Crypto World

Three AI Chip Stocks Trading Below Their Potential: Micron (MU), AMD, and TSMC (TSM)

Key Highlights

- Micron’s Q2 fiscal 2026 quarterly sales surged nearly 200% compared to the prior year, with records set in all divisions

- AMD delivered $10.3 billion in Q4 2025 sales, marking a 34% jump year-over-year alongside a 57% non-GAAP gross margin

- TSMC forecasts approximately 30% revenue expansion in 2026 when measured in U.S. dollars

- Despite strong AI exposure, these three companies maintain more modest price-to-earnings multiples than leading AI chipmakers

- TSMC anticipates its AI accelerator division will expand at a compound annual rate in the mid-40 percent range through 2029

Three semiconductor powerhouses—Micron, AMD, and Taiwan Semiconductor Manufacturing—are riding the artificial intelligence wave with impressive momentum. Yet despite robust financial performance and accelerating growth trajectories, market analysts suggest these stocks may be undervalued relative to their sector peers.

The ongoing buildout of AI infrastructure has created surging demand across the semiconductor supply chain, from specialized memory modules to cutting-edge processors and advanced fabrication services. While these companies occupy distinct positions within this ecosystem, they share a compelling characteristic: substantial revenue acceleration without the elevated valuation multiples commanded by other AI-focused names.

Micron: Transforming from Commodity Memory to Critical AI Component

Micron has undergone a remarkable repositioning in investor perception, evolving from a cyclical commodity producer into an essential AI infrastructure provider.

During the company’s fiscal second quarter of 2026, revenues expanded almost threefold versus the same period twelve months prior. The semiconductor manufacturer achieved unprecedented performance levels across its entire product portfolio, including DRAM, NAND flash, high-bandwidth memory, and all operating segments.

Profitability metrics showed equally dramatic improvement. The company’s fiscal third-quarter outlook alone is projected to surpass total annual revenue figures from any fiscal year ending through 2024.

Artificial intelligence servers demand massive quantities of specialized high-bandwidth memory, and Micron has positioned itself as a primary supplier for this critical component. Company leadership indicated that robust demand coupled with constrained supply conditions will likely persist well into 2027.

The manufacturer is also negotiating extended, multi-year supply agreements with major customers, potentially transforming the business model toward greater predictability and reducing the historical boom-bust patterns that characterized the memory industry.

Despite these fundamental improvements, Micron continues trading at a valuation discount compared to AI chip designers, even as memory has become indispensable to the AI computing architecture.

AMD: Impressive Performance in Nvidia’s Shadow

AMD announced record quarterly sales of $10.3 billion for Q4 2025, representing a 34% year-over-year increase. The company achieved a non-GAAP gross margin of 57%.

Advanced Micro Devices, Inc., AMD

Chief Executive Lisa Su characterized 2025 as a transformational year and emphasized that the company began 2026 with substantial forward momentum. She highlighted the EPYC processor family and expanding data center AI operations as primary growth engines.

AMD is constructing a comprehensive AI ecosystem that encompasses data center graphics processors, server central processing units, and strategic system-level collaborations.

Market participants frequently position AMD as a direct competitor to Nvidia and sometimes dismiss it as the inferior alternative. However, AMD’s investment thesis doesn’t require outperforming Nvidia entirely. The company simply needs to capture increasing market share within a rapidly expanding addressable market while maintaining healthy profit margins.

If AMD sustains its AI accelerator growth trajectory while preserving margin discipline, several analysts believe current valuations may prove significantly discounted when viewed retrospectively.

TSMC: The Essential Manufacturing Infrastructure Powering AI Innovation

TSMC produces the sophisticated semiconductor chips that power much of today’s AI economy. The foundry giant projects 2026 revenues will expand by nearly 30% when denominated in U.S. currency.

Taiwan Semiconductor Manufacturing Company Limited, TSM

AI accelerator production represented a high-teens percentage of total 2025 revenue. Management forecasts this segment will grow at a compound annual growth rate in the mid-40 percent range during the five-year period beginning in 2024.

TSMC’s strategic position differs fundamentally from Micron or AMD. The company maintains diversification across products and customers rather than depending on any single offering or client relationship. As long as demand for leading-edge semiconductor manufacturing remains robust, TSMC occupies an irreplaceable position within the global supply chain.

The manufacturer operates production facilities throughout Taiwan, Japan, and the United States, with additional American expansion projects currently in development.

Final Thoughts

Micron, AMD, and TSMC have all delivered compelling financial results in their latest reporting periods. Each company maintains substantial exposure to AI hardware demand while demonstrating expanding revenues and improving profitability. The sustainability of these growth trends will largely depend on whether AI infrastructure investment maintains its current pace throughout the remainder of 2026 and beyond.

TLDR:

- SUI broke above the $0.89–$0.90 consolidation range on the one-hour chart, signaling a bullish trend shift.

- Price pulled back to the $0.91–$0.905 demand zone, where analysts expect buyers to defend key support.

- Wyckoff accumulation patterns and bullish order blocks on the weekly chart point to targets of $10–$20.

- SUI’s market cap stabilized above $3.6B after spiking to $3.85B, reflecting long-term holder conviction.

SUI price prediction is flashing signals that seasoned traders rarely ignore. A textbook breakout above a weeks-long consolidation range, a controlled pullback into fresh demand, and a weekly chart carrying the fingerprints of prior 1,000% rallies, the setup is building quietly but deliberately.

Whether the next move targets $0.97 or something far more ambitious, the chart is making its case without apology.

SUI Breaks Out, Pulls Back, and Sets Up a Second Shot

SUI flashed a textbook breakout on the one-hour chart this week, clearing the $0.89–$0.90 consolidation range that had capped price for an extended period. The move was sharp and deliberate.

Bullish candles stacked above prior resistance, volume followed, and the chart shifted from a downtrend structure to a clear bullish bias in a matter of hours.

The rally did not hold its highs. SUI pulled back toward the $0.91–$0.905 area shortly after, a move that initially spooked short-term traders. However, analysts tracking the asset noted the correction lacked the hallmarks of a genuine reversal.

No heavy sell volume. No breakdown of structure. Just a measured retreat into what is now a recognized demand zone, where previous resistance has flipped into support.

That flip is the crux of the current setup. Traders are now watching for bullish confirmation at the $0.91–$0.905 zone before positioning for another push toward the $0.96–$0.97 resistance band.

Until that confirmation arrives, the market remains in a wait-and-see posture at a level that could determine SUI’s next directional move.

Weekly Structure Points to Targets Far Beyond Current Levels

Step back to the weekly chart and the short-term noise gives way to a much larger technical picture. SUI has printed this pattern before.

In mid-2024 and again in mid-2025, the price dipped toward a key trendline support, gathered liquidity at those lows, and then staged parabolic advances.

Those rallies registered gains north of 500% and, in one instance, crossed 1,000% within a matter of months. Analysts point out that SUI is currently sitting at a structurally similar position.

Bullish order blocks are visible at the current support zone, consistent with what Wyckoff analysis describes as smart money accumulation — a phase where institutional-level buying absorbs retail selling before a major directional move develops.

Resistance between $3 and $5 is flagged as a potential speed bump on any extended advance. Even though historical precedent suggests momentum tends to build rather than stall once that band is cleared.

Market cap data from the past seven days adds a layer of confirmation to the broader thesis. SUI’s market cap spiked toward $3.85 billion on April 7 before pulling back and stabilizing above $3.6 billion through several corrective sessions.

The base is holding. Long-term participants appear to be absorbing the dips rather than exiting, a dynamic that analysts say keeps the structural case for $10–$20 price targets firmly on the table.

Adam Back, the Blockstream CEO named by the New York Times as the most likely candidate behind Satoshi Nakamoto, may have had a more practical reason for cooperating with the investigation.

Several industry figures now suggest Back used the global media attention as free publicity for Bitcoin Standard Treasury Company (BSTR), his Bitcoin (BTC) treasury firm approaching a public listing.

