Crypto World

XRP Price Prediction: Can XRP Price Ever Reach The $100 Dream ? While Pepeto Delivers the True 150x Entry

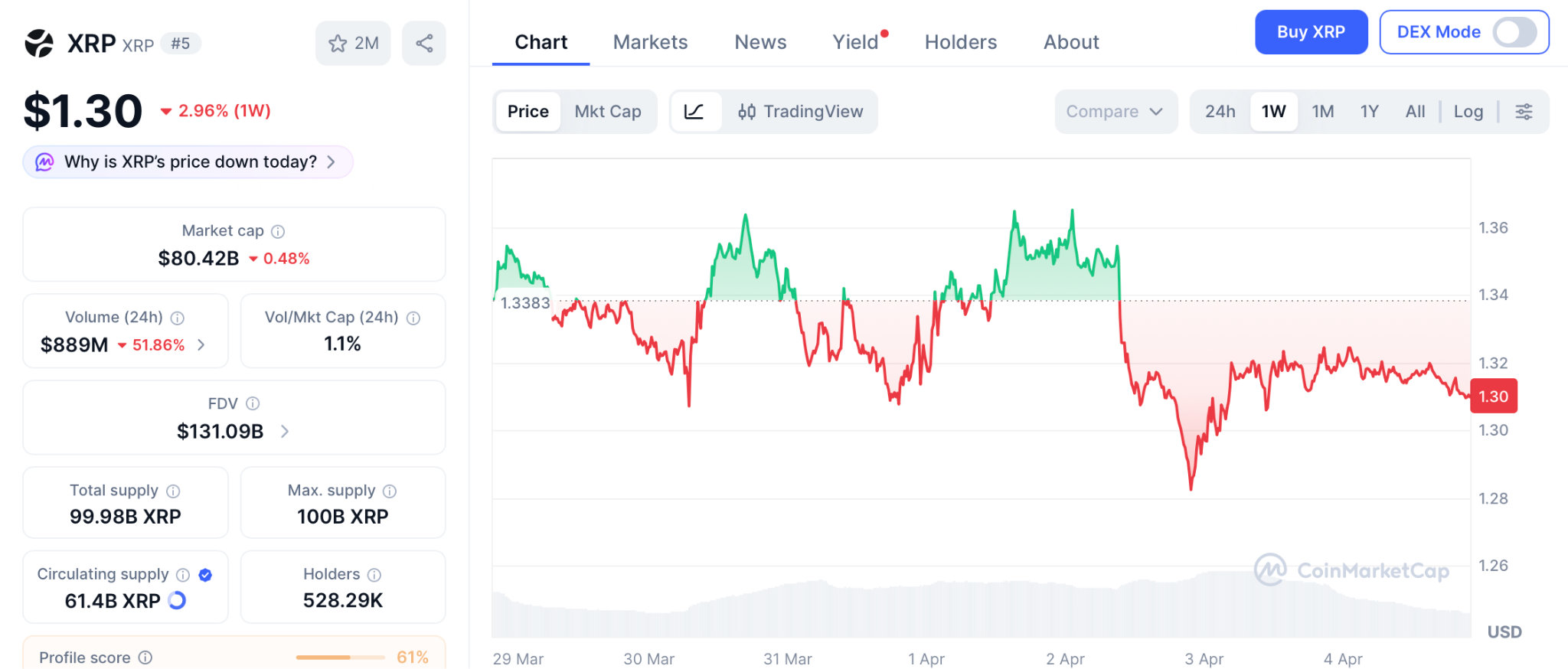

The xrp price prediction crowd has chased the $100 target for years. Goldman Sachs just revealed a $153.8 million position spread across four XRP ETFs, making it the largest institutional holder by a factor of six, according to 24/7 Wall St. The CLARITY Act faces its make-or-break Senate markup in late April, and if it passes, Standard Chartered projects $4 to $8 billion in fresh ETF inflows that could push XRP toward $3.50 to $6, according to Yahoo Finance.

Yet XRP sits at $1.30, and reaching $100 still demands a $5.7 trillion market cap, larger than the entire crypto market combined. While XRP holders wait for a target that math alone cannot justify, one presale built by the team behind a $7 billion token is offering 150x at a price most investors have never seen this low. This piece breaks down the xrp price prediction reality and where the return math actually lives.

Goldman Sachs Loads XRP ETFs as CLARITY Act Approaches Binary Vote

24/7 Wall St reported that Goldman Sachs holds $153.8 million across Bitwise, Franklin Templeton, Grayscale, and 21Shares XRP ETFs, while CoinMarketCap confirmed $11.4 billion in XRP left Binance on April 2, tightening exchange supply to multi-month lows. The partnership validates XRP’s institutional case, but a validated use case and a profitable entry from $1.30 remain entirely different calculations.

