Crypto World

Trump touts Nvidia and Tesla days after buying their shares

President Donald Trump has promoted more than 20 companies, including Nvidia, Tesla and Apple, within days of purchasing their shares, according to a CNN investigation.

Summary

- CNN linked Trump’s company promotions to stock purchases made only days earlier.

- Trump bought up to $500,000 in Nvidia shares before announcing faster AI permits.

- The findings have added pressure to include ethics rules in the CLARITY Act.

CNN found that several Truth Social posts announced or praised government actions that could benefit companies held in Trump’s investment accounts. The report has renewed questions about whether his financial interests conflict with decisions made by his administration.

Among the cases examined, CNN pointed to a 2025 post in which Trump announced that his administration would speed up the permits needed by Nvidia and similar companies to build artificial intelligence supercomputers in the United States.

Financial records reviewed by CNN showed that Trump had purchased between $200,000 and $500,000 worth of Nvidia shares several days before publishing the post. The investigation also linked the timing of his purchases to later public comments involving Tesla, Apple and other major companies.

CNN did not report evidence that Trump personally ordered the trades or made the related government decisions to raise the value of his holdings. However, the outlet reported that Trump has not placed his assets in a blind trust, leaving open the possibility that he could know what his investment managers are buying or selling.

White House denies Trump controls the trades

Responding to the report, White House spokesperson Anna Kelly said Trump does not manage the accounts involved in the transactions. According to Kelly, his assets are “held in fully discretionary accounts managed by independent third-party financial institutions.”

Trump has also previously said that professional fund managers control his investments, according to an earlier crypto.news report. His defense separates the timing of the trades from his own actions, although CNN noted that the arrangement does not meet the requirements of a blind trust.

Rep. Rosa DeLauro criticized the transactions after CNN published its findings. Writing on X, the Democratic lawmaker described the situation as: “Profits for him and his billionaire friends, higher prices for you.”

Neither the White House response cited by CNN nor Trump’s earlier comments addressed every company identified by the investigation. CNN also reported no finding that the trades broke federal securities law.

Stock scrutiny adds pressure to CLARITY talks

Questions over Trump’s stock holdings have surfaced as lawmakers debate whether the CLARITY Act should restrict senior government officials from participating in the crypto industry. According to the report, an ethics provision remains a key point of disagreement in efforts to secure bipartisan support for the market structure bill.

Trump’s 2025 annual financial disclosure has added to the dispute by showing that he received as much as $1.4 billion from crypto-related activities. Critics in Congress have cited those earnings while calling for rules that would limit the president’s ability to profit from digital assets during his term.

When previously questioned about his crypto income, Trump denied knowing the amount he had earned, according to CNN. He also argued that receiving the income would not be illegal even if he knew about it.

The stock investigation is expected to follow Trump into his meeting with senators on the CLARITY Act. Lawmakers have yet to resolve whether the bill will include conflict-of-interest restrictions covering the president and other senior officials.

Network School founder Balaji Srinivasan is seeking a memorandum of understanding with Malaysia after authorities probed his Forest City tech community over allegations it was hosting Israeli citizens using second passports.

Malaysia’s Home Affairs Ministry said Tuesday it was investigating Srinivasan’s start-up community in Johor following claims it included Israelis in violation of immigration laws. Initial checks found all 266 foreigners held valid documents.

Srinivasan said the agreement would give Network School legal certainty to continue investing in Malaysia. Without it, he said, the community could take its capital to countries that are more welcoming.

“I’d like to have a document which says not just abstractly that tech is welcome … but rather that we’re personally welcome,” Srinivasan said in a video directed at Malaysian Prime Minister Anwar Ibrahim on Thursday.

The episode highlights a tension faced by many crypto utopias, which aspire to build digital-native communities with their own institutions and economies, but still depend on conventional states for legal certainty.

Balaji, the former chief technology officer of Coinbase, launched his Network School in August 2024 in Johor’s Forest City, which is located about an hour from Singapore. It is marketed as a physical community of tech builders, creators and founders.

Srinivasan did not give the specifics of what a deal with Malaysia could include, but suggested it could be a memorandum of understanding or a modification of a special economic zone provision.

Related: Balaji calls for more ‘crypto tools’ for refugees amid Middle East tensions

“If not, then we will readily go somewhere else because I don’t want to be where we’re not welcome,” he said.

Srinivasan also announced that he is putting any further investment in Malaysia, including a $122 million plan to expand its community, on hold until it gets “sufficient assurance” that such issues don’t recur.

Instagram post led to immigration probe

Claims that the Network School was harboring Israeli citizens have been traced back to a social media post on Friday from activist group “Malaysian Protest 4 Palestine,” which accused the school of becoming a “gathering place for Israeli entrepreneurs.”

Israeli passport holders are forbidden from entering Malaysia, a Muslim-majority country, without written permission from the Malaysian Ministry of Home Affairs, as Malaysia does not recognize Israel and does not have any diplomatic relations with the country.

Magazine: Gambling on random Pokémon cards: Onchain gagcha hits record high as crypto sinks

South Korea has raised interest rates for the first time since January 2023, shifting monetary policy toward tighter conditions in one of the world’s most active retail crypto markets.

Summary

- South Korea raised rates to 2.75%, marking its first monetary policy increase since January 2023.

- Tighter borrowing conditions could cool speculative crypto demand as local trading activity has already weakened.

- Strong growth, persistent inflation and won weakness may keep additional Bank of Korea hikes possible.

The Bank of Korea raised its benchmark rate by 25 basis points from 2.50% to 2.75% on July 16. All seven members of the Monetary Policy Board supported the decision. The central bank also said further increases may be needed depending on inflation, growth and financial stability conditions.

Bank of Korea shifts toward tighter monetary policy

The rate increase was widely expected. A Reuters poll found that 36 of 37 economists expected the central bank to raise its policy rate to 2.75%.

The Bank of Korea cited stronger exports and investment, persistent inflation and risks to financial stability. June consumer inflation reached 3.2%, while the central bank expects economic growth to exceed its previous 2.6% forecast by a wide margin.

Governor Hyun Song Shin said developments in growth, inflation and financial stability all supported a rate increase. The bank also said monetary policy may need to remain on a tightening path, with future decisions depending on economic data.

Higher interest rates generally raise borrowing costs and can reduce demand for speculative assets. For crypto markets, the direct effect may depend on whether tighter local financial conditions reduce the amount of won available for trading.

South Korea remains a major retail crypto market

South Korea continues to play an important role in global cryptocurrency trading. Local exchanges such as Upbit and Bithumb regularly generate large volumes in won-denominated markets, especially for altcoins.

As previously reported by crypto.news, XRP briefly became the most traded asset on Upbit in May, recording about $110.9 million in daily volume compared with $88.6 million for Bitcoin and $67 million for Ethereum. That trading pattern showed the continued influence of Korean retail traders on individual crypto markets.

Recent listings also show that crypto exchanges continue to target Korean traders. As reported by crypto.news, Upbit added Derive’s DRV token to its KRW, BTC and USDT markets on July 14, while Bithumb also introduced a won trading pair.

Crypto demand had already weakened before the rate hike

The rate increase comes after local crypto activity had already fallen from earlier peaks. However, cryptocurrency holdings among South Korean investors dropped from about $83.3 billion in January 2025 to $41.4 billion by February 2026.

Daily trading volume across five major domestic exchanges also declined from about $11.6 billion in December 2024 to roughly $3 billion in February. Won deposits held at exchanges fell from 10.7 trillion won to 7.8 trillion won, pointing to weaker cash demand for crypto trading.

Higher rates could add another restraint on speculative activity if households choose deposits, bonds or other yield-bearing assets over cryptocurrencies. However, crypto prices also depend heavily on global monetary policy, institutional flows and broader market conditions.

