Crypto World

Verra Mobility (VRRM) Stock Plummets 46% as Avis Budget Pulls Out of Partnership

Key Takeaways

- Shares of Verra Mobility (VRRM) collapsed more than 46% during Wednesday’s premarket session following Avis Budget Group’s decision to terminate their partnership, set to take effect in September 2026.

- The terminated agreement will eliminate $135M–$145M in annual commercial services revenue and reduce segment profits by $120M–$125M.

- Management slashed 2026 revenue projections to $985M–$995M, a significant drop from the previous $1.02B–$1.03B forecast.

- David Roberts, the company’s CEO, expressed shock and disappointment over the unexpected termination following extensive negotiation efforts.

- Baird analyst David Koning downgraded VRRM from Outperform to Neutral and reduced the price target from $20 to just $8.

Shares of Verra Mobility were hovering around $13.08 during Wednesday’s premarket hours, representing a staggering 46% decline after the company disclosed late Tuesday that Avis Budget Group has decided to end their business relationship. The partnership will officially conclude in September 2026.

Verra Mobility Corporation, VRRM

The Avis partnership represents approximately 13.5% of Verra Mobility’s total 2025 revenue — making this a substantial blow to the company’s financial foundation. Management projects the contract loss will strip away $135 million to $145 million in annualized commercial services revenue, while segment profitability will decline by $120 million to $125 million annually, even before implementing any operational efficiency measures.

David Roberts, the company’s CEO, expressed his candid reaction. “We were surprised and disappointed to receive this notice from Avis Budget Group given our longstanding partnership and the significant time invested by both parties in ongoing extension negotiations,” he stated.

Roberts emphasized that management is now implementing cost reduction strategies, adjusting operational frameworks, and recalibrating the business for future expansion.

Avis Budget Group has not issued a public statement regarding the decision as of this reporting.

Financial Outlook Revised Downward

Verra Mobility has substantially revised its 2026 full-year projections following the contract termination. Total revenue expectations have been lowered to a range of $985 million to $995 million, marking a decrease from the $1.02 billion to $1.03 billion range the company provided just weeks ago.

Adjusted EBITDA forecasts were reduced to $380 million–$385 million, compared to the earlier projection of $405 million–$415 million.

Adjusted earnings per share guidance was lowered to $1.19–$1.25 from the previous $1.32–$1.38 range, while free cash flow expectations dropped to $140 million–$150 million from $150 million–$160 million.

This represents a comprehensive reduction in financial expectations for a company whose commercial division was already showing signs of weakness.

Wall Street Responds

Baird wasted no time adjusting its position. David Koning, an analyst at the firm, downgraded VRRM from Outperform to Neutral while dramatically cutting the price target from $20 down to $8.

Koning highlighted concerns that leverage ratios will now climb to approximately 3.5 times on a pro forma basis. He also warned that should Verra lose contracts with Enterprise or Hertz — both scheduled for renewal during 2027 — the commercial segment’s sustainability would face serious questions. Comparing to similar companies like FISV, FIS, and GPN that trade at 4–7 times 2027 projected earnings with comparable leverage, Baird’s analysis suggests VRRM could be valued between $4 and $8 per share using the same valuation methodology.

According to InvestingPro analytics, six analysts have reduced their earnings projections for the company’s upcoming reporting period.

Before this announcement, Verra Mobility had delivered first quarter 2026 revenue of $223.6 million, slightly exceeding analyst expectations, with adjusted earnings per share of $0.25 compared to the $0.24 consensus estimate. However, commercial services revenue had already declined 4% year-over-year during that period to $97.8 million, a red flag that, in hindsight, signaled potential trouble ahead.

Prior to Wednesday’s dramatic decline, the stock had already fallen 41.6% year-to-date through Tuesday’s market close and was down 44% over the past twelve months. The latest selloff has pushed shares perilously close to the 52-week low of $12.83.

Analyst ‘Reflection’ warned of a brutal Bitcoin liquidation cascade below $59,000, claiming over $1.6 billion in long leverage is stacked in one zone around $58,000 based on CoinGlass data.

“In all my years trading, I’ve never seen this much long-side liquidity stacked in one single zone,” they said on Wednesday.

That liquidation zone is not far away, as Bitcoin fell to $59,175 on Wednesday, matching its early June low.

Everyone will get liquidated

The analyst continued to warn that “Every influencer who screamed ‘the bottom is already in’ is about to get liquidated.” They attached a liquidity heatmap video that visually demonstrates dense long-side positions, framing the potential wipeout as a classic liquidity hunt that historically forms macro bottoms.

“When that liquidity gets taken, there’s nothing left to dump. That’s how every macro bottom has formed.”

Over the past 24 hours, around 178,000 traders were liquidated, with the total liquidations coming in at $984 million, according to CoinGlass. More than 80% of them were long positions.

DUMP BELOW $59,000 WILL BE BRUTAL

In all my years trading, I’ve NEVER seen this much long-side liquidity stacked in one single zone

More than $1.6 BILLION in longs gets wiped if price loses $58,000

Do you understand how much that is?

$1.6 billion in leveraged bets, gone -… https://t.co/kO2kGamdDw pic.twitter.com/WMDK9LIdQr

— Reflection

(@0xReflection) June 24, 2026

CryptoQuant analyst ‘Darkfost’ observed that yearly realized profits eventually fall below the level of realized losses in every bear market.

