Crypto World

XRP ETF inflows surge as network activity hits March highs

XRP Ledger activity rose sharply after XRP briefly moved above $1.54 for the first time in two months, according to Santiment data shared on May 16.

Summary

- XRP network activity hit two-month highs after price briefly reclaimed levels last seen in March.

- Spot XRP ETFs logged $60.50 million weekly inflows, their strongest week since late December 2025.

- ETF demand failed to hold the breakout as XRP slipped back below key resistance again.

The analytics firm said active addresses reached 48,453, the highest level since March 30.

Santiment also reported 3,317 new network addresses, the highest reading since March 19. The firm said part of the move came from “general price FOMO,” but added that more transactions can support mid- and long-term growth when activity reflects real adoption.

Spot XRP ETFs also recorded a strong inflow week. SOSoValue data showed $60.50 million in net inflows for the week, the strongest reading since the week ending Dec. 26. May inflows reached nearly $95 million, already above April’s total.

Crypto.news had already reported a rebound in XRP ETF demand before the latest weekly data. U.S. spot XRP ETFs posted $25.8 million in daily net inflows on May 11, the strongest single-day total since Jan. 5.

XRP breakout fails near resistance

XRP tried to extend its rally after ETF inflows improved and the CLARITY Act advanced in Washington. As crypto.news previously reported, Standard Chartered expected $4 billion to $8 billion in additional XRP ETF inflows if the CLARITY Act moved through the Senate Banking Committee before May 21.

The move did not hold. XRP pushed into a familiar resistance zone before retreating. Crypto.news data showed Ripple’s native token (XRP) trading around $1.42, with a market cap near $87 billion, placing it behind BNB among major crypto assets.

Moreover, the latest ETF streak follows a strong April. Crypto.news reported that XRP ETF products pulled in $81.63 million during April, making it their best inflow month of 2026. The figure reversed March’s $31.16 million monthly outflow.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

On July 7, 3 weeks after the largest IPO in history, SPCX enters the Nasdaq-100 with billions in passive index buying behind it. The more interesting market is the one Wall Street does not run: tokenized shares on Solana, perpetual futures that priced the listing before bankers did, a $557 million subscription campaign that had to refund almost everyone, and 18,712 Bitcoin sitting on the rocket company’s balance sheet.

Summary

- SpaceX’s Nasdaq-100 entry will bring estimated passive buying while crypto markets already trade its exposure around the clock.

- Tokenized shares, tracker products, and perpetual futures turned SPCX into a live test of equity trading on crypto rails.

- The SpaceX cycle exposed both the promise and risks of tokenized markets, from global access to failed allocations and liquidations.

Index inclusions are usually the sleepiest events in finance. A committee updates a list, passive funds rebalance, and the market moves on. SpaceX joining the Nasdaq-100 before the open on Tuesday, July 7, is not sleepy, partly because the company only went public on June 12 and partly because the estimated $4.3 billion in passive buying tied to the inclusion is arriving into one of the strangest market structures any stock has ever had.

SpaceX, ticker SPCX, is the first mega-cap whose entire public life has run in parallel on crypto rails. Its valuation was traded around the clock for weeks before the IPO priced. Its shares exist simultaneously as Nasdaq stock, as redeemable tokens on Solana, as tracker certificates on half a dozen exchanges, and as cash-settled perpetual futures that liquidated more than $50 million in positions during one bad 48-hour stretch. Its balance sheet holds 18,712 Bitcoin. And when the index funds start buying on Tuesday morning, a meaningful part of the price discovery will already have happened overnight, on-chain, while the exchange was closed.

This is what it looks like when the market structure conversation stops being theoretical. Here is the full map of the SpaceX trade, and what Tuesday tests.

The listing that broke records and brokers

The numbers behind the underlying event deserve a restatement, because everything else sits on top of them. SpaceX sold 555.6 million Class A shares at $135 on June 12, raising $75 billion, the largest initial public offering in United States history, at a valuation near $1.75 trillion. Goldman Sachs led the syndicate alongside Morgan Stanley, Bank of America Securities, Citigroup, and JPMorgan. The company dual-listed on Nasdaq’s Texas exchange under the same ticker, and in a sharp break from mega-cap convention, allocated 30% of the offering to retail investors instead of the usual sliver near 10%.

The stock opened at $150, traded as high as the mid-$160s, and then did what heavily hyped listings often do: it came back down, slipping below its opening price in late June during the broader market drawdown, leaving buyers above the $135 offer price with a live lesson in post-IPO volatility. The first public earnings report lands in September, and the first quarterly disclosure period, ending June 30, has just closed.

One filing detail turned the listing into a crypto story on its own. SpaceX’s registration statement disclosed 18,712 BTC on the balance sheet, acquired back in 2021 at a cost basis of roughly $661 million and worth around $1.2 billion at recent prices. As a public company, SpaceX now reports that position, its cost basis, and its fair-value changes every quarter, joining the small club of corporates whose earnings calls double as Bitcoin disclosures. The June market slide made that holding a talking point immediately, with analysts noting that the $75 billion raise itself competed for the same pool of risk capital that had been holding up crypto prices.

The perpetuals that front-ran the bankers

The most consequential crypto layer of the SpaceX trade started weeks before the stock existed. On May 18, the builder TradeXYZ deployed a pre-IPO perpetual futures market for SpaceX on Hyperliquid under the ticker xyz:SPCX, using the HIP-3 framework that lets outside builders launch perpetual markets on the chain.

Centralized exchanges followed with their own contracts, and by listing day the pre-IPO complex had processed $3.2 billion in volume across 8 venues with open interest peaking above $390 million, including more than $190 million on Hyperliquid alone before the Nasdaq open.

What makes those markets more than a curiosity is how well they priced the event. Aggregated pre-IPO contracts traded at a volume-weighted average near $155 in the final stretch against the $135 offer price, and closed the pre-listing period at an average of $157, within 4.7% of the $150 opening print. The precedent held from the Cerebras listing months earlier, where the equivalent contract landed within 1.3% of the opening price. Synthetic, around-the-clock markets built on crypto infrastructure produced a credible forecast of where one of the most oversubscribed offerings in history would open, while the traditional book-building process kept that information inside the syndicate.

The same markets also delivered the cautionary chapter. Once Nasdaq trading began, the contracts converted into standard equity-linked perpetuals using the live stock price as an oracle, and when SPCX slid below its $150 opening level in late June, leveraged longs paid for the enthusiasm: more than $50 million in SPCX perpetual liquidations in 48 hours, a total that briefly ranked the contract behind only Bitcoin and Ethereum among crypto derivatives. A perpetual future on a stock inherits crypto’s speed in both directions, and the liquidation engine does not wait for an opening bell.

Four things called SpaceX exposure, one of them actual stock

The tokenized layer is where the SpaceX trade turned into a market structure exam that much of the industry failed. By late June, a retail buyer reaching for SpaceX exposure through crypto could end up holding four legally distinct instruments, and the differences only became obvious under stress.

The first is the real thing: a Nasdaq share, whether through a traditional broker or through exchange offerings that route whole-share orders to an introducing broker with standard clearing. Real equity, real shareholder claim, real trading halts.

The second is the redeemable token. Backpack Securities issued a Solana-native SpaceX token backed 1:1 by actual shares in regulated custody, redeemable into the underlying equity and transferable to a conventional brokerage. Ondo launched its own 1:1 tracker on Ethereum and Solana with daily custody attestations. These are the instruments the tokenization thesis has been promising: the stock, wrapped, portable, and trading around the clock.

The third is the tracker certificate. The xStocks product, launched by Kraken parent Payward and distributed across exchanges including Bybit, delivers price exposure through bearer debt instruments with no shareholder rights, no voting, and no legal claim on the underlying shares, and its own terms allow the collateral behind them to be assets other than the stock itself. It is exposure, not ownership, and the paperwork says so for anyone who reads it. Payward has spent 2026 planting flags across mainstream finance, from tokenized equities to its FIFA World Cup sponsorship, and xStocks is the ambitious middle of that portfolio.

The fourth is the perpetual, which owns nothing at all and tracks the price purely through funding mechanics.

The stress test arrived before the stock did. Binance Wallet ran a tokenized subscription campaign for SpaceX exposure through xStocks that raised $557 million from 27,689 wallet addresses, one of the largest tokenized offering campaigns ever, with Bybit running a parallel program. Then the supply failed to show up: the xStocks provider received a smaller pre-IPO share allocation than expected, and Binance, Bybit, and Bitget canceled customer allocations and refunded in full, with Binance distributing a consolation $1 million in shares through its newer bStocks platform. The fine print had warned that allocations were not guaranteed, and the fine print won. Tokenization can wrap a share, but it cannot conjure one, and the biggest tokenized IPO campaign in history ended as a refund notice.

None of that stopped the sector’s growth. Tokenized stock volumes hit a record $20 billion during the SpaceX cycle, pre-IPO tokenized trading volume surged over 1,000%, and tokenized equities as a category kept compounding, with Citi projecting tokenized real-world assets to grow from around $17 billion today to $5.5 trillion by 2030. SpaceX was simultaneously the category’s best advertisement and its most public quality-control failure.

How a market for a private company actually works

Since pre-IPO perpetuals are about to become a fixture of every major listing, the mechanics deserve a proper walkthrough, because the instrument is stranger than its chart suggests.

