Crypto World

Stablecoins are quietly becoming the internet’s money

In 2025, stablecoins settled more transactions than Visa. Real-world stablecoin payments doubled to $400 billion. Visa, Mastercard, Stripe, PayPal, and Western Union all turned on stablecoin rails inside their existing products. The GENIUS Act became U.S. law. And almost no one outside crypto noticed. The most important shift in the global payments system in twenty years happened in plain sight, and it is still being misread as a crypto story.

Summary

- Stablecoin transaction volume reached levels comparable to Visa in 2025 as payment giants integrated blockchain-based settlement rails into existing products.

- Real-world stablecoin payments doubled to $400 billion last year, with most activity tied to business payments, payroll, and cross-border settlements.

- The GENIUS Act gave banks and regulated firms a legal framework to issue and integrate stablecoins, accelerating adoption across the financial sector.

The biggest story in crypto is not about crypto

Strip away the meme coins, the price predictions, the ETF flow charts, and the regulatory drama. The single most consequential thing happening in digital assets right now has nothing to do with any of it. It is not Bitcoin. It is not even speculation. It is the quiet, accelerating absorption of stablecoins into the actual plumbing of how the world moves money.

Some numbers, because the numbers are the story.

The global supply of fiat-backed stablecoins crossed $319 billion in April 2026, up from roughly $7 billion six years earlier. A forty-fold expansion in an asset class that did not meaningfully exist before 2020. Adjusted stablecoin transaction volume grew ninety-one percent in 2025 to $10.9 trillion, closing in on Visa’s $14.2 trillion. By Plasma’s accounting, total settlement volume hit $33 trillion last year, past Visa’s annual throughput. Stablecoins processed roughly twenty times the volume PayPal did. Morph’s research projects that 2026 stablecoin settlement could top $50 trillion.

The most telling figure is not the size. It is the mix. Real-world stablecoin payments, the share of activity that is not crypto trading but actual commercial movement of money, doubled in 2025 to $400 billion. Sixty percent of that was business-to-business: companies paying suppliers, settling cross-border invoices, managing treasury, and moving payroll. Stablecoins are no longer just chips at the crypto casino. They have become an operating layer of international finance.

The reason this has happened without much public attention is mostly aesthetic. Stablecoins look boring. A dollar-pegged token does not 10x. There is no narrative, no chart porn, no influencer screaming about a new all-time high. They are infrastructure, and the great rule of infrastructure is that it stays invisible until it does not. The whole point of a stablecoin is that nothing dramatic happens to it. The dramatic thing is what gets built on top.

That is now being built. Fast.

What “internet money” actually has to do

For anyone who has spent any time around crypto, the phrase “internet money” has been thrown around for a decade, usually attached to assets that turned out not to be anything of the kind. Bitcoin was supposed to be it. Then Ethereum. Then a parade of L1s. None of them quite worked as money, because money has a job description far more demanding than “store of value” or “speculative asset.” It has to be reliable in unit, accepted broadly, transferable cheaply, and usable for the boring middle ninety percent of economic life: paying rent, settling invoices, sending payroll, buying coffee.

Stablecoins fit that job description in a way no prior digital asset did. They are pegged to the dollar, so a stablecoin is not really an investment; it is just a dollar that happens to live on a blockchain. Reserves, when properly backed, sit in cash and Treasury bills, the same instruments that already underpin trust in the financial system. Transactions are near-instant, run twenty-four hours a day, settle on weekends, cross borders without correspondent banking, and cost a fraction of what wire transfers do.

What changed in 2025 and 2026 was not the technology. Stablecoins have done these things for years. What changed was that the actual companies that move money for everyone else started building stablecoins into their products as a default, not an experiment.

The list reads like a roll call of global payments. Visa runs a stablecoin settlement program that hit a $7 billion annualized run rate in late April 2026, up fifty percent from the previous quarter, and operates across nine blockchains, including Ethereum, Solana, Avalanche, Base, and Polygon. Visa’s broader Visa Direct stablecoin payout product is live in over fifty countries. Mastercard, Stripe, PayPal, Western Union, Klarna, Cloudflare, Meta, Intuit, Fiserv, and Zelle have all either launched or announced integration plans. PayPal’s own stablecoin, PYUSD, sits in their consumer app alongside fiat balances.

The shape of the change is what matters. None of these companies is making a bet on a speculative asset. They are quietly upgrading the rails their existing products run on. A Visa card customer in Bogotá does not know, and does not need to know, that the back-end settlement between the issuing bank and Visa now travels as USDC on Solana rather than as fiat through a correspondent banking chain. The user experience is unchanged. The plumbing underneath is being replaced.

The two stablecoins that run the world

The market is, for now, a duopoly. Tether’s USDT holds roughly $189.6 billion in circulation. Circle’s USDC sits at around $77.6 billion. Together, they account for well over eighty percent of the global stablecoin supply.

They are not the same product, and the difference matters more in 2026 than it did before.

USDT is the offshore stablecoin. It dominates emerging-market trading, runs the largest share of remittance corridors in Latin America, Africa, Southeast Asia, and the Middle East, and serves as the dollar substitute in countries where local currencies are volatile or banking access is poor. Tether’s reserves, increasingly weighted toward U.S. Treasury bills (a $113 billion Treasury position as of Q1 2026), have made the company one of the largest non-sovereign holders of US debt in the world. USDT’s market share is slowly shrinking as regulated alternatives emerge, but its absolute supply continues to grow.

USDC is the compliance stablecoin. It is the one U.S. bank, payment companies, and large enterprises actually want to integrate with. Circle is publicly traded, USDC is attested monthly by Deloitte, it is licensed under Europe’s MiCA framework, and it sits in the strongest position under the new U.S. GENIUS Act regime. Where USDT wins on liquidity and reach, USDC wins on the things that matter to a compliance officer: clarity of reserves, regulatory approval, and the absence of legacy controversy.

The next tier of issuers is small but growing. Sky’s USDS at $8.4 billion, the rebuilt DAI at $4.7 billion, PayPal’s PYUSD, Ripple’s RLUSD now climbing toward $1.6 billion, USDe, and various yield-bearing variants. The duopoly is not breaking up, but the long tail is starting to matter. Banks and fintechs that want to issue their own stablecoins under the new U.S. framework are building the next wave now.

What the GENIUS Act actually changed

To understand why 2025 was the inflection point, you have to understand what the GENIUS Act did, because almost every meaningful piece of the stablecoin acceleration traces back to it.

The Guiding and Establishing National Innovation for U.S. Stablecoins Act was signed into law in July 2025. It is the first comprehensive US federal framework for payment stablecoins, and it does three things that, together, changed the calculus for every serious financial institution.

First, it answered the question of what a payment stablecoin legally is. The act establishes that permitted payment stablecoins are not securities, commodities, or deposits. They are a new regulated category with their own regime, administered principally by the Office of the Comptroller of the Currency alongside the FDIC, the Federal Reserve, the Treasury, and state banking regulators. That clarity matters because the absence of a category was, for years, the single biggest reason serious institutions stayed out.

Second, it set the rules of issuance. Stablecoin issuers must hold one-to-one reserves in high-quality liquid assets, publish monthly attestations, undergo audits, and comply with anti-money-laundering and sanctions requirements. Permitted issuers are limited to insured depository institutions (banks and credit unions), subsidiaries of such institutions, and certain approved nonbank entities. In effect, the law turned stablecoin issuance into a regulated banking activity.

Third, it opened the door for banks themselves to issue. A national bank can now issue a payment stablecoin under OCC supervision. Tokenized deposits, where a bank’s actual liabilities to its customers are represented as tokens on a ledger, sit within reach. Banks that spent years watching Tether and Circle gather a sector they were structurally locked out of now have a path in.

