Crypto World

Ulta Beauty (ULTA) Stock Plunges 10% Post-Earnings: Is This a Buying Window?

Key Takeaways

- Shares of Ulta Beauty tumbled over 10% following its Q4 earnings release, pressured by conservative fiscal 2026 projections and a modest bottom-line shortfall

- The company’s Q4 earnings per share of $8.01 exceeded both internal projections and analyst consensus, while sales reached $3.90B, marking an 11.8% year-over-year increase

- Comparable store sales climbed 5.8% in Q4, with positive momentum across all primary product segments

- Fiscal 2026 comp sales outlook of 2.5%–3.5% fell short of Street expectations, with management signaling flat operating margin performance ahead

- The beauty retailer announced a $1 billion share repurchase program for this year; institutional shareholders control 90.39% of shares, while analyst consensus leans “Moderate Buy” at $671.27 price target

Ulta Beauty delivered what would typically be considered a strong fourth-quarter performance, yet investors fixated on softer full-year projections and a minor earnings shortfall against elevated expectations. Shares plummeted more than 10% following the earnings announcement, extending losses to approximately 19% since Barron’s recommended the stock less than 30 days prior.

The beauty retailer reported Q4 earnings of $8.01 per share, surpassing the consensus forecast of $7.93 by eight cents. Top-line results reached $3.90 billion, representing an 11.8% year-over-year improvement and exceeding analyst projections of $3.81 billion. Gross profit margins also came in ahead of estimates. What triggered the selloff? Earnings missed certain higher-end projections, and the company’s fiscal 2026 outlook proved more conservative than investors anticipated.

For the current fiscal year, management projected comparable sales expansion of 2.5% to 3.5% — landing below Wall Street’s midpoint expectations — while signaling operating margins would remain essentially unchanged. Elevated marketing expenditures, rising incentive-based compensation, and strategic reinvestment initiatives are compressing profitability. The company also faces more challenging year-over-year comparisons following a robust FY25 performance.

With a new chief financial officer recently appointed, the measured guidance approach may reflect fresh leadership caution. Raymond James analyst Olivia Tong observed that the conservative stance aligns with Ulta’s traditional guidance philosophy, potentially reinforced by current macroeconomic and geopolitical uncertainty.

Wall Street Moderates Targets While Maintaining Support

Though the market’s response was severe, few analysts issued downgrades. UBS maintained its “buy” recommendation with an $810 price objective. William Blair analyst William Carden suggested the sharp decline “could reverse quickly” following the reset of 2026 expectations around stable margins. TD Cowen’s Oliver Chen emphasized Ulta’s “low-to-luxe” product range as an enduring competitive advantage.

Overall analyst sentiment remains at “Moderate Buy,” comprising 15 Buy ratings, 10 Hold recommendations, one Strong Buy, and a single Sell rating. The consensus price target stands at $671.27, compared to Monday’s opening price of $535.72 — suggesting substantial upside potential if operational execution meets projections.

Zacks Investment Research shifted its rating from “Strong Buy” to “Hold” in February, ahead of the earnings release. Jefferies, which initiated coverage in January, maintains a “Hold” stance with a $700 target.

Institutional Investors Increasing Stakes

Despite the post-earnings turbulence, several institutional investors expanded their holdings. Holocene Advisors LP increased its ULTA position by 339.6% during Q3, acquiring an additional 293,516 shares for a combined stake valued at approximately $207.7 million. Focus Partners Wealth, Intech Investment Management, and multiple other institutional funds similarly added exposure in recent quarters.

Institutional ownership currently represents 90.39% of outstanding shares.

The company’s Q4 comparable sales growth of 5.8% compares favorably against flat performance in Kohl’s Sephora partnership. Digital channels continue gaining traction, with artificial intelligence-powered personalization identified as a key catalyst. The retailer also plans to introduce a curated TikTok Shop presence, aiming to capture younger demographic segments.

Ulta’s 52-week trading range spans from $323.36 to $714.97. Monday’s opening price of $535.72 sits notably below the 50-day moving average of $665.60 and the 200-day average of $587.65.

Management established fiscal 2026 EPS guidance at $28.05–$28.55, compared to the current analyst consensus of $23.96 for the period.

The relationship between Bitcoin and US dollar–denominated liquidity is shaping how crypto markets behave in 2026. According to Sam Lyman, head of research at the Bitcoin Policy Institute, the coexistence of BTC with dollar-backed stablecoins like USDT has become a mutually reinforcing dynamic that benefits both sides of the ecosystem. In practice, the leading BTC trading pairs are anchored in USD, a reality that helps sustain demand for dollar liquidity even as crypto markets expand globally.

More than a simple trading pattern, the dynamic sits at the intersection of market structure, regulation, and geopolitics. Lyman argues that the BTC-dollar relationship mirrors the broader role the dollar plays in commodity and macro markets — a framework that has long been embedded in the way crypto trades are priced and settled. In his view, Bitcoin’s strongest leverage point remains its liquidity expressed in dollars, which challenges the notion that BTC could undermine the dollar system. The observation is supported by data showing the dominance of dollar-based markets for Bitcoin, a trend that Kaiko highlighted in its 2024 analyses of on-chain and off-chain activity.

Key takeaways

- Bitcoin’s liquidity core is anchored to USD trading, with BTC/USD pairs supported by stablecoins like USDT that maintain dollar-denominated rails for buyers and sellers.

- Regulatory direction in the United States — notably GENIUS Act-aligned stablecoin policy — could shape how dollar-pegged tokens operate within crypto markets without sacrificing the dollar’s role in liquidity provision.

