Crypto World

What is CASHCAT? Robinhood Chain’s memecoin

CASHCAT is a token named after a company name that was thrown away sixteen years ago. It reached a $156 million market cap, briefly outweighed every real asset on Robinhood’s blockchain, and its own website calls it fan fiction with a ticker.

Summary

- CASHCAT is a community memecoin on Robinhood Chain with a fixed supply of one billion tokens. It has no affiliation with Robinhood Markets, and its own site says so.

- The name comes from real history: before Robinhood was Robinhood, Vlad Tenev and Baiju Bhatt called their company CashCat. A New Yorker profile preserved the detail and a token resurrected it.

- It surged more than 2,100% in a week to a market cap near $156 million, at one point worth roughly twelve times every tokenized real-world asset on the chain combined.

- CEO Vlad Tenev dismissed utility-free assets on July 2, then posted six days later that the chain works great for memes too, and followed the token’s account.

- The token fell more than 33% in 24 hours after Noxa, the launchpad driving the boom, stopped accepting launches on July 11 and went dark two days later.

In 2010, two Stanford graduates building a trading company had a name for it. The name was CashCat. They discarded it, called the company Robinhood instead, and the detail survived only in a New Yorker profile and in the memory of people who read startup lore for fun. Sixteen years later, Robinhood launched a blockchain designed to settle tokenized stocks for institutions, and within days the busiest thing on it was a token named after the name they threw away. CASHCAT reached a market capitalization near $156 million, out-massed every real asset the chain was built for, and made a handful of anonymous wallets millionaires. Its website describes it as fan fiction with a ticker. That is not a criticism. It is the project’s own self-assessment, and it is more honest than most.

The basics

CASHCAT is a memecoin native to Robinhood Chain, the Ethereum layer 2 that Robinhood launched on July 1, 2026. For readers new to the network, crypto.news has also explained the chain it launched on.

Its supply is fixed at one billion tokens, with no further issuance. Its contract address is 0x020bfC650A365f8BB26819deAAbF3E21291018b4, and verifying that string against a trusted source before any transaction is the single most useful thing in this article. It does not have its own blockchain or application. It is a fungible token deployed on someone else’s chain, which is what almost every memecoin is.

It has no product, no roadmap in any meaningful sense, and no utility. The project does not pretend otherwise. Asked what the utility is, the site answers that the utility is cat.

Most importantly, and against what a large number of buyers appear to believe: it is not a Robinhood product. It is not owned, endorsed, backed, listed, or affiliated with Robinhood Markets in any way, and the token’s own website disclaims any connection to the company or to Tenev personally.

Where the name comes from

The connection is entirely historical and it is worth getting right, because the ambiguity is the asset.

Before the company became Robinhood, Tenev and co-founder Baiju Bhatt called their venture CashCat. The detail appears in a New Yorker profile of the company and had circulated among people who follow startup history for years. When Robinhood Chain launched, someone recognized that a discarded corporate name attached to a live corporate blockchain was a nearly perfect memecoin: instantly legible to anyone who knew the story, plausible to anyone who did not, and impossible for the company to claim without endorsing it.

That is the entire link. A name the founders rejected in 2010, revived as a token in 2026 by people with no relationship to them. There is no corporate partnership, no licensing arrangement, and no shared ownership. What exists is a shared piece of trivia, and the token converted that trivia into a market capitalization.

There is a small extra layer that fueled it: Tenev himself had tweeted about CashCat back in April 2021, which meant the lore was not merely documented but personally acknowledged by the CEO years before the token existed. None of that constitutes affiliation. All of it makes affiliation feel more plausible than it is.

What happened

The timeline is short and steep.

Robinhood Chain went live on July 1. CASHCAT deployed shortly after. Within roughly 24 hours it had rallied more than 1,700%, and over its first week it climbed more than 2,100%, reaching an all-time high above $0.17 and a market capitalization near $156 million, with some measurements putting the peak higher.

At its peak day on July 8, the token generated roughly $98 million in 24-hour volume, which was about 17% of the entire chain’s decentralized exchange volume. Set that against what the chain was built for: tokenized real-world assets on Robinhood Chain totalled roughly $12.8 million. At its high, one joke token was worth approximately twelve times every real asset on the network combined.

It did not stay alone. Cash Dog in Hood, Little John, Hoodrat, and Arrow followed within days, none of which existed before July 1. Noxa, the launchpad feeding the wave, was averaging roughly 18,600 new token launches per day. On July 8, Pump.fun added Robinhood Chain support, opening the chain to Solana’s memecoin crowd without bridging. For more context, crypto.news has covered the full story of the takeover.

Then it turned. On July 11, at the precise moment CASHCAT was hitting peak trading volume, Noxa stopped accepting new token launches. Two days later it went dark, citing concerns about low-quality tokens flooding the platform, having generated an estimated $12 million in cumulative fees. CASHCAT fell more than 33% in 24 hours. One prominent trader who claims to have ridden the token from a $10,000 market cap to $230 million dismissed the selloff as noise.

The Tenev problem

The CEO’s involvement is the reason this token is confusing rather than merely amusing, and the sequence matters.

On July 2, the day after the chain went live, Tenev told CNBC that the future of crypto is in real-world assets, drawing a line between productive tokenized assets and speculative tokens without underlying utility. His framing was that an asset not tied to an underlying utility is not a productive asset. It was a clean statement of the thesis the entire chain was built to prove, and it was, in effect, a dismissal of exactly the category CASHCAT belongs to.

Six days later, as CASHCAT climbed, he posted on X that while the company is building Robinhood Chain to be the best chain for real-world assets, it works great for memes too. He then followed the token’s account.

Both readings of that reversal are defensible. The charitable one: a permissionless chain cannot control what deploys on it, refusing to acknowledge the most visible thing on your own network would look ridiculous, and a light-hearted post is not an endorsement. Robinhood’s crypto chief stayed rigorously on message throughout, saying the company remains focused on building a secure and scalable foundation for real-world assets.

The uncharitable one: the follow and the post told the market what the company actually values, which is volume, and a retail buyer who sees the CEO engaging with a token named after his own company is going to draw a conclusion the disclaimer will not undo. The distinction between acknowledging and endorsing is clear to a lawyer and invisible to someone who just downloaded a wallet.

Who made money, and from whom

This is the part that gets celebrated and should be read carefully, because every one of these numbers has a counterparty.

One early buyer spent $838 and received 15.04 million tokens. They sold roughly 13.5 million for about $917,600 and held a remainder worth around $133,700, producing a return in the region of 1,250 times. A second wallet turned $85 into 17.4 million tokens and realized about $687,700 while sitting on roughly $1.2 million more on paper. The five most profitable wallets banked close to $3.7 million between them.

Now the other side. That $3.7 million came from the opposite end of roughly 12,300 sell orders. Every dollar of realized profit in a memecoin is a dollar someone else paid at a higher price, because the token produces no revenue and holds no assets. There is no external cash flow funding those returns. The gains are transfers.

The liquidity structure makes it worse than the market cap suggests. CASHCAT’s trading pool has been worth far less than the token’s headline capitalization, which means a $156 million number sits on a pool that cannot absorb anything close to $156 million of selling. Large trades swing price hard in both directions. A market capitalization is a multiplication, not a promise that the money is there.

And the standard verification does not exist. Security audits of the CASHCAT contract were not possible because Robinhood Chain is too new for the tooling to have caught up. That is a chain-wide condition, not a CASHCAT-specific failure, but it removes the check that would ordinarily flag a malicious contract before a nine-figure market cap forms on top of it.

How a memecoin actually prices

Because CASHCAT is the first token most Robinhood users will look at closely, it is worth walking exactly how a number like $156 million comes to exist, since almost nobody who quotes it understands what it measures.

Market capitalization is a multiplication. Take the last traded price, multiply by circulating supply, print the result. CASHCAT has a fixed supply of one billion tokens, so at a price above $0.15 the arithmetic produces something in the region of $156 million. That is the whole calculation. It is not a valuation, not an appraisal, and not a statement that $156 million exists anywhere.