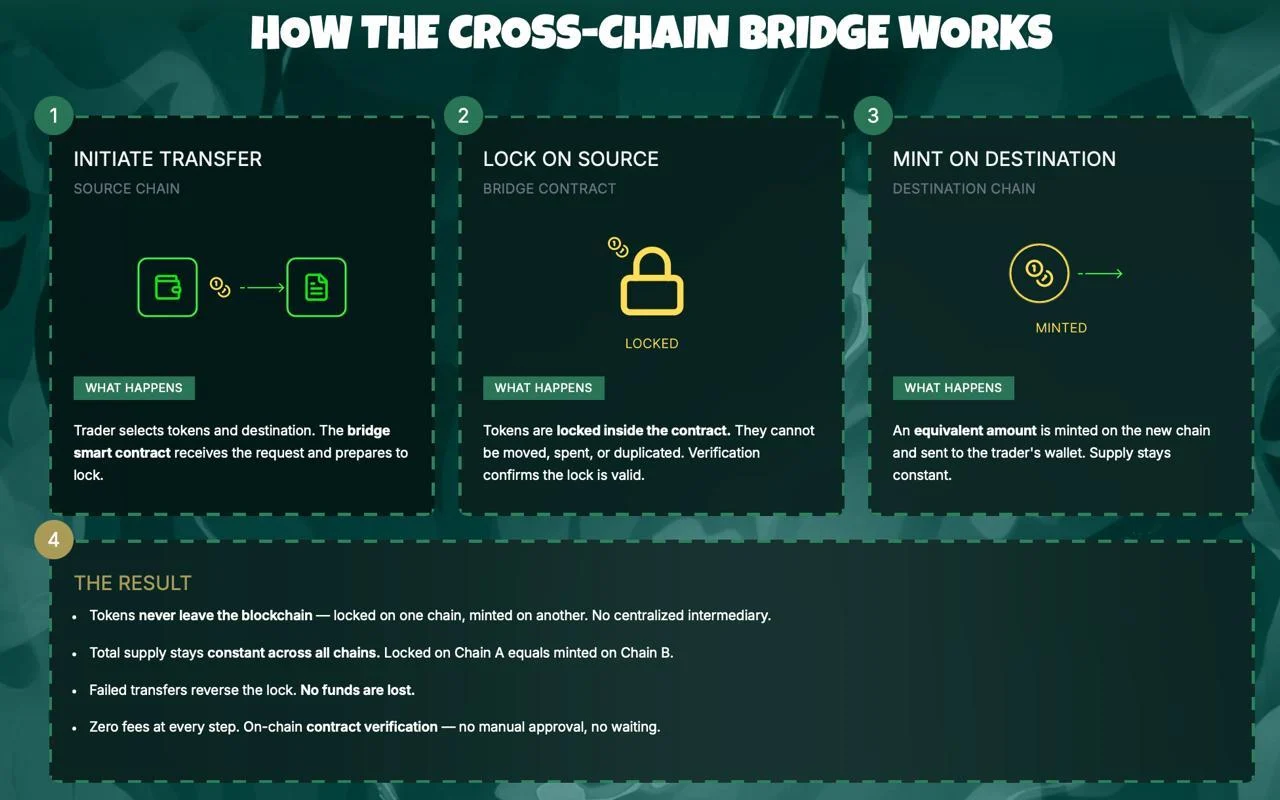

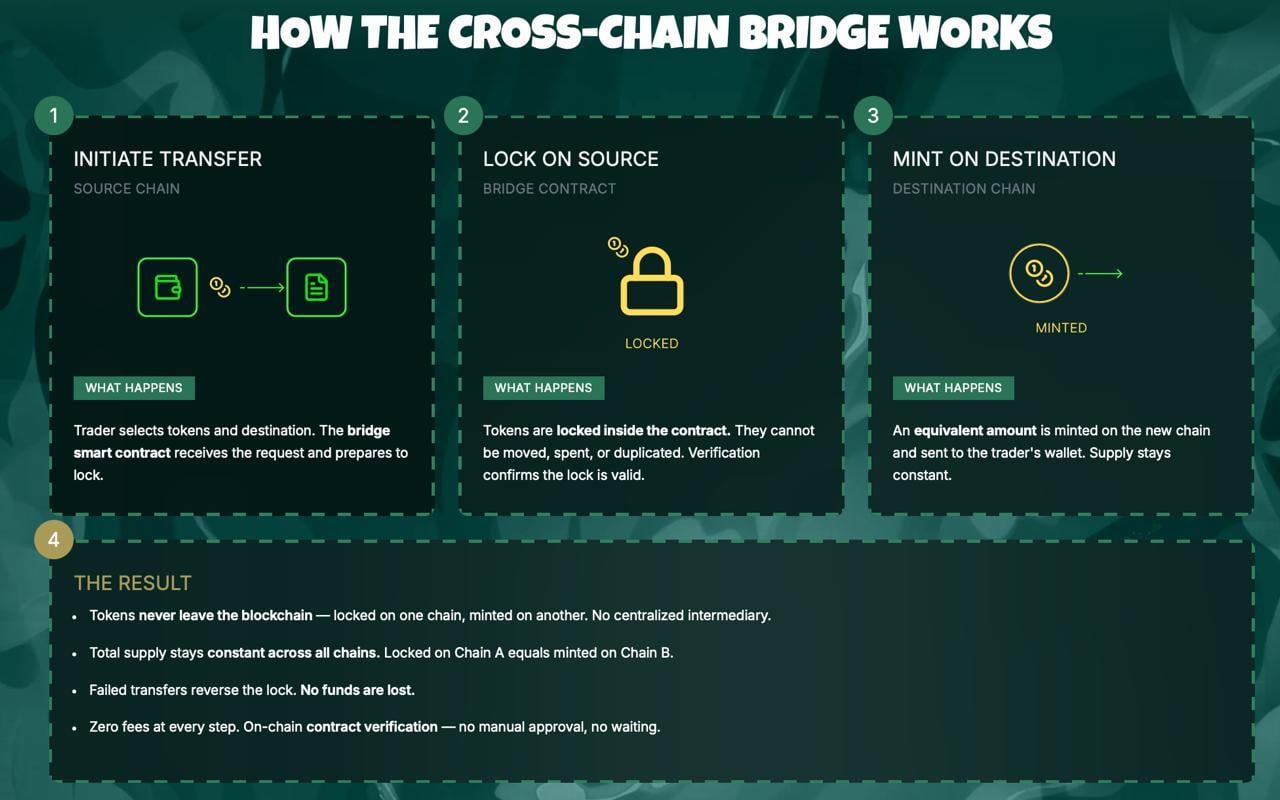

The XRP Price Prediction Ceiling vs the Pepeto Floor: Where Returns Actually Live

Pepeto: The Presale That Converts XRP’s Validation Into Actual Holder Wealth

Finding a presale that combined meme token pricing with functional exchange infrastructure used to be nearly impossible. Most projects offered dashboards, chatbots, or lending tools that thousands of competitors already shipped. Pepeto changed the equation by delivering a full exchange ecosystem with zero-fee trading, a cross-chain bridge spanning Ethereum, BNB Chain, and Solana, and 188% APY staking that compounds daily.

These tools are not placeholder features on a roadmap. The exchange processes volume across three blockchains simultaneously, and every component runs on smart contracts verified through a SolidProof audit. That foundation keeps Pepeto in structural demand regardless of whether the market trends up or down, because utility drives volume in every condition.

At $0.0000001862, a $1,000 entry secures billions of tokens. The original Pepe shares the same 420 trillion total supply and peaked at an $11 billion market cap with zero products behind it. Reaching that valuation turns a $1,000 position into approximately $150,000, a 150x return that analysts treat as conservative because Pepeto has the audited exchange, the cross-chain bridge, and the working infrastructure Pepe never built. The cofounder who took Pepe from zero to $7 billion architects this project, and a former Binance executive shapes the listing strategy.

With the Binance listing approaching, these projections mirror BNB’s trajectory from $0.15 at ICO to over $700 once real trading activity powered the token. Staking at 188% APY grows every position daily before listing day. The wealth that changed lives in every prior cycle was captured by wallets that entered infrastructure presales while others hesitated, and Pepeto’s confirmed Binance listing will permanently eliminate this entry along with the 150x math attached to it.