The OCC proposed its implementing rules in late February 2026, with the comment period closing on May 1. The act’s effective date arrives at the earlier of eighteen months after enactment (January 2027) or 120 days after final regulations. Practical impact, then, takes full effect roughly from mid-2026 onward.

The first-order effect was psychological. Once U.S. law existed, the asset class became investable to a class of institutions that had been waiting on a green light. The second-order effect, which is now playing out, is the wave of bank and fintech stablecoin pilots, tokenization initiatives, and payment integrations that have hit the market since the bill was signed.

The use cases that are no longer hypothetical

Three real-world use cases are now operating at scale, and a fourth is approaching.

Cross-border B2B payments are the largest and most boring. A U.S. importer paying a Vietnamese supplier traditionally goes through correspondent banks, taking three to five days and losing three to seven percent to fees, intermediary charges, and FX spread. The same transaction in stablecoins settles in seconds for cents. Sixty percent of stablecoin payment volume in 2025 was B2B precisely because the cost-benefit is overwhelming and the regulatory exposure for a corporate treasury team has dropped sharply under the new framework.

Cross-border consumer payments and remittances are the most socially significant. In countries where banking is shallow, local currencies are weak, or capital controls are tight, stablecoins have quietly become the preferred way to receive money from abroad. A migrant worker in the Gulf sending money home to family in Lagos increasingly does so in USDT, which the recipient can hold, spend at a growing number of merchants, or convert locally. The “informal” stablecoin economy is not on most balance sheets, but Chainalysis and others have documented its scale year after year.

Card-linked stablecoin spending is the bridge between crypto-native dollars and the real economy. Companies like Rain issue Visa-network cards that draw against stablecoin balances and settle directly in stablecoins with Visa. A BVNK and YouGov survey of over 4,000 stablecoin users found that seventy-one percent said they would use a linked debit card to spend their stablecoins. The infrastructure is now there. The “spend” leg of the payments lifecycle, the one missing piece until late 2024, is closing.

AI-agent payments are the fourth use case, still emerging but worth flagging because they may end up being the largest. A new generation of protocols, the most discussed being x402, lets AI agents transact with each other directly: paying for data, GPU time, API calls, or other agent services without human approval and without traditional invoicing. The economic case requires payments that are programmable, instant, sub-cent in cost, and machine-readable. Stablecoins are the only existing form of money that meets all four. As AI commerce scales, an enormous share of it will, by necessity, run on stablecoin rails.

The framing matters here. The first three use cases describe stablecoins replacing parts of the existing payment infrastructure. The fourth describes them enabling a payment market that does not yet exist in fiat form. Both expansions are happening at once.

What can still go wrong

A piece that only described the upside would be marketing, not journalism, so here is the other side.

Stablecoins remain only as good as their reserves and their operators. The 2022 collapse of TerraUSD wiped $40 billion in three days and is the cautionary tale every regulator now writes against. Even fiat-backed stablecoins are not risk-free: USDC briefly de-pegged in March 2023 when Circle’s exposure to the failing Silicon Valley Bank surfaced. The reserves were ultimately recovered, but the episode showed that even properly backed stablecoins can wobble under banking stress. The GENIUS Act explicitly addresses some of these failure modes, but the law’s allowance for issuers to hold uninsured bank deposits as reserves has drawn warnings from the Brookings Institution and other observers who note it creates a two-way coupling between bank risk and stablecoin risk.

Banks themselves are watching stablecoin growth uneasily, because every dollar that migrates from a bank deposit into a stablecoin balance is a dollar the bank no longer has to lend. The American Bankers Association and similar groups in Europe have lobbied hard, and largely unsuccessfully so far, for tighter restrictions on stablecoin yield and on competition with deposit accounts. If deposits drain faster than legislators expect, the banking lobby will push back harder.

Geopolitical risk runs in two directions. Dollar-pegged stablecoins are extending dollar reach into corners of the world that local sovereigns would rather control, which is already producing capital controls pushback in several emerging markets. At the same time, the dominance of U.S.-dollar stablecoins (more than ninety-nine percent of fiat-backed stablecoin value is dollar-pegged) makes the asset class an instrument of dollar hegemony, which both helps and complicates the geopolitics of payments. China is pushing its own central bank digital currency in parallel. The EU has MiCA and a digital euro project on a slower timeline. The next decade of payments policy will be partly a contest between these models.

Finally, the most boring risk is the most likely. Implementation matters. The rules being written by the OCC and other regulators between now and final implementation in 2026 and 2027 will determine whether the stablecoin sector grows into a regulated, integrated piece of finance or fragments into a series of jurisdictional silos that limit the benefits of a borderless rail.

What this means in the end

The shorthand for what is happening is “stablecoins are eating payments.” That is not quite right, because payments are not a single thing being replaced. What is actually happening is that the dollar itself is being upgraded into a new technical form, one that runs on open networks, settles in seconds, costs almost nothing to move, and operates twenty-four hours a day. Stablecoins are the vehicle. The dollar is the cargo.

If you zoom out, this is a bigger development than the launch of spot Bitcoin ETFs, the CLARITY Act, or any of the other crypto stories that have dominated headlines this cycle. ETFs gave institutions a way to hold Bitcoin. Stablecoins are giving the entire global economy a new way to use dollars. Those are not comparable in scale.

What makes the shift hard to see is that it does not look like a revolution. It looks like a payment is landing in your account faster than you remember it landing before. It looks like a supplier in another country is getting paid the same day instead of the next week. It looks like a Visa card that works the same as it always did, even though the settlement underneath has fundamentally changed. It looks like nothing, until one day you realize most of the dollars in the global digital economy live on rails that did not meaningfully exist five years ago.

That is what infrastructure does. It disappears. And once it disappears, it is hard to put it back.

The internet got money. Almost no one noticed. The next decade of finance will be spent catching up.

This article is for informational purposes and does not constitute financial or investment advice. Stablecoin regulations, transaction volumes, and reserve compositions can change quickly; the figures described reflect reporting available as of mid-May 2026. Always do your own research.

