Crypto World

Valinor raises $25m to put private credit on-chain

Ex-Blackstone staffers raised $25M for Valinor, a startup using smart contracts to move private credit workflows on-chain and lend first to crypto firms.

Summary

- On-chain private credit startup Valinor has closed a $25 million seed round led by Castle Island Ventures, according to Fortune.

- The firm, founded by ex-Blackstone private credit staff, wants to replace spreadsheet-based workflows with smart contracts that automate fund routing and loan execution.

- Valinor has already originated loans to several fintech and crypto companies and plans to expand its book, client base and six-person team with the new capital.

Valinor, an on-chain private credit startup co-founded by former Blackstone employees, has raised $25 million in seed funding to move the mechanics of private lending onto public blockchains. Fortune reports that the round was led by Castle Island Ventures, with participation from the crypto arm of trading giant Susquehanna, venture firm Maven11 and the founder of bitcoin miner TeraWulf, which is currently pivoting part of its business toward artificial intelligence. The capital will go toward scaling Valinor’s loan book, broadening its customer base and hiring beyond its current six-person team.

In its current form, Valinor’s core pitch is straightforward: take the revolving credit lines and structured loans that dominate traditional private credit, and transplant the back-office process onto smart contracts. As Fortune explains, conventional lenders still lean heavily on “manual verification and spreadsheet collaboration” to manage covenants, drawdowns and repayments, a structure that is slow, opaque and operationally brittle. Valinor plans to replace those workflows with contracts that “automate routing of funds and condition-triggered execution,” essentially turning legal and operational terms into on-chain logic that runs by itself once parameters are met.

Both Valinor co-founders come out of traditional finance, having worked in banking and in Blackstone’s private credit division before moving into crypto in 2022. That background gives them familiarity with how large allocators think about risk, documentation and recovery—skills they now want to port into a blockchain-native environment. In its first phase, the company is focusing on lending to crypto companies rather than trying to underwrite the entire corporate universe at once, using the sector it knows best as a testing ground for its on-chain underwriting and servicing rails.

Fortune notes that Valinor “has completed lending for several fintech and crypto companies through blockchain technology,” suggesting that the platform is already live with real borrowers rather than just in pilot mode. Over time, the founders say they intend to introduce more of the loan lifecycle—origination, servicing, covenant monitoring—onto the chain, with the goal of improving efficiency and transparency for both lenders and borrowers. That aligns with a broader tokenization and real-world-asset push in credit markets, where other projects have started to bring trade finance, consumer loans and SME receivables on-chain under regulated structures.

The timing of Valinor’s raise underscores how quickly private credit has become a focal point for both traditional funds and crypto-native investors. In earlier crypto.news coverage of real-world-assets, asset managers described private credit as one of the most promising use cases for blockchain rails, precisely because of its fragmented data and heavy operational burden. A separate crypto.news story on tokenization highlighted how on-chain structures can give lenders near real-time visibility into collateral and payment flows, a sharp contrast with quarterly PDF reports and email chains. Another crypto.news story on institutional DeFi noted that some of the most active experiments now pair off-chain underwriting with on-chain execution, a model Valinor appears to be embracing.

For now, the startup’s immediate challenge is execution: proving that smart contracts can handle the messy edge-cases of private credit as reliably as seasoned back offices, and convincing conservative allocators that on-chain rails reduce, rather than add, operational risk. If it can do that at scale, the $25 million seed round led by Castle Island may look less like a niche crypto bet and more like an early stake in a new operating system for private lending.

Key Takeaways

- ServiceNow (NOW) climbed approximately 14% Friday, spearheading a significant software sector upswing

- Investor excitement built around new AI capabilities announced at Knowledge 2026, featuring the Otto assistant

- Bank of America resumed coverage with an optimistic perspective, positioning NOW as an agentic AI frontrunner

- The company’s board authorized a $4.2 billion stock repurchase program, boosting investor confidence

- The positive momentum rippled through software equities, lifting Snowflake, Oracle, Atlassian, and cybersecurity stocks

Shares of ServiceNow (NOW) skyrocketed approximately 14% during Friday’s trading session, delivering one of the year’s most impressive single-day performances in the software industry. By midday, the stock maintained its gains while the iShares Expanded Tech-Software Sector ETF (IGV) climbed 5% in parallel.

This surge follows several weeks of downward pressure on software equities. Prior to Friday’s rally, NOW shares had declined nearly 29% year-to-date, reflecting market concerns about artificial intelligence potentially cannibalizing traditional enterprise software revenues.

The market sentiment appears to be reversing course.

During the Knowledge 2026 event, ServiceNow introduced cutting-edge generative AI capabilities, highlighted by the Otto assistant, while announcing strategic collaborations with Experian and Boomi. These revelations demonstrated how the company is integrating AI directly into its platform architecture instead of positioning it as a standalone offering.

At the Jefferies Software, Internet and AI conference this week, ServiceNow’s COO and Chief Product Officer Amit Zavery tackled the AI disruption narrative head-on.

“We don’t want to have a non-AI and AI mindset anymore inside the company,” Zavery explained. “Our customers don’t want it. They want to be able to adopt AI as part of the same products they buy from us.”

Zavery further articulated why enterprise system-of-record platforms like ServiceNow maintain critical importance in an AI-dominated landscape.

“For IT managers and IT system owners, I already have all the other visibility. I don’t want to go to a third-party system for only AI-related stuff,” he noted.

Board Approves $4.2 Billion Repurchase; BofA Returns with Positive View

The stock benefited from two supplementary drivers. ServiceNow’s board greenlit a $4.2 billion share repurchase initiative, demonstrating management’s conviction in the company’s current price levels.

Separately, Bank of America resumed its ServiceNow coverage with an upbeat assessment, characterizing the firm as a pioneer in the developing agentic AI landscape. Such institutional endorsement typically influences hesitant investors to reconsider their positions.

Combined, these developments amplified what was already shaping up to be an exceptional trading day for the equity.

Broader Software Sector Experiences Widespread Gains

ServiceNow’s performance didn’t occur in isolation. Snowflake (SNOW), fresh off Thursday’s 36% surge to record highs following quarterly results, tacked on another 4.5% Friday.

Oracle (ORCL) vaulted 8% higher, Atlassian (TEAM) rocketed 11%, GitLab (GTLB) advanced 7.5%, and monday.com (MNDY) rose 6%. Microsoft (MSFT) inched up 3.7% in anticipation of next week’s Build 2026 conference, where fresh AI model announcements are anticipated.

Cybersecurity equities participated in the rally as well. Rubrik (RBRK) surged nearly 9%, CrowdStrike (CRWD) climbed 7.5%, Palo Alto Networks (PANW) appreciated 6.3%, and Fortinet (FTNT) gained 4%.

Company leadership also established a long-range revenue objective of $30 billion by 2030, providing investors with enhanced visibility into the company’s AI-driven growth trajectory.

