Crypto World

WLFI vs Justin Sun: The Tron-Trump feud explained

The dispute between World Liberty Financial and Tron founder Justin Sun is one of the most operatic feuds in crypto history.

Summary

- Justin Sun invested about $75M in WLFI before becoming its loudest critic.

- WLFI froze Sun’s wallet after alleging a $9M token-transfer violation.

- Sun sued WLFI in California, while WLFI countersued him in Florida.

- The feud raises larger questions about DeFi governance and token blacklists.

Sun became WLFI’s single largest investor in late 2024, putting approximately $75 million into the project and receiving 1 billion tokens as an advisor. WLFI publicly credited him with rescuing the project from a slow start.

In September 2025, WLFI froze 272 wallets including Sun’s after a phishing incident, alleging he had moved approximately $9 million in tokens in violation of investment terms. Sun denied any intent to sell. By December 2025, his locked position had lost $60 million in value. In April 2026, after CoinDesk reported WLFI’s circular borrowing on Dolomite, Sun broke publicly with the project, calling the team a “personal ATM” and accusing it of extracting illegitimate fees.

WLFI responded with “See you in court” and on May 4 countersued in Florida for defamation, alleging Sun violated contractual limits and engaged in short-selling against the WLFI token. Sun had already filed in California federal court on April 21 for breach of contract, fraud, and conversion, with his claimed losses now exceeding $320 million.

The dispute exposes deep structural questions about smart contract governance, the limits of DeFi decentralization, blacklisting mechanisms in governance tokens, and what happens when crypto’s most controversial figures fall out with its most politically connected project. This piece walks through the full timeline, the actual legal claims, the structural issues the feud reveals, and what it means for the broader WLFI ecosystem.

How Sun became WLFI’s largest backer

The Sun-WLFI relationship started as the kind of partnership both sides publicly celebrated, and the early dynamics matter because they establish how high the stakes became when things fell apart.

Justin Sun is one of the most controversial figures in cryptocurrency. The Tron founder built one of the largest blockchain ecosystems by total value locked and stablecoin transaction volume, made and lost multiple fortunes, faced an SEC fraud and market manipulation lawsuit eventually dropped in February 2025, and has been a constant presence at industry conferences and political events. His investment style is aggressive, his public persona is theatrical, and his willingness to deploy major capital at speed has made him one of the most consequential individual investors in the sector.

According to Sun’s April 2026 court filing in the US District Court for the Northern District of California, Sun invested $45 million in WLFI tokens between November 2024 and January 2025, with additional purchases bringing his total cash investment to approximately $75 million. Sun also received 1 billion WLFI tokens as an advisor to the project. The advisor allocation reflected what was at the time a productive working relationship: Sun’s industry network, Tron’s distribution channels for USDT, and his willingness to publicly champion the project gave WLFI credibility and reach during its critical launch phase.

WLFI publicly acknowledged Sun’s role. The project credited Sun with helping rescue WLFI from a slow start. Sun made statements supporting the venture and President Trump’s broader crypto-friendly policy direction. The early relationship represented something unusual in crypto: a politically connected project receiving major support from one of the industry’s most controversial individual investors, with both sides benefiting from the association.

The structural dynamics Sun’s position created were significant. He became WLFI’s single largest token holder. His Tron network became a major distribution channel for USD1 (the WLFI stablecoin). His public statements moved the WLFI token price. His access to other major crypto investors meant his endorsement carried weight beyond his personal capital deployment. In effect, Sun was not just an investor in WLFI. He was a structural participant in the venture’s growth strategy.

The timing of Sun’s investment matters in retrospect. Sun deployed capital into WLFI starting in November 2024, immediately after Trump’s election victory and before the inauguration. The investment took place while Sun was actively fighting his SEC fraud case. By February 2025, after Trump took office and his SEC appointees began reviewing pending enforcement actions, the SEC dropped its case against Sun. The dropping of the case was widely interpreted as part of the broader administration shift in crypto enforcement priorities, though no formal documentation established direct causation between Sun’s WLFI investment and the case resolution.

Sun himself has been consistent in framing his support for WLFI as ideological rather than transactional. He has repeatedly stated his support for President Trump’s crypto-friendly policy direction. In his April 2026 lawsuit filing and accompanying public statements, Sun stressed he had “always been, and remain, an ardent supporter of President Trump” while specifically criticizing WLFI leadership. The framing matters because it shapes how Sun positions himself within the dispute: as a loyal Trump supporter pushed into legal action by misconduct of project leadership rather than by political disagreement.

What the early relationship established was the structural foundation for how serious the eventual breakdown would become. Sun was not a marginal investor whose departure could be quietly absorbed. He was the single largest token holder, a structural distribution partner, and a publicly endorsed early backer. When the relationship broke down, it broke down with proportional intensity.

The September 2025 freeze

The first inflection point in the WLFI-Sun relationship was WLFI’s decision in September 2025 to freeze Sun’s wallet as part of a broader security action, and the mechanics of that freeze deserve careful unpacking because they established the legal framework for everything that followed.

In September 2025, WLFI announced it had frozen 272 wallets as part of a security response to a phishing incident. According to WLFI’s public statements at the time, the freeze was a defensive measure meant to protect user funds from exploitation following the phishing attack. The 272 wallets included addresses WLFI flagged as potentially compromised, addresses showing patterns consistent with token-sale violations, and addresses linked to suspicious trading activity.

Sun’s wallet was one of the 272. WLFI’s specific justification for including Sun’s wallet was the project’s allegation that Sun had moved approximately $9 million worth of WLFI tokens, an action WLFI characterized as a potential attempt to cash out early in violation of his investment terms. The original WLFI token sale terms included contractual restrictions on token transfers and sales during specific vesting periods, meant to prevent early backers from dumping holdings into thin markets.

Sun denied any intent to sell. His public statements at the time framed the token movements as routine wallet management rather than sale attempts. He argued the freeze was disproportionate to the alleged behavior and lacked due process. WLFI’s response was the freeze was contractually authorized and operationally necessary.

The market impact on Sun’s position was substantial. By December 2025, his locked WLFI tokens had lost approximately $60 million in value as the WLFI token declined sharply from its October 2025 trading peak. The token had already fallen more than 40 percent since trading began. Sun’s inability to sell or move his tokens meant he was structurally exposed to ongoing price decline without recourse.

The legal architecture of the freeze raised structural questions central to the eventual lawsuit. According to Sun’s April 2026 court filing, WLFI’s smart contract for the WLFI token includes a blacklisting function letting the project freeze any holder’s tokens without notice or recourse. Sun’s lawsuit alleges this function constitutes a “secret backdoor” embedded in the smart contract, and the existence of the function was not adequately disclosed to investors at the time of token purchase.

WLFI’s response to this characterization has been the freeze function was disclosed in the token sale documents and Sun’s purchase agreements specifically authorized the project’s ability to enforce contractual restrictions through technical means including freezing. WLFI’s May 2026 countersuit argues Sun’s claims about the freeze are factually inaccurate because the freeze capability was contractually disclosed.

The structural question the freeze raised is fundamental to DeFi governance: can a project marketing itself as decentralized infrastructure simultaneously keep centralized control mechanisms over its own governance token? The WLFI smart contract clearly includes the technical capability to freeze any holder’s tokens. The disclosure question is whether this capability was adequately communicated to investors as material risk. The contractual question is whether enforcement of the freeze against Sun’s specific behavior was authorized by the agreements he signed.

These questions are now in active litigation. Both sides have strong public positions. The eventual judicial resolution will likely set significant precedents for how DeFi projects can structure their token contracts, what counts as material disclosure for governance tokens, and what limits exist on centralized control of supposedly decentralized assets.

The April 2026 breakdown

The relationship between Sun and WLFI deteriorated through late 2025 and early 2026 as Sun’s locked position kept losing value while WLFI made decisions Sun increasingly viewed as harmful to ordinary token holders. The full breakdown came in April 2026 in direct response to the Dolomite controversy.

