Crypto World

Warsh Confirmation Vote Set for Wednesday

Senator Thom Tillis lifted his blockade of Kevin Warsh’s Federal Reserve nomination on April 27 after the Department of Justice dropped its criminal investigation into current Fed Chair Jerome Powell, clearing the path for a Senate Banking Committee vote on Wednesday.

Summary

- Tillis announced April 27 he would no longer block Warsh’s nomination after the DOJ closed its Powell investigation and redirected oversight to the Fed inspector general.

- The Senate Banking Committee is scheduled to vote on Warsh’s nomination Wednesday, with a full Senate vote expected before Powell’s term expires on May 15.

- Warsh’s confirmation would make him the most crypto-literate Fed chair in history, with prior venture investments across DeFi, stablecoins, Layer 1 networks, and prediction markets.

Warsh confirmation prospects cleared decisively on April 27 when Senator Thom Tillis told NBC’s Meet the Press that he is “prepared to move on with the confirmation of Mr. Warsh” after the Department of Justice dropped its criminal investigation into Fed Chair Jerome Powell over alleged cost overruns on the Fed’s headquarters renovation. The Senate Banking Committee confirmed it will vote on Warsh’s nomination on Wednesday, with a full Senate floor vote expected to follow before Powell’s term expires on May 15.

Warsh Confirmation Clears Its Last Major Obstacle

Tillis had blocked Warsh since January, arguing that the DOJ investigation of Powell was a “bogus and vindictive prosecution” that threatened the Fed’s independence. The block was enough to deadlock the 13-to-11 Republican-majority Banking Committee, as even one Republican defection would have stalled Warsh’s path forward. On Friday, US Attorney for DC Jeanine Pirro announced her office was closing the investigation and handing oversight of the Fed renovation project to the Fed’s inspector general, who had already been conducting a review since last July. CNBC reported that Tillis received assurances from DOJ officials that the probe was “completely and fully ended” and that any future investigation would require a criminal referral from the inspector general, not an executive-branch decision. “I needed to feel like they were not using DOJ as a weapon to threaten the independence of the Fed,” Tillis said. As crypto.news reported, Warsh had already pledged at his April 21 confirmation hearing that he would act as “an independent actor” and had made no commitments to the White House on interest rate decisions.

Why Warsh’s Confirmation Matters for Crypto Markets

Warsh is positioned to become the most crypto-literate Fed chair in the institution’s history. As crypto.news documented, his financial disclosures revealed indirect stakes across DeFi lending, decentralized derivatives, Layer 1 and Layer 2 networks, prediction markets, and Bitcoin payments infrastructure through venture fund structures. He has publicly described Bitcoin as having a positive disciplinary effect on economic policy and told senators at his April 21 hearing that “digital assets are already part of the fabric of our financial services industry.” As crypto.news tracked, Bitcoin climbed approximately 10% to trade near $78,000 in recent weeks as the Warsh confirmation odds improved, with analysts describing him as the most constructive possible outcome for crypto from a Fed chair appointment. Polymarket confirmation odds had fallen to 28% while Tillis held his block, but are expected to surge sharply following Sunday’s announcement.

The Race Against Powell’s May 15 Deadline

The timeline is compressed. Powell’s term as chair expires on May 15, and the Senate historically has rarely confirmed a Fed chair nominee in less than three weeks. The Banking Committee vote on Wednesday must be followed by a full Senate floor vote, and Democratic opposition remains unified. Senator Elizabeth Warren called Warsh a “sock puppet” and said no Republican claiming to care about Fed independence should support moving the nomination forward. As crypto.news noted, the FOMC is also scheduled to meet on Wednesday, with markets expecting rates to remain unchanged for the third consecutive meeting. If Warsh is not confirmed before May 15, Powell has indicated he plans to remain in place as a voting member of the Fed’s board until January 2028, providing continuity even if the confirmation timeline slips.

Acting Attorney General Todd Blanche confirmed Sunday that the investigation is now in the hands of the Fed inspector general and that the DOJ would only reopen a probe if the IG uncovered evidence of criminal conduct and made a formal referral.

Avraham “Avi” Eisenberg, the trader convicted over the 2022 Mango Markets exploit, denied ever threatening to attack Aave (AAVE). His pushback followed an Arkham post claiming his wallet had become active again.

The on-chain analytics firm shared screenshots of a transaction signed by an address tied to Eisenberg. Arkham framed the activity as his potential return to crypto after a prison sentence on fraud and manipulation charges.

Eisenberg Rejects the Threat Framing on Aave

Eisenberg insisted that he never targeted Aave with an exploit, describing the 2022 episode as responsible disclosure. He said he privately notified the team about a potential risk before going public.

“I informed the team privately about a potential risk, then disclosed it publicly after they said they were aware and monitoring,” he explained.

The 2022 narrative traces back to Eisenberg’s attempt to liquidate Curve (CRV) founder Michael Egorov’s large CRV position.

That trade ended with Eisenberg getting liquidated instead. He later went to prison after pleading guilty on a separate charge.

Chaos Labs DM Dispute Adds Heat

Eisenberg also rejected claims from Chaos Labs founder Omer Goldberg, whose firm previously advised Aave on risk parameters. Chaos Labs ended its risk engagement with Aave on April 6, 2026.

Goldberg told Laura Shin’s Unchained podcast earlier in April that Eisenberg had requested access to Chaos Labs’ attack-cost models. The remarks referenced the period after the Mango incident.

“The DM described here never happened,” he articulated.

The dispute revives long-running tensions in DeFi. Probing a protocol’s weaknesses could be seen as a threat or as white-hat work, and the line remains contested.

Eisenberg’s address was never blacklisted, and no fresh exploit activity has surfaced beyond the flagged signature.

The post Aave Dragged Into New Avi Eisenberg Controversy appeared first on BeInCrypto.

Institutional crypto capital is concentrated across a small group of fund managers. From venture and hedge funds to ETFs and asset managers, these firms raise and deploy capital across crypto markets.

Fund Manager of the Year is an award category within The BeInCrypto Institutional 100, an annual research-driven program recognising institutional digital asset excellence across 26 categories and six pillars.

This category sits in Pillar 3: Access to Digital Assets. The 15 firms below are its longlist, drawn from crypto-native fund managers active between April 2025 and March 2026. A shortlist will be named in May 2026, and the winner will be announced at Proof of Talk in Paris on June 2–3, 2026.

- Longlist: 15 firms covering venture capital, multi-strategy hedge, ETF/ETP issuers, and diversified crypto asset management

- Candidates screened: Starting pool of more than 30 crypto-native fund managers; 15 advanced to this longlist, with 5 additional firms held in the outreach pool

- Scoring (Track B): Editorial quantitative 30% | Expert Council 50% | Disclosed data 20%

- Criteria assessed: AUM (assets under management) and growth, investment performance, product suite breadth, institutional credibility, regulatory standing, thought leadership, team quality and stability

- Sources: SEC Form ADV filings (Fortune, April 2026), PitchBook, Tracxn, Crunchbase, Fortune Crypto 40, firm disclosures, and reporting by WSJ, Bloomberg, and other mainstream financial press

| # | Firm | Founded · HQ | Key People | AUM & Recent Fund | Investment Focus | Representative Work |

|---|---|---|---|---|---|---|

| 1 | Grayscale | 2013 · Stamford, USA | Peter Mintzberg (CEO) Michael Sonnenshein (former CEO) |

$35B AUM IPO filed Nov 2025 |

ETF issuer, crypto trusts, index products | Filed for NYSE IPO (2025) GBTC and ETHE dominate AUM |

| 2 | a16z Crypto | 2018 · Menlo Park, USA | Chris Dixon (Founder) Sriram Krishnan (GP) |

$9.5B AUM Fund V targeting $2B |

Crypto venture investing | Fund I returned 5.4x DPI Portfolio includes Coinbase, Uniswap |

| 3 | Paradigm | 2018 · San Francisco, USA | Matt Huang (Co-Founder) Fred Ehrsam (Co-Founder) |

$12.7B AUM New fund targeting $1.5B |

Research-driven venture | Expanding into AI and robotics Backed Uniswap, StarkWare |

| 4 | Pantera Capital | 2003 / 2013 crypto · SF, USA | Dan Morehead (CEO) Paul Veradittakit (Managing Partner) |

Fund V closed 2025 $547M realized on $137M invested |

Multi-strategy venture and tokens | First US Bitcoin fund (2013) 16 portfolio IPOs including Circle |

| 5 | Galaxy Digital | 2018 · New York, USA | Mike Novogratz (CEO) Christopher Ferraro (President) |

Nasdaq-listed (2026) $1.4B project financing |

Diversified crypto platform | Helios data center (1.6 GW) Shifted listing fully to Nasdaq |

| 6 | Haun Ventures | 2022 · Menlo Park, USA | Katie Haun (CEO) Diogo Mónica (GP) |

$2.5B AUM (+30% YoY) Raising ~$1B new funds |

Crypto venture (early + growth) | BVNK and Bridge exits (2025) Only major VC with AUM growth |

| 7 | Polychain Capital | 2016 · San Francisco, USA | Olaf Carlson-Wee (CEO) | $2.6B AUM Multi-fund structure |