- China’s stance remains a paradox: while Beijing reiterates a ban on permissionless crypto activity and push for a CBDC, Chinese mining pools still command a sizable share of global hashrate, underscoring control dynamics beyond formal prohibitions.

- The rise of the digital yuan and capital controls continue to influence cross-border flows, illustrating how policy choices in major economies can impact crypto market structure and risk exposure for miners and validators.

- Investor and builder attention should focus on regulatory clarity, mining geography shifts, and the evolving balance between centralized fiat rails and permissionless borderless networks.

The dollar–Bitcoin nexus in a changing regulatory and geopolitical landscape

At the heart of the current narrative is the “symbiotic” relationship between Bitcoin and dollar liquidity. Lyman notes that the largest BTC trading pair remains USD-based, a reality that makes dollar stability and regulatory certainty influential for crypto markets. Stablecoins pegged to the dollar, particularly USDT, act as a bridge for traders seeking quick exposure to BTC without stepping into traditional bank rails. This arrangement creates a feedback loop: as more capital flows into dollar-denominated BTC markets, the dollar’s role in crypto deepens, and stablecoins gain further prominence as liquidity vehicles.

The discussion around stablecoins is not purely technical; it sits squarely within a regulatory framework that currently anchors many of the market’s most important rails. Advocates of prudent regulation argue that stablecoins, if backed by robust reserves and transparent governance, can provide stable liquidity channels that bolster market depth and resilience. In this framing, policy proposals such as the GENIUS Act aim to codify oversight and guardrails for stablecoins. For observers and participants, the question is not whether stablecoins are here to stay, but how the rules of the road will shape innovation, settlement speed, and cross-border payments in the crypto economy.

On the data side, independent researchers have flagged the dollar’s dominance in BTC markets in 2024, with analyses from Kaiko illustrating the extent to which dollar-based trading pairs anchor liquidity. This backdrop matters for traders who rely on predictable settlement assets, and it informs long-term bets on infrastructure that underpins dollar-denominated trading, such as stablecoin liquidity pools, exchange markets, and on-chain custody solutions.

Policy, control, and China’s ongoing paradox

Policy tensions also extend beyond the United States. China has repeatedly framed Bitcoin and stablecoins as threats to the country’s capital controls, a central feature of its economic management. Lyman emphasizes that Beijing’s approach reflects a broader objective: to keep financial activity within the country’s regulatory perimeter while guiding capital flows through a state-backed mechanism. In 2025, China reaffirmed its stance on stablecoins even as it advances a separate digital yuan project designed to exert tighter control over foreign exchange and capital movements.

Yet regulatory bans have not eliminated crypto activity in practice. While China maintains a blanket ban on Bitcoin mining and other permissionless crypto activities, mining pools within the country continue to represent a substantial portion of the global hashrate. Hashrate Index places Chinese pools at more than 36% of the worldwide hashrate, underscoring a disconnect between formal prohibitions and actual network participation. The outcome is a nuanced mining map: a political impulse to restrict is in tension with economic incentives and cross-border capital flows that crypto miners leverage wherever policy allows.

These dynamics intersect with the broader push toward a centralized, programmable digital currency framework. The CBDC landscape, led by China’s digital yuan, is often cited as a tool for precision control over capital movements and monetary policy transmission. Proponents argue CBDCs can offer programmable features that improve settlement efficiency and cross-border interoperability, while critics warn they could erode financial privacy and curb the openness that has driven permissionless innovation in crypto markets.

What investors and builders should watch next

As policy debates evolve in the US and abroad, the crypto market stands at a crossroads where liquidity, regulatory clarity, and governance will shape momentum more than any single price move. The dollar-centered liquidity regime is likely to persist in the near term, reinforcing the role of dollar-denominated stablecoins as the primary conduit for BTC trading. For investors, the key questions relate to how changes in stablecoin regulation could affect market depth, settlement speed, and counterparty risk in major exchanges and over-the-counter desks.

From a construction and infrastructure perspective, the ongoing emphasis on stablecoin resilience, transparent reserve management, and compliance will influence which platforms gain network effects. Traders and institutions may prioritize products and services that align with GENIUS Act principles—namely, clarity around custody, reserve standards, and reporting—without compromising the efficiency that makes USD-based crypto liquidity compelling.

On the geopolitical front, observers should monitor how the CBDC push interacts with global capital flows and whether central banks will pursue interoperability initiatives that either complement or complicate existing crypto rails. The tension between centralized, programmable fiat and permissionless networks will continue to shape debates about financial sovereignty, market accessibility, and the future of cross-border payments.

For now, the market appears to be navigating a period of regulatory refinement and strategic repositioning. The next few quarters will test how well dollar-denominated liquidity and stablecoins can adapt to evolving rules and shifting mining geographies, while the ongoing CBDC experiments and capital-control policies will help illuminate the long-term balance between centralized control and decentralized finance.

Readers should watch for updates on GENIUS Act developments and any concrete regulatory guidance around stablecoins, as well as continued data on mining geography and hashrate distribution. These factors will shape liquidity availability, market depth, and the resilience of the BTC ecosystem as it matures within a complex regulatory and geopolitical landscape.

Community Banks Increase Compliance Issues

The Independent Community Bankers of America has been critical of the application and its compliance framework has been challenged. The group stated that the proposal does not meet required standards on risk management and profitability. Also, banks claimed that crypto companies must be subject to the same stringent regulations as their conventional counterparts. Bank representatives emphasized that companies cannot be given charter benefits without being regulated in full. They cautioned that unequal requirements might pose dangers to customers and the institutions. In addition, this issue is symptomatic of a broader conflict between digital asset companies and traditional financial organizations.