On April 9, 2026, CoinDesk published its detailed on-chain analysis of WLFI’s Dolomite borrowing activity. The report documented WLFI had pledged 5 billion of its own WLFI governance tokens as collateral on Dolomite (a lending platform whose co-founder is a WLFI advisor) and borrowed approximately $75 million in stablecoins. The borrowing drained the Dolomite USD1 lending pool to nearly 100 percent utilization, meaning other depositors who had supplied USD1 expecting to earn interest could not withdraw their funds because WLFI had borrowed nearly all of it.

For Sun, the Dolomite events represented confirmation of structural concerns he had been developing for months. From his perspective, the project he had backed was now using its own infrastructure to extract value for insiders while ordinary depositors had their funds trapped. The pattern was consistent with concerns about whether WLFI ran as legitimate DeFi or as a value-extraction mechanism for the Trump-affiliated entities controlling the venture.

On April 12, 2026, Sun publicly broke with WLFI. In a series of social media posts and public statements, he accused the project of treating its users as a “personal ATM” and extracting illegitimate fees. His specific language was pointed: “Every action taken by the WLFI team to extract fees from users and to treat the crypto community as a personal ATM is illegitimate.” He called himself “the project’s first and single largest victim” of WLFI’s practices.

Sun’s framing of his criticism was important: he positioned himself as a loyal Trump supporter who had been victimized by misconduct of WLFI’s operational leadership, rather than as a political opponent. He repeatedly stressed his continued support for President Trump while specifically criticizing the people running WLFI day-to-day. The framing was strategically sophisticated. It let him keep political alignment while creating maximum pressure on WLFI’s leadership.

WLFI’s response on April 13 escalated rapidly. The project published a public statement on X accusing Sun of running a pressure campaign with “baseless allegations” meant to “cover up his own misconduct.” The statement ended with the phrase “See you in court,” signaling WLFI’s intent to pursue legal action. WLFI’s specific accusations against Sun included allegations he had attempted to sell tokens in violation of his investment terms, engaged in market manipulation through short-selling activity, and made defamatory public statements.

The public exchange marked the formal end of the Sun-WLFI relationship. Both sides moved from internal dispute resolution to public confrontation. The legal positions hardened. Each side began preparing for protracted litigation. The market response was swift: WLFI token dropped approximately 10 percent in the immediate aftermath as the public dispute compounded concerns about the project’s governance and stability.

The structural breakdown reflected something deeper than just the immediate Dolomite trigger. Sun’s accumulated frustrations included the September 2025 freeze, the ongoing decline in his locked token value, what he viewed as inadequate governance representation despite his position as the largest token holder, and what he characterized as a pattern of insider value extraction at the expense of ordinary participants. The Dolomite events were the visible trigger, but the underlying dynamics had been building for months.

WLFI’s accumulated frustrations included Sun’s perceived violation of token transfer restrictions, his public criticism the project viewed as undermining institutional credibility, and his alleged actions through related entities to short the WLFI token and move tokens through unauthorized channels. From WLFI’s perspective, Sun had become a hostile insider whose continued participation in the project was operationally harmful.

The April 2026 breakdown made resolution through private negotiation effectively impossible. Once both sides committed to public confrontation and legal action, the dispute became a winner-take-all litigation matter with major implications for both parties and for the broader DeFi sector.

Sun’s lawsuit: the legal claims

Sun filed his lawsuit on April 21, 2026 in the US District Court for the Northern District of California. The filing was made by Sun personally along with two British Virgin Islands companies he controls: Blue Anthem Limited and Black Anthem Limited. The defendant is World Liberty Financial. The legal claims and the specific allegations deserve careful unpacking because they will shape the eventual judicial outcome.

The legal claims in Sun’s lawsuit are breach of contract, fraud, and conversion. Sun seeks damages (estimated at over $320 million based on the peak value of his locked tokens) and injunctive relief requiring WLFI to unfreeze his tokens, restore his governance voting rights, and refrain from burning his tokens.

The specific factual allegations include the following. WLFI embedded a “secret backdoor” in the WLFI smart contract giving the project the ability to blacklist and freeze any holder’s tokens. The existence of this backdoor was not adequately disclosed to investors at the time of token purchase. WLFI froze Sun’s tokens twice (initially in September 2025 and again in a subsequent action) without proper justification or due process. WLFI stripped Sun of his governance voting rights despite his position as the largest token holder. WLFI threatened to permanently destroy (“burn”) his tokens, wiping out his investment entirely. WLFI attempted to extort Sun into minting additional tokens or taking other actions through the threat of token destruction.

The contractual basis for Sun’s claims is WLFI’s actions violated the token purchase agreements he signed and the public representations WLFI made about how the governance token would function. The fraud claim is WLFI made representations about decentralization, governance, and investor rights it did not intend to honor or could not honor given the smart contract’s actual technical structure. The conversion claim is WLFI’s freeze of Sun’s tokens constituted unlawful interference with his property rights.

The expert analysis on the lawsuit has stressed the gap between WLFI’s public marketing and the smart contract’s actual technical capabilities. Decrypt’s coverage of the filing quoted experts noting the defensibility of WLFI’s position “weakens sharply” when the public marketing of decentralization conflicts with the smart contract’s actual centralized control mechanisms. If a court finds the freeze function was material to investor decisions and was not adequately disclosed, WLFI faces significant legal exposure.

The damages calculation Sun seeks reflects both the value of his original investment ($75 million) and the appreciation he claims was wrongfully wiped out through the freeze. At peak WLFI token prices (October 2025), Sun’s combined position was worth substantially more than his initial cash investment. The $320 million figure represents Sun’s view of what his position would be worth absent the freeze, including both his purchased tokens and his advisor allocation.

The injunctive relief Sun seeks is in some ways more significant than the damages claim. If a court orders WLFI to unfreeze Sun’s tokens and restore his governance rights, Sun would regain his position as the largest WLFI token holder with full ability to vote on governance proposals, transfer tokens, and exercise the rights of ownership. This would create immediate market pressure as Sun could potentially sell substantial holdings, and would also create governance disruption as Sun could potentially vote against WLFI leadership on key proposals.

The legal strategy reflects Sun’s broader objective. He is not seeking a settlement exiting him from the project quietly. He is seeking full restoration of his rights as a WLFI token holder, with full ability to keep taking part in (or disrupting) the project as he sees fit. This makes the lawsuit more existentially threatening for WLFI than a simple monetary dispute would be.

WLFI’s countersuit: the response

WLFI filed its countersuit on May 4, 2026 in Florida state court. The legal claim is defamation. The specific allegations and the structural strategy behind WLFI’s counter-legal action deserve equal attention because they reveal WLFI’s view of the broader dispute.

The defamation claim is based on Sun’s public statements through April 2026, particularly his “personal ATM” allegations and his characterization of WLFI’s leadership as engaging in deceptive DeFi practices. WLFI argues these statements were factually inaccurate, were made with knowledge of their inaccuracy or with reckless disregard for the truth, and caused measurable harm to WLFI’s business reputation and operational position.

The specific factual allegations supporting WLFI’s countersuit include the following. The freeze function in the WLFI smart contract was disclosed in the token sale documents Sun signed, contradicting his “secret backdoor” characterization. Sun’s freeze was specifically justified by his violation of contractual transfer restrictions, contradicting his claim it was without justification. Sun-linked entities moved WLFI tokens to Binance in violation of contractual limits. Sun-linked entities bought WLFI tokens for other investors in arrangements that may have violated securities regulations. Sun-linked parties engaged in short-selling activity against the WLFI token, creating financial incentive for Sun to publicly attack the project.

The legal strategy behind the countersuit is defensive rather than primarily offensive. WLFI is not realistically expecting to win major monetary damages from Sun. The countersuit serves three strategic purposes. It establishes WLFI’s narrative that Sun is the bad actor in the dispute rather than the victim. It creates legal exposure for Sun that raises settlement pressure on Sun’s California lawsuit. It signals to other potential plaintiffs that WLFI will aggressively defend against legal action including through counter-litigation.