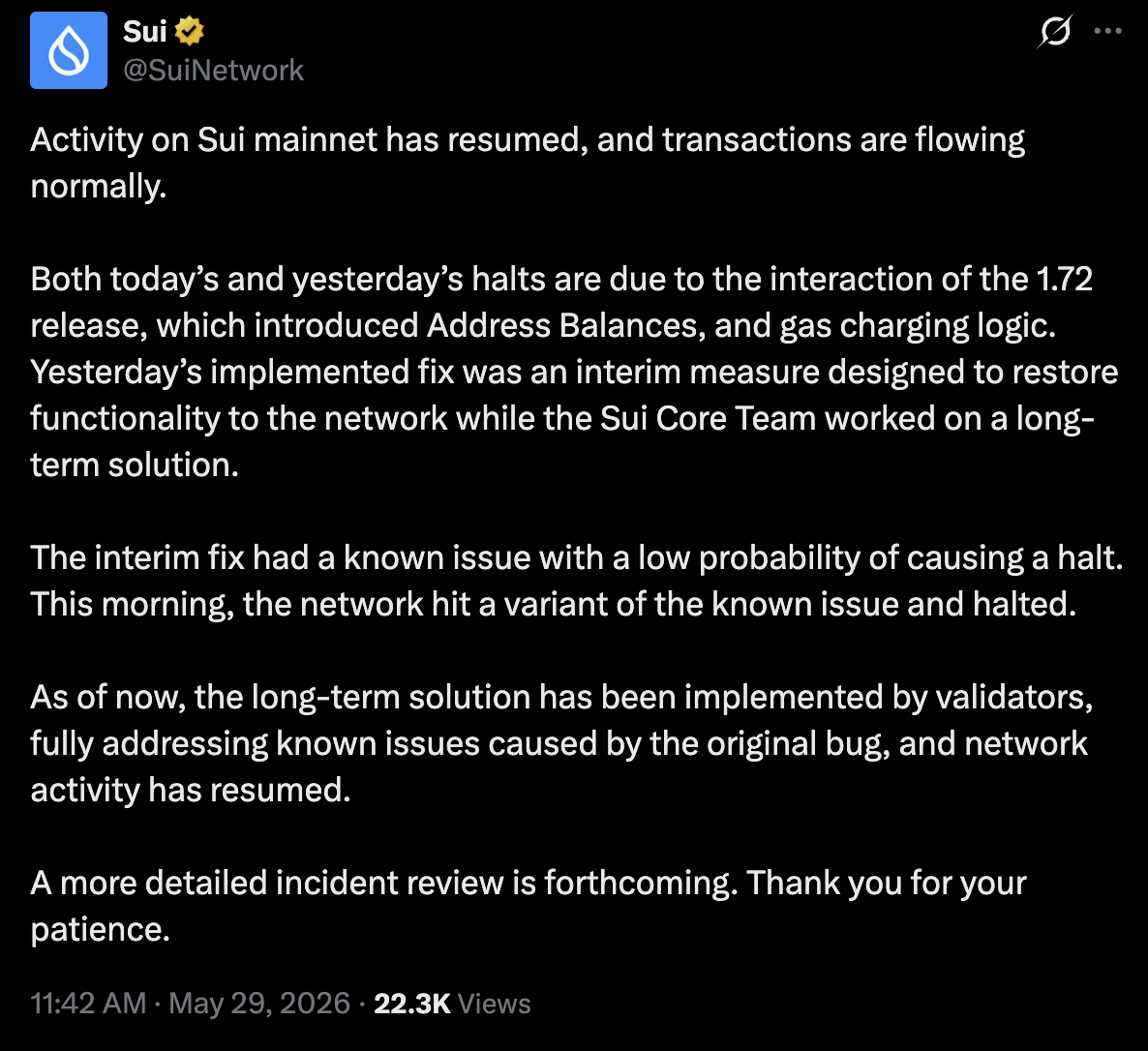

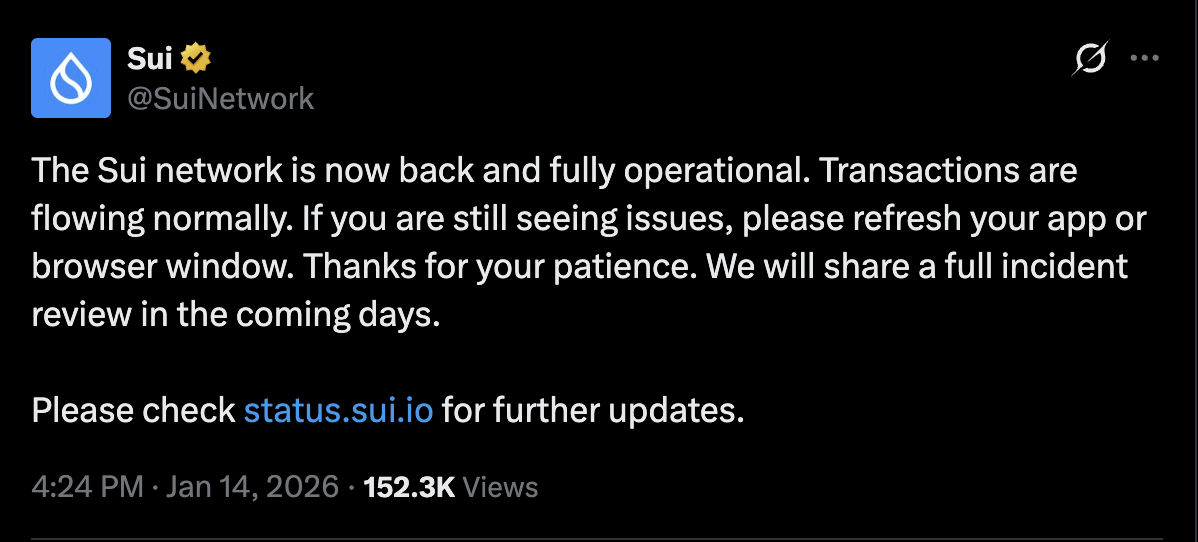

The Sui layer-1 blockchain faced another disruption this week, triggering a network stall that halted block production for more than three and a half hours before activity resumed. The incident, detailed by the Sui team and reflected in the network’s status dashboards, marks the second consecutive day of instability for the chain’s mainnet validators.

According to Sui status updates and the Suiscan block explorer, the last block prior to the disruption was produced at roughly 11:51 UTC on Friday, with network activity picking up again around 03:30 UTC. The team attributed the stall to the interaction between the recently released v1.72 software and the network’s address balances and gas charging logic. An interim fix had been deployed to restore functionality ahead of a more durable solution adopted by a majority of validators.

“Both today’s and yesterday’s halts are due to the interaction of the 1.72 release, which introduced address balances and gas charging logic. Yesterday’s implemented fix was an interim measure designed to restore functionality to the network.”

The interim patch was described as having a low probability of causing further disruption, with the long-term software fix now implemented by most validators. The incident follows a sequence of disruptions that began with Thursday’s outage, which was caused by a crash bug in the gas charging logic and led to a nearly six-hour downtime, according to the Sui team.

Beyond these events, Sui’s broader 2026 disruption history includes a high-profile outage in January 2026. The network went offline for more than six hours due to a consensus bug—validators submitted conflicting transactions to the protocol’s checkpoint mechanism, preventing the network from reaching the required consensus threshold. The post-mortem on that incident emphasized that the issue was contained by Sui’s checkpoint certification and quarantine mechanisms, which prevented a user-visible fork but halted progress in the process. The team stressed that user funds were never at risk and that no certified transactions were rolled back.

These recent incidents highlight the inherent fragility that can accompany high-throughput blockchain systems, where data availability, execution, and validator consensus layers intersect. The Sui team’s emphasis on checkpoint certification and quarantine underscores the defensive design choices intended to minimize user impact even when the network halts. Still, outages on a public network ripple outward, affecting centralized services that depend on live blockchain data and uptime. The episode also calls attention to the broader ecosystem, where outages at major service providers—such as cloud platforms—can compound the disruption for users and exchanges alike. For example, Coinbase faced a temporary service disruption in May due to an AWS outage, illustrating how a single failure point in the infrastructure stack can affect trading and liquidity even when the underlying blockchain remains theoretically resilient.

Key takeaways

- The latest Sui mainnet stall lasted over three and a half hours, with block production halted and later resumed after an interim patch and a longer-term fix.

- The disruption is attributed to the interaction between the 1.72 release—specifically address balances and gas charging logic—and the network’s existing execution and consensus flow.

- A durable software fix has been adopted by a majority of validators, following an interim repair rated as having a low likelihood of introducing new disruptions.