Nevertheless, Coinbase declared that it is not interested in being a traditional bank. The company stated that the charter of the trust would facilitate custody services and not deposits or lending. In addition, it seeks to enhance legal safeguards and facilitate financial activities that are under federal supervision. The National Community Reinvestment Coalition also protested against the approval and had concerns about the public interest. Its representatives claimed that the action would allow access to federal systems without fulfilling greater duties. They also referred to threats associated with previous enforcement measures and cybersecurity attacks.

Americans for Financial Reform Education Fund also commented on the decision and cautioned against risks to financial stability. The group raised issues related to fraud, money laundering, and market volatility in relation to crypto activities. Therefore, the charter’s revision continues to be debated in policy circles. Simultaneously, Coinbase continues to oppose regulations proposed by the US Securities and Exchange Commission concerning tokenized securities. The company argued that these restrictions could inhibit innovation and run contrary to how the market actually operates. Additionally, this conflict adds another dimension to its regulatory participation. The struggle between Coinbase and US banks underscores growing tension over crypto companies’ entry into the financial system.

James Wynn, the high-leverage crypto trader known for turning $7,600 into $25 million on PEPE, warned traders that markets will deteriorate further before recovering. Wynn outlined a multi-asset defensive strategy, shorting US equities and going long on oil while selectively buying Bitcoin (BTC) dips with spot capital.

All these is amid the US President Donald Trump’s fiery geopolitical message on Sunday against Iran and the Strait of Hormuz.

James Wynn’s Macro Bets and the Iran Factor

The trader’s positioning reflects a broader macro thesis tied to geopolitical escalation. James Wynn said he is short the S&P 500 and Nasdaq, long on WTI crude oil, and accumulating BTC on pullbacks.

He also flagged positive expected value in the Singapore dollar, Chinese yuan, euro, and British pound. He expects gold to hold its price or reach new all-time highs soon.

On real estate, Wynn acknowledged his own exposure to the sector, calling it a losing position while stressing the importance of diversification.

His strategy aligns with the current geopolitical environment. President Donald Trump gave Iran a 48-hour ultimatum on Truth Social, threatening to strike power plants and bridges if Tehran does not reopen the Strait of Hormuz by Tuesday.

Iran has kept the Strait effectively closed since the US-Israel military operation began on February 28, disrupting roughly 20% of the world’s oil supply.

Low Liquidity Wicks and Liquidation Hunts

Separately, James Wynn warned about Bitcoin price action. He flagged a Sunday manipulation wick on BTC that occurred during low trading volume, calling it further proof of what is coming next.

“Another classic low-volume manipulation wick on Bitcoin on a Sunday further proves what’s about to come,” he indicated.

Indeed, a $1,000 BTC price pump within 10 minutes on Sunday liquidated $28 million in short positions in a single hour, amid continued low-liquidity leverage hunting.

BTC is trading near $67,201 as of this writing, with the Fear and Greed Index stuck at 12, deep in extreme fear territory. The token has held a $65,000 to $73,000 range for weeks despite sustained bearish sentiment.

With Trump’s self-imposed Tuesday deadline approaching and oil prices hovering above $100 per barrel, the macro backdrop for risk assets remains volatile.

The post James Wynn Reveals His Defensive Play Amid Trump’s Fiery Iran Message appeared first on BeInCrypto.

Polymarket has removed a betting market tied to the rescue of U.S. service members in Iran, after intense backlash and criticism from lawmakers this weekend.

The market allowed users to wager on when the U.S. would confirm the rescue of two airmen after an F-15E fighter jet was shot down over Iran. The crew members have since been rescued.

Rep. Seth Moulton, a Democrat from Massachusetts, criticized the listing in a post on X, calling it “disgusting” and arguing it reduced a military rescue effort to a financial trade.

Moulton has taken a hard line on prediction markets, recently banning his staff from using platforms such as Polymarket and Kalshi over concerns that financial incentives could influence policy decisions.

A Polymarket spokesperson said the listing did not meet its integrity standards removed shortly after it appeared. The company added that it is reviewing how the market passed internal safeguards.

The incident comes as prediction markets face rising pressure in Washington. A group of congressional Democrats last month introduced legislation that would ban contracts tied to elections, war and government actions.

Separately, several senators have urged the Commodity Futures Trading Commission to prohibit markets linked to individual deaths, citing national security concerns.

Regulators are also asserting authority over the sector. The CFTC said this week it filed lawsuits against three states over efforts it believes attempt to bypass federal oversight of prediction markets.

Industry scrutiny has expanded beyond politics. The NFL has asked operators to avoid offering contracts it views as objectionable or open to manipulation, including bets tied to officiating decisions or events known in advance.

Still, the market is expanding. Kalshi has late last month secured a license to offer margin trading to institutional investors, while new players are entering the market. Among them is JPMorgan, whose CEO, Jamie Dimon, has signaled that it is looking to enter the fray.

Latest Acquisitions Drive Overall Holdings To Greater Heights

The recent purchase comes after a huge one announced last week. Bitmain has already accumulated more than 71,000 ETH, boosting total holdings to more than 4.7 million ETH. It now holds nearly 4 percent of the total Ethereum supply. The company still aims to own five percent of Ethereum’s supply in the market. In addition, the strategy signals a long-term accumulation plan that targets market positioning. The aggressive buying has, however, exposed it to price volatility.