The Florida venue choice is also strategic. Florida state courts are generally considered favorable to defendants in defamation cases compared to California federal courts. The forum split (Sun’s case in California federal court, WLFI’s case in Florida state court) means the dispute will likely be litigated in two jurisdictions with potentially different procedural rules, creating complexity that may favor whichever party has more resources for sustained litigation.

WLFI’s specific allegations about Sun’s market activities are interesting structurally. The accusations that Sun moved tokens to Binance in violation of contractual limits, bought tokens for other investors, and engaged in short-selling against the WLFI token, if substantiated, would establish patterns of behavior that could support securities law violations beyond just the contractual disputes. The countersuit functions in part as a discovery vehicle that may let WLFI obtain documentation about Sun’s broader trading activities through the legal process.

The Consensus Miami appearance on May 7, 2026 by Donald Trump Jr. and WLFI CEO Zach Witkoff served as a public extension of the countersuit narrative. Both Trump Jr. and Witkoff stressed WLFI would not have filed the case without strong evidence, signaled confidence in the legal position, and addressed broader rumors about the project’s stability. The public appearances were strategically coordinated with the legal action to project strength and stability despite the ongoing dispute.

WLFI’s broader strategy appears to be using the litigation to reset the narrative around the dispute. From WLFI’s perspective, Sun is a hostile insider whose public criticism is motivated by personal financial interest (his frozen position) rather than by legitimate concerns about the project’s governance. The countersuit is designed to reframe the dispute in those terms and to create legal exposure for Sun that may force him toward settlement on WLFI’s terms.

What the dispute reveals about smart contract governance

The Sun-WLFI dispute exposes structural questions about how governance tokens actually function in supposedly decentralized projects, and the implications go far beyond just this specific feud.

The first structural question is about disclosure of centralized control mechanisms. WLFI’s smart contract includes the technical capability to freeze any holder’s tokens. This capability is functionally equivalent to a centralized authority keeping the ability to seize assets from individual users. The existence of this capability is not unusual in tokens that have compliance or regulatory requirements. The disclosure question is whether the existence of such capabilities should be prominently communicated to token purchasers as material to their investment decision, or whether burying the capability in smart contract code with limited documentation is adequate disclosure.

The marketing-versus-technical-reality gap is structurally important. WLFI marketed itself as building “DeFi platforms” and stressed decentralization, governance participation, and user empowerment. The smart contract technically includes mechanisms allowing centralized override of holder rights. Whether this represents adequate disclosure or material misrepresentation depends on what reasonable investors should be expected to investigate before purchasing, and what platforms can reasonably claim about decentralization given the technical reality of their contracts.

The Sun lawsuit will likely produce judicial guidance on this question. If a court finds the disclosure was adequate, it establishes smart contract code itself counts as adequate disclosure of all capabilities embedded in it, regardless of how the project markets itself. If a court finds the disclosure was inadequate, it establishes projects need to clearly communicate centralized control mechanisms in plain language to investors. Either ruling will have significant implications for how DeFi projects structure their disclosures going forward.

The second structural question is about due process for blacklisting decisions. WLFI’s freeze of Sun’s wallet happened without prior notice, without a formal hearing, and without an appeal process. From a centralized financial institution’s perspective, freezing an account suspected of misconduct is routine. From a DeFi project’s perspective marketing itself as alternative to traditional finance, applying centralized control mechanisms without due process represents exactly the dynamic DeFi is supposed to avoid.

The legal question is whether token purchase agreements can validly waive due process protections that would otherwise apply, or whether some minimum procedural protections are required regardless of contractual terms. The judicial answer will likely depend heavily on whether tokens are classified as securities (in which case investor protection requirements apply) or as commodities (in which case more permissive contractual flexibility applies). The SEC’s evolving treatment of governance tokens makes this categorization itself contested.

The third structural question is about the nature of decentralization claims. The crypto industry routinely markets projects as decentralized while keeping substantial centralized control mechanisms. WLFI is far from unique in this dynamic. Many major DeFi projects have admin keys, governance multisigs, or other mechanisms letting centralized actors override the supposedly autonomous operation of the protocol. The question Sun’s lawsuit raises is whether the gap between decentralization claims and centralization reality is large enough in WLFI’s case to constitute misrepresentation.

The implications for the broader DeFi sector are substantial. If WLFI’s contract structure (governance token with embedded freeze function) is found to be inadequately disclosed, similar structures across the DeFi sector will face scrutiny. If WLFI’s contract structure is upheld as adequately disclosed, projects will keep maintaining centralized control mechanisms while marketing decentralization, with the legal protection of “the code is the disclosure.”

The fourth structural question is about insider conflicts and value extraction. The Dolomite events Sun cited as the trigger for his public break with WLFI involved WLFI using its own governance tokens as collateral to borrow against its own stablecoin from a lending platform with insider relationships to the venture. This pattern is not necessarily illegal, but it raises questions about whether DeFi projects can simultaneously serve as legitimate infrastructure for outside users and as value-extraction mechanisms for insiders. Sun’s allegation is WLFI prioritized the latter at the expense of the former.

The resolution of these structural questions through Sun’s litigation will likely take years. The immediate dispute will probably be resolved through some combination of settlement negotiations, dismissals on procedural grounds, and partial judicial rulings on specific claims. The broader structural questions about DeFi governance, smart contract disclosure, and decentralization claims will keep evolving through subsequent cases, regulatory actions, and industry practices.

What it means for WLFI and the broader ecosystem

The implications of the Sun-WLFI dispute go beyond just the immediate legal battle and reach into the broader trajectory of the WLFI project and the political-crypto integration story.

For WLFI specifically, the dispute is operationally damaging regardless of the eventual legal outcome. The ongoing litigation creates persistent uncertainty about the project’s governance and stability. Sun’s public statements keep generating critical coverage. Other large token holders may be reluctant to commit additional capital while the legal situation is unresolved. Institutional partners may delay integrations until they can assess the legal exposure. The project’s WLFI governance token has been under sustained selling pressure since the dispute began, falling approximately 76 percent from its October 2025 all-time high.

The narrative impact may be more significant than the financial impact. WLFI has been working to position itself as institutionally credible (BitGo custody, BlackRock reserve management, Chainlink Proof of Reserves, pursuit of national trust bank charter for USD1). Sun’s public criticism that the project treats users as a “personal ATM” is exactly the kind of narrative undermining institutional credibility. Even if WLFI prevails in court, the reputational damage from the sustained public dispute is substantial.

For Sun specifically, the dispute represents both opportunity and risk. The opportunity is regaining access to his frozen tokens (potentially worth substantial amounts even after the WLFI decline) and establishing himself as a champion of legitimate DeFi against insider extraction. The risk is the countersuit, the potential securities law exposure from his market activities, and the reputational damage from being publicly identified as a hostile actor against a Trump-aligned project. Sun’s political alignment efforts (his continued public support for Trump while criticizing WLFI leadership) suggest he understands the political dimensions of his risk profile.

For the broader DeFi sector, the dispute creates several precedents that will shape future project structures. The judicial rulings on the freeze function disclosure will affect how all DeFi projects structure their smart contracts and disclosures. The handling of the cross-jurisdictional litigation (California versus Florida) will influence forum-shopping strategies in future disputes. The eventual resolution will likely become reference precedent in how courts handle disputes between token holders and project teams about governance rights and protocol control.

For the political-crypto integration story, the Sun-WLFI dispute is one of the clearest examples of how crypto’s political alignments can fracture under operational pressure. Sun was politically aligned with WLFI through his Trump support and through the perceived favorable treatment his SEC case received from the Trump administration. The breakdown of his WLFI relationship took place despite, not because of, the political alignment. This suggests political alignment is not a stable substitute for operational alignment in cryptocurrency businesses.

For institutional users evaluating WLFI products (USD1 specifically), the dispute adds another layer of consideration alongside the political and operational concerns previously documented. The institutional architecture of USD1 (BitGo, BlackRock, Chainlink) stays technically credible. The political controversies surrounding WLFI generally stay documented. The Sun litigation adds specific operational and governance concerns separate from but related to the broader political dimensions. Each layer affects different institutional users differently based on their specific risk tolerances.

