Crypto World

What is OTC trading in crypto? How whales buy big

When a company buys hundreds of millions of dollars of Bitcoin and the price barely moves, it did not use an exchange. It used an OTC desk. This guide explains over-the-counter crypto trading: why large orders cannot go through order books, how OTC desks source liquidity and settle trades, the difference between principal and agency desks, why so much real volume is invisible, and how to tell when the whales are quietly accumulating.

Here is a puzzle that confuses almost everyone new to crypto markets. A public company announces it bought $500 million of Bitcoin. On any exchange, an order that size would tear through the order book, spike the price, and cost the buyer a fortune in slippage, everyone would see it coming and front-run it. Yet the announcements keep arriving, the purchases keep completing, and the price frequently barely reacts. How?

The answer is a corner of the market most retail traders never touch and much of the real money never leaves: over-the-counter trading. OTC desks are where whales, institutions, corporate treasuries, miners, funds, and governments buy and sell crypto in sizes that would be impossible on public exchanges, through private, negotiated transactions that never appear in any order book. A large and growing share of crypto’s genuine volume happens here, off-screen, and the on-exchange charts that most analysis obsesses over are, in a real sense, only the visible tip of the market.

This guide explains that hidden layer. It covers why large orders cannot use exchange order books, what an OTC desk actually does and how a trade flows from request to settlement, the crucial difference between principal and agency desks and what each costs you, where OTC liquidity comes from, why this volume stays invisible and what that means for reading the market, the risks specific to OTC trading, and the on-chain signals that let outsiders glimpse the whales the order books hide.

Why big orders cannot use the order book

To understand OTC, first understand what it exists to avoid. An exchange order book is a ladder of resting buy and sell orders at various prices, and it has finite depth: only so much is available to buy at the current price, then a bit more slightly higher, then more higher still. A small order fills at the top and barely moves anything. A large order eats through level after level, filling at progressively worse prices, the price impact that grows as depth runs out, and a truly large order can move the market several percent against itself before it completes.

Worse, it does so in public. Order books are visible, and a large order climbing the ladder is a signal every other participant, and every bot, reads instantly: the moment the market sees a whale buying, prices run ahead of it, and the whale ends up chasing a rising market it created, paying a premium that compounds with every remaining coin. This is the reason a $500 million market order is not merely expensive but nearly impossible to execute well: the order’s own footprint is the enemy, and the bigger the order, the worse the self-inflicted damage. Splitting it into small pieces over time, algorithmic execution, helps and is widely used, but it takes time the buyer may not have and still leaks information across the many fills.

OTC exists to solve exactly this. A negotiated, off-book trade transfers a large block at a single agreed price, privately, with no order-book footprint and no public signal until, at most, a disclosure long after the fact. For size, it is not merely cheaper than the exchange; it is the only realistic venue.

What an OTC desk actually does

An OTC desk is a firm that stands between large buyers and large sellers, providing a private venue and, usually, its own liquidity, to move blocks the public market cannot absorb. The major exchanges run OTC desks, specialized firms run independent ones, and the largest trading houses run desks that serve institutions exclusively, and the same firms that act as authorized participants for spot ETFs often source their coin through exactly these channels. Their product is simple to state and hard to deliver: a firm price for a large quantity, executed discreetly, settled reliably.

A trade flows roughly like this. A buyer, say a corporate treasury acquiring $200 million of Bitcoin, contacts the desk, often through a relationship manager, and requests a quote for the size. The desk responds with a price, a single number for the whole block, that reflects the current market plus a spread covering the desk’s risk and margin. The buyer accepts or negotiates; on agreement, the trade is locked at that price regardless of where the public market moves in the next minutes. Settlement follows: the buyer sends funds, the desk delivers the coins, often through an escrow or simultaneous-exchange arrangement that protects both sides, and the whole transaction completes without a single order touching a public book. The buyer got certainty, one price, no slippage, no signal, and the desk earned its spread for absorbing the risk and sourcing the other side.

The relationship layer matters more here than anywhere else in crypto. OTC is a business of trust, credit, and compliance: desks run know-your-customer and anti-money-laundering checks, extend settlement terms to vetted counterparties, and compete on reliability and discretion as much as price. It is, in texture, far closer to traditional institutional finance than to the anonymous, permissionless world of on-chain trading, which is precisely why institutions are comfortable there.

Principal versus agency: who takes the risk

The single most important distinction among OTC desks is whether they trade as principal or as agent, because it determines where the risk sits and how you pay.

A principal desk trades against you from its own book: when you buy, the desk sells you coins it owns or immediately sources, taking the other side of your trade itself. It quotes you a firm price and then bears the risk of covering that position in the market, which is why principal quotes include a spread compensating for that risk. The advantage to you is certainty and speed: you get one price, immediately, and the desk’s problem of sourcing the coins without moving the market becomes the desk’s problem, not yours. The disadvantage is that the spread is the desk’s, and its interests and yours diverge at the margin, since it profits from the spread it can command.

An agency desk, by contrast, works on your behalf to find the other side, executing into the market or matching you against another client, and charges a transparent commission rather than trading against you. Your interests align better, the desk is your agent, not your counterparty, but you bear more of the execution risk and timing uncertainty, because the desk is not guaranteeing you a price, it is promising to work your order well. Large sophisticated players often prefer agency execution for its alignment and transparency; players who value certainty and speed over squeezing the spread prefer principal desks. Many desks offer both, and knowing which model a given trade uses is the first question a serious OTC counterparty asks, because it changes the entire cost and risk structure of the transaction.

Where the liquidity comes from

An OTC desk’s core skill is sourcing the other side of a block without disturbing the public market, and it draws on several pools to do it. The first is its own inventory: principal desks hold positions precisely so they can fill client orders instantly from stock. The second is a network of counterparties, other institutions, miners with coins to sell, funds rebalancing, other desks, that the desk can match against each other, so that a large buyer and a large seller cross privately at a price that serves both and moves nothing publicly. The third is the public market itself, worked carefully: a desk that takes a large buy order as principal must eventually cover it, and it does so by feeding the position into exchanges gradually, algorithmically, over hours or days, absorbing the price impact itself in exchange for the spread it charged the client.

Miners are a structurally important source, because they are natural, continuous sellers, they earn coins and must sell to cover costs, and routing that supply through OTC desks instead of exchanges keeps steady sell pressure off the public books, one reason miner-desk relationships are a quiet load-bearing feature of market structure.

This matching function is the desk’s real value: at its best, OTC is a mechanism for letting large buyers and large sellers find each other without either one’s size becoming a weapon against them, and the better a desk’s network, the more it can match internally and the less it must move the public market at all.

A worked block, and who is on the other side

A concrete example turns the abstraction into mechanics. A treasury company wants $200 million of Bitcoin and calls a principal desk. The desk quotes a single price, say the current market plus a spread of a few tenths of a percent, and the buyer accepts; the price is now locked for the full block regardless of what the public market does next. The buyer wires funds, the desk delivers coins through escrow, and the trade is done, no chart moved, no order book touched, one number for the whole $200 million.

Behind that clean surface, the desk now has a problem it was paid to take: it just sold $200 million of Bitcoin it must replace. If it held inventory, it draws it down and restocks over time; if it did not, it works the public market quietly for hours or days, buying in small algorithmic slices that each move the price a little, absorbing exactly the slippage the client paid to avoid. The spread the client paid is the desk’s compensation for that work and that risk, and a skilled desk that can match the buyer against a natural seller, a miner offloading a month’s production, a fund rebalancing out, avoids touching the public market at all and keeps more of the spread. This is why the desk’s counterparty network is its crown jewel: every internal match is a trade that moves nothing publicly and costs the desk nothing to cover.

The cast of characters on the other side of OTC blocks is worth knowing, because it is the market’s real supply and demand. Miners are the structural sellers, earning coins continuously and needing fiat for costs. Corporate treasuries and funds are episodic buyers and sellers, moving in size around strategy shifts. Early holders and whales distribute long positions through desks precisely to avoid signaling. Exchanges and other desks trade with each other to balance inventory. And increasingly, the intermediaries serving regulated products, the machinery behind spot ETFs and tokenized assets, source and offload through OTC channels, which is why a growing share of the market’s most consequential flows, the ones that actually set the balance of supply and demand, never appear on a single exchange chart.