Further rate hikes could keep liquidity under pressure

The Bank of Korea has left the door open to additional tightening. Reuters reported that many economists expect at least one more increase this year, potentially taking the benchmark rate to 3.00%.

For South Korea’s crypto market, the policy shift comes as local retail participation has already cooled from previous highs. Further increases could keep domestic liquidity tighter, while stronger global institutional demand may become more important in supporting broader crypto risk appetite.

Cantor and Securitize have formed a partnership to bring blockchain infrastructure directly into initial public offerings and follow-on stock sales, creating a pathway for companies to raise capital and issue securities onchain.

Summary

- Cantor and Securitize will combine capital markets expertise with regulated infrastructure for blockchain-based public offerings.

- The partnership targets IPOs and follow-on offerings while keeping issuers within existing capital market frameworks.

- Securitize previously tokenized its own NYSE shares, providing an early model for issuer-sponsored digital securities.

Under the agreement announced on July 15, Cantor will provide its equity capital markets and trading capabilities. Securitize will handle the infrastructure used to issue, distribute and service the tokenized securities. Its SEC-registered broker-dealer affiliate, Securitize Markets, will also participate in the offering and settlement process.

Partnership takes tokenization into primary markets

The collaboration differs from many existing tokenized stock products because it brings blockchain technology into the original issuance process. Companies could conduct IPOs or later share offerings using onchain infrastructure while remaining within the established framework for regulated public offerings.

The companies said the approach could modernize ownership records, distribution and settlement. Carlos Domingo, co-founder and CEO of Securitize, said “public companies shouldn’t have to choose” between traditional capital markets and blockchain infrastructure. The partnership does not yet name a company planning to use the new model or provide a date for its first offering.

Securitize builds on its own tokenized public shares

The agreement follows Securitize’s own move into public markets. The company listed on the New York Stock Exchange under the SECZ ticker on July 2 and simultaneously issued tokenized versions of its common shares on Solana and Avalanche.

Those blockchain-based shares represent the same SECZ common stock rather than a separate share class or synthetic product. Securitize had entered public markets through a business combination with Cantor Equity Partners II, a deal expected to deliver about $400 million in gross proceeds before expenses.

Wall Street expands its tokenization efforts

The Cantor partnership arrives as large financial institutions move more traditional securities onto blockchain networks. As reported by crypto.news, DTCC recently launched a tokenization initiative involving BlackRock, JPMorgan, Goldman Sachs, Vanguard and other major financial firms.

The New York Stock Exchange has also taken steps toward blockchain-based securities. As previously reported, the exchange proposed allowing eligible tokenized shares to trade alongside traditional securities while retaining the same rights, ticker and other ownership features. Securitize has separately worked with the NYSE on its planned tokenized securities platform.

Issuer-sponsored model keeps the actual security onchain

The Cantor-Securitize model centers on issuer-sponsored tokenization. Under the structure described by the companies, the blockchain token would represent the actual security rather than a wrapper, special-purpose vehicle or synthetic exposure linked to a stock.

Cantor Co-CEO and Global Head of Equities Pascal Bandelier said “tokenization is becoming part of mainstream capital markets.” The partnership now aims to apply that technology directly to capital raising rather than limiting it to funds or secondary-market trading.

Securitize has already expanded across institutional tokenization, including work with major asset managers and more than 650 funds, according to earlier crypto.news coverage. The new Cantor partnership extends that strategy into IPOs and follow-on offerings, although the companies have not yet announced the first issuer that will use the platform.

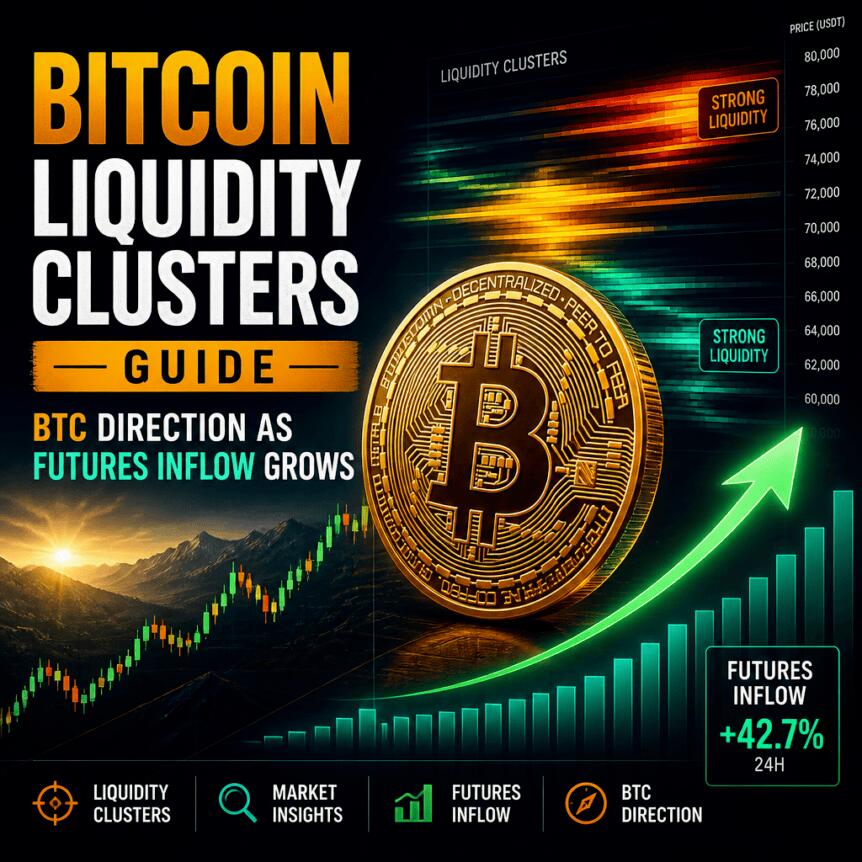

Bitcoin’s near-term direction appears increasingly tied to where leverage is concentrated in the futures market, according to liquidation heatmap readings. As BTC tests the area around the low-$60,000s—holding above $64,000 at the time of writing—price action is gravitating toward liquidity “magnets” where traders have the most to lose if the market moves.

Hyblock’s liquidation heatmap points to a key cluster of short positions between $65,500 and $66,000, positioned about 3% away from current pricing. If BTC pushes through roughly $65,600, that pocket of liquidity could be triggered, potentially helping fuel a move toward the next notable ceiling around $67,000.

Key takeaways

- A dense short-position cluster sits between $65,500 and $66,000, roughly 3% above current price, making $65,600 a potential inflection point.

- Support is layered below with a notable long-side liquidity band around $63,500 to $63,750, about 1% under current pricing.

- Deeper liquidity pools are visible at $63,000 to $63,250 and $62,500 to $62,750, which may matter if the market slips lower.

- Across the tracked window, long-side liquidity outweighs short-side liquidity by nearly 2-to-1, hinting that leverage built over the past month may not be fully unwound.

- A bearish outlier liquidation band near $55,000 stands out, suggesting that a breakdown—especially below $62,500 to $63,750—could accelerate downside.

Where liquidation clusters could pull price

Liquidation heatmaps illustrate how concentrated leverage is at specific price levels. When markets move toward those levels, forced position closings can compound the move, creating short-term momentum in either direction.

In this case, the most prominent overhead liquidity comes from shorts stacked between $65,500 and $66,000. This area sits close enough to current trading to plausibly act as a near-term target if BTC continues to grind higher. Hyblock’s data suggests that a push beyond $65,600 could put the cluster “in play,” increasing the odds of a faster run toward $67,000.

On the downside, Hyblock shows multiple long-side support zones. The closest concentration lies between $63,500 and $63,750, roughly 1% below current pricing. Additional liquidity pockets appear at $63,000 to $63,250 (about 1.5% lower) and $62,500 to $62,750 (about 2.3% lower). Together, these levels form a tiered map of where liquidations could either cushion dips—or, if breached, remove support quickly.

