Crypto World

ZachXBT flags JuCoin reserves as users report withdrawal delays

JuCoin is facing fresh scrutiny after on-chain investigator ZachXBT flagged user complaints about withdrawal delays and questioned the exchange’s reserve claims.

Summary

- ZachXBT said JuCoin users reported withdrawal delays over the past week, raising exchange risk concerns.

- JuCoin’s reported reserves face questions over USDC and USDT issued on its own JuChain.

- JuCoin blamed delays on upgrades and restructuring while critics pointed to past JuDAO incidents.

Wu Blockchain reported that several users had raised withdrawal issues over the past week. ZachXBT also questioned JuCoin’s reported $511 million reserves, saying much of the value appeared tied to USDC and USDT issued on JuCoin’s own JuChain.

ZachXBT flags JuCoin withdrawal issues

ZachXBT said multiple users reported problems withdrawing funds from JuCoin. The complaints arrived during a period of added concern around centralized exchange reserves and user access to funds.

JuCoin attributed the delays to platform upgrades and restructuring, according to Wu Blockchain. The exchange’s explanation did not fully end concerns because users were also asking about reserve quality.

“Multiple users have reported withdrawal issues on JuCoin over the past week,” Wu Blockchain said, citing ZachXBT’s comments.

The issue remains developing. There has been no public proof that JuCoin is insolvent, but withdrawal delays often draw fast attention because users depend on exchanges to process funds on demand.

Reserve claims face JuChain stablecoin questions

The larger concern centers on JuCoin’s reported $511 million reserve figure. ZachXBT questioned whether the reserves were backed by clear third-party assets.

A separate PANews-linked report said JuCoin claimed a 123.81% reserve ratio. It also said assets listed as USDC and USDT on JuChain were project-issued tokens, not clearly linked to Circle or Tether-issued stablecoins.

That claim matters because a token named USDC or USDT on a private or smaller chain may not carry the same backing as official stablecoins unless verified by the issuer or a supported bridge.

The report also said the reserve address held nearly all of those tokens, with only a small number of holders. That raised more questions about whether the reserve figure reflected real liquid assets.

Past JuDAO incidents add pressure

Wu Blockchain also cited ZachXBT’s note that JuDAO suffered a $20 million incident in 2025 and a $225,000 exploit in April 2026.

Those past events have added pressure to the current withdrawal debate. Users often look at past security events when judging whether an exchange or linked ecosystem can manage stress.

JuCoin has said the current delays relate to upgrades and restructuring. That explanation may be valid, but users still need clear timelines and proof that withdrawals can resume normally.

In exchange crises, communication matters. Unclear updates can increase fear even before any full technical or financial review is complete.

Exchange reserves remain a market concern

The JuCoin case comes as traders remain sensitive to exchange reserve claims. Crypto.news previously reported heavy withdrawal pressure after the Bybit hack, showing how fast users move funds during stress.

Reserve reports can help build trust, but only when users can verify the assets, issuers, chains, and wallet controls. Self-issued assets may need more explanation than widely traded mainnet assets.

Moreover, JuCoin faces two separate questions. Users want withdrawals processed, and the market wants clearer proof behind the $511 million reserve claim.