Why it is invisible, and what that means

The defining feature of OTC volume is that it does not appear on the charts, and internalizing that fact reshapes how you read the market. Exchange volume, the number on every ticker, captures only trades that crossed a public book; the enormous flow that crosses privately through desks is absent, disclosed at best in aggregate and after long delays, if at all. Estimates consistently suggest that OTC and off-exchange volume rivals or exceeds visible exchange volume, which means the market analysts scrutinize is a large but partial sample of the real one.

The consequences are concrete. Price can move on thin visible volume while enormous OTC flow crosses unseen, so a quiet chart does not mean a quiet market. Accumulation and distribution by the largest players often happen almost entirely off-book, which is why major holders can build or exit positions that only become visible later, through disclosures or on-chain forensics, the reason exchange-reserve and whale-wallet data matter so much for reading real supply. And the relationship between on-exchange price and true supply-demand is looser than it appears, because the marginal large trade increasingly does not touch the exchange at all. Reading crypto markets well means constantly remembering that the visible order books are a screen in front of a much larger room, and that the biggest participants prefer the room.

OTC and the rise of on-chain settlement

The OTC world described so far is largely off-chain in its plumbing, private deals settled through escrow and banking rails, and one of the quiet shifts underway is the migration of parts of it onto blockchains themselves. Stablecoins changed the settlement leg first: instead of wiring dollars through correspondent banks, counterparties increasingly settle the cash side of OTC blocks in regulated stablecoins that move in minutes, around the clock, with the coin leg delivered simultaneously on-chain, collapsing settlement risk that once took days into a single atomic-adjacent exchange. The institutional stablecoins built for exactly this purpose have made the cash leg of large crypto trades faster and safer than its traditional-finance equivalent.

The deeper shift is that the assets themselves are becoming programmable in ways that touch OTC’s core function. As tokenized real-world assets and on-chain settlement layers mature, the historical trade-off OTC exists to manage, moving size without moving the market, gains new tools: dark-pool-style on-chain venues, request-for-quote systems that solicit private quotes from multiple desks, and settlement rails that let large blocks change hands with cryptographic finality rather than bilateral trust. None of this has replaced the relationship-driven desk business, which remains dominant for the largest and most sensitive flows, but it is steadily converting OTC from a purely private, trust-based world into a hybrid where the discretion of a negotiated block meets the finality of on-chain settlement. For a market whose largest trades have always happened in the shadows, the direction of travel is toward shadows with receipts, private in price discovery, verifiable in settlement, and the institutions bringing serious size on-chain are precisely the ones driving it.

Risks and the on-chain tells

OTC trading carries risks distinct from exchange trading, and they are worth naming. Counterparty and settlement risk is the central one: in a private bilateral trade, one side sends first unless a trusted escrow or simultaneous-settlement arrangement intervenes, and the history of OTC includes losses from failed settlement and bad actors, a bilateral counterparty exposure closer to traditional finance than to the atomic, trustless settlement of on-chain trades, which is why counterparty vetting and reputable desks matter enormously. Pricing opacity is another: without a public book, a client must trust that the quoted spread is fair, and less sophisticated counterparties can be quoted worse prices precisely because the market is private. Regulatory and compliance exposure runs throughout, since OTC desks are exactly where large flows attract scrutiny. And access is itself a barrier: OTC is a world of minimums, relationships, and vetting, effectively closed to retail, which is part of why its flows stay opaque to the public.

For outsiders, the compensating gift is on-chain data, which offers glimpses the order books hide. Large transfers into and out of known desk and exchange wallets, tracked by analytics firms, can signal OTC-scale accumulation or distribution before it shows in price; shrinking exchange reserves suggest coins moving to storage through private channels; and settlement patterns around major disclosed purchases sometimes leave on-chain fingerprints. None of it is as clean as an order book, but it is the closest an outsider gets to seeing the room where the size actually trades, and learning to read it, transfers, reserves, whale-wallet flows, is learning to see the market’s hidden majority.

The honest summary is that the crypto market most people watch and the crypto market where the largest decisions execute are substantially different places. The order books are real, useful, and public; they are also the retail-facing surface of a market whose deepest liquidity moves privately, negotiated, off-screen, through desks built so that size does not have to announce itself. Understanding OTC does not give a retail trader access to it, but it does something nearly as valuable: it corrects the illusion that the chart is the whole market, and it explains the puzzle with which this guide began, how the whales keep buying, in enormous size, without the price ever seeming to notice.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Details are current as of July 9, 2026. Always do your own research.

Frequently asked questions

What is OTC trading in crypto in simple terms?

OTC, or over-the-counter, trading is the buying and selling of crypto through private, negotiated deals rather than on public exchanges. A desk stands between large buyers and sellers, quoting a single price for a big block and settling it privately, so the trade never appears in any order book. It exists so that large orders can execute without the slippage and public signaling that exchanges would impose.

Why do large buyers use OTC desks instead of exchanges?

Because a large order on an exchange would eat through the order book, filling at progressively worse prices and moving the market against itself, while broadcasting the buyer’s intent to everyone watching. OTC delivers a single agreed price for the whole block, privately, with no order-book footprint, which for large size is both far cheaper and far more discreet than any exchange execution.

What is the difference between a principal and an agency OTC desk?

A principal desk trades against you from its own book, quoting a firm price and taking the other side of your trade itself, earning a spread and bearing the risk of covering the position. An agency desk works on your behalf to find the other side and charges a transparent commission instead of trading against you. Principal offers certainty and speed; agency offers better alignment and transparency.

How does an OTC trade actually settle?

After a price is agreed, the two sides exchange funds and coins, usually through an escrow or simultaneous-settlement arrangement that protects both parties from the other defaulting. Reputable desks run compliance checks and may extend credit terms to vetted counterparties. Settlement reliability is a core part of what a desk sells, since bilateral private trades carry real counterparty risk.

Why does so much crypto volume stay invisible?

Because OTC and off-exchange trades never cross a public order book, so they do not appear in the volume figures on tickers and charts. Estimates suggest this hidden flow rivals or exceeds visible exchange volume, meaning the market most people analyze is only a partial sample. It is why prices can move on thin visible volume while enormous flow crosses privately.

Can regular retail traders use OTC desks?

Generally not. OTC is a world of large minimums, standing relationships, credit, and vetting, effectively closed to retail-sized orders. Its whole purpose is moving blocks far larger than any individual trades. Retail traders interact with the same underlying market through exchanges, and can only glimpse OTC activity indirectly through on-chain data and disclosures.

How can I tell when whales are accumulating through OTC?

You cannot see it directly, but on-chain analytics offer clues: large transfers into and out of known desk and exchange wallets, shrinking exchange reserves suggesting coins moving to private storage, and settlement patterns around disclosed institutional purchases. These signals are noisier than an order book but are the closest an outsider gets to seeing OTC-scale accumulation before it shows in price.

Is OTC trading safe?

It carries risks distinct from exchange trading, chiefly counterparty and settlement risk in bilateral deals, pricing opacity without a public book, and the need to trust the desk’s fairness and reliability. Working with reputable, compliant desks and using proper escrow or simultaneous-settlement arrangements mitigates most of it, which is why relationships and reputation dominate the OTC business far more than in anonymous exchange trading.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

The US government moved nearly $300 million in seized Bitcoin and Ether to Coinbase Prime on Monday, renewing speculation that the assets could be sold.

Data from Arkham shows 3,940 Bitcoin (BTC) (worth $243.95 million) and 30,014 Ether (ETH) (worth $53.09 million) were sent to Coinbase Prime on Monday. The funds were linked to several high-profile US government crypto seizures.

“These coin movements were comprised of coins seized from ryan farace (“xanaxman”) and defunct crypto exchange btc-e,” said Galaxy Research head Alex Thorn, referring to the Bitcoin movements. The Ether is linked to Brian Krewson, an Oracle employee implicated in a $54 million crypto storage and money laundering scheme.

The transfers have drawn attention because a sale would appear to conflict with US President Donald Trump’s March 2025 executive order, which said Bitcoin seized by the US government should form part of the Strategic Bitcoin Reserve and should not be sold.

However, the deposits do not confirm a sale, as Coinbase Prime provides institutions with custody, trading, financing and staking services, meaning the transfers may simply reflect asset consolidation.

Related: US Bitcoin reserve hits snag as federal agencies debate for control: Bloomberg

Although the US government has previously transferred cryptocurrency to Coinbase Prime, Monday’s transfer was one of the largest from government-linked wallets this year.

