. The dollar’s reserve share has dropped gradually, from 72 percent in 2001 to roughly 58 percent in 2026, but the pace is erosion, not collapse.

The paradox is that stablecoins, the very instrument that lets a Russian importer or an Iranian merchant settle a transaction without touching the U.S. banking system, are themselves overwhelmingly dollar-pegged. Ninety-seven percent of the stablecoin market is denominated in dollars. So when a BRICS-aligned exporter in Brazil sells soybeans to a buyer in the UAE and they choose to settle in stablecoins to avoid U.S. correspondent banking, they are still, in effect, transacting in dollars. They have escaped American banks. They have not escaped the dollar.

This is the contradiction at the heart of the de-dollarization movement, and the unstated reason the U.S. is comfortable with stablecoins extending into hostile jurisdictions. Even the workarounds reinforce the system. As Tether’s CEO Paolo Ardoino has argued, stablecoins like USDT reinforce dollar hegemony precisely by offering a decentralized alternative that happens to be dollar-pegged. The political instinct to flee the dollar runs straight into the practical reality that no other currency offers comparable depth, liquidity, or trust.

The economist Brad Setser at the Council on Foreign Relations has flagged a related paradox. U.S. policy that tries to coerce countries into using the dollar, through tariff threats or sanctions, may actually speed up the search for alternatives. The dollar’s strength comes partly from being the path of least resistance. The moment it becomes a path of political compulsion, more actors will pay the cost of building around it.

The Trump administration’s repeated tariff threats against BRICS members for “de-dollarization” arguably did more to motivate alternative-payment-system construction than any Russian or Chinese initiative could have on its own.

So the race is not as simple as U.S. versus China. It is a contest in which the dominant power, the United States, is winning on infrastructure expansion while at the same time creating the political conditions that push counterparties to keep building alternatives. And it is one in which the challenger, China, is building a real, scaled alternative for a narrower slice of the world even as its broader currency, the renminbi, stays structurally constrained by capital controls and limited convertibility.

What the EU and the rest of the world are doing

The two-power framing of “U.S. versus China” is the loudest version of the race, but it is not complete. Two other actors matter.

The European Union has its own model, anchored by the Markets in Crypto-Assets regulation (MiCA), which has been in phased application since 2024. MiCA created a comprehensive licensing regime for stablecoin issuers operating in the EU and is widely considered the most carefully designed regulatory framework of the three. The European Central Bank is also developing a digital euro on a slower timeline, with implementation realistically running into 2027 and beyond. The euro’s share of global FX reserves has actually grown in 2025 as central banks diversify out of dollars, but the eurozone’s structural weakness, a shared currency without a shared treasury, limits how far the digital euro can carry the bloc’s monetary ambitions.

Other CBDC projects are real but smaller. The Bahamas, Jamaica, and Nigeria have launched retail CBDCs with mixed adoption. India’s UPI-linked CBDC pilot is one of the most operationally significant in the developing world. The UK and Japan are advancing slowly on their own digital currency designs. None of these projects threatens the dollar-yuan binary, but several stretch the architecture of state-backed digital money beyond the two superpowers.

The most interesting wildcard is the Global South. Stablecoins, particularly USDT, have quietly become a de facto financial layer in dozens of countries where local currencies are weak or banking is shallow. The 400 million-plus users who now rely on dollar-backed stablecoins are mostly outside the U.S., and many are in jurisdictions where their own governments would, politically, prefer they not use the dollar. The American digital-dollar empire is being built largely by people who do not live in America.

What actually matters from here

Three things to watch over the next two to three years will tell you which way this race is bending.

The first is how the e-CNY’s interest-bearing transition affects cross-border adoption. If digital yuan deposits become an attractive store of value in countries that already do significant trade with China, the dollar’s grip on those corridors weakens. If the transition is mostly a domestic event and the e-CNY remains a thin layer for cross-border trade between China and a handful of allies, the dollar holds.

The second is whether the United States can keep stablecoin expansion uncoupled from political backlash. The Hudson Institute and other Washington policy shops are openly arguing for stablecoin promotion as a counter to BRICS. That framing, useful in policy memos, becomes a liability the moment foreign governments start to see USD-pegged stablecoins as instruments of U.S. strategy rather than neutral infrastructure. The current strategy works because it does not look like a strategy. The moment it does, the political costs of using it rise sharply in target jurisdictions.

The third is the technology layer. The next decade of payments will involve programmable money, AI agents transacting on their own, tokenized real-world assets, and settlement networks that move money in seconds at near-zero cost. The system that wins those use cases at scale wins the next layer of finance. The U.S. has more developer momentum, more capital, and more open networks. China has more state coordination, more captive trade flows, and a willingness to mandate adoption that no democratic system can match. Both edges matter.

What this means in the end

The crypto industry has spent a decade explaining itself to outsiders as a fight between competing technologies. Bitcoin or Ethereum. Proof-of-work or proof-of-stake. Layer one or layer two. Those are interesting debates, and they will continue. But they are debates inside a smaller story.

The bigger story is that two states have realized digital money is now a geopolitical instrument, and they are competing to define what it looks like. The United States is using regulated private stablecoins to spread the dollar at internet speed into the global digital economy. China is using a state-issued, interest-bearing digital currency and a parallel settlement network to build an exit ramp for the share of world commerce that wants one. Every other digital money story is, in one way or another, downstream of those two strategies.

For an investor, the implication is that the assets sitting closest to that geopolitical contest, dollar stablecoin issuers, infrastructure providers, payment rails, on/off-ramp networks, will likely matter more over the next decade than the latest layer-one token battle. For a holder of any cryptocurrency, the implication is that the regulatory environment your asset operates in is being shaped by considerations far larger than crypto itself. The CLARITY Act will pass or not pass partly based on how policymakers read the U.S.-China contest. The GENIUS Act was already passed partly because of it.

For everyone else, the implication is simpler. The future of money is being decided right now, not in white papers or token launches but in central bank press releases and Treasury speeches. The next time you read a thread about whether Bitcoin or Ethereum is the future, remember that both of them will end up settling, on the margin, in dollar-pegged stablecoins or yuan-denominated CBDCs. The interesting question is not which crypto wins. It is which currency?