XRP Price Prediction: Why $100 Demands More Capital Than Crypto Has Ever Seen

XRP trades at $1.30 according to CoinMarketCap with an $80 billion market cap. Hitting $100 would require a valuation above $5.7 trillion, exceeding the entire crypto market’s current $2.38 trillion capitalization by more than two times. The bullish xrp price prediction from ChatGPT targets $3.50 to $6 if the CLARITY Act passes in late April, delivering 160% to 340% from current levels, according to 24/7 Wall St.

Even reaching $10 demands a $570 billion valuation that rivals Ethereum at its historic peak. The xrp price prediction is constructive long term, but the math confirms the largest percentage returns already happened for holders who entered under $0.20. From $1.30, the upside is measured in percentages while Pepeto measures it in multiples.

Conclusion

Goldman Sachs loaded $153.8 million into XRP ETFs and the token barely moved. That is the ceiling of an $80 billion asset. Pepeto sits at $0.0000001862 with a SolidProof audited exchange, 188% APY staking, and a Binance listing approaching.

A $1,000 entry targets $150,000 at a fraction of what Pepe achieved with nothing. XRP needs $5.7 trillion for $100. Pepeto needs a sliver of what Pepe reached for 150x. The gap is not close. Visit the Pepeto official website and secure the entry that the xrp price prediction will never offer you at this stage.

Click To Visit Pepeto Website To Enter The Presale

FAQs

Is $100 a realistic target for the xrp price prediction?

Reaching $100 requires a $5.7 trillion market cap. Most analysts see $3.50 to $6 as realistic if the CLARITY Act passes.

Why does Pepeto offer stronger return math than XRP from here?

At $0.0000001862 with 420 trillion supply, matching Pepe’s ATH delivers 150x, a multiple XRP at $80 billion cannot produce.

What impact does Goldman Sachs buying XRP ETFs have on price?

Goldman holds $153.8M in XRP ETFs, confirming institutional interest, but XRP remains rangebound until the CLARITY Act advances.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Quick Overview

- Rocket Lab achieved 38% revenue growth, reaching $601.8 million in 2025, backed by a $1.85 billion record backlog

- An $816 million Space Development Agency contract strengthened Rocket Lab’s position in government aerospace

- AST SpaceMobile generated $70.9 million in 2025 revenue as it continues early-stage commercial infrastructure development

- AST maintains over $3.9 billion in pro forma liquidity to support satellite constellation expansion

- Analyst consensus favors Rocket Lab with a Moderate Buy rating, while AST receives a Reduce rating

Among space sector equities, Rocket Lab and AST SpaceMobile stand out as two of the most discussed investment opportunities. However, these companies pursue fundamentally different strategies and carry distinct risk-reward profiles. One has established a diversified operational foundation. The other represents a transformative vision for global mobile connectivity.

Rocket Lab delivered impressive financial performance throughout 2025. The company recorded 38% year-over-year revenue expansion, totaling $601.8 million. Its fourth-quarter performance reached a milestone with $179.7 million in revenue. Perhaps most significantly, the firm concluded 2025 with a $1.85 billion backlog—a 73% increase from the previous year. This substantial order book provides greater revenue visibility than most competitors in the space industry can demonstrate.

The company’s revenue composition demonstrates meaningful diversification beyond launch services. Product sales generated $371.6 million during 2025, complemented by $230.2 million from service operations. Today’s Rocket Lab manufactures complete spacecraft, subsystems, and specialized components for defense and intelligence agencies.

Government Contract Wins Strengthen Rocket Lab’s Position

A significant milestone arrived when the company secured an $816 million agreement with the Space Development Agency. This substantial contract validates Rocket Lab’s capabilities for executing complex, multi-year government programs. Meanwhile, the Neutron medium-class launch vehicle represents management’s primary catalyst for the next phase of expansion.

Profitability remains elusive despite operational progress. Rocket Lab recorded a $198.2 million net loss for 2025. Leadership projected continued negative adjusted EBITDA for the opening quarter of 2026. Market valuations currently reflect anticipated future scale rather than present earnings performance.

AST SpaceMobile pursues an entirely different opportunity. The enterprise aims to deploy a satellite constellation providing cellular broadband connectivity directly to unmodified smartphones—eliminating requirements for specialized equipment. Successfully executing this vision at scale could unlock previously inaccessible market segments that conventional satellite providers cannot economically serve.

AST remains in the foundational stages of its mission. The company reported $70.9 million in total 2025 revenue. Fourth-quarter performance contributed $54.3 million, primarily from gateway equipment deliveries, mobile network operator partnerships, and government development milestones.

Strong Liquidity Position Supports AST SpaceMobile’s Deployment Plans

The company maintained $2.8 billion in cash and equivalents as of year-end 2025. Following additional capital raises completed in early 2026, pro forma liquidity exceeded $3.9 billion. This financial cushion enables continued satellite deployment without near-term funding pressures.

AST has secured more than $1.2 billion in contracted revenue commitments from strategic partners. For a company just beginning to recognize meaningful revenue, this represents substantial commercial validation. Nevertheless, significant losses continue, and ultimate success depends critically on deployment velocity and network performance metrics.

Analyst sentiment clearly distinguishes between the two opportunities. Rocket Lab earns a Moderate Buy consensus rating, comprising 2 Strong Buys, 7 Buys, 7 Holds, and 1 Sell recommendation. AST SpaceMobile receives a Reduce consensus, with 2 Buys, 6 Holds, and 3 Sells.

Final Thoughts

Investment community confidence runs higher for Rocket Lab’s proven business model. While acknowledging AST’s substantial upside potential, analysts find the opportunity more challenging to quantify at this development stage. Rocket Lab offers greater operational maturity, revenue diversification, and broader analytical support. AST represents a higher-risk proposition with correspondingly larger potential returns if its satellite broadband architecture achieves technical and commercial success.

Rocket Lab presents the more established investment thesis currently. AST SpaceMobile offers the more ambitious transformational opportunity. The appropriate choice depends entirely on individual investor risk tolerance and portfolio objectives.

TLDR

- The British government is actively pursuing Anthropic for expanded UK operations

- Offers include London headquarters expansion and dual stock exchange listing opportunities

- Prime Minister Keir Starmer’s administration is directly supporting the initiative

- Anthropic faced US blacklisting after declining to permit Claude for military surveillance or weaponized systems

- Federal courts have temporarily halted the blacklist enforcement, with additional legal challenges underway

British officials are making aggressive moves to attract Anthropic, the developer of the Claude AI assistant, as reported by the Financial Times. The UK sees a strategic opening to expand the company’s presence following escalating tensions between Anthropic and the Pentagon.

