Crypto World

Top Trends Followed by Crypto-Friendly Neobanks in 2026

Why does sending money internationally still feel like mailing a letter in the age of instant messaging? A wire transfer takes three days, costs $45 in fees, and loses another chunk to unfavorable exchange rates.

Freelancers struggle to access basic banking services because traditional institutions can’t process cryptocurrency income. Small businesses watch profits evaporate in currency conversion fees while waiting for payments to clear.

These are not minor obstacles; they’re symptoms of a financial system built around outdated infrastructure. Banking currently moves more slowly than the digital world requires, while cryptocurrency systems are far too unpredictable for living, day-to-day lives. This disconnect can be filled by a crypto Neo bank development company having deep expertise in blockchain technology.

Now, let’s have a look at the statistics.

| According to Mordor Intelligence, the global Neobanking market is set for strong growth, rising from USD 7.38 trillion in 2025 to USD 8.18 trillion in 2026, and further accelerating to USD 13.67 trillion by 2031, at a CAGR of 10.82%. |

Crypto-friendly Neobanks do not symbolize incremental improvement; they symbolize the rebuilding of finance from scratch. Blockchain technology and bank stability are no longer topics of the future; they are happening right now, and the year 2026 will be the year of essential digital banking trends and not experimentation.

How Decentralized Banking is Reshaping Finance

Decentralized banking is the act of removing the old gatekeepers who managed our monetary systems for centuries. The simple question being asked is, why should anyone need permission to access their own money?

- Self-Custody Meets User-Friendly Design

Modern crypto banking solutions combine blockchain’s security with interfaces that feel familiar. Users maintain ownership of assets through private keys while navigating apps that look and function like traditional banking platforms. This removes the technical barriers that held mainstream acceptance at bay during the early days of crypto.

- Smart Contracts Enable Programmable Finance

Money becomes dynamic through smart contracts. Savings accounts can automatically invest surplus funds when balances exceed thresholds. Bills pay themselves on schedule. Emergency reserves are released only under predefined conditions. White label crypto Neo bank platform development is bringing these capabilities to regional providers who lack the resources to build proprietary systems.

- Geographic Borders Become Irrelevant

A user in Lagos accesses the same crypto-friendly Neobanks available in London or Los Angeles. This matters tremendously for the 1.4 billion unbanked adults worldwide. They are the people for whom traditional finance has systematically failed. The decentralized infrastructure is location-neutral and therefore allows financial services to become global for the first time.

6 Game-Changing Trends Defining Crypto Neo Banking in 2026

The landscape of crypto banking solutions is transforming rapidly. These six emerging trends are reshaping how a crypto Neo bank development company builds platforms and how users experience digital finance.

Trend #1: Agentic Banking & AI Financial Copilots

The role of artificial intelligence in crypto banking solutions is no longer limited to mere automation. Today, intelligent agents carry out complex financial maneuvers without any assistance. For instance, they analyze every spending situation and optimize every transaction.

- Transaction Routing Optimization

AI copilots evaluate gas fees, exchange rates, and settlement times in real-time. When paying an invoice in euros, the system automatically converts cryptocurrency at the optimal moment through the most cost-effective channel. No manual intervention required.

- Proactive Financial Management

A top crypto Neo bank development company uses Artificial Intelligence to forecast cash flow problems before they happen. The tools can help track forgotten subscriptions, make suggestions on how to revise the budget based on impending expenses, and flag questionable transactions, which may be evidence of fraud.

Trend #2: Embedded Finance Ecosystems

Banking is becoming integrated into systems that are frequented by the people daily. The shift represents a fundamental change in how crypto banking solutions reach users.

- Social Platform Integration

Restaurant bills get split in group chats with automatic currency conversion. Payments are routed via these kinds of messaging apps along with social networks without any detour to banking interfaces. This makes these apps popular among many people who fear accessing banking apps.

E-commerce sites integrate the crypto-friendly Neobanks directly into their payment systems. Consumers get instant stablecoin financing, rewards on pending orders, and payment options via multiple digital currencies without the need to leave the site. Those indulged in White label crypto Neo bank platform development enable this integration without merchants becoming licensed financial institutions.

Trend #3: Cross-Border Banking & Multi-Currency Wallets

International payments are finally catching up to the internet’s borderless nature. Modern crypto banking solutions treat geography as irrelevant.

Cross-border transactions are processed within minutes, not in days. A freelancer in Vietnam invoices a Canadian client and receives payment in the preferred currency before lunch ends. The three-day wire transfer is becoming as outdated as the fax machine.

- Intelligent Currency Management

In advanced wallets, assets are held in multiple denominations at any given time, allowing them to optimize based on spending patterns as well as market conditions. This means that they avoid any need for manual rebalancing while benefiting from optimal currency exchange rates.

Trend #4: Crypto-Fiat Hybrid Accounts

The distinction between cryptocurrency and traditional money is no longer absolute. Users want unified financial management, and a seasoned crypto Neo bank development company promises to deliver it without fail.

- Consolidated Financial Views

Modern platforms show traditional, crypto, and asset tokens in a singular screen or dashboard. Money is money, and the distinction between “crypto” and “fiat” matters less than how each serves specific financial needs.

Users can specify how they want their money allocated, for example, with 70% stablecoins, 20% bitcoin, 10% traditional currency, and accounts will regularly update as values shift. Similarly, portfolio management, which is only accessible to certain high-net-worth individuals, can now be found in new crypto-friendly Neobanks.

Trend #5: Mainstream Stablecoin & Tokenized Asset Integration

Stablecoins have shifted from experimental technology to financial infrastructure in 2026.

- Yield-Generating Transaction Accounts

Checking account balances earn competitive yields through stablecoin protocols. Money waiting to pay bills generates returns instead of sitting idle at zero percent interest. This represents a fundamental shift in digital banking trends, and transactional accounts are becoming productive assets.

- Fractional Asset Ownership

Tokenization enables ownership of real estate fractions, startup shares, or artwork portions, and everything is accessible through standard banking apps. White label crypto Neo bank platform development democratizes access to asset classes that once required significant wealth to enter.

Trend #6: Quantum-Safe Security & Invisible Biometrics

Security infrastructure in crypto banking solutions is evolving faster than threats emerge.

A forward-thinking crypto Neo Bank development company can employ quantum-proof algorithms, a process that is advantageous as upgrades will be done before a quantum threat actually occurs.

- Behavioral Authentication

Continuous verification is carried out through typing rhythms, device interactions, and walking gaits. Security works transparently in the background. Passphrase tension is done away with, and illegal activity is out of the question.

Develop A Compliant Neo Bank Platform Designed For Global Financial Markets

Why Regulation Will Make or Break Crypto Banking This Year

It is expected that the level of clarity that will be achieved by regulators in 2026 will be used to separate those who are viewed as legitimate crypto-friendly Neobanks from those who do business in gray areas. The framework emerging across jurisdictions will determine which platforms thrive and which disappear.

- Compliance Becomes Competitive Advantage

Clear regulations enable partnerships between crypto banking solutions and traditional financial institutions. Banks that previously avoided cryptocurrency due to uncertainty now actively pursue white label crypto Neo bank platform development partnerships to enter markets safely.

- Navigating Fragmented Requirements

The EU’s MiCA regulation, evolving US frameworks, and diverse Asian approaches create complex compliance landscapes. Successful crypto Neo bank development companies build flexible systems that adapt to multiple regulatory regimes simultaneously, turning fragmentation from an obstacle into a moat.