What makes the number misleading is where the price comes from. The last trade might have been for a few hundred dollars. In an automated market maker, price is set by the ratio of assets in a liquidity pool, and the pool behind CASHCAT has been worth far less than the token’s headline capitalization. So a relatively small purchase moves the ratio, moves the price, and instantly revalues all one billion tokens at the new level. That is why memecoins can add nine figures of notional value in a day: a thin pool is a lever, and modest buying at the margin repriced the entire supply.

The lever works identically in reverse, which is what July 13 showed. When Noxa exited and sentiment turned, sellers hit the same shallow pool and the price fell more than 33% in a day. Nothing about the token changed. Supply was still one billion. The contract was unaltered. The only thing that moved was the ratio in the pool, and the market cap followed it down mechanically.

This is why the comparison that ran through every headline, that CASHCAT was worth twelve times every real-world asset on the chain, is both true and slippery. It is true as arithmetic: $156 million against $12.8 million. It is slippery because the two numbers are not the same kind of thing. The tokenized asset figure represents real instruments with real backing that could be redeemed. The memecoin figure represents a price multiplied by a supply, sitting on a pool that could not absorb a fraction of it. One number is a balance. The other is an echo.

The practical implication for anyone holding: your position is worth the market cap right up until you try to sell, at which point it is worth whatever the pool gives you. In a token where five wallets extracted roughly $3.7 million against 12,300 sell orders, the people who found out first were the ones who tried. That is why thin liquidity moves price so hard.

What this token actually shows

Set the price action aside and CASHCAT is the cleanest available case study in how new chains actually bootstrap, which is why it is worth understanding even if you would never touch it.

The optimistic reading, which serious traders make: memecoins are the ignition sequence. A new chain needs transactions, wallets, and liquidity to look alive, and speculation delivers all three faster than tokenized Treasuries do. Solana grew through a memecoin cycle before producing serious infrastructure, and one veteran trader explicitly compared Robinhood Chain’s early ecosystem to Solana’s. The automated market makers, oracles, and routing built to service speculation are the same rails that tokenized equities will eventually need. In that reading CASHCAT is not a distraction from the strategy; it is the first stage of it. That in the category CASHCAT belongs to.

The pessimistic reading, which the timeline supports: memecoin traders are mercenary by construction, loyal to activity rather than to any chain, and the moment a flashier venue offers quicker returns the volume leaves and the $12.8 million of tokenized assets is what remains. The launchpad that produced the entire boom extracted $12 million in fees and exited within eleven days of the chain going live. That is not the profile of a bootstrapping sequence. It is the profile of an extraction cycle, and the 33% drop when the launchpad left is the evidence.

Which reading is right gets settled by a single number, and it is not CASHCAT’s price. It is whether tokenized real-world assets on Robinhood Chain grow well beyond roughly $13 million while the speculation fades. Robinhood’s second-quarter earnings on July 29 are the first real look. Until then, CASHCAT is a token named after a discarded company name, worth more than everything the chain was built to carry, running on an unaudited contract, on a network whose CEO spent one week explaining why assets like it do not last and the next week noting they work great anyway.

What to watch

If you are tracking this token instead of trading it, three things carry information.

Whether the ecosystem keeps spawning. STONKCAT opened a $SCAT presale on July 16, and a MemeToro presale is running alongside it, both borrowing Robinhood Chain’s branding and pitching future products. New entrants arriving weeks after the launchpad that started the wave exited tells you the branding gap is now a repeatable business, which is bearish for CASHCAT specifically: every new token competes for the same attention that is the only thing holding its price up. It also shows how launchpads mint tokens on demand.

Whether the chain’s real assets grow. Tokenized real-world assets on Robinhood Chain sit around $12.8 million against roughly $312 million in total value locked. That figure, not CASHCAT’s price, decides whether the memecoin wave was an ignition sequence or an extraction cycle. Robinhood’s second-quarter earnings on July 29 are the first look at Stock Token adoption from the company’s own books.

Whether liquidity deepens or thins. The pool behind CASHCAT has been worth far less than the token’s headline capitalization, which is the mechanism behind both the rise and the 33% single-day fall. A token whose pool deepens is a token that can absorb selling. A token whose pool thins as attention rotates is a token whose market cap becomes progressively more theoretical. Also relevant: Robinhood Chain’s 90-day gas subsidy has been making trading artificially cheap, and its expiry is a real test.

The broader point for anyone reading this as a lesson instead of a trade: CASHCAT did nothing unusual. It is a well-executed example of an entirely standard pattern, distinguished only by the quality of its joke and the fact that a public company’s CEO engaged with it. The pattern will repeat on the next chain, with a different name, and the mechanics will be identical. What makes this instance worth remembering is the setting. Most memecoins erupt on chains built by anonymous developers for exactly this kind of activity, where nobody claims to be surprised. CASHCAT erupted on a network built by a listed American brokerage, marketed to institutions, staffed with compliance officers, and launched with a keynote about the future of finance. It took six days for the joke to become the chain’s largest asset by market capitalization, and the company could do nothing about it, because permissionless means permissionless. That is the lesson worth carrying: a corporate chain cannot choose its users any more than a public square can. Robinhood built the venue and the crowd decided what it was for.

Frequently asked questions

What is CASHCAT?

A community memecoin on Robinhood Chain, the Ethereum layer 2 Robinhood launched on July 1, 2026. It has a fixed supply of one billion tokens and a contract address of 0x020bfC650A365f8BB26819deAAbF3E21291018b4. It has no product, no utility, and no affiliation with Robinhood. Its own website describes the project as fan fiction with a ticker and says the utility is cat.

Is CASHCAT affiliated with Robinhood?

No. It is not owned, endorsed, backed, or listed by Robinhood Markets, and the token’s own website disclaims any connection to the company or to Vlad Tenev. The name references CashCat, the working name Tenev and co-founder Baiju Bhatt used before the company became Robinhood, a detail preserved in a New Yorker profile. That is trivia, not a relationship.

Why did CASHCAT rise so fast?

A combination of legible lore and a new chain with nothing else on it. The name connected instantly to Robinhood’s founding story, Robinhood Chain had just launched with cheap fees and easy token creation, and attention concentrated on the first breakout token. It rallied more than 1,700% in 24 hours and more than 2,100% over its first week, reaching a market cap near $156 million.

Did Vlad Tenev endorse CASHCAT?

Not formally. On July 2 he told CNBC that assets not tied to an underlying utility are not productive assets. On July 8, as the token climbed, he posted that while the company is building the chain for real-world assets, it works great for memes too, and he followed the token’s account. That is acknowledgement rather than endorsement, but the distinction is clearer to a lawyer than to a retail buyer.

How much was CASHCAT worth compared to the chain’s real assets?

At its peak, roughly twelve times more. Tokenized real-world assets on Robinhood Chain total around $12.8 million, while CASHCAT reached a market capitalization near $156 million. On its biggest day the token generated approximately $98 million in 24-hour volume, about 17% of the entire chain’s decentralized exchange volume.

Why did CASHCAT crash?

Noxa, the launchpad driving the chain’s memecoin wave, stopped accepting new launches on July 11 as CASHCAT hit peak volume, then went dark two days later, citing low-quality tokens flooding the platform. It had generated an estimated $12 million in cumulative fees. CASHCAT fell more than 33% in 24 hours following the exit.

Who made money on CASHCAT?

A small number of early wallets. One turned $838 into roughly $1.05 million across realized and unrealized value, about 1,250 times. Another turned $85 into roughly $687,700 realized plus $1.2 million on paper. The five most profitable wallets took close to $3.7 million between them. That money came from the other side of roughly 12,300 sell orders, since a memecoin produces no revenue and gains are transfers between participants.

What are the risks?

