Crypto World

UNI cash flow token thesis

On July 12, Uniswap founder Hayden Adams posted a number that would have sounded like satire during the governance-token winter: the protocol is generating 5.2 million dollars in daily fees, more than any protocol in crypto other than the two giant stablecoins, and far more than the perpetuals and memecoin venues that dominated the fee leaderboard for the past two years.

Summary

- Uniswap is generating more than 5 million dollars in daily fees, driven largely by Robinhood Chain activity.

- Robinhood Chain recorded 500 million dollars in daily Uniswap volume within eight days of launch.

- The UNIfication program burns UNI against protocol fees, turning fee capture into supply reduction.

- The key question is whether Robinhood Chain volume remains durable after gas subsidies expire.

- UNI’s repricing depends on fee-switch votes passing, sustained volume, visible burns, and regulatory stability around tokenized equities.

DefiLlama’s independent count for the same 24 hours, 5.16 million dollars, backs him up. The source of the surge is the least crypto-native venue imaginable: Robinhood Chain, the brokerage’s new Ethereum layer 2, supplied roughly 4.38 million dollars of that daily total, dwarfing Ethereum mainnet at 296,000 dollars and Base at 288,000.

The volume statistics behind those fees arrived at a pace no layer 2 debut has matched. Within eight days of the July 1 launch, Robinhood Chain recorded 500 million dollars in daily Uniswap trading volume, a tenfold jump from the day before, making it the second largest network for Uniswap activity after Ethereum mainnet. Cumulative swap volume crossed 1 billion dollars by July 10. Across the first seven days, the chain generated 10.98 million of Uniswap’s 20.1 million dollars in total weekly fees. Daily active Uniswap traders surged to roughly 220,000, more than ten times the prior week. Adams described the network as the most active blockchain layer outside Ethereum mainnet itself.

And this is the part that turns a volume story into an investment thesis: for the first time in the protocol’s history, that fee firehose is being plumbed directly into the token. The UNIfication program, passed by the DAO in December 2025 with 125.34 million UNI in favor and a rounding error against, burns UNI against protocol fees on 11 chains. A snapshot vote that ran from July 7 to July 12 asked holders to extend the mechanism to v4 pools, with binding on-chain votes following the week of July 13. A parallel temperature check, running July 10 through 15, proposes switching on protocol fees for the Robinhood Chain deployment itself. If both pass, the loudest new fee source in DeFi connects to a supply-destruction machine, and UNI completes a conversion that the entire sector is attempting: from governance token to cash flow asset.

This feature examines the machine, the money, and the two serious objections, that the volume is subsidized and that the fee switch drives away the liquidity it taxes.

From governance token to burn machine: how UNIfication works

For five years, UNI was the emblem of a category problem. The token governed a protocol that processed trillions in cumulative volume and captured none of it; every basis point of swap fees flowed to liquidity providers, and UNI’s value proposition reduced to voting rights over a treasury and the perpetual promise of a fee switch that governance never dared flip. The token traded at 3.23 dollars on July 7 against a 2021 peak of 44.97, a 93 percent drawdown that priced the promise at roughly nothing.

UNIfication changed the architecture. Under the system live since December, protocol fees collected on each chain flow into contracts called TokenJar. Anyone who wants to claim the accumulated assets, in practice arbitrage searchers, must first burn an equivalent value of UNI. The burned tokens are bridged back to Ethereum and sent to the dead address, permanently removing them from supply. The design is deliberately mechanical: no dividends, no staking claims, no legal distribution to holders that might attract securities analysis, just a standing market operation that converts fee revenue into supply reduction at whatever pace trading activity dictates. The program already runs on 11 networks: Ethereum, Arbitrum, Base, Celo, OP Mainnet, Soneium, X Layer, Worldchain, Zora, BNB Chain, and Polygon.

The July votes address the two gaps in coverage, and the v4 gap is the technically interesting one. Uniswap v2 and v3 pools carry fixed fee tiers, so collecting a protocol share is a matter of setting one rate per pool. v4 is built around hooks, smart contract plugins that let developers customize pool behavior, including fees that can change block by block. Taxing something that mutable required new machinery: the proposal introduces a V4FeePolicy contract that determines the protocol fee for any pool and a V4FeeAdapter that collects and routes it into the burn pipeline. More than 1,500 builders are working with v4 hooks, and institutional-scale flow has already arrived, with Spark, the liquidity arm of Sky, pushing 1.5 billion dollars in stablecoin volume through v4 in the past month. The Robinhood Chain temperature check would extend fees across the v2, v3, and v4 deployments there, using the expedited governance track that UNIfication authorized for fee-parameter updates.

The market has started doing the arithmetic. UNI rallied about 21 percent from its July 1 low of 2.70 dollars to 3.30 by July 8, touched moves of 14 percent on the volume headlines, and trades near 3.63 with resistance mapped at 3.73. A 2 billion dollar market capitalization against a protocol annualizing north of 1.8 billion dollars in gross fees, if the July run rate held, is the kind of ratio that makes traditional investors reach for spreadsheets, with the enormous caveat that only the protocol’s share of fees, not the LP share, feeds the burn: in the measured 24 hours, protocol earnings were about 73,454 dollars against the 5.2 million gross, because the switch is not yet flipped on the newest and largest sources.

The distribution deal of the cycle

The reason the fee conversation suddenly matters is distribution, and the scale of what Robinhood connected deserves to be stated plainly.

Robinhood operates between 24 and 28 million funded accounts and posted record first-quarter revenue of 1.07 billion dollars. Its chain, built on Arbitrum’s stack with 100-millisecond blocks and full EVM compatibility, shipped with Uniswap v2, v3, v4, and UniswapX deployed from day one as the default liquidity layer. The flagship product is Stock Tokens: tokenized versions of more than 90 US equities and ETFs, tradable around the clock by eligible retail users in more than 120 countries, with Chainlink as the oracle layer, 1inch for routing, BitGo for custody, and Morpho powering a yield product on the USDG stablecoin. A trader in Manila can buy tokenized Nvidia exposure at 2 a.m. through Uniswap liquidity and settle instantly, no T+1, no market hours. Developers deployed more than 13,900 smart contracts in the first week. Ethena moved 50 million dollars into a Morpho vault in a single transaction, driving total value locked above 106 million dollars, up 159 percent in a day. Even the memecoin economy arrived on schedule, with Pump.fun integration and chain-native tokens amplifying volume, as crypto.news reported when the network crossed the 500 million dollar mark.

Standard Chartered’s head of digital asset research, Geoff Kendrick, argued the market was underpricing the partnership, calling it a real strategic alliance rather than a listing announcement. The structural point underneath his claim: DeFi protocols have spent years competing for the same recycled on-chain capital, and Robinhood represents something the sector has never had, a mainstream brokerage routing its retail flow through a decentralized venue by default. For Uniswap specifically, it means the protocol’s addressable market expanded overnight from crypto natives to anyone with a Robinhood account and a tokenized equity order, and the fee data shows the expansion is not theoretical. One venue, eleven days old, is out-earning Ethereum mainnet fifteenfold.

The rotation context makes the timing sharper. In a market where everything outside Bitcoin and Ethereum lost roughly 23 percent in six months, capital has crowded toward the handful of assets with verifiable revenue: perpetuals venues, stablecoin issuers, and now, abruptly, the largest DEX. The same repricing logic runs through the stablecoin wars, where volume quality has become the scoreboard, a shift crypto.news examined in the USDC-Tether flippening, and through Ethereum itself, which is rebuilding its entire execution roadmap around being credible settlement infrastructure for exactly this kind of institutional flow, the project crypto.news detailed in the Lean rebuild. UNI’s real revenue moment is one instance of a sector-wide migration from narrative to cash flow.

