Crypto World

UK Delays Capital Gains Tax Rules for Some Crypto Using “No Gain, No Loss”

The UK tax authority has announced plans to change how cryptocurrency lending and liquidity pool arrangements are taxed, moving toward a “no gain, no loss” treatment for certain disposals. The policy is designed to defer capital gains tax until a participant makes what HM Revenue & Customs (HMRC) calls an “economic disposal.”

In a notice released on Monday, HMRC said the approach would apply starting April 6, 2027. The move is aimed at aligning tax outcomes with the underlying economics of crypto lending and decentralized liquidity arrangements, where investors may not realize a profit in the usual sense until they dispose of their crypto exposure.

Key takeaways

- HMRC plans to apply a “no gain, no loss” approach to certain disposals tied to crypto loans and liquidity pools from April 6, 2027.

- The change is intended to defer capital gains tax on digital assets until an “economic disposal,” rather than taxing interim events.

- HMRC expects the update to affect around 700,000 individuals and trustees.

- The policy contrasts with earlier HMRC guidance for crypto lending and liquidity pools issued in 2022 after consultation.

- UK capital gains tax rates for 2025–2026 remain in the 18% to 24% range depending on the taxpayer’s rate band, but the timing of when gains are recognized would shift for covered arrangements.

What HMRC is changing for crypto loans and liquidity pools

HMRC’s announcement focuses on “certain disposals” related to cryptocurrency lending and liquidity pool participation. Under the new approach, HMRC says it will treat covered transactions under UK capital gains rules as “no gain, no loss” for situations including acquisition and disposal of an interest in a lending arrangement in exchange for the same type of asset.

The tax authority also indicated that its treatment would extend to cases involving borrowed assets acquired at market value, as well as arrangements operating under similar conditions using automated market makers.

Why “no gain, no loss” is meant to defer tax

HMRC’s stated rationale is that taxing these activities immediately could produce results that do not reflect when economic benefit is actually realized. The authority said the measure supports fairness in the UK tax system and “aligns the tax treatment more closely with the economics of these arrangements” by recognizing gains and losses “only when the participant makes an economic disposal of the cryptoassets.”

In practical terms, the policy is aimed at reducing instances where taxpayers might face capital gains tax consequences from events that are not, from an investor’s perspective, a final exit from their economic position.

Industry feedback and the move away from older guidance

HMRC described the change as significant and connected it to a broader consultation period that followed the authority’s 2022 guidance on crypto liquidity pools and lending. The notice indicates that the update is expected to affect roughly 700,000 people and trustees.

While the precise boundaries of HMRC’s “certain disposals” will matter to taxpayers planning their activities, HMRC’s direction is clear: it intends to reduce administrative pressure on taxpayers by adopting an approach that better matches how crypto lending and liquidity participation are commonly structured.

Aave founder and CEO Stani Kulechov said in an X post on Monday that “This is the right direction,” adding that industry feedback suggested alternative approaches would create “significant admin burden for the tax payer.”

Tax rates remain, but the timing could change

UK rules for 2025–2026 set capital gains tax rates for crypto at between 18% and 24%, depending on whether the taxpayer falls within the basic-rate or higher-rate band, according to UK income tax rate guidance. HMRC’s announcement does not change these headline rates.

Instead, the key difference is when gains and losses would be recognized for covered lending and liquidity pool transactions. By deferring capital gains tax until an “economic disposal,” HMRC is effectively shifting attention from intermediate events within an arrangement to the point at which the taxpayer’s exposure is actually disposed of.

For investors, traders, and liquidity providers, this can matter as much as the headline tax percentage: timing can affect cashflow, how gains line up with other income, and how accurately tax reporting corresponds to realized outcomes.

Separately: a Solana community leader files to run in UK by-election

While HMRC’s announcement reshapes crypto taxation policy, UK politics is also seeing a crypto-adjacent candidate enter the spotlight. Reform leader Nigel Farage will face challengers in a by-election in Clacton following his resignation last week, after reports tied him to donations connected to the crypto industry.

On Tuesday, Stephen Newnham, described as the leader of the Solana community group Superteam UK, said he will run as an independent candidate against Farage and others. The by-election is scheduled for Aug. 13 and, according to reporting that includes non-traditional candidates, will also include comedian and author Jon Harvey in costume as Count Binface.

Farage’s resignation triggered the by-election, and the political narrative around his campaign includes allegations and reporting about financial contributions. Earlier coverage cited a $6.7 million donation connected to crypto billionaire Christopher Harborne, which Farage described at different times as both a “reward” related to the UK’s exit from the European Union and later as a “gift,” and also referenced other assistance linked to George Cottrell, described in that coverage as a convicted fraudster associated with a crypto casino.

For crypto participants in the UK, the next watch points are how HMRC will define and operationalize “certain disposals” and what it will consider an “economic disposal” in practice. With the new framework set to begin in April 2027, taxpayers and platforms alike should prepare for reporting changes and monitor further guidance that turns today’s principle into day-to-day compliance.

South Korea has unveiled plans for a new law that will bring cryptocurrencies and other digital assets into the country’s state asset management framework, expanding rules that have remained largely unchanged for more than seven decades.

Summary

- South Korea plans a new law that will bring cryptocurrencies and other digital assets into the country’s state asset management framework.

- The proposal expands government asset rules beyond real estate to include virtual assets and intellectual property.

- The move comes as South Korea continues work on digital asset legislation, stablecoin rules, and blockchain infrastructure projects.

South Korea’s Ministry of Economy and Finance said during a July 15 policy briefing at the President’s Blue House that it will introduce the National Asset Basic Act, replacing an approach built around the existing State Property Act enacted in 1950.

The ministry said the current law was designed for an economy where government assets were largely limited to real estate. The proposed framework will instead cover newer categories, including intellectual property and virtual assets, while introducing specialized management and development standards for different types of state-owned assets.

Under the proposal, authorities plan to move away from treating public assets mainly as property to preserve, sell, or develop. Instead, the ministry said the new framework will focus on creating more value from government-owned assets through modern management practices.

Crypto legislation remains part of wider blockchain strategy

The latest proposal follows another digital asset policy update released earlier this week. After Monday’s State Council meeting, the Ministry of Economy and Finance confirmed that blockchain development will remain part of South Korea’s economic growth strategy for the second half of 2026, even as artificial intelligence receives a larger share of government investment.

As part of that roadmap, the ministry said it will continue work on the Digital Asset Basic Act, legislation intended to establish rules for the country’s digital asset industry, including business conduct standards and a legal framework for Korean won-pegged stablecoins. Authorities also said they plan to create legal foundations for cross-border stablecoin transactions and support amendments that would allow spot cryptocurrency exchange-traded funds.

Plans for blockchain infrastructure also continue to expand. The ministry previously announced that a pilot program linking tokenized government bonds with an institutional central bank digital currency project will begin in 2027, while the Bank of Korea will study how its CBDC can interact with other blockchain networks.

At the provincial level, Gyeonggi Province is preparing to launch an eight-month blockchain stablecoin pilot in August.

According to blockchain media outlet NexBlock, blockchain security company ZKrypto will lead the trial, which will test stablecoin issuance, circulation, settlement, fraud prevention, privacy protections, and public benefit payments through February 2027. The system will use zero-knowledge proofs to prevent double-spending and proof-of-reserves technology to verify backing assets throughout the pilot.

Coinbase spent 2025 losing an argument about what it was. Trading volumes softened, the stock fell from $419.78 in July to the mid-$160s, and the market delivered its verdict on a company whose revenue still rose and fell with bitcoin: a leveraged bet on crypto activity, priced accordingly. Then in December it launched four new businesses at once, including one nobody had asked it for.

Summary

- Coinbase prediction markets reached $100 million in annualized revenue in under two months.

- The product’s early growth reflects Coinbase’s distribution advantage through existing funded accounts.

- Most prediction market volume is tied to sports, complicating the category’s information-market framing.

- State regulators are challenging sports-related event contracts as illegal gambling.

- The real test is whether volume holds after the World Cup and legal challenges progress.

By the first quarter of 2026, that one had passed $100 million in annualized revenue in under two months. Coinbase called prediction markets one of the fastest scaling products in its history, which is a striking claim from a company that once onboarded a country’s worth of retail traders in a single bull run. It sits in the same quarterly report as a $394.1 million net loss and revenue down to $1.43 billion from $2.03 billion a year earlier.

That juxtaposition is the whole story. Coinbase’s fastest growing product is not crypto. It is an event contract business that mostly trades sports, launched into a category that Kalshi and Polymarket have already scaled to volumes exceeding America’s legal sportsbooks, and that attorneys general in at least four states are currently arguing is illegal gambling.

What the $100 million number actually measures

Precision first, because the figure is doing rhetorical work that deserves inspection.The metric is annualized revenue, meaning a run rate extrapolated from a short period, not $100 million collected. The window was less than two months from a December 2025 launch. Coinbase disclosed the figure in its first quarter 2026 shareholder materials alongside the claim that retail derivatives annualized revenue exceeded $200 million and that derivatives volume over the trailing twelve months had grown 169% year over year. Every one of those numbers is a rate, and rates from launch windows measure enthusiasm as much as they measure business.

Against Coinbase’s own scale, $100 million annualized is roughly 7% of a single quarter’s total revenue projected across a year. It is not, on its own, a company changing number. What makes it interesting is the derivative: how fast the line rose, from zero, in a category the company entered late, against two incumbents with years of liquidity advantage. Growth that steep from a standing start is either a real demand signal or a launch spike with a decay curve, and the two look identical for exactly one quarter.