- The Friday incident follows Thursday’s six-hour outage caused by a crash bug in gas charging logic, and January’s six-plus hour stall caused by a consensus bug in the checkpoint mechanism.

- Analysts and developers note that outages on public blockchains can ripple into centralized services, highlighting the importance of robust recovery mechanisms and cross-layer resilience.

Context and implications for validators and users

From a technical perspective, Sui’s recurrent outages appear tied to how new software revisions interact with core network logic—specifically around how balances are tracked and how gas is charged. The 1.72 release introduced new balance-tracking and gas-charging semantics, and the subsequent halts suggest that the edge cases in those changes require careful handling to avoid cascading pauses in block production. The Sui team’s post-mortem emphasizes that the interim fix was designed to restore functionality quickly, while the long-term patch has now been broadly deployed to reduce the chance of another disruption.

For developers and validators, these events underscore the importance of rigorous rollout processes for critical protocol changes, especially on networks that aim for high throughput and low-latency finality. They also highlight the value of quarantine and checkpoint mechanisms as safeguards that can prevent user-visible forks even if network progress stalls. Investors and users should watch how quickly the ecosystem stabilizes after major releases and whether any secondary issues emerge as the new code paths become fully saturated in production workloads.

Looking ahead, the Sui network’s roadmap will likely focus on hardening the 1.72-induced changes, validating their behavior across a range of transaction loads, and ensuring that governance and operator tooling align to minimize operator risk during upgrades. Observers will also be watching to see whether further incidents emerge as validators complete the switch to the long-term fix and begin stress-testing the network under real-world conditions.

In the meantime, the episodes serve as a reminder of the delicate balance in building scalable, developer-friendly blockchains: the pursuit of higher throughput must be matched by robust validation, fault tolerance, and rapid, transparent post-mortems that translate into stronger resilience over time.

Readers should keep an eye on Sui’s official status updates and validator communications as the ecosystem digests the full implications of the latest patching cycle and gauges the network’s readiness to sustain higher loads without recurring interruptions.

US-listed spot Bitcoin exchange-traded funds (ETFs) are sliding into their longest withdrawal stretch since launch, signaling a shift in how institutions seek Bitcoin exposure through the ETF structure. Data compiled by Farside Investors show another $223 million net outflow on Thursday, pushing the nine-session decline to a record for funds that began trading in 2024. The streak has surpassed the previous eight-session low set in February 2025, though total withdrawals remain below the earlier peak of roughly $3.2 billion during that sell-off period.

The evolving flow pattern fits a broader picture of diverging demand across crypto ETF products. While traditional spot BTC exposure via ETFs continues to see selling pressure, newer strategies and class-focused funds have begun attracting fresh capital, underscoring a nuanced shift in investor preferences as the market contends with macro headwinds and evolving custody and liquidity dynamics.

Key takeaways

- Spot Bitcoin ETFs in the US posted a nine-day outflow streak, with a single-day drain of about $223 million on Thursday, according to Farside Investors.

- BlackRock’s IBIT remains the largest US spot BTC ETF by assets, but it led the pullback with roughly $2.04 billion in cumulative outflows between May 15 and Thursday.

- New entrants like Hyperliquid’s HYPE ETFs continued to attract inflows, surpassing the broader slowdown with cumulative net inflows above $100 million since May 12, per SoSoValue.

- Ethereum spot ETFs extended a separate weakness, sustaining 13 consecutive days of outflows totaling around $694 million, as investors rotate toward newer products.

Spot Bitcoin ETFs: the nine-day drain and what it signals

Among the primary drivers of the recent weakness in US spot Bitcoin ETFs is a persistent outflow trend that has stretched to nine consecutive sessions. The latest reading shows a $223 million net outflow on Thursday, marking the ninth consecutive session of declines and highlighting a continued retreat from the ETF-linked channel for BTC exposure since the start of the month.

Analysts have pointed to a combination of factors behind the retreat: a tempered institutional appetite for BTC via ETFs, ongoing macro uncertainty, and a flight toward different risk-managed or yield-bearing crypto products. The cumulative impact is evident—the total withdrawals from the US spot BTC ETF complex have approached roughly $2.84 billion across the nine-session run. That figure sits below the earlier sell-off trough of about $3.2 billion but nonetheless underscores a meaningful reallocation away from the traditional ETF vehicle for Bitcoin exposure.

Despite the pressure, the aggregate market remains attentive to where demand continues to emerge. The continued outflows in BTC ETFs contrast with pockets of growth in other crypto strategies, painting a market landscape where capital is re-deploying rather than exiting the crypto space altogether. The divergence also mirrors a broader theme: while canonical BTC exposure through ETFs has faced persistent redemptions, investors appear willing to allocate to newer, more specialized or diversified product types that claim to offer distinct risk/return profiles or liquidity nuances.

IBIT: the dominant fund in retreat, but still the largest holder

BlackRock’s iShares Bitcoin Trust (IBIT) remains the flagship US spot BTC ETF by assets under management, but it has borne a sizable portion of the current outflows. Between May 15 and Thursday, IBIT saw about $2.04 billion in cumulative withdrawals, with a single-day exit of $527.8 million on May 27 marking its second-largest daily outflow on record—just shy of the $528.3 million monthly peak posted on Jan. 30, 2025.

On the holdings side, IBIT continues to carry a dominant share of the US spot BTC ETF ecosystem. Wallet data show that, as of the close of trading on a recent Wednesday, IBIT held approximately 792,000 BTC, representing around 62% of all US-listed spot BTC ETF holdings. The concentration underscores BlackRock’s centrality in the sector, even as outflows weigh on its ETF’s near-term performance.

The dynamic raises questions about concentration risk within the ETF space. While IBIT remains the most significant single-holder, its outsized position means that large, concentrated redemptions can have outsized impact on overall ETF liquidity and price discovery during periods of broad selling pressure. Investors and practitioners will be watching whether new entrants or rebalanced portfolios can absorb the flow and stabilize market pricing in the near term.

HYPE and XRP: inflows diverge from the BTC ETF trend

Against the backdrop of cooling demand for Bitcoin exposure via traditional spot ETFs, a different segment of the market has been attracting interest. Hyperliquid’s HYPE ETFs, a newer entrant in the US-listed spot crypto ETF landscape, have continued to draw capital, with cumulative net inflows surpassing $100 million since their May 12 inception. SoSoValue tracks the daily inflows and notes a steady accumulation of fresh money, signaling investor appetite for products that promise rapid liquidity, flexible exposure, or novel token constructs.

Beyond BTC, other altcoin-focused funds have also reported inflows. In particular, XRP spot ETFs logged steady gains over the same period, adding roughly $120 million in net new money between May 4 and Thursday. The shift toward XRP and similar products highlights a growing investor interest in crypto assets beyond Bitcoin and Ethereum when packaged into regulated ETF formats.

The broader implication is twofold: first, investors are diversifying away from a sole reliance on BTC ETFs for crypto exposure; second, issuers are expanding their product tapes to capture demand for alternative tokens and novel strategies. This evolving ecosystem could shape liquidity patterns in the ETF space for the months to come, especially as market participants weigh regulatory clarity, custody, and tax considerations across a wider array of tokens.

Ether ETFs under pressure as flows turn negative

US-listed spot Ether ETFs have not shared the same resilience a few months ago. They have experienced persistent selling pressure, logging 13 consecutive days of outflows between May 11 and Thursday. The cumulative losses on the Ether ETF side total roughly $694 million over the period examined.

The contrast between BTC ETF flows and Ether ETF flows contributes to a broader re-pricing of crypto exposure in regulated vehicles. While BTC-specific products have faced sustained withdrawals, some investors appear to be experimenting with altcoin-linked strategies or new wrappers that may offer different liquidity and risk profiles. This rotation matters for traders and index designers alike, as it could influence the composition and liquidity of crypto ETF baskets in the near term.