Statistics indicate that Bitmain has a large unrealized loss on its Ethereum investment at present. The average purchase price is above current market rates, which has impacted portfolio value. This puts the firm under pressure as market conditions remain uncertain. Since the beginning of the year, Bitmain’s stock has fallen more than 30 percent. Nonetheless, it posted a small profit in the last week along with a slight uptick in Ethereum’s price. Moreover, this movement suggests a more favorable mood even amid ongoing geopolitical threats.

According to Tom Lee, the company will continue purchasing at current levels despite the unstable markets. He explained that the plan rests on optimism about the broader economic outlook. Therefore, current pricing is seen as an opportunity rather than a risk for the firm. Lee noted that present oil prices are lower than historical highs when adjusted for inflation. He compared current levels with those observed in previous market cycles. He added that this analogy supports the belief that the economy can sustain higher energy prices.

Notably, the leading cryptocurrencies have remained relatively stable even amid geopolitical tension. Both Bitcoin and Ethereum have avoided further losses during the recent conflict period. Consequently, Bitmain is still consolidating its assets in line with the long-term plan.

Bitcoin price now reflects capital inflows over halving cycles. Institutional adoption reshapes Bitcoin’s long-term market behavior. Credit systems and banks now influence Bitcoin growth trajectory. Bitcoin traded near $68,000 as market structure signals a major shift in price drivers. Michael Saylor said the four-year cycle no longer defines market behavior. He added that capital flows now guide Bitcoin’s direction across global financial systems.

For years, traders linked price growth to halving events that reduced mining rewards. Saylor now rejects that model and points to structural market evolution. As a result, Bitcoin’s role continues to expand beyond its early speculative phase.

Institutional adoption continues to reshape demand patterns across regulated financial platforms. Large firms now integrate Bitcoin into treasury strategies and financial products. Consequently, the asset reflects broader economic forces instead of isolated supply shocks.

Capital Flows Replace Halving Cycles

Saylor emphasized that capital movement now determines Bitcoin price trends in modern markets. He linked this shift to increased access through banks and digital credit systems. Liquidity conditions now influence price behavior more than programmed supply changes.

Financial institutions have expanded Bitcoin access through structured investment products. These platforms allow broader participation from corporate and traditional finance sectors. As a result, capital inflows and outflows now drive short-term and long-term price movements.

Analysts now focus on fund allocation trends rather than historical halving timelines. This shift reflects a deeper connection between Bitcoin and global financial systems. Consequently, Bitcoin responds more directly to macroeconomic conditions and liquidity cycles.

Institutional Adoption Redefines Market Structure

Traditional finance has increased its involvement in Bitcoin through custody, trading, and reserve strategies. This participation has improved liquidity while stabilizing extreme price swings over time. Institutional demand now plays a central role in shaping market direction.

Companies continue to build services that integrate Bitcoin into regulated financial ecosystems. These developments expand access and improve trust among large-scale participants. Bitcoin gains recognition as a global digital capital asset across multiple sectors.

The asset now appears in portfolios alongside traditional financial instruments. This integration reflects growing acceptance across banking and corporate environments. Consequently, Bitcoin’s valuation aligns more closely with broader capital market dynamics.

MicroStrategy Strategy Fuels Ongoing Debate

MicroStrategy remains a focal point in discussions about institutional Bitcoin accumulation strategies. The company built a large Bitcoin position through consistent and aggressive purchases. Therefore, it holds a unique position within the evolving digital asset landscape.

Market commentator Adam Livingston noted that early accumulation created a strong competitive advantage. He suggested that replicating such a strategy now requires significantly higher capital. As a result, few firms can match the company’s scale and timing.

At the same time, this approach continues to influence corporate treasury strategies worldwide. Firms now evaluate Bitcoin as a reserve asset within diversified portfolios. Consequently, MicroStrategy’s model remains central to discussions about institutional adoption.

Michael Saylor, Executive Chairman of Strategy (MicroStrategy), hit back at Peter Schiff after the goldbug posted data suggesting Bitcoin (BTC) had lagged gold, silver, and equities over five years.

The exchange reignited a long-running public feud between two of the loudest voices on opposite sides of the Bitcoin-versus-gold divide.

Schiff’s Five-Year Window and Why It Matters

Schiff highlighted Bitcoin’s measly 12% gain over the past five years, comparing that figure to the NASDAQ’s 57.4% gain, the S&P 500’s 59.4% rise, gold’s 163% surge, and silver’s 181% rally.

“If the appeal of Bitcoin is its superior long-term performance, why should anyone keep HODLing it?” posed Schiff.

The five-year window he cited begins near April 2021, when BTC traded close to its then all-time high of approximately $69,000.

That starting point captures both the 2022 crypto crash and the slower 2024-2026 recovery. As of this writing, BTC trades for $66,847.

Gold, meanwhile, has surged above $4,700 per ounce. That represents a gain of over 160% from its April 2021 level near $1,780, confirming Schiff’s figures.

The precious metal hit an all-time high of $5,602 in late January 2026 before pulling back amid broader macro volatility tied to the Iran conflict and rising inflation expectations.

Schiff followed up with a separate post targeting Strategy directly. He noted that MSTR stock had outperformed the NASDAQ, gaining 68.5% over five years, but argued the rally had nothing to do with BTC’s performance.