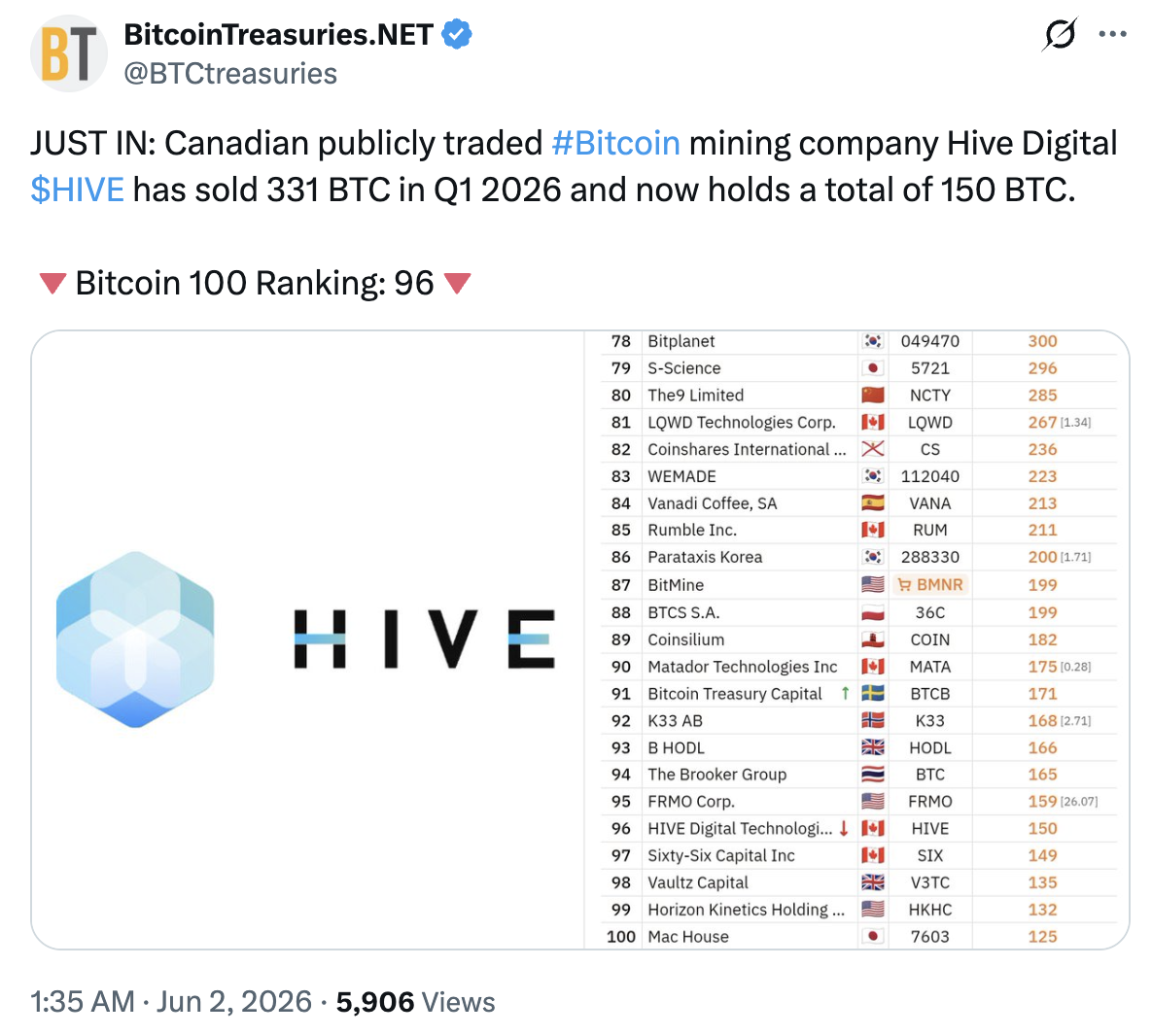

Canadian Bitcoin miner HIVE Digital Technologies is pushing deeper into artificial intelligence infrastructure, signing a three-year GPU cloud contract intended to support AI startup Cohere and its enterprise and government customers. The company says its BUZZ HPC arm will provide high-performance computing capacity at a Bell Canada data center in British Columbia.

HIVE disclosed that the agreement is valued at approximately $220 million and involves the deployment of 2,304 NVIDIA Grace Blackwell GPUs. Once the project is in service, HIVE expects the deal to generate about $70 million in contracted annual recurring revenue, lifting its contracted HPC revenue target to more than $100 million.

Key takeaways

- HIVE’s BUZZ HPC has signed a three-year GPU cloud contract worth about $220 million with Bell AI Fabric for Cohere.

- The contract calls for deploying 2,304 NVIDIA Grace Blackwell GPUs at a Bell Canada data center in British Columbia.

- After rollout, HIVE expects roughly $70 million in contracted annual recurring revenue from the project and a total HPC target above $100 million.

- HIVE plans to finance the AI infrastructure using proceeds from its April $115 million convertible note financing.

- The move aligns with a broader shift among miners toward AI and HPC, even as Bitcoin mining difficulty has recently fallen.

A major GPU cloud contract extends HIVE’s AI pivot

For HIVE, the new contract is part of a larger strategy to diversify beyond Bitcoin mining by monetizing HPC and AI infrastructure. The company’s BUZZ HPC unit will deliver the GPU capacity required for Cohere’s artificial intelligence models and services, according to the terms HIVE described.

The scale of the deployment—2,304 NVIDIA Grace Blackwell GPUs—signals a long-term commitment to serving AI workloads rather than treating AI compute as an incremental add-on. Instead, HIVE is positioning BUZZ HPC as a provider of dedicated GPU cloud capacity delivered from a major regional data center footprint.

HIVE also tied expected revenues directly to the project’s operating phase. The company said that once the deployment enters service, it anticipates about $70 million in contracted annual recurring revenue attributable to the contract. It further claims this would increase its contracted HPC revenue target to more than $100 million.

Funding plan and why contracted revenue matters

HIVE stated it will fund the AI infrastructure purchase using a portion of the proceeds from its April convertible note financing totaling $115 million. By pairing capital funding with a multi-year contract structure, HIVE is effectively aiming to reduce uncertainty around demand for compute capacity—at least for the specific workload allocation covered by the agreement.

From an investor perspective, contracted annual recurring revenue can be a more predictable indicator than ad hoc performance tied purely to market cycles. While Bitcoin mining economics depend heavily on network difficulty, power costs, and Bitcoin price, the company’s HPC revenue claims focus on signed arrangements intended to translate into recurring cash flows once infrastructure is deployed.

How this fits with HIVE’s recent operational trajectory

This latest contract arrives alongside other disclosures about HIVE expanding its AI footprint. In May, the company said its BUZZ HPC subsidiary planned a 320-megawatt AI data center campus near Toronto, designed to support more than 100,000 GPUs.

More recently, HIVE reported improvements in its HPC business. According to the company’s update, revenue from its HPC division rose to $19.5 million in fiscal 2026—nearly doubling from a year earlier. It also said contracted annual recurring revenue from the segment reached $35 million, supported by deployments of NVIDIA-powered GPU clusters and new enterprise contracts.

The company has also pointed to changes in its Bitcoin holdings. HIVE reported a decline in its Bitcoin treasury balance, falling to 150 BTC from 481 BTC earlier in the prior quarter, as tracked by BitcoinTreasuries.NET. While the note about treasury movement does not specify causation, readers should view it in the context of HIVE’s broader reallocation of capital toward AI and HPC infrastructure.