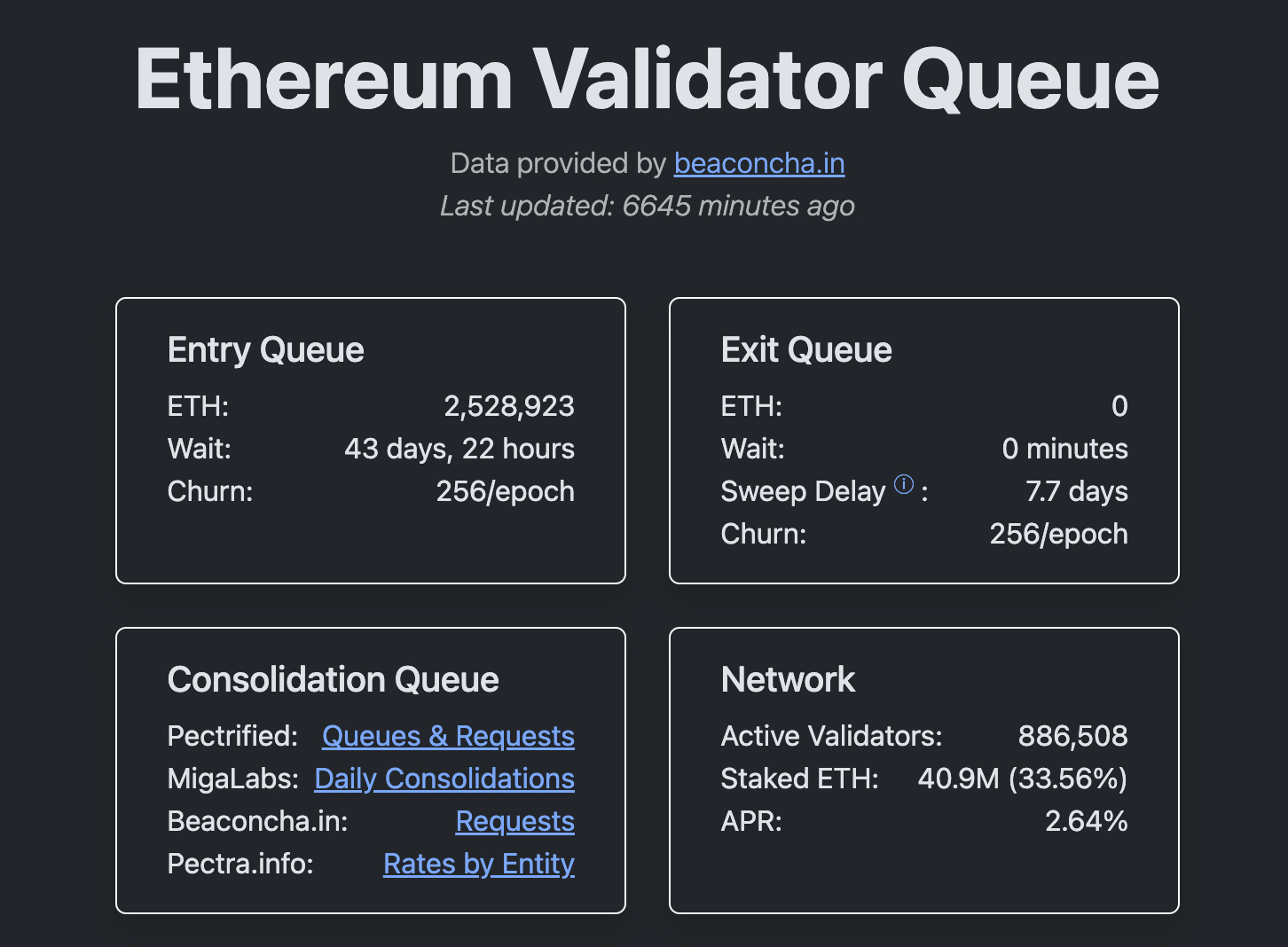

Ethereum validator exit queue has fallen to zero, marking a sharp reversal from a bearish price prediction less than a year ago. ETH itself trades around the $1,950 level, trying to reclaim the key $2,000 resistance. The staking data tells a story that the price chart has yet to confirm. What happens over the next few sessions could shape the recovery.

Validator Queue data shows the exit queue has fully cleared after swelling to roughly 2.6 million ETH last year. At the time, validators faced withdrawal waits of about 45 days. Now, the picture has flipped. More than 2.5 million ETH is waiting to enter staking, creating an activation delay of nearly 44 days.

Total staked ETH has climbed to about 40.9 million coins, representing roughly 33.6% of the circulating supply. That marks the highest staking ratio in Ethereum’s history. Nearly 887,000 active validators now secure the network, showing demand remains firmly tilted toward long-term participation instead of exits.

Those staking dynamics could eventually influence price. A growing share of ETH remains locked, reducing the amount readily available for trading. At the same time, the cleared exit queue removes one of last year’s biggest bearish concerns, when traders feared a wave of unstaked ETH could flood exchanges. If demand stays strong, the supply picture may continue to support Ethereum’s recovery.

Discover: The Best Crypto to Diversify Your Portfolio

Ethereum Price Prediction: Break Above $2,000 and Target $2,400?

ETH is consolidating near the $1,970 level after recovering from recent lows. Intraday trading has stayed between roughly $1,880 and $1,970, showing buyers and sellers remain locked in a battle. Price action still reflects a contested zone rather than a clear directional trend.

The technical picture remains straightforward. ETH continues trading inside a well-defined $1,900 to $2,200 range. Immediate resistance sits around $2,000, followed by the $2,080 to $2,120 area. A sustained move above $2,200 would strengthen bullish momentum, while $2,400 remains the level many traders view as confirming a lasting trend reversal.

The bullish scenario remains simple. ETH needs to reclaim and hold $2,000 before pushing through the $2,080 to $2,120 resistance zone. If buyers maintain momentum, the next target becomes $2,200, with $2,400 still acting as the major breakout level. Recent staking queue data continues to support that longer-term setup.

The base case still favors consolidation. ETH could spend several more sessions moving between $1,900 and $2,200 before choosing a direction. However, a daily close below $1,900 would shift attention toward the $1,850 to $1,800 support area. Losing $1,800 would weaken the short-term outlook, even if the long-term thesis remains intact.

Funding rates and derivatives positioning remain the key signals alongside spot price action. Together, they should reveal whether buyers have enough conviction to break resistance or if another rejection is coming.

Trade Ethereum on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

Maxi Doge Targets Early Mover Upside as Ethereum Tests Key Levels

ETH at $2,000 is a structural story with compelling long-term math, but the upside from current prices to $7,500 represents a roughly 3.5x move, distributed across 18 months of potential volatility. Traders looking for asymmetric exposure during the same window tend to look earlier on the risk curve, where entry prices and market caps haven’t already digested the thesis.

Maxi Doge ($MAXI) is a meme token currently in presale on Ethereum (ERC-20), built around a trading community identity centered on high-conviction, high-energy market participation. The project describes its mascot as “a 240-lb canine juggernaut embodying 1000x leverage trading mentality.”

The current presale price sits at $0.0002831, with $4.8 million raised to date. The project features dynamic APY staking, holder-only trading competitions with leaderboard rewards, and a Maxi Fund treasury allocated to liquidity and partnerships.

For traders sizing appropriately and tracking the presale-to-listing cycle, the early entry price and community mechanics are worth researching Maxi Doge before the next stage closes.

Discover: The Best Token Presales

The post Ethereum Price Prediction: Unstaking Queue Hits Zero as ETH USD Approaches $2,000 appeared first on Cryptonews.

Coinbase CEO Brian Armstrong is pushing back against calls for crypto to pivot to artificial intelligence, arguing AI agents will instead stoke demand for crypto-based financial services.

Armstrong took to X on Sunday to tout agentic finance (AiFi), highlighting Coinbase’s Base network, USDC and x402 as the infrastructure for autonomous machine-to-machine payments.

“AI being a megatrend takes nothing away from crypto,” Armstrong wrote, because AI agents will need programmable money rather than traditional banking rails. “If anything, it makes crypto more important,” he added.

