Crypto World

Why Altcoin Season Is Unlikely in Early 2026, Data Shows

Altcoin market capitalization (TOTAL2) remained below $1 trillion in February, while market sentiment fell to its most extreme level in years. Many investors expect altcoins to form a bottom soon after five consecutive months of decline.

The first quarter of 2026 may still offer opportunities. However, investors need objective signals to evaluate the broader picture.

Sponsored

Sponsored

Persistent Selling Pressure and Fragmented Liquidity Weigh on Altcoins

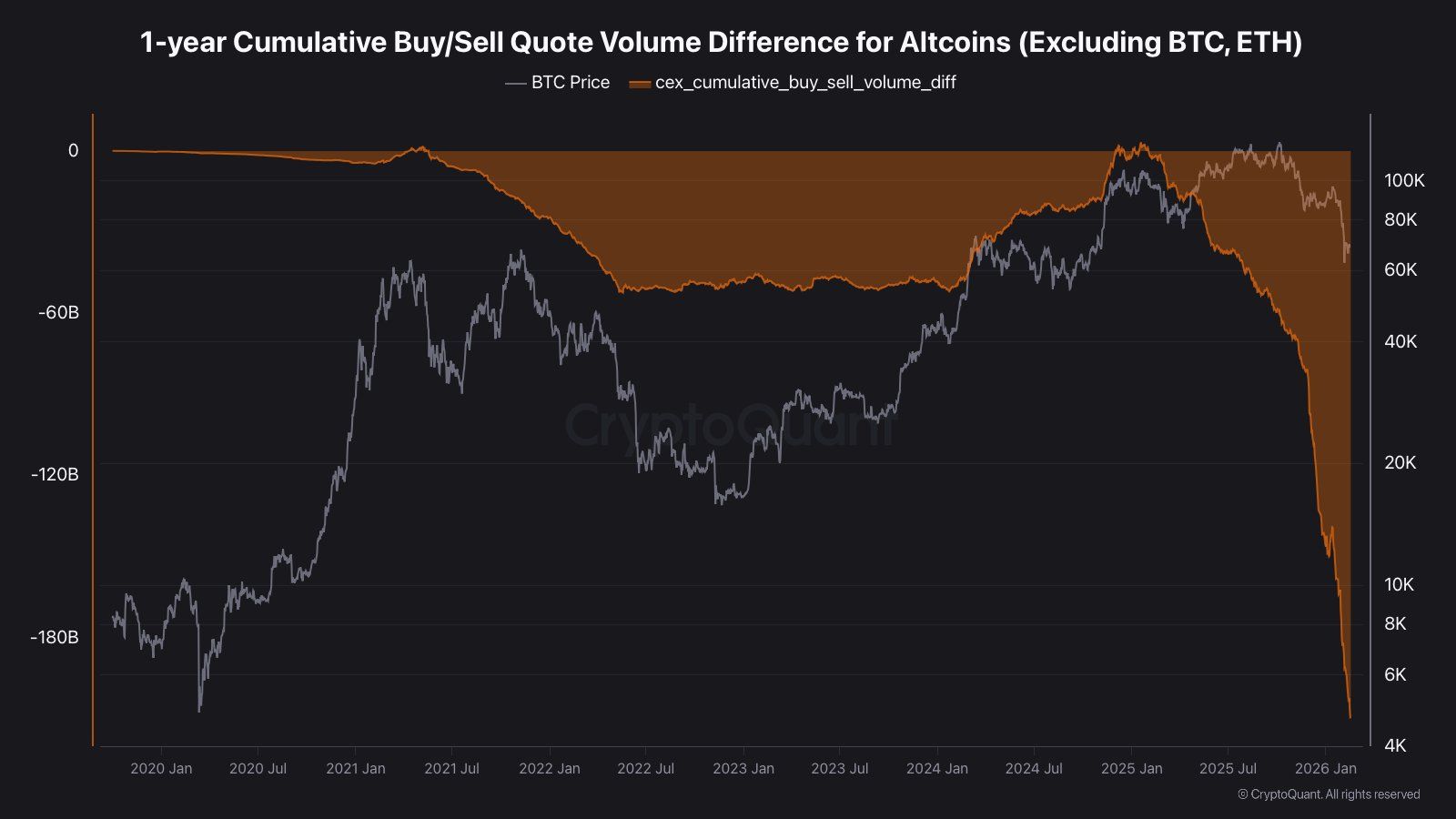

A report from CryptoQuant states that selling pressure on altcoins (excluding BTC and ETH) has reached its most extreme level in five years.

Cumulative buy/sell delta data has reached -$209 billion over the past 13 months. In January 2025, this delta was nearly zero, which reflected balanced supply and demand. Since then, it has continued to decline without any reversal.

This extreme condition differs completely from the 2022 bear market. During 2022–2023, selling pressure slowed, allowing the market to enter a sideways phase before recovering. That slowdown has not occurred in the current cycle.

“This is not a dip. It’s 13 months of continuous net selling on CEX spot. -209B doesn’t mean bottom. It means buyers are gone,” analyst IT Tech stated.

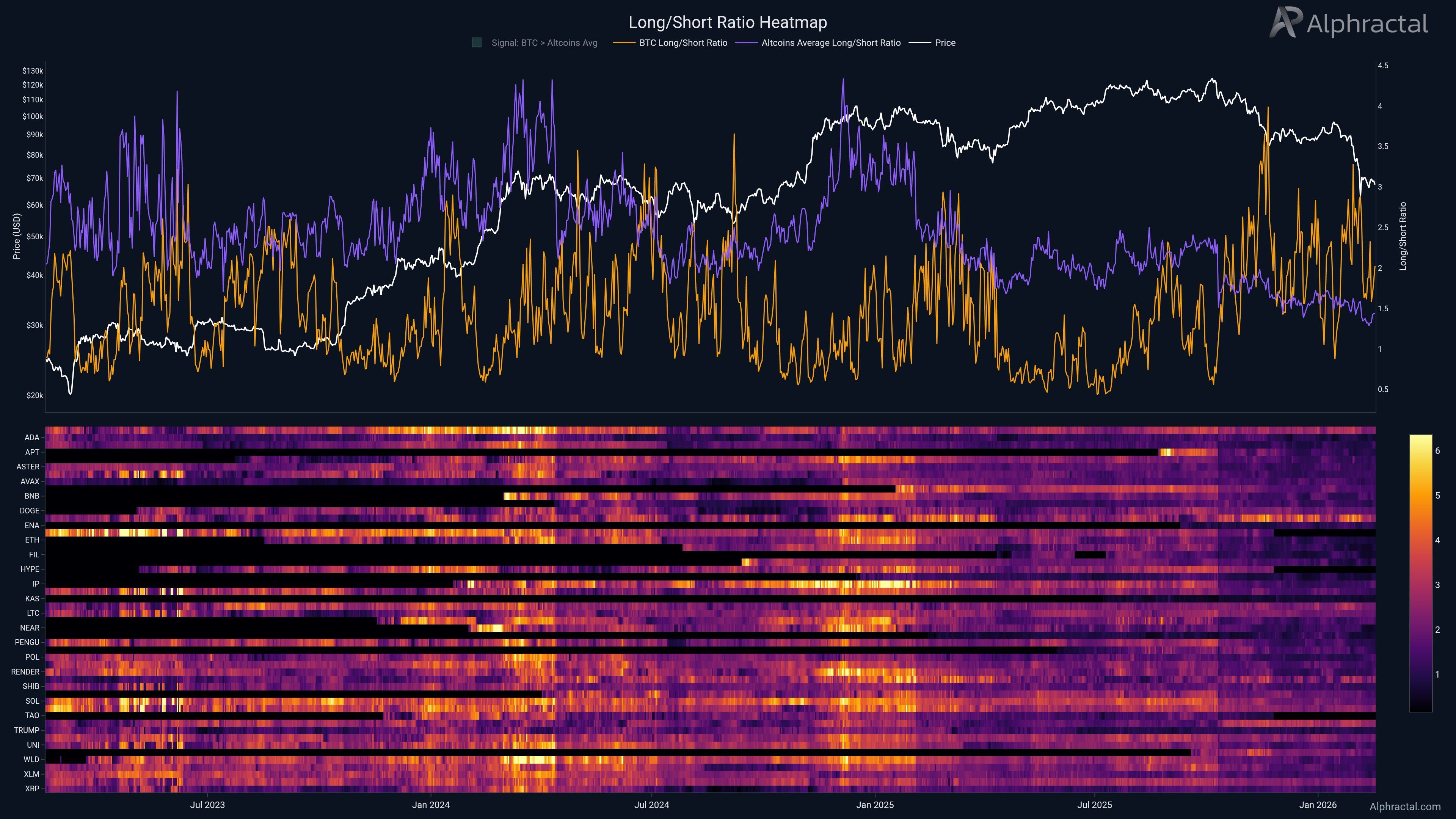

Additionally, derivatives data can provide additional short-term insights. Traders are currently holding significantly more long positions in Bitcoin than in altcoins, as reflected in Alphractal’s Long/Short Ratio data.