The British government’s pitch encompasses expanding Anthropic’s current London operations and facilitating a dual stock market listing. The UK’s Department of Science, Innovation and Technology is spearheading these initiatives.

Prime Minister Keir Starmer’s administration has thrown its weight behind the department’s outreach efforts. Officials plan to present these proposals directly to Anthropic’s Chief Executive Dario Amodei during his anticipated UK visit scheduled for late May.

Both Anthropic and the UK’s Department of Science, Innovation and Technology declined to provide statements when contacted by Reuters.

The Pentagon Dispute Explained

The Department of Defense labeled Anthropic as a national-security supply-chain threat. The designation stemmed from the company’s firm stance against permitting its Claude AI system to be deployed for US military surveillance operations or autonomous weaponry applications.

This classification resulted in Anthropic being added to a government blacklist. Such listings typically limit a company’s capacity to collaborate with federal agencies and approved contractors.

Anthropic mounted a swift legal response. A federal judge granted temporary relief, preventing the blacklist from becoming operational while litigation proceeds.

The AI company has simultaneously launched a separate legal challenge targeting the supply-chain threat classification itself. This additional lawsuit remains pending judicial review.

Britain’s Strategic Proposal

The UK’s aggressive courtship represents part of a wider strategy to capitalize on uncertainty surrounding American technology governance.

A dual stock listing arrangement would enable Anthropic shares to trade on British exchanges parallel to any potential US market debut. This structure would provide UK-based investors with immediate access to company equity.

Expanding the London facility would strengthen Anthropic’s European footprint significantly. Britain has cultivated a thriving AI ecosystem, with government officials making tech investment attraction a cornerstone policy objective.

The Financial Times report did not indicate whether Anthropic has shown interest in or rejected the British proposals.

Amodei’s late May UK visit is anticipated as the critical juncture when officials will formally present their complete package.

The temporary judicial stay on the blacklist designation leaves Anthropic’s regulatory status in flux. The resolution of both ongoing legal battles will probably determine the company’s strategic direction going forward.

Key Takeaways

- Wall Street Zen shifted its SPCE rating from “hold” to “sell” on April 4, 2026

- Shares currently trade near $2.43, while the analyst consensus price target stands at $3.45

- Virgin Galactic has resumed accepting reservations at $750,000 per seat for Delta Class flights

- First quarter earnings showed a loss per share of ($0.98), surpassing expectations, though revenue of $0.31 million fell short of projections

- Jefferies lowered its price objective from $8.00 to $5.00 while maintaining a “buy” stance, pointing to cash flow timing issues

Virgin Galactic (SPCE) stock began Friday’s session at $2.43, declining 1.4% during trading.

Virgin Galactic Holdings, Inc., SPCE

Wall Street Zen revised its outlook on SPCE from “hold” to “sell” on April 4, 2026. This shift reinforces a generally bearish analyst sentiment, with MarketBeat reporting a consensus rating of “Reduce” and a mean price target of $3.45.

Morgan Stanley maintains an “underweight” stance with a $2.30 price objective. Weiss Ratings similarly assigns a “sell” grade. Among six tracked analysts, one recommends buying, three suggest holding, and two advise selling.

Jefferies reduced its price forecast from $8.00 to $5.00 recently, while retaining its “buy” recommendation. The investment firm highlighted cash flow timing uncertainties within the developing space industry.

SPCE has fluctuated between $2.13 and $6.64 over the past 52 weeks. The stock’s 50-day moving average sits at $2.56, with the 200-day average at $3.25. A beta of 2.20 indicates significant volatility compared to broader market movements.

On March 30, Virgin Galactic announced Q1 earnings per share of ($0.98), outperforming the ($1.12) consensus forecast. Revenue reached $0.31 million, missing the anticipated $0.41 million.

Return on equity registers at negative 108.78%, while net margin sits at negative 18,063.93%. The company carries a debt-to-equity ratio of 1.87, though its current ratio of 2.87 indicates sufficient near-term liquidity.

Market capitalization currently stands around $177 million. Wall Street projects full-year earnings per share of ($16.05) for the ongoing fiscal period.

Fresh Reservations for Next-Generation Spacecraft

Coinciding with the rating downgrades, Virgin Galactic reopened its reservation system for flights aboard the upcoming Delta Class vehicle. Tickets now cost $750,000 per person — a $150,000 increase from the $600,000 price point in 2023.

The Delta Class accommodates six passengers, representing a two-seat capacity boost over previous models. Virgin Galactic plans to conduct test flights this summer, followed by commercial operations launching in the fall. Research missions will precede passenger journeys by six to eight weeks.

The initial offering includes 50 available seats before the company temporarily closes bookings. CEO Michael Colglazier indicated that future pricing rounds will feature higher rates, though specific amounts remain undisclosed.

Additionally, a queue of 675 “founding astronauts” — early customers who secured spots with deposits years earlier — will board flights at discounted rates compared to new purchasers.

Ambitious Monthly Flight Goals

Virgin Galactic’s most recent commercial mission, Galactic 07, took place on June 8, 2024. That flight marked the final journey of VSS Unity, the organization’s inaugural spacecraft.

Colglazier has established an ambitious goal of conducting 10 flights monthly by 2027, which would transport approximately 60 passengers each month. Achieving this frequency hinges on successful summer testing of the Delta Class vehicle.

Institutional investors control 46.62% of SPCE shares. Multiple funds expanded their holdings in recent quarters, with Truist Financial Corp boosting its position by 78.2% during Q4.

Susquehanna established a $3.50 price target in January 2026.

Key Takeaways

- Micron’s share price has tumbled approximately 20% following its second-quarter results released March 18, as investors worry about Google’s TurboQuant potentially cutting memory requirements

- Mizuho’s Vijay Rakesh continues to rate the stock as Outperform with a $530 target, characterizing the downturn as an attractive entry point

- The company’s DRAM average selling prices climbed in the mid-60% range during Q2, while NAND ASPs jumped in the high-70% range, demonstrating robust pricing strength

- Wall Street remains divided: certain analysts view the selloff as panic-driven, while others highlight risks from customer concentration and pricing sustainability

- Over the trailing twelve months, Micron shares have surged 324%, eclipsing gains from Nvidia, AMD, TSMC, and Broadcom

The past several weeks have proven turbulent for Micron. Following one of the most impressive rallies in the chip industry — climbing 324% year-over-year — the memory specialist encountered serious resistance. The trigger came from Google’s unveiling of TurboQuant, a lossless compression algorithm that sent jitters through the investment community about potential declines in DRAM and NAND requirements. Markets responded swiftly.