The race that matters is not Bitcoin versus Ethereum. It is the dollar versus the yuan, in digital form, for the architecture of how money moves for the next hundred years. And it is happening right now, while almost nobody is looking at the right scoreboard.

This article is for informational purposes and does not constitute financial or investment advice. Geopolitical and monetary policy developments evolve quickly; the figures and policy positions described reflect reporting available as of mid-May 2026. Always do your own research.

Crypto World

Iren (IREN) Stock Surges on Jefferies Buy Rating: AI Infrastructure Play Gains Momentum

TLDR

- Jefferies launched coverage of Iren (IREN) with a Buy recommendation and $79 price objective; shares were hovering near $58.11.

- The stock rallied approximately 5% during premarket hours Thursday after the bullish analyst report.

- Analysts emphasized IREN’s approximately 6 gigawatt land portfolio and fully integrated GPU cloud infrastructure.

- The firm has secured a five-year, $9.7 billion agreement with Microsoft and a $3.4 billion Nvidia AI cloud partnership, aiming for $3.1 billion in yearly recurring revenue.

- Revenue at IREN surged 105% in the trailing twelve-month period as the business shifted from cryptocurrency mining operations to AI infrastructure services.

Shares of Iren (IREN) gained approximately 5% during Thursday’s premarket session following Jefferies’ initiation of coverage featuring a Buy recommendation and a price objective of $79. Trading around $58.11 when the coverage began, the target represents potential upside of roughly 36%.

Jefferies analyst Jonathan Petersen spearheaded the coverage launch, emphasizing IREN’s standing as a fully integrated AI cloud infrastructure company backed by an extensive powered land portfolio spanning approximately 6 gigawatts.

The investment firm underscored IREN’s strategic partnerships with Microsoft and Nvidia as fundamental pillars supporting the bullish thesis. Combined, these agreements are projected to generate $3.1 billion in recurring annual revenue.

The Microsoft partnership encompasses a five-year arrangement valued at $9.7 billion for Nvidia GB300 GPU infrastructure, centered at IREN’s 200 MW Childress location. The deal structure features a $1.9 billion advance payment alongside $3.65 billion in GPU financing carrying approximately 6% interest.

According to Jefferies, this framework enables IREN to recover its $8.8 billion capital outlay during the contract period, delivering unlevered internal rates of return above 20%.

Additionally, IREN maintains a distinct $3.4 billion AI cloud partnership with Nvidia. Jefferies noted these strategic relationships position IREN alongside industry players like CoreWeave (CRWV) and Nebius (NBIS) in the competitive landscape.

Transformation From Cryptocurrency Mining to AI Cloud Services

IREN originally operated predominantly as a Bitcoin mining operation. The organization has successfully transitioned into a vertically integrated AI cloud infrastructure provider, a transformation Jefferies characterized as a “compelling strategic pivot.”

Revenue climbed 105% during the trailing twelve months, demonstrating the velocity of this operational shift.

Controlling its own real estate and data center facilities provides IREN with operational agility to accommodate diverse customer requirements — ranging from powered shell environments to comprehensive GPU cloud implementations, according to Jefferies.

Geographic Growth Into European and Australian Markets

Beyond its current operations in the United States, IREN recently finalized the purchase of Ingenostrum, S.L., operating as Nostrum Group, a Spanish AI data center developer. This transaction delivers approximately 490 megawatts of secured, grid-connected capacity and represents IREN’s inaugural expansion into Europe.

IREN has also executed a transmission connection agreement for a projected 800 MW data center facility in Bundey, South Australia — anticipated to rank among the largest data center installations across the Asia-Pacific geography.

After the Australian development announcement, B. Riley elevated its price target on IREN to $96 while maintaining a Buy rating. Macquarie reaffirmed an Outperform stance with a $90 price objective.

Needham has adopted a more conservative perspective, reducing its financial estimates for IREN based on expectations of a slower AI cloud revenue acceleration extending through calendar year 2026 and diminished forecasts for Bitcoin-related contributions.

The stock has delivered approximately 493% returns over the preceding twelve-month period.

US President Donald Trump took it to his social media platform Truth Social to declare that oil has begun flowing, jobs are at record levels, and prices in the US are dropping, which will increase affordability.

While there are some controversies about the last few statements, oil prices are indeed dropping now, with USOIL dipping below $73 per barrel.

Today’s decline to $73 and just under it means that USOIL has dropped by roughly 40% since the peak after the war broke out at almost $120 per barrel. However, its price is yet to reach the lows before the US and Israel started the war against Iran.

Trump also said Iran “can never have a nuclear weapon,” which will make the world safer, as part of the Iran-US deal that is reportedly agreed to, but it’s still not signed.

The POTUS also bragged that the “stock markets are roaring, jobs are at records, and prices are dropping (affordability). He explained that the US is “strong, safe, and respected like never before.” He ended his statement with, “YOU’RE WELCOME!”

It’s worth noting that the US CPI numbers for the past two months hit multi-year highs, so the decline in prices and rising affordability have yet to be proven. The US stock market is close to its record level, but not quite there.

Bitcoin’s price, on the other hand, has followed USOIL’s path south in the past 24 hours. Yesterday’s decline was mostly attributed to the US Fed refusing to change the rates and the new Chairman’s hawkish stance.

Today, though, BTC dipped once again to $63,600 after Trump’s statement went live. Although it rebounded to $64,200 immediately, it was stopped once again and now sits well below $64,000.

The post Trump Says ‘You’re Welcome’ as Oil Is Flowing and Prices Are Dumping appeared first on CryptoPotato.

U.S. regulators have proposed requiring certain payment stablecoin issuers to verify customer identities under a new rule issued as part of the GENIUS Act framework.

Summary

- U.S. regulators have proposed requiring certain payment stablecoin issuers to adopt customer identification programs similar to those used by banks and credit unions.