Mining difficulty declines as AI investment continues

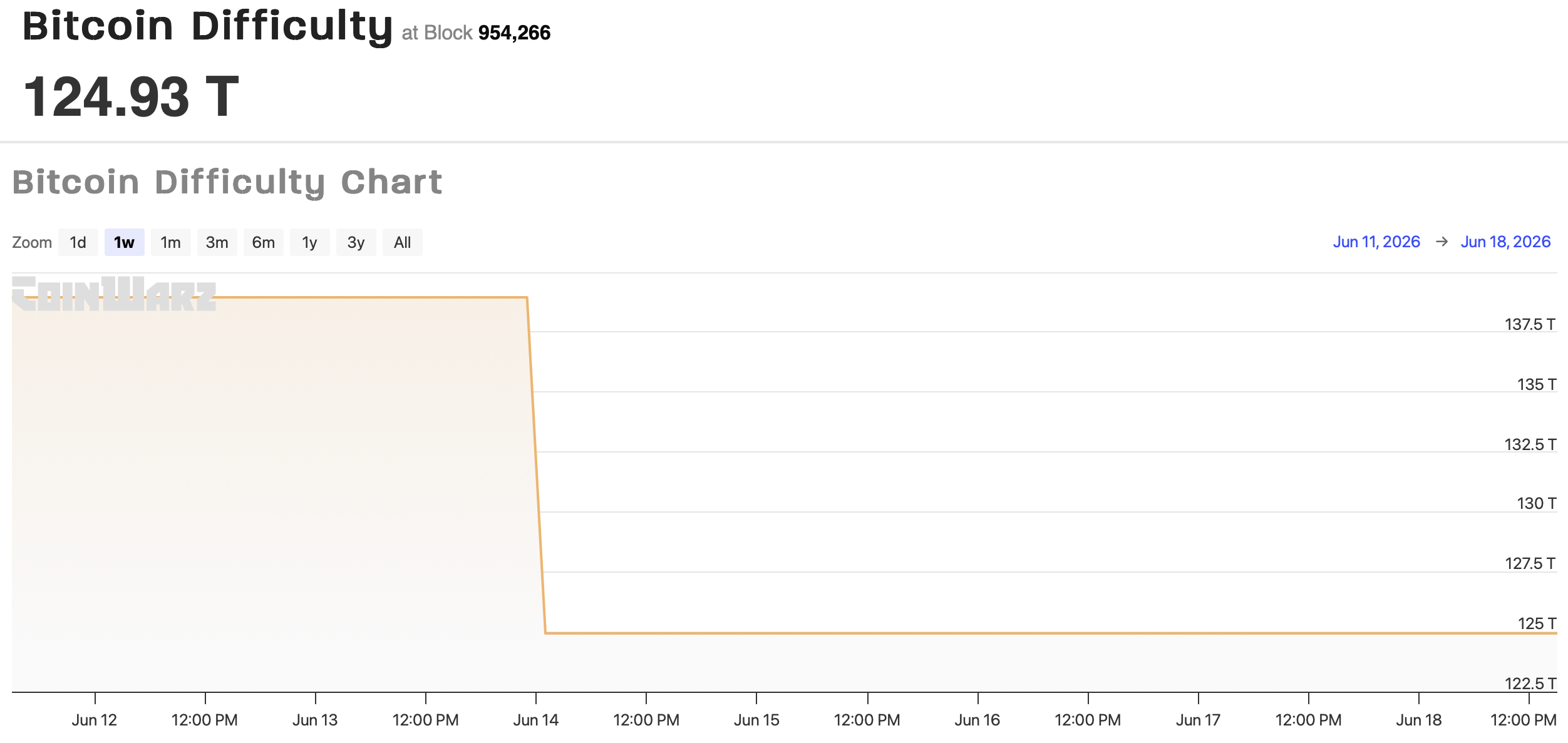

While HIVE is building AI compute capacity, the Bitcoin network itself has been experiencing near-term downward pressure on mining difficulty. The Energy Mag (formerly The Miner Mag) reported that Bitcoin mining difficulty fell 10.09% on June 14—described as one of the largest downward adjustments in the network’s history. The outlet attributed the decline to weaker mining economics, Bitcoin’s price drop, seasonal power curtailment in Texas, and wider power-market dynamics.

The same report also raised a longer-term question: if miners divert some power and operational capacity toward AI and HPC projects, that could influence future hashrate growth by reducing the amount of capacity available for Bitcoin mining. In other words, the AI expansion trend could affect the balance between Bitcoin-secured hashpower and compute allocated to other high-demand workloads.

Cointelegraph previously reported that Bitcoin mining profitability had fallen to record lows, making it harder for some operators to stay profitable. Together with the difficulty drop, these signals suggest a more challenging near-term mining environment—even as capital investment and contract-making in AI compute continues to accelerate across parts of the mining sector.

Other firms have also continued moving into AI-adjacent infrastructure. Earlier this week, Cointelegraph reported that IREN completed its acquisition of Spanish data center developer Nostrum Group, while TeraWulf recently added a development site in Kentucky that it said could eventually support more than 1 gigawatt of AI and HPC capacity.

For HIVE and investors watching the broader miner-to-AI transition, the key next question is execution: whether contracted GPU capacity scales on schedule and whether additional enterprise and government AI contracts expand beyond the initial pipeline. With Bitcoin mining conditions fluctuating and difficulty recently stepping down, investors will likely monitor how quickly miners convert AI infrastructure commitments into sustained, measurable HPC revenue.

The Aster DEX unveiled a huge change to its tokenomics on June 17, allocating 99% of fees generated through its platform to an ASTER token buyback, with one-to-one burns from its reserves for each token purchase.

The #48-ranked cryptocurrency witnessed a massive rebound shortly after the announcement but has since given back most of those gains.

DEX Pushes Token Buybacks to 99% of Fees

In a post on X, the YZ Labs-supported perp exchange said its upgraded tokenomics model went live at 12:00 PM UTC on June 17. Under the new framework, 99% of daily platform fees will be used to automatically buy back ASTER through time-weighted average price purchases executed throughout the day and settled on-chain.

Every token bought back will trigger an equal burn from Aster’s reserve, with the team allocation burned first, resulting in what they called a 198% buyback: 99% repurchased and 99% burned from reserve.

However, the coins that’ll be bought back won’t disappear. They’ll go directly to stakers after being added to the protocol’s Loyalty Reward pool, which already distributes 300,000 ASTER in every epoch.

And the burn target is quite significant. Recall that the DEX launched with a total supply of 8 billion tokens, and it intends to burn that down to 3 billion, meaning more than 60% of that supply has been earmarked for destruction.

CoinGecko states that the present circulating supply is at about 2.68 billion, while the total supply is 7.82 billion, so there’s still a long way to go before the burn target is reached.

Where ASTER Stands Now

News of the new tokenomics mechanism had an immediate effect in the market. It saw ASTER’s value jump 23%, going from around $0.64 to $0.79 per CoinGecko. But it has since given back a fair bit of that gain and was trading near $0.65 at the time of writing, almost 73% below its September 2025 all-time high of $2.41.

Back in December 2025, the exchange announced a similar repurchase program, but at the time, the plan was to allocate 80% of daily fees to hoover up the token.

That was split between automatic daily buys, which took 40% of the fees, while another 20% to 40% was to be held in a discretionary strategic reserve, allowing the platform to conduct targeted purchases based on market conditions.

That announcement also coincided with a brief price uptick, with ASTER spiking 30% to $1.30, buoyed by news that ex-Binance CEO Changpeng Zhao was holding more than $2.5 million worth of the cryptocurrency.

The new plan has removed the strategic reserve approach entirely and pushed allocation much higher, with nearly all platform fee revenue going into automatic buybacks.

The post ASTER Flies 23% After DEX Redirects 99% Fees to Token Buybacks appeared first on CryptoPotato.

Breaking Solana news: Moody’s Ratings deployed its credit ratings infrastructure on Solana mainnet on June 17, 2026, through a partnership with AlphaLedger, making Solana the first major public, permissionless blockchain to carry live Moody’s credit ratings in machine-readable form.

The integration embeds ratings directly into the token metadata of tokenized bonds and other fixed income securities, meaning the credit signal travels with the asset on-chain rather than sitting behind a proprietary terminal.

For institutional participants building on Solana’s RWA stack, this closes one of the most obvious gaps in tokenized debt markets: access to standardized, independent credit analysis at the protocol level.

The distinction from Moody’s earlier Canton Network rollout matters structurally. Canton is a permissioned, institutional-grade blockchain with a defined set of vetted participants.

Solana is open infrastructure, any wallet, trading venue, or DeFi protocol can now query Moody’s credit data directly from on-chain token metadata without credentialing through a closed network. That shift from permissioned to permissionless delivery is what makes this announcement materially different from what Moody’s has done before.

Discover: The Best Crypto to Diversify Your Portfolio

Solana News: How the Token Integration Engine Actually Works on Solana

Moody’s Token Integration Engine, known as TIE, is designed as network-agnostic infrastructure: ratings are assigned off-chain using Moody’s standard methodology, then pushed on-chain via API through

AlphaLedger’s platform, where they are embedded into the token metadata of the underlying security. When a rating changes, upgrade or downgrade, that update propagates on-chain automatically, so any application consuming the data gets a live credit signal rather than a static snapshot.

The system was first validated in a June 2025 proof-of-concept on Solana’s devnet, where AlphaLedger simulated a municipal bond issuance, Moody’s ran a full credit assessment, and the resulting rating was written into the token’s metadata and made queryable by smart contracts.

The mainnet rollout scales that proof-of-concept to production, with early focus on U.S. municipal bonds and other fixed income instruments.

Manish Dutta, Chief Executive Officer of AlphaLedger, said the integration allows tokenized markets to use the same credit information that investors rely on in traditional fixed-income markets. That framing is precise: the goal is not to create a parallel ratings system but to make the existing one programmatically accessible on a public chain.