Importantly, the balance of liquidity is not symmetrical. Hyblock’s tracked window shows long-side liquidity outweighing short-side liquidity by nearly two to one. While that does not guarantee upside, it implies that—based on where leverage appears to sit—the market may be more prone to short-term upward pressure if BTC reaches the upper liquidity shelves first.

Rangebound trade structure backed by open interest and funding

The liquidation picture is only part of the story. The article notes that recent price behavior has leaned toward a $60,000 to $67,000 range, and that derivatives positioning metrics broadly align with a market that is not fully trending.

Two signals in particular are cited: aggregate open interest (OI) and the funding rate. Open interest had been elevated earlier, but it has since eased. Specifically, the data referenced shows OI has come down by more than 3% from a Tuesday peak, yet BTC’s price has barely moved in the same span.

At the same time, funding is described as having cooled toward neutral. Funding neutrality often corresponds with reduced directional conviction in perpetual markets; it can also mean traders are less aggressively paying for long or short exposure at that moment, even if liquidation levels remain influential.

The piece further states that spot and futures flows have been skewed toward the buy side over the past week, with spot activity and cumulative volume flows—also sourced from Hyblock—supporting the idea that dip-buying has not fully disappeared.

The $55,000 liquidation band: a risk scenario to monitor

Beyond the near-term clusters around $65,500–$66,000 and the layered support below $63,500, Hyblock’s month-long liquidation heatmap highlights a much larger bearish outlier.

A wide liquidation band near $55,000 is described as standing out more than almost anything else on the chart when using a full month lookback. The logic is straightforward: if price action weakens enough to break through key supports—particularly the $62,500 to $63,750 zone—then the market could become exposed to lower-price leverage unwinds that have been building over longer horizons.

In other words, while the most “actionable” levels may currently be close to the prevailing price, the existence of a substantial liquidity magnet farther down adds asymmetry to the downside risk. It suggests that a deeper move would not just be a continuation of the existing range—it would likely involve a regime shift where forced selling dynamics become more pronounced.

What traders should watch next

For the next decision point, focus on whether BTC can move cleanly toward $65,600 and test the short-heavy shelf between $65,500 and $66,000; doing so would be consistent with the liquidation-driven upside path toward $67,000. If instead BTC loses the nearest support bands around $63,500–$63,750 and then $62,500–$63,750, the heatmap implies that downside could accelerate toward deeper liquidity pockets, including the prominent band near $55,000.

With three weeks left on the Senate calendar, the President stopped selling crypto’s biggest bill on its merits and started selling it as a race against Beijing. The pitch is a tell, and it reveals exactly which argument Washington has already lost.

Summary

- On July 13, Trump urged the Senate to pass the CLARITY Act and framed it as a contest with China over both crypto and artificial intelligence, warning that Beijing wants total control of the sector.

- The framing arrived at a moment of maximum weakness for the bill: no floor vote scheduled, roughly three weeks of Senate calendar left, and prediction markets pricing 2026 passage far below where it sat earlier in the year.

- The bull case is that regulatory certainty is a genuine competitiveness asset, and that the CFTC chairman, a 200-company coalition, and the White House all agree the cost of delay is measured in offshore migration.

- The bear case is that the China frame is a lobbying device aimed at Democrats who are blocking the bill over ethics, not over geopolitics, and that Beijing is not competing for the market CLARITY would regulate.

- The frame cannot route around the actual obstacle: the merged draft released July 14 omits any ethics provision, and three Democratic senators immediately declared their opposition.

For most of its life, the Digital Asset Market Clarity Act has been sold on plumbing. It would decide which American regulator supervises which digital asset, split jurisdiction between the Securities and Exchange Commission and the Commodity Futures Trading Commission, and replace a decade of enforcement-by-lawsuit with written rules. That is a technocratic argument, and it is the argument that carried the bill through the House and out of the Senate Banking Committee. For readers new to the market-structure fight, crypto.news has also explained how the bill splits SEC and CFTC jurisdiction. On July 13, with the bill stalled and the calendar closing, the President changed the pitch. In a Truth Social post, Trump said the Senate should pass the CLARITY Act, warned that China and other countries would like to take complete and total control of this major financial moment as well as artificial intelligence, and closed by telling lawmakers not to let China win on either front. The plumbing argument had not worked. The new one is about national power, and the switch itself is the most informative thing that has happened to this bill in weeks.

The post that reframed the bill

The specifics of the moment matter, because the timing was not accidental. Trump opened the post by invoking Senator Lindsey Graham, the South Carolina Republican who died on July 11 at 71 following a sudden illness, and who advocacy groups had counted as a reliable supporter of the industry, including his vote for the stablecoin law CLARITY builds on in 2025. Framing passage as a tribute to a dead colleague is a legislative pressure tactic as old as Congress. Attaching it to a warning about Beijing is newer, and it tells you which audience the White House thinks it still has to move.

The administration amplified the message in unison. Patrick Witt, the White House digital-assets adviser, called the days ahead a critical week and pointed to the one-year anniversary of the GENIUS Act on July 18 as proof of what coordinated action can produce. Federal regulators joined in: CFTC Chairman Mike Selig urged lawmakers to write clear statutory standards, arguing that continued reliance on enforcement actions and statutes drafted before blockchain markets existed threatens American leadership across crypto, artificial intelligence, and financial technology. A coalition of more than 200 companies pressed Senate leadership to bring the bill to the floor. The House Financial Services digital-assets subcommittee scheduled a field hearing at Federal Hall in New York for July 17, titled around the idea that CLARITY enables innovation.

That is a full-court campaign, and campaigns of that intensity are not run from positions of strength. The bill missed the July 4 signing ceremony the White House had informally targeted. It has sat since June 1 at Calendar No. 423 on the Senate Legislative Calendar, eligible for a floor vote nobody has scheduled, with no cloture motion filed. The Senate returned July 13 with roughly three working weeks before the August recess, after which the midterm campaign consumes the political oxygen. The China frame is what a bill sounds like when its sponsors have run out of runway and are reaching for the one argument that has historically moved reluctant senators of both parties.

What Washington is actually selling against

The comparison Trump is drawing deserves scrutiny, because the two systems are not competing to do the same thing. Mainland China has banned the private crypto activities that CLARITY would regulate, including trading and mining. What Beijing has built instead is the e-CNY, a central bank digital currency issued and supervised by the People’s Bank of China, a state-run digital money that gives the central bank direct visibility into transactions. That is not a rival crypto market. It is the philosophical opposite of one.

The American model, as the administration frames it, puts privately issued dollar stablecoins at the center and keeps the state out of retail digital money entirely. This is where the CLARITY Act contains a detail that complicates the China pitch in an interesting way: the House version of the bill carries anti-CBDC provisions, barring Federal Reserve banks from offering certain products directly to individuals and prohibiting the use of a central bank digital currency for monetary policy. In other words, the bill Trump is selling as the answer to China is partly built to prevent America from ever fielding China’s actual product. The competition is not two countries racing to build the same thing faster. It is two countries betting on incompatible architectures, one state-issued and surveilled, one private and regulated.

There is a third model that goes unmentioned in the framing, and its absence is telling. Europe already passed comprehensive crypto market rules under MiCA, which means the honest competitive comparison for the United States is not with Beijing but with Brussels, a jurisdiction that did the boring legislative work first and now has the regulatory certainty American firms say they want. Naming Europe would make the argument about American legislative dysfunction. Naming China makes it about a foreign threat. The second frame is more useful politically, which is precisely why it was chosen.

The case that clarity is a competitiveness asset

Strip away the rhetoric, and there is a serious argument underneath, one that does not depend on Beijing at all. American crypto regulation has been conducted for years primarily through enforcement, with agencies applying securities statutes written in the 1930s and 1940s to assets that did not exist when those laws were drafted. Firms have responded rationally by domiciling offshore, which means the activity continues, the jurisdiction changes, and American regulators lose visibility over the very conduct they wanted to police. Selig’s point stands on its own merits: a country cannot supervise what it has pushed out of its borders.