In June, a US government-linked wallet moved 98,589 Chainlink (LINK) tokens to the platform, with the funds traced to assets seized from FTX and Alameda Research. In April, around 8.2 Bitcoin tied to the 2016 Bitfinex hack was sent to Coinbase Prime.

US government-linked wallets are estimated to still hold $20.6 billion in crypto, including around 325,000 BTC, 28,000 ETH, 146 million USDT and 750 Wrappd Bitcoin (WBTC).

Magazine: Bitcoin nearing late stages of bear market: Jamie Coutts, Real Vision

The Digital Asset Market Clarity Act, commonly known as the CLARITY Act, is gaining momentum in the US as a second major law enforcement organization publicly endorses the bill ahead of a critical Senate deadline. The Federal Law Enforcement Officers Association (FLEOA) said it submitted a letter to the Senate Banking Committee supporting the legislation, while urging targeted revisions—particularly around how decentralized finance (DeFi) protections are structured and how accountability is defined.

FLEOA’s July 10 endorsement arrives after earlier backing from the National Organization of Black Law Enforcement Executives (NOBLE) and comes as lawmakers weigh whether the bill can clear Congress before the Senate’s August recess. Industry observers have framed the recess period as a potential make-or-break window for final action this year.

Key takeaways

- FLEOA has endorsed the CLARITY Act in a letter to the Senate Banking Committee, calling it progress toward balancing innovation and public safety.

- The association supports the bill’s consumer-protection goals but wants changes to narrow DeFi-related protections and clarify who is accountable in decentralized systems.

- Law enforcement groups have previously raised concerns that portions of the bill—especially around developer liability—could create overly broad exemptions that hinder investigations.

- The timing is tight, with the Senate’s Aug. 8 recess cited as a key milestone for whether the legislation can pass this year.

Second endorsement—support with conditions

In its statement, FLEOA characterized the current CLARITY Act draft as “meaningful progress” toward establishing a regulatory framework for digital assets while preserving authorities needed to combat crime. The organization said the legislation should maintain existing capabilities related to criminal enforcement, anti-money laundering, counterterrorism financing, sanctions enforcement, and investigative work.

At the same time, FLEOA emphasized that lawmakers should refine specific DeFi provisions. According to FLEOA’s recommendations, the bill’s DeFi protections should be narrowed, clearer accountability should be established for participants within decentralized finance systems, and the legislation should prevent entities from avoiding regulation simply by portraying themselves as decentralized.

FLEOA also asked Congress to adjust the “specific intent” language to make liability easier to establish, and to explicitly confirm that the CLARITY Act does not limit existing federal investigative authority. The request reflects a core tension that has followed the bill through prior negotiations: how to protect legitimate innovation without inadvertently creating gaps that prosecutors and investigators could struggle to navigate.

Crypto Council CEO Ji Kim linked FLEOA’s support to a broader argument that the bill strengthens consumer protection and preserves law enforcement effectiveness, noting the endorsement in a public statement Monday.

Why law enforcement scrutiny has mattered

The fresh FLEOA letter lands on the heels of earlier objections from law enforcement organizations that challenged parts of the CLARITY Act—particularly around developer liability for misuse by users on decentralized platforms.

Earlier reporting highlighted that in June, four law enforcement organizations contacted the White House with concerns centered on Section 604, which aims to protect developers from liability tied to illicit activity conducted by users on decentralized networks. The organizations argued that the language, as written, might function as a broad exemption, potentially complicating investigations into crypto-related crime.

Those concerns prompted attention within the administration. The White House invited law enforcement groups objecting to the bill’s language to a late-June meeting—an indication that the disputes were not merely academic. In July, the Major County Sheriffs of America shifted from opposition to neutrality, reflecting that negotiations and proposed changes were actively shaping positions across law enforcement.

FLEOA’s new letter suggests that—while support for the CLARITY Act is increasing—there remains a category of legal uncertainty that enforcement advocates want addressed before the bill locks in. For investors, traders, and builders, the practical effect is straightforward: the scope of developer protection and the definition of responsibility in DeFi can influence how compliance strategies, product design, and risk management decisions are made.

What the Senate deadline means for prospects

FLEOA’s endorsement also underscores the political urgency surrounding the CLARITY Act. The letter was released less than four weeks before Aug. 8, when the Senate is expected to recess. According to Senator Cynthia Lummis, the window to pass a digital assets bill could be limited this year, warning that failure to enact meaningful legislation could leave rulemaking to other jurisdictions and prolong uncertainty for US market participants.

For the crypto sector, the legislative calendar matters not just for timelines, but for predictability. When a bill is approaching a recess, negotiations often compress: controversial language becomes more difficult to rewrite in depth, and stakeholders may shift their focus toward narrower edits rather than sweeping redesigns.

That dynamic helps explain why the FLEOA letter emphasizes targeted adjustments rather than a fundamental withdrawal of support. The group is signaling that it can back the overall approach—while still pushing for clarifications that could reduce enforcement friction later.

DeFi protections and accountability: the remaining fault line

At the heart of FLEOA’s requests is the question of how the CLARITY Act treats decentralized systems in practice. Supporters of the bill have argued that rules should recognize technological realities and avoid punishing developers for actions they do not control. Enforcement advocates, however, have warned that overly protective language could unintentionally insulate individuals or firms whose conduct resembles regulated activity—even if marketing or structural claims point toward decentralization.

FLEOA’s call to narrow DeFi protections and clarify accountability is therefore not just legal fine-tuning. It goes directly to whether investigators can build cases effectively, and whether compliance obligations remain aligned with operational control and influence.

Equally important is FLEOA’s emphasis on “specific intent” language and an explicit preservation of existing investigative authority. In legislative drafting, intent requirements can determine what must be proven in court. Changes here can shift burdens of proof and affect litigation risk for market participants.

What remains unclear—until lawmakers see the evolving text—is the balance Congress will strike between encouraging responsible development and ensuring that decentralization claims cannot be used as a shield against enforcement. Readers should watch whether forthcoming amendments address the specific points raised by FLEOA and other law enforcement organizations, or whether compromises keep the legislation’s enforcement implications ambiguous.

With the Senate’s August recess approaching, the next steps will likely hinge on how quickly the committee can incorporate these requested revisions into a final bill text—and whether additional groups move toward alignment or raise new objections as the calendar tightens.

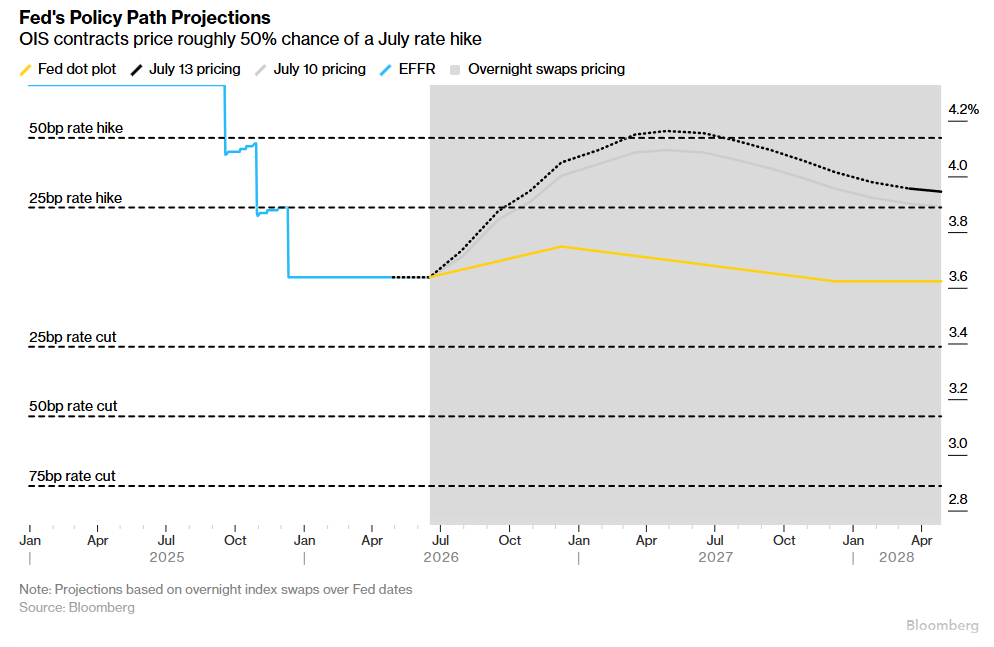

Federal Reserve Chairman Kevin Warsh testifies before Congress Today, July 14, and tomorrow. Bond traders increasingly bet the week will confirm what markets already suspect. A rate hike is coming in July.

