Crypto World

XRP reserves at 7-year low: the signal that matters

XRP on exchanges just hit a seven-year low. Whales now hold a record share of supply. Both are bullish-sounding headlines, but one of them is the signal that actually matters, and understanding which is the difference between reading the chart and reading the noise.

Summary

- XRP exchange reserves are the cleaner signal because they measure sellable supply.

- Whale concentration is dramatic but ambiguous, because large holders can hold or sell.

- Thin exchange supply can amplify a CLARITY-driven demand shock.

- The setup points to higher sensitivity, not guaranteed upside.

Two on-chain numbers are circulating about XRP right now, and both sound bullish. The first: whale wallets, those holding 10 million or more XRP, now control 68.5% of the circulating supply, the highest concentration since May 2018.

The second: XRP held on exchanges has fallen to a seven-year low of roughly 1.6 billion tokens, down about 50% from the 3.76 billion peak of October 2025. Both get cited as evidence that something bullish is building, but they are not equally meaningful, and treating them as interchangeable misreads the setup.

One describes who owns XRP, which is interesting but ambiguous. The other describes how much XRP is available to sell, which is the number that actually shapes what happens when demand arrives.

The exchange-reserve drawdown matters more than the whale count, and understanding why is the difference between reading the signal and repeating the headline.

This piece works through both metrics and explains why the exchange-reserve figure is the one to watch. It covers what exchange reserves actually measure and why a seven-year low matters, why the whale-concentration number is more ambiguous than it sounds, how the two combine with the CLARITY Act catalyst to create a genuine supply-demand setup, and how to read all of it without overreacting.

The goal is not to predict a price but to understand the mechanics. Thin available supply meeting a potential demand catalyst is what would drive a violent move if one comes, and those mechanics are frequently misunderstood.

What exchange reserves measure, and why a seven-year low matters

That exchange-reserve figure is the more important of the two, so it deserves the careful explanation, because its significance is precise and often muddled.

Exchange reserves are the amount of a cryptocurrency held in wallets belonging to exchanges, and they function as a proxy for the supply readily available to be sold. When XRP sits on an exchange, it is positioned to be sold quickly, because selling on an exchange is frictionless.

Exchange-held coins therefore represent the most immediately available sell-side liquidity. When XRP leaves exchanges and moves into private wallets, it generally signals that holders are moving it into longer-term storage, off the trading venues and out of immediate selling range.

So a falling exchange reserve means less XRP is sitting in a position to be sold. The seven-year low of roughly 1.6 billion tokens, down about half from the late-2025 peak, means the readily sellable supply of XRP has compressed dramatically to a multi-year minimum.

This matters because of what it implies for price dynamics when demand arrives. Price is set at the margin by the balance between buyers and sellers, and the supply available to sell is one half of that balance.

When the readily available supply is large, incoming demand can be met by sellers without the price moving much, because there is plenty of XRP positioned to sell into the buying. When the readily available supply is thin, as a seven-year reserve low indicates, incoming demand has less supply to absorb it.

The same amount of buying pressure therefore produces a larger price move because there is less XRP available to satisfy it. A compressed exchange reserve is, in effect, a coiled spring on the supply side: it does nothing on its own, but it sets up a condition where any significant demand meets thin supply and the price can move violently.

That is why the seven-year low is the number that matters. It describes the supply side of the equation that determines how XRP responds to demand.

Why the whale-concentration number is more ambiguous

The whale figure draws more attention because it sounds dramatic, but it is more ambiguous than the reserve number, and the ambiguity is worth understanding rather than glossing over.

The fact that wallets holding 10 million or more XRP control 68.5% of circulating supply, the highest since 2018, is usually presented as bullish, on the logic that whales are accumulating and their conviction signals confidence. There is something to that: the broader accumulation data is real, with the number of wallets holding 10,000 or more XRP at an all-time high and the millionaire tier adding addresses and tokens through the drawdown.

But the concentration figure itself cuts both ways, and the bullish reading is not the only one. High concentration means a large share of the supply sits in a small number of hands, and those hands can sell as well as hold.

That makes high whale concentration also a concentration of potential selling pressure, a risk that a few large holders deciding to exit could move the price down hard. Concentration is not inherently bullish; it is a description of who holds the supply, and what that means depends on what those holders do.

A deeper ambiguity: whale wallets are hard to interpret cleanly. A wallet holding 10 million XRP could belong to a long-term accumulator, an exchange’s cold storage, a custodian holding on behalf of many clients, an institution, or an early holder sitting on a position, and these have very different implications.

Escrow activity adds another layer of complexity to the supply picture, because large token movements can look dramatic without directly translating into immediate sell pressure. That is why the context around locked and re-locked XRP matters.

Rising whale concentration could mean conviction-driven accumulation, or it could partly reflect coins moving into custodial and institutional storage as the asset matures, which is a different phenomenon with a different meaning. The whale count tells you that supply is concentrated, but it does not reliably tell you why or what those holders intend.

That makes it a noisier signal than the clean supply-availability reading of the exchange reserve. The whale number is interesting context, but it is ambiguous in a way the reserve figure is not, and leaning on it as a clear bullish signal reads more certainty into it than it supports.

Why the reserve figure is the cleaner signal

Putting the two side by side clarifies why one is the signal and the other is the context, and the distinction comes down to what each number actually determines.

The exchange-reserve figure measures something mechanically connected to price action: the supply available to sell. That connection is direct and not very ambiguous, because whatever the reason XRP is leaving exchanges, the effect is the same: less supply positioned to sell, which tightens the supply side of the market.

A seven-year reserve low means thin sell-side liquidity, and thin sell-side liquidity means demand moves the price more, regardless of the motivations behind the reserve drawdown. The signal is clean because it does not require interpreting intent.

It describes a structural condition of the market that holds however it came about. This is the kind of on-chain metric that really informs how the price might behave, because it measures the actual scarcity of sellable supply.

Whale concentration, by contrast, measures who holds the supply, which is one step removed from price action and heavily dependent on interpretation. To translate whale concentration into a price implication, you have to guess what the whales are and what they will do.

That guess is where the signal gets noisy, because the same concentration number is bullish if the whales hold and bearish if they sell, and you usually cannot tell which from the number alone. The reserve figure tells you the supply is scarce; the whale figure tells you the supply is concentrated and leaves you to guess what that means.

Escrow headlines work similarly: they can matter, but they need interpretation before they become a price signal. A lockup can reduce immediate circulating pressure, but it still has to be read alongside exchange balances, market demand, and timing.

For reading how XRP might respond to a demand catalyst, the scarcity of sellable supply is the more useful and more reliable input. That is why the seven-year reserve low deserves more weight than the record whale concentration, even though the whale number makes the more dramatic headline.

The cleaner signal is the one that does not depend on reading minds.

How it combines with the CLARITY catalyst

The reserve figure matters most because of what it sets up in combination with a specific potential demand catalyst, and that combination is the real story underneath both numbers.

XRP sits in front of a concrete potential demand event: the CLARITY Act. If passed, it would codify XRP’s commodity status into federal law and, by analysts’ projections, could unlock $4 billion to $8 billion in ETF inflows as institutions gain the legal certainty they have waited for.