The context that makes the bullish reading credible is the sector data. Combined monthly trading volume across Kalshi and Polymarket rose from under $5 billion in September 2025 to roughly $24 billion by April 2026, according to a Pew Research analysis of figures from The Block. For scale, legal American sportsbooks handled around $14 billion a month on average across 2025. Prediction markets, a category that spent a decade as an academic curiosity and a regulatory orphan, now move more money monthly than the entire regulated sports betting industry that lobbied for a decade to exist.Coinbase did not create that demand. It arrived after the demand was proven and applied the one thing the incumbents lack: an existing base of funded accounts.

How the category got here

The speed of prediction markets’ arrival is easy to underrate, because the idea is old and the business is not.Event contracts existed for decades as academic instruments and offshore curiosities. Intrade, Augur, PredictIt: small, legally embattled, intellectually respected, commercially irrelevant. The turn came in October 2024, when a United States court ruled that Kalshi could legally offer election contracts, and the platform relaunched within hours, thirty two days before a presidential election. The press coverage that followed did what a decade of academic papers had not, and gave the category a proof of concept moment in front of a mass audience.

What followed was a distribution war instead of a product war. Kalshi launched sports contracts across all fifty states in January 2025. A March 2025 partnership put Kalshi’s markets in front of Robinhood’s twenty seven million funded brokerage accounts, and Super Bowl volumes alone exceeded $1 billion. Polymarket acquired QCEX, a CFTC registered contract market and clearing organization, creating a legal path back to American users. Google Finance began embedding live odds. Prediction market prices started appearing in mainstream news coverage as though they were data, which drove users back to the platforms, which deepened the markets, which made the prices better data.

By February 2026, geopolitics had taken over from crypto as the volume driver. A single contract on whether the United States would strike Iran attracted $73 million, the largest geopolitical market in Polymarket’s history, and the platform set a single day volume record of $425 million on February 28, surpassing its Election Day 2024 peak. The category had escaped its founding use case.

Coinbase launched in December 2025, roughly fourteen months after the court ruling that made the category viable and two months after ICE announced its Polymarket investment. That is late by crypto standards and early by any other. The company did not spot the trend. It waited for the trend to be proven and then applied the largest retail distribution base in American crypto to it, which is a different decision and arguably a better one.

Why it worked, and what that says about Coinbase

The mechanics of a prediction market are not the interesting part, and crypto.news has covered what a prediction market is and how event contracts settle in detail. The interesting part is distribution.

Kalshi and Polymarket had to acquire every user they have. Coinbase had millions of funded accounts already holding balances, already verified, already accustomed to a trading interface. Adding an event contracts tab to that base is not a product launch in any meaningful sense. It is a shelf placement. The company’s December expansion, which added stocks, commodity futures, perpetual futures, and prediction markets simultaneously, was an explicit bet that distribution beats product in retail finance, and the first quarter’s numbers say the bet is paying.

That thesis has a name inside the company, the Everything Exchange, and prediction markets are its proof of concept. Coinbase’s argument is that a user who trades bitcoin, equities, perpetual futures, and the World Cup through one login is worth vastly more than a user who trades only crypto, and is vastly harder to lose to a competitor. Analysts covering the stock have picked up the framing directly: Cantor Fitzgerald noted that investors increasingly view prediction markets as the next growth leg for platforms like Coinbase and Robinhood precisely because traditional crypto trading volumes are softening. The product is not a hedge against the crypto business. It is a hedge against crypto.

The acquisition tells the same story. In December, Coinbase agreed to buy The Clearing Company, a prediction markets startup founded that same year on a $15 million seed round, for an undisclosed sum. That is not a technology purchase. A company with Coinbase’s engineering base does not need a one year old startup to build binary contracts. It is a purchase of regulatory positioning and domain staff, which tells you what Coinbase thinks the scarce resource in this category actually is.

The thing nobody wants to say about the volume

Here is the part that complicates every bullish framing: this is mostly sports betting.Sports has accounted for roughly 80% of Kalshi’s total trading volume since July 2024, and in March 2026 the figure was closer to 87%. Sports, politics, and crypto together account for 91% of Kalshi’s global volume and 90% of Polymarket’s. The 2026 World Cup has been described by analysts as the largest gambling event in history, and the numbers support it: Kalshi cleared more than $30 billion in June volume, up over 70% from May’s $17.9 billion, running above $1 billion a day since the tournament opened on June 11. Polymarket set a record $10.8 billion in the same month. Sector wide daily volume rose roughly 75% from the tournament’s start. Open interest reached $1.8 billion by the end of June, a 54% monthly increase.

Look at Coinbase’s own prediction markets interface on any given day this month and the composition is unambiguous. World Cup outcomes clearing $16 million on a single match. Total points in a basketball game. LeBron James’s next team. What a reality television cast will say during a finale. Somewhere in the mix sit contracts on the Federal Reserve’s July decision and where bitcoin closes, the markets that justify the category’s intellectual case, and they are dwarfed by the ones that do not.

The information markets argument, that event contracts aggregate dispersed knowledge into a price that beats polls and pundits, is real and demonstrably useful. Prediction market odds on the CLARITY Act have become the industry’s most watched barometer of the bill’s fate, a dynamic crypto.news examined in its coverage of the Senate showdown, and Google Finance now embeds live Polymarket and Kalshi odds directly. That is genuine market infrastructure performing a genuine public function.

It is also roughly a tenth of the volume. The other nine tenths is people betting on football, and the honest description of Coinbase’s fastest growing product is that it is a sportsbook with better epistemics attached as a garnish.

The regulatory bill is already in the mail

Which is why the legal exposure is not a tail risk. It is the central case.On April 23, Wisconsin sued Kalshi, Polymarket, Robinhood, Crypto.com, and Coinbase over sports related event contracts, arguing they function as sports wagers and violate state gambling law, and seeking orders to stop them being offered in the state. New York and Illinois have opened their own fronts. Nevada’s gaming regulators sued Kalshi in February. Arizona’s attorney general filed in March. The industry’s federal position rests on the Commodity Exchange Act and a CFTC that withdrew proposed restrictions in January 2026 and issued Polymarket a no-action letter, which is a strong federal hand and precisely the kind of hand that invites a preemption fight rather than settling one.

The structural problem is that states run gambling. That authority is old, jealously guarded, and enormously lucrative, and the sector’s entire growth story consists of routing around it by calling a bet on a football match a commodity derivative. Regulators have already delayed event contract ETFs while they decide whether these products belong in retail fund wrappers at all. Kalshi has been penalizing congressional candidates for betting on their own races, which is exactly the sort of headline that writes state legislation.

Coinbase now sits as a named defendant in that fight, and it does so having just lost its chief legal officer: Paul Grewal, the architect of the company’s regulatory strategy through the SEC years, exited on the eve of the CLARITY endgame. The company entered the most legally contested growth category in American finance and changed the driver at the same moment.

What the incumbents’ numbers say about the ceiling

The most useful way to size Coinbase’s opportunity is to look at what the leaders have already built, because it frames both the prize and the problem.Kalshi’s disclosed figures are extraordinary for a company that was a niche regulated venue two years ago: $178 billion annualized volume, annualized revenue above $1.5 billion, institutional trading volume up 800% in six months, a $22 billion valuation on a $1 billion round led by Coatue. Polymarket carries an $8 billion valuation with the New York Stock Exchange’s parent company on the cap table. Neither is public, so neither faces quarterly scrutiny of whether the growth is durable, which is a structural advantage Coinbase does not have.

Those numbers cut two ways for Coinbase. On one hand they prove the category can support a real business at scale, which is the entire bull case: if Kalshi generates $1.5 billion annualized, a $100 million run rate from a standing start is a beginning, not a ceiling. On the other hand they describe exactly how far behind Coinbase is, and in venue businesses the gap tends to widen instead of closing. Liquidity is the product. The deepest book gets the largest orders, which deepens it further, and a $4,500 ticket that clears at a two cent spread on the leading venue moves the price six cents somewhere thinner. Traders do not choose venues for the interface.

The one asymmetry favoring Coinbase is that it does not need to win. Kalshi and Polymarket are prediction market companies whose valuations demand category dominance. Coinbase is a distribution company for which event contracts are one surface among several, and a permanent third place at a $300 million run rate would still be a good outcome against a product that cost almost nothing to launch. The strategic question is not whether Coinbase beats Kalshi. It is whether the surface stays legal and whether the flow stays after the tournament.

The case for Coinbase

Take the bull argument at full strength, because it is not weak.Diversification is working, measurably. Coinbase’s crypto trading volume market share hit an all time high of 8.6% in the first quarter while it simultaneously stood up four new business lines, which is not the behavior of a company losing its core. Retail derivatives passed $200 million annualized. Prediction markets passed $100 million. The company shipped eighteen products in six months, a pace Rosenblatt called impressive while assigning a $240 target, and Bernstein reiterated a Street high $330 on the strength of the platform thesis. Ark Invest bought $44 million of stock into the June selloff.

The regulatory position is also stronger than the headlines imply. Coinbase’s whole institutional identity is being the compliant venue, and it enters this category as a CFTC regulated participant with an acquired specialist team, not as a crypto native platform improvising legality. If the state challenges resolve into a federal framework, the winners are the operators with the cleanest regulatory posture, which is precisely the position Coinbase has spent a decade and hundreds of millions of dollars purchasing.