Considerable. The trading pool is worth far less than the headline market capitalization, so large trades swing price sharply and the stated value cannot be exited at that value. Security audits of the contract were not possible because Robinhood Chain is too new for verification tooling. The token has no revenue, no assets, and no utility, so price depends entirely on attention, which has already proven it can leave in a day.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. Memecoins are extremely speculative, frequently trade on thin liquidity, and most participants lose money. Contract addresses and project claims should be verified independently before any transaction. Nothing here is a recommendation to buy any token. Always do your own research. Figures are accurate as of July 17, 2026 and move rapidly.

ECB’s Piero Cipollone said stablecoin adoption could erode bank deposits, but the digital euro will keep banks at the center of payments.

The part that rattles valuations is the license. K3 is open-weight, with the full model due for public release on July 27. Anyone will be able to download it, run it on their own hardware, and pay nobody.

Anthropic released Fable 5 last month, and OpenAI shipped GPT-5.6 a week ago, both closed and metered. The assumption underwriting hundreds of billions of dollars in AI infrastructure spending is that frontier capability stays scarce, expensive and American.

A free Chinese model at the top of a coding leaderboard is a direct argument against that.

Meanwhile, Moonshot’s domestic rivals took it worst, with Z.ai falling about 27% and MiniMax about 16%.

For crypto, the headwinds run through the tape rather than through anything onchain. Bitcoin has spent this entire week taking direction from semiconductors.

Last Friday, it rose 4% on the day South Korea’s Kospi jumped 8% and SK Hynix priced $26.5 billion of American depositary shares. This Friday, it fell because a model release in Beijing made the same trade look expensive.

There is, however, a more concrete exposure underneath.

Bitcoin miners have spent two years repositioning themselves as AI data center landlords, signing long-term leases with model developers on the assumption that demand for training and inference compute keeps rising.

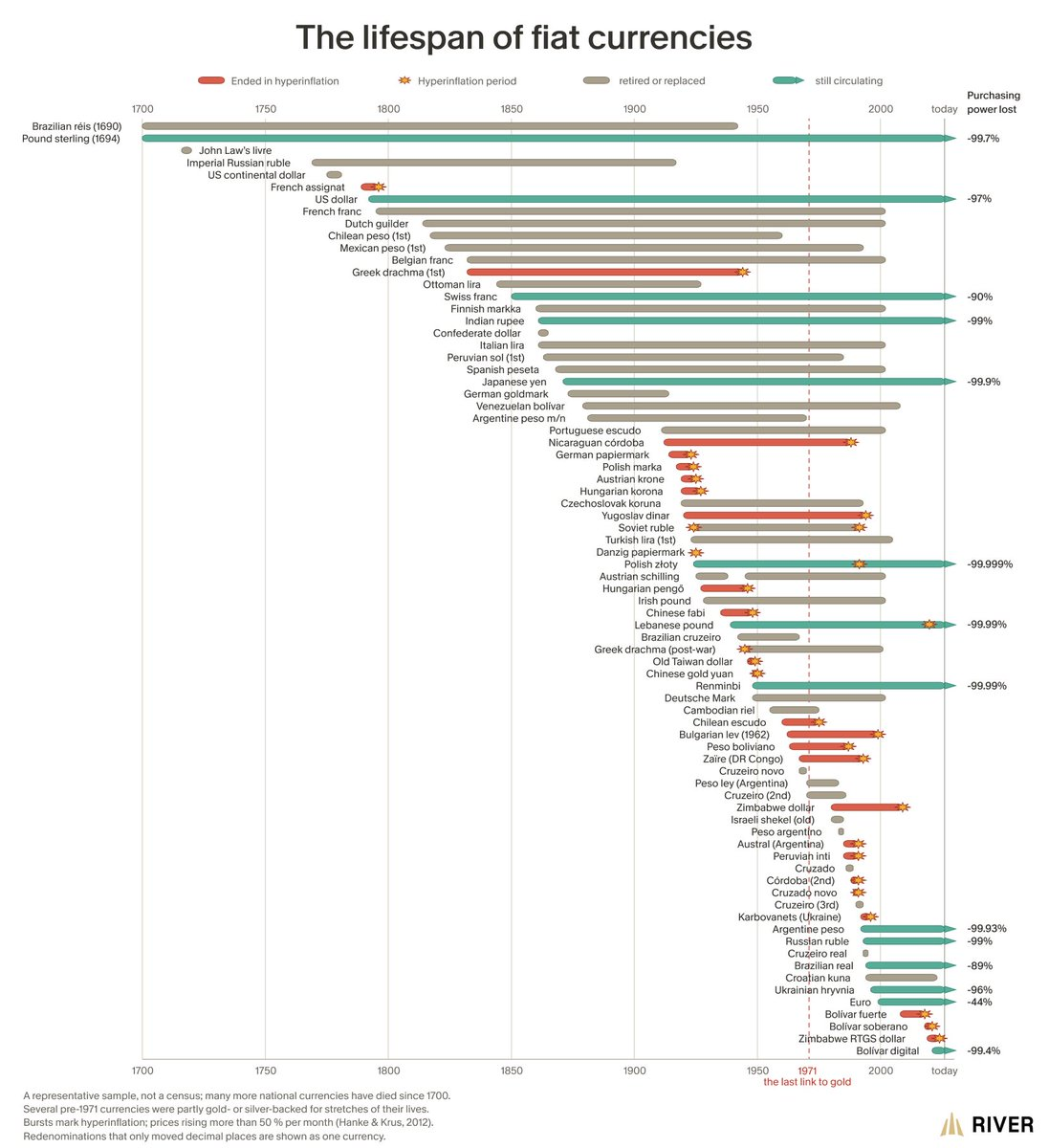

Michael Saylor is making the case for Bitcoin (BTC) with a history lesson. The MicroStrategy chairman shared River research tracking over 60 government currencies since 1700. His point is simple. Paper money keeps failing, and Bitcoin was built to fix that.

River, a Bitcoin financial services firm, published the chart this week. It claims the average fiat currency lasts just 27 years.

326 Years of Fiat History Behind Saylor’s Bitcoin Pitch

The chart tells a grim story. Dozens of currencies died in hyperinflation, defined by economists Steve Hanke and Nicholas Krus as prices rising by more than 50% in a month.

Germany’s papiermark (or Paper Mark) went that way in 1923. Hungary’s pengő followed in 1946, when prices doubled roughly every 15 hours. Zimbabwe’s dollar collapsed in 2008.

The survivors did not do much better. The US dollar has lost 97% of its buying power. The British pound is down 99.7%, and the Japanese yen 99.9%. Even the euro, the youngest and best performer, has lost 44% since 1999.

River is upfront about the chart’s limits. It calls the data a representative sample, not a census, and notes many pre-1971 currencies had partial gold backing. That year gets its own dashed line, marking when the dollar cut its final tie to gold.

“Fiat currency is the problem. Companies, institutions, securities, and technologies that strengthen Bitcoin are part of the solution. We can debate ideas without mistaking allies for enemies,” Saylor commented.

Follow us on X to get the latest news as it happens

Notably, Michael Saylor’s next-decade Bitcoin outlook calls the pioneer crypto a digital property whose strength lies in its base layer barely changing. He sees Bitcoin as scarce global capital for final settlement, not mainly for everyday payments.

His bigger bet is that Bitcoin will support a new financial system built on digital capital, credit, and money.

River Says Most Cryptocurrencies Fail the Same Test

River’s warning is not just about fiat. The firm says the average cryptocurrency does not even last a year. Nearly all of them fall to zero when priced in Bitcoin.

“All of these currencies suffer from the same problem: Centralized power and an infinite money supply. Bitcoin was designed to outlast all fiat currency,” the firm said in its post.

Meanwhile, not everyone agrees that Bitcoin’s design is settled. StarkWare CEO Eli Ben-Sasson recently challenged Bitcoin’s fixed cap, arguing lost keys will shrink the usable supply forever.

Chainalysis estimated that up to 3.79 million BTC were already unrecoverable by 2017. Supporters rejected his 4% issuance fix, since 95.5% of all Bitcoin now exists.

The market adds a twist to Saylor’s pitch. Bitcoin trades near $63,252, down about 47% in a year.