“It’s due to investors’ willingness to overpay for MSTR so Saylor could keep overpaying for Bitcoin. Sell MSTR before it crashes,” warned Schiff

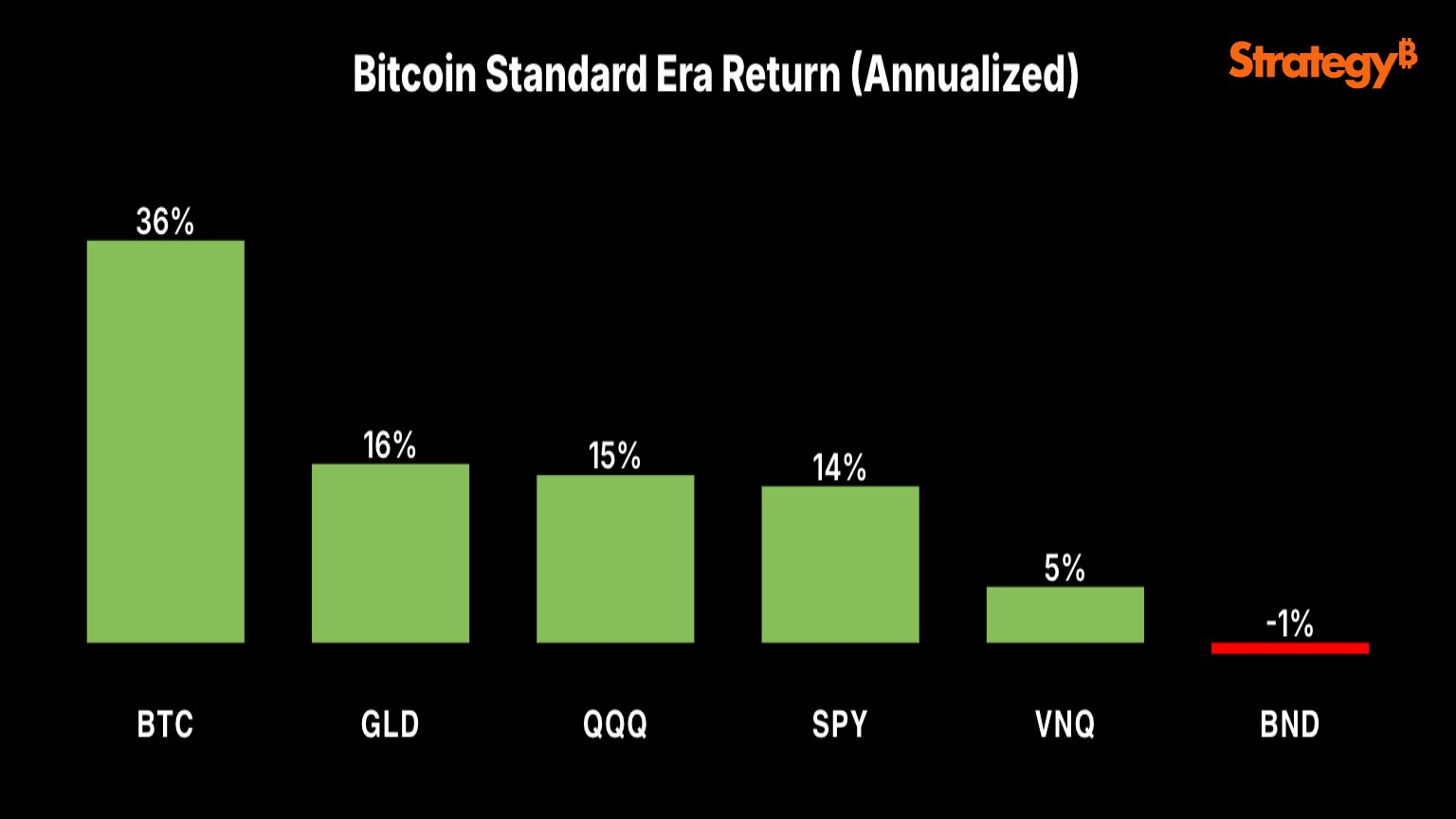

Saylor Responds With Annualized Returns

However, according to Michael Saylor, Schiff’s analogy is flawed. Saylor measured Bitcoin’s performance from August 2020, the month Strategy began its corporate BTC treasury strategy.

With this, the Bitcoin believer highlighted BTC annualizing at 36%, compared to 16% for gold (GLD), 15% for the Nasdaq-100 (QQQ), 14% for the S&P 500 (SPY), 5% for real estate (VNQ), and negative 1% for bonds (BND).

“Timeframes matter. Since Aug 2020, Bitcoin has been the top-performing major asset, and it’s not even close. Zoom out further, and the gap only widens,” Saylor challenged.

Strategy held 762,099 BTC as of this writing, making it the largest corporate holder of the cryptocurrency. The company acquired its holdings at an average price of roughly $75,699 per coin, putting its position below break-even at current spot prices.

A Familiar Feud With Higher Stakes

The Schiff-Saylor rivalry has become a recurring feature of crypto commentary. Schiff has called Strategy’s business model a “fraud” and predicted the company would eventually go bankrupt.

In December 2025, he challenged Saylor to a public debate at Binance Blockchain Week in Dubai. Saylor did not accept.

However, Schiff and CZ, the founder and former CEO of Binance, recently debated on the same topic, Bitcoin versus gold, with the outcome exposing a core divide between gold-backed stability and crypto innovation.

The post Michael Saylor Exposes the Fatal Flaw in Peter Schiff’s Anti-Bitcoin Argument appeared first on BeInCrypto.

Crypto World

Bitcoin Price Prediction: OCC Grants Crypto Bank Charter as Pepeto Targets 100x While ETH and XRP Hold

Bitcoin price prediction shifted this week after the OCC granted conditional approval for the biggest US crypto exchange to become a federally regulated trust bank, pulling digital assets deeper into the traditional banking system.