The comparables: what a fee-earning DEX token is worth

The rotation to cash flow gives UNI a peer group for the first time, and the comparisons cut in both directions.

The flattering comparison is to the fee leaders UNI just passed. Hyperliquid, Pump.fun, and the perpetuals venues built the template of the past two years: tokens with direct revenue linkage, aggressive buyback or burn mechanics, and valuations that survived the altcoin drawdown better than the governance-token cohort precisely because holders could point at income. Adams’ framing, more daily fees than anything except USDC and USDT, deliberately places Uniswap atop that leaderboard. On raw multiples, a 2 billion dollar capitalization against 20.1 million dollars in weekly gross fees puts the protocol at roughly two times annualized gross fees, a figure that looks absurd against any traditional exchange until the LP share is subtracted, at which point the multiple on actual protocol take becomes very large and entirely dependent on the pending votes. The valuation case is therefore not that UNI is cheap on current protocol revenue. It is that governance controls a dial connected to a gross fee stream of unprecedented size, and the July votes are the market’s first chance to watch the dial turn on the newest and largest sources.

The unflattering comparison is to the treasury-heavy tokens whose burns never outran their supply overhangs. UNI carries a circulating supply near 630 million against a total of 1 billion, with treasury and team allocations that dwarf any plausible near-term burn rate. At the current protocol take, the burn is symbolic; even at meaningfully higher fee capture, supply destruction measured in tens of millions of dollars annually meets a token with hundreds of millions of units yet to circulate. The burn thesis is a direction, not a floor, and direction gets repriced quickly when the underlying volume proves cyclical. The December UNIfication rally faded within weeks for exactly that reason: mechanics without volume are a press release. What is different now is that the volume arrived, from a source nobody’s model included, which is why the token’s 21 percent July move happened on the news of usage, not the news of tokenomics.

There is one more comparable worth naming because it frames the strategic stakes: the launch chain itself. Robinhood Chain’s opening fortnight has minted its own equity narrative, with HOOD shares up more than 40 percent in a month and insiders selling into the enthusiasm, and the network’s headline metrics, hundreds of millions in early volume against liquidity measured in the low tens of millions, drew immediate scrutiny about depth and durability. The tokenization trade rewards networks that convert launch attention into recurring activity, the pattern that has kept capital concentrated in venues with verifiable usage, as crypto.news observed when tokenized assets drove a rival network to record throughput. Uniswap is the venue where those questions get answered in public, block by hundred-millisecond block, because it is where the trades actually clear.

Objection one: subsidized volume is not revenue

The skeptics’ first argument is about the quality of the 500 million dollars, and it is not hand-waving.

Robinhood is waiving gas fees on the chain for the first 90 days. Zero gas removes the single largest natural brake on wash trading, incentive farming, and volume inflation; when round trips cost nothing, volume statistics measure enthusiasm for free transactions as much as demand for the assets traded. Analysts made exactly this objection in the launch week, noting that enormous AMM volume does not automatically create value for UNI without activated fee capture, and that if a meaningful share of the headline number reflects farming, the late-September expiry of the gas subsidy becomes the first genuine stress test of the entire thesis. The launch-week TVL data reinforces the concentration worry: a single Ethena deposit produced most of the day’s growth, and liquidity that arrives in one transaction can leave in one.

The honest response is that swap fees, unlike gas, were never waived. Every dollar of the 4.38 million in daily Robinhood Chain fees was paid by traders to liquidity providers at market rates, which makes the fee number a harder signal than raw volume. Wash trading a pool with a 30 basis point fee costs 60 basis points per round trip; nobody launders volume at that price for long. But the composition question survives the rebuttal: how much of the activity is durable tokenized-equity demand from Robinhood’s international base, and how much is launch-window speculation in memecoins and farmed incentives? The September subsidy cliff will answer it empirically. Until then, annualizing an eleven-day-old fee run rate is exactly the kind of extrapolation that DeFi cycles exist to punish.

There is also a counterparty concentration risk that has no precedent in Uniswap’s history: the protocol’s second largest venue is controlled by a publicly traded brokerage with its own regulatory exposure, its own commercial incentives, and, eventually, its own ability to route order flow elsewhere or deploy a competing AMM. Uniswap earned its position on Robinhood Chain by being the best liquidity software available on day one. Nothing guarantees the position is permanent, and the SEC’s January guidance flagging tokenized equity products for scrutiny means the flagship use case operates under a regulatory question mark of its own.

Objection two: the fee switch taxes the people who make the venue work

The second objection comes from inside the machine, and it is the oldest tension in the protocol’s design. Every dollar routed to the burn is a dollar that no longer goes to liquidity providers, the capital that actually fills the pools traders swap against.

Panoptic founder Guillaume Lambert put the LP case bluntly during the v4 vote, warning that applying the fee switch to v4 leaves providers with nowhere to migrate except competing AMMs or Uniswap forks, and that the proposal risks killing the protocol by favoring token holders over the capital that makes it function. The v4 version of the proposal sharpens his point, since reports around the vote indicated LP economics on affected pools could be reduced by as much as a third relative to the status quo. Liquidity is the most mercenary capital in crypto; it moved for 50 basis points of incentives throughout DeFi summer, and a protocol that taxes it while competitors do not is running a live experiment in how much brand and routing dominance are worth.

The bull rebuttal rests on what LPs actually get in exchange. Uniswap’s aggregated depth, its integration surface, the API now embedded in MetaMask, Zerion, and OKX routing across 18 plus chains with more than 3,000 developer keys issued, and now the Robinhood flow itself all mean an LP on Uniswap sees order flow that no fork can replicate. A fork with zero protocol fee but a fraction of the volume pays LPs less in absolute terms than Uniswap does after the tax. That was the empirical result of the vampire-attack era, and the UNIfication rollout across 11 chains has so far produced no measurable LP exodus. But v4 raises the stakes because hooks make pools programmable, and programmable pools are easier to replicate elsewhere; the fee controller architecture being voted on will tax precisely the segment of liquidity most capable of leaving. The vote closing July 12 and the on-chain sequence in the following week are, in effect, governance pricing that migration risk in real time.

The third mechanism: fee discount auctions

Alongside the burn expansion, Uniswap quietly shipped a second monetization primitive in the same week, and it deserves attention because it answers the LP objection from an unexpected angle.

Protocol Fee Discount Auctions, rolled out for the first time in early July, let sophisticated participants bid for reduced protocol fees on specific flow. The design logic runs like this: the largest source of LP pain in an AMM is not the protocol fee but adverse selection, the losses providers take when arbitrageurs pick off stale prices faster than pools can update. Auctioning fee discounts to the searchers and market makers who generate that flow converts a pure extraction into a priced privilege, captures for the protocol some of the value that MEV bots previously kept entirely, and gives high-volume participants a reason to route through Uniswap even after the fee switch activates. It is, in effect, a mechanism for taxing the taxers.