- License Acquisition Drives Consolidation

Multiple banking licenses and operational permissions enable broader market access. This advantage accelerates industry consolidation as smaller players either scale rapidly or face acquisition by larger licensed operators. Regulatory compliance infrastructure becomes as valuable as technical capabilities in determining which digital banking trends gain traction.

How to Create the Ultimate Digital Bank

The development of a successful crypto-friendly Neobank in 2026 demands this balance:

Different stakeholders, like cross-border workers, cryptocurrency traders who require fiat currency access, and businesses with multiple currency systems, require separate features. Serving all of these stakeholders makes the features less effective.

- Strategic Build-vs-Buy Decisions

Building proprietary systems offers maximum customization but demands enormous resources. White label crypto Neo bank platform development provides proven infrastructure and faster market entry. A successful crypto Neo bank development company adopts hybrid approaches, customizing white label platforms for specific market segments.

Architectural decisions are to be made about multi-signature wallets, hardware security modules, verification of smart contracts, and audit trails. It is a fact that security bolted onto existing systems creates vulnerabilities that sophisticated attacks will exploit. Every element of crypto banking solutions should consider security implications from the initial design.

Infrastructure should handle 100x the initial user base without architectural changes. Digital banking trends demonstrate that successful platforms grow exponentially. The appropriate selection of blockchain networks, putting in place effective scaling solutions, and designing flexible databases determines whether platforms can leverage growth opportunities or collapse under success.

Concluding Thoughts

The financial services market is split into two segments: those who adjust to change and those who formulate new paradigms of their own. Crypto-friendly Neobanks represent the convergence of blockchain’s potential with banking’s practical necessity.

AI financial copilots, quantum-safe security, embedded finance ecosystems, and tokenized assets aren’t isolated developments. They’re interconnected components of fundamental transformation in how people interact with money. Geographic Borders, banking hours, and even gatekeepers are becoming less relevant, whereas speed, transparency, and self-serve are becoming a minimum expectation.

The development of such infrastructure requires specialized expertise in blockchain technology, regulation, security configuration, and user experience. Not many teams have such a pool of expertise within their own organization, and partnerships with experts become important for success.

Ready to Launch a Neo Bank?

Antier holds expertise in white-label crypto neo-bank platform development, enabling faster market entry without compromising security and usability. As a quality crypto neo bank development company, we have successfully implemented crypto bank solutions across multiple continents.

Recognizing the rapid pace of digital banking trends and innovations, our team helps take that pace one step forward by implementing extensive crypto banking solutions that include smart contract development and highly scalable, compliant solutions.

Let’s partner together and make banking relevant for the way we live and work today.

Frequently Asked Questions

01. Why do international wire transfers take so long and cost so much?

International wire transfers can take up to three days and incur fees of around $45, along with losses from unfavorable exchange rates, due to outdated banking infrastructure that struggles to keep pace with modern digital demands.

02. What challenges do freelancers face with traditional banking systems?

Freelancers often struggle to access basic banking services because traditional institutions typically cannot process cryptocurrency income, limiting their financial options.

03. How are crypto-friendly Neobanks changing the financial landscape?

Crypto-friendly Neobanks are revolutionizing finance by combining blockchain technology with user-friendly interfaces, allowing users to maintain ownership of their assets while benefiting from features like smart contracts for automated financial management.

At Kaiko’s Cannes conference, S&P DJI and Kaiko unveiled plans to tokenize the iBoxx U.S. Treasury index on Canton, turning it into programmable on-chain IP.

Summary

- iBoxx U.S. Treasuries is being brought natively on Canton alongside DTCC’s on-chain Treasuries to support index-linked product issuance on the same infrastructure.

- S&P will distribute the index as a smart contract token embedding full index data, IP rights, licensing terms, fees and access controls.

- The model treats index data “like a financial asset,” enabling traceability, automated fee collection and reusable, scalable licensing on-chain.

At the Agora Kaiko conference in Cannes on March 31, S&P Dow Jones Indices’ Chief Product and Operations Officer Cameron Drinkwater and Kaiko CEO Ambre Soubiran unveiled a partnership to tokenize one of S&P’s flagship fixed-income benchmarks, the iBoxx U.S. Treasury index, on the Canton network, turning the index itself into a programmable on-chain IP product rather than a simple price feed.

New Canton, Kaiko and S&P DGI partnership announced

Kaiko CEO Ambre Soubiran announced that “Kaiko and S&P DGI, we’ve been partnering now in tokenizing one of the biggest S&P benchmarks, the iBoxx index, and bringing that onto the Canton Network.” The move follows DTCC’s decision to bring U.S. Treasuries natively onto Canton (CC), which Drinkwater described as “a natural opportunity for us to bring the iBoxx Treasury index also on Canton to give product developers or counterparties a tool to use with the physical underlying also on that chain.”

Soubiran emphasized this is “not just publishing the price of the benchmark on the network.” Instead, S&P is “actually creating a smart contract token that contains all of the index data,” so that clients receive “a smart contract containing the index data but also explicitly having licensing and fees and access control all embedded into a smart contract.” She framed it as “more about a distribution play rather than a data play,” delivering the full index product on-chain.

Drinkwater said choosing iBoxx was a “total no-brainer” because with DTCC putting U.S. Treasuries on Canton, “you have the underlying” and “a very active kind of treasury institutional trade landscape on Canton” plus “real demand for the iBoxx Treasury index to be used as a underlying for product issuance on the Canton chain.”

On-chain IP and data-as-asset

For S&P, tokenizing indices as full IP products changes how licensing and economics work. Drinkwater argued that “one of the great advantages for an IP issuer like ourselves on chain is we actually have better auditability, visibility in how IP is being used, reporting on that use case and… instantaneous reporting and potentially commercial exchange based on that smart contract.” In traditional markets, he noted, S&P is “dependent on delayed reporting on volumes,” often disputed, followed by “multiple months on contract settlement,” whereas on chain “the whole timeline pulls in quite considerably” with “far less opportunity for dispute.”

Soubiran linked this to a broader shift: “the more we bring capital markets applications on chain, the more we bring data on chain, especially private and IP protected data, the more we need to treat data like a financial asset.” Blockchain infrastructure, she said, enables “traceability of data and treat data like a financial asset and trace where that data goes,” which is “great from a IP protection standpoint” and for “programmatically” managing monetization of IP in financial products.

Drawing on Kaiko’s own index business, she noted that many index fee arrangements are tied to AUM and turnover, with end-of-year reconciliations still “quite heavily manual.” Moving indices on-chain allows firms to “on chain verify what is the AUM related to the financial product that is linked to your index or your benchmark” and enable “daily fee collection based on daily turnover.” It is, she said, “not necessarily a novel product, it’s just a novel way of distributing” existing benchmarks.

Composability, evergreen contracts and Canton

Both speakers highlighted composability as a key benefit of this design. “The idea of tokenizing an index is for product issuers… to consume that index product natively on chain and wrap it into a index-linked financial product,” Soubiran explained, calling the application of composability to data products “extremely new and powerful.”