Following Micron’s fiscal second-quarter report on March 18, shares have declined approximately 20%. This represents a significant pullback for a business that recently stood as a poster child for the artificial intelligence boom.

The downturn revolves around one core concern: if Google’s TurboQuant technology enables superior data compression while preserving model precision, cloud giants may require substantially less physical memory for their AI operations. Reduced DRAM and NAND consumption translates to weakened pricing leverage for Micron. This narrative, though, faces pushback from multiple industry watchers.

Vijay Rakesh from Mizuho mounted a strong counterargument. He retained Outperform classifications for both Micron and Sandisk (SNDK), assigning price objectives of $530 and $710 respectively. Rakesh invoked the Jevons paradox — an economic principle suggesting efficiency gains frequently stimulate increased usage rather than decreased demand. His reference point: when DeepSeek emerged in 2025 and initially shook GPU equities, AI infrastructure investments ultimately intensified.

Rakesh further noted that Google’s TurboQuant documentation itself suggests possibilities for expanded models and accelerated inference capabilities, which would still necessitate considerable memory resources. He characterizes the present decline as excessive market pessimism.

Examining the Financial Performance

Micron’s second-quarter results painted an impressive picture. DRAM unit shipments increased mid-single digits on a sequential basis, while average selling prices surged in the mid-60% range. NAND unit volumes expanded low-single digits, accompanied by ASP growth in the high-70% territory. These represent exceptional pricing premiums, propelled by constrained availability rather than explosive volume expansion.

Seeking Alpha’s Oliver Rodzianko highlighted this pattern. He noted that Micron currently faces greater supply limitations than demand constraints, and that DRAM and NAND market tightness should persist past 2026 based on company guidance. His apprehension doesn’t center on technological factors — rather, he questions how much of Micron’s profitability stems from price inflation versus sustainable structural advantages.

Should pricing revert to historical norms, profit margins could face pressure. Rodzianko additionally emphasized customer concentration concerns: Micron maintains heavy exposure to hyperscaler capital expenditure, meaning any slowdown in that deployment cycle would deliver swift and substantial stock impact.

Optimistic Voices Emphasize AI Infrastructure Growth

Analyst Dmytro Lebid offered a decidedly positive perspective. He attributed the decline to “irrational investor behavior” and suggested the market is overstating deceleration threats. From his vantage point, cloud providers’ hunger for HBM3E memory remains undiminished, while Micron’s supply-limited status preserves margin health.

Nvidia’s ongoing requirements alone should sustain growth momentum, he contended, establishing a solid foundation beneath Micron’s pricing structure.

The company is simultaneously expanding production capabilities across Idaho, Tongluo, and Singapore facilities stretching into 2027–2028 — representing a strategic commitment that AI-powered memory consumption will maintain its upward trajectory.

As of early April 2026, Micron traded near $366 per share, commanding a market capitalization approaching $413 billion within a 52-week trading band of $61.54 to $471.34.

TLDR:

- Binance USDT inflows are nine times higher than levels recorded during Bitcoin’s all-time high of $123K in June 2025.

- The BWCI reached a one-year record of 74.58%, confirming that institutional players are driving the current liquidity surge.

- Binance Open Interest climbed 2.22% to $6.17B, with USDT reserves acting as direct collateral for derivatives expansion.

- Bitcoin’s $54K downside risk persists unless ETF flows confirm the reversal and global risk aversion sentiment fully fades.

Binance is registering USDT inflows nine times higher than those seen at Bitcoin’s all-time high of $123,000 in June 2025.

Bitcoin trades at $66,990 as of writing amid a geopolitical risk-off environment. On-chain data reveals a massive buildup of institutional liquidity on the platform. The Binance Whale Concentration Indicator, or BWCI, has reached a one-year high of 74.58%. This places Binance at the center of global digital dollar liquidity.

BWCI Signals Institutional Takeover on Binance

The BWCI measures liquidity quality by crossing inflow data with capital retention on the exchange. At Bitcoin’s June 2025 all-time high, the indicator registered just 8.25%, pointing to a retail-driven top.

Today’s reading of 74.58% confirms that large players are now absorbing panic liquidity. This marks a one-year record for institutional-grade capital concentration on the platform.

On-chain analyst GugaOnChain shared the data on social media, noting the scale of this divergence. The post stated that USDT flow is serving as direct collateral for Open Interest expansion. Open Interest on Binance rose 2.22% throughout the day, reaching a total of $6.17 billion.

USDT Exchange Reserves on Binance reached $3.4993 billion within a 24-hour window. Whales are deploying this capital to establish support levels in spot markets.

At the same time, they are directing derivatives activity using the same reserves. The BWCI confirms this flow is the direct engine behind the observed Open Interest growth.

This activity surpasses the flow recorded during the “Trump Tariff Flush” of April 9, 2025, which stood at 20.11%. The current BWCI reading of 74.58% places Binance above every other venue for deployable digital liquidity. Large players are consolidating strategic order book control not seen in recent months.

ETF Flows and Macro Sentiment Remain Key Variables for Bitcoin

Despite the strong liquidity buildup on Binance, downside risk for Bitcoin has not disappeared. A move toward $54,000 remains possible if ETF flows fail to confirm a trend reversal.

On-chain data strength alone cannot guarantee a new macro expansion. Broader geopolitical uncertainty continues to weigh on overall market direction.

ETF flows serve as a bridge between traditional finance and the crypto market. Without their confirmation, Binance’s accumulation may not translate into a sustained recovery. Global risk aversion sentiment must fully exhaust itself before the bullish case can materialize.

The current market structure on Binance differs from what was seen in prior downturns. Institutional players are not retreating; they are positioning with clear precision and scale.

This behavior reflects a degree of confidence in Bitcoin’s longer-term trajectory. Short-term risks tied to macro conditions, however, remain present.

The BWCI at its one-year high confirms this is not a retail-driven accumulation phase. Smart money is making deliberate moves while fear remains elevated in the broader market.

Macro headwinds will ultimately determine whether this positioning pays off. Binance, for now, stands as the clearest measure of institutional intent in the global crypto market.