That is the demand catalyst the supply meets. Its impact depends heavily on the supply conditions it meets.

If a multi-billion-dollar wave of institutional buying arrives into a market with abundant sellable supply, the supply absorbs much of the demand and the price moves less. If it arrives into a market with a seven-year low in available supply, the thin sell side cannot absorb the demand without a much larger price move.

The exchange-reserve drawdown is precisely what would amplify the effect of a CLARITY-driven demand shock. It turns a given amount of buying into a larger price response because there is so little XRP positioned to sell into it.

This is why the reserve figure is the one to watch in the current setup: it is the supply-side condition that determines how violently XRP would react to the demand-side catalyst that the CLARITY Act represents. Two blades of the scissor are demand and supply: the potential CLARITY inflows on one side and the compressed available supply on the other.

A sharp move requires both, strong demand meeting thin supply. Whale accumulation is consistent with this picture and may be part of why reserves have fallen, as large holders move coins off exchanges into storage.

But it is the resulting supply scarcity, not the concentration itself, that would amplify a demand shock. That is why the demand side of the setup matters as much as the reserve chart: the supply squeeze only becomes price action if buyers actually arrive.

The setup that matters is thin sellable supply waiting in front of a potential large demand catalyst, and the seven-year reserve low is the measure of how thin that supply has become. That combination, not the whale headline, is what would drive a violent move if CLARITY passes.

The bearish reading, honestly stated

A fair analysis has to state the other side, because the same setup that could amplify an upside move carries real risks, and the supply-squeeze story is not a guarantee of anything.

One caution is that thin supply amplifies moves in both directions. A compressed exchange reserve means demand moves the price more, but it also means that if selling pressure arrives, perhaps from the very whales whose concentration is at a record, the thin liquidity amplifies the downside too.

There are fewer buyers positioned to absorb a wave of selling. A coiled spring can release in either direction, and a market with thin liquidity and concentrated holdings is one where a few large holders deciding to sell could produce a sharp decline.

That is exactly the risk the whale-concentration figure embodies. The supply-squeeze setup is not inherently bullish; it is a condition of heightened sensitivity to whatever demand or supply shock arrives, and the direction depends on which shock comes first.

Another caution is that the entire upside case depends on the CLARITY catalyst actually arriving, which is deeply uncertain. The demand shock that thin supply would amplify is contingent on the bill passing and the institutional inflows materializing.

That is why a statute changes the picture: without legal certainty, the institutional demand side may not arrive in the size the setup needs.

If CLARITY stalls or fails, the demand catalyst does not arrive, the thin supply does nothing on its own, and XRP can continue to drift or fall on the same macro forces pressuring the whole market. A coiled spring with no force applied to it simply sits there.

A supply squeeze without a demand catalyst is not a bullish setup but a neutral one waiting for an input that may not come. The honest reading is that the seven-year reserve low is a genuine and meaningful supply-side condition, but it is a setup, not a prediction.

It points to amplified volatility, not guaranteed upside, with the direction and the timing both dependent on catalysts outside the on-chain data. The mechanics are real; the outcome is not foreordained.

What it means for investors

For anyone reading these on-chain figures, the practical lesson is about which numbers to trust and how to think about what they imply.

One takeaway is to weight the exchange-reserve figure over the whale-concentration figure when assessing XRP’s setup, because the reserve number cleanly measures sellable supply while the whale number ambiguously measures ownership. Sellable supply is what shapes how the price responds to demand.

An investor watching XRP should treat the seven-year reserve low as the more meaningful signal, the indication that the supply side is tight and that any significant demand would have outsized price impact. The record whale concentration should be treated as interesting but ambiguous context that could be bullish accumulation or a concentration of selling risk.

Reading the cleaner signal over the dramatic headline is the discipline that distinguishes informed analysis from repeating talking points.

Another takeaway is to understand the setup as conditional, not predictive. Thin supply is a real condition, but it produces a move only when a catalyst applies force, and the most likely near-term catalyst is the binary CLARITY vote, which could unlock major demand or fail to arrive at all.

XRP’s broader ecosystem also matters here, because the supply-demand setup sits alongside XRP’s institutional utility case, including tokenized settlement and RLUSD-linked infrastructure. Utility can support the long-term thesis, but it still needs a clear demand channel to move price.

An investor should hold the supply-squeeze setup as a reason XRP could move sharply if a demand catalyst lands, not as a standalone bullish signal. It should be paired with a clear-eyed view of the catalyst’s uncertainty and of the downside risk that thin liquidity and concentrated holdings also create.

The setup amplifies whatever comes; it does not determine what comes. That is also part of the longer-term outlook, where legal clarity, ETF flows, tokenized settlement, and supply conditions all interact rather than moving in isolation.

None of this is investment advice; it is a frame for reading two widely cited on-chain numbers accurately, weighting the one that measures available supply over the one that measures concentration, and understanding both as conditions that shape volatility, not predictions of direction.

The signal and the noise

Two on-chain numbers about XRP are circulating, and they are not equally meaningful. The record whale concentration of 68.5% makes the dramatic headline, but it is ambiguous, measuring who holds the supply without reliably telling you why or what they will do.

It cuts both ways between bullish accumulation and concentrated selling risk. The seven-year low in exchange reserves makes the quieter headline, but it is the cleaner signal.

It measures the supply available to sell and points to a multi-year minimum in sellable XRP, a structural condition that shapes how the price would respond to demand regardless of anyone’s intentions.

The reserve figure matters more for what it sets up: thin sellable supply waiting in front of a potential large demand catalyst in the CLARITY Act, a combination where a multi-billion-dollar inflow meeting a compressed supply could produce an outsized move. That is a genuine and meaningful setup, but it is a setup, not a prediction, because the thin supply amplifies moves in both directions and the upside depends entirely on a demand catalyst that may or may not arrive.

Read accurately, XRP’s on-chain picture is one of tight available supply and concentrated ownership sitting in front of a binary legislative catalyst. It is a condition of heightened sensitivity rather than a guarantee of direction.

The seven-year reserve low is the number that matters, the whale count is the number that gets attention, and knowing the difference is the difference between reading the signal and repeating the noise.

Frequently asked questions

What does it mean that XRP exchange reserves hit a seven-year low?

Exchange reserves are the amount of XRP held in exchange wallets, a proxy for the supply readily available to sell. The seven-year low of roughly 1.6 billion tokens, down about 50% from October 2025’s 3.76 billion peak, means the readily sellable supply of XRP has compressed to a multi-year minimum. This matters because thin sell-side supply means incoming demand has less to absorb it, so the same buying pressure can produce a larger price move.

Why does the article say reserves matter more than the whale count?

Because the reserve figure cleanly measures sellable supply, which directly shapes how the price responds to demand, while the whale-concentration figure ambiguously measures who owns the supply, one step removed from price action. To turn whale concentration into a price implication, you have to guess what the whales are and will do. The reserve figure needs no such guess, since less supply on exchanges tightens the market regardless of why it left. The cleaner signal is the more reliable one.

Is the record whale concentration bullish for XRP?