A perpetual future normally needs a reference price to anchor its funding mechanism: longs pay shorts when the contract trades above the index, shorts pay longs below it, and the payments tether the derivative to the underlying. A private company has no underlying. The pre-IPO contracts solved this by letting the funding mechanism anchor to itself, with the contract price representing the market’s continuously updated estimate of the eventual listing value, disciplined by traders willing to take the other side of any drift. It is price discovery with no ground truth until listing day, which sounds like astrology and behaved like arbitrage.

The Cerebras listing was the controlled experiment. The chipmaker’s pre-IPO perpetual traded for weeks before its Nasdaq debut, and when the stock opened, the contract’s final pre-listing price sat within 1.3% of the $350 opening print. Spreads on the contract compressed to a 0.07% median once the live stock price became the oracle, and open interest rolled off in an orderly unwind as positions reconciled against reality. The experiment answered the core objection to synthetic pre-IPO markets, that with no underlying to arbitrage they would drift into fantasy, with a data point: they did not.

SpaceX ran the experiment at 40 times the size. The Hyperliquid contract launched on May 18 with the IPO reference at $135, and the market immediately priced the company richer, clustering between $180 and $200 in the first weeks, an implied valuation near $2.5 trillion that said more about scarcity hunger than fundamentals. Then something instructive happened: as the roadshow progressed and allocation details leaked, the contracts converged, sliding into the $160 to $170 range by June 8 and settling near $155 aggregate VWAP into listing week. The synthetic market did not just guess; it updated, absorbing information through the exact process equity analysts describe as price discovery, running around the clock on rails the syndicate did not control.

At listing, the contracts flipped their oracle to the live Nasdaq price and became ordinary equity-linked perpetuals, which is where the second lesson arrived. An around-the-clock leveraged derivative on a stock means the stock effectively trades around the clock too, with all of crypto’s liquidation mechanics attached. When SPCX broke below $150, the cascade cleared more than $50 million in 48 hours, forcing exits firing at 3 a.m. against a reference asset whose actual venue was closed. Equity investors got their first taste of a dynamic crypto traders know in their bones: in a leveraged 24-hour market, the price you are liquidated at and the price the asset deserves are frequently different numbers, and only one of them empties your account.

The regulatory seam running through everything

Every layer of the SpaceX crypto complex operates around a single inconvenient fact: most of it is unavailable to Americans, on purpose.

The tokenized products draw the sharpest lines. xStocks excludes users from the United States, the United Kingdom, Canada, and Australia outright. Ondo’s tracker is for non-United States users. Backpack’s redeemable token operates through securities registrations that carefully fence its distribution. The pattern is uniform because the legal exposure is: a tokenized share offered to a United States retail investor is a securities offering, and nobody in the stack wants to run that experiment ahead of legislation. The result is an inverted access map, where a trader in Lagos or Manila can hold around-the-clock SpaceX exposure through a phone wallet while a trader in Ohio needs a brokerage account and market hours, for a company whose rockets launch from Texas and Florida.

The perpetuals live in the same seam. The offshore exchanges listing SPCX contracts exclude United States persons as a matter of stated policy, with all the enforcement rigor that phrase historically implies, and the domestic regulated path for equity perpetuals is still being fought over between the CFTC and the exchanges. Meanwhile, the pending market structure legislation grinding through the Senate would redraw several of these lines at once, which is why every player in the tokenized stock complex is building now and lobbying simultaneously: the rails that exist when the rules finalize tend to get grandfathered into legitimacy, and the ones that do not get built never do.

The seam also explains the industry’s strange incentive alignment around Tuesday. A clean, liquid, boring index inclusion, with the tokenized layer tracking faithfully and no structural embarrassments, is a lobbying exhibit for the entire sector. A blowup is an exhibit for the other side. Rarely has a passive rebalancing event carried this much narrative weight for people who do not own the stock.

What Tuesday actually tests

The Nasdaq-100 inclusion, effective before the market opens on July 7, is mechanically simple: index-tracking funds led by the QQQ complex must hold SPCX, and the estimated $4.3 billion in passive demand tied to that rebalancing arrives on a schedule everyone can see. The flow is not new money deciding it likes rockets; it is rule-following capital buying whatever the index says, funded by trimming whichever component fell out of the top 100, which is why inclusion effects are usually front-run, faded, and forgotten within a week. The wrinkle this time is that the front-running venues never close. The same June liquidity squeeze that drained a record $4 billion from Bitcoin ETFs while whales accumulated on-chain showed how sharply passive flows and conviction flows can diverge; Tuesday runs that experiment inside a single ticker. For a normal stock, the interesting question is how much of the flow is already priced in. For this stock, there are three better questions.

First, where does the price discovery happen? The inclusion takes effect at the open, but the tokenized shares and the perpetuals trade through the weekend and overnight. Whatever the market decides about the inclusion will be visible on-chain hours before the first Nasdaq print on Tuesday, the same way the pre-IPO perps front-ran the offer price. Index events used to be a bell-to-bell affair. This one has a 24-hour shadow market attached, and the arbitrage between the two is now a professional trade.

Second, does the passive bid meet the leveraged crowd? SPCX perpetual open interest rebuilt after the June flush, and a scheduled, well-telegraphed buying event is exactly the setup that attracts leverage on both sides. The last time the stock moved sharply, the liquidation cascade outpaced anything the equity market itself did. A calm inclusion would be a small landmark for the tokenized complex; a violent one would be a reminder that bolting crypto market structure onto a stock imports crypto’s failure modes along with its hours.

Third, does the index bid revalue the Bitcoin on the books? Passive funds buying SPCX are, at one remove, buying 18,712 BTC without an opinion about it, the same way index investors have been buying corporate Bitcoin treasuries through other tickers for years. It is a small position against a $1.7 trillion company, but the symbolism runs the other direction: Bitcoin exposure is now something the Nasdaq-100 carries by default, embedded in a rocket company, disclosed quarterly, and owned by every retirement account tracking the index.

The precedent being set in real time

Step back from the ticker and the SpaceX cycle reads like a preview of how every major listing will eventually work. A company’s valuation now starts trading the moment the market cares, not the moment a syndicate allows it. The pre-IPO perps priced SpaceX within a few percent while the roadshow was still running. The tokenized wrappers extended the stock into jurisdictions and hours the exchange cannot reach, the same premise Robinhood just built an entire blockchain around. The failures were real, from the xStocks allocation collapse to the liquidation cascade, but they were failures of capacity and leverage, not of the premise.

The IPO pipeline behind SpaceX makes the preview matter. OpenAI and Anthropic perpetuals already trade the same way SPCX did in May, meaning the market is currently pricing companies that have not filed anything, continuously, with open interest in the hundreds of millions. Whenever those listings arrive, the crypto layer will not be an afterthought bolted on for retail access. It will have been the market of record for months, with the exchange listing arriving as the settlement event that reconciles everyone’s positions.

The retail geography of the trade is the part traditional finance keeps underestimating. SpaceX allocated 30% of its offering to retail, an unprecedented share for a listing this size, and the tokenized layer extended that populism to jurisdictions the allocation never reached: on-chain SPCX products let buyers in more than 100 countries take positions from a phone, in fractions, at any hour, with no brokerage relationship. The demand was not hypothetical. The pre-IPO tokenized trading complex grew over 1,000% in volume during the SpaceX cycle, the Binance Wallet campaign alone pulled in $557 million of subscription demand from under 28,000 wallets, and the perpetuals cleared billions from traders who could never have participated in the actual book. Whether regulators read that as democratized access or as an unlicensed parallel offering is precisely the fight the next 2 years of market structure policy will settle, and SpaceX supplied both sides with their best evidence.

There is also a quieter institutional lesson in how the instruments behaved relative to each other. Through the June volatility, the redeemable tokens tracked the stock tightly because arbitrageurs could actually redeem them, the tracker certificates drifted on their own supply and demand because nobody could, and the perpetuals overshot in both directions because leverage always does. The dispersion between four instruments referencing one asset is a live measurement of how much each layer of trust costs, updated every minute, and desks have started trading the basis between the wrappers the way they trade the futures basis in any mature market. Market structure people call this the instrument stack finding its pricing; everyone else calls it confusing, and both are right.

That inversion, crypto markets first and the stock exchange as confirmation, would have sounded absurd during the last cycle. On Tuesday morning, when the index funds show up to buy a stock whose weekend price action already happened on Solana and Hyperliquid, it will just be how the SpaceX trade works. The rocket company did not set out to become the test case for the merger of equity and crypto market structure. It became one anyway, because it was the biggest thing on the launchpad when the rails were finally ready, and markets, like rockets, use the heaviest available payload to prove the vehicle.

The score going into the open

The scoreboard so far: the perpetuals called the IPO price better than the commentary did, the redeemable tokens worked exactly as designed, the tracker certificates exposed the difference between exposure and ownership, the subscription campaigns found the hard limit of tokenized supply, and the leverage got punished on schedule. That is a remarkably complete stress test for a market structure that barely existed 2 years ago, administered by a single stock in 3 weeks.