MicroStrategy still holds 843,775 BTC, the largest corporate stash, even after selling 3,588 BTC this month, its biggest sale since 2022.

History says fiat money fades. The coming months will test whether investors still believe Bitcoin is the escape.

The post MicroStrategy’s Saylor Pitches Bitcoin Bull Case With 300 Years of Fiat History appeared first on BeInCrypto.

Bitcoin (BTC) endured a brutal first half of 2026, dropping to a multi-year low of $57,717 on July 1, a level not seen since September 2024. The flagship cryptocurrency has declined over 30% so far this year and is trading around $63,300 at the time of writing.

Improving macro conditions and whale accumulation briefly pushed BTC above $65,000 this week. However, it fell back into the red, highlighting the fragility of its recovery during current market conditions.

Bitcoin (BTC) Recovery On Shaky Ground

Bitcoin (BTC) has endured a difficult few months, falling to its lowest level since September 2024 on July 1, when it plunged to a low of $57,717. The flagship cryptocurrency has declined over 30% during the first half of 2026, and chances of a recovery remain low until ETF inflows rebound and prevailing macroeconomic conditions improve. BTC also faces the prospect of a deeper decline as investors pivot to AI stocks.

BTC extended its decline for a third day after Tuesday’s rebound and has slipped below $63,000 after stalling around the $65,000 level. While the flagship cryptocurrency has struggled, the S&P 500 and Nasdaq are trading at record levels. This may suggest that the decline is BTC-specific. However, several factors are at play, including geopolitical tensions and crypto-specific factors like ETF outflows, liquidations, and Strategy’s decision to leverage some of its BTC holdings.

What’s Keeping Bitcoin (BTC) Price Action Subdued

Bitcoin (BTC) has been in the doldrums since the start of the year. The flagship cryptocurrency has been declining since hitting its all-time high in October 2025. The bullish narrative around President Trump’s victory and a crypto-friendly administration quickly faded as key crypto-specific legislation stalled. The delay in establishing a strategic Bitcoin reserve and passing the CLARITY Act has had a significant impact on investor sentiment and laid bare the friction between the banking sector and the crypto industry.

Institutional demand, one of the primary drivers of BTC’s rally to its all-time high, has also declined. According to data from CoinMarketCap, spot Bitcoin ETFs recorded total net inflows of $21.4 billion in 2025. In comparison, they have recorded around $5.8 billion in net outflows year-to-date, a distinct shift in investor sentiment and weakening institutional demand.

Artificial Intelligence (AI) and the threat of quantum computers have also impacted investor sentiment and price action. Capital rotation into AI stocks and initial public offerings of companies like SpaceX, OpenAI, and Anthropic has also pulled BTC lower.

Additionally, Strategy’s decision to sell some of its BTC to fund a dollar reserve has dealt a psychological blow to the market and directly put pressure on the asset’s price. The Bitcoin treasury company has authorized selling up to $1.25 billion in BTC and has already executed two sales. The company sold 32 BTC in May for $2.5 million before liquidating 3,588 BTC for $216 million in July. Unsurprisingly, the large sale was a shock to the market, and the flagship cryptocurrency fell nearly 4% in the aftermath of the transaction.

Can Bitcoin (BTC) Price Action Recover

BTC’s recovery hinges on several factors. The passage of the CLARITY Act could be a significant boost for the market. It establishes a clear market structure to regulate the industry and could boost institutional confidence and drive adoption. The bill has advanced from the Senate Banking Committee but faces a crucial test on the Senate floor.

Spot Bitcoin ETF demand is crucial for a sustainable recovery. ETFs have registered substantial outflows so far as investors pulled capital. However, heavy outflows have slowed as sell-side pressure declines. After recording substantial outflows in June, Bitcoin ETFs have recorded considerable inflows in July, a sign that institutional interest could be returning.

BTC registered a sharp bounce after US CPI data revealed inflation declined 0.4% month-on-month in June, the first monthly decline in six years. Headline inflation fell from 4.2% to 3.5%, while core CPI fell to 2.6%. However, inflationary risks remain thanks to renewed US-Iran tensions. Escalating Middle East tensions could push oil prices higher, raising inflationary risks. The markets have also tempered expectations of a rate hike, with the probability of such a hike falling from 78% to 58%.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

Cointelegraph is committed to providing independent, high-quality journalism across the crypto, blockchain, AI, and fintech industries.

All news, reviews, and analyses are produced with full journalistic independence and integrity. For more details on our standards and processes, please read our Editorial Policy.

Lighter is the exchange running perpetual futures inside Robinhood Wallet. It is also the clearest attempt yet to rebuild payment for order flow on a blockchain, backed by the company that made the practice famous.

Summary

- Lighter is a decentralized perpetual futures exchange built as an Ethereum layer 2 using custom zero-knowledge circuits, founded in 2022 by Vladimir Novakovski and live on mainnet since October 2025.

- It is the official perpetuals partner of Robinhood Chain. Eligible users trade perps inside Robinhood Wallet, with USDG as collateral and quote asset, and Robinhood and Lighter split the revenue 50/50.

- The relationship runs deep. Robinhood Ventures joined a $68 million round in November 2025 at roughly $1.5 billion, Tenev serves as an advisor, and Novakovski mentored Tenev early in his career.

- The business model is payment for order flow, rebuilt on-chain: zero fees for retail, with revenue coming from selling access to that order flow to sophisticated firms through premium accounts.

- Americans cannot use it. Perps through Robinhood Wallet are unavailable to residents of the US, UK, Canada, Switzerland, UAE, and Singapore.

Most people encountering Lighter will not encounter it by name. They will open Robinhood Wallet, tap into perpetual futures, and trade. Underneath that tap is a separate company running a zero-knowledge rollup, taking half the revenue, and executing a strategy that would be familiar to anyone who followed the GameStop hearings. Lighter is not simply a venue Robinhood integrated. It is a bet that the most valuable thing in trading is not fees but order flow, and that the way to win the perpetual futures market is to give the trading away and sell what the trading reveals. That idea has a name in traditional finance, and the company whose name is synonymous with it is the one funding this.

What Lighter is

Lighter is a decentralized exchange specializing in perpetual futures, built as an Ethereum layer 2 using custom zero-knowledge circuits. It was founded in 2022 by Vladimir Novakovski, and launched its public mainnet in October 2025 after an extended beta.

The technical pitch addresses a real tension in on-chain derivatives. Perpetual exchanges historically had to choose: sacrifice decentralization for speed, or sacrifice speed for trustlessness. Centralized venues match orders fast and ask you to trust them. Fully on-chain venues are verifiable and slow. Lighter uses zero-knowledge rollup architecture to attempt both, processing transactions off-chain for speed while posting cryptographic proofs on-chain, which produces verifiable order matching and liquidations at latency competitive with centralized exchanges.

That matters more for perps than for most products. A perpetual futures position is leveraged and margined, which means liquidation is automatic and mechanical. If you cannot verify that a liquidation was executed correctly, you are trusting the venue at the exact moment the venue has the least incentive to be honest with you. Verifiable liquidation is not a marketing feature. It is the point.

Its token is LIT. The market has valued the project in the region of $2.75 billion fully diluted, which is a valuation built on distribution rather than on current fee revenue, for reasons the rest of this article explains.

The Robinhood relationship

The integration went live with Robinhood Chain’s mainnet on July 1, 2026, announced at the company’s The World is Flat livestream from the Old Royal Naval College in London.

The mechanics: a revamped Robinhood Wallet gives eligible users access to perpetual futures through Lighter. USDG, a dollar stablecoin, serves as both the collateral and the quote asset. Users can deposit Robinhood Chain assets into Lighter’s smart contracts as margin, and the whole experience sits inside Robinhood Wallet, so users never navigate an unfamiliar DeFi interface. When Lighter added Robinhood Chain collateral support, LIT rose roughly 15%.