Sponsored

Sponsored

The chart shows that this is the first time in history that Bitcoin’s long ratio has remained above the altcoin average for four consecutive months. This indicates that short-term traders have reduced their exposure to altcoins and that expectations for altcoin volatility have weakened.

In addition, the total altcoin market capitalization has dropped back to levels five years ago, below $1 trillion. The altcoin analytics account OverDose pointed out that the biggest difference lies in the number of tokens. Five years ago, only about 430,000 coins were listed. Currently, that figure has surged to 31.8 million, an increase of roughly 70 times.

Too many tokens are competing for a market “pie” that has not grown larger. This dynamic makes recovery more fragile and threatens the survival of low-cap tokens.

Excluding the top 10, the remaining market capitalization stands at less than $200 billion. The technical structure shows a head-and-shoulders pattern, and this capitalization is moving toward its neckline support. Analyst Pentoshi commented that even if altcoins rebound, the gains will likely not be substantial.

“Even if alts bounce here, it likely won’t be substantial. I think eventually they make new lows… Imo it’s going to take some time to work through,” analyst Pentoshi predicted.

According to CoinGecko research, 53.2% of all cryptocurrencies listed on GeckoTerminal had failed by the end of 2025. In 2025 alone, 11.6 million tokens collapsed.

The current bear market may permanently reshape how investors allocate capital within the altcoin sector. Market participants may become more selective, prioritize liquidity and fundamentals, and reduce exposure to speculative low-cap assets.

The European Central Bank is edging closer to a full-fledged digital euro pilot, signaling a shift from exploratory talks to concrete testing. In remarks delivered after an executive committee meeting of the Italian Banking Association, ECB Executive Board member Piero Cipollone outlined a staged timetable that prioritizes the selection of payment service providers (PSPs) in early 2026 and a 12-month pilot during the second half of 2027. The plan envisions a small group of PSPs, merchants and Eurosystem staff participating in the initial phase, with broader involvement contingent on legislative and technical readiness. The remarks underscore the bank’s aim to validate a central bank digital currency in practical settings while preserving the integrity of European card schemes and keeping banks at the core of the payments ecosystem. held

Cipollone stressed that the digital euro would be designed to protect European card schemes and preserve banks’ central role in Europe’s payments system, a framing that aligns with Reuters’ coverage of the central bank’s approach. The pilot is intended to be modest in scope at the outset, focusing on a limited number of PSPs, merchants and Eurosystem staff to test onboarding, settlement and liquidity management in a real-world environment. This phased approach is positioned to give participating PSPs an early-readiness edge should a broader rollout follow, while generating practical data on infrastructure, compliance and staffing costs for planning purposes.

Key takeaways

- PSP selection for the digital euro pilot is scheduled to begin in the first quarter of 2026, setting the stage for a 12-month trial in the latter half of 2027.

- The pilot will involve a limited cohort of PSPs, merchants and Eurosystem staff, enabling hands-on testing of onboarding, settlement and liquidity management within a controlled environment.

- European authorities emphasize that the digital euro is intended to shield domestic payment ecosystems and card schemes, rather than displace them, with a focus on preserving the role of banks in payments.

- Governance and cost visibility are key aims of the pilot, offering participating players clearer insights into future infrastructure, compliance and staffing needs.

- Industry expectations are shaped by a longer-term roadmap that includes potential broader rollout and a 2029 launch target, contingent on legislative progress in 2026 and subsequent regulatory steps.

Market context: The push for a digital euro sits within a broader European effort to modernize payments, reduce dependence on international card networks, and ensure a stable, centrally governed digital currency option for residents and businesses. The central bank’s framing of the pilot as a way to protect domestic systems while engaging with private sector participants mirrors ongoing debates around stablecoins and private payment solutions that could otherwise erode the traditional banking role in payments.

Why it matters

The ECB’s move toward a structured pilot signals a careful balance between innovation and incumbency. By enabling a controlled test environment that includes EU-licensed PSPs and direct Eurosystem involvement, the central bank aims to gather actionable data on how a digital euro could function in real commerce. This includes practical issues around onboarding new users, ensuring seamless settlement between participants, and managing liquidity—areas that have historically proven complex for central bank digital currency platforms to operationalize at scale.

From a banking perspective, the digital euro is envisioned not as a threat to banks, but as a mechanism to preserve their centrality in a payments landscape that increasingly incorporates digital solutions. Cipollone highlighted that the project would aim to protect domestic payment rails and card schemes while offering a more cost-efficient option for merchants. The stated goal is to place a cap on merchant fees for the digital euro network that would be lower than the charges typical of international card networks, yet higher than those charged by domestic schemes. This pricing dynamic is designed to keep EU-based payment ecosystems competitive while ensuring that the digital euro remains attractive to merchants and consumers alike.

European policymakers are also mindful of broader industry shifts. The plan explicitly notes the European Bancomat and Bizum-type networks as areas where the digital euro could help preserve domestic alternatives against private, cross-border payment rails. In this context, the pilot is less about displacing existing networks and more about integrating a central bank digital currency in a way that complements, rather than competes with, established infrastructures. This approach aligns with the broader aim of safeguarding financial stability and ensuring that Europe maintains strategic control over its payments architecture as new digital forms of money emerge.

What to watch next

- First-quarter 2026: Official PSP selection process begins, narrowing the field for the pilot.

- Second half of 2027: Primary 12-month digital euro pilot period commences with participating PSPs and merchants.

- 2026–2027: Legislation and regulatory steps to enable or adjust digital euro deployment, shaping the timeline for broader rollout.

- 2029: Potential full-scale launch if legislative and technical milestones are met and stakeholders achieve sufficient readiness.

- Ongoing infrastructure planning: ECB and Eurosystem continue to map future ecosystem costs, staffing needs and compliance requirements tied to the digital euro’s operation.

Sources & verification

- ECB press release and accompanying document outlining the PSP selection and pilot plans (Sp260218) and related materials.

- Reuters coverage detailing Cipollone’s remarks and the digital euro design goals to protect European banks’ card schemes.

- Cointelegraph reporting on the digital euro trajectory, including references to the 2029 launch plan and next-phase progression.

- Historical reporting on the ECB’s progression toward a digital euro, including discussions around legislation timelines in 2026.

ECB advances digital euro pilot as PSP selection begins in 2026

The European Central Bank is advancing toward a tangible digital euro pilot, signaling a transition from theoretical exploration to real-world testing. The plan, presented in the wake of a meeting with the Italian Banking Association’s executive committee, centers on naming payment service providers (PSPs) in early 2026 and launching a 12-month trial in the second half of 2027. The pilot’s initial footprint will be deliberately modest: a limited cadre of PSPs, a handful of merchants and Eurosystem staff will participate to validate core operational flows, including onboarding, settlement and liquidity management. This approach aims to deliver measurable insights while preserving the primacy of existing European card schemes and banks within the payments system.

In explaining the design philosophy, Cipollone stressed that the digital euro should bolster domestic payment networks rather than replace them. By anchoring the rollout in EU-licensed PSPs, the ECB seeks to ensure merchant access, interoperable settlements and a governance structure that keeps banks at the center of the payments ecosystem. The broader objective is to strike a balance between innovation and stability—allowing the digital euro to co-exist with established rails while mitigating the risk of private, non-government-controlled systems displacing traditional players.

A key element of the planned approach is the potential to test and refine future infrastructure, compliance and staffing costs. The pilot’s visibility into these cost dimensions could inform investment decisions for PSPs and banks, helping them plan capital deployment with greater certainty. Direct Eurosystem involvement is intended to yield practical feedback from participants, shaping both product design and governance arrangements as the project evolves.

Beyond the technical and financial considerations, the ECB’s digital euro initiative is framed as a strategic safeguard for Europe’s payments sovereignty. The project explicitly envisions protecting local networks, such as Italy’s Bancomat and Spain’s Bizum, from losing ground to private, cross-border platforms. In Cipollone’s view, the digital euro should offer an affordable alternative for merchants—pricing that is lower than the typical charges on international networks but higher than the minimums charged by domestic schemes. This pricing nuance reflects a deliberate effort to maintain domestic competitive advantages while embracing the efficiencies associated with central bank money in digital form.