It is more ambiguous than it sounds. Whales holding 68.5% of supply, the highest since 2018, is often read as bullish accumulation, and the broader data does show large holders buying through the drawdown. But high concentration also means potential selling pressure sits in few hands, a risk if those holders exit. And whale wallets can be accumulators, custodians, exchanges, or institutions, with different meanings, so the number is noisy context rather than a clear bullish signal.

How does the supply squeeze connect to the CLARITY Act?

The CLARITY Act, if passed, would codify XRP’s commodity status and could unlock $4 billion to $8 billion in ETF inflows by analyst projections, a large demand catalyst. Thin available supply amplifies the effect of demand: a multi-billion-dollar inflow meeting a seven-year low in sellable XRP could produce a much larger price move than the same demand meeting abundant supply. The reserve drawdown is what would amplify a CLARITY-driven demand shock.

Does a low exchange reserve guarantee the price will rise?

No. Thin supply amplifies moves in both directions: if selling pressure arrives, perhaps from concentrated whale holders, thin liquidity amplifies the downside too. And the upside case depends on a demand catalyst, mainly the CLARITY vote, actually arriving; if it stalls, the thin supply does nothing on its own and XRP can keep drifting on macro forces. The reserve low is a setup that heightens sensitivity to catalysts, not a prediction of direction.

What should investors take from these on-chain numbers?

Weight the exchange-reserve figure over the whale-concentration figure, because it cleanly measures sellable supply while the whale number ambiguously measures ownership. Treat the seven-year reserve low as a meaningful sign that supply is tight and demand would have outsized impact, and the whale concentration as ambiguous context. Understand the setup as conditional: thin supply produces a move only when a catalyst applies force, and the main near-term catalyst, the CLARITY vote, is uncertain and could push either way.

As of June 19, 2026. On-chain data and markets change quickly; verify current figures before relying on this analysis. This article is information, not investment advice.

Bitcoin (BTC) has fallen roughly 50% since Michael Saylor’s Strategy launched Stretch (STRC), its flagship Bitcoin-funding vehicle, in late July 2025.

BTC/USD monthly chart. Source: TradingView

Key takeaways:

- STRC is acting like a classic Ponzi scheme, argue Peter Schiff and other critics.

- Other analysts disagree, noting that STRC’s drop below the $100 par is due to a leverage wipeout.

Critics say STRC looks like a “classic centralized Ponzi”

STRC was designed to trade near its $100 par value, enabling Strategy to raise capital to buy more Bitcoin. The instrument is now trading at a deep discount, suggesting that the BTC buying channel is under pressure.

On Thursday, STRC fell to a record low of $82.53 before closing at $88.59, still below the $100 par value.

STRC daily chart. Source: TradingView

Launched in July 2025, STRC was designed to trade near par through adjustable dividends, currently 11.5% annualized, with proceeds used primarily to acquire Bitcoin.

The widening discount has pushed STRC’s effective yield above 12.9% and contributed to a pause in at-the-market share issuance. That risks slowing down the capital-raising flywheel behind Strategy’s Bitcoin treasury, which now holds more than 846,000 BTC.

In finance, a “flywheel” is a self-reinforcing business model where growth in one metric directly helps grow another, compounding momentum.

But trading 13% below par has revived criticism of Strategy’s funding model.

Bitcoin critic Peter Schiff has repeatedly described STRC as “a classic centralized Ponzi,” arguing that it depends on Strategy’s ability to raise fresh capital through new share sales or sell Bitcoin to meet obligations.

Source: X/Peter Schiff

Crypto trader DonAlt also questioned STRC’s recent price action, asking why the instrument was “trading like a Ponzi” after its sharp move below par.

Strategy has not directly addressed this in recent statements, instead continuing to present STRC as preferred equity supported by its Bitcoin-focused treasury strategy.

However, the company has moved STRC to a semi-monthly dividend schedule, with payouts now designed to occur twice a month rather than monthly.

Strategy’s Bitcoin buying pace slows as STRC slumps

The pace of Strategy’s Bitcoin accumulation has slowed sharply as STRC trades below par value.

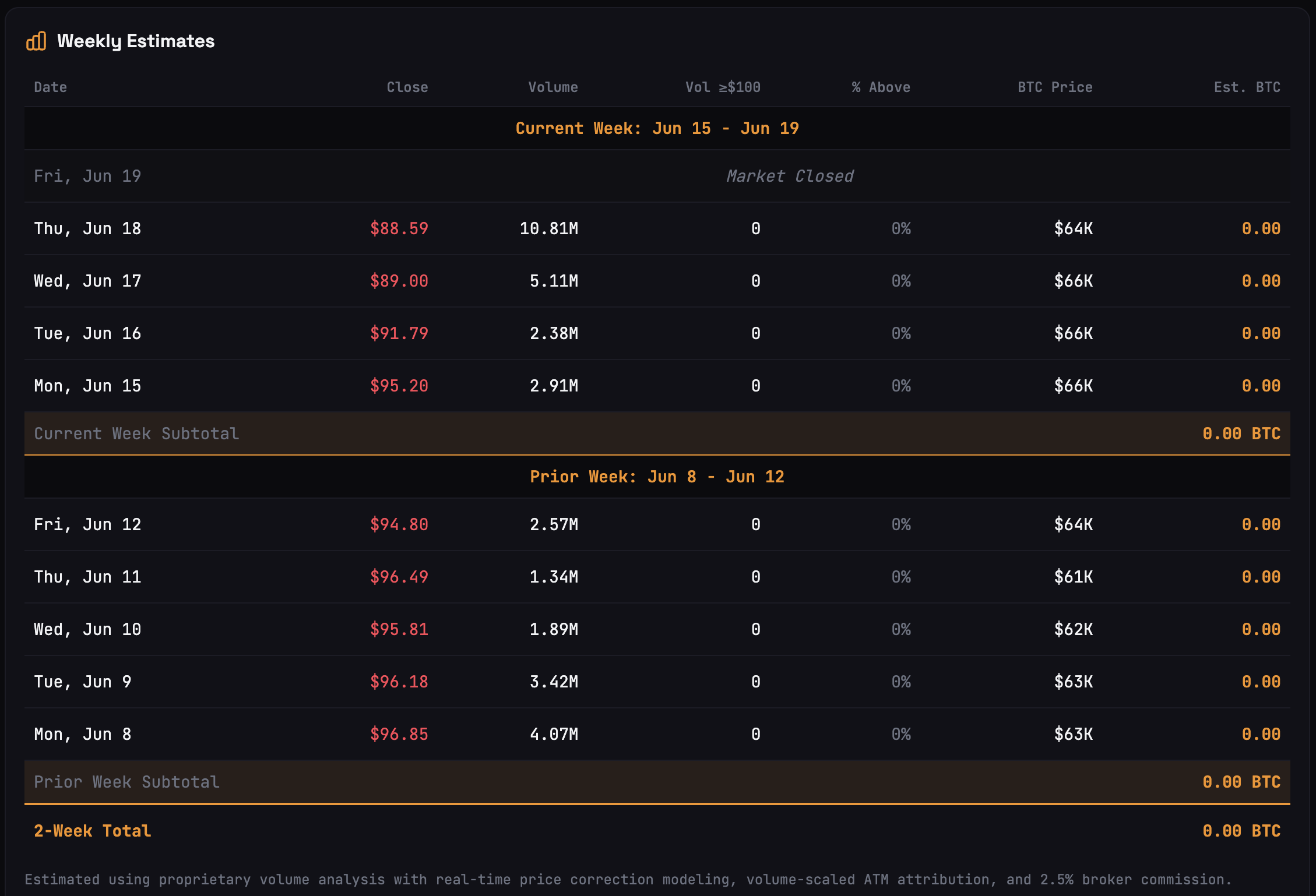

The company added 1,550 BTC for $101 million in the week ending June 8 and another 1,587 BTC for $100 million in the week ending June 15, lifting total holdings to 846,842 BTC.