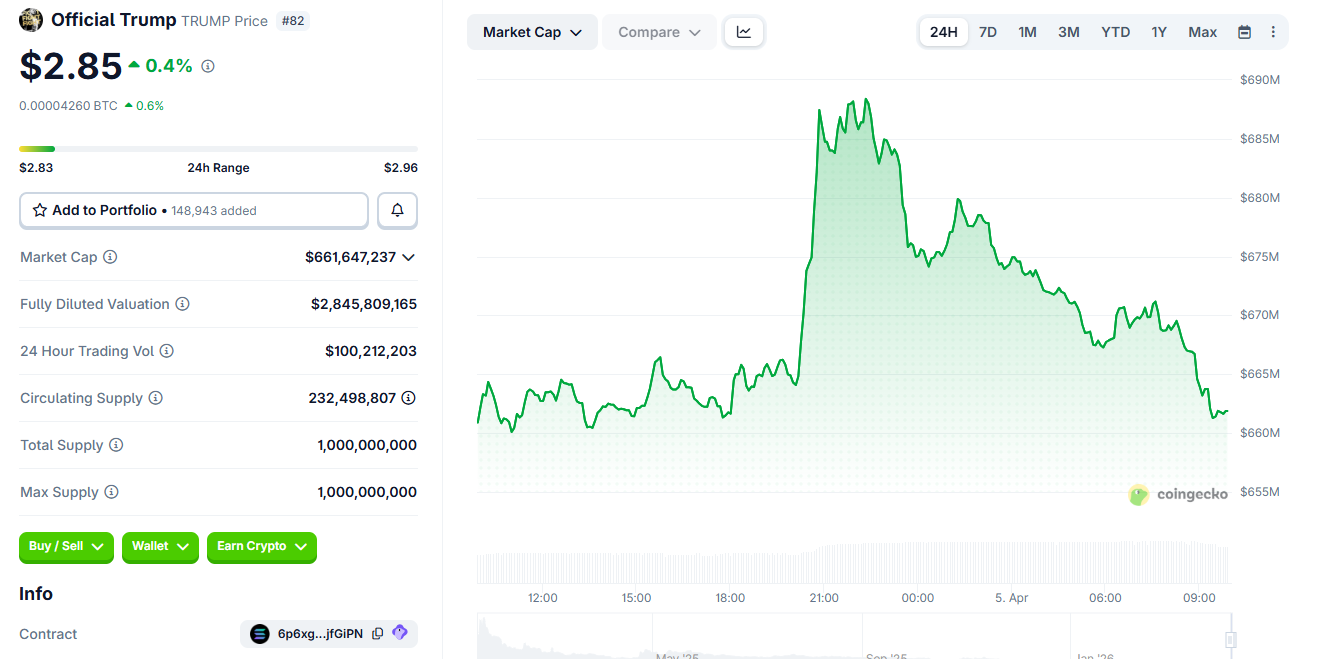

The meme coin Official TRUMP (TRUMP) surged on Saturday, April 4, 2026, amid rumors about President Donald Trump’s health.

An old video from 2024 (of the attempted attack in Butler, Pennsylvania) was shared again, and correspondents published images of a Marine sentry at the entrance to the West Wing.

The TRUMP Meme Coin Soars Amid Health Uncertainty

The rumors began after Donald Trump canceled his public appearances.

At the same time, rumors circulated that Trump had been rushed to Walter Reed National Military Medical Center following a medical emergency.

However, minutes later, presidential spokesman Steven Cheung slammed the news, indicating that Trump was still working.

“There has never been a president who has worked harder for the American people than President Trump. This Easter weekend, he worked nonstop at the White House and the Oval Office. God bless him,” Cheung articulated.

According to available information, Trump remained in Washington and was working at the White House and the Oval Office, without trips to his golf course or Walter Reed hospital.

Despite the denials, the TRUMP meme coin saw its price and trading volume rise over the past 24 hours.

After nearly 5% gains in the immediate aftermath of this news, TRUMP price was up by o.5% on Sunday, trading for $2.85 as of this writing. Other Trump-themed meme coins also saw a sharp rally.

These types of speculative assets are highly sensitive to news related to the US president. It reflects how rumors, even when debunked, can generate immediate movement in the political meme coin market.

Nevertheless, the TRUMP meme coin remains 96% below its all-time high of $73.43 recorded in January 2025.

The post Trump Coins Rally Following Rumors of the President’s Health appeared first on BeInCrypto.

Key Highlights

- Hon Hai Precision’s first-quarter revenue climbed 29.7% annually to T$2.13 trillion (approximately $66.6 billion)

- Cloud and networking products division spearheaded expansion; smartphone manufacturing showed robust performance amid fresh Apple releases

- Monthly revenue for March reached an all-time high of T$803.7 billion, representing a 45.6% annual increase

- Management highlighted “volatile” geopolitical landscape, especially Middle East tensions, as a primary concern

- Shares have declined 16% since January, significantly trailing Taiwan’s benchmark index which gained 12%

Hon Hai Precision Industry — widely recognized as Foxconn — announced first-quarter revenue totaling T$2.13 trillion ($66.6 billion) this past Sunday, marking a 29.7% increase from the same period last year. The figure narrowly missed the LSEG SmartEstimate consensus of T$2.148 trillion.

The primary catalyst behind this impressive performance was the cloud and networking products unit, which benefited from explosive growth in AI infrastructure requirements. As Nvidia’s principal server manufacturer, Foxconn has positioned itself at the center of the AI hardware revolution, and this strategic partnership continues to deliver substantial returns.

The smart consumer electronics division — home to iPhone assembly operations — similarly demonstrated robust expansion following the introduction of new Apple products. As one of Foxconn’s most critical clients, Apple’s product refresh cycles consistently generate significant revenue momentum for the manufacturing giant.

March delivered particularly impressive results. The company generated T$803.7 billion in revenue, setting a new record for the month and representing a 45.6% surge compared to the previous year. These are the types of figures that capture Wall Street’s attention.

AI Infrastructure Momentum Continues

Foxconn indicated that demand for AI rack systems should maintain its upward trajectory throughout the second quarter, with operational metrics expected to improve both sequentially and year-over-year. While the company refrained from issuing precise numerical targets — consistent with its typical practice — the overall tone remained decidedly optimistic.

Comprehensive first-quarter financial results are scheduled for release on May 14, which will provide investors with deeper insights into profit margins and overall profitability beyond the top-line revenue figures.

The ongoing expansion of AI infrastructure remains the fundamental growth driver. Hyperscale data center operators show no signs of reducing their capital expenditure, and Foxconn maintains a crucial position within this critical supply chain.