For crypto.news readers specifically, the practical takeaway is the Sun-WLFI dispute is not yet resolved and will likely keep evolving through 2026 and into 2027. The immediate legal proceedings (Sun’s California case, WLFI’s Florida countersuit) will produce filings, motions, and potentially partial rulings over the coming quarters. The eventual judicial outcomes will affect WLFI’s operational position and broader DeFi precedents. Both parties have substantial resources and strategic incentives to pursue the litigation aggressively. Quick settlement is possible but not the most likely outcome based on the trajectory of public statements so far.

The bottom line

The Sun-WLFI dispute is one of the most operatically dramatic feuds in crypto history, and the structural significance goes beyond just the personal dynamics between Justin Sun and the WLFI leadership.

The timeline is documented. Sun invested approximately $75 million in WLFI tokens between November 2024 and January 2025, plus 1 billion tokens as an advisor allocation. He became WLFI’s single largest backer. WLFI publicly credited him with helping rescue the project from a slow start. In September 2025, WLFI froze Sun’s wallet as part of a 272-wallet security action following a phishing incident, alleging Sun had moved approximately $9 million in tokens in violation of investment terms. Sun denied any intent to sell. By December 2025, his locked position had lost $60 million in value. The relationship deteriorated through Q1 2026.

The breakdown came in April 2026 in direct response to the Dolomite controversy. On April 9, CoinDesk reported WLFI’s circular borrowing on Dolomite. On April 12, Sun publicly accused WLFI of treating users as a “personal ATM.” On April 13, WLFI responded with “See you in court.” On April 21, Sun filed his lawsuit in the US District Court for the Northern District of California, alleging breach of contract, fraud, and conversion, seeking damages over $320 million and injunctive relief. On May 4, WLFI countersued in Florida state court for defamation. On May 7, Trump Jr. and Zach Witkoff defended WLFI publicly at Consensus Miami.

The legal claims are substantive on both sides. Sun’s case turns on whether WLFI’s smart contract freeze function was adequately disclosed and whether his specific freeze was justified by his actual behavior. WLFI’s case turns on whether Sun’s public statements meet the legal standard for defamation given the public-figure nature of the dispute. Expert analysis has suggested Sun’s case is stronger on the disclosure question than WLFI’s is on the defamation question, but both parties have credible legal arguments and substantial resources for sustained litigation.

The structural questions the dispute exposes are bigger than the immediate feud. Smart contract disclosure of centralized control mechanisms is a fundamental question for the DeFi sector. The gap between decentralization marketing and centralization technical reality is industry-wide, not just WLFI-specific. Due process protections for blacklisting decisions are unresolved. The classification of governance tokens as securities versus commodities affects what protections apply. Insider value extraction patterns in projects with concentrated ownership create governance questions independent of the specific WLFI case.

For WLFI as a venture, the dispute is operationally damaging regardless of legal outcome. The WLFI token has fallen approximately 76 percent from its October 2025 peak. The institutional credibility WLFI has been building through USD1’s BitGo/BlackRock/Chainlink architecture is undermined by the ongoing public dispute. Even prevailing in court would not erase the reputational damage from sustained public confrontation with the project’s largest backer.

For Sun as an investor, the dispute represents both opportunity to recover his frozen position and risk of broader legal exposure from his market activities. His strategy of keeping political alignment with Trump while specifically criticizing WLFI leadership is sophisticated and may produce the best available outcome given the constraints of his situation. The dual lawsuits (his California case and WLFI’s Florida countersuit) will likely produce extended litigation through 2026 and 2027.

For the broader DeFi sector, the dispute creates precedents that will shape how projects structure smart contracts and disclosures going forward. The judicial rulings on the freeze function disclosure issue will be reference points for future cases. The handling of cross-jurisdictional litigation will influence forum-shopping strategies. The eventual settlement or judicial resolution will become part of the developing legal framework around governance tokens, decentralization claims, and protocol-level control mechanisms.

For the political-crypto integration story, the Sun-WLFI breakdown shows political alignment is not a stable substitute for operational alignment. Sun was politically aligned with WLFI through his Trump support and the favorable treatment of his SEC case under the new administration. The breakdown took place despite this political alignment because of operational disputes about governance, smart contract control, and value extraction. The implication is crypto projects relying on political relationships for stability are exposed to the same operational risks as any other business.

What happens next depends on factors playing out over months and years rather than weeks. The legal proceedings in California and Florida will produce filings, motions, and rulings that gradually narrow the disputed issues. The market response to each development will affect the WLFI token price and the broader perception of the project’s stability. Political developments around the broader Trump administration crypto policy environment will create context affecting both parties’ strategic positions.

Other major WLFI stakeholders (MGX, the various institutional integrations) will make their own decisions about continued participation based on how the dispute evolves.

The honest read is the Sun-WLFI dispute is not just a celebrity crypto feud. It is a structural case study in how decentralization claims, smart contract control mechanisms, governance token rights, insider relationships, and political alignments interact when major participants in a crypto venture have a serious operational falling out. The specific facts of this dispute will likely produce judicial precedents shaping how the broader sector runs for years to come.

For now, what is established is the dispute is real, the legal claims are substantive on both sides, the operational damage to WLFI is significant, and Sun’s strategic position combines genuine grievances with sophisticated political positioning. Where it ends depends on what courts decide, how the parties strategically maneuver through the litigation, and how the broader political and regulatory environment evolves.

The Tron-Trump feud is the kind of story crypto produces uniquely. Largest backer becomes loudest critic. Political alignment fractures under operational pressure. Smart contract code becomes evidence in federal court. Dueling lawsuits cross jurisdictions. The participants are crypto’s most distinctive figures. The stakes are measured in hundreds of millions of dollars. The implications reach into the foundations of how decentralized finance actually functions.

The story is still being written. The judgments and resolutions will come over the next several years through specific legal milestones rather than through any single defining event. What is certain is the dispute has already shaped how crypto operators, regulators, and investors think about the gap between decentralization marketing and centralization reality. Whatever the eventual resolution, that shift in industry consciousness is already established.

This article is for informational purposes and does not constitute legal or investment advice. The legal proceedings, factual allegations, and operational developments described reflect reporting available as of late May 2026. Both parties have substantive legal positions and the ultimate resolution will be determined by judicial proceedings rather than by media coverage. Always do your own research.

TLDR:

- Stellar now holds over $2B in tokenized RWAs as payment volume climbs 72% year-over-year to $5.5B.

- Circle’s CCTP brings native USDC to Stellar, enabling transfers across 23+ chains without bridge risk.

- Figure’s SEC-registered YLDS offers compliant yield on Stellar, targeting fintechs and LATAM markets.

- Bermuda is migrating wages, government fees, and payments onto Stellar in a full national deployment.

Stellar is moving beyond its payments roots in 2026, stepping into tokenized real-world assets, compliant yield products, and institutional settlement infrastructure.

The network now holds over $2 billion in tokenized RWAs. Payment volume has grown 72% year-over-year to $5.5 billion.

Developer participation is up 86%. These figures point to active usage across the ecosystem, not just projected growth.

Cross-Chain Liquidity and Regulated Yield on Stellar

Circle’s Cross-Chain Transfer Protocol is now live on Stellar. Native USDC can move between Stellar and more than 23 blockchains without wrapped tokens.

This removes traditional bridge risks for payments, exchanges, and DeFi applications. The integration gives these platforms access to deeper liquidity at a critical time for the network.

Figure has also launched YLDS on Stellar, an SEC-registered yield-bearing dollar asset. It is designed to serve as a compliant onchain savings product for fintechs and retail users.

Markets like Latin America stand to benefit from combining stablecoin liquidity with money-market-style yield. This fills a gap that standard stablecoins have not addressed within a regulated framework.

The DTCC is also engaging with Stellar’s settlement infrastructure. This adds a major institutional layer to the network’s growing financial stack.

Settlement-grade infrastructure alongside regulated yield products creates a more complete offering. Institutions looking for compliant, onchain alternatives now have more options on Stellar.

Stablecoin activity and enterprise participation are both growing alongside these product launches. The network is attracting users who need more than simple transfers.

