Crypto World

DeFi Lending’s Risk-Reward Ratio Sparks Debate Between Researchers and Curators

An analysis of Morpho markets finds depositors are undercompensated by 5-10x. Curators counter that empirical loss data tells a different story.

Overcollateralized lending has emerged as one of DeFi’s most durable primitives.

Morpho alone holds roughly $7 billion in TVL, according to DeFiLlama, with distribution via Coinbase, Kraken, and other front ends. Apollo Global Management has committed to acquiring up to 9% of MORPHO’s token supply over four years, and the Ethereum Foundation has deployed nearly $19 million into the protocol’s vaults.

But a quantitative analysis published Sunday by Dirt Roads, a DeFi research publication authored by Luca Prosperi, has sparked a debate over whether the depositors fueling that growth are being systematically undercompensated, or whether the lending primitive is working exactly as it should.

Bear Case: Depositors Are Selling Puts They Don’t Understand

Prosperi’s analysis adapts the Black-Cox first-passage framework – a refinement of Merton’s 1974 structural credit model – to DeFi collateralized debt positions. In this context, depositing USDC into a Morpho vault backed by ETH collateral is equivalent to holding a risk-free bond and simultaneously selling a put option on that collateral, with the liquidation loan-to-value (LLTV) acting as the strike price.

Calibrated to ETH’s approximately 75% annualized realized volatility, jump intensity of 1.5 events per year with a mean jump size of -8.3%, and an LLTV of 86% against a 70% starting LTV, the model shows that the appropriate credit spread ranges from 250 to 400 basis points above the risk-free rate, in this case the Fed’s Secured Overnight Financing Rate (SOFR).

Observed depositor rates in flagship Morpho USDC markets are roughly 2-4% APY – thin margins above SOFR, which currently stands at 3.65%.

Crypto investor Santiago Roel endorsed the findings, arguing that $11.7 billion in Morpho vaults is retail capital funding crypto-collateralized lending “thinking it’s a savings account.” No institution, he says, would accept near risk-free rates to come on-chain. He pointed to a structural shift from early DeFi — when triple-digit APYs at least compensated for risk — to a present where vaults with completely different risk profiles present the same thin yields, and depositors simply pick the highest number.

“Last cycle we saw a lot of retail pour savings into algo stablecoins promising ‘risk-free’ yield,” Roel wrote. “This cycle vaults have a lot of demand but they are mispriced for the level of risk.”

Bull Case: It’s a Repo, Not a Put Option

The pushback came swiftly from practitioners with skin in the game and challenged not just the model’s inputs but its foundational analogy.

Steakhouse Financial’s adcv, whose firm curates the primary Morpho vaults that Coinbase routes retail deposits through, argues that on-chain lending is structurally closer to a repurchase agreement than a put option sale.

In a repo, one party temporarily exchanges an asset for cash with a commitment to repurchase and, critically, the lender holds the collateral outright throughout the transaction. On Morpho, collateral is locked in smart contracts and can be seized and liquidated atomically if value declines toward the LLTV threshold. The lender’s exposure is bounded not by the theoretical option payoff on the collateral’s full volatility distribution, but by the narrow residual risk that liquidation mechanics fail to make the lender whole.

This reframing leads to adcv’s central empirical objection: the loss-given-default (LGD) parameter. Prosperi’s model sets LGD at approximately 5%, derived from Morpho’s formulaic liquidation incentive. But the liquidation penalty is a cost borne by borrowers — not a loss absorbed by lenders. For liquid crypto-native collateral on prime markets, on-chain liquidation has historically resulted in near-zero bad debt for depositors because the overcollateralization buffer, continuous oracle monitoring, and open liquidator competition work as designed.

Steakhouse’s own data supports the claim. During the sharp selloff in late January and early February, when BTC fell 17% and ETH dropped 26% in a single week, Morpho processed approximately $238 million in liquidations. Users of Steakhouse’s vaults absorbed zero bad debt and maintained full withdrawal liquidity throughout.

“If you set the LGD parameter to a few basis points over 0% rather than approximately 5%, the model outputs fall exactly in line with observed rates at around 3-30 basis points,” adcv wrote.

Hasu, a strategy lead at Flashbots, made the same point more bluntly.

“Great model, but bad data in, bad data out,” he wrote. “If you use the historically observed level of bad debt on Morpho prime markets, even with a big safety buffer, the result changes: Now, depositors should demand an excess return of only 3-30bps, which is in line with rates observed in the wild.”

The Real Risk Is Fundamental, Not Market

MonetSupply, a contributor at Spark, offered a third perspective that aligns broadly with the curators’ position but redirects the risk conversation entirely. The bulk of the risk in on-chain prime repo, he argued, is not from market price-jump risk – the variable that Prosperi’s model centers on – but from fundamental and technical risks embedded in collateral assets and oracle mechanisms.

Most blue-chip collateral in Ethereum DeFi consists of tokenized Bitcoin (WBTC, cbBTC) or liquid staking tokens (wstETH, weETH). These issuers have long track records, but remain subject to custody and key management failures, smart contract vulnerabilities, and business continuity risks. Oracle providers introduce an additional dependency layer. The probability of incidents across these vectors is low, MonetSupply argues, but losses in a failure case can reach 100% of exposure – a fat-tailed distribution that Merton-style market risk models do not capture.

He pointed to the most recent major DeFi loss events – the Resolv exploit and the Drift Protocol vault drain – as evidence. Both were driven by fundamental risk factors, not market volatility. “As a DeFi lender, the primary driver of risk is these fundamental factors rather than jump risk,” he wrote.

MonetSupply also offered the most rigorous version of the structural premium argument, framing it through the lens of liquidity premia and convenience yield. For traditional finance investors, prime money market funds and T-bills are the benchmark liquid assets, and they would never accept sub-SOFR yields. But for crypto-native actors, the relevant measure of liquidity is not speed-to-bank-account but speed-to-on-chain-execution. A directional crypto fund facing even a one-hour delay between requesting redemption of a money market fund and receiving a wire to their exchange account could miss a 5-10% move in a volatile asset, he argued, wiping out years of excess risk-adjusted return over on-chain repo.