Drinkwater described the structure as layered: “you can think of the token being the index and then the smart contract being wrapped around it and that’s the use case, the use case specific terms and conditions, audit rights, etc.” That wrapper “can be tailored to whatever use case clients come to us for, but then it’s repeatedly usable. It’s evergreen. It’s on chain.” Compared with today’s model, where “clients have to come to us for every use case, it’s a new schedule on their MSA,” he said this offers “a very frictionless process of getting new product issued on chain, massively speeding up timelines,” and a “reusable infrastructure that really benefits all parties.”

On why Canton matters, Drinkwater pointed to its ability to straddle public and private workflows. On fully public chains like Ethereum, “that reporting is going to be public,” which does not fit “a lot of our use cases” such as “private exchange swaps… between institutions and they don’t want that public.” Canton’s setup, he said, lets reporting be “private when it needs to be private, public where it can be public, but back to us nonetheless,” unifying reporting across use cases in a way that “in TradFi is not the case.”

Soubiran framed the broader aim as servicing “almost a new addressable market that is your existing clients moving to an infrastructure that is programmatic and a little bit more disintermediated,” stressing that “a lot of great things exist in our current financial system,” but that the opportunity lies in “making things more automated… more programmatic in the transfer of information, the transfer of data.”

S&P’s broader digital roadmap

Drinkwater placed the Kaiko and Canton partnership within S&P’s longer digital asset strategy. He recalled that SPY “was not SPY for the first decade of its life, but it flag planted,” and said S&P understands “the power of moving first and establishing real use cases in new technology.” With a brand “known and trusted by institutions and retail alike,” S&P wants “to move first and early when we have conviction in new products and new technologies because we need our brand to be firmly planted there as an established entity.”

Over the last year, he said, S&P has “very selectively” chosen “high quality players as partners and putting IP on chain where we saw very discrete and tangible use cases,” citing the on-chain S&P 500 token with Centrifuge and the Digital Markets 50 index with Genari that bundles blockchain-exposed equities and cryptocurrencies in a structure “hard to replicate in TradFi.” Even so, he signaled he is “most excited about the innovation that we’re pushing today” with tokens wrapped in smart contracts that are “tailored to use cases, but extensible and evergreen on chain,” because this “unlocks so many use cases and scalability of our IP.”

The US Senate could soon hear testimony to confirm financier Kevin Warsh as the new chair of the Federal Reserve.

Warsh, who previously served on the Fed’s Board of Governors from 2006 to 2011, has criticized the central bank’s policies under current chair Jerome Powell. Warsh has called for “regime change” and lower interest rates.

Regarding crypto, Warsh has a somewhat nuanced approach. He hails Bitcoin as a sustainable store of value, but claims it doesn’t function as money.

Lower interest rates and a fairly open attitude toward crypto could be good news for digital asset prices, which most investors perceive as risk-on. But even if Warsh passes his nomination, there’s no guarantee he’ll affect the changes expected.

Warsh wants to lower Fed interest rates, but can he?

Warsh, a graduate of Stanford and Harvard, started his career at Morgan Stanley, where he eventually became a VP and executive director. He then served as an executive secretary of the White House National Economic Council under President George W. Bush.

Bush nominated him to the Board of Governors of the Federal Reserve in 2006, where his hawkish views on inflation often differed from his colleagues. He was critical of the aggressive use of its balance sheet, which he said led to a period of “monetary dominance” that artificially depressed rates.

Some of this appears to have changed in recent years. In a November 2025 op-ed for the Wall Street Journal, Warsh criticized Powell’s leadership at the Fed, claiming that “inflation is a choice, and the Fed’s track record under Chairman Jerome Powell is one of unwise choices.”

He said “credit on Main Street is too tight” and that the Fed’s balance sheet, which is “bloated” due to past crisis-management efforts, “can be reduced significantly.”

“That largesse can be redeployed in the form of lower interest rates to support households and small and medium-size businesses,” he said.

Plans for cutting interest rates come at an economically fraught time. The US and Israel’s joint attack on Iran, which could soon escalate into an invasion if US President Donald Trump so decides, has wreaked havoc on oil prices.

Increasing oil prices had a direct effect on the core inflation metrics the Federal Reserve uses when considering rate changes. This could put the damper on any plans for rate cuts, at least certainly under Powell.

Warsh told Barron’s that the “core theory of inflation that the Fed is using” is “mistaken.” He said that “we need to fundamentally rethink macro, which is a fundamental rethink of the core economic models that the Fed is using.”

In his accounting, rising wages and commodity prices are not to blame for inflation. Rather, “at the core, I think inflation comes about when the government spends too much and prints too much.”

Returning to monetarism, as well as dumping some of the debt held by the Federal Reserve, could help address inflation concerns, in his view.

Bankers and former Bush administration officials have congratulated Warsh on the nomination. Former US Secretary of State Condoleezza Rice said the Fed would “benefit from his steady, principled leadership.”

“He understands the central bank’s key role for the United States and our allies around the world,” she said.

Bank of England Governor Andrew Bailey has also welcomed Warsh’s nomination. He said that he knew both Powell and Warsh well, and that “They’re both very qualified.”

Qualifications aside, Warsh may find it difficult to enact his preferred policies.

Roger W. Ferguson Jr., the Steven A. Tananbaum Distinguished Fellow for International Economics at the Council on Foreign Relations (CFR), and Maximilian Hippold, a research associate for international economics at CFR, wrote that Warsh won’t revolutionize the Fed.

They said that the chair alone does not make inflation rate decisions. “They are determined by the Federal Open Market Committee (FOMC), a twelve-member body that includes seven Fed governors and five regional Fed presidents.” The chair can’t change policy without convincing a majority.

Others argue that Warsh’s interest in lowering interest rates is a recent pivot and may not be a core conviction around which he will focus central bank policy. A December 2025 analysis from Deutsche Bank noted Warsh’s response to the global financial crisis in 2008, when he was a Governor at the Fed.

“His views while he was a Governor around the GFC [global financial crisis] at times skewed more hawkish than his colleagues,” the report read. “Although Warsh has argued for lower rates recently, we do not view him as structurally dovish.”

They further questioned Warsh’s plans to lower interest rates and cut assets on the Fed balance sheet. “This trade-off would only be feasible if regulatory changes are made that lower banks’ demand for reserves. While several Fed officials have made this argument recently, including Vice Chair of Supervision Bowman and Governor Miran, it is not obvious these changes are realistic in the near-term.”

“The chair has just one vote amongst a particularly divided committee.”

Warsh’s nomination and Fed independence

Commentators have also drawn attention to Warsh’s connection to the Trump administration. Warsh’s father-in-law, Ronald Lauder, is a classmate of Trump and a major donor to his political campaigns.

His relatively recent opinions on low interest rates also make him uniquely suited to the role, at least in Trump’s eyes. Ferguson and Hippold wrote, “Trump believes he has found a successor who will align with his economic priorities in Warsh.”

The president has long bemoaned Fed officials who supposedly promise rate cuts, but then raise them once in office. “It’s too bad, sort of disloyalty, but they got to do what they think is right,” he said in a speech at Davos last year.

Trump has long pushed for lower interest rates, claiming that they are needed to spur his economic development plans. Powell’s refusal to acquiesce to the White House’s request led to political scandal.

Last year, the Department of Justice (DoJ) opened a criminal investigation into Powell, alleging that he misappropriated billions of dollars for new offices for the Federal Reserve.