As @ourcryptotalk noted, this is usage, not just another roadmap. That distinction matters when evaluating where the network stands today.

Bermuda Builds a National Economy on Stellar

Bermuda is conducting one of the most ambitious real-world tests of blockchain infrastructure. The country is migrating wages, merchant payments, government fees, and stablecoin disbursements onto Stellar.

Financial services are also moving to the network as part of this national effort. This is a live deployment, not a pilot program.

The scale of Bermuda’s adoption is rare in the blockchain space. No comparable national economy has attempted a full transition of this kind on a public network.

Stellar’s existing focus on cross-border payments made it a practical fit for this use case. The infrastructure was already built for speed, low fees, and compliance.

For Stellar, sovereign adoption adds a concrete use case to its institutional narrative. Bermuda’s activity will generate real transaction data across government and commercial settings.

That data will be visible on-chain and open to analysis by developers and institutions alike. It gives Stellar a proof point that few other networks can match.

XLM is currently trading near $0.19, testing a key support zone between $0.18 and $0.20. On the four-hour chart, the price is compressing inside a falling wedge with RSI forming higher lows.

A confirmed breakout above $0.20 would be the first technical signal of buyer control returning. The coming weeks will show whether the fundamental activity translates into price recovery.

Bitcoin’s price tried to break out above $64,000 yesterday, but it was stopped, and it still trades close to that level on Saturday morning.

Most larger-cap alts have posted minor gains over the past day, including ADA and HYPE, both up around 3%. In contrast, XMR has dumped hard.

BTC Calms at $64K

The primary cryptocurrency reacted well to the massive price decline observed during the first week of June, culminating that Friday in a nosedive to $59,100. After dumping to this 19-month low, the asset rebounded and jumped toward $64,000 on June 8.

The controversial developments on the US-Iran war front, which included new attacks against numerous countries in the region, halted bitcoin’s attempted recovery. So did the May CPI numbers, which were the highest in years.

BTC dipped below $61,000 on a couple of occasions during the week, but managed to defend that level and aimed at a more profound recovery. The highest price came yesterday, just hours before SPCX went live for trading on Wall Street, with a surge to almost $64,500. However, the bears intervened, and BTC now trades just under $64,000.

Its market capitalization has climbed to almost $1.280 trillion on CG. Its dominance over the alts, though, has increased further to 56.4%.

XMR Dumps

Ethereum continues to inch closer to $1,700 after another minor daily increase. BNB, XRP, and TRX have marked similar increases of under 1%. DOGE and SOL are up by 1.6%-1.7%, while HYPE has jumped by more than 3% to $59. Cardano’s native token continues with its recovery attempts. The token is up by 3% to well above $0.17 after the recent massacre.

In contrast, XMR has erased all the gains from earlier this week, dropping by more than 12% to $340. NEAR and ZEC are also slightly in the red. In contrast, BEAT, TAO, and ICP have marked substantial gains of up to 11%.

The total cryptocurrency market cap has remained near $2.270 trillion on CG.

The post Bitcoin (BTC) Calms Close to $64K, Cardano (ADA) Eyes Recovery: Weekend Watch appeared first on CryptoPotato.

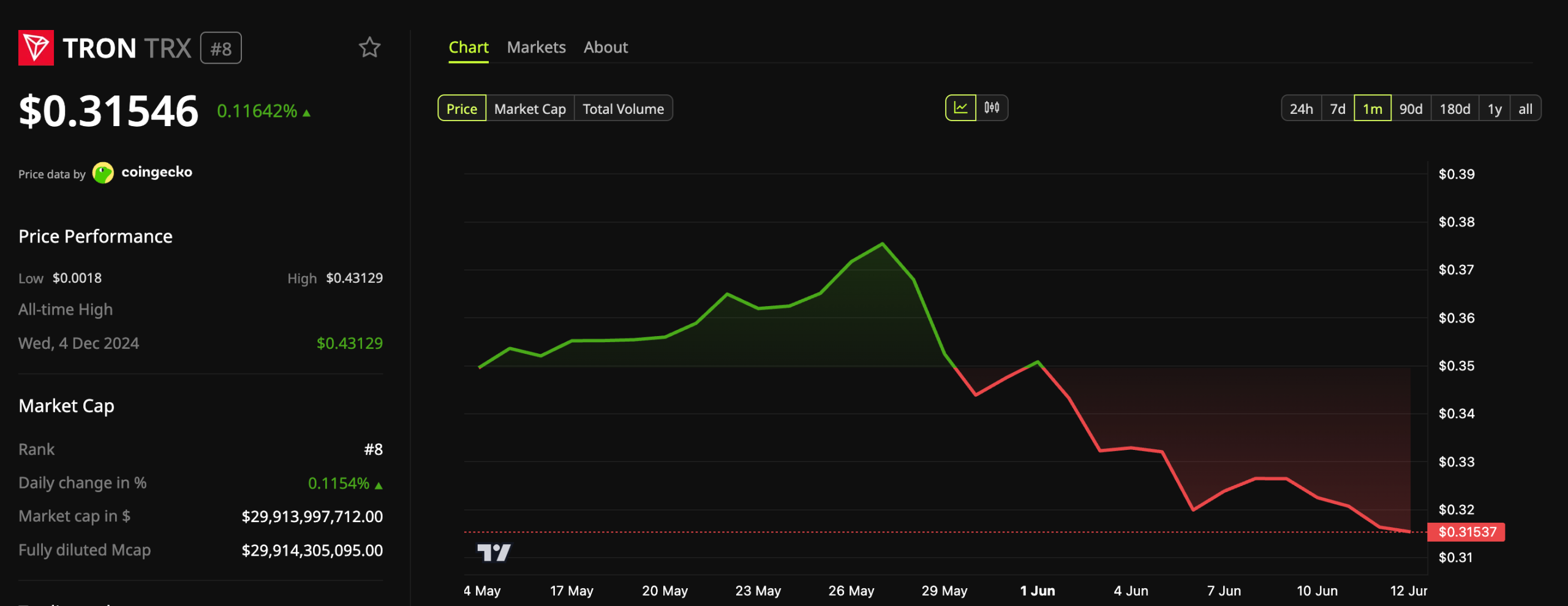

Tron (TRX) ranked as the worst weekly performer among the top 10 crypto assets, even as three bullish indicators formed beneath the price.

TRX traded near $0.315 on Saturday, holding the eighth spot by market value at roughly $29.9 billion. The token fell about 1.5% over the week. It also dropped close to 10% across the past 30 days.

3 Bullish Factors Stack Up for Tron as Price Dips

Price action lagged the supportive on-chain and corporate signals. Daily transactions on Tron surpassed 14.3 million, a record for the network.

Activity climbed 15% over the previous 30 days. The figures point to rising demand for the chain’s settlement capacity.

Follow us on X to get the latest news as it happens

CertiK also reported that the stablecoin value on Tron set a record this quarter. It reached $90.96 billion on May 24 and sits near $90.3 billion today. That marks a 4.9% rise since the end of Q1 and a 16.4% gain over the past year.

Decentralized exchange (DEX) activity also recovered. The firm noted that DEX volume rose 28% over the past 30 days, rebounding from multi-quarter lows.

In addition to network growth, institutional accumulation also continued. Tron Inc., the Nasdaq-listed treasury company, bought 159,118 TRX today. The purchase lifted its holdings above 700.3 million TRX. Overall, the firm has added 1.8 million TRX so far this month.

Regulated market access marked the third supportive signal. TRX gained a spot listing on Bitnomial, a CFTC-regulated US exchange and clearinghouse. The June 5 debut expanded access for American investors and institutions.

Days earlier, OKX Europe listed TRXUSD expiry perpetuals. The MiFID-regulated crypto derivatives product is available to eligible traders across 30 European Economic Area jurisdictions, with up to 10x leverage.

Together, the two listings stretched institutional reach across two continents. Tron founder Justin Sun framed the move as a step toward broader market participation.

“As demand for compliant digital asset products continues to grow, the availability of TRX on regulated platforms supports broader market access, greater transparency and the continued maturation of the digital asset ecosystem,” Sun said.