Convenience yield — the implied return on holding inventory close at hand — provides the same logic from a different angle. If on-chain actors derive meaningful benefit from having capital instantly deployable within the crypto ecosystem, even if that benefit is realized infrequently, it can be entirely rational to accept risk-adjusted returns below SOFR on prime repo.

Spark’s own USDT savings vault, MonetSupply noted, maintains over $700 million in available withdrawal capacity against $885 million in total deposits, far exceeding those of typical on-chain lending markets, which already offer a significant liquidity advantage over off-chain cash equivalents.

DeFi’s Structural Advantages

A separate thread in the debate argues that the risk-free rate comparison itself is flawed on even simpler grounds.

Pseudonymous trader MilliΞ contends that DeFi yield carries structural properties traditional fixed income does not: composability that enables permissionless derivative applications, censorship-resistant access without custodians who can “play silly games with you,” and instant withdrawals versus the 30-day redemption windows typical of money market instruments.

“This may not matter to most of us first-worlders,” they wrote, “but it sure matters to the remainder of the planet.”

Where Both Sides Agree

Nobody disputes that the vast majority of retail depositors flowing into Morpho through exchange front-ends do not understand the credit exposure they are taking, and that vault risk profiles vary dramatically even when headline yields look similar.

Similarly, no one disputes that the track record supporting the curators’ optimistic loss assumptions is short and tested only in broadly favorable conditions; a point underscored by the Resolv exploit that cascaded across fifteen Morpho vaults in March, and the Stream Finance collapse that hit lending markets in November 2025. Steakhouse’s own vaults avoided those losses, but other curators’ depositors were not as fortunate.

Prosperi’s analysis also flags concerns outside the LGD debate. Leverage looping strategies, such as recursive wstETH/WETH or sUSDe loops at 7-10x effective leverage, behave not as credit products but as leveraged carry trades on mean-reverting basis spreads, where a 5% depeg at 10x leverage triggers liquidation. And the growing push to onboard non-crypto-native collateral breaks every assumption in the framework simultaneously: unobservable volatility, discrete oracle monitoring, multi-week liquidation delays, and jurisdictional enforcement risk.

The Real Test

The core disagreement is over which measure of risk matters: the structural exposure embedded in the position, or the empirical loss history of the platform. Prosperi and Roel argue the former; Hasu, adcv, MonetSupply, and the curator ecosystem argue the latter – while adding that the model is looking at the wrong risk entirely, and that rational actors may have good reasons to accept thin or even negative spreads over SOFR.

Structural models can overstate market risk by assuming passive borrower behavior and ignoring the efficiency of on-chain liquidation mechanics, which have performed as advertised even under severe conditions. But they may understate the fundamental risks that MonetSupply identifies, which lie entirely outside the analysis framework. Meanwhile, empirical models can understate risk by extrapolating from a short, favorable sample.

As institutional allocators expand on-chain credit exposure, the question may ultimately be settled not by models but by the next sustained drawdown, or the next fundamental failure.

“The mispricing will become visible when the market turns,” Prosperi wrote. The curators are betting it won’t, and vault depositors agree with them, at least for now.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

Spot Bitcoin ETFs recorded their strongest daily inflows since February on Monday despite ongoing geopolitical tensions.

Crypto markets retreated on Tuesday as President Donald Trump’s self-imposed deadline for Iran to reopen the Strait of Hormuz drew closer, dampening risk appetite across global markets.

Bitcoin is trading at $69,200, according to CoinGecko, recovering from an intraday dip below $68,000 but still well off Monday’s brief push above $70,000. Ethereum is changing hands at $2,112, while Solana trades at $82. XRP fell 1.6% to $1.32.

The total cryptocurrency market capitalization stands at approximately $2.45 trillion, down less than 1% in the past 24 hours.

Among the top 100 tokens by market cap, Rain (RAIN) led gainers with a 9.8% rise, followed by Zcash (ZEC), up 8% to $276. On the downside, Algorand (ALGO) dropped 7%, and Avalanche (AVAX) fell 6.2% to $8.75.

Iran Deadline Dominates Sentiment

Trump escalated his rhetoric early Tuesday, posting on Truth Social that “a whole civilization will die tonight” if Iran fails to comply with demands to reopen the critical shipping lane that handles roughly one-fifth of global oil and gas flows. Vice President J.D. Vance said the military objectives of the war in Iran have been achieved, but the administration’s ceasefire demands remain unmet.

U.S. equities ended the day mostly unchanged, while West Texas Intermediate crude held above $110 per barrel as fears of continued supply disruption weighed on energy markets.

Traders widely expect the Federal Reserve to hold rates steady at its April meeting, reflecting the view that wartime inflation will keep the central bank sidelined.

ETF Inflows Defy Risk-Off Mood

Despite the geopolitical turmoil, spot Bitcoin ETFs posted $471 million in net inflows on Monday, the largest single-day intake since Feb. 25, according to SoSoValue.

The figure sits well below January’s peak flow regime, when multiple trading days topped $700 million, but marks a notable acceleration after BTC and ETH ETFs reversed a multi-week outflow streak in late February. March saw $1.32 billion in total net inflows, coinciding with Bitcoin’s first green monthly candle in six months.

Liquidations and Derivatives

Bitcoin alone accounted for roughly $92 million in liquidations over the past 24 hours, according to CoinGlass. Liquidations were almost equally shared between long and short positions amid choppy trading.

The Crypto Fear & Greed Index sits at 11, deep in extreme-fear territory and near the lowest sustained readings since the Terra collapse in mid-2022.