And the strategic logic is sound on its own terms. Prediction markets were the most funded category in crypto in the first half of 2026, drawing $1.85 billion of $7.1 billion across the top ten categories, ahead of exchanges at $1.57 billion and artificial intelligence at $1 billion. Venture capital is rarely early and rarely wrong about direction, only about timing. Intercontinental Exchange, the owner of the New York Stock Exchange, announced a strategic investment in Polymarket at an $8 billion valuation, with reported commitments ranging up to $2 billion. Kalshi raised $1 billion from Coatue at a $22 billion valuation on $178 billion of annualized volume and over $1.5 billion of annualized revenue. When the NYSE’s parent and a $22 billion private company are both in the category, calling it a fad requires arguing that the smartest capital in two industries is confused.

Sitting out was never an option that produced a better outcome than participating. A Coinbase that watched Kalshi build a $22 billion business adjacent to its own funded accounts, and did nothing, would be facing a harder set of questions this quarter than the ones it faces now.

The case against

Now the other side, which is mostly about what happens after the World Cup ends.The category’s growth curve has already broken once. Combined Kalshi and Polymarket lifetime volume crossed $150 billion in April, and the same month ended a seven month streak of monthly growth. Polymarket’s active traders fell from more than 733,000 in March to roughly 643,000 in April. The June record was not organic reacceleration. It was a global tournament that occurs every four years, and it concludes this month. A business whose volume rises 75% on a World Cup will discover what its baseline is in August, and there is no version of that discovery that flatters the annualized figures currently being quoted.

The competitive position is also weaker than the growth rate suggests. Coinbase is third at best in a category where liquidity compounds: Kalshi took roughly 80% of June volumes, Polymarket holds 97% of political markets and about half of non-sports open interest. Deeper books attract larger traders, which deepen the books. Coinbase brings distribution, and distribution wins customers, but it does not on its own win the flow that makes a venue the price. Meanwhile Kalshi and Polymarket are both pushing into perpetual futures, which is to say they are attacking Coinbase’s business while Coinbase attacks theirs, and Coinbase’s derivatives business is far more valuable than its event contracts business.

Then the numbers underneath. Coinbase lost $394.1 million in the first quarter. Revenue fell 30% year over year. The price to earnings ratio sits near 69, price to sales near 7.6, and Barclays maintains an Underweight with a $107 target on the argument that new products cannot offset muted crypto volumes. The stock is down 53% over twelve months and 31% year to date, and the Coinbase Premium, the spread between bitcoin’s price on Coinbase and Binance, has been negative for fifty consecutive days, the market’s plainest statement that American demand is not returning soon. Against a $1.43 billion quarter and a $394 million loss, $100 million annualized from event contracts does not close a gap. It decorates one. Even quadrupled, it would not return the company to profitability on its own, and quadrupling assumes the World Cup was a floor.

And the deepest objection is definitional. Coinbase’s mission statement concerns economic freedom and updating a century old financial system. Its fastest scaling product lets people bet on Love Island. There is no rule requiring a company’s growth engine to match its stated purpose, and plenty of firms have quietly funded their mission with something less noble. But a company arguing to Congress that digital assets deserve their own market structure, while deriving its best growth from event contracts that four state attorneys general call gambling, is carrying a contradiction that its opponents in that argument will not be too polite to name.

The bet underneath the bet

What Coinbase actually did in December was not diversify. It changed what business it is in, and the prediction markets number is the first evidence the change is real.For a decade the company was a bet on crypto adoption. Volumes up, revenue up; volumes down, revenue down; the stock traded as a levered proxy and everyone understood the deal. The Everything Exchange rejects that identity. It says Coinbase is a distribution business that happens to have been founded on crypto, that a funded account with a trading interface is the asset, and that whatever the account holder wants to trade is a detail. Stocks, commodity futures, perps, event contracts, and tokenized real world assets are not five strategies. They are one strategy with five surfaces.

Prediction markets validate that thesis harder than any of the others, because the company had no advantage there except distribution. No technology edge, no first mover position, no liquidity, no brand association with event contracts at all. It shipped a tab and cleared $100 million annualized in seven weeks. If distribution alone can do that in a category with entrenched incumbents, the thesis is not marketing.

One more thing the quarter proved, quietly. Coinbase shipped stocks, commodity futures, perps, and event contracts in a single month and none of them broke. For a company whose operational reputation was built entirely on custody and spot trading, executing a four product launch without an incident is a competence signal that no analyst target captures. The Everything Exchange was always plausible as a slide. The first quarter is the first evidence it is plausible as an engineering organization.

The unresolved question is whether the surface Coinbase chose to prove it on survives contact with American law. That is not a question the company can engineer its way out of, and it will be answered in courtrooms in Wisconsin, Nevada, and Arizona instead of in a shareholder letter. The fastest growing product in Coinbase’s history is also the one whose existence a growing list of state governments disputes, and the company is discovering, again, that being right about where the demand is has never been the same as being allowed to serve it.August will settle the first half of it. The World Cup ends, the volume normalizes, and the market finds out whether $100 million annualized was a business or a tournament. The courts will take longer.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Revenue figures cited are annualized run rates disclosed by Coinbase, not realized revenue. Sector volume, valuation, and market share data derive from third party sources including The Block, Pew Research Center, CryptoRank, and company disclosures, and some reported figures vary between sources. Litigation described is ongoing and no outcome should be inferred. Details reflect information current as of July 14, 2026, and are subject to change. Always do your own research.

In June 2025, a week before the XRP Ledger’s EVM sidechain went live, the team building it published the arithmetic of what was coming. Polygon had contributed somewhere between $2 billion and $6 billion in total value locked to Ethereum, up to a tenth of the whole.

Summary

- The XRPL EVM sidechain promised a $600 million to $12 billion TVL uplift but holds only $25,741 after one year.

- The chain is technically live, audited, and maintained, but almost no users or capital have arrived.

- Moai Finance has recorded just $95,008 in cumulative spot volume across the sidechain’s entire existence.

- XRPL’s institutional mainnet activity grew while permissionless EVM DeFi failed to gain traction.

- The result suggests EVM compatibility alone does not create demand without users already waiting for cheaper or better execution.

If the XRPL EVM sidechain matched that trajectory, the post argued, the uplift to the XRP Ledger would run from $600 million to $12 billion, and it would fundamentally change the demand curve for XRP. Ninety entities were already building. Sixty days of testnet had pulled in developers who had never touched the XRP ecosystem. The technology was ready. The builders were here.The sidechain launched on June 30, 2025. The anniversary passed two weeks ago.

As of July 14, 2026, total value locked on the XRPL EVM sidechain is $25,741, according to DefiLlama. Chain fees over the past 24 hours: zero. Chain revenue: zero. Decentralized exchange volume over 24 hours: zero. Over seven days: also zero. The largest protocol on the chain, a decentralized exchange called XRiSE33 Network, holds $11,909. The second largest, a launchpad named Riddle, holds $8,831. Moai Finance, the only protocol on the chain that has ever recorded meaningful trading, has done $95,008 in cumulative spot volume across its entire existence and currently holds $1,117.

The low end of the projection was $600 million. The delivery is $25,741. That is not a shortfall. It is a rounding error against a rounding error, and it is the most instructive number in the XRP ecosystem right now, because of what else the same ledger accomplished during the same twelve months.

What was actually built

The technical work was not the problem, and it is worth stating that clearly before the autopsy.The XRPL EVM sidechain is a Cosmos SDK chain running Ethereum Virtual Machine compatibility, connected to the XRP Ledger mainnet through the Axelar bridge, which links more than eighty networks. XRP is the native gas token. Bridged XRP locks on mainnet and mints a synthetic version on the sidechain, so the design preserves mainnet supply integrity while freeing the asset for smart contract use. Consensus is proof of authority, targeting up to 1,000 transactions per second at fees far below Ethereum’s. Squid handles cross-chain transfers as the official interface. Band Protocol supplies oracles, Grove supplies public RPC endpoints. Wormhole integration was slated to follow, extending reach to more than 200 applications across 35 ecosystems.

Ripple built it with Peersyst and contributors from the Cosmos community. crypto.news covered the mainnet launch on June 30, 2025, where Ripple’s David Schwartz framed the sidechain as extending the ecosystem without altering what makes the XRP Ledger reliable. The launch roster included Strobe, a money market for lending and overcollateralized borrowing; Securd, a lending protocol for financing collateralized leverage; Vertex, a derivatives venue; plus Moai, Elys, XRise, and Hammy. The infrastructure was audited end to end. Subsequent releases hardened it further, with a v11 upgrade focused on economic security, IBC transfer hardening, and proof of authority validator management, and an upgrade to Cosmos EVM v0.4.1 adding ERC-20 mint and burn plus current Ethereum improvement proposals.

None of that is vaporware. Every component works. Someone can bridge XRP to the sidechain right now, deploy a Solidity contract, and trade on a decentralized exchange. The chain is live, secure, and functionally complete.It is also empty.That is the part worth sitting with, because it inverts the usual crypto post-mortem. The standard failure story is a project that promised more than it could build: the whitepaper outran the engineers, the deadlines slipped, the product never shipped or shipped broken. XRPL EVM shipped, on schedule, working, audited, and maintained through multiple upgrades over the following year. Every promise about the technology was kept. The only promise that failed was the one about people.