Did Adam Back Use NYT Satoshi Story as Free BSTR Publicity?

John Carreyrou, the investigative reporter behind the explosive expose revealed that Back agreed to pose for a NYT photographer in Miami weeks before the story ran.

“If you’re IPO’ing a company — it’s pretty damn good PR. Particularly when the cost is roughly zero,” commented ETF analyst James Seyffart.

The timing matters because BSTR is completing a SPAC merger with Cantor Equity Partners I. The deal includes a $1.5 billion PIPE, the largest ever announced for a Bitcoin treasury vehicle.

BSTR plans to launch with over 30,000 BTC on its balance sheet, which would catapult its ranks among the largest public Bitcoin treasury.

The merger was originally expected to close in Q1 2026, subject to SEC review and shareholder approval.

Whether Back intended the headlines or simply welcomed them, the Satoshi spotlight landed at the most commercially convenient moment possible.

The post Free PR or Confession? Expert Thinks Adam Back Played the NYT Like a Prospectus appeared first on BeInCrypto.

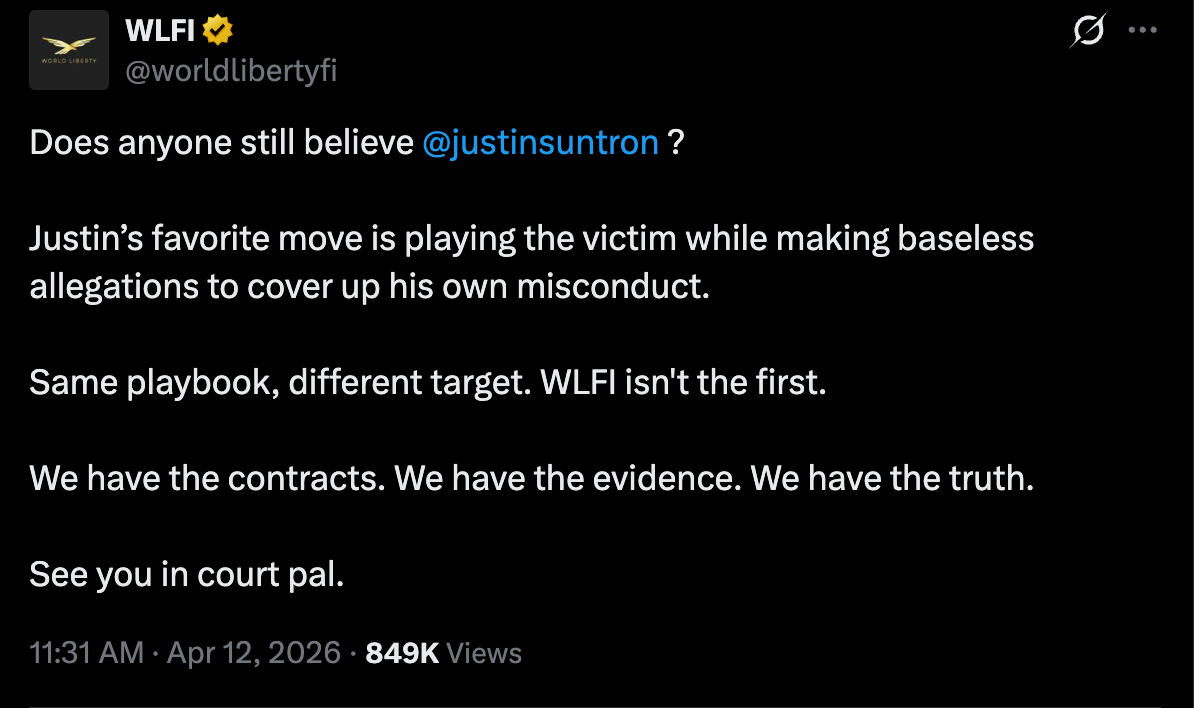

Justin Sun, the founder of the Tron layer-1 blockchain network, criticized World Liberty Financial (WLFI), a decentralized finance platform co-founded by US President Donald Trump’s sons, over lengthy lock-up periods for the platform’s governance token.

Sun said that he invested “significant capital” in WLFI as an early investor and also said that a March WLFI governance proposal to determine token lock-up periods, in which more than 76% of the voting tokens came from 10 wallets, lacked transparency. In a Sunday post on X, Sun wrote (in translation):

“The governance votes cited to justify the above actions were not conducted through fair or transparent procedures. Key information was withheld from voters, meaningful participation was restricted, and outcomes were predetermined.”

“Justin’s favorite move is playing the victim while making baseless allegations to cover up his own misconduct,” World Liberty Financial said in response, threatening legal action against Sun over his claims.

The incident came amid community pushback against WLFI and confirmation that the platform was using its own governance tokens as loan collateral, causing the price of WLFI to sink to an all-time low and renewed backlash against Trump for his crypto activities.

Cointelegraph reached out to World Liberty Financial but did not obtain a response by the time of publication.

Related: World Liberty signals phased WLFI unlock vote after early holder backlash

WLFI token sinks to all-time low as community backlash mounts

The WLFI token hit a new all-time low on Saturday, falling to just $0.07 following news of the platform using WLFI tokens as collateral to borrow stablecoins.

Wallets linked to World Liberty Financial used WLFI tokens as collateral on Dolomite, a DeFi platform co-founded by the project’s chief technology officer, Corey Caplan, to take out the stablecoin loan.

WLFI confirmed that it acts as an “anchor” borrower, which generates yield for the platform and value for token holders, adding that it is “one of the largest suppliers and borrowers” in the WLFI ecosystem.

“Treating the crypto community as a personal ATM is unjust and has never been authorized through any fair, transparent, good-faith community governance process,” Sun said.

Magazine: Trump’s crypto ventures raise conflict of interest, insider trading questions

Crypto World

Aave Will Win Proposal Passes: AAVE Token Now Controls Protocol Revenue, Brand, and Full Product Stack

TLDR:

- Aave Will Win proposal directs application revenue from Aave Pro, Aave App, and Horizon directly to the DAO treasury.

- Aave’s protocol revenue reached $140 million in 2025, with 2026 tracking similarly despite market weakness.

- Swaps on Aave.com and Aave Pro are generating $10–20 million in new revenue on top of existing protocol income.

- Aave Labs commits to zero-bureaucracy governance, requiring measurable SP goals and full financial transparency.

Aave has passed what its community calls the most important proposal in the protocol’s history. The Aave Will Win (AWW) proposal secured a landslide governance vote, reshaping how the protocol generates revenue.

The new framework positions the AAVE token as the central asset across all products and brand assets. It also introduces new application revenue streams beyond the core protocol. These earnings are directed entirely to the DAO treasury for the first time.

Aave Moves Toward a Full-Stack Revenue Model

The AWW proposal creates a new revenue layer on top of existing Aave Protocol earnings. Application and product revenue from Aave Pro, Aave.com, Aave App, Horizon, and Aave Kit will now flow to the DAO.

This represents a clear expansion beyond the protocol-only revenue model that has existed since the project launched.

According to Aave Labs founder Stani Kulechov, the DAO accumulated $140 million in protocol revenue in 2025. Revenue for 2026 is tracking at a similar level despite broader market weakness.

That growth was achieved through protocol-only income alone, making the addition of application revenue a notable shift.

Kulechov noted on X that swaps on Aave.com and Aave Pro are already generating between $10 million and $20 million.

This revenue is additive, sitting on top of what the protocol already generates. Together, the two streams begin building the full-stack revenue model the proposal envisions.

Aave V4’s reinvestment feature allows idle capital in pools to generate additional yield for the protocol. New V4 Spokes will also unlock further collateral and address the demand side of the DeFi liquidity market. These technical upgrades work in tandem with the revenue changes introduced under AWW.

Aave Labs has committed to working exclusively on the protocol’s own products going forward. This means AAVE token holders now own the protocol’s brand, users, and integrations through one unified asset.