As policymakers weigh the next steps, observers will be watching how the proposed timeline aligns with legislative developments in 2026 and how the pilot’s findings influence the path toward a broader rollout. The ECB’s timeline currently contemplates a 2029 launch under favorable regulatory and technical conditions, with a potential early start to the pilot if legislation is enacted in 2026. This braided timetable underscores the delicate balance the central bank must strike between experimentation, market readiness and fiscal prudence in a rapidly evolving digital payments landscape.

TLDR

- Canary Capital launched the Canary Stake SUI ETF on Nasdaq, offering exposure to the SUI token and staking rewards.

- Grayscale converted its SUI trust into an ETF, providing investors with direct access to the SUI token through NYSE Arca.

- The new SUI ETFs allow both institutional and retail investors to participate in the growing SUI blockchain ecosystem.

- SUI is a Layer 1 blockchain developed by Mysten Labs, with its token used for transaction fees and smart contract execution.

- The SUI ETFs enable investors to earn rewards through SUI’s proof-of-stake mechanism while tracking the spot price of the token.

Two new exchange-traded funds (ETFs) linked to SUI token launched on Wednesday, offering investors direct exposure to SUI’s price. Canary Capital debuted the Canary Stake SUI ETF on Nasdaq, while Grayscale converted its SUI trust into an ETF on NYSE Arca. Both funds will track SUI’s price, with the added benefit of enabling investors to earn staking rewards.

Canary Capital’s SUI ETF: Canary Stake SUI ETF (SUIS)

Canary Capital launched its Canary Stake SUI ETF, trading under the ticker symbol SUIS on Nasdaq. This new fund tracks the spot price of SUI and allows investors to benefit from staking rewards. SUI operates on a proof-of-stake mechanism, which the ETF integrates into its structure, allowing investors to earn net staking rewards.

Steven McClurg, CEO of Canary Capital, emphasized the importance of this fund, saying, “The Canary Staked SUI spot ETF (SUIS) brings exposure to SUI in a registered, exchange-traded structure, while also enabling investors to benefit from net staking rewards generated through SUI’s proof-of-stake mechanism.” The ETF provides a regulated way for investors to engage with the SUI ecosystem and benefit from staking.

Grayscale Launches SUI Fund as an ETF

Grayscale followed suit, launching its own SUI fund on the same day. The company converted its SUI trust into an ETF, trading under the ticker GSUI on NYSE Arca. This ETF will provide investors with exposure to the SUI token, offering another way to participate in the growing blockchain ecosystem.

Grayscale’s decision to turn its SUI trust into an ETF aims to provide easier access for institutional and retail investors. By offering direct exposure to the SUI token, the fund offers an alternative to buying the token directly on cryptocurrency exchanges.

SUI’s Growing Ecosystem

SUI, developed by Mysten Labs, is a Layer 1 blockchain used to power decentralized applications and smart contracts. The SUI token plays a vital role in the blockchain, serving as a means to pay for transaction fees and support various other network functions. SUI is currently ranked 31st by market capitalization, valued at approximately $3.7 billion.

The launch of these SUI ETFs marks an important milestone for the blockchain’s adoption. It allows a broader range of investors to gain exposure to the SUI ecosystem in a regulated, traditional investment format. The ETFs make it easier for individuals to invest in the blockchain’s native token while also earning rewards through its proof-of-stake mechanism.

The European Union, often criticized for prioritizing rulemaking over innovation, is pointing to the European Blockchain Sandbox as an example of how regulation can boost innovation.

After three cohorts of confidential dialogues, the initiative has produced a 230-page best practices report and drawn in nearly 125 regulators and authorities.

The European Commission tapped law firm Bird & Bird and its consortium partners to lead the initiative, which matches blockchain use cases with regulators for confidential dialogues aimed at clearing legal challenges.

Marjolein Geus, a partner at Bird & Bird, told Cointelegraph that the process has shown compliance need not be a deterrent.

“For use case owners, it helps them better understand the relevant regulations and how those rules apply to their projects,” she said. “It allows regulators and authorities to deepen their understanding of how those technologies interact with the regulatory frameworks within their areas of competence.”

In the latest cohort, “mature” use cases were increasingly operational and embedded in sectors such as energy, healthcare and artificial intelligence, bringing along more complex compliance discussions.

How MiCA became a test of regulatory timing for blockchain

When the Markets in Crypto-Assets Regulation (MiCA) was adopted, observers warned that strict obligations would raise barriers for startups. Stablecoin rules drew particular scrutiny as Tether — issuer of the world’s largest stablecoin — ultimately decided against seeking MiCA authorization for USDt (USDT).

The brain drain narrative predates crypto. European founders have often incorporated in jurisdictions perceived as having a lighter touch.

Similar fears surfaced when the General Data Protection Regulation (GDPR) took effect in 2018. Businesses complained of interpretive confusion and administrative burden. Some foreign firms scaled back EU exposure. However, the GDPR has since become a global reference point, with many multinationals aligning operations to its standards.

The criticism that Europe “regulates first and innovates later” rests on the idea that legal certainty follows market development. MiCA was adopted before the crypto sector reached institutional maturity. In theory, that sequencing risks locking rapidly developing tech into rigid categories too early.

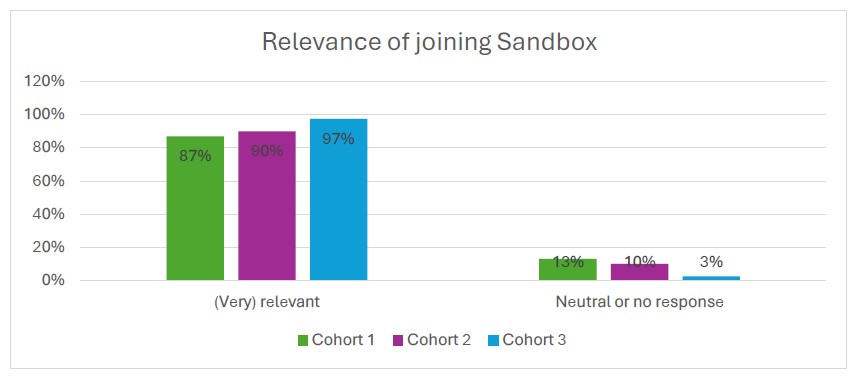

But the sandbox advanced a counterpoint, suggesting that early legislation combined with regulatory dialogue can enhance clarity and accelerate compliance. In the third cohort, 77% of respondents described the sandbox as having a crucial or valuable impact on innovation and regulation, and none reported no impact.

While the EU opted for early codification and dialogue, the world’s largest economy, the US, lacks a comprehensive federal framework for digital assets despite presidential pledges to become a global hub. Its proposed Digital Asset Market Clarity Act has stalled after key industry figures withdrew support over provisions, including restrictions on stablecoin yield.

Related: When will crypto’s CLARITY Act framework pass in the US Senate?

Smart contracts and the limits of decentralization

While the best practices report spans over 20 chapters across multiple regulatory domains, its sections on smart contracts and decentralization focus on how blockchain systems are structured at the code and governance level.

“Virtually all blockchain DLT use cases use smart contracts. They are subject to regulation, with security requirements often relevant, as well as obligations under the GDPR,” Geus said.

The dialogues examined how those contracts interact with existing EU frameworks, not just MiCA. Depending on their function and the degree of control retained by identifiable actors, smart contracts may trigger obligations ranging from cybersecurity source code reviews to operational resilience testing and conformity declarations.

“The question then becomes how to ensure those smart contracts are secure and GDPR compliant and how to test whether they meet the applicable regulatory frameworks. That is an area where further clarification, harmonization and standardization are needed,” Geus said.

Another focal point of the third cohort report is the qualification of services provided “in a fully decentralized manner without any intermediary” under MiCA.

MiCA references the term “fully decentralized” but doesn’t define it.

Like smart contracts, determining full decentralization in Europe requires further clarification. The report did attempt to lay out a checklist within the limits of how MiCA and the Markets in Financial Instruments Directive are structured.

Among those are identifiable fee recipients or entities capable of modifying the protocol, which may suggest the existence of an intermediary. Where such influence exists, MiCA is likely to apply, and authorization as a crypto service provider may be required.

Related: Crypto’s decentralization promise breaks at interoperability

Crypto in Europe’s legal architecture

The European Blockchain Regulatory Sandbox’s participation neither implies legal endorsement or regulatory approval nor does it grant derogations from applicable law.