Hybrid hedge + venture | Early $1B crypto fund (2017) Active governance across protocols |

| 8 | Bitwise Asset Management | 2017 · San Francisco, USA | Hunter Horsley (CEO) Matt Hougan (CIO) |

$11B+ assets 70+ investment products |

ETFs, SMAs, staking strategies | BITB ETF publishes on-chain data Broad institutional product suite |

| 9 | Multicoin Capital | 2017 · Austin, USA | Tushar Jain (Managing Partner) Kyle Samani (Co-Founder) |

$2.7B AUM Down from 2024 peak |

Venture + liquid tokens | Early Solana backer Leadership transition in 2026 |

| 10 | Electric Capital | 2018 · Palo Alto, USA | Avichal Garg (Managing Partner) Maria Shen (Partner) |

$1B+ raised Early-stage focus |

Infrastructure, developer tooling | Developer Report benchmark Backed Aave, dYdX, NEAR |

| 11 | Dragonfly Capital | 2018 · San Francisco, USA | Haseeb Qureshi (Managing Partner) Tom Schmidt (GP) |

$4B AUM Fund IV: $650M (2026) |

Multi-stage venture | Avoided Terra, Yuga Labs Backed Ethena, Polymarket |

| 12 | CoinShares | 2013 · Jersey | Jean-Marie Mognetti (CEO) Daniel Masters (Co-Founder) |

$6B+ AUM Nasdaq listed (2026) |

Crypto ETPs, asset management | $1.2B SPAC listing (2026) 34% EU ETP market share |

| 13 | Coinbase Ventures | 2018 · United States | Shan Aggarwal (CBO) Justin Mart (Investor) |

500+ investments Funded via Coinbase balance sheet |

Strategic venture arm | Backed OpenSea, FalconX 35+ acquisitions under team |

| 14 | Bain Capital Crypto | 2022 · San Francisco, USA | Alex Evans (Managing Partner) Stefan Cohen (Managing Partner) |

$560M first fund Bain parent $165B AUM |

Early-stage crypto venture | Backed Superstate, M0, Turnkey Linked to Bain Capital platform |

| 15 | Blockchain Capital | 2013 · San Francisco, USA | Bart Stephens (Managing Partner) Brad Stephens (Managing Partner) |

$2B AUM $580M latest fund |

Early-stage through growth | First tokenized VC fund (2017) Backed Coinbase, Kraken |

About This List

The BeInCrypto Institutional 100 — Fund Managers (2026 Long List) identifies crypto-native firms managing institutional capital across venture, hedge, and asset management strategies. These firms raise capital from institutional investors and deploy it across digital asset markets.

Methodology

This category evaluates fund managers under Track B of the BIC 100 methodology: 30% quantitative metrics, 50% Expert Council scoring, and 20% disclosed data.

Assessment spans seven criteria: AUM and growth, investment performance, product breadth, institutional credibility, regulatory standing, thought leadership, and team stability.

Data was verified using SEC Form ADV filings, company disclosures, and private-market sources, including PitchBook, Tracxn, and Crunchbase. Figures reflect the most recent available data at the time of publication.

The post BeInCrypto Institutional Research: 15 Firms Managing Crypto Capital and Liquidity appeared first on BeInCrypto.

Jury selection opened on April 27 in federal court in Oakland, California, in the civil trial pitting Elon Musk against OpenAI and CEO Sam Altman over the company’s transformation from a nonprofit research lab into a for-profit enterprise worth approximately $852 billion.

Summary

- Jury selection began April 27 in Oakland before Judge Yvonne Gonzalez Rogers in a trial expected to last four weeks.

- Musk is seeking to force the return of profits to OpenAI’s nonprofit arm, strip Altman and Greg Brockman of their positions, and reverse the for-profit conversion he argues was illegal.

- Scheduled witnesses include Musk, Altman, Microsoft CEO Satya Nadella, and current and former OpenAI board members, with a remedies phase set for May 18 if the court finds liability.

The Musk OpenAI trial opened on April 27 in Oakland’s federal district court, with jury selection beginning in a civil case that Yahoo Finance reported carries the potential to determine OpenAI’s corporate structure at precisely the moment the company is preparing for a blockbuster IPO. Judge Yvonne Gonzalez Rogers, who is presiding, has described the case as “billionaire vs. billionaire” and will retain ultimate authority over any remedies, with the nine-person jury serving in an advisory capacity only.

Musk OpenAI Civil Trial Puts the Future of the Company on the Stand

Musk co-founded OpenAI in 2015 with Altman and a small group of others as a nonprofit organization explicitly committed to developing AI for the benefit of humanity rather than shareholders. He claims he donated more than $44 million under that premise and that Altman subsequently manipulated the company into a for-profit structure to enrich himself and others, in what Musk’s lawyers called “perfidy and deceit of Shakespearean proportions.” NPR reported that OpenAI’s current valuation sits at approximately $852 billion according to the company’s own court filings, with close to a billion people using its products weekly, making the remedies Musk is seeking among the most consequential ever sought in a Silicon Valley civil case. OpenAI has dismissed the litigation as a campaign driven by jealousy and competitive spite, arguing that Musk was aware of and at times advocated for the for-profit conversion, and that he pushed to fold OpenAI into Tesla before leaving the board in 2018 after a power struggle.

What a Musk Victory Would Mean for OpenAI’s IPO Ambitions

The trial arrives at what may be OpenAI’s most commercially exposed moment. As crypto.news reported, a finding against OpenAI in the Musk lawsuit could disrupt SoftBank’s commitment to OpenAI’s $40 billion funding round, which was already reported to be at risk of shrinking from $30 billion to $20 billion if the company’s restructuring faced legal interference. OpenAI completed a recapitalization in October 2025 that left the nonprofit with a controlling stake in the for-profit business, a structure the attorneys general of California and Delaware approved. Among the remedies Musk is seeking is the forced return of all profits from the for-profit conversion to OpenAI’s charitable foundation, and the removal of Altman and co-founder Greg Brockman as officers. A finding of liability would trigger a separate remedies phase before Judge Gonzalez Rogers alone, beginning May 18.

The Broader AI Governance Question Behind the Lawsuit

Musk has framed the case as having implications well beyond OpenAI. In court filings, he argued that OpenAI’s conduct “could represent a paradigm shift for technology start-ups,” claiming that if allowed to stand, the structural conversion sets a precedent for how AI safety commitments made during nonprofit fundraising can be abandoned for commercial gain. As crypto.news documented, OpenAI has been rapidly expanding its commercial infrastructure into financial services, advertising, and enterprise AI tooling throughout 2026, moves that reinforce how far the company has moved from its founding safety-first mandate. Musk himself has since launched xAI, a for-profit AI competitor, which OpenAI cites as evidence that his lawsuit is commercially rather than ethically motivated. As crypto.news tracked, OpenAI crossed $10 billion in annual revenue in mid-2025 and is projecting close to $30 billion in 2026, a commercial scale that makes the question of who controls the company’s mission more consequential than at any prior point in its history.

Opening arguments are scheduled to follow jury selection on April 27, with the trial expected to run approximately four weeks before the advisory jury delivers its liability finding to Judge Gonzalez Rogers.

The Bitcoin 2026 Conference opened Monday in Las Vegas to a backlash from early adopters. They say the event has drifted far from Bitcoin’s anti-establishment origins.

Speakers include the Securities and Exchange Commission chair, the acting US attorney general, and the Trump family. Purists argue the gathering now celebrates the institutions Bitcoin was built to bypass.