A federal judge recently quashed the DoJ’s subpoenas in the case. Judge James Boasberg wrote in a memorandum opinion, “A mountain of evidence suggests that the dominant purpose is to harass Powell to pressure him to lower rates. For years, the President has publicly targeted Powell because the Fed is not delivering the low rates that Trump demands.”

Regarding his pick, Trump said in a January press event in the Oval Office that it would be “inappropriate” to ask Warsh about his stance on interest rates. “I want to keep it nice and pure, but he certainly wants to cut rates, I’ve been watching him for a long time.”

Just a couple of weeks later, in an interview with NBC, Trump said Warsh understands that he wants to lower interest rates. “But I think he wants to anyway. If he came in and said ‘I want to raise them’ […] he would not have gotten the job.”

But Warsh hasn’t “gotten the job,” at least not yet. He will face tough questioning from Democrats on the Senate Banking Committee, possibly as soon as April 13.

In a letter lambasting Warsh’s role in bailing out banks in 2008, Senator Elizabeth Warren, who serves on the committee, said, “I have no doubt that you will serve as a rubber stamp on President Trump’s Wall Street First agenda.”

Warren expected written responses to this, and to Warsh’s opinion about Trump’s “witch hunts” against Powell and Fed Governor Lisa Cook, by April 2.

Magazine: Nobody knows if quantum secure cryptography will even work

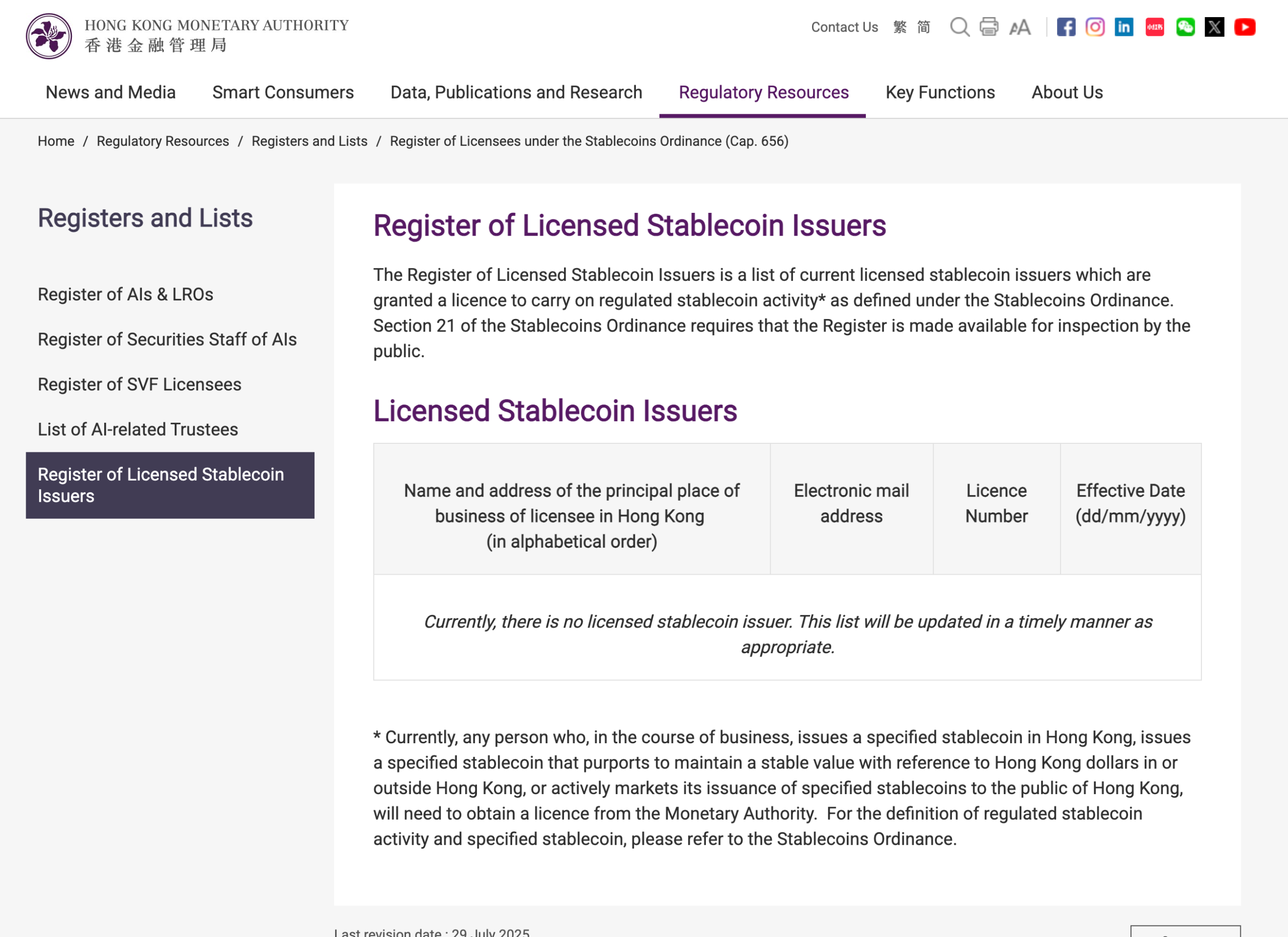

Hong Kong’s first stablecoin licences failed to materialize by the expected end of March target, with the HKMA saying only that it is still advancing the process.

Hong Kong has missed an earlier end of March target for awarding its first stablecoin licences, with the Hong Kong Monetary Authority saying only that the licensing process is advancing and decisions will be announced shortly.

A spokesperson for the Hong Kong Monetary Authority (HKMA) told Cointelegraph that the HKMA is “actively taking forward the licensing matter and will announce further details in due course,” without offering a revised timetable.

The HKMA’s public register still showed no licensed stablecoin issuers at the time of writing.

The March timetable had been set out earlier by HKMA chief executive Eddie Yue, who reportedly told lawmakers in February that only a very small number of issuers would be approved initially and that reviews were focusing on use cases, risk management, anti-money laundering controls and backing assets.

HKMA misses March stablecoin target

Earlier reports indicated that global banking giants HSBC and a Standard Chartered-backed venture were among the frontrunners to receive approvals in the initial cohort, although the HKMA did not confirm the names of any successful applicants.

Hong Kong’s caution is partly a function of how strict the regime is. Cointelegraph previously reported that the city’s stablecoin framework requires issuers to fully back tokens with high-quality liquid reserves, process redemptions within one business day and maintain a physical presence in Hong Kong, alongside broader Know Your Customer and transaction monitoring controls.

The missed deadline comes as Hong Kong places stablecoin regulation at the heart of its strategy to become a global crypto and fintech hub.

China pressure clouds Hong Kong rollout

Cointelegraph previously reported that major fintech players, including Ant International, were preparing to seek Hong Kong stablecoin licenses as the city rolled out its new regime.

Related: How Hong Kong is turning tokenized bonds into real market infrastructure

In October 2025, the FT reported that Ant Group and JD.com had paused their Hong Kong stablecoin plans after regulators in mainland China, including the People’s Bank of China and the Cyberspace Administration of China, raised concerns about privately controlled digital currencies.

Big Questions: Is China hoarding gold so yuan becomes global reserve instead of USD?

Michael Saylor’s Strategy (MSTR) looks set to restart its Bitcoin (BTC) accumulation engine after a short pause, with its STRC preferred stock likely funding fresh crypto purchases this week.