What this means for investors and the road ahead

The current flow environment suggests a market in transition rather than a straight decline in interest for crypto assets via regulated products. The strongest signal is not a blanket loss of faith in BTC or Ethereum, but rather a reallocation toward products that promise differentiated exposures, enhanced liquidity, or targeted token bets like XRP and new thematic ETFs such as HYPE.

For investors, the key takeaway is the importance of understanding product design, custody frameworks, and liquidity sources behind each ETF. The outsized role of IBIT in asset concentration means that its performance will have outsized influence on the overall US spot BTC ETF sector in the near term. At the same time, inflows into HYPE and XRP products indicate there is capital appetite for alternative crypto exposure that can coexist with, but diverge from, BTC-centric narratives.

Regulatory clarity and institutional risk management considerations remain critical factors shaping these flows. As authorities refine guidance around custody, valuation, and surveillance, ETF issuers may adjust product features to align with evolving risk tolerances. In the meantime, market participants will likely keep close track of daily inflows and outflows across each ETF line to gauge whether the current rotation constitutes a longer-term trend or a temporary reallocation as investors reassess risk in a volatile macro environment.

The coming weeks should reveal whether demand for BTC exposure via ETFs stabilizes or whether inflows for newer products like HYPE and XRP-based funds gain momentum at the expense of legacy BTC ETFs. Investors should monitor ongoing fund flow data, liquidity metrics, and the relative performance of these vehicles against broader crypto market moves and macro indicators to determine where capital might settle next.

As broader market dynamics unfold, watchers will also want to see if ETH-related exposure regains traction or remains a laggard relative to alternative token-focused ETFs. The picture that emerges will influence asset allocation conversations, risk management frameworks, and the pace at which regulated crypto funds can evolve to reflect market realities.

Next steps for participants include watching daily inflow metrics for HYPE and XRP funds, tracking changes in IBIT’s share of total spot BTC ETF assets, and assessing whether ETH ETF outflows abate in the absence of a larger shift toward Bitcoin or XRP products. With regulatory and liquidity factors still in flux, the path for US-listed crypto ETFs remains nuanced—offering both opportunities and caveats for investors seeking regulated, exchange-traded crypto exposure.