- The proposed GENIUS Act rule would require issuers to verify customer identities while treating permitted payment stablecoin issuers as financial institutions under the Bank Secrecy Act.

- Regulators said secondary market stablecoin transactions generally would not trigger customer identification requirements, limiting the rules to direct relationships between issuers and customers.

The Federal Reserve Board said Thursday that it is seeking public comment on a joint proposal that would require covered stablecoin issuers to maintain effective Customer Identification Programs, or CIPs.

The proposal was issued alongside the Financial Crimes Enforcement Network, the Federal Deposit Insurance Corporation, the Office of the Comptroller of the Currency, and the National Credit Union Administration.

An 117-page notice published by the agencies said the rule would implement provisions of the Guiding and Establishing National Innovation for U.S. Stablecoins Act, known as the GENIUS Act. The proposal would formally treat permitted payment stablecoin issuers as financial institutions under the Bank Secrecy Act and require them to maintain customer identification procedures.

Comments on the proposal will be accepted for 60 days after publication in the Federal Register.

Rule would apply bank style identity checks to stablecoin issuers

The agencies said permitted payment stablecoin issuers would need to collect and verify customer information before opening an account relationship. Required information would generally include a customer’s name, address, date of birth or formation, and identification number.

The proposal would require issuers to adopt risk-based procedures designed to establish a reasonable belief that they know the true identity of each customer. Regulators said those procedures should take into account an issuer’s size, business model, customer base, account types, and methods used to open accounts.

“This is the next step to ensure that permitted payment stablecoin issuers are fully integrated into Bank Secrecy Act regulations,” NCUA Chairman Kyle Hauptman said, adding that the proposal mirrors existing customer identification requirements used by credit unions and sets standards for identifying and verifying account holders.

“It sets clear standards for identifying and verifying account holders and safeguards the interests of credit unions and their members. By establishing robust customer identification requirements, we are reinforcing our commitment to preventing money laundering and terrorist financing in our financial system.”

The proposal follows earlier NCUA rulemakings related to payment stablecoins. The agency said it issued a proposed rule last month covering operational and risk management standards for licensed payment stablecoin issuers and released a separate proposal in February 2026 governing applications from issuers under its jurisdiction.

Regulators exclude most secondary market transactions

The proposed rule draws a distinction between direct dealings with a stablecoin issuer and transactions that occur elsewhere in the market.

Regulators said customer identification requirements would apply when a user establishes a formal relationship with a permitted payment stablecoin issuer through activities such as issuance, redemption, custody, reserve management, or other authorized services.

The agencies also proposed that simply holding or transferring a payment stablecoin would not create an account relationship with the issuer. The document states that secondary market activity, including transfers between users and transactions conducted through intermediaries, generally would not trigger customer identification obligations for the stablecoin issuer.

The agencies said applying customer identification requirements to every stablecoin transfer could be impractical because issuers often do not have direct relationships with users participating in secondary market transactions.

The proposal arrives days after a bipartisan group of U.S. senators urged the Treasury Department to preserve a role for state regulators under the GENIUS Act. In a June 16 letter to Treasury Secretary Scott Bessent, lawmakers led by Senator Cynthia Lummis asked Treasury to provide clearer guidance on how states can obtain certification for their own stablecoin regulatory frameworks.

The GENIUS Act allows issuers with no more than $10 billion in outstanding stablecoins to operate under certified state regulatory regimes. The customer identification proposal states that its requirements would apply not only to federally supervised issuers but also to stablecoin issuers operating under eligible state frameworks established under the law.

Crypto World

International Business Machines (IBM) Stock Slides 4% Following Accenture Revenue Warning

Key Takeaways

- IBM shares declined more than 4% in Thursday’s premarket session following Accenture’s reduced fiscal 2026 revenue outlook

- Accenture revised its annual sales forecast to $71.76B–$72.46B, lowering the previous upper target of $73.16B

- Despite Accenture posting Q3 EPS of $3.80 that surpassed projections, its $18.7B quarterly revenue fell short of the $18.745B analyst forecast

- According to GF Value metrics, IBM trades at approximately 9.9% above fair value at $262.35, carrying a GF Score of 78/100

- IBM’s Q2 financial results are scheduled for release on July 22, with Wall Street projecting $3.00 EPS and $17.85B in revenue

Shares of International Business Machines experienced a significant decline Thursday morning after Accenture revised downward the upper limit of its fiscal 2026 revenue forecast, creating headwinds across the IT services industry.

International Business Machines Corporation, IBM

IBM’s premarket price stood at $251.01, reflecting a 4.32% decline for the session. The stock had previously closed at $262.35 on June 17, marking a 3.1% drop from the day before.

The downturn wasn’t the result of IBM-specific developments. Rather, market participants reacted to Accenture’s adjusted financial projections.

Accenture tightened its annual revenue forecast to between $71.763 billion and $72.460 billion, reducing the prior high-end estimate of $73.157 billion. Market analysts had anticipated $74.006 billion for the full year.

This type of forecast adjustment typically creates downstream effects among industry competitors — and IBM became a casualty of that sector-wide pressure.

From a profitability standpoint, Accenture exceeded expectations on earnings. The company delivered Q3 diluted EPS of $3.80, surpassing the $3.69 analyst estimate. However, quarterly revenue of $18.700 billion narrowly missed the $18.745 billion consensus figure, and the forward-looking guidance adjustment triggered the sector weakness.

Accenture CEO Julie Sweet highlighted robust artificial intelligence demand, citing 104 client agreements worth $100 million or more year-to-date through Q3, representing 13% growth. The firm also revealed intentions to acquire majority ownership in Dragos while purchasing runZero and NetRise outright, expanding its operational technology cybersecurity capabilities.

IBM’s Q2 Financial Release Approaches on July 22

IBM’s quarterly financial disclosure is set for July 22. Wall Street consensus calls for EPS of $3.00 alongside revenue of $17.85 billion for the second quarter.

During Q1, IBM delivered EPS of $1.91, exceeding the $1.81 projection. Revenue reached $15.92 billion, topping the $15.66 billion consensus estimate. This performance extended IBM’s streak of surpassing EPS forecasts to eight consecutive quarters — a pattern investors will monitor closely in the upcoming report.