“It is precisely at that moment that capitulation reaches its bear market peak,” they said.

Currently, the annual average of realized profits remains above realized losses, at $305 billion versus $198 billion, suggesting that further losses are imminent in a final capitulation.

“The market suggests that capitulation could extend further, to the point where annual realized losses become dominant.”

Meanwhile, permabull ‘Sykodelic’ observed that Bitcoin has now reached only 46% of the supply in profit, which equals the 2022 bear market low. However, in this cycle, BTC reached this level after a 52% drop, compared to 2022, which was a 75% drop.

BTC Price Outlook

Bitcoin hit its lowest level for almost two years yesterday, just above $59,000. Asian trading on Thursday morning saw a minor recovery to reclaim $61,000, where it trades at the time of writing.

The $60,000 level is key long-term resistance, with two-year lows around $54,000 being the next major leg down should the predicted liquidity cascade unfold.

Additionally, previous bear market bottoms have also seen a dip below the realized price, which is currently a little over $53,000.

The post Brutal Bitcoin Liquidation Cascade Imminent Below $59K, Warns Analyst appeared first on CryptoPotato.

For centuries, institutions have played a central role in organizing society. Governments enforce laws, banks facilitate financial transactions, courts resolve disputes, and corporations coordinate economic activity. These institutions exist because trust is difficult to establish between strangers. They provide rules, oversight, and accountability that enable large-scale cooperation.

Today, advances in software, blockchain technology, artificial intelligence, and smart contracts have sparked a provocative question: Can code replace institutions?

While code is increasingly taking over functions traditionally performed by institutions, the answer is more nuanced than a simple yes or no. Rather than completely replacing institutions, code is reshaping how they operate and challenging the need for certain intermediaries.

Why Institutions Exist

Institutions emerged to solve coordination problems.

When individuals interact, there are several challenges:

- How can agreements be enforced?

- How can trust be established?

- Who resolves disputes?

- How are resources allocated fairly?

- How can large groups cooperate efficiently?

Historically, institutions answered these questions through legal frameworks, regulations, bureaucracies, and centralized authority.

Banks verify transactions. Governments enforce contracts. Courts interpret laws. Corporations coordinate workers and capital.

Without these structures, large-scale economic and social systems would struggle to function.

The Rise of Code as Governance

Software has gradually automated many institutional functions.

Online platforms process billions of transactions daily without direct human involvement. Algorithms manage logistics networks, coordinate marketplaces, and execute financial operations.

Blockchain technology pushed this idea even further.

Instead of relying on trusted intermediaries, blockchain networks use cryptographic rules and distributed consensus mechanisms to verify transactions and enforce agreements.

The phrase “code is law” emerged from the idea that software rules can automatically determine outcomes without requiring human judgment.

A smart contract, for example, can:

- Hold assets in escrow

- Execute payments automatically

- Enforce lending conditions

- Distribute rewards

- Govern digital organizations

Once deployed, these rules operate independently according to predefined logic.

Areas Where Code Is Replacing Institutions

Financial Services

Traditional banking relies heavily on intermediaries.

Code-based systems can automate:

- Payments

- Lending

- Trading

- Asset issuance

- Settlement processes

Transactions that once required multiple institutions can now occur directly between participants through programmable systems.

This reduces costs, increases transparency, and enables global accessibility.

Corporate Coordination

Digital organizations increasingly rely on software-driven governance.

Voting mechanisms, treasury management systems, and automated workflows allow distributed communities to coordinate without traditional corporate hierarchies.

In some cases, participants can collectively manage resources through transparent rules encoded into software.

Marketplaces

Platforms increasingly automate trust functions once performed by regulators or brokers.

Reputation systems, escrow mechanisms, and algorithmic dispute resolution reduce the need for centralized oversight.

Code enables strangers from different parts of the world to transact with minimal friction.

Information Management

Institutions have traditionally served as gatekeepers of information.

Today, decentralized networks, open databases, and AI systems can organize, verify, and distribute information at unprecedented scale.

The cost of coordinating knowledge continues to fall as software becomes more sophisticated.

The Limits of Code

Despite its capabilities, code has important limitations.

Code Cannot Anticipate Every Situation

The real world is complex and unpredictable.

Laws often contain flexibility because human circumstances vary.

Software, by contrast, follows predefined instructions.

Unexpected events can expose flaws in code that are difficult to address once systems are deployed.

Human Judgment Still Matters

Many institutional decisions involve ethics, context, and interpretation.

Consider issues such as:

- Criminal justice

- Public policy

- Child welfare

- International diplomacy

These areas require values-based decision-making that cannot easily be reduced to programmable rules.

Humans often disagree about what outcomes are fair, making rigid automation problematic.

Disputes Require Resolution

Even when agreements are encoded, disputes still arise.

Questions such as:

- Was fraud involved?

- Was coercion present?

- Were participants adequately informed?

Often require investigation and interpretation.

Code can enforce rules, but it cannot always determine whether those rules should apply in a particular context.

Power Does Not Disappear

A common assumption is that automation eliminates power structures.

In reality, power often shifts rather than disappears.

Developers, protocol designers, infrastructure operators, and platform owners may gain influence over systems that appear decentralized.