Looking Ahead

The immediate catalyst for market direction is the 8 PM ET Iran deadline. Trump has repeatedly extended similar ultimatums in recent weeks, blunting their market impact, but the scale of rhetoric suggests tonight could break the pattern in either direction.

Bitcoin has been range-bound between $62,000 and $75,000 since early February. A resolution in the Strait of Hormuz standoff would likely trigger a relief rally across risk assets.

TLDR

- The number of Cardano whale wallets holding over 10 million ADA has reached a four-month high.

- Whale activity increased by 5.2% over the past nine weeks, despite ADA’s price remaining depressed.

- ADA’s price is 11% higher than its lowest point in February, but has not shown significant upward movement.

- Cardano’s network processed over 4 billion ADA in transactions, amounting to over $1 billion in on-chain volume.

- Large holders accumulated 220 million ADA in March, bringing their total holdings to nearly 14 billion tokens.

The number of wallets holding over 10 million ADA tokens has reached a four-month high of 424. According to Santiment, this marks a 5.2% rise over the past nine weeks, even though Cardano’s price remains subdued. Despite the increased whale activity, ADA continues to trade below its previous highs.

Cardano Whale Activity Shows Strong Accumulation

Recent data from Santiment reveals that ADA’s price is 11% higher than its February 5 low this year. However, the rise in whale activity has not led to an immediate price surge. Santiment suggests that if the accumulation persists while the price remains low, it could eventually lead to a bullish divergence.

Analytics platform TapTools reported a 4 billion ADA transaction volume over the last five days, equating to over $1 billion. This shows that the increased activity among whales is paralleled by rising network usage. Despite this, the price of ADA has not yet reacted positively, remaining stuck below key resistance levels.

ADA’s Struggles Continue Amid Increased Whale Holdings

Whale interest in Cardano has been noticeable for weeks, with analysts like Ali Martinez highlighting that large holders accumulated 220 million ADA in late March. These whales now hold nearly 14 billion ADA, making up around 37% of the total supply. However, ADA’s price continues to remain stagnant, trading at $0.24, a 42% decline in the past three months.

Even with the accumulation trend, ADA’s price remains 92% lower than its all-time high of over $3. Cardano’s recent performance in terms of trading volume also lags behind competitors like Solana and XRP, which processed $2.6 billion and $1.5 billion in transactions, respectively, over the same period. This shows that while whale activity is increasing, ADA’s broader market performance remains underwhelming.

Bearish Trend Persists Despite Growing Whale Interest

Despite the uptick in whale holdings, ADA continues to trade below its 50, 100, and 200-day exponential moving averages. This keeps the broader trend bearish, regardless of the accumulation. On Twitter, user gnarleyquinn raised concerns, suggesting that Cardano’s market dominance, which has dropped from 4.5% in 2021 to around 0.3% today, may lead to a decline in the coming years.

The ongoing price struggles show that Cardano has not decoupled from the broader altcoin market. While whales continue to accumulate, ADA’s future price movements remain uncertain. It remains to be seen whether the increasing accumulation will ultimately lead to a change in price dynamics for Cardano.

According to the bureau, a large number of minors aged 17 and younger were included in complaints related to crypto or crypto ATMs, resulting in more than $5 million in losses.

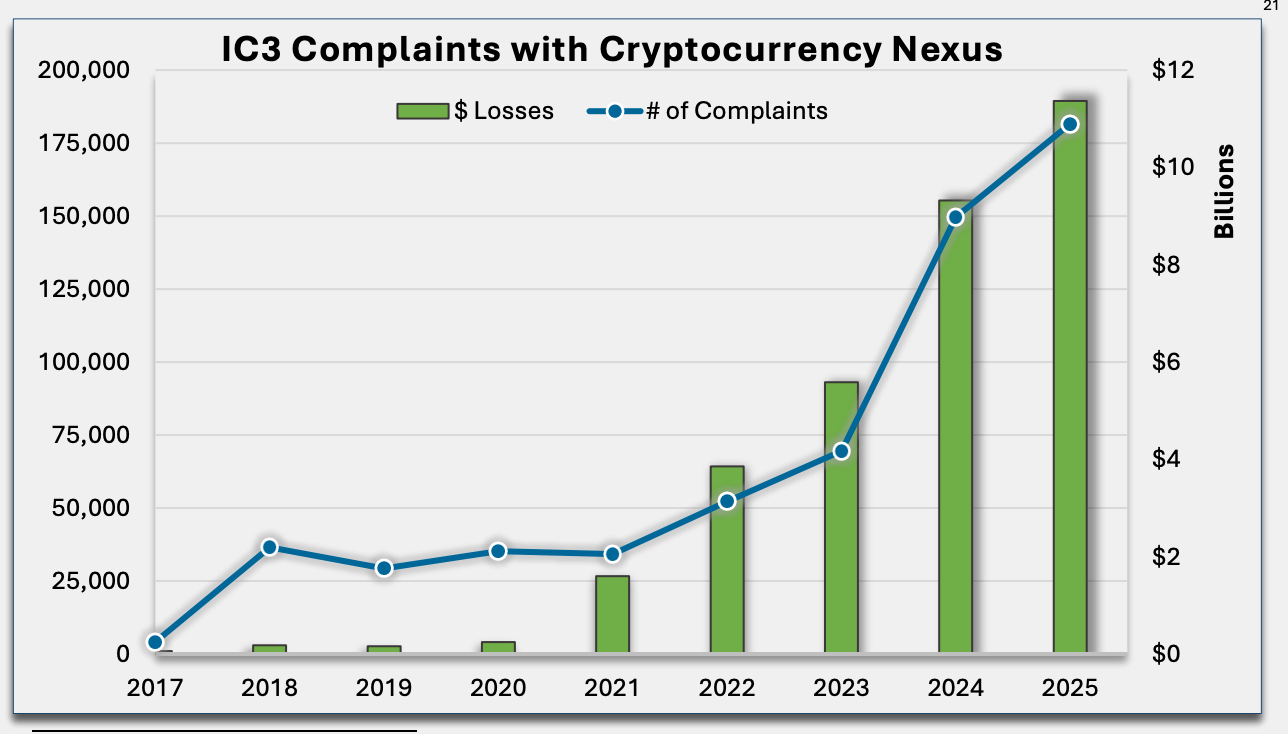

The US Federal Bureau of Investigation (FBI) reported that Americans’ losses from crypto-related scams increased to more than $11 million in 2025.