The auctions matter to the cash flow thesis for two reasons. First, they diversify protocol revenue beyond the flat fee share, adding a component that scales with the competitiveness of order flow, not raw volume, which is more durable through volume downturns. Second, they are a structural answer to Lambert’s migration warning: if the auction design succeeds in reducing the toxic share of flow that LPs absorb, providers could end up better off under the taxed regime than the untaxed one, because their gross fee cut shrinks while their adverse selection losses shrink faster. That claim is unproven and the mechanism is days old, but it reframes the fee switch debate from a zero-sum split between holders and LPs into an engineering question about who pays for price discovery. The December governance package, the v4 fee architecture, and the auctions together read as a coherent program: convert every form of value the protocol creates, swap fees, flow priority, and MEV, into revenue, then convert revenue into supply reduction.

The program’s ambition invites one more skeptical note. Every additional mechanism is additional surface area for governance capture, parameter mistakes, and the slow bureaucratization that has damaged other DAOs. A protocol that once had a single immutable design now has fee policies, adapters, controllers, auctions, and an expedited voting track, each a dial someone can turn. The bet is that Uniswap Labs and the delegate ecosystem can operate a genuinely complicated fiscal machine better than competitors can copy a simple one. The early revenue data supports the bet. The history of DeFi governance urges keeping the champagne corked.

What the UNI repricing actually requires

Assembling the pieces, the cash flow thesis for UNI needs four things to stay true simultaneously, and each has a visible checkpoint.

The votes must pass. The snapshot for v4 fees closed July 12; on-chain votes run the week of July 13; the Robinhood Chain temperature check closes July 15. The December UNIfication vote passed with near-unanimity, so the base case is passage, but the LP backlash around v4 is the loudest internal opposition the program has faced, and a diluted compromise on fee rates would proportionally dilute the burn.

The volume must survive September. The gas subsidy expires roughly 90 days after the July 1 launch. Fee revenue that persists through the cliff is real demand for tokenized equities and on-chain trading; fee revenue that evaporates was a marketing expense on Robinhood’s income statement. This is the single most informative scheduled event in the entire thesis.

The burn must be visible at scale. TokenJar mechanics mean supply reduction tracks protocol fee accrual with a lag. Watching claimed-and-burned totals over the coming quarter, rather than gross fee headlines, measures the machine’s actual throughput, and the gap between 5.2 million dollars gross and 73,454 dollars of current protocol take is the distance the switch still has to travel.

And the regulatory perimeter must hold. Tokenized equities traded by a global retail base through a brokerage’s chain sit at the intersection of securities law, the pending market structure bill, and the SEC’s tokenization scrutiny. The same institutional wave lifting fee revenue is also pulling DeFi into fights it has historically avoided, including the yield and revenue-sharing battles that banks are waging against crypto’s cash-flowing products, a conflict crypto.news has covered at the stablecoin layer. A token whose value accrues from fee capture is a token whose classification arguments get harder, not easier, which is presumably why the burn was engineered as supply destruction rather than distribution in the first place.

The remarkable thing about the past two weeks is not the volume record or even the fee record. It is that the oldest criticism of the largest DEX, that the token captures nothing, is being retired by governance vote in the same fortnight that the largest new fee source in DeFi history came online. Whether UNI at 3.63 dollars is cheap depends on September’s subsidy cliff, next week’s on-chain votes, and how much of a brokerage’s retail flow proves durable. Whether UNI is finally a claim on something is, for the first time since 2020, no longer the question.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Bitcoin traded near $62,600 on Tuesday, down 0.3% over 24 hours and roughly flat on the week, per CoinDesk data. The market is steady on the surface but the macro backdrop underneath it has turned.

President Trump reinstated the U.S. blockade of Iranian ships through the Strait of Hormuz and demanded a 20% fee on all other cargo moving through the waterway, reviving a conflict that a June peace deal had appeared to settle.

Brent crude rose as much as 2.8% to about $85 a barrel, its second day of gains, and traders lifted bets on a Fed rate hike.

That combination runs directly against crypto. Oil pushing higher feeds the inflation pressure that kept the Fed hawkish through June, and the easing of that pressure was much of what let bitcoin recover from its late-June lows near $58,000. The peace trade is now unwinding, and rate-hike odds are climbing back.

Bitcoin has spent a month between roughly $59,000 and $66,000, and the majors are mixed. Ether held near $1,783 and is up on the week, while Solana, XRP and Hyperliquid are all down 5% or more over seven days.

Today’s June inflation print is the more immediate test. A soft number would ease the rate-hike pressure the Iran news just revived. A hot one, especially with oil climbing, would stack a second hawkish signal onto the first, two weeks before the Fed meets July 28 and 29.

Most crypto brands disappear because they cannot make anyone feel the difference, not because their technology is weak, according to Jordi Urbea, CEO of Ogilvy Spain. He says sameness, not code, is the real killer.

Urbea spoke with BeInCrypto at the Ibiza Tech Forum 2026. He has spent 25 years helping brands stand out. His verdict on crypto marketing is blunt, and the data backs it up.

Every Crypto Brand Looks the Same

In an expert council interview with BeInCrypto, Urbea argued that crypto advertising has collapsed into one template. Swap the logo, he says, and the message barely changes.

“If you look at the crypto sector and all the advertising, the ads are exactly the same. You change the logo, and it’s the same.”

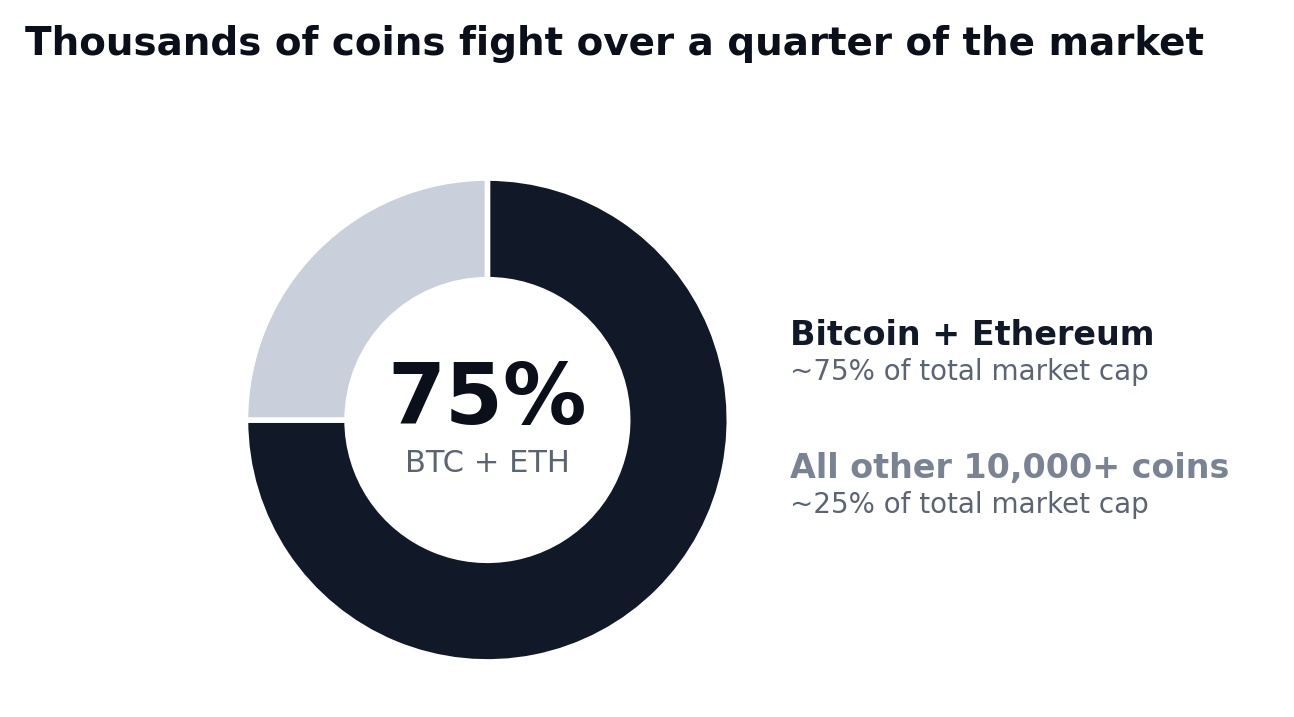

The numbers explain why sameness spreads so easily. Between 150 and 300 new coins launch every week, and roughly 10,700 remain active. Yet Bitcoin and Ethereum hold close to 75% of the total market value.