Owning the full vertical stack is increasingly important as protocol competition intensifies across the DeFi space.

Governance Rules Tighten as Risk Management Expands

The governance model under AWW is shifting to a zero-bureaucracy structure focused on execution. Service providers will now be held to real, measurable goals rather than process-heavy deliverables.

The change reflects the DAO’s intent to compete with well-funded and efficient organizations in the broader financial sector.

Kulechov stated plainly on X: “Payments for posting governance proposals are over.” The DAO has already consolidated service providers to direct resources more effectively.

Going forward, SPs who align with token holder interests will receive budget support, provided their requests remain reasonable.

Under the new rules, full transparency from all service providers is a firm requirement. Relationship gating and value leakage away from the protocol will not be tolerated. Everything built with the DAO’s funds must benefit the protocol and remain owned by it.

On the risk side, Aave will maintain a dual-layer approach covering both economic and technical risk assessment. External managers such as Llama Risk and Token Logic will continue operating in their current roles. Their work will be supported and coordinated by a new internal team at Aave Labs.

Aave Labs will build a permanent internal risk management function to sit alongside external managers. This combined structure makes the overall risk framework more resilient.

Better coordination between layers is expected to strengthen the protocol’s response to market and technical risks ahead.

Crypto World

Whales Keep Buying TRUMP Meme Coin Before Mar-a-Lago Event, But Price Drops to Record Low

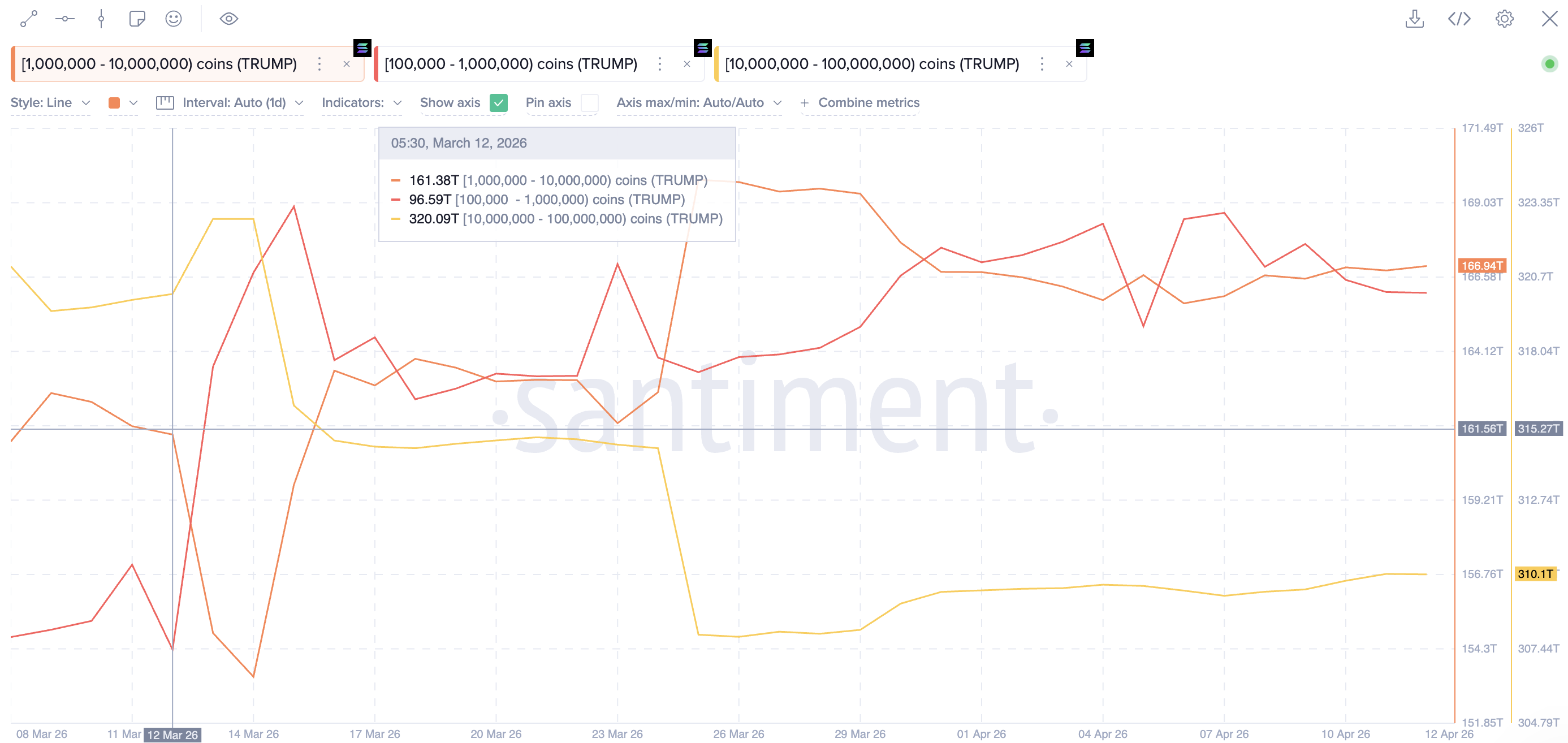

Whale activity around Official Trump (TRUMP) is intensifying, with holders accumulating tokens ahead of the April 25 crypto conference and gala luncheon at Donald Trump’s Mar-a-Lago resort.

On-chain tracker Lookonchain reported that one wallet withdrew 850,488 TRUMP worth $2.4 million from Bybit over the past two days. Moreover, a second wallet pulled 105,754 TRUMP from Binance. The wallet now holds 1.13 million tokens valued at $3.2 million.