The governance of code itself becomes an institutional challenge.

The Future: Institutions Powered by Code

The most likely future is not one where institutions disappear.

Instead, institutions will increasingly integrate software as a foundational layer.

Code excels at:

- Automation

- Transparency

- Consistency

- Scalability

- Efficiency

Humans excel at:

- Judgment

- Ethics

- Adaptability

- Negotiation

- Conflict resolution

The strongest systems will combine both.

Governments may use programmable infrastructure for public services. Financial systems may rely on automated settlement layers. Organizations may use algorithmic governance for routine operations while preserving human oversight for complex decisions.

Rather than replacing institutions entirely, code may transform them into more transparent, efficient, and accessible forms.

Conclusion

The question is not whether code can replace institutions, but which institutional functions can be automated and which require human judgment.

Code is exceptionally effective at enforcing clear rules and coordinating large-scale activity. However, society depends on more than efficiency alone. Trust, legitimacy, ethics, and adaptability remain deeply human concerns.

As technology advances, the future will likely belong neither to pure institutions nor pure code, but to hybrid systems where software handles execution and humans provide governance.

In that world, institutions do not disappear—they evolve.

REQUEST AN ARTICLE

Crypto World

Forget max pain. Bitcoin is well below the $72,000 magnet going into $10 billion options expiry

Bitcoin’s price drop ahead of Friday’s quarterly options settlement has once again cast doubt on the popular “max pain theory.”

The max pain level for this expiry stands at $72,000, significantly above current spot prices of around $61,700. On Friday at 8:00 ET, options worth $10 billion will expire on Deribit, the world’s largest crypto options exchange.

Max pain, as the name suggests, refers to the price level where options buyers – those who purchased call and put contracts to hedge against volatility – would lose the most money on expiry. In that scenario, option buyers suffer maximum losses, while their counter parties who sold options (also known as writers) stand to benefit.

The theory suggests that ahead of expiry, these option writers actively try to push the spot price toward the max pain level, effectively pinning bitcoin there. Crypto social media has long embraced the idea, particularly after BTC appeared to gravitate toward the max pain point ahead of several monthly and quarterly settlements in 2020–2021. That pattern, even if partly coincidental and driven by other market forces, helped solidify belief in the theory.

Key Takeaways

- The prediction market platform is pursuing funding at a $40 billion price tag, approaching twice its May 2026 valuation of $22 billion

- Negotiations could reach completion by the third quarter of 2026

- Should the deal materialize, the company’s value would have multiplied eight times in less than twelve months

- Company leadership has acknowledged exploring a potential public listing, though not anticipated before 2027

- Legal challenges emerged as Kentucky filed suit against Kalshi and four competitors, alleging unauthorized sports wagering activities

The forecasting platform Kalshi is pursuing a significant capital injection that would establish its worth at $40 billion. This represents nearly twice the $22 billion figure achieved during its most recent financing, which concluded in May just weeks earlier.

Reporting from the Financial Times on Wednesday revealed these discussions, citing sources with knowledge of the negotiations. The financing arrangement could potentially finalize during the third quarter of 2026.

Kalshi’s previous capital raise in May — a $1 billion Series F investment — saw Coatue Management take the lead. The investor roster also featured Andreessen Horowitz, Sequoia Capital, Morgan Stanley, and Ark Invest.

Should negotiations conclude successfully at the $40 billion mark, the company’s worth will have expanded eight times over in under twelve months. In October 2025, Kalshi carried a valuation of merely $5 billion.

Widening Lead Over Competition

This prospective valuation would establish Kalshi’s dominance over its primary competitor, Polymarket. Reports from April indicated Polymarket was pursuing investment at a $15 billion valuation.

The competitive dynamics between these platforms have shifted considerably over recent months. Polymarket maintained superiority in transaction volumes throughout much of 2024, propelled by political election activity. Kalshi surged ahead around September 2025 following its strategic alliance with Robinhood to provide sports outcome contracts.

By May 2026, Kalshi reported notional trading activity totaling $17.9 billion monthly. During the identical timeframe, Polymarket registered $7.1 billion, based on Token Terminal figures.

Kalshi functions as a federally supervised exchange within the United States. Polymarket leverages blockchain technology and executes transactions using digital currencies.

Public Offering Under Consideration

Tarek Mansour, Kalshi’s chief executive, acknowledged Wednesday that management is evaluating a public market debut. During a CNBC appearance, he indicated that while an IPO remains under consideration, it wouldn’t occur prior to 2027.

“A company of our financial profile with the rate of growth that we’re seeing, that sort of conversation has to happen,” Mansour said.

The company’s origins trace back to 2018, with its public platform launching in July 2021.

The prediction markets sector is capturing increasing mainstream interest. Meta’s Mark Zuckerberg has allegedly instructed his team to develop a competing prediction markets application called “Arena,” the New York Times reported. Cboe Global Markets, a major exchange operator, also made its entry this week, unveiling “Cboe Predicts” featuring binary contracts linked to the S&P 500.

Regarding regulatory matters, Kentucky initiated legal proceedings against five prediction market operators last week, naming both Kalshi and Polymarket. State authorities claim these platforms operate unlicensed sports gambling services.