Key takeaways:

-

Strategy may purchase at least $76.25 million in Bitcoin this week.

-

Combined with a technical setup, Bitcoin may rise to $80,000 in April.

Strategy may buy at least 1,111 BTC this week

On Tuesday, STRC closed at $100.02, just above its $100 par value. Trading at or above par gives Strategy room to issue new shares, raise fresh capital and deploy the proceeds into Bitcoin.

Estimates from STRC.LIVE suggest Strategy had raised enough by Tuesday’s close to fund the purchase of more than 1,085 BTC, with the weekly total rising to over 1,111 BTC. That is equivalent to around $76.25 million.

This is a shift from the previous week, when STRC traded mostly below par and generated no estimated BTC purchases.

As of late March, the company held 762,099 BTC at an average acquisition price of about $75,694, according to its latest filings.

BTC rebounds as Strategy’s buying window reopens

The renewed buying window has coincided with a bounce in Bitcoin prices.

Since Tuesday, BTC/USD has climbed more than 5%, briefly reaching nearly $69,300. The move mirrors earlier gains seen during periods when Strategy was actively raising capital through STRC to buy Bitcoin.

One example came in the week ending March 15, when Bitcoin rose more than 10% despite weak broader risk sentiment. Over the same period, Strategy purchased 22,337 BTC worth about $1.57 billion.

The opposite dynamic emerged afterward. Bitcoin fell 14.55% over the next two weeks, roughly aligning with Strategy’s pause in purchases as STRC slipped below its $100 par value.

On March 23, Strategy unveiled a $44.1 billion capital-raising capacity to buy more Bitcoin via the sales of STRC and other preferred stocks, indicating that it would remain a meaningful source of Bitcoin demand in the coming months.

Stretch Dividend Rate maintained at 11.50% for April 2026. $STRC pic.twitter.com/8Jl0QlfNhK

— Michael Saylor (@saylor) April 1, 2026

Bitcoin eyes $80K after bouncing from flag support

From a technical standpoint, Bitcoin’s rebound began after it retested the lower boundary of its prevailing bear flag pattern as support.

BTC could advance toward the flag’s upper trendline near $80,000 in April if the recovery gains further traction, particularly if boosted by renewed Strategy buying and signs of easing Iran war tensions.

The $80,000 upside target also aligns with the 50-period exponential moving average on the three-day chart, making the area a key near-term resistance zone.

Related: Bitcoin ETFs post $1.3B in March inflows, first monthly gain of 2026

Conversely, Bitcoin risks losing the flag’s lower trendline support and confirming the pattern’s typical bearish breakdown if those supportive catalysts fade.

In that scenario, the measured downside target would come in near the $49,000–$50,000 zone. That aligns with the downside projections shared by multiple analysts in the past.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

Global asset manager Franklin Templeton is set to expand its crypto footprint by acquiring a spinoff of the crypto-native investment firm CoinFund.

Franklin Templeton said Wednesday it plans to acquire 250 Digital, a CoinFund spinoff that runs liquid crypto investment strategies, expanding the asset manager’s digital asset business. The deal will form part of a new unit called Franklin Crypto once it closes.

The move follows CoinFund’s decision earlier this year to spin out its liquid strategies business into 250 Digital as the company sharpened its focus on venture investing.

Christopher Perkins will lead the new Franklin Crypto, and Seth Ginns will serve as chief investment officer alongside Franklin Templeton digital assets veteran Tony Pecore, as the company broadens its crypto investment platform for institutional clients.

The deal will incorporate BENJI tokens, which represent ownership shares in the Franklin OnChain US Government Money Fund (FOBXX), a regulated money market fund tokenized by Franklin Templeton in 2021.

Acquisition involves all liquid strategies previously run by CoinFund

Franklin said the undisclosed transaction includes the 250 Digital investment team and all liquid cryptocurrency strategies previously run by CoinFund, and that it will also invest in those strategies as part of the agreement.

The transaction is expected to close in the second quarter of 2026, subject to the execution of definitive transaction agreements, client consents and other customary closing conditions.

Franklin Templeton’s digital asset arm manages around $1.8 billion in assets and is a major institutional player in the crypto industry, where it has been building a presence since 2018.

The company is known for being one of the first to launch a US-listed spot Bitcoin ETF alongside other major asset managers such as BlackRock in 2024.

Related: Franklin Templeton, Ondo to launch tokenized ETFs with 24/7 trading via crypto wallets

The acquisition comes during a prolonged slump in the crypto market, with Bitcoin down around 45% from its peak above $126,000 recorded in October 2025.

However, Franklin Templeton says the environment is attracting talent and creating opportunities to build long-term infrastructure.

Franklin’s head of innovation, Sandy Kaul, told The Wall Street Journal the recent market selloff helped create an opening to expand.

“This big selloff that we had in the crypto markets is creating a very unique opportunity that really made us all decide that this is the right time to pull the trigger,” Kaul said.

Ripple has added digital asset capabilities to its treasury management platform, allowing corporate finance teams to hold, track and manage cryptocurrencies and fiat balances within a single system, the company said.

According to a company announcement, the update introduces Digital Asset Accounts and a unified dashboard that aggregates balances across bank accounts, custody providers and onchain wallets, giving treasury teams real-time visibility into both cash and digital assets.

The system supports assets including XRP (XRP) and Ripple USD (RLUSD), with balances updated in real time and recorded alongside fiat transactions. APIs connect external custodians and sync activity into the platform, according to Ripple.

Ripple said the update embeds digital asset functionality directly into its treasury system, rather than requiring separate crypto platforms. The company said this could reduce reliance on manual reconciliation and fragmented reporting across banking and custody systems.

Mark Johnson, chief product officer at Ripple, told Cointelegraph the shift is about making digital assets “a core part of treasury operations,” allowing companies to manage them alongside traditional balances while enabling use cases such as stablecoin settlement and yield on idle cash.

The launch follows Ripple’s October acquisition of GTreasury for $1 billion. The company said the product is already live for customers in beta ahead of a broader rollout, with availability varying by jurisdiction depending on regulatory requirements and geography.

Related: Ripple CEO says stablecoins could be crypto’s ‘ChatGPT moment’ for businesses

Digital assets move into financial infrastructure

A survey published by Ripple in March found that 72% of more than 1,000 global finance leaders believe companies must offer digital asset solutions to remain competitive, reflecting growing focus on custody, security and infrastructure.

The findings point to a broader shift from adoption to integration, as institutions look to incorporate these assets into existing financial systems rather than manage them separately.

That transition is driving increased activity across financial infrastructure. In July, Visa expanded its settlement platform to support additional stablecoins and blockchain networks, building on its initial use of USDC (USDC) for settlement in 2021.

Banks have also begun integrating tokenized money into their operations. In November, JPMorgan expanded access to its JPM Coin deposit token, allowing institutional clients to move funds on blockchain networks for real-time settlement.

Similar efforts are emerging in credit and capital markets. In October, Securitize and BNY said they would collaborate to bring instruments such as collateralized loan obligations onchain.