Bitcoin 2026 Conference Stages Wall Street and Washington

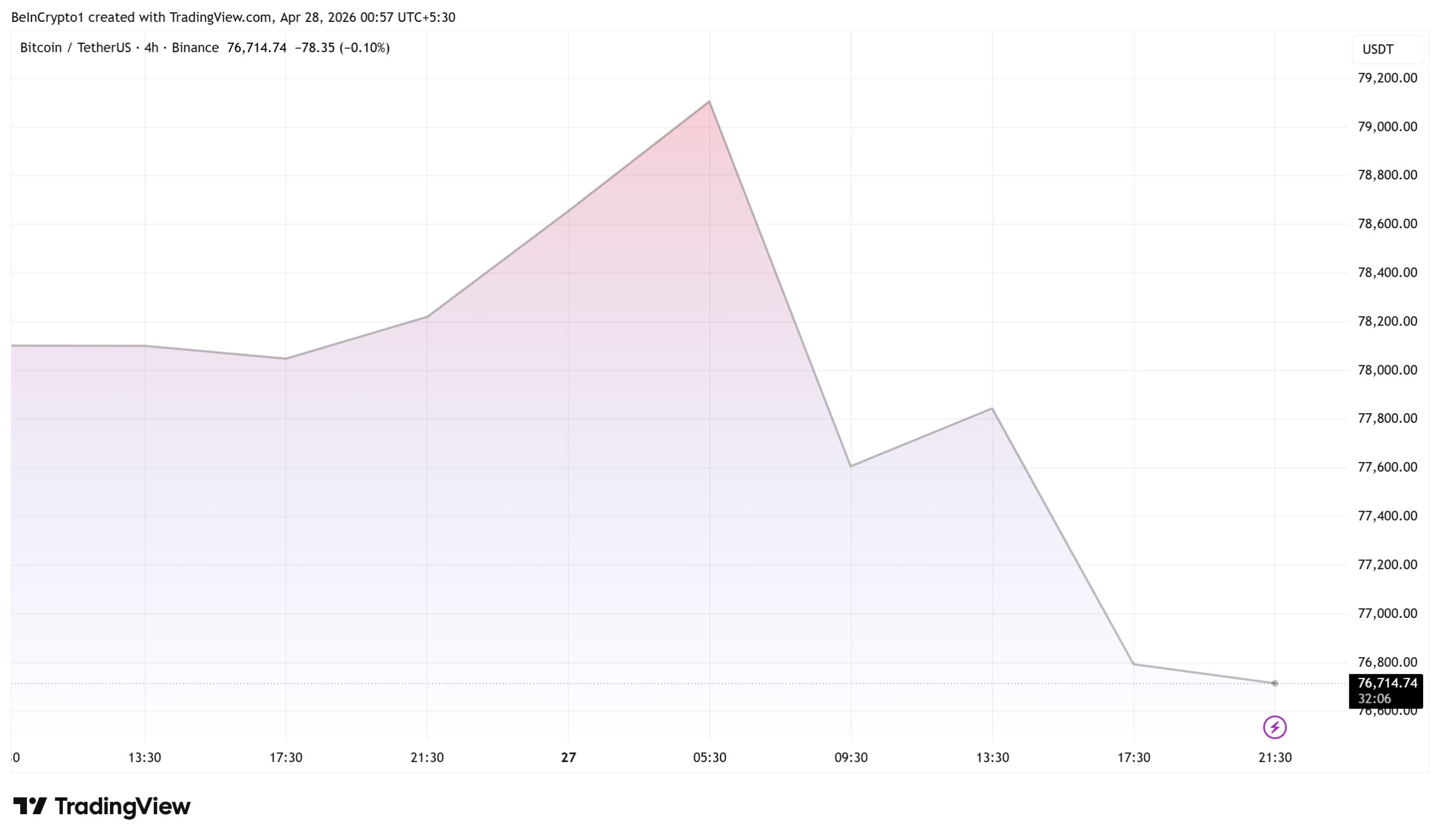

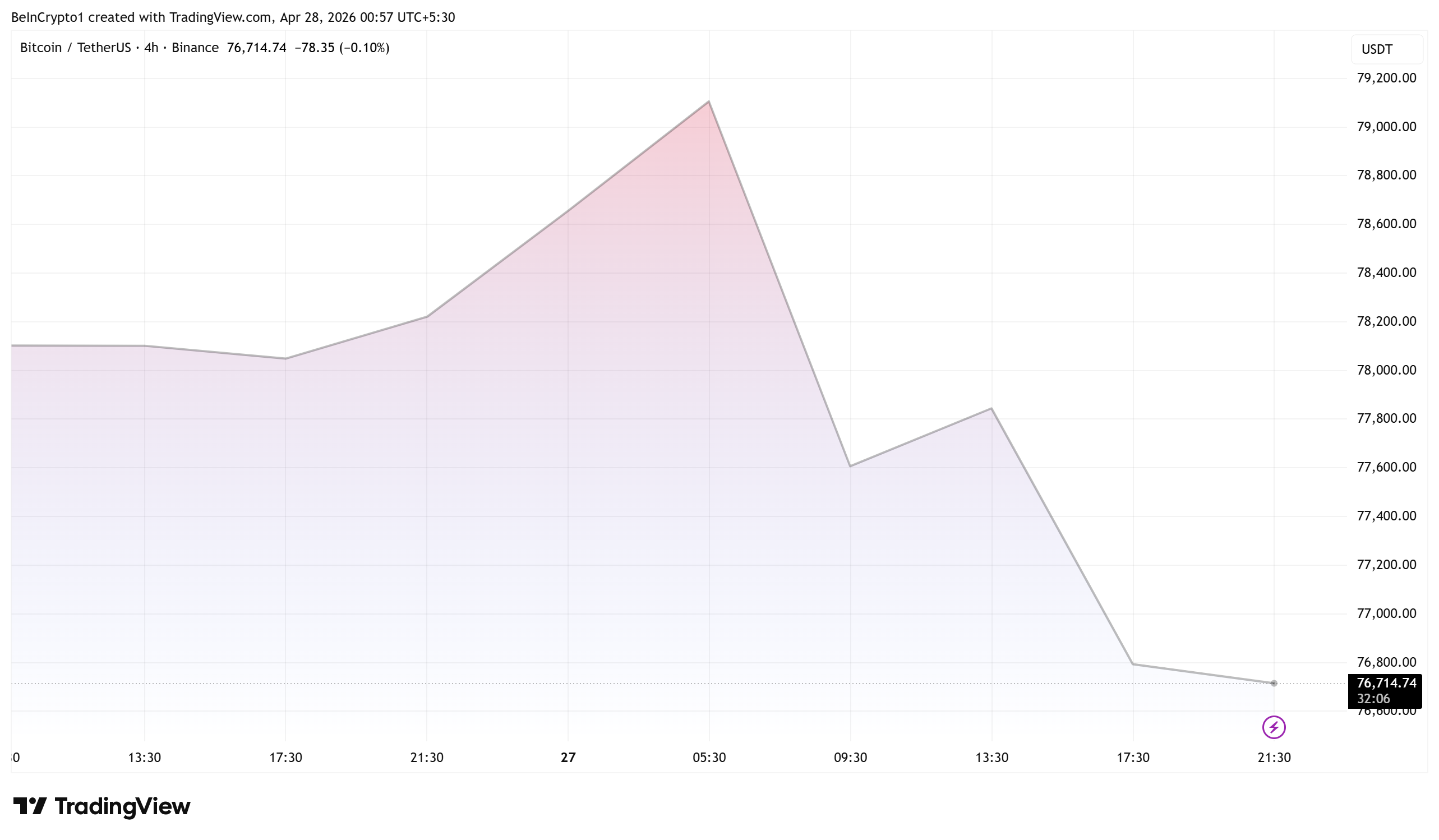

The BTC price was trading for $76,714 as of this writing, recording lower highs on the 4-hour timeframe amid sour sentiment from Day-1 of the Bitcoin 2026 Conference. With this, it has effectively erased all the Sunday gains.

The three-day event runs through Wednesday at The Venetian. Organizer BTC Inc. expects more than 40,000 attendees across 500 scheduled speakers.

The agenda features regulators, lawmakers, and corporate executives. Strategy founder Michael Saylor, Tether chief Paolo Ardoino, and Senator Cynthia Lummis headline the main stage.

US officials carry equal weight. SEC Chairman Paul Atkins, CFTC Chairman Mike Selig, and Acting Attorney General Todd Blanche are all scheduled to appear. Eric Trump represents American Bitcoin as co-founder.

Tickets range from $699 for general admission to $12,999 for the Whale Pass with luxury perks. The official theme this year is “All In On the Future of Money.”

Bitcoin’s Cypherpunk Roots Meet 2026 Reality

Bitcoin emerged from the cypherpunk movement of the 1990s. Satoshi Nakamoto’s whitepaper framed the network as a way to bypass banks and governments.

That positioning is what makes the 2026 lineup jarring for early holders. Many speakers represent the agencies and corporations the protocol was built to route around.

Simon Dixon, an early Bitcoin investor and inaugural conference speaker, posted his frustration on the eve of the event.

“Let’s face it, this Bitcoin conference is compromised. Bitcoin is open source code… It’s a big mistake not to understand the difference,” he wrote.

Supply Shift Worries the Bitcoin Faithful

Beyond the speaker list, critics point to a deeper structural shift. Bitcoin holdings are moving from individual wallets toward spot ETFs, corporate treasuries, and custodial platforms.

That trend pushes a network built for individual sovereignty closer to traditional finance. Self-custody advocates argue the conference now markets products that reverse Bitcoin’s founding promise.

Spot Bitcoin ETFs collectively hold more than a million coins. That concentration would have been unthinkable to the network’s earliest users.

“Meet the 2026 Bitcoin Conference speakers. Or how Bitcoin slowly became the system it was built to escape,” one user quipped.

Other accounts amplify the criticism, framing the lineup as proof of institutional capture rather than mass adoption.

A Conference That Won the Mainstream and Lost the Faithful

BTC Inc. has not publicly responded to the criticism. The conference could win mainstream legitimacy this week. Yet it could also lose the holders who built Bitcoin to escape exactly this.

Sessions through Wednesday will either deepen that divide or test whether institutional adoption can coexist with the cypherpunk crowd.

The post Bitcoin Las Vegas Faces Cypherpunk Revolt Over Regulator-Heavy Lineup appeared first on BeInCrypto.

Industry coalition says JPX’s consultation would add a vague, asset-specific screen to a benchmark that already has objective investability rules.

Nashville, TN — April 26, 2026 — Bitcoin For Corporations (BFC), in coordination with member companies and other affected market participants, today called on JPX Market Innovation & Research, Inc. (JPX) to withdraw its proposed exclusion of companies whose principal asset is cryptoassets from new inclusion in TOPIX and other periodically reviewed indices.