By the third cohort, dialogues increasingly engaged horizontal legislation such as the GDPR and the Data Act. Projects were assessed not as isolated crypto experiments, but as embedded digital systems interacting with financial, cybersecurity and data governance frameworks.

Johannes Wirtz, partner at Bird & Bird’s finance regulation group, observed that regulators involved in the dialogues demonstrated deeper familiarity with crypto than expected.

“This was actually something which surprised me in certain regards because you always had this assumption that they are more or less bound to the old world, but they have their innovation departments, which are really good at identifying the issues,” Wirtz said.

If the early criticism of European policy assumed that law would constrain experimentation, Bird & Bird representatives claimed that structured dialogue clarifies how that perimeter applies in practice.

Magazine: Is China hoarding gold so yuan becomes global reserve instead of USD?

Cointelegraph Features and Cointelegraph Magazine publish long-form journalism, analysis and narrative reporting produced by Cointelegraph’s in-house editorial team and selected external contributors with subject-matter expertise. All articles are edited and reviewed by Cointelegraph editors in line with our editorial standards. Contributions from external writers are commissioned for their experience, research or perspective and do not reflect the views of Cointelegraph as a company unless explicitly stated. Content published in Features and Magazine does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate. Cointelegraph maintains full editorial independence. The selection, commissioning and publication of Features and Magazine content are not influenced by advertisers, partners or commercial relationships.

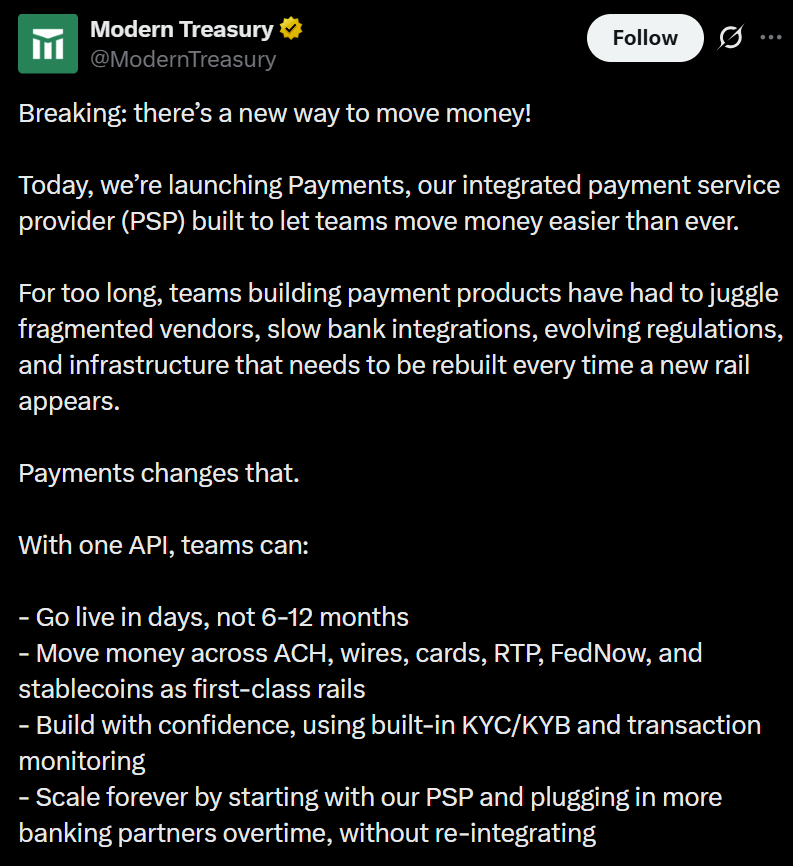

Modern Treasury, a payments operations software provider that helps companies manage and reconcile money movement, has introduced an integrated payment service provider (PSP) that supports both traditional fiat rails and stablecoins.

On Wednesday, the company announced that it has added stablecoin settlement to the same infrastructure that businesses already use for ACH transfers, wire payments and real-time payment networks. At launch, the platform supports Global Dollar (USDG), Pax Dollar (USDP) and USDC (USDC), with USDt (USDT) expected to be added in the future.

Modern Treasure acquired stablecoin and fiat payment platform Beam in October.

The company has partnered with Paxos to integrate regulated stablecoins and settlement capabilities into its platform and has joined the Global Dollar Network. San Francisco-based Modern Treasury also participates in Circle’s Alliance Program, a partner network that supports the broader use of the USDC stablecoin in payments and financial services.

With the move, stablecoins are incorporated into a single compliance framework alongside traditional banking rails. Companies using Modern Treasury no longer need separate vendors or technical integrations to process crypto-based and fiat payments.

The update effectively makes stablecoins another settlement option within a conventional payment flow, potentially lowering the operational barrier for businesses seeking to integrate blockchain-based payment rails.

Related: Crypto’s 2026 investment playbook: Bitcoin, stablecoin infrastructure, tokenized assets

Stablecoins move deeper into mainstream financial infrastructure

Modern Treasury’s latest integration comes as stablecoins see broader uptake across the payments industry, particularly following the passage of the US GENIUS Act last July, which established a federal framework for dollar-backed stablecoins.

The total value of stablecoins in circulation grew by nearly 50% last year, surpassing $300 billion for the first time. Growth has slowed in recent months, with supply hovering around that level amid tighter liquidity conditions and a cooling crypto market.

Still, issuance remains near record highs, reflecting sustained demand for dollar-pegged digital assets in trading, cross-border transfers and settlement.

America’s largest banks have also signaled interest in stablecoins and related technology. JPMorgan Chase, Bank of America, Citigroup and Wells Fargo have been reported to be in early discussions about a jointly operated stablecoin initiative, though the plans are still at a conceptual stage.

Last month, Fidelity Investments announced plans to issue a new stablecoin called the Fidelity Digital Dollar. Fidelity Digital Assets president Mike O’Reilly described stablecoins as “foundational payment and settlement services.”

Related: How TradFi banks are advancing new stablecoin models

Once holding over 100,000 ETH, ETHZilla liquidated some to cover debt and repurchase stock.

Peter Thiel and his Founders Fund have sold $74.5 million worth of ether (ETH) through ETHZilla Corp., fully exiting the company’s crypto treasury. The SEC filing confirmed Thiel’s entities no longer hold any shares in ETHZilla.

The sale follows a series of ether liquidations by ETHZilla to cover debt and buy back stock. The company previously held over 100,000 ETH at its peak, according to DefiLlama.

ETHZilla Faces Market Pressure

ETHZilla started as a biotech firm, 180 Life Sciences Corp., before making a full pivot to cryptocurrency management in August. The Palm Beach-based company rebranded and shifted its operations entirely to focus on holding ETH, signaling a major change from its original biotech focus.

The timing of this shift coincided with a broader crypto market downturn, which immediately affected the company’s treasury. Ether has fallen nearly 60% from last year’s peak, trading around $2,000 at press time. The decline put pressure on ETHZilla’s newly acquired crypto holdings, making careful financial management a priority.

To stabilize its finances, ETHZilla sold ether in October and December. In late October, it liquidated roughly $40 million to repurchase shares. Two months later, it sold $74.5 million to repay senior secured convertible notes, according to filings.

A Shift to Real-World Assets

ETHZilla has launched a subsidiary, ETHZilla Aerospace, to offer tokenized equity in leased jet engines. The move signals a shift toward real-world, asset-backed offerings beyond its cryptocurrency holdings.

Meanwhile, the company has not publicly commented on Thiel’s exit or its recent ETH sales. However, observers say these actions reflect the financial pressures facing crypto-focused public firms.

You may also like:

Notably, the development underscores the caution high-profile investors are showing amid volatile markets. It also highlights the challenges of maintaining a public ether treasury during rapid price swings.

Looking ahead, market watchers will follow ETHZilla’s aerospace venture and broader strategy for clues about its next steps. The pivot may indicate a new approach for digital asset companies seeking revenue outside of pure crypto holdings. It also shows how quickly corporate strategies can evolve in the crypto space.

SECRET PARTNERSHIP BONUS for CryptoPotato readers: Use this link to register and unlock $1,500 in exclusive BingX Exchange rewards (limited time offer).

Bitcoin may need drastic fix against quantum threats as CryptoQuant founder urges freezing inactive wallets holding billions in BTC.

Ki Young Ju, founder of CryptoQuant, has proposed that a future Bitcoin (BTC) quantum upgrade may require freezing old addresses to protect against potential theft by quantum computers.