On the technical front, BeInCrypto’s analysis found that TRX trades inside an ascending triangle on the weekly chart, with resistance near $0.365 and a rising trendline that has held since mid-July 2024.

A confirmed break above resistance could open the door to further gains.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Tron Shows 3 Bullish Signals While Topping Weekly Loser List appeared first on BeInCrypto.

Anthropic has suspended access to its newly launched Fable 5 and Mythos 5 artificial intelligence models after receiving a U.S. government export control directive tied to national security concerns.

Summary

- Anthropic suspended Fable 5 and Mythos 5 after receiving a U.S. export control directive.

- The company said officials cited national security concerns linked to a potential jailbreak method.

- The move comes days after the launch of the new AI models and amid a major infrastructure expansion push.

According to a statement published by Anthropic on Friday, the company received the directive at 5:21 p.m. ET, instructing it to block access to Fable 5 and Mythos 5 for all foreign nationals, regardless of whether they are located inside or outside the United States. The order also applied to foreign-national employees working at Anthropic.

Faced with the directive, Anthropic said it disabled both models for all users to ensure compliance with the government’s requirements. The company added that its other models, including Opus 4.8, remain available and are not affected by the restrictions.

“We are complying with the government’s legal directive and are removing access to Fable 5 and Mythos 5 for all users.”

The move comes only days after Anthropic introduced Fable 5 as a generally available Mythos-class model and released Mythos 5 for a limited group of approved cybersecurity and infrastructure users.

According to Anthropic, Fable 5 was designed to handle longer and more complex tasks than previous Claude models and delivered strong performance across software engineering, scientific research, finance, vision, memory, and knowledge work.

Government concerns center on potential model jailbreak

While authorities did not provide detailed evidence supporting the order, Anthropic said it believes the government is concerned about a possible jailbreak technique that could bypass some of Fable 5’s safeguards.

According to Anthropic, officials have so far presented only verbal evidence of what the company described as a narrow, non-universal jailbreak. The company said the reported method involves asking the model to analyze a specific codebase and identify or repair software vulnerabilities.

Anthropic explained that a non-universal jailbreak differs significantly from a universal jailbreak because it does not broadly remove a model’s safety protections across a wide range of tasks.

“We disagree that the finding of a narrow potential jailbreak should be cause for recalling a commercial model deployed to hundreds of millions of people. If this standard was applied across the industry, we believe it would essentially halt all new model deployments for all frontier model providers.”

At the same time, Anthropic said it is working with authorities and believes the directive may have resulted from a misunderstanding. The company stated that it is seeking to restore access as quickly as possible.

Infrastructure expansion continues despite model restrictions

Even as access to Fable 5 and Mythos 5 remains suspended, Anthropic continues to expand its computing capacity for future AI systems.

As reported by crypto.news, private credit firms Blackstone and Apollo Global Management are syndicating approximately $36 billion in financing to support Anthropic’s next phase of infrastructure spending. Reuters reported that the funds will be used to acquire custom tensor processing unit chips from Google, backed by Broadcom technology, which Anthropic plans to lease for its AI operations.

Separately, Anthropic has been urging governments to establish rules for frontier AI systems as model capabilities advance. The company has proposed policy measures covering dangerous deployments, independent evaluations, cybersecurity safeguards, and economic preparation for workers affected by AI adoption.

Those policy recommendations now arrive as Anthropic finds itself at the center of one of the most significant government interventions involving a newly released frontier AI model.

TLDR:

- FinCEN clarifies how banks can share suspected fraud data under Section 314(b) program rules

- Guidance allows sharing of IP addresses, login patterns, and fraud indicators across institutions

- Move supports Treasury effort to disrupt fraud networks through faster interbank coordination

- Regulators push risk-based AML modernization to improve fraud detection and compliance efficiency

FinCEN issued updated guidance on information sharing under Section 314(b) of the USA PATRIOT Act on June 12, 2026. The move clarifies how banks and financial institutions can exchange fraud-related data in real time.

Treasury officials said the framework targets fraud, money laundering, and other illicit financial activity. The guidance arrives as regulators intensify efforts to curb scams affecting both traditional finance and crypto markets.

FinCEN Fraud Guidance Expands 314(b) Information Sharing for Financial Institutions

The Financial Crimes Enforcement Network clarified how institutions can share information on suspected fraud cases under Section 314(b). Eligible banks, credit unions, and other financial firms can now exchange data linked to illicit activity.

The update aims to remove uncertainty that previously slowed cross-institution cooperation. It also reinforces legal safe harbor protections for participating institutions. This clarification strengthens operational confidence for compliance teams handling real-time fraud alerts.

FinCEN said institutions may share cyber indicators such as IP addresses and login patterns. They can also exchange fraud signals including unusual payee additions and large transfers.

Video surveillance and identity mismatches were also listed as usable data points. These categories reflect broader digital and behavioral fraud detection techniques used in modern compliance systems.

The guidance reinforces voluntary participation in the 314(b) safe harbor program.

Authorities stressed that timely data sharing improves detection of money laundering and fraud networks. It also supports faster identification of coordinated criminal activity across accounts.

Participation remains optional but is strongly encouraged by regulators for systemic risk reduction.

Officials noted that fraud continues to drain significant value from consumers and businesses annually. The updated framework focuses on enabling quicker responses before illicit flows spread further.

Regulators said improved coordination remains central to financial system resilience. This approach prioritizes prevention rather than post-incident investigation.

Treasury Fraud Crackdown Links Institutions with Broader Crypto Monitoring Efforts

The Treasury Department framed the update within a broader fraud prevention initiative. It aligns with a task force focused on eliminating fraud across financial channels.

The effort includes coordination with federal banking agencies and enforcement bodies. It forms part of a wider national strategy to strengthen financial integrity systems.

Officials said financial crime increasingly overlaps with digital asset ecosystems. Banks and compliance teams often monitor transactions that intersect with crypto platforms.

Improved data sharing may help detect laundering patterns tied to digital asset flows. Regulators continue to examine risk exposure across both traditional and blockchain-based rails.

The guidance emphasizes rapid communication between institutions during suspicious activity events.

Faster exchange of indicators can help prevent fraud from spreading across multiple accounts. This reduces delays that criminals often exploit in fragmented reporting systems.

Speed of coordination remains a key variable in effective fraud disruption.

FinCEN also highlighted modernization of anti-money laundering frameworks. The shift moves toward risk-based supervision and more efficient resource allocation.

Institutions are encouraged to focus on high-risk activity rather than low-risk accounts. This adjustment aims to improve enforcement precision while reducing compliance burden.

Anthropic said it has suspended access to its Fable 5 and Mythos 5 AI models after receiving a U.S. government export control directive tied to national security concerns. The company disabled access for all users, including foreign nationals, effective immediately after it received the order at 5:21 p.m. ET on Friday.

In a statement posted on its website, Anthropic said the directive instructed it to suspend “all access” to Fable 5 and Mythos 5 by any foreign national, regardless of whether they are located inside or outside the United States. The company also said its other models, such as Opus 4.8, are not affected by the order.

Key takeaways

- Anthropic suspended global access to Fable 5 and Mythos 5 after a U.S. export control directive citing national security concerns.

- The order was received at 5:21 p.m. ET and required the company to halt access “by any foreign national,” including foreign national employees.

- Other Anthropic models, including Opus 4.8, are reported as unaffected.

- Anthropic says the government provided only verbal evidence of a narrow, non-universal jailbreak risk.

- The company disputes the premise that such a finding should trigger a recall-style response for models used at large scale.

Export-control order forces worldwide suspension

According to Anthropic, the directive it received compelled the company to remove access to Fable 5 and Mythos 5 for all users. Anthropic said it acted abruptly to comply with the government’s legal instruction and ensure the directive’s requirements are met.

While the company did not provide additional details in the statement about the specific nature of the alleged threat, it said it understands authorities are concerned about a potential “jailbreak” method that could bypass the models’ safeguards.