The testimony lands alongside fresh inflation data and a wave of bank earnings. That makes this one of the most consequential weeks for anyone with a mortgage, a savings account, or a credit card balance.

Why Rate-Hike Odds Have Jumped

Traders have pushed the market-implied chance of a quarter-point hike this month to about 50%. Just weeks ago, that number sat under 10%. Two-year Treasury yields, which track Fed policy expectations closely, have stayed above 4.25%.

Fed Governor Christopher Waller triggered the shift. Markets had viewed him as one of the central bank’s most dovish officials. Waller said policymakers should consider a hike soon if upcoming data show another “hot reading” on core prices.

June’s Consumer Price Index, also releasing Tuesday, should show headline inflation easing to around 3.8% from May’s 4.2%. Falling gas prices are driving that drop.

Core inflation, which strips out food and energy, should tick down only slightly, to around 2.8% from 2.9%. That keeps it well above the Fed’s 2% target. This stickiness is exactly why rate-sensitive chip stocks still face CPI risk.

Don’t Expect Warsh to Tip His Hand

Warsh took office in May and he has already built a reputation for avoiding forward guidance. He made that clear this month at a central-bank symposium in Portugal.

“I want us to have a good family fight. When we get into that room and shut the door, we’re going to have a good debate, but I don’t have much more for you than that.”

So the testimony itself likely won’t confirm a hike. Instead, expect lawmakers to press Warsh on Fed independence from the Trump White House.

They’ll also ask whether AI-driven demand is adding to inflation, and how tariffs and Middle East oil disruptions keep filtering into consumer prices.

The real decision arrives at the Fed’s July 29 meeting, not this week’s hearings.

What a Hike Would Mean for Regular Households

A hike would raise rates on credit cards, home equity lines, and adjustable mortgages. That’s unwelcome news for borrowers already stretched by elevated inflation. Savers benefit more directly. Banks typically raise yields on savings accounts and CDs when the Fed hikes.

The post Warsh Testifies to Congress Today: Will He Bring a Rate Hike in July? appeared first on BeInCrypto.

West Texas Intermediate crude futures have surged to nearly $80 a barrel from $67 at the start of the month, stoking fresh concerns about inflation.

Focus on CPI and Warsh testimony

Investors will receive a fresh read on price pressures Tuesday when the Labor Department releases the June consumer-price index at 8:30 a.m. ET.

Economists surveyed by Bloomberg forecast that headline CPI will fall below a 4% annual rate. The report is expected to show the first declines in both headline and core inflation since January, following May’s readings of 4.2% and 2.9%, respectively.

Even if the figures meet expectations, they risk being viewed as backward-looking in light of the recent oil price surge. Should inflation instead prove more persistent, the data could amplify concerns about the Fed’s path forward.

Attention will then turn to Mr. Warsh’s testimony on Capitol Hill. Given the Fed chair’s preference for limited forward guidance, investors will be watching closely for any signals on rates and inflation.

According to analysts at ING, he could “if he chooses, emphasize the tameness of inflation expectations.”

They added that Mr. Warsh “has enough ammunition here to ride the rate hike risk and instead hold pat. Even if he comes under pressure to hike, the richness attached to the 5yr part of the curve tells us that any hike (if delivered) is likely to be subsequently reversed, with the prospect still for bigger cuts than hikes.”

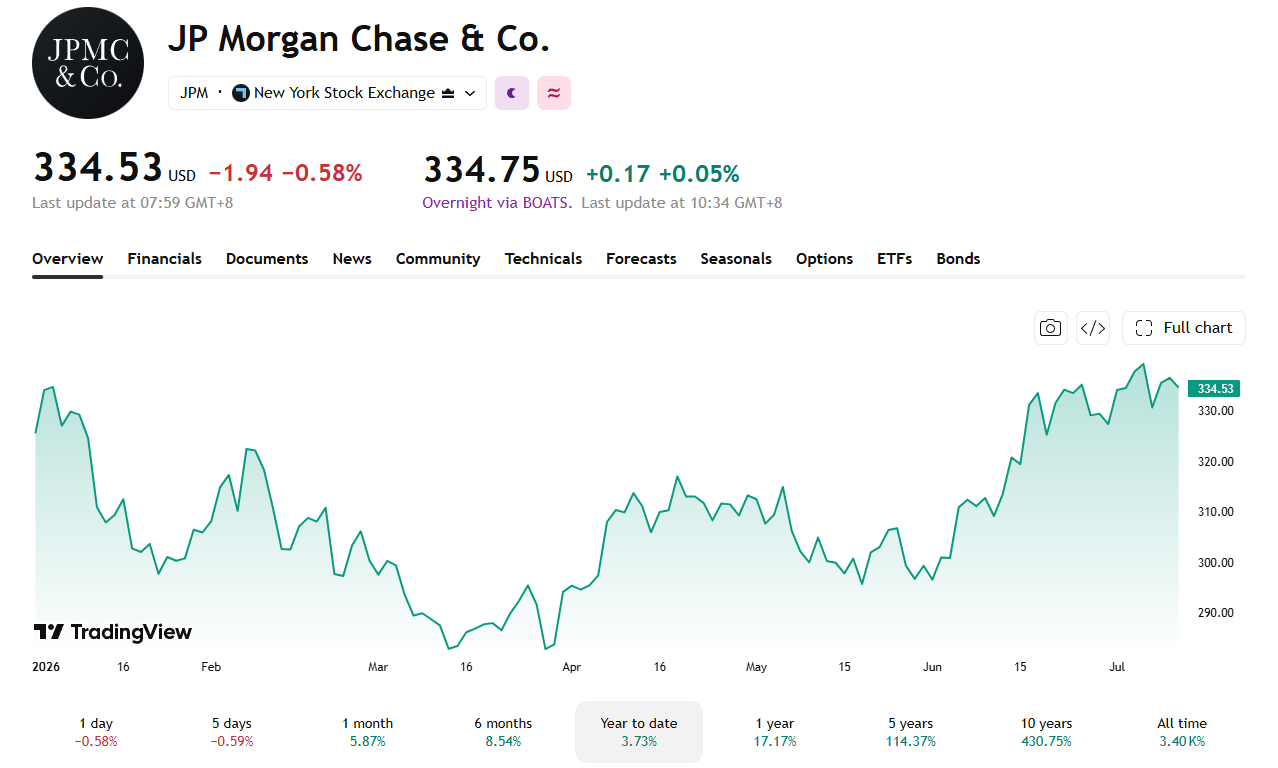

JPMorgan Chase, Bank of America, Wells Fargo, and Goldman Sachs report second quarter earnings Today, July 14. Analysts expect all four banks to post higher year over year revenue and profit, even as war in Iran and stubborn inflation weigh on markets.

The reports arrive as investors search for signs the US economy can absorb geopolitical shocks and elevated interest rates. Executives’ comments on lending, trading, and deal activity will shape sentiment for the rest of earnings season.

Why This Earnings Batch Matters

The four lenders report against a volatile backdrop; Renewed fighting in Iran has pushed oil prices higher, and inflation remains stickier than expected. However, the Federal Reserve has yet to cut interest rates this year, keeping borrowing costs elevated for consumers and businesses.

Fed Chair Kevin Warsh also testifies before Congress this week. That adds another variable for markets already digesting the bank results.

Jay Woods, chief market strategist at Freedom Capital Markets, said in an optimistic tone from bank executives could reshape how investors view the broader economy.

“If the banks paint an optimistic picture while credit quality remains strong, it could reinforce the narrative that the economy is proving far more resilient than many expected.”

What Analysts Expect From Each Bank

Analysts project Analysts expect JPMorgan to post the strongest growth of the four, with revenue up nearly 14% to $51.1 billion. Its wealth management business is driving most of that gain.

Goldman Sachs should see revenue climb 11% and profit jump 26%. Bank of America’s revenue should grow over 16%, while Wells Fargo, the weakest performer of the group this year, is expected to grow just 5%.

Strong bank earnings this week would send a reassuring signal to the wider market. Banks sit at the center of the economy, so healthy profits suggest consumers are still spending, businesses are still borrowing, and credit quality hasn’t cracked despite war in Iran and stubborn inflation.

For everyday investors, that could mean more confidence in stocks generally, since bank results often set the tone for the rest of earnings season.

But the picture isn’t all upside. Rising deposit costs and pressure on lending margins suggest banks may need to work harder for the same profits ahead, a dynamic that could eventually show up in loan rates or account fees for regular customers.