Current Valuation Analysis

GuruFocus estimates IBM’s GF Value at $238.63, indicating the stock traded at approximately a 9.9% premium relative to this fair value calculation when priced at $262.35.

IBM’s present P/E ratio of 23.2x registers modestly below its five-year median of 24.4x. The forward-looking P/E stands at 21.1x.

The company’s GF Score of 78/100 indicates above-average positioning versus industry peers, with profitability representing the strongest metric at 8/10. Financial strength registers at 5/10, while momentum scores 4/10 — the latter aligning with Thursday’s negative price action.

Notably, insider transaction records show zero activity over the preceding three-month period.

IBM’s 52-week trading range spans from $212.34 to $332.46, positioning Thursday’s premarket level of $251.01 in the lower portion of that spectrum.

The next significant market-moving event for IBM arrives on July 22.

Bitcoin lending platform Ledn has expanded its services to include Tether Gold (XAUt), allowing investors to hold the tokenized asset and borrow against it in much the same way they can borrow against Bitcoin.

Ledn announced Thursday that clients can use XAUt as collateral for loans instead of selling their holdings for cash. Under the company’s existing lending model, client collateral is held one-to-one and is not rehypothecated, lent out or used to generate yield.

Loans are issued and repaid in Tether’s USDT or USAt stablecoins and can be repaid at any time without scheduled monthly payments. Tether launched USAt in the United States in January as a stablecoin designed to comply with the GENIUS Act.

The launch expands the range of digital assets that can be used as loan collateral, giving investors another way to access liquidity without triggering a taxable sale. While Bitcoin-backed lending has become a common feature of the crypto market, the addition of tokenized gold reflects growing efforts to bring real-world assets into digital asset financial services as gold prices hover near record highs.

The new products are rolling out across most jurisdictions where Ledn operates but are not currently available in Canada or the European Union.

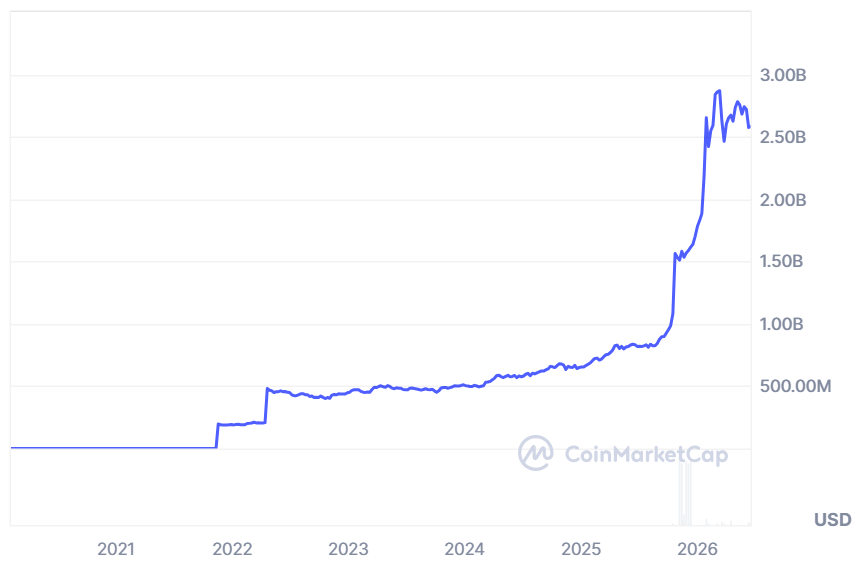

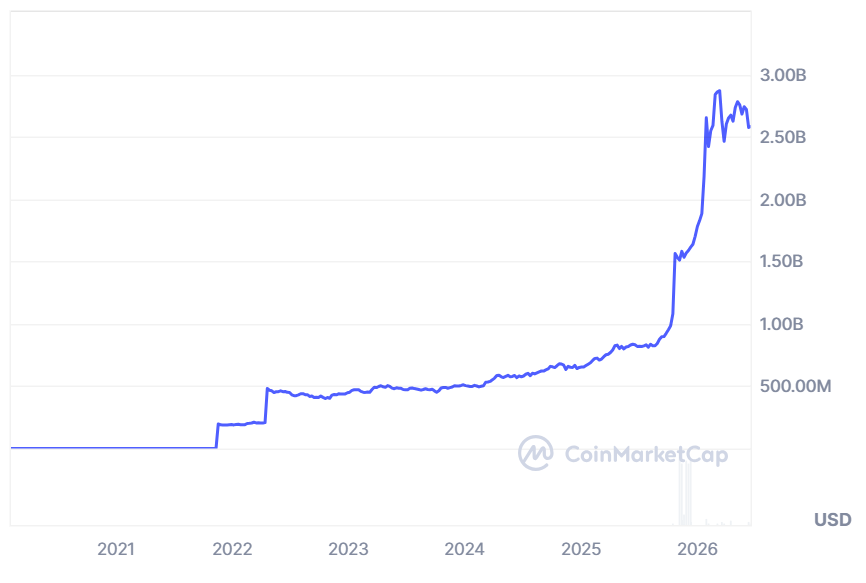

The market capitalization of Tether Gold peaked at around $2.89 billion. Source: CoinMarketCap