JPXI’s April 3, 2026 consultation does not publicly propose a specific numerical threshold. Instead, it states that, “for the time being,” companies whose principal asset is cryptoassets would be deferred from new inclusion in TOPIX and other periodically reviewed indices. The consultation also states that the proposal would not apply to companies already in the index.

BFC and participating companies oppose the proposal because it is not a true investability rule. TOPIX already has objective criteria designed to protect investability and stability, including liquidity screens, free-float-adjusted market capitalization criteria, continuation buffers, and existing treatment for delistings and other listing-quality events. The proposed crypto-asset exclusion does not measure liquidity, free float, replicability, or listing quality. It instead excludes companies because of the composition of their balance sheet.

“TOPIX is meant to be a broad, neutral, investable benchmark of the Japanese equity market,” said George Mekhail, Managing Director of Bitcoin For Corporations. “If a company satisfies the ordinary market-based eligibility standards, excluding it because of one asset category is not a normal investability screen. It is a policy judgment about one asset class, and it does not belong in the methodology of a flagship market benchmark.”

BFC said the proposal raises four core concerns

- It is not a proper investability rule. The consultation is framed in the language of investability and stability, but the proposed exclusion does not address the criteria that normally determine whether a stock belongs in a broad market index: liquidity, free float, market capitalization, and listing quality. It introduces an asset-specific screen into a benchmark that already has objective eligibility rules.

- It is too vague to administer coherently. The consultation refers to companies whose “principal asset is cryptoassets,” but does not explain how that standard would be applied in practice. It does not say whether the test would be based on parent-company holdings or consolidated holdings, whether it would look through subsidiaries or affiliates, or whether indirect exposure through securities or similar instruments would be captured. A rule that cannot be applied clearly and consistently should not be inserted into a flagship benchmark.

- It creates obvious form-over-substance arbitrage. If direct Bitcoin holdings by a parent company are disfavored, but equivalent exposure through a wholly owned subsidiary, an affiliated company, or a strategic equity position is not, then the rule is targeting legal form rather than economic substance. That would encourage balance-sheet engineering rather than improve index quality.

- It is preemptive and open-ended. October 2026 will be the first periodic review under the next-generation TOPIX framework in which Standard and Growth market companies can become eligible through the new process. Yet JPX is proposing to exclude a category of companies before they have even been assessed under the ordinary criteria. At the same time, the consultation says the exclusion would apply “for the time being,” without setting out a clear review period, exit standard, or sunset mechanism. That is not a disciplined framework. It is an indefinite deferral with uncertain boundaries.

BFC also noted that major global index providers have treated this issue with greater caution. MSCI considered a threshold-based exclusion for digital-asset treasury companies and ultimately did not adopt a blanket exclusion, instead acknowledging the need for further work to distinguish operating companies from non-operating or investment-like entities. FTSE Russell has not announced a comparable blanket exclusion. In BFC’s view, JPX should show the same restraint rather than moving ahead with a crypto-only exclusion before a broader principle has been defined.

More broadly, BFC said the issue extends to the neutrality, credibility, and representativeness of Japan’s flagship equity benchmark.

“If JPX believes there is a broader question about highly concentrated or investment-like companies, then an asset-neutral framework applied consistently would be more appropriate,” Mekhail said. “Singling out one asset class by introducing a vague rule that is easy to evade and difficult to administer would be unprecedented and untethered from TOPIX’s actual investability criteria.”

Bitcoin For Corporations and participating market participants are calling on JPXI to:

- Withdraw the proposed exclusion for companies whose principal asset is cryptoassets.

- Preserve TOPIX as a neutral, broad, rules-based benchmark tied to objective investability and listing-quality standards.

- Refrain from adopting an open-ended deferral without a clear review process, exit standard, or sunset mechanism.

- Engage with issuers and market participants on any broader, asset-neutral framework before changing TOPIX methodology.

Organizations and individual investors may review the full position letter and add their signatures at: topix.bitcoinforcorporations.com

About BTC Inc

BTC Inc. is the world’s leading Bitcoin media enterprise, operating Bitcoin Magazine, The Bitcoin Conference, and Bitcoin for Corporations. Through its media, events, and educational platforms, BTC Inc. delivers trusted news, research, and experiences that advance Bitcoin adoption among individuals, institutions, and enterprises worldwide.

BTC Inc is a subsidiary of Nakamoto Inc. (NASDAQ: NAKA), a publicly held Bitcoin company that owns and operates a global portfolio of Bitcoin-native enterprises.

Forward-Looking Statements

Certain statements in this press release constitute forward-looking statements, as defined under U.S. federal securities laws. Forward-looking statements can be identified by the use of words such as “estimate,” “project,” “predict,” “believe,” “expect,” “anticipate,” “potential,” “intend,” “could,” “would,” “may,” “plan,” “will,” “seek,” “target,” or the negative of such terms or other variations thereof. However, the absence of these words does not mean that a statement is not forward-looking.

Forward-looking statements in this press release include, but are not limited to, statements regarding BTC Inc.’s business plans and strategies, including plans for new products, services, and media platforms; projected or targeted audience size, reach, impressions, and distribution; expected launch dates and production schedules; the Company’s advocacy positions and the expected outcomes of industry and regulatory engagement; and the anticipated role and growth of Bitcoin-related media, events, and educational services.

These forward-looking statements are inherently uncertain and involve numerous assumptions and risks. Factors that could cause actual results to differ materially from those projected include, but are not limited to: (i) the volatility of Bitcoin prices and its effect on audience interest, advertiser demand, and the commercial viability of Bitcoin-focused media; (ii) changes in audience size, engagement, or platform distribution that could affect BTC Inc.’s reach or revenue; (iii) the risk that new products or services, including new media platforms, may not launch on schedule, achieve projected audience levels, or generate anticipated revenue; (iv) the risk that advocacy or industry engagement efforts may not achieve their intended outcomes; (v) dependence on third-party distribution platforms whose policies, algorithms, or terms of service may change; competition from other media companies and content providers; (vi) the evolving regulatory environment for digital assets and its potential impact on BTC Inc.’s operations, content, and audience; (vii) reliance on key personnel and creative talent; the risk that projected audience metrics, impressions, or distribution figures may not be achieved or sustained; (viii) risks associated with the integration of BTC Inc. into Nakamoto Inc.’s operations following the February 2026 acquisition; (ix) general economic conditions and their impact on advertising and events revenue; and (x) other important factors detailed in Nakamoto Inc.’s Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and other documents that are filed, or will be filed, with the SEC and that are or will be available on Nakamoto’s website at www.nakamoto.com and on the website of the SEC at www.sec.gov.

Because Nakamoto Inc. (NASDAQ: NAKA) is the parent company of BTC Inc., investors in Nakamoto Inc. common stock should be aware that the performance and risks of BTC Inc.’s media, events, and educational businesses may affect Nakamoto Inc.’s business, financial condition, results of operations, and stockholder value.

A new policy analysis from Blockchain for Europe contends that the European Union’s landmark Markets in Crypto-Assets Regulation (MiCA) has produced euro-denominated stablecoins that are ultra-safe but commercially weak. The authors argue this has left the bloc lagging behind US dollar–pegged tokens in digital payments, liquidity provision, and on-chain trading, even as the euro remains a dominant global currency. According to Cointelegraph, DeFiLlama data show euro stablecoins account for less than 1% of global stablecoin volume, a stark underutilization given Europe’s broader financial footprint.

Drafted by European Central Bank official Ulrich Bindseil and Blockchain for Europe’s Erwin Voloder, the report centers on MiCA’s rules for euro electronic money tokens (EMTs). These tokens must be fully backed and are prohibited from paying interest. That remuneration ban was intended to prevent stablecoins from acting as deposit substitutes; however, the authors argue it pushes MiCA-compliant euro EMTs into a “downward-sloping” portion of a regulatory Laffer curve, where heightened restrictions depress the activity the framework is designed to govern. In a world of rising rates, the zero-interest remit is presented as a structural handicap.

The paper also takes aim at MiCA’s reserve requirements, noting that at least 30% of EMT reserves must be held as bank deposits, a threshold that climbs to 60% for significant issuers. The authors call this provision a feature not paralleled in stablecoin regulation abroad and advocate a shift toward a principle-based approach compatible with the EU’s Liquidity Coverage Ratio (LCR) framework and a broader mix of high-quality euro assets. Rather than a wholesale rewrite, the study urges targeted reforms to EMT reserve, remuneration, and transparency rules while proposing that large issuers should have carefully bounded access to central bank settlement accounts during severe stress scenarios.

Key takeaways

- MiCA’s euro EMT framework prioritizes safety and transparency but may curtail market activity by prohibiting yield on reserves and imposing strict reserve-rule thresholds.

- DeFi and on-chain liquidity in euro stablecoins remain disproportionately small relative to Europe’s financial scale, suggesting a competitive gap with USD-backed tokens and their yield mechanisms.

- A shift toward principle-based liquidity standards and a broader asset mix could preserve safety while improving competitiveness for euro EMTs.

- The debate feeds into broader policy considerations about MiCA 2.0, with regulators weighing safety safeguards against the need for market maturity and cross-border competitiveness.