Two details tell you this is a partnership and not a vendor arrangement. The revenue splits 50/50 between Robinhood and Lighter. And Lighter committed $11 million of its LIT tokens to the Robinhood community, with eligible users earning points on perp trades and double points when trading through Robinhood.

The history behind it runs further than the deal. Robinhood Ventures participated in Lighter’s $68 million funding round in November 2025, which valued the company at roughly $1.5 billion. Tenev serves as an advisor to Lighter and has publicly called it a step forward for decentralized infrastructure. And Novakovski and Tenev share a professional history stretching back over a decade, with Novakovski having mentored Tenev early in his career. Novakovski described the deal as twelve years in the making, which reads as hyperbole until you notice that Robinhood picked a perps partner run by the person who mentored its CEO.

Lighter frames the Robinhood integration as its first Domain, a template for how the exchange plans to scale: rather than acquiring users directly, it becomes the engine underneath someone else’s front end.

The order flow model

Here is the part that makes Lighter interesting instead of merely well-connected.

Lighter offers zero fees to retail traders. That is not a promotional rate. It is the business model. The revenue comes from the other side: sophisticated firms and high-frequency traders pay for premium accounts that give them access to the venue’s order flow.

Anyone who followed the 2021 retail trading hearings will recognize this immediately. In traditional equity markets, Robinhood does not charge commissions. It routes its customers’ orders to market makers such as Citadel and Virtu, who pay for the privilege. The industry term is payment for order flow, and the economic logic is that retail orders are valuable precisely because they are uninformed. A market maker filling a retail order is unlikely to be trading against someone who knows something. Filling an order from a sophisticated fund is dangerous, because that fund may well know something the market maker does not. Uninformed flow is profitable to intermediate. Informed flow is toxic.

Lighter reproduces that structure on-chain. Aggregate uninformed retail flow by making it free, then monetize access to it. The valuation logic follows: at a multibillion-dollar fully diluted value, the bet is not that Lighter will eventually raise fees. It is that if Lighter becomes the default engine behind Robinhood Wallet’s crypto users, the value of that order flow to market makers rises accordingly. Retail flow crossing over from stock trading is generally less sharp than crypto-native flow, which makes it more valuable to the firms buying access.

That is a genuinely coherent strategy and it is also the reason Lighter’s current fee generation looks thin against competitors running conventional models. The company is not trying to earn on volume. It is trying to own the pipe.

A worked example of the flow trade

The order flow argument is abstract until you price it, so walk the logic the way a market maker would.

Imagine two venues, each routing $200 billion of monthly perpetual futures volume. The first is crypto-native, populated by professional traders, arbitrage desks, and funds running systematic strategies. The second is retail crossover, populated by people who mostly trade equities and take directional views on Bitcoin when it is in the news.

To a market maker, those two order books are not remotely the same asset, and the identical volume figure conceals the difference. On the professional venue, a large share of incoming orders carry information. When a systematic fund lifts your offer, there is a meaningful chance it knows something about the next few seconds that you do not, and you are now holding inventory that is about to move against you. The industry term is toxic flow, and market makers price it by widening spreads, which is the cost of being adversely selected.

On the retail venue, the incoming orders are largely uninformed in the technical sense. Not stupid, and not badly intentioned, simply not carrying private information about the immediate direction of price. A market maker filling those orders can hedge calmly and earn the spread with far less adverse selection. That flow is worth substantially more per dollar of volume, and firms will pay for access to it.

Now the business model resolves. Lighter gives retail trading away for free, because the free trading is what aggregates the valuable flow. It sells premium access to the firms that want to interact with that flow. The more retail volume it aggregates, and the less contaminated that volume is by professional activity, the more the access is worth. Robinhood’s distribution is the input: millions of retail stock traders crossing into perps are close to the ideal population for this model, which is precisely why the partnership exists and why the revenue splits evenly.

That also explains a valuation that looks strange against current fees. At a fully diluted value in the billions, the market is not pricing Lighter’s fee revenue, which is thin by design. It is pricing the possibility that Lighter becomes the default engine behind Robinhood Wallet, at which point the flow it controls becomes considerably more valuable to the firms buying it. The bet is on distribution, not on eventually charging.

The honest counterpoint is that this model has been tested before, at scale, in equities, and it works commercially while generating a permanent argument about whether the customer is the buyer or the product. Nothing about a zero-knowledge proof settles that argument. It only proves that whatever happened, happened as described.

Where it sits in the market

Context matters here, because the perpetuals market is not empty.

Hyperliquid dominates the decentralized perpetuals category and has for some time, having built its position by serving crypto-native traders with high-performance execution. Aster competes on similar ground. Both are fighting for the same audience: sophisticated on-chain traders who care about latency, depth, and fee structure. For more context on the venue Lighter competes against, crypto.news has also examined why HYPE is different inside Hyperliquid’s buyback.

Lighter has explicitly chosen not to fight there. Its positioning is the traditional finance bridge, and its distribution advantage is a pipeline to millions of retail stock traders that no crypto-native competitor can access. That is a defensible strategic choice: the crypto-native segment is contested and price-sensitive, while the retail crossover segment is large, uncontested, and, for the reasons above, more commercially valuable per unit of volume.

The wider context is that fees across perpetual decentralized exchanges are trending toward zero. In a market where nobody can charge, whoever captures the most valuable flow wins. Lighter is not making an unusual bet so much as making the traditional finance bet earlier than its competitors.

Robinhood has expanded the surface around it, offering commodity, ETF, and foreign exchange perpetuals with up to 10x leverage to European users, while its Earn product pays roughly 7% APY on USDG through Morpho infrastructure. USDG therefore does double duty: yield when idle, margin when deployed.

Who cannot use it

The restriction list is long and it includes the country where Robinhood has most of its customers.

Perpetual futures through Robinhood Wallet are unavailable to residents of the United States, United Kingdom, Canada, Switzerland, the United Arab Emirates, and Singapore, along with other restricted jurisdictions.

The American exclusion is the one worth understanding, because it is the same wall that blocks Stock Tokens. Perpetual contracts occupy an unresolved zone in US financial law. The CFTC has historically treated perps as swaps, which places them under derivatives regulation that most crypto platforms are not structured to satisfy. That question is live: the CME is currently litigating against the CFTC over precisely how a perp should be classified, and the CLARITY Act would hand the agency primary authority over digital commodity spot markets while the agency itself operates with a single commissioner.

So an American Robinhood customer can hold the stock of the company that co-owns the revenue from a perps exchange they are legally barred from using. That is not an accident. It is a map of where American crypto regulation currently stands.

The questions worth asking

Three things about this arrangement deserve more scrutiny than they have received.

Whether on-chain payment for order flow attracts the same criticism. The traditional practice drew sustained regulatory attention on the argument that free trading is not free, that customers pay through worse execution, and that the arrangement creates a conflict between a broker’s duty to its customers and its revenue from the firms buying their orders. None of those critiques become less true because the venue posts zero-knowledge proofs. Verifiable matching proves the trade executed as stated. It does not prove the trade was routed to your benefit.

Whether the relationships are disclosed clearly enough. Robinhood Ventures is an investor in Lighter. Tenev is an advisor to Lighter. Novakovski mentored Tenev. Robinhood takes half the revenue. Each of those is individually unremarkable and publicly reported. Together they describe a venue selected through a network of overlapping interests, integrated as the default option inside an app used by millions, and a retail user tapping the perps tab is unlikely to know any of it.

Whether the traffic is real. Robinhood Chain ran a 90-day gas fee subsidy from launch, which inflates transaction counts and makes comparisons with other chains unreliable during the subsidy window. Perps activity routed through the wallet during that period should be read with the same caution. The honest test arrives when the subsidy expires and the flow either persists or does not.

None of this makes Lighter a bad product. The zero-knowledge architecture is a real answer to a real problem, and verifiable liquidation is worth having. It makes Lighter a product whose economics are worth understanding before you use it, which is a different claim and a more useful one. The trade is free. Something is still being sold.

What to watch

Three concrete signals will settle whether this integration is infrastructure or a distribution experiment.