Tuesday adds the last missing scenario, a scheduled institutional flow event, to the record. Whichever way SPCX trades, the more durable result is already in: the parallel market did not blink, did not halt, and did not wait for anyone’s opening bell. The index committee added a company to a list. The market around that company had already added itself to something bigger.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile, and you can lose your entire investment. Always do your own research. Information current as of July 4, 2026.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

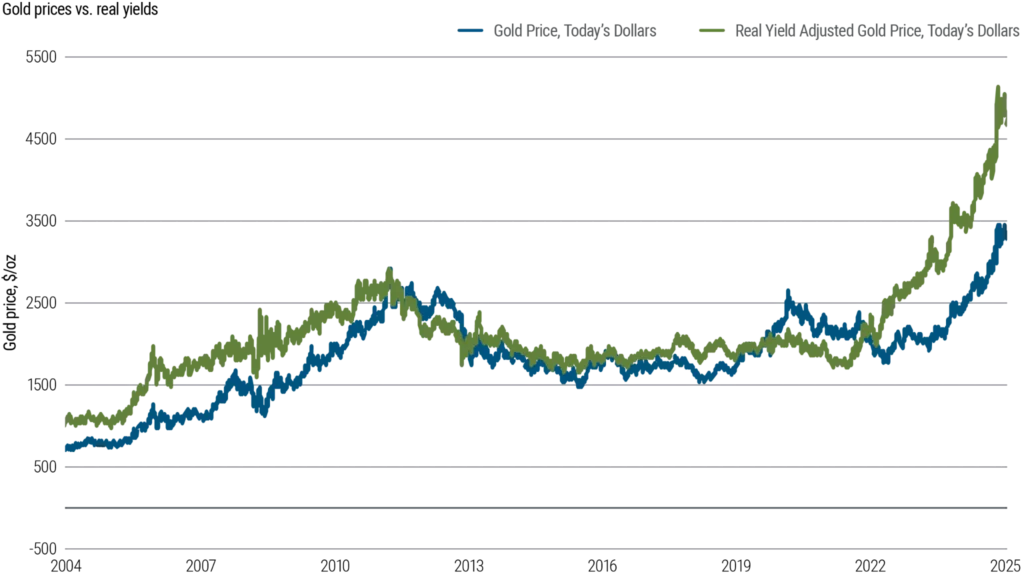

Gold’s modern market history reflects decades of price swings shaped by inflation, interest rates, central bank actions, and geopolitical events.

Summary

- Gold’s post-1971 history reflects decades of inflation, monetary policy, crises, and shifting investor sentiment.

- Gold prices have been shaped by inflation, central bank policies, and geopolitical events since leaving the gold standard.

- From Bretton Woods to the 2008 crisis, gold’s market history highlights the impact of macroeconomic and policy shifts.

In open markets, gold has only been on the free market for the last 50-some years. Until the month of August 1971, its value had been pegged at $35 per ounce under the Bretton Woods monetary system.

However, the Nixon administration gave up on dollar convertibility to gold, which put the metal into a market that it had not known in living memory. The history that ensued is one of the more instructive in the history of prices in modern finance, driven by oil shocks, conscious rate policy, concerted institutional action, and periodic crises not foreseen by most of the actors until they actually happened.

The 1970s: Gold’s first decade without a fixed price

There were no fireworks following the move to a market-determined price. However, inflation rates in the Western world rose dramatically during the 1973 Arab oil embargo, and the gold chart started to move in a decade-defining manner. The metal was up to nearly $195 per ounce by the end of 1974, a nearly fivefold increase in three years. In 1975, the U.S. government legalized private gold ownership for American citizens, which brought some profit-taking and halted the upward trend for a short while. But structural factors – weak dollar, high inflation and growing geopolitical tension – held strong.

In January 1980, gold hit $850.00 an ounce due to the Iranian Revolution, the Soviet invasion of Afghanistan, and a series of inflationary pressure events during the Carter administration. That would be the first time the level is not matched in real, inflation-adjusted dollars in more than 30 years, something that is often overlooked when people talk about the bull market of the 2000s just in nominal terms.

The 1980s and 1990s: Two decades of consistent decline

The period since gold peaked in 1980 has been one of the most instructive in recent gold history, not for any one event, but rather because of the persistent conditions that held gold prices down for 20 years.

The Volcker rate environment

Under Paul Volcker, the Federal Reserve hiked rates hard to squelch “embedded inflation”. This did work, but the environment, with real rates quite positive and a strengthening dollar bringing in capital to U.S. assets, was fundamentally not good for a commodity that did not yield. From 1980, gold dropped consistently and found a range of $300-$500 during most of the decade. This was not caused by any one factor but by a combination of macro factors that were unfavorable to the metal.

Institutional selling in the 1990s

Another big negative wind was the coordinated central bank selling in the 1990s. A number of European governments decided to cut their gold stocks because they were unproductive and produced no return. Known publicly in advance, the UK’s auction of 415 tonnes between 1999 and 2002 took place close to what proved to be multi-decade low prices and became a benchmark in reserve management debates, which still exist today. The larger picture of Europe’s institutional sell added to the pressures on prices.

The 1999 low and the Washington agreement

In 1999, gold was almost $252 an ounce at the bottom. The Washington Agreement on gold, negotiated by European central banks in September this year, contained annual limits on the volume of sales and assisted in stabilizing the cycle low. By this time, the sentiment on gold was universally negative, and as the next decade proved, this was a good contrarian indicator.

The pattern that defined this era

The 1980s and 1990s form a pattern that can be seen numerous times on the longer time frame. Gold was found to underperform when the following occurred at the same time:

- Interest rates were meaningfully positive for a considerable amount of time.

- General trust in the financial system and in equity markets was largely not affected.

- The U.S. dollar was structurally strong on a trade-weighted basis

- Institutional reserve holders were net sellers

This combination is not a mechanical rule, but it did occur with uncanny uniformity during two successive decades. It also shows why the lows of gold in the latter part of the 1990s (now appearing to be extraordinary) seemed to be reasonable for the times.

The 2000s: A new bull market, then a crisis that surprised both ways

Gold’s bounce from the 1999 low was subdued initially. The metal started to rise from about $270 per ounce in 2001. The dot-com bubble burst, bringing into doubt the valuation of equities; the events of 9/11 drove up geopolitical risk premiums in all markets, and the U.S. fiscal budget increased dramatically to pay for military operations outside the country. The general trend of a falling dollar was an underlying theme.

In 2007, gold reached $800 an ounce for the first time since 1980. Then the financial crisis of 2008 had a chain reaction, surprising many observers. gold was hit hard in the last few months of 2008 as institutions began to dump assets in all asset classes to recoup losses and satisfy redemptions, and gold was no different. But with monetary easing having begun globally and with several major central banks applying near-zero rates as well as large-scale asset purchases, real interest rates went deeply negative, and gold began to rise again with a vengeance. It was at about $1,920 per ounce by September 2011, more than seven times higher than the 1999 low.

The following table outlines the general price ranges and main factors for each decade:

Decade

Approx. Low

Approx. High

Key Driver

1970s

$35 (fixed, 1971)

$850 (Jan 1980)

Inflation, oil shocks, USD weakness

1980s

~$280

~$500

Positive real rates, disinflation

1990s

~$252 (1999)

~$415

Central bank selling, equity boom

2000s

~$270 (2001)

~$1,000 (2008)

Dollar weakness, financial instability

2010s

~$1,050 (2015)

~$1,920 (2011)

QE, then rate normalization

2020s

~$1,700 (2022)

$3,000+ (2025)

Pandemic, geopolitics, central bank buying

The 2010s: A steep correction and a gradual return

When it peaked in 2011, not many expected gold to fall so much and so far. The metal’s annual decline was its worst since 1981 after the Fed indicated it would begin to slow asset purchases, which sent real yields higher and took one of gold’s primary props out from under the market. As of December 2015, prices had dropped to approximately $1,050 per ounce. The mining industry balance sheets were seriously strained, and analysts were generally negative.

An adjustment from that trough was slow and took place due to a number of factors — partly the weaker geopolitical demand from Brexit uncertainty, the U.S.-China trade tensions, and the uncertainty surrounding some of the world’s larger economies, and partly due to a structural change in how central banks manage their reserves. Emerging market institutions also started to add gold to their holdings in amounts never again witnessed in the modern history of gold demand: gold purchases in the countries of the modern data series exceeded 1,000 tonnes per year for the first time in more than 55 years. By mid-2019, gold had made a comeback, trading well over $1,500 per ounce and reclaiming the ground lost over the years.

The 2020s: New records and more nuanced drivers

COVID-19 has changed the global monetary landscape quickly and dramatically and gold prices have reacted as such. The metal’s historical record indicated that conditions in the form of near-zero interest rates and large-scale fiscal stimulus programs and significant monetary expansion would be favorable for the metal. Gold’s intraday price in August 2020 breached the $2,000-an-ounce threshold for the first time in history, topping out at about $2,075.

The inflation surge and why gold’s response was muted

The price reaction to the surge in inflation in 2021 and its following years has been weaker than many observers expected and there’s a reason why. The link between gold and inflation is often misunderstood and misinterpreted in the media. The message of the longer history is that the metal has been a better indicator of real interest rates, that is, it tends to do best when the inflation is higher than the nominal yield and real interest rates are negative. The nominal rate environment in many markets changed when central banks responded aggressively in 2022-2023, lifting nominal rates above the rate of price increases. That offset also weighed on gold’s ability to rally despite the high levels of headline inflation, as the metal spent much of 2022 trading between $1,700 and $2,000.