Those were meaningful purchases, but they were far smaller than Strategy’s weekly buys earlier in 2026.

For instance, in April, Strategy bought 34,164 BTC for $2.54 billion in a single week. In May, it added another 24,869 BTC for roughly $2.01 billion. By contrast, June’s weekly additions have been closer to $100 million each.

The slowdown also coincided with a small but notable 32 BTC sale earlier in June, worth about $2.5 million, to help cover dividend obligations.

Related: Bitcoin price sets $64.5K week-to-date low as Strategy selling worries return

The sale was tiny compared with Strategy’s overall Bitcoin treasury, but it showed that cash obligations can still force limited BTC sales when STRC-led funding becomes less efficient.

STRC-led weekly BTC buying estimates. Source: STRC.LIVE

Analyst says STRC drop is a leverage wipeout

The STRC sell-off looked more like a leverage wipeout than a deterioration in Strategy’s fundamentals, according to Jesse Myers, head of Bitcoin strategy at The Smarter Web Company.

“Strategy is fine,” he said in a Thursday post, adding that the company could pay STRC dividends for 32 years if conditions remain unchanged, and indefinitely if Bitcoin appreciates at roughly 2% annually.

STRC’s long stretch near $99–$100 encouraged investors to use heavy leverage, with some assuming the instrument would stay above $95. Once the price slipped, margin calls and forced selling accelerated the decline.

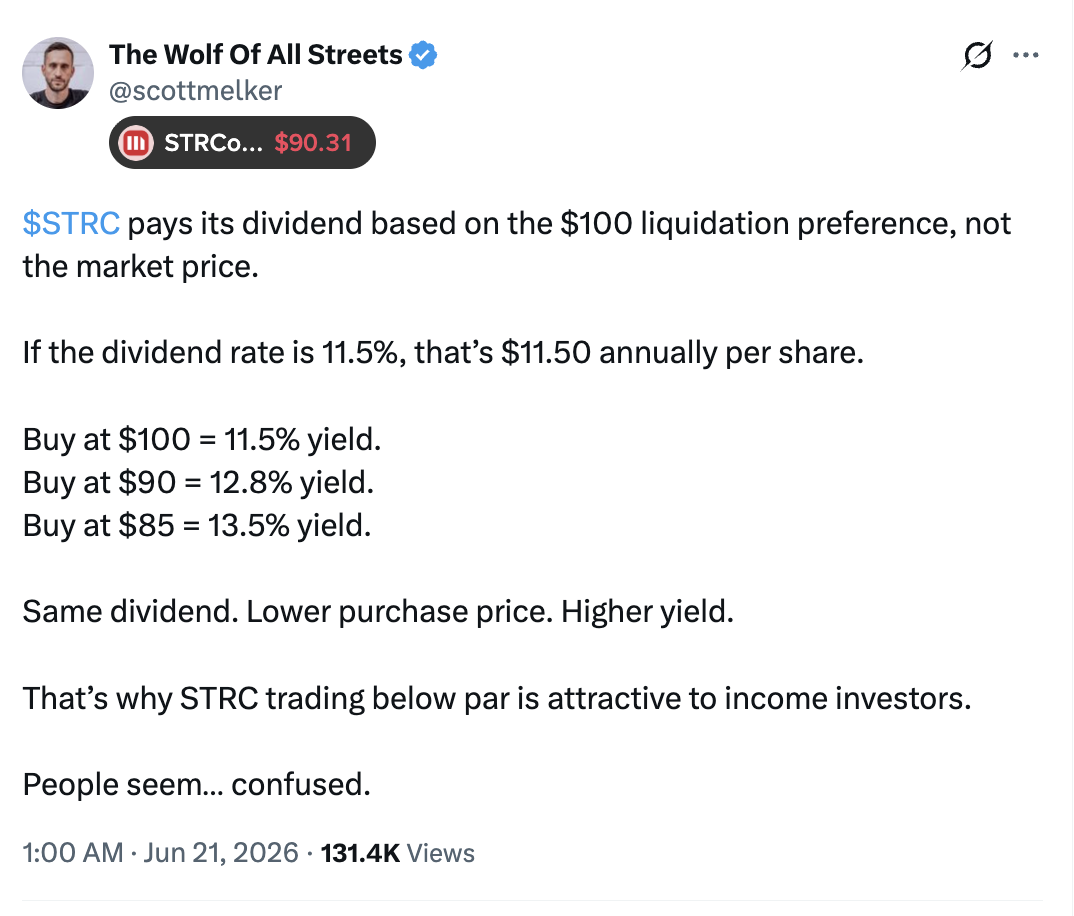

The discount may also attract income buyers, according to analyst Scott Melker.

In a Sunday post, he noted that STRC’s dividends are based on the $100 liquidation preference, not the market price. At an 11.5% dividend rate, buyers at $90 earn about 12.8%, while buyers at $85 earn roughly 13.5%.

Source: X/Scott Melker

At current prices, STRC offers an effective yield of about 13%. Strategy may announce its next dividend rate on June 30, while retaining other options, including MSTR share issuance and cash reserves, to fund its Bitcoin purchases.

Bitcoin can survive another price crash as it has done so many times in the past, reassured the CEO of CryptoQuant, Ki Young Ju.

However, he envisions another major threat for the asset – boredom, and he linked it to Strategy’s STRC shares, which have raised some eyebrows in the past few weeks.

Boredom, Not a Crash

If you have followed the cryptocurrency industry for a few (or more) years, you are probably aware of its intense volatility at times. Bitcoin has been the object of some mind-blowing fluctuations, up or down. Of course, the skyrocketing liquidations on the way down are usually the ones people read about, and don’t get me wrong, there have been plenty of instances in which the asset has tumbled by double digits daily. However, it has also risen in the opposite direction violently before.

Naturally, the current market state and the past several months, starting with the early October massacre, the February calamity, and the June crash, are examples of bear-dominated trends. Nevertheless, BTC has managed to withstand all of those and has (for now) returned stronger than before.

Consequently, CryptoQuant’s chief exec didn’t seem too bothered about the potential of another crash. However, he believes boredom could pose a more profound threat, especially if Strategy’s controversial Stretch (STRC) fails to operate as intended.

“Strategy’s STRC structure becomes truly dangerous not when Bitcoin simply crashes, but when Bitcoin spends years moving sideways, and the bear market drags on.”