Related: Tether makes $150M investment in Gold.com in latest gold play

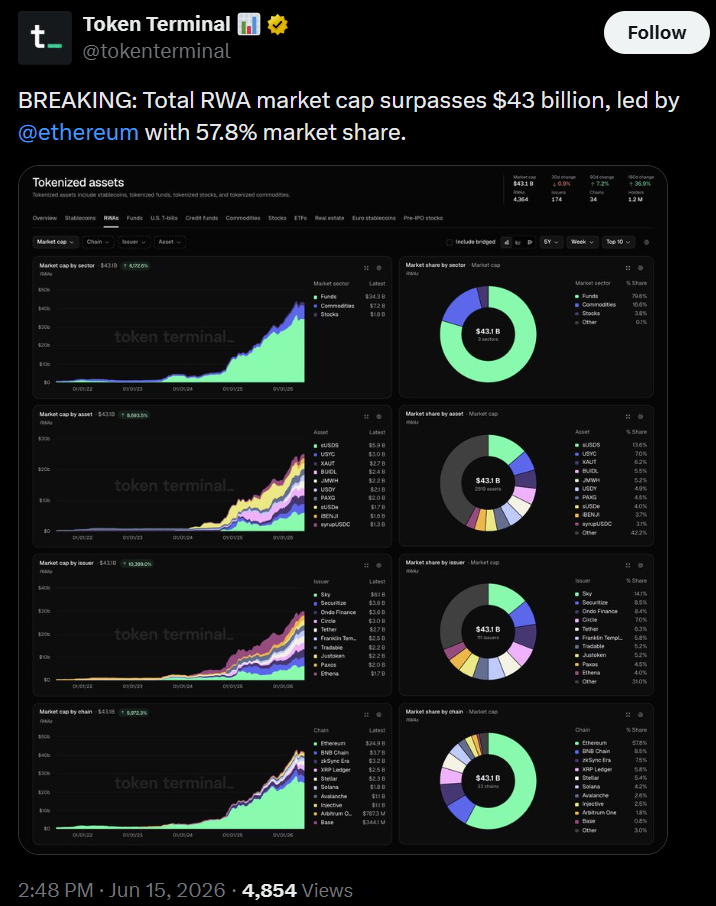

Tokenized commodities gain traction in RWA market

The announcement comes as commodities play an increasingly prominent role in the tokenization market. According to a recent Token Terminal report, tokenized financial assets have surpassed $43 billion, with commodities accounting for nearly 17% of the market.

Unlike commodity derivatives and futures, tokenized assets such as gold are backed by the underlying asset, giving holders direct ownership while enabling faster transfers and trading on blockchain networks.

Commodities account for a bigger share of the tokenization market.

Source: Token Terminal

Tether Gold benefited from this year’s rally in bullion prices, with the token’s market capitalization expanding as gold climbed to record highs above $5,600 per troy ounce. The precious metal has since pulled back to around $4,300 an ounce but remains up on the year.

Google, for example, has warned organizations to begin preparing for the transition to post-quantum cryptography and has been integrating quantum-safe cryptographic standards into parts of its infrastructure with a 2029 completion target. The U.S. National Institute of Standards and Technology (NIST) has been leading efforts to standardize post-quantum algorithms and has set timelines for the eventual retirement of certain legacy cryptographic systems.

Within crypto, several major ecosystems have elevated quantum preparedness as a strategic priority. The Ethereum Foundation earlier this year announced a dedicated post-quantum security initiative aimed at researching migration paths for blockchain’s vast ecosystem of wallets, applications and validators. Solana developers likewise published proposals exploring how users and the network could transition to quantum-resistant cryptography if the threat becomes more immediate.

The Algorand Foundation noted that blockchain networks need to begin making preparations well before a so-called “Q-Day,” the hypothetical moment when a quantum computer becomes capable of breaking the cryptography currently used to secure digital assets.

The foundation said its roadmap builds on work it began in 2022, extending those efforts to the rest of the protocol, with the goal of achieving what Algorand describes as broad quantum resilience by the end of 2027. The foundation said it expects to reach that milestone before NIST retires certain legacy cryptographic standards and three years ahead of a timeline set by the U.S. National Security Agency for national security systems.

- Solana price sits at around $71 with strong resistance at $75.95.

- Indicators and EMAs show a bearish market trend.

- Weekly gains contrast with weak momentum and extreme fear sentiment.

Solana price continues to trade in a tight range around the low $70s, with the asset struggling to reclaim the $72 level.

At the time of writing, SOL was trading near $71.26, after a mild 24-hour decline of about 0.7%.

Despite a stronger weekly rebound of roughly 10%, the broader market pattern still shows clear resistance overhead and weakening momentum across multiple technical indicators.

Over the past 24 hours, the Solana price has remained trapped between $70.69 and $74.24, without a decisive trend forming.

Technical structure still favours sellers

Looking at the charts, Solana (SOL) remains under pressure from a layered resistance structure formed by major moving averages.

Recent price movements show that SOL has only managed to reclaim the 10-day exponential moving average (EMA), while the 20-day, 50-day, 100-day, and 200-day EMAs are all positioned above the current price level.

This configuration confirms that the broader trend remains bearish, as rallies continue to encounter resistance before reaching higher momentum zones.

The most immediate technical barrier is located at $75.95, a level that must be cleared to signal a potential shift in trend direction.

If this level is broken, projections place the next resistance at $83.32.

On the downside, structural support is clearly defined at $62.40.

A breakdown below $62.40 would expose the Solana price to deeper losses, extending the current corrective phase and potentially triggering accelerated selling pressure.

Notably, the daily Relative Strength Index (RSI) is positioned at 44.38, reflecting a neutral condition and suggesting indecision in short-term price direction.

However, the weekly RSI has dropped to around 33.07, placing it near the oversold territory and signalling that while selling pressure has been persistent over a longer timeframe, we could see some bullish recovery soon.

The overall market sentiment remains weak

Sentiment conditions continue to reflect caution across the broader market.

The Fear and Greed Index is positioned near 15, a level typically associated with extreme fear.

Such an environment often coincides with defensive positioning, reduced risk appetite, and lower conviction in upward price movements.

Derivative market data also supports this cautious outlook, with the funding rates remaining negative in recent sessions, while short positioning has increased relative to long exposure.

In addition, the long-to-short ratio has remained below equilibrium levels, indicating that traders are still leaning toward downside protection rather than sustained bullish positioning.

At the same time, Solana has recorded modest institutional inflows, including small allocations into Solana ETFs totalling just over $1 million.

However, these inflows remain limited in size and have not been sufficient to offset broader bearish positioning in derivatives markets.