So thousands of near-identical projects compete for a shrinking slice of attention. In that crowd, a copied message vanishes on contact.

“It’s very strange to find one company that says, ‘This crypto is completely different.’ The rest are just repeating, message by message. And people say it’s boring, it’s all the same.”

Great Technology, No Story

For Urbea, the failure is rarely technical. He has watched strong projects die for a simpler reason.

“For many years I collaborated with many startups, and most of them disappeared because they couldn’t explain the difference between one brand and another. There are people with amazing technology and amazing ideas, but they don’t have the capacity to explain it.”

Startup data backs him almost exactly. CB Insights found the top reason companies fail is no market need, cited in about 42% of cases. Marketing and go-to-market problems account for a further large share.

Running out of money tops some lists at 70%, yet that is the final symptom. The root cause usually sits upstream, in a value no one managed to communicate.

Crypto shows the pattern at an extreme scale. More than 53% of all tokens launched since 2021 have already failed, and 2025 was the deadliest year on record.

Most of those projects were not undone by broken code. They simply never gave the market a reason to remember them.

The Follow-the-Leader Trap

Urbea believes imitation is the mechanism behind the sameness. Teams copy whatever seems to work for a rival.

“In some cases people repeat the formulas that work for others. ‘It goes well for that company, so I’ll repeat it.’ Follow the leader and repeat. But by the tenth message, your brand disappears, your message disappears, and you’re a big ship lost in the night.”

Marketing science adds a useful twist here. Byron Sharp and the Ehrenberg-Bass Institute argue brands grow by being distinctive rather than merely different, because buyers choose fast and rarely study fine detail.

That view sharpens Urbea’s point instead of breaking it. Copying rivals erases the distinctive assets, the voice, colors, and language that let a brand register at all. Without them, recall collapses.

The same logic haunts Web3 marketers who chase trends. When every campaign borrows the same hooks, none of them stick.

Building a Brand Nobody Can Copy

Jordi Urbea has a direct remedy. Stop borrowing formulas and build your own.

“If you create your space, you create your language, you create your own way to work. That is my humble advice.”

The payoff is measurable. Kantar analyzed 40,000 brands and found a strong link between relative uniqueness and the amount consumers are willing to pay. Distinctive brands command higher margins and lower price sensitivity.

Research also shows that fresh, varied advertising lifts recall, while repetition fades fast. A distinct voice is therefore an asset, not a cost.

For crypto founders, the lesson mirrors classic marketing wisdom. Technology may open the door, but identity is what keeps a brand alive.

As automation floods every channel with more content, Urbea’s warning grows louder. In a market of copies, the only safe move is to be impossible to copy.

The post Why Most Crypto Brands Disappear, According to Ogilvy Spain’s CEO appeared first on BeInCrypto.

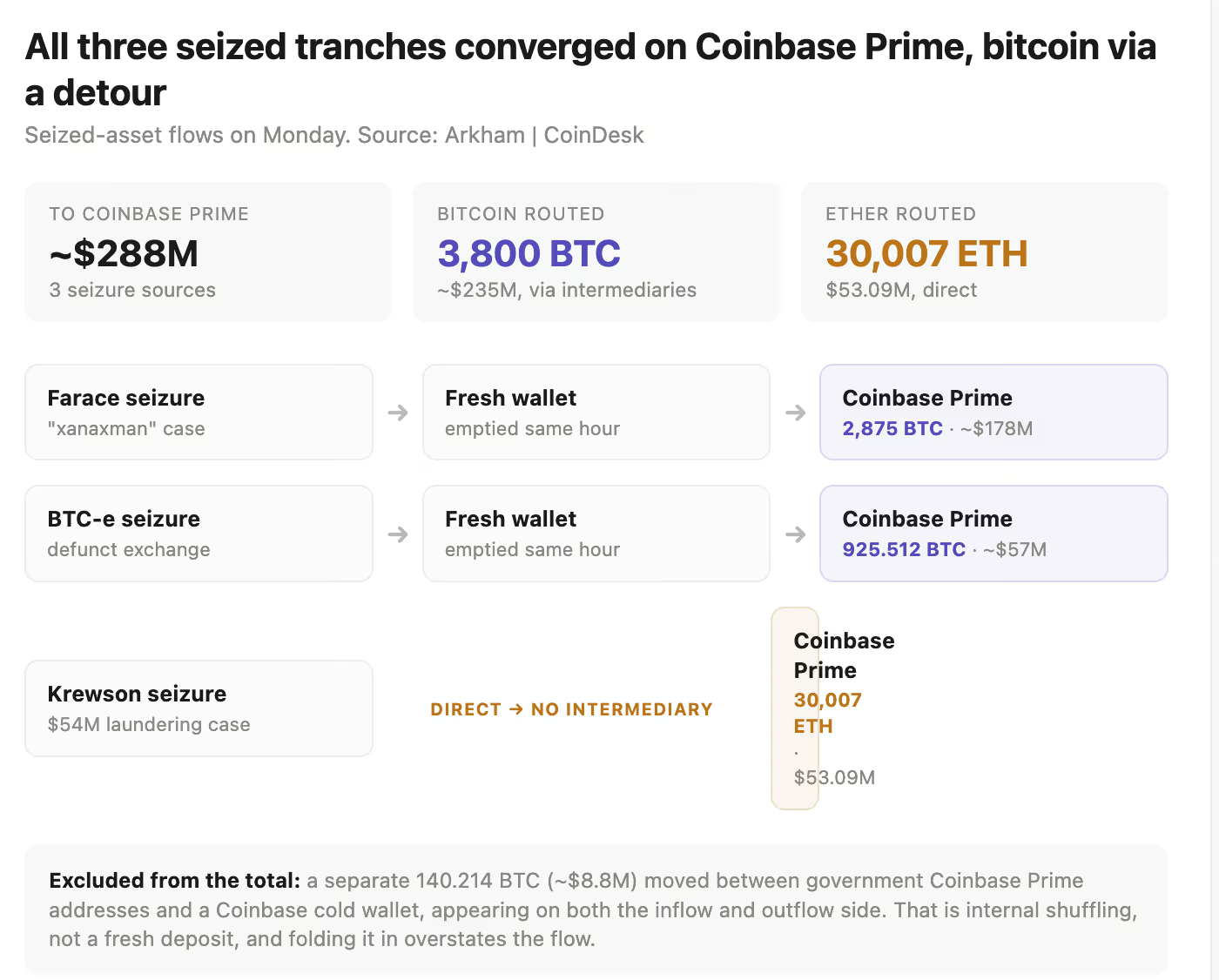

The US government just staged its seized crypto for an exchange, and it took an extra hop to get there.