In its annual internet crime complaint report released on Monday, the FBI said that cryptocurrency and AI-related scams were “among the costliest” for Americans in 2025, with 181,565 complaints totaling more than $11 billion. According to the bureau, it received more than one million complaints in 2025 reporting losses of about $21 million due to cyber-enabled crimes.

The FBI’s Internet Crime Complaint Center reported that investment scams resulted in the highest percentage of victims reporting losses in crypto as opposed to cash, debit cards, gift cards and other media of exchange. In addition, about 10% of the 13,168 complaints involving cybercrimes targeting minors aged 17 and younger were related to crypto or crypto ATMs, resulting in more than $5 million in losses.

The complaints the FBI received were despite the bureau’s efforts to “identify and notify people who are currently falling victim to cryptocurrency investment fraud” through its Operation Level Up in 2024. Globally, blockchain analytics platform Chainalysis reported in March that illicit addresses received $154 billion in 2025, driven in part by sanctions evasions.

Related: Cambodian lawmakers propose severe prison time for crypto scammers

Scammers use Tron blockchain token to con users using FBI

According to the FBI report, there were 32,424 complaints involved in impersonation of government officials, resulting in about $800 million in losses. However, the report did not mention bureau officials issuing a March notice warning Americans that a token on the Tron blockchain was impersonating the FBI with the goal of obtaining personal information.

Tron users reported receiving a token with the FBI logo claiming that their wallet was “under investigation.” The users were then prompted to enter personal information under the guise of an FBI anti-money-laundering verification to avoid their accounts being frozen.

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

A fresh wave of online backlash is now building around Pakistan’s request to extend Trump’s Iran deadline, with users questioning whether the move was genuinely independent.

The speculation centers on the edit history of Prime Minister Shehbaz Sharif’s post on X. History shows an earlier version of the message, followed by a more detailed “draft” version that explicitly calls for a two-week extension and reopening of the Strait of Hormuz.

Some users claim this suggests coordination behind the scenes. The theory is simple: if the US agrees to extend the deadline, framing it as a response to Pakistan’s request allows Washington to avoid appearing to back down under pressure.

There is no evidence supporting this claim. Neither the White House nor Pakistani officials have indicated any coordinated messaging strategy.

Still, the timing has fueled suspicion. The post appeared just hours before Trump’s deadline, as negotiations intensified and markets reacted sharply.

In volatile geopolitical moments like this, narratives form quickly. Right now, this one is being driven by inference, not confirmation.

The post Internet Questions Pakistan’s Role in Trump’s Iran Deadline Twist appeared first on BeInCrypto.

TLDR

- Charles Schwab outlines two approaches for integrating cryptocurrencies into investment portfolios.

- The return-based approach focuses on expected returns, volatility, and asset correlations.

- Schwab recommends modest allocations to bitcoin and ether based on expected returns.

- The risk-based approach focuses on managing overall portfolio risk from crypto exposure.

- Schwab warns that even small allocations to crypto can significantly raise portfolio risk.

Charles Schwab, the leading U.S. brokerage firm managing over $12 trillion in assets, recently outlined two approaches for integrating cryptocurrencies into investment portfolios. The firm emphasized that while there is no fixed method for crypto allocations, investors should carefully consider their risk tolerance and long-term objectives. Schwab’s research highlights the potential for diversification, though it warns that even small allocations to crypto can significantly increase portfolio risk.

Return-Based Approach to Crypto Investments

In its white paper, Charles Schwab detailed a return-based approach to crypto investing, which is rooted in expected returns. This method examines the anticipated returns, volatility, and correlations with traditional assets like stocks and bonds. Schwab suggests that if investors expect a return of 15% per year from Bitcoin, a conservative portfolio might allocate around 1%, while a more aggressive one could allocate up to 8.8%.

The firm noted that ether, due to its higher volatility, would warrant smaller allocations. For example, a conservative portfolio might allocate just 0.1% to ether, while a more aggressive portfolio might allocate up to 2.5%. Schwab also stressed that if returns for either bitcoin or ether fall below 10%, it might not justify any allocation, even for more risk-tolerant investors.

Risk-Based Approach to Crypto Exposure

Charles Schwab also presented a risk-based approach to crypto allocation, where the focus shifts from returns to managing overall portfolio risk. In this approach, the crypto exposure is determined by the amount of total portfolio risk that comes from cryptocurrencies. For instance, in a conservative portfolio, a 1.2% allocation to bitcoin or 0.9% to ether could represent 10% of the total portfolio risk.

For moderate to aggressive portfolios, Schwab suggests allocating up to 4% in bitcoin and nearly 3% in ether to achieve similar risk levels. Schwab explained that this risk-based method is particularly useful for investors who want to understand how crypto fits into their broader asset mix. While crypto may offer diversification benefits, Schwab cautioned that increasing exposure comes with heightened portfolio concentration risk.

Charles Schwab’s Crypto Exposure Options

As Schwab moves forward with its new crypto offering, Schwab Crypto, it has also been providing exposure through various products like crypto-related stocks and exchange-traded products. Schwab has introduced a waitlist for clients interested in buying and selling bitcoin and ether directly. For now, the brokerage firm offers crypto exposure through over-the-counter trusts and futures for approved clients.

Despite initially dismissing cryptocurrencies as “purely speculative” in 2019, Schwab has evolved its stance on digital assets over time. The firm now encourages investors to carefully evaluate the role that crypto could play in their portfolios, keeping in mind the elevated risks associated with even a small allocation.