What Anthropic says the government’s concern is

Anthropic characterized the government’s evidence as limited and not universal in scope. The company said the government did not provide detailed technical information but instead offered “verbal evidence” of a potential narrow, non-universal jailbreak. Anthropic described that type of jailbreak as involving requests for the model to read a specific codebase and then fix software flaws found there.

In Anthropic’s framing, a non-universal jailbreak is fundamentally different from a “universal jailbreak”—the latter would enable broad, repeatable bypasses that work across many contexts. Anthropic argued that the alleged risk, as presented to the company, appears narrower than what would be required for a universal safeguard failure.

The company also expressed disagreement with treating a narrow, potential jailbreak as justification to roll back a frontier model that it said is deployed at very large scale. Anthropic argued that if the same threshold were applied industry-wide, it would effectively stop new frontier model deployments.

Timeline: new releases followed by compliance shutdown

The suspension came only days after Anthropic released Fable 5 and Mythos 5. The release followed the company’s earlier work with “Mythos Preview,” a general-purpose language model that Anthropic has previously said identified thousands of vulnerabilities in critical software.

Earlier coverage noted that Fable 5 and Mythos 5 were built on top of Mythos Preview and designed to demonstrate advanced capabilities, including security-relevant behaviors. The company’s current statement indicates that the export-control directive arrived in the middle of this rollout cycle, leaving Anthropic to disable access immediately rather than adjust the models incrementally.

Anthropic also said it believes the government’s order may stem from a misunderstanding and that it is working toward restoring access for users as soon as possible.

Why this matters beyond AI product access

For investors, developers, and users, the episode highlights how quickly geopolitics and compliance requirements can intersect with frontier AI deployment. Even when a company believes an identified risk is narrow and non-universal, a government directive can still force immediate operational changes—particularly when export-control rules are interpreted to cover access by foreign nationals.

The situation also underscores a practical tension in model governance: technical risk assessments can point to targeted mitigation, while legal directives may impose broad suspension measures to ensure compliance. Anthropic’s claim that other models are not affected suggests the company may be trying to isolate the impacted releases, but the pathway back to normal availability is uncertain and depends on the government’s engagement.

Going forward, market participants and AI users will likely watch for any update on what additional evidence or clarification the government provides, whether Anthropic can demonstrate that the risk is contained, and how quickly access can be restored to Fable 5 and Mythos 5 without repeating the compliance-triggering conditions.

Following last week’s market-wide calamity in which the cryptocurrency markets shed over $400 billion and all major assets plummeted to yearly lows, many analysts have started speculating on where the bottom is.

The latest to do so was Ali Martinez, who outlined the lowest targets during this cycle for BTC, ETH, and XRP. Hint: there’s more pain ahead for all, according to his findings.

Bitcoin Bottom

The analyst with over 165,000 followers on X began with the largest cryptocurrency by market cap, indicating that the asset is “approaching a market bottom.” He noted that the MVRV Pricing Bands suggest the ultimate capitulation zone, and that level has historically been around the 0.8 MVRV Band.

If history repeats itself, it would represent another major leg down that will drive BTC toward $43,000. The other, less painful option would be a nosedive to the 1.0 MVRV Band, which is currently at $54,000.

Interestingly, another recent analysis on BTC’s potential bottom suggested that it could arrive during the ongoing World Cup in North America. BIT Research justified their prediction with bitcoin’s A-B-C structure it has been following since the October 2025 rejection and subsequent bear market.

ETH Major Decline

While the leg down for bitcoin could see a more modest 32% drop from the current levels to bottom out, ETH’s projected crash is a lot worse. Basing his analysis on Ethereum’s Delta Price model, which measures the relationship between investor cost basis and miner production costs, Martinez warned that the largest altcoin can plummet to $700.

This level has “consistently flagged generational accumulation floors.” If such a major decline indeed transpired, then ETH will dump by another 60%. Moreover, its crash from last year’s all-time high at almost $5,000 would be north of 85%, which will be ‘shitcoin’ territory.

XRP Bottom Closeby

The landscape for ETH seems the most grim given Martinez’s projections. XRP, on the other hand, might be a lot closer to his targeted bottom. He noted that a dominant rising trendline on the monthly chart has “successfully defined every major cycle bottom for nearly a decade.”

If XRP is to find its bottom again there, it could drop to somewhere between $0.70 and $0.90. The lower target would mean a 40% decline, while the higher one is only 21% away from XRP’s current price tag of around $1.15.

5/5 If these projections fully mature, I will be executing a heavy spot-layering strategy directly inside these deep-value windows:$BTC: $43,200$ETH: $700$XRP: $0.90

Pacing capital at these levels keeps the portfolio aligned with structural-cycle data.

— Ali Charts (@alicharts) June 12, 2026

The post BTC vs. ETH vs. XRP: Which Is Closest to a Major Reversal? Analyst Explains appeared first on CryptoPotato.

TLDR:

- CFTC sues New Mexico over attempts to apply state gaming laws to derivatives markets

- KalshiEX case triggers wider jurisdiction clash between federal and state regulators in US markets

- CFTC cites Commodity Exchange Act as basis for exclusive authority over event contracts nationwide

- Multiple US states now challenge prediction markets, raising regulatory uncertainty across the sector

The Commodity Futures Trading Commission has filed a federal lawsuit against New Mexico over jurisdictional authority on prediction markets. The CFTC argues the state is attempting to apply gaming laws to federally regulated derivatives platforms.

New Mexico previously targeted CFTC-registered KalshiEX, escalating tensions between state and federal oversight. The dispute centers on whether states can regulate event contracts already covered under federal law.

CFTC New Mexico Lawsuit Over Prediction Markets Jurisdiction

The CFTC New Mexico lawsuit was filed in federal court in Washington, marking a direct challenge to state-level enforcement actions. The agency seeks to block New Mexico from applying gaming statutes to CFTC-registered contract markets.

According to the filing, federal law grants the commission exclusive authority over derivatives trading venues. The CFTC also requested declaratory relief and a permanent injunction.

New Mexico had earlier filed its own case in state court against KalshiEX LLC.

The state alleged the firm’s prediction markets function as unlawful online sports betting platforms. It also argued the company was attempting to bypass state gaming regulations. That action triggered the federal response from the CFTC.

At the center of the dispute is the Commodity Exchange Act. The law gives the CFTC exclusive jurisdiction over designated contract markets and event contracts.

The commission argues this framework preempts conflicting state gaming laws. It maintains that only federal regulators can oversee such derivatives activity.

CFTC Chairman Michael Selig defended the agency’s position in a statement tied to the filing. He said the state’s approach conflicts with established legal precedent and federal authority.

The commission reiterated that it will continue defending its jurisdiction over commodity derivatives markets.

KalshiEX and Expanding State Challenges in Prediction Markets

The CFTC New Mexico lawsuit is part of a broader wave of state actions targeting prediction markets.

Similar disputes have emerged in Arizona, Connecticut, Illinois, New York, Minnesota, Rhode Island, and Wisconsin. These cases generally focus on whether event-based trading resembles sports wagering. The CFTC has consistently rejected that framing.

KalshiEX sits at the center of the regulatory friction. The platform offers event contracts that allow users to trade on outcomes of real-world events.

States argue these products resemble gambling instruments. The CFTC classifies them as federally regulated derivatives.

The federal agency is seeking to prevent states from enforcing laws that could restrict CFTC registrants. It argues that fragmented regulation would undermine national market consistency. The lawsuit requests a court ruling affirming federal exclusivity. It also seeks to block state interference moving forward.

Market operators now face growing legal uncertainty as jurisdictional lines tighten.

The outcome of the CFTC New Mexico lawsuit could shape how prediction markets expand in the United States. It may also define how far states can extend gaming laws into federally governed financial instruments.

Crypto search interest is rising again in June, according to Alphractal data, as retail investors appear to be paying closer attention to digital assets after months of weaker activity.

Summary

- Crypto searches rose again in June as retail investors started tracking digital assets more actively.

- Alphractal said search spikes often appear during moments of market euphoria and fear.

- Rising crypto search interest shows attention is returning, but it does not confirm fresh buying.