The competitiveness case has a concrete shape. American leadership in digital finance rests on capital markets, legal certainty, developer talent, banking access, and exchange liquidity. Delayed rules weaken each of those, even while demand for the assets themselves stays strong. A framework that tells firms which regulator governs them, what disclosures they owe, and what registration path exists would let institutional capital participate at a scale that legal ambiguity currently prevents. That argument explains why more than 200 companies signed on and why the industry treats this as its top policy priority, and none of it requires believing that China is about to seize the crypto market.

The geopolitical version of the argument, at its strongest, is about the dollar. The GENIUS Act created a framework for payment stablecoins, the overwhelming majority of which are dollar-denominated, and dollar stablecoins have become an unexpectedly effective instrument of American monetary reach, putting dollar exposure in the hands of people who cannot easily access dollar banking. If digital money is where cross-border payments eventually migrate, then the country whose currency dominates that layer inherits a meaningful advantage. In that reading, the CLARITY Act is not about beating China at crypto. It is about extending the dollar’s incumbency into the next rail, which is a real strategic interest even if the invocation of Beijing is theatrical.

The case that China is a lobbying device

The skeptical reading is simpler: the frame is aimed at a domestic audience, not a foreign adversary, and it is designed to make a stalled negotiation feel like a national emergency. Nothing about China’s posture changed in July. The e-CNY has been in development for years, the trading ban is old news, and no Chinese policy shift prompted the post. What changed was the Senate calendar and the vote count. When the substance of a bill cannot close the deal, urgency becomes the substitute, and few things generate urgency in Washington faster than the suggestion that Beijing is winning.

The framing also collides with an inconvenient fact about the electorate. A survey commissioned by CoinDesk found that just 1 percent of registered voters ranked crypto as a top priority heading into the 2026 election. Senator Elizabeth Warren has made that number a centerpiece of her opposition, arguing the Senate is spending its scarce floor time on legislation written by the crypto industry for the crypto industry while voters are preoccupied with the cost of groceries, utilities, and health care. Whatever one makes of her policy views, the political arithmetic is hard to dispute: there is no constituency pressure driving this bill, which is exactly why its advocates need an external threat to manufacture stakes.

There is a further problem with the competitiveness claim as applied. If the concern is that activity migrates offshore without rules, the natural rejoinder is that America already has a stablecoin law and a functioning, if messy, enforcement regime, while the specific provisions holding CLARITY up are not the ones foreign competitors care about. Nobody in Beijing has a view on whether Coinbase may pass through yield on USDC balances, or on the precise wording of a developer liability shield. Those are domestic fights among American banks, American law enforcement, and American politicians. Wrapping them in a flag does not resolve any of them, and the senators blocking the bill are unlikely to be persuaded that their objections are unpatriotic.

The obstacle the frame cannot route around

Here is where the China pitch runs into the wall it was built to avoid. The reason CLARITY has no floor vote is not insufficient urgency about foreign competition. It is that Democrats have conditioned their support on an ethics provision restricting government officials from profiting from the industry they regulate, and the President is the reason such a provision exists. Trump’s most recent financial disclosure showed roughly $1.4 billion in crypto-related income, with about $636 million from the memecoin bearing his name and more than $500 million tied to World Liberty Financial, the DeFi venture his family co-founded. Crypto was his single largest income stream in the preceding year.

The merged Senate Banking and Agriculture draft, released on July 14, omits any ethics provision. Senators Chris Murphy, Chris Van Hollen, and Jeff Merkley responded with a press conference declaring their opposition, with Murphy arguing that there is no point building a new regulatory system for crypto if it fails to stop what he characterizes as the President’s corruption. Senator Kirsten Gillibrand has pushed to make it illegal for presidents to issue or sponsor digital assets, citing the memecoin figure directly. Warren has demanded hearings on the national-security implications of the President’s holdings before any floor vote. The White House position, articulated by Witt, is that it will accept ethics language applying across the board, from the president to the intern, but nothing aimed specifically at the President’s holdings. A proposal to let state attorneys general enforce the rules was rejected as structurally insufficient.

This is the structural bind, and it is worth stating plainly because the China frame is designed to obscure it. Democrats argue it is incoherent to build a federal framework classifying digital assets while the sitting President earns his largest income from those assets with no enforceable restriction. The White House argues it will not accept a bill that singles out the President. Both positions are internally consistent, and together they are irreconcilable without someone conceding. A Truth Social post about Beijing does not move that stalemate one inch, and the two committee Democrats who voted the bill out of Banking, Ruben Gallego and Angela Alsobrooks, have both warned their committee votes do not extend to the floor absent a deal.

The math

The vote count is where sentiment meets arithmetic, and the arithmetic is unforgiving. The bill needs 60 votes for cloture in the Senate, which requires a significant bloc of Democrats. It cleared Senate Banking 15-9, with only Gallego and Alsobrooks crossing over, and both have since qualified their support. The House passed its version 294-134 in July 2025 with dozens of Democrats, which is the precedent supporters cite, and the GENIUS Act cleared the Senate 68-30 the same year, which is the precedent they cite more often. But the Republican margin has narrowed. Graham’s death and Mitch McConnell’s continued absence leave the conference with almost no room for error.

The calendar compounds the problem. The House leaves for recess on July 23, the Senate on August 7, and Senate Majority Leader John Thune wants a floor vote before the work period ends. Advocates hoped the bill could reach the floor the week of July 20, but the procedural sequence, filing cloture, burning floor time for debate, reconciling with the House version, consumes days the bill does not have. And CLARITY is competing for that floor time against the National Defense Authorization Act, a farm bill, a housing bill, and a war-powers debate. Every hour spent elsewhere reduces the odds. Even if the Senate passes something, the House would need to approve the Senate’s version before it reached the President’s desk.

The market has noticed. Traders on Polymarket priced 2026 passage in the mid-20s to upper-30s percent range in mid-July, down from above 70 percent earlier in the year, showing how traders are pricing the bill’s odds. Galaxy Digital’s head of research cut his firm’s odds to roughly 50 percent, citing the shrinking calendar and competition for floor time. Optimists remain: the Solana Policy Institute’s president has said momentum is building and a pre-recess vote is achievable, and CFTC leadership has called the bill close. The fallback everyone whispers about is the lame-duck session after the November elections, a crowded and unpredictable window that has buried better-positioned bills than this one.

Whether the frame lands

So does the China argument work? On the merits, it is the weakest version of a strong case. The genuine argument for CLARITY is domestic and unglamorous: regulation by enforcement is a bad way to run a market, offshore migration costs American oversight, and firms deserve to know which agency governs them. That case does not need Beijing, and dressing it in geopolitics arguably cheapens it, because it invites the obvious rebuttal that China banned the thing America is trying to regulate and therefore is not racing anyone.

On the politics, the calculation is more defensible than it first appears. The frame is not aimed at Murphy or Warren, who were never going to be moved by it. It is aimed at the marginal Democrat who wants a reason to vote yes that is not about crypto, and for whom competitiveness with China offers cover that industry lobbying cannot. That is a real, if narrow, use. The problem is that the marginal Democrat’s stated price is an ethics provision, and the merged draft did not pay it. No amount of framing substitutes for the thing the votes are actually for sale for.

The most honest read is that the China pitch is a symptom rather than a strategy. It tells you the White House has exhausted the arguments it prefers and is now reaching for the one that generates urgency without requiring concession. Whether crypto gets its rulebook this year will be settled by whether someone blinks on ethics in the next three weeks, not by whether senators fear Beijing. If the bill dies, the industry will spend the fall arguing that America ceded ground to foreign competitors. The more accurate autopsy will be that the most consequential crypto bill in American history failed over a fight about one man’s memecoin income, and that no external adversary was required to stop it.