The Risk Beneath the Optimism

Morgan Stanley strategist Michael Wilson noted that banks are funding loan growth with costlier deposits. That dynamic could pressure profits further into 2027, prompting modest earnings estimate reductions across the sector.

Still, the industry’s balance sheet looks unusually strong. Tom Michaud, CEO of KBW, projects a tangible common equity ratio of 9.7% by the end of 2027 and that level would sit over 50% above where the industry stood entering the 2008 financial crisis. Banks could use that cushion to raise dividends, buy back stock, or pursue acquisitions.

Tuesday’s results will set the tone for a busy earnings week that also features major tech and consumer names. Whether banks can sustain growth while inflation and geopolitical risk persist remains the open question for markets.

The post Big Bank Earnings Today: Will Results Calm Economic Fears? appeared first on BeInCrypto.

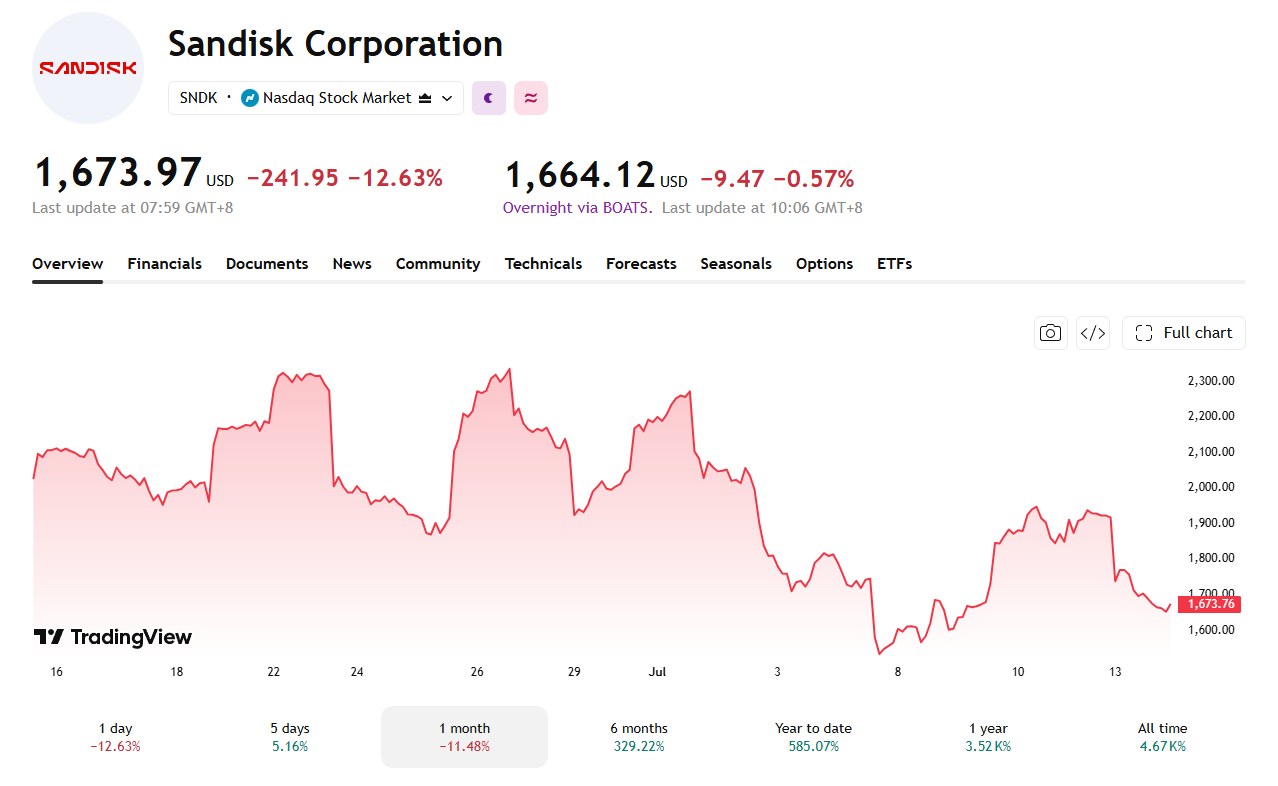

SanDisk (SNDK) stock fell 12.63% Monday, July 13, and slid further after hours, as a broad selloff hit memory and chip stocks. Several Wall Street analysts still raised or reaffirmed their price targets on the company despite the drop.

The moves show analysts trust SanDisk’s earnings outlook, even as memory sector volatility has rattled the wider group in recent weeks.

Analysts Defend Bullish Case Despite the Slide

Citigroup reiterated its $2,500 price target on SanDisk with senior analyst, Asiya Merchant, issuing a bullish note and maintaining a buy rating on SNDK. The price target implies roughly 30% upside from the most recent close.

Evercore ISI analyst Amit Daryanani went further, he raised his target to $3,100 from $1,400 and kept an “Outperform” rating. The new target implies nearly 62% upside from the last close. Daryanani argues investors underestimate the durability of SanDisk’s earnings and pricing power through 2027.

Bernstein analyst Mark Newman lifted his target to $3,000 from $1,700. He points to structural changes in how memory suppliers now write long-term supply agreements.

Wedbush analyst Matthew Bryson told MarketWatch the memory market remains “in a very good place.” He said Micron (MU) and SanDisk both benefit from AI-driven demand that chipmakers cannot quickly match, since new fabs take years to build.

Retail Sentiment Stays Extremely Bullish

Stocktwits data showed “extremely bullish” retail sentiment on SNDK, with high message volume. A related poll of nearly 1,800 respondents put Micron ahead for best returns, at 57%. SanDisk drew 19%, still reflecting continued capital flowing into memory stocks despite the pullback.

Data puts 18 of 22 analysts covering SanDisk at “Buy” or “Strong Buy,” with an average target of $2,112.32. Shares remain up nearly 600% year to date, a run that has also stirred renewed AI bubble concerns across the sector.

The next earnings cycle will show whether SanDisk can grow into targets north of $3,000.

The post SanDisk Stock Keeps Sinking, So Why is Wall Street More Bullish? appeared first on BeInCrypto.

The US government sent $297 million in Bitcoin (BTC) and Ether (ETH) to Coinbase Prime in two transfers on Monday. Blockchain intelligence firm Arkham tracked an initial $8.8 million deposit, then a second $288.33 million deposit three hours later.

The larger transfer combines forfeitures from three separate criminal cases. It includes assets tied to Brian Krewson, the defunct BTC-e exchange, and dark web drug dealer Ryan Farace.

A Pattern Tracked Before

This is not the first false alarm from a Coinbase Prime deposit. Forfeited funds moved the same way in January, sparking Samourai Bitcoin sale rumors. The government has repeated the move with other seized assets since then.

It sent seized FTX Chainlink tokens to Coinbase Prime in June and seized Alameda altcoins in May. Neither transfer turned into a confirmed sale.

Monday’s transfers follow the same script, but at a larger scale. Three unrelated forfeiture cases moved to Coinbase Prime within hours of each other, but the question stays open until Treasury or the Marshals Service comments directly on a sale.

Executive Order, Still Not Law

Trump’s March 2025 executive order created the Strategic Bitcoin Reserve partly aimed at baring the government from selling its Bitcoin holdings. But the rule exists only by executive decision, not statute.

Congress introduced the codify Bitcoin reserve bill in May to lock in a 20-year holding period. It has not advanced past committee with many seeing it as a strong indicator of this administrations belief in Bitcoin. However, as BTC continues to be sent to exchange wallets, people are speculating as to the intention behind these moves.

The US’s Dark Bitcoin

Much of the US government’s Bitcoin holdings trace back to criminal forfeitures. Monday’s deposit combines three of the highest-profile cases.

Krewson helped store and launder $54 million in crypto for two convicted drug traffickers, the Department of Justice said. BTC-e ran as an unlicensed exchange from 2011 to 2017. It processed more than $9 billion before its shutdown, according to DOJ court filings.

Farace generated over 9,138 Bitcoin from dark web drug sales. He received a 54-month sentence in 2023.

The post US Government Sends $297 Million in Seized Crypto to Coinbase in One Day appeared first on BeInCrypto.

Japanese convenience store operator Lawson will test payments with the yen-denominated JPYC stablecoin in early August.

Summary

- Lawson will connect JPYC payments directly to its POS system during a single-store Tokyo trial.