Geopolitical Concerns Shadow Outlook

Notwithstanding the impressive financial performance, company leadership adopted a measured approach regarding future prospects. Foxconn emphasized that it “remains necessary to monitor the impact of the volatile global political and economic situation,” though the statement lacked detailed elaboration.

Chairman Young Liu has previously singled out the Middle East conflict as the most significant external threat confronting the organization throughout 2025. Vulnerabilities in supply chain networks and international logistics present legitimate risks to sustained operations.

This cautious stance appears to be influencing investor sentiment. Hon Hai shares have tumbled 16% year-to-date, presenting a dramatic divergence from Taiwan’s primary stock index, which has appreciated 12% during the identical timeframe.

The stock finished Thursday’s trading session down 2% ahead of the revenue announcement, largely mirroring broader market movements. Taiwan’s financial markets were shuttered Friday and resume operations Tuesday.

Market participants will be monitoring whether the exceptional March performance — combined with persistent AI sector tailwinds — proves sufficient to reverse sentiment on a stock that has underperformed the broader market by nearly 30 percentage points in 2025.

Complete quarterly earnings arrive May 14.

Pershing Square CEO Bill Ackman refuses to settle what he calls a fabricated gender discrimination claim from a terminated family office employee, weeks before his $10 billion IPO.

The post, which quickly went viral, drew immediate public support from Elon Musk and venture capitalist Chamath Palihapitiya, both of whom framed such lawsuits as a hidden tax on business.

The Family Office Blowup Behind the Post

Ackman revealed that he founded a family office called TABLE roughly 15 years ago and hired a trusted friend to run it.

Over the past decade, operational costs and headcount ballooned while his investment portfolio remained largely passive.

After growing concerned about runaway expenses and high staff turnover, Ackman brought in his nephew, a recent Harvard graduate who had spent several years executing a turnaround at UK watchmaker Bremont. The nephew began interviewing employees and evaluating operations.

What followed was a reduction in force. Ackman fired the president and about a third of the team. All but one departed professionally.

The exception was an in-house lawyer he referred to as “Ronda.” She had been employed for 30 months at a salary of $1.05 million plus benefits.

After her termination, she demanded two years of severance, roughly $2 million, and hired a Silicon Valley law firm to send a threatening letter alleging gender discrimination and a hostile work environment.

Why Ackman Went Public

Ackman argued that the claims were constructed after the fact. He wrote that the lawyer had been responsible for workplace compliance at TABLE and had personally delivered sensitivity training to his nephew following earlier complaints.

The American hedge fund manager also alleged she had no prior record of raising alarms about pervasive harassment.

He then laid out the timing. On March 4, when the lawyer was terminated, Ackman’s daughter had suffered a brain hemorrhage on February 5 and had not yet regained consciousness.

He was simultaneously finalizing the private placement round for his Pershing Square IPO, which was filed with the SEC on March 10, targeting $5 billion to $10 billion on the NYSE.

Ackman alleges the lawyer calculated that the reputational risk of a public discrimination lawsuit, combined with the pressure of his daughter’s medical crisis and the IPO timeline, would force him to settle quietly.

Instead, he chose to go public.

“I am going to fight this nonsense to the end of the earth in the hope that it inspires other CEOs to do the same so we shut down this despicable behavior that is a large tax on society, employment, and the economy,” wrote Ackman.

Musk and Chamath Weigh In

The response from other billionaires was swift, with Tesla CEO Elon Musk endorsing that discrimination claim abuse has gone too far.

In the same tone, Chamath Palihapitiya, a VC, revealed his own experience with what he called a shakedown pattern.

He said he had repeatedly paid small settlements of a few million dollars each time before realizing he had become a mark.

He described drawing a hard line and winning in court, vowing never to settle again.

The framing echoes Chamath’s earlier comments on California’s proposed billionaire tax, which he blamed for driving over $1 trillion in taxable wealth out of the state.

BeInCrypto previously reported that the tax debate accelerated relocations to Florida. Among the affected tech and crypto elites are figures like Mark Zuckerberg and Jeff Bezos, who are purchasing properties in Miami’s Indian Creek neighborhood.

A Broader Billionaire Backlash

Ackman’s post fits a growing pattern of high-net-worth individuals pushing back against what they view as legal and fiscal extraction.

From courtroom shakedowns to state-level wealth taxes, billionaires are increasingly choosing confrontation over quiet compliance.

Ackman framed the employment litigation industry as structurally harmful. He argued that because plaintiff attorneys work on contingency and settlements are almost always confidential, there is no reputational cost to filing false claims.

He added that the system increases hiring risk for protected classes rather than reducing discrimination.

Whether his legal strategy succeeds or backfires during a critical IPO window will test whether other CEOs follow his lead or continue paying what Chamath called the tax.

The post Bill Ackman Risks $10 Billion IPO to Expose the ‘Tax’ Every CEO Pays appeared first on BeInCrypto.

Key Takeaways

- Bitcoin hovers between $67,000 and $68,000, attracting investment from ETF managers and national wealth funds

- Ethereum dominates decentralized finance and asset tokenization, while Layer-2 networks slash transaction costs

- Solana continues rapid user expansion thanks to minimal fees and exceptional processing speeds

- Chainlink bridges smart contracts with external data sources and secures partnerships with mainstream finance players

- Bittensor offers decentralized AI infrastructure, rewarding network participants with native tokens

As early 2026 arrives, the cryptocurrency market capitalization hovers around $2.5 trillion. Investors with long time horizons are shifting attention away from volatile price movements toward digital assets backed by genuine utility and adoption.

What follows is an examination of five cryptocurrencies that market observers believe possess robust fundamentals as the industry enters its next growth phase.

Bitcoin: Institutional Treasuries Embrace Digital Scarcity

[[LINK_START_2]]Bitcoin[[LINK_END_2]] operates with a strict ceiling of 21 million tokens. This immutable supply limit establishes a scarcity dynamic unmatched by any traditional or digital asset.

The cryptocurrency presently changes hands in the $67,000 to $68,000 range. Exchange-traded funds holding actual Bitcoin have recorded substantial capital inflows throughout the previous twelve months.

National investment vehicles have incorporated Bitcoin into their asset allocations. Companies following MicroStrategy’s blueprint have increasingly adopted Bitcoin for corporate reserves.

Major financial players now categorize Bitcoin alongside traditional stores of value like precious metals. The asset continues drawing sustained investment from those seeking protection against macroeconomic volatility.

Ethereum: Dominant Force in Programmable Blockchain

[[LINK_START_4]]Ethereum[[LINK_END_4]] runs the vast majority of decentralized financial applications. The network also supports digital collectibles, stablecoins, and an expanding ecosystem of tokenized traditional assets.