From $2,500 to $3,000 and the current environment

Gold ventured into fresh nominal highs in late 2023 as rate expectations eased, geopolitical fragmentation continued, and the structural central bank buying by reserve holders wanting to unwind dollar-denominated holdings continued. It crossed $2,500 in 2024 and breached $3,000 per ounce in early 2025. Today, prices are still at historically high levels as of mid-2026. The share of gold in global foreign exchange reserves has been gradually improving in recent years and has turned the tide in the long-term structural deterioration of the precious metal’s share, as several major countries are actively diversifying their reserves away from dollar-dominated portfolios.

What the full 50-year chart actually reveals

There are 50 years of price data to provide context but not certainty. This chart doesn’t show a consistent cycle or a reliable formula to follow in the future, but it does show which conditions have been reliable indicators of a significant price move and which areas confident stories have consistently missed.

Historical factors that historically signal bull markets in gold are:

- When the real interest rate is very negative, that is when the nominal interest rate is less than the rate of meaningful inflation

- Widespread loss of trust in key financial institutions or money systems

- Structural, persistent dollar weakness (trade-weighted basis)

- Near-term crises with no immediate resolution prospects (geopolitical crises)

- A significant continuous net purchase from institutional reserve buyers

- Monetary expansion that brings up issues of long-term purchasing power of currency

- Increased uncertainty about statements of sovereign debt paths in key economies

Factors that have been a drag on the price:

- With positive real interest rates, yield-bearing assets have a clear competitive edge.

- Favorable and sustainable financial position and widespread trust in equities.

- A structurally strong dollar combined with contained and declining inflation

Important turning points in the 50-year history:

1971: Fixed pricing ends, market discovery of gold begins, $35

1980: $850 peak as a result of compounding crises and entrenched inflation

1999: Price bottoms near $252, and the bearish consensus is at its lowest ebb.

2011: $1920 – end of the second major bull run with monetary conditions returning to normal levels.

2020: the first year to cross $2,000 in a pandemic environment

2025: Gold breaks through $3,000 and heads into new nominal space on structural and macro forces.

2026: Institutional demand for safe haven reaches an all-time high of $5,600.

History also reveals the challenges that have historically befallen overarching narratives. During the first stages of the crisis in 2008, gold gave back, just as it is usually considered a safe haven, and then rose when policy took action. Despite a strong inflation period in 2022, it still underperformed for much of the year. It fell over ten years for two decades, and recovery was called for each and every one, but the calls always proved to be premature.

Being honest about reading the 50-year chart means taking into account the periods when gold acted out of the ordinary and when it did what it was supposed to do. The price is a combination of financial policy, institutional flows, currency dynamics, and investor positions — all of which are interdependent and all of which are complex and cannot be summarized by a one-size-fits-all explanatory variable that is consistent through every time period.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

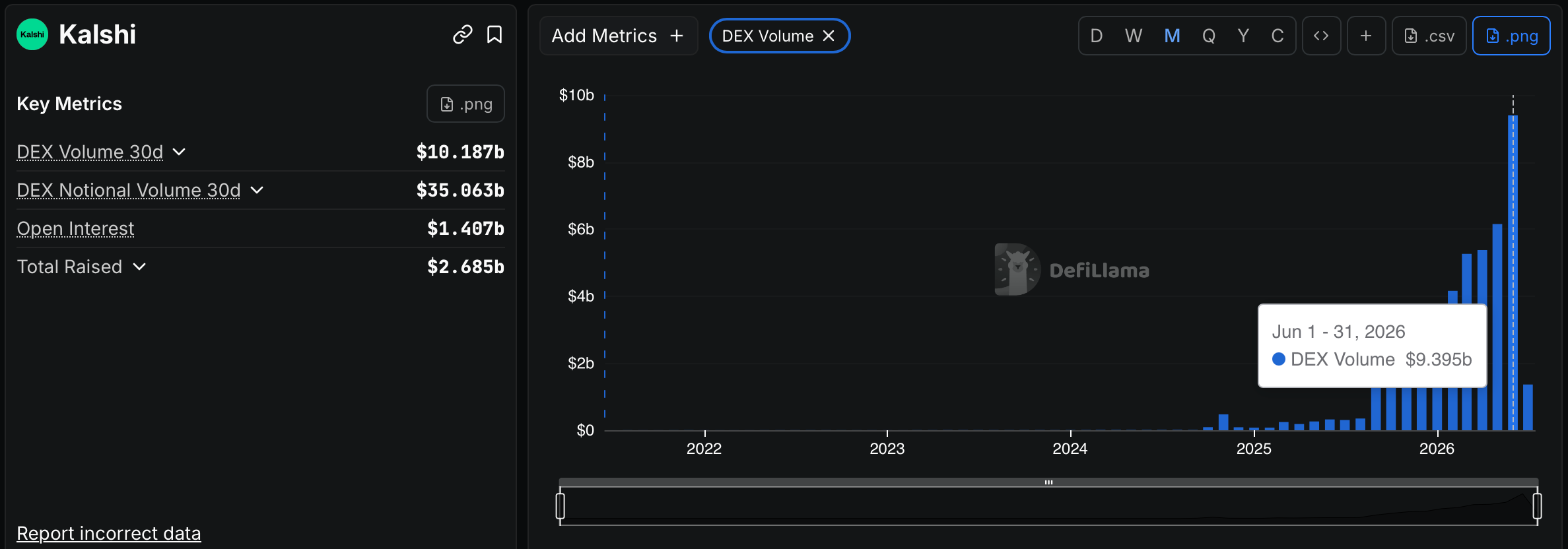

Prediction markets have found an unexpected new liquidity magnet: the 2026 FIFA World Cup. According to DefiLlama data cited by CNBC, trading volume surged across major US prediction platforms after the tournament began on June 11—at a time when the sector is simultaneously facing intensified regulatory pressure.

DefiLlama shows Kalshi handled nearly $9.4 billion in trading volume in June, up from about $5.3 billion in May. Polymarket International also rose to roughly $4.3 billion in June, compared with about $3.5 billion the month prior. CNBC reported that the World Cup became the biggest driver of prediction market volumes in June, with Dune Analytics highlighting record notional trading activity on both Kalshi and Polymarket.

Key takeaways

- Kalshi’s June trading volume nearly hit $9.4 billion, rising from about $5.3 billion in May, as World Cup activity accelerated.

- Polymarket climbed to about $4.3 billion in June from roughly $3.5 billion in May, also pointing to the tournament as a major catalyst.

- High-stakes World Cup knockout matchups are generating tens of millions in daily volume on both exchanges, with some fixtures surpassing $48 million on Kalshi.

- The growth is unfolding alongside escalating US legal and regulatory disputes over whether prediction markets should fall under federal derivatives authority or state gambling frameworks.

World Cup liquidity floods prediction platforms

The jump in activity aligns with the tournament’s expanded format. The 2026 World Cup is the first FIFA edition featuring 48 teams, up from 32 previously. That increase has effectively created more matches, more outcomes, and more trading opportunities—especially around qualification and match advancement markets.