He also believes that addressing the risk would be challenging because the crypto community has historically struggled to agree on protocol changes.

Solution to Quantum Risk

In a social media post, Ju explained that anyone holding BTC in old address types faces the same risk. This is because the digital assets could either be frozen by design or stolen if quantum machines evolve enough to break BTC’s cryptography. He added that even securely stored private keys could become useless if owners fail to adopt protocol upgrades in time.

“In simple terms, coins that appear perfectly safe today could become spendable by an attacker tomorrow,” warned Ju.

In response to the threat, the CryptoQuant founder has suggested freezing old addresses, including the one containing Satoshi’s 1 million BTC, to prevent them from being stolen or compromised.

“Would you support freezing dormant coins, including Satoshi’s, to save BTC from quantum attacks?” he asked.

Bitcoin’s security relies on cryptography that is effectively unbreakable by classical computers. However, quantum computers change this assumption. Under certain conditions, a sufficiently powerful machine of this kind could get a private key from an exposed public key.

Once a public key is revealed on-chain, the risk is permanent. Ju estimates that roughly 6.89 million BTC are currently exposed to such attacks. Data shows that about 3.4 million BTC have been dormant for over a decade, including Satoshi’s stash, representing hundreds of billions of dollars in potential value. He explained that with so much value at risk, hackers could be very motivated if the technology becomes cheaper and easier to use.

Social Consensus Challenges

Even if freezing dormant BTC is technically possible, achieving community agreement is still a major challenge. This is because such solutions move quickly, while social consensus happens slowly.

You may also like:

The Bitcoin ecosystem has historically struggled with agreeing on protocol changes. This can be seen in the block size debate, which lasted more than three years and led to hard forks. Another example is the failed SegWit2x upgrade, demonstrating how difficult coming to an agreement can be.

Freezing coins, even to prevent quantum attacks, would likely face similar resistance because it conflicts with the OG cryptocurrency’s core philosophy of decentralization and user control.

Ju cautioned that the lack of full agreement could potentially lead to rival BTC forks as quantum technology progresses. According to him, the real question is not whether the threat will arrive in five or ten years, but whether the crypto community will be united on how to handle it before then.

Elsewhere, Bankless co-founder David Hoffman believes that in the event of a quantum attack, ETH would continue functioning normally even if BTC were to fail because it has been long prepared for these challenges.

SECRET PARTNERSHIP BONUS for CryptoPotato readers: Use this link to register and unlock $1,500 in exclusive BingX Exchange rewards (limited time offer).

PIPPIN has entered a volatile phase after failing to sustain its recent breakout. The altcoin rallied sharply but has since retraced, placing many recent buyers at a loss.

Price action now threatens to invalidate a projected 221% breakout from a broadening descending wedge pattern.

Sponsored

Sponsored

PIPPIN Holders Run To Buy

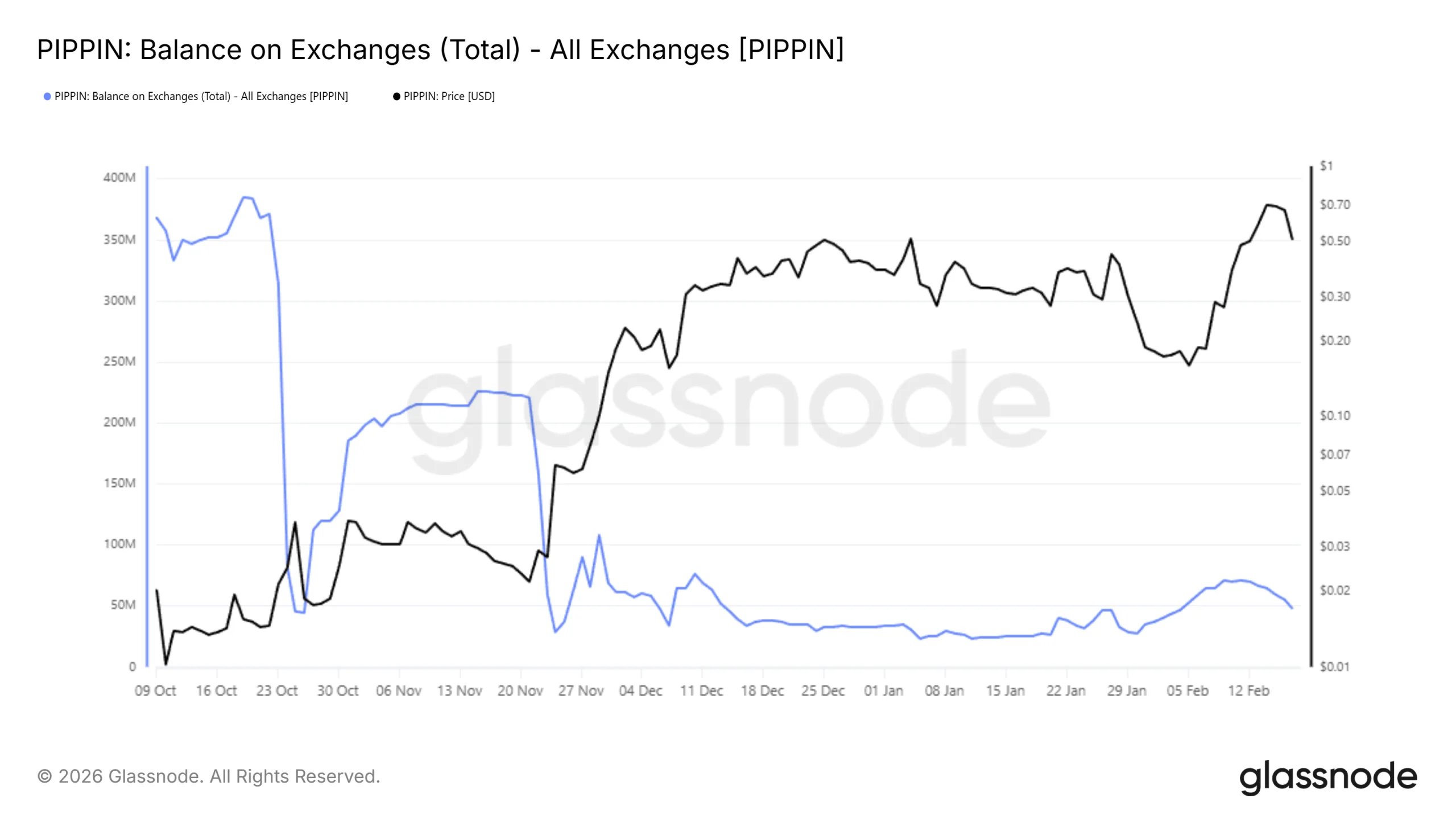

Exchange balance data reveals notable accumulation following the recent all-time high. Since the peak three days ago, investors have purchased approximately 16.6 million PIPPIN. At current valuations, this represents roughly $7.7 million in buying activity.

This accumulation pattern is not new. Historical data shows that PIPPIN holders often buy aggressively near peaks. As prices decline, panic selling frequently follows. Similar behavior appeared during the late January surge and again during the October 2025 spike.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

These cycles tend to delay sustained recovery. Early buyers accumulate at elevated levels, then exit during pullbacks. If the price weakens further, selling pressure may intensify again. This pattern raises the probability of renewed volatility in the near term.

Momentum indicators signal caution. The Money Flow Index currently sits above 80.0, placing PIPPIN in overbought territory. Elevated readings often precede cooling phases as capital inflows slow.

Broader market indecision compounds the risk. Without strong directional cues from major cryptocurrencies, speculative altcoins often struggle to sustain rallies. Unless holders begin aggressive distribution, however, a full reversal may remain delayed rather than immediate.

Sponsored

Sponsored

Will LTHs Prove To Be Pippin’s Saviour?