Wallets tied to the government moved about $288 million in seized bitcoin and ether onto Coinbase Prime over roughly half a day on Monday, blockchain data from Arkham shows. The ether went direct, while the bitcoin took a detour through fresh intermediary wallets first.

The movements are despite an executive order in March 2025 by President Donald Trump, which designated seized bitcoin for the country’s Strategic Bitcoin Reserve and said it should not be sold.

A government wallet tied to Ryan Farace, the “xanaxman” case, sent 2,875 BTC worth roughly $178 million to a new address, which forwarded the full 2,875 BTC to a Coinbase Prime deposit wallet minutes later.

A second wallet linked to defunct exchange BTC-e sent 925.512 BTC worth $57 million through the same pattern, in from the seizure address, straight out to Coinbase Prime. Both intermediary wallets were emptied out.

The ether skipped the middle step, however. A wallet connected to Brian Krewson, the Oracle employee named in a $54 million laundering scheme, sent 30,007 ETH worth $53.09 million directly to a Coinbase Prime deposit address.

Patrick Witt, the White House point person for the Digital Asset Market Clarity Act, is set to take a leave of absence at the end of July to begin several months of military training, according to Crypto In America. Witt is expected to finish his White House duties on July 24 before reporting for Judge Advocate General (JAG) training with the Georgia Army National Guard.

The timing matters politically: the CLARITY Act is moving through a narrow window in the Senate before lawmakers depart for the Aug. 8 recess, a deadline that supporters have framed as critical for the bill’s odds this session. With Witt stepping away, attention is turning to how the White House’s advisory team will manage ongoing negotiations while the Senate considers the proposal.

Key takeaways

- Patrick Witt plans to wrap up his role by July 24 before starting JAG training with the Georgia Army National Guard.

- Witt’s absence comes as the CLARITY Act faces a tight Senate calendar before the Aug. 8 recess.

- Crypto In America reports that Harry Jung, the President’s Council of Advisors for Digital Assets deputy director, is expected to cover Witt’s responsibilities during training.

- Witt has helped broker talks between crypto and banking stakeholders, including issues tied to stablecoin yield and ethics provisions.

- Witt intends to stay engaged with the process during his training, though day-to-day coverage will likely shift.

Leave of absence as CLARITY hits a Senate deadline

Crypto In America reports that Witt’s military leave will begin after he completes work on July 24. The report describes the subsequent JAG training as qualifying him to serve as a legal officer in the Guard.

While the move is personal, it lands during a period when lawmakers are weighing whether they can advance the CLARITY Act in time. The bill, which would establish what supporters describe as the first comprehensive U.S. regulatory framework for crypto, must clear a narrow path through the Senate before the Aug. 8 recess. Many observers view that break as a point after which legislative momentum becomes harder to sustain.

Digital Chamber CEO Cody Carbone said Witt had previously informed stakeholders about the upcoming military leave. In a comment relayed by Crypto In America, Carbone said Witt had been “forthcoming and honest with every stakeholder” about taking the leave later in July.

Witt’s role in shaping market structure negotiations

Before stepping away, Witt has been described as a central figure in negotiations between representatives from the crypto industry and banking sector. Crypto In America says his involvement has extended to specific areas of the market structure bill, including questions surrounding stablecoin yield and disputes tied to ethics provisions.

Those topics are among the most sensitive parts of any attempt to align crypto rules with traditional financial oversight. Stablecoin yield-related provisions can determine how token holders may earn returns and how issuers structure incentives, while ethics provisions can influence how market participants and institutions manage conflicts of interest.

For investors and builders, the practical takeaway is that the regulatory text under discussion is unlikely to be shaped in a vacuum. Instead, it reflects ongoing negotiation between stakeholders with different incentives—an effort Witt helped coordinate. As the bill approaches a potential Senate push, the continuity of that negotiating function becomes more important.

Who will cover Witt’s responsibilities

According to Crypto In America, the President’s Council of Advisors for Digital Assets deputy director, Harry Jung, is expected to take on Witt’s responsibilities during his training. At the same time, sources cited by Crypto In America say Witt plans to remain involved in the process while he is away.

Cointelegraph attempted to seek comment from both the White House and Witt directly, the report notes. The outcome of that outreach is not included in the provided text, but the expectation is clear: someone else will likely manage the day-to-day coordination even if Witt stays engaged at some level.

That shift could affect the speed and tone of talks as the Senate calendar tightens. Even when a figure remains “in the process,” institutional momentum often depends on who is most actively present during negotiations and as legislative language is finalized.

What to watch during Witt’s training

With Witt stepping away just as the CLARITY Act approaches the Senate’s pre-recess window, the immediate watchpoints are whether the advisory team maintains its negotiating cadence and how remaining issues are handled as lawmakers move toward a vote.

Readers tracking the bill should focus on whether there are substantive changes to language related to stablecoin yield and the ethics provisions that Witt previously helped navigate, and whether Jung’s involvement results in new compromises—or indicates that negotiations are already mostly settled before the July transition. The next few legislative weeks before the Aug. 8 recess may offer the clearest signal of whether the CLARITY Act can keep moving without Witt’s direct presence.

HashKey Exchange, Shanghai Commercial Bank and Visa launched a co-branded credit card in Hong Kong.

Summary

- HashKey members can earn up to 4% rewards, converted monthly into HKD cash vouchers automatically.

- Cardholders may use vouchers to buy supported cryptocurrencies or offset trading fees on HashKey Exchange.

- Shanghai Commercial Bank issues the card, while Visa provides global payment acceptance and transaction infrastructure.

Eligible HashKey Exchange members can apply for the Shanghai Commercial Bank HashKey Visa Signature Credit Card through the two companies’ mobile applications.

The card links everyday spending with rewards that customers can use on the licensed exchange. The program does not pay cryptocurrency directly. Instead, it converts reward points into HashKey HKD Cash Vouchers monthly. Users can apply the vouchers toward crypto purchases or trading fees.

Card offers up to 4% rewards during promotion

Shanghai Commercial Bank’s card product page lists 2% rewards on eligible local spending and 4% on eligible overseas spending during the promotion. New customers may also receive up to HK$1,200 in HashKey HKD Cash Vouchers or HK$1,000 in spending credit, subject to the offer’s terms.

Cardholders earn one point for every HK$1 spent. On each monthly statement date, the program converts 250 points into HK$1 in HashKey HKD Cash Vouchers. Customers receive the vouchers in their HashKey accounts and can use them to buy any supported cryptocurrency or offset transaction fees.

Shanghai Commercial Bank issues and manages the card

Shanghai Commercial Bank issues the card and handles all banking and credit services. HashKey’s credit card disclosure says the exchange does not provide credit or banking services. The bank also decides whether to approve each application.

Applicants must hold a HashKey account, live in Hong Kong and be at least 18 years old. The application starts in the HashKey mobile app before redirecting users to Shanghai Commercial Bank’s app. The card also lights up during contactless payments.

HashKey targets practical digital asset use

HashKey Exchange Business Group CEO Haiyang Ru said the partnership seeks to expand regulated digital asset use beyond trading. He said the company wants to move “beyond speculative trading” by linking digital assets with broader financial services.

Visa Hong Kong and Macau general manager Paulina Leong said the companies aim to connect digital asset services with familiar payment methods. Visa supplies the payment network, while the bank and HashKey manage the card, rewards and customer accounts under their separate regulated roles.

The product follows an October 2025 announcement that Shanghai Commercial Bank and HashKey planned to develop a co-branded Visa card. The July launch moves that plan into a product open for applications by eligible exchange members.