Crypto searches rise again in June

Alphractal said Google searches for cryptocurrencies are increasing in June. The analytics platform described the move as a sign that retail investors are starting to search more about different crypto assets again.

“Google searches for cryptocurrencies are rising again in June,” Alphractal said.

The move comes after a quieter period for digital asset interest. Search activity often drops when prices move sideways or when retail traders leave the market after heavy volatility.

Alphractal also noted that Google Trends spikes are not always bullish. Search jumps can appear during strong rallies, but they can also happen when traders react to fear, crashes, or uncertainty.

Retail attention returns to crypto

The latest rise suggests that crypto is moving back into retail focus. More users are searching for coins, market direction, and exchange-related terms as the market tries to stabilize.

Search activity is often used as a soft sentiment gauge. It does not show actual buying, but it can show when retail investors start watching the market again.

As previously reported by crypto.news, Bitcoin search interest reached 12-month highs during 2026 volatility. That report noted that fear-driven searches do not always mean new buyers are entering the market.

The same report also said small holders were still selling while whales were accumulating. That means renewed attention must be separated from real capital inflows.

Bitcoin volatility drives interest

Bitcoin’s price action has remained one of the main drivers of crypto searches. The asset traded near the low $60,000 area in June after a deep pullback from its 2025 record high.

Sharp price moves tend to pull retail users back into search engines. Some look for dip-buying chances, while others search because they fear deeper losses.

The recent search rise follows a period when broad crypto attention had dropped sharply. As reported earlier this month, global search interest for “crypto” had fallen to one-year lows earlier in 2026.

That earlier drop showed how much retail attention had weakened even while institutions, ETFs, and treasury buyers played a larger role in the market.

Search data gives mixed signals

The return of search activity can help market watchers track sentiment, but it does not confirm a full retail comeback. Stronger proof would require higher retail trading volume, new exchange deposits, and small-holder accumulation.

For now, the data shows that crypto is gaining attention again. It also shows that traders are reacting to volatility after months of weaker interest.

Search spikes can appear near both tops and bottoms. That makes them useful for tracking emotion, but less reliable as a standalone price signal.

The key question is whether June’s rise turns into sustained participation. If searches keep climbing alongside stronger spot demand, retail activity may become a larger force in the market again.

Michael Saylor defended Strategy’s small Bitcoin sale at BTC Prague, saying the move did not change the company’s long-term Bitcoin position.

Summary

- Strategy sold 32 BTC for $2.5 million to fund preferred stock dividend payments due June.

- Saylor said his never-sell advice targeted individual holders, not corporate treasury management decisions at Prague.

- Strategy later bought 1,550 BTC, lifting current reserves to 845,256 Bitcoin after the sale disclosure.

Michael Saylor addressed Strategy’s 32 BTC sale during an appearance at BTC Prague on June 11. The comments followed criticism from traders who questioned the sale after years of “never sell” messaging around Bitcoin.

Strategy sold 32 BTC between May 26 and May 31 for about $2.5 million. The sale came at an average price of $77,135 per coin and marked the company’s first disclosed Bitcoin sale since December 2022.

“I said to YOU never sell your bitcoin,” said Michael Saylor at BTC Prague.

The remark drew attention because Saylor separated personal investor advice from corporate treasury actions. His response framed the sale as a company-level funding decision, not a change in Bitcoin conviction.

Strategy sold BTC to fund dividends

Strategy’s June 1 filing showed that proceeds from the Bitcoin sale were expected to support preferred stock distributions. The board had declared June 30 cash dividends across its preferred share series.

Those obligations include payments tied to STRF, STRC, STRE, STRK, and STRD. The STRC dividend for June carried an annual rate of 11.50%, according to the company filing.

The sale represented only about 0.0038% of Strategy’s Bitcoin balance at the time. That made the transaction small compared with the company’s overall treasury, but it carried more weight because of Saylor’s public messaging.

As previously reported by crypto.news, Strategy’s 32 BTC sale raised debate because the company had built its identity around long-term Bitcoin accumulation. The report noted that the sale was small in size but large in market attention.

Strategy later resumed Bitcoin buying

Strategy later bought 1,550 BTC between June 1 and June 7 for $101.3 million. The company paid an average price of $65,332 per coin and lifted its total Bitcoin reserve to 845,256 BTC.

The purchase was nearly 50 times larger than the 32 BTC sale. It also came as Strategy increased its U.S. dollar reserve by $100 million to $1 billion.

The new purchase eased some concerns over whether Strategy had moved away from accumulation. The same update showed that the company used proceeds from its at-the-market share program to fund the purchase and rebuild cash reserves.

Strategy’s dashboard now lists 845,256 BTC at an average acquisition price of $75,680. That keeps the company as the largest public corporate Bitcoin holder by a wide margin.

Dividend model remains in focus

The debate now centers on how Strategy funds future obligations. Preferred stock dividends create recurring cash needs, while Bitcoin remains the main asset on the company’s balance sheet.

Saylor’s comments suggest that Strategy may separate personal Bitcoin advice from corporate liquidity management. That approach leaves room for limited sales when the company has dividend or financing needs.

Investors will watch the June 30 dividend date for more clues. The key question is whether Strategy uses cash reserves, capital markets, or small Bitcoin sales to meet future payments.

The company’s latest purchase shows that Strategy remains a net Bitcoin accumulator for now. Still, the 32 BTC sale has changed how some traders read the company’s “never sell” message.

World Cup co-hosts US thrash Paraguay in dominant Group D opener

Maine disables data breach notification portal after fake disclosures

Wayne Rooney in live TV clash with BBC colleague as Gabby Logan addresses ‘heat’ in studio

-

NewsBeat5 days ago

NewsBeat5 days agoAlexander Zverev wins the French Open to finally earn a 1st Grand Slam title

-

Entertainment6 days ago

Entertainment6 days agoThe Best Mystery Series of All Time Is Surging on Streaming 30 Years After It Ended

-

Crypto World5 days ago

Crypto World5 days agoAnatomy of the June crypto crash: Fed, Iran, Saylor

-

Crypto World2 days ago

Crypto World2 days agoOppenheimer backs SpaceX as $70 billion retail frenzy builds

-

Crypto World2 days ago

Crypto World2 days agoMarkets Rally as SpaceX IPO Looms Amid Iran Tensions and Inflation Surge

-

Crypto World7 days ago

Senator Cynthia Lummis Calls CLARITY Act the Most Consequential Financial Legislation of This Generation

-

NewsBeat6 days ago

NewsBeat6 days agoAlexander Zverev conquers demons and outlasts Flavio Cobolli to win French Open for first major title

-

Tech6 days ago

Tech6 days agoMicrosoft unveils seven homegrown AI models in new bid for ‘long term self-sufficiency’

-

Business5 days ago

Business5 days agoHigh Stakes for Wembanyama as New York Pushes for 3-0 Lead

-

Tech5 days ago

Tech5 days agoNotion restores access to Anthropic after service disruption

-

Business6 days ago

Business6 days agoThe Pain Points Taking a Fragile Tech Rally Down a Notch

-

Crypto World5 days ago

Crypto World5 days agoEli Lilly (LLY) Stock Surges 4% Following Breakthrough Sleep Apnea Trial Results

-

Business6 days ago

Business6 days agoThe investment to transform historic St Helen’s ground in Swansea

-

Crypto World6 days ago

Crypto World6 days agoTrump’s AI Ownership Plan Could Benefit Anthropic at OpenAI’s Expense

-

Business7 days ago

Business7 days agoForensic Expert Floats Handyman Theory in Disappearance of Savannah Guthrie’s Mother

-

Sports4 days ago

Sports4 days agoBangladesh beat Australia after 20 years in ODIs, register only their second win over six-time world champions | Cricket News

-

Tech7 hours ago

Tech7 hours agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Tech17 hours ago

Tech17 hours agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

Politics2 days ago

Politics2 days agoPolitics Home | Healey Resignation Is “Colossal Failure Of Government”, Says Former Labour Defence Secretary

-

Sports2 days ago

Sports2 days agoFirst Time Since 1971: Australia Register Historic Low In ODI Cricket

You must be logged in to post a comment Login