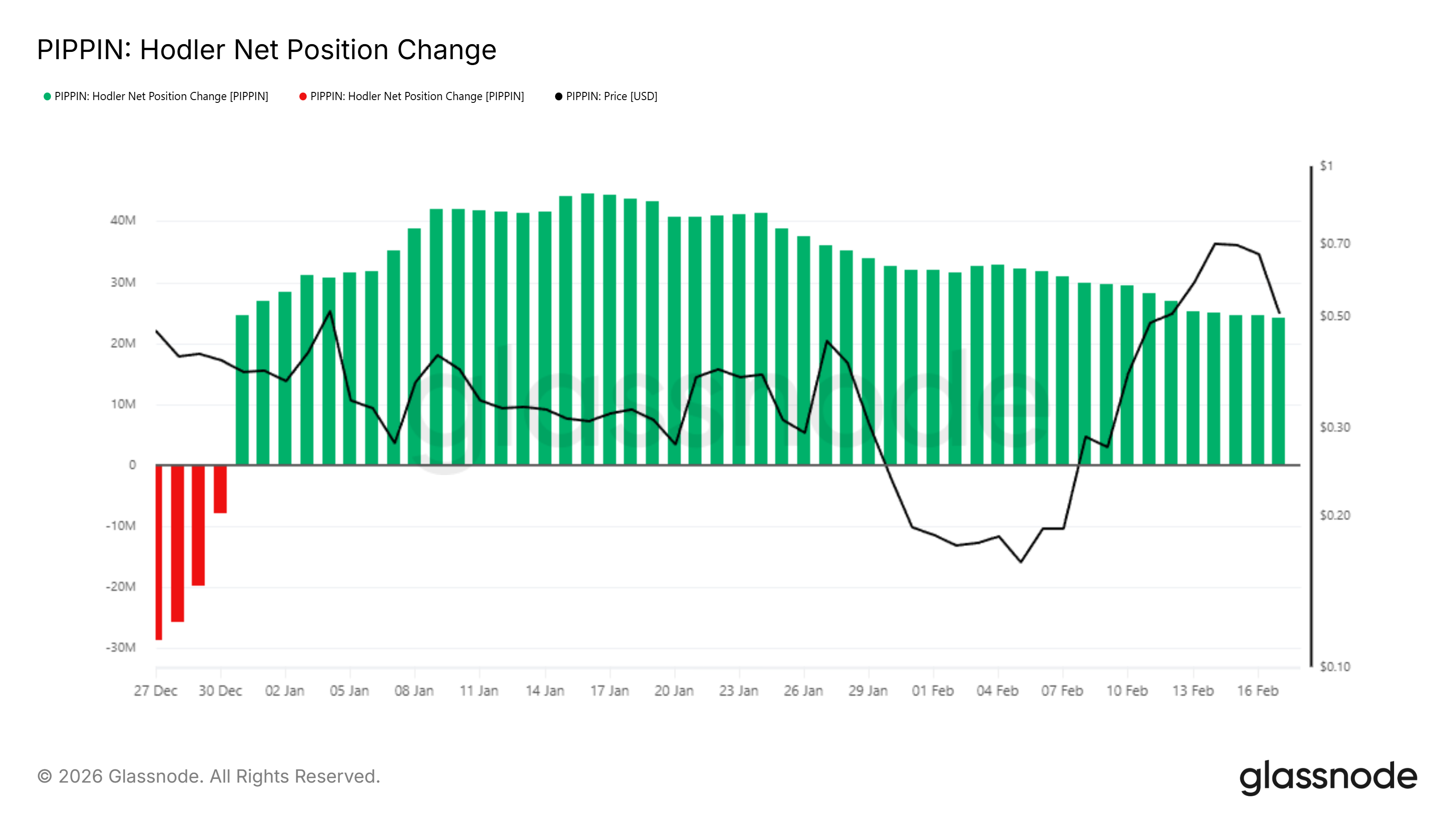

The HODLer Net Position Change metric provides a mixed outlook. Long-term holders continue to accumulate, as indicated by persistent green bars. Although the slope has weakened, net buying remains intact.

This ongoing support is critical. If long-term PIPPIN holders shift to distribution, downside risk would escalate quickly. A transition from accumulation to selling could accelerate losses and confirm bearish control over the trend.

PIPPIN Price Faces a Crash

PIPPIN previously broke out of a broadening descending wedge pattern. That formation projected a potential 221% upside move. However, current price action suggests the breakout is at risk of invalidation if support levels fail.

If long-term holder support stabilizes the token, PIPPIN could rebound from the $0.449 support zone. A sustained bounce may drive the price toward $0.600. Strong follow-through could retest the $0.772 all-time high, recovering recent losses.

Conversely, downside risk remains substantial. Many investors who bought at the all-time high are currently facing losses of about 40%. If panic selling resumes, PIPPIN could break below $0.449. A drop toward $0.372 would invalidate the bullish pattern and confirm the breakdown scenario.

Bitwise Asset Management wants to offer a prediction markets for the next U.S. presidential election through exchange-traded funds (ETFs).

Under “Prediction Shares” branding, the San Francisco-based crypto asset manager filed to list two ETFs tracking prediction markets betting on the outcome of the 2028 election — one for a Democratic winner, one for Republican — with the Securities and Exchange Commission (SEC) on Tuesday.

Bitwise also listed four equivalent products for 2026 mid-terms, predicting Democratic and Republican wins in the House of Representatives and the Senate.

Each ETFs will invest their assets in prediction markets bets supporting the applicable outcome denoted by that fund.

The same way that a bitcoin ETF allows investors to invest in BTC without purchasing the underlying cryptocurrency, these ETFs will allow users to bet on the outcome of U.S. elections without using a prediction platform like Polymarket.

Prediction markets came to prominence during the last U.S. election and now process trading volumes of around $10 billion monthly.

With ETFs also having opened the door to crypto investment for a wider array of prospective investors including institutions, Bitwise appears to trying to replicate this model for prediction markets, with the 2026 mid-terms as its testbed.

Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Leo Mindyuk on how executable liquidity at scale is more fragmented and fragile than most institutions assume

- Top headlines institutions should pay attention to by Francisco Rodrigues

- Helium’s deflationary flip in Chart of the Week

Expert Insights

Crypto’s liquidity mirage: why headline volume doesn’t equal tradable depth

– By Leo Mindyuk, co-founder and CEO, ML Tech

Crypto looks liquid, until you try to trade large volumes. Especially during periods of market stress and even more so if you want to execute on coins outside of the top 10-20.

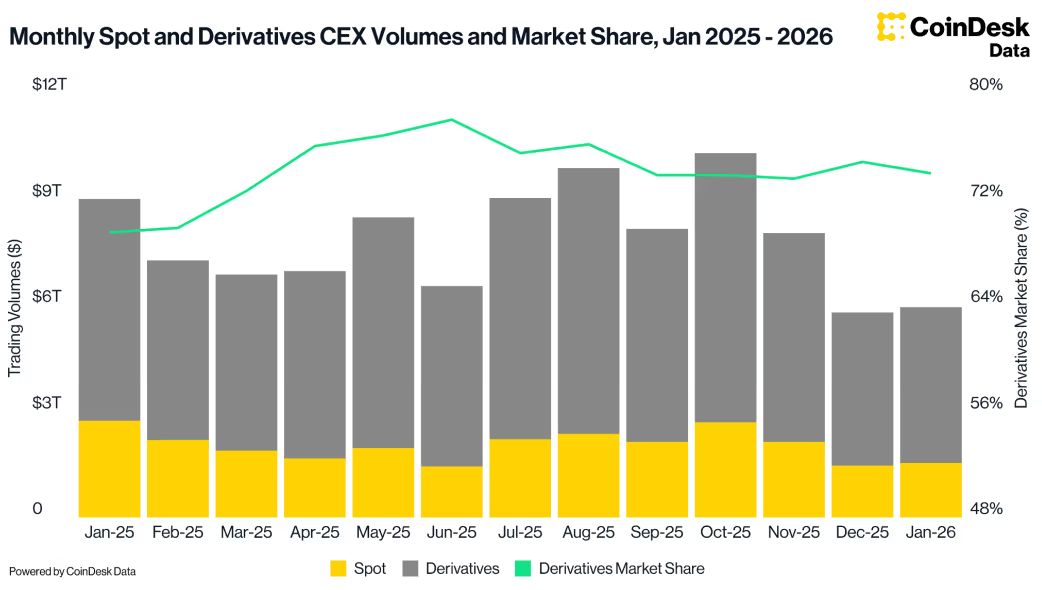

On paper, the numbers are impressive. Billions traded in daily volume and trillions traded in monthly volume. Tight spreads on bitcoin and ether (ETH). Dozens of exchanges competing for flow. It resembles a mature, highly efficient market. The beginning of the year saw around $9 trillion of monthly spot and derivatives volumes, then October 2025 saw around $10 trillion in monthly volume (including a lot of activity around the October 10th market bloodbath). Then in November, derivatives trading volumes decreased 26% to $5.61 trillion, recording the lowest monthly activity since June, followed by even larger declines in December and January, according to CoinDesk Data. Those are still some very impressive numbers, but let’s zoom in further.

At first glance there are a lot of crypto exchanges competing for flow, but in reality just a small group of exchanges dominate (see the graph below). If those have liquidity thinning out or connectivity issues preventing the execution of volume, the whole crypto market is impacted.