Frequently asked questions

What is the CLARITY Act?

The Digital Asset Market Clarity Act would create a federal regulatory framework for digital assets in the United States, dividing oversight between the Securities and Exchange Commission and the Commodity Futures Trading Commission. It would grant the CFTC authority over digital commodity spot markets while the SEC retains jurisdiction over investment contract assets, and it builds on the stablecoin framework created by the GENIUS Act in 2025.

What did Trump actually say about China?

In a July 13 Truth Social post, he urged the Senate to pass the bill in honor of the late Senator Lindsey Graham, warned that China and other countries want total control of the digital asset sector as well as artificial intelligence, claimed America currently leads while China competes hard, and closed by telling lawmakers not to let China win on either front.

Is China really competing with the United States on crypto?

Not in the market CLARITY would regulate. Mainland China has banned private crypto trading and mining, and has instead built the e-CNY, a state-issued central bank digital currency supervised by the People’s Bank of China. The two systems are architecturally opposed. The CLARITY Act itself contains anti-CBDC provisions, meaning the bill partly exists to prevent America from building China’s actual product.

Why is the bill stalled?

Primarily over ethics. Democrats have conditioned support on provisions restricting officials from profiting from the crypto industry, prompted by Trump’s disclosure of roughly $1.4 billion in crypto income. The merged draft released July 14 omitted any ethics language, and Senators Murphy, Van Hollen, and Merkley immediately announced opposition. Disputes over a DeFi developer shield and stablecoin yield also remain unresolved

How many votes does it need

Sixty, to clear cloture in the Senate, which requires meaningful Democratic support. The bill cleared the Senate Banking Committee 15-9 with only two Democrats crossing over, and both have said their committee votes do not guarantee floor support. Graham’s death and McConnell’s absence have narrowed the Republican margin, making Democratic buy-in more decisive than at any earlier point.

What is the deadline?

The Senate leaves for its August recess on August 7, and the House on July 23, after which the midterm campaign dominates. Advocates view the remaining weeks as the bill’s last realistic chance in 2026. A lame-duck session after the November elections is the theoretical fallback, but that window is crowded and unpredictable.

What do prediction markets say about passage

Traders have grown sharply more pessimistic. Polymarket priced 2026 passage in roughly the mid-20s to upper-30s percent range in mid-July, down from above 70 percent earlier in the year. Galaxy Digital’s research head cut his estimate to about 50 percent, citing calendar pressure. Those figures move quickly and should be checked against current markets.

What happens to crypto if the bill fails?

The status quo persists: regulation through enforcement, unresolved SEC and CFTC jurisdiction, and continued legal ambiguity that firms cite when domiciling offshore. That does not halt the industry, since demand is unaffected by legislative failure, but it delays institutional participation that depends on legal certainty and pushes the next serious attempt into a new Congress with a potentially different composition.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or legal advice. It describes pending legislation and the political debate surrounding it, and legislative outcomes are inherently uncertain. Nothing here is a recommendation to buy or sell any asset. Always do your own research. Information is accurate as of July 16, 2026, and this situation is developing quickly.

South Korean retail investors have reportedly lost about 2.15 trillion won, or roughly $1.45 billion, from leveraged trading over the past month as sharp market swings triggered widespread margin calls.

Summary

- South Korean retail investors reportedly lost $1.45 billion as leveraged positions unraveled during market volatility.

- Traders in their 20s and 30s represented 62% of accounts facing forced liquidation, reports estimate.

- Korea’s stock leverage unwind follows a retail shift from crypto into equities during the rally.

According to market reports, more than 1.2 million retail leverage accounts had reached margin-call thresholds by July 13. Estimates placed the number of accounts fully liquidated by brokerages between 320,000 and 460,000, although the broader account figures have not been independently confirmed by regulators.

Young investors bear the largest share of liquidations

Investors in their 20s and 30s reportedly accounted for 62% of accounts hit by full forced liquidations. Many retail traders had built leveraged positions during South Korea’s strong equity rally, increasing their exposure to losses when prices reversed.

The losses followed months of heavy borrowing by retail investors. Reuters reported in June that borrowed investment in South Korean equities had reached a record 60 trillion won by the end of May. Regulators were already reviewing safeguards around leveraged exchange-traded funds after acknowledging concerns about their rapid growth.

Forced sales accelerate during volatile market swings

The Korea Financial Investment Association has recorded a sharp increase in forced stock sales linked to unpaid brokerage balances. Market reports put actual forced sales from unsettled trades at 451.9 billion won between July 1 and July 13.

The pressure had already been building before July. According to Seoul Economic Daily, forced sales reached 1.12 trillion won in June, the highest monthly total of 2026. The figure rose from 707.6 billion won in May as sharp KOSPI swings repeatedly caught leveraged investors on the wrong side of the market.

When investors use short-term brokerage credit, they must provide additional funds if their positions fall below required levels. Brokers can sell the shares when clients fail to cover the shortfall, locking in losses during periods of falling prices.

Retail money had shifted from crypto into stocks

The leverage rout follows a major change in how South Korean retail investors allocated their money. As previously reported by crypto.news, crypto holdings on the country’s major exchanges fell from $83.3 billion in January 2025 to $41.4 billion by February 2026 as investors increasingly moved toward equities.

Crypto trading activity also weakened as the stock market gained momentum. A later crypto.news report found that won-based crypto trading volume fell 71% between August 2025 and May 2026, while KOSPI trading volume rose 243%.

The current equity-market losses therefore affect a retail investor base that had already moved substantial capital away from digital assets and into stocks.

Tighter financial conditions add another pressure point

The deleveraging comes as South Korea also shifts toward tighter monetary policy. The Bank of Korea raised its benchmark interest rate by 25 basis points to 2.75% on July 16, its first increase since January 2023.

Higher borrowing costs could place additional pressure on leveraged trading while making investors more cautious toward risk assets. The effect may extend beyond equities because South Korea remains an active crypto market where retail trading can influence global volumes, particularly for altcoins such as XRP. As previously reported, Korean trading activity remains an important source of liquidity for several major digital assets.

Bitget has launched a Cross-Asset Unified Account that combines cryptocurrency and tokenized U.S. equities within one margin system.

Summary

- Bitget combines 370+ eligible assets and 100 tokenized U.S. stocks within a single margin pool.

- Eligible rTokens can support trading, borrowing and margin use while preserving exposure to underlying equities.

- Reality’s rToken ecosystem has now surpassed $100 million in assets under management, according to Bitget.

The exchange said the new structure supports more than 370 eligible assets, including 100 US stock tokens known as rTokens.

According to the official Bitget announcement, users can hold eligible stock tokens while also using them as margin for futures and margin trading. They can also pledge supported rTokens as collateral to borrow stablecoins rather than selling their positions.

Bitget expands unified margin beyond crypto

Traditional exchange accounts often separate collateral across individual products and positions. Bitget’s Unified Trading Account already allowed several cryptocurrencies to contribute toward one collateral pool. The latest update extends that model to tokenized equities and other eligible real-world assets.

The initial list includes tokens linked to Apple, Amazon, Tesla, Nvidia, Microsoft, Meta, JPMorgan, Walmart, Strategy, the S&P 500 ETF and the Nasdaq-100 ETF. Bitget applies collateral discount rates of up to 95%, depending on the asset and the amount held. Borrowing rates change hourly based on market supply and demand.

Bitget CEO Gracy Chen said “the real breakthrough” comes when tokenized stocks can work with the same flexibility as crypto. She said a stock position should be able to support another trade or provide liquidity instead of remaining isolated within an account.

rTokens gain a wider role across trading products

The launch expands an earlier rollout that covered a smaller group of tokenized assets. Bitget enabled 15 tokenized stocks and ETFs as collateral for USDT-margined futures in June. The list included assets linked to Apple, Tesla, Nvidia, Microsoft, Amazon, SPY and QQQ.