Magazine: XRP yet to ‘price in’ 3 bullish catalysts, Bitcoin to $80K? Trade Secrets

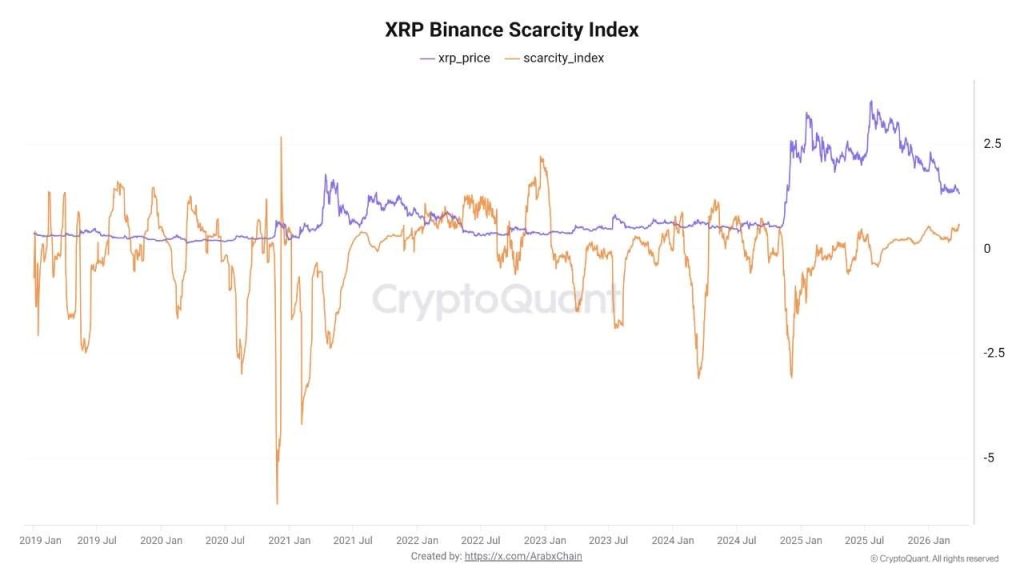

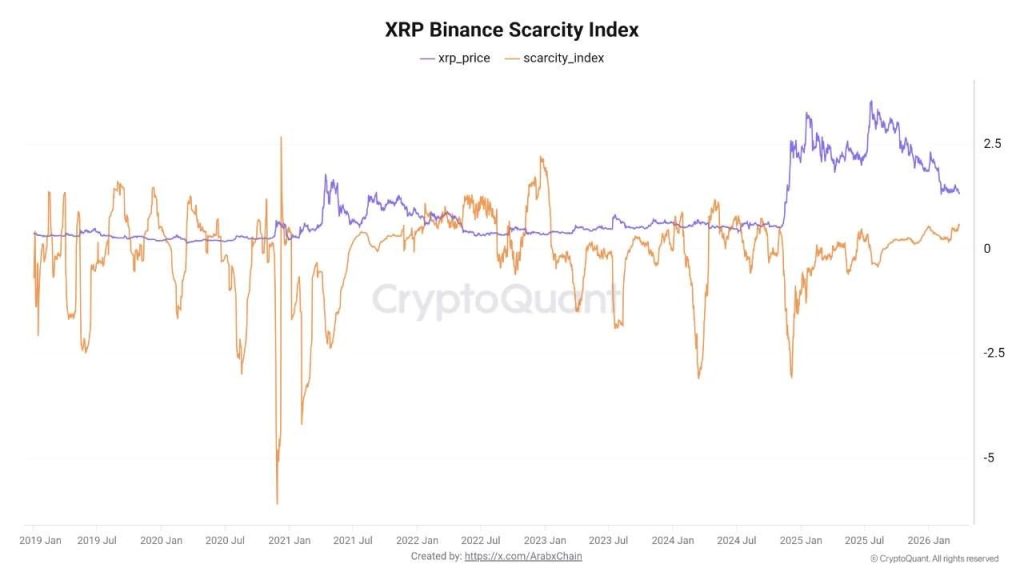

XRP crypto is trading at $1.32, and while the price chart looks fragile, the on-chain data underneath it is telling a different story.

Chain’s scarcity indicator for XRP on Binance has hit 0.59 – its highest reading since 2024 – as coins leave exchanges at a pace that is mechanically compressing the available sell-side pool.

The magnitude is not subtle. On March 10 alone, approximately $738 million worth of XRP was withdrawn from major platforms in a single 24-hour window, described by analysts as one of the most substantial single-day net outflows recorded year-to-date.

February saw 7.03 billion XRP exit centralized exchanges entirely, with Binance accounting for roughly 3.38 billion of that volume. The supply mechanics are shifting – but the price hasn’t fully priced it in yet.

Discover: The best pre-launch token sales

XRP Crypto Price Prediction: Can $1.40 Hold as Exchange Balances Drop?

XRP is pressing against the $1.40 resistance zone that analysts have flagged as the critical battleground. Below it, the $1.27–$1.30 band represents the next meaningful support cluster.

The RSI on the daily is hovering near 42 – not oversold, but not generating momentum signals either. The 50-day EMA sits just above spot price, capping intraday recovery attempts.

The on-chain divergence is the real tension here. Whale wallets accumulated approximately 40 million XRP in March even as US-listed XRP spot ETFs – now holding a combined $1.02 billion in assets – recorded $30.12 million in net outflows over the same period.

CoinShares data puts global XRP fund outflows at $130 million for the month. Institutional selling and whale buying are colliding directly at $1.40.

On the chart, $1.27 is the line that really matters, because as long as price holds above it, the accumulation story stays intact, especially with whales stepping in and ETF flows starting to stabilize, which could open the door for a push through $1.40 and a move higher if momentum follows.

But right now it is more of a tug of war, with XRP likely chopping between $1.27 and $1.40 while the market figures itself out, because you have strong accumulation on one side and lingering sell pressure on the other, and neither has fully taken control yet.

If that $1.27 level breaks clean with volume, the whole setup starts to fall apart fast and opens the door for a deeper pullback, because at that point price is no longer respecting the accumulation zone, and that always takes priority over any on chain signal.

What makes this cycle different is the institutional layer, with players like Bitwise holding massive chunks of XRP through ETF products, meaning even small outflows can hit the order book hard, while Ripple keeps building out its infrastructure in the background, which is exactly the kind of long term story bigger players tend to front run.

Explore: Best crypto assets to diversify your portfolio

The post XRP Crypto Holders Pull Coins Off Exchanges, On-Chain Data Signals Supply Shock appeared first on Cryptonews.

Pearl is Olas’s consumer gateway to a future where narrow AI agents quietly trade, curate and create prediction markets at a scale humans will never touch, says co‑founder David Minarsch.

Summary

- Olas co‑founder David Minarsch traces Pearl back to early agent work at Fetch.ai and Valory, then pivots from B2B DAO tools to a consumer app for owning AI agents.

- Pearl backs tightly scoped, long‑running agents like Polystrat, which filters Polymarket markets, applies prediction tools and has at times outperformed human traders by 2–3x.

- Minarsch sees prediction markets as economic training grounds for AI, with agents already a large share of activity and the long tail of markets increasingly served by machines, under real regulation.

David Minarsch sat down with crypto.news on March 31 on the sidelines of ETHCC to explain why Pearl’s narrow, long‑running AI agents are remaking prediction markets from the inside out.

From Fetch.ai to Pearl

Minarsch’s route into autonomous agents is textbook crypto‑AI convergence. “I got drawn into the space by my background in economics and game theory,” he told crypto.news, recalling his move into crypto after several years working on machine learning applications.