- Stability and supervisory concerns persist, including potential concentration of demand in euro-area sovereign bonds during redemptions and the risk of regulatory arbitrage if safeguards are weakened.

MiCA’s euro EMT framework: safety versus market relevance

The analysis underscores a fundamental tension in MiCA’s euro EMT rules. By mandating full collateral backing and banning remunerations, the framework aims to curb the risk that EMTs become mere substitutes for bank deposits. Still, the authors argue that this combination—strict safeguards paired with zero interest—creates a competitive disadvantage in a positive-rate environment. In practice, euro EMTs may appeal to risk-conscious institutions seeking stability, but their utility for yield-seeking users or liquidity providers could be limited relative to dollar-pegged tokens or euro-denominated products that distribute yields through alternative mechanisms.

Beyond the remuneration constraint, the 30% reserve floor (60% for larger issuers) is highlighted as a distinctive EU feature. The report contends that these thresholds are not aligned with comparable regimes in other major jurisdictions, potentially raising funding costs and dampening liquidity. The authors propose replacing rigid numeric thresholds with a more flexible, risk-based regime that mirrors the EU’s LCR language and would allow a diversified reserve mix consisting of high-quality euro assets that meet liquidity objectives without the rigidity of a fixed percentage.

Regulatory context and policy debate

The paper situates its recommendations within a broader, ongoing policy conversation around MiCA’s global competitiveness. As Europe contemplates “MiCA 2.0,” officials signal a willingness to revisit the framework to keep pace with market maturation, a stance echoed by Brussels’ policy discourse. At the same time, supervisory authorities warn against diluting safeguards. The European Banking Authority (EBA) has warned that proposed changes to MiCA’s technical standards could erode protections and elevate arbitrage risk if not carefully calibrated. This tension highlights the high-stakes balancing act facing regulators: foster innovation and cross-border activity while preserving safety and financial stability.

On a cross-jurisdictional basis, comparisons with U.S. policy are instructive. The US Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act, which prohibits interest payments on balance holdings of payment stablecoins, shares a similar safety motive but operates in a different market architecture. In the U.S., dollar-pegged stablecoins remain central to DeFi lending pools and other on-chain yield strategies, which helps attract liquidity without issuer-paid yields. The divergent design choices between MiCA and U.S. policy frameworks illuminate how regulatory intent translates into distinct market structures and risk profiles.

Stability considerations and macroprudential context

Macroprudential analysis from the European Central Bank this year has drawn attention to the potential systemic implications of large-scale euro-stablecoin adoption. The ECB cautions that significant growth in euro stablecoins could concentrate demand in short-dated euro-area government bonds, potentially impacting yields and liquidity during periods of redemptions. The report’s authors echo the concern that supervisory frameworks must carefully manage these dynamics as stablecoins scale within Europe’s financial ecosystem. In this view, the rigidities embedded in MiCA’s EMT rules could hamper timely risk management and liquidity provisioning in stress scenarios, unless reforms are crafted to preserve both safety and operational resilience.

Overall, the analysis frames MiCA’s euro EMT regime as a carefully calibrated, safety-first model that may need calibrated adjustments to remain effective as markets mature. The authors advocate a targeted reform path rather than a sweeping overhaul, arguing that a more flexible reserve and remuneration regime, grounded in robust liquidity standards and asset diversity, would better align EU policy with evolving market practice while maintaining the protective intent of MiCA.

Prospects for MiCA 2.0 and regulatory oversight

The report arrives as policymakers weigh the scope of a potential MiCA 2.0 overhaul. Proponents argue that updates could refine liquidity principles, enhance transparency, and ensure Europe remains competitive in a global digital-asset landscape. Critics, however, warn that loosening safeguards could invite arbitrage and stability risks if not matched with rigorous supervisory standards. Regulators are likely to consider empirical evidence from market development, including euro-stablecoin usage, cross-border settlements, and the resilience of EMT issuers under stress.

For market participants—issuers, banks, exchanges, and institutional allocators—the discussion signals a shifting preference for clarity on reserve composition, yield mechanics, and settlement access. The policy trajectory will bear on licensing decisions, cross-border cooperation, and the integration of stablecoins with traditional payment rails and central-bank money infrastructure. In particular, the debate touches on licensing regimes for EMT issuers, eligibility criteria for settlement accounts, and the alignment of EMT operations with AML/KYC frameworks and broader compliance standards.

Closing perspective

As Europe weighs refinements to MiCA, the central questions revolve around preserving financial stability and investor protection without stifling innovation or liquidity. The ongoing dialogue signals a nuanced policy path: targeted adjustments that acknowledge market realities while retaining the safeguards essential to regulatory resilience. Watch for further regulatory filings, official statements, and sectoral feedback as MiCA’s evolution continues to unfold, with implications for institutions, markets, and cross-border operations alike.

The $500 million superyacht Nord, linked to sanctioned Russian billionaire Alexey Mordashov, transited the Strait of Hormuz over the weekend. The crossing has drawn fresh scrutiny to gaps in Western sanctions enforcement.

The 142-meter Lürssen-built yacht sailed openly from Dubai to Muscat between April 24 and 26. It broadcast its position via the automatic identification system while commercial shipping stalled at both ends of the chokepoint.

Sanctions On Paper, Not At Sea

Mordashov has carried United States, European Union, and United Kingdom sanctions since 2022 over his close ties to Vladimir Putin.

The designations cite his roughly 77% stake in Severstal, Russia’s largest steelmaker. They also target his interests in Bank Rossiya and state-aligned media.

The yacht itself has never been seized. Public registries do not list Mordashov as the owner. Shipping records instead tie Nord to a Russian firm controlled by his wife, Marina Mordashova. The structure is widely seen as a buffer against Western asset freezes.

Reuters reported the vessel departed a Dubai marina at around 1400 GMT on April 24. It crossed Hormuz the next morning and reached Muscat early Sunday. MarineTraffic data tracked the route in real time.

Selective Passage Through Hormuz

Hormuz traffic has collapsed since the United States imposed a maritime blockade on Iranian ports on April 13.

Daily transits have fallen from roughly 140 vessels to single digits. Hundreds of tankers now wait at both ends of the strait.

Iran has granted preferential passage to Russia-linked vessels under a 2025 cooperation pact, according to reporting from The Independent.

Nord followed an Iranian-declared safe lane south of Larak Island while bound for Oman. The route placed it outside the US enforcement focus on Iranian-port traffic.

The crossing illustrates how layered ownership structures and aligned host states insulate sanctioned Russian assets from coordinated Western action.

Broader maritime restrictions continue to tighten elsewhere across the Gulf.

The post Sanctioned Russian Billionaire’s $500 Million Yacht Slips Through Hormuz Blockade appeared first on BeInCrypto.