Whether flow persists after the subsidy. Robinhood Chain ran a 90-day gas fee subsidy from launch. Perps routed through the wallet during that window are trading in artificially cheap conditions. The honest measurement of whether retail crossover users actually want perpetual futures arrives when they start paying real costs, and any volume figure quoted before then carries an asterisk.

Whether premium accounts materialize. The entire valuation thesis rests on sophisticated firms paying for access to Robinhood’s retail order flow. That is a testable claim. If market makers commit at scale, the model works and Lighter’s fully diluted value makes sense. If they do not, Lighter is a zero-fee exchange with no revenue and a large token supply, which is a considerably worse business.

Whether the regulatory position moves. Americans are barred from perps through the wallet because perpetual contracts sit in an unresolved zone of US law, where the CFTC has historically treated them as swaps. Two things could change that: the CME’s litigation against the CFTC over how a perp is classified, and the CLARITY Act, which would hand the agency primary authority over digital commodity spot markets. If perps come onshore, Robinhood’s largest customer base becomes addressable overnight and this integration stops being a foreign product.

The last one is the real prize and it explains the patience. Building the perps rail now, with a partner run by the CEO’s mentor, in jurisdictions where it is already legal, means that on the day American rules change the distribution is already wired. Robinhood is not building for the market it has. It is building for the one it expects, which is either foresight or an expensive bet on Congress. Worth noting that the agency holding the decision, the CFTC, currently operates with a single confirmed commissioner out of five seats and has lost roughly a fifth of its staff, while simultaneously writing perps rules, asserting jurisdiction over prediction markets, and preparing to inherit crypto spot markets if the CLARITY Act passes. The timeline for American perps therefore depends less on what Robinhood or Lighter build than on whether one understaffed regulator can produce a rulebook. For a user, the practical takeaway is narrower and more useful: the product exists, it works, it is free, and the reason it is free is that something about your trading is being sold to someone. That is not a scandal. It is the deal, and it is worth knowing you are in it.

Frequently asked questions

What is Lighter?

A decentralized perpetual futures exchange built as an Ethereum layer 2 using custom zero-knowledge circuits, founded in 2022 by Vladimir Novakovski and live on mainnet since October 2025. Its architecture processes trades off-chain for speed while posting cryptographic proofs on-chain, producing verifiable order matching and liquidations at latency competitive with centralized venues. Its token is LIT.

How is Lighter connected to Robinhood?

It is the official perpetuals partner of Robinhood Chain, live since the July 1, 2026 mainnet launch. Eligible users trade perps inside Robinhood Wallet using USDG as collateral and quote asset, and the two companies split revenue 50/50. Robinhood Ventures invested in Lighter’s $68 million round in November 2025 at roughly $1.5 billion, and Vlad Tenev serves as an advisor to the company.

Why does Lighter charge retail nothing?

Because the order flow is the product. Lighter offers zero fees to retail traders and generates revenue by selling sophisticated firms access to that flow through premium accounts. This mirrors payment for order flow in traditional equity markets, where uninformed retail orders are valuable to market makers precisely because they are unlikely to be trading on superior information.

Can Americans use Lighter through Robinhood?

No. Perpetual futures through Robinhood Wallet are unavailable to residents of the United States, United Kingdom, Canada, Switzerland, the United Arab Emirates, and Singapore, among other restricted jurisdictions. Perpetual contracts sit in an unresolved area of US law, where the CFTC has historically treated them as swaps subject to derivatives regulation.

How does Lighter differ from Hyperliquid?

Positioning. Hyperliquid dominates the decentralized perpetuals category by serving crypto-native traders with high-performance execution, and Aster competes on the same ground. Lighter has explicitly chosen not to fight there, positioning itself as a bridge to traditional finance retail through Robinhood’s distribution. Its advantage is access to millions of retail stock traders that crypto-native venues cannot reach.

What is USDG’s role?

It is both the collateral and the quote asset for perpetual futures on the Lighter integration. Users deposit USDG from Robinhood Wallet into Lighter’s smart contracts as margin. The same stablecoin also earns roughly 7% APY through Robinhood Earn’s lending product, built on Morpho infrastructure, giving it a dual purpose: yield when idle, margin when deployed.

What is the LIT token for?

LIT is Lighter’s native token. Lighter committed $11 million of LIT to the Robinhood community as a partner incentive, with eligible users earning points on perpetual trades and double points when trading through Robinhood. LIT rose roughly 15% when Lighter added support for Robinhood Chain collateral. It is a Lighter token, not a Robinhood Chain token, which does not exist.

What are the risks?

Perpetual futures are leveraged instruments and positions can be liquidated rapidly. Beyond that, the order flow model raises the same questions that payment for order flow attracts in equities: free trading may be paid for through execution quality, and the arrangement creates a conflict between routing decisions and revenue. The overlapping relationships between Robinhood and Lighter are publicly reported but unlikely to be visible to a retail user tapping a tab. Traders should also understand reading positioning on perp venues and how collateral works across positions before using leveraged products.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. Perpetual futures are leveraged products carrying substantial risk of loss, including losses exceeding the margin posted, and availability varies sharply by jurisdiction. Nothing here is a recommendation to trade any instrument or use any platform. Always do your own research. Information is accurate as of July 17, 2026.

Key takeaways

- Pi Network (PI) is showing signs of recovery after several days of consolidation and easing selling pressure.

- Rising Open Interest suggests speculative traders are positioning for a potential rebound.

- The upcoming Stellar Protocol v25 mainnet upgrade and improving market sentiment could support PI’s recovery.

Pi Network (PI) posted modest gains on Friday after three consecutive sessions of sideways trading, suggesting that selling pressure may be easing following a sharp correction earlier this month.

Although the token remains in a broader downtrend, increasing derivatives activity and deeply oversold technical indicators are fueling speculation that PI could be preparing for a short-term rebound.

Speculative demand begins to strengthen

Pi Network remains one of the cryptocurrency market’s most speculative community-driven assets, making its price particularly sensitive to shifts in investor sentiment.

After a steep sell-off earlier this month, optimism has started to improve as broader market risk appetite stabilizes.

Another potential catalyst is the Stellar Protocol version 25 mainnet upgrade, scheduled for July 22, which could support sentiment across ecosystems connected to Stellar-based infrastructure.

Meanwhile, derivatives data points to growing speculative interest. According to CoinAnk, Pi Network Open Interest increased to $10.73 million on Friday from $10.44 million a day earlier.

Open Interest has steadily recovered from $9.11 million recorded on Monday, indicating that traders are gradually returning to the market after the recent correction.

The increase suggests retail investors are beginning to position for a possible recovery, although conviction remains relatively modest.

PI remains oversold despite stabilizing price action

From a technical perspective, Pi Network continues to trade below the key $0.0800 resistance level, leaving the broader trend bearish.

However, the token has managed to hold near the lower boundary of a falling channel, where technical support is reinforced by the 161.8% Fibonacci extension level at $0.06793.

Holding above this area could provide the foundation for a relief rally if buying momentum continues to build.

Technical indicators are beginning to show early signs that the recent decline may be losing momentum.

The Relative Strength Index (RSI) has fallen to around 17, placing PI deep in oversold territory. While oversold readings do not guarantee a reversal, they often indicate that selling pressure has become stretched.

At the same time, the Moving Average Convergence Divergence (MACD) remains below the zero line but is showing signs of weakening bearish momentum, suggesting sellers may be losing control.

If PI extends its recovery, the first resistance level is the 127.2% Fibonacci extension at $0.09613.

A stronger rebound would then face resistance near $0.110, where the upper boundary of the falling channel could limit further gains unless broader market sentiment improves.

On the downside, the 161.8% Fibonacci extension at $0.06793 remains the most important support level.

A decisive break below that area could expose the 227.2% Fibonacci extension near $0.01463, significantly increasing downside risk.

For now, Pi Network’s deeply oversold technical setup, combined with rising Open Interest and improving market sentiment, suggests that a short-term recovery remains possible, although the broader trend will remain bearish until key resistance levels are reclaimed.