It’s not just that the volumes are concentrated on a few exchanges, they are also highly concentrated in BTC, ETH and a couple of other top coins.

The liquidity seems quite solid with a number of institutional market makers active in the space. However, the visible liquidity is not the same as executable liquidity. According to Amberdata (see the graph below), markets that showed $103.64 million in visible liquidity suddenly had just $0.17 million available, a 98%+ collapse. The bid-ask imbalance flipped from +0.0566 (bid-heavy, buyers waiting) to -0.2196 (ask-heavy, sellers overwhelming the market at a 78:22 ratio).

For institutions deploying meaningful capital, the distinction becomes obvious very quickly. The top of the book might show tight spreads and reasonable depth. Go a few levels down, and liquidity thins out fast. Market impact doesn’t increase gradually, it accelerates. What looks like a manageable order can move price far more than expected once it interacts with real depth.

The structural reason is simple. Crypto liquidity is fragmented. There is no single consolidated market. Depth is distributed across venues, each with different participants, latency profiles, API systems (that can break or have disruptions) and risk models (that can come under stress). Reported volume aggregates activity, but it does not aggregate liquidity in a way that makes it easily accessible for large execution. This is specifically apparent for smaller coins.

That fragmentation creates a false sense of comfort. In calm markets, spreads compress and books look stable. During volatility, liquidity providers reprice or pull entirely. They get unfavorable inventory and are unable to de-risk and pull out their quotes. Depth disappears faster than most models assume. The difference between quoted liquidity and durable liquidity becomes clear when conditions change.

What matters is not how the book looks at 10:00 a.m. on a quiet day. What matters is how it behaves during stress. Experienced quants know that but most of the market participants do not, as they struggle to close open positions gradually and then get liquidated during the stress events. We saw this in October, and a couple of times since.

In execution analysis, slippage does not scale linearly with order size; it compounds. Once an order crosses a certain depth threshold, impact increases disproportionately. In volatile conditions, that threshold shrinks. Suddenly, even modest trades can move prices more than historical norms would suggest.

For institutional allocators, this is not a technical nuance. It is a risk management issue. Liquidity risk is not only about entering a position, it is about exiting when liquidity is scarce and correlations rise. Want to execute a couple of millions of some smaller coins? Good luck! Want to exit losing positions in less liquid coins when the market is busy like during the October crash? It can become catastrophic!

As digital asset markets continue to mature, the conversation needs to move beyond headline volume metrics and top level liquidity snapshots during the calm markets. The real measure of market quality is resilience and how consistently liquidity holds up under pressure.

In crypto, liquidity isn’t defined by what’s visible during normal stable conditions. It’s defined by what’s left when the market gets tested. That’s when capacity assumptions break and risk management takes center stage.

Headlines of the Week

Wall Street giants have kept moving deeper into the cryptocurrency space over the past week, while new data has shed light on just how large the space is in Russia and how big it could become in Asia. Major market participants Binance and Strategy have meanwhile doubled down on their massive BTC reserves.

- Wall Street giants enter DeFi market with token investments: BlackRock has made its tokenized U.S. Treasury fund BUIDL tradable on decentralized exchange Uniswap, as part of a deal that saw it invest an undisclosed amount in UNI. Similarly, Apollo Global Management (APO) struck a cooperation agreement with Morpho.

- Russia’s daily crypto turnover exceeds $650 million, the Ministry of Finance says: The country’s government and central bank are pushing for legislation to regulate cryptocurrency activities, while the Moscow Exchange is looking to deepen its presence in the market.

- Binance converts its $1 billion safety net into 15,000 BTC: Leading cryptocurrency exchange Binance has finished converting the Secure Asset Fund for Users (SAFU) into bitcoin, turning about $1 billion into 15,000 BTC.

- BlackRock exec says 1% crypto allocation in Asia could unlock $2 trillion in new flows: BlackRock’s head of APAC iShares, Nicholas Peach, has said that even a modest portfolio allocation to crypto in Asia could unlock $2 trillion in new flows.

- Strategy says it can survive even if bitcoin drops to $8,000 and will ‘equitize’ debt: Strategy, the largest bitcoin treasury firm with 714,644 bitcoin on its balance sheet, said it can withstand a bitcoin price drop to $8,000 and still cover its roughly $6 billion in debt.

Chart of the Week

Helium’s deflationary flip

Helium has surged 37.5% month-to-date, decoupling from the broader market as its fundamentals shift toward a deflationary model. Since the start of 2026, the protocol’s net emissions have turned negative, effectively neutralizing long-standing sell pressure. This transition is fueled by a jump in network demand, with daily Data Credit burns climbing from $30,000 to over $50,000 since the beginning of the year, signaling that utility-driven token destruction is now outpacing new issuance.

Listen. Read. Watch. Engage.

Looking for more? Receive the latest crypto news from coindesk.com and explore our robust Data & Indices offerings by visiting coindesk.com/institutions.

Note: The views expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc., CoinDesk Indices or its owners and affiliates.