The decline, measured

The most damning fact is not the small number. It is the direction.In August 2025, roughly six weeks after launch, DefiLlama showed the sidechain hosting three decentralized exchanges and a single launchpad, with combined total value locked of $100,818. Twenty four hour volume across the entire chain was $3,238, every dollar of it from Moai Finance. Riddle, XRiSE33 Network, and SurgeDefi recorded no trading activity whatsoever. Developer data at the time counted 168 developers on XRPL EVM against 8,448 on Ethereum, a gap of roughly 98%.

That was the bad news at six weeks. Today, eleven months later, total value locked is $25,741. The chain lost roughly three quarters of the little it had. The protocol count is nominally higher, with Midas RWA, Hyperithm, Portal, Axelar, and an NFT marketplace called Mintiq now listed, but every one of those additions reports zero total value locked on this chain. They are multi-chain protocols that support XRPL EVM the way a restaurant supports a dietary restriction: the option exists on the menu and nobody orders it.

The volume figures are what turn an underperformance into something stranger. Zero over 24 hours. Zero over seven days. Moai Finance, the chain’s only functioning exchange by any historical measure, shows $95,008 in cumulative volume since inception. Not per day. Total, across a year of operation, on the flagship DeFi venue of a chain built for a token with a market capitalization near $68 billion.

A chain with $25,741 of capital and no trading is not a slow start. It is a chain nobody is using, and the trend line says that fewer people are using it every month.For scale, the entire TVL of the sidechain is currently less than the value of roughly 24,000 XRP. Ripple releases a billion tokens from escrow on the first of every month. The whole DeFi economy built on top of the XRP Ledger, through the official sidechain, could be funded out of forty thousandths of a single monthly escrow tranche.

Who was supposed to show up

Reading the launch roster a year later is the clearest way to see what went wrong, because the roster was not thin. It was specific.Strobe was announced as a money market for lending and overcollateralized borrowing on XRPL. Securd was to provide passive income by financing collateralized leverage across DeFi positions. Vertex was a derivatives platform optimizing capital efficiency. Between them, those three cover the load-bearing categories of any DeFi economy: lending, leverage, and derivatives. Add a decentralized exchange for spot, an oracle from Band, RPC infrastructure from Grove, and a cross-chain interface from Squid, and the stack on paper was complete. Nothing essential was missing.

Today none of those three names appears among the protocols holding capital on the chain. The entire TVL sits in two decentralized exchanges and a launchpad. The lending market that would have made bridged XRP productive, the derivatives venue that would have given traders a reason to keep collateral there, the leverage layer that generates the recursive deposits which inflate every chain’s TVL figure: none of it materialized in a form anyone funded.

That absence explains the volume better than any macro argument. A chain with only spot DEXs and no credit has no reason to hold capital between trades. Money arrives, swaps, and leaves. On chains where TVL compounds, it compounds because deposits are collateral, collateral is borrowed against, and the borrowings are redeposited. Without a lending market, TVL is just the float sitting in a few pools, and $25,741 is what that float looks like when almost nobody is swapping.

The irony is precise. The lending layer the sidechain needed and never got is now being built on the mainnet instead, in a permissioned, institutionally underwritten form that has nothing to do with the EVM. The sidechain was the place DeFi was supposed to happen. Credit went somewhere else, and the sidechain was left holding the part of DeFi that cannot sustain itself alone.

Why the projection was never plausible

The Polygon comparison that produced the $600 million to $12 billion range deserves scrutiny, because in retrospect it was comparing two things that share almost no structural features.

Polygon captured Ethereum overflow. It existed because Ethereum’s fees became unbearable during periods of intense demand, and there was a vast population of users and developers already transacting on Ethereum who wanted the same applications for less money. The demand preceded the chain. Polygon did not create appetite for DeFi; it captured appetite that already existed and had nowhere cheaper to go. Add hundreds of millions of dollars in liquidity incentives and a mature Ethereum tooling ecosystem that ported over with a config change, and the TVL followed the demand.

XRPL EVM inverted every one of those conditions. There was no congestion to relieve, because the XRP Ledger has never been congested. There was no population of XRPL DeFi users seeking cheaper execution, because XRPL DeFi barely existed: the ledger’s total value locked has run under 0.05% of its market capitalization, against roughly 20% for Ethereum and 10% for Solana. That statistic was cited in the launch material as the size of the opportunity. It is more accurately read as the size of the demand problem.

Six million XRPL wallet holders were presented as a distribution advantage, but they were six million holders of a payments asset who had spent a decade not asking for smart contracts. The sidechain did not remove a barrier between XRP holders and DeFi. It tested whether the barrier was the reason, and the answer came back no.The Peersyst material was explicit that testnet momentum arrived organically, without incentives or paid marketing, and treated that as evidence of underlying pull. Ninety logos on a testnet is a real signal of developer curiosity. It is not a signal of user demand, and the distinction is the whole story: developers show up to explore new chains constantly, at near zero cost, and the tourism ends when nobody trades.

The comparison that hurts

Here is why this matters beyond a dead sidechain: the XRP Ledger had an extraordinary year, on the mainnet, at exactly the same time.

Tokenized real-world assets on the XRP Ledger grew from under a billion dollars at the start of 2026 to roughly $3.5 billion, and the ledger has led the market on 90-day RWA inflows, adding $1.9 billion. In May 2026, Ondo Finance executed the first cross-border, cross-bank redemption of tokenized United States Treasuries on the XRPL, clearing in seconds, with JPMorgan and Mastercard involved in the surrounding work. RLUSD grew past a $1.5 billion market capitalization. The native automated market maker and multi-purpose token amendments both passed validator votes. The XLS-65 and XLS-66 lending amendments are in validator voting now, an effort crypto.news examined in its analysis of what on-chain credit would mean for XRP.

The mainnet, in other words, went and built exactly the thing the sidechain was supposed to enable, using its own native primitives, aimed at institutions instead of Solidity developers, and it worked. Institutional tokenization found the XRP Ledger without an EVM. Permissionless DeFi did not find it with one.

That contrast reframes the sidechain from a failed product into a resolved question. The bet was that XRPL’s problem was programmability, and that giving Ethereum developers a familiar environment on top of XRP liquidity would unlock a DeFi economy. Twelve months of data says the problem was never programmability. It was that the XRP ecosystem’s actual demand is institutional settlement, and institutional settlement does not want an EVM sidechain with proof of authority consensus and a bridge. It wants permissioned pools, credentialed counterparties, and off-chain underwriting, which is precisely what the mainnet amendments deliver.

Notice also where XRP-adjacent DeFi capital actually went. VivoPower allocated $100 million through Flare, a separate network built specifically to give XRP holders DeFi access, rather than through Ripple’s own sidechain. When money did move toward XRP DeFi, it routed around the official product.

The case that this is unfair

The bearish read above deserves an honest counterweight, and there is a real one.Timing first. The sidechain launched on June 30, 2025, roughly three weeks before XRP’s cycle high near $3.65, and spent its entire first year inside the worst crypto drawdown since 2022. Bitcoin fell more than 40% from its October peak. Digital asset funds ran multi-billion dollar outflow streaks. Three consecutive losing quarters, the longest streak since the last bear market, with institutional capital rotating into artificial intelligence equities. TVL across the market compressed. Judging a new chain’s ecosystem formation against a projection written in a bull market, and measured entirely inside a bear market, stacks the comparison. Polygon’s $2 billion to $6 billion was built during a mania.

Second, no incentives. Polygon’s TVL was purchased. Hundreds of millions in liquidity mining subsidies pulled capital that largely left when the subsidies stopped. XRPL EVM launched with none, which is defensible as a matter of discipline and fatal as a matter of cold-start economics. Liquidity begets liquidity, and a chain with $25,741 cannot attract a trader who needs to move $50,000 without moving the price against themselves. Every DeFi ecosystem that reached scale bought its first users. Refusing to do so is a choice with predictable consequences, not evidence that the underlying idea is wrong.

Third, sequencing. The credit layer was always the point. RippleX’s own framing describes a deliberate progression: represent value, move value, trade value, finance value. The lending amendments now in voting are the fourth step, and they are being built on the mainnet with institutional design constraints, not on the sidechain. If the strategy is institutional DeFi rather than retail DeFi, then the sidechain was never the main line. It was an option that Ripple bought cheaply, and options that expire worthless are still rational to have purchased.

Fourth, the infrastructure persists. A chain is not a startup that folds. It runs, it gets upgraded, and it costs almost nothing to leave running. If the market turns, if incentives arrive, if a single application finds product-market fit, the environment is there, audited and connected to eighty networks. Twelve months is a short window for infrastructure that took years to build.

Fifth, and least comfortable for the bears: the metric itself is contested. Total value locked measures deposited capital, not usefulness, and it is trivially gamed by recursive lending and mercenary liquidity on chains that do buy their numbers. A chain with honest, unincentivized TVL of $25,741 and a chain with subsidized TVL of $500 million are not obviously ranked the way the figures suggest. That argument does not rescue XRPL EVM, because zero volume is not a metrics artifact, but it is a fair caution against treating one number as a verdict on an entire architecture.