The new account raises that number to 100 stock tokens and adds broader uses for the assets. Eligible rTokens can now contribute to margin requirements, support borrowing and provide exposure to their linked equities. Bitget also says holders can receive cash dividend distributions where applicable.

The company warns that using tokenized assets as collateral can increase overall account leverage. A fall in collateral value can lead to margin calls or liquidation, while borrowed funds also carry interest costs.

Reality platform supports Bitget’s tokenized stock push

The Cross-Asset Unified Account builds on Bitget’s Reality platform, which launched in May. As reported by crypto.news, Reality offers rTokens linked to publicly traded US stocks and ETFs, with Bitget saying the assets are backed 1:1 through regulated brokerage arrangements.

Bitget now says Reality-linked rTokens have passed $100 million in assets under management during their first month and generated more than $671 million in cumulative trading volume. Those figures come from the company and have not been independently verified in the announcement.

The exchange has also reported stronger liquidity across some tokenized markets. As previously reported, a Bitget and Block Scholes study found that its Nvidia-linked perpetual market reached about 75% of the liquidity depth of its Bitcoin spot market.

Exchanges push tokenized assets toward broader utility

Bitget’s latest rollout comes as crypto platforms move tokenized stocks beyond simple price exposure. The company is positioning rTokens as assets that can serve several purposes inside a single account instead of functioning only as instruments that track equity prices.

The broader trend is also extending into wallets and trading infrastructure. Bitget Wallet upgraded its trading infrastructure in June to support direct transactions involving tokenized real-world assets.

Bitget plans to add more assets to its Cross-Asset Unified Account. The launch expands its earlier collateral framework while placing tokenized stocks, crypto assets and borrowing functions inside the same capital pool.

ORANGE JUICE has raised $40 million to launch a permanent capital company that plans to acquire American businesses and build a Bitcoin treasury from their cash flow.

Summary

- ORANGE JUICE raised $40 million to acquire profitable businesses while building a long-term Bitcoin treasury.

- The company plans permanent ownership, avoiding traditional private equity fund cycles and forced portfolio exits.

- Cash flow from acquired companies may fund new deals or future Bitcoin purchases over time.

According to the company’s July 15 announcement, the Connecticut-based firm will initially target companies generating between $1 million and $10 million in annual cash flow across different industries.

Permanent capital model targets long-term ownership

ORANGE JUICE plans to permanently own the companies it acquires rather than operate under a traditional private equity structure that often requires portfolio businesses to be sold after several years. The firm said acquired companies will keep their existing identities and continue operating as separate businesses.

Founders will have the option to retire, remain involved or gradually hand over management. Sellers will also receive part of their compensation in ORANGE JUICE equity, allowing them to retain exposure to the wider company after completing a transaction.

Founding partner Nico Lechuga said “building a business takes decades,” arguing that owners should have more than one option when deciding how to transfer control. The company has not yet named its first acquisition target or disclosed how much of its $40 million raise will go directly toward Bitcoin.

Bitcoin treasury will draw from business cash flow

ORANGE JUICE said cash generated by its portfolio companies can fund further acquisitions or additions to its Bitcoin treasury. The firm plans to use leverage and capital markets conservatively as it expands.

The model links Bitcoin accumulation to operating businesses rather than depending entirely on repeated stock or debt issuance. A similar cash-flow approach has appeared elsewhere. As previously reported by crypto.news, Cardone Capital has directed rental income from selected real estate assets toward long-term Bitcoin purchases.

Ricardo Salinas, founder and chairman of Grupo Salinas, joined the raise as an anchor investor. Salinas said “cash flow is king” and backed the company’s combination of operating businesses and a Bitcoin reserve.

Jeff Booth and Lyn Alden join founding group

The company was founded by several figures linked to Bitcoin-focused venture firm ego death capital. The founding group includes Jeff Booth, Lyn Alden, Nico Lechuga and Andi Pitt, alongside Adrian Steckel. Ruben Zweiban will serve as operating partner.

ORANGE JUICE is also building an internal operating team to help acquired companies improve their businesses and adopt artificial intelligence tools. The company said operational development will remain part of its strategy alongside acquisitions and Bitcoin accumulation.

The firm also intends to pursue a public listing in the future. Management said access to public markets could provide additional capital and create liquid equity that may support future acquisitions. No timetable or planned exchange has been announced.

Bitcoin treasury models face a changing market

ORANGE JUICE enters the market as corporate Bitcoin treasury strategies face closer scrutiny following the 2026 crypto downturn. Some companies have relied heavily on securities issuance to finance Bitcoin purchases, creating ongoing obligations alongside their digital asset holdings.

As reported by crypto.news, Strategy recently sold Bitcoin after building a large system of preferred securities carrying dividend obligations. The episode showed how treasury structures that rely on external financing can face different pressures when capital markets weaken.

ORANGE JUICE is proposing a different structure built around cash-generating operating companies that it plans to own permanently. Its ability to expand the Bitcoin treasury will depend on acquisition performance, business cash flow and future capital decisions.

The company has not disclosed a Bitcoin purchase target or a timetable for its first treasury acquisition. For now, the $40 million raise provides the initial capital for its plan to combine permanent business ownership with a long-term Bitcoin strategy.

Open interest counts how many derivative positions are alive right now, not how many changed hands. It is the closest thing crypto has to a leverage gauge, and reading it alongside price tells you whether a move is built on new conviction or on people being forced out.

Summary

- Open interest is the total number of derivative contracts currently open and unsettled. It measures live positions, not activity, which is what separates it from volume.

- A trade only increases open interest when both sides are opening new positions. If either side is closing, the number stays flat or falls.

- Read alongside price, open interest tells you what kind of move you are watching: rising price with rising open interest means new money, while rising price with falling open interest usually means shorts being squeezed out.

- Open interest matters more in crypto than in traditional markets because perpetual futures dominate trading here, and the aggregate figure functions as a rough gauge of how much leverage sits in the system.

- The number has real limits. It is venue-specific, dollar-denominated figures move with price even when positions do not, and a high reading tells you leverage exists without telling you which direction it will break.

Every derivatives trader eventually runs into a number that sounds like it should be obvious and is not. Volume is easy: it counts how much traded. Price is easy: it is what people paid. Open interest is the third figure on every dashboard, quoted constantly in market commentary, and routinely misunderstood, because it measures something neither of the other two does. It counts what is still alive. Not what traded today, not what it cost, but how many bets remain open right now, waiting to be closed or liquidated. In a market where perpetual futures are the most heavily traded instrument in existence, that number is the closest thing available to a measure of how much risk is loaded into the system at any moment. This guide explains what open interest counts, how a single trade moves it, what the four price-and-open-interest combinations mean, and where the signal breaks down.

What open interest actually counts

Open interest is the total number of derivative contracts that have been opened and not yet closed, settled, or liquidated. Each contract represents an agreement between two parties, one long and one short, and it stays in the count until one of them exits. If a thousand Bitcoin perpetual contracts are open across a venue, that means a thousand live agreements are sitting there, each with someone on both sides who has money at stake.

The critical word is outstanding. Open interest is a snapshot of positions that exist at this instant, which makes it a stock measure instead of a flow measure. Your account balance is a stock. Your monthly spending is a flow. Volume is a flow: it counts trades over a period and resets. Open interest is a stock: it carries forward, rising and falling as positions are opened and closed, and it does not reset at the end of the day.

This has a consequence people miss. Open interest is not cumulative. It does not grow forever the way total historical volume does. It can rise for weeks as traders pile into a trend and then collapse in an hour when a price move liquidates thousands of positions at once. Watching it fall by a third in a single session tells you something important happened, and that something is almost always forced.