Follow us on X to get the latest news as it happens

TRUMP Meme Coin Whales Stack Tokens

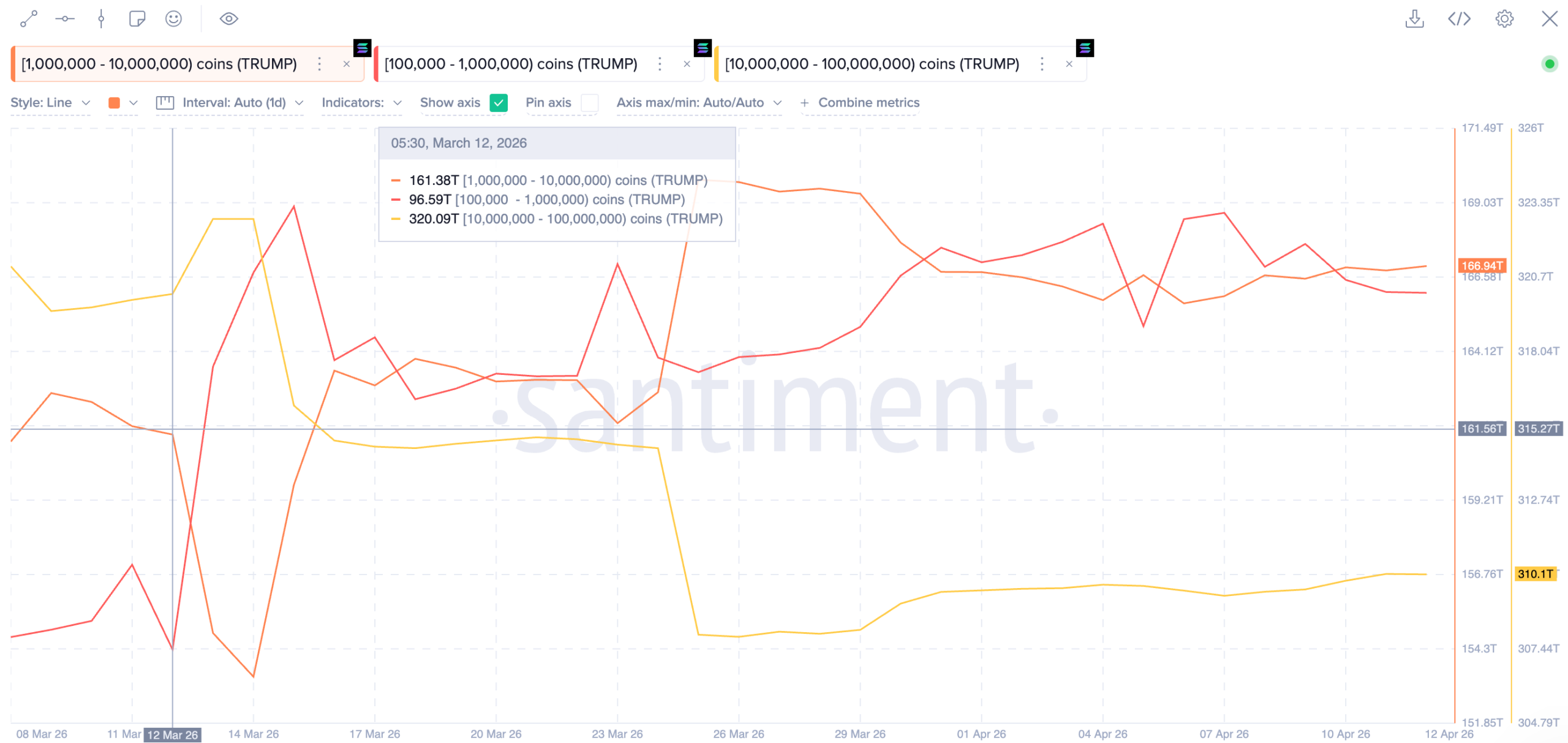

On-chain data from Santiment reveals a clear redistribution pattern since the event was announced on March 12. The largest holder tier, wallets holding between 10 million and 100 million tokens, trimmed positions from 320.09 trillion to as low as 307.95 trillion in late March.

However, the buying activity picked up after, with holdings increasing to 310.1 trillion on April 12.

Whales in the 1 million to 10 million range moved in the opposite direction. Those wallets added 5.56 trillion tokens during the same period, bringing their holdings to 166.94 trillion.

Wallets in the 100,000-1 million bracket followed a similar trajectory. Their holdings grew 5% from 96.59 trillion to 101.46 trillion.

BeInCrypto previously reported that the top 297 holders on the leaderboard will earn a seat at the conference. The 29 largest wallets receive VIP access to a private reception with the president.

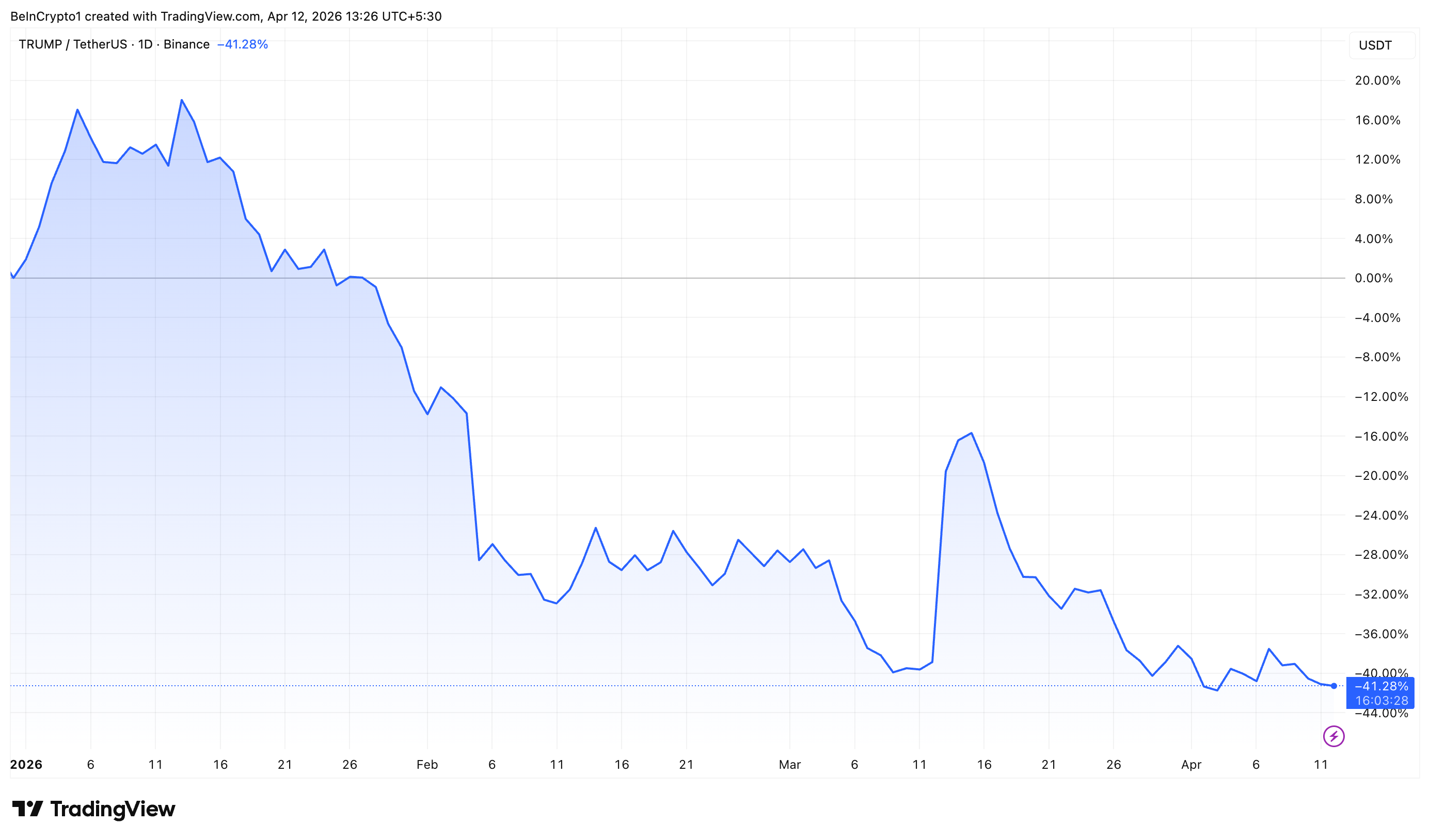

TRUMP surged over 50% following the March announcement, briefly touching $4.49. However, the token has since given back all of those gains. It traded at approximately $2.8 on April 12.

Overall, in 2026, the meme coin is down by more than 41% and has lost more than 11% over the past month alone. With the event less than two weeks away, the gap between ongoing whale accumulation and falling prices sets up a volatile stretch for TRUMP holders.

The post Whales Keep Buying TRUMP Meme Coin Before Mar-a-Lago Event, But Price Drops to Record Low appeared first on BeInCrypto.