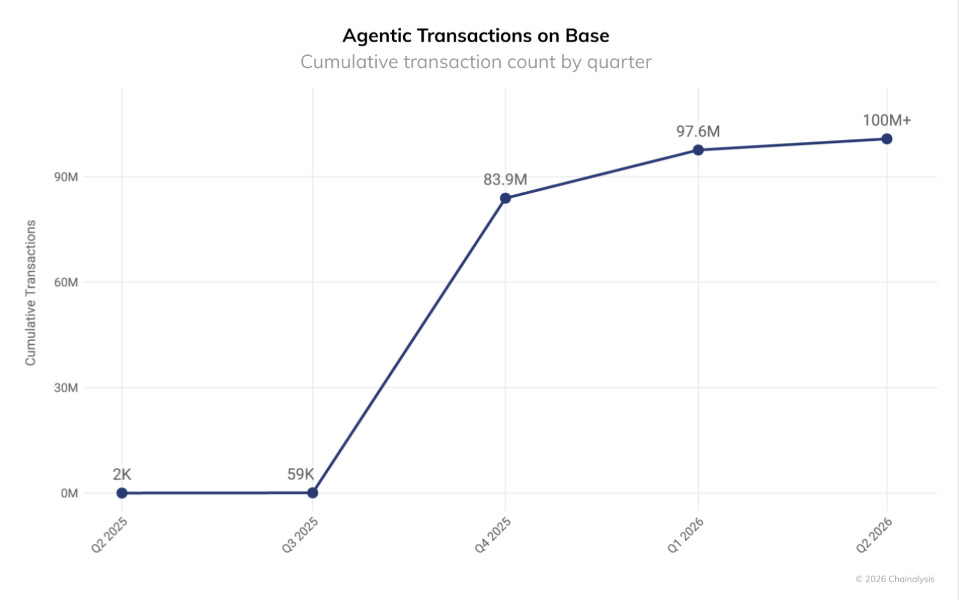

His comments come as crypto companies increasingly position blockchain networks as payment infrastructure for AI agents, with agentic payment activity on Base topping 100 million transactions in June.

How Coinbase’s AiFi stack came together

Armstrong’s AiFi vision centers on the idea that AI agents will become active participants in the digital economy, making payments and interacting with financial services without human intervention.

Coinbase launched Base in 2023 as an Ethereum layer-2 network designed to make onchain applications faster and cheaper to use. The network was built as general-purpose blockchain infrastructure rather than specifically for AI payments.

Two years later, Coinbase introduced x402, a payment protocol built around the HTTP “402 Payment Required” standard that enables automated stablecoin payments between software applications. The protocol allows AI agents and other autonomous systems to pay for digital resources such as APIs and data without traditional accounts or manual checkout flows.

Related: Base’s 1:1-backed tokenized equities launch ‘imminent,’ Pollak says

USDC, the dollar-pegged stablecoin launched by Circle and Coinbase-backed Centre Consortium in 2018, is one of the assets used for x402 payments, allowing software agents to make automated transactions.

Base, x402 and USDC together form the core of Coinbase’s current approach to building infrastructure for agentic payments.

Coinbase is slated to report second quarter earnings on Thursday. Analysts average is for revenue of $1.29 billion, with sales estimated to show a 13.8% decline over last year’s comparable period, Yahoo Finance data shows. Earnings per share are expected to be flat.

Base agentic activity tops 100 million transactions

Chainalysis reported in June that agentic payments on Base via x402 surpassed 100 million transactions within roughly nine months of activity.

The analytics firm said it tracked the activity by identifying x402-related payment flows onchain, with transactions worth at least $1 accounting for 95% of total value transferred.

Source: Chainalysis

Chainalysis also found that agentic payment wallets were typically newer, held more asset types and carried smaller balances than average Base users.

Cointelegraph asked Chainalysis for updated x402 activity figures and details on its tracking methodology, but the firm had not responded by publication time.

Magazine: CLARITY hopes fade, BitMEX shuts as lawsuit looms: Hodler’s Digest, July 26

Sberbank, Russia’s largest bank, plans to roll out crypto trading infrastructure by December 2026. The announcement comes ahead of new regulations for crypto trading, custody, and settlement that come into force from September 1, 2026.

Russia’s crypto push comes as the European Union readies new sanctions targeting the country over the ongoing Ukraine conflict.

Sberbank Plans Crypto Infrastructure Rollout

Sberbank plans to build and launch critical crypto trading infrastructure, including a digital depository, by December 1, 2026. The bank is leading Moscow’s efforts to bring cryptocurrency trading, custody, and settlement into the mainstream financial system. Sberbank’s announcement comes after Russia approved new rules for cryptocurrency exchanges, brokers, banks, and digital depositories. The new regulations come into force on September 1, 2026. Companies will also be given additional time to ensure compliance with the new requirements.

“Russia’s Largest Bank Sberbank Plans Crypto Trading Infrastructure: Sberbank, Russia’s largest bank, plans to build cryptocurrency trading infrastructure and launch a digital custody system by Dec. 1 to support regulated crypto trading, custody and settlement.” – Wu Blockchain

The digital depository will record cryptocurrency ownership and process transactions outside the primary blockchain. Sberbank will also operate wallets for client deposits, withdrawals, and transfers. Alexander Vedyakhin, first deputy chairman of Sberbank’s management board, stated,

“One of the key elements of the new infrastructure will be a digital depository, which will maintain records of clients’ cryptocurrency rights and account for transactions outside the main blockchain. It will also facilitate transactions on active wallets to fulfill clients’ currency transfer orders.”

However, the bank is yet to disclose eligibility, fees, withdrawal limits, or which cryptocurrencies are supported by the framework.