Rajeev Bamra, Head of Digital Economy Strategy at Moody’s Ratings, said investors increasingly need access to independent credit analysis in on-chain environments.

The specific problem TIE targets is automated risk management, giving DeFi protocols and digital asset platforms a trusted, machine-readable credit input they can use for collateral decisions, margin policies, and investment eligibility filters without routing through proprietary data feeds.

That use case has been largely theoretical in tokenized bond markets until now.

Discover: The Best Token Presales

Solana’s Institutional RWA Position: What This Integration Confirms

The Moody’s integration arrives as Solana’s institutional real-world assets pipeline has deepened considerably. Western Union launched a U.S. dollar stablecoin on the network targeting lower-cost remittances.

Blockchain developer R3, whose Corda network counts HSBC, Bank of America, the Bank of Italy, and the Monetary Authority of Singapore as participants, partnered with the Solana Foundation to port tokenized assets from Corda onto Solana.

Asset managers including BlackRock, Franklin Templeton, and Apollo have already launched tokenized investment products across the broader RWA space. Boston Consulting Group and Ripple estimate the tokenized asset market could reach $18.9 trillion by 2033.

Nick Ducoff, Head of Institutional Growth at the Solana Foundation, said the Moody’s integration improves transparency and accessibility for tokenized assets on the network.

The more concrete read is that embedding Big Three credit ratings into on-chain securities removes a key objection from fixed income desks evaluating Solana-based products: the absence of standardized, independently verifiable credit data.

Institutional fixed income buyers do not price risk without Moody’s, S&P, or Fitch, having that layer queryable on a public chain is a structural prerequisite for serious adoption, not a cosmetic feature.

Moody’s has indicated TIE will expand beyond municipal bonds to corporate, sovereign, and structured finance instruments as tokenization volumes grow, and will extend to additional blockchains beyond Canton and Solana.

The multi-chain framing is deliberate, Moody’s is positioning TIE as ratings infrastructure for the tokenized debt market broadly, not as a Solana-exclusive product.

Solana’s accelerating institutional deal flow suggests the network is establishing a durable lead in public-chain RWA issuance, but the Moody’s deployment itself is chain-agnostic by design.

Whether that early-mover position compounds or gets competed away depends on how quickly issuers and protocols integrate TIE data into live products, and how fast the rest of the tokenized fixed income stack catches up to meet it.

SOL’s price performance has been tracking broader market conditions more than protocol-level news, which is consistent with where institutional adoption sits right now: real infrastructure progress, not yet reflected in near-term price catalysts.

The post Solana Scores Crypto’s First Moody’s Credit Ratings Onchain appeared first on Cryptonews.

Crypto World

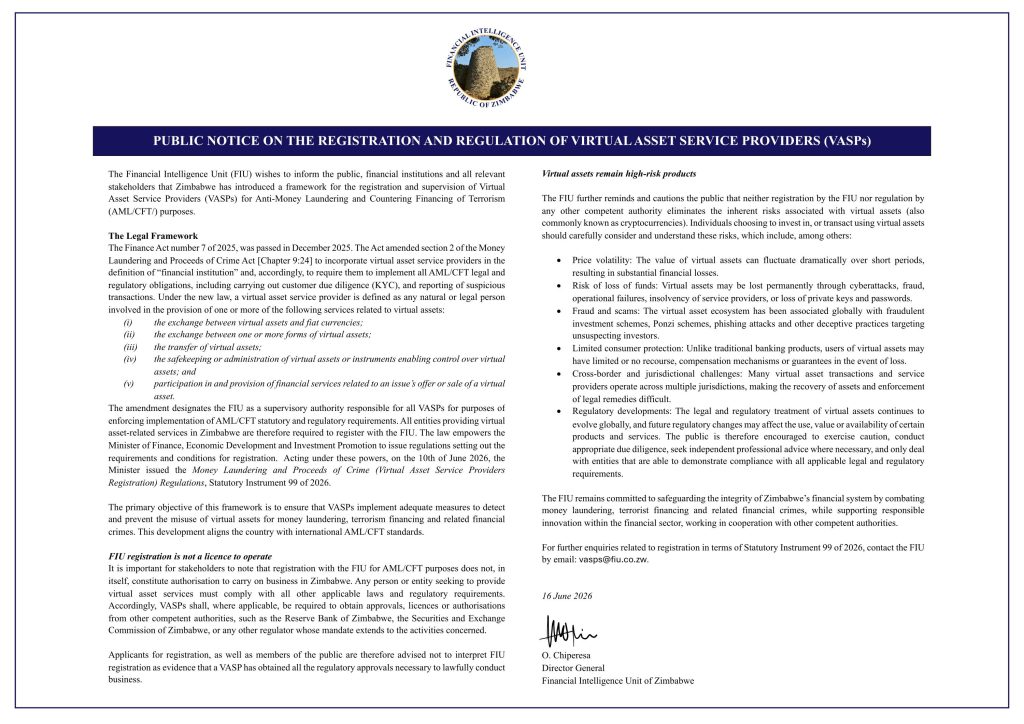

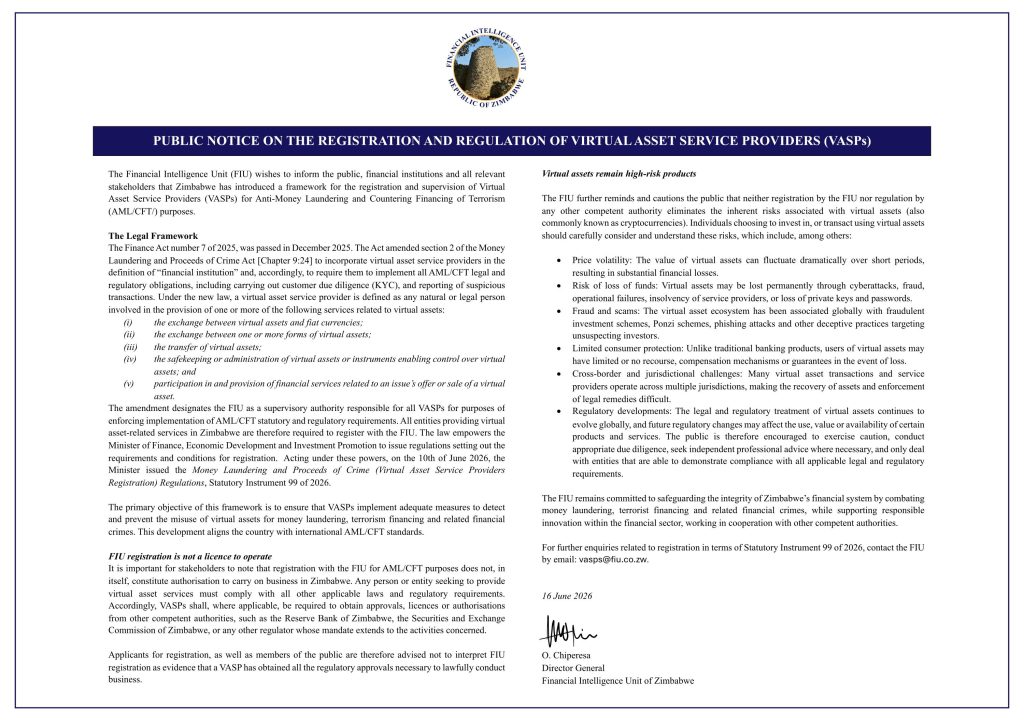

Bitcoin News: Zimbabwe Just Regulated Crypto, But Could a Bitcoin Treasury Save Its Economy?

In the most recent Bitcoin News, Zimbabwe’s Financial Intelligence Unit issued a binding mandate on June 16, 2026 requiring all virtual asset service providers to register under Statutory Instrument 99 of 2026, the country’s first dedicated crypto regulatory framework, effective immediately, with criminal liability for non-compliance.