The case that it is worse than it looks

Now the harder reading, which the numbers support more directly.The bear market explains compression. It does not explain zero. Solana’s memecoin economy generated tens of billions of dollars of volume through the same drawdown. Robinhood Chain launched on July 1, 2026 into the identical macro and did more than $3 billion in decentralized exchange volume in two weeks, with 19,586 tokens created on a single day. Hyperliquid, Base, and BNB Chain all sustained real activity. Capital did not stop moving in 2026. It moved somewhere else. The absence of incentives explains a smaller number; it does not explain a chain where the flagship exchange has done $95,000 in trading across its entire existence while a two-week-old competitor chain did $3 billion.The declining trend is the tell. $100,818 in August 2025 to $25,741 in July 2026 is not a chain waiting for conditions to improve. It is a chain being abandoned by the little capital that tried it. Bear markets thin the field; they do not usually take three quarters of the liquidity from a chain that started with almost none.

And the developer number from August was the leading indicator everyone skipped: 168 developers against Ethereum’s 8,448. Chains are not built by logos on a testnet. They are built by people shipping applications that someone wants to use, and the ratio said, six weeks in, that the ninety entities had not converted into an ecosystem. The launch roster is the proof. Strobe, Securd, Vertex: named as launch partners, and today the chain’s entire TVL sits in two DEXs and a launchpad nobody trades on. The applications that were supposed to give the chain a reason to exist either never shipped at scale or shipped and found nobody.

The strategic cost is subtler than the wasted engineering. For a year, “XRPfi” and the EVM sidechain functioned as an answer to the hardest question about XRP, which is how any of Ripple’s progress reaches the token. The sidechain made XRP the gas asset of a DeFi economy, which would have generated real, recurring token demand. That answer is now empirically closed, and it closes at the same moment as the structural finding that most of Ripple’s bank partners never touch XRP at all. Two of the three main value-accrual arguments for the token have now been tested against data in the same quarter. Both came back thin.

What the $25,741 is actually evidence of

Step back from XRP entirely, because the finding generalizes.The industry has spent five years treating EVM compatibility as a growth strategy. The reasoning is seductive: Ethereum has the developers, the tooling, the mental models, and the applications, so any chain that speaks Solidity inherits access to all of it at the cost of an engineering project. Dozens of chains have run this play. A few worked. Most produced exactly what XRPL EVM produced, which is a technically excellent environment with nobody in it.

The reason is that EVM compatibility removes a supply-side constraint and does nothing to the demand side. It makes building easier. It does not make anyone want the thing built. When a chain has organic demand and a technical barrier, removing the barrier unlocks enormous value, which is the Polygon story and the Arbitrum story. When a chain has a technical option and no demand, removing the barrier produces an empty room with excellent acoustics.

The diagnostic question is therefore simple and almost never asked before a chain commits to the work: is there a queue? Not a waiting list of developers, who are cheap to attract and cost nothing to lose, but users currently doing the thing somewhere worse and paying for the privilege. Polygon had a queue. Arbitrum had a queue. XRPL EVM had a hypothesis that six million payment-asset holders would become DeFi users once the tooling arrived, and hypotheses are not queues.

XRPL had the cleanest possible version of the test. Six million wallets. A top-ten asset. Twelve years of uptime. Deep liquidity. Real regulatory standing. A functioning native DEX. Every input the thesis requires, and a year later the DeFi economy built on top of it holds less capital than a used car. If EVM compatibility were the unlock, it would have worked here. The mechanics of liquidity pools and automated market makers are identical on XRPL EVM to what they are on Ethereum. The pools are simply empty, because pools are filled by people who want something, and nobody wanted this.

The lesson costs Ripple very little and should cost the next chain a great deal. The company retained an option, learned that its DeFi demand is institutional rather than permissionless, and redirected to native amendments aimed at exactly that. That is a reasonable outcome from a cheap experiment. The problem belongs to everyone still pitching an EVM layer as a demand strategy, because the most rigorous public test of that thesis just returned $25,741 and no volume, and the DeFi industry has not noticed.

The number to remember

The projection was $600 million to $12 billion. The delivery is $25,741 and zero trading volume, twelve months later, on a chain that works perfectly.That gap is not a failure of engineering, marketing, timing, or macro, though each contributed at the margin. It is a measurement. Somebody asked, with real money and real code and a well-built product, whether the XRP ecosystem wanted permissionless DeFi. The ecosystem answered. The answer was no, and it took a year and a nine-figure projection to hear a number that fits on a single line of a spreadsheet.

XRPL’s institutional story is doing better than it has ever done. Its DeFi story is a chain with $25,741 on it and nobody trading. Both of those things are true at once, and anyone building a thesis on XRP needs to hold both, because the second one used to be an argument and is now just a data point.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Total value locked, volume, and protocol figures are drawn from DefiLlama as of July 14, 2026, and change continuously; TVL is a contested metric and methodologies differ between trackers. Historical figures are attributed to the sources that reported them at the time. Projections cited were published by the sidechain’s development team and are not forecasts by crypto.news. Details reflect information current as of July 14, 2026. Always do your own research.

Ripple CTO Emeritus David Schwartz has defended XRP advertising in college sports after critics called for tighter restrictions on crypto promotion.

Summary

- David Schwartz argues truthful XRP advertising receives First Amendment protection against broad government restrictions nationwide.

- His argument cites Supreme Court rulings that struck restrictions on lawful alcohol and gambling advertising.

- Commercial speech remains regulable, meaning the Constitution does not automatically block every potential advertising restriction.

The debate followed the University of Kansas athletics program’s decision to place XRP branding on team uniforms under a multi-year partnership with Ripple.

In a July 15 post on X, Schwartz argued that governments cannot broadly suppress truthful advertising for lawful products simply because officials believe consumers may make poor decisions. His position centers on First Amendment protections for commercial speech.

Schwartz turns XRP advertising debate into constitutional question

The discussion began after critics compared crypto promotion in college sports with advertising for gambling, tobacco and alcohol. They argued that universities should not expose students and younger sports fans to digital asset marketing.

Schwartz responded with a legal argument rather than a defense of XRP as an investment. He wrote that the government cannot suppress truthful commercial speech merely to prevent people from making “bad, but lawful, decisions.” His argument draws a distinction between regulating an activity and banning truthful speech about that activity.

Supreme Court cases support protection for lawful advertising

Schwartz cited 44 Liquormart v. Rhode Island, a 1996 Supreme Court case that struck down restrictions on advertising liquor prices. The Court found that Rhode Island could not broadly block truthful price information simply because the state wanted to reduce alcohol consumption.

He also pointed to Greater New Orleans Broadcasting Association v. United States. In that case, the Supreme Court ruled that a federal restriction could not block advertisements for lawful private casino gambling under the circumstances before the Court.

However, those rulings do not make every restriction on XRP advertising automatically unconstitutional. Under the Supreme Court’s Central Hudson framework, commercial speech receives protection when it concerns lawful activity and is not misleading. Governments may still impose properly tailored restrictions that directly serve a substantial public interest.

Kansas deal puts XRP logo across college sports

Kansas Athletics announced the Ripple partnership on July 8. The XRP logo will appear on uniforms across the university’s athletic programs, making it the first cryptocurrency jersey patch used across a major college athletics program, according to Kansas.

The agreement also covers branding at athletic venues, digital properties and events. Ripple will fund financial and technology education programs for student-athletes and the wider campus community. The partnership also expands an existing recruitment link between Ripple and Kansas graduates.

As previously reported, the agreement runs for five years and has personal ties to Ripple CEO Brad Garlinghouse, a University of Kansas alumnus. The sponsorship has since drawn wider attention to how universities should handle digital asset advertising.

XRP legal history adds context to advertising dispute

The debate comes three years after a federal court issued its split ruling in the SEC’s case against Ripple. The court found that Ripple’s programmatic XRP sales did not qualify as securities transactions under the circumstances examined, while certain institutional sales violated securities laws. The case formally ended in 2025 with a $125 million penalty and an injunction remaining in place.

That history makes broad claims about XRP’s legal status more complex than simply calling the asset universally exempt from financial regulation. Schwartz’s First Amendment argument instead rests on a narrower point: truthful commercial speech concerning lawful activity receives constitutional protection.

A government attempt to impose a blanket ban on XRP advertising could therefore face a serious First Amendment challenge. But existing Supreme Court doctrine still allows some commercial advertising rules when regulators can satisfy the required constitutional test.