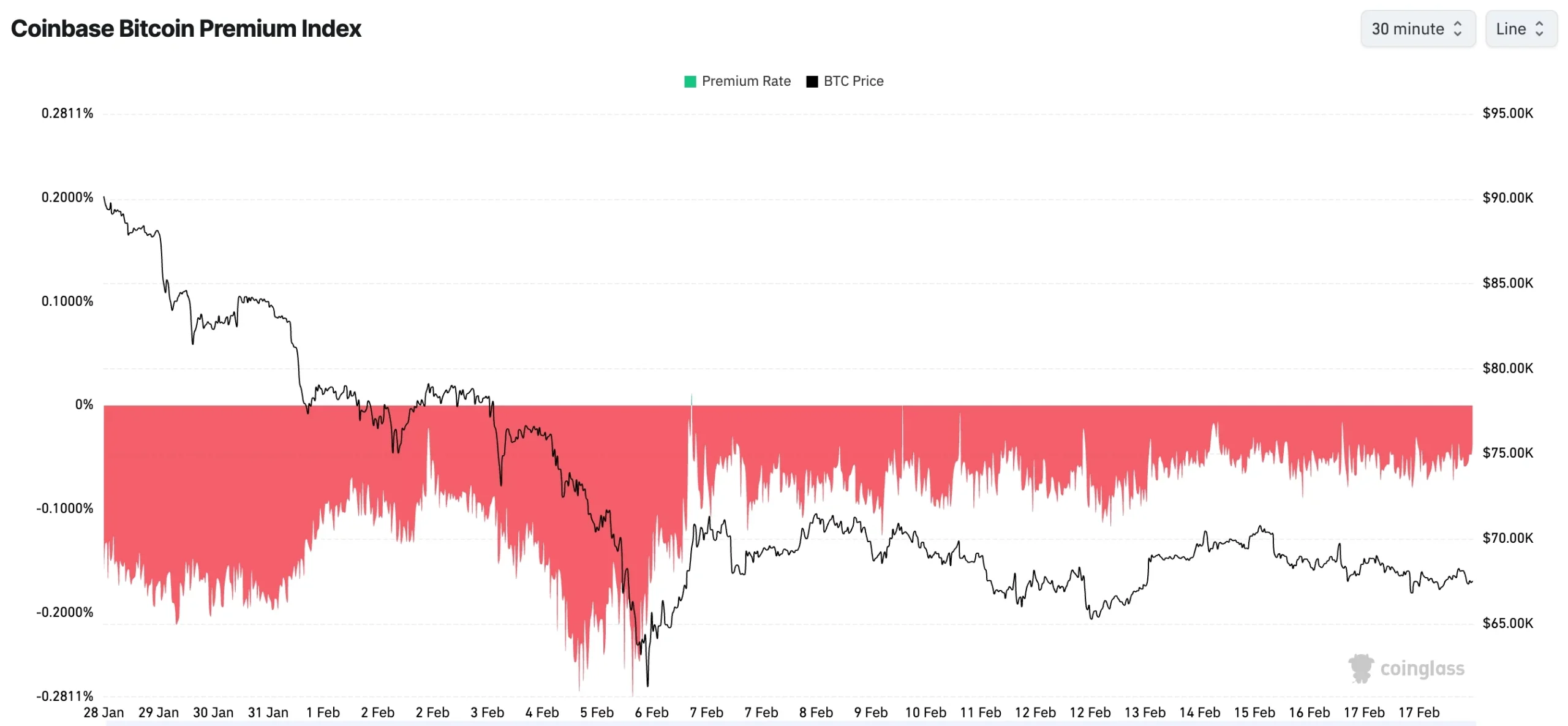

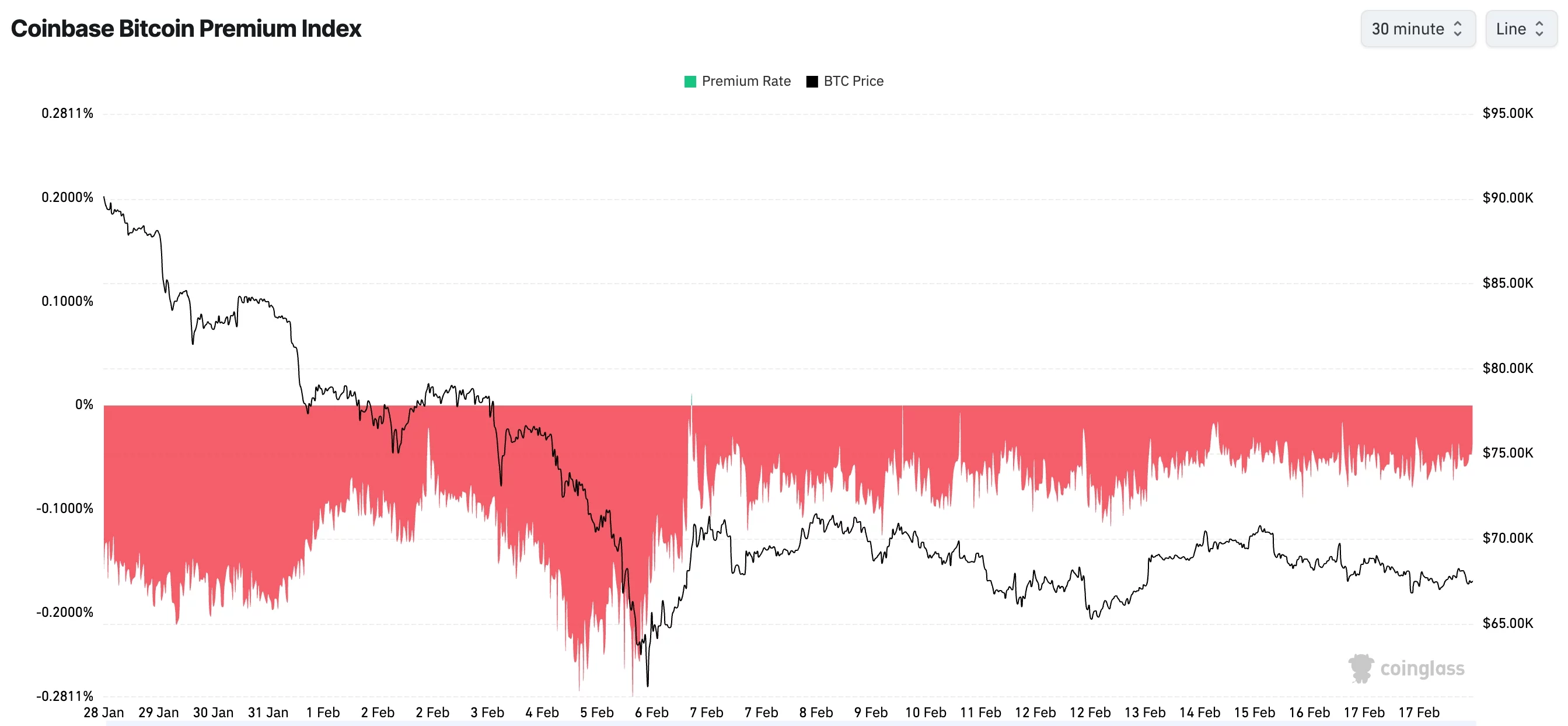

Bitcoin price remained in a tight range this week, and the waning Coinbase Premium Index points to more downside as institutional demand wanes.

Summary

- Bitcoin price has formed a bearish pennant pattern on the daily chart.

- The Coinbase Premium Index has remained in the red, a sign of weak demand from the US.

- Futures open interest has continued falling this month.

Bitcoin (BTC) was trading at $67,420 on Wednesday, down modestly from last weekend’s high of over $70,000. It has slumped by double digits from its all-time high of $126,300.

One major risk facing Bitcoin is that institutional demand has largely waned in the United States, which explains why the Coinbase Premium Index has remained in the red throughout this year. Coinbase is the most preferred platform for Bitcoin investing by American investors.

Additionally, only a handful of Bitcoin treasury companies are accumulating Bitcoin as they did last year. Strategy continued buying Bitcoin last week, bringing its total holdings to over 717,000. American Bitcoin and Strive have also bought Bitcoin this year.

Meanwhile, SoSoValue’s data shows that spot Bitcoin ETF outflows have jumped in the past few months. All these funds have shed over $8 billion in assets since October last year, and the trend is continuing.

According to Bloomberg, institutions have largely given up on Bitcoin because it has not fulfilled its role as a hedge against inflation and equity market stress. It has also not served its perceived role as a hedge against currency debasement.

Bitcoin’s futures open interest has continued falling in the past few months and now sits at $44 billion, down sharply from last year’s high of over $95 billion. Also, demand for borrowed exposure on CME has remained muted into the past few months.

Bitcoin price technical analysis suggests a crash

The daily timeframe chart shows that Bitcoin price is flashing red alerts. For example, the coin is slowly forming a large bearish pennant pattern. It has already completed forming the vertical line and is now in the process of forming the triangle section.

The Supertrend indicator has remained red since January 19 this year. It has also remained below the 50-day and 100-day Exponential Moving Averages.

Therefore, the coin will likely continue falling, with the initial target being the year-to-date low of $60,000. A drop below that level will signal further downside, potentially to the psychological $50,000 level, as Standard Chartered analysts predicted last week.

Leaked Email Suggests Ring Plans To Expand ‘Search Party’ Surveillance Beyond Dogs

Everything that could change in Urmston town centre as 15-year vision laid out

Poland stocks higher at close of trade; WIG30 up 1.75%

-

Sports7 days ago

Sports7 days agoBig Tech enters cricket ecosystem as ICC partners Google ahead of T20 WC | T20 World Cup 2026

-

Video2 days ago

Video2 days agoBitcoin: We’re Entering The Most Dangerous Phase

-

Tech4 days ago

Tech4 days agoLuxman Enters Its Second Century with the D-100 SACD Player and L-100 Integrated Amplifier

-

Video5 days ago

Video5 days agoThe Final Warning: XRP Is Entering The Chaos Zone

-

Tech2 days ago

Tech2 days agoThe Music Industry Enters Its Less-Is-More Era

-

Sports2 days ago

Sports2 days agoGB's semi-final hopes hang by thread after loss to Switzerland

-

Crypto World1 day ago

Crypto World1 day agoCan XRP Price Successfully Register a 33% Breakout Past $2?

-

Business17 hours ago

Business17 hours agoInfosys Limited (INFY) Discusses Tech Transitions and the Unique Aspects of the AI Era Transcript

-

Video1 day ago

Video1 day agoFinancial Statement Analysis | Complete Chapter Revision in 10 Minutes | Class 12 Board exam 2026

-

Entertainment3 hours ago

Entertainment3 hours agoKunal Nayyar’s Secret Acts Of Kindness Sparks Online Discussion

-

Crypto World5 days ago

Crypto World5 days agoBhutan’s Bitcoin sales enter third straight week with $6.7M BTC offload

-

Tech8 hours ago

Tech8 hours agoRetro Rover: LT6502 Laptop Packs 8-Bit Power On The Go

-

Crypto World7 days ago

Crypto World7 days agoPippin (PIPPIN) Enters Crypto’s Top 100 Club After Soaring 30% in a Day: More Room for Growth?

-

Video7 days ago

Video7 days agoPrepare: We Are Entering Phase 3 Of The Investing Cycle

-

NewsBeat3 days ago

NewsBeat3 days agoThe strange Cambridgeshire cemetery that forbade church rectors from entering

-

Business6 days ago

Business6 days agoBarbeques Galore Enters Voluntary Administration

-

Business9 hours ago

Business9 hours agoTesla avoids California suspension after ending ‘autopilot’ marketing

-

Crypto World6 days ago

Crypto World6 days agoEthereum Price Struggles Below $2,000 Despite Entering Buy Zone

-

NewsBeat3 days ago

NewsBeat3 days agoMan dies after entering floodwater during police pursuit

-

Crypto World5 days ago

Crypto World5 days agoKalshi enters $9B sports insurance market with new brokerage deal