He added that “long stagnation kills the story,” as BTC can survive another crash if the market still believes in the next leg up. However, weak demand due to stagnation leads to compressed MSTR premium and makes “Saylor’s capital-raising machine much harder to sustain.”

A Reason to Believe

Young Ju further explained that the real challenge for Saylor and his company is not just to keep buying bitcoin, but to give the market “a new reason to believe.”

“After nearly a decade in this industry, I’ve realized Bitcoin’s core has not really changed. What changes every cycle is the story around why BTC price should keep going up. But, most of those stories now feel exhausted.”

He warned that BTC failed to serve as digital gold when it was needed, as it traded like a tech stock. It was supposed to be freedom money built by cypherpunks, but many OGs are now shilling other coins. It also faces the rising threat of advanced quantum computing.

Although he remains a firm believer that “the pool of capital that could flow into Bitcoin is massive,” he noted that the “sense of an inevitable catalyst feels much weaker” now compared to 10 years ago.

“It makes me a little sad to see the ideas that originally pulled me in gradually get consumed and diluted: freedom money, energy money, and institutional adoption.”

The post Bitcoin’s Biggest Risk Is Boredom, Not Another Price Crash: CryptoQuant CEO appeared first on CryptoPotato.

TLDR

- The XRP Ledger’s core server software xrpld v3.2.0 launched June 15, targeting 30–40% memory optimization

- Node operators and developers identified several technical issues via GitHub shortly after deployment

- A node operator experienced complete sync failure post-upgrade despite previous version stability

- Reported issues encompass configuration parsing problems, transaction relay defects, and validator data distribution gaps

- Adoption remains at 26% network-wide; no critical network failures documented

Following the June 15 deployment of xrpld version 3.2.0, the XRP Ledger development community has documented numerous technical issues with the network’s updated core server infrastructure.

The software update promised notable enhancements including performance optimization and a projected 30% to 40% decrease in memory consumption. The release also transitioned the server nomenclature from “rippled” to “xrpld” while incorporating enhanced security protocols.

Yet, shortly following the launch, node administrators and software engineers started documenting problems through the official GitHub issue tracker.

Synchronization Problems and Configuration Glitches

A node administrator documented that their infrastructure running v3.2.0 completely failed to retrieve ledger information following the update. The system maintained connection status but synchronization ceased entirely. Notably, identical hardware performed flawlessly under version 3.1.3. This issue, submitted June 18, awaits resolution.

Another documented problem reveals that configuration files containing inline comments trigger server crashes during initialization. The legacy parsing system fails to properly handle comments in specific parameters, generating a “BadLexicalCast” exception.

Project maintainers have validated multiple reports as legitimate defects requiring technical assessment.

Relay and Validator Network Concerns

Engineers identified a defect affecting transaction propagation mechanisms to network peers. A computational error restricts the number of peers receiving transaction broadcasts, potentially causing insufficient network distribution.

The resource fee tracking mechanism also drew scrutiny. The current implementation only preserves the maximum fee value while discarding previous entries, behavior developers classify as erroneous.

Validator list propagation presented another challenge. Currently, validator metadata transmits exclusively to inbound peer connections while excluding outbound links. This asymmetry affects validator information distribution throughout the network infrastructure.

Developers identified potential unsigned integer overflow vulnerabilities during ledger sequence validation processes. Additional reports highlighted inconsistent transaction routing parameters and compromised node identification when utilizing ephemeral cryptographic keys.

A further report outlined a logical deficiency in ledger state tracking that can strand nodes in undefined states without established recovery procedures.

Current Status Assessment

Presently, none of the documented defects have triggered network-wide service disruptions. The XRP Ledger Foundation alongside open-source development contributors continue examining all submitted reports via the project’s GitHub platform.

Network adoption of version 3.2.0 currently stands at 26%. The substantial majority of nodes continue operating on previous software releases.

The XRP Ledger Foundation has not released official communications or remediation patches at publication time. All identified issues remain under ongoing technical evaluation.

Key Takeaways

- Scaramucci anticipates Bitcoin will begin its upward momentum in Q4 2026 through early 2027

- He dismisses concerns about Michael Saylor and Strategy, calling them financially secure

- Strategy maintains approximately $52 billion in Bitcoin holdings plus $1 billion cash reserves

- Declining retail interest and reduced Google search activity represent bullish indicators in his view

- ETF capital flows and institutional accumulation have created a less volatile cycle compared to previous periods

Anthony Scaramucci, founder of SkyBridge Capital, told CNBC that Bitcoin remains aligned with its traditional four-year market cycle. He anticipates an upward price movement commencing in late 2026 and extending into the first quarter of 2027.

According to Scaramucci, the current market cycle has exhibited less volatility than previous iterations. Bitcoin experienced approximately 50% retracement from peak levels, significantly less than the 60–70% corrections observed in earlier cycles. He attributes this moderation to sustained ETF capital inflows and growing institutional participation.

“I think Bitcoin starts to rally late in the fourth quarter of 2026 into early 2027,” he said.

Scaramucci identified diminishing market attention as an encouraging development. Search volume for Bitcoin on Google has declined substantially, and retail investor enthusiasm has waned. He characterized this apathy as a pattern that typically emerges near cycle lows rather than market peaks.

He emphasized that Bitcoin’s market remains comparatively modest in size. Consequently, even limited fresh capital entering the market can generate substantial price appreciation. Scaramucci disclosed that he maintains significant personal Bitcoin exposure.

“I still like it. I own a lot of it,” he said.

Strategy’s Position Draws Support From Scaramucci

Scaramucci dismissed criticisms surrounding Strategy’s substantial Bitcoin position. He highlighted Michael Saylor’s access to robust capital markets and a solid financial foundation.

“You have to really understand the mechanisms of the balance sheet to understand that Bitcoin can go a lot lower, and he’s virtually not in trouble,” he said.

Strategy’s Bitcoin treasury stands at approximately $52 billion in current value. This reserve provides coverage for 31 months of dividend payments and interest commitments. The firm additionally maintains $1 billion in liquid cash reserves.

No significant debt obligations come due before 2028. Saylor has stated publicly that Strategy can continue servicing its preferred stock dividends and enhancing shareholder returns as long as Bitcoin appreciates by a minimum of 1.25% annually.

Scaramucci observed that Strategy’s equity continues trading at a premium relative to its underlying Bitcoin reserves. He suggested this premium provides investors with “necessary arbitrage” opportunities that justify the investment thesis.

“I like him. I think he’s going to be right,” Scaramucci said of Saylor.

He further mentioned that recent geopolitical developments and declining energy costs could suppress inflationary pressures. Should this scenario materialize, the Federal Reserve might implement interest rate reductions, potentially benefiting Bitcoin and broader risk assets.

Drawing on nearly four decades of investment experience, Scaramucci characterized the present market conditions as a late-cycle deceleration rather than the conclusion of Bitcoin’s long-term appreciation trajectory.

Quick Summary

- Total net revenue for 2025 reached $4.5B at Robinhood, representing a 52% annual increase

- First quarter 2026 brought $1.07B in revenue (up 15%), while Gold membership reached 4.3 million users

- Wall Street’s consensus 12-month target averages approximately $112, marginally exceeding today’s ~$108 trading level

- Projections for 2031 suggest a baseline target near $148, with optimistic scenarios approaching ~$293

- Probability-weighted analysis indicates a 2031 price around $156, representing potential gains of ~44% from present values

Robinhood (HOOD) stock currently hovers around the $108 mark, prompting investors to question its trajectory over the coming half-decade.