TLDR:

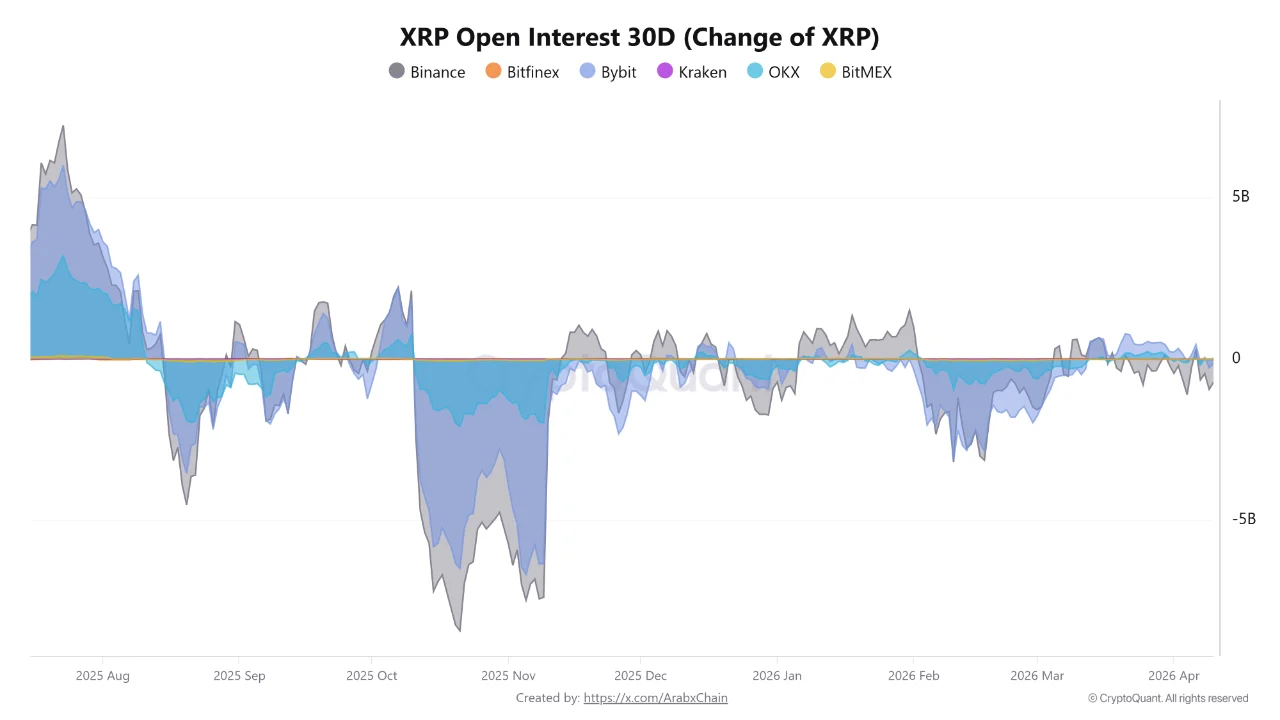

- Binance recorded the largest XRP open interest decline, dropping by approximately 721.49 million XRP in recent periods.

- Bybit posted a fall of around 132.10 million XRP in open interest, reflecting weakened speculative momentum across the platform.

- Bitfinex added to the downtrend with a decline of roughly 10.96 million XRP, completing a consistent drop across all three major exchanges.

- Falling XRP open interest may reduce liquidation risks and set early conditions for a potential recovery once liquidity returns.

XRP open interest has fallen sharply across major futures trading platforms in recent periods. Binance, Bybit, and Bitfinex each recorded a drop in open positions, pointing to reduced speculative activity.

Traders appear to be pulling back from leveraged exposure in the XRP market. Position closures have outnumbered new entries across all three platforms.

The data reflects a broader shift in market sentiment as liquidity exits XRP futures at a steady pace.

Binance Leads Drop as Bybit and Bitfinex Also Record Declines

Binance recorded the steepest fall, with XRP open interest declining by roughly 721.49 million XRP. As one of the largest futures exchanges globally, its movements tend to mirror broader market behavior. The sharp drop points to substantial position closures, possibly tied to recent price volatility in XRP.

Bybit ranked second, posting a decline of approximately 132.10 million XRP in open interest. While smaller than Binance’s figure, the drop still reflects reduced speculative momentum in the market. Traders on Bybit also appear to have pulled back from active positioning in XRP futures.

Source: Cryptoquant

Bitfinex came in third with a decline of around 10.96 million XRP in open interest. The figure, though smaller, adds to the consistent downward pattern seen across the other platforms. Three major exchanges declining together builds a coherent picture of retreating market liquidity.

Across all three platforms, position closures have dominated trading activity in this period. The combined exit of open interest reflects a measurable weakening of futures participation in XRP. This type of retreat often follows price instability or a wave of forced liquidations across the market.

Lower Liquidity Could Create Conditions for a Market Recovery

A decline in XRP open interest does not necessarily point to a permanent bearish trend. In many cases, falling open interest reflects a temporary pause as traders reassess their exposure.

When liquidity exits a market, the resulting calm can precede a stronger directional price move. Analysts typically monitor these conditions for early signs of a potential trend reversal.

The exit of liquidity from XRP futures also lowers the risk of cascading liquidations going forward. With fewer open positions on record, sudden price swings are less likely to trigger large sell-offs. This dynamic can help form a more stable foundation for price recovery over time.

The current pullback in XRP open interest also takes place amid wider turbulence in crypto derivatives. XRP futures are particularly sensitive to sentiment shifts given the asset’s trading volume.

Monitoring these data points will remain important for traders tracking directional movement in XRP.

Once liquidity returns and new positions begin to form, market activity in XRP may pick up again. Open interest recovery, particularly on Binance, would serve as an early indicator of renewed demand. The sessions ahead will likely determine whether this retreat marks a floor or a deeper exit.

TLDR:

- Average ROI across 2026 token launches sits at -54%, with RNBW losing nearly 90% from its ICO price.

- Attention and liquidity both peak at TGE and consistently fail to recover, trapping retail buyers at the top.

- Projects like MegaETH and Polymarket are now delaying TGEs until real usage milestones and traction are confirmed.

- Tokens with proven product-market fit like Pendle and Hyperliquid continue holding narrative ground above newer launches.

Token launches in 2026 are delivering deeply negative returns for early participants, according to recent on-chain data.

Average ROI across this year’s launches sits at approximately -54%, raising serious questions about the current fundraising model.

Projects like RNBW, ZAMA, and AZTEC have each lost between 43% and nearly 90% of their value after their token generation events.

Market analysts now point to structural flaws in how new tokens reach the market. The pattern is consistent, and it is hitting retail investors hardest.

The Data Behind the Decline

Recent figures paint a troubling picture for anyone entering early-stage token sales. RNBW dropped 89.87% from its ICO price, while ZAMA fell 43% after its TGE. AZTEC declined nearly 50% shortly after going live on exchanges.

These are not isolated cases. The -54% average ROI across 2026 launches points to a recurring structural problem with token distribution and pricing at launch.

Crypto researcher Nick Research flagged this pattern publicly, noting that both attention and liquidity peak at TGE and then never recover. That observation lines up with what data consistently shows across multiple project launches this cycle.

The core issue is the low float, high fully diluted valuation model combined with heavy venture capital allocations. This structure creates what analysts describe as an exit liquidity machine, where early backers offload holdings onto retail buyers at peak hype.

A Market Pivoting Toward Usage and Revenue

Despite weak performance data, token launches are not disappearing entirely. However, the model is clearly evolving in response to consistent losses by retail participants.

MegaETH has chosen to delay its TGE until specific key performance milestones are met. Polymarket and OpenSea have also withheld firm launch dates, a move that signals growing caution among project teams about launching before real traction exists.

This shift reflects a broader recalibration in how investors assess new projects. The speculation-first approach that defined earlier cycles is giving way to a usage-first standard that the market now rewards more visibly.

Tokens with genuine product-market fit continue to hold narrative ground. Assets such as Pendle and Hyperliquid retain attention in ways newer launches simply cannot match.

BTC, ETH, SOL, TAO, and HYPE still dominate market conversation, crowding out newer entrants almost entirely within days of any new launch.

New experiments in attention markets and cashback incentive models are also emerging as alternative frameworks. These designs attempt to align token value with real platform usage rather than speculative demand.

For now, the market is sending a clear message: proof of traction before TGE is no longer optional for any project seeking long-term viability.

Crypto World

CFTC Chair Mike Selig argues for agency’s ‘exclusive regulatory authority’ in prediction markets fight: State of Crypto

Commodity Futures Trading Commission Chairman Mike Selig told CoinDesk that the agency will continue to defend its “exclusive regulatory authority” to oversee prediction markets in court. “It doesn’t matter if it’s on sports, politics or anything else, if it’s a validly offered product within a CFTC-regulated exchange, then we regulate that,” Selig said.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

NASHVILLE, Tenn. — The Commodity Futures Trading Commission is just defending its territory in suing states over prediction markets, the regulator’s head told CoinDesk.