The US Commodity Futures Trading Commission has contested this action, maintaining it possesses sole jurisdiction over such platforms. The CFTC filed suit against Kentucky on Tuesday seeking to prevent the state’s regulatory enforcement.

Kalshi representatives declined to provide statements regarding the reported fundraising negotiations.

Key Takeaways

- On June 23, 2026, BlackRock’s Investment Institute issued formal guidance recommending 1–2% Bitcoin exposure in diversified portfolios

- The research was distributed directly to wealth managers and financial advisors, not merely published for institutional audiences

- In a typical 60/40 portfolio, a 1% Bitcoin position accounts for approximately 2% of overall portfolio volatility

- BlackRock’s iShares Bitcoin Trust manages approximately $62 billion, representing nearly 49% of total U.S. spot Bitcoin ETF holdings

- Bitcoin currently trades near $59,692, having declined more than 50% from its October 2025 peak of $126,080

On June 23, 2026, BlackRock’s Investment Institute distributed a detailed research document titled “Sizing Bitcoin in Portfolios” to financial advisors throughout the United States.

The guidance establishes a specific allocation range of 1% to 2% for Bitcoin within conventional multi-asset investment strategies. BlackRock positions Bitcoin as a “complementary diversifier” rather than a primary portfolio component.

Four senior BlackRock officials co-authored the document, including leadership from Digital Assets and Global Portfolio Research. This represents the most explicit portfolio sizing recommendation any major asset management firm has released regarding cryptocurrency.

Understanding the Risk Calculation

BlackRock’s analysis centers on risk contribution rather than purely on potential returns. When added to a traditional 60/40 equity-bond allocation, a 1% Bitcoin position generates approximately 2% of the portfolio’s total volatility.

Increasing the allocation to 2% elevates the risk contribution to roughly 5%. BlackRock notes this matches the risk profile of holding a single stock from the Magnificent Seven technology companies.

Allocations exceeding 2% result in disproportionate risk increases. A 4% Bitcoin position could account for approximately 14% of total portfolio risk, potentially overshadowing other holdings.

This methodology provides advisors with terminology and metrics already familiar to compliance departments and investment committees.

Addressing the Fiduciary Challenge

While Bitcoin ETFs have been accessible to financial advisors, most lacked institutional backing to justify cryptocurrency allocations to clients and regulatory oversight.

BlackRock’s guidance directly resolves this challenge. By comparing Bitcoin to individual equity positions within a risk framework, advisors can now document investment suitability using established portfolio management terminology.

The target audience includes advisors and wealth management firms overseeing trillions in retail and high-net-worth capital. These professionals previously operated without formal Bitcoin allocation standards.

BlackRock has incorporated this allocation methodology into its proprietary Target Allocation ETF model strategies.

Market Position of IBIT

BlackRock’s iShares Bitcoin Trust currently manages approximately $62 billion in total assets. This represents roughly 49% of all U.S. spot Bitcoin ETF holdings.

The product debuted in January 2024 following SEC authorization of spot Bitcoin exchange-traded funds. It attracted substantial capital inflows throughout late 2024 and into mid-2025.

Following a sharp market correction in October 2025, the fund experienced significant redemptions. June 2026 outflows totaled $2.09 billion through June 23.

Institutional capital now comprises approximately 38% of total spot Bitcoin ETF assets, compared to 24% in the prior year.

Bitcoin currently trades around $59,692. This represents a decline of more than 50% from its record high of $126,080 established on October 6, 2025.

BlackRock’s total assets under management reached $13.9 trillion as of Q1 2026.

Stablecore has launched an early access stablecoin and digital asset program for U.S. credit unions, allowing participating institutions to test blockchain-based financial services before deciding whether to integrate them into their banking platforms.

Summary

- Stablecore has launched an early access stablecoin program with Circuit and Curql for credit unions managing about $25 billion in assets.

- Participating credit unions can test stablecoins, tokenized deposits, Bitcoin, staking and crypto payment services before full integration.

- The launch adds to Stablecore’s banking expansion as more U.S. credit unions prepare for potential stablecoin regulation.

The program was announced on Wednesday through a partnership between Stablecore, Circuit, formerly known as Members Development Company, and Curql, a fintech investment collective backed by more than 160 credit unions.

Stablecore said the initial group includes RBFCU, Stanford Federal Credit Union, and La Capitol Federal Credit Union, with the participating institutions representing about $25 billion in combined assets.

Participating credit unions will be able to evaluate stablecoin payments, tokenized deposits, Bitcoin, crypto on and off ramps, staking, and other digital asset services through Stablecore’s platform before deciding whether to offer those products to members. The company said the products are designed to operate within existing digital banking experiences.

“Members trust their credit unions because of their ability to provide secure, trusted access to the financial products and services they care about within a single experience,” said Alex Treece, CEO and co-founder of Stablecore.

He added that the company is helping credit unions “stay relevant against competitive threats, retain their deposits and continue to be the trusted, primary financial partner for their members” by enabling them to offer digital asset products.

Meanwhile, Ethan Cunningham, chief strategy officer at Circuit, said the program gives participating institutions “a collaborative space” to evaluate stablecoins and digital assets together while learning how the technology could shape financial services without moving away from their member-first approach.

According to Stablecore, the program also includes education for credit union staff and members to support future digital asset adoption. The company added that former FDIC regulator Ben Hailey recently joined as head of risk and compliance to oversee governance, risk, and compliance frameworks for partner institutions.