Sberbank Expanding Crypto Services

Sberbank joined Russia’s register of information system operators in 2022, and has since issued several digital financial assets and products linked to Bitcoin (BTC), Ethereum (ETH), and other assets. As mentioned earlier, the bank was already working on a digital asset depository and cryptocurrency wallet. It could also give customers access to foreign cryptocurrency exchanges depending on prevailing regulatory requirements. Sberbank has also dabbled in cryptocurrency-backed lending, completing a pilot loan with Bitcoin miner Intellion Data. According to reports, the bank has considered offering similar loans to corporate customers.

Russia’s Crypto Market Framework

Russian lawmakers concluded a final reading on a bill to regulate cryptocurrencies in the country. The bill gives the Bank of Russia oversight of the cryptocurrency market, including the authority to dictate which cryptocurrencies are offered through licensed intermediaries. The bill categorizes market participants, dictating which entities can buy, sell, hold, and exchange crypto assets once the framework comes into effect. The Bank of Russia has set an average market capitalization of over 5 trillion rubles (~$64 billion) and an average 24-hour volume of 1 trillion rubles (~$12.8 billion) over two years for cryptocurrencies offered under the framework.

Moscow’s push for a regulated crypto framework comes as the EU imposed another tranche of sanctions and also listed the HTX cryptocurrency exchange in the sanctions for “providing crypto asset services or payment services established outside of the Union that are significantly frustrating the purpose of the prohibitions against Russia.”

EU officials have also barred Belarusian nationals and residents from owning, controlling, or managing cryptocurrency exchanges in compliance with the Markets in Crypto Assets (MiCA) framework.

According to the Bank of Russia, the new framework allows investors to purchase crypto assets through regulated intermediaries. However, qualified and non-qualified investors are subject to different limits. Both qualified and non-qualified investors must pass a test to become eligible to purchase crypto assets. However, qualified investors can access more cryptocurrencies and are not subject to an annual limit when investing. On the other hand, non-qualified investors can access limited digital assets and can only purchase 300,000 rubles worth of crypto per year through a single intermediary.

Russian Companies Prepare For New Framework

Other entities are also preparing for the new framework. VTB and T-Bank are developing their own digital depository services, while the Moscow Exchange is considering offering regulated crypto operations. Alfa Bank has also tested custody tools and cryptocurrency services, a clear indicator that major players in Russia’s financial sector are preparing themselves before the licensing deadline.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

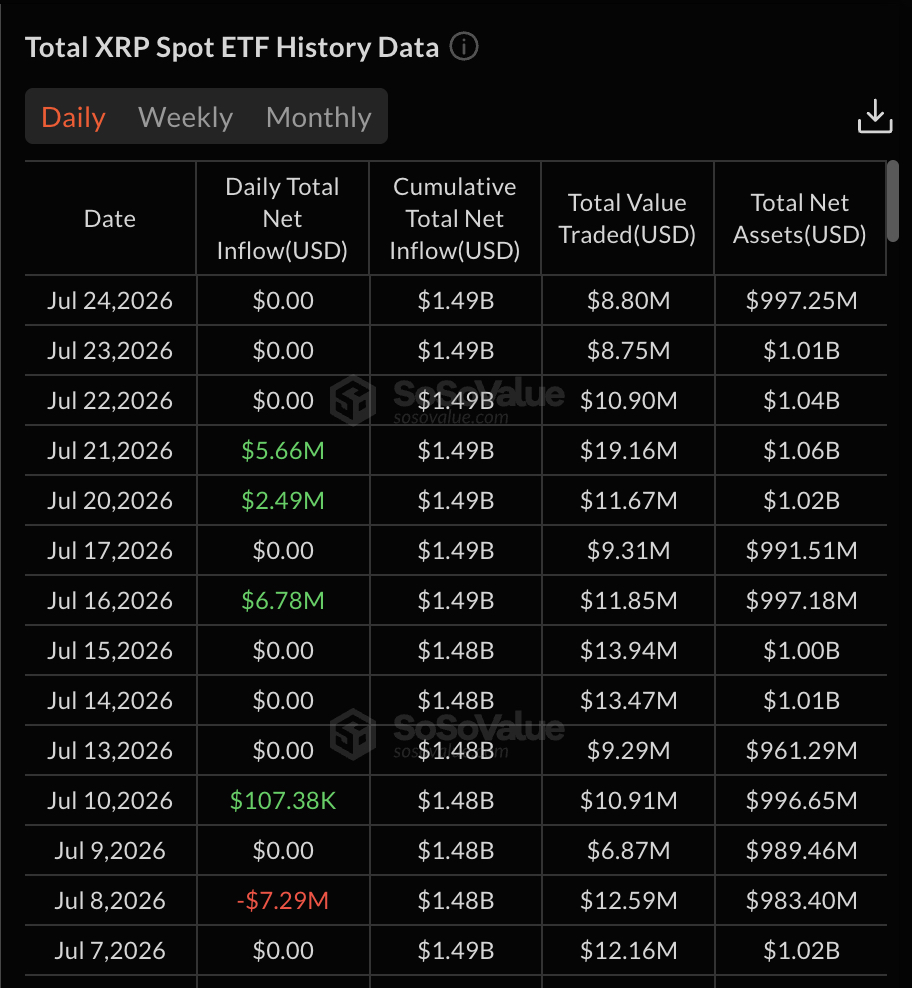

XRP price prediction remains neutral as XRP trades around $1.10, with strong ETF inflows failing to trigger a sustained price breakout. Price remains mostly flat despite strong institutional demand.

According to SoSoValue, XRP spot ETFs recorded $8.15 million in net inflows during the July 20 to 24 trading week. Franklin Templeton’s XRPZ led with $5.66 million, lifting its cumulative inflows to $421 million. Bitwise followed with $2.49 million, bringing its total to $501 million.