CFTC Chairman Mike Selig, speaking on the sidelines of the Digital Assets and Emerging Tech Policy Summit hosted by Vanderbilt University and the Blockchain Association on Monday, said the agency’s lawsuits against Arizona, Illinois and Connecticut make it “very clear … that the CFTC has exclusive regulatory authority when it comes to commodity derivatives markets.”

Selig, who is speaking at CoinDesk’s Consensus Miami conference next month, said Monday’s Third Circuit Court ruling that the CFTC has to oversee prediction markets bolstered his agency’s view.

Under Selig, the CFTC has embarked on a major litigation effort to bolster prediction markets’ arguments that they are providing derivatives products under the Commodity Exchange Act, rather than gambling services regulated by states.

“Our view is that the statute is very clear that when you offer a swap on a federally regulated Designated Contract Market, that transaction, those trades, are subject to federal regulation,” he said. “It doesn’t matter if it’s on sports, politics or anything else; if it’s a validly offered product within a CFTC-regulated exchange, then we regulate that, and the states don’t have the ability to nullify federal oversight and substitute gambling laws where derivatives laws apply.”

Asked why the CFTC did not sue Nevada or Massachusetts — two states that have successfully secured preliminary injunctions against prediction market providers — Selig said that “I wouldn’t say, just because these are the first states, that they’ll be the last.”

He pointed out that the CFTC filed an amicus brief in a consolidated case before the Ninth Circuit Court of Appeals, which will be heard next week. The Ninth Circuit includes Nevada.

Dodd-Frank swaps

Under the Dodd-Frank Act, the CFTC can regulate swaps and can block certain types based on whether they are in the public interest. These categories include war, terrorism, assassination, gaming, anything otherwise illegal or “other similar activity.”

Selig said the main issue is that, under the law, the CFTC decides whether a product is contrary to the public interest. The lawsuits it’s engaged in are focused on that aspect — regardless of the events underlying the contracts.

“Even if those categories of underlyings, whether it’s war terrorism, assassination, gaming, and so on and so forth, even if we have to do a public interest analysis, or we choose to do a public interest analysis, that doesn’t mean that that’s not within our exclusive regulatory authority,” he said. “And so that’s what the cases are about, and that’s what we’re fighting for.”

The CFTC is currently going through the formal rulemaking process to clarify its oversight of prediction markets.

“We’re open to suggestions as to what that process should look like and how to evaluate it,” he said. “We’re certainly considering that provision of the Dodd-Frank Act.”

Interpretative guidance

Outside prediction markets, Selig said the CFTC would review any comments on the final interpretation it published with the Securities and Exchange Commission last month.

“To the extent we get feedback on certain things we might change or need to reconsider, we’ll certainly do that,” he said.

More importantly, he said, the creation of a taxonomy means if any company wants to self-certify a futures product tied to a digital asset, the CFTC and SEC can just look to their guidance to ensure the token is not a security.

“To the extent you have a tokenized security, we’re not butting heads on the CFTC claiming it’s a commodity or the SEC claiming a different type of commodity as a security,” he said. “We’ve got clear lines drawn in the statute.”

The guidance was intended to be comprehensive, so both the companies and the agencies had examples, he said.

“We should be very much aligned across agencies,” he said.

Monday

- 13:00 UTC (9:00 a.m. ET) SEC Chair Paul Atkins will speak at the IMF-IOSCO conference on new technologies.

Thursday

- 14:00 UTC (10:00 a.m. ET) The House Agriculture Committee will hold a hearing with CFTC Chair Mike Selig. There are not many details about the topic of the hearing — it just said it’s “for the purpose of receiving testimony.”

- 16:00 UTC (9:00 a.m. PT) A Ninth Circuit Court of Appeals panel will hear arguments in a consolidated set of cases around prediction markets and state regulators. The CFTC filed an amicus brief in this case and will also speak during the arguments.

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at nik@coindesk.com or find me on Bluesky @nikhileshde.bsky.social.

You can also join the group conversation on Telegram.

See ya’ll next week!

TLDR:

- Michael Saylor posted “Think ₿igger” on X, widely read as a signal of Strategy’s next Bitcoin purchase.

- Bitcoin dropped to $71,500 after US-Iran peace talks in Islamabad collapsed without an agreement.

- Strategy holds 766,970 BTC worth $54.47B, buying at 2.2x the rate of newly mined supply in 2025.

- With $2.25B in reserves and a $42B ATM facility, Strategy has the firepower for continued buying.

Bitcoin watchers are on high alert. Michael Saylor, The Strategy executive chairman dropped two words on X — “Think ₿igger”.

With 766,970 BTC already on the books and geopolitical fires burning from the Strait of Hormuz to Islamabad, Saylor’s latest post is making markets wonder what comes next and how large the next purchase will be.

Saylor’s “Think ₿igger” Post Stops the Crypto World in Its Tracks

Two words. That is all it took. Michael Saylor posted “Think ₿igger” on X on April 12, attaching the Orange Dots chart that has become one of the most anticipated visuals in institutional crypto circles.

Each orange dot marks a Bitcoin purchase by Strategy. More dots have always followed.

The post landed at a moment when Bitcoin was already bleeding, sliding toward $71,500 as news broke that high-stakes US-Iran peace talks in Islamabad had collapsed without a deal.

The negotiations, the most direct diplomatic exchange between Washington and Tehran in decades, fell apart over nuclear commitments and control of the Strait of Hormuz. Markets did not take it well.

The Strait of Hormuz is no small flashpoint. Roughly one-fifth of the world’s oil supply moves through that narrow waterway daily.

When the US Navy began minesweeping operations in the region, risk sentiment cracked across equities, commodities, and crypto alike.

Bitcoin dropped approximately 2.5%, caught in the crossfire of a geopolitical standoff with no clear resolution in sight. Yet there was Saylor, unfazed, pointing toward something larger.

Last week, Strategy confirmed a $330 million Bitcoin purchase shortly after a similar Orange Dots post appeared. The pattern is well-established at this point. When Saylor posts the chart, a buy announcement tends to follow within days.