The framework formalizes what has been an eight-year grey market built largely on hyperinflation-driven demand for dollar-denominated alternatives to a succession of collapsing local currencies.

The regulatory event is straightforward. The question it reopens is not: if Zimbabwe can build the institutional scaffolding to supervise crypto, is there a coherent case for the state itself to hold a Bitcoin reserve as a monetary anchor? The answer cuts both ways, and the arithmetic deserves a serious look.

Discover: The Best Crypto to Diversify Your Portfolio

Bitcoin News: SI 99 of 2026: What the FIU Mandate Actually Covers

The legal chain is worth anchoring precisely. The Finance Act No. 7 of 2025, passed in December 2025, amended Section 2 of Zimbabwe’s Money Laundering and Proceeds of Crime Act to incorporate VASPs into the statutory definition of a financial institution.

Acting under those expanded powers, the Zimbabwean Minister of Finance gazetted the Money Laundering and Proceeds of Crime (Virtual Asset Service Providers Registration) Regulations on June 10, 2026, codified as Statutory Instrument 99, and the FIU issued its public enforcement mandate six days later.

The scope is broad and technology-neutral. Any entity exchanging cryptocurrencies for fiat, providing custody services, or facilitating crypto-related financial transactions must register. Notably, decentralization is not an exemption: if an operator can adjust smart contracts, route funds, or set transaction fees, the FIU considers them a VASP.

Registration carries a US$500 initial fee and US$400 annual renewals, requires a locally incorporated entity, director background checks, KYC implementation, transaction monitoring, and compliance with the FATF Travel Rule.

The FIU was explicit about what registration does not provide. “Registration with the FIU for AML/CFT purposes does not, in itself, constitute authorization to carry on business in Zimbabwe,” the public notice stated.

VASPs still need separate operational approvals from the Reserve Bank of Zimbabwe or the Securities and Exchange Commission of Zimbabwe, depending on their business model. This two-layer structure – crypto regulation for AML monitoring on one track, commercial licensing on another, is standard FATF architecture, and Zimbabwe is explicitly aligning itself with those international standards.

The historical context makes the policy shift sharper. In 2018, the RBZ issued Circular No. 2/2018 ordering all banks to cease servicing crypto exchanges and exit existing relationships within 60 days.

Local exchange Golix challenged the ban in court and obtained a provisional High Court order lifting it specifically against Golix, but broader regulatory uncertainty persisted for years.

SI 99 is effectively the formal end of that ambiguity, a supervised integration model replacing blanket exclusion, driven by the recognition that hyperinflation and chronic currency instability had already pushed citizens into crypto regardless of official policy.

Discover: The Best Token Presales

The post Bitcoin News: Zimbabwe Just Regulated Crypto, But Could a Bitcoin Treasury Save Its Economy? appeared first on Cryptonews.

Canadian Bitcoin miner HIVE Digital Technologies said its AI subsidiary BUZZ HPC has signed a three-year GPU cloud contract worth approximately $220 million with Bell AI Fabric for AI startup Cohere, expanding the company’s push into high-performance computing (HPC) and AI infrastructure.

The agreement calls for BUZZ HPC to deploy 2,304 NVIDIA Grace Blackwell GPUs at a Bell Canada data center in British Columbia, where the infrastructure will support Cohere’s artificial intelligence models and services for enterprise and government customers.

After the deployment enters service, HIVE expects the project to contribute about $70 million in contracted annual recurring revenue, increasing its contracted HPC revenue target to more than $100 million, according to the company.

HIVE said it will fund the purchase of the AI infrastructure using a portion of the proceeds from the $115 million convertible note financing it completed in April.

The company’s stock price was up around 9% at the time of writing and almost 24% in the past month, according to Yahoo Finance data. Sector tracking exchange-traded fund CoinShares Bitcoin Mining ETF (WGMI) was up 5.4% on the day, and up more than 30% in the past month. HIVE stock is the fund’s eighth-biggest holding.

Source: Yahoo Finance

Related: Georgia targets illegal crypto mining in Mestia crackdown: Report

HIVE grows AI business as Bitcoin holdings decline

The deal is the latest move in HIVE’s broader expansion into AI infrastructure. In May, the company said its BUZZ HPC subsidiary planned a 320-megawatt AI data center campus near Toronto, capable of supporting more than 100,000 GPUs.

Earlier this month, HIVE reported that revenue from its HPC division increased to $19.5 million in fiscal 2026, nearly doubling from a year earlier. The company also said contracted annual recurring revenue from the business reached $35 million, supported by deployments of Nvidia-powered GPU clusters and new enterprise contracts.

HIVE also reported a decline in its Bitcoin (BTC) treasury holdings, which fell to 150 BTC from 481 BTC a quarter earlier.

Source: BitcoinTreasuries.NET

Related: Nvidia’s $20 billion debt boom reinforces Bitcoin miners’ AI pivot

Hashrate declines as AI investments grow

On Thursday, The Energy Mag (formerly The Miner Mag) noted that Bitcoin mining difficulty, a measure of how hard it is for miners to produce new blocks, fell 10.09% on June 14, one of the largest downward adjustments in the network’s history.

The publication attributed the decline to weaker mining economics, Bitcoin’s price decline, seasonal power curtailment in Texas and broader power-market dynamics. It also argued that miners dedicating power to AI and HPC projects could alter future hashrate growth by reducing the amount of capacity available for Bitcoin mining.

Bitcoin mining difficulty. Source: Coinwarz.com

The decline came days after Cointelegraph reported that Bitcoin mining profitability had fallen to record lows, making it harder for some operators to remain profitable.

Meanwhile, miners continue expanding into AI and high-performance computing. On Tuesday, IREN completed its acquisition of Spanish data center developer Nostrum Group, while TeraWulf recently added a Kentucky development site that it said could eventually support more than 1 gigawatt of AI and HPC capacity.

Magazine: Does ‘Paper Bitcoin’ mean there’s an unlimited supply of BTC?

The Chicago Mercantile Exchange (CME) Group has filed a lawsuit in federal court challenging the U.S. Commodity Futures Trading Commission (CFTC) over its approvals of cryptocurrency-linked perpetual futures. The complaint, submitted to the U.S. District Court for the District of Columbia, targets the CFTC, its chair Michael Selig, and asks the court to vacate the agency’s actions.

The case highlights an expanding regulatory dispute over how U.S. derivatives rules apply to crypto products that do not fit neatly into traditional futures structures. For crypto exchanges, broker-dealers, market operators, and institutional investors, the outcome could affect product design, compliance expectations, and supervisory oversight of crypto derivatives—particularly where regulatory interpretations hinge on whether a contract is treated as a “futures” product or as a “swap” under the Commodity Exchange Act (CEA).

Key takeaways

- CME filed a D.C. federal lawsuit against the CFTC and chair Michael Selig relating to the agency’s approval of crypto perpetual futures tied to Bitcoin spot prices.

- The complaint centers on a CFTC notice dated May 29 involving Kalshi prediction market products and a no-action position for similar products involving Coinbase.

- CME alleges the CFTC improperly applied the CEA by effectively treating “futures” as “swaps” with expiration dates, and argues Selig acted without a full five-commissioner panel.

- The CFTC, through a spokesperson, rejected the claims as “frivolous” and characterized CME’s litigation approach as “lawfare.”

CME’s lawsuit challenges CFTC approvals for crypto perpetual futures

In its Thursday filing, CME sought judicial review of CFTC actions approving certain perpetual futures contracts linked to Bitcoin’s spot price. The dispute traces back to a May 29 CFTC notice that (1) approved perpetual futures contracts tied to Bitcoin for Kalshi, a platform operating prediction markets, and (2) issued a “no-action” position for similar perpetual products referenced in connection with Coinbase.