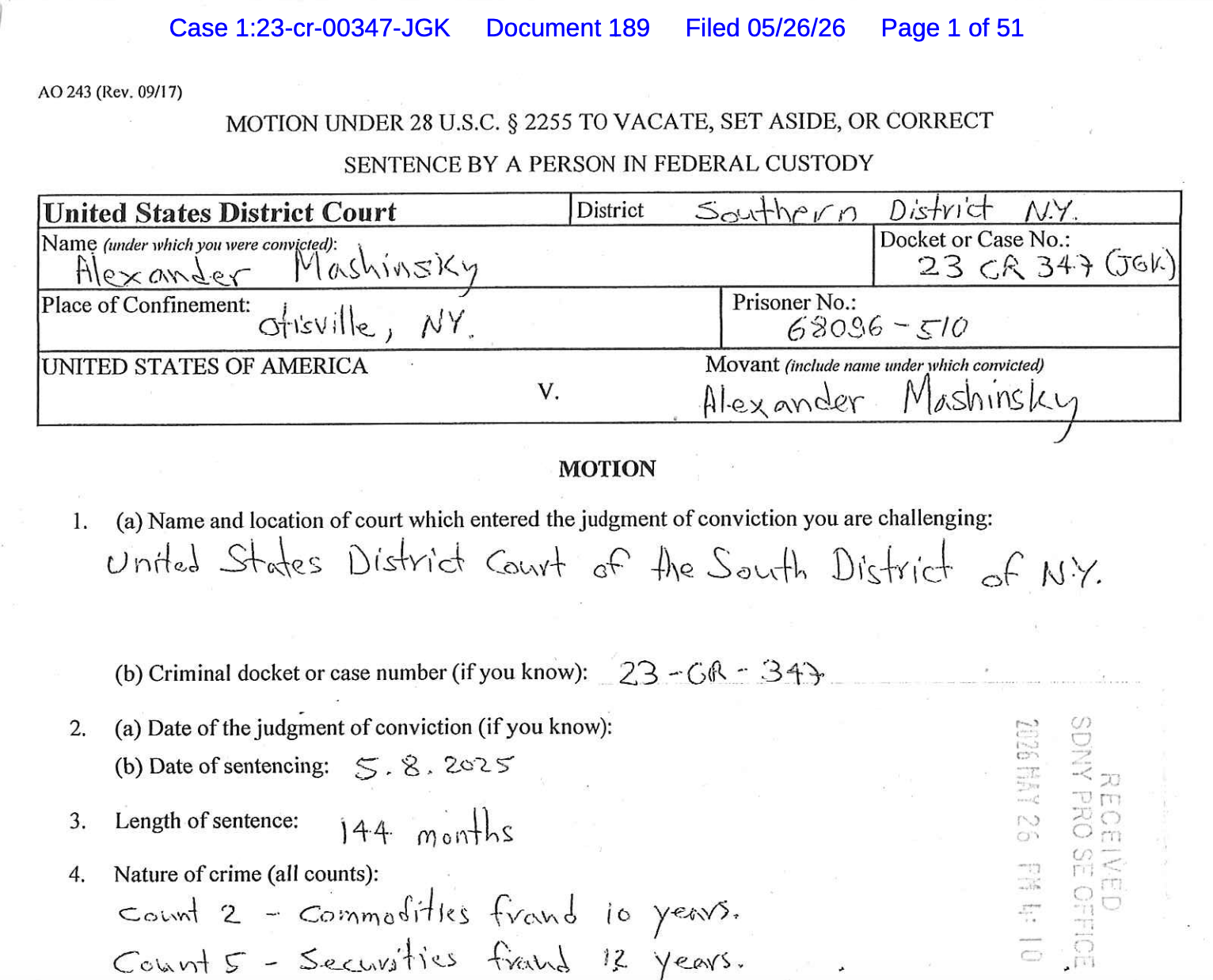

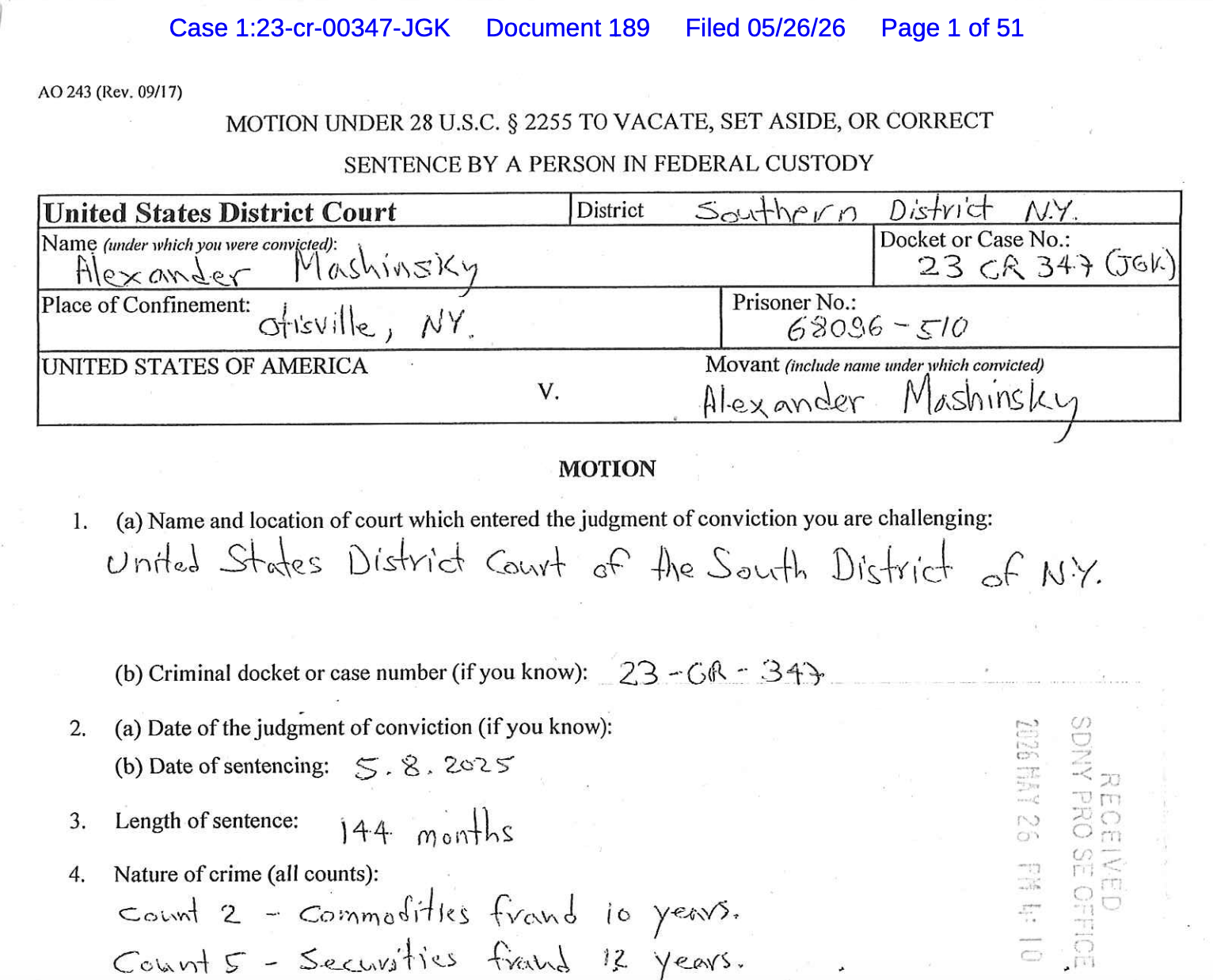

Alex Mashinsky, the former Celsius Network chief executive, has filed a motion in the Southern District of New York seeking to vacate his 144-month sentence for commodities and securities fraud. The pro se filing—submitted after Mashinsky announced on May 5 that he would proceed without counsel—asks the court to overturn the sentence imposed by Judge John Koeltl in May 2025. The move comes as part of ongoing post-conviction proceedings tied to Celsius’s 2022 bankruptcy and the broader collapse of the crypto lending sector amid the FTX crisis.

In the petition, Mashinsky contends that he received ineffective representation and that the record contains “fruit of the poisonous tree” material—evidence tainted by authorities’ alleged misconduct. He states that his counsels stopped communicating with him, prompting the pro se reply he filed directly with the court. The motion to vacate underscores the defendant’s effort to challenge both the quality of legal representation and the legitimacy of the underlying proceedings.

According to court documents summarized by Cointelegraph, Mashinsky also advances claims tied to the broader Crypto Valley upheaval, arguing that former FTX CEO Sam Bankman-Fried sought to destroy Celsius and that this dynamic contributed to market manipulation surrounding Celsius’s CEL token on the FTX exchange. He submitted text messages with Celsius’s former chief revenue officer, Roni Cohen-Pavon, alleging a hostile takeover attempt at the platform and urging the court to reject any FTX-related trust arrangements. The filing notes Celsius filed for bankruptcy in 2022 as bears and insolvencies ravaged the crypto lending sector, a context that continued through the FTX collapse and related regulatory actions.

The Celsius case has been subject to parallel regulatory and criminal scrutiny. Mashinsky and Cohen-Pavon were indicted in July 2023 on charges including fraud and market manipulation; both subsequently pleaded guilty. Cohen-Pavon was sentenced to time served in September 2023 after prosecutors cited substantial assistance, including willingness to testify against Mashinsky. The court’s judgments against Celsius executives were issued against a backdrop in which several crypto firms faced bankruptcy and heightened regulatory enforcement as U.S. authorities escalated their actions against misrepresentation, manipulation, and other illicit market activities within crypto markets.

Among the ongoing financial penalties, Mashinsky was ordered to forfeit $48 million as part of a 2025 criminal settlement. He also agreed to a $10 million payment as part of a separate regulatory settlement with the U.S. Federal Trade Commission tied to a largely suspended $4.72 billion monetary judgment. Cohen-Pavon, who was sentenced to time served, agreed to pay more than $1 million and a $40,000 fine in connection with his guilty plea. The outcomes illustrate the interplay between criminal penalties and civil or administrative remedies in high-profile crypto compliance cases.

Key takeaways

- Alex Mashinsky has filed a pro se motion in the SDNY to vacate his 144-month sentence for commodities and securities fraud, arguing ineffective counsel and tainted evidence.

- The filing cites alleged interference by authorities and invokes the “fruit of the poisonous tree” doctrine, asserting that the misconduct affected the case’s integrity.

- Mashedinsky’s submission reiterates claims linking FTX’s Sam Bankman-Fried to efforts against Celsius and to market manipulation surrounding Celsius’s CEL token on the FTX exchange.

- Former Celsius executive Roni Cohen-Pavon is central to the related legal narrative, with text-message evidence described as indicating a hostile takeover attempt and the broader disputes that surrounded Celsius’s business prospects.

- Criminal and regulatory penalties continue to shape the Celsius matter: Mashinsky faces forfeiture and FTC-related judgments, while Cohen-Pavon faced a time-served sentence and nominal civil penalties.

Procedural posture and grounds for vacatur

The core of Mashinsky’s motion rests on two arguments: ineffective assistance of counsel and the “fruit of the poisonous tree” doctrine, which contends that tainted evidence should not be used to sustain a conviction. The defendant elected to proceed without counsel after indicating his intention to litigate pro se, a move that US courts scrutinize carefully given the complexity of securities and commodities regulation, as well as the procedural intricacies of criminal sentencing.

While the court has not indicated a ruling on the vacatur motion, the filing itself underscores the ongoing legal contest surrounding Mashinsky’s conviction and sentence. The 12-year term, set in May 2025 by Judge Koeltl, remains a focal point of the case as Mashinsky seeks to challenge both the sentence and the underlying conduct that led to the conviction.

FTX disruption, internal Celsius dynamics, and regulatory context

The motion’s referenced material ties Mashinsky’s defense strategy to a broader narrative: the fall of Celsius amid the 2022 crypto downturn and the later collapse of FTX. The docket cites communications suggesting that Sam Bankman-Fried’s actions or intentions may have influenced Celsius’s market environment, including CEL token trading on the FTX platform. While these assertions are contested and central to Mashinsky’s position, they must be weighed against the court’s assessment of the facts and applicable law in a sentencing context.

Regulatory and enforcement considerations loom large in the Celsius saga. The indictments of Mashinsky and Cohen-Pavon in 2023, their guilty pleas, and the subsequent penalties illuminate how US authorities are pursuing cases of misrepresentation, manipulation, and other alleged improprieties in crypto-lending and related platforms. The outcomes contribute to a growing body of precedent on the liability of corporate leaders in crypto firms, the credibility of disclosures, and the steps agencies take to deter and remedy market abuses in crypto markets.

From a policy perspective, the matter intersects with broader enforcement themes—ranging from the DOJ’s crypto-related prosecutions to CFTC and SEC oversight of commodities and securities aspects of crypto tokens and offerings. The Celsius proceedings also sit against a global regulatory backdrop where frameworks such as MiCA in the European Union influence cross-border considerations, licensing regimes, and the alignment of crypto lending activities with consumer protection standards and anti-money-laundering (AML) requirements. The case thus offers material context for institutions assessing regulatory risk, governance standards, and the sufficiency of internal controls in asset-backed and algorithmic finance ventures.