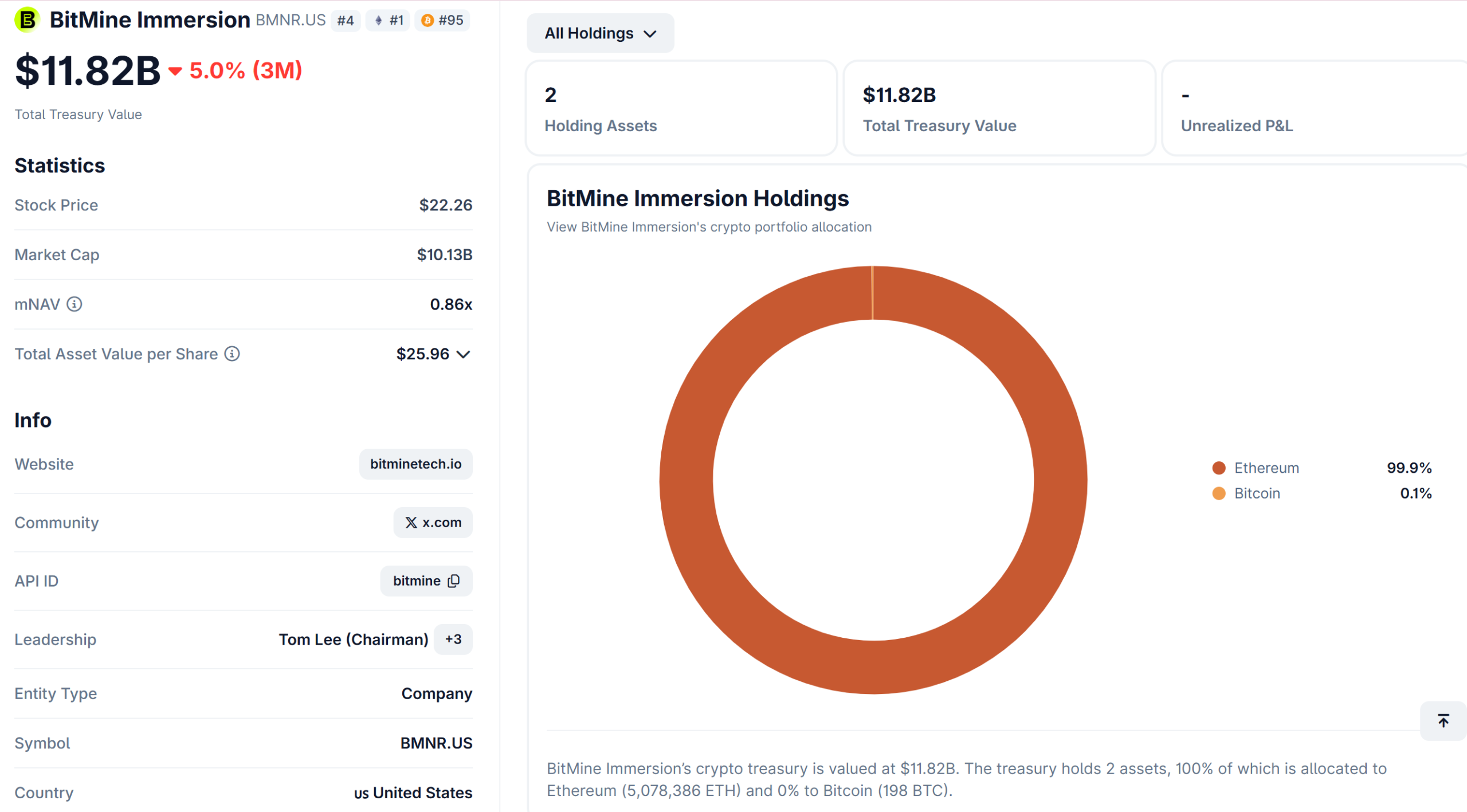

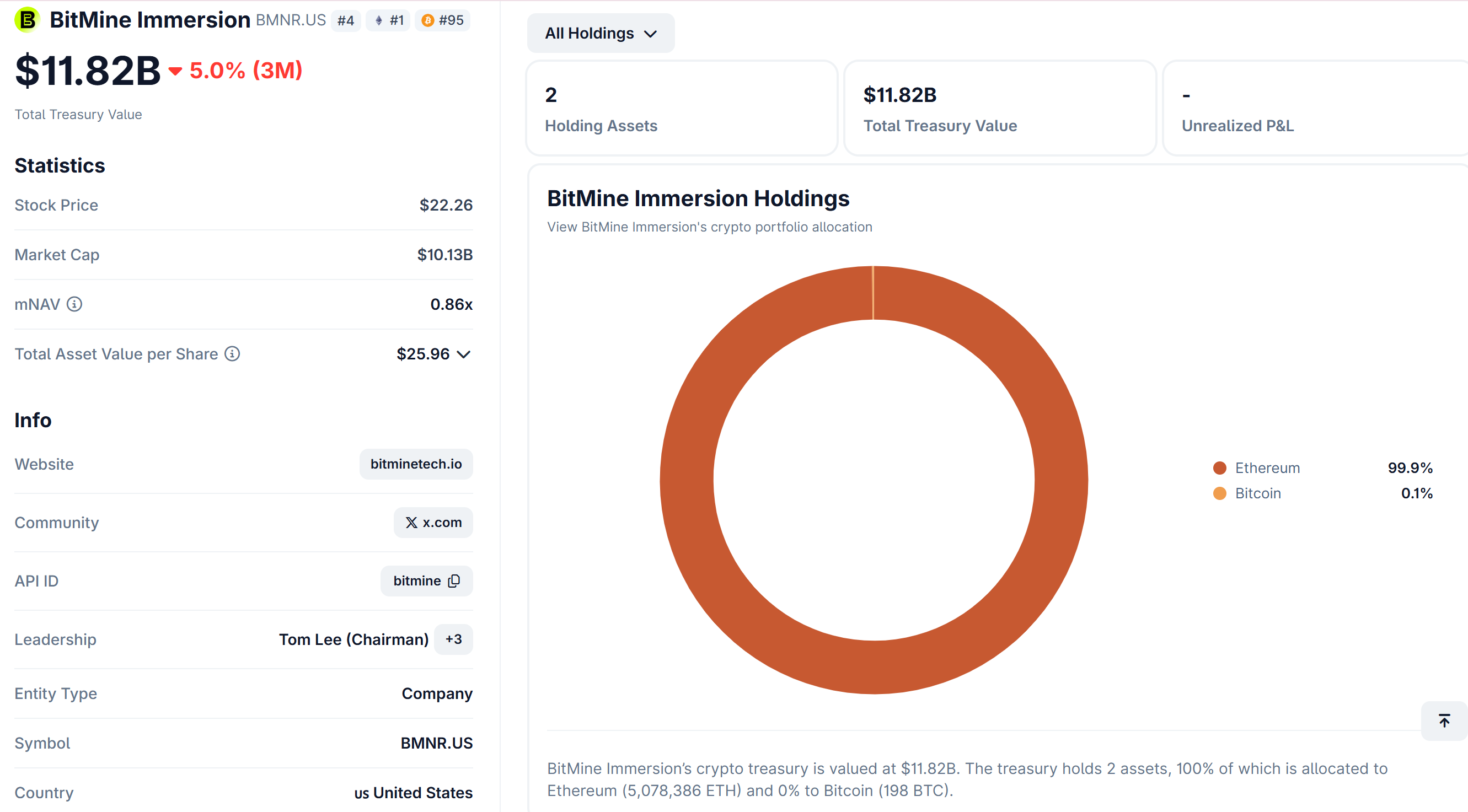

BitMine Immersion Technologies, the Ether treasury company backed by Fundstrat’s Tom Lee, expanded its ETH holdings for a second straight week, purchasing an additional 101,901 ETH last week. The new addition lifts BitMine’s ETH stash to roughly 5.08 million and pushes its overall crypto-and-cash reserves to about $13.3 billion, according to market tracking and disclosures cited by industry observers.

The ongoing accumulation comes even as the firm sits on sizable unrealized losses tied to its ETH tranche, highlighting the risk-reward calculus involved in large-scale crypto treasury management during periods of elevated volatility.

The latest buy follows an earlier move of 101,627 ETH a week prior, which Cointelegraph described as the largest accumulation by BitMine since December 2025. That earlier purchase was noted by Cointelegraph as a notable uptick in sustained treasury buying during a period of price fluctuations for Ether.

In addition to the hard-layer exposure, BitMine’s public disclosures show a substantial gap between the book value of its ETH holdings and the current mark-to-market value. Unpacked, the company’s unrealized losses on the ETH treasury exceed $6.5 billion, based on total investments around $17.6 billion. The figure underscores how recent Ether price swings have amplified the drag on balance sheets even as the company continues to deploy capital into ETH.

The stock market side of BitMine reflects a separate pressure. BMNR, the NYSE-listed ticker for BitMine Immersion Technologies, has declined more than 20% year-to-date, according to Yahoo Finance data. That performance contrast—strong buy activity in the treasury alongside a downbeat equity mood—illustrates the divergent paths crypto-focused corporates can navigate when asset prices and broader risk sentiment diverge.

Nevertheless, BitMine has not stood idle on the yield front. The company reports staking roughly 3.7 million ETH, a step that generates rewards by contributing to Ethereum’s security and transaction validation process. In a market where price moves dominate headlines, staking offers a potential ongoing income stream that can help offset some near-term declines, though it does not fully shield balance sheets from drawdowns during sharp downturns.

Context for these moves is crucial. Ether’s price action in recent weeks has offered a glimmer of stabilization after a wave of declines through March. Ether rebounded above $2,400 last week after a dip to around $1,800 earlier in the year, according to TradingView data cited by Cointelegraph. Even with the rebound, Ether remains well below its year-to-date highs, and the asset remains roughly 23% lower on the year. The broader market backdrop—an improving tilt in risk assets alongside still-fragile sentiment—helps explain why treasury players like BitMine are doubling down on holdings amid volatility.

Analysts and market observers point to the tension at play in large crypto treasuries: the upside of accumulating strategic reserves during price weakness versus the downside of mark-to-market losses when markets turn against those accumulations. The yield from staking provides a counterpoint to this risk, but it does not replace the need for discipline in capital deployment or risk management. For investors and managers alike, the question remains how much longer these large-scale purchases can continue if Ether’s price remains volatile or if regulatory and macro conditions shift meaningfully.

BitMine’s approach also highlights a broader question for corporate and institutional treasuries in crypto: when does ongoing accumulation begin to tilt the balance toward longer-term strategic positioning vs. the immediacy of mark-to-market volatility? The company’s leadership—backed by notable figures such as Fundstrat’s Tom Lee—appears to envision a thesis where continued accumulation is part of a multi-year strategy, but the path is clearly defined by price cycles, staking yields, and the evolving risk landscape.

Additionally, observers are watching how such treasury strategies interact with the broader market’s liquidity environment. As Ether price cycles evolve, the ability of large holders to realize or offset losses may hinge on liquidity, staking rewards, and the pace at which new capital can be deployed without triggering outsized price impact. In this context, BitMine’s ongoing purchases and staking activity provide a real-world case study in how corporate crypto reserves can navigate a choppy market while pursuing yield-generation opportunities.

What comes next remains uncertain. If Ether continues its tentative stabilization alongside a broader improvement in risk appetite, BitMine and peers may press further into accumulation, potentially signaling institutional confidence in Ethereum’s long-run fundamentals. Conversely, renewed volatility or macro headwinds could test the durability of this strategy and the capacity of treasuries to sustain large, mark-to-market losses while maintaining growth of reserves and yield streams.