Stablecore expands banking partnerships

The latest initiative builds on Stablecore’s effort to bring stablecoin and tokenized asset services to financial institutions through existing core banking systems. In February, the company joined the Jack Henry Fintech Integration Network, which provides access to about 1,670 bank and credit union core clients.

Stablecore also expanded its banking partnerships in May after the Tennessee Bankers Association selected the company as a preferred digital asset technology provider for its more than 175 member institutions. The agreement gave member banks access to stablecoin accounts, tokenized deposits, crypto-backed lending, payment acceptance, and digital asset accounts through their existing banking systems.

Colin Barrett, president and CEO of the Tennessee Bankers Association, said at the time that customers would benefit from digital asset tools delivered through the “secure and trusted environment of their local bank.”

U.S. credit unions have also begun preparing for potential stablecoin regulation. In February, the National Credit Union Administration proposed a licensing framework that would require payment stablecoin issuers operating through subsidiaries of federally insured credit unions to obtain an NCUA license before issuing stablecoins.

The proposal focused on licensing and supervisory requirements, while additional rules covering reserves, capital, liquidity, and risk management are expected through future rulemaking.

A bipartisan wave of AI tools is moving into retail investing, and U.S. lawmakers are now pressing the Securities and Exchange Commission (SEC) for clarity on how “agentic” trading platforms should be supervised. In a letter to SEC Chair Paul Atkins, a group of Democratic members of the House Financial Services Committee questioned whether the current regulatory framework adequately covers AI-powered investment advice and trading executed on behalf of retail customers.

The lawmakers said that while these tools may begin with limited capabilities, they could rapidly expand into additional asset classes, including cryptocurrency, options, futures, and other derivatives-like products. They warned that the way broker-dealers and AI developers allocate responsibility—especially where platforms disclaim responsibility for outputs—may leave investors insufficiently protected and regulators unclear on enforcement expectations.

Key takeaways

- House Democrats asked the SEC for written answers on how it regulates AI trading agents used by retail investors.

- The letter raises concerns about investor protection, broker-dealer duties, market integrity, and accountability for AI developers.

- Lawmakers highlighted that disclosures often limit platform guarantees and do not clearly establish monitoring, auditing, or responsibility for AI outputs.

- The group requested guidance on when AI agents should register and whether the SEC needs additional authority from Congress.

Why “agentic” trading is drawing SEC scrutiny

The letter centers on AI agents that can initiate or recommend trades based on algorithmic decision-making without traditional human involvement at every step. While the tools may be marketed as convenience features inside consumer trading applications, lawmakers argue they can still produce material trading decisions that affect retail investors.

According to the lawmakers, these systems can operate “largely outside” the securities regulatory framework, even though they are used to make consequential investment choices. The concern is not only technical risk, but regulatory classification: whether the agent’s function constitutes investment advice, brokerage activity, or another regulated service under existing SEC authorities.

From an institutional compliance perspective, the letter underscores a common gap when emerging technologies are deployed quickly: firms may treat AI features as software assistance, while regulators may treat them as advisory or broker-dealer conduct depending on how the product works in practice. That mismatch can create legal uncertainty for both exchanges and AI vendors, particularly around supervisory controls, recordkeeping, and suitability obligations.

Retail-facing tools, disputed responsibility, and the role of disclosures

A focal point of the lawmakers’ concerns is how platforms describe limitations in product disclosures. The letter states that materials accompanying AI agents indicate brokerage platforms cannot guarantee the accuracy or suitability of AI-generated outputs and may not be able to control, monitor, or audit the agents.

Lawmakers argued that such disclaimers raise “urgent questions” about regulatory treatment and create uncertainty about legal responsibility among multiple parties, including brokers, AI developers, and retail investors. This is a key point for risk and governance teams: if an AI system is embedded in a platform that is otherwise acting as a broker or adviser, the platform’s compliance program—supervision, testing, incident response, and documentation—may need to address how the system performs and how it affects client decision-making.

The issue is heightened by the cross-border and cross-entity nature of modern AI deployments. Many AI features are built by third parties, integrated into broker interfaces, and delivered to customers as app functionality. That creates complex lines of accountability, particularly when disclosures attempt to shift responsibility away from the broker.

Scope expansion and crypto’s compliance implications

The letter does not limit the inquiry to traditional equities. Lawmakers warned that agentic trading could expand beyond an initial set of products into others such as options, cryptocurrency, event contracts, and futures. For the crypto industry, this matters because regulatory expectations differ significantly across U.S. agencies and between securities and non-securities products.

The SEC’s jurisdiction is central where the underlying instrument or the advisory conduct implicates U.S. securities laws. But AI agent deployment can also intersect with commodities oversight—especially for crypto-related derivatives and trading structures—bringing the CFTC into the broader enforcement and supervision landscape.

Recent developments illustrate how quickly major crypto platforms are integrating AI features that claim to provide trade guidance. Cointelegraph previously reported that Coinbase introduced an AI agent integrated into its app, describing it as a financial adviser registered with both the SEC and the CFTC that can provide guidance on trades. The lawmakers’ letter points to concerns that such tools may still be effectively operating beyond the securities framework, suggesting that mere registration of an entity or function may not be sufficient if the agent’s behavior, supervision, or outputs are not aligned with regulatory requirements.