At Fetch.ai, where he spent two years, his team built one of the first agent frameworks in crypto, anchored on a simple but loaded idea: wallets controlled by machines, not humans.

“We actually wrote a detailed paper on this, which was way ahead of its time,” he adds. In 2021, he spun those lessons out into Valory, the core lab behind Olas, which has since experimented with a range of applications and go‑to‑market strategies.

The first bet was B2B: autonomous agents sold to DAOs such as CowSwap, Balancer and Ceramic. “That went okay but never sort of really took off,” Minarsch concedes. The real pivot came in 2023, when “general purpose usable large language models like ChatGPT” landed and Olas “switched more to B2C.” Pearl is the result: “a B2C application which has different agents in it,” built for users, not governance forums.

By the time Pearl launched in February 2025, the rest of the industry had caught up to Olas’s early agent thesis. “The crypto space and the AI space had moved towards agents, now everyone is building agents or using agents or both,” Minarsch says. But he argues most people’s idea of an agent is still shaped by chat interfaces like ChatGPT: “a co‑pilot synchronous experience” where you prompt and it replies, in front of you, in real time.

Olas is explicitly betting against that dominant pattern. “When you have long long‑running agents with like autonomy but tightly scoped so they can’t just do anything but they can do interesting things within a certain scope. That’s where it becomes very interesting,” he says. Pearl is designed around those tightly scoped, background processes rather than generalist assistants, Minarsch points out.

“With Pearl we intentionally go very narrow in terms of the capabilities of an agent,” he explains. He points to new tools like OpenClaw—as both validation and warning. “OpenClaw validated a lot of our core assumptions that people do want llocal first experiences with AI agents,” he says, but “the product can do too much, which causes a bunch of problems, including secruity, but also just a problem for the user.”

In his view, that kind of system is built for tinkerers “who just sort of want to mold this thing into something that’s useful to them.” The “low friction user” wants to “just press a button” and get a consistent result. “I have one and I asked it to send me daily report and half the time it’s broken,” he says of OpenClaw. “That’s not a good product experience.” Pearl’s agents, by contrast, are designed to do one thing—trading, yield seeking, market creation—reliably. Limited scope, high definition, low problem latency.

Polystrat is the cleanest demonstration of that philosophy. Polystrat is an example because here’s just the idea: provide some capital, have it trade in prediction markets,” Minarsch says. Instead of facing Polymarket’s UX—wallet setup, funding, market selection, position sizing—the user delegates funds to Polystrat and lets the agent do the work.

“Polystrat is just like a user of Polymarket,” he stresses. “If you want to use Polymarket you as a human need to set up a wallet, fund it and then you’re faced with the decision of what market to trade in. Polystrat abstracts all this and the idea is for it to simply trade on your behalf.” The agent focuses on geopolitical and political news markets, “not so short‑lived” and generally closing “within the next four to five days.”

Technically, the flow is simple but ruthless. The agent filters markets using rules like liquidity and time to close, then applies “prediction tools,” which Minarsch describes as “workflows that sit on top of models and data sources.” “There’s many different prediction tools and the agent learns over time which ones to take and which ones not to take,” depending on the market. A local pricing and sizing engine converts those predictions into positions and the system trades autonomously on your behalf.

Performance wise, Polystrat ranges between 56 and 69% accuracy, Minarsch says. As a fleet, “our agents… have performed two to three times as well as human traders,” although they are “not yet at a fleet‑wide break even.” Individual Polystrat instances, however, can deliver “up to 100% ROI overall and like several 100% ROI per individual trade.” The goal is not anecdotes but a statistical edge: “to have a Polystrat fleet on average a positive ROI.”

Trading is only half the story. As more agents enter Polymarket and its predecessors, Minarsch sees prediction markets becoming “early prototypes for these market‑driven AI systems… environments that encode truth discovery at an economic scale.”

He doesn’t pretend the rails are clean. On controversial questions—or markets with contested outcomes—information lags and disputed outcomes are common. Polystrat nor other agents on Pearl attempt to solve that. “Polystrat itself is just a trading agent on top of Polymarket,” it’s neither consensus building nor a truth serum.

But AI is already reshaping participation, creation and policing. “It’s unclear exactly how many traders in prediction markets are already AI agents but it’s probably more than 30%,” Minarsch believes. “Potentially already more than half,” he adds. As such, humans have limited attention, so “the whole long tail of prediction markets will basically be served to AI agents,” he predicts.

Crucially, Minarsch breaks from crypto libertarianism on governance. “We take the view that there should be regulation of prediction markets,” he says flatly, citing markets that “effectively look like assassination markets” or “incentivizing bad behaviors.” With “a certain degree of regulation or self‑regulation,” more markets and more AI participants should “drive prices to equilibrium” and “improve the information embedded in the markets,” opening the door to derivatives, hedging and other instruments built on top.

Asked whether Olas agents could become “data liquidity providers operating autonomously across multiple networks,” Minarsch shrugs off the distinction. “Liquidity provision is effectively also trading strategy,” he says.

In that framing, Pearl is less a single app and more an operating system for narrow, long‑running agents: Polystrat for prediction markets, Optimus for yield, Omenstrat for market creation and whatever comes next for liquidity across venues. The consistent design choice is scope: each agent does one thing, over long horizons, with as little human intervention as possible.

“We were just very early to something that a lot of people are now doing,” Minarsch says of the agent wave. The difference now is that Pearl is pushing those agents into retail‑facing products, turning prediction markets into both a playground and a proving ground for AI‑driven liquidity and truth discovery.

Elon Musk’s aerospace company SpaceX has reportedly filed confidentially for an initial public offering, moving it closer to what could be the biggest public listing in US history.

SpaceX submitted its IPO confidentially to the US Securities and Exchange Commission, according to a report from Bloomberg on Wednesday, citing people familiar with the matter. The IPO could be finalized as early as June, the sources said.

SpaceX could seek a valuation exceeding $1.75 trillion in the IPO, sources told Bloomberg in February. A valuation of that size would make the aerospace company more valuable than Meta (META), Tesla (TSLA) and Bitcoin (BTC).

SpaceX could also raise up to $75 billion from the IPO, a size that would more than double Saudi Aramco’s record $29 billion debut in 2019.

SpaceX’s potential IPO follows its acquisition of Musk’s AI startup xAI in early February, putting the company in an AI race against OpenAI, Anthropic and other private AI startups.

OpenAI, the creator of ChatGPT, closed its last funding round with $122 billion in committed capital on Tuesday, bumping its valuation to $852 billion.

IPO investors to be briefed on more details this month

SpaceX reportedly told prospective IPO investors to expect briefings from company executives later this month, Bloomberg noted.

SpaceX is weighing a dual-class share structure that would give insiders, including Musk, greater voting control.

The IPO is expected to allocate up to 30% of shares for individual investors.

Wall Street firms Bank of America, Goldman Sachs, JPMorgan Chase, Morgan Stanley and Citigroup are expected to be involved in SpaceX’s transition to a public company.

SpaceX also continues to hold 8,285 Bitcoin worth more than $565 million on its balance sheet.

However, the company shifted its Bitcoin to a new wallet address in October, prompting speculation over whether it intends to hold the cryptocurrency in the long term.