As investors weigh these developments, market watchers will monitor Ether’s price trajectory, staking yields, and corporate treasury disclosures for signs of how risk-taking is evolving in crypto-native balance sheets. The coming weeks will be telling in whether BitMine’s strategy proves resilient amid ongoing price swings or whether the unrealized losses will force a re-evaluation of appetite for heavy ETH exposure.

Watch next for how Ether’s price action interacts with treasury strategies across the sector, and whether BitMine’s continued purchases will influence market sentiment or simply reflect a broader risk posture among crypto-linked enterprises.

References: Wu Blockchain reported the latest ETH purchase; Cointelegraph noted the prior week’s 101,627 ETH as the largest accumulation since December 2025; Dropstab data cited unrealized losses topping $6.5 billion on a roughly $17.6 billion ETH portfolio; Yahoo Finance tracks BMNR stock performance; Ether price context drawn from TradingView data via Cointelegraph.

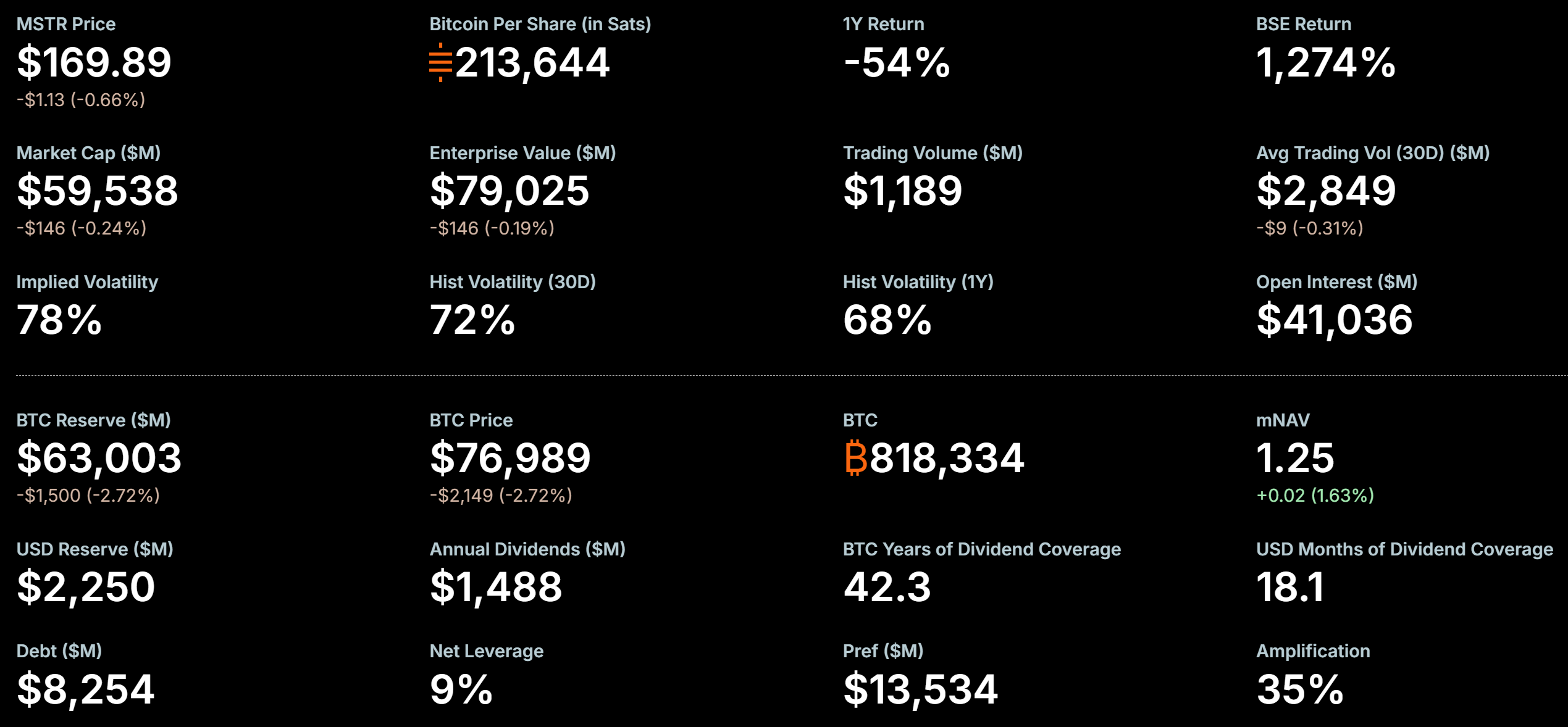

MicroStrategy and BitMine Immersion Technologies are racing toward different crypto accumulation targets. BitMine has pulled ahead. The Ether treasury is 16% short of its goal, while Strategy still trails by roughly 18%.

BitMine crossed 5 million Ether (ETH) on April 27, a milestone that puts it 84% of the way to 5% of all ETH. Strategy holds 818,334 Bitcoin (BTC) and is 181,666 tokens short of 1 million.

Race to Corporate Crypto Dominance

BitMine, chaired by Tom Lee, holds 5.078 million ETH worth roughly $11.5 billion at $2,314 per coin. The company adds $940 million in cash, $200 million in Beast Industries, and $91 million in Eightco Holdings. Total assets reach $13.3 billion.

MicroStrategy, led by Executive Chairman Michael Saylor, has paid an average of $75,537 per BTC. Its cost basis sits at $61.81 billion. The latest weekly purchase added 3,273 BTC for $255 million at $77,906 per coin.

BitMine Has the Shorter Runway

BitMine needs about 1 million more ETH to reach its 5% of supply goal. At current prices, that means roughly $2.4 billion in additional buying.

Meanwhile, MicroStrategy needs nearly $14 billion at $77,000 per BTC. The dollar gap is almost six times (6x) larger. BitMine could close that gap with a single quarter of capital raising at recent run rates.

The funding model differs. MicroStrategy raises capital through STRC perpetual preferred shares and at-the-market equity sales.

The company carries $8.25 billion in debt and $13.53 billion in preferred stock. Annual dividend obligations sit at $1.49 billion on a non-yielding asset.

BitMine generates yield. The company stakes 3.7 million ETH through its Made in America Validator Network (MAVAN) platform at roughly 3%.

That produces $264 million in annualized revenue. Full staking would push rewards toward $363 million a year.

Are Bitcoin and Ethereum the Ultimate Winners in Any Scenario?

MicroStrategy reaching 1 million BTC would lock up 4.76% of Bitcoin’s capped supply under one corporate roof.

“Based on their 2026 average weekly buys, they will have 1 Million Bitcoin by December of this year. 1M BTC is 4.76% of the ending total supply once fully mined. Why do I buy MSTR? Duh,” remarked one investor.

Persistent absorption at that scale shrinks the float available to spot markets. That could pressure BTC higher in tight liquidity conditions.

However, BitMine controlling 5% of Ethereum carries a different effect. Most of those coins remain staked, removing them from the circulating supply while reinforcing network security.

The combined accumulation and staking lockup may amplify ETH price sensitivity to fresh demand.

“If just 3-4 more institutions follow BitMine’s playbook, we’re looking at a supply crisis that makes 2021 look tame…319K ETH removed + staking lockup = deflationary pressure accelerating…$15K ETH by December isn’t optimistic. It’s mathematical inevitability if this institutional FOMO spreads. Smart money is positioning NOW. Retail will chase at $8K+,” wrote investor and technologist Paul Barron.

Tom Lee has framed Ether as a store of value and collateral for tokenized finance. He points to its outperformance versus the S&P 500 since geopolitical tensions escalated.

The growing demand for tokenization and AI-driven blockchain infrastructure adds to the case.

BitMine trades $845 million a day on the NYSE main board, ranking 129th among US-listed equities. The investor roster includes ARK Invest’s Cathie Wood, Founders Fund, Pantera Capital, Galaxy Digital, and Kraken.

Strategy’s MSTR, on the other hand, sits at a 1.25x premium to net asset value.

BitMine looks set to cross the line first if its current pace and capital access hold.

While this could mean ETH outperforms BTC, it depends on how cleanly both treasuries fund the final stretch.

The race may also test whether Saylor’s pace of 5,250 BTC a week remains repeatable over the next eight months.

The post MicroStrategy vs Tom Lee’s BitMine: Who Hits Target First? appeared first on BeInCrypto.

Key takeaways:

- Persistent spot market accumulation from Bitcoin ETFs and Strategy provided a price floor for Bitcoin and threatens to trigger a short squeeze.

- Negative funding rates and cautious options skews could trap bears if the Federal Reserve policy shifts or high oil prices trigger higher inflation.