Crypto World

Next Crypto to Explode as Bitcoin Stands Firm Above $68K and Solana ETFs Hold $1.5 Billion, but Pepeto Is the Entry That Defines This Cycle

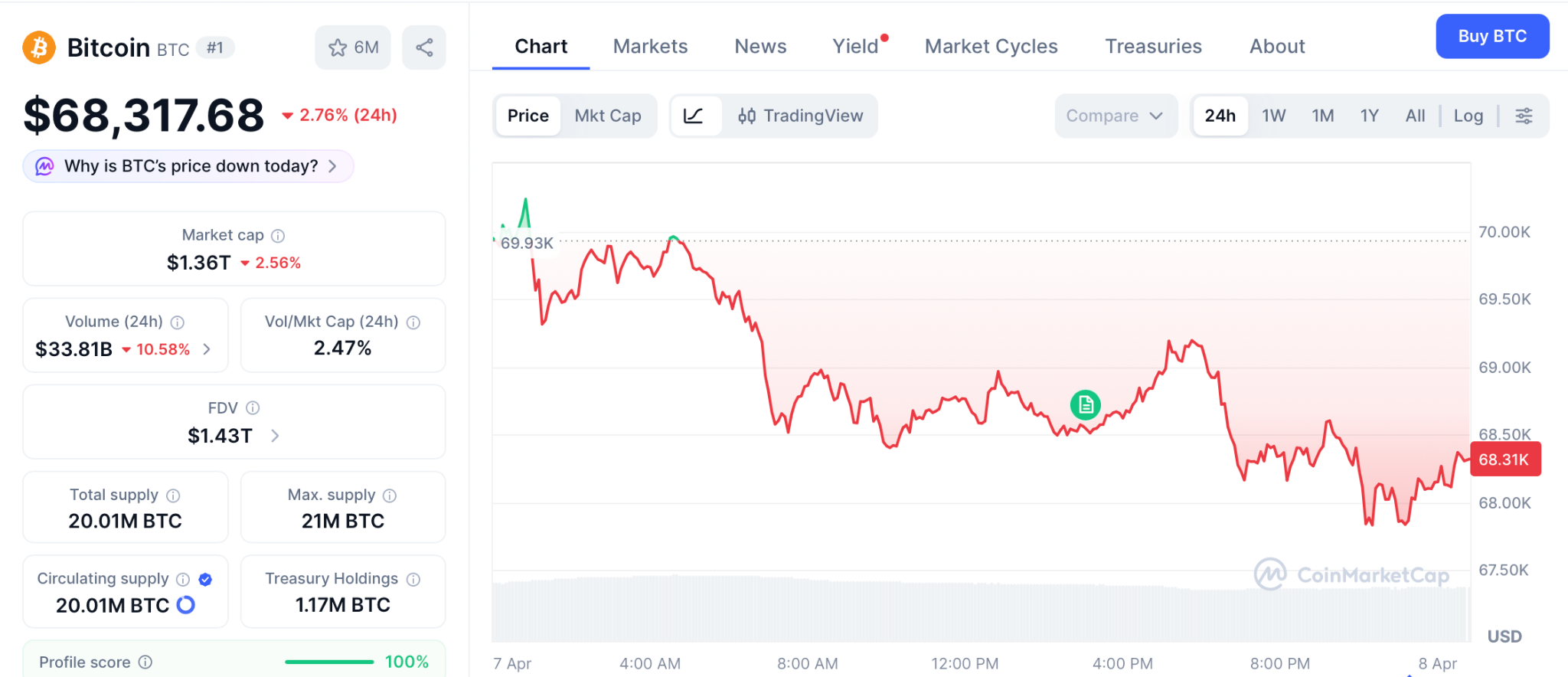

The crypto market is heating up, and the prices sitting in front of you right now will not be here when the rally kicks in. Bitcoin held $68,317 on April 7 after Iran rejected the ceasefire, per CoinDesk, and Solana ETFs kept $1.5 billion in total inflows despite SOL crashing 57% from its peak. Every indicator that marks the start of a rally is lighting up.

But the next crypto to explode is never the coin everybody already holds at a trillion-dollar valuation. It is the presale where listing day creates the gain and exchange revenue locks it in. Here is which one ticks every requirement.

Bitcoin sat at $68,317 on April 7 after absorbing Iran.s ceasefire rejection, per CoinDesk, while BTC ETFs pulled $471 million on April 6. The Fear and Greed Index sits at 9, and altcoins bounced broadly.

The market is shifting bullish, and the traders who connect those dots are searching for the breakout alt at presale cost before the listing turns cheap entries into the bags everybody else spends the cycle regretting.

The Next Crypto to Explode Sits Below the Rally While Large Caps Grind

Pepeto: Revenue Sharing That Pays From Every Trade, at a Price the Bull Market Will Erase

Bull runs pay the people who bought during panic. The wallets that loaded Pepeto during the crash are now watching the market prove them right. Revenue sharing gives every presale holder a lasting share of trading fees based on position size, confirmed by Business Insider. BTC, SOL, and XRP generate zero income for holders. Pepeto earns on every single transaction.

SolidProof cleared the contract before the presale opened, and a former Binance executive is leading the listing plan for the exchange with its cross-chain bridge, zero-cost swaps, and token risk scoring. The $8.82 million raised came from wallets that checked every alternative and picked this one. The founder who took the original Pepe coin to $7 billion is channeling that same viral pull into tools that generate actual revenue.

At $0.0000001863, the gap between presale and listing gives a floor that no large cap can offer. 186% APY staking adds to your position while the listing gets closer, but that is just the extra.

The real payoff comes when a revenue-earning exchange token hits live bull market trading, and every bag at this price turns into supply that post-listing buyers have to purchase from you. The next crypto to explode door is closing quicker than anyone expects.