For institutional stakeholders, the practical challenge is determining whether existing advice-and-supervision obligations can be met when decision-making is delegated to autonomous or semi-autonomous systems. Compliance programs may need to address questions such as: what constitutes “advice” when generated dynamically; how suitability is assessed when outputs depend on ongoing market signals; and how monitoring is performed when the system’s reasoning cannot be fully controlled by the broker-dealer.

Questions to the SEC and the path toward clearer authority

The House letter—led by Bill Foster, the top Democrat on the House Financial Services Subcommittee on Financial Institutions, and Brad Sherman, the top Democrat on the Capital Markets Subcommittee—requests written responses by July 31. The lawmakers asked for SEC answers covering guardrails and analysis used on AI agent tools, when an AI agent would need to register, and the extent of consultations with broker platforms over AI functionality.

They also asked whether the SEC already has sufficient authority to address the risks posed by AI agents, or whether Congress would need to act to provide additional direction. This is a significant policy point: where regulatory boundaries are uncertain, enforcement can become unpredictable, and firms may face divergent interpretations across jurisdictions.

Representatives Stephen Lynch, Jim Himes, Sean Casten, Rashida Tlaib, Brittany Pettersen, and Sylvia Garcia also signed the letter, signaling that the issue is likely to remain on the agenda for U.S. financial regulators as AI features spread across retail investing platforms.

Closing perspective

For compliance teams and regulated firms, the immediate next step is to monitor the SEC’s written responses and assess whether current AI disclosures, supervisory procedures, and registration positions are sufficient for the regulators’ evolving expectations. The letter also suggests that lawmakers may seek additional legislative or rulemaking action if the agency concludes its existing authority is inadequate to address autonomous trading guidance tools.

By extending its collaboration with long-term local partner SBI Group, Ripple has received approval from the Japanese Financial Services Agency (JFSA) to launch its stablecoin available in the country.

The company’s Senior Vice President of Stablecoins praised the Japanese regulatory environment and called it a leader in cryptocurrency adoption.

RLUSD in Japan

The green light became possible from SBI Holdings, through its Electronic Payment Instruments Exchange Service Provider-licensed subsidiary SBI VC Trade Co., LTD, announced the launch of RLUSD in the Japanese market.

The partners initially signed a memorandum of understanding (MoU) in August this year. They explained this official launch marks the stablecoin’s major entry into one of the most “sophisticated and forward-looking digital assets markets.”

The license from the JFSA reads that RLUSD is described as a new type of electronic payment instrument under the country’s Payment Services Act. It’s designed for foreign-issued stablecoins that ensure the safety and regulatory standards required under local law. The statement added that both institutional and retail users will have access to Ripple’s stablecoin through SBI VC Trade’s VCTRADE platform.

“Japan has long been a leader in digital asset adoption, underpinned by both regulatory clarity and financial innovation. This launch marks an important step in expanding access to transparent, regulated USD-backed stablecoins like RLUSD for financial institutions, consumers, and businesses in Japan,” commented Jack McDonald, Ripple’s Senior VP of Stablecoins.

Meanwhile, SBI VC Trade CEO, Tomohiko Kondo, praised the long-standing partnership between his entity and Ripple, and highlighted RLUSD’s launch in Japan as the latest major milestone reached by both parties.

We’re proud to announce that Ripple USD ($RLUSD) is now officially available in Japan, following approval from the Japan Financial Services Agency (JFSA): https://t.co/5rJZBrFaIM

Through our partnership with SBI Group and @sbivc_official, $RLUSD will be accessible to both…

— Ripple (@Ripple) June 25, 2026

RLUSD Keeps Growing

Despite its then-legal issues in the US, Ripple managed to launch its own stablecoin at the end of 2024. It’s primarily focused on institutions, but it has experienced substantial adoption growth across several fronts in the past two years, including from Mastercard.

The company has collaborated with numerous exchanges to enhance its usability and liquidity. Data from CoinGecko shows that RLUSD’s market cap has grown to $1.6 billion, slightly off the $1.7 billion claimed by Ripple. Nevertheless, it’s still among the 50 largest cryptocurrencies by market cap, and it’s the 10th-biggest in its stablecoin niche.

The post Major Ripple (XRP) Adoption News for Users in Japan: Details appeared first on CryptoPotato.

Key Takeaways

- Historical support at the ETH Realized Price Lower Band near $1,150 suggests a potential 30% decline from current levels

- Spot Ethereum ETFs in the US saw $82.3 million exit on Tuesday, marking the seventh consecutive week of negative flows

- Andreessen Horowitz (a16z) pulled $42.62 million in ETH from Binance on June 23

- Bitmine, backed by Tom Lee, acquired 35,138 ETH valued at $58.65 million, following a $92 million purchase the week before

- Crypto analyst Ted Pillows warns that sellers are preventing rallies beyond $1,700, with new lows likely unless this resistance is broken

Ethereum is hovering near $1,615 on Wednesday, registering a decline of over 3% as bearish momentum persists across various indicators.

An important onchain metric known as the ETH Realized Price Lower Band is currently positioned around $1,150. During previous bear cycles in 2018 and 2022, Ethereum found its floor near this threshold. Should history repeat itself, this indicates a possible additional 30% drawdown from present price levels.