Second-layer scaling technologies have dramatically reduced costs while increasing network capacity. The combination of staking rewards and token-burning mechanisms introduced through EIP-1559 creates deflationary pressure on supply.

Exchange-traded products tracking Ether have maintained strong institutional demand. Ethereum continues registering the highest development engagement among all programmable blockchain platforms.

Solana: Speed Meets Affordability

[[LINK_START_6]]Solana[[LINK_END_6]] processes several thousand transactions each second while maintaining negligible fees. The network captured significant market share from users priced out of Ethereum during periods of network congestion.

Consumer-facing applications, viral tokens, and mobile-first crypto experiences have fueled expansion across Solana’s ecosystem. Network stability has strengthened following infrastructure improvements.

Solana’s total valuation remains considerably smaller than Ethereum’s. Market analysts point to this differential as potential upside territory should institutional offerings broaden.

Chainlink: Bridging On-Chain and Off-Chain Worlds

Chainlink operates the most widely adopted oracle infrastructure. The network enables smart contracts to access external information including market prices and third-party application interfaces.

Its Cross-Chain Interoperability Protocol functions across numerous blockchain ecosystems. Chainlink has established relationships with conventional financial entities investigating distributed ledger technology.

As the tokenization of physical assets accelerates, the requirement for trustworthy external data sources should expand in parallel.

Bittensor: Building Decentralized Artificial Intelligence

Bittensor operates an open marketplace for computational power and machine learning algorithms. Network participants receive token compensation for contributing AI resources.

This project involves greater uncertainty compared to the four others discussed here. Both developer engagement and market attention have intensified during the past year.

Bittensor positions itself within decentralized artificial intelligence—a sector gaining prominence as policymakers scrutinize concentrated AI development.

Bitcoin and Ethereum represent the predominant holdings within exchange-traded fund products accessible during 2026.

Crypto World

Drift Protocol Hack: How a North Korean Group Spent Six Months Infiltrating a DeFi Protocol

TLDR:

- Drift Protocol froze all functions after a targeted exploit on April 1, 2026, linked to a state-backed group.

- Attackers posed as a trading firm for six months, meeting contributors in person across multiple countries.

- Three attack vectors were identified, including a silent code execution flaw in VSCode and Cursor editors.

- SEAL911 attributed the attack with medium-high confidence to UNC4736, a North Korean state-affiliated threat actor.

Drift Protocol suffered a major exploit on April 1, 2026, triggering a full protocol freeze. The incident has since been revealed as a structured, months-long intelligence operation.

Forensic partners, including Mandiant, are assisting law enforcement in investigating the breach. Preliminary findings point to a North Korean state-affiliated threat group as the likely perpetrators.

This marks one of the most deliberate social engineering campaigns documented in decentralized finance to date.

A Six-Month Social Engineering Campaign

The attack on Drift Protocol did not begin on the day it occurred. It traces back to Fall 2025, when contributors were approached at a major crypto conference.

The group presented themselves as a quantitative trading firm seeking protocol integration. They were technically fluent and carried verifiable professional backgrounds.

Over the following months, individuals from this group continued meeting Drift contributors in person. These encounters occurred at multiple industry conferences across several countries.

A Telegram group was established from the very first meeting. What followed were months of detailed conversations around trading strategies and vault integrations.

From December 2025 through January 2026, the group onboarded an Ecosystem Vault on the protocol. They deposited over $1 million of their own capital and participated in multiple working sessions.

By February and March 2026, the protocol noted that “these were not strangers; they were people Drift contributors had worked with and met in person.” Links to projects, tools, and applications were routinely shared throughout this period.

The investigation later revealed that “the profiles used in this operation had fully constructed identities including employment histories, public-facing credentials and professional networks.”

Contributors engaged with them across detailed product discussions. This built a credible operational presence inside the Drift ecosystem over time.

Three Attack Vectors and North Korean Attribution

After the April 1 exploit, a forensic review of affected devices and communications flagged the trading group as the likely intrusion vector.

Their Telegram chats and malicious software were completely wiped right after the attack. Three potential attack vectors have since emerged from the ongoing investigation.

One contributor may have cloned a code repository shared by the group. It was presented as a frontend deployment for their vault. Another contributor was induced to download a TestFlight application framed as the group’s wallet product.

Regarding the repository-based vector, “simply opening a file, folder, or repository in the editor was sufficient to silently execute arbitrary code, with no prompt or indication to the user, clicks, permissions dialog or warning of any kind.”

Full forensic analysis of affected hardware remains ongoing. Drift has since urged the broader ecosystem to “check in on your teams, audit who has access to what, and treat every device that touches your multisig as a potential target.”

With medium-high confidence, the SEALS 911 team assessed this as the work of UNC4736. That group is a North Korean state-affiliated actor tracked as AppleJeus or Citrine Sleet.

On-chain fund flows and overlapping personas connect this campaign to the October 2024 Radiant Capital hack. The individuals who appeared in person were not North Korean nationals, as DPRK threat actors are known to use third-party intermediaries for direct contact.

Oscar De La Hoya says he’s ready to make come back to face one man: “I’ve put in the work”

Milestone moon mission is getting a push from Pacific Northwest tech

Easter treat that can help lower blood pressure – but Brits must be specific on choice

-

NewsBeat3 days ago

NewsBeat3 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business2 days ago

Business2 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Spanx – Corporette.com

-

Entertainment6 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World4 days ago

Crypto World4 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech6 days ago

Tech6 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World5 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech6 days ago

Tech6 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Business3 days ago

Business3 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Sports13 hours ago

Sports13 hours agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech6 days ago

Tech6 days agoApple will hide your email address from apps and websites, but not cops

-

Sports5 days ago

Sports5 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech5 days ago

Tech5 days agoEE TV is using AI to help you find something to watch

-

Politics6 days ago

Politics6 days agoShould Trump Be Scared Strait?

-

Tech5 days ago

Tech5 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech7 days ago

Tech7 days agoElon Musk’s last co-founder reportedly leaves xAI

-

Fashion6 days ago

Fashion6 days agoThe Best Spring Trends of 2026

-

Tech5 days ago

Tech5 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Crypto World6 days ago

Bitcoin’s Six-Month Losing Streak: What On-Chain Data Says About the Market’s Next Move

-

Politics6 days ago

Politics6 days agoBBC slammed for ignoring author of The Fraud

You must be logged in to post a comment Login