Key Highlights

-

CoinMENA partners with Standard Chartered for enhanced UAE fiat payment infrastructure

-

Partnership improves funding channels, settlement mechanisms, and operational clarity

-

Standard Chartered broadens services to licensed UAE digital asset platforms

-

CoinMENA strengthens client fund safeguards through enhanced banking infrastructure

-

UAE digital asset platforms increasingly compete on regulated fiat access and settlement quality

The UAE’s digital asset sector has secured another significant banking partnership as CoinMENA announced collaboration with Standard Chartered for fiat payment infrastructure. This arrangement enhances local currency accessibility for platform users and verified partners. The development demonstrates how banking relationships increasingly influence competitive dynamics among licensed digital asset platforms.

CoinMENA Enhances Fiat Payment Infrastructure

Through this partnership, CoinMENA will leverage Standard Chartered’s banking systems to facilitate fiat entry and exit points across the UAE. The platform will implement protected client fund accounts alongside virtual account-based payment mechanisms. Consequently, users can expect improved visibility into funding movements and enhanced settlement workflows.

This collaboration provides CoinMENA with more robust banking foundations as digital asset oversight continues developing throughout the region. The arrangement enables accelerated funding processes, improved transaction monitoring, and enhanced clarity for authorized counterparties. Accordingly, this partnership extends beyond simple payment access to deliver comprehensive operational infrastructure.

CoinMENA functions within an ecosystem where fiat connectivity remains critical for crypto platforms. While users engage with digital assets through blockchain networks, exchanges require traditional banking for local currency operations. Consequently, dependable banking partnerships enhance platform credibility, market liquidity, and user satisfaction.

Standard Chartered Expands Support for Licensed Digital Asset Platforms

Standard Chartered’s involvement illustrates how established financial institutions can facilitate regulated digital asset operations without directly operating trading venues. The institution will deliver payment processing and account management infrastructure rather than proprietary cryptocurrency trading platforms. This model enables banks to participate in sector expansion while maintaining distinct operational frameworks.

The UAE has developed among the region’s most dynamic digital asset ecosystems through comprehensive licensing frameworks and regulatory oversight. Authorities have enabled virtual asset service providers, payment processors, stablecoin initiatives, and financial technology operators. Nevertheless, these enterprises require established banking relationships to achieve meaningful scale.

CoinMENA benefits from this evolution because regulated infrastructure now carries equal importance to platform capabilities. Robust fiat connectivity enables exchanges to accommodate retail customers, high-net-worth individuals, and institutional participants. Simultaneously, Standard Chartered reinforces its presence within UAE digital finance infrastructure development.

UAE Digital Finance Landscape Grows More Competitive

The CoinMENA partnership emerges as additional fintech operators advance their UAE market strategies. Revolut recently obtained Stored Value Facilities and Retail Payment Services authorizations from the UAE Central Bank. These regulatory approvals position the company toward potential market entry.

Revolut intends to deliver multi-currency accounts, payment cards, domestic transactions, and cross-border transfers within a unified application. Its market presence could intensify competition across payments and international money movement. However, these licenses do not necessarily indicate authorization for virtual asset trading activities within the UAE.

CoinMENA advances into this competitive environment equipped with strengthened bank-supported infrastructure for fiat operations. The partnership demonstrates how digital asset platforms require robust compliance frameworks, settlement systems, and client fund governance to achieve sustainable growth. Ultimately, UAE digital finance increasingly depends on regulated infrastructure rather than speculative market momentum.