- Customers will scan mobile wallet barcodes, while HashPort updates balances using verified checkout transaction data.

- Japan’s megabanks are also preparing yen stablecoins, widening competition across regulated digital payment networks nationwide.

The company will run the trial at its Takanawa Gateway City store in Tokyo’s Minato Ward. HashPort, a digital asset wallet provider, will support the payment system and process balance changes linked to purchases.

Lawson described the project as Japan’s “first” stablecoin payment trial connected directly to a point-of-sale system. That claim comes from the company and the test has not yet started. Lawson has not announced a chainwide launch.

It will decide on wider use after checking system stability and transaction speed. The company will also review whether the process fits normal store operations without slowing customers or adding extra work for employees during busy periods.

How the POS-integrated payment will work

Customers will open a supported mobile wallet and display a barcode on their phones. A Lawson employee will scan the barcode with the store’s existing POS terminal. HashPort will then use the payment information to update the customer’s JPYC balance. The process keeps the checkout within Lawson’s current store system.

The POS link will also allow Lawson to manage purchase details, including product quantities and payment times, alongside its usual sales data. The trial will measure how reliably the systems connect and how long each payment takes.

Customers will use stablecoins at checkout, but staff will still handle the scan through the normal sales terminal. Lawson can compare the stablecoin flow with card and QR payments, including processing steps, error handling and the time needed to finish each sale.

JPYC moves into everyday retail

JPYC Inc. began issuing JPYC on October 27, 2025. The token tracks the Japanese yen and uses yen deposits and Japanese government bonds as reserve assets. As crypto.news reported, the stablecoin initially waived transaction fees and aimed to support payments and transfers under Japan’s regulated framework.

Lawson’s test follows smaller retail and service launches. Japanese okonomiyaki restaurant operator Chibo started accepting JPYC at selected stores in April, according to Financial News. Dental clinics in Tokyo and Chiba also plan to add JPYC payments with HashPort.

The Lawson trial differs because it links the stablecoin payment directly with a major retailer’s POS system. The report said stablecoins may offer merchants lower fees than cards or QR services, though Lawson has not released fee figures for this pilot.

Japan expands regulated stablecoin activity

Japan’s large banks are also preparing yen-based stablecoin services. MUFG Bank, Sumitomo Mitsui Banking Corporation and Mizuho Bank plan to begin live transactions during fiscal 2026, which ends in March 2027. As crypto.news reported, the banks formed a council to develop shared rules for issuance, governance, systems and future participation.

Moreover, the banking project follows an FSA-backed test involving corporate cross-border payments and Progmat’s blockchain infrastructure. Japan has also opened regulated access to foreign stablecoins. Ripple and SBI launched the dollar-backed RLUSD through SBI VC Trade in June 2026 after approval from the Financial Services Agency.

American Bitcoin shares have fallen more than 95% from their peak, according to Bloomberg, cutting over $600 million from the value of Eric Trump’s roughly 6% stake.

Summary

- American Bitcoin’s stock lost over 95% despite its treasury growing beyond 8,000 BTC this month.

- The reverse split lifted ABTC’s quoted price but left the company’s underlying market value unchanged.

- A $117.2 million Bitcoin charge drove Q1 losses while mining costs fell sharply per coin.

The Bitcoin miner and treasury company reached a record low on Wednesday after months of selling pressure. ABTC closed at $6.13 on July 10, the latest available market close.

The fall followed a 1-for-15 reverse stock split that took effect after trading on July 2. Split-adjusted trading began on July 6 under the same Nasdaq ticker. The company reduced its issued share count from about 1.09 billion to roughly 73 million. A reverse split raises the quoted share price but does not increase the business’s total value.

Reverse split fails to stop selling pressure

American Bitcoin used the reverse split to support compliance with Nasdaq’s minimum bid-price rule. Shareholders approved the move at the company’s annual meeting in June. Crypto.news reported the approval on June 25, when ABTC remained under pressure despite the planned change. The stock then fell after split-adjusted trading started.

The company has not said the split can reverse its market decline. Reverse splits can help a listed company meet exchange rules, but investors still price its earnings, assets, debt and outlook. Bloomberg’s calculation places the stock more than 95% below its peak. That decline reflects split-adjusted prices rather than a direct loss caused by the share consolidation.

Bitcoin reserve grows beyond 8,000 BTC

American Bitcoin continues to mine and accumulate Bitcoin while its share price falls. The company added 500 BTC in its latest update, taking its reserve above 8,000 BTC. As crypto.news reported on July 7, the treasury had more than tripled since the company’s Nasdaq debut. The firm also said its satoshis-per-share measure had nearly tripled.

Eric Trump promoted the treasury growth and described the company’s operating model as “virtually unmatched” during an earlier selloff. That statement represents his view, not an independent measure of performance. The company’s strategy combines large-scale Bitcoin mining with direct purchases. It keeps mined coins rather than selling them to cover routine costs, according to management.

Bitcoin charge weighs on first-quarter results

American Bitcoin reported a $118.2 million operating loss for the first quarter of 2026. The result included a $117.2 million non-cash charge tied to the lower market value of its Bitcoin holdings. The company reported an $81.8 million net loss and $62.1 million in mining revenue. Bitcoin fell about 22% during the quarter.

Management said the accounting charge masked stronger mining operations. Chief executive Mike Ho said the “underlying business was profitable” after excluding the mark-to-market adjustment, and said American Bitcoin did not sell any coins. The company mined 817 BTC during the quarter and cut its production cost per Bitcoin to $36,200, down from $46,900 in the prior quarter.

The balance sheet still links American Bitcoin stock closely to Bitcoin prices and mining economics. Lower Bitcoin prices reduce the market value of its reserve and can weaken revenue per mined coin. Higher power, equipment or hosting costs can also narrow margins. Hut 8 provides key infrastructure and remains central to the company’s mining setup.

American Bitcoin’s growing reserve gives shareholders Bitcoin exposure, but treasury growth has not supported its market price. The company must keep Nasdaq compliance while funding mining and purchases. Its next results will show whether lower production costs can offset Bitcoin prices and whether the 8,000-BTC reserve can support the business without pressure on shareholders.

While Washington’s attention fixes on whether the CLARITY Act can find seven Democratic votes before the August recess, the Securities and Exchange Commission has been quietly assembling the framework that governs American crypto if the bill dies, and much of it even if the bill passes.

Summary

- Regulation Crypto would create a four-year startup exemption for crypto projects raising up to 5 million dollars per year.

- A separate fundraising exemption would let more mature issuers raise up to 75 million dollars annually with lighter disclosure than full registration.

- The safe harbor would give tokens a defined path out of securities classification once issuer-led managerial efforts permanently end.

- The rule could operate alongside the CLARITY Act, but if the bill fails, it may become the main US crypto capital-formation framework.

- The biggest fights ahead are over dollar thresholds, decentralization standards, investor protections, and litigation risk.

On July 7, the agency confirmed plans to formally propose Regulation Crypto, its first major crypto-specific rulemaking under Chair Paul Atkins. The proposal, expected to run past 400 pages, sits under review at the White House Office of Information and Regulatory Affairs, the final gate before publication for public comment, and Atkins has said release is expected shortly after that review completes.

The package does three concrete things. It gives new crypto projects a startup exemption from full securities registration for up to four years while they build toward network maturity, raising up to 5 million dollars annually against whitepaper-style disclosures. It creates a fundraising exemption allowing more mature issuers to raise up to 75 million dollars in any 12-month period with audited financials and semiannual reporting, a burden far lighter than full registration. And it writes an investment contract safe harbor: a rules-based path for a token to exit securities classification entirely once its issuer has permanently ceased the essential managerial efforts that made it an investment contract in the first place.

Atkins has repeatedly described the framework as a bridge to the CLARITY Act. The description is honest and incomplete at the same time. A bridge implies something temporary that the statute replaces; in reality, Regulation Crypto answers questions the bill does not reach, will operate for years regardless of the Senate outcome, and, if the bill fails, becomes the entire de facto constitution of American crypto capital formation. This feature decodes what the rule actually does, where it came from, why Senate Democrats consider it an end-run, and what it means for the market that one of these two frameworks is arriving no matter what happens in the next three weeks.