Open interest gets quoted two ways, and the difference matters. Some venues report it in contracts, meaning a raw count of units. Others report it in notional dollars, meaning the count multiplied by the current price of the underlying asset. The second version is more intuitive and more misleading, for reasons covered later.

Open interest versus volume

The cleanest way to separate the two is to notice that they answer different questions.

Volume asks how busy the market was. Open interest asks how much of that activity left something behind.

Picture a market where two traders spend all day passing the same contract back and forth. Each transfer adds to volume. By the close, volume looks enormous. But no new positions were created, because each trade had one party opening and one party closing. Open interest never moved. Enormous volume, unchanged open interest, and nothing about the market’s underlying risk changed at all.

Now picture the opposite. Ten new traders open long positions and ten new traders take the other side. That is a modest amount of volume and a direct increase in open interest of ten contracts. Small activity, real change in exposure.

Real markets mix both constantly, which is why the two figures move independently and why reading them together is more informative than reading either alone. High volume with flat open interest describes churn: the same positions rotating between hands, common during choppy sideways action. High volume with sharply rising open interest describes new participation: fresh capital committing to a view. High volume with sharply falling open interest describes an exit: people closing, willingly or otherwise, and that last case is what a liquidation cascade looks like on a chart.

How one trade moves the number

The mechanics reward a worked example, because the rule is not intuitive until you see it.

Every derivatives trade has a buyer and a seller. Each of them is doing one of two things: opening a new position, or closing one they already had. That gives four combinations, and the combination determines what happens to open interest.

Start with a market where open interest is 100 contracts.

Case one: both sides open. Alice wants to go long and has no position. Bob wants to go short and has no position. They trade one contract with each other. A new agreement now exists that did not exist before. Open interest rises to 101. Volume for the session records one contract.

Case two: both sides close. Alice already holds a long and wants out. Bob already holds a short and wants out. They trade with each other, and both positions are extinguished at once. The agreement is gone. Open interest falls to 99. Volume still records one contract.

Case three: one opens, one closes. Alice holds a long and wants out. Carol has no position and wants to go long. Carol takes Alice’s position over. The contract still exists; only the name on one side changed. Open interest stays at 100. Volume records one contract.

Case four: the mirror of case three. A short holder exits and a new short takes their place. Same result. Open interest unchanged at 100.

Notice that volume recorded one contract in every case while open interest did three different things. That is the whole distinction in a single table. Volume counts the transaction; open interest counts whether the transaction created or destroyed a live position. And notice that open interest only ever rises when both parties are new to the trade, which means an increase always signals fresh capital entering, never rotation.

One more detail that trips people up: open interest counts contracts, not participants, and it counts each contract once, not twice. A single agreement between one long and one short is one unit of open interest, not two. The long side and the short side of the market are always exactly equal in size, because every contract has both. Anyone claiming that open interest shows more longs than shorts has misunderstood the instrument. What they mean is that positioning or funding leans one way, which is a different measurement entirely.

Reading price and open interest together

On its own, open interest is close to meaningless. A reading of $20 billion tells you nothing without knowing whether it was $10 billion or $30 billion yesterday, and what price did in the meantime. Paired with price direction, it produces four readings that traders use constantly.

Price up, open interest up. New money is opening positions into strength. Fresh longs are entering and someone is willing to take the short side. This is the combination most often read as a healthy trend, because the move is supported by new commitment instead of by people unwinding. It also means leverage is accumulating, which is the setup for a violent reversal later.

Price up, open interest down. Positions are closing while price rises. The usual explanation is short covering: traders who were short are buying to exit, which pushes price up while destroying open interest. The move is real, but it is powered by people leaving instead of by people arriving, and it tends to exhaust when the shorts are done. Rallies with falling open interest have a reputation for disappointing.

Price down, open interest up. New positions are opening into weakness, typically new shorts. Fresh bearish conviction is entering the market. Like the first case, this builds leverage, and a crowded short book is exactly what a squeeze needs.

Price down, open interest down. Positions are closing as price falls. This is the signature of long liquidation: leveraged longs being forced or choosing out, which removes both the position and the price support. In its extreme form it is capitulation, and it is why the sharpest drops often come with the largest single-session collapses in open interest.

Treat these as vocabulary instead of as prophecy. They describe what has already happened in a way price alone cannot. They do not predict the next move, and every one of the four has failed plenty of times.

Why the number matters more in crypto

Open interest exists in every derivatives market. Wheat futures have open interest. It matters differently in crypto for structural reasons.

The first is dominance. In equities, derivatives sit alongside a far larger spot market. In crypto, perpetual futures are the single most heavily traded product in the entire asset class, and perp volume reached roughly $61.8 trillion in 2025 according to CryptoQuant data, up about 29% year on year. Offshore perpetual volume alone grew from around $28 trillion in 2023 to more than $90 trillion in 2025. When the derivative dwarfs the underlying, the derivative’s positioning drives the spot price instead of reflecting it, and open interest is the measure of that positioning.

The second is leverage. Perps offer leverage multiples that traditional venues do not permit, and because they never expire, positions can accumulate indefinitely. There is no quarterly settlement forcing a reset. Open interest can therefore build for months, which means the aggregate figure functions as a rough gauge of how much borrowed exposure is stacked in the system waiting for a catalyst.

The third is the liquidation engine. Because positions are leveraged and margined, a price move against a crowded book does not produce a gentle unwind. It produces automatic, forced closure, which pushes price further, which forces more closure. The October 10, 2025 event, in which roughly $19 billion of positions were liquidated across the market in a single episode, is the reference case. Elevated open interest is the fuel for that. It does not tell you when the match gets struck, but it tells you how much is stacked.

The fourth is that crypto has finally started measuring it onshore. Perps have moved from offshore venues into regulated American markets, with Coinbase cleared for perpetual futures and the CME suing the CFTC over whether a perp is legally a swap. As the product comes onshore, open interest data becomes more reliable and more consequential, because regulated venues report it consistently.

Where to find it and how it is measured

Every derivatives venue publishes its own open interest. Aggregators such as CoinGlass combine figures across exchanges to produce a market-wide number, which is the version quoted in most commentary.

Three practical measurement issues are worth carrying with you.

Aggregation is imperfect. Venues report differently, some in contracts and some in notional, some including inverse contracts and some not. Adding them produces an estimate, not a census. Different aggregators publish different totals for the same moment, and the discrepancy is normal.

Dollar-denominated open interest moves with price. This is the most common misreading in circulation. If open interest is quoted in notional dollars and the price of the asset rises 10% while every position stays exactly as it was, the dollar figure rises 10%. Nothing changed. No new positions opened. The number went up because the multiplier went up. Anyone pointing at rising dollar open interest during a rally as proof of new participation may be describing arithmetic. Contract-denominated open interest, or the ratio of open interest to market capitalization, avoids the trap.

The ratio is often more useful than the level. Open interest divided by market capitalization gives a crude but real sense of how leveraged an asset is relative to its size. A token with open interest approaching a large fraction of its market cap is carrying leverage that a token with a tiny ratio is not, and the first will move far more violently on the same news.

A worked reading of a real cascade

Abstract rules are easier to hold when attached to a sequence, so walk through the shape of a leverage unwind as open interest describes it.

Phase one is the build. Price grinds higher over several weeks. Open interest climbs steadily alongside it, in contract terms and not merely in dollars, which tells you positions are actually being added instead of the multiplier rising. Funding turns positive and stays there, meaning longs are paying shorts to hold the trade, which is the market charging rent for a crowded direction. Nothing is wrong yet. This is what a trend looks like. But each new contract is a position with a liquidation price attached, and those prices cluster, because leverage settings and entry points cluster. The book is getting heavier and the heaviness is concentrated in bands.

Phase two is the stall. Price stops advancing but open interest does not fall. This is the tell worth learning. Traders who entered late are underwater on funding and unwilling to close, so exposure stays on the books while the reason for holding it weakens. Open interest at a high level with price going sideways describes a market where a lot of people are waiting to be proven right, and the longer it persists the more of them are paying to wait.