The trading platform delivered $4.5 billion in consolidated net revenue throughout 2025, marking a substantial 52% year-over-year expansion. Profitability metrics showed strength as well, with net income totaling $1.9 billion while adjusted EBITDA surged 76% to reach $2.5 billion.

Momentum carried into the first quarter of 2026. Robinhood generated $1.07 billion in quarterly revenue, reflecting 15% growth compared to the same period a year earlier. Earnings per share on a diluted basis landed at $0.38, representing a 3% improvement. The premium Gold subscription service expanded its user base by 36%, hitting an all-time high of 4.3 million subscribers.

Operational metrics from May painted an even stronger picture. The platform’s funded customer count climbed to 27.7 million, while aggregate platform assets swelled to $377 billion—a 48% year-over-year jump. During Q1 alone, net deposits totaled $17.7 billion.

The company has evolved significantly beyond its original retail equity trading roots. Today, Robinhood encompasses options trading, cryptocurrency transactions, retirement planning tools, banking services, credit card offerings, prediction market participation, and access to private market opportunities.

Exploring Three Distinct Price Scenarios

Three potential pathways illustrate where HOOD shares might trade by 2031.

Under a bearish scenario, annual revenue reaches approximately $6.5 billion, but compressed margins and subdued trading activity constrain profitability. Applying a 22x price-to-earnings ratio yields a potential stock price around $35.

The baseline projection estimates annual revenue of roughly $10 billion by 2031. Assuming net profit margins stabilize around 35% and earnings per share hit $3.90, a 38x valuation multiple suggests a price target near $148.

An optimistic scenario envisions Robinhood successfully constructing a comprehensive financial ecosystem. Should revenue climb to $14 billion with EPS reaching $6.50, a 45x earnings multiple would support a stock price approaching $293.

Balancing these scenarios through probability weighting produces a 2031 target price around $156—translating to approximately 44% appreciation from current levels, or roughly 7.5% compound annual growth.

Wall Street’s Current Perspective

Analyst sentiment toward Robinhood remains constructive, though enthusiasm appears measured.

MarketBeat data reveals HOOD holds 18 Buy recommendations, 5 Hold ratings, and no Sell opinions. The overall consensus stands at Moderate Buy. However, the mean 12-month price objective sits around $112—only marginally higher than current trading levels.

This modest near-term target despite positive ratings suggests analysts recognize the long-term opportunity while acknowledging limited immediate upside following the stock’s recent appreciation.

Several headwinds warrant consideration. Current valuation multiples appear elevated. Transaction-based revenue streams face cyclical pressures. Cryptocurrency markets exhibit high volatility. The regulatory environment remains uncertain. Established financial institutions pose formidable competitive challenges.

Conversely, Robinhood possesses meaningful competitive strengths—including a substantial, demographically young customer base, expanding subscription-driven revenue from Gold memberships, growing assets under administration, and continuous product portfolio diversification.

Realistic modeling places the 2031 price range between $150 and $160. Achieving the $293 bull case target would require Robinhood to successfully transform into a comprehensive financial super app serving next-generation consumers.

Blockstream CEO Adam Back said concerns over Strategy’s small Bitcoin sale are overblown, framing the move as normal treasury management rather than a warning sign for the company’s Bitcoin plan.

Summary

- Adam Back said Strategy’s small Bitcoin sale showed balance sheet flexibility, not bearish treasury change.

- Strategy sold 32 BTC for about $2.5 million to fund preferred stock dividend payments due.

- Crypto.news later reported Strategy bought 1,550 BTC, keeping its accumulation story active for now again.

Speaking in a Bloomberg interview shared on YouTube, Back addressed questions about Strategy selling 32 BTC to help pay preferred stock dividends. He said the sale showed the firm could meet obligations while keeping Bitcoin at the center of its balance sheet.

Back frames sale as balance sheet use

Back argued that the market should not treat the 32 BTC sale as a bearish signal. In his view, Strategy used a small part of its Bitcoin position to support investor payments and reduce pressure on the capital structure.

He also said the move showed how Bitcoin can function inside a corporate treasury. Rather than showing weak conviction, it showed that a company can hold Bitcoin, raise capital against it and use a limited amount when cash needs arise.

Back’s argument also places the sale inside a larger shift in corporate Bitcoin finance, where companies use BTC alongside preferred shares, debt, common equity, and market tools today.

Strategy’s first sale drew attention

As previously reported by crypto.news, Strategy disclosed on June 1 that it sold 32 Bitcoin between May 26 and May 31 at an average price of $77,135. The sale raised about $2.5 million.

The filing said proceeds were expected to fund distributions on the company’s preferred stock. The sale represented about 0.0038% of Strategy’s Bitcoin holdings at the time, but it drew attention because Michael Saylor had long promoted a “never sell” message around Bitcoin.

Crypto.news later reported that Saylor separated personal investor advice from corporate treasury actions. “I said to YOU never sell your bitcoin,” Saylor said at BTC Prague.

Preferred dividends remain in focus

The debate centers on Strategy’s preferred stock model. Preferred shares can give investors yield, but they also create recurring cash needs that the company must meet through cash reserves, equity issuance or limited Bitcoin sales.

Strategy’s STRC preferred stock has faced pressure after falling below its $100 par value. As crypto.news reported, Saylor defended the company’s Bitcoin-backed strategy and said its Bitcoin and cash reserves still exceeded outstanding debt by about $48 billion.

Some critics argue that dividend obligations could become harder to manage if market conditions weaken. Supporters say the 32 BTC sale showed Strategy has several funding tools and does not need to abandon its long-term accumulation plan.

Strategy remains a net accumulator

The sale did not stop Strategy from buying more Bitcoin. Crypto.news reported that the company later bought 1,550 BTC for $101.3 million, lifting its holdings to 845,256 BTC after the sale disclosure.

That purchase was nearly 50 times larger than the 32 BTC sale. It helped support Back’s view that the transaction was not a broad retreat from Bitcoin.

Saylor has also argued that Bitcoin does not need staking or protocol-based yield. In a separate post covered by crypto.news, he framed Bitcoin as the base layer for credit, money, yield and equity products.

For now, the issue is not whether Strategy still wants Bitcoin. The question is how it funds preferred dividends while keeping investor trust and managing balance sheet risk.

TLDR

- STRC, Strategy’s preferred stock instrument, plunged to an all-time intraday low of $83 on June 18, trading approximately 17% beneath its $100 par value — marking the worst performance since launching in July 2025.

- The company’s $1.5 billion convertible bond repurchase depleted Strategy’s cash reserves, slashing projected dividend coverage from an intended 24-month buffer down to approximately 6 months.

- With bitcoin declining from highs above $80,000 in May to approximately $62,500, Strategy’s BTC portfolio now carries an unrealized deficit of roughly $11.14 billion.