Regulatory outcomes and corporate accountability

The financial penalties tied to the Celsius executives—Mashinsky’s $48 million forfeiture and the roughly $10 million related to FTC settlement terms in connection with a largely suspended $4.72 billion judgment—illustrate the multilayered enforcement approach in this space. Cohen-Pavon’s time-served sentence, along with more than $1 million in payments and a $40,000 fine, demonstrates that prosecutors and regulators have continued to pursue both criminal accountability and civil remedies for senior executives involved in crypto market manipulation or misrepresentation schemes.

These developments bear on how exchanges, lenders, and other crypto firms manage compliance risk, disclosures, and internal governance. Institutions operating in or alongside crypto markets should monitor ongoing judicial developments, as vacatur motions and related post-conviction relief efforts can shape the interpretation of corporate responsibility, the treatment of evidence, and the standards applied to future enforcement actions. The evolving landscape also informs licensing considerations, supervisory expectations, and collaboration between federal agencies in cross-border contexts, where enforceability and recognition of judgments may vary.

Closing perspective

The Mashinsky case remains an active legal matter with a pending vacatur petition that could influence sentencing outcomes and the enforcement posture for senior executives in the crypto sector. As regulators continue to sharpen their toolkit for addressing misrepresentations, manipulation, and governance failures, observers should watch for how the court weighs ineffective counsel claims, the admissibility and impact of contested evidence, and any subsequent motions that could reshape the balance between punishment and relief in high-profile crypto cases.

JPMorgan Chase CEO Jamie Dimon on Friday yet again sharply criticized Coinbase CEO Brian Armstrong and warned that the latest version of the Clarity Act could ultimately fail if lawmakers do not address concerns from traditional banks over stablecoin regulation.

In an interview with Maria Bartiromo on Fox Business, Dimon appeared frustrated by the direction of the debate around stablecoins and digital asset legislation. Asked whether he was satisfied with the current draft of the Digital Asset Market Clarity Act, the crypto market structure bill that will formalize rules around how federal securities and commodities regulators oversee crypto, Dimon said he was not.

“No, because it allows them to effectively pay interest on deposits, stablecoins or something like that, without protection that they should have,” Dimon said. “The banks will not accept it that way. … I’m not worried about stablecoins but if it happened I’m telling you I will have nothing to do with it and it will eventually blow up.”

The comments come amid a growing divide between the banking industry and crypto firms as lawmakers prepare for a key markup process that will determine whether the Clarity Act can advance through Congress. Lawmakers are expected to continue negotiating provisions governing stablecoin issuers, consumer protections, reserve requirements and whether crypto companies should be permitted to offer yield-bearing products that resemble traditional bank accounts.

For the legislation to ultimately become law, it must clear the full Senate and House of Representatives, and be signed by President Donald Trump. The Senate Banking Committee advanced its version of the bill through a markup earlier this month, and the Senate Agriculture Committee advanced its own version earlier this year. At the moment, representatives from the two committees are merging the bills, a key step before the full Senate can take a look.

At the center of the dispute which dragged out the Banking Committee’s process is the question of stablecoin rewards. Armstrong and Coinbase have argued that traditional banks are pushing lawmakers to curb stablecoin rewards programs, which function similarly to high-yield interest accounts and could threaten banks’ deposit-based business models. Banking executives, meanwhile, contend that firms offering bank-like products should face comparable oversight and regulatory obligations.

The disagreement has become one of the primary reasons the legislation has stalled in Washington and failed to gain sufficient momentum earlier this year, despite broad bipartisan interest in creating a regulatory framework for digital assets.

Tensions between Armstrong and Wall Street executives have been building for months. During meetings at the World Economic Forum in Davos earlier this year, Dimon told Armstrong, “You are full of s—,” according to people familiar with the exchange who spoke with The Wall Street Journal.

Bank of America CEO Brian Moynihan reportedly dismissed Armstrong’s arguments, telling him, “If you want to be a bank, just be a bank.” Wells Fargo CEO Charlie Scharf declined to engage, while Citigroup CEO Jane Fraser spent less than a minute with him, according to that prior reporting.

Coinbase and JPMorgan did not respond to requests for comment in time for publication.

This Friday, we examine Ethereum, Ripple, Cardano, Binance Coin, and Hyperliquid in greater detail.

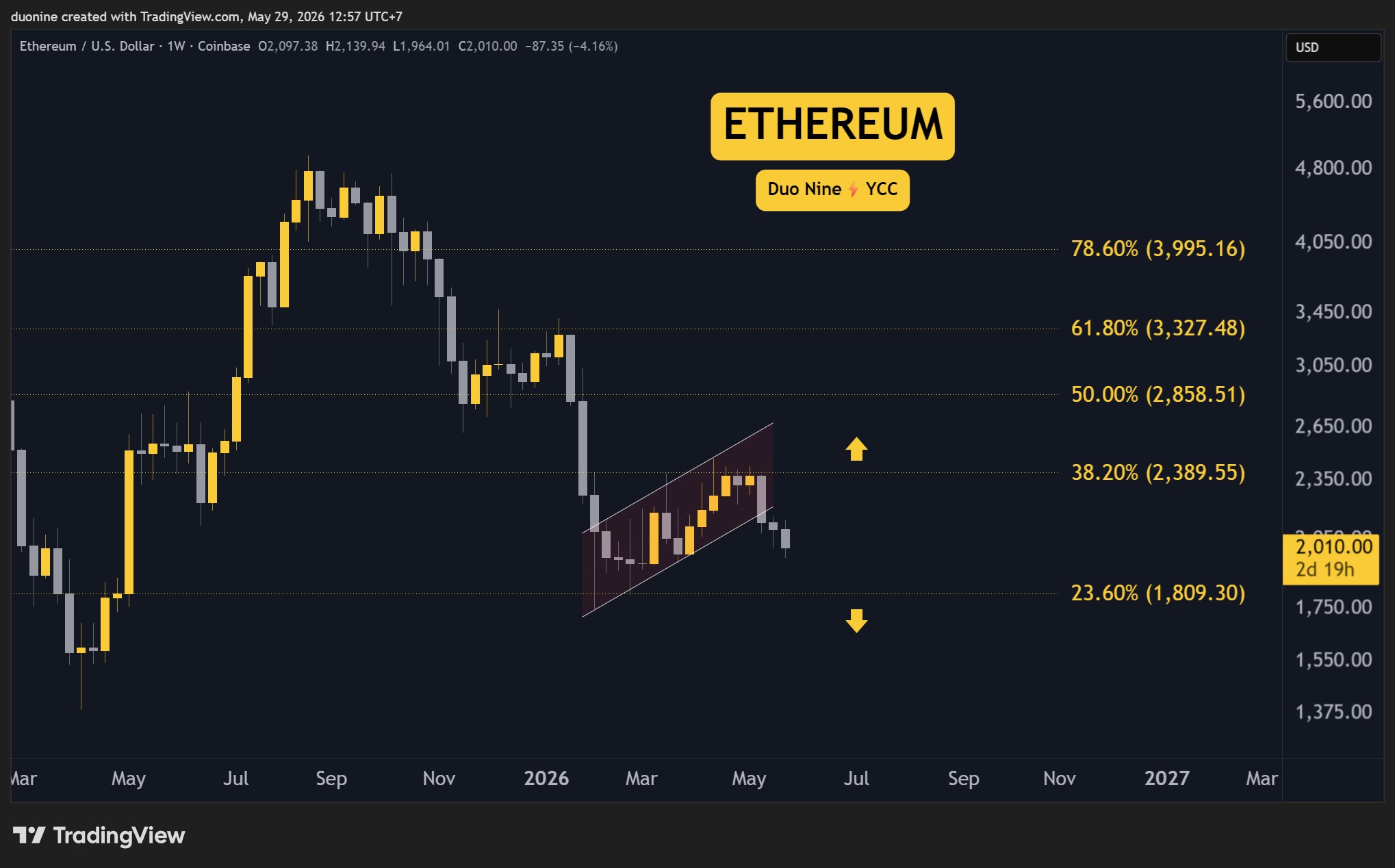

Ethereum (ETH)

Ethereum is down 6% this week after sellers managed to put pressure on the $2,000 support. At the time of this post, this level appears to be holding, but only by a thread. Another push later could turn it into key resistance.