CME’s complaint argues that the CFTC’s approach conflicts with directives from Congress, particularly by treating “futures” as “swaps” for purposes of regulatory classification. Under CME’s theory, the classification matters because it determines which statutory and regulatory requirements apply to the relevant derivatives framework.

Beyond the substantive challenge, CME also raised procedural concerns. The exchange contends that Selig acted unilaterally rather than through a full panel of five CFTC commissioners, implying that the agency’s internal governance or decision-making process was not properly followed for the actions at issue.

“With one stroke of his pen, [Selig] overrode Congress’s definition of the term ‘swap’ and circumvented the regulatory regime Congress required for that form of derivative.”

CME further asserted that the CFTC’s handling of these approvals could harm competition and destabilize derivatives markets, arguing the agency failed to apply the CEA consistently and evenly.

Congress, contract classification, and why the dispute matters

At the core of CME’s legal argument is the classification of perpetual futures contracts—contracts that, in typical market practice, can be designed to trade without a fixed expiration date, while still resembling derivative instruments whose regulatory treatment depends on statutory definitions.

From a compliance standpoint, how a product is categorized can determine whether market participants must register, seek approvals, adopt particular operational controls, and comply with specific surveillance or reporting expectations under U.S. derivatives oversight. The lawsuit therefore sits at the intersection of contract engineering and statutory interpretation: market operators and intermediaries may need clarity on whether certain crypto-linked “perpetual” structures fit within futures frameworks or instead trigger swap-like regulatory pathways.

The broader institutional issue is that perpetual crypto derivatives have increasingly blurred lines between legacy derivative categories. That raises practical uncertainty for exchanges and clearing entities, and it can create compliance friction for financial institutions that must meet regulatory expectations for eligible contract types and risk controls. In that context, CME’s challenge is not merely a technical disagreement: it is aimed at shaping the legal boundaries that govern future approvals and market access.

Selig’s position and the CFTC’s response

The dispute escalated publicly shortly before CME’s filing. One day earlier, CME CEO Terrence Duffy said the exchange operator would take legal action against the CFTC. In a subsequent interview, Selig maintained that perpetual futures contracts “trade very similarly” to other derivatives and argued that the CEA does not define the term “futures contract.”

The CFTC rejected CME’s complaint. A CFTC spokesperson told Cointelegraph that CME had engaged in “lawfare” against the agency and the administration’s broader crypto policy approach, characterizing the lawsuit as “frivolous.” The exchange’s response, in turn, underscores a high-stakes policy conflict: if courts accept CME’s reading, it could compel the agency to revisit approvals tied to its prior interpretive stance and potentially adjust how it evaluates similar applications or regulatory notices.

CFTC leadership structure and timing: a procedural and policy flashpoint

CFTC chair Michael Selig was confirmed by the U.S. Senate in December 2025 and, as of the time of CME’s filing, remains the chair and sole commissioner in a leadership panel intended to include five commissioners. The lawsuit comes amid uncertainty about whether the CFTC’s full bipartisan composition will be restored in time for complex contested decisions—an issue that CME highlights through its allegation that Selig acted without a complete panel.

Political context also matters for the regulatory process. As of Thursday, President Donald Trump had not announced nominations to fill the CFTC seats, despite calls from members of Congress to do so. That governance vacuum can become consequential when markets depend on consistent, multi-member commission decision-making for contested interpretations of the CEA.

The dispute also arrives as crypto perpetual derivatives are proliferating across U.S. venues and regulated infrastructure. For example, Kraken announced it would offer perpetual futures to U.S. users through a CFTC-regulated platform, Bitnomial. While that development is separate from CME’s lawsuit, it reflects the practical stakes of regulatory clarity: product expansion continues, but the legal foundations supporting classification and approval pathways are actively contested.

What to watch next

Courts will determine whether CME’s claims succeed on statutory interpretation and whether the challenged approvals can stand procedurally under the CFTC’s decision-making requirements. For market participants, the most immediate watchpoints are how the court frames the futures-versus-swaps classification issue and whether the CFTC revises its approach to approvals of crypto perpetual derivatives pending the litigation’s outcome.

Kraken has expanded access to more than 2,500 Solana-based tokens through on-chain trading while SOL has fallen nearly 8% amid a wider crypto market selloff.

Summary

- Kraken has launched on-chain trading for more than 2,500 Solana-based tokens across 100+ countries.

- The feature gives users access to many unlisted Solana tokens using USD or USDC.

- SOL fell nearly 8% as a broader crypto market selloff outweighed the positive platform update.

According to Kraken, customers in the United States and more than 100 countries can now trade thousands of Solana ecosystem tokens directly through the exchange’s platform, including assets that have not yet been listed on centralized exchanges.

The rollout allows users to buy and sell eligible Solana tokens using USD or USDC without relying on separate self-custody wallets or external decentralized finance tools.

Kraken said the feature removes several steps that have traditionally required users to manage seed phrases, bridge assets between platforms, or interact with multiple applications.

Speaking on the launch, Kraken Chief Data Officer Kamo Asatryan said the company wants to simplify access to blockchain-based assets by reducing the complexity associated with activities such as paying gas fees and moving funds across networks.

Kraken expands beyond traditional exchange listings

Rather than focusing only on tokens that pass through the centralized exchange listing process, Kraken is opening access to a much larger segment of the Solana ecosystem. According to the company, many of the newly available assets are not listed on conventional trading platforms.

“Our customers in the US and more than 100 countries can now trade 2,500+ Solana-based tokens directly from the Kraken app they already use, including many not yet listed on any centralized exchange.”

The launch adds another product line to Kraken’s recent expansion efforts. As crypto.news reported on June 15, the exchange introduced perpetual futures for eligible U.S. customers through a Commodity Futures Trading Commission-regulated venue.

Following the rollout, eligible users can trade perpetual futures on Kraken Pro alongside spot, margin, and traditional futures products within a single account. The offering was enabled by Kraken parent company Payward’s acquisition of Bitnomial, a CFTC-licensed derivatives platform acquired earlier this year.

Kraken noted that support for additional blockchain networks is expected in the future, which would allow users to trade assets from ecosystems beyond Solana through the same interface.

Market weakness keeps pressure on SOL

Despite the exchange’s latest Solana-focused product launch, the token has remained under pressure as risk appetite continues to weaken across digital asset markets.

At the time of writing, Solana (SOL) was trading at $68.45, down nearly 7% over the previous 24 hours. The decline has unfolded alongside a broader market downturn that pushed the total cryptocurrency market capitalization down roughly 4% to $2.24 trillion.

According to a previous crypto.news analysis, a break below the key $70 support level could shift attention back to the June low around $62 and increase the likelihood of a move toward the $60 region.

Elsewhere in the market, Bitcoin traded near $62,620 after falling more than 4%, adding to pressure across major altcoins and speculative digital assets.

Recent activity suggests Kraken continues to increase its presence across multiple parts of the crypto market.

In May, the exchange launched regulated margin trading services, while earlier this month it joined several industry organizations in urging the U.S. Senate to advance the CLARITY Act, legislation designed to establish a clearer regulatory framework for digital assets.

- Legacy Aztec Network contracts were drained of over $4M in three days.

- Attacks exploited flaws in zero-knowledge proof verification logic.

- The core Aztec network and AZTEC token were not affected by the exploits.

Aztec’s legacy infrastructure has come under a coordinated wave of attacks, leading to losses that crossed $4 million within just three days.

The exploits targeted deprecated smart contracts that had already been shut down years earlier but still held on-chain liquidity.

Despite being labelled as inactive and immutable, the contracts remained accessible to attackers who exploited weaknesses in zero-knowledge proof verification logic.

While the attacks did not affect the current Aztec network or its AZTEC token, they exposed long-standing risks tied to retired DeFi systems that continue to exist on Ethereum without active maintenance or upgrade paths.