BTC is less volatile than South Korea’s stock market. Since the start of June, South Korea’s benchmark KOSPI has swung an average of 3.8% a day, more than double BTC’s 1.7%.

On Thursday alone, South Korea’s benchmark KOSPI fell 6.4% to 6,820, tripping its 37th program-trading halt of 2026, a five-minute regulatory pause to restore order to chaotic markets.

However, that crash wasn’t even its worst session of the week.

Meanwhile, BTC and crypto indices appear to be sailing calmer waters by comparison. On a 12-month basis, KOSPI’s annualized volatility has climbed to 57% against BTC’s 47% — still higher than BTC over this impressive timespan.

One analyst remarked, “Compared to KOSPI, BTC has become a low-volatility asset. SK Hynix and Samsung Electronics showed volatility of 90% and 78% respectively, an extreme level previously observed only in thematic stocks.”

Investors have swept up SK Hynix and Samsung into the recent frenzy of AI stocks. Both companies make hardware related to the boom in AI chatbots and coding tools like Gemini, Claude, ChatGPT, Grok, and others.

Remarkably, even after its sharp decline in recent days, KOSPI remains 2026’s top-performing stock market of a major economy, still up about 60% despite shedding a quarter of its valuation since June.

Seven market-wide circuit breakers this year

The KOSPI set its record close of 9,114.55 on June 22. One day later it dropped 9.99%, one of the largest single-day declines in the index’s history.

Monday was nearly as brutal. An 8.95% plunge through the 7,000 level triggered its seventh 20-minute, market-wide circuit breaker of 2026.

A market-wide circuit breaker halts all trading of listed stocks for 20 minutes after an 8% drop. The more common program-trading halt, also known as a sidecar, pauses only certain programmatic orders after sharp futures moves.

By Wednesday the machinery was working in reverse. The index rebounded 6.24% to 7,284.41. Then Thursday took most of it back.

The Bank of Korea didn’t help, raising rates 25 basis points to 2.75%, its first rate rise since January 2023.

All the while, BTC has been trading relatively calmly in the $60,000s since the start of June.

Read more: SK Hynix wipes out US debut gain in one day of trading

Two AI stocks overtake S. Korea’s stock market

South Korea’s index has a structural problem with its arithmetic.

Two companies, Samsung Electronics and SK Hynix, are worth half of the KOSPI’s market value. Moreover, exposure to these two companies is amplified by a variety of funds, derivatives, and leveraged funds.

The timing was no accident. SK Hynix joined the $1 trillion club in the same session, with the KOSPI up 95% on the year.

Hungry for leverage to amplify their gains during the upswing, investors demanded new, “2X” single-stock ETFs, which became the market’s center of gravity within weeks.

These leveraged funds churned 212 trillion won of volume in June alone, over a quarter of the country’s ETF turnover.

Then leverage did what leverage always does: unwind. Their combined assets collapsed 41% between July 1 and July 13, from 15.9 trillion won to 9.3 trillion.

Bloomberg noted that a single Hong Kong-listed fund tied to SK Hynix grew so large that it had become the tail wagging the dog — more responsible for SK Hynix’s volatility than SK Hynix’s common stock itself.

‘Correction of a known policy error’

South Korea’s president promised at the Korea Exchange in June 2025 to “make investing in stocks a primary mode of investment on par with real estate.”

Retail investors obliged with borrowed money. One 24-year-old who turned as little as 10 million won into 300 million on margin told Reuters, “Just as it went up explosively, it went down explosively.”

Brokers liquidated 1.12 trillion won of margin-called stock in June, the year’s highest monthly total, according to Korea Financial Investment Association data.

A viral Bull Theory post contextualized 1.2 million “accounts” being margin-called as equivalent roughly one in 30 working age adults. However, no regulator has published account-parsing figures to know precisely how many discrete humans received margin calls.

The downturn has caused real world consequences.

Sadly, Protos reported this week that a stock trading YouTuber was stabbed in Busan after the market crash.

Seven weeks after approving the products, and after the financial watchdog’s chief conceded the rollout was too hasty, the Financial Services Commission on Thursday halted new listings of 2X single-stock ETFs until markets stabilize.

It also tripled minimum deposits to 30 million won (about $20,300), effective August 5.

Exness strategist Inki Cho called the move “overdue” and said, “This is a correction of a known policy error.”

BTC, meanwhile, spent the same stretch doing comparatively little. It traded near $64,000 on Thursday, roughly half below its October 2025 peak of about $126,000.

Its CME implied volatility gauge came within three points of a 12-month low last week.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Introduction

Autonomous Market Makers (AMMs) transformed decentralized finance (DeFi) by replacing traditional order books with smart contracts that automatically provide liquidity and execute trades. Platforms like Uniswap, Curve, Balancer, and many others proved that anyone can become a liquidity provider while enabling permissionless trading around the clock.

However, the next generation of AMMs is poised to become far more intelligent than today’s liquidity pools. Rather than simply following fixed mathematical formulas, future AMMs will leverage artificial intelligence, real-time market data, programmable liquidity, and cross-chain infrastructure to optimize trading, reduce risks, and maximize capital efficiency.

The evolution of AMMs may redefine how liquidity functions across the entire digital economy.

From Passive Liquidity to Intelligent Liquidity

Today’s AMMs generally rely on predetermined algorithms such as the constant product formula (x × y = k). While revolutionary, these systems still face several limitations:

- Impermanent loss

- Capital inefficiency

- Fragmented liquidity

- Static fee structures

- Slow adaptation to market volatility

Future autonomous market makers will actively respond to market conditions instead of waiting for liquidity providers to manually adjust positions.

Imagine liquidity pools that automatically:

- Shift liquidity where trading demand is highest

- Modify trading fees during periods of volatility

- Rebalance portfolios continuously

- Hedge exposure against extreme market swings

- Allocate idle capital into yield-generating strategies

Liquidity becomes dynamic instead of passive.

AI-Powered Liquidity Management

Artificial intelligence will likely become one of the biggest upgrades for AMMs.

Machine learning models could analyze:

- Trading volume

- Historical volatility

- On-chain activity

- Wallet behavior

- Macroeconomic events

- Stablecoin flows

- Cross-chain liquidity movements

Using these insights, AMMs could predict liquidity demand before it happens.

Rather than reacting after volatility occurs, intelligent AMMs may reposition liquidity in anticipation of changing market conditions.

This could significantly reduce impermanent loss while improving execution quality for traders.

Cross-Chain Autonomous Liquidity

The blockchain ecosystem is no longer confined to a single network.

Assets now move between:

- Ethereum

- Solana

- Base

- Arbitrum

- Optimism

- Avalanche

- BNB Chain

- Sui

- Aptos

Future AMMs won’t be limited to one blockchain.

Instead, autonomous market makers will coordinate liquidity across multiple ecosystems simultaneously.

A single liquidity position could automatically migrate toward whichever blockchain currently offers:

- Higher trading volume

- Better yields

- Lower transaction costs

- Greater user demand

Liquidity becomes globally optimized rather than trapped on isolated chains.

Intent-Based Trading

Intent-based architecture is emerging as one of Web3’s most exciting innovations.

Instead of specifying every trading parameter, users simply express what outcome they want.

For example:

“Swap my USDC into ETH at the best possible price before tomorrow.”

An autonomous market maker can then:

- Search multiple DEXs

- Split orders

- Route across chains

- Minimize slippage

- Reduce gas fees

- Complete execution automatically

The user focuses on outcomes rather than execution mechanics.

Self-Optimizing Fee Models

Today’s AMMs often charge fixed trading fees.

Future systems could dynamically adjust fees based on:

- Market volatility

- Liquidity depth

- Trade size

- Arbitrage opportunities

- Network congestion

During periods of high volatility, fees may increase to better compensate liquidity providers.

During quieter periods, fees could decrease to attract more trading activity.

This creates a healthier balance between traders and liquidity providers.

Autonomous Risk Management

Risk management may eventually become fully automated.