Solana: $1.5 Billion in ETF Inflows but SOL Stuck at $79

SOL trades near $79 with $1.5 billion in cumulative ETF capital proving institutional belief even as the price dropped 57% from its high, per CoinGecko. A break above $86 could push toward $100 as the broader market builds.

Strong base, but from $79 the upside is capped for anyone searching for the next crypto to explode that transforms a portfolio.

Bitcoin: Holding $68K With $80,000 as the Next Major Target

BTC held $68,317 on April 7 per CoinMarketCap and $74,500 is the final resistance before a clean run to $80,000. The $471 million in ETF capital on April 6 proves institutional appetite, and analysts keep their sights above $150,000 by December 2026.

Bitcoin is out front with clear strength, but the next crypto to explode requires numbers that go past what a $1.3 trillion coin can deliver.

The Bull Market Is Here and the Entry That Defines It Is Still Open

Step back and the whole picture becomes clear. The market tips bullish, Bitcoin refuses to break, institutions keep arriving, and Pepeto is sitting in the setup that appears once per cycle: permanent revenue sharing, SolidProof audit, a founder who generated $7 billion in demand, and exchange tools the Binance listing switches on.

Every massive crypto winner follows one pattern: a few wallets entered first, everyone else found out after, and the cheap price was gone. That sequence is playing out right now, and once the listing drops the presale cost disappears forever. Visit the Pepeto official website and make the move that puts you on the side that caught this cycle instead of the side that watched it happen. The next crypto to explode never waits for the crowd to agree, it moves while they debate, and Pepeto at $0.0000001863 is already moving.

Click To Visit Pepeto Website To Enter The Presale

FAQs

Why is the crypto market turning bullish right now?

Bitcoin held $68,317 after Iran rejected ceasefire, ETFs pulled $471 million on April 6, and Fear and Greed at 9 historically marks the bottom before major rallies.

Where can I find the next crypto to explode before listing?

Visit the Pepeto official website at $0.0000001863 with 186% APY staking and exchange tools ready for bull market volume.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

The latest AI news artificial intelligence US military Iran war 2026 debate has crystallized around one figure: in the first 24 hours of Operation Epic Fury on February 28, the US military struck more than 1,000 targets in Iran using Palantir’s Maven Smart System with Anthropic’s Claude embedded inside it — a pace CENTCOM head Admiral Brad Cooper confirmed publicly, and one that human rights experts say has raised serious questions about AI-assisted targeting and civilian harm.

Summary

- CENTCOM Commander Admiral Brad Cooper confirmed in a March 11 video statement that US forces are “leveraging a variety of advanced AI tools” that allow commanders to make decisions “faster than the enemy can react,” with tasks that previously took hours or days now completed in seconds

- Palantir’s Maven Smart System with Anthropic’s Claude embedded processes satellite imagery, drone feeds, radar data, and signals intelligence into prioritized target lists with GPS coordinates, weapons recommendations, and automated legal justifications — what previously required roughly 2,000 intelligence analysts now reportedly requires approximately 20

- A US strike on a girls’ elementary school in Minab killed over 165 civilians, according to Iranian reports; the Pentagon is investigating whether the school was on an AI-assisted target list, and more than 120 House Democrats have demanded answers

The latest AI news artificial intelligence US military Iran war 2026 story is both a technological milestone and a humanitarian reckoning. According to IBTimes, more than 1,000 targets were struck in the first 24 hours of Operation Epic Fury on February 28 — more than double the air power deployed during the entire opening phase of the 2003 Iraq invasion. That pace is only possible with AI. A human-led targeting process would have required thousands of analysts working for weeks to generate and validate that many aim points.

The system at the center of it is Palantir’s Maven Smart System, running on Anthropic’s Claude large language model. Maven fuses classified feeds from satellites, surveillance drones, and archived intelligence into a unified platform. Claude synthesizes that information into prioritized target lists, complete with precise GPS coordinates, weapons recommendations, and automated legal justifications for strikes.

Admiral Brad Cooper confirmed the AI role in a publicly released video statement: “These systems help us sift through vast amounts of data in seconds so our leaders can cut through the noise and make smarter decisions faster than the enemy can react. Humans will always make final decisions on what to shoot and what not to shoot and when to shoot. But advanced AI tools can turn processes that used to take hours and sometimes even days into seconds.”

Cooper did not identify specific AI systems by name. What the statement left unaddressed was Maven’s reported accuracy rate: approximately 60%, compared with 84% for human analysts in some assessments.

The School Strike and the Accountability Gap

The most serious accountability question surrounds a US strike on the Shajareh Tayyebeh girls’ elementary school in Minab that killed over 165 civilians. The school was reportedly on a target list generated with AI assistance. Pentagon officials said outdated intelligence contributed to the strike and a full investigation is underway. More than 120 House Democrats have formally demanded answers about AI’s role. As warfare expert Craig Jones told Democracy Now!, AI targeting is “reducing a massive human workload of tens of thousands of hours into seconds and minutes” — but “automating human-made targeting decisions in ways which open up all kinds of problematic legal, ethical and political questions.”

The conflict carries direct implications for commercial tech. Iran has explicitly named Palantir, Google, Microsoft, Amazon, and other US companies as legitimate military targets because of their infrastructure’s role in the war. Iranian strikes have already damaged AWS data centers in the UAE and Bahrain. As crypto.news reported, Iran has demonstrated willingness to strike economic and technology infrastructure across the Gulf — a threat that now extends to the commercial cloud backbone powering US AI military systems.

What the Iran war has confirmed, as analysts have begun calling it “the first AI war,” is that commercial AI and warfare are no longer separate domains. As crypto.news noted, every escalation in this conflict reaches financial markets within hours. The AI targeting dimension adds a new layer of systemic risk: not just military escalation, but the weaponization of commercial technology infrastructure itself.