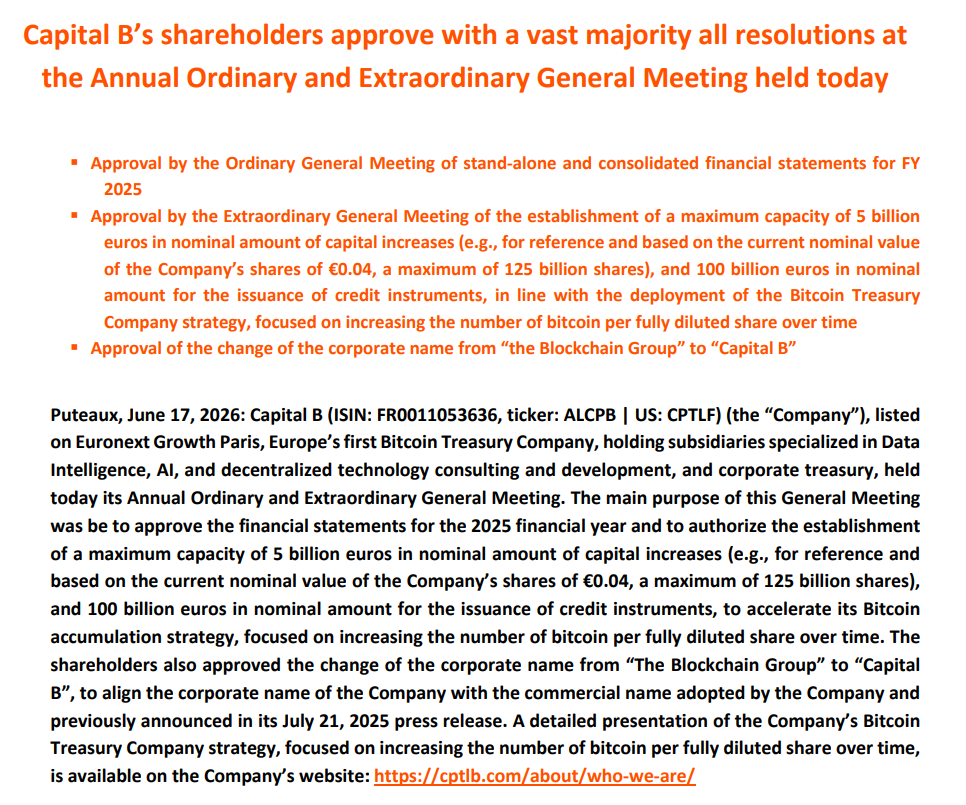

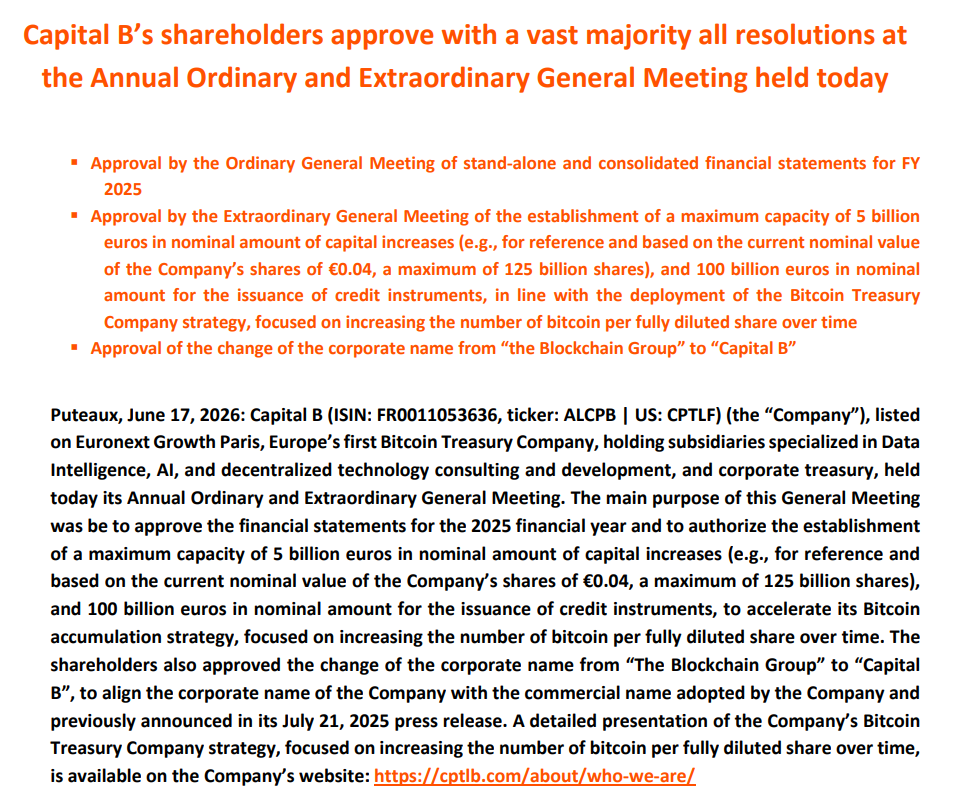

France-listed Bitcoin treasury company Capital B’s shareholders approved authorizations allowing the company to raise up to 105 billion euros ($120.4 billion) to fund future Bitcoin purchases.

Over 95% of shareholders approved the establishment of up to 5 billion euros in capital increases, equivalent to as many as 125 billion new shares at the current nominal value, as well as the issuance of up to 100 billion euros in credit instruments, Capital B announced on Wednesday.

The company said the issuance of the new capital instruments will “accelerate its Bitcoin accumulation strategy, focused on increasing the number of Bitcoin per fully diluted share over time.”

During its general meeting on Wednesday, Capital B reported 300.65 million in total shares with voting rights. If fully exercised, issuing 125 billion in new shares would result in existing shareholders being diluted to about 0.24% of the company’s ownership.

Shareholders also approved changing the company’s name from The Blockchain Group to Capital B, aligning its corporate name with the commercial brand adopted in 2025.

Source: Capital B

Capital B shares were little changed following the announcement, according to Yahoo Finance data.

Crypto treasury companies take different approaches

Capital B is Europe’s second-largest Bitcoin treasury company, holding 3,139 BTC, currently valued at $200 million. It ranks behind Germany-based Bitcoin Group SE, which holds 3,604 Bitcoin, currently worth $230 million, Bitcoin Treasuries data shows.

To date, Capital B said it raised about $325 million in capital, following its $17.8 million raise from strategic investors, including Blockstream CEO Adam Back and Paris-based asset manager TOBAM.

Related: Mystery Bitcoin burn destroys 107 BTC worth about $8.5M

The fundraising initiative contrasts with moves by some treasury companies to reduce or actively manage their Bitcoin exposure.

On May 28, France-based semiconductor company Sequans Communications said it had concluded its previously announced crypto treasury strategy. The company held 658 Bitcoin and said it would “monetize remaining holdings over time,” which led to a share price increase of about 14.5%.

Magazine: Bitcoin, the ‘canary in the coal mine,’ XRP transaction demand falls 91.5%: Market Moves

Crypto World

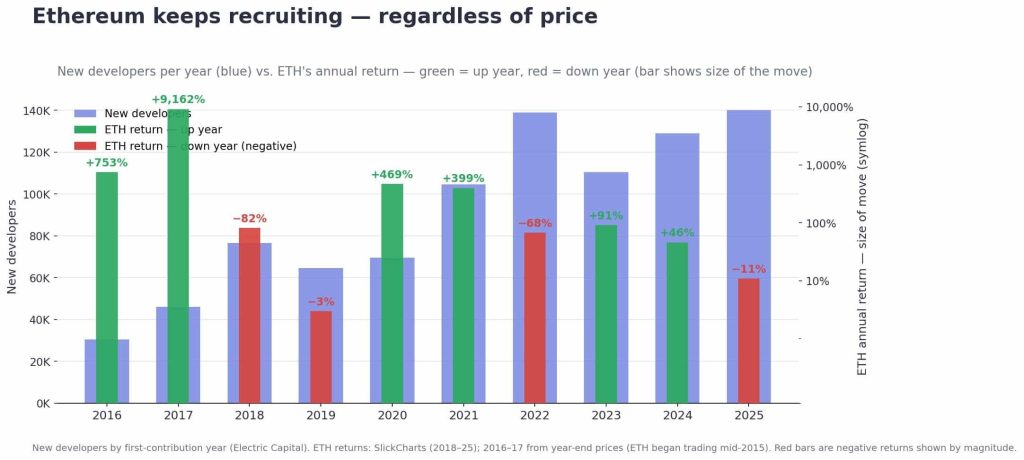

Ethereum News: ETH Developers Hit Near Record Highs Even as ETH Dumped Below $1,750, Is the Network Stronger Than the Price Suggests?