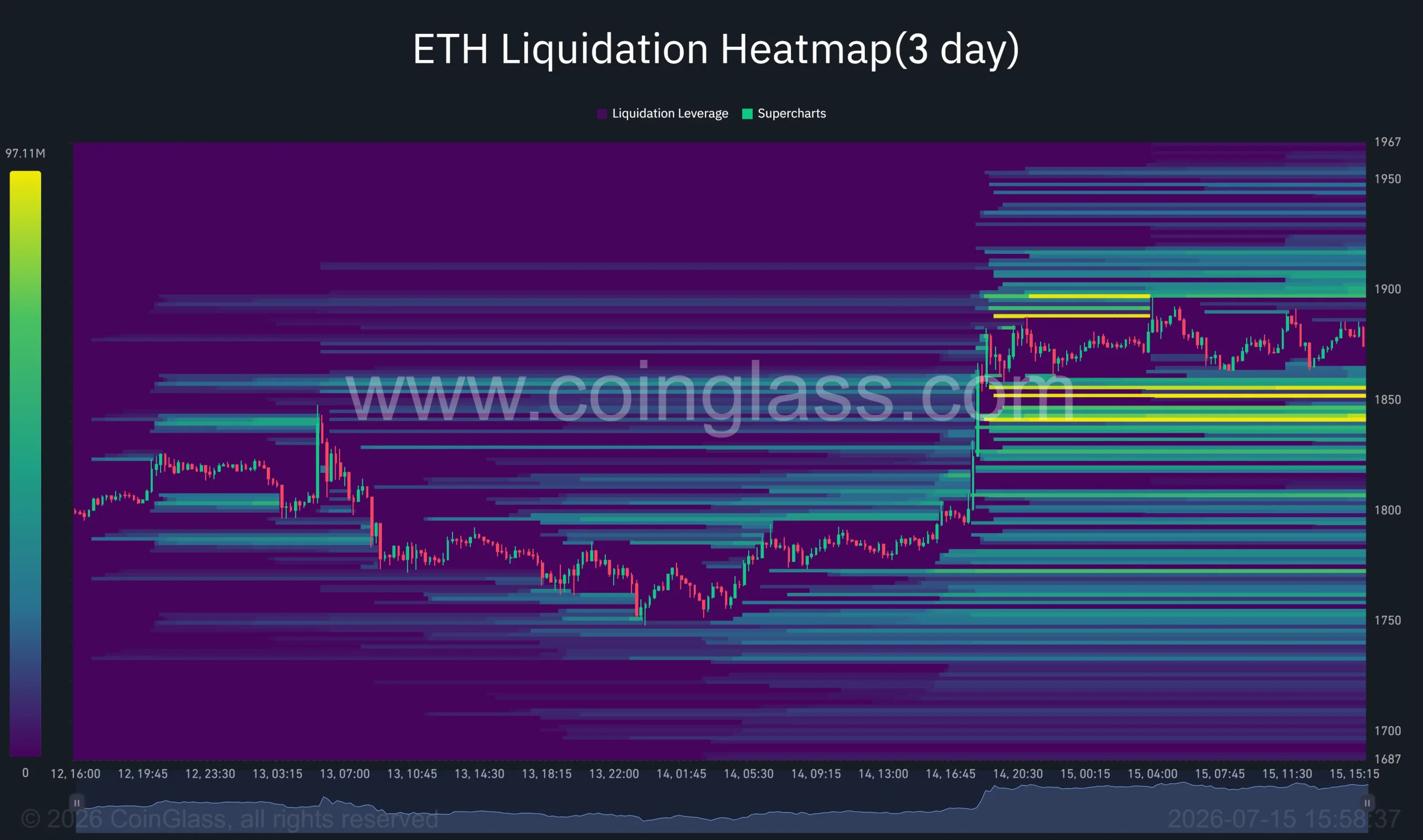

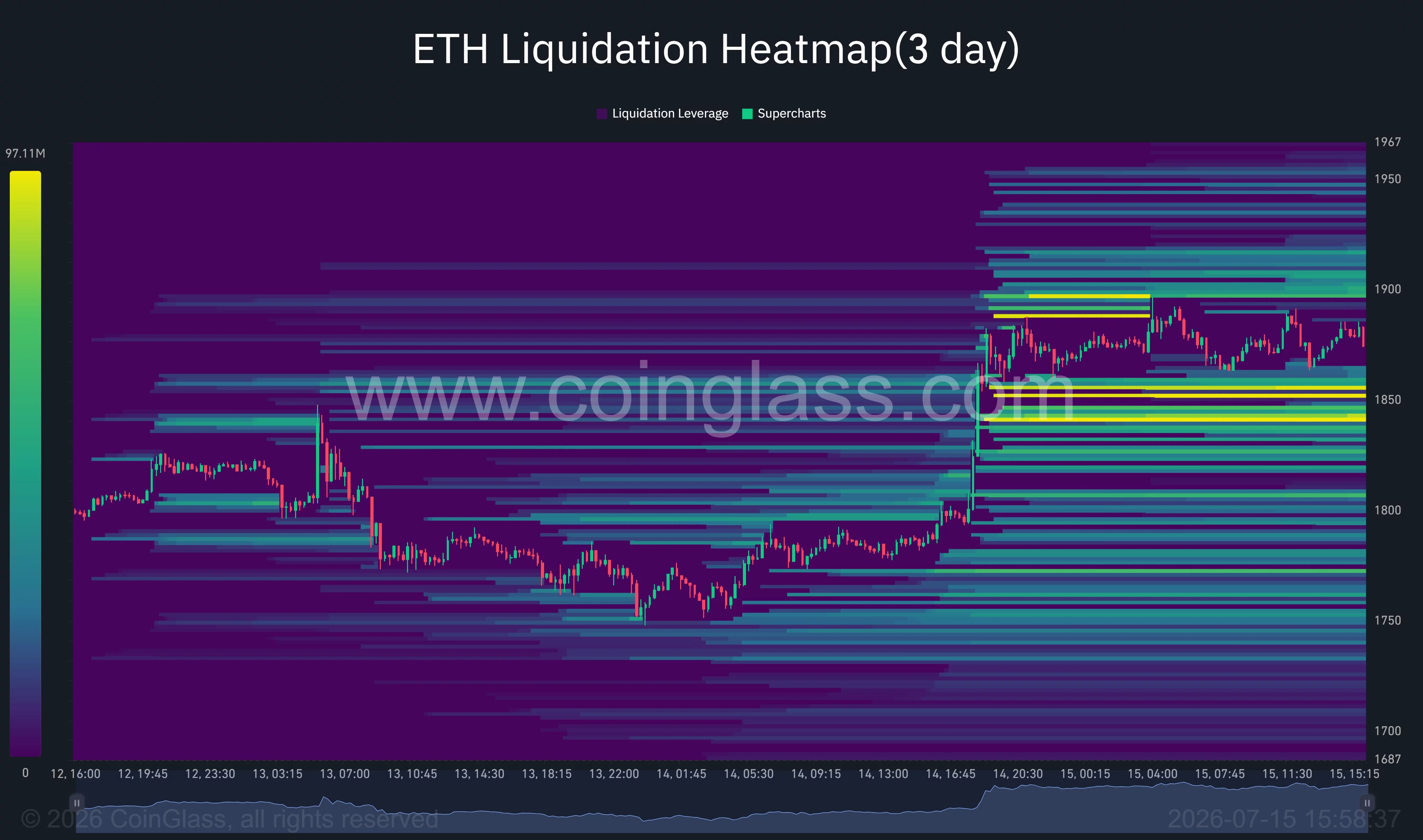

Ethereum price has reclaimed the $1,850 resistance after softer-than-expected U.S. inflation data triggered a sharp short squeeze, putting the $2,000 level back into focus for traders.

Summary

- Ethereum price broke above $1,850 after softer U.S. CPI data sparked a broad crypto rally.

- Technical charts and liquidation clusters suggest $2,000 is the next major price target.

- Analysts say holding $1,850 as support is key to sustaining the current bullish trend.

The second-largest cryptocurrency climbed nearly 5% on July 15 after June’s Consumer Price Index came in below expectations, easing concerns that Federal Reserve Chair Kevin Warsh would resume aggressive rate hikes. Risk assets rallied across global markets, with tech stocks advancing alongside cryptocurrencies as investors priced in a more accommodative policy outlook.

Derivatives markets amplified the move. CoinGlass liquidation data shows a dense cluster of leveraged short positions between $1,800 and $1,850 was wiped out as Ethereum broke through resistance. Forced buybacks accelerated the rally toward $1,900, while the latest liquidation heatmap now shows fresh liquidity pockets concentrated around $1,900-$1,950.

A successful push through that zone could expose another wave of liquidations and open a path toward the psychological $2,000 level.

Technical breakout puts $2,000 back in play

Ethereum’s daily chart shows the recovery has developed from a series of rounded-bottom formations that formed after June’s selloff to nearly $1,500. Price has now completed a breakout above the neckline near $1,850, a level that capped several recovery attempts over recent weeks. The measured move from the pattern projects a target close to $2,190, matching a major resistance zone from earlier this year.

Momentum indicators continue to favor buyers. The Aroon Up indicator stands above 92 while Aroon Down has dropped to zero, suggesting bulls retain control of the prevailing trend. Relative Strength Index has climbed to around 63, leaving room for additional gains before reaching overbought territory.

The 4-hour chart reinforces the bullish structure. Ethereum has reclaimed the 100% Fibonacci retracement level near $1,897 after holding above the 78.6% retracement around $1,815. MACD remains in positive territory with widening bullish momentum, while the Chaikin Money Flow reading above zero suggests capital continues to enter the market rather than leave it.

Commenting on the breakout, crypto analyst Daan Crypto Trades wrote on X:

“ETH Breaking above the $1.8K level and saw some good continuation so far. The market structure has flipped back to bullish on this timeframe.”

He added that the next major high-timeframe resistance sits near the $2,100 region, while maintaining $1,800 as support remains critical for bullish momentum.

Another closely followed trader, Ted Pillows, believes the next milestone could arrive quickly if buyers defend current levels. “$ETH has fully reclaimed its key resistance level. If Ethereum manages to hold above the $1,850 level, the pump towards $2,000 will be next,” he wrote.

Outside the charts, Ethereum continues to benefit from tightening on-chain supply. A large share of circulating ETH remains locked in staking, limiting readily available exchange balances even as demand improves.

At the same time, regulatory progress surrounding U.S. crypto legislation and spot ETF adoption has kept institutional interest intact after several weeks of macro-driven volatility tied to Middle East tensions and government-linked crypto transfers.

Loss of $1,850 support would weaken the bullish case

Despite the improving setup, Ethereum still faces several hurdles before reclaiming $2,000. The liquidation heatmap shows heavy leveraged positioning between $1,900 and $1,950, where sellers may attempt to defend resistance. Failure to absorb that supply could trigger another round of profit-taking after the recent rally.