Future AMMs could continuously monitor:

- Oracle anomalies

- Flash loan attacks

- Liquidity concentration

- Whale movements

- Smart contract risks

- Bridge vulnerabilities

If abnormal conditions are detected, liquidity parameters could automatically tighten or temporarily pause certain functions to reduce exposure.

This makes decentralized exchanges more resilient without requiring constant human intervention.

Tokenized Real-World Assets

As tokenized real-world assets (RWAs) continue to expand, AMMs will likely become the liquidity engine for:

- Tokenized Treasury bills

- Real estate

- Carbon credits

- Commodities

- Private credit

- Corporate bonds

- Tokenized equities

Autonomous liquidity systems will help price these assets more efficiently while maintaining deep, global liquidity around the clock.

Personalized Liquidity Strategies

Not every liquidity provider has the same goals.

Future AMMs may allow users to select AI-driven strategies tailored to their preferences, such as:

- Conservative income generation

- Low-volatility portfolios

- Aggressive yield optimization

- Stablecoin-focused liquidity

- Long-term asset accumulation

Instead of manually managing positions, users could delegate optimization to autonomous agents that continuously adjust strategies according to predefined risk preferences.

The Rise of Autonomous Financial Infrastructure

Eventually, autonomous market makers may evolve beyond decentralized exchanges.

They could become foundational infrastructure powering:

- Lending markets

- Stablecoin issuance

- Prediction markets

- Gaming economies

- Tokenized securities

- Machine-to-machine payments

- AI agent economies

As autonomous software agents begin conducting transactions on behalf of humans, intelligent AMMs could provide the liquidity layer that enables these machine-driven economies to function efficiently.

Challenges Ahead

Despite their promise, autonomous market makers still face significant hurdles:

- Ensuring AI decision-making remains transparent and auditable

- Protecting against manipulation of automated strategies

- Maintaining decentralization while increasing complexity

- Securing cross-chain infrastructure

- Navigating evolving regulatory frameworks

- Balancing automation with user control

Addressing these challenges will be essential to building trust and encouraging widespread adoption.

Climax

Autonomous Market Makers represent the next major evolution of decentralized finance. By combining AI, cross-chain interoperability, programmable liquidity, and automated risk management, they have the potential to make markets smarter, more efficient, and more accessible than ever before.

Rather than relying on static formulas alone, future AMMs will continuously learn, adapt, and optimize in real time. As blockchain ecosystems mature and financial activity becomes increasingly automated, these intelligent liquidity engines could serve as the backbone of a truly autonomous global financial system—one where capital flows seamlessly, markets respond instantly, and decentralized finance operates with unprecedented efficiency.

REQUEST AN ARTICLE

The UK’s National Crime Agency (NCA) and City of London Police have secured prison sentences for two men they say were involved with the “Scattered Spider” hacking group, a cybercrime crew prosecutors link to ransomware and cryptocurrency extortion schemes across the UK and the United States.

According to an NCA press release, the men pleaded guilty at Woolwich Crown Court on June 22 and were sentenced to five years and six months on Thursday. Authorities say the case is part of broader efforts to dismantle financially motivated cyberattacks in which cryptocurrency often plays a central role.

Key takeaways

- Two men connected to Scattered Spider received five years and six months in prison after guilty pleas at Woolwich Crown Court.

- UK investigators linked the group to intrusion activity targeting London’s public transport network in September 2024.

- US prosecutors have associated Scattered Spider with collecting at least $115 million in crypto ransom payments from dozens of US companies.

- Prosecutors say earlier attacks included a Caesars Entertainment breach and a subsequent Bitcoin ransom payment.

- The US Department of Justice previously reported an FBI seizure of about $36 million tied to wallets linked to the group.

UK sentencing follows a high-profile transport network breach

The NCA and City of London Police stated that the two defendants were associated with Scattered Spider. Investigators have previously linked the group to an intrusion into London’s public transport network in September 2024, an incident reported to have produced losses and recovery costs totaling 29 million British pounds (about $38.9 million).

That alleged breach underscores why cybercrime attributed to Scattered Spider has drawn attention beyond typical corporate fraud: public-sector and critical services are often targeted because operational disruption can be immediate and expensive, even when organizations ultimately recover their systems.

US prosecutors tie the group to crypto extortion at scale

The UK case comes as US authorities describe Scattered Spider’s wider footprint. A September press release from the Department of Justice (DOJ) said US prosecutors linked the group to collecting $115 million in cryptocurrency ransom payments from at least 47 US companies.

In the same DOJ release, prosecutors also characterized the attacks as disruptive to a broad range of targets—including critical infrastructure and the federal court system—suggesting that Scattered Spider’s activity was not limited to isolated enterprises but extended to organizations with heightened operational and regulatory importance.

That pattern matters for crypto investors and exchange and compliance stakeholders as well, because extortion campaigns can drive recurring demand for laundering services and complicate efforts to trace stolen funds once ransoms are paid.

Earlier allegations include Caesars Entertainment ransom in Bitcoin

The DOJ press release also accused Scattered Spider of breaching Caesars Entertainment and stealing a large customer database in September 2023. In connection with that incident, prosecutors said Caesars paid a $15 million ransom in Bitcoin (BTC).

For readers tracking the intersection of ransomware and cryptocurrency payments, this detail reflects a recurring dynamic in extortion cases: victims may seek to move quickly to stop ongoing damage, while attackers often demand digital assets that are typically easier to move than traditional payment rails.

FBI action targeting Scattered Spider-linked crypto wallets

The DOJ’s September release further reported that, in July 2024, the FBI seized approximately $36 million worth of cryptocurrency from wallets said to be linked to Scattered Spider.

According to the DOJ, investigators tied the group to at least 120 computer network intrusions. The agency said it traced and seized digital assets connected to wallets allegedly controlled by group members as part of its investigation.

While the UK sentencing is focused on two individual defendants, the seizure case highlights how law enforcement actions often span multiple stages—identifying suspected actors, attributing intrusions, and then attempting to disrupt the money movement that fuels ransomware and related extortion.

Looking ahead, the key uncertainty is how these cases will translate into sustained disruption of Scattered Spider’s operational capabilities. Readers should watch for further announcements on additional arrests, more wallet-related seizures, and any follow-up reporting that clarifies the extent of responsibility for the reported London transport breach and other high-profile targets.

Andy Burnham vows to be ‘pro-business Prime Minister’ and to reindustrialise Britain

Stablecoin growth will erode bank deposits, says ECB’s Cipollone

The 3 Best Netflix Shows to Binge This Weekend All Have One Thing in Common

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

NewsBeat22 hours ago

NewsBeat22 hours agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Crypto World2 days ago

Crypto World2 days agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Business1 day ago

Business1 day agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Politics2 days ago

Politics2 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Entertainment2 days ago

Entertainment2 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

News Videos3 days ago

News Videos3 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech3 days ago

Tech3 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Crypto World17 hours ago

Crypto World17 hours agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Tech3 days ago

Tech3 days agoDark Secrets Emerge When Jailbreaking LLMs

-

Business1 day ago

Business1 day agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

Sports2 days ago

Sports2 days agoNew Cornerback Enters Vikings Trade Rumor Mill

-

News Videos7 hours ago

News Videos7 hours agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

-

Business12 hours ago

Business12 hours agoBanco Bilbao Vizcaya Argentaria, S.A. (BBVA) Discusses Global Macro Environment and Economic Outlook for Core Markets Transcript

-

Tech4 days ago

Tech4 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

News Videos4 days ago

News Videos4 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Entertainment2 days ago

Entertainment2 days agoVicki Gunvalson Defends Discussing Heather Dubrow’s Money

-

Crypto World3 days ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

-

Crypto World15 hours ago

Crypto World15 hours agoClaude Fable 5 Slips to Second in AI Coding Leaderboard

-

Business13 hours ago

Nephros, Inc. (NEPH) Discusses Evolving Water Safety Strategies and Expansion Beyond Filtration Transcript

You must be logged in to post a comment Login