Launch joins Asia’s growing crypto rewards card market

HashKey was among the first exchanges licensed to serve retail crypto customers in Hong Kong. As reported by crypto.news, the platform began licensed retail operations in August 2023 and supports direct bank transfers in Hong Kong dollars and U.S. dollars.

The card arrives as HashKey expands as a publicly listed digital asset company. In June, its board approved a share repurchase plan worth up to HK$100 million after its stock rose from recent lows.

Elsewhere, other Asian finance groups have also linked card spending with digital asset rewards. As previously reported, SBI and Visa introduced a Japanese credit card program tied to Bitcoin, Ether and XRP rewards in May.

The HashKey program uses a different structure. Customers receive HKD-denominated vouchers and choose whether to use them for crypto purchases. That model keeps the credit card, reward conversion and exchange transaction as separate steps, rather than paying cryptocurrency directly at checkout.

Key takeaways

- Stellar (XLM) extends losses as renewed U.S.-Iran tensions fueled a risk-off market environment.

- XLM is currently hovering near critical support around $0.177.

- XLM could test support near $0.173 if selling pressure intensifies.

Stellar (XLM) remains under pressure on Tuesday as investors reduced exposure to risk assets following escalating geopolitical tensions between the United States and Iran.

The broader cryptocurrency market weakened after renewed military developments in the Middle East increased uncertainty, pushing investors toward safer assets while weighing on altcoins.

US-Iran escalation dampens investor confidence

According to reports, the U.S. Central Command (CENTCOM) confirmed that American forces carried out additional strikes on Iranian military targets while maintaining more than 50,000 U.S. troops across the Middle East.

Iranian state-affiliated media also reported strikes in southern Iran, while the Islamic Revolutionary Guard Corps (IRGC) said it had disabled two supertankers in the Strait of Hormuz, accusing them of violating navigation warnings.

The IRGC warned that continued military activity in the region could delay the reopening of the strategic waterway and disrupt global energy supplies.

The heightened geopolitical tensions pushed West Texas Intermediate (WTI) crude oil above $80 per barrel, reinforcing a broader risk-off mood across financial markets and placing additional pressure on cryptocurrencies such as XLM.

Futures market data indicates traders are becoming increasingly cautious on both assets.

According to CoinGlass, XLM open interest dropped to approximately $182.21 million, extending the decline from elevated levels recorded in June.

Falling open interest alongside declining prices often signals that traders are closing positions rather than opening new ones, reflecting weakening market participation and reduced confidence.

Funding rates have also turned negative for XLM and now read -0.0021%. Negative funding rates indicate that short sellers are paying long-position holders, highlighting increased demand for bearish positions in the perpetual futures market.

Stellar (XLM) price analysis: Momentum remains weak

Stellar also continues to struggle as it trades near $0.179, below its major moving averages.

Current resistance levels include the 50-day EMA at $0.186, the 100-day EMA ($0.190), and the 200-day EMA ($0.196)

The RSI remains near 41, reflecting subdued momentum, while the MACD continues to trend in negative territory, suggesting buyers have yet to regain control.

The first major support is located near $0.177, followed by the 78.6% Fibonacci retracement level around $0.173.

If bearish momentum strengthens, XLM could decline toward a broader support zone near $0.142.

Should buyers return, resistance awaits at $0.186, $0.190, and $0.196, with additional upside barriers near $0.200, $0.218, $0.237, and $0.260.

White House crypto adviser Patrick Witt will take a months-long leave at the end of July to complete mandatory military legal training with the Georgia Army National Guard.

Summary

- Patrick Witt will leave the White House for mandatory Georgia Army National Guard legal training.

- Harry Jung is expected to assume Witt’s duties as CLARITY Act negotiations approach their deadline.

- Witt plans to remain involved during training, although his full-time return remains unclear after completion.

The move comes as Senate negotiators work to advance the CLARITY Act before the chamber leaves Washington for its summer break.

Crypto In America reported that Witt is expected to finish his White House work on July 24 and begin Judge Advocate General training on July 27. The program would qualify him to serve as a JAG officer. Witt and the White House had not commented publicly when the report was published.

Witt leaves during a key CLARITY Act phase

Witt serves as executive director of the President’s Council of Advisors for Digital Assets. He has acted as the administration’s main contact for lawmakers, banks, crypto companies and law enforcement groups working on the market structure bill.

The report said Witt helped manage talks over stablecoin rewards, government ethics rules and protections for decentralized software developers. Those areas remain part of Senate negotiations. Witt previously postponed his training from April as discussions continued, but a second delay was reportedly unavailable.

Harry Jung expected to assume responsibilities

Deputy director Harry Jung is expected to take over Witt’s main responsibilities during the leave. Jung has worked beside Witt during negotiations and attended many of the same meetings, according to people familiar with the transition.

Witt plans to remain involved where possible while completing training. However, the report said it remains unclear whether he will return to the White House role full time afterward. His departure will also affect work on the Strategic Bitcoin Reserve, GENIUS Act implementation and proposed crypto tax changes.

Senate calendar narrows bill’s path

The Senate’s official 2026 schedule lists a state work period from Aug. 10 through Sept. 11. That makes Aug. 7 the final scheduled session day before the break. Supporters have treated that date as a major target because the midterm campaign period may make floor action harder later.

As previously reported, Senate staff still need to combine the Banking and Agriculture committee texts before a full chamber vote. The bill likely needs 60 votes, requiring support from several Democrats. Ethics provisions, anti-money laundering rules and decentralized finance protections remain active disputes.

Witt called the current week “critical” for the legislation in a July 13 post. He said lawmakers had already lost time and “cannot afford to delay any longer.” His planned leave starts less than three weeks before the Senate’s last scheduled session day before recess.

CLARITY Act talks continue without chief negotiator

The CLARITY Act would create federal rules for digital asset markets and divide oversight between the Securities and Exchange Commission and Commodity Futures Trading Commission. It would also set requirements for exchanges, customer assets and crypto intermediaries.

The bill has gained support from law enforcement groups, although some organizations still want changes to developer protections and investigative authority. The Federal Law Enforcement Officers Association backed the measure while seeking tighter language for decentralized finance and federal enforcement powers.

President Donald Trump and Senator Cynthia Lummis have also called for passage before the break. The White House transition to Jung offers continuity, but Witt’s absence removes the administration’s main negotiator during the final scheduled weeks before recess later this summer.

Europe’s crypto market is large enough for licensing to change the competitive map. Chainalysis said regional crypto volumes recovered to a monthly peak of $234 billion in December 2024, while Germany, France, the United Kingdom, and other major European markets each received hundreds of billions of dollars in crypto value between July 2024 and June 2025.

MiCAR has now placed this market behind a stricter authorization filter. The transition period ended on July 1, 2026, and Luxembourg’s CSSF said virtual asset service providers are no longer permitted to offer services in the EU without authorization as crypto-asset service providers, or CASPs.

Le Monde reported that about 230 of 1,200 providers secured the European authorization needed to keep operating, while many others withdrew, sought buyers, or lost access to EU clients.

Europe’s Crypto Access Now Runs Through Authorization

MiCAR replaces Europe’s fragmented national registration model with a common EU rulebook for crypto-asset service providers. ESMA says the regulation covers transparency, disclosure, authorization, and supervision for crypto-asset activity, including asset-referenced tokens and e-money tokens.