While the wider market has cooled with major coins pulling back, Pepeto stands out as the top presale entry with its Binance listing getting closer every day.

With a working exchange already live and $8.68 million raised, Pepeto combines real technology with a presale that analysts see running 100x once the listing opens, making it the play that the next rally is about to reward.

The OCC gave Coinbase conditional approval for a national trust bank charter on April 2, placing the largest US crypto exchange under direct federal oversight, according to CoinDesk.

The charter lets Coinbase handle custody services across all 50 states under one set of rules instead of juggling separate state licenses, according to Bitcoin Magazine. Pension funds and sovereign wealth funds often need bank-grade oversight before moving capital into crypto, and this approval knocks down one of the last walls.

The biggest stamp of trust in crypto history just dropped, and the presale entries set to ride that wave are where the real gains live.

Pepeto: The Presale Where 100x Lines Up as the Bitcoin Price Prediction Turns Bullish on Federal Backing

While the CLARITY Act sits stuck in committee, the direction is obvious, and sharp traders are hunting for the best entries to catch the recovery forming underneath.

Pepeto ranks near the top because a live exchange with $8.68 million committed and a Binance listing closing in gives it everything needed to stand as one of the best plays of 2026.

The math speaks for itself. At $0.0000001862, analysts see 100x once the Binance listing opens. The person who created the original Pepe token, which hit $11 billion on hype alone, built this exchange with a veteran from Binance’s listing team. Every swap runs through PepetoSwap at zero cost, every cross-chain move between ETH, BNB, and Solana lands at full value, and every token gets flagged for scam patterns before your capital touches it, all verified clean by SolidProof.

What drives Pepeto daily is real utility, and 188% APY staking grows every position while the listing window gets tighter. The entries that turned early believers into millionaires in past cycles all shared one trait: they found a working project before the crowd showed up, and Pepeto at presale pricing is that exact setup right now.

Ethereum (ETH)

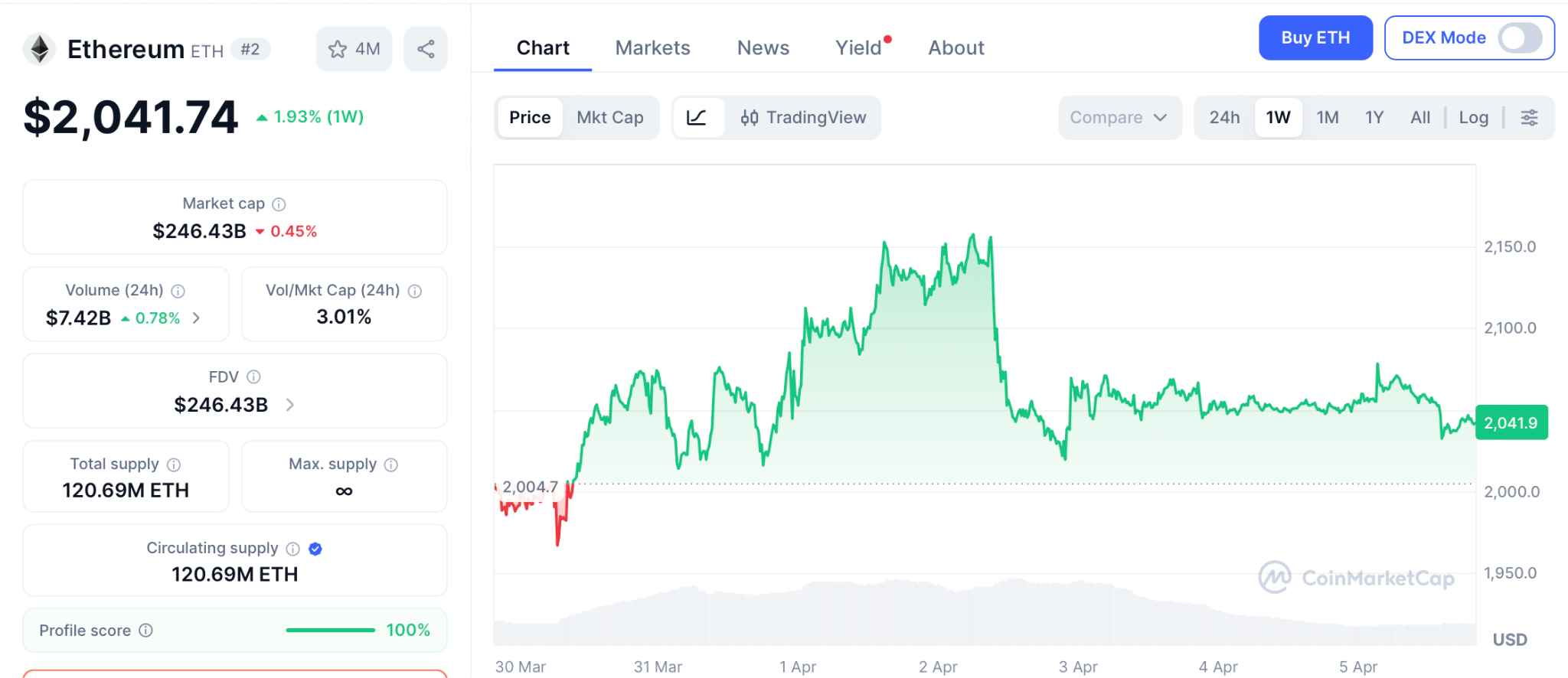

ETH trades at $2,041 per CoinMarketCap, holding just above the $2,000 floor as the broader rally has not yet carried altcoins higher.