First breach: Aztec Connect drained of $2.1 million

The first incident occurred on June 14, when attackers exploited the Aztec Connect protocol, a deprecated privacy-focused bridge that had been officially shut down after its retirement phase.

The contract was already considered inactive, yet it still contained residual funds.

The attacker managed to drain approximately $2.1 million in digital assets, including around 909 ETH, 270,000 DAI, and 167 wstETH, alongside other smaller holdings.

The exploit was linked to flaws in the way rollup proof verification was handled, allowing invalid or manipulated proofs to be accepted as legitimate.

What made the situation more critical was the nature of the contract itself.

Aztec Connect was described as immutable, meaning it could not be paused or patched once deployed.

Even though users had previously been encouraged to withdraw funds before shutdown, the remaining balance became an easy target for exploitation years later.

Security teams reviewing the incident pointed to a breakdown in the relationship between zero-knowledge proof validation and on-chain settlement logic.

In simple terms, the system accepted proofs that did not correctly match the underlying transaction state, allowing the attacker to trigger unauthorised withdrawals.

Second attack: Private Rollup Bridge exploited for $2.15 million

Just three days later, a second exploit hit another legacy system known as the Private Rollup Bridge.

This contract was also part of Aztec’s older infrastructure and had been deprecated following the transition away from earlier rollup designs.

In this case, attackers drained roughly 1,158 ETH, valued at close to $2.15 million at the time of the incident.

The method used was different in execution but similar in technical root cause.

Instead of directly manipulating withdrawals through basic proof mismatch, the attacker leveraged a vulnerable “escape hatch” mechanism embedded in the bridge design.

By submitting a specially crafted zero-knowledge proof, the attacker was able to trigger the contract’s exit logic.

The system incorrectly validated the proof and released funds without proper verification of the underlying state transitions.

This allowed the attacker to extract liquidity in a single coordinated sequence.

Like the earlier exploit, this breach did not involve private key compromise or reentrancy vulnerabilities.

Instead, it highlighted deeper issues in how proof validation was structured in legacy rollup systems, particularly when contracts remain permanently active on-chain after being officially sunset.

Response from Aztec and security firms

Following both incidents, Aztec Labs and the Aztec Foundation confirmed that the affected systems were deprecated products with no connection to the current Aztec network or AZTEC token ecosystem.

The Aztec Foundation was made aware of a potential exploit targeting a deprecated product which occurred on June 17, 2026. There are no links between this product and any smart contracts related to the current network or the AZTEC ERC20 token.

The product was deprecated 4 years… https://t.co/kANaIuw8HF

— Aztec Foundation (@aztecFND) June 18, 2026

They emphasised that neither contract could be upgraded, paused, or controlled, as both were designed to be immutable at deployment.

Security firm CertiK Alert also flagged the Private Rollup Bridge exploit, identifying the attacker’s address and confirming the movement of funds tied to a specific Ethereum transaction.

Their analysis aligned with other reviews, suggesting that the vulnerability stemmed from flaws in zero-knowledge proof verification rather than conventional smart contract bugs.

Aztec representatives also clarified that the Private Rollup Bridge and Aztec Connect incidents were separate events, even though they occurred within a short timeframe and shared similar technical weaknesses.

Crypto World

Bitcoin’s (BTC) nemesis, the Dollar Index (DXY), is on the verge of a major breakout: Daybook: Crypto Daily

Bitcoin and the Dollar Index (DXY) are moving in opposite directions, with the latter on the verge of a major move that may embolden crypto bears.

The largest cryptocurrency is under pressure for a third straight day, trading near $63,900 and down nearly 1% since midnight UTC. The broader market is mostly showing similar losses, with the exception of a few tokens such as HASH, XLM and ENA, which gained 7% or more.

The Dollar Index, which tracks the U.S. currency’s value against major fiat currencies, has gained 0.26% to 100.66, extending Wednesday’s 0.8% rise. What’s notable is that the index is now on the verge of firmly breaking out of a 13-month-long trading range.

This type of setup usually leads to more momentum chasing by traders, resulting in further gains. Strength in the greenback typically weighs on dollar-denominated assets such as bitcoin.

BTC has historically tended to move in the opposite direction to the dollar. Its 90-day correlation coefficient with the DXY was recently minus 0.82.

Crypto World

Mounting AI costs and weaker performance are driving investors toward AI infrastructure

The biggest winners from the rotation have been memory and semiconductor stocks. Memory-chip maker Sandisk (SNDK) has surged roughly 800% this year and the Global X Artificial Intelligence & Technology ETF, which focuses on memory-related companies (DRAM), is up about 140%. In microprocessors, Micron Technology (MU) has gained about 230% this year, and the VanEck Semiconductor ETF (SMH) 67%.

The investments highlight a growing preference for the companies supplying the infrastructure behind the AI boom rather than the hyperscalers funding it.

In addition, capital has been attracted SpaceX (SPCX), Elon Musk’s space exploration company that is also expanding into AI. Last week, the company raised $75 billion in the largest IPO in history.

While AI has become the market’s dominant investment theme, the cash required to feed the growth is rising even faster. Google parent Alphabet (GOOGL), Amazon, Microsoft and Meta are expected to spend a combined $725 billion on capital expenditures this year, a 77% increase from last year’s record level.

Free cash flow is no longer fully funding these ambitions. Alphabet, Amazon and Meta, collectively borrowed some $93 billion last year, accounting for roughly 6% of total corporate bond issuance.

Another source of support is also fading. Share repurchases have fallen 33% to $132 billion in 2025, reducing a key pillar of demand for these stocks.

Is football coming home? English fans tell FRANCE 24

How returning to education mid-career ‘changes your thinking’

World Cup LIVE: Switzerland vs Bosnia updates as Messi statement released, major visa U-turn

-

Business4 days ago

Business4 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World4 days ago

Crypto World4 days agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Crypto World6 days ago

Crypto World6 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Tech6 days ago

Tech6 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Tech6 days ago

Tech6 days agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

NewsBeat7 days ago

NewsBeat7 days agoEl Nino has formed in the Pacific and could set records, forecasters say

-

NewsBeat6 days ago

NewsBeat6 days agoFBI searches office of Ohio voter registration group

-

Tech7 days ago

Tech7 days agoAnthropic is spending $150M to embed 1,000 AI fellows inside nonprofits. No degree required.

-

Entertainment7 days ago

Entertainment7 days ago‘The Pitt’s Fan-Favorite Doctor Confirms Noah Wyle Gave His Blessing to Return [Exclusive]

-

Tech7 days ago

Tech7 days agoFormer AWS CEO Adam Selipsky to lead new $10B AI data center venture

-

Crypto World7 days ago

Crypto World7 days agoRipple and Bitso Bring MXNB Stablecoin to XRP Ledger

-

Entertainment4 days ago

Entertainment4 days agoMatt Damon’s Viral Sci-Fi Thriller Has Taken Over HBO Max

-

Business4 days ago

Business4 days agoAnthropic staff to meet White House officials next week, Axios reports

-

Tech4 days ago

Tech4 days agoAs AI companies race to go public, who else is along for the ride?

-

Business7 days ago

Business7 days agoJustin Bieber Prepares for 2026 Tour Return with New Music and Promoter Talks

-

Crypto World4 days ago

Crypto World4 days agoBitcoin could crash to $48,000, if this historical pattern is triggered

-

Politics4 days ago

Politics4 days ago“Israel’s” ban on ICRC visits ruled illegal, but Knesset moves to stop them permanently

-

Tech7 days ago

Tech7 days agoEuro-Office 1.0 Arrives To Open-Source Infighting: ‘Compatibility Is Not Sovereignty’

-

Entertainment7 days ago

Ana Navarro unleashes explosive tirade on ex-Trump aide, Disney Channel star in epic on-air fight: 'Have you no shame?'

You must be logged in to post a comment Login