Strategy’s War Chest Positions the Firm for Another Major BTC Move

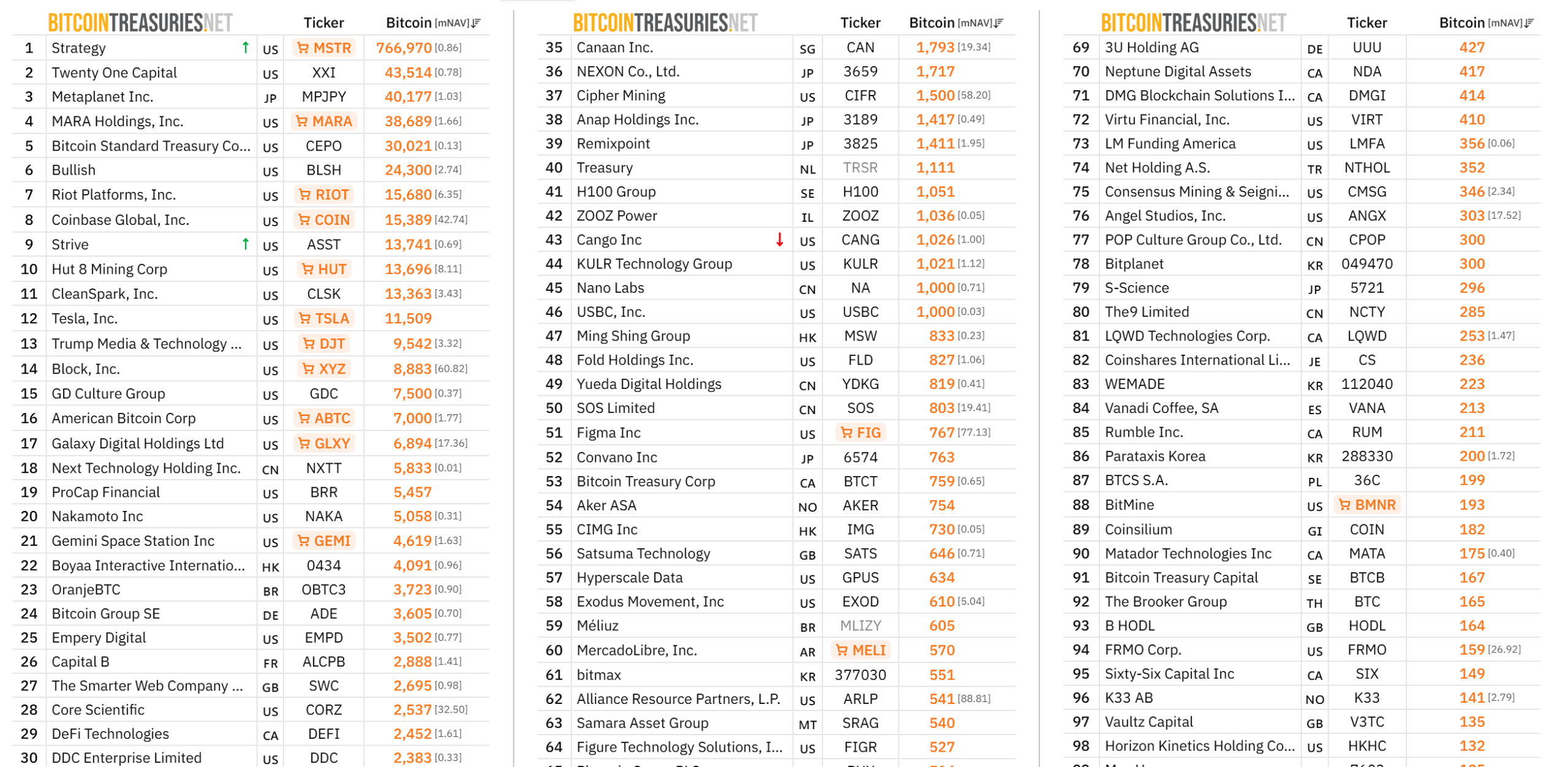

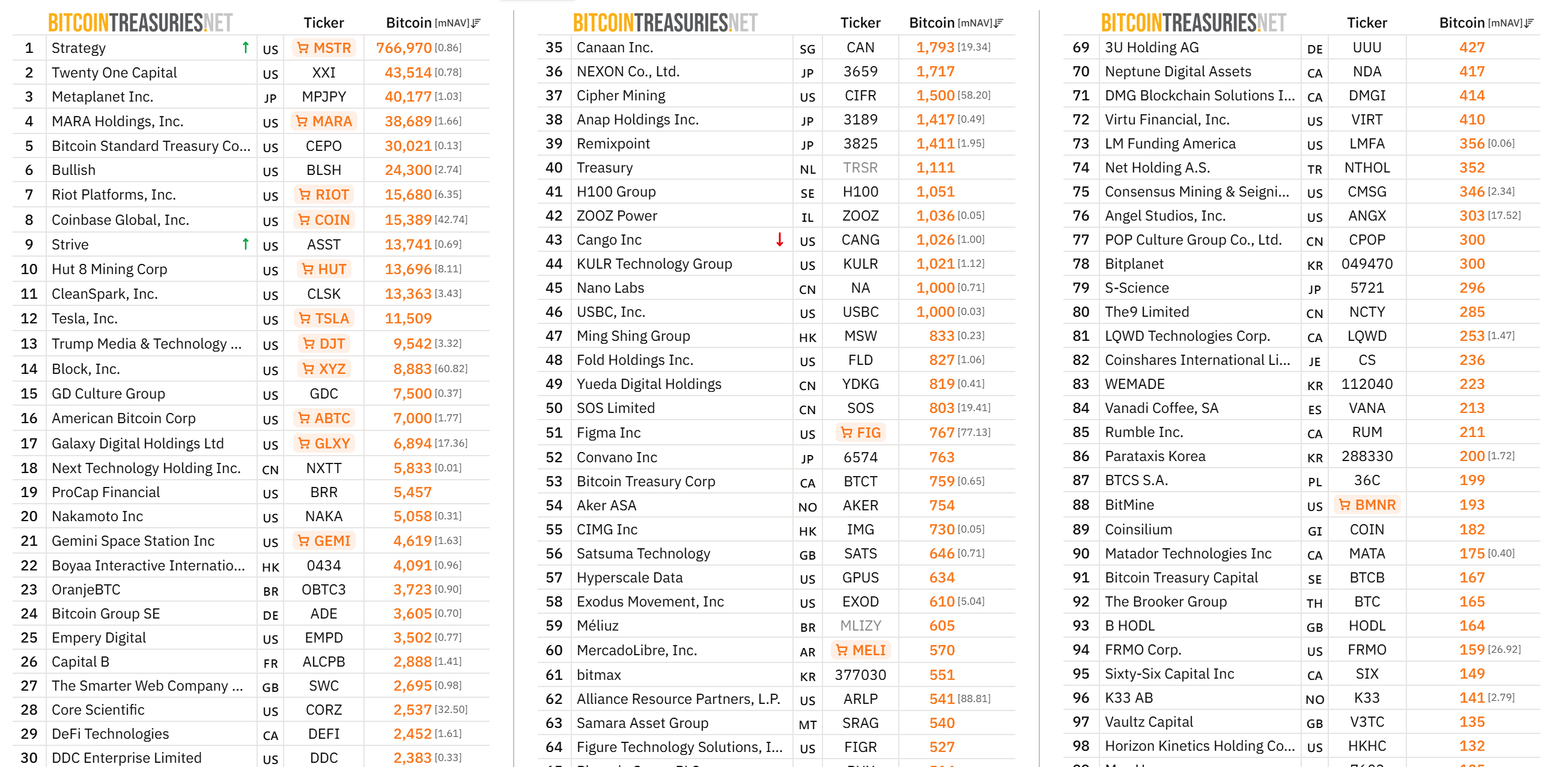

Strategy is not operating on hope. The numbers behind the firm’s Bitcoin ambitions are striking. The company currently holds 766,970 BTC, valued at approximately $54.47 billion, accumulated at a pace running 2.2 times faster than the newly mined supply entering the market.

That kind of buying velocity does not happen without serious financial infrastructure behind it. The balance sheet backs up the aggression.

Strategy carries $2.25 billion in USD reserves against $8.25 billion in total debt, with net leverage holding at a disciplined 11%. Enterprise value has climbed to $60.9 billion, comfortably ahead of its $44.6 billion market capitalization.

These are not the numbers of a firm about to slow down. The capital pipeline tells the same story.

A $42 billion at-the-market equity facility remains available, with additional runway coming through ongoing STRC fundraising. Strategy paused a 13-week consecutive buying streak in late March, but that pause now looks brief.

With Saylor’s post circulating and the financial machinery still running at full capacity, another major Bitcoin acquisition may already be in motion.

Strategy, the Bitcoin treasury vehicle led by Michael Saylor’s publicly traded company, continues to accumulate BTC even as the market retreats from the week’s high. After Bitcoin briefly topped the $73,000 mark, Strategy reaffirmed its intent to keep adding, underscoring a deliberate, long-horizon bet on digital assets despite broader macro headwinds.

On Sunday, Saylor circulated a chart tracking Strategy’s BTC purchase history and urged followers to “Think bigger,” a refrain that has become closely tied to the firm’s ongoing accumulation. The most recent disclosed buy occurred on April 6, when Strategy bought 4,871 BTC for more than $329.8 million, according to a filing with the U.S. Securities and Exchange Commission. With this addition, Strategy’s total holdings rose to 766,970 BTC, a stake valued at roughly $54.5 billion using contemporaneous prices cited in the filing. The Tysons Corner, Virginia-based company continues to be widely cited as the largest BTC treasury by holdings, a standing corroborated by BitcoinTreasures data.