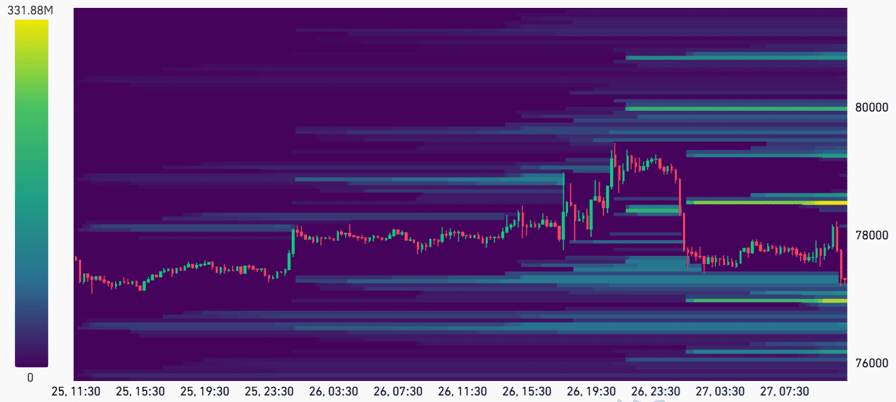

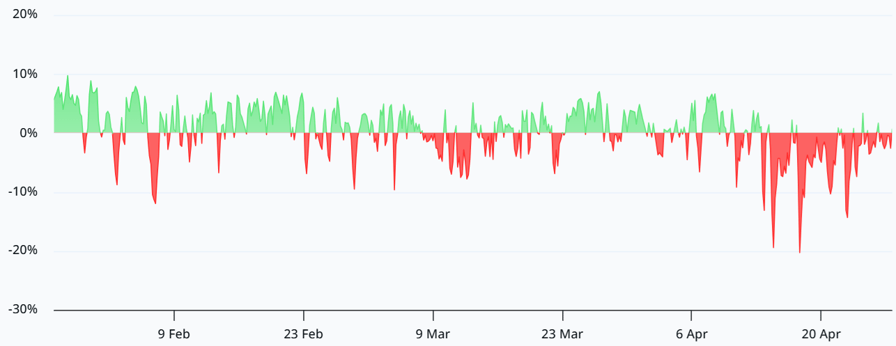

Bitcoin (BTC) price sustained levels above $76,000 for the past week, distancing itself from its year low at $60,500. The recent bullish momentum came as crude oil prices jumped above $100 and the S&P 500 hit new trading highs, but futures market data may point to a short-term rally-ending outcome for Bitcoin.

A total of $1.4 billion in leveraged short positions near $80,000 has been built over the past 48 hours, according to CoinGlass data, and Bitcoin’s rejection at $79,500 has raised alarm.

Estimated Bitcoin futures liquidation levels, USD. Source: CoinGlass

Federal Reserve decision, inflation data may push Bitcoin above $80,000

The lack of investors’ appetite for bullish Bitcoin leverage has been evident, but a bear trap could spring if the US Federal Reserve adopts a less restrictive monetary policy or if investors anticipate higher inflation, which would reduce the expected net returns from fixed-income assets.

Bitcoin perpetual futures annualized funding rate. Source: Laevitas

The Bitcoin perpetual futures annualized funding rate has remained mostly negative over the past two weeks, a typical sign of growing bearish confidence. Curiously, this happened while Bitcoin’s price jumped to $78,000 from $72,000 on April 9 and most of those bets are at a loss at $76,700. A rally above $80,000 would likely force traders to close their positions.

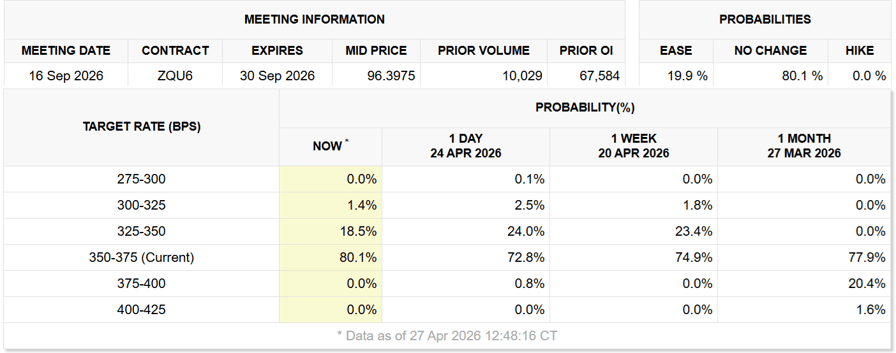

Data show investors are no longer anticipating interest rate hikes from the Fed, even as Brent crude prices have reclaimed the $100 level. The pressure from high energy prices has a cascading impact on inflation expectations, but the Fed is also concerned with the weakening job market and economic growth.

Implied target rate probabilities for Sept. 16 Fed meeting. Source: CME FedWatch tool

US government bond futures contracts presently indicate 20% odds of interest rates decreasing by September, marking a complete turnaround from one month prior. Traders realized that the Fed is in a tough spot, hence the 3.95% yield on 5-year US Treasury became less appealing. An interest rate cut exerts upward pressure on inflation.

Sustained spot Bitcoin buying supports BTC’s bullish momentum

Bitcoin’s bullish momentum has been driven by the spot market, evidenced by Strategy (MSTR US) adding $255 million in BTC between April 20 to April 26 and the $824 million net inflows into US-listed Bitcoin exchange-traded funds (ETFs). Bitcoin buyers continued to accumulate despite the failed attempts to hold above $79,000.

Related: Critical Bitcoin trend change in works, but analysts say daily close above $80K required

To determine if professional Bitcoin traders are effectively leaning bearish, one should assess the options markets.

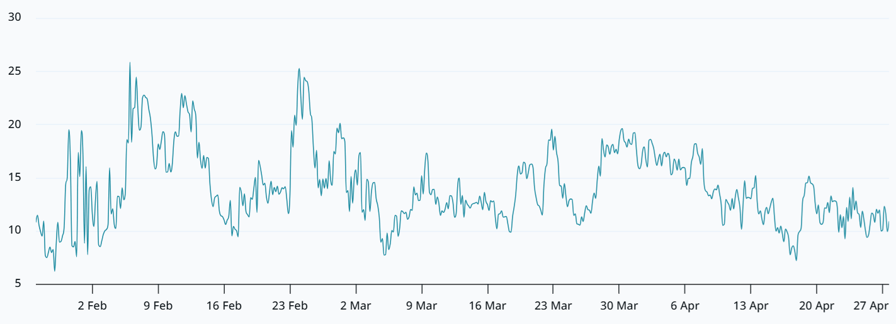

Bitcoin options 30-day delta skew (put-call) at Deribit. Source: Laevitas

The Bitcoin options delta skew shows put (sell) options trading at an 11% premium relative to call (buy) options, consistent with a bearish market. Whales and market makers are uncomfortable with downside risk, which reinforces the thesis of a potential bear trap if Bitcoin reclaims $80,000 in the near term.

Further Bitcoin bullish momentum remains far from certain, but as long as spot market demand remains strong, the pressure on short positions may continue to mount. If the current accumulation trend persists alongside a softening of Federal Reserve policy, the resulting liquidity squeeze could easily propel the price well beyond the $80,000 resistance level.

How RX Pros Is Reshaping Telehealth Access

Aave Dragged Into New Avi Eisenberg Controversy

Seth Rollins blames 28-year-old star for not headlining WrestleMania 42 this year

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread – Corporette.com

-

Tech9 hours ago

Tech9 hours agoRegister Renaming | Hackaday

-

Crypto World2 days ago

Crypto World2 days agoHyperliquid $HYPE Rally Builds Momentum as AI Sector Enters Prove-It Phase

-

Politics5 days ago

Politics5 days agoMaking troops accountable for war crimes threatens US alliance, ex-SAS colonel warns

-

Politics5 days ago

Politics5 days agoDisabled people challenge government SEND proposals over segregation concerns

-

Business4 days ago

Business4 days agoPatterson-UTI Energy, Inc. (PTEN) Q1 2026 Earnings Call Transcript

-

Business6 days ago

Business6 days agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Crypto World7 days ago

Crypto World7 days agoFive Value Stocks with Recovery Potential in 2026: PayPal (PYPL), Nike (NKE), and More

-

Sports2 days ago

Sports2 days agoIPL 2026: Ruturaj Gaikwad registers slowest fifty of the season, enters all-time unwanted list | Cricket News

-

Politics5 days ago

Politics5 days agoStarmer handler McSweeney to be dragged from shadows by Foreign Affairs Committee

-

Politics5 days ago

Politics5 days agoZack Polanski responds to home secretary’s taser threat

-

Politics5 days ago

Wings Over Scotland | How To Get Away With Crimes

-

Crypto World6 days ago

Crypto World6 days agoNew York sues Coinbase, Gemini over prediction market offerings

-

Entertainment7 days ago

Sydney Sweeney cameo cut from “The Devil Wears Prada 2”, source explains why (exclusive)

-

Crypto World6 days ago

Crypto World6 days agoCrypto’s great hope in Senate’s Clarity Act still has a path to survive tight calendar

-

Business6 days ago

Business6 days agoHCL Tech share price tank over 9% after weak Q4. JPMorgan, HSBC & 3 others cut target price

-

Fashion7 days ago

Fashion7 days agoKilkenny Design New Beauty Arrivals for Spring 2026

-

Politics5 days ago

Politics5 days ago‘Iran is still a nuclear threat’

-

Sports5 days ago

Sports5 days agoTim Bradley names the current best in the world: “Better than Inoue and Usyk”

-

NewsBeat2 days ago

NewsBeat2 days agoLK Bennett closes all stores after entering administration

You must be logged in to post a comment Login