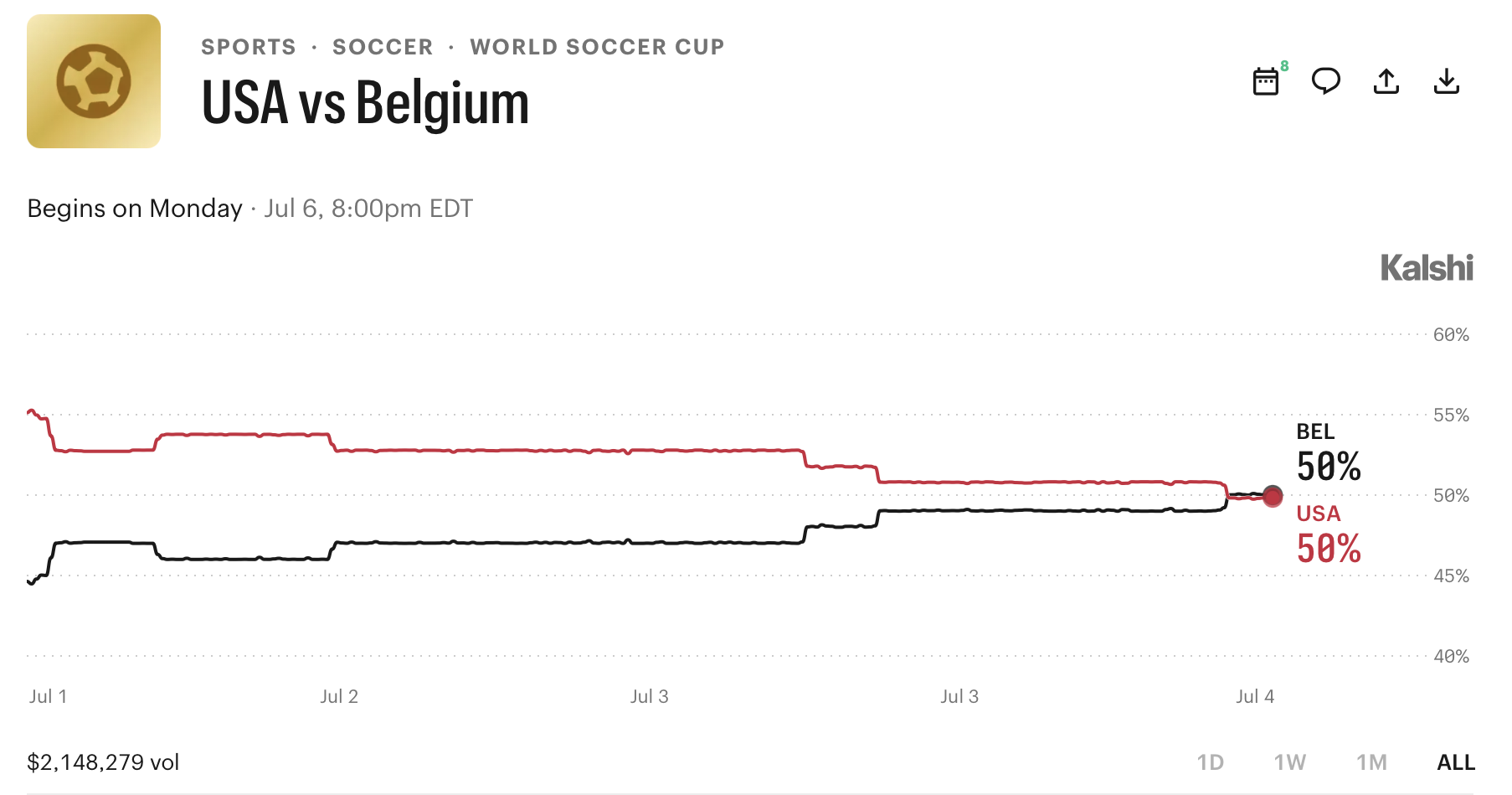

Knockout-stage matchups appear to be particularly attractive to traders. For example, Canada’s Round of 16 match against Morocco—scheduled for Saturday—had generated more than $48 million in trading volume on Kalshi and over $26.8 million on Polymarket at the time of reporting.

The pattern extends to the US Round of 16. Kalshi’s market on which team advances recorded more than $2.1 million in volume, while a comparable Polymarket market attracted around $1.6 million as of Saturday. While these figures are smaller than the Canada–Morocco matchup, they show how quickly attention can shift between fixtures as brackets lock in.

What matters for market participants is not just overall volume, but where it concentrates. World Cup-related contracts create repeatable, time-bound narratives that traders can model—often with clear deadlines and an intense news cycle. That combination helps explain why notional activity can spike even for markets that are narrower than broad political or macro event themes.

Regulatory pressure rises as trading expands

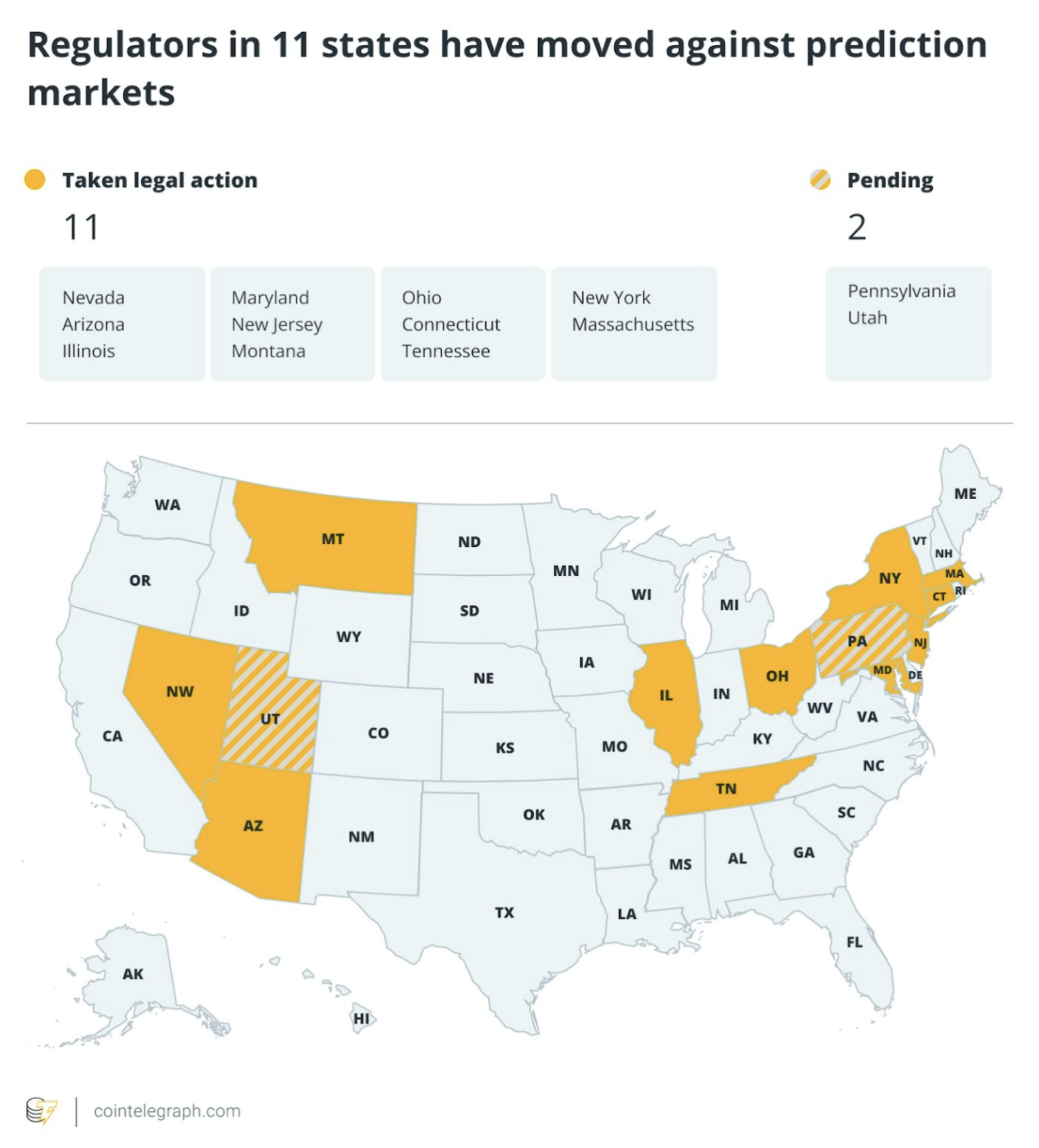

The World Cup-driven surge is occurring against a backdrop of growing controversy over prediction markets in the United States. Earlier this year, Cointelegraph noted that by March nearly a dozen US states had moved against companies including Kalshi and Polymarket. Some states sought to halt such markets, while others argued they should be brought under existing gambling laws and related tax regimes.

At the federal level, regulators have pushed back. In the following month, CFTC Chair Michael Selig accused states of pursuing what he called “illegal enforcement actions” against federally regulated exchanges. In remarks reported via a CFTC press release, Selig argued that Congress granted the agency sole authority over commodity derivatives markets, which can include prediction markets, warning that any state effort to nullify federal law could lead to court challenges.

This is not merely an abstract legal dispute. For platforms, regulatory uncertainty can influence which contracts can be offered to different users, how product structures are shaped, and what compliance costs may look like in practice. For traders, the risk is that market access could change rapidly depending on court outcomes or agency interpretations.

Congress and Europe weigh in with different approaches

The debate is also expanding beyond regulators and into Congress. In June, casino operators, tribal organizations, and labor groups urged lawmakers to amend the Digital Asset Market Clarity (CLARITY) Act by removing sports-event contracts from the CFTC’s authority. Their argument, as described in Cointelegraph reporting, is that sports contracts should instead remain under state gambling laws and existing gaming oversight.

Europe’s approach is different. In a recent reminder, the European Securities and Markets Authority (ESMA) told firms that many event contracts may already fall under existing restrictions tied to binary options. ESMA’s stance emphasized that whether a product is regulated depends on its characteristics rather than merely the label “event contract.” For market operators contemplating cross-border expansion, that distinction is crucial: product design details, not marketing terminology, can determine regulatory treatment.

Taken together, the picture is uneven. The US environment appears to hinge on jurisdiction—whether prediction markets are treated as commodity derivatives under federal authority or as gambling under state law. In Europe, the focus shifts more toward how the contract functions under binary-options-like rules. These differences can shape where liquidity travels, which venues can scale fastest, and how quickly new market formats can be launched.

What to watch next

With the World Cup supplying an immediate, high-volume catalyst, the key question for investors and builders is whether these trading surges translate into longer-term user growth or just prove how concentrated liquidity becomes during major events. Just as importantly, readers should track how ongoing legal challenges—and potential congressional or European regulatory clarifications—affect market access, contract structures, and the durability of platform volume beyond the tournament.

Bitcoin climbed above $63,000 in U.S. morning hours Saturday, up 1.4% over 24 hours and 3.6% on the week, per CoinDesk data, its highest in two weeks and a full reversal of the losses that closed out June.

XRP led the day’s majors, up 5.3% to $1.18 and nearly 10% on the week, a move that lifted it past the USDC stablecoin to fifth place by market value at about $73 billion.

The gain came alongside onchain data showing XRP holders at their deepest average losses on record – the kind of washed-out positioning some traders buy against. Ether added 3.2% on the day to about $1,793, up 11.5% over seven days, while dogecoin rose 2.6% and solana held near $82.50 with a 13.2% weekly gain.

The surge extended a week built on a friendlier macro turn. Fed Chair Kevin Warsh’s comment that inflation risks have come down, a soft June jobs report and a squeeze on bearish traders carried bitcoin from below $60,000 to above $63,000 in five sessions.