The taxonomy underneath: five buckets instead of one question

Regulation Crypto did not appear from nothing. Its foundation is a joint SEC and Commodity Futures Trading Commission interpretive release from March 17, 2026, which replaced the enforcement era’s single endless question, is this token a security, with a working taxonomy of five categories: digital commodities, digital collectibles, digital tools, stablecoins, and digital securities. Under the interpretation, only digital securities, tokenized versions of traditional financial instruments, remain fully subject to the securities laws. The other categories may still trigger securities obligations if sold as part of an investment contract, which is where the Howey analysis survives, but the default presumption flipped: most tokens are not securities by nature, and the legal question becomes how they were sold, not what they are.

Atkins introduced the exemption framework the same day, in a speech at the DC Blockchain Summit titled Regulation Crypto Assets: A Token Safe Harbor, and the agency submitted the proposed rules to the White House within the week. The sequencing matters for understanding what kind of project this is. The interpretive release stated how the agency reads existing law; interpretations bind nobody and evaporate with the next chair. The proposed rule converts the reading into formal regulation, with notice, comment, and the full Administrative Procedure Act process, which makes it dramatically harder to unwind. The past year’s accommodations, staff guidance, no-action letters, dropped enforcement actions, carry no binding force at all; a future commission could reverse them by memo. A finalized Regulation Crypto could only be undone by a new rulemaking that survives its own comment period and litigation. Durability is the entire point, and durability is exactly what the industry has said it needs.

The chair’s broader agenda frames the rule as one panel of a triptych. Atkins has described crypto market structure, custody, and capital formation as the agency’s three crypto priorities, with the stated goal of making the United States the leading crypto capital. He has asked staff to evaluate letting non-security crypto assets that were sold under investment contracts trade on venues not registered with the Commission, to clear paths for state-licensed platforms to list such assets, and to let CFTC-regulated platforms offer them with margin. He also shut down the agency’s crypto innovation hub, arguing the Gensler-era version was so tainted that industry participants feared subpoenas after visiting, a symbolic demolition that tells its own story about how completely the agency’s posture has inverted.

The three exemptions, decoded

The startup exemption is the on-ramp. A new project receives up to four years of relief from full registration while it develops its network, during which it can raise up to 5 million dollars per year. The disclosure standard is principles-based and deliberately modeled on what serious projects already publish: whitepaper-style documentation of the technology, the token economics, and the team, plus required financial statements to investors. The four-year clock is the regulatory embodiment of an idea the industry has argued since 2018, that decentralization takes time, and that forcing registration at launch, when a network is inescapably centralized, guarantees either noncompliance or offshoring. The exemption’s wager is that a project given four lawful years will either mature into something the safe harbor releases or grow into something the fundraising tier can carry.

The fundraising exemption is the growth pathway, and its design is more conservative than the headline suggests. The 75 million dollar annual cap is borrowed directly from Regulation A+, the existing exemption for smaller public offerings by conventional issuers; Atkins adapted a tested framework instead of inventing one. The obligations scale accordingly: audited financial statements and ongoing semiannual reporting, meaningfully heavier than the startup tier’s whitepaper standard, meaningfully lighter than a full registration. For the mid-sized token issuer, the practical effect is a lawful domestic alternative to the offshore foundation structures that became the industry’s default architecture, with a compliance bill measured in hundreds of thousands of dollars instead of tens of millions.

The investment contract safe harbor is the philosophical core and the piece with no statutory parallel. It answers the question the Torres ruling in the Ripple case raised but could not settle: when does a token that was sold as a security stop being one? The safe harbor’s answer is a rule-based test keyed to managerial effort. Once an issuer has permanently ceased the essential managerial functions that investors relied on, the token exits securities classification, full stop. That converts decentralization from a rhetorical claim into a compliance milestone with legal consequences, and it gives every project in the startup tier a defined destination. It is also, not coincidentally, the provision that most directly generalizes the industry’s hardest-won litigation outcomes into standing law, the same conceptual territory Ripple spent 150 million dollars mapping, as the token-versus-sale distinction moved from courtroom argument to regulatory architecture.

The objection: an agency legislating around the legislature

Senate Democrats have noticed that the SEC is building, by rule, much of what Congress has not agreed to build by statute, and their objection deserves a full hearing because it is not frivolous.

Elizabeth Warren and Chris Van Hollen wrote to Atkins directly, charging that the agency plans to exempt most cryptocurrencies from the securities laws with significant potential harm to investors, and calling on Congress to close the loopholes as it considers market structure legislation. Financial industry commenters have warned that broad exemptive relief could import cybersecurity risks, illicit-finance exposure, and flash-crash volatility into markets stripped of their traditional guardrails. The constitutional-order version of the critique is sharper still: an agency whose chair previously advised crypto firms is using administrative discretion to deliver, in advance, the deregulatory half of a bill the elected branch has not passed, while the accountability provisions Democrats attached to that bill, the ethics rules aimed at the president’s 2.3 billion dollars in crypto exposure, have no administrative equivalent and can only exist in statute. Regulation Crypto, on this reading, is not a bridge to CLARITY. It is a mechanism for harvesting CLARITY’s benefits without paying CLARITY’s political price, and every week it advances reduces the industry’s urgency to compromise on the ethics language currently blocking the bill, a standoff crypto.news has followed into its decisive month.

The rebuttal has two layers. Legally, exemptive authority is not a loophole; Congress wrote it into the securities laws deliberately, and Regulation A+, Regulation D, and Regulation Crowdfunding are all products of the same power. An agency tailoring registration requirements to a novel asset class through notice-and-comment rulemaking is the administrative state working as designed, and the courts, not letters, will test whether this rule exceeds the statute. Practically, the alternative to Regulation Crypto is not the status quo Democrats prefer; it is the pre-2025 regime of regulation by enforcement that a federal judge partially repudiated and that nearly dissolved companies later vindicated. Between an imperfect rule with a comment period and an enforcement lottery with none, the rule is the more accountable instrument, whatever one thinks of its content.

What both sides quietly agree on is the stakes of reversibility. Democrats want the ethics and consumer provisions in statute because statutes bind future administrations; the industry wants the exemptions in a finalized rule for precisely the same reason. The entire fight, in Congress and at the agency simultaneously, is about who gets to make their preferences durable first.

How the agency got here: from Hinman speech to Howey off-ramp

The rule reads differently with a decade of institutional history attached, because every one of its provisions answers a specific wound.

The startup exemption answers the original sin of the ICO era. In 2017 and 2018, hundreds of projects raised capital from Americans with no disclosure standard at all, the agency responded with a wave of enforcement that treated every token sale as an unregistered offering, and the surviving industry drew the obvious lesson: incorporate in Zug, exclude Americans, and disclose nothing. The exemption’s whitepaper-based standard is a wager that a lawful middle existed all along, and that the agency’s refusal to build it, not the industry’s refusal to use it, drove a decade of capital formation offshore.

The safe harbor answers the Hinman problem. In 2018, a senior SEC official famously suggested in a speech that Ether, whatever its origins, had become sufficiently decentralized that its sales were no longer securities transactions. The industry spent years trying to hold the agency to that logic, the agency spent years insisting the speech was one man’s opinion, and the internal documents Coinbase later pried loose in litigation showed officials themselves could not agree on what the standard was. Commissioner Hester Peirce proposed a formal token safe harbor twice, in 2020 and 2021, and was ignored by her own agency both times. The current safe harbor is Peirce’s idea with Atkins’ signature, arriving seven years after the speech that made everyone realize the question had no answer.

And the fundraising tier answers the enforcement era’s quietest casualty: the mid-sized compliant issuer that never existed because there was no rule to comply with. Between the 5 million dollar seed rounds that Regulation D could awkwardly cover and the public listings that only exchanges and miners attempted, an entire capitalization band of the industry simply had no American on-ramp. Borrowing Regulation A+’s 75 million dollar ceiling is the agency conceding that the band was a regulatory artifact, not a market verdict.

The arc from Gensler to Atkins, from an agency that sued first and declined to write rules even under court order, to an agency proposing 400 pages of them, is the sharpest institutional reversal in modern financial regulation, and it happened without a single statute changing. That fact is the strongest argument for the rule and the strongest argument against relying on it, at the same time.

What can still change: the comment period is not a formality

Between OIRA clearance and a final rule stand months of process in which the package’s most important parameters remain genuinely contestable, and market participants pricing the framework as finished are early.