If $2,000 is lost next week, buyers will likely retreat to support at $1,800. This level managed to halt the downtrend previously, but another visit there could be interpreted as bearish, with a higher chance of a breakdown.

Looking ahead, this cryptocurrency remains in a bearish trend with sentiment being quite negative. This will likely fuel new lows as the downtrend continues into the summer of 2026.

Ripple (XRP)

XRP also had a bad week, closing with a 4% loss. Its price fell below the blue pennant, which is now acting as resistance. Sellers are defending the level at $1.4 and the key support levels are found at $1.2 and $1 where buyers are likely to return.

If this weakness continues, this cryptocurrency is likely to revisit the support levels in the coming weeks. Sellers are also controlling the price and have dominated for over three weeks with no relief.

Looking ahead, XRP is in a difficult position because its downtrend has been ongoing for almost a year. There were no major relief rallies, and any bounce was short-lived. Hopefully, a bottom is found soon, with $1 as a prime candidate.

Cardano (ADA)

ADA has entered dangerous territory after its price pierced through the support at $0.24. While it is still early to call it, this breakdown could be a significant loss of trust as the price falls to new lows.

Cardano also closed the week with a 7% loss, being unable to stop sellers from pushing the price down. The support at $0.24 held well for several months, but it seems this latest push may seal its fate.

Looking ahead, if $0.24 becomes resistance in the coming days, this cryptocurrency may make new lows not seen since 2021. If so, key target areas will be found at $0.20 and $0.15.

Binance Coin (BNB)

Binance Coin continues to disappoint, as its price has failed to break the $690 resistance level several times. This has forced it to bounce in a flat trend for months, testing the support at $580 and resistance at $690 several times. It also closed the week with a 3% loss.

Without a clear breakout, BNB could end up making lower lows, as the overall market bias is bearish. Therefore, sellers have the advantage and they could soon try their luck again at the key support. If that won’t hold, bears will target $ 500 next.

Looking ahead, this cryptocurrency may pause, moving sideways before its downtrend resumes. This is contingent on the overall market remaining bearish. Should Bitcoin make new lows, BNB is likely to follow as well based on this price action.

Hype (HYPE)

HYPE closed this week 6% higher, but it appears to have hit a ceiling somewhere around $64. Since that level was visited, sellers managed to put a stop to the rally and the price has been hesitating to make new gains.

With sellers becoming more aggressive, the most likely scenario here is a pullback towards the low $50 before HYPE attempts new highs. A correction would also be ideal to consolidate the recent gains after such a spectacular performance in recent weeks.

Looking ahead, if HYPE manages to test and confirm $52 as support, then it can use that level as a base towards new highs later. The current resistance at $63 continues to hold and will need to turn into support for the rally to resume.

The post Crypto Price Analysis May-29: ETH, XRP, ADA, BNB, and HYPE appeared first on CryptoPotato.

On May 29, the world’s largest corporate holder of Bitcoin Strategy transferred 411.48 BTC, worth over $30 million, to Coinbase Prime, a move that immediately drew attention across the crypto community as traders tried to read the intent from the on-chain activity.

The timing was especially hard to ignore considering that on Polymarket, the probability that Strategy will sell some of its Bitcoin before December 31, 2026 has now hit 84%.

What the Transfer Could Mean

Depositing BTC to an exchange does not automatically mean that the holder is looking to sell. This was noted by pseudonymous crypto analyst COINBOY, who pointed out that funds moved to Coinbase Prime could be for OTC trading, collateral arrangement, or institutional fund management rather than outright liquidation. Keep that distinction in mind before reading too much into a single on-chain transaction.

However, what gave Strategy’s move more weight is the context around it, with the company’s Executive Chairman Michael Saylor recently declining to rule out selling some BTC before year-end, a notable departure from the hold-at-all-cost image he’s spent years building.

That change in mindset was revealed on Strategy’s Q1 2026 earnings call, where the firm reported $12.5 billion in net losses for the period. During the call, Saylor suggested that the company could liquidate part of its BTC stash to pay dividends, a position that was defended by Bitcoin maximalist Samson Mow, who said that the “never sell” mantra long associated with Saylor should not be taken as some kind of corporate oath but as guidance for individual holders, since any BTC treasury company that completely rules out selling would be handing a roadmap to short sellers that could hurt it.

There’s also the question of what Strategy did earlier this week when, instead of buying more Bitcoin as is the tradition, it repurchased approximately $1.5 billion of its own 0% convertible senior notes that were due in 2029. Analyst Darkfost framed the move as a balance sheet cleanup rather than the company rethinking its BTC plan, although Saylor himself had once again hinted in an interview that one of the options Strategy had considered to fund the repurchase was Bitcoin sales.

Interestingly, hours before on-chain tracking platform Lookonchain reported on Strategy’s 411 BTC deposit on Coinbase Prime, the executive posted a one-word tweet on X that simply read, “HODL.”

Where Bitcoin Stands

While speculation about Strategy’s intention was running rife, BTC itself was being buffeted by geopolitical developments, with the OG cryptocurrency losing more than $2,000 from its value after hostilities between the USA and Iran resumed. That session was quite rough, as it saw crypto markets shed over $100 million in total capitalization, with liquidations across derivatives topping $1 billion.

Today, at the time of writing, BTC was about $300 short of $74,000, having dipped by almost 5% in 7 days and nearly the same percentage in the last month. For Strategy, whose 843,738 BTC were purchased at around $75,700 per coin, the current price range puts its overall position modestly in the red on paper.

The post Strategy Moves $30 Million in BTC to Coinbase Amid Sell Speculation appeared first on CryptoPotato.

Alex Mashinsky, the former CEO of defunct cryptocurrency lending platform Celsius, has filed a motion in a New York court to vacate his 12-year sentence for fraud and market manipulation.

In a Tuesday filing in the US District Court for the Southern District of New York, Mashinsky filed a motion to vacate his 144-month sentence, set by Judge John Koeltl in May 2025. The former Celsius CEO filed the paperwork without additional counsel, having announced on May 5 that he would be proceeding pro se in his case.

Although Mashinsky pleaded guilty to commodities fraud and securities fraud related to “manipulative and deceptive devices,” he filed a motion to vacate on the grounds that he had ineffective counsel and “fruit of [the] poisinous [sic] tree,” a legal doctrine referring to evidence tainted by authorities’ misconduct.

“I did not discharge my counsel at this time but they stopped communication with me so I had no choice but to file my reply directly with the court,” said Mashinsky.

Source: Courtlistener

In documents attached to his motion to vacate, Mashinsky said former FTX CEO Sam Bankman-Fried intended to “destroy Celsius,” blaming him for much of the market manipulation of the network’s CEL tokens on the crypto exchange. He asked that the judge deny any FTX trust request, and provided text messages with Celsius’ former chief revenue officer Roni Cohen-Pavon, claiming he had attempted a “hostile takeover” of the platform.