Trading was thin on Saturday with U.S. markets shut for the Independence Day holiday, the kind of liquidity that exaggerates moves in both directions.

Bitcoin entered the third quarter at 21-month lows and has now recovered the ground lost in June’s final slide. Whether the momentum holds turns on the coming U.S. inflation print and on whether buying continues once U.S. desks return from the holiday.

Nearly 1 million buyers of the Official Trump (TRUMP) meme coin are sitting on a combined $3.81 billion in losses, according to blockchain analytics firm Nansen. The TRUMP meme coin now trades roughly 98% below its January 2025 record high.

The losses look like the final stage of a familiar meme coin cycle. Early buyers captured most of the gains, while later arrivals absorbed the decline that followed the launch hype.

The TRUMP Meme Coin Cycle Played Out in 18 Months

TRUMP launched on January 17, 2025, three days before President Donald Trump’s second inauguration. Its price jumped from below $1 to a record $73.43 within two days. That briefly lifted its market value near $15 billion.

Nansen tracked about 1.48 million wallets that bought the token. Just under 500,000 locked in profits worth roughly $4 billion. Most of those gains went to early traders who sold into the first rally.

The buyers who followed became the exit liquidity. Nansen counted 988,905 wallets underwater, about two out of every three, once paper losses are included. The token’s own website had warned that it was not an investment.

Follow us on X to get the latest news as it happens

The outcome fit a pattern that analysts flagged for celebrity meme coins from the start. A month later, Argentina saw a faster version. President Javier Milei promoted the LIBRA token in February 2025. Its near $4 billion valuation collapsed within hours, triggering a fraud probe.

The Token Earned for Its Backers Regardless of Price

The design meant the decline barely touched the people behind it. The token’s code routes a share of every trade to creator-linked wallets. Chainalysis traced more than $324 million in such fees to those addresses in the months after launch.

Those fees accrued whether buyers won or lost. Trump’s 2025 financial disclosure later listed a $636 million windfall from the meme coin. The royalties were routed through CIC Digital, the Trump-linked entity behind the token.

Retail buyers had little legal cover. In a February 2025 statement, the Securities and Exchange Commission said meme coins are not securities. That left the market outside its oversight.

Economist Peter Schiff has called the tokens a way to buy access to the president rather than a real investment.

“He’s actually had events at the White House where the top owners of Trump coin are allowed to attend. But it’s really a way to bribe the president. You don’t have to give him money directly, just buy his token, because who else would buy the token? It’s a lousy investment,” he said.

The White House rejects that view. According to a New York Times report, Spokeswoman Anna Kelly said there are no conflicts of interest and that the president acts in the public interest.

TRUMP set an all-time low of $1.50 in early June and has barely recovered. Appetite across the wider meme coin market has stayed subdued. The token now trades close to $1.79, little changed over the past month. Its market value sits near $424 million, ranking around 115th.

Political branding drew far more attention than a typical meme coin. It did not rewrite the math. The TRUMP token traced the same boom-and-bust arc as the speculative coins that came before it.

The post Nearly 1 Million TRUMP Meme Coin Buyers Lost $3.81 Billion: Is the Cycle Complete? appeared first on BeInCrypto.

He authored Bitcoin Improvement Proposal 361 (BIP-361), which outlines a phased migration to quantum-resistant cryptography.

“The goal is to create incentives and deadlines so users, exchanges, custodians, wallets and institutions actually migrate in a timely fashion,” saidLopp, who in April said it would be better to freeze Satoshi’s hoard and millions of other dormant bitcoins than to let hackers steal them.

Matt Hougan, chief investment officer at Bitwise, rejected both letting the coins be stolen and freezing them outright.

Instead, he pointed to a proposal by Castle Island Ventures partner Nic Carter that would place Satoshi’s bitcoin into a legal trust until ownership could be proven through historical electronic records.

Avoiding philosophical challenges

“I actually like Nic Carter’s proposal,” Hougan said via email. “It avoids the philosophical challenges of both CZ’s suggestion and the ‘let whatever happens’ perspective.”

Hougan said the market already treats Satoshi’s holdings as effectively unavailable, meaning almost any change would create more risk than opportunity.

“I don’t think there is any way that developments around Satoshi’s coins are positive for the ecosystem,” he said. “The market already accounts for them as frozen forever.”

For now, the debate remains largely theoretical. Researchers are still working on practical post-quantum cryptography for Bitcoin, and no consensus has been reached on how the network should respond if its encryption does become vulnerable.

Coinbase CEO Brian Armstrong said AI has changed how engineers work inside the crypto exchange. He described the shift as the rise of the “super builder,” where one engineer can deliver far more output. According to Armstrong, Coinbase now ships twice as much code overall. He said some engineers act as ten-times contributors who share effective AI practices.

Armstrong said Coinbase has become one of the most AI-enabled companies in the world. The Coinbase AI engineering strategy focuses on productivity, cost control, and wider adoption. A user reacting to his remarks said former Coinbase employees at other crypto firms describe the company as ahead in AI integration. That reaction added context to Armstrong’s claim about Coinbase’s engineering culture.

Coinbase Cuts Ai Costs As Usage Rises

The update covered how Coinbase reduced AI spending while usage continued to rise. Armstrong said the company nearly halved AI costs even as token usage grew sharply across systems. “How to keep AI spend flat while token usage grows exponentially: not with friction and spend alerts. With better defaults, routing, and caching,” Armstrong said.

Source:

The Coinbase AI engineering approach uses smarter model routing to match tasks with suitable models. This method sends simple work to cheaper tools and reserves stronger models for harder tasks. The company also uses caching to avoid paying for repeated answers when teams ask similar queries. Coinbase uses cheaper open-weight models for routine work where advanced models add little value.

Armstrong Links Ai Growth To Infrastructure

Armstrong framed the savings as a scaling decision rather than a limit on AI use. He said the goal does not involve cutting access or slowing engineers through controls. Instead, Coinbase wants infrastructure that allows AI usage to grow without future budget pressure. That view places cost efficiency at the center of Coinbase AI engineering operations.

The comments connect with Armstrong’s earlier view on AI bottlenecks. In June, he argued that access to energy and compute matters more than model quality for AI growth. His latest comments extend that position into company operations through routing, caching, and model selection. As a result, Coinbase AI engineering reflects productivity gains and infrastructure discipline.

For Coinbase, the message points to AI as an operating layer for software teams. Engineers use AI to write, review, and ship code faster, while management tracks costs. The company’s approach suggests that AI adoption depends on workflow design, not only model access. Coinbase AI engineering shows how a crypto firm can scale AI while watching spend.

Kalshi posted a record month for trading volume in June as the 2026 FIFA World Cup fueled activity across prediction markets.

DefiLlama data shows Kalshi recorded nearly $9.4 billion in trading volume in June, up from about $5.3 billion in May. Polymarket International also climbed to roughly $4.3 billion from about $3.5 billion a month earlier.

The tournament kicked off on June 11 and is the first FIFA World Cup to feature 48 teams, up from 32 in previous editions. CNBC reported the competition became the biggest driver of prediction market trading in June, with Dune Analytics showing record notional trading volumes on Kalshi and Polymarket.

Kalshi trading volume hits June record. Source: DefiLlama

The tournament’s knockout matches are attracting some of the highest trading activity. Canada’s Round of 16 match against Morocco, scheduled for Saturday, had generated over $48 million in trading volume on Kalshi and over $26.8 million on Polymarket at the time of writing.

The United States’ Round of 16 match has also drawn significant attention from traders. Kalshi’s market on which team will advance had generated more than $2.16 million in volume, while a comparable market on Polymarket had attracted around $1.6 million as of Saturday.

Source: Kalshi

Related: US dominates Polymarket political bets despite geoblock: Report

Legal battles intensify as prediction markets grow

The high trading volumes come as prediction markets remain at the center of a growing legal and regulatory debate in the United States.

By March, nearly a dozen US states had already moved against companies including Kalshi and Polymarket, with some seeking to halt the markets while others pushed to bring them under existing gambling laws and state tax frameworks.

Source: Cointelegraph

Federal regulators have rejected states’ attempts to police prediction markets. The following month, CFTC Chair Michael Selig accused states of pursuing “illegal enforcement actions” against federally regulated exchanges, arguing Congress had given the agency sole authority over commodity derivatives markets, including prediction markets. “To any state that seeks to nullify federal law and seize authority over these markets,” Selig said, “we will see you in court.”

The debate has broadened beyond regulators. In June, casino operators, tribal organizations and labor groups urged Congress to remove sports-event contracts from the CFTC’s authority with an amendment to the Digital Asset Market Clarity (CLARITY) Act, arguing the contracts should instead remain under state gambling laws and existing gaming oversight.

Europe has taken a different approach. On Friday, the European Securities and Markets Authority (ESMA) reminded firms that many event contracts may already fall under existing restrictions on binary options, saying whether a product is regulated depends on its characteristics rather than the “event contract” label attached to it.

Magazine: AI is banking the unbanked in Africa… faster than crypto

On June 30, more than 140 companies, including Visa, Mastercard, Stripe, BlackRock, Google, and Circle’s most important ally, Coinbase, unveiled a stablecoin designed to give away the exact revenue stream Circle lives on. CRCL cratered 17% in a day and is down nearly 40% on the month. This is the story of how a moat made of partnerships gets drained by the partners.