Related: OpenAI kills off AI video app Sora after 6 months

Trading platforms such as Robinhood and Kraken have been seeking to offer tokenized shares in high-profile private companies like SpaceX, OpenAI and others on the blockchain, giving retail investors a way to invest in nonpublic companies.

Robinhood CEO Vladimir Tenev said in February 2025 that investors have had limited access to these private tech firms, but that blockchain tokenization could help broaden participation.

However, OpenAI is expected to file for an IPO in 2026, and Anthropic is also exploring a public listing, which would make their shares available for trading on regular stock exchanges.

Magazine: IronClaw rivals OpenClaw, Olas launches bots for Polymarket — AI Eye

Opinion by: Francesco Mosterts, co-founder of Umia.

Crypto prides itself on being a market-driven system. Prices, incentives, and capital flows determine everything from token valuations to lending rates and blockspace demand. Markets are the industry’s primary coordination mechanism. Yet, when it comes to governance, crypto suddenly abandons markets altogether.

Recent governance disputes at major protocols have once again exposed the tensions inside DAO decision-making. Participation remains extremely low and influence is highly concentrated. A study of 50 DAOs found “a discernible pattern of low token holder engagement,” showing that a single large voter could sway 35% of outcomes and that four voters or fewer influence two-thirds of governance decisions.

This is not the decentralized future crypto originally set out to build. The early vision of the industry was to remove concentrated power and replace it with systems that distributed influence more fairly. Instead, DAO governance often leaves most tokenholders passive while a small group determines the protocol’s direction.

Token voting was crypto’s first attempt at decentralized governance. It is a broken incentive system, and it needs to change.

The promise of token governance

The original “DAO” launched in 2016 as a decentralized venture fund where token holders would vote on which projects to finance. The earliest DAOs were inspired by the idea that organizations could run purely through code.

At crypto’s conception, token voting felt intuitive. It borrowed from familiar concepts like shareholder voting, yet DAOs promised a new form of management called “decentralized governance.” Tokens would represent both ownership and decision rights, meaning anyone who held them could participate in shaping the direction of a protocol.

Related: ‘Raider’ investors are looting DAOs

Token voting was supposed to solve problems seen across many industries, including centralized control, opaque decision-making, and misalignment between teams and users. It offered a simple promise: if the community owned the token, the community would run the project. In practice, however, this miraculous solution hasn’t delivered on its promise.

The reality of why token voting fails

Token voting comes with three core problems: participation, whales, and incentives.

Participation is self-explanatory: most token holders don’t vote. With lots of material to review, particularly when many governance decisions need to be made, governance fatigue is a real problem. The result of this, which we now see every day in crypto, is that most token holders are ultimately passive and a small minority decides the outcomes.

When it comes to whales, it is obvious that large holders are dominating. It’s demoralizing for ordinary voters who feel like their opinions don’t matter, even though the original promise of DAOs was that they would have a real voice. What is the point of voting if whales have the final say?

Finally, there’s an incentive problem. Voting has no economic signal. Votes hold the same weight whether you’re informed or not. There’s no cost to being wrong and no incentive for being right. There’s nothing motivating participants to research and vote according to their beliefs.

Realistically, in current governance, voting simply expresses opinions. It does not express conviction.

The missing piece lies in pricing decisions

Crypto is fundamentally market-driven, and it works remarkably well. Markets aggregate information, price risk, and reveal conviction in ways few other systems can. The industry has built markets for practically everything, including tokens, derivatives, blockspace, and lending rates. They sit at the core of how crypto coordinates economic activity. Yet when it comes to governance, the system suddenly abandons markets entirely.

Decision markets introduce pricing into governance. Instead of merely voting on proposals, participants trade outcomes, pricing the possible decisions and backing their views with capital. This transforms governance from a system of expressed preferences into one of measurable conviction.

By tying decisions to economic incentives, participants are encouraged to research proposals and think carefully about outcomes. The result is a governance process that reflects informed expectations rather than passive opinion.

This matters now

Crypto is reaching a turning point in how it coordinates decisions. Governance conflicts, treasury disputes, and stalled proposals have exposed the limits of token voting. Even major protocols struggle to translate tokenholder input into clear, effective action. This has left governance slow, contentious, and dominated by a small group of participants.

At the same time, interest in market-based coordination is resurging across the ecosystem. Prediction markets have demonstrated how effectively markets can aggregate information, while broader discussions around mechanisms like futarchy are returning to the forefront. These systems highlight markets as powerful tools for revealing conviction and aligning incentives.

If crypto believes in markets as coordination engines, the next step is applying that same logic to governance. The next phase of crypto coordination will move beyond simply trading assets and toward pricing and executing decisions themselves.

Token voting was crypto’s first attempt at decentralized governance, and it was an important experiment. It gave tokenholders a voice, but it didn’t solve the deeper incentive problem.

Markets already power nearly every part of the crypto ecosystem. They aggregate information, reveal conviction, and align incentives at scale. Extending that same mechanism to decisions is the natural next step.

Decision markets also extend beyond governance votes into capital allocation itself. If markets can price decisions about a protocol’s direction, they can also price decisions about what to build and fund. This opens the door to a new generation of ventures built directly on crypto rails, where projects can raise capital and allocate resources through transparent, incentive-aligned mechanisms from day one. Instead of relying on passive token voting, markets can actively guide how onchain organizations form and grow.

Governance without pricing is incomplete. If crypto truly believes in markets as coordination engines, the future of onchain organizations cannot be decided by votes alone, but by markets.

Opinion by: Francesco Mosterts, co-founder of Umia.

This opinion article presents the author’s expert view, and it may not reflect the views of Cointelegraph.com. This content has undergone editorial review to ensure clarity and relevance. Cointelegraph remains committed to transparent reporting and upholding the highest standards of journalism. Readers are encouraged to conduct their own research before taking any actions related to the company.

Blackpool care home fire: Police update as two hospitalised after major incident

Constellation Brands to add Hopwtr to non-alcoholic portfolio

S&P Dow Jones Indices and Kaiko Bring iBoxx Treasury Index On-Chain via Canton Network

-

Business6 days ago

Business6 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Tech6 days ago

Tech6 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

NewsBeat5 days ago

NewsBeat5 days agoThe Story hosts event on Durham’s historic registers

-

Sports5 days ago

Sports5 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment2 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment4 days ago

Entertainment4 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World2 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech3 days ago

Tech3 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World5 hours ago

Crypto World5 hours agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Sports1 day ago

Sports1 day agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech2 days ago

Tech2 days agoEE TV is using AI to help you find something to watch

-

Tech2 days ago

Tech2 days agoApple will hide your email address from apps and websites, but not cops

-

Entertainment7 days ago

Entertainment7 days agoHBO’s Harry Potter Series Will Definitely Fail For One Big Reason, And It’s Not J.K. Rowling Or Snape

-

Tech2 days ago

Tech2 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech2 days ago

Tech2 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Fashion6 days ago

Fashion6 days agoEn Vogue in Brown Leather and Tailored Neutrals by Atelier Savoir, Styled by J Bolin

-

Politics2 days ago

Politics2 days agoShould Trump Be Scared Strait?

-

Crypto World2 days ago

Crypto World2 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Fashion5 days ago

Fashion5 days agoWeekly News Update, 3.27.26 – Corporette.com

-

Fashion6 days ago

Fashion6 days agoWhat Are Your Favorite T-Shirts for the Weekend?

You must be logged in to post a comment Login