- CEO Michael Saylor maintained the company’s financial strength, noting that combined BTC and USD reserves surpass total debt obligations by approximately $48 billion.

- While skeptics like Peter Schiff have questioned the legality of Strategy’s approach, advocates contend STRC’s framework remains viable provided Bitcoin experiences long-term appreciation.

On June 18, Strategy’s STRC preferred shares collapsed to an unprecedented intraday bottom of $83, ultimately settling at $88.59 — approximately 17% under the $100 par value benchmark. Since its July 2025 introduction, the instrument was engineered to maintain trading levels at or close to par while delivering an 11.5% annualized return.

This sharp decline wasn’t an abrupt event. Rather, it emerged from a sequence of corporate actions and bitcoin’s persistent price deterioration spanning several weeks.

Heading into its monthly ex-dividend date on May 14, STRC maintained its $100 level while bitcoin commanded prices exceeding $80,000. Superficially, the situation appeared stable. However, BTC had already retreated significantly from its October 2024 peak of $126,000.

That identical day, competitor Strive Asset Management unveiled SATA, its own preferred instrument featuring daily distributions at a 13% yield — immediately creating competitive pressure for Strategy.

Convertible Note Repurchase Drains Cash Cushion

The following day, May 15, Strategy disclosed plans to repurchase $1.5 billion worth of its 2029 convertible bonds at an 8% discount. The company financed a portion of this transaction by tapping into cash reserves initially designated for dividend distributions and debt service obligations.

This crucial information wasn’t immediately transparent. When details surfaced on May 26, the reserve balance had contracted to $871 million — dramatically reducing STRC dividend coverage from the advertised 24-month projection to merely 6 months.

STRC slipped to $99.33 that session. Bitcoin was changing hands around $77,000.

Despite this, Strategy persisted with bitcoin accumulation. On May 18, the firm acquired 24,869 BTC while prices descended toward $76,000.

June 1 delivered another unexpected development. Strategy disposed of 32 BTC — representing its first bitcoin divestment since 2022. Though minuscule at just 0.0038% of total holdings, the transaction alarmed market participants. MSTR shares declined 5.9% that day. Bitcoin tumbled to lows near $70,500. STRC settled at $98.07.

Accelerating Bitcoin Weakness Compounds Challenges

By June 5, bitcoin had penetrated below $60,000 for the first time since October 2024. STRC touched lows of $90 before recovering to close at $93.40.

Strategy shareholders authorized a transition to semi-monthly STRC dividend distributions on June 8, an adjustment intended to minimize volatility surrounding ex-dividend periods. The company simultaneously disclosed its dollar reserve had rebounded to $1 billion following the purchase of 1,550 BTC.

On June 15, Strategy added another 1,587 BTC to its portfolio. Reserve balances reached $1.1 billion.

Then June 18 arrived. STRC plummeted to $83 during trading hours before finishing at $88.59 as bitcoin declined 2.4% to $62,880. Strive CEO Matt Coles, whose SATA instrument also suffered losses, attributed the downturn to forced liquidations from leveraged positions rather than fundamental credit deterioration.

Strategy currently maintains 846,842 BTC, accumulated at an average acquisition cost of $75,656 per unit. With bitcoin hovering around $62,500, the corporation faces an unrealized portfolio loss approaching $11.14 billion.

MSTR common equity trades near $112, representing roughly an 80% decline from its November 2024 record high.

Michael Saylor countered critics this week, declaring via X that combined BTC and USD reserves now surpass the company’s total debt burden by approximately $48 billion. He drew comparisons to 2022, when debt temporarily exceeded reserves by $300 million while BTC traded near $20,000.

Peter Schiff has advocated for shareholder litigation and suggested Saylor potentially breached SEC promotional regulations while marketing STRC. Conversely, Bitcoin proponent Samson Mow characterized STRC as a “brilliant instrument,” maintaining there are no inherent structural deficiencies unless one assumes bitcoin won’t appreciate over extended timeframes.

Key Takeaways

- Q1 2026 marked Coinbase’s second consecutive quarterly loss, posting $1.43 billion in revenue against a $394 million net deficit.

- Strategic diversification includes stablecoins, derivatives trading, payment solutions, and prediction market platforms.

- The newly launched prediction markets division achieved more than $100 million in annualized revenue within months.

- Deribit acquisition strengthens Coinbase’s competitive stance in cryptocurrency derivatives trading.

- Wall Street consensus targets approximately $250 for 12 months, with 2031 base-case projections between $300–$400.

Since going public through a direct listing in 2021, Coinbase (COIN) stock has experienced significant volatility — climbing to impressive peaks before retreating sharply. While near-term movements capture headlines, the more compelling analysis focuses on where this cryptocurrency platform could stand by 2031.

Current analyst consensus places COIN at approximately $250, derived from 33 Wall Street analysts monitored by MarketBeat. The overall rating stands at Hold, comprising 18 Buy recommendations, 12 Hold positions, and 3 Sell ratings.

Recent performance has been challenging. The stock has retreated from previous highs, and first-quarter 2026 earnings reflected this pressure. The company reported roughly $1.43 billion in revenue while recording a $394 million net loss — marking back-to-back quarters in the red. Declining cryptocurrency trading volumes directly impacted transaction-based income.

This represents the immediate reality. The extended-term narrative, however, tells a different story.

Coinbase has systematically constructed a diversified portfolio of services extending beyond its primary exchange operations. The company now operates across stablecoins, derivatives markets, institutional infrastructure, payment processing, and Base — its proprietary Ethereum Layer 2 blockchain solution.

The Deribit purchase represents a strategic milestone. As among the world’s leading platforms for cryptocurrency options and futures, Deribit’s integration significantly enhances Coinbase’s capabilities in derivatives — a rapidly expanding market segment.

Rapid Growth in Prediction Markets

One recent initiative has generated particular interest: Coinbase’s entrance into prediction markets. Company leadership revealed the segment surpassed $100 million in annualized revenue shortly after deployment. This rapid scaling demonstrates the viability of new product categories.

This development illustrates Coinbase‘s capacity to execute swiftly when identifying market opportunities, with several initiatives already delivering meaningful returns.

Constructing a 2031 Valuation Framework

Valuing Coinbase through current earnings metrics presents challenges — cryptocurrency markets operate cyclically, and the company remains in transformation mode. A more practical approach examines potential revenue generation five years forward.

In a base-case projection — assuming continued institutional cryptocurrency adoption, expanding stablecoin utilization, and growing derivatives activity — Coinbase could achieve approximately $12 billion in annual revenue by 2031. Applying roughly $9 in earnings per share with a 32x earnings multiple suggests a stock price approaching $300.

This represents the moderate scenario. A pessimistic outlook, where adoption stagnates and fee compression intensifies, could drive shares toward $20–$50. Conversely, an optimistic scenario featuring mainstream digital asset integration and Base establishing itself as a major blockchain network could propel valuations beyond $800.

Rosenblatt recently confirmed its Buy rating with a $240 target. Multiple analysts continue positioning COIN as a long-term investment thesis on cryptocurrency adoption.

Probability-weighted modeling currently suggests a base estimate near $370 by 2031, according to current analytical frameworks.