That changes how crypto companies reach users. A national registration once gave firms a local route into the market.

Under MiCAR, companies serving EU clients need a CASP authorization tied to a specific legal entity, and ESMA has warned that MiCAR protections apply only to the authorized EU entity, not to affiliated companies elsewhere.

This makes licensing part of distribution. Wallets, exchanges, fintechs, merchants, and stablecoin companies need counterparties able to handle regulated crypto services inside the bloc.

Firms without authorization face limits on marketing, onboarding, and service continuity, while authorized providers can become gateways for partners seeking EU access.

OSL Group’s Austrian MiCAR authorization

OSL announced on July 9, 2026, that its European subsidiary had received CASP authorization from Austria’s Financial Market Authority under MiCAR. The authorization allows OSL EU to provide passport-approved services across the 30 countries of the European Economic Area.

The approved service set covers several core parts of crypto market access. OSL said the Austrian authorization covers custody and administration of crypto-assets, spot trading, on and off-ramp and conversion services, and crypto-asset transfers.

Banxa Adds the Payment Layer

Banxa became part of OSL Group after the take-private transaction was completed in January 2026. The purchaser acquired all issued and outstanding Banxa shares for about C$80.36 million, making Banxa a wholly owned subsidiary.

Banxa now acts as the payment processor and crypto exchange while handling payments, compliance and crypto delivery.

This is important because on and off ramps connect regulated financial systems with blockchain networks, and those flows often touch services covered by CASP rules, including conversion, transfer, and custody.

Payment companies with strong distribution but limited licensing may need authorized partners, while licensed firms may need payment networks to make their approvals commercially useful.

Stablecoins and the Licensing Question

Stablecoins add another reason for payment and custody services to converge. TRM Labs said EUR-denominated stablecoins grew from $69 million in monthly volume in January 2025 to $777 million in March 2026, a 12-fold increase over 15 months, with MiCA clarity and exchange integration among the drivers.

At the same time, stablecoin usage still depends on reliable fiat access. Reuters reported in January 2026 that stablecoin circulation exceeded $270 billion, while Visa’s head of crypto said mainstream merchant acceptance remained limited and stablecoin activity still came heavily from trading rather than consumer payments.

That is where the OSL-Banxa structure offers a useful example:

- Banxa brings payment access and conversion;

- OSL EU brings a regulated European entity covering custody, trading, transfers and conversion services.

Together, they show how firms may try to package stablecoin payments, crypto ramps and asset services under one licensing model.

Authorization Still Leaves Commercial Tests

MiCAR authorization gives providers a route into the EEA, but it does not solve every commercial issue. Crypto payment providers still compete on banking access, payment methods, approval rates, asset coverage, pricing, settlement speed, uptime, and partner support.

The post-MiCAR market may become smaller, but it will also become more demanding. Firms seeking European users will assess whether a provider can support local payment habits, maintain fiat liquidity, process refunds, handle compliance requests, and keep service levels stable during market stress.

OSL’s Austrian approval gives the group a regulated European base after the Banxa acquisition. Its value will depend on how effectively the combined business turns authorization into usable payment and trading services across different European markets.

The Wider Trend

Europe’s crypto market is entering a phase where regulatory status controls access. Before MiCAR, companies could build around national registrations, offshore entities and fragmented local approvals.

After July 1, 2026, authorized CASPs occupy a stronger position in the market because they can offer partners a recognized route into the EEA.

That trend may push more consolidation. Payment companies may seek licensed owners or partners. Exchanges may add payment and stablecoin services. Custody firms may expand into conversions and transfers. Banks, fintechs and merchants may prefer fewer counterparties with wider permissions.

OSL and Banxa show how European crypto access is being rebuilt around licensed entities able to connect fiat payments, custody, trading, transfers and stablecoin services.

In the post-MiCAR market, distribution follows authorization, and payment reach will increasingly depend on who holds the license behind the user experience.

The post MiCAR is Turning European Crypto Payments Into a Licensed Market appeared first on BeInCrypto.

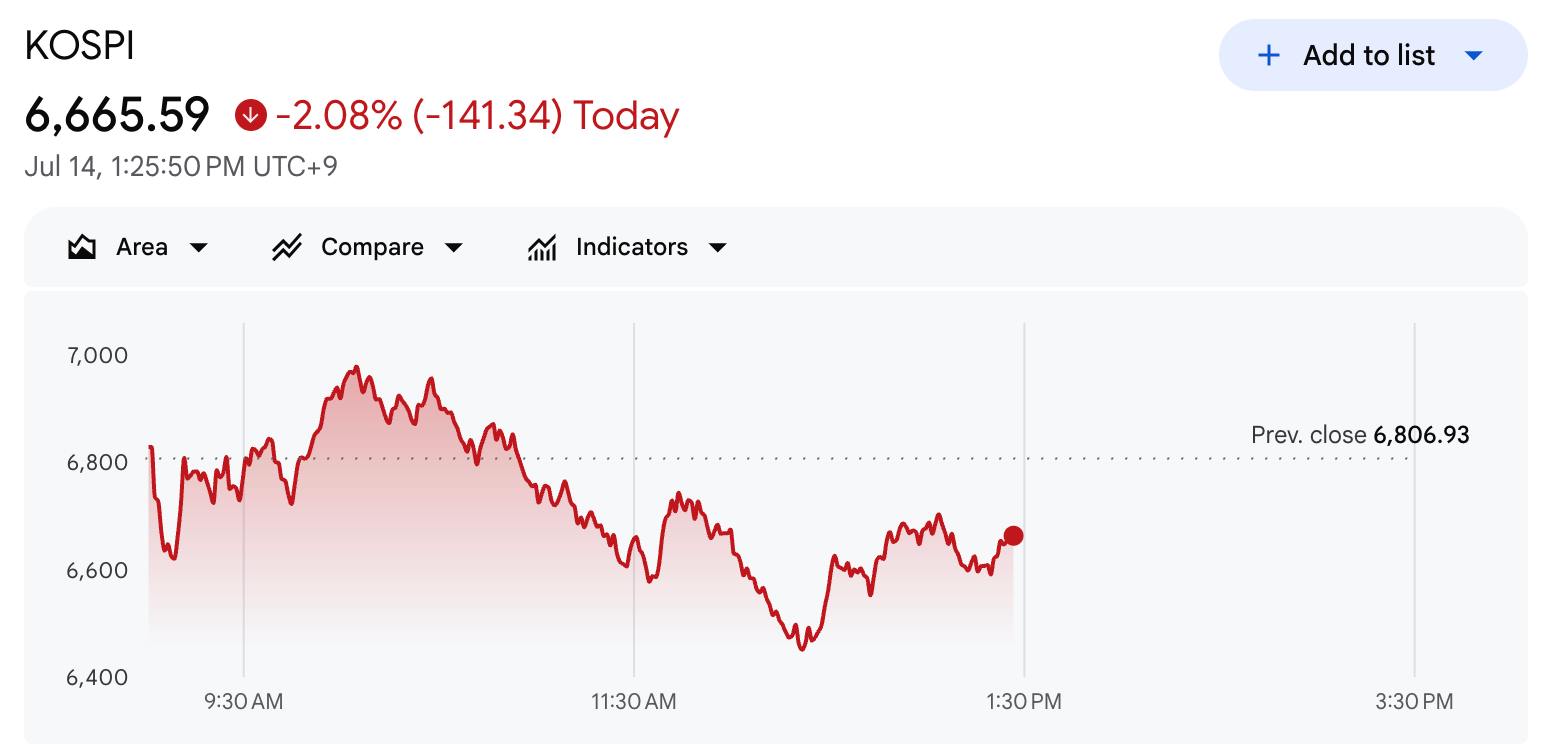

Upbit’s reported 24-hour trading volume surged 1,437% today, as South Korea’s KOSPI index tumbled and equity markets across Asia weakened.