Cryptocurrency analyst Ted Pillows highlighted this vulnerability on social platforms, noting that selling pressure emerges above $1,700 and suppresses upward movement. According to Pillows: “Until Ethereum breaks and reclaims the $1,700 level with strong spot demand, the chances of new lows will go up.” This assessment corresponds with current technical formations.

Examining the price action, ETH is positioned beneath its 20-day, 50-day, and 100-day moving averages, which range from $1,740 to $2,050. The Relative Strength Index stands at approximately 34, indicating deeply oversold conditions.

Should the selloff persist, immediate support exists at $1,611, followed by $1,524, with more substantial backing at $1,404. Dropping below this zone would create a path toward $1,156.

ETH exchange net flows have demonstrated a gradual increase during the past fortnight, indicating more tokens are being transferred to trading platforms — typically interpreted as preparation for selling activity.

Major Institutional Accumulation Continues

Notwithstanding the bearish pressure, significant accumulation is occurring. On June 23, a wallet associated with venture capital powerhouse Andreessen Horowitz (a16z) transferred 25,560 ETH — approximately $42.62 million — out of Binance.

Bitmine, affiliated with Tom Lee, purchased an additional 35,138 ETH valued at $58.65 million on that same date. During the prior week, the company allocated $92 million toward acquiring 52,203 ETH.

Sharplink, ranked as the second-largest Ethereum treasury entity, staked another 509 ETH this week, elevating its cumulative staked position to 22,102 ETH.

Distribution Data Reveals Long-Term Holder Confidence

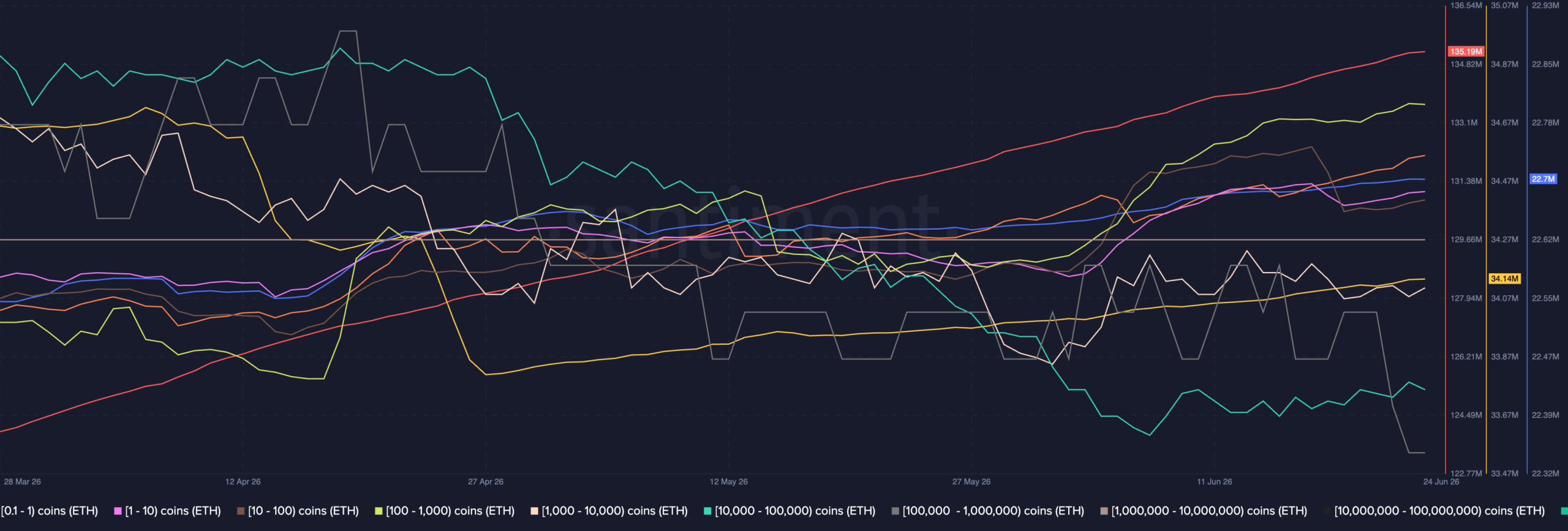

Data from Santiment reveals that the largest whale addresses — those controlling between 10 million and 100 million ETH — have expanded their holdings to approximately 135.2 million ETH. Medium-tier holders have similarly been accumulating since the end of May.

Addresses holding 10,000–100,000 ETH and 100,000–1 million ETH have decreased their positions, pointing to redistribution dynamics rather than wholesale liquidation.

US-based spot Ethereum ETFs experienced outflows of $82.3 million on Tuesday alone. Throughout June, these products have witnessed $346.39 million in withdrawals, following $540.88 million in outflows during May.

MemeCore fell more than 74% in 24 hours, dropping to about $0.7169 on June 25, according to crypto.news price data.

Summary

- MemeCore’s 75% crash erased billions in value and pushed the token below key market-cap rankings.

- ZachXBT’s old warnings returned as traders questioned supply concentration, exchange listings, and thin liquidity.

- The M chart remains bearish, with RSI oversold and MACD still showing strong selling pressure.

The token traded between $0.5055 and $2.92 during the same period, with 24-hour volume at about $22.3 million.