SEC Commissioner Hester Peirce, widely known in the digital asset industry as “Crypto Mom,” said she will leave the agency in November and join Regent University School of Law as an associate professor.

Summary

- Peirce said she will leave the SEC in November and join Regent Law as professor.

- Her exit comes as the SEC weighs crypto rules, tokenization and a narrow innovation exemption.

- The SEC will have only Paul Atkins and Mark Uyeda as active commissioners after departure.

Peirce confirmed the plan during an appearance on The Rollup podcast, saying she will be “moving to the beach” after nearly three decades in Washington, D.C. As previously reported by crypto.news, Regent announced in May that she will teach securities regulation, financial markets, digital assets and public policy.

Peirce confirms move to Regent Law

Peirce has served as an SEC commissioner since January 2018. The Senate confirmed her for a second term in 2020, and that term expired on June 5, 2025.

SEC rules allow commissioners to remain for up to 18 months after a term expires if no successor has been confirmed, according to the SEC commissioners page. Peirce could have stayed until December 2026, but her November move means she will leave slightly earlier.

On the podcast, Peirce said she looks forward to working with students. “I’m going to be teaching law school. So, I’m excited about working with the next generation,” she said.

Crypto task force faces transition

Peirce has led the SEC’s Crypto Task Force since January 2025. The task force seeks to draw clearer lines around digital assets, token status, disclosure rules, registration paths and enforcement priorities. It also gives market participants a channel to send written input and request meetings during the current rule review.

Her departure will leave the commission with Chairman Paul Atkins and Commissioner Mark Uyeda as the two active sitting members, unless new nominees are confirmed before then. The SEC is designed to have five commissioners, with no more than three from the same political party.

Peirce’s final priorities include helping shape a crypto framework, changing rules so more companies can go public earlier and removing the trade-through rule. These items remain part of a wider market-structure debate at the agency.

Innovation exemption remains pending

The SEC’s possible “innovation exemption” for digital assets has drawn strong attention from crypto firms and tokenization platforms. Peirce used the podcast appearance to lower expectations around what the proposal may include.

“First, the innovation exemption has not yet been released. So that’s one myth that should be dispelled,” Peirce said. She also said synthetic securities were not part of what officials had in mind.

Her comments followed reports that the SEC could give firms limited room to test blockchain-based products while broader rules remain under review. Peirce said the exemption should not be treated as a blanket approval for every tokenized product.

Exit comes during crypto policy reset

Peirce gained the “Crypto Mom” nickname after years of criticizing enforcement-led crypto oversight and calling for clearer rules. Her public dissents made her one of the industry’s most followed SEC officials.

The agency has shifted under Atkins toward new crypto policy work, including tokenization, custody and market access. The question now is whether that work continues at the same pace after Peirce leaves.

For crypto firms, the timing matters because several rulemaking paths remain open. Peirce’s exit does not stop the SEC’s crypto agenda, but it removes one of its most visible advocates inside the commission.

A Japanese corporate pension fund serving about 1,200 small and medium-sized businesses plans to allocate roughly 1% of its assets to cryptocurrency during fiscal 2026.

According to Nikkei, the Nationwide Business Corporate Pension Fund, based in Okayama, will invest in a passive fund managed by a major hedge fund that holds multiple crypto assets. The pension fund reportedly manages about 21.3 billion yen in assets, or about $130 million.

Japanese crypto news site CoinPost reported that the fund is adding crypto as part of an effort to diversify its exposure. The fund reportedly allocates 80% of its assets to yen, 15% to US dollars and 5% to other currencies.

The move suggests crypto is beginning to gain acceptance among Japan’s more conservative institutional investors as the country prepares to integrate digital assets more closely with traditional finance.

Japan brings crypto closer to traditional finance

The planned pension allocation comes as Japanese lawmakers and financial institutions prepare for digital assets to play a larger role in the country’s traditional financial system.

On June 11, Japan’s House of Representatives passed legislation that would bring crypto assets under the Financial Instruments and Exchange Act, subjecting them to rules more closely aligned with those governing conventional financial products.

The legislation is expected to proceed to the House of Councilors and could create a path for crypto exchange-traded funds and a shift to a 20% flat tax on digital-asset gains.

Related: Polymarket seeks Japan entry despite gambling law hurdles: Report

Japanese financial groups are also developing new ways for retail and institutional investors to access crypto. SBI Shinsei Bank has begun testing a deposit-linked rewards program offering vouchers redeemable for Bitcoin, Ether or XRP, ahead of a planned permanent launch this autumn.

On June 12, Metaplanet, Japan’s largest publicly listed Bitcoin holder, also agreed to acquire Siiibo Securities for 2.1 billion yen. The company said the acquisition would support the development and distribution of Bitcoin-linked yield products through a newly formed securities arm.

Magazine: China’s 107 Bitcoin memory thief, Bithumb CEO booked: Asia Express

Is this $3000 Toonie Error in Your Pocket Change? #coins #crh #money #shorts

Hundreds of runners at R U Taking the P? York fun run

5 Stocks Analysts Say Look Like Better Buys Than SpaceX Right Now

-

Business7 days ago

Business7 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Miami – Corporette.com

-

Crypto World6 days ago

Zimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Business1 day ago

Business1 day agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Entertainment7 days ago

Entertainment7 days agoMatt Damon’s Viral Sci-Fi Thriller Has Taken Over HBO Max

-

Tech7 days ago

Tech7 days agoAs AI companies race to go public, who else is along for the ride?

-

Business7 days ago

Business7 days agoAnthropic staff to meet White House officials next week, Axios reports

-

Crypto World1 day ago

Crypto World1 day agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World7 days ago

Crypto World7 days agoBitcoin could crash to $48,000, if this historical pattern is triggered

-

NewsBeat7 days ago

NewsBeat7 days agowhat doctors are seeing in ebike crashes

-

NewsBeat7 days ago

NewsBeat7 days agoWarning of disruption as Cardiff Crossrail works to start

-

NewsBeat7 days ago

NewsBeat7 days agoTributes to former deputy head teacher at Cambridge school among death and funeral notices

-

Entertainment7 days ago

Entertainment7 days agoKate Middleton Glare Goes Viral After Kids Booed At Royal Event

-

Politics7 days ago

Politics7 days ago“Israel’s” ban on ICRC visits ruled illegal, but Knesset moves to stop them permanently

-

News Videos7 days ago

News Videos7 days agoFinancial Accounting | Last Day Revision Strategy and Booster | CMA Inter – June 2026

-

Crypto World7 days ago

Crypto World7 days agoXRP ETFs Outperform As Bitcoin And Ethereum Funds Extend Outflow Trend

-

Tech6 days ago

Tech6 days agoOver 400 Arch Linux packages compromised to push rootkit, infostealer

-

Business7 days ago

Business7 days agoInvesco Quality Income Fund Q1 2026 Commentary

-

NewsBeat7 days ago

NewsBeat7 days agoSinger Oliver Tree dies aged 32 in helicopter crash in Brazil

-

Crypto World7 days ago

Crypto World7 days agoMarket Preview: SpaceX (SPCX) IPO Record, Federal Reserve Meeting, and Iran Nuclear Agreement

You must be logged in to post a comment Login