The dollar thresholds are the obvious pressure point. Consumer advocates and Senate Democrats will push the 75 million dollar ceiling down and load the startup tier with conditions; industry commenters will push for inflation indexing and aggregate-cap clarity, since the current design names annual limits without a publicly specified lifetime ceiling. The decentralization test inside the safe harbor is the subtle one. Permanently ceased essential managerial efforts is a phrase that will absorb tens of thousands of comment pages, because it decides whether the off-ramp is a real destination or a mirage: too strict, and no foundation-supported network ever qualifies; too loose, and every project theatrically dissolves its team on paper while running development through affiliates. The illicit-finance overlay is the political one. The same law enforcement coalition currently fighting the CLARITY Act’s developer protections, a split crypto.news dissected as the Senate vote approached, will demand that exempted issuers carry monitoring obligations the statute never imposed, and the agency’s answer will determine whether the exemptions are usable by actually decentralized projects or only by companies that look like broker-dealers with extra steps.

Litigation risk frames all of it. A finalized rule this consequential draws challenges from both flanks: investor-protection groups arguing the agency exceeded its exemptive authority by hollowing out registration, and, conceivably, industry plaintiffs attacking whatever conditions survive comment. Post-Chevron, courts owe the agency’s statutory reading no deference, and a single adverse circuit decision could stay the framework for years. This is the structural reason Atkins keeps calling the rule a bridge and pressing Congress to act anyway: he is building the most durable thing an agency can build while publicly acknowledging it is the second-most durable thing available.

Regulation Crypto versus the CLARITY Act: substitutes, complements, or race

Mapping the two frameworks against each other shows they overlap less than the political rhetoric implies, which is why the with-or-without framing in this feature’s title is literal.

The CLARITY Act’s center of gravity is market structure: which agency supervises trading, how exchanges and brokers register, how the CFTC gains spot authority over digital commodities, how developers escape money transmitter liability. Regulation Crypto’s center of gravity is capital formation: how tokens are launched, funded, and eventually released from securities status. The bill barely touches primary issuance mechanics; the rule barely touches secondary market supervision. A world with both is coherent: CLARITY sorts the assets and assigns the regulators, Regulation Crypto governs how new assets are born. Atkins’ bridge metaphor undersells his own product; the honest description is that the rule is the bill’s missing chapter, written by the agency because the legislature never drafted one.

The substitution effect appears only in the failure scenario, and there it is nearly total. If the Senate misses the August window and the 2030 warnings prove accurate, Regulation Crypto plus the March taxonomy plus the CFTC’s stretched existing authority become the entire American framework: token launches under the exemptions, classifications under the five buckets, trading under a patchwork the rule’s platform provisions try to rationalize. That regime would function, and its existence is precisely what Galaxy Research and others cite when they note that CLARITY’s failure would be a slow bleed rather than a catastrophe. But it would be a framework resting on one commission’s rulemaking, contestable in court, reversible by a hostile successor with patience, and silent on everything from illicit finance funding to the ethics questions that stalled the bill. The GENIUS Act fight already previewed what statute-versus-regulator arguments look like when real money is at stake, with state and federal authorities wrestling over stablecoin turf in a battle crypto.news covered throughout its Senate run, and the yield wars that followed passage show how much conflict survives even a signed law, a standoff crypto.news has tracked between banks and issuers over 6 trillion dollars in deposits.

There is also a timing race with the bill’s own politics. The rule’s OIRA review and comment period run on an administrative calendar indifferent to the Senate’s. If the merged CLARITY draft stalls on ethics while Regulation Crypto publishes for comment, the industry’s cost of legislative failure drops in real time, which weakens the coalition pressing moderate Democrats and strengthens the members arguing the bill can wait. Agency action meant as a bridge can function as an off-ramp. The three weeks in which both instruments reach their decisive stages, the merged bill text and the published rule, will reveal which metaphor the market believes.

What it means for issuers, and the European mirror

Before the issuer decision tree, the market implications deserve a paragraph of their own, because the rule reprices assets that already exist, not just launches that have not happened. Tokens whose largest discount is classification ambiguity, the mid-cap layer ones, the DeFi governance assets, the infrastructure tokens that trade below comparable revenue because American institutions cannot categorize them, gain a defined path to non-security status through the safe harbor even if the CLARITY Act never assigns them a commodity label. Exchange listing committees, which spent the enforcement era rationing US availability by litigation risk, get a compliance framework to point to. And the venture pipeline reopens domestically: funds that structured around offshore token warrants for a decade can underwrite American issuance with actual rules attached, which changes where the next cycle’s projects incorporate, hire, and pay taxes. None of this requires the rule to be generous. It requires the rule to exist, because the binding constraint was never severity. It was undefined risk, the one input no allocation committee can price.

For anyone actually launching a token, the practical decision tree changes shape the moment the rule publishes. A credible path now exists to raise seed capital domestically under the startup tier, scale through the 75 million dollar pathway with audit-grade disclosure, and target the safe harbor as the legal finish line where the token sheds its securities character by verifiable decentralization. The offshore foundation, the airdrop-to-avoid-sale contortions, and the deliberate exclusion of American buyers, the entire defensive architecture of the past eight years, become choices rather than necessities. The projects most affected are the serious middle: too big for a fair launch to fund, too small to carry registration costs, which describes most of the infrastructure layer the industry claims to want.

The comparison that will define the rule’s success is the one across the Atlantic. Europe’s MiCA regime just completed its transition, locking unlicensed firms out of a 30-country market and elevating the licensed few, a sorting crypto.news documented as the deadline hit. MiCA’s strength is comprehensiveness backed by statute; its weakness is rigidity, a stablecoin regime severe enough to expel the largest issuer on earth. Regulation Crypto inverts the trade: flexible, innovation-forward, and administratively fast, but resting on agency authority in a country where agencies change hands every four years. An American founder in 2026 chooses between a European rulebook that cannot easily be improved and an American one that cannot easily be trusted. The CLARITY Act is, among everything else, an attempt to give the American framework the one property it lacks, and the rule arriving with or without it is both the industry’s insurance policy and the bill’s quiet competitor.

The decode, compressed: Regulation Crypto is the most consequential piece of American crypto policy that almost nobody outside Washington is reading, precisely because it advances on the boring calendar of administrative law while the Senate supplies the drama. Four-year runways, 75 million dollar raises, and a legal exit from securities status are arriving through the Federal Register, on a timeline no filibuster can touch and no recess interrupts. The comment period will bend the parameters, the courts may test the boundaries, and a future commission could someday attempt the long unwind. What no plausible scenario now delivers is a return to the world where the only American rulebook was a lawsuit. The only question the Senate’s three weeks will answer is whether the new rulebook arrives as a chapter of a statute or as the whole book.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Why is SK Hynix stock sliding today?

Google Home Speaker (2026) review: Smarter and punchier, with a subscription pinch

Principles Of Football At VfL Bochum: Inside German Football’s Striker vs Midfielder Problem

-

News Videos7 days ago

News Videos7 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Fashion5 days ago

Fashion5 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Tech7 days ago

Tech7 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Sports4 days ago

Sports4 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports6 days ago

Sports6 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Tech6 days ago

Tech6 days agoAnthropic brings Claude Cowork to mobile and web as usage data shows most users aren’t coding

-

Sports4 days ago

Sports4 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Sports6 days ago

We have punished the disrespect

-

Tech5 days ago

Tech5 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Crypto World7 days ago

Crypto World7 days agoClaude AI Created Something Anthropic Never Designed

-

News Videos7 days ago

News Videos7 days ago“What’s going on?!” Carl Froch discusses Floyd Mayweather Jr financial issues

-

Crypto World6 days ago

Crypto World6 days agoNasdaq arthritis company holding Moshe Hogeg crypto hits all-time low

-

News Videos5 days ago

News Videos5 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

Tech6 days ago

Tech6 days agoKeychron is stepping outside keyboards with a $349 Thunderbolt 5 dock aimed at power users

-

Business6 days ago

Business6 days agoASX 200 Slides Over 0.6% as Rare Earths and Lithium Stocks Tumble Amid Global Semiconductor Sell-Off Today

-

Business6 days ago

Business6 days agoWill Trent shares rebound after Q1 update triggers 13% crash? Here’s what technical charts indicate

-

NewsBeat5 days ago

NewsBeat5 days agoMajor update after Huntingdon train attack as man enters plea

-

Tech6 days ago

Tech6 days agoOpenAI teams with Work Louder to launch Codex-native keyboard, weeks after CEO of Apps told staff ‘not to be distracted by side quests’

-

Business6 days ago

Business6 days agoSpaceX Shares Slide Nearly 6% Amid Post-IPO Volatility and Starship Test Focus

You must be logged in to post a comment Login