Summary

- More than 140 major firms backed Open USD, a shared-economics stablecoin that directly challenges Circle’s reserve-yield business model.

- Circle’s stock plunged after the launch, as investors priced in the risk of partners capturing stablecoin reserve income themselves.

- Circle still has defenses in regulation, liquidity, and trust, but OUSD could pressure its margins and partner leverage.

The most dangerous sentence in Circle’s business model was always hiding in plain sight, in its own filings: nearly all of the company’s revenue comes from interest earned on the reserves backing USDC. Not fees. Not technology. Interest. Circle holds tens of billions of dollars of customer money, parks it in United States Treasuries, and keeps the yield, a business so profitable and so simple that the only real question was how long the companies generating that float would let someone else collect it.

On June 30, the answer arrived. A consortium of more than 140 companies announced Open USD, a dollar stablecoin with free minting and redemption, shared governance, and, most importantly, reserve income distributed back to the participants instead of retained by an issuer. The backer list reads like the org chart of global payments: Visa, Mastercard, American Express, Discover, and Stripe from the card and processing world; BlackRock, BNY, Standard Chartered, BBVA, Mizuho, U.S. Bank, and DBS from asset management and banking; Google, Samsung, IBM, and Shopify from technology; and Coinbase, Ripple, OKX, Bybit, Gemini, Fireblocks, Anchorage Digital, MetaMask, Aave, Solana Labs, and Polygon from crypto.

The market read the announcement correctly and instantly. Circle’s stock fell as much as 18% intraday and closed down 17.55% at $62.63, its worst day since March, extending the monthly drawdown to 39%. The launch was the top trending story in crypto by nightfall, and the one-line verdicts wrote themselves: Circle’s closest partners had gathered in a room and designed its replacement.

The stock’s full 2026 chart shows a company the market keeps re-underwriting shock by shock. The March 20% plunge came on a draft proposal threatening the yield model from the regulatory side; June’s came from the commercial side; between them, the shares have swung on every headline touching reserve economics, because a business this concentrated converts every threat to one revenue line into a threat to the whole valuation. Wall Street’s consensus target near $120, roughly 91% above the post-crash price, is less a disagreement about the facts than about the timeline: the analysts are pricing the years OUSD needs to actually ship and scale, while the tape prices the strategic position, which changed in an afternoon.

The reality is more layered than the verdict, and more interesting. Here is how the stablecoin business actually works, why the consortium model attacks it at the load-bearing wall, and what Circle can still do about it.

A beautiful business with one assumption

Circle’s economics are worth spelling out, because they explain both the 91% analyst upside targets before the announcement and the 17% single-day repricing after it.

USDC circulates around $73 billion. Circle invests the reserves behind those tokens in short-term Treasuries and cash equivalents, and at prevailing rates that float generates several billion dollars a year, roughly 96% of company revenue. The model has effectively no credit risk, no inventory, and no marginal cost per dollar of growth. What it has instead is a single giant assumption: that the businesses and users who hold USDC will keep letting Circle pocket the yield on their money.

Defending that assumption is expensive, and the expense is the tell. Circle paid Coinbase $908 million in a single recent year as a distribution fee for carrying USDC, a payment that is best understood as yield-sharing under a different name, negotiated bilaterally with the one partner large enough to demand it. Every other participant in the USDC economy, the fintechs settling on it, the exchanges quoting it, the merchants accepting it, generated float for Circle and received nothing. The consortium’s founding insight is simply that the Coinbase deal should be everyone’s deal, structurally, by default.

The history rhymes hard enough to sting. USDC itself began life inside a consortium, the Centre venture that Circle and Coinbase governed jointly until 2023, when the structure dissolved, Circle bought out its partner, and shared governance gave way to a single issuer with a paid distributor. Our explainer on consortium stablecoins covers that arc in full, and the short version is uncomfortable for the incumbent: the industry tried single-issuer economics, watched the issuer keep the money, and has now come back for the original model with 70 times as many partners.

What Open USD actually is

Strip the launch-day theater and the product has 5 defining features.

It is issued by an independent operator, Open Standard, led by Zach Abrams, whose stablecoin infrastructure company Bridge was acquired by Stripe in 2024, which makes the venture a Stripe alumni project with the parent’s full weight behind it. Stripe has already committed to making OUSD the base stablecoin across its commerce ecosystem.

It is free at the point of use. Businesses mint and redeem with no fees and no volume limits, removing the toll booths that large-scale users complain about with incumbent issuers.

It shares the money. Reserve income flows back to participating partners after a management fee, governed by a board drawn from the membership. This is the feature that hit Circle’s stock, because it converts every consortium member from a customer of stablecoin issuers into a shareholder of one.

It launches natively on Solana later this year, with the distribution map already sketched by the membership: MetaMask at the wallet layer, Aave in lending, Fireblocks and Anchorage in custody, Shopify and Mercado Pago at the merchant edge, and the card networks wherever they decide interoperability suits them.

And it is aimed at enterprise treasury and merchant payments first, the exact segments where stablecoins have been compounding fastest and where Ripple’s decision to join the consortium made strategic sense for RLUSD, since a shared standard grows the settlement pie that every issuer’s adjacent businesses feed on.

The consortium is not even alone in its category. The Paxos-led Global Dollar Network has run the shared-economics playbook with Robinhood, Kraken, and Galaxy since 2024, and European banks are building the euro-denominated Qivalis venture on the same logic. The GENIUS Act‘s 2025 passage is the common enabler: once federal law defined what a compliant dollar stablecoin is, the risk of issuing one collapsed, and the strategic question flipped from whether regulated institutions should touch stablecoins to why they would hand the float to a third party.

The spectator with the biggest stake

Any Circle analysis that stops at OUSD misses the largest player in the market, who spent June 30 doing what it always does: nothing visible, profitably.

Tether’s USDT circulates at more than double USDC’s size, and its dominance rests on a base the consortium barely touches: offshore exchange liquidity, emerging-market dollar demand, and the informal settlement flows where compliance surface area is a cost, not a feature. The consortium’s enterprise-treasury-and-merchant thesis attacks Circle’s home market precisely because that is the market where its members live, which leaves the incumbent conveniently out of the crossfire.

Post-GENIUS market share data already showed the shape of the fight: Tether’s share drifted from 62% to 59% since the act passed while Circle’s climbed from 19% to about 24%, meaning the regulated segment was growing at the offshore leader’s relative expense. OUSD’s arrival splits the regulated segment’s future growth without touching the offshore base at all.

The regulatory chessboard adds pieces weekly. Banks outside the consortium responded to the launch by asking regulators for tighter oversight of the entire category, a move that reads as incumbents calling the referee on other incumbents. Europe’s MiCA regime, having just shown its teeth on exchange licensing, applies its own e-money rules to stablecoins and has already reshaped which tokens can circulate in the bloc, with Tether conceding ground there while Circle’s EU authorization became a genuine asset. And the same United States framework that made OUSD possible constrains it: the GENIUS Act’s prohibition on paying yield directly to retail holders is why the consortium’s revenue sharing flows to member businesses instead of end users, a design detail that keeps the product enterprise-shaped and leaves the consumer yield question, the truly disruptive one, for another regulatory fight on another day.

The DeFi layer chooses quietly

One constituency will vote on this war earlier than the treasurers and the regulators: decentralized finance, where the default settlement asset is chosen by liquidity gravity, integration inertia, and a handful of protocol governance decisions.

USDC’s position in DeFi took years to compound. It is the reserve asset of major lending markets, half of the deepest trading pairs on every serious venue, and the collateral standard that risk frameworks were written around. That inertia is real protection: migrating a lending market’s base asset is a governance fight, an oracle change, and a liquidity bootstrap all at once, and protocols do not undertake it for a marginally better logo. But the consortium roster shows the attack vector, because Aave, MetaMask, Solana Labs, and Polygon are members. The protocols and platforms that decide DeFi defaults are, in several key cases, now economically aligned with the challenger, and OUSD launching natively on Solana drops it into the ecosystem where new-asset liquidity bootstraps fastest.

The adjacent battleground is machine payments, the fastest-growing new demand source for dollars on-chain. USDC is currently the default settlement asset of the x402 agentic payments stack, an incumbency worth compounding volumes as autonomous agent commerce scales. But the consortium overlaps suspiciously well with that stack’s infrastructure: Stripe co-authored the machine payments standards, Google and the card networks sit in both stories, and a consortium coin with zero mint and redeem friction is engineered for exactly the high-frequency, low-margin flows agents generate. If the agent economy’s plumbing quietly swaps its default dollar, Circle loses the growth segment before the incumbency ever shows up in a market share chart.

The bear case for Circle, steelmanned

The market’s 17% answer contains a specific chain of logic, and it is worth walking honestly.

The consortium members control distribution, and distribution is the whole game in a commodity product. A dollar token is a dollar token; what differs is where it is accepted, quoted, and defaulted. Stripe alone processed $1.9 trillion in payments last year. Shopify fronts millions of merchants. Coinbase decides what tens of millions of retail users see first. When the companies that own those surfaces share in OUSD’s economics, every integration decision tilts one way, not through conspiracy but through arithmetic.

The Coinbase position is the sharpest edge. Circle’s largest distribution partner, the recipient of that $908 million annual payment, is a founding member of the rival. Coinbase’s implicit calculation, that a governance seat and revenue share in a coin running through its own ecosystem beats collecting fees as Circle’s middleman, is exactly the calculation every other large USDC holder will now run. Even if Coinbase never demotes USDC, the negotiating leverage in every future renewal just changed hands.