Total net assets across XRP spot ETFs now stand at $997 million. Meanwhile, cumulative historical net inflows have reached $1.49 billion. ETF assets also represent about 1.46% of XRP’s total market capitalization. Those numbers point to steady institutional accumulation even as spot prices remain stuck in a range.

An eight-figure institutional demand in a single week without a lasting price reaction is more than market noise. It suggests persistent selling is absorbing fresh capital. As a result, next week’s setup looks more complex than the inflow headlines alone suggest, making any breakout dependent on buyers finally overwhelming that supply.

Discover: The Best Token Presales

XRP Price Prediction: Hold $1.10 While ETF Demand Builds Overhead?

XRP remains trapped in a tight range. The $1.10 level marks the lower edge of immediate demand, while $1.11 caps recent buying pressure. Despite steady ETF inflows, the token has struggled to build momentum. XRP is up roughly 1.2% over the past seven days, a modest gain considering institutional demand.

XRP market capitalization is about $69.1 billion, and that scale requires sustained institutional buying to produce a meaningful move. In that context, weekly ETF inflows of about $8 million remain too small to materially shift prices.

Three scenarios frame the near term. The bull case sees ETF assets decisively pushing above the $1 billion mark, encouraging buyers to reclaim resistance at $1.11. The base case keeps XRP trading between $1.10 and $1.11 as retail participation stays muted. Meanwhile, a break below $1.10 could expose the psychological $1.00 level if selling pressure increases.

For active traders, the demand zone around $1.10 and the resistance near $1.11 deserve close attention. A convincing close above resistance with strong volume would shift the outlook. Until that happens, range trading remains the dominant theme.

Trade XRP on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

LiquidChain Targets Early Mover Upside as XRP Tests Key Levels

XRP’s ETF flows confirm that institutional capital is moving into crypto infrastructure, but at a $69 billion market cap, the upside math is fundamentally different from early-stage exposure. Traders who understand that dynamic are increasingly scanning for where structural positioning still offers asymmetric returns.

LiquidChain is an L3 infrastructure project with a specific thesis: fuse Bitcoin, Ethereum, and Solana liquidity into a single execution environment, eliminating the fragmentation that currently forces developers to choose between ecosystems. The architecture powers Unified Liquidity Layer, Single-Step Execution, Verifiable Settlement, and the Deploy-Once design, which target the cross-chain coordination problem that costs DeFi protocols measurable volume every day.

The view is different from the third layer. — LiquidChain (@getliquidchain) July 27, 2026

You’ll understand soon. pic.twitter.com/P2WOELSTjI

The presale is currently priced at $0.01484, with $920K raised to date. For traders comfortable with early-stage exposure, the infrastructure angle is worth researching.

Review the LiquidChain presale details here.

Discover: The Best Crypto to Diversify Your Portfolio

The post XRP Price Stalls Despite Huge Weekly ETF Net Inflows appeared first on Cryptonews.

Interest rates could set the direction for crypto this week, with the Federal Reserve, Bank of England and Bank of Japan all expected to hold while markets look for signs that higher energy prices have brought further tightening closer.

CME’s FedWatch shows a 33% chance of a U.S. rate increase, while prediction markets odds are at 19%, up from next to nothing earlier in the month. Gregory Daco, the chief economist for EY-Parthenon, said September could be the first meaningful test of the Fed’s stance, CBS News reported.

More immediate tests come Thursday, with U.S. second-quarter GDP and June Personal Consumption Expenditure (PCE) due. Strong growth alongside persistent inflation would reinforce higher-for-longer interest-rate expectations and pressure crypto prices through higher yields and a stronger dollar, while softer readings could unwind that trade.

All 70 economists in a Reuters poll expected the BOE to hold at 3.75%, while the BOJ is forecast to remain at 1% before potentially raising rates again later this year.

Cointelegraph is committed to providing independent, high-quality journalism across the crypto, blockchain, AI, and fintech industries.

All news, reviews, and analyses are produced with full journalistic independence and integrity. For more details on our standards and processes, please read our Editorial Policy.

South Korea has moved to deepen venture capital ties with Silicon Valley as President Lee Jae-myung has urged six of the world’s largest venture capital firms to invest in Korean startups while the National Pension Service has signed long-term investment cooperation agreements with them.

Summary

- South Korea has partnered with six leading Silicon Valley venture capital firms while the National Pension Service signed long term investment cooperation agreements with them.

- President Lee Jae myung has asked the global investors to increase funding for Korean startups as the government expands support for technology industries.

- The government is pairing the initiative with its planned 200 trillion won National Growth Fund to support sectors including AI and semiconductors.

- Industry observers have warned that heavy investment into a small number of startups could inflate valuations and affect future investment returns.

According to South Korean newspaper Asiae, President Lee Jae-myung has asked six major Silicon Valley venture capital firms, including Sequoia Capital, Andreessen Horowitz (a16z), Khosla Ventures, Lightspeed Venture Partners, General Catalyst and New Enterprise Associates (NEA), to increase investments in South Korean startups as the country pushes to attract more global capital into its technology sector.

The report said the National Pension Service (NPS) also signed separate memorandums of understanding with the six venture capital firms to establish long-term investment cooperation, creating a framework to explore investment opportunities together, exchange market information and strengthen links between Korea’s startup ecosystem and global venture capital networks.

The latest agreements come as the South Korean government continues introducing policies designed to draw overseas investors into domestic technology companies while supporting local innovation through public funding initiatives.

Silicon Valley firms join Korea’s startup investment push

Asiae said the government is pairing the new venture capital partnerships with its planned National Growth Fund, a 200 trillion won investment vehicle expected to support future industries including artificial intelligence and semiconductors.

The publication said market participants expect policy funding, private investment and overseas capital to enter the Korean venture ecosystem at the same time if the initiatives move forward as planned. Technology sectors such as AI and semiconductors are expected to receive increased investor attention under that framework.

Rather than treating the agreements as a source of capital alone, the newspaper said Silicon Valley firms also bring decades of experience identifying early-stage technology companies, helping founders build growth strategies and connecting startups with international markets.

According to Asiae, firms such as Sequoia Capital and Andreessen Horowitz have previously backed companies that later developed into major global technology businesses, giving Korean startups access not only to funding but also to operational knowledge and international business networks.

The publication argued, however, that attracting overseas investment should not become the government’s only objective.

Asiae said policymakers now face a second challenge after securing investor interest by creating conditions that encourage successful startups to continue expanding from South Korea instead of relocating high-value operations overseas.

The editorial said the country should strengthen tax rules surrounding stock options so startups can compete more effectively for skilled employees while also improving visa policies and long-term residency conditions for foreign founders, engineers and technical specialists.

In addition, the newspaper said South Korea should develop stronger exit opportunities through mergers and acquisitions alongside public listings, arguing that a healthier acquisition market would provide investors with more ways to realize returns.

The publication also called for closer cooperation between universities, research institutions and startup companies so academic technologies can move into commercial businesses more efficiently. Improving English-language disclosures and simplifying investment-related administrative procedures would also make Korea more attractive to international investors, according to the report.

Asiae argued that business-friendly conditions, rather than restrictive regulations, will ultimately determine whether companies continue building products and creating jobs inside the country.

National Pension Service faces calls to preserve investment independence

Alongside the government’s efforts to attract foreign investors, the National Pension Service has become one of the key institutions participating in the cooperation agreements.

Asiae said the pension fund should continue making investment decisions independently despite its partnerships with globally recognized venture capital firms.

According to the newspaper, the retirement savings managed by the NPS should not become a policy instrument for industrial development, adding that investment decisions should continue following established return and risk principles.

The publication also cautioned that partnerships with internationally known venture capital firms do not eliminate investment risks simply because of their reputations.

Industry participants cited by Asiae also warned that excessive capital flowing into a small number of highly sought-after startups could inflate company valuations, creating pressure if those valuations later decline during initial public offerings or merger transactions. Such corrections could reduce investment returns for participating funds.

South Korea expands digital finance alongside startup investment

The latest venture capital initiative comes as South Korea continues expanding investment and financial infrastructure across its technology sector.

Earlier this month, Mirae Asset completed its acquisition of cryptocurrency exchange Korbit after receiving regulatory approval, becoming the first affiliate of a traditional Korean financial group to acquire a domestic crypto exchange. The company has said the acquisition is intended to support future business opportunities tied to digital assets.

Separate partnerships have also emerged across the country’s digital finance industry. Circle recently signed memorandums of understanding with Kakao Group and fintech operator Toss to study blockchain payments, stablecoin infrastructure and cross-border settlement, while stressing that the agreements focus on infrastructure rather than launching a Korean won stablecoin.

At the same time, South Korean authorities have continued developing blockchain-based payment systems through the Bank of Korea’s Project Hangang. Last week, government agencies launched a 9.6 billion won project to extend CBDC-backed deposit token payments into commercial use, with commercial banks, payment companies and merchants participating in the next stage of testing.

Brazil has launched a nationwide operation targeting an alleged transnational drug trafficking and money laundering network that investigators say used crypto brokers, shell companies and luxury assets to conceal up to R$1 billion in illicit proceeds.

Summary

- Brazil has launched a nationwide operation targeting an alleged drug trafficking and money laundering network that investigators say used crypto brokers.

- Authorities froze up to R$1 billion in assets while carrying out arrests and searches across four Brazilian states.

- Investigators allege the group shipped about 6.5 tons of cocaine to Europe since 2021 using concealed cargo methods.

- The Federal Police said the network allegedly laundered proceeds through shell companies, luxury assets, real estate and crypto brokers.

According to Brazil’s Federal Police, officers on Thursday carried out Operation Commodity across four states, executing 13 preventive arrest warrants and 44 search and seizure warrants as part of an investigation into an alleged criminal organization involved in international cocaine trafficking and large-scale money laundering.

The operation forms part of the Redentor II Mission and received support from the Integrated Force to Combat Organized Crime (FICCO) in São Paulo and Minas Gerais. Authorities said nine people had been arrested during the action.

Brazilian courts also ordered the seizure of assets and the freezing of property worth up to R$1 billion belonging to individuals and companies under investigation. In addition to the arrests and searches, judges approved other precautionary measures against the suspects.

Crypto brokers allegedly helped conceal illicit proceeds

Federal Police investigators alleged that the criminal network built an international logistics chain with links across South America, Europe and Asia to export cocaine by sea to European destinations.

According to investigators, the organization shipped around 6.5 metric tons of cocaine to several European countries beginning in 2021. Authorities also said the network maintained operational ties with two criminal organizations active inside Brazil.

The investigation further alleged that the group relied on several methods to hide its financial activity after drug shipments generated proceeds. Alongside shell companies, luxury goods and real estate, investigators identified the use of crypto brokers as one of the mechanisms allegedly employed to disguise ownership and move illicit funds.

Brazilian authorities did not identify the cryptocurrencies involved or specify whether centralized exchanges or over-the-counter crypto brokers participated knowingly in the transactions.

Investigators also described how cocaine was concealed before export. According to the Federal Police, traffickers allegedly hid the drug inside bags of coffee, cement and mortar while also using chemical alterations to make detection during customs inspections more difficult.

The suspects are expected to face charges including participation in a transnational criminal organization, international drug trafficking and money laundering, alongside any additional offenses uncovered as the investigation continues.

Investigation adds to global scrutiny of crypto money laundering

Although authorities described cryptocurrencies as only one part of the alleged laundering operation, the case follows a series of recent investigations in which digital assets have appeared alongside conventional financial channels used to move criminal proceeds.

Earlier this month, Pakistan’s Federal Investigation Agency established a dedicated cryptocurrency investigation unit within its National Command and Control Centre to investigate suspected use of digital assets in money laundering, terrorism financing and other financial crimes. The unit operates separately from the Pakistan Virtual Assets Regulatory Authority, which supervises licensed crypto businesses, creating distinct roles for regulation and criminal enforcement.

Recent enforcement activity has also expanded elsewhere.

Earlier in July, Turkish prosecutors charged 504 people over an alleged illegal betting and money laundering network that investigators said moved nearly 40 billion Turkish liras through shell companies, jewelry businesses, payment providers and cryptocurrency transactions before transferring part of the proceeds overseas.

Chinese judicial officials have likewise called for changes to strengthen enforcement against virtual currency laundering. In an article published this month in the People’s Procuratorate Daily, prosecutors and legal researchers proposed new investigation guidelines, wider use of blockchain analytics, improved evidence rules and standardized procedures for recovering seized digital assets in criminal cases.

Several governments have also updated anti-money laundering policies as cryptocurrencies become more common in financial crime investigations.

In June, Ireland’s Department of Finance identified crypto assets as a “very significant” money laundering and terrorism financing risk in its latest National Risk Assessment. The government said it plans to introduce industry standards governing crypto-related sources of funds by the second half of 2027 while strengthening anti-money laundering controls across the financial sector.

Blockchain analytics companies have also reported rising compliance standards among regulated firms. Chainalysis said in a report released earlier this year that organizations entering the crypto market have adopted increasingly strict monitoring settings, although indirect exposure to illicit funds moving through intermediary wallets remains more difficult to detect than direct transfers.

Authorities across multiple jurisdictions have repeatedly emphasized that blockchain transactions often remain traceable, but investigators increasingly require specialized tools to follow funds moving through multiple wallets, bridges, exchanges and cross-chain networks.

One suspect dies after exchanging gunfire with police

During Thursday’s operation, the Federal Police said one suspect was killed after resisting arrest in the municipality of Igaratá in São Paulo state.

According to the agency, the individual opened fire on officers serving an arrest warrant. Police returned fire, and the suspect was wounded before receiving first aid. Authorities said he later died from his injuries.

The Federal Police added that no officers were injured during the incident.

The investigation remains ongoing as authorities continue examining the group’s alleged trafficking routes, financial structure and cross-border connections while pursuing additional evidence related to the suspected laundering network.

Introduction

For years, decentralized finance (DeFi) has been associated with crypto-native users navigating wallets, seed phrases, gas fees, and decentralized exchanges. While this ecosystem has unlocked billions of dollars in value, mainstream adoption has remained limited because the experience is often too technical for everyday users.

That is beginning to change.

The next evolution of DeFi isn’t about creating more standalone crypto apps—it’s about embedding decentralized financial services directly into the applications people already use. Whether it’s social media, e-commerce, gaming, ride-sharing, messaging platforms, or digital banking, embedded DeFi is transforming blockchain from a visible product into invisible infrastructure.

Just as most people use the internet without thinking about TCP/IP or DNS, future users may access DeFi every day without even realizing blockchain is powering the experience.

What Is Embedded DeFi?

Embedded DeFi refers to integrating decentralized financial services seamlessly into non-crypto applications.

Instead of requiring users to:

- Download a crypto wallet

- Purchase cryptocurrency separately

- Connect to decentralized applications

- Understand blockchain mechanics

Applications can provide financial services directly within familiar interfaces.

Examples include:

- Instant stablecoin payments inside shopping apps

- Tokenized rewards in food delivery platforms

- Yield-generating savings in digital banking apps

- Crypto-backed loans inside fintech applications

- Blockchain-powered loyalty programs

- Cross-border payments in messaging apps

The blockchain operates quietly behind the scenes while users simply enjoy better financial experiences.

One of crypto’s biggest challenges has never been technology—it has been usability.

Most consumers don’t want to learn:

- Gas optimization

- Private key management

- Wallet connections

- Token bridges

- Network switching

They simply want financial products that are:

Embedded DeFi removes complexity while preserving the advantages of decentralization.

This shift dramatically lowers the barrier to entry for millions of new users.

Everyday Applications Already Moving Toward Embedded Finance

Digital Banking

Many fintech companies are beginning to explore blockchain rails for:

- International transfers

- Stablecoin settlements

- Yield-bearing accounts

- Programmable payments

Users interact with familiar banking interfaces while blockchain improves efficiency underneath.

E-Commerce

Online stores can integrate DeFi-powered payment systems that offer:

- Near-instant settlements

- Lower transaction fees

- Global payment acceptance

- Automatic escrow

- Smart contract refunds

Customers enjoy faster checkout while merchants reduce payment costs.

Gaming

Modern blockchain games are moving away from speculative NFTs toward practical financial utilities.

Players can:

- Own in-game assets

- Trade items securely

- Borrow against digital collectibles

- Earn rewards automatically

- Receive revenue-sharing distributions

Financial services become part of gameplay rather than separate experiences.

Social Media

Creators can receive:

- Instant global tips

- Revenue sharing

- Tokenized memberships

- Subscription payments

- Community rewards

Instead of relying entirely on advertising revenue, creators gain direct monetization through decentralized payment rails.

Travel

Imagine booking hotels, flights, or transportation with stablecoins while receiving tokenized cashback automatically.

Smart contracts can also simplify:

- Insurance claims

- Refund processing

- Loyalty rewards

- Cross-border payments

Travel becomes faster and more transparent.

Stablecoins Make Embedded DeFi Possible

Stablecoins have become one of blockchain’s most practical innovations.

Unlike volatile cryptocurrencies, stablecoins maintain relatively stable values, making them suitable for everyday financial activity.

They enable:

- Payroll

- Merchant payments

- International remittances

- Subscription billing

- Treasury management

- Consumer savings

Because prices remain stable, businesses are increasingly comfortable integrating blockchain-based payment systems.

Stablecoins are becoming the financial foundation of embedded DeFi.

AI and Embedded Finance

Artificial intelligence makes embedded DeFi even more powerful.

Imagine AI assistants that automatically:

- Optimize savings

- Find better lending rates

- Rebalance investments

- Pay recurring bills

- Detect fraud

- Execute transactions securely

Rather than manually managing finances, users receive intelligent financial automation powered by decentralized infrastructure.

Challenges Ahead

While the future looks promising, embedded DeFi still faces important challenges.

Regulatory Compliance

Financial regulations differ across countries, requiring platforms to balance decentralization with legal requirements.

User Security

Wallet recovery, identity protection, and fraud prevention remain essential for mainstream adoption.

Scalability

Applications serving millions of users require blockchain infrastructure capable of handling massive transaction volumes with low fees.

Interoperability

Different blockchains must communicate efficiently to create seamless user experiences.

Cross-chain technologies continue to improve this capability.

The Road Ahead

The future of DeFi is likely to be defined less by standalone crypto platforms and more by invisible integration into the apps people use every day.

Instead of asking users to adapt to blockchain, developers are bringing blockchain to users in familiar, intuitive ways. This shift has the potential to accelerate global adoption by making decentralized finance accessible without requiring technical expertise.

As stablecoins, scalable blockchain networks, account abstraction, and AI continue to mature, embedded DeFi could become the standard financial layer beneath digital experiences—from shopping and gaming to social media and international payments.

The most successful blockchain products of the next decade may not be the ones with the most visible crypto features, but the ones where users never have to think about blockchain at all.

Conclusion

Embedded DeFi represents a major step toward mass adoption by hiding complexity while preserving the benefits of decentralized finance. Instead of asking users to navigate wallets, bridges, and gas fees, future applications will quietly deliver faster payments, smarter savings, global access, and programmable financial services within the apps people already trust.

The future of finance isn’t just decentralized—it’s seamlessly embedded into everyday digital life. When blockchain becomes invisible and financial experiences become effortless, DeFi will move beyond a niche technology and become an essential part of how the world interacts with money.

The company’s STORJ token fell 16% to about 6 cents. Almost $20 million worth of the token changed hands against a market value of about $27 million, meaning close to the entire supply turned over in a day. The token is down 79% over the past year and 98% from its March 2021 peak of $3.81.

The restructuring proposal contains a provision rarely seen in bankruptcy: Storj said it plans to share ownership of the reorganized company among management, token holders and investors.

Token holders normally have no legal claim on an issuer and receive nothing in a Chapter 11 process.

The filing extends an unusually heavy week. BitMEX, the exchange that invented the perpetual swap, said on July 23 it would shut down after 11 years, with daily volume down to roughly $400,000 and its BMEX token falling more than 90%.

Its parent, HDR Global Trading, said the platform was not insolvent and that assets exceeded liabilities, pointing instead to a strategic review that followed some $200 million in regulatory fines and a sale process that found no buyer.

BitMart announced its own wind-down on Sunday, halting new deposits and trading orders immediately, ending all trading on Aug. 26 and setting a January 2027 closure, with its BMX token down 58% on the news.

‘Why different rules for different players?’ – Abhishek Sharma’s poor form sparks Sanju Samson debate

Making sense of the panic over Chinese AI

BITCOIN: This Is Why It’s PUMPING! (massive) – BTC Price Prediction Today

Renter of Home in Anne Heche Crash Denies Settlement With Son

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Weekend Open Thread: Staud – Corporette.com

BITCOIN: This Is Why It’s PUMPING! (massive) – BTC Price Prediction Today

How much to fly the world’s biggest plane? #antonov #aviation #money

Bitcoin (BTC): The Hidden Pattern No One Is Watching! Another Crash Incoming? (WATCH ASAP)

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World6 days ago

Crypto World6 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat6 days ago

NewsBeat6 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech6 days ago

Tech6 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech6 days ago

Tech6 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

NewsBeat7 days ago

NewsBeat7 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Tech10 hours ago

Tech10 hours agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Business5 days ago

Business5 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment6 days ago

Entertainment6 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Tech7 days ago

Tech7 days agoWatch Flock Safety CEO Garrett Langley discuss the future of surveillance at TechCrunch Disrupt 2026

-

Crypto World4 days ago

Crypto World4 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

NewsBeat6 days ago

NewsBeat6 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Crypto World7 days ago

Crypto World7 days agoCircle’s President Sold Over 360,000 Shares, The Filings Explain Why

-

Sports14 hours ago

Sports14 hours agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

News Videos4 days ago

News Videos4 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Sports3 days ago

Sports3 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Politics22 hours ago

Politics22 hours agoSpain sweeps the board at 2026 World Cup with individual awards

-

Fashion3 days ago

Fashion3 days ago16 Dresses for the High Summer Event

-

Crypto World6 days ago

Crypto World6 days agoAndrew Cuomo joins OKX board as crypto exchange expands in U.S.

-

Tech7 days ago

Tech7 days agoThe 35 Best Board Games for Family Game Night

You must be logged in to post a comment Login