Phase three is the trigger, and it is usually mundane. A macro print, an exchange outage, a large spot sale. Price drops into the first cluster of liquidation levels. Those positions close automatically, and automatic closure means market sell orders hitting a book that has just widened. That pushes price into the next cluster.

Phase four is the cascade, and this is where open interest earns its reputation. The number does not drift down. It falls off a cliff, because thousands of positions are being extinguished in minutes. Volume spikes to extraordinary levels at the same moment. High volume plus collapsing open interest plus falling price is the unambiguous signature of forced exit, and it is the one combination that admits almost no alternative reading. The October 10, 2025 episode, roughly $19 billion liquidated, is the canonical version.

Phase five is the aftermath, and it is the most useful part for anyone still holding. Open interest is now far lower than it was. The leverage that fueled the drop has been removed from the system, which is why sharp liquidation events are frequently followed by calmer trading: the fuel burned. A market with low open interest after a cascade is structurally different from the same price level reached with high open interest intact, because the second one still has a loaded book underneath it and the first does not. Same price, completely different risk.

Notice what open interest did and did not do across those five phases. It described the build accurately. It flagged the stall, which price alone did not. It confirmed the cascade in real time. It told you afterward that the leverage was gone. What it never did, at any point, was tell you when phase three would arrive or which direction it would run. That is the honest scorecard: a superb descriptive instrument and a poor predictive one, which is worth far more than the reverse if you know which you are holding.

The limits of the signal

Open interest deserves the attention it gets and considerably less certainty than it receives. Its limits are structural, and knowing them separates using the number from being used by it.

It is directionless. High open interest tells you leverage is present. It does not tell you which way that leverage breaks. A crowded book can unwind up or down, and the same reading precedes both. Commentary that treats elevated open interest as inherently bearish, or as inherently a sign of a healthy trend, is adding a conclusion the data does not contain.

It says nothing about position size distribution. Ten thousand contracts might be one enormous institutional hedge or ten thousand retail gamblers at maximum leverage. Those two books behave completely differently under stress: the hedge sits still, the gamblers cascade. Open interest cannot distinguish them.

It ignores what the positions are for. A short is not necessarily a bearish bet. Market makers run shorts as inventory hedges. Basis traders hold spot and short the perp to harvest the spread, with no directional view whatsoever. Miners hedge forward production. A meaningful share of any open interest figure is not speculation at all, and treating the whole number as a sentiment gauge misreads it.

It is venue-fragmented. Open interest on one exchange can rise while it falls on another as positioning migrates, which looks like a signal and is a transfer. Only the aggregate captures the system, and the aggregate is an estimate.

And it lags the thing you actually want. By the time open interest confirms a trend, the trend has been running. By the time it collapses, the liquidation already happened. Open interest is excellent at describing what occurred and poor at telling you what comes next, which is true of most indicators and rarely admitted about this one.

Used properly, it is a context tool. It answers a specific question well: is this price move backed by people arriving or by people leaving? That question is worth answering, and no other single number answers it. Just do not ask it to do more.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or trading advice. Derivatives carry substantial risk of loss, and leveraged positions can be liquidated rapidly, in some cases exceeding the margin posted. Nothing here is a recommendation to trade any instrument. Always do your own research. Figures are accurate as of July 16, 2026.

Frequently Asked Questions

What is open interest in crypto?

Open interest is the total number of derivative contracts, most often perpetual futures, that are currently open and have not been closed, settled, or liquidated. It measures live positions at a point in time instead of trading activity over a period. Each contract counts once and always has a long and a short on opposite sides, so the two sides of the market are always equal in size.

What is the difference between open interest and volume?

Volume counts how many contracts traded during a period and resets each session. Open interest counts how many positions are still alive and carries forward. A market can post huge volume with no change in open interest if traders are simply passing existing positions between each other. Volume measures activity; open interest measures accumulated exposure.

Does rising open interest mean price will go up?

No. Open interest is directionless. It tells you that new positions are being opened, not which way they will resolve. Rising open interest alongside rising price suggests new money entering a trend. Rising open interest alongside falling price suggests new shorts. The same reading precedes both rallies and crashes, and treating it as a directional forecast misreads what it measures.

What does falling open interest mean?

Positions are being closed, either voluntarily or through liquidation. Falling open interest with falling price is the signature of long liquidation and, in extreme form, capitulation. Falling open interest with rising price usually indicates short covering, where traders buy to exit shorts. Either way, the move is powered by participants leaving instead of arriving, which tends to limit how far it runs.

Why does open interest matter more in crypto?

Because perpetual futures dominate crypto trading to a degree unmatched in other asset classes, with perp volume around $61.8 trillion in 2025, and because perps never expire, so leveraged positions accumulate indefinitely with no settlement date forcing a reset. The aggregate figure therefore works as a rough gauge of how much leverage sits in the system, which is the fuel for liquidation cascades.

Can open interest be higher than the spot market?

Yes, and in crypto it frequently is for individual assets. Derivatives positioning can exceed the size of the underlying market, which is one reason perps often lead spot price instead of following it. The ratio of open interest to market capitalization is a useful gauge here: a high ratio indicates an asset carrying leverage disproportionate to its size, which typically means more violent moves.

Where can I check crypto open interest?

Individual exchanges publish their own figures, and aggregators such as CoinGlass combine them into market-wide estimates. Treat aggregates as approximations, since venues report on different conventions and different aggregators disagree. Check whether the figure is quoted in contracts or in notional dollars, and check the timestamp, because open interest can change dramatically within hours.

Why does dollar open interest rise when price rises?

Because notional open interest is the contract count multiplied by the current price. If price rises 10% and not a single new position opens, the dollar figure still rises roughly 10%. This is arithmetic, not participation, and it is the most common misreading of the metric. To see whether positions are actually being added, look at contract-denominated open interest or the open-interest-to-market-cap ratio.

Zama says a lending vault that accepts only confidential USDC has grown into one of the largest USDC vaults on Morpho’s Ethereum deployment, weeks after opening to depositors.

Summary

- Zama says confidential USDC deposits reached $23.23 million, ranking eighth among Ethereum Morpho USDC vaults.

- The vault lets users earn DeFi yield while keeping individual balances and deposit positions encrypted.

- Morpho’s growing institutional use shows privacy tools are entering established onchain lending infrastructure at scale.

According to a July 16 post from Zama, the Steakhouse Confidential Prime USDC vault held $23.23 million at Ethereum block 25,544,806. The company said that placed it eighth by total deposits among Morpho V1 and V2 USDC vaults on Ethereum. The ranking and deposit figure reflect Zama’s stated snapshot and can change as users deposit or withdraw funds.

Confidential USDC moves into established DeFi infrastructure

The Steakhouse Confidential Prime USDC vault opened on June 23. Steakhouse Financial curates the strategy, Morpho provides the lending infrastructure, and Zama supplies the confidentiality technology.

Users deposit confidential USDC, or cUSDC, rather than standard USDC. Zama uses Fully Homomorphic Encryption to keep individual balances and transaction amounts encrypted while allowing the assets to interact with applications on Ethereum. Deposits ultimately enter a strategy using Morpho lending markets backed by collateral including cbBTC, WBTC and wstETH.

Zama points to $23.23M TVL as a demand signal

Zama described the vault’s growth as evidence that users are willing to place capital into confidential financial infrastructure. The company said “capital is ready to flow through confidential rails,” while acknowledging that an ongoing incentive program has also helped attract deposits.

The vault launched with a 12-week reward program on top of the yield generated by its underlying Morpho strategy. Zama said the native strategy was producing about 4% when the product launched, while additional incentives rewarded early depositors. The company had reported more than $14 million deposited by July 2, before the total reached the $23.23 million figure reported on July 16.

Morpho attracts more institutional-style vault products