And the margin math bites even in the scenarios where Circle keeps its users. If OUSD’s default yield-sharing forces Circle to extend Coinbase-style economics across its partner base to defend circulation, revenue compresses without a single dollar of USDC leaving. A company with 96% of revenue from one stream does not need to lose the stream to be repriced. It only needs to lose pricing power over it, and June 30 was the day pricing power visibly moved to the other side of the table.

The precedent from adjacent markets is not comforting either. Interchange, card processing, and index funds all followed the same arc: a profitable intermediary, a coalition of its largest customers, and a shared-ownership alternative that turned margin into member rebates. Payments infrastructure trends toward mutualization once the customers are big enough to build their own, and 140 of them just did.

The bull case the selloff ignored

The counterarguments are real, which is why the stock clawed back part of the loss by Thursday and why Clear Street and KeyBanc both called the plunge overdone.

Start with the oldest lesson in consortium history, the one sitting in Circle’s own past: shared governance is easy to announce and brutal to operate. Centre could not align two partners; Open Standard proposes to align 140, including direct competitors, across banking, cards, tech, and crypto, with a product that has not launched, on a timeline of later this year. Visa and Mastercard sitting on the same board as Aave and Solana Labs is a press release until the first hard decision about chain support, freeze policies, or fee changes, and the graveyard of bank consortia is full of ventures that died at exactly that meeting.

Circle’s actual moat may also be misidentified. USDC’s advantage was never that partners lacked alternatives; it was regulatory surface area. Circle holds licenses and registrations across the United States and Europe, survived a decade of scrutiny, kept its peg through the 2023 banking crisis, and is the counterparty compliance departments have already approved. Europe’s MiCA enforcement just showed what that is worth, locking the world’s largest exchange out of an entire continent for compliance history, and a not-yet-launched consortium coin starts that decade-long accumulation from 0. Enterprise treasurers do not move to a token because its governance is philosophically nicer. They move when it is approved, liquid, and boring, and USDC currently owns boring.

The market-size argument does the rest of the bullish work. Stablecoins circulate above $300 billion today, with Citi projecting $4 trillion by 2030 and BNY sketching $1.5 trillion as a conservative case. In a market growing that fast, USDC’s share, which climbed from 19% to around 24% since the GENIUS Act while Tether’s slipped from 62% to 59%, can shrink relatively while growing absolutely, which is precisely how Jeremy Allaire framed his response. Competition validating the category is a real phenomenon; ask any index fund pioneer how terminal the arrival of rivals proved.

There is also a stickiness argument hiding in the float itself. Stablecoin balances are not portfolio allocations that rebalance on a committee vote; they are working capital embedded in exchange accounts, smart contracts, payment flows, and treasury operations, each with its own migration cost. USDC’s $73 billion is distributed across millions of holders and thousands of integrations, and history says such bases erode slowly even under direct assault: Tether has survived a decade of existential headlines with its dominance dented, not broken, because the marginal holder’s laziness is the strongest force in payments. OUSD must not merely exist and pay better; it must be worth the operational work of switching, integration by integration, and the burden of proof sits with the challenger for years.

And Tether looms over the whole fight as the unbothered variable. OUSD’s enterprise-and-merchant focus attacks Circle’s home turf, not the offshore, trading, and emerging-market flows where the market leader, at more than double USDC’s circulation, actually lives. It is entirely possible the consortium’s main casualty is the number-two coin’s growth rate while number one watches from a distance.

Circle’s option tree

The defense does not have to be passive, and Circle’s realistic moves sort into 4 branches, each with a cost.

Match the economics. Extending Coinbase-grade revenue sharing across the partner base is the direct counter, and the most expensive: it concedes the model, compresses the margin that justifies the stock’s multiple, and converts Circle from toll collector to utility overnight. The consolation is that a utility with USDC’s regulatory footprint and liquidity is still a formidable business, just a differently valued one. The market spent June 30 pricing exactly this branch.

Sell what the consortium cannot ship. Circle’s decade of licenses, audits, banking relationships, and crisis-tested redemption infrastructure is not replicable by press release, and the company’s cleanest play is to weaponize the gap: court the treasurers, banks, and regulated funds for whom counterparty diligence is the product, while OUSD spends its first years earning the approvals USDC already holds. Every quarter the consortium’s launch slips, this branch compounds.

Climb the stack. Circle’s own network buildout, including the Arc chain project, follows the same logic driving every player in the infrastructure race: if issuance economics commoditize, own the settlement layer where the volume clears and charge there instead. It is the identical conclusion Stripe, Coinbase, and Robinhood reached about their own businesses, and it puts Circle in the corporate chain land grab as a competitor instead of a casualty.

Become the acquirer or the acquired. A $60-something CRCL with the category’s best regulatory position is simultaneously a consolidation vehicle and a target, and the same banks lobbying against the consortium have balance sheets that could decide the question. Stranger outcomes have printed in payments; the interchange wars ended with the networks owning pieces of their disruptors.

None of the branches is comfortable, and the honest read is that Circle’s management now has to pick among them under a deadline the consortium set. That is what June 30 actually changed: not the revenue, which is intact, but the initiative, which is gone.

What to watch as the war starts

The battle turns operational from here, and the checkpoints are concrete. Watch whether OUSD ships this year at all, because consortium timelines slip as a rule. Watch the first anchor migrations, especially anything Stripe or Shopify announces about defaults, since defaults move float in ways press releases do not. Watch Circle’s counter-moves: expanded revenue-sharing, new distribution deals, and progress on its own network ambitions, including the infrastructure race where Stripe’s Tempo chain already showed how seriously the payments giants take owning the rails. Watch the banks outside the consortium, who greeted the launch by asking regulators for tighter oversight, a reminder that the incumbents have moves of their own. And watch the Coinbase relationship above all, because the day that renewal changes is the day the thesis resolves.

The challenger has its own proof burden, and it is heavier than launch-day coverage implied. OUSD must clear the same licensing gauntlet in every jurisdiction where its members want to use it, keep a peg through its first crisis, build redemption infrastructure that works at institutional scale on the worst day of the year, and do all of it while a 140-member board negotiates every consequential decision. Circle has already paid those tuition bills; the consortium’s members have only agreed to split the check. Markets price announcements instantly and operations slowly, which is exactly why the definitive verdict on June 30 will not arrive until OUSD survives something.

The deepest reading of June 30 is not that Circle dies. It is that the era of the stablecoin issuer as a standalone toll collector just ended, on a Tuesday, by consensus of everyone who pays the tolls. Circle built the proof that a regulated digital dollar could work at scale, and the reward for proving it is 140 companies deciding the model is too good to leave to one company. Being replaced by your own success story is a very specific kind of defeat, and it is also, sometimes, survivable. Circle has 4 to 6 months before its replacement takes its first breath. What it does with them decides whether June 30 was the day the moat drained, or just the day everyone finally saw how much water was in it.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile, and you can lose your entire investment. Always do your own research. Information current as of July 4, 2026.

Charles Hoskinson expects the Ouroboros Leios upgrade to multiply Cardano’s capacity by 60 times, a leap that would put the network on par with the XRP Ledger in terms of speed.

The founder also defended Midnight City against critics and outlined the upgrade’s next steps.

Leios: Cardano’s Bet to Catch the XRP Ledger

Ouroboros Leios is an upgrade to Cardano’s protocol designed to multiply transaction capacity without sacrificing decentralization or security. Charles Hoskinson explained its scope during an interview with David Gokhshtein on “The Breakdown podcast”.

According to the founder, the technology will increase the network’s internal throughput by up to 60x. That jump, he said, would leave Cardano with performance comparable to the XRP Ledger, a network known for its efficiency.

“Leios will be a 60x in terms of throughput inside the system, so we’re good, we’re as performant as XRP, and we still kept our principles,” Hoskinson said.

Follow us on X to get the latest news as it happens.

The comparison carries weight. The XRPL built its reputation on settlements between three and five seconds and a maximum capacity of 1,500 transactions per second. In March 2026, that network surpassed 120 TPS during a peak with roughly 650 operations.

Hoskinson stressed that these improvements do not mean giving up the project’s founding principles. The industry knows this dilemma as the blockchain trilemma, where scaling often demands trade-offs between decentralization and security. Cardano wants to prove that exchange is not inevitable.

The path is already underway. The public Leios testnet, named Musashi Dojo, debuted on June 23, 2026. It marks the protocol’s first operation in a live network environment. Mainnet deployment is expected before the end of this year.

Hoskinson Defends Midnight City After Big Pey’s Criticism

Hoskinson also responded firmly to questions about Midnight City. Content creator Big Pey labeled the initiative an example of wasteful spending within the ecosystem.

According to the critic, the team invested millions of dollars in a project that was unable to attract new users. He described that strategy as the “Cardano Way,” referring to investments that yield no immediate commercial returns.

The reply came at once. Hoskinson said he had lost all respect for Big Pey as an entrepreneur and criticized him for failing to understand how consumer products evolve. He even challenged the critic to save the post and return in a year to apologize.

Midnight City works as an interactive showcase for Midnight Network, the privacy-focused chain tied to Cardano. The platform translates complex blockchain mechanics into a retro-futuristic 2D city inhabited by AI agents.