Celsius filed for bankruptcy in 2022 amid a market downturn that saw the collapse of many crypto exchanges, including FTX. US authorities indicted Mashinsky and Cohen-Pavon in July 2023 on charges related to fraud and market manipulation, with both men later pleading guilty.

Related: Acting AG Todd Blanche confirms ‘code is not a crime’ in DOJ pivot

Cohen-Pavon was sentenced to time served after pleading guilty in September 2023, with prosecutors citing his “substantial assistance” to the government, including being prepared to testify against Mashinsky. His sentencing followed the court officially closing the criminal cases against the Celsius executives.

Alex Mashinsky at the Bitcoin 2021 conference in Miami. Source: Cointelegraph

Financial penalties against Celsius execs

Although the court may still consider Mashinsky’s motion to vacate, the former CEO was already ordered to pay $48 million as part of a forfeiture in his criminal case settled in 2025. He also agreed to pay $10 million as part of a settlement with the US Federal Trade Commission in a mostly suspended $4.72 billion monetary judgment.

Cohen-Pavon, sentenced to time served, agreed to pay more than $1 million and a $40,000 fine.

Magazine: HYPE chases $100 target, ETH could dump below $1800: Market Moves

U.S. Treasury Secretary Scott Bessent announced today that America has now seized a cumulative total of approximately $1 billion in Iranian cryptocurrency assets under its escalating sanctions campaign.

Cumulative Total Hits $1 Billion

The figure represents the running total seized to date, not a single new action announced today.

It builds on earlier milestones, including a major April 2026 freeze of $344 million in USDT on the Tron blockchain.

Bessent had previously reported nearly $500 million in late April, with today’s update reflecting additional freezes accumulated since then.

Operation Economic Fury Accelerates

Launched in March 2025, Operation Economic Fury targets Iran’s sanctions-evasion networks. Iran has relied on stablecoins, particularly USDT on Tron, to move funds for oil sales and IRGC operations.

The U.S. works with issuers like Tether and blockchain analytics firms to identify and immobilize wallets.

Bessent noted Iran previously moved $400–500 million per month through crypto channels before intensified pressure.

Assets are held “on behalf of the Iranian people” and some face claims from terrorism victims.

Expect continued OFAC wallet designations and potential forfeitures in coming months. Iran’s economy already grapples with rial devaluation, banking strains, and reduced oil revenue.

This cumulative milestone marks a significant escalation in financial warfare, showing how traceable blockchain activity can be weaponized against sanctions evasion.

The post US Reaches $1 Billion Seized Iran Crypto to Date: Bessent’s Big Update appeared first on BeInCrypto.

The Sui layer-1 blockchain experienced another disruption on Friday, causing a “network stall” that temporarily halted block production, before normal activity resumed, according to the Sui team.

Network activity “may be paused,” the Sui team said. The network disruption lasted for over three hours and 30 minutes at the time of publication, according to the Sui network’s uptime dashboard.

Sui’s mainnet validators experienced disruptions on both Thursday and Friday. Source: Sui

The last block before the disruption was produced at about 11:51 UTC on Friday, according to the Suiscan block explorer. Network activity on the Sui mainnet resumed at about 3:30 UTC. The Sui team said in an update:

“Both today’s and yesterday’s halts are due to the interaction of the 1.72 release, which introduced address balances and gas charging logic. Yesterday’s implemented fix was an interim measure designed to restore functionality to the network.”

The interim fix had a “low probability” of causing a network disruption, and the long-term software fix has now been implemented by a majority of Sui validators.

Source: Sui

The incident follows several major disruptions and network outages, including Thursday’s outage, which caused a nearly six-hour outage due to a “crash bug in the gas charging logic,” according to the team. The crash was the second major network disruption in 2026.

Related: SUI spikes 50% amid staking moves, zero-fee stablecoins, privacy push

The Sui network went down in January due to a consensus bug

In January, the network went offline for over six hours, halting block production due to a consensus bug. Validators submitted conflicting transactions to the protocol’s checkpoint mechanism, and the network was unable to reach the necessary threshold for consensus, according to the post-mortem report.

Source: Sui

January’s disruption was not caused by network congestion, user funds were “never at risk,” and no “certified transactions” were rolled back, the Sui team said at the time.

“The issue was detected and contained by Sui’s checkpoint certification and quarantine mechanisms, which prevented any user-visible fork at the cost of halting progress,” according to the post-mortem report.

High-throughput smart contract blockchain networks feature several layers, including data availability, transaction execution and validator consensus, which introduce more potential points of failure.

However, network outages in crypto also impact centralized service providers, including exchanges, which have fewer coordination challenges than decentralized blockchain networks.

In May, crypto exchange Coinbase suffered a temporary service disruption due to an Amazon Web Services (AWS) outage, forcing it to switch markets to an “auction” mode before restoring full service.

Magazine: AI-driven hacks could kill DeFi — unless projects act now

ServiceNow (NOW) Stock Rockets 14% on AI Innovations and Software Sector Rally

The Canary tracks the Top 7 contenders for the 2026 World Cup title

Spanish tennis star Rafael Jodar denies pushing ball girl during dramatic French Open win

-

Business5 days ago

Business5 days agoNYT Strands Answers May 24 2026 Revealed for Puzzle No. 812 Theme Summer Essentials

-

Politics4 days ago

Politics4 days agoBridgerton Season 5: Cast, Release Date And Everything We Know So Far

-

Crypto World6 days ago

Crypto World6 days agoRobinhood crypto COO Tanya Denisova exits

-

Tech4 days ago

Tech4 days agoMicrosoft’s quiet Claude Code retreat and the real cost of enterprise AI

-

Business3 days ago

Business3 days agoSelena Gomez Reportedly Upset Over Benny Blanco’s Comments on Her ‘Terrible’ Diet

-

Crypto World3 days ago

Crypto World3 days agoMicron Crosses $1 Trillion Market Cap as AI Demand Reshapes Memory Sector

-

Business4 days ago

Business4 days agoBTS Sells Out Four Las Vegas Shows at Allegiant Stadium for ARIRANG World Tour

-

Tech2 days ago

The Samsung pay deal is the moment Korean unions changed register

-

Tech4 days ago

Tech4 days agoWestone Audio and Etymotic Acquired by Fidelity Collective in Major IEM Market Move

-

Tech16 hours ago

Tech16 hours agoWaymo dominates autonomous vehicle registrations as Tesla trails behind

-

Tech3 days ago

Tech3 days agoMillions of AI agents imperiled by critical vulnerability in open source package

-

Crypto World4 days ago

Crypto World4 days agoNvidia (NVDA) CEO Calls on Super Micro to Strengthen Export Controls Amid Smuggling Probe

-

Tech4 days ago

Tech4 days agoChina assigns ID codes to 28,000+ humanoid robots

-

Crypto World2 days ago

SpaceX’s $2 Trillion IPO: Why Tech Giants Nvidia (NVDA), Apple (AAPL), and Microsoft (MSFT) May Face Pressure

-

Tech3 days ago

Tech3 days agoNASA taps Blue Origin to deliver lunar rovers for Moon Base initiative

-

Entertainment4 days ago

Entertainment4 days ago‘Breaking Bad’ Star’s Easy-to-Binge 6-Part Crime Series Spin-Off Is Finally Heading to Free Streaming

-

Crypto World5 days ago

Brian Armstrong Outlines Crypto Vision for the Future Financial System

-

NewsBeat2 days ago

NewsBeat2 days agoIsrael says it has killed new Hamas military leader in Gaza City airstrikes

-

Business4 days ago

Business4 days agoYatra Online, Inc. 2026 Q4 – Results – Earnings Call Presentation (NASDAQ:YTRA) 2026-05-25

-

Crypto World3 days ago

Crypto World3 days agoSpain blocks prediction markets Polymarket Kalshi

You must be logged in to post a comment Login