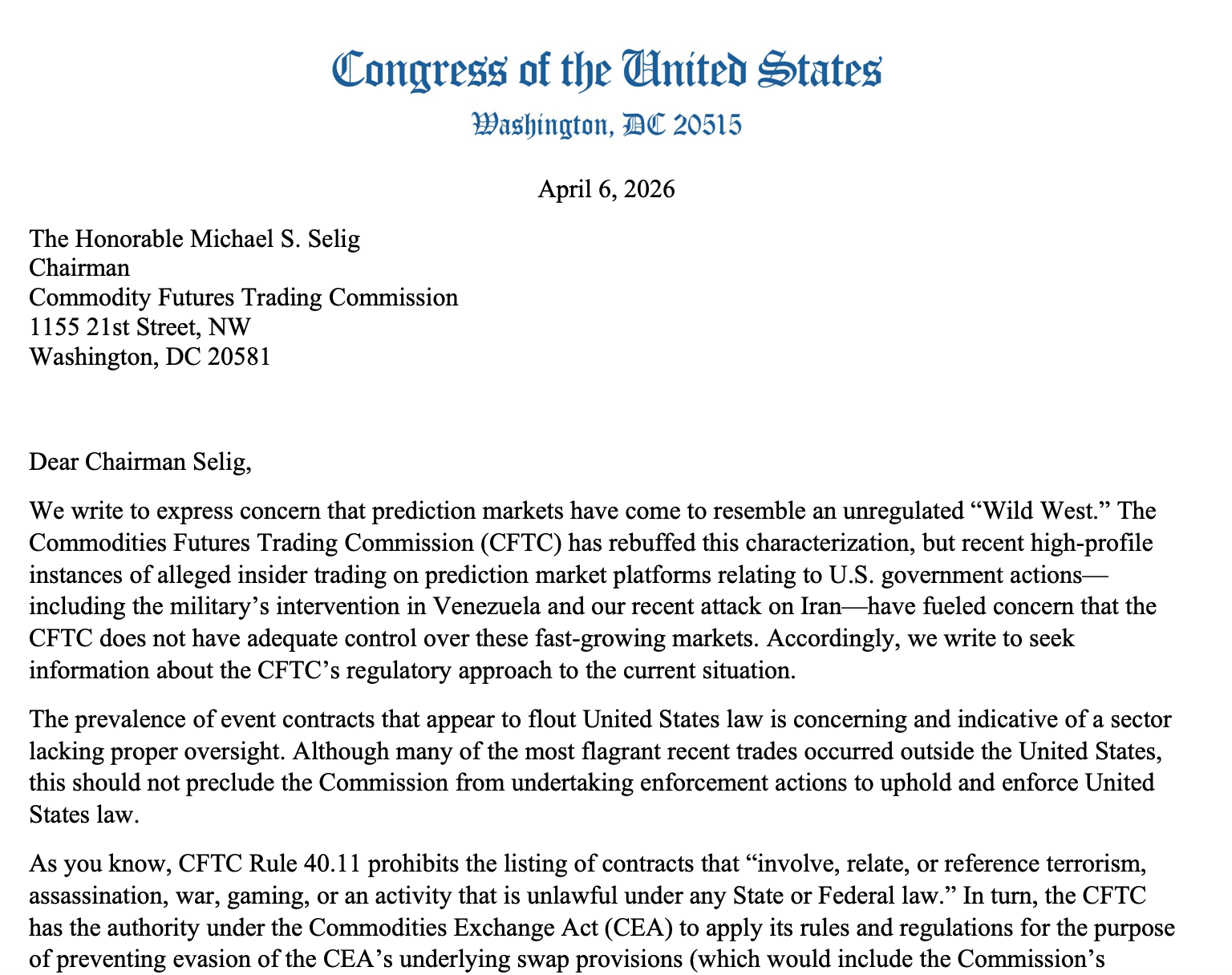

The seven House members may have affirmed the commission‘s authority over prediction markets, but asked questions about its inaction on insider trading.

Seven members of the US House of Representatives sent a letter to Commodity Futures Trading Commission (CFTC) Chair Michael Selig, asking for information on the agency’s inaction on insider trading on prediction markets and event contracts related to war and conflicts.

In a Monday letter, the seven US lawmakers said that the CFTC had the authority under the Commodities Exchange Act “to apply its rules and regulations for the purpose of preventing evasion of the [act’s] underlying swap provisions.” The statement signaled that the representatives affirmed Selig’s position that the commission had jurisdiction over prediction markets.

However, the House members expressed concerns about how the CFTC was policing “morally obscene” event contracts, including those on US military actions in Iran and Venezuela — in those cases, there were suspicious trades related to the timing and outcomes of US military involvement.

“Such corrupt trades deserve swift and decisive oversight,” said the letter. “Allowing these contracts to persist raises troubling concerns about the Commission’s desire and capacity to fulfill a global regulatory role.”

The legal battles over regulating prediction market platforms like Kalshi and Polymarket are being waged both at a federal and state level. Several US state gaming authorities have filed lawsuits alleging that the companies are illegally offering sports bets, while the CFTC, under Selig, claims that the event contracts on the platform amount to swaps and fall under its federal regulations.

The seven House members requested that Selig respond to their six questions by April 15.

Related: Polymarket bags 97% of onchain prediction market fees after pricing overhaul

In one of the most recent legal decisions, the US Court of Appeals for the Third Circuit affirmed a lower court ruling blocking New Jersey gaming authorities from filing enforcement actions against Kalshi. Two out of three circuit judges said that the company had a ”reasonable chance of success” in arguing that federal commodities laws preempted state authorities.

CFTC enforcement director says agency is “watching” for insider trading

The Monday letter followed CFTC enforcement director David Miller responding to concerns over insider trading, which has also resulted in legislation proposed by Democrats. According to Miller, the commission would only prosecute instances “against those who tip or trade with misappropriated information,” but not dedicate resources to “trivial” cases.