Ethereum News: ETH price is sitting near $1,750, down roughly 1.4% in the last 24 hours, and the bears are clearly running the short-term narrative.

But strip out the price action, and something more durable is happening underneath. Developer growth tells a story that the chart currently refuses to.

New developers building on Ethereum have climbed from approximately 30,000 in 2016 to nearly 140,000 in 2025, and crucially, that growth did not pause during the brutal drawdowns.

When ETH dropped 82% in 2018, roughly 77,000 new developers joined the network anyway. When ETH shed 68% in 2022, new developer additions hit approximately 139,000, one of the strongest cohort years on record.

Even now, with ETH down around 11% year-to-date, developer intake remains close to that same 140K ceiling. Block production has also stabilized near the 7,000-blocks-per-day range since approximately 2023, regardless of where spot price traded.

The gap between price performance and network health is widening. That divergence is worth taking seriously before the next macro catalyst forces a re-rating. Upcoming protocol decisions and FOMC positioning will likely be the near-term triggers that determine which way that gap closes.

Ethereum News: Can ETH Price Reclaim $2,000 or Is a Drop to $1,500 the More Likely Path?

The technical setup is uncomfortable. ETH broke below a key demand zone, and Yahoo Finance’s technical analysis marks $1,700 as the line in the sand, with the path to $1,400 largely unobstructed if that level fails.

Overhead resistance compounds the problem. The 50-day EMA sits near $2,194 and the 200-day EMA near $2,510, and both have capped every recent bounce attempt.

If $1,700 holds as weekly support, macro sentiment stabilizes after FOMC, and ETH reclaims $2,000 within two to three weeks on renewed risk appetite.

However, if $1,700 fails on a daily close, derivatives pressure accelerates the slide toward $1,400-$1,500. Liquidation cascades, not fundamentals, have been the primary driver of recent drawdowns, the flush could move fast rather than gradual.

Standard Chartered and other institutional desks still hold constructive multi-year ETH price targets, which keeps the capitulation thesis incomplete until on-chain accumulation data turns materially bearish.

LiquidChain Could Replace Ethereum For Smart Traders In The Future and Here is Why

When Ethereum bleeds, it tends to flush speculative capital out of the broader ecosystem, and that capital often rotates into early-stage infrastructure plays with asymmetric upside profiles that large-cap ETH can no longer offer at current market cap.

The question is where that rotation lands. Whale accumulation patterns during ETH weakness suggest sophisticated money is positioning in infrastructure, not exiting crypto entirely.

LiquidChain (LIQUID) is an L3 infrastructure project positioning itself as a cross-chain liquidity layer that fuses Bitcoin, Ethereum, and Solana liquidity into a single execution environment.

The core proposition, deploy once, access all three ecosystems, directly addresses the fragmentation problem that costs Ethereum developers time and TVL every cycle.

Key architecture features include a Unified Liquidity Layer, Single-Step Execution, Verifiable Settlement, and a Deploy-Once Architecture designed to reduce cross-chain overhead.

The presale is currently priced at $0.01471 per $LIQUID with $852,080.07 raised to date. As with any early-stage presale, liquidity and execution risk are real — this is not a liquid position and vesting schedules matter.

That said, for traders who want infrastructure exposure without riding ETH’s current technical uncertainty, Visit LiquidChain’s full presale terms here.

The post Ethereum News: ETH Developers Hit Near Record Highs Even as ETH Dumped Below $1,750, Is the Network Stronger Than the Price Suggests? appeared first on Cryptonews.

People power saves popular Coatbridge ice rink as North Lanarkshire Council confirms U-turn on replacement plans

Marvell Technology stock hits all-time high at 324.3 USD

Iren (IREN) Stock Surges on Jefferies Buy Rating: AI Infrastructure Play Gains Momentum

-

Business4 days ago

Business4 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World7 days ago

Crypto World7 days agoOppenheimer backs SpaceX as $70 billion retail frenzy builds

-

Crypto World7 days ago

Crypto World7 days agoMarkets Rally as SpaceX IPO Looms Amid Iran Tensions and Inflation Surge

-

Crypto World4 days ago

Zimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Crypto World5 days ago

Crypto World5 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Tech6 days ago

Tech6 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Tech6 days ago

Tech6 days agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

NewsBeat7 days ago

NewsBeat7 days agoEl Nino has formed in the Pacific and could set records, forecasters say

-

Tech7 days ago

Tech7 days agoDutton Ranch star claims they ‘didn’t see any disruption’ on set following Chad Feehan’s exit from Yellowstone spinoff fueled by Taylor Sheridan clash rumors

-

Entertainment7 days ago

Entertainment7 days agoDonnie Wahlberg & More Heat Up Las Vegas at Circa’s Barry’s Downtown Prime

-

Tech7 days ago

Tech7 days agoOpendoor Ends India Operations, Fueling a Bigger Conversation About AI and Outsourcing

-

Politics7 days ago

Politics7 days agoBelfast burns, while Met chief points finger at Iran and Russia

-

NewsBeat6 days ago

NewsBeat6 days agoFBI searches office of Ohio voter registration group

-

Business7 days ago

Business7 days agoAT&T: Verizon's 27% Outperformance Sets Up A Solid Entry Point

-

Tech7 days ago

Tech7 days agoAnthropic is spending $150M to embed 1,000 AI fellows inside nonprofits. No degree required.

-

Politics7 days ago

Politics7 days agoModi thanks Trump for wishes as US attacks Indian seafarers

-

Entertainment7 days ago

Entertainment7 days ago‘The Pitt’s Fan-Favorite Doctor Confirms Noah Wyle Gave His Blessing to Return [Exclusive]

-

Crypto World7 days ago

Crypto World7 days agoRipple and Bitso Bring MXNB Stablecoin to XRP Ledger

-

Tech7 days ago

Tech7 days agoKlipsch Heritage First Listen at High End Vienna 2026: Rebellion, OJAS and Klipschorn Bring the Horns

You must be logged in to post a comment Login