Macro risks also remain. Any resurgence in inflation, renewed geopolitical tensions that drive oil prices sharply higher, or unexpectedly hawkish comments from Federal Reserve officials could reverse sentiment across risk assets.

From a technical perspective, losing the newly reclaimed $1,850 support would invalidate the breakout and shift attention back toward $1,815, followed by the stronger demand zone around $1,750. As long as Ethereum continues to post higher highs while defending $1,850, however, the probability of a move toward $2,000 and potentially the $2,100-$2,190 resistance region remains favorable.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

The Czech Ministry of Finance has added Polymarket to its list of unauthorized online gambling websites, triggering mandatory blocking by internet service providers (ISPs). The move brings another European jurisdiction into the growing crackdown on prediction markets that regulators argue operate without the right licenses.

According to the ministry, Polymarket’s website was included under the Czech Gambling Act, which bars operators from offering unlicensed online gambling services to people in the country. ISPs are required to block the listed site within 15 days of the blacklist publication, as described in the ministry’s published data and the relevant law.

Key takeaways

- The Czech Ministry of Finance has formally blacklisted Polymarket under the Gambling Act and ordered ISP blocking within 15 days of listing.

- Regulators across Europe are increasingly scrutinizing prediction-market contracts, particularly when they resemble binary options.

- ESMA warned that marketing labels like “event contracts” may not change the legal assessment if a product meets the definition of a financial instrument.

- Similar restrictions have emerged beyond Europe, including actions tied to gambling concerns in other jurisdictions and state-level disputes in the US.

How the Czech blacklist affects access

In a notice published by the Czech Ministry of Finance, Polymarket was added to the publicly available list of unauthorized internet gambling websites. The ministry’s classification is tied to the country’s Gambling Act framework, under which offering online gambling to Czech users without authorization is prohibited.

The practical effect is straightforward: once a domain is included on the ministry’s blacklist, ISPs must block access. The ministry’s materials point to the legal obligation to implement such blocks within 15 days after the name is published.

For Polymarket, which operates as a prediction market where users trade contracts tied to the outcomes of future events, this kind of restriction can directly limit retail participation from affected networks, even if the platform remains accessible in other countries.

Why prediction markets keep running into regulation

The Czech action follows a broader regulatory pattern. Regulators in multiple jurisdictions argue that some prediction-market contracts effectively function as gambling products—or, in certain cases, fall within existing financial market rules—depending on how the contracts behave.

Earlier this year, the European Securities and Markets Authority (ESMA) issued guidance warning that many prediction market contracts could already be captured by restrictions on binary options under EU rules. ESMA emphasized that firms cannot sidestep regulatory obligations merely by branding binary-style products as “event contracts” instead of derivatives.

ESMA’s point was technical but consequential: whether a contract is treated as a financial instrument depends on its characteristics rather than its marketing label. ESMA further noted that companies offering qualifying contracts to retail investors may already face national restrictions reflecting the EU’s 2018 ban on binary options, while offerings to professional clients may require authorization under MiFID II (the Markets in Financial Instruments Directive).

For market participants, the implication is that compliance risk does not hinge on naming conventions. Platforms may need to evaluate contract structures—such as how payouts are determined, how the products are offered, and the target investor base—because regulators are increasingly treating substance as the deciding factor.

EU scrutiny is part of a wider global trend

While EU authorities have been vocal about the potential overlap between prediction-market contracts and regulated financial products, the issue is not limited to Europe. Cointelegraph previously reported that regulators in several other countries have restricted access to Polymarket citing gambling-related concerns.

In the Asia-Pacific region, similar actions have been described in Australia, Indonesia, and Singapore. Elsewhere, the core debate has also played out in the United States, where Polymarket and rival platform Kalshi have faced regulatory challenges at the state level over whether their event contracts are illegal gambling.

At the same time, the Commodity Futures Trading Commission (CFTC) has maintained that such products fall under its exclusive jurisdiction as federally regulated derivatives. This disagreement has contributed to a patchwork environment, including conflicting court outcomes, and has fueled calls for clearer congressional guidance on whether sports and political event contracts should be treated as gambling or handled as derivatives under federal frameworks.

The result for users is uneven market access: depending on where they live and how regulators classify the same underlying contract mechanics, the same platform can be permitted, restricted, or blocked.

What to watch next

With the Czech blacklist now active and ESMA continuing to frame the issue around contract characteristics, investors and users should expect more compliance-driven changes across jurisdictions—either through licensing, product redesign, or restricted access. The key uncertainty remains how quickly courts and regulators converge on a consistent legal classification for prediction-market contracts that sit between gambling and financial derivatives.

For Polymarket specifically, the immediate question is whether it will take steps to operate within Czech requirements or adjust its distribution approach to mitigate access blocks. More broadly, market watchers should monitor how EU guidance translates into enforcement actions and whether similar measures spread through additional member states.

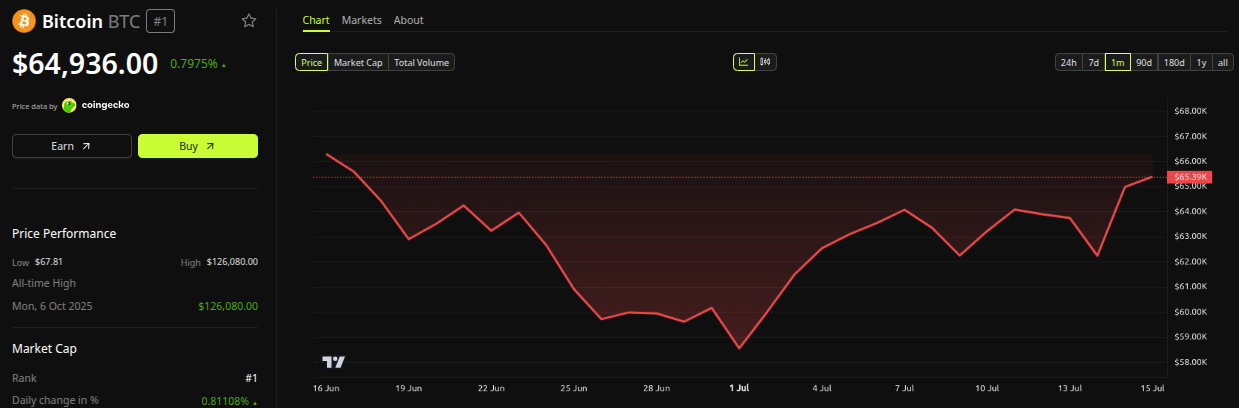

Peter Schiff attacked Bitcoin and Michael Saylor on July 15, predicting a slide to $20,000 (nearly 70% below current prices) and questioning MicroStrategy’s decision to sell stock rather than BTC.

The economist argues that Saylor is trapped and that holders who refuse to sell today will regret it soon.

Schiff Targets Strategy’s $450 Million Stock Sale

Strategy (formerly MicroStrategy) is the corporate vehicle through which Michael Saylor accumulated more than 847,000 Bitcoin, making it the largest public holder of the asset.

Schiff dedicated part of his latest podcast episode to dissecting the company’s latest financial moves. His conclusions were predictably harsh.

The firm has gone three consecutive weeks without buying Bitcoin. It has not sold any either since disposing of 3,588 BTC last week, opting instead to raise $450 million through a common stock sale.

That decision pushed cash reserves to $3 billion while the stock traded at a steep discount to its Bitcoin holdings. Schiff called the operation a needless dilution of shareholders. The company chose paper over its own reserves.

His reasoning centers on a trap. According to the economist, Saylor avoids selling BTC because any meaningful liquidation would sink the price. The market, he claims, already understands that perfectly well.

“Saylor knows if he starts really selling Bitcoin, the price is gonna crash. Now, the problem is it’s gonna crash anyway because the market realizes the bind that he’s in, and even if he doesn’t sell, the market is gonna crash out from under him. But he is so nervous about selling Bitcoin that he’s willing to sell his own stock at a massive discount,” Schiff noted.

Follow us on X to get the latest news as it happens.

Why Does Schiff Expect Bitcoin to Reach $20,000

Schiff went further with his forecast. He identified resistance near $65,000 and support around $58,000, warning that a break below could drag Bitcoin under $50,000. His floor sits between $30,000 and $20,000, a level not seen for years.

Curiously, the critic admitted some regret. He said buying Bitcoin 15 years ago would have made perfect sense, though he feels absolutely no remorse about skipping the last five years of the rally.

“I don’t regret not buying it three, four, five years ago… But yeah, 15 years ago, sure, I should have bought it,” the economist confessed.

The timing of the criticism, however, looks awkward. Bitcoin trades just under $65,000 at the time of writing, up nearly 5% in the last week, according to BeInCrypto data.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

The broader debate, however, extends beyond Schiff’s predictions. Analysts have been reassessing the corporate Bitcoin accumulation model, and Strategy sits at the center of that reevaluation.

Investors now scrutinize cash reserves, equity issuances, and funding conditions before assuming that future purchases will remain sustainable. Headline-grabbing buys no longer carry the same automatic credibility they once did in the market.

The post Peter Schiff Predicts a 70% Bitcoin Crash and Warns Holders Will Regret Not Selling appeared first on BeInCrypto.