The activity spike coincided with a broad regional selloff. Trading turnover jumped even as major benchmark indices in Seoul, Hong Kong, Tokyo, and Taipei all trended lower.

Trading on Upbit Rockets 1,437% as KOSPI Sinks 4%

The turnover reflects heightened trading activity rather than a confirmed shift of capital out of equities. The dollar total reached $4.24 billion as of press time, according to CoinGecko data.

Upbit ranks as South Korea’s largest cryptocurrency exchange by volume. A surge of this size signals a jump in participation across the platform’s markets.

The jump coincided with the KOSPI’s sharp decline on July 14. According to Wu Blockchain, the index fell 4% intraday to 6,534.34 before recovering some ground. It traded down about 2% as of press time.

Follow us on X to get the latest news as it happens

South Korea’s secondary market fared worse. The tech-heavy KOSDAQ Composite dropped 3.97% to 767.66 on the day.

SK Hynix, a major chip supplier, dropped 3.52% after sliding 15% in the previous session. The stock has led losses among Korean technology names.

Nonetheless, Samsung bucked the trend, gaining 2.36% on the day. The split performance points to uneven pressure across the region’s largest technology stocks.

Technology shares carry heavy weight in both Korean indices. Sharp moves in names like SK Hynix and Samsung, therefore, drive much of the daily swing.

Broader Asian markets also weakened. The Hang Seng Index slipped 0.47% to 24,099.89, and Japan’s Nikkei 225 edged down 0.086%. Taiwan’s TAIEX fell 1.93% to 44,503.61.

The coming sessions will show whether the surge marks a lasting increase in Korean crypto trading.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Is South Korean Capital Fleeing Stocks for Crypto? Upbit Volume Says Maybe appeared first on BeInCrypto.

Stablecoin cross-border payments priced below interbank foreign exchange rates in every month of the second quarter, according to Borderless.xyz’s Q2 2026 benchmark.

Summary

- Stablecoin cross-border payments priced below interbank rates throughout Q2 across Borderless’s global payment network tracked.

- Single-provider routing cost businesses an extra $2,330 for every $1 million moved during Q2 operations.

- African corridors saw the sharpest volatility while Latin American spreads continued narrowing during the quarter.

The report tracked 260 payment corridors across 108 countries and 59 currencies, using 2.96 million rate observations.

The median Parity Gap stood at minus 3.2 basis points for the quarter. One basis point equals 0.01%. The measure compares the delivered stablecoin price with the interbank midpoint. It moved from minus 2 basis points in April to minus 5.9 basis points in June, its lowest reading this year.

Stablecoin FX moves below interbank pricing

A negative Parity Gap means stablecoin delivery reached customers below the rate banks use when trading with each other. Borderless said that result remained rare across cross-border payment systems. Some provider rates include fees inside the exchange rate, so the measure reflects all-in pricing rather than pure FX execution.

The median cost of delivering a $10,000 payment stayed near $27 through Q2. It has remained within 30 cents of that level for five months. The median provider spread also held at 98.8 basis points from March through June after most compression occurred during Q1.

Routing becomes the largest remaining cost lever

Borderless found that provider choice now creates the widest avoidable cost. A business using the median provider instead of the best available route paid 23.3 basis points more. That equals $2,330 for every $1 million moved across 81 corridors.

The cheapest provider changed frequently. On the USDT-to-Brazilian-real corridor, the lead changed 34 times during 88 days, or about every 2.6 days. No provider held first place for half the quarter. The report called this difference the “Routing Tax.”

The network included 377 payout routes across seven blockchains. Borderless counted 82 corridors with at least two steady providers, including 18 with three or more. Those backup routes kept payments moving when a leading quote became less competitive.

Asset and corridor choices change final prices

USDC and USDT differed by only 0.4 basis points across the network, but individual corridors produced much larger gaps. USDC traded at a persistent 99-basis-point discount to USDT in Peru. Chile and Switzerland showed smaller pricing advantages for USDT.

Large payment flows also increased the cost of weak routing. Mexico’s 21.5-basis-point USDT routing gap applied to $67.6 billion in annual remittance inflows. Borderless estimated the same annual leakage as Colombia, where a 122.8-basis-point gap applied to much lower volume.

Regional pricing remains uneven

Africa’s median provider spread widened by 166 basis points to 512.8 during Q2. Malawi recorded the largest repricing. Its typical spread moved from about 296 basis points to 1,975 after a 5.8% change on April 9, with no backup provider available.

Ghana also faced wider pricing, but several providers remained active. The best quote stayed 258 basis points below the median on a day. Borderless cautioned, “None of these numbers is your number,” because each business pays according to its corridors, providers and ticket sizes.

As previously reported, stablecoin payment use has moved beyond crypto trading into business payments, payroll and cross-border settlement. Real-world stablecoin payments doubled to about $400 billion in 2025, with business-to-business transfers making up activity.

Payment companies are also widening stablecoin coverage. dLocal launched stablecoin services across more than 44 markets, while SBI Remit partnered with Fasset on infrastructure spanning over 50 payment corridors. Borderless said businesses can now save more through dynamic routing than by relying on one fixed provider under competitive market conditions.

Tencent to become Manus’s largest shareholder amid deal discussions

Financial Advisors React to Jaw Dropping Money Clips

Can scientists make a new element for the periodic table?

-

Fashion5 days ago

Fashion5 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Tech7 days ago

Tech7 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Sports5 days ago

Sports5 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports7 days ago

Sports7 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Tech6 days ago

Tech6 days agoAnthropic brings Claude Cowork to mobile and web as usage data shows most users aren’t coding

-

Sports4 days ago

Sports4 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Sports7 days ago

We have punished the disrespect

-

Tech5 days ago

Tech5 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Crypto World7 days ago

Crypto World7 days agoClaude AI Created Something Anthropic Never Designed

-

Crypto World7 days ago

Crypto World7 days agoNasdaq arthritis company holding Moshe Hogeg crypto hits all-time low

-

Tech2 hours ago

Tech2 hours agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

News Videos5 days ago

News Videos5 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

Tech6 days ago

Tech6 days agoKeychron is stepping outside keyboards with a $349 Thunderbolt 5 dock aimed at power users

-

Business6 days ago

Business6 days agoASX 200 Slides Over 0.6% as Rare Earths and Lithium Stocks Tumble Amid Global Semiconductor Sell-Off Today

-

Business6 days ago

Business6 days agoWill Trent shares rebound after Q1 update triggers 13% crash? Here’s what technical charts indicate

-

NewsBeat5 days ago

NewsBeat5 days agoMajor update after Huntingdon train attack as man enters plea

-

Tech6 days ago

Tech6 days agoOpenAI teams with Work Louder to launch Codex-native keyboard, weeks after CEO of Apps told staff ‘not to be distracted by side quests’

-

Business6 days ago

Business6 days agoSpaceX Shares Slide Nearly 6% Amid Post-IPO Volatility and Starship Test Focus

-

Entertainment7 days ago

Entertainment7 days agoSZA Shares She Was Formally Diagnosed With Autism

You must be logged in to post a comment Login