Standard Chartered keeps a $7,500 year-end target, but from here that is a 3.6x over nine months, decent for big portfolios, while Pepeto at presale pricing targets 100x from a single listing event the Binance debut is set to kick off.

XRP

XRP trades at $1.29 per CoinMarketCap, drifting below key moving averages as sellers stay in control.

Standard Chartered recently cut its year-end call to $2.80, roughly a 2x that takes patience, but presale entries grab the multiples that XRP at an $81 billion cap can no longer produce.

Conclusion

The picture is forming fast and the math is simple. The OCC handing a federal bank charter to the largest US exchange means the bitcoin price prediction just got backed by the same system that watches over Wall Street. ETH at $2,041 targets $7,500 over nine months, a 3.6x that pays patience, and the investors who grabbed ETH at $0.30 turned $1,000 into $16,000 because they spotted a working platform at early pricing and moved.

The bitcoin price prediction shows early bull signals building while the presale window gets tighter by the day. Visit the Pepeto official website and secure your spot before this chance turns into a headline you read about instead of a gain you earned, because projects with real products, viral buzz, and a Binance listing on deck do not sit at presale prices for long.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the Coinbase OCC charter and how does it change the bitcoin price prediction?

The OCC gave Coinbase a federal trust bank charter, pulling crypto under Wall Street-grade rules. The bitcoin price prediction turns structurally bullish.

What are ETH and XRP targets next to the bitcoin price prediction?

ETH targets $7,500 by year end, XRP targets $2.80, and Pepeto targets 100x from the Binance listing. The Pepeto official website still takes entries.

Why is Pepeto the top pick as the bitcoin price prediction shifts bullish?

Pepeto has a live exchange, a SolidProof audit, $8.68 million raised, and 100x projected from the coming Binance listing.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

MicroStrategy, the largest publicly traded corporate holder of Bitcoin, appears set to resume BTC purchases this week. This comes after a brief pause that interrupted one of the longest buying runs in its treasury strategy.

On Sunday, Executive Chairman Michael Saylor resurrected his customary “Orange Dot” tracker on the social media platform X, posting the phrase, “Back to work.”

STRC Rebound Raises Odds of Another MicroStrategy Bitcoin Purchase

Notably, similar phrases have served as a highly reliable leading indicator for multi-million-dollar Bitcoin buy orders over the past several months.

MicroStrategy currently holds 762,099 Bitcoin, valued at more than $50 billion. Another purchase this week would extend that lead and further separate the company from every other listed firm holding the token on its balance sheet.

Meanwhile, the size of any new purchase has not been disclosed.

Still, market watchers following the company’s financing activity say the latest issuance tied to its STRC preferred stock may have restored enough buying capacity. That would be enough to fund the acquisition of at least 1,500 Bitcoin.

That would mark a reversal from the previous week, when STRC traded mostly below par and appeared to curb the company’s ability to raise fresh capital for additional Bitcoin purchases.

Meanwhile, the focus is shifting beyond the next headline purchase to the mechanics supporting it. STRC, one of the instruments used to finance the company’s Bitcoin strategy, pays a variable annualized dividend of 11.5% as of April 2026.

Since launch, STRC alone has financed the purchase of 50,792 Bitcoin. That has made the preferred stock an important part of the company’s broader funding structure as it continues to build what is already the largest corporate Bitcoin treasury in the market.

The strategy, however, continues to divide opinion.

MSTR supporters view the company’s financing model as a high-conviction way to accumulate Bitcoin at scale and tighten its identity as a proxy for the asset in equity markets.

However, critics argue the growing dividend burden tied to its preferred investors leaves the company more exposed if Bitcoin enters a sharp or prolonged downturn.

The post MicroStrategy May Resume Bitcoin Purchases as Saylor Revives ‘Orange Dot’ appeared first on BeInCrypto.

The Solana Foundation has launched a new developer toolkit aimed at bridging artificial intelligence with its blockchain network.

Last week, the Swiss-based non-profit organization introduced “Agent Skills” to allow AI programs to autonomously execute on-chain transactions.

AI Agents Payments Market Still Small

The open-source toolkit allows developers to install pre-built modules with a single line of code. This enables AI agents to handle automated tasks, process payments, and trade assets across the Solana network.

The foundation provided official modules for security and compatibility, alongside more than 60 community-contributed skills from major Solana ecosystem platforms like Jupiter Exchange, Raydium, and Helius.

However, the foundation noted that community-contributed tools are not officially endorsed. Users are warned that integrating autonomous AI agents with unvetted decentralized finance (DeFi) protocols carries inherent security risks, and inclusion in the toolkit does not imply a warranty.

The launch highlights the cryptocurrency industry’s broader push to capture the emerging market of “agentic payments.” These transactions are initiated and completed by AI without human intervention.

Last year, consulting firm McKinsey & Co. pointed out that more businesses will need to adapt to this AI-driven operating environment. According to the firm, this could create a $5 trillion market by 2030, encompassing retail, logistics, and commerce platforms.

Despite the rapid development of blockchain infrastructure tailored for AI integration, current market demand remains negligible, exposing a significant gap between technological capability and real-world adoption.