Key takeaways

- Strategy pressed on with BTC accumulation, adding 4,871 BTC in the April 6 purchase for more than $329.8 million, bringing total holdings to 766,970 BTC.

- The average acquisition cost for Strategy’s BTC is $75,644 per coin; the current market value circumscribed by the cited prices places the cost basis notably below the prevailing price at publication.

- Strategy reports unrealized losses of about $14.5 billion on its BTC holdings for Q1 2026, according to its SEC filing, highlighting the contrast between cost basis and mark-to-market value during a prolonged bear phase.

- In March, Strategy’s accumulation outpaced new supply from miners, with miners producing ~16,200 BTC and Strategy purchasing 46,233 BTC that month—roughly three times the newly mined output.

- BitcoinTreasuries still ranks Strategy as the largest BTC treasury holder, with Twenty One Capital as the next-largest holder at 43,514 BTC; other notable activity includes MARA Holdings’ March sale of 15,133 BTC to finance a debt repurchase, signaling mixed treasury strategies in the sector.

Strategy’s unyielding BTC accumulation and what it signals

The ongoing accumulation posture by Strategy matters because it represents a steady, high-profile load of supply being absorbed by a single entity. The April 6 purchase—4,871 BTC for more than $329.8 million—keeps Strategy’s aggregate holdings near a threshold that many market observers consider a floor for the firm’s long-term bets on Bitcoin adoption and macro hedging. With the latest purchase, the total BTC reserve sits at 766,970 coins, a level that places Strategy well ahead of all other corporate treasuries tracked publicly by BitcoinTreasuries. The market value cited in the filing—about $54.5 billion at the prices of that day—illustrates the scale at which the firm operates within the sector’s balance-sheet dynamics.

The company’s stance sits in contrast to the capitulation narratives that have surrounded other large holders in a challenging operating environment. As Strategy continues to accumulate, it maintains a cost basis of roughly $75,644 per BTC on average. That figure sits below the current price band, offering a cushion relative to recent volatility. Still, the unrealized losses reported for the quarter magnify the tension between long-term confidence in Bitcoin’s narrative and the short-term mark-to-market realities that press publicly traded treasuries to disclose in quarterly filings.

Unrealized losses, mining dynamics, and the broader market context

Strategy reported approximately $14.5 billion in unrealized losses on its BTC position for the first quarter of 2026. Such a figure underscores that profitability on paper can diverge sharply from the firm’s long-term conviction in the asset class, particularly when accounting for ongoing accumulation strategies that deploy fresh capital into BTC during price drawdowns.

From a market dynamics perspective, Strategy’s buying cadence appears to be outpacing the rate at which new BTC is minted by miners. March data indicated miners produced about 16,200 BTC, while Strategy added 46,233 BTC during the same period. That delta—nearly three times the newly mined supply in a single month—has fed speculation about potential supply constraints in a market that has already seen years of gradual adoption and institutional interest intensify during bullish phases. Analysts cited in coverage have noted that persistent demand from large treasuries could influence Bitcoin’s supply dynamics, particularly if the pace of adoption by corporate and high-net-worth actors remains elevated despite cyclical headwinds.

Amid these developments, Strategy’s leadership has continued to articulate a long-horizon thesis. In April, Saylor emphasized that BTC represents digital capital and suggested that the market’s drivers were shifting away from a fixed four-year cycle toward flows of capital, underpinned by traditional and digital credit channels. That framing aligns with Strategy’s approach: accumulate on weakness, maintain a long-dated exposure, and view BTC as a form of capital allocation rather than a pure price-forecasting instrument.

Positioning within the BTC treasury ecosystem and notable market contrasts

Strategy’s 766,970 BTC reserve makes it the largest publicly known BTC treasury by holdings, according to BitcoinTreasuries. The next-largest known treasury is Twenty One Capital, which holds about 43,514 BTC. This ranking underscores the outsized influence Strategy commands in the corporate-BTC landscape and helps frame the possible ceiling for what a single, well-capitalized entity can accumulate over an extended period of time.

The sector’s dynamics are further colored by other corporate actions. MARA Holdings, for example, took a different route in March by selling 15,133 BTC for roughly $1.1 billion to fund a buyback of zero-coupon convertible notes due in 2030 and 2031. The company framed the move as enhancing financial flexibility and strategic optionality as it pursues a broader business portfolio beyond mining into “digital energy and AI/HPC infrastructure.” The contrast between MARA’s opportunistic sale to optimize the balance sheet and Strategy’s continued accumulation highlights a broader spectrum of treasury management strategies within the crypto market.

What these moves mean for investors and the road ahead

For investors observing BTC’s price action and treasury activity, Strategy’s continued purchases serve as a persistent signal of institutional confidence in Bitcoin’s long-term value proposition. While the unrealized losses on Strategy’s portfolio remind readers that mark-to-market accounting can be painful in the near term, the company’s willingness to deploy capital during a bear market suggests a belief in the asset’s durability and eventual appreciation potential. The dynamic between Strategy’s accumulation pace and miners’ production—where a single entity is rapidly absorbing a chunk of new supply—could influence liquidity and the marginal cost of capital for BTC in future cycles. If capital inflows accelerate or if macro conditions alter the calculus for large holders, the market could see shifts in supply-demand balance that ripple through mining economics, on-chain activity, and price discovery.

Looking forward, readers should monitor several moving parts: the cadence of Strategy’s purchases, any new disclosures around unrealized losses and cost basis, and evolving comparisons with other large holders. The regulatory environment, as well as broader credit and liquidity conditions that shape “digital capital” flows, will also influence how these corporate treasuries navigate future cycles. As Saylor has pointed out, BTC’s value proposition as digital capital remains central to the argument for long-term accumulation, even as near-term volatility persists.

For now, the market’s focus remains on Strategy’s next move. Will the firm press ahead with additional buys in the near term, or will macro volatility temper the cadence? The answer will help gauge whether the current accumulation trend can withstand ongoing price fluctuations and what it portends for BTC’s role as a strategic asset for institutions.

Where is “The Sandlot” cast now? See its pint-sized players over 30 years later

financial freedom ala raditya dika #andryhakim #stockwise #financialfreedom #investasisaham #mindset

Man ‘drank beer and watched after starting New York building fire’ killing four

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

financial freedom ala raditya dika #andryhakim #stockwise #financialfreedom #investasisaham #mindset

MAIS UM BLOCO DE BITCOIN ENCONTRADO! Com a NerdQaxe++ #web3 #bitcoin #nerdqaxe

How Ray Dalio Predicted the 2008 and 2010 Financial Crises

-

Business7 days ago

Business7 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Politics2 days ago

Politics2 days agoUS brings back mandatory military draft registration

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Veronica Beard

-

Tech5 days ago

Tech5 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Politics4 hours ago

Politics4 hours agoWorld Cup exit makes Italy enter crisis mode

-

Sports2 days ago

Sports2 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion6 days ago

Fashion6 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Crypto World3 days ago

Crypto World3 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Fashion5 days ago

Fashion5 days agoLet’s Discuss: DEI in 2026

-

Business2 days ago

Business2 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Crypto World4 days ago

Crypto World4 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics3 days ago

Politics3 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Business2 days ago

Business2 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Business1 day ago

Business1 day agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Tech6 days ago

Tech6 days agoItalian court says Netflix must refund customers up to $576 over price hikes

-

Tech6 days ago

Tech6 days agoHaier is betting big that your next TV purchase will be one of these

-

Tech6 days ago

Tech6 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

-

Tech6 days ago

Tech6 days agoThe Xiaomi 17 Ultra has some impressive add-ons that make snapping photos really fun

-

Tech6 days ago

Tech6 days agoSamsung just gave up on its own Messages app

-

Politics3 days ago

Politics3 days agoLBC Presenter Mocks Trump Over Iran War Failures

You must be logged in to post a comment Login