The crash cut MemeCore’s market cap to about $940.9 million. Its fully diluted valuation fell to about $3.85 billion. The token also lost more than 75% over seven days and more than 76% over the past month.

M fell from nearly $3 to about $0.50 within hours, wiping out close to $3 billion in market value. There was no confirmed exploit, hack, or official announcement that explained the sharp move.

The crash also pushed M outside the top group of large-cap tokens after previously trading at much higher valuation levels. MemeCore reached an all-time high of $4.82 on Apr. 24, before the current drawdown.

ZachXBT questions MemeCore after crash

On-chain investigator ZachXBT said on Telegram that M’s FDV fell from about $14 billion to $3.8 billion after a sudden 75% decline on centralized exchanges. He said he, Mlm, and Wazz had earlier pointed to red flags around supply concentration and what he called deceptive user-growth practices.

ZachXBT also said Arkham data showed no single transfer above $50,000 on BSC in more than two weeks. He added that Dexscreener data showed less than $100,000 in total on-chain liquidity on BSC.

The investigator questioned why Binance and Bybit listed M perpetuals, and why Kraken and Bitget listed M spot. He said such “highly manipulated tokens” damage the industry and extract value from retail users.

ZachXBT also replied to MemeCore figure Rudy Rong on X, asking, “How many retail investors lost funds due to the MemeCore teams $M manipulation?” MemeCore had not issued a clear public response to the crash at the time of writing.

Earlier warnings centered on supply

As crypto.news reported in April, ZachXBT had already pressed MemeCore to explain how M reached a multibillion-dollar valuation while a large share of supply appeared concentrated among a few holders. He asked the project to provide data supporting its market cap and claims around insider holdings.

That report also cited blockchain data showing that a Binance deposit address was the largest holder, with about 41.3% of supply. Another wallet held 50 million M tokens, worth about $178 million at the time, or 21.77% of supply.

Previously, crypto.news explored MemeCore’s dilution risk by comparing it with Shiba Inu. The report said MemeCore’s FDV sat several times above its circulating market cap, leaving a large future-supply overhang.

That earlier article noted that only part of MemeCore’s supply was live in the market. It said future unlocks and FDV pressure could become important for price action if demand failed to keep pace.

The latest crash makes those earlier supply questions more urgent for traders. A token can fall fast when liquidity is thin, supply is concentrated, and selling begins on centralized venues.

Technical setup stays weak

The M/USDT daily chart shows a severe breakdown. Price fell from around $2.84 to $0.692 on the day, a drop of about 75.63%. The intraday low near $0.524 shows that buyers did not defend the prior range.

The move broke the sideways zone around $2.80 to $3.20. That shift changed the short-term trend from range-bound trading to a sharp bearish move. Volume rose to about 1.49 million, showing the selloff came with strong trading activity.

The RSI dropped to 18.18, far below its moving average near 45.71. That places M deep in oversold territory. An oversold RSI can support a short bounce, but it does not confirm a recovery after such a large break.

The MACD also remains bearish. The MACD line is around -0.2260, below the signal line near -0.0769. The histogram is negative at about -0.1491, showing sellers still control momentum.

M would need to reclaim lost levels and hold them before the chart looks stronger. A move back above the broken $2.80 area would matter more than a short relief bounce. Until then, the setup remains weak.

Exchange due diligence comes under focus

The crash has shifted attention from price alone to exchange screening. ZachXBT had questioned Kraken’s spot listing in April, citing $7.9 million in suspicious withdrawals to 18 newly created addresses and alleged team-linked transfers to Kraken deposit addresses.

The same April warning accused insiders of pushing M to a $6 billion market cap and $18 billion FDV. The claims remain allegations and have not been independently confirmed by all parties.

The key issue now is whether listed venues reviewed supply concentration, liquidity depth, and market structure before opening M markets. Perpetual futures can add more volatility when the spot market is thin or when real liquidity sits below headline market-cap numbers.

For retail traders, the case shows how fast a high-FDV token can collapse when confidence breaks. MemeCore still trades, but the crash has raised hard questions about liquidity, supply control, and whether exchanges gave users enough protection before listing M.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Wishaw rugby star gains a different cap by graduating from university

Why is Soitec stock rallying today?

Brutal Bitcoin Liquidation Cascade Imminent Below $59K, Warns Analyst

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment4 days ago

Entertainment4 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports2 days ago

Sports2 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech3 days ago

Tech3 days agoMicrosoft accidentally kills epic Outlook email threads

-

Business4 days ago

Business4 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Crypto World1 day ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Politics5 days ago

Politics5 days agoAndy Burnham and the meaning of Makerfield

-

Politics7 days ago

Politics7 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Crypto World1 day ago

Crypto World1 day agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business1 day ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

NewsBeat6 days ago

NewsBeat6 days agoKeir Starmer Allies Question His Chances For No 10

-

Business5 days ago

Business5 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Tech7 days ago

Tech7 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

Crypto World5 days ago

Crypto World5 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World5 days ago

Crypto World5 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World5 days ago

Crypto World5 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Entertainment5 days ago

Entertainment5 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Tech4 days ago

Tech4 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Tech3 days ago

Tech3 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Sports6 days ago

Sports6 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

You must be logged in to post a comment Login