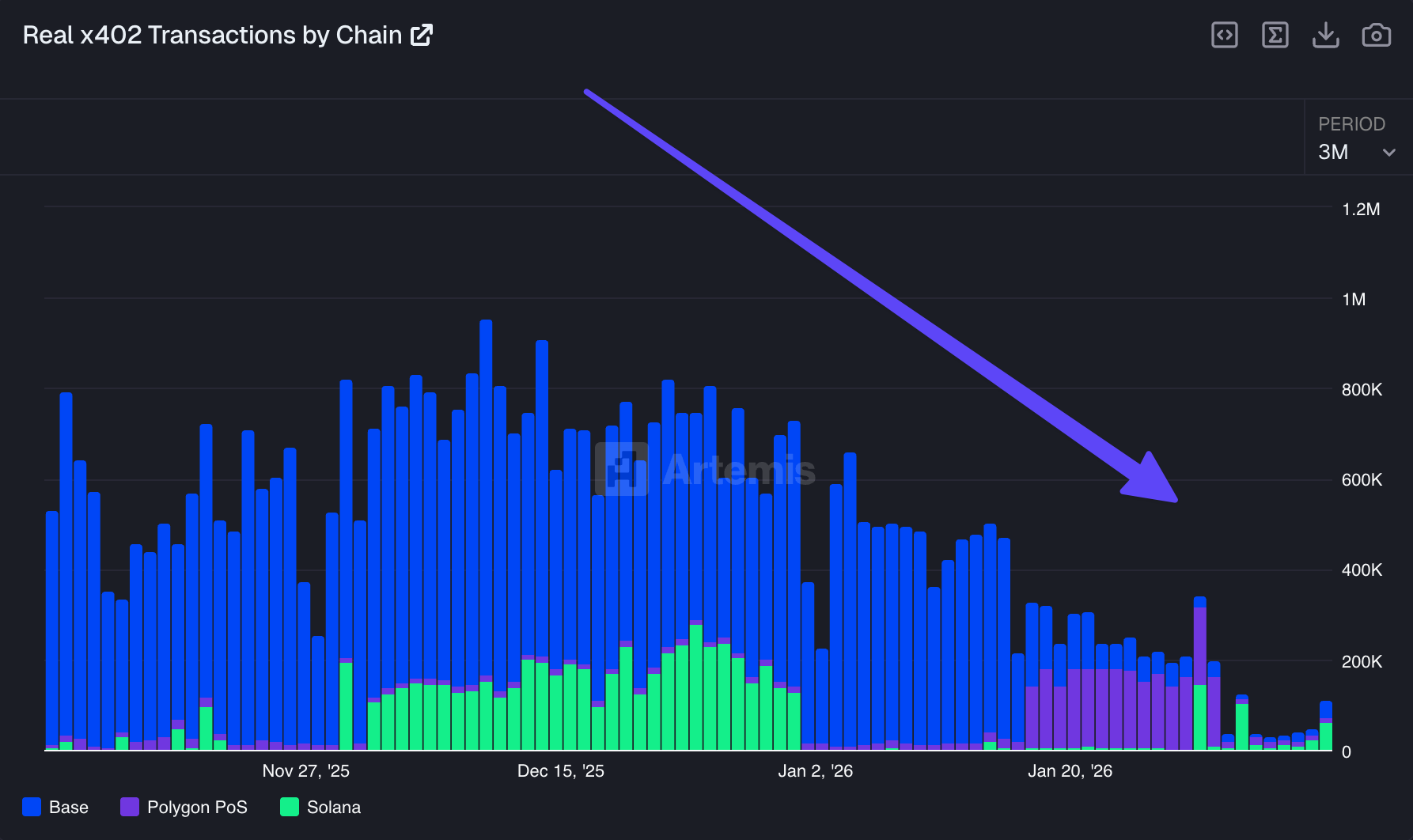

For example, x402, an existing agentic payment protocol, processed only about $24 million in volume during the last 30 days.

Furthermore, blockchain analytics firm Artemis pointed out that “x402 ‘agent payments’ boom is still mostly a mirage.” It noted that x402-related activities had collapsed from a peak of over 731,000 transactions per day in December to around 57,000 transactions per day in February.

This data underscores that while networks like Solana are building the rails for an AI-driven economy, the merchants and users required to sustain it have not yet arrived.

The post Solana Targets $5 Trillion AI Market With New Developer Toolkit appeared first on BeInCrypto.

Who to call if you see rats in your house or garden

Bitcoin and U.S. dollar form symbiotic bond, says BPI exec

Starfleet Academy’s Most Progressive Character Is Secretly Star Trek’s Most Offensive

-

NewsBeat3 days ago

NewsBeat3 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business3 days ago

Business3 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Spanx – Corporette.com

-

Entertainment6 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World4 days ago

Crypto World4 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech7 days ago

Tech7 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World5 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech7 days ago

Tech7 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Sports22 hours ago

Sports22 hours agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business4 days ago

Business4 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech6 days ago

Tech6 days agoApple will hide your email address from apps and websites, but not cops

-

Tech5 days ago

Tech5 days agoEE TV is using AI to help you find something to watch

-

Sports5 days ago

Sports5 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Politics6 days ago

Politics6 days agoShould Trump Be Scared Strait?

-

Tech6 days ago

Tech6 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Fashion6 days ago

Fashion6 days agoThe Best Spring Trends of 2026

-

Sports6 days ago

Sports6 days agoWomen’s hockey camp eyes fitness boost, tactics ahead of WC 2026 campaign | Other Sports News

-

Tech6 days ago

Daily Deal: StackSkills Premium Annual Pass

-

Tech5 days ago

Tech5 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Crypto World7 days ago

Crypto World7 days agoBitcoin’s Six-Month Losing Streak: What On-Chain Data Says About the Market’s Next Move

You must be logged in to post a comment Login