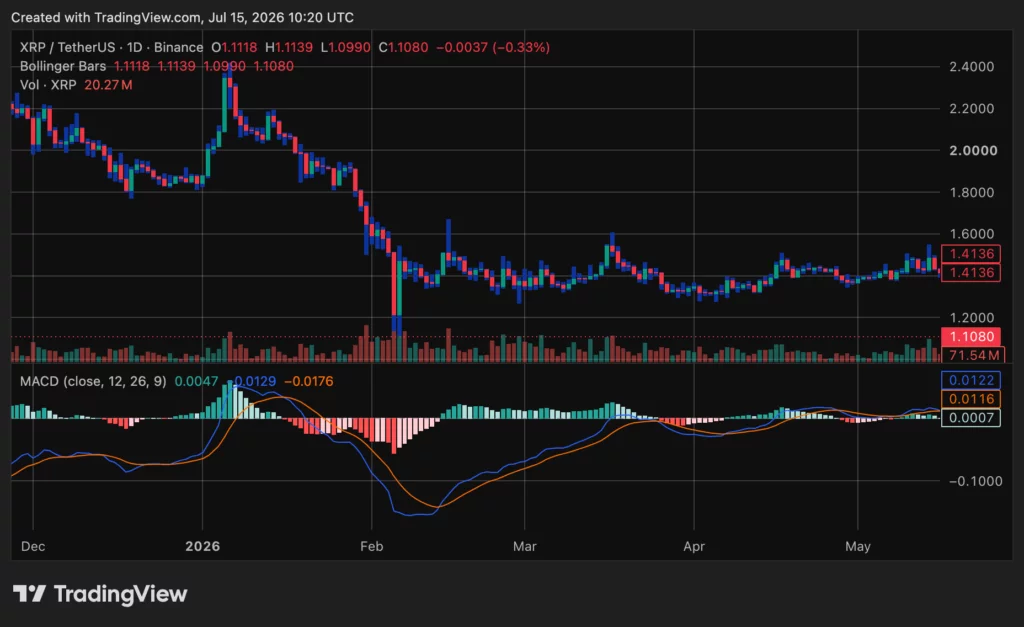

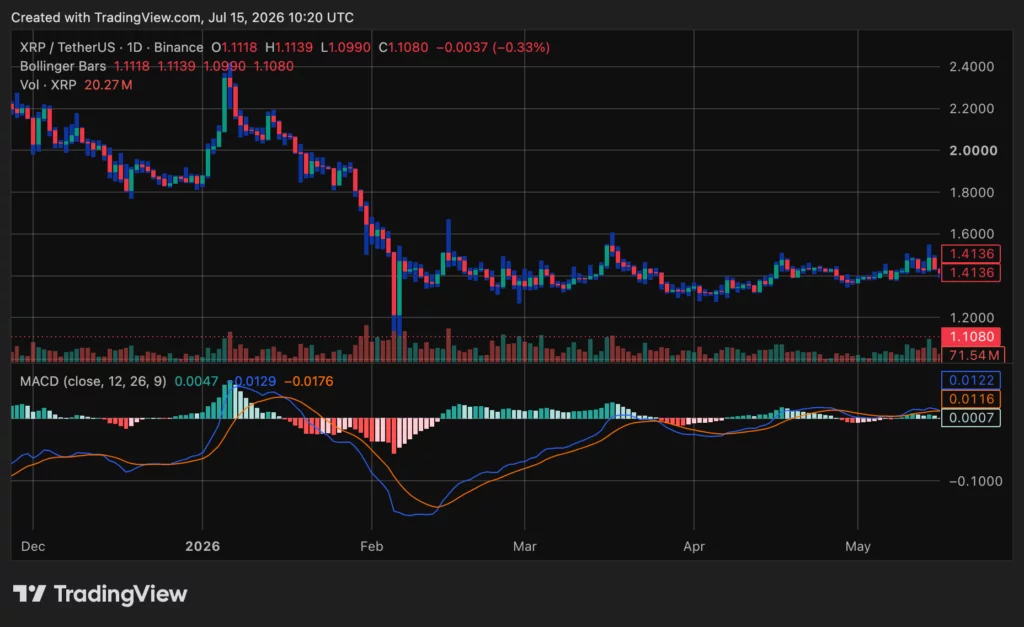

XRP rebounded to around $1.11 on July 15, recovering from the $1.07 area after gaining about 3.8% over 24 hours.

Summary

- XRP rebounded to $1.11, but analysts still view $1.12 as crucial near-term resistance for buyers.

- Bearish targets extend toward $1.058 and $1.00 if XRP fails to hold its latest recovery.

- A $50 XRP scenario requires a hypothetical $100 trillion crypto market and unchanged market dominance.

The token traded between $1.07 and $1.12, while daily trading volume increased to roughly $1.29 billion, according to the latest crypto.news XRP market data.

Despite the recovery, XRP remains about 6% lower over the past month and nearly 70% below its July 2025 record high of $3.65. Analysts are now watching whether buyers can break resistance around $1.12 or whether the latest rebound will give way to another test of the $1 psychological level.

XRP price reaches a major resistance zone

The XRP/USDT chart still shows a broader bearish structure after the token fell from above $2 earlier this year. Recent price action has stabilized near the lower end of that decline, but XRP has yet to recover the stronger resistance zones that would confirm a wider trend change.

The MACD shows limited improvement, with its histogram slightly above zero and the MACD and signal lines close together. This points to mild recovery pressure rather than strong bullish momentum. A sustained move above $1.12 could strengthen the short-term structure, while the $1.30 to $1.40 region remains a larger hurdle.

XRP price chart, source: crypto news

Crypto analyst Crypto Patel said XRP had entered a high-confluence resistance area following a bearish market structure shift. He identified a bearish order block, fair value gap and breakdown retest around the current price area.

Patel said the bearish setup remains active while XRP stays below $1.12. His downside targets sit at $1.058, $1.013, $0.95 and $0.90. The levels represent a technical scenario rather than guaranteed future prices.

Analysts remain cautious despite XRP rebound

Cryptorphic also warned that XRP’s short-term structure continues to favor sellers. The analyst wrote that “lower levels seem likely as long as $1.08 remains resistance.” XRP has since moved above that level, making $1.12 the next immediate test for the recovery.

A close above $1.12 could weaken the bearish setup and allow buyers to challenge higher resistance. Failure to hold the recent rebound would return attention to $1.058 and the broader $1.00 to $1.06 support zone.

Notably, XRP recently faced persistent selling pressure on Binance while struggling below $1.08. Negative spot order flow had kept sellers in control even as social sentiment remained heavily bullish.

The latest rebound has improved the immediate price picture, but XRP still needs stronger buying volume to confirm that the previous selling pressure has eased. Recent crypto.news analysis identified $1.00 to $1.06 as the main support zone and $1.18 to $1.20 as the larger resistance range for July.

$50 XRP scenario depends on massive crypto market growth

Under that assumption, XRP could theoretically trade near $50.10. A 1% market share would imply about $16.01 per XRP, while 5% would produce a value near $80.08. Moon Lambo stressed, “I’m not making a prediction.”

The scenario depends on the entire crypto market growing to $100 trillion while XRP retains the assumed market share. Changes in circulating supply and market dominance would also alter the calculation.

For the near term, the market remains focused on much closer levels. XRP must hold above the recent recovery zone and clear $1.12 before testing the $1.18 to $1.20 resistance area. Failure to maintain the rebound could place $1.058 and $1.00 back in focus as sellers attempt to regain control.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Actor and cryptocurrency critic Ben McKenzie has taken his campaign against the Digital Asset Market Clarity Act to Capitol Hill as the legislation approaches a possible Senate vote.

Summary

- Ben McKenzie lobbied senators against the CLARITY Act as lawmakers prepare for possible floor action.

- His campaign joins Democratic calls for stronger ethics rules covering President Trump’s growing cryptocurrency interests.

- The bill needs sixty Senate votes, making bipartisan support essential before lawmakers leave for recess.

McKenzie spent Tuesday meeting with lawmakers and joined Democratic senators at a Capitol Hill press conference opposing the CLARITY Act. The former The O.C. actor argued against legislation that he and other critics say lacks adequate consumer protections and government ethics rules.

McKenzie joins senators opposing CLARITY Act

McKenzie appeared alongside Senators Chris Murphy, Jeff Merkley and Chris Van Hollen, as well as representatives from Americans for Financial Reform and Indivisible. The group called on senators to reject the current bill unless lawmakers address their concerns.

The opposition centers partly on President Donald Trump’s financial ties to digital assets. Critics have called for restrictions preventing senior government officials and their families from benefiting financially from industries they oversee. The White House has rejected allegations of improper conflicts and has argued that ethics rules should apply equally to officials rather than target the president specifically.As previously reported, the ethics dispute has become one of the main barriers to securing the Democratic votes needed for passage.

Actor has become a prominent crypto critic

McKenzie is best known for playing Ryan Atwood in The O.C. and later appearing in Southland and Gotham. In recent years, he has become an outspoken critic of cryptocurrency markets, celebrity token promotions and claims that blockchain technology can remove the need to trust financial intermediaries.

His work has included interviews with investors, industry critics and former FTX CEO Sam Bankman-Fried. McKenzie has argued that software cannot fully remove human control from financial systems, pointing to failures at centralized crypto companies as examples of why management and oversight still matter.

His latest lobbying effort moves that campaign directly into the legislative debate. A social media post documenting his Capitol Hill activity showed McKenzie participating in the campaign against the market structure bill.

CLARITY Act faces a narrowing Senate window