Magazine: All 21 million Bitcoin is at risk from quantum computers

TLDR

- Anthropic unveiled its new AI model, Claude Mythos, designed to enhance cybersecurity by identifying high-severity vulnerabilities in systems.

- The Mythos model has already detected thousands of flaws across major operating systems and web browsers.

- Anthropic launched Project Glasswing, a partner program offering select organizations early access to the Mythos model for defensive tasks.

- The company committed up to $100 million in usage credits and $4 million in donations to support open-source security initiatives.

- Anthropic decided not to release the Mythos model widely, citing the need for further safeguards to ensure its safe deployment.

Anthropic introduced its latest AI model, Claude Mythos Preview, on Tuesday, focusing on cybersecurity. The model aims to strengthen defenses against cyber threats by identifying vulnerabilities and developing exploits with little human oversight. This move comes weeks after a security lapse exposed Claude’s code, which drew significant attention to Anthropic’s internal security measures.

New AI Model Targets Cybersecurity Threats

Claude Mythos Preview represents Anthropic’s cutting-edge effort in cybersecurity, designed to uncover high-severity vulnerabilities. In its testing, Mythos has already identified thousands of flaws across major systems, including operating systems and web browsers. According to the company, this new model aims to equip defenders with advanced tools before cyber attackers can harness similar AI capabilities.

Project Glasswing, a partner program, was also announced alongside the Mythos model. It offers early access to the new AI system for select companies like AWS, Google, and Microsoft, among others. More than 40 organizations will be part of the initiative, with Anthropic committing up to $100 million in usage credits to support the program.

Anthropic Pushes for Secure Deployment

Despite Mythos’s promising capabilities, Anthropic has decided against a wide release. The company emphasized the need for further safeguards before deploying Mythos at scale. “Our goal is to ensure that this powerful tool can be deployed safely and responsibly,” an Anthropic representative stated.

This caution follows a mishap earlier this year when a packaging error exposed Claude’s code. The incident led to the accidental release of over 500,000 lines of code, causing a significant security breach. Anthropic’s attempt to take down the leaked files further escalated the issue, as it mistakenly removed thousands of GitHub repositories.

Large-Scale Support for Cybersecurity Defenders

Project Glasswing’s partner organizations will be among the first to test Claude Mythos. These partners include some of the largest players in technology and infrastructure, with the Linux Foundation and Palo Alto Networks joining the program. The initiative aims to harness Mythos’s ability to identify and exploit vulnerabilities while prioritizing the security of its deployment.

Along with the partner program, Anthropic has pledged $4 million in donations to open-source security groups. The company’s focus on supporting cybersecurity initiatives highlights its commitment to safeguarding against advanced cyber threats. However, Mythos’s future remains uncertain, as Anthropic continues to refine its defensive capabilities before making the model more widely available.

The development of Mythos marks a significant step in the AI-driven defense against cybersecurity risks, though Anthropic remains cautious about its broader use.

Three suspects in a crypto wrench attack ring have been charged, according to reporting from the San Francisco Chronicle.

According to the reporting, the three men have been charged in two specific crimes, but police believe that they’re part of a larger operation and are tied to several similar crimes.

The criminals apparently used a similar technique for these crimes, namely:

- Identifying a major cryptocurrency holder.

- Researching and surveilling that cryptocurrency holder. A detective who spoke to the Chronicle described this, saying, “They figure out your trends, your life cycle, what do you normally order online, What do you normally order for takeout?”

- The criminals attempt to gain access to accounts; in the case of one victim who spoke to the Chronicle, “for me, it was my DoorDash and Uber Eats accounts.”

- The criminals would then create a fake delivery, meet the victim at the door, and then threaten them.

Wrench attacks are inherent risk

Cryptocurrency’s censorship-resistant transfers as well as its pseudonymous nature make holders an attractive target for these types of attacks.

These attacks that don’t try to bypass the cryptographic security that protects the assets but use threats and violence to influence the person who has access to the keys.

Indeed, kidnappings and extortion have become an international problem for cryptocurrency holders and firms.

Read more: French crypto tax firm targeted in ShinyHunters extortion attempt

These attacks have included French firm Waltio and UK-based Sillytuna.

France has become something of a leader when it comes to this type of activity, with even Ledger co-founder David Balland targeted.

The utility of cryptocurrency for this type of attack has resulted in even non-cryptocurrency holders having ransoms demanded in bitcoin (BTC). Prominently, Nancy Guthrie, the mother of TODAY Show host Savannah Guthrie, has been kidnapped and her apparent kidnappers have sought the ransom in BTC.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Tesco giving away free food and drink – but only in very specific part of store

Bitcoin Hovers Around $69,000 as Trump’s Iran Deadline Looms

Barcelona, Atletico Madrid face off again but this time the stakes are higher

-

NewsBeat5 days ago

NewsBeat5 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business5 days ago

Business5 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business2 days ago

Business2 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business4 days ago

Business4 days agoExpert Picks for Every Need

-

Sports3 days ago

Sports3 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business6 days ago

Business6 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech2 hours ago

Tech2 hours agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business3 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Crypto World7 days ago

Bitcoin stalls below key resistance as technical signals skew bearish

-

Tech5 days ago

Tech5 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Politics7 days ago

Politics7 days agoStarmer’s centre has collapsed, and the left was right all along

-

Crypto World6 days ago

Crypto World6 days agoRipple rolls out enterprise crypto treasury platform for corporates

-

Fashion2 days ago

Fashion2 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Crypto World6 days ago

Crypto World6 days agoWhy It’s Partnering, Not Issuing

-

Tech6 days ago

Tech6 days agoDrawing Tablet Controls Laser In Real-Time

-

Business3 days ago

Business3 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Tech7 days ago

Tech7 days agoSolo Leveling: Ranking All Sung Jinwoo Shadows by Power

-

Sports6 days ago

Tom Pelissero Drives the Final Nail in